Abstract

The concept of an inclusive financial ecosystem is crucial in enabling microfinance institutions (MFIs) to effectively serve small-scale businesses. This study examines the complexity of Indonesia’s microfinance ecosystem by analyzing MFI performance in relation to collaboration and competition, and assessing the role of support systems in serving micro and small enterprises. Surveys and in-depth interviews were conducted with MFIs in West Java, South Sulawesi, and Maluku. Findings show that performance gaps between rural banks and MFIs are driven by differences in institutional capacity, outreach, and human resource quality. Rural banks (BPR/BPRS) and micro units of PT Pegadaian and PT PNM demonstrate superior performance through low non-performing loan (NPL) or loan default rates and high profitability, indicating ecosystem deficiencies. With limited collaboration among microfinance players, government micro-credit programs have created imbalances in competition between banks and MFIs, reinforcing disparities. The gap is further exacerbated by inadequate governance support systems—such as deposit insurance, apex institutions, and credit bureaus—burdened by high operational costs. This study offers two recommendations: redesigning microcredit programs to enhance collaboration between MFIs and banks for balanced competition, and strengthening the role of local governments and community institutions as support systems for prudent MFI practices.

Plain Language Summary

Microfinance helps small businesses grow but depends on a strong financial ecosystem. This study, based on surveys and interviews across three provinces, finds significant performance gaps between bank and non-bank MFIs and highlights unfair competition from government programs that favor large banks. Support institutions also struggle with high costs. The study recommends encouraging collaboration between banks and MFIs and strengthening MFIs through local government and community support.

Introduction

Over the years, the interrelated networks of various financial players have composed the complex nature of the microfinance ecosystem in Indonesia. It encompasses not only traditional financiers such as moneylenders and pawnshops but also a large number of rural credit institutions, including savings and loans cooperatives, rural banks, and micro units of large banks (e.g., Bank Rakyat Indonesia/BRI Units; Nugroho, 2009; Seibel & Parhusip, 1997; Zainal et al., 2021). Yet, despite the wide variety of MFIs that coexist in the country, their role in promoting inclusive growth remains challenging (ADB, 2020). Most micro and small enterprises (MSEs) in Indonesia are exposed to credit constraints due to insufficient collateral, low financial literacy, and limited financial information (Bank Indonesia, 2022). While microfinance policies mainly focus on subsidized interest rates to encourage bank credit, they often disregard the complexity of the microfinance ecosystem and the varying abilities of MFIs to address these financial challenges. Cai et al. (2025) identify such constraints associated with fragmented regulation and a lack of innovative credit scoring. Comparably, MSEs also face barriers like inadequate collateral, poor credit information, and low financial literacy (Das & Guha, 2019; IMF, 2024).

It is evident that MFIs’ role are beneficial in smoothing the risk of adverse events, serving as resilience institutions by empowering people and reducing vulnerability against poverty (Gatto & Sadik-Zada, 2022). Access to finance is a human right to achieve Sustainable Development Goals (SDGs) because credit provision to MSEs and low-income groups will contribute to eliminating extreme poverty (SDG 1; Kara et al., 2021; Tay et al., 2022), fostering economic growth and decent work (SDG 8; ADB, 2020; ILO, 2025; Tay et al., 2022), and reducing inequality (SDG 10; Desfiandi & Putra, 2024; Habib et al., 2024). MFIs also strengthen financial inclusion and entrepreneurship among MSMEs (Mishra et al., 2024)by providing working capital to sustain business expansion and income (Banerjee et al., 2014; Meager, 2019). Thus, well-designed and effectively regulated MFIs serve as cross-cutting instruments for poverty and inequality reduction, as well as inclusive finance, underscoring the need to examine Indonesia’s financial ecosystem in pursuit of SDG targets.

In the context of Indonesia, the heterogeneity of MFIs—ranging from cooperatives and microfinance firms to commercial banks—requires deeper investigation into how their business momdels, governance, regulatory frameworks, and technological adoption capabilities determine their performance and their ability to address MSEs’ credit needs. The microfinance performance across different institutional types (e.g., cooperatives vs. commercial bank-based MFIs), their sustainability, and their effectiveness in delivering microcredits to MSEs are influenced by the same factors in the financial ecosystem. The role of support systems—such as digital infrastructure, credit guarantee schemes, and financial literacy programs—in facilitating microcredit delivery to MSEs is acknowledged but not thoroughly investigated. Financial support systems are theoretically critical for bridging the gap in access to credit between MFIs and MSEs. Correspondingly, credit information systems and promoting financial literacy are essential to support and increase the MSEs’ access to credit (Indonesian Business Council, 2024).

Studying the complexity of microfinance ecosystems in Indonesia involves examining the core problem of MSEs facing credit constraints, linked to the varying performance of MFIs, and the role of support systems in delivering microcredit to MSEs. The existing studies on MFIs often focus on specific microfinance contexts, such as credit access and MFI sustainability and clustering (Lwesya & Mwakalobo, 2023), without integrating these into a comprehensive framework. The interplay between MSEs, MFIs, regulatory frameworks, and support systems (e.g., government policies, financial technology, and digital infrastructure; ADB, 2020; Hermes & Hudon, 2018) remains underexamined. What had been studied by Armstrong et al. (2018), Das and Guha (2019), Lwesya and Mwakalobo (2023), Cai et al. (2025), and IMF (2024), still present limited exploration of how these barriers vary across sectors and regions (urban vs. rural), and demographic groups (e.g., women-led MSEs), and their integration within the microfinance ecosystem into the analysis. The variation in the business performance of MFIs within Indonesia’s ecosystem has not been comprehensively studied.

Unlike the financial market approach, the present study utilizes the ecosystem perspectives to investigate the core problem of MSEs facing credit constraints. This study presumes that MSEs exposed to credit constraints are not merely associated with financial market imperfection, instead, the insufficient functioning of microfinance ecosystems inhibits MFIs from serving MSE segments (Armstrong et al., 2018; Das & Guha, 2019; Ledgerwood, 1998). Using this approach, the empirical contribution of the study is to comprehend the extent to which the insufficient functioning of microfinance ecosystems leads to the diverging business performance of MFIs linked with the incapability of the ecosystem to promote collaborative competition across different MFIs, and facilitate the working of supporting institutions in serving MSEs (ADB, 2020; Hermes et al., 2011).

To address the gaps, a comprehensive study of Indonesia’s microfinance ecosystem. Firstly, the business performance of various MFIs is analyzed to comprehend whether or not the diverging performance of MFIs is associated with the modes of operational collaboration and competition across MFIs, as well as between large banks and MFIs in serving MSEs (Armstrong et al., 2018). Secondly, we then explore the role of support systems in affecting the working of MFIs in delivering micro credits to MSEs (Ledgerwood, 1998; Ledgerwood & Gibson, 2013). By integrating insights from stakeholders’ interactions (MFIs, Banks, and MSEs), supporting systems, and government regulation, the research intends to provide actionable recommendations for policymakers and players in MFIs to create balanced competition between MFIs and other players in the ecosystem and to set up the support systems in facilitating the prudent practices of MFIs.

The next section explores literature reviews emphasizing heterogeneous institutions linked to their market competition strategies and the working of support systems in the functioning of the microfinance ecosystem. Then, we present the research methodology, followed by the results and discussion of the research. The last part of the paper provides the implications, conclusion, recommendations, and limitations of the study.

Literature Review

Collaboration–Competition Nexus in the Microfinance Ecosystem

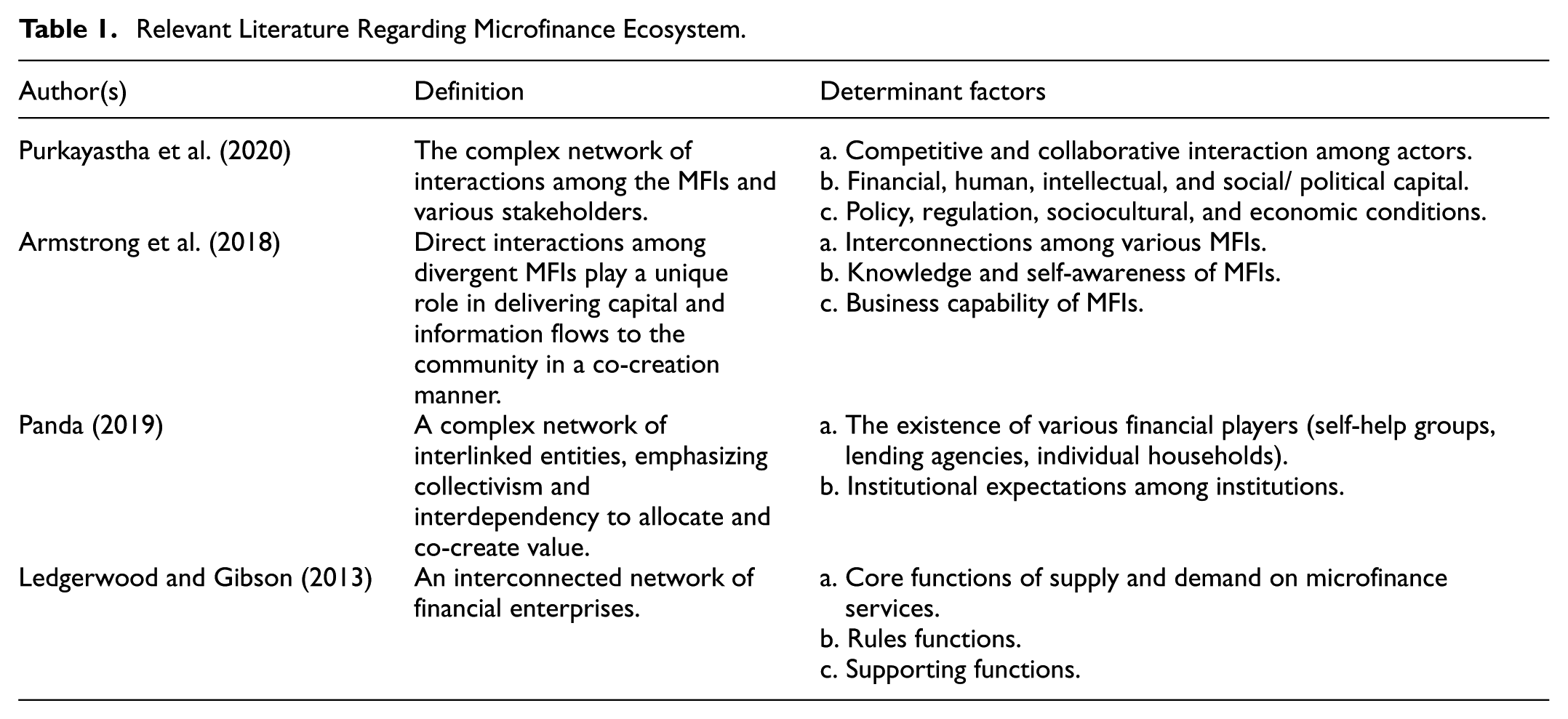

As in other developing countries, a large number of MFIs coexist in Indonesia, shaping the microfinance ecosystem. Such heterogeneity is in parallel to the needs of MSEs for a wide variety of financial services (Farooq et al., 2024). Yet, unlike large financial businesses, the unequivocal characteristics of MFIs are especially associated with employing simple business procedures, and face-to-face networks and interactions to effectively reach their customers (Ndiaye et al., 2019). Ledgerwood (1998) and Ledgerwood and Gibson (2013) assert that heterogeneous MFIs, when constructing the inclusive microfinance ecosystem, underpin the effectiveness of financial services for unbankable MSEs. As such, they go on to say that the microfinance ecosystem refers to interrelated networks of financial businesses across different MFIs and stakeholders that affect their business operations (see Table 1). Hence, the functioning of the microfinance ecosystem will be fostered by the presence of collaborative operations and competition between the wide array of MFIs (Purkayastha et al., 2020). The collaborative-competition nexus can lead to divergent strategies and performance among MFIs serving MSEs (Abrar, 2019).

Relevant Literature Regarding Microfinance Ecosystem.

Given the heterogeneous nature of MFIs, the escalating competition in microfinance markets is shown by the growing number of MFI players (Al-Azzam & Parmeter, 2021). Such competition is partly as a result of deregulation and product diversification of various MFIs in Indonesia (Dela Cruz et al., 2023). The increasing competitive forces indicate that most MFIs consider their business competitiveness landscape (Ahamad et al., 2023).

The impact of competition, as mentioned by Al-Azzam and Parmeter (2021), depends on how optimal the information resources obtained by both MFIs and borrowers. For MFIs, information on the repayment capacity of potential borrowers, including those with a history of default, is crucial to prevent competition among MFIs from increasing the risk of loan defaults. Within such a framework, operational efficiency of MFIs can only be achieved in competitive markets through which they can enforce the improvement in the quality of financial services to gain customer loyalty (Sari & Chofifah, 2025) . Thus, fair competition among MFIs can contribute to reducing the costs of service deliveries through operational efficiency, innovation, and better service quality (Hossain et al., 2020).

However, accelerating degrees of competition among MFIs can have adverse consequences, such as deteriorating the quality of relationships between MFIs and their customers, reducing adherence to prudent lending practices, and potentially increasing the risk of defaults (Baraton & Léon, 2021; Hossain et al., 2020). Al-Azzam and Parmeter (2021) view that intensifying competition among MFIs can also pose disadvantages for the weakest groups of customers due to insufficient knowledge and bargaining power. Referring to Hossain et al. (2020), this can reduce the outreach to the poor. Consequently, the social mission of MFIs diminished (Ahamad et al., 2023) and prompting them to reduce their outreach to MSEs (Nisa et al., 2022).

In the context of business at the community level, the diverse players in MFIs need operational collaboration to finance various MSEs. According to Armstrong et al. (2018) collaboration and operational synergy are required to create shared value among the four main actors in microfinance (small-scale MFIs, large-scale MFI players, and supporting institutions, such as government, non-governmental organizations, and social investors). In the functioning of the microfinance ecosystem, MFIs performance can then be achieved when each actor can focus on strengthening their respective social value to sustain their business operation. In the Middle East and North Africa, however, financial performance is more likely determined by managers’ ability to accommodate the needs of clients from communities adhering to Islamic values (Wadi et al., 2022). Meanwhile, MFIs in Europe and Central Asia rely more on commercial methods than on their social performance (Khan & Shireen, 2020).

Claessens (2009) put forward the notion that reinforcing internal and external networks across different MFIs can minimize the risks associated with competition in microcredit markets. At the internal level, interconnections among MFIs can improve business capabilities through knowledge sharing and increased self-awareness (Armstrong et al., 2018). At the external level, aligning business operations closely to the community networks can foster social bonding between MFIs and community institutions, thereby enhancing access to information about their services to meet the needs of MSEs (Bongomin et al., 2017). It can stimulate MFIs to expand their services and promote community empowerment through various training programs (Choudhury et al., 2017). In this regard, the present study argues that the interplay between collaboration and competition in microfinance is critical to finance MSEs effectively. For Indonesia, microfinance policies that emphasize more competition, such as through interest rate subsidies given to banks in serving MSEs, will undermine operational collaboration between banks and MFIs in microfinance markets.

Critical Role of Support Systems

Apart from varying degrees of collaboration and competition across MFIs, the presence of support systems is shaping the working of the microfinance ecosystem for MSEs. The support systems associated with infrastructures of information and communication technology (ICT) play a role in expanding microfinance outreach to unbankable MSEs (Makoni, 2014; Mushtaq & Bruneau, 2019) and the financial performance of MFIs (Ali et al., 2020). Microfinance as an integral part of financial inclusion requires adequate infrastructure (Staschen & Nelson, 2013) to serve low-income customers (Lapenu & Zeller, 2002). For instance, internet access can enhance cost-effectiveness, productivity, and social objectives of MFIs (Ammar & Ahmed, 2016; Ssewanyana, 2009) .

Moreover, Sun and Im (2015) state that support systems, including government, business, and community institutions, can enable the functioning of a microfinance ecosystem to serve the poor and MSEs. According to Hermes and Hudon (2018), the accountable practices of government are a favorable environment for MFIs’ business to serve MSEs. Conversely, regulatory bodies imposing complex reporting procedures can impede microfinance services to MSEs (Kauffman & Riggins, 2012). O’Keeffe et al. (2013) elaborate further that the supporting systems include payment systems, clearing, settlement, a technology-based payment integrator, insurance, and a credit bureau. For instance, surveillance as a credit bureau can impact MFIs outreach (Damane & Ho, 2024). The performance of MFIs in Asia is strongly influenced by support from partner institutions such as commercial banks, NGOs, and credit bureaus (Bibi et al., 2022). In the Middle East and North Africa, financial performance is largely determined by managers’ ability to accommodate the needs of clients from communities adhering to Islamic values (Wadi et al., 2022).

Furthermore, various types of sociocultural institutions also play a role in enhancing the quality of microfinance business operations through information exchange and collaboration among MFIs (Dang & Vu, 2020; Minani et al., 2018; Purkayastha et al., 2020). Central to the collaboration-induced exchange of information is that it can reduce moral hazard problems in microfinance practices (Dowla, 2006; Tahmasebi & Askaribezayeh, 2021; Zhao & Han, 2020). Also, developing social networks within the community can facilitate MFIs in fostering brand loyalty and effective marketing (Colliander et al., 2015). This can be achieved through linking local culture (Astawa et al., 2021) or religious institutions with MFIs’ business operation in serving MSEs (Zitouni & Ben Jedidia, 2022). Efforts to link social institutions with MFIs’ business operations also work in parallel with enhancing MSEs’ financial literacy (Armstrong et al., 2018; Zhao & Han, 2020). In addition, financial literacy and education are among the key aspects that enable MFIs to balance financial performance with social outreach in promoting financial inclusion (Lahnech & Chami, 2025).

Although numerous studies have examined the dynamics of competition and collaboration, as well as the role of supporting systems in microfinance, the existing literature remains insufficiently compiled into a structured argument. Several unresolved debates persist, including whether competition enhances efficiency and business performance or, conversely, undermines the social mission of microfinance, and whether or not regulatory arrangements strengthen the provision of microfinance services. At the same time, prior research consistently highlights that supporting systems, including ICT infrastructure, government institutions, and socio-cultural networks, contribute to expanding service outreach, operational efficiency, and facilitating information exchange among MFIs. However, limited understanding remains of how these supporting systems interact with competition and collaboration dynamics in shaping the functioning of the microfinance ecosystem, particularly in increasingly competitive environments such as Indonesia. Accordingly, a critical research gap emerges from the absence of an integrated analysis explaining how competition and collaboration dynamics, along with supporting systems, jointly influence the business performance of MFIs in serving micro and small enterprises.

Methodology

Based on the theoretical framework, this research methodology is designed to explore the interactions that form between competition and collaboration among microfinance institutions, while also examining the role of supporting institutions in maintaining the sustainability of the microfinance ecosystem.

Research Framework

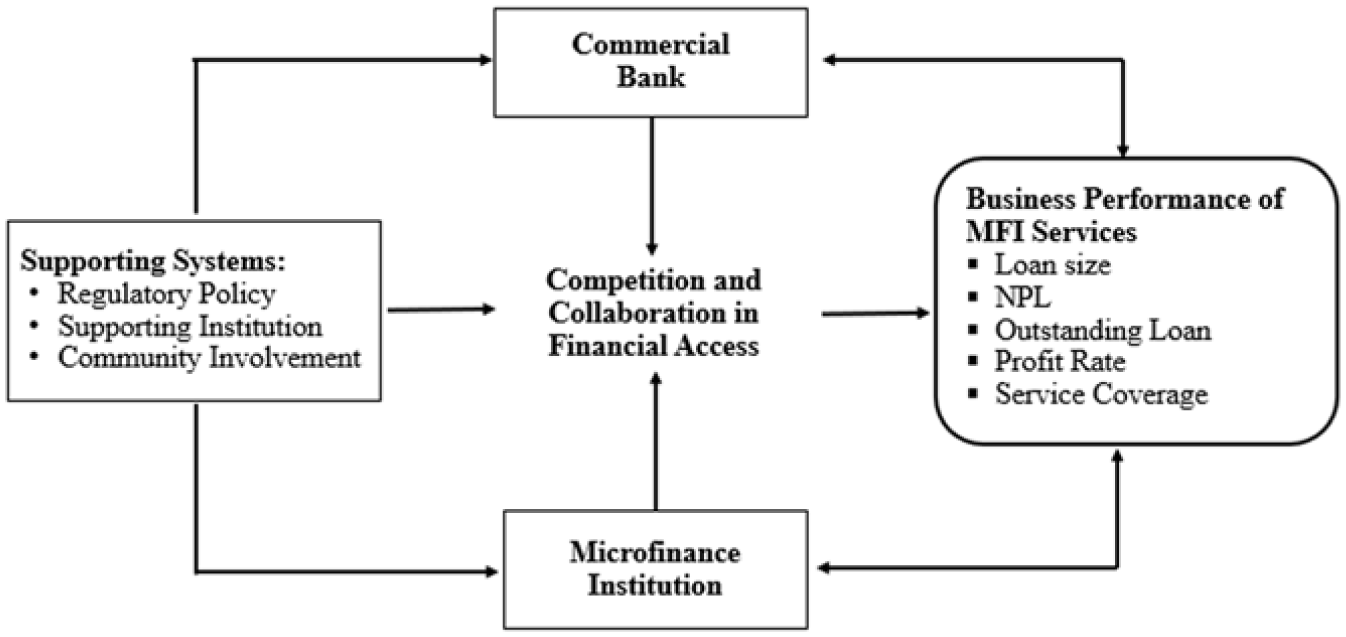

The microfinance ecosystem in Indonesia can be conceptualized as the interaction of three core components: commercial banks, microfinance institutions (MFIs), and supporting systems that mutually reinforce one another in expanding financial access and improving service delivery (Figure 1). The relationship between commercial banks and MFIs forms the center of the competition-collaboration nexus, where both institutions do not operate in isolation but interact within a dynamic system shaped by feedback loops. Competition encourages innovation and service improvement, while collaboration enables capacity strengthening and broader credit outreach, particularly for the underserved segment. The supporting system—comprising regulatory policies, technical support institutions, and community involvement—acts as an enabling mechanism that ensures competitive and collaborative interactions occur within a healthy, inclusive, and sustainable environment. This role is especially critical in the Indonesian context, where many MFIs operate within tightly knit social and religious community networks, making community trust and participation integral to credit performance and institutional reliability.

Research framework: MFIs’ business ecosystem.

Within this conceptual framework, the business performance of MFIs is positioned as the primary outcome influenced by the interplay between commercial banks and MFIs and further enhanced by the strength of supporting systems. This performance is reflected in indicators such as outstanding loans, non-performing loans (NPL) levels, profitability, loan size, and service coverage. Collaboration with banks—such as through linkage programs—offers MFIs access to liquidity, technology, and risk-sharing mechanisms that enhance their operational reach. Conversely, competition motivates MFIs to improve managerial capabilities and develop more competitive financial products to remain relevant to micro and small enterprises. A robust supporting system then functions as both a stabilizing and accelerating factor, ensuring that the bank-MFI relationship generates optimal impact on MFI service performance. Taken together, the interactions among commercial banks, MFIs, and the supporting system form an adaptive microfinance ecosystem that enhances the effectiveness of MFIs in achieving their social and financial objectives.

Data Collection and Analysis

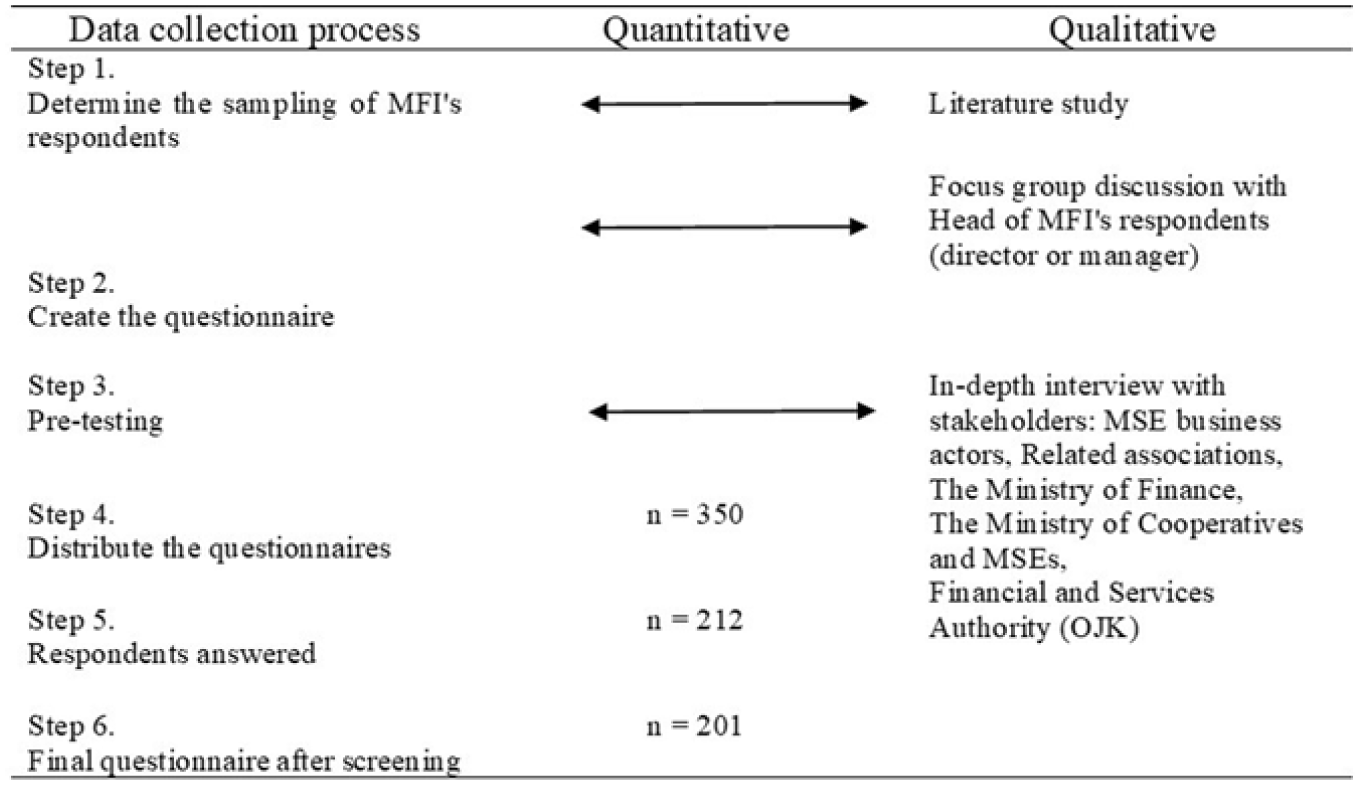

This study used a mixed method designed with an explanatory sequential strategy to comprehend the complexity of the microfinance ecosystem in Indonesia. The method was undertaken in two steps procedures. The first step involved collecting and analyzing quantitative data to comprehend the diverging performance of various MFIs. Quantitative data on the business performance of MFIs were obtained through a survey of microfinance practitioners. The survey was conducted by administering a questionnaire to high officials of MFIs during the period September–November 2022. We analyze the survey data with descriptive statistics and a t-test to determine the relationship between competition, collaboration and MFIs’ performance.

In the second step, we analyzed qualitative information to investigate further the quantitative results (Cheung et al., 2025; Wood et al., 2025). We also triangulated the findings with all stakeholders through a series of focus group discussions (FGDs) and in-depth interviews. Several FGDs were held with associations, including the Indonesian rural banks association, MFIs association, and Islamic MFIs association, as well as the Financial Services Authority (OJK), credit guarantee institutions (Indonesian Multifunctional Loan Insurance and Credit Guarantee Corporation), and the Cooperatives and Micro, Small, and Medium Enterprises Offices. These FGDs used both offline and online formats. In-depth interviews were carried out with representatives of MFIs, MFI associations, micro and small enterprise clients of MFIs, and relevant local government officials. The interviews took place during July and August 2022. The FGDs and interviews aimed to capture the perspectives of key informants on the development and strengthening of Indonesia’s microfinance ecosystem. The discussions covered the current state and progress of the ecosystem, the role of supporting institutions, policies implemented by relevant agencies, as well as constraints, opportunities, and challenges in building a healthier and more sustainable microfinance ecosystem in the future. Recordings from the FGDs and interviews were transcribed verbatim, coded, and organized into categories and themes. This process supported the systematic analysis and discussion of the findings.

The interviews, FGDs, and surveys were conducted only after we received the respondent’s approval. All participation was voluntary, no sensitive personal information was requested, and respondents were informed that they could decline at any time without consequence. Informed consent was obtained through oral and written by asking respondent’s consent prior to the interview, FGD, or survey activity. This study was designed to have no financial risk to the MFIs respondents and the findings will provide valuable information to help strengthen their microfinance business.

To enhance the clarity of the study, the core construct variables were operationalized based on indicators used: MFIs performance, competition and collaboration. MFIs performance refers to loan size, NPL, outstanding loan, profit rate, and service coverage that lead to varying levels of business performance of bank-based and non-bank MFIs. For the competition indicator, it is necessary to see how the respondents’ perception of the competition among the microfinance market, commercial banks, and cooperatives compares to other savings and loans cooperatives, other financing credits, financial technology (fintech) lending, large commercial banks, other credit banks, pawnshops other than PT Pegadaian, and other lenders. Likewise, for collaboration indicators, it is necessary to examine partnership strategies to expand MFI services in the community, as well as cooperation between microfinance institutions, banks, and other financing institutions. This study also sought to determine respondents’ opinions on the roles of stakeholders, such as the government, community leaders, and religious leaders, in supporting MFIs. In addition, we also want to know the supporting institutions needed by respondents, such as deposit guarantees, apex institutions, credit guarantees, insurance companies, skill certification and others that is, rating agencies and credit bureaus.

We classified MFIs into two categories: banking-based MFIs and non-bank MFIs. The types of institutions and informant criteria for each group of MFIs are summarized in Table 2. The first group refers to banking-based MFIs, namely Rural Banks with both conventional and sharia-based operations (BPR/BPRS). The second group refers to non-bank MFIs, including conventional and sharia Savings and Loans Cooperatives (KSP/KSPPS), MFIs licensed by the financial services authority (LKM/LKMS), microloan units of pawnshops (PT Pegadaian), and ultra-micro units of financing institutions (PT PNM). PT PNM encompasses the Developing Prosperous Family’s Economy program (PNM-Mekaar), offering group-based capital loans to pre-prosperous women microentrepreneurs, and the Micro Capital Service Unit (PNM-ULaMM) providing capital loans and business development assistance to MSEs.

Group of MFI respondents by Types of Institution and Informant Criteria.

Based on data from OJK and the Ministry of Cooperatives and Small and Medium Enterprises (SMEs), the population of MFIs in Indonesia is estimated at 22,860 units. This study used a simple random sampling technique across three provinces: West Java, South Sulawesi, and Maluku. These locations were selected to represent the western (West Java), central (South Sulawesi), and eastern (Maluku) regions of Indonesia. Each of the selected provinces ranks among the top five in terms of the number of cooperatives within its respective area. In addition, the operational characteristics of microfinance actors in general also do not differ much across regions; thus, selecting three provinces can represent the microfinance ecosystem in Indonesia. The distribution of respondents by location, gender, type of MFIs, educational qualifications, and MFIs establishment is presented in Table 3.

Respondents’ Profiles.

After the screening process, the number of respondents collected was 201 MFIs, consist of 19 units of BPR/BPRS, 78 units of KSP/KSPPS, 14 units of LKM/LKMS, 41 units of PT Pegadaian, 32 units of PNM-Mekaar, and 17 units of PNM-ULaMM (see Figure 2). This is also in accordance with Statistics Indonesia (BPS) data (2020), which shows that the majority of MFIs in Indonesia were dominated by cooperatives.

The data collection process.

Results and Discussion

Financial Performance, Competition-Collaboration Nexus and Support System in Shaping the Microfinance Ecosystem

MFI Financial Performance

The heterogeneity of MFIs in Indonesia, with respect to loan sizes and operational coverage, led to varying levels of business performance across MFIs. This heterogeneity in microfinance creates fierce competition among players involved (Purkayastha et al., 2020). A notable indicator of such competition is the varying interest rates charged to customers. The lowest interest rate charged by pawnshop units of PT Pegadaian, at about 12% annually. Meanwhile, MFIs in the form of KSP/KSPPS, LKM/LKMS, and BPR/BPRS tend to charge higher interest rates on loans, ranging from 17% to 18% annually. The microfinance units of PT PNM posed the highest interest rate, ranging between 20% (PNM-UlaMM) to 25% (PNM-Mekaar; see Supplemental Appendix 1). Imposing relatively lower interest rates by KSP, LKM, and BPR than those of PT Pegadaian and PT PNM is a response to competition pressure from these MFIs. BPR, KSP and LKM have to offer lower interest rates to attract more customers. This condition raises concern that the existence of state-owned MFIs (PT Pegadaian and PT PNM) creates unfair competition in the microfinance ecosystem.

In response to competitive pressures, different MFIs tend to focus on different market segments. As presented in Supplemental Appendix 1, PNM-Mekaar focus on the very micro segments with a loan size of only 3 IDR million per borrower (US$187.5). In response to insufficient collateral, some MFIs have implemented group lending to build peer monitoring and mutual trust, thereby reducing the risk of loan default. This finding is consistent with Nayak and Samanta’s (2023) study, which found that MFIs are able to achieve social transformation by forming small groups that accumulate financing assets as business development capital. Ledgerwood (1998) explains that the plafond scheme offered by group lending can enhance the outreach capabilities of empowering marginal lenders in the ecosystem.

Furthermore, MFIs in the form of cooperative credit, such as KSP and LKM are operate in micro segments with loan sizes of around IDR 13–16 million per borrower (US$812.5–1,000). Meanwhile, PNM-ULaMM, BPR/BPRS, and PT Pegadaian are more focused on small segments, distributing loans ranging from IDR 21-30 million (US$1,312.5–1,875). These MFIs can also have wider service coverage across sub-districts of operation. This broadening outreach is supported by a relatively large number of lending staff with better educational qualifications. Our interviews found that the majority of lending staff at PNM-ULaMM, BPR/BPRS, and PT Pegadaian have university education.

Given the divergent profitability across different MFIs, PNM-Mekaar recorded the highest average annual profit at 32.5%, followed by BPR/BPRS and PNM-ULaMM, which ranged from 10% to 13%. PT Pegadaian and KSP/KSPPS are in the range of 3% to 5%, and the lowest are LKM/LKMS, which recorded negative average profits. This variation in profit is particularly related to diverging non-performing loan rates. On average, the NPL rate for BPR/BPRS units of PT Pegadaian and PNM-ULaMM is mostly below 10% per year. However, MFIs focused on microloans tend to have NPL rates above 10%, specifically KSP/KSPPS (12.3%) and LKM/LKMS (21%). This finding suggests that, in terms of financial performance, many MFIs remain exposed to high loan default with relatively low profitability. The high NPLs and low profitability observed among many MFIs appear to result from weak monitoring systems and limited staff capacity, which undermine credit evaluation processes and increase default risks. In-depth interviews further support this explanation, highlighting that these institutional constraints play a central role in shaping the weak performance of Indonesia’s microfinance ecosystem.

The findings above indicate that bank-based and state-owned MFIs outperform privately owned and community-based non-bank MFIs in terms of profitability and NPLs, differing from Latin America, where NGO-based institutions perform better (Piot-Lepetit & Tchakoute Tchuigoua, 2022). In South Asia, MFIs emphasize social performance over financial soundness (Hussain & Rasheed, 2023; Khan et al., 2025; Memon et al., 2022). Performance is shaped not only by profitability and NPLs but also by competition and collaboration within the microfinance ecosystem, which requires coordination, fair competition, and clear role differentiation (Purkayastha et al., 2020). Similarly, in Indonesia and East–Southeast Asia, MFIs operate within integrative, commercially oriented frameworks supported by banks and fintech (Nisa et al., 2021), whereas in Africa and Sub-Saharan Africa, hybrid and community-based models often incorporate informal institutions (Hatlebakk, 2024; Littlewood & Holt, 2020; Pienaah & Luginaah, 2024; World Bank, 2006).

Level of Competition and Collaboration Between MFIs

In microfinance markets, various types of MFIs coexist, undertaking business networks to serve MSEs. Not only to respond to competitive pressures, but the development of such networks can also promote operational collaborations among MFIs to sustain their market positions (Armstrong et al., 2018; Nisa et al., 2022; Widjajanti, 2015). According to Al-Azzam and Parmeter (2021) and Deb and Sinha (2022), the interplay between competition and collaboration can lead MFIs to generate various forms of innovation to serve MSEs effectively. In this regard, the market share across different types of MFIs in the operational area is worth noting. Based on the survey results, PNM-Mekaar identifies itself as the dominant player in group lending, accounting for about 40% to 50% market share. This method has been a major strength of PNM-Mekaar, providing intensive assistance to sustain consumer loyalty. This finding is consistent with the informant’s opinion:

Mekaar is actually unique among competitors (…). Because our strength is to empower groups of women that support each other, we are relatively unaffected by competition. Our customers remain loyal because we provide empowerment. PNM builds an ecosystem that helps those who did not have a business before, then grows and develops their business. Our established ecosystem guides customers from Mekaar to Mekaar plus to ULaMM, ensuring ongoing development and support (MB from PNM Mekaar, South Sulawesi, 24 August 2022).

Meanwhile, KSP/KSPPS estimate their market share at about 30% in their operational area. This position is followed by the units of PNM-ULaMM contributing to around 5% to 10% of the market share, while BPR/BPRS accounts for less than 5%. The greater market shares of cooperatives over BPR/BPRS and PNM-ULaMM because they link financial services with social values of the community. Thus, they are more likely to gain the community’s trust than BPR/BPRS. The informant explained that member loyalty is maintained through good service and informal networking. These findings reinforce that cooperatives gain public trust through the closeness of the community and the social values that accompany their financial services. Here’s an excerpt of the interview:

KSP Mallomo finances businesses around here, probably around 20%, as there are numerous cooperatives in Makassar, with PNM being the most dominant in this area…. Here, members remain loyal and will borrow again once they are finished, because we maintain a good approach to members. The strength of KSP Mallomo: First, from employee service to members, on how to communicate and approach. Then, members spread through word of mouth, so if our service is good, one member will tell another. We handle payment delays calmly and involve management to mediate any disputes between employees and members, ensuring a consistent, supportive approach (HS from KSP, South Sulawesi, August 25, 2022).

Moreover, Table 4 shows that the major competitor of MFIs in serving MSEs is commercial banks, while PNM Mekaar recognizes credit cooperatives as the main competitor. The informants (JL from KSPPS, South Sulawesi, 22 August 2022) argued that the major competitor for us is commercial banks, as they already exist in the market. Many BMT members have switched to banks because of KUR. Team from Pegadaian in the FGD session also echoed this statement:

PT Pegadaian’s main competitors are BSI and regional banks, such as Bank Sulselbar….. We were not worried about fintech because of its high interest rates. What we’re worried about is the KUR. The hope is that banks won’t take loans under 10 million, but rather those above 10 million. Those under 10 million should be given to cooperatives and BMTs so they can survive (NN from unit of PT. Pegadaian, South Sulawesi, 24 August 2022).

The Percentage of Main Competitors in Financing From the Perspectives of Respondents.

BRI, BSI, Mandiri, BNI, BPD, etc.

Commercial banks are seen as a major threat to microfinance markets for MFIs because they have greater financial capacity, business acumen, and higher-quality human resources. Hence, the micro-units of banks are much more capable of penetrating to microfinance markets compared to MFIs. Based on the interview with the informant:

Our competitors in this area are commercial banks. BPRs are struggling to grow as the government enables commercial banks to enter the microfinance segment. For example, if BRI expands to ultra-micro, how can we compete with those who have large capital, strong networks, advanced technology, competitive pricing, and adequate human resources? There should be market segmentations, and existing regulations are not implemented effectively. The margin levels between commercial banks and BPRs differ, ultimately allowing BPRs to capture segments that commercial banks have neglected (third-class customers). Furthermore, commercial banks are permitted to offer KUR (People’s Business Credit) at 6% interest, with loans of up to IDR 100 million available without collateral. So, the main competitors are commercial banks, particularly the larger ones (FR from BPRS, West Java, 22 August 2022).

Based on these findings, government programs, such as the People’s Business Credit (KUR), indirectly encourage unfair forms of competition in the distribution of microfinance. The significant increase in KUR outstanding from IDR 140 trillion in 2019 to IDR 280 trillion in 2024 reflects a considerable expansion of subsidized credit disbursement, especially by commercial banks disbursing KUR. At the same time, the rapid growth of KUR strengthens competition between KUR distributing institutions—most of which are banks—and non-KUR financial institutions, including BPRs and various types of MFIs. This dynamic has been proven to contribute to a decrease in the number of non-KUR institutions: the number of BPRs has gradually decreased with an average of 10 to 20 institutions per year, from 1,709 in 2019 to 1,460 in 2024, while the number of MFIs has also decreased from 5,681 in 2019 to 5,143 in 2024 (BPS and OJK, 2019–2024).

However, numerous MFIs consider that they compete with one another, especially KSP (21.8%), units of PNM-Mekaar and PNM-UlaMM (28.1%). This finding is consistent with the result of an in-depth interview with the informant (FL from KSP, Maluku, 10 August 2022), who stated that the main competitors are commercial banks. Meanwhile, secondary competitors are other savings and loan cooperatives that offer instant loans at higher interest rates. As stated by the informant, as follows:

Non-banks, such as cooperatives, have a strong presence here because they offer entrepreneurs financial options outside traditional banks. Of course, cooperatives become competitors, besides rural banks (BPRs) themselves, as all serve the same segment. The entry of cooperatives increases competition for market share. Often, cooperatives benefit from more flexible compliance requirements. Still, we must remember that compliance is important, as cooperatives also enjoy greater freedom (YD from BPR, West Java, 26 August 2022).

Although MFIs vary in form and institutional performance, they share the same target market, services, and operating areas. This encourages competition between MFIs and affects their performance. The relationship between the level of competition and institutional performance is also strengthened by the results of the t-test presented in Supplemental Appendix 2, which show significant differences in performance indicators (outstanding credit, NPL ratio, profitability, loan size, and service coverage) and the level of competition between microfinance institutions. Thus, in conditions of relatively tight competition, MFIs are required to further improve operational efficiency (Hartarska & Mersland, 2012; Mersland & Øystein Strøm, 2009) and offer more competitive interest rates (Ahlin & Waters, 2016; Al-Azzam & Parmeter, 2021; Deb & Sinha, 2022).

In addition to competition, several MFIs are also trying to build operational partnerships with each other and with commercial banks. As shown in Table 5, the pawnshop unit of PT Pegadaian and the PNM-Mekaar unit have established business partnerships primarily with commercial banks (over 80%), as well as with PT PNM and PT Pegadaian itself. Meanwhile, the majority of PNM-ULaMM have partnered with the pawnshop unit PT Pegadaian (52.9%) and commercial banks (47.1%). According to the results of the T-test in Supplemental Appendix 2, there is a significant correlation between collaboration and MFI performance. For example, business cooperation between the pawnshop unit of PT Pegadaian and PNM-ULaMM with large banks is mostly through a channeling scheme. Although the scheme is less attractive to banks due to the associated risk burden, PT Pegadaian and PNM-ULaMM benefit by extending loans to customers. On the other hand, small cooperatives and MFIs tend not to be involved with banks due to limitations in meeting administrative requirements, such as guarantees, and significant differences in interest rates.

The Percentage of Financing Partners From the Perspectives of Respondents.

Based on these findings, the structure of the microfinance market in Indonesia is shaped by the interaction among institutional models, the strength of social capital, and the operational capacity of each MFI. The dynamics of competition and collaboration determine how MFIs position themselves, innovate, and provide effective financial services to the MSE sector.

Support System for the Functioning of the Microfinance Ecosystem

The support system within the microfinance ecosystem consists of the government, community and supporting institutions. These institutions can take up the role as enablers in influencing the business operations of MFIs. They can also facilitate better service delivery, reduce costs, reshape stakeholder relationships in microfinance institutions (MFIs), enhance governance risk mitigation, and foster innovation and inclusion, ultimately benefiting both MFIs and their clients (Agrawal, 2017; Aifiah Binti Ibrahim, 2024; Albarrak & Alokley, 2021; Indra et al., 2022; Mia, 2023; Offiong et al., 2024; Ray & Mahapatra, 2016; Sarfo et al., 2024).

Table 6 shows that the majority of all MFIs surveyed state the important role of the government to their business. The central government is specifically involved in enhancing MFIs’ operational accountability. This finding aligns with the results of an in-depth interview with the informant stated:

It is reasonable for OJK to increase the minimum capital requirement for BPR/BPRS to IDR 12 billion by 2025. We cannot operate at our full potential with only IDR 3 billion in capital. Moreover, we cannot attract qualified human resources, as this requires substantial financial investment to cover competitive employee salaries (AM from BPRS, South Sulawesi, 25 August, 2022).

Stakeholders Involvement From the Perspectives of Respondents (%).

Meanwhile, local governments are involved in socialization and supervision of MFIs and KSP operating in provincial/regency/city areas. As stated by the informant as follows:

The Cooperative Service provides guidance on bookkeeping, operational management, and strategies for developing cooperatives. They make regular visits twice a month to deliver advice and training. Their capacity to offer direction is strong and effective, making us feel well-supported. Through their frequent visits, they can identify any shortcomings and promptly inform us (HS from KSP, South Sulawesi, 25 August, 2022).

Interestingly, the community leaders take up the role in influencing MSEs’ participation in accessing financial services of MFIs through engaging in informal gatherings. In the business operation of PNM-Mekaar and pawnshop units of PT Pegadaian, the majority of respondents state that involvement of community leaders can influence MSE clients in access to their microfinance services. The involvement of the community leaders occur especially in the process of recruitment and mentoring MSE clients of PNM-Mekaar, while the role played by religious leaders is in the process of improving awareness of MSEs toward the benefits of accessing to microfinance services. An in-depth interview with the informant revealed the following:

Community and religious leaders maintain strong patron–client relationships due to the community’s high dependence on them. To leverage this influence, we identify ‘opinion leaders’ in each region as the first parties to approach when entering a new area. We also engage with religious figures, community leaders, and prominent business-people, particularly when public trust in cooperatives is low (AA from KSPPS, South Sulawesi, 27 August, 2022).

Furthermore, as mentioned by Gatto and Sadik-Zada (2022) that the functioning of supporting institutions can facilitate the advancement of MFIs in empowering MSEs. For example, Table 7 reveals that in the business operations of BPR/BPRS and KSP/KSPPS, the need for having the support systems of deposit insurance provider is critically urgent, while PT Pegadaian and PT PNM (Mekaar and ULaMM) require support systems of having credit guarantee institutions. This indicates that BPR/BPRS and KSP/KSPPS require supporting institutions that can provide protection against liquidity and solvency risks to maintain their financial operations. Deposit guarantee institutions are expected to increase public trust in BPR/BPRS and KSP/KSPPS as reliable MFIs to save. As Jia and Wang (2011) point out that such a deposit guarantee scheme can reduce liquidity risks of MFIs, which are perceived as vital to maintain sufficient capital adequacy. Meanwhile, credit guarantee institutions are needed by PT Pegadaian, PT PNM (Mekaar and ULaMM) to help reduce risks of providing small loans to MSEs with insufficient collateral. The presence of credit guarantee schemes can facilitate these MFIs to expand small-scale loans with inadequate collateral requirements (Porretta et al., 2013).

The Percentage of Supporting Institutions Needed by Microfinance Institutions From the Perspective of Respondents.

Supporting institutions in the form of human resource certification are needed to ensure the standardized qualification of skills and competency required in microfinance. A criticism of human resource certification is that MFIs can convince business partners and regulators toward their operational credibility which can improve the business performance, as stated by the informant:

To enhance the quality of the workforce, particularly in the financial sector, skills certification is essential. This requires the establishment of an authorized institution to certify workers in the financial industry (FR from BPRS, West Java, 25 August, 2022).

The presence of microfinance associations is a crucial component in strengthening the microfinance ecosystem. These associations facilitate collaboration among MFIs by sharing resources and information, as well as by developing new products and services to enhance business networks (Hudak, 2011). Moreover, associations functioning as apex institutions can increase financial capacity, promote knowledge sharing, and advocate strategies to manage the high risks of serving MSEs. Overall, the roles of government, society, and supporting institutions provide a vital foundation for improving MFI operational stability, expanding service coverage, and enhancing the quality of financial access for MSEs.

Toward the Working of a Healthy Ecosystem of Microfinance

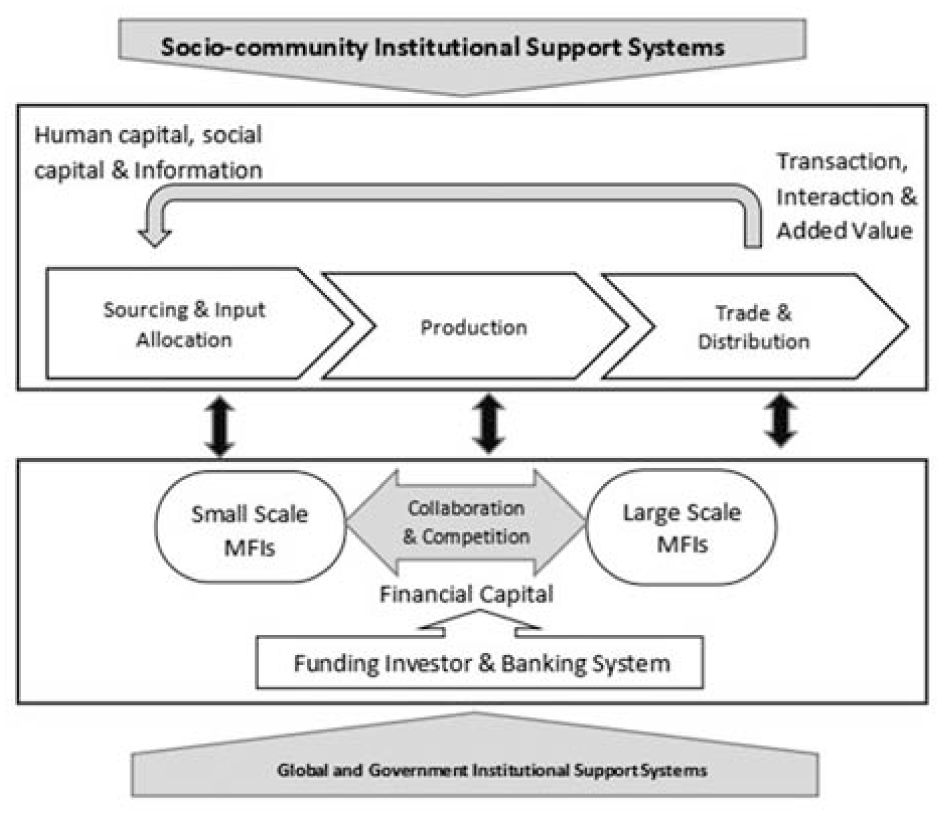

With regard to the research results described above, this study presents Figure 3 to outline the functioning of the microfinance ecosystem in serving MSEs. In the Figure, the collaboration and competition nexus between large and small MFIs is vital for facilitating improvement in MSEs’ business performance (Armstrong et al., 2018). Critical to the functioning of ecosystem is that the microfinance services provided shall facilitate not only the procurement of inputs but also the sustainable process of production, distribution, and trading of goods and services generated by MSEs. As stated by Yanuarta et al. (2023), the effectiveness of the ecosystem hinges on the financing process that enhances MSEs’ capabilities to accumulate added value, including profit, interest income, and wages. It was further affirmed that strengthening collaboration networks enables MFIs to access external financing from investors or large banks. The increasing business acumen of MSEs can, in turn, enhance economic activities, social capital, and information accumulation perceived as vital for MFIs’ business performance (Postelnicu & Hermes, 2018).

Microfinance ecosystem of MSE capital reproduction.

The microfinance ecosystem having various MFIs with sound business performance can then provide greater financial services to MSEs. However, the prevailing competition between MFIs in Indonesia has led to a situation where they compete to provide attractive incentives that benefit MSEs, but this adversely impacts to the financial performance of MFIs. This unfair competitive environment result in insufficient functioning of microfinance ecosystem in Indonesia. To address this issue, Armstrong et al. (2018) suggests that promoting operational collaboration between MFIs can help creating conducive competition. Maintaining competition and collaboration nexus is crucial for the success of microfinance operations that benefit MSEs while also supporting the financial performance of MFIs. The healthy microfinance ecosystem will be capable of providing sustainable microfinance services to MSEs, especially through fostering collaboration and competition nexus between MFIs in microfinance markets (Purkayastha et al., 2020).

Furthermore, the interplay of both collaboration and competition can be achieved through financial strategies tailored to the specific characteristics of MSEs (Abrar, 2019). This is particularly the case as most MFIs in Indonesia compete fiercely with one another and with commercial banks to serve MSEs. This is consistent with a study by Dela Cruz et al. (2023) that many MFIs mostly have the same target, service types, and operational location, encouraging significant competition among them. The intense competition in the microfinance market has turned into an unfair business rivalry due to gaps in business capabilities, financial capacity, human resources quality, and technological capabilities across MFIs. This is the case because the process of commercialization, which is facilitated by MFIs’ ability to maintain credit quality to make respectable profits, encourages other parties, including large banks, to directly participate in serving MSEs (Ayodele et al., 2019; Doddy Ariefianto et al., 2024). In contrast, while small-scale MFIs often have limited capacity to attract public savings due to perceptions of high default risk, large banks receive government credit programs in the form of interest subsidies, leaving their MFIs counterparts unable to compete by charging low interest rates.

However, the working of microfinance ecosystems requires various support systems that can facilitate the business operations of the MFIs involved (Forcella & Lucheschi, 2015). In general, the availability of supporting systems tends to vary depending on the regional and geographical conditions of MFIs’ operations, including infrastructure, ICT, social capital, supporting institutions and regulations. For instance, MFIs ability to serve multiple MSEs, especially in remote areas, requires supporting institutions to reduce operational costs and risks of serving their clients. Reliable internet access and infrastructure are required to strengthen digital financial services and effectively expand outreach to achieve financial inclusion (Lahnech & Chami, 2025). The t-test results (see Supplemental Appendix 2) confirm highly significant differences in MFI performance, which are reflected in the extent of service outreach, associated with variations in managerial and service technology, and internet network quality.

The availability of credit guarantee institutions, microinsurance and associations can also play a role in reducing the risk of lending to MSEs, especially with insufficient collateral. Furthermore, the role of religious and community leaders is quite significant in supporting MFIs’ business operations. Yet, our findings show that the involvement of community and religious leaders is limited to improving financial literacy and providing recommendations for potential MSE consumers. As Mansori et al. (2020) emphasized, religious leaders can influence MSEs’ literacy and intention to use microfinance services. The importance of financial literacy among MSEs is supported by the statistical inferential results (Supplemental Appendix 2) indicating significant differences in MSE’s literacy across all MFI performance indicators examined in this study.

The findings align with the perspectives of Xu et al. (2019), who demonstrated that the efficacy of microfinance is influenced by both internal and external variables. The management of microfinance institutions needs to define their activities in collaboration with other entities within the ecosystem to generate shared value and achieve sustainable business outcomes (Armstrong et al., 2018). Armstrong et al. (2018) identified four primary participants in the financial ecosystem: customers, small-scale microfinance institutions, large-scale microfinance institutions, and financial institutions, which exhibit interdependent relationships that cultivate mutual trust. This picture sharply contrasts with the situation in Indonesia, where financial institutions are embroiled in intense market rivalry. Iheanachor et al. (2023) assert that enhancing the microfinance ecosystem necessitates more collaboration among financial players, regulators, and other stakeholders. In this context, microfinance authorities must have a more proactive role in ensuring that all participants within the ecosystem comply with the established values (Iheanachor et al., 2023).

Practical and Social Implications

Several practical implications of this study include: (1) The government and financial authority (e.g., OJK) need to simplify regulations to improve the governance system of MFIs by implementing effective monitoring and evaluation and encouraging operational collaboration. (2) The government needs to improve MFI performance by initiating human resource and managerial training, improving physical and digital infrastructure, and supporting institutions (i.e., guarantee, insurance, rating institutions). (3) Expanding cooperation between the government and community leaders is required to strengthen social collateral in microlending.

Meanwhile, with improvements in regulation, governance, infrastructure and collaboration, the microfinance ecosystem has social implications that help stabilize and sustain the economy and make community welfare more equitable. This can be achieved by improving competition and collaboration, as well as by expanding financial outreach to underserved areas, thereby reducing economic inequality and providing more equal opportunities for MSEs. In social implications, social networks and community participation are also strengthened by involving community leaders and religious institutions in the microfinance business.

Conclusion and Recommendations

This study has analyzed the microfinance performance linked to the collaboration and competition nexus across MFIs toward the functioning of the microfinance ecosystem. The following conclusions are worth noting in the study. First, the heterogeneous performance of microfinance business is associated with the diverging capacity and capability of MFIs’ business, outreach, and human resource quality. Bank-based MFIs (e.g., BPR/BPRS) and micro-units of state-owned enterprises (such as PT Pegadaian, and PT PNM) tend to have better performance in terms of low default rates and greater profitability. This finding theoretically implies that microfinance businesses are not homogeneous entities providing uniform microfinance services to MSEs. Rather, they are varied in many respects, forming the financing ecosystems of MSEs.

Second, microfinance competition tends to be segmented in the sense that a competition occurs among and across MFIs, but is more intense with commercial banks. Segmented competition arises from differences in the business and financial capacities of MFIs that can induce operational collaboration between MFIs and commercial banks, especially to gain greater financial access. The theoretical implication of this finding is that, in segmented microfinance markets, the varying degrees of collaboration and competition are central in building a microfinance ecosystem compatible with MSEs that demand different types of financing. Third, support systems in the form of community and/or religious leaders, as well as the supporting institutions, such as deposit insurance, credit guarantors and apex institutions, have a significant role in creating a healthy microfinance ecosystem.

Considering the above conclusions, some affirmative actions are needed to strengthen the microfinance ecosystem in Indonesia: Firstly, the government and financial authorities are required to help improving the business capabilities and financial capacity of non-bank MFIs, in particular, the KSP/KSPPS and LKM/LKMS. To enhance the capacity of microfinance institutions (MFIs) in supporting the Sustainable Development Goals, the Government of Indonesia should run the program focusing on the Roadmap for the Development and Strengthening of Microfinance Institutions (MFIs) for the 2024 to 2028, led by the Financial Services Authority (OJK), together with the Ministry of Cooperatives and SMEs. For human resources and management, OJK will mandate competency certification for all MFI managers and loan officers through the National Agency for Professional Certification (BNSP) and existing accredited providers. A subsidized mentorship and training initiative can be promoted among microfinance entrepreneurs to build their leadership and digital finance skills at minimal additional cost. In addition, reforming the KUR program to prioritize partnerships with MFIs for credit distribution to MSEs, with a focus on those serving rural/remote areas.

Secondly, the financial authority should focus on strengthening the business governance of MFIs by enhancing the effectiveness and frequency of supervisory activities, streamlining regulatory frameworks to reduce complexity, and enforcing compliance mechanisms. To do so, the OJK should finalize and roll out the Risk-Based Supervision (RBS) framework already piloted in 2023 to 2024, mandating annual on-site supervision for BPRs and licensed MFIs via the OJK-SLIK and P2P platforms for smaller and cooperative-based institutions (KSP/LKMS and others). These concrete, budgeted, and institutionally anchored measures will strengthen governance, foster healthy competition and collaboration, and reduce operational risks in a realistic, measurable manner for MFIs. These efforts aim to improve accountability, transparency, institutional credibility, and the overall governance system of MFIs in a measurable and sustainable manner. Practical steps include streamlining the compliance system and creating a user-friendly platform for risk assessment tools.

Thirdly, the importance of creating fair competition between very diverse MFIs is critical to enhance collaboration between MFIs and large banks. This can be undertaken by developing regulatory systems that categorizes MFIs based on their size, services, risk profiles, and operational model (targeted groups of women empowerments, sharia and conventional). Fourthly, improving infrastructure quality, particularly internet access, can streamline and enhance the use of virtual transactions within MFIs. The utilization of supporting institutions such as rating agencies, credit bureau and guarantee systems can also lead MFIs to minimize the cost and risks of serving MSEs.

This study only surveyed registered MFIs in three provinces of Indonesia. As such, the sample composition does not fully capture the heterogeneity of MFIs nationwide, which varies in terms of legal status, governance structure, operational scale, and service delivery models, such as digital-based financial services. MFIs operating in other provinces may face distinct regulatory regimes, socio-cultural norms, and economic constraints that could shape their competitive behavior and collaborative practices differently. Therefore, future research should purposively include unregistered MFIs, microfinance units within large-scale banks, fintech lending, and MFIs from provinces with contrasting policy frameworks and socio-economic contexts to enable cross-regional comparisons and a more nuanced understanding of the sector.

Furthermore, on the demand side, this study relied solely on self-reported data from MFI representatives, which may introduce institutional bias and overlook the service recipients’ perspectives. Future studies should incorporate viewpoints from other stakeholders in the microfinance ecosystem, particularly MSEs borrowers, as well as the growing user of fintech to assess how institutional strategies play a role in small scale financing. Such multi-perspective analysis could reveal gaps between institutional intentions and client experiences, thereby providing actionable insights for effective policy and practice of MFIs.

Supplemental Material

sj-docx-1-sgo-10.1177_21582440261417015 – Supplemental material for Strengthening the Microfinance Ecosystem in Indonesia: Competition-Collaboration Nexus and Supporting System

Supplemental material, sj-docx-1-sgo-10.1177_21582440261417015 for Strengthening the Microfinance Ecosystem in Indonesia: Competition-Collaboration Nexus and Supporting System by Tuti Ermawati, Agus Eko Nugroho, Isbandi Rukminto Adi, Muhammad Soekarni, Bitra Suyatno, Jiwa Sarana, Chitra Indah Yuliana, Yeni Saptia, Erla Mychelisda, Zamroni Salim, Ragil Yoga Edi and Septian Adityawati in SAGE Open

Footnotes

Acknowledgements

This research has been funded by the Fiscal Policy Agency, Ministry of Finance of Indonesia, project number KEP-3/KF.5/2022. The authors would like to thank the Centre for Financial Sector Policy, Fiscal Policy Agency, Ministry of Finance of Indonesia, for providing research funds and microfinance practitioners, and other stakeholders who participated in this research. Any remaining error is ours.

ORCID iDs

Ethical Considerations

All procedures (including the questionnaire and methodology) involving human participants in this study were conducted under the ethical standards of the institution and the principles of the Declaration of Helsinki. The ethics review committee of social and humanities research of the National Research and Innovation Agency approved this study on 28 April 2022 with Decision Letter Number: 077/KE.01/SK/4/2022.

Consent to Participate

Informed consent was obtained through oral and written by asking respondents’ consent prior to their participation in in-depth interview, FGD, and survey.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The authors received financial support from the Fiscal Policy Agency, Ministry of Finance, the Republic of Indonesia, for the research of this article.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The datasets generated during and/or analyzed during the current study are available from the corresponding author only on reasonable request.*

Supplemental Material

Supplemental material for this article is available online.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.