Abstract

The role played by microfinancing in the empowerment of women has been a subject of debate in recent literature. By employing the case study method, this paper explores the influencing determinants. Data was obtained from a field interview comprised of 20 female microfinance borrowers and their male family members, as well as focus group discussions and participant observation. The economic, social, and political empowerment of the interviewed women were assessed using Kabeer’s empowerment framework, and the results reveal that microfinancing does not influence the economic and political dimensions of female empowerment; instead, microfinancing was observed to empower women socially, particularly with respect to their participation in major decision-making. The results further indicate that the age, family type, educational level, financial literacy, and training of female microfinance clients play important roles in their empowerment.

Introduction

Women’s empowerment can be described as the capacity of women to reduce their socio-economic vulnerability and dependency on men; to improve their involvement and control in the implementation of household decisions, economic activities, and resources; to participate in the payment of household expenses; and to improve their self-confidence and awareness of social issues (Aggarwal et al., 2015). Such empowerment is an important goal among the 17 Sustainable Development Goals (SDGs) of the United Nations (2018); it is also a significant indicator of socio-economic development (Geleta et al., 2017; Nassani et al., 2019). In a male-dominated society, women experience discrimination within their families and their social, economic, and political lives. Their traditional duty—managing the household—further hinders their social and economic empowerment (Kabeer, 1999). Clement et al. (2019) claimed that the empowerment of women is an effective approach to combatting poverty and promoting socio-economic development. Since women are likely to expend their income on the feeding, healthcare, and education of their children, they also contribute to the long-term economic advancement of families, communities, and, ultimately, countries. Women’s empowerment plays a pivotal role in the annihilation of gender inequality, as well as enabling women to contribute to socio-economic development through their self-employment and involvement in income-generating activities (Nawaz, 2015). Particularly, women’s lack of access to credit facilities has proven to be the main obstacle between them and their self-employment, necessitating the implementation of several development strategies and tools—such as microfinancing, education, training, and entrepreneurial programs—to fill the void (Clement et al., 2019). Microfinancing is considered the most effective tool for poverty alleviation and women’s empowerment (Schuler et al., 1996), representing a form of social enterprise which provides small-scale collateral-free loans mainly to poor women in support of their self-employment and personal development (Postelnicu & Hermes, 2018).

Microfinance contributes to female empowerment by increasing their access to credit facilities, health, and education, as well as contributing to the accumulation of social capital, promotion of entrepreneurship, and alleviation of poverty (Khandker, 2005; Westover, 2008). In addition, it gives them an opportunity to exercise their empowerment and improve their economic conditions, thus granting them control over their lives (Galiè et al., 2019).

Although microfinance positively influences several social indicators such as income, consumption, savings, empowerment, and general welfare, it has also been criticized for deviating from its original values (Nawaz, 2015). Owing to their high interest rates charged on loans, microfinance institutions (MFIs) have been unable to attain their outreach goal of improving the socio-economic development of the nation (Ganle et al., 2015). Consequently, adverse effects have been recorded, including the exploitation of women, increased or unchanged poverty levels, income inequality, increased workloads, the use of child labor (F. Hossain, 2002), increased risk of debts (Snow & Buss, 2001), dependencies and barriers to sustainable development, and moral hazards (Hudon & Sandberg, 2013). Hence, the report on microfinancing’s promotion of female empowerment can be regarded as inconclusive and contradictory.

Previous studies have identified various factors influencing women’s empowerment, such as age (Alkire et al., 2013), education (Sell & Minot, 2018), marital status and ethnicity (Allendorf, 2007), preference for male children (Saha & Sangwan, 2019), nationality, social roles, economic activities, intra-household distribution (Kabeer, 1994; Sell & Minot, 2018; Sen, 2009; Trommlerová et al., 2015), and financial literacy (Nawaz, 2015). Therefore, it is worth mentioning that the role of microfinancing in women’s empowerment may also be influenced by various demographic features. Outside of the study conducted by Rahman et al. (2009), the role that the demographic attributes of microfinance clients plays in female empowerment has never been studied in the literature.

To promote women’s empowerment and attain SDGs, the identification of the dynamic microfinance, individual, household, and community factors influencing such empowerment is essential. Therefore, this study aims to examine the influence of microfinancing on women’s empowerment in Bangladesh and also identifies the demographic factors affecting the relationship. This study deviates from the Rahman et al. (2009) study in two major ways. First, Rahman et al. (2009) employed a control group method, as opposed to our case study method. Second, the authors studied the effects of microfinancing on general empowerment, while we considered female empowerment from economic, social, political, and psychological dimensions while employing Kabeer’s (1999) frameworks for resources, agency, and achievement.

Women’s empowerment in a developing country like Bangladesh is of great importance, as 17.6% of its citizens live in abject poverty. Of these impoverished citizens, nearly 40% are women, with approximately 30% being both economically and socially impoverished (M. Hossain et al., 2019). According to the United Nations Development Programme (UNDP, 2018), Bangladesh ranked 134th amongst 187 countries in the hierarchy of gender inequality. These statistics, therefore, suggests the need to achieve gender equality in the country through the empowerment of women. Moreover, Bangladeshi women are perceived to be less empowered than men, owing to their high involvement in activities with no monetary value in the mainstream economy (M. Hossain et al., 2019). In addition, Bangladesh is still ranked very lowly in terms of women’s empowerment, despite being considered the origin and haven for microfinance-related studies, which justifies the need to examine the relationship between microfinancing and female empowerment in the country.

This study contributes to the existing literature in the areas of microfinance and women’s empowerment in several ways. First, it identifies the key demographic factors influencing the role of microfinance on this type of empowerment. Second, it administers an in-depth case study method to identify the influence of microfinance in women’s empowerment. This contrasts with the quantitative method adopted in earlier studies, which may not present an in-depth picture. Third, to understand the perception people have about women’s empowerment, 20 female microfinance clients were interviewed, along with male members of their families. Finally, for the first time, this study employs the resource, agency, and achievement frameworks in investigating the influence of microfinancing on the different dimensions of women’s empowerment. Such frameworks help to break down the various dimensions and determine which is influenced by microfinancing the most.

The remainder of the paper is structured as follows: the second section presents the literature review; the third section, the conceptual framework of the study; the fourth and fifth sections, the research design and findings, respectively; the sixth section, the discussion of the findings; and the seventh section, which includes the conclusion of the study.

Literature Review

The literature review summarizes five themes, which are organized into the following subsections: (i) a background study on Bangladeshi women, (ii) microfinance and women’s empowerment, (iii) the determinants of women’s empowerment, (iv) the measurement of women’s empowerment, and (v) the Grameen Bank (GB) model.

A Background Study on Bangladeshi Women

Bangladeshi women have been observed to endure the most societal barriers, restrictive gender norms, and social customs of anyone around the world (M. Hossain et al., 2019). They have had to endure the dominance of men in their households, and have little agency in their choice of jobs, sexuality, spouses, movement, savings, assets, and sources of income, which are determined through legal bodies and local decision-making (M. Hossain et al., 2019). The legal bodies and decision-making authorities in rural Bangladesh are comprised of the village court and family head, respectively (M. T. Islam, 2019). The village court is organized by union parishad, which is local government and the smallest rural administrative unit in Bangladesh. The village court informally resolves disputes through a local tribunal known as the Shalish. The Shalish is governed by the local power structure, social norms, and formal judicial system of the country (M. T. Islam, 2019). Despite the great emphasis placed on gender equality in the constitution of the Articles 19 and 28, women encounter discrimination via state legislation and institutional advocacy favoring gender subordination and dependence (Alim, 2009; M. Hossain et al., 2019). Pitt et al. (2006) claimed that, in Bangladesh, 78% of women were forced to surrender their money to their husbands, while another 56% were prevented from even working outside their homes (Goetz & Gupta, 1996). Goetz and Gupta (1996) also noted that women were only permitted by their husbands to participate in microfinance programs to obtain loans. In recent years, there has been improvement in the participation of Bangladeshi women in economic activities, which stems from the increase in employment opportunities due to rural road infrastructure projects (Khandker et al., 2009), the readymade garment industry (Feldman, 2009), and involvement in microfinance activities (Kabeer, 2005; Schuler et al., 1996). The government’s initiative to improve female education has also played a significant role in elevating the status of Bangladeshi women (Asadullah et al., 2014).

Despite the improvement in women’s involvement in economic activities, the life choices and empowerment of women in rural areas are still constrained by traditional gender norms, patriarchal attitudes, purdah norms, and seclusion from the public (Asadullah & Wahhaj, 2019). In addition, reproductive responsibilities and gender-specific burdens—like unremunerated house chores—further inhibit them from engaging in paid employment (Mahmud, 2003). Most of the income-generating activities of women residing in rural areas are located in the home environment and are funded by microfinancing. The overall rate of women’s empowerment remains low, as highlighted in the country’s Human Development Index rank (134 out of 187 countries). Due to such contradicting trends in gender norms in Bangladesh, an empirical analysis of women’s empowerment, particularly focusing on those involved in microfinance, is long overdue.

Literature on Microfinance and Women’s Empowerment

Previous literature has highlighted access to credit as a critical aspect of women’s empowerment. According to the empowerment theory, women require credit facilities to be involved in economic activities (Hashemi et al., 1996). Poor women have very limited access to loans in credit institutions, owing to their lack of creditworthiness (Nader, 2008). The research project carried out by Professor Mohammad Yunus in 1976 reveals that microloans offered to poor households, especially to women, could greatly contribute to their well-being and empowerment. Additionally, it has also been observed that women tend to repay credit facilities reliably under the mechanism of group lending and the mutual guarantee of group members (Khalily et al., 2010). Past studies have highlighted microfinancing as an important tool for poverty alleviation (Wahid & Hasnat, 1993), economic growth (Barr, 2004), economic stability, and women’s empowerment (Hashemi et al., 1996). Microfinance programs based on empowerment mainly target women, as they tend to be more trustworthy and have a greater social impact (Tsiboe et al., 2018). These advantages are evident in the loan repayment rates of female borrowers, as such microfinance clients tend to have a better repayment history than their male counterparts (Rosenberg et al., 2009).

Portes et al. (2019) claimed that, by empowering women, issues of poverty and income inequality would decline, ultimately resulting in an improvement of household well-being and food intake. Similarly, Mayoux (1998) suggested that women’s access to microfinance services is a precondition for the alleviation of their poverty and the fostering of their empowerment. As a result, microfinance as an empowerment tool is garnering interest and popularity under the aegis of policy development. Therefore, to reduce gender inequality and improve economic growth, the empowerment of women via access to microfinance services should be emphasized. Since empowerment is the process of granting an individual the authority, power, or control over their life or situation, women’s empowerment is described as the expansion of their abilities to make important life choices and exercise agency that was previously unavailable to them in their daily lives (Kabeer, 2001; Schuler & Rottach, 2010).

The influence of microfinance on women’s empowerment is widely debated in recent literature (Mersland et al., 2019; Wang & Ran, 2019), as some studies have recorded a positive impact, while others discovered the exact opposite. Al-Shami et al. (2018) and Li et al. (2011) remarked that microfinancing empowers women, fosters gender equality, and increases their participation in both income-generating activities and household decision-making processes, which ultimately influences their economic and social empowerment. In a similar vein, Weber and Ahmad (2014) also observed that women who had higher loan cycles tended to be more empowered. The univariate analysis employed in the study suggests that higher loan cycles affect the ability of female microfinance clients to decide on the use of requested loans, since loan use was considered an important indicator for financial empowerment (Kabeer, 2001). Jamadar (2014) reported that the involvement of women in microfinance has resulted in improving their confidence and expanding their social networking atmosphere, both inside and outside of their communities. Consequently, they have won local government elections and have been subsequently recognized by local government officials and political leaders. They have also become involved in the management and decision-making functions of society.

On the other hand, Garikipati (2008) highlighted that microfinance loans, especially those granted to female clients, were mainly used to increase household assets or income. She remarked that, owing to patriarchal norms and existing socio-cultural practices, women merely use loans to pay household expenses, thereby actually leading to their disempowerment. Ganle et al. (2015) reported that, although microfinancing empowered some women to certain degrees by equipping them with the credit facilities necessary for business activities, some were not empowered; instead, those women experienced harassment and abuse. They further remarked that women who have either limited or no control over their loans were incapable of empowering themselves. Dichter (2007) established that microfinance funding was primarily utilized for debts and consumption, rather than for real income-generating activities. Copestake et al. (2002) and Morduch (1998) also discovered that a dependency on microfinancing will result in an excessive workload and contribute to domestic violence against women, which will, in turn, impede women empowerment. Overall, no conclusive evidence exists showing the empowerment of women by microfinance institutions. Therefore, the topic is subject to further in-depth analysis.

Key Determinants of Women’s Empowerment

Women’s empowerment is influenced by several factors. Saha and Sangwan (2019) identified the position of male children (particularly the eldest) in the family as a factor influencing female empowerment in India. In another study conducted by Yount et al. (2018), marriages that were carried out at a legal age (18+) tend to positively influence women’s empowerment. Bushra and Wajiha (2015) suggested that the level of education, economic participation, poverty level, availability of economic opportunities, and possession of bank accounts influence women’s empowerment positively. Suwana (2017) also revealed that digital media literacy promotes their empowerment, contrasting the usual effects of inadequate education, lack of opportunities, and the presence of a patriarchal system. Also, the available level of education, training, leadership, and opportunities for personal growth all also determine the level of women’s empowerment, according to Bowen and Miller (2018). Anderson and Eswaran (2009) also corroborated this claim by revealing that earned income gives women more autonomy and empowerment than unearned income. In the same vein, information communications technology (ICT) has also been observed to have a great impact on social capital and self-efficacy, which, in turn, contributes to female empowerment (Crittenden et al., 2019).

In her study, Nader (2008) remarked that MFIs contribute positively to women’s socio-economic well-being in the areas of children education, income, and the ownership of assets. She further claimed that MFIs play a significant role in the eradication of poverty and improvement of family well-being. The aforementioned literature supports the general assumption that microfinance has an impact on women’s socio-economic welfare, although the existence of other factors must be acknowledged. Additionally, Rahman et al. (2009) reported that microfinance has an indirect effect on women’s empowerment based on factors such as age and levels of education and income. In a similar vein, Noreen (2011) highlighted microfinance as influencing their empowerment through factors including age (Jejeebhoy, 2000), level of the husband’s education, status of the family head (Roy & Niranjan, 2004), inherited assets from the family, marital status of the woman, and the number of male children alive. She also claimed that the loans utilized by females resulted in better outcomes compared to those utilized by males. In addition, Nawaz (2015) highlighted the significant relationship between financial literacy and women’s empowerment, arguing that a combination of microfinancing, financial literacy, and training could significantly transform the economic positions and power relations of women.

In summary, microfinance is capable of influencing women’s empowerment both directly and indirectly. Past studies have revealed that its effect on such empowerment is also influenced by a couple of other factors. It is unclear, however, as to which factors play particularly crucial roles. Therefore, to determine the overall level of empowerment, different dimensions of women’s empowerment (economic, social, political, and psychological) need to be identified and examined. In this regard, this study aims to examine the experiences of female microfinance clients to ascertain whether the microfinancing itself or the clients’ demographic characteristics contribute to their economic, social, political, and psychological empowerment.

Measuring Women’s Empowerment

Women’s empowerment—the process of increasing women’s autonomy and control over personal and household decision-making—increases their ability to transform different dimensions of their lives (Akram, 2018). The various dimensions of this empowerment have been developed, each encompassing different constructs of their lives, including economic, interpersonal, socio-cultural, political, and psychological empowerment (Malhotra et al., 2002), each an essential aspect of life. While an understanding of the concept of empowerment is of the utmost importance (Saha & Sangwan, 2019), a standardized tool for the assessment of empowerment is still nonexistent (Malhotra et al., 2002). Feminists and economists have proposed various approaches to female empowerment, such as the change (Rowlands, 1995), power (Mayoux, 1997), and capability approaches (Sen, 2009). The UNDP’s Human Development Report (UNDP, 2018) also introduced two complementary indices: the Gender-Related Development Index and the Gender Empowerment Measure. These indices, along with the aforementioned approaches, remain deficient, as they do not account for the identification of real power (Bardhan & Klasen, 1999), real change, and real visibility (Swain, 2007). Similarly, both Mahmud (2003) and Khan and Maan (2008) also reported the absence of a uniform yardstick for the assessment of women’s empowerment, since empowerment is a context-specific construct that may vary from one socio-cultural scenario to another (Kabeer, 1999). Therefore, a different approach has been adopted to measure the various dimensions of empowerment. In this regard, Kabeer (1999) suggested that the dimensions of empowerment must be evaluated by integrating and comparing the factors of resources, agency, and achievement; resources are social and material resources, agency entails the processes of decision-making, and achievements are the various outputs (e.g., improved well-being and increased political participation) attained from the agentic use of resources.

Grameen Bank

The study adopted a single-case approach in which Grameen Bank (GB) was considered, as it represents a specialized and pioneering MFI among the 731 active MFIs in Bangladesh (MRA, 2018). GB (2017) accounts for 25% of the 26 million total microfinance clients in Bangladesh. The growth of the bank is very progressive, and, as of December 2017, it had extended its lending services to 1,381,103 groups from 140,262 centers under 2,568 branch level offices located in 246 areas and 40 zones across the country. The bank’s network encompasses 81,400 villages—over 93% of the country’s 87,362 villages. The expansion of women’s numbers in terms of loan distribution is also impressive, and, as of December 2017, there were 8,934,874 cumulative members in the organization, of which a staggering 8,635,961 were women. At the end of 2017, women accounted for 97% of all members, indicating the GB’s focus on women and their empowerment.

In addition to Bangladesh, GB has extended its operations to over 50 countries across Asia, Europe, Africa, Oceania, and the US (Suzuki et al., 2011). Grameen Bank helps to reproduce its model through its offshoot, the Grameen Foundation. This foundation established the Grameen Bank Replication Program to provide the financial and technical resources needed to assist in the launching of new microfinance programs. The bank earned a net profit of USD 28.08 million, declaring a 30% cash dividend for its shareholders in 2017 (GB, 2017).

Grameen Bank originated in 1976 as an action research project adjacent to the University of Chittagong, aimed at modeling a credit facility that could provide capital to the poor for productive self-employment. The GB was formally established by the Bangladeshi Government in 1983 as a specialized financial institution providing collateral-free microcredit to the poor in rural Bangladesh; its members are also its borrowers, holding 75.19% of the shares. The remaining 24.81% are held by the Bangladeshi Government, Sonali Bank Ltd., and Bangladesh Krishi Bank. The GB requires individuals requesting a loan to own either less than a half acre of cultivable land or assets not exceeding the worth of one acre of land (M. Hossain, 1988). The bank issues collateral-free loans to borrowers with a structured interest rate, as presented in Table 1.

Interest Rate of Grameen Bank Loan for Different Loan Categories.

Source. GB (2017).

Table 1 shows that the bank charges a 20% interest rate on loans for income-generating activities, 8% on housing loans, and no interest charges on higher education loans during the study period (but 5% afterwards). The bank grants loan provisions to struggling members such as beggars, offering them loans with zero interest. In addition, it calculates interest based on a declining balance method to ease its borrowers’ debt repayment burdens.

Grameen Bank model

The GB model was conceptualized by the Nobel laureate professor and economist, Dr. Mohammed Yunus, who eventually established the Grameen Bank. After the successful launch of the GB pilot project, the GB model became the standard for microfinancing in most parts of the world. A unit covering an area of between 15 and 22 villages was set up, in which the field manager supervises a group of bank officers. Subsequently, the bank manager and officers survey the area, acquainting themselves with the environment to identify potential clients. The bank officers then proceed to explain the objectives, functions, and working procedures of the bank to the local folks. In awarding loans to clients, several steps are followed. First, a group of five prospective borrowers is formed, of which only two are initially eligible for the loan. Thereafter, the officers closely monitor the group for a month to ensure their compliance with the bank’s rules and regulations. If the first two borrowers can repay the loan within a period of 50 weeks, the remaining members of the group also become qualified for loans. Under this practice, the pressure to be keep their records clean exists among the individuals, and this pressure acts as the loan collateral.

Conceptual Framework

Figure 1 shows the conceptual framework, depicting the relationship between microfinance and the key determinants of women’s empowerment, such as age, education, family type, financial literacy, and training. Here, various dimensions of women’s empowerment were considered, in line with the empowerment framework of Kabeer (1999).

Conceptual framework.

Despite microfinancing being an effective tool for women’s empowerment, there is a dilemma stemming from the differing positive and negative influences microfinancing has on such empowerment; thus, this validates the need for further investigation. In addition, whether or not microfinancing affects different dimensions of women’s empowerment is influenced by key determinants (age, level of education, family type, and financial literacy and training) is yet to be identified. This study also identifies the major determinants affecting the relationship between microfinance and empowerment. The framework used by Kabeer (1999) was adopted in the assessment of women’s empowerment, and, thereafter, the three dimensions of empowerment—resources, agency, and achievement—were considered. In this context, the access to resources demonstrates economic empowerment, organizational capacity through agency indicates social empowerment, and achievement indicates political and psychological empowerment. According to Kabeer (1999), empowerment is the totality of economic, social, political, and psychological empowerment; therefore, our framework considered activities and resources as input, agency or the exercise of power in the presence of resources as the process, and the achievement is the outcome of the combination of resources and agency (Sen, 2009).

Methods

Previous studies investigating the relationship between microfinance and female empowerment in Bangladesh, such as Hashemi et al. (1996), Morduch (1998), Khandker (2005), and A. Islam et al. (2015), were quantitative in nature, and, therefore, could not capture the experiences and perceptions of the female borrowers. This study, however, explores how microfinancing and the demographic factors of female borrowers influence women’s empowerment by analyzing the experiences and perceptions of actual female borrowers in Bangladesh. We argue that a more comprehensive study on the perspective of female microcredit borrowers is an essential starting point for supporting empowerment through better-directed microcredit financing. Hence, a qualitative approach has been deemed suitable for this research, as it better provides an in-depth understanding of the perception of relevant female clients. This study administered this qualitative approach by employing a case study method on female clients from GB.

Data Collection

To examine the influence of microfinance on women’s empowerment, this study collected data from female GB clients and male members of their families, as well as conducting a focus group discussion and observation. Data was obtained from respondents during the period between July 2017 and February 2018. A semi-structured questionnaire (attached in Supplemental Appendix A) was used to conduct an in-depth interview with the respondents, following the work of Nwokoro and Ogba (2019). The interviews were held in a conducive setting: the respondents’ houses at agreed-upon times. An informal verbal consent was sought from the participants before data collection, as the concept of written consent was alien to the villagers. Each interview spanned a duration of 50 to 60 minutes.

In accordance with the studies conducted by Denzin (2001) and for credibility’s sake, this study employed different triangulation techniques to observe interrelated phenomena from different perspectives. First, the various methods of data collection—observations, interviews, focus group discussions, and document analysis—were triangulated. Second, we also triangulated the theories we would employ. Lastly, data sources were triangulated in an attempt to verify similar sets of evidence drawn from different sources, such as the knowledge held by different people about the studied phenomena, documents, public records, personal papers, and photographs, among other sources. To avoid potential bias and dependency issues, special care was taken considered to eliminate pressure and tension for the participants. The participants were also familiarized with the Code of Ethics when making their choice to be a part of the study. The researcher only proceeded to interview those who volunteered, also providing them with an open and conducive setting for the honest and confident expression of their thoughts.

The semi-structured questionnaire prepared for the interview was composed of different sections, each concerning different dimensions of women’s empowerment. First, it requested the demographic information of female microfinance clients (name, age, education, marital status, family type, primary and secondary activities, number of children, level of schooling, and husband’s educational level and profession). After that, the questionnaire proceeded to request information regarding their level of income, number of income earners in the house, and their need for microfinancing. This section is succeeded by the empowerment constructs of the questionnaire, in which inquiries are made about resources to identify the client’s economic empowerment, which is determined by considering economic security and control over loan utilization and management. Subsequently, information about agency was requested to identify social empowerment, which is comprised of mobility in the public domain, women’s small and large-scale purchasing behaviors, the management of family assets, involvement in major decisions, relative freedom from domination by the family, and spousal violence. Finally, questions relating to achievement were asked to determine the participants’ political and psychological empowerment, and was measured in terms of political participation, political and legal awareness, participation in public protests and social supports, access to media and phones, and their self-efficacy.

The data for this study was obtained from the centers of Salimpur and Unsattorpara in the Chittagong district of Bangladesh due to their easy accessibility from the city of Chittagong. In addition, a study in Chittagong provides important background for research on microfinance and women’s empowerment, as it represents the birthplace of microfinancing and is also identified as a traditional and patriarchal society (M. Hossain et al., 2019). Therefore, identifying the influence of microfinancing on female empowerment in such a society would be very revealing.

Following the findings of Rehman et al. (2015), we employed convenient sampling in the selection of 20 cases due to limitations in time and budget. Besides, Coyne (1997), and Emory and Cooper (1991) all argued that convenient sampling was an appropriate technique for drawing samples from large populations. The entire process of data collection took place over 2 months, with the most important interviewees coming from the Unnosattorpara branch, as opposed to the Salimpur branch, where poor quality responses were recorded. This poor response was due to their shyness, busy schedules, and disinterest in the interviews, as some women were concerned that the interview may hamper their subsequent loan approval process. One such response states, “I have nothing to say. Whatever you need to ask, simply ask the bank officer sir, as we are unsure of what might happen subsequently” (Interviewee; GB, Salimpur).

Regardless, 5 women from the Salimpur branch and 15 women from the Unnosattorpara branch participated in the study.

Data Analysis Process

The main objective of this study is to explore the influence asserted by microfinancing and the demographic factors of GB clients on women’s empowerment. To fulfil these objectives, the researchers created nodes and subnodes in NVivo 10 for all important dimensions and aspects related to microfinance and women’s empowerment, while considering the important themes and feedback of the respondents. For the coding process, the researchers combined deductive and inductive approaches. During the field study, it was observed that four factors were crucial in the analysis of data: age, family type, level of education, and financial literacy and training. Hence, all charts were prepared using one of those attributes and their probable impacts on one or more elements of women’s empowerment. Similarly, two attributes were selected against one or more dimensions of the empowerment in question. Next, the researchers created treemaps, which were used to compare the nodes based on the number of references they contained and their important features, using colors and box sizes to visually display the response trends of the participants. Meanwhile, matrix coding queries were run to obtain important patterns based on references to certain words in text search queries, visualizing the words with a word tree that compares the respondents’ comments based on demographic attributes.

Results and Findings

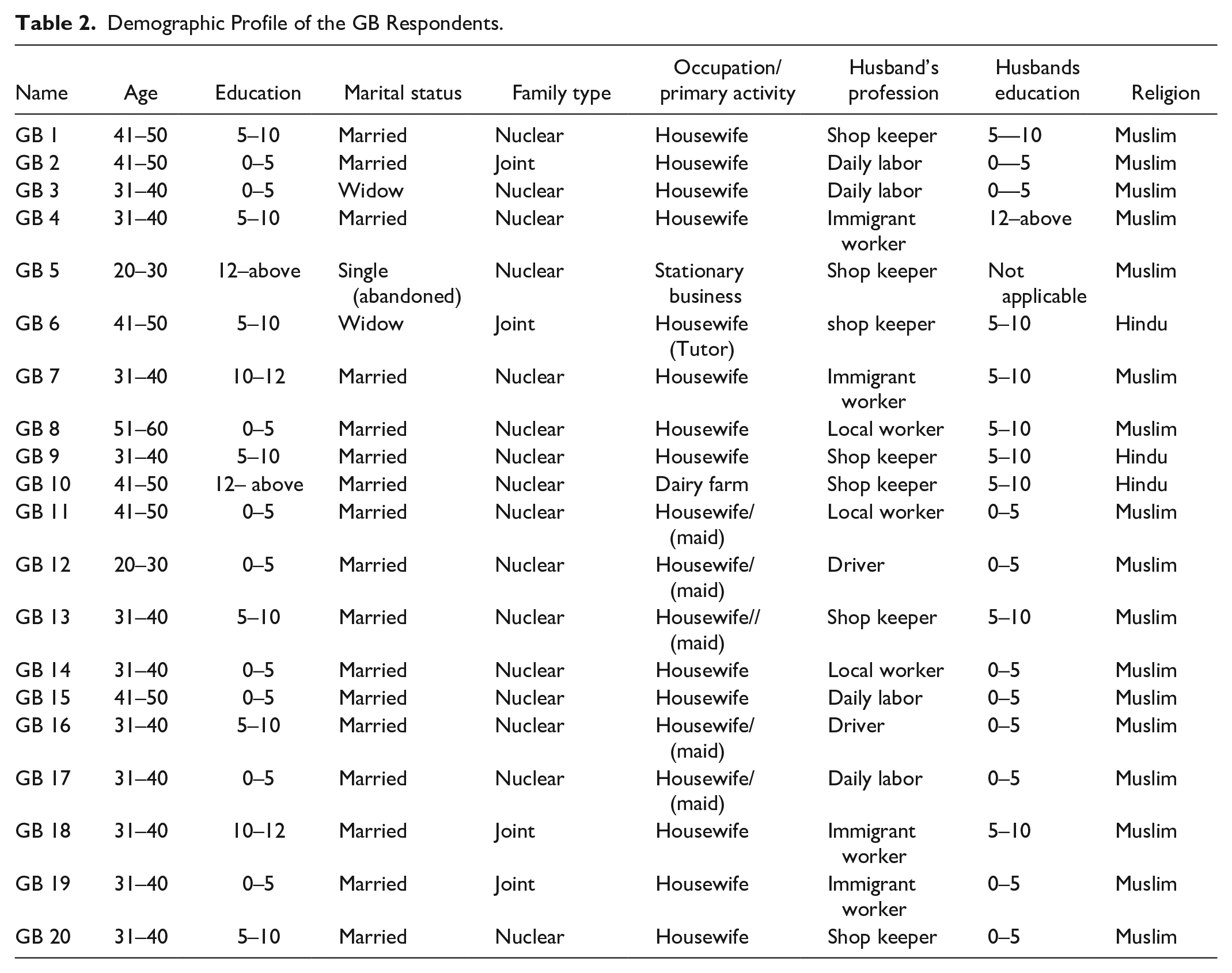

Table 2 presents the demographic characteristics of the interview participants. The variables considered here include age, education, marital status, family type, occupation/primary activity, husband’s profession and education, and religion.

Demographic Profile of the GB Respondents.

Table 2 shows that the respondents belong to four age groups: 20 to 30, 31 to 40, 41 to 50, and 51 to 60 years. This table further reveals that the majority of the respondents (55%) were within the 31 to 40 age range; followed by 30% falling within 41 to 50; and, lastly, 15% were from the age ranges of 20 to 30 and 51 to 60, indicating that most respondents in this study were young and energetic. Table 2 shows the respondents’ levels of education, which were categorized into four groups: 0 to 5th grade, 5 to 10th grade, 10 to 12th grade, and 12th grade and above. All 20 respondents were married, and, among the 20, 2 were widowed and 1 was single due to being abandoned by her husband. Table 2 further reveals that all the respondents either belonged to a joint or nuclear family. About 16 respondents (80%) were from nuclear families, while the remaining 4 (20%) were from joint families. Table 2 also shows that the majority of the respondents (90%) were housewives, while only 2 (10%) were engaged in entrepreneurial activities, such as stationery businesses and dairy farms.

In line with the objectives of this study, female borrowers were interviewed to investigate their levels of empowerment as the result of microfinance programs. Following the framework established by Kabeer (1999), resources, agency, and achievement were considered as the three dimensions of empowerment. These dimensions are subsequently described based on themes identified from the field of study.

Economic empowerment

In order to assess economic empowerment, we have considered economic security, control over loan utilization, and general management of the borrowers.

Economic security

With regards to the ownership of households or residences, most of the replies were either “inherited homestead is owned by husband” and “no ownership.” As for the ownership of productive assets or income, the majority of the participants remarked that their assets or incomes were either family-owned or owned by their husband, with some possessing none. For questions concerning cash savings, the replies ranged from having a deposit pension scheme (DPS) in GB, to small amounts of savings in GB, to no savings at all. When asked about the use of cash savings for businesses or other productive purposes, many responded that their savings were utilized for their husbands’ treatment, shops, vans, and consumption.

From Table 3, it is noticeable that 12 (60%) of the respondents had no ownership over their residences. During the field study, a respondent claimed that her husband inherited a residence, but had yet to receive his portion due to some rules on the division of properties. She remarked, “There are lots of landed properties in my in-laws’ village house, which are yet to be shared. Due to that, we do not own any property for personal use” (Interviewee; GB 7).

Detail Responses on Economic Security.

On the other hand, 4 respondents (20%) said they were living in houses owned by their husbands, while another 2 (10%) were staying in houses inherited by their husbands.

With regards to the ownership of productive assets, 11 (55%) confirmed not having any productive assets; another 7 (35%) claimed that their husbands or families owned a productive asset, and, of those 7, 4 (20%) of the respondents’ husbands owned a van, shop, or compressed natural gas (CNG) as productive assets, while the families of the remaining 3 (15%) owned a rice mill, a tree plantation, and a CNG garage. Lastly, 2 (10%) women in this study confirmed that they own productive assets such as a shop, training center, or dairy farm.

In the GB field study, it was observed that MFIs had an impact on the attitude respondents held toward savings, as almost all of them had cash deposits with the GB. To corroborate this, a GB bank officer remarked, “There is a different saving scheme for borrowers to encourage savings and ensure their security.”

This was also suggested by the Microfinance Regulatory Authority (MRA, 2018) to encourage microfinance borrowers to open savings accounts. The clients’ attitudes about saving is depicted in the GB’s total savings of BDT 128.83 billion (USD 1.61 billion), a figure highlighted in their annual report (GB, 2017). Although 7 respondents (35%) in the field study denied having any personal savings, 13 (65%) confirmed otherwise. Besides, borrowers with savings were further categorized into those with small amounts of savings in GB (4, or 20% respondents), monthly DPS in GB (4, or 20% respondents), and both DPS and fixed deposit (FD) in GB (5, or 25% respondents). One of the respondents remarked, “I have an FD and DPS in the GB, and other saving schemes with GB” (Interviewee; GB 5).

This study confirms that the GB encourages its members to save under different schemes. With regards to the disbursement of cash savings, only one woman (5%) claimed to had spent it on herself or for income generation, while others claimed otherwise. Moreover, most of them confirmed that they mostly spent their savings on consumables, medical bills, and for their husbands’ income generation purposes. This confirms the selfless and submissive nature of Bangladeshi women (Amin et al., 1994). About 11 respondents (55%), however, confirmed to have not expended their cash savings, while 7 (66%) lacked cash savings altogether. On the contrary, 8 (40%) respondents revealed that they expended their cash savings for the fulfilment of their husbands’ necessities and the family’s expenditure or consumption, while 2 (10%) reported expending their savings on their husbands’ treatment.

Another three women (15%) confirmed having expended their savings on their husbands’ businesses, with one of them providing the following feedback: “I gave up all my savings for my husband’s business, and, this time, it was to procure a van” (Interviewee; GB 16).

Another woman (5%) exhausted her savings on family expenditures and consumption, explaining, “Whenever I save some money, I end up spending it on family needs. There are several instances of emergent needs in the family. Sometimes, I have to expend my savings on necessities in the household” (Interviewee; GB 7).

The summary in Table 4 on economic security highlights that only two women (GB 5 and GB 10) have their own residence and land. These two women (10%) also have their cash savings, which they use for their business expansion. Also, 13 of the respondents (65%) have their cash savings, with 1 of them (5%) using it for business and productive purposes. From the table presenting data on economic security, it is confirmed that GB encourages cash savings. The influence is not substantial in all aspects of economic security, however, as only five respondents (20%) have better economic security—an established indicator of women’s economic empowerment and their control over income and assets (Johnson et al., 2016). The findings of this study fail to confirm the impact of microfinance on women’s economic security, though; therefore, these findings disagree with the observation of Hashemi et al. (1996) that microfinance has a positive impact on women empowerment.

Summary of the Responses on Economic Security.

Control over loan utilization and its general management

The results of the case of control over loan utilization and general management are presented in Tables 5 and 6.

Detail Responses on Control Over Loan Utilization and Management.

Summary of the Responses on Control Over Loan Use and Management.

The summary in Table 6 shows that 55% of the women knew the sources of input and productive assets; 20% were aware of the procurement; 40% were aware of the cost and production processes; 30% were acquainted with the price and output or market destination; 45% were familiar with the problems involved in the production process; and 10%—specifically respondents GB 5 and GB 10—were the main users of their loans. It was observed from Table 2 that the respondents used the loans to invest in stationery and dairy farm businesses.

The statements of these two borrowers are reported below:

“I have my land and store, and I was able to accomplish all these after borrowing and owning a business” (Interviewee; GB 10). “I have a half acre of land, a stationery shop, and a training centre, which I singlehandedly acquired without the help of my family members” (Interviewee; GB 5).

On average, only seven of the respondents (35%) have control over or are knowledgeable about loan use and its management. Among these seven women, some of them admitted to not being the major user of the loan, but were aware of how it was utilized, as they were informed by their husband or son, who was the major user.

These findings suggest that microfinancing may not influence borrowers’ control over loan utilization and its management. Therefore, the observations concur with Goetz and Gupta (1996) and Kabeer (2001), but disagree with Hashemi et al. (1996), since microfinance has a positive impact on having control over loan utilization and its general management.

Social empowerment

For the identification of social empowerment, we have included different dimensions of women’s agency, namely decision-making power, freedom of movement, and relative freedom from domination by family and spousal violence.

Decision-making includes the ability to make small purchases or a large purchase, as well as involvement in the major decision-making and management of family assets.

Ability to make small purchases

Tables 7 and 8 present answers from respondents with regards to their ability to make small purchasing decisions (such as items used for daily food preparation, personal items, ice-cream, sweets, or clothes for the children, and simple health care needs) in detail (Table 7) and summarily (Table 8).

Detail Responses on Ability to Make Small Purchase Response.

Summary of Responses on the Ability to Make Small Purchase Decision.

Table 8 shows that 35% of the 20 participants can make small purchasing decisions, while 65% of women lack such ability. In this regard, one of the respondents remarked:

Everything in my in-laws’ house is decided by my father-in-law, regardless of being a purchase decision or other decision. We have to follow the instructions of our father-in-law in every respect. Although my husband is the breadwinner of the house, he has no say. As long as my father-in-law is still active, we have to obey him” (Interviewee; GB 18).

Speaking on this matter, a male member from the respondent’s house asked, “What can women (mohilara) contribute to important family decisions? They do not understand so many things about the outside world” (Interviewee; GB18’s father-in-law).

Ability to make large purchasing decisions

Tables 9 and 10 depict the detailed and summarized responses, respectively, which cover the woman’s ability to make large purchasing decisions, including the decision-making agency of respondents. The summary in Table 10 shows that 55% of respondents can make large purchasing decisions, while 45% cannot. In terms of decision-making agency, the study considered the responses of women participation in discussions among their family or as a couple, including their role in making large purchasing decisions.

Detail Responses on Ability to Make Large Purchase.

Summary of Responses on the Ability to Take Large Purchase Decision.

Regarding women’s participation in large purchase decisions, a respondent replied, “I can select the cow that I wish to purchase, as I am responsible for its maintenance. Moreover, since the cow will be purchased from our neighborhood, it is easier for me to make a selection. Ultimately, my husband handles the income I earn from the cow” (Interviewee; GB 16).

Involvement in the major family decisions

The involvement of women in major family decisions is considered based on the frequency and impact of their decisions on household purchase, house repairs, land leasing, children’s education, health, and marriage.

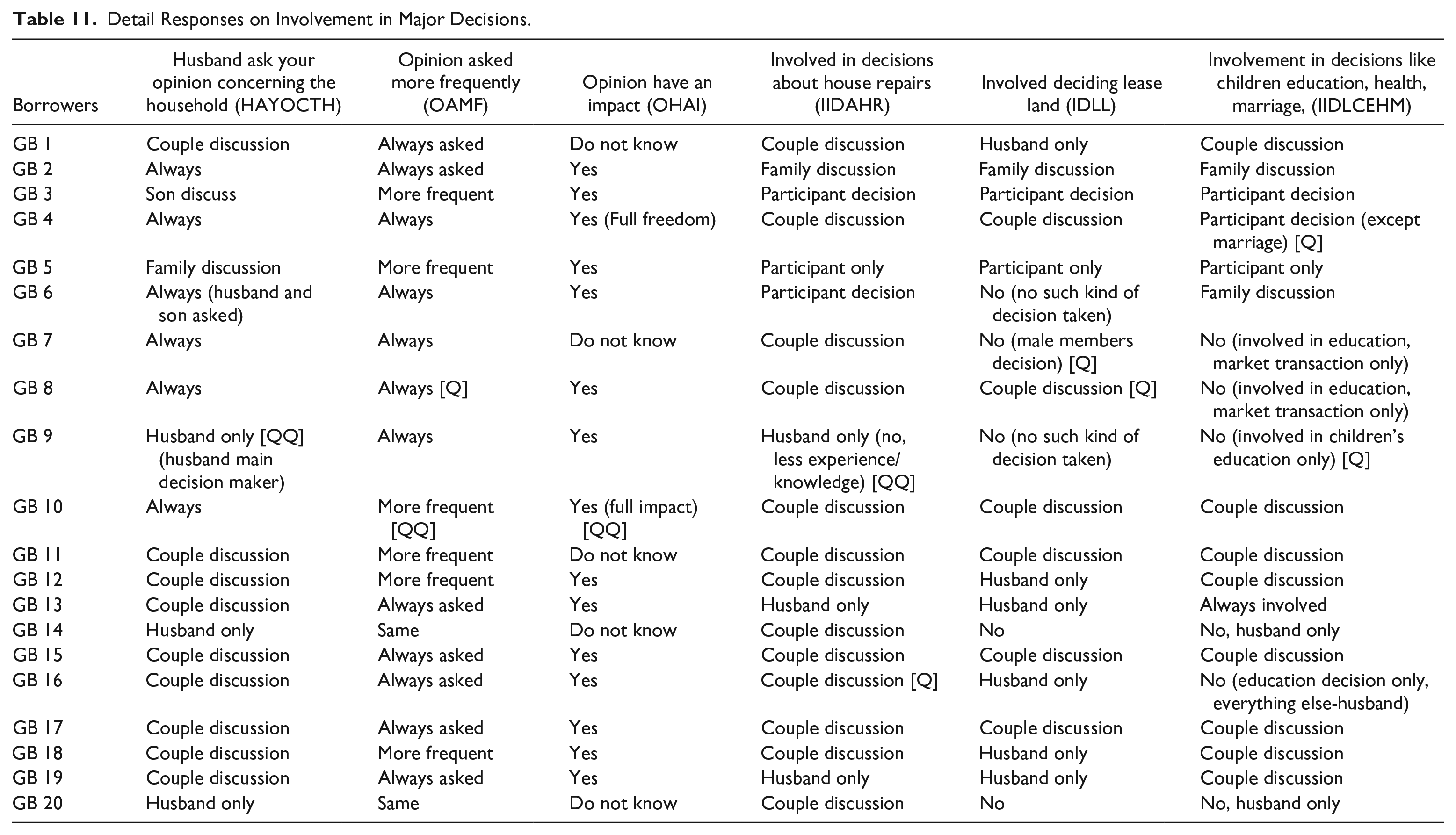

Tables 11 and 12 show the detailed and summarized responses, respectively, to questions of major family decisions. Table 12 reveals that, on average, 65% of women participate in major family decisions. Concerning this, a respondent remarked:

“I have been borrowing money from the beginning of my marriage. I borrow for him, and he, therefore, seeks my opinion in decisions relating to house repairs, children’s education, health, marriage, etc.” (Interviewee; GB 10).

Detail Responses on Involvement in Major Decisions.

Summary of Responses on Involvement in Major Decisions.

On the other hand, 35% of women do not take part in making major family decisions, as their household’s decision power remains within the domain of its male members. Therefore, they do not perceive any changes in their decision-making capacity.

Management of family assets

In terms of the management of family assets, the respondents were asked if they ever fully or partially managed land or other family assets.

Tables 13 and 14 show the responses of borrowers regarding the management of family assets in detail and in summary, respectively. The summary in Table 14 indicates that only an average of 30% of women responded in the affirmative, while 70% reported that the management of family assets is mainly handled by their husbands, sons, and other male family members.

Detail Responses on the Management of Family Assets.

Summary of Responses on the Management of Family Assets.

Freedom of movement

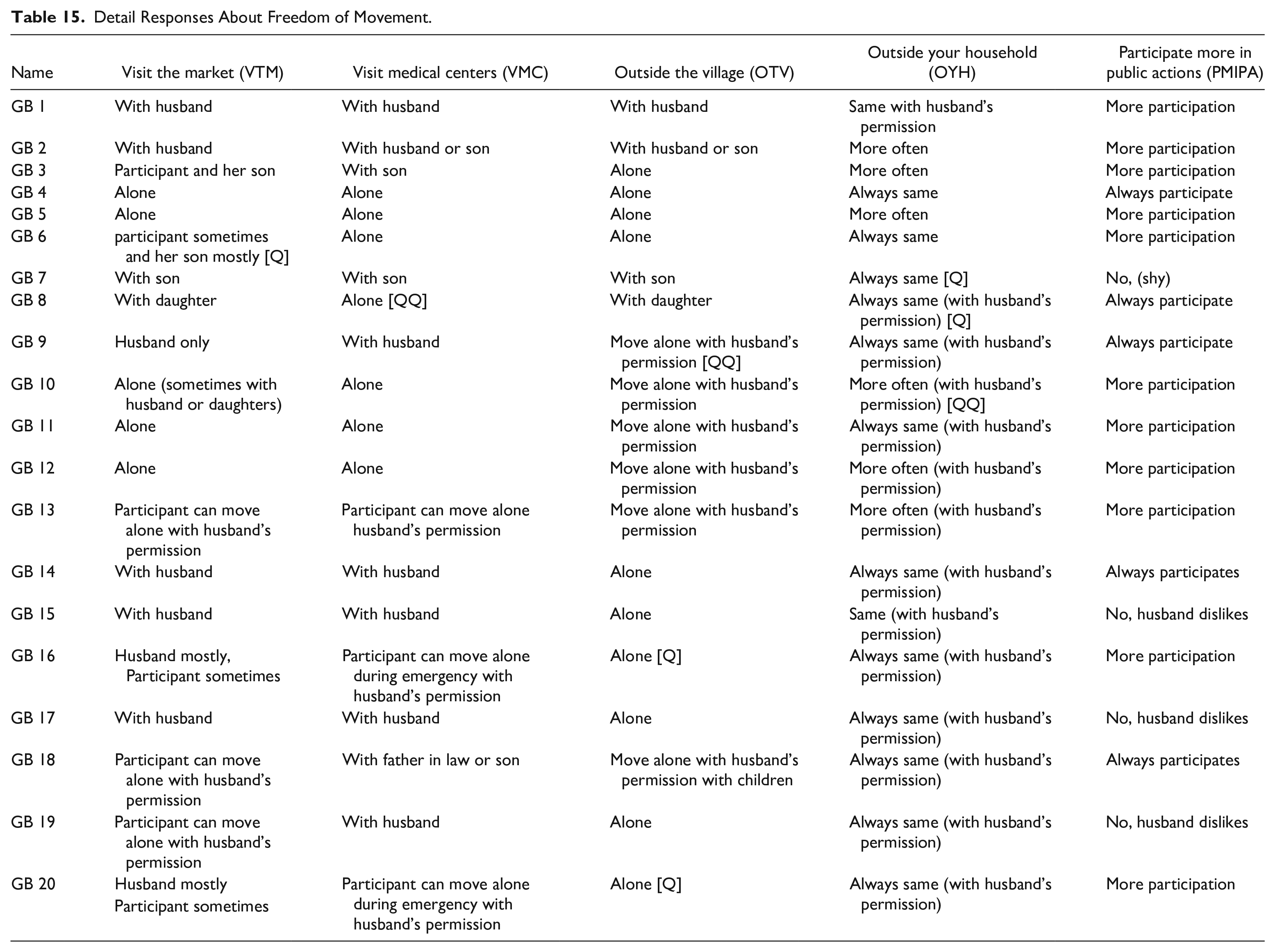

With regards to freedom of movement, the respondents were asked about their ability to independently visit markets, medical centers, and settlements outside the village and households, as well as being able to engage in public discussions.

Tables 15 and 16 exhibit the responses of the borrowers regarding their freedom of movement in detail and in summary, respectively. Table 16 shows that an average of 40% of women had freedom of movement, while 60% were restricted, with their visits being subject to their husband’s approval and/or the availability of someone to accompany her. In this regard, two male members of the interviewee’s family stated the following:

“Women should not go anywhere alone. It is unsafe and indecent for women to move around in our society” (Interviewee; GB 14’s husband). “Why would women go outside alone? She is our daughter-in-law (ghorer bou). We have some dignity (ijjot somman) in society. If our daughter-in-law (ghorer bou) moves around alone, how will people react?” (Interviewee; GB 18’s father-in-law).

Detail Responses About Freedom of Movement.

Summary of Responses About Freedom of Movement.

Voice with the husband and family members

This indicator concerns women’s freedom from domination by the family and from spousal violence, both of which are described below.

Relative freedom from domination by the family

In this indicator, respondents were asked whether money, land, jewellery, or livestock were taken from them against their free will, or if they were prevented from visiting their natal homes or disallowed from working outside their homes.

Tables 17 and 18 show the responses of borrowers with regards to their relative freedom from domination by family in detail and in summation, respectively. Table 18 reveals that 55% of women are relatively free from domination by their families’, while 45% are subjected to the control of their families. Regarding this perspective, a respondent remarked:

My husband prevented me from accepting a job offer on family planning. If I had commenced the job at that time, I would have probably retired now. Nevertheless, the organisation (family planning) has hired people who only studied up to class 6/7. My bad luck, my husband, had prevented me from accepting the job offer, as he was a little kind of different (Interviewee; GB 5).

Detail Responses on the Relative Freedom From Domination by the Family.

Summary of the Responses on Relative Freedom From the Domination by the Family.

Spousal violence

To understand the perception and disapproval of spousal violence by the women, we asked if they had previously encountered physical and verbal violence from their husbands or male members of their families. They were also asked if they ever protested against it.

Tables 19 and 20 present the responses of the participants concerning spousal violence in detail and in summation, respectively. Table 20 illustrates that 35% and 30% of the respondents had never encountered physical and verbal violence, respectively. When asked about their objection against violence, 10% replied affirmatively, indicating that, on average, only 10% of women are free from violence. In our interviews, however, 70% of women confirmed being victims of spousal violence.

Detail Responses of Spousal Violence.

Summary of the Responses of Spousal Violence.

Political and psychological empowerment

The category of political and psychological empowerment examines the respondents’ political participation, political and legal awareness, participation in public protests and social supports, access to media and phone, and self-efficacy.

Political participation

Pertaining to political participation, the women were asked about their involvement in politics, political contests, and campaigns for any political candidate.

Tables 21 and 22 present the extensive and summarized responses, respectively, concerning their political participation. Table 22 shows that only 5% of the respondents admitted to participating in politics.

Detail Response of Political Participation.

Summary of Responses About Political Participation.

On the contrary, 95% of the respondents had never participated in politics, and one of them commented, “No, we are not involved in it, as we do not have any interest in it” (Interviewee, GB 9).

Political and legal awareness

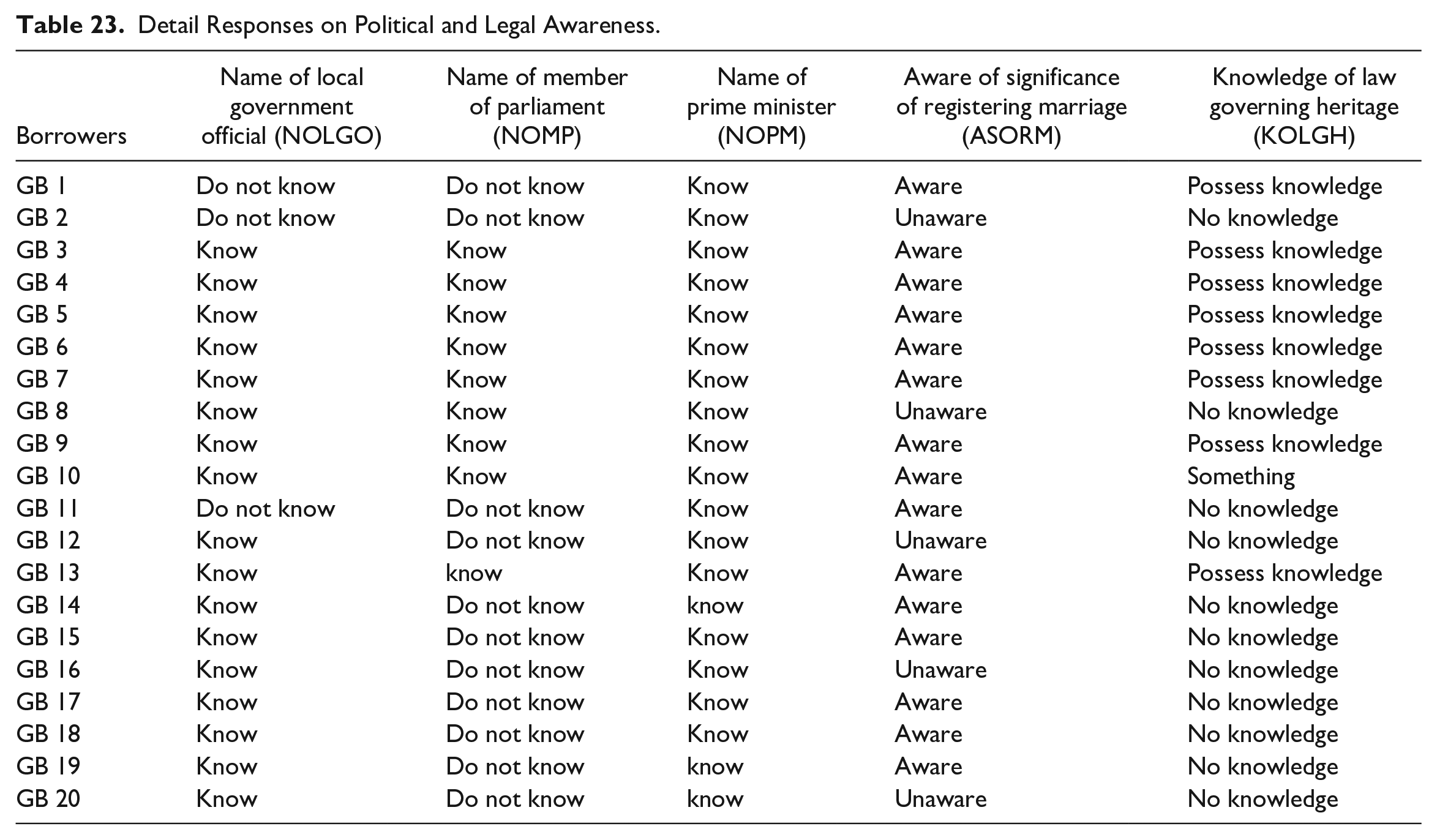

Concerning the respondents’ levels of political and legal awareness, they were asked to name a local government official, member of parliament, and the Prime Minister, as well as to explain the significance of marriage registration and laws governing heritage.

Tables 23 and 24 show the detailed and summarized responses of the borrowers, respectively, with regards to their political and legal awareness. Table 24 shows that 70% of the respondents have political and legal awareness, while 30% this same awareness.

Detail Responses on Political and Legal Awareness.

Summary Responses on Political and Legal Awareness.

Participation in public protests and social supports

Concerning participation in public protests and social supports, respondents were asked about publicly participating in protests against incidents such as men’s abusive behaviors and spousal abandonment, unfair wages, unjust price hikes, misappropriation of relief goods, and the high-handedness of government or police officials.

Tables 25 and 26 show the detailed and summarized responses of clients, respectively, with respect to their participation in public protests and social supports. Table 26 highlights that only 5% of the respondents participated in public protests and social supports. On the other hand, 95% were not involved in public protests and social supports, and, in this regard, one of them remarked, “We are not involved in any trouble! Those of us who applied for a loan and repayment process cannot pay attention to anything else. We only have one thing in mind: how can we return the loan?” (Interviewee; GB 9).

Detail Responses of Participation on Public Protests and Social Support.

Summary of the Responses on Participation and Public Protests.

Access to media and phone

Regarding access to media .and phones, respondents were quizzed about their access to handphones, television, radio, and newspaper.

Tables 27 and 28 show the responses of the borrowers when asked about access to media and phones, both in detail (Table 27) and in summary (Table 28). Table 28 shows that, on average, 65% of respondents have access to media and phone. Concerning that, one of them replied, “I have a handphone in the house which I use to communicate with my husband, who stays at the shop while we remain at home” (Interviewee; GB 9).

Detail Response About Access to Media and Phone.

Summary of Responses on the Access to Media and Phone.

On the other hand, 35% of respondents reported that they lack access to media and phone. In this respect, one woman mentioned, “I use my husband’s handphone for communication and other purposes, as I do not need it that much. Besides, my husband does not like that I keep a separate phone” (Interviewee; GB 1).

Another woman stated that she had access to the television and handphone, but could not read the newspaper due to her limited education.

Self-Efficacy

Self-efficacy indicates the respondents’ confidence and propensity to engage in conversations with community and family members.

Tables 29 and 30 depict the responses of participants when asked their self-efficacy, both in detail and in summation. Table 30 illustrates that only 25% of the women had discussions before their communities and 60% of the women did the same with their families. In addition, 30% possessed the confidence to engage in conversations in the public domain.

Detail Responses on Self-Efficacy.

Summary of Responses on the Self-Efficacy.

Furthermore, the demographic characteristics of the respondents were presented through graphs, treemaps, and queries, which were used to explain the influence demographic characteristics have on the empowerment of microfinance clients.

Figure 2 highlights that women who lived in nuclear families were more authoritative in all three dimensions of empowerment when compared to those in joint families. This may be attributed to the majority of the borrowers (16 of 20) being from a nuclear family, as opposed to the four respondents from a joint family.

Three dimensions of women empowerment according to family type.

In Figure 3, the word “education” has been displayed, showing its link to different terms and how it appears in relation to women’s participation in their children’s educational decisions. The query showed that women from both family types were concerned with making decisions about their children’s education, health, and marriage. In the field of study, when asked whether they had the authority to make decisions on their children’s education, a respondent from a nuclear family remarked:

“Um, yes, I can take all decisions regarding education. Other decisions are taken by my husband, as everything depends on the loan. Majorly, we need the money to pay for our children’s tuition. Sometimes, BDT 20,000 is insufficient for household expenses. However, with less than BDT 20,000, it is even harder to live, as we have to spend much on the children’s education. Moreover, it is tough to study now without a private tutor whose minimum fee is BDT 1,000 for an SSC candidate. However, I think it is a big problem if the children do not study. This is high time to educate the girls. If they do not study, they cannot do anything. . . So, before you send them outside, you have to equip them with education” (Interviewee; GB 9).

Text search query-decisions related to education aspects.

On the other hand, one of the respondents from the joint family mentioned the following regarding education:

“My husband is the main decision-maker of the house; although he is an immigrant worker, he takes most of the decision of the house. However, with respect to the children’s education, we take the decision together. Since my husband is sometimes unavailable, I discuss their education with the children’s teacher” (Interviewee; GB 18).

Figure 4 indicates that there are four levels of the respondents’ education and resource dimension explaining their economic empowerment. Figure 4 further shows that those respondents who have completed their 12th-grade education or beyond are better represented in the economic (resources) dimension compared to their counterparts with lower levels of education. This suggests that the level of education influences the economic empowerment of the microfinance borrowers.

Matrix coding query of resources based on the level of education.

Figure 5 demonstrates that there are four age groups and three dimensions of empowerment, indicating the existence of a connection between the dimensions of women’s empowerment and different age groups. Apparently, it has been observed that the age group of 41 to 50 years has more control over all three dimensions of empowerment than the others.

Matrix coding query of the age group and three dimensions of empowerment.

In Figure 6, the matrix coding query results outline the relationship between education level and the three dimensions of empowerment. It was discovered that those who have studied up to 12th grade or above are empowered in all three categories of empowerment, thereby confirming the substantial role higher education plays in female empowerment.

Three components of empowerment based on the level of education.

Figures 4 and 5 show that women who have completed a 12th-grade education or higher and who are also between 41 and 50 years old are more empowered in all three categories of empowerment.

Figure 7 shows the matrix coding query for financial literacy and training, as well as the three dimensions of women’s empowerment (resource, agency, and achievement). It was observed that respondents with financial literacy and training are more empowered in all three categories than their counterparts who are financially illiterate.

Three categories of empowerment against the financial literacy and training.

Figure 8 presents an NVivo-generated tree map, which shows the concentration of the dimensions of women’s empowerment, namely economic (resources) and social (agency) as well as political and psychological (achievement). The size of each box represents the trend of the respondents’ answers, their major areas of authority, and their priorities in life. The separate illustration of each dimension is also given above. Figure 8 indicates that the size of the agency dimension is larger than those of achievement and resources. Therefore, women are more likely to be empowered in the agency (social) dimension. This suggests that the women are most likely involved in major decision making, owing to the fact that microfinance borrowers participate in both family and couple discussions. In particular, they are highly conscious and involved in their children’s education. In addition, Figure 8 further reveals that the response for the achievement dimension is also higher than the resource dimension. This may be attributed to the good access most borrowers have to media and phones. Besides, they are also politically and legally aware, despite their limited participation in politics and public protest.

Tree map: three components of women empowerment based on the number of items coded.

Discussion

Microfinancing is considered an important tool to alleviate poverty and reduce gender inequality through women’s empowerment, as well as as one of several strategies for achieving the goals of sustainable development. This study aims to investigate the role of microfinancing on women’s empowerment and to further examine the influence of demographic characteristics on the empowerment of women microfinance borrowers. This section will examine the findings of the above results.

Family Type

There are two types of family structure—joint family and nuclear family. It was observed that women who belong to a nuclear family have high decision-making power in all aspects of their lives as opposed to those from joint families. It was also observed that women from nuclear families participate in all three dimensions of empowerment more than their counterparts from joint families. Furthermore, the findings from the field study revealed that women (from both family types) are most influential particularly on decisions concerning their children’s health and education, which is part of the decision-making agency of social empowerment. On the other hand, women who lived in joint families are the least influential in the decision-making process. Therefore, this study endorses family type as an influential factor in women’s empowerment, particularly in regards to microfinancing. These findings are consistent with the research of Rehman et al. (2015), who confirmed family type’s importance. In addition, Khan and Maan (2008) also suggested that family type and family head both determine the status of female empowerment, since women from a joint family structure cannot undertake anything, except when their aspirations converge with those of other family members. Further, Roy and Niranjan (2004) observed that women have a better chance of being involved in family decisions if the family head happens to be her husband instead of her father-in-law. Roy and Niranjan’s (2004) findings have also been supported by the reports of respondents in our field study.

Age Group

There are four age groups identified in this study: 20 to 30, 31 to 40, 41 to 50, and 51 to 60 years. It was observed that women who belong to the age group of 41 to 50 years are more empowered in all three dimensions compared to other age groups. This finding is consistent with the works of Jejeebhoy (2000), and Rehman et al. (2015), who argued that age is an important determinant of women’s empowerment.

Level of Education

Education is important for the socio-economic development of a country. The social class, context, prevailing norms, customs, and constraints of education also influence a nation’s gender inequality and socioeconomic development (Kabeer, 1999). The matrix coding query in Figure 4 shows the relationship that exists between education and resources. This relationship indicates that women who have completed 12th grade or higher are better represented in the resource dimension. In addition, the matrix coding query of the level of education against the three components of empowerment (Figure 6) shows that women who have studied up to 12th grade or above are more empowered in all three dimensions when compared to the other levels of education. It is mentionable, however, that most of the women—irrespective of their levels of education—are very much concerned with their children’s education. Furthermore, their income is mostly spent on their children’s education, followed by household necessities. This finding is in line with the observations of Rahman et al. (2009), who identified the existence of a positive relationship between education and women’s empowerment. This outcome is inconsistent with the findings of Rehman et al. (2015), however, which indicate that age, marital status, and type of family determine women’s empowerment, rather than education.

Financial Literacy and Training

Our findings revealed that the respondents who are trained in financial literacy are empowered in all three dimensions of empowerment when compared to those who are financially illiterate. This finding is consistent with the works of Nawaz (2015), which establish the positive influence financial literacy has on the association between microfinance and women’s empowerment. Moreover, claimed that financial literacy positively impacts gender equality.

Dimensions of Women Empowerment

Figure 8 illustrates the three dimensions of empowerment, as well as indicating the major areas of authority and priorities in the lives of the respondents. It was discovered that women are more empowered by agency, which relates to the dimension of social empowerment. This is due to their involvement in the major family decisions on matters such as children’s education, health, marriage, and market transaction, in addition to large purchasing decisions and the management of family assets. Concerning the achievement dimension, however, women only have good, reliable access to media and phones, but not the newspaper. In the case of participation in politics and public protests, they are very reluctant, as very few of them vote during the elections of the local chairman of the union or any member of Parliament. Moreover, very few respondents participate in the public protests, citing their occupation with family responsibilities. In addition, they also stated that those who are engaged with the loan program cannot focus on other issues, as they are always preoccupied with finding the means for their loan repayment.

Conversely, it was observed that most of the women were politically and legally sound, as they were conversational about the Prime Minister, the local member of Parliament, local government officials, and the importance of marriage registration. Although they are well-informed politically and legally, their participation in politics is very low, which confirms the findings of Bleck and Michelitch (2018), who reported the poor political participation of rural women. In addition, the “Global Gender Gap Report” (2012) highlighted that the economic empowerment of women is more progressive than their political empowerment in developed countries. In terms of the resource dimension’s influence on women’s empowerment, improvement was observed in their economic security, as they have savings at the GB, which confirms the advantages of economic empowerment for women. This observation concurs with the “Global Gender Gap Report” (2012). On the contrary, the women in our study have limited or no control over the loan and its management activities, which hinders their economic empowerment. Hence, this issue needs to be monitored and addressed for further improvement.

Conclusion

Women’s empowerment is an important indicator of a country’s socio-economic development. Microfinance does not only promote such empowerment, it also represents an important tool for its measurement. The role played by microfinancing in empowering women remains inconclusive, however, as a host of determinants may influence the relationship. In a bid to add evidence to this debate, this study examines that role, further evaluating the key determinants that influence the effect of microfinance on women’s empowerment. In this context, a case study was conducted on borrowers from GB in Chittagong, Bangladesh. Using an innovative and multi-dimensional framework for empowerment, we conducted in-depth interviews with GB borrowers and male members of their family, focus group discussions, and participant observations, which allowed us to assess the role of microfiancing in empowering women economically, socially, and politically.

Our results indicate that the impact of microfinancing on women’s empowerment is very marginal in the absence of other determinants of said empowerment. The results further signify the significance of age, family type, and level of education, as well as financial literacy and training when it comes to women’s empowerment. In addition, we observed that the aforementioned key factors mediate the relationship between microfinance and women’s empowerment. In this regard, it was observed that female microfinance borrowers who studied up to the 12th grade and above, belong to a nuclear family, are aged between 41 and 50 years, and possess financial literacy and training are more empowered than the other women in all three dimensions of empowerment. Hence, microfinancing’s effect on female empowerment is influenced by other factors, such as age, family type, education level, and financial literacy and training. Additionally, concerning the dimensions of women’s empowerment, the results indicate that the borrowers are mainly empowered in the social (agency) dimension, particularly when it comes to deciding their children’s education. The study also identifies the following reasons for lower levels of women’s empowerment: insignificant level of education, lack of self-determination, lack of involvement in income-generating activities, the influence of the existing social structure (apatriarchal society), social norms, male dominance, and loan-use behavior. Our results also suggest that microfinancing brings economic well-being to the borrowers’ lives by increasing their income, consumption, savings, and children’s education. Societal discrimination, prevailing norms, and fixed mindsets are—among others—issues that still need to be addressed to achieve the desired empowerment outcomes.

Supplemental Material

sj-docx-1-sgo-10.1177_21582440221096114 – Supplemental material for Does Microfinance Singlehandedly Empower Women? A Case Study of Bangladesh

Supplemental material, sj-docx-1-sgo-10.1177_21582440221096114 for Does Microfinance Singlehandedly Empower Women? A Case Study of Bangladesh by Sajeda Pervin, Mohammad Nazari Ismail and Abu Hanifa Md Noman in SAGE Open

Footnotes

Acknowledgements

We would like to thank the Article editor and four anonymous referees for their constructive comments and suggestions. We believe that the quality of the paper has substantially improved after addressing the comments and suggestions. All remaining errors are our own. The usual caveats apply.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Supplemental Material

Supplemental material for this article is available online.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.