Abstract

Since the institutionalization of microcredit as the flagship poverty alleviation program, its potential has been under constant scrutiny by practitioners and researchers. This article extends previous work by analyzing two issues: (a) whether microcredit has the potential to alleviate poverty and (b) whether the conclusion drawn from the first issue is sensitive to interest rate variations. We first theoretically show that there is reason to believe that microcredit has the potential to change the fortunes of poor communities. However, the direction of the change in fortunes is uncertain and depends on how costly microfinance institutions’ financial services are perceived by the poor. We then test these theoretical assertions against data collected from 568 individuals from Northern Pakistan. By comparing various sub-groups using Ordinary Least Square and Binary Logistic regression analysis, our results reveal that higher interest rates more than offset the positive effects of microcredit on clients’ income. We also discuss policy implications of the findings.

Plain language summary

This article addresses whether microcredit has the potential to alleviate poverty, and whether the conclusion derived to the first issue is sensitive to interest rate variations. For the purpose data were collected from six tehsil of Lower Dir Khyber Pukhtunkhwa, Pakistan and four MFIs. They are, Agricultural Development Bank/Zarai Taraqiati Bank (ZTBL), Bank of Khyber (BOK), Association of Behavioral Knowledge Transformation (ABKT), and Helping Hand (HH). The first two charge interest rate on loans while the later ones extend grants based on micro loan. Client of all these institutions are in thousands but 567 household received loan in the last 5 years. We found that the change in fortune can be in any direction, depending on how costly the financial services of the microfinance institutions are felt by the poor. Before closing, it is imperative to mention that the present study is conducted in one district of Khyber Pakhtunkhwa and do not cover the entire MFIs and NGOs of Pakistan. Moreover, the sampling method employed for data collection was convenient sampling and not random sampling. Hence further research with more sophisticated designs is needed to cover more MFIs and districts across Pakistan.

Background of the Study

For most practical purposes, poverty can be understood as a lack of resources to meet basic needs such as food, shelter, and clothing. Therefore, any intervention aimed at poverty reduction should in some way augment the income of the poor. Transfer payments such as social security and unemployment compensation have historically been used to meet this goal. However, such transfers can at best only temporarily reduce the deprivation felt by the poor and cannot create a sustainable way out of the poverty trap. A sustainable poverty reduction policy should include efforts that enable the poor to continually earn sufficient income to meet their basic needs.

In line with this objective, most developing countries around the world started rural credit programs to develop their agriculture sector soon after World War II. The plan was to provide farmers with cheap credit so that modern cultivation, with promising positive externalities, could be encouraged. Although the policy was a good one, it failed to deliver as expected (Imai et al., 2010) and efforts to provide cheap rural credit ceased until the discovery of Grameen Bank and its microcredit program.

Before the advent of Grameen Bank, poor communities were considered unbankable because they lacked the required collateral that conventional banks demand in exchange for advancing credit. According to recent estimates, some 44.3% of the global and 53% of the population in Pakistan are excluded from the formal financial services (State Bank of Pakistan, 2021; World Bank, 2021). In the absence of formal financial service providers, poor people sought to borrow from relatives and friends, local traders, moneylenders and some other well-off people in the community (Armendariz & Morduch, 2010). However, resources in the informal sector were limited and became a major source of exploitation of the rural poor (Bateman, 2010). Microfinance is seen as the solution that, on one hand, provides much-needed credit to the rural poor (Miyashita, 2000) and on the other hand, frees them from exploitation by local moneylenders. It was believed that most underdeveloped areas have indigenous potential (i.e., their human capital) to break the vicious circle of poverty (Hulme & Mosley, 1996; Imai et al., 2010; Sievers & Vandenberg, 2007) but all they need is microcredit (Armendariz & Morduch, 2010; Dunford, 2001; Littlefield et al., 2003) at affordable rates.

The idea behind the role of microcredit in alleviate poverty is straightforward. Economic theory suggests that the provision of microcredit, like any other income transfer, should increase income and consumption (Fang et al., 2020; Morduch, 1999), but there are two counterbalancing effects: the income and substitution effects on the labor supply. Empirical research has shown that the substitution effect dominates the income effect at lower levels of income, making labor more attractive (Sharp et al., 2012). Thus, the initial expectations from microfinance were to increase income and consumption of the poor; to make their labor more productive; and reduce their vulnerability to adverse shocks (Sievers & Vandenberg, 2007). The provision of microcredit is also expected to have additional positive effects, such as improving education, health and housing, and empowering women (Hermes & Lensink, 2011).

Sufficient time has passed since Muhammad Younas extended the first micro loan in Bangladesh, and we have seen enough replications and extensions of the Grameen Bank model around the world. But where do we stand now? Have there been any visible improvements in the living standards of the poor in the Third World, or is microfinance an exercise in futility? Initial research findings in this regard were very encouraging (e.g., Imai et al., 2012; Morduch, 1999; Morduch & Haley, 2002; Mosley & Hulme, 1998; Robinson, 2001).

The optimism associated with MFIs, and particularly with the Poverty Lending Approach (PLA), was short lived. As happened with subsidized agricultural credit in the past (Adams et al., 1984), subsidized microcredit was ill-treated by rent seekers (Miyashita, 2000). As a result, default rates became higher as microcredit ended up in the wrong hands, and MFIs continued to rely heavily on government and donor agencies’ exchequer (Morduch, 2000). Meanwhile, research findings of Ghate (1992), Mustafa et al. (2000), Helms and Reille (2004), Wang and Ran (2019), and W. Khan et al. (2020) suggested that poor households are more interested in continuous availability of microcredit rather than cheap credit, led to the advent of the Financial System Approach (FSA). This new approach provided a single remedy to the dual problem of rent seeking and non-sustainability of the PLA based MFIs.

The FSA is based on the same innovative ideas, especially with respect to collateral requirements, as the old PLA, except that markup rates are either at par or above the market rate of interest (Miyashita, 2000; although to Cull et al. (2009), NGO-based microfinance institutions are charging much higher mark-up rates than FSA). The argument for a higher than market rate of interest is based on the interest insensitive demand for microloans and several other restricting assumptions (Morduch, 2000). There is hardly any empirical support for the hypothesis that the impact of microcredit on poverty is directly associated with financial sustainability of MFIs (except in Mosley & Hulme, 1998). On the contrary, Sheremenko et al. (2017) argued that increasing interest rates beyond a threshold level of 80% adversely affects financial sustainability. Still, it is widely accepted that financial sustainability and outreach (i.e., advancing credit to the core poor) are inversely related (Arun, 2005; Arun & Hulme, 2003; Bateman, 2010; Goetz & Gupta, 1996; Hermes & Lensink, 2011; Hulme & Mosley, 1996; Kirkpatrick & Maimbo, 2002; Marr, 2004; Mba et al., 2021; Mosley, 2001; Scully, 2004; Simanowitz, 2002; Siwale, 2015). Expensive microcredit may allow poor households to smooth consumption, expand, and diversify income generating activities (Bakhtiari, 2006), but it also carries with itself the risk of default (Adams & Pischke, 1992).

Recent empirical studies on the impact of microcredit on poverty alleviation have produced mixed results. For instance, while Samer et al. (2015), Lacalle-Calderon et al. (2018), Tasos et al. (2020), Latif et al. (2020), and Ahmed and Kitenge (2022) found that microcredit significantly reduces poverty, the study of Abdallah et al. (2022) found no association between microcredit and multidimensional poverty. Even worse, Kandie and Islam (2022) found that microcredit has increased the depth and severity of poverty.

One possible source of variation in the impact of microcredit on poverty may be the type of MFI advancing the credit, as different types of MFIs may charge different interest rates and may have different repayment schedules (Rashid & Ejaz, 2019). For instance, Barry and Tacneng (2014) compared NGO and bank type MFIs and concluded that NGO-type MFIs are the best to serve the poor (see also S. Khan & Akbar, 2017; Zulfiqar, 2017). Although limited in number, previous research has shown that the impact of microcredit on poverty depends on the cost of borrowing (see for instance Ali et al., 2017; Mahmood & Bakhsh, 2020; Rashid & Ejaz, 2019; Shafique & Siddique, 2020; Ullah et al., 2020). However, most of the results of these previous studies are based on very small samples (e.g., Rashid & Ejaz, 2019 interviewed only four women entrepreneurs) or are descriptive in nature (e.g., Mahmood and Bakhsh, 2020). This study, therefore, adds to the limited literature on the impact of different types of MFI and their interest rate variations on the welfare of their clients.

The rest of the paper is organized in three sections. Section “Theoretical Model” starts with a brief introduction to the two approaches to microfinance, and then presents and solves our basic theoretical model. Implications of the theoretical model for the two approaches to poverty alleviation are also discussed in this section. Section “Empirical Evidence” presents the empirical support for the theoretical implications of the model, while Section “Conclusion and Recommendations” concludes with some policy recommendations for the stake holders of the microfinance sector.

Theoretical Model

Since its inception, two types of microfinance institutions (MFI) have been operational. The first type provides low-cost credit to the rural poor without the conventional collateral requirements (Arun, 2005) but relies heavily on grants and subsidies, making its sustainability questionable. To address this issue, a new financial system approach was introduced in the early 1990s. This new approach follows usual banking practices but adopts the collateral mechanism from the old approach. The major difference between the two approaches is the rate of interest charged from clients. The new approach considers providing credit to the poor as the solution to eradicating poverty, no matter how high the interest rate charged, while the old approach believes in cheap availability of credit to help the poor out of poverty trap. The higher interest rate makes MFIs more sustainable, but its impact on poverty alleviation remains unclear.

With this background, let’s explore how microcredit can help rural poor communities. Our evaluation criteria should consider the increase in income, consumption, and production, which can also lead to better education, health, and self-esteem.

Consider a rational consumer with convex and monotone preferences who consumes L = 1, 2, 3, …n commodities, denoted by a consumption vector

We assume no inheritance or any other sources of income of the individual and thus his consumption is constrained by the maximum income he produces. Thus, the utility of the individual is constrained by his production function given by:

Where

Invoking the Weierstrass extreme value theorem (Intriligator, 2002), the above maximization problem has a solution if the constraint set is compact, and the utility function is continuous. For compactness of

Explicit in this formulation is the fact that our hypothetical individual chooses the optimal input bundle first, given his resources and input prices, so that output/income is produced at the minimum possible cost and then the earned income is consumed optimally to choose

The maximum value function, known as the indirect utility function, associated with the problem specified in equation (3) can be stated as (it is also guaranteed to exist by the continuity of U(

Given that U(

The two properties associated with equation (5) have important antipoverty implications. According to the first property, income augmenting interventions are always welfare-enhancing since they expand the feasible consumption set. For instance, provision of skills to the unskilled labor force, and modern production and processing technologies all are welfare-enhancing since they increase income, expand the feasible consumption set, and should result in a sustainable exit out of poverty. However, all these changes require money/capital, which profit-seeking financial institutions will never provide at affordable rates (as such institutions will internalize all the cost associated with banking with the unbankable), leaving room for antipoverty interventions such as microfinance.

Secondly, the property implies that consumer welfare is non-increasing in prices, that is, the markup charged on microcredit. Given the interest insensitivity claim of the microcredit extended under FSA (Ghate, 1992; Helms & Reille, 2004; Miyashita, 2000; Morduch, 2000; Mustafa et al., 2000), this aspect of the property is particularly interesting. The consumers will either avoid microcredit at higher markup rates since a higher markup can never enhance their welfare, or if they accept microcredit at higher markup rates, then microcredit is essentially a Giffen commodity and may decrease the welfare of the consumers by altering their consumption basket. Hence, neither of these outcomes is poverty reducing.

Let us suppose that microloans are truly interest-insensitive, which is one of the building blocks on which the old poverty-alleviating microcredit intervention was abandoned in favor of the new wave. Abandoning the old, subsidized microcredit in favor of the new wave involves charging higher interest rates from the clients. Doing so, as the proponents of the new wave claim, would not cause MFIs to lose clients. Rather, adopting the new financial system approach would enable MFIs to advance more loans than before. A recent study by Ali et al. (2017) reported that 87.5% of their respondents stated that, “we are poor and have no alternative but to accept these loans” (p. 6). This is exactly the case with giffen goods. Theory suggests that giffen goods are likely to be found in impoverished areas, especially where there are very limited substitution possibilities for the goods under consideration (Jensen & Miller, 2008a). Thus, accepting that microloans are interest insensitive is equivalent to accepting that microloans are giffen commodities. However, the very definition of a giffen commodity implies that a rise in its price (interest rate in this case) would cause consumers to shift their budgets from other expenditure to purchase the giffen commodity (Jensen & Miller, 2008b). In the case of microcredit, charging a higher interest would imply, and accepting that microloan are giffen goods, that people cut back on other expenditures, such as food, clothing, shelter, education, health, and the like, to pay back the principle and the mark up (Hulme & Mosley, 1996). Would it make sense to call such an intervention antipoverty? Clearly not.

Let’s examine the previous analysis from a different perspective. Equation (5) and its associated properties suggest that any relaxation of the budget constraint will not decrease consumer’s utility (call it the income augmenting effect of microcredit) and any tightening of the budget constraint cannot increase utility (call it the budget tightening effect of higher interest rate). Therefore, the practices of microcredit institutions have two opposing effects on individual welfare: the income augmenting effect of receiving microcredit and budget tightening effect of higher interest rates. Whether these effects result in a positive or negative net welfare depends on their relative magnitudes, which is largely an empirical question.

The current practice of microcredit institutions, or the financial system approach, implicitly assumes that the income augmenting effect is greater than the budget tightening effect. Proponents of this approach rely on the Inada (1964) conditions, which state that “the marginal product of capital is very large when the capital stock is sufficiently small and that it becomes very small as the capital stock becomes large” (Romer, 2006, p. 9). In the context of current practices of microcredit, these conditions imply that small businesses (characterized by small capital holdings) should produce more from any given increment in their capital than big businesses (characterized by large capital holdings). This is the economic principle used to justify the higher interest rate charged on microloans. Evidence, however, suggest that poor communities usually use microcredit to finance their consumption (Hulme & Mosley, 1996)

However, this application of the Inada conditions is problematic. Although the principle is theoretically sound, it application is quite wrong (Armendariz & Morduch, 2010; Morduch, 2000). The applicability of the Inada conditions to microcredit rest on so many assumptions (Morduch, 2000) which are not likely to hold in poor communities. Consequently, it is likely that the budget tightening effect of the current practices of microfinance institutions outweighs the income augmenting effect, suggesting that these practices may have a negative impact on individual welfare.

Empirical Evidence

Data and Variables

The Date used in this study was collected from six administrative Tehsil in Lower Dir, Khyber Pakhtunkhwa, Pakistan. At the time of data collection, there were 11 MFIs operating in the area with the core objective of eradicate poverty. Six of these MFIs were extending microcredit based on the FSA, while the remaining five were not-for-profit organizations (i.e., PLA). Four MFI are selected based on their notable number of clients, namely Agricultural Development Bank/Zarai Taraqiati Bank (ZTBL), Bank of Khyber (BOK), Association of Behavioral Knowledge Transformation (ABKT), and Helping Hand (HH). The first two charged interest rates on loans while the later two extended grants based on microcredit. Together, these four MFIs provided microcredit to 567 households in the last 5 years. To balance the sample frame, we randomly selected 567 rejected applicants as control group, resulting in a sample frame of 1,134 households (see S. Khan & Akhter, 2017; Tasos et al., 2020; Abdallah et al., 2022, who utilized similar sampling frames). Using Cochran’s (1977) formula for optimal size selection with finite population correction, a 1% risk margin, and a 5% margin of error, we over-sampled by a factor of 1.3 to correct for the design effect (Henry, 1990; Kalton, 1983). The final sample size consisted of 317 MFI clients and 251 rejected applicants. Data has been collected from random respondents out of the two strata. The Key characteristics of the selected sample respondents are outlined in Table 1, while the variables selected for subsequent analysis and their measures are given in Table 2.

Sample Information.

Note. *ABKT and HH offer welfare-based lending while BOK and ZTBL offer market/interest-based lending.

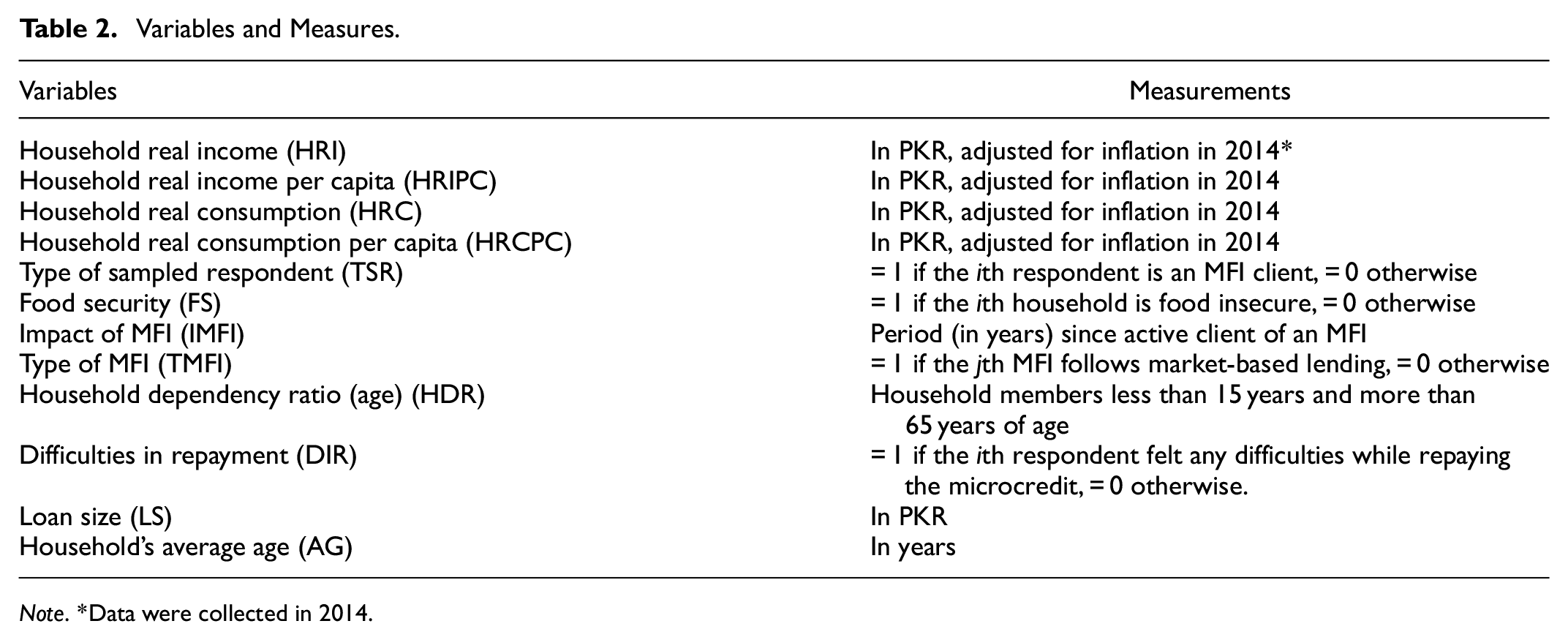

Variables and Measures.

Note. *Data were collected in 2014.

To measure household income and consumption under various categories, the questionnaire asked respondents to report both for two-time periods - at the time of submitting the microcredit application and their current income/consumption levels. To measure real changes in these magnitudes, the variables were adjusted for an annual inflation rate of 8% during 2014. Food security (FS) was measured as a binary response (yes/no) to a single statement asking respondents if their household had to eat less during the last 12 months due to resource limitations. Similarly, difficulties in repayment (DIR) were measured using a single statement that asked respondents if they experienced any repayment difficulties during the repayment cycle. Responses were recorded as 0 (no) and 1 (yes). The remaining measures, as provided in Table 2, are self-explanatory.

Results and Discussion

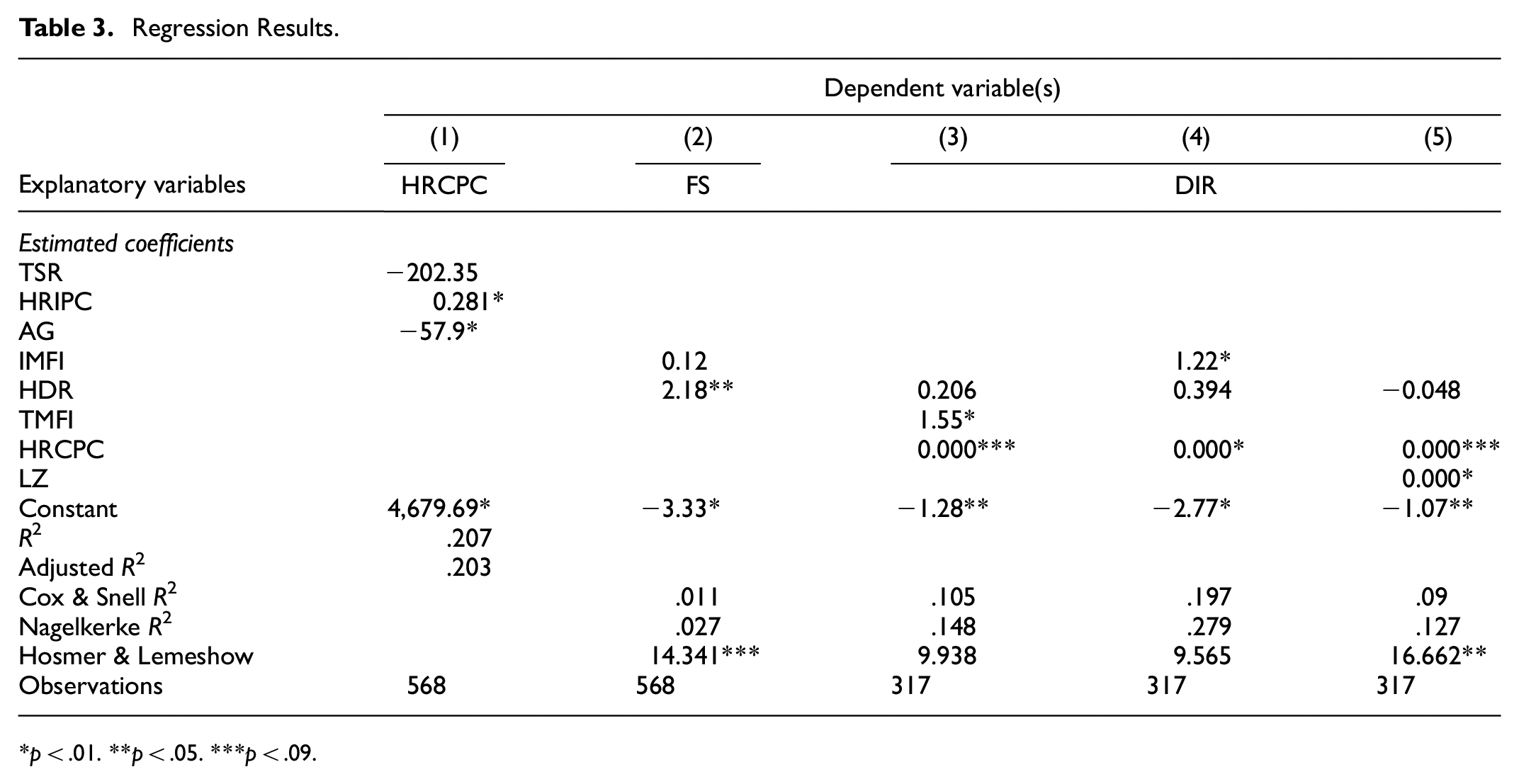

The regression results, which evaluate whether the income-augmenting or the budget-tightening impact of the microcredit dominates, are presented in Table 3 below. The results are based on the following set of five equations.

The Ui, Vi,

Regression Results.

p < .01. **p < .05. ***p < .09.

Equation (6) is estimated using the Ordinary Least Square (OLS) method while the rest of the equations are estimated using the binary logistic regression specifications (see Samer et al., 2015 for more details). Results corresponding to each equation are represented by the same numbered column in Table 3.

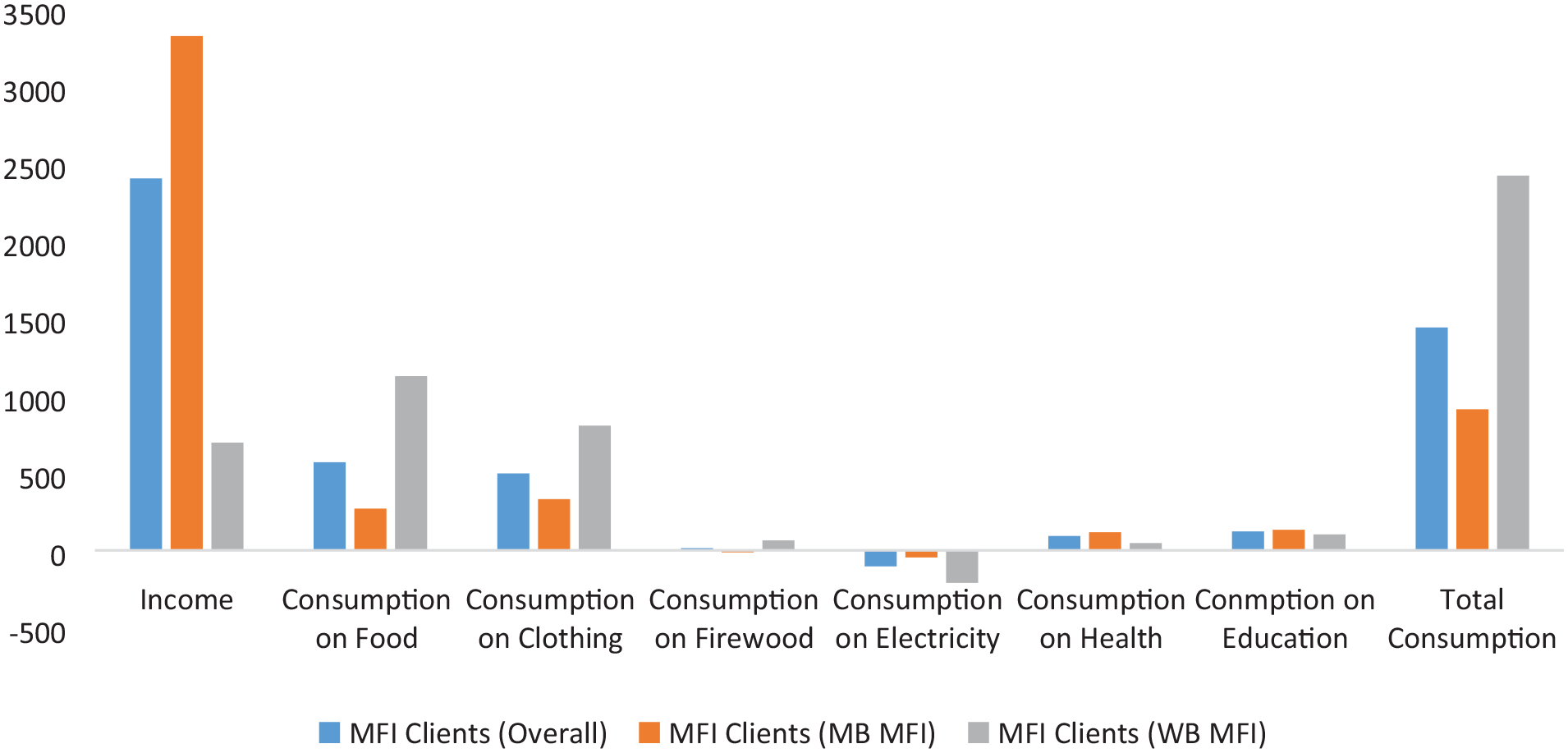

In column (1), the OLS results show that HRCPC is negatively influenced by being a client of an MFI and AG, while positively by HRIPC. Although the coefficient of TSR is insignificant, Figure 1 further elaborates the relationship between being a client of different types of MFIs and changes in household income and consumption across various categories. It is evident that income of the FSA-based MFIs changed more than that of PLA-based MFIs. This is the income-augmenting impact of the microcredit. However, when we compare the budget-tightening impact of the microcredit, as proxied by changes in consumption across various categories, PLA-based MFIs outperform FSA-based MFIs. These findings are in line with prior research (see for instance, Augsburg et al., 2015; Banerjee et al., 2015; Bukari et al., 2020; Goli et al., 2019; Gubert & Roubaud, 2011; Mahmud, 2019; Mohindra et al., 2008; Qejvanaj, 2021).

Changes in household real income and consumption.

The results of equations (7), (8), (9), and (10) further strengthen the notion that the budget tightening impact of microcredit must be greater than its income augmenting impact. For instance, according to the results of equation (7), food insecurity is directly related (although insignificantly) to having more time with MFIs as an active borrower. However, according to the results of equation (9), having more time with MFIs as an active borrower significantly causes difficulties in repayment. The results of equation (8) reveal that being a client of an FSA-MFI causes more difficulties in repayment than being a client of a PLA-MFI. Likewise, LS (a characteristic feature of the FSA-MFIs) also directly influences difficulties in repayments. But the most interesting results of all is the positive influence of household real consumption per capita on difficulties in repayment. This implies that the budgetary impact of microfinance loans is contractionary, as implied by the theoretical model of Section “Theoretical Model.”

Conclusion and Recommendations

Microfinance is a relatively old concept, but researchers are still skeptical about its impact on poverty reduction. The difference in opinion seems to stem from various donor agencies and multilateral financial institutions wanting to replace the old poverty reduction approach with the new financial system approach. As we have shown, the neo classical optimization model has clear-cut implications for the impact of microloans on poverty reduction. In other words, microcredit can potentially enhance the productivity of each factor of production and increase the consumption boundaries for the poor masses. There is no difference of opinion in this regard.

The major difference in opinion between the old and new approaches of microfinance centers on the rate of interest that an MFI should charge from its clients. The old microfinance model is based on the idea that MFIs should be provided grants and subsidies to enable greater outreach at minimum cost. The new wave sees inefficiencies in the subsidized credit (Miyashita, 2000; Morduch, 1999, 2000) and stresses the sustainability aspects of the MFIs. Hence, the new wave advocates market-based or even a mark-up above the market-based rate of interest. While the logic behind cheap credit, advocated by the old model, is more philanthropic and less backed by rigorous economic theory, the new wave claims that charging a higher rate is what the principles of economics suggest. Our findings, however, suggest otherwise.

The neoclassical utility maximization model implies that household utility cannot be enhanced by charging a higher price for microloans. Therefore, the claim that microloans are interest-insensitive cannot be true unless we either accept zero demand for microcredit or that microcredit is a giffen commodity. The first scenario could not be the case as millions of people around the world approach MFIs and take loans for various purposes. Then, we have to accept that microloans belong to the category of giffen commodities, and theory may not refute this conclusion either. Once we accept microloans in the category of giffen commodities, we come across another strong theoretical justification for providing cheap microcredit to the poor.

This is because giffen commodity is a commodity that the poor cannot do without, and if its price is raised, poor people will reshuffle their expenditure to make room for a greater consumption of the giffen commodity. What other expenditure of the poor are likely to be affected if a higher interest rate is charged on microloans? Some of the subsistence food, shelter, health, and education will be affected. Consequently, this impact of microcredit would hardly be acceptable to anyone, as it implies making the poor even poorer. Our empirical results rigorously show that consumption is indeed adversely affected by the higher interest rates, as proxied by difficulties in repayments.

To be objective about the market economy, the benefits that the market economy carries with itself can hardly be denied. However, there are always some grey areas where the market cannot be trusted, and microfinance is one of those grey areas which, if left to the market, would produce catastrophic results. Enough evidence has been found and serious arguments accumulated that poverty and some of its most undesirable consequences, for example, crime and terrorism, are strongly associated with each other. This is one kind of externality that private markets will never consider in its cost-benefit analysis while extending credit to the poor. Naturally, the state and the donor agencies have a role to play in this regard, and interest rate subsidies are a valuable option (Armendariz & Morduch, 2010; Jensen & Miller, 2008b) to provide cheap credit to the poor. We do acknowledge the huge volume of literature on the negative consequences of subsidized microcredit (Miyashita, 2000; Morduch, 1999, 2000), but we have also shown that market is not the solution. Moreover, the policy of subsidized microcredit has nothing inherently wrong with it, but problems on the execution side make it worse. There will always be some effort needed on the execution side to get the desirable consequences even from the best of economic policies. Subsidized microcredit is not an exception in this regard.

Before closing, it is imperative to mention that the present study was conducted in one district of Khyber Pakhtunkhwa and does not cover all MFIs and NGOs of Pakistan. Furthermore, the sampling method employed for data collection was not strictly random but a blend of random and convenient sampling. Although previous related empirical research has utilized such sampling designs (see for instance Abdallah et al., 2022; S. Khan & Akhter, 2017; Tasos et al., 2020), future researchers are recommended to apply more sophisticated sampling designs to corroborate the findings. Additionally, there is ample evidence that direct questions regarding income and consumption may be subject to social desirability bias (see for instance Andersen & Mayerl, 2017; Stecklov et al., 2018), and the current study did not account for the socially desirable answer in the questionnaire. Therefore, we would recommend that future researchers control for social desirability responding in their surveys.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Ethical Approval

No misconduct, informed consent. Data fabrication, double publication has been observed by the authors.

Data Availability Statement

The data supporting the findings of this study are available from the corresponding author upon request.