Abstract

Financial sustainability is one of the major issues in the development process, particularly in developing countries. Microfinance started with two basic objectives of poverty reduction and women empowerment. However, unsustainable microfinance providers cannot assist the poor for a longer period of time, due to uncertainty about their existence. This study investigates that how financial sustainability of Pakistan’s microfinance sector is affected by various factors. A new financial sustainability index has been developed to measure the financial sustainability. Generalized Method of Moments (GMM) approach is employed to analyze the panel data from 34 Pakistani MFPs, yielding 344 MFI-years of observations from 2006 to 2018. The findings reveal that increase in loan size, female borrowers, liquidity, and leverage significantly enhances the financial viability of Microfinance Providers in Pakistan. However, the total borrowers and the operating cost per borrower negatively affect the financial sustainability of MFPs in Pakistan. MFIs needs to be financially independent, with less or no support from government or donor agencies. Financially sustainable MFPs contributes in the achievement of the 8 out of 17 Sustainable Development of Goals (2030 SDGs) of the United Nation. The data for 2018 onwards is seriously affected by COVID-19, which cannot be included in the current data set. Hence, researchers in future analyze the data from the pre-COVID-19 and post-COVID-19 periods to compare the analysis and examine the pandemic’s impact.

Plain language summary

This study investigated the relationship between organizational structure, growth outreach, women’s empowerment, liquidity, capital structure, cost efficiency, and financial stability using data from 34 MFPs in Pakistan over the 2006–2018 periods. The financial sustainability index was developed using principal component analysis and was used as a proxy of financial sustainability. ROA, ROE, OSS, and FSS were used as components for developing the financial sustainability index. Due to the inclusion of lagged dependent variables as part of explanatory variables for the persistency of the estimates, the model becomes dynamic. Hence, the Generalized Method of Moment (GMM) is arguably the right regressor for estimating the dynamic panel data. Organizational structure has a significant positive impact on the microfinance sector of Pakistan. Proxies for measuring growth outreach: the average loan per borrower has a significant positive impact, and the number of active borrowers has a negative effect on FSI in Pakistan. The percentage of women borrowers significantly positively impacts FSI in Pakistan. Liquidity has a significant positive effect on FSI in the Pakistan context. The capital structure (D/E) has a significant positive impact on FSI in the microfinance sector of Pakistan. The cost per borrower has a significant negative impact on the financial sustainability of the microfinance sector of Pakistan. The control variable MFP size also has a significant positive effect on FSI in the microfinance sector of Pakistan. GDP growth negatively affects FSI in the Pakistani context.

Keywords

Introduction

The two main problems that need to be addressed are financial sustainability and poverty alleviation to attain the goal of sustainable development (Atara, 2023; Marti-Ballester, 2021). Microfinance sector arose as a vital catalyst to promote financial inclusion and social development (Khachatryan & Avetisyan, 2018). Unlike the established financial system, microfinance provides micro level collateral-free credit using innovative, progressive, and group lending (Sangwan & Nayak, 2020). Microfinance received considerable attention during the last decade (Maeenuddin et al., 2023). MFIs can’t accomplish their main objectives of reaching the maximum portion of the poor part of the society if they are not sustainable financially (Maeenuddin et al., 2023). If MFIs cannot cover their cost of operations from income from interest on loans, then MFIs are more reliant on subsidies (Githaiga, 2021). Similarly, charging a higher rate of interest on the loan is not feasible due to the unique nature of the demand side (Quayes, 2012), as focusing on increasing borrowers exposes the microfinance institutions more to credit risk, It negatively affects the ability of the microfinance providers to maintain their financial stability. Poor people cannot be helped by unsustainable microfinance providers in the long term since they will cease to exist (Agboklou & Özkan, 2023; Li et al., 2023). It encourages microfinance providers to maximize their profit in order to pay for their costs in the absence of donations and subsidies (Maeenuddin et al., 2021; Naz et al., 2019).

Various studies showed that, funding had been significantly decreased (Adhikary & Papachristou, 2014), and internal sources are no longer sufficient for sustainable financial service provision to the poor. As a result, MFIs commercializing it’s services (Atara, 2023). As a result, MFIs begin to use commercial funding and mobilize interest-earning deposits, which results in a mission drift, or a reduction in outreach (Beisland et al., 2019). Financial sustainability enables the smooth and effective operations of the microfinance activities (Mashalaghu & Mutunga, 2023). According to Beisland et al. (2019), with the increased focus on commercialization and financial sustainability, MFIs have become a formal financial sector and are no longer the universal poverty reduction tool. Similar to this, some said that MFIs needed to use market-based concepts to achieve their dual objectives of maximizing social wealth (helping more people) and economic success (financial sustainability). Therefore, the most crucial component for the long-term existence of businesses is financial sustainability. Given these realities, researchers and policymakers are analyzing the variables influencing the financial viability of the microfinance industry. However, in terms of microfinance studies, this field of study is still relatively unexplored.

Poverty reduction has been a major challenge for every reigning government in Pakistan. Since it has been deeply rooted, the governments always try to find the best solution to this issue. There have been several studies on financial sustainability, but owing to Pakistan’s cultural, economic, social, and other peculiarities, the findings from other nations cannot be applied (Naz et al., 2019; Maeenuddin et al., 2021). According to Pakistan Microfinance Network (2019), out of the 10.20 million active loans issued by regulated financial institutions, 6.9 million (68%) were issued by microfinance providers. With political instability and economic hurdles, MFPs of Pakistan shown marvelous growth over the preceding decades. According to Pakistan Microfinance Review (2020) report, From 3.6 million in 2015 to 7.4 million in 2019, the number of active borrowers increased by more than twice that amount. The gross loan portfolio grew by more than 200% over that time, from 90.1 billion Pakistani rupees to 301.90 billion (Malik et al., 2020). 53% of the borrowers are rural, and 50% of them are women.

The average loan principle is about $300, with a 12 month repayment period and an interest rate ranging from 0% to 40%; 13% of loans had 0% interest rates (Basharat & Sheikh, 2019). With a write-off of less than 1% of the overall loan portfolio, the microfinance industry maintained a low default rate (Farooq, 2018). According to Pakistan Microfinance Network (2019), the MFPs of Pakistan have shown consistent growth for the last 6 years and are expected to add customers at the rate of about 22% per year (45% of portfolio growth) till 2025. The Pakistan’s microfinance sector shown fantastic growth during the past decades, but unfortunately, the MFIs failed to execute their poverty reduction and women’s empowerment objectives. Unfortunately, this tremendous growth has not been reflected in the attainment of the basic objectives of the microfinance sector. According to the World Bank’s report-modeled ILO estimates (2020), the total labor force’s unemployment percentage increased from 1.83% in 2014 to 3.02% in 2019. The male unemployment percentage of the entire labor force grew from 1.78% in 2014 to 2.44% in 2019, and the female unemployment percentage of the total labor force increased from 2.01% in 2014 to 5.08% in 2019.

According to a 2019 Asian Development Bank report, 2.8% of employed people live on less than USD 1.90 PPP per day. The average annual growth rate from 2013 to 2018 was 2.9%. As per the data available in 2017, 3.90% of the total population lives below USD 1.90 PPP a day. The poverty rate in Pakistan is 24.10% of the total population. Pakistan Microfinance Review’s (2020) report claims that, the total revenue increased from the period 2015 to 2019 at a tremendous rate, but the net income increased. It has been noted that the sector’s total revenue increased from 33 billion PKR in 2015 to 111 billion PKR in 2019, but on the other hand, the sector’s net income decreased from 5 billion PKR in 2015 to a loss of 6 billion PKR in 2019. The conventional measures of return on assets and equity show the sector’s financial position. The return on assets ratio, which shows how efficiently the available resources have been utilized, shows that the ratio ROA decreased from 3.6% in 2015 to a negative (−1.8%) in 2019. The ROE, which shows the efficient utilization of the shareholder’s wealth, shows that the ratio decreased from 15.0% in 2015 to a negative of (−1.4%) in 2019.

The efficiency ratios show a decline during the period. The Operational Self-Sufficiency (OSS) ratio has been decreased from 124%, said to be a stable position, to an unsustainable position of 97% in 2019. The Financial Self-Sufficiency (FSS) ratio also shows a downward movement from a sustainable to an unsustainable position. The FSS declined from 121% in the year 2015 to 95% in the year 2019. These efficiency ratios show that the microfinance sector showed an unsustainable financial position during the period. Mohsin et al. (2018) noted that Pakistan’s microfinance banks (MFBs) recorded low growth in outreach and poor performance compared to the South Asian benchmarks. Naz et al. (2019) noted that there is a substantial growth in the number of MFBs in Pakistan due to their unconventional offering mechanism and outreach in the remote region, while microfinance institutions are not cost-efficient, which affects their financial sustainability. Ahmad & Satti (2017) stated the microfinance sector is inefficient and working below its optimum scale measurement. Ahmad et al. (2019) noted that the number of products and institutions has increased but fell short of the goals. Inappropriate and costly strategies of overexpansion affect the overall cost and productivity of the sector. As a result, there is a problem with financial sustainability that has to be fixed.

The top MFIs in Pakistan have provided a variety of solutions outside microfinance-specific actions as part of their COVID-19 answers. However robust they have been in the past, MFIs are nevertheless feeling the effects of COVID-19. So, considering this unsettled debate and the need for generating additional context based evidences, the current study endeavors to produce additional context based evidences on the issue by addressing the following specific research objectives. The results of the previous studies about financial performance are inconsistent and contradictory. Similarly, measurement of the MFP’s financial sustainability is always tricky, because most of the MFIs are subsidized; consequently, it is still a challenge (Saad et al., 2018). Thus, due to the contradictory and inconclusive results of the previous studies and ambiguity in the measurement of financial sustainability. In this study, a new financial sustainability matrix was created, and the effects of organizational structure, growth outreach, women’s empowerment, liquidity, leverage, and cost effectiveness on the financial sustainability of microfinance providers in Pakistan were investigated.

Literature Review

In this study, the effects of organizational structure (MFBs, NBMIFs), growth outreach (ALPB, NAB), women’s empowerment (PWB), liquidity, leverage (D/E), and cost per borrower are examined in relation to the financial sustainability of MFPs in Pakistan.

Profit Incentive Theory

The Profit Incentive Theory (PIT) under the Institutionalist paradigm serves as the theoretical bedrock for financial sustainability. According to the Profit Incentive Theory (PIT), sustainable microfinance can help to eliminate poverty. According to the institutionalist viewpoint, the Profit Incentive Theory notes that donors’ money is constrained, making it impossible to locate MFIs on a large scale, given the rising demand for small loans. According to this approach, MFIs should aim to maximize revenue, cut operational costs, pay bills, and generate surpluses. MFIs that depend on grants and subsidies do not budge when pushed to increase revenues and cut expenditures; thus, they choose to extend their reach rather than maximize efficiency by providing services to the poorest and most rural clients, who pay higher borrowing rates (Bogan, 2012; Morduch, 2005). Financial sustainability enables the smooth and effective operations of the microfinance activities (Mashalaghu & Mutunga, 2023). Ahmad et al. (2019) investigate the microfinance industry’s growth plans for Pakistan from 2013 to 2017. The findings indicate that despite the sector’s phenomenal expansion, the goal was not achieved. The sustainability level is weak, per-borrower cost and productivity ratios are also low. Weak sustainability results from the use of expensive and ineffective growth strategies.

Financial Intermediation Theory (Outreach and Financial Sustainability)

Financial Intermediation Theory (FIT) asserts that banks are financial intermediaries, collect deposits and then lend them out without having the ability to create money. MFBs qualify as financial intermediaries due to their involvement in collecting and lending deposits. The theory aims to explain the role of MFPs in connecting savers and borrowers (outreach indicators), which lays a solid groundwork for attaining financial sustainability. The theory describes the outreach (depth & breadth) and how these factors affect long-term financial viability (Mutua et al., 2020). Maeenuddin et al. (2023), Churchill (2020), Fuertes-Callén & Cuellar-Fernández (2019), Mutua et al. (2020) also supported this theory.

Agency Theory (Leverage and Financial Sustainability)

As cited by Cheboi et al. (2019), Jensen and Meckling (1976) established conflict between the principal (stakeholders) and the agent (manager) in which managers (agents) engage in self-seeking actions at the expense of the stakeholders (principals). The management is under increasing pressure to create sufficient cash flow for debt payments (Jensen, 1986; cited by Cheboi et al. (2019)). The Agency theory supports that an increase in external debt can reduce internal managerial conflicts, increasing the financial viability of the MFPs (Maeenuddin et al., 2023). Increase in financial leverage can enhance the financial viability of the MFPs (Mashalaghu & Mutunga, 2023; Maeenuddin et al., 2023).

Sustainability has emerged as a major global issue, specifically in emerging economies and cases of ignorance. It leads the institution to a huge financial loss and a market reputation (Jamwal et al., 2021). MFPs must improve their financial sustainability in response to natural calamities and major shocks like the pandemic (Aracil et al., 2021). Accordingly, Atara (2023) observed the association between financial sustainability and poverty outreach in Ethiopia. The author noted the existence of a trade-off between social outreach and financial viability of the microfinance institutions which is not a good indication for the long term operation of the MFIs. It demonstrates how putting more emphasis on financial stability can widen the gap between microfinance institutions and the poor part of the society. Reichert (2018) conducted a meta-analysis on the performance of MFIs by analyzing the data from 3,088 overall and synthesized data from 623 empirical findings. They found that MFIs have to choose between their social and financial goals more often when the outreach cost, the depth of outreach, and efficiency indicators are high.

MFIs in Pakistan are working below their optimum scale (Maeenuddin et al., 2021). Mashalaghu and Mutunga (2023) states that, financial sustainability enables smooth and effective operations of the microfinance institutions. They studied the impact of firm specific characteristics on the financial viability of MFIs. Their study was supported by agency theory and institutional theory. By using the descriptive and inferential statistics they and found that financial stability is positively affected by liquidity, age, and leverage. Similarly, Donou-Adonsou and Sylwester (2017) found that, MFI’s loans are not mainly invested as physical capital; instead, they manage total productive efficiency, and banks might be financing non-productive investments. Accordingly, Aziz and Aziz (2019) investigated the financial sustainability of microfinance institutions in Pakistan. They analyzed data from 24 MFIs and 11 MFBs from 2006 to 2017. They used ROA, ROE, and OSS ratios to measure the financial sustainability. The findings show that, number of female borrowers, adjusted cost per loan, adjusted cost per borrower, and risk coverage ratios significantly impact the performance of MFBs.

Similarly, Agboklou and Özkan (2023) noted that financial sustainability is positively influenced by the size of the MFI and negatively affected by the deposits per borrower & PAR >90. Abrar (2019) looked at how MFIs’ social and financial performance and financing interest rate impacted their lending interest rates. The author examined data from year 2006 to 2012 from 382 MFIs in 70 different countries. The number of active borrowers and the average loan size were utilized to measure the financial performance. The findings indicate that the funding interest rate and financial performance (ROA, ROE, and OSS) have a positive influence on the lending interest rate. Age as a control variable has little impact, whereas size has a substantial impact on the loan interest rate. The author came to the conclusion that there is no difference between conventional and Islamic MFIs if the MFIs neglect the social goal and concentrate exclusively on financial success. In Pakistan’s microfinance industry, Javid and Abrar (2015) discovered a trade-off between financial viability and social impact. Positive factors include the capital structure, earnings, and size of the MFI. An increase in number of women and active borrowers reduces the poverty level of the household. Additionally, the depth of outreach has a positive impact on sustainability while having a negative impact on social outreach.

The microfinance industry of Pakistan has two dominant institutional models. The formal sector includes microfinance banks (MFBs), which are commercially oriented, and the informal sector includes microfinance institutions (MFIs) and rural support programs (RSPs), which can be concluded as non-governmental organizations (NGOs) (Hussain et al., 2020). It is ideal for a comparative study that will serve as the basis for a reliable inquiry into the tradeoff between the microfinance sector’s social and financial objectives. It was also suggested by Ahmad & Satti (2017), Akter et al. (2021), Burki et al. (2018). Historically, MFIs depends on donations, yet their sustainability is doubtful as donations alone are inadequate (Akter et al., 2021; Maeenuddin et al., 2020). According to Burki et al. (2018), the financial viability of MFIs was strongly influenced by financing costs and the outreach share of female borrowers. The magnitude of the loan positively affects Pakistan’s microfinance institutions’ ability to remain financially stable. Burki et al. (2018) analyzed the data of 25 MFIs operating in Pakistan for a period of 7 years, 2008 to 2015. They used multiple regressions for data analysis. They noted that the financial sustainability of the MFIs in Pakistan is highly dependent on the loan size of the MFIs. MFIs must achieve financial sustainability to reach the maximum number of poor people in society (Saad et al., 2018). Li et al. (2023) examined the factors affecting the financial sustainability of the MFIs in Chinese context by using primary data. They used Principal Components Analysis (PCA) to analyze the relationships. They found that financial condition, external environment and size enhance the financial sustainability of the MFIs in China.

According to Mumi et al. (2018), MFIs were created with varying capital structures and institutional goals, leading to numerous organizational structures. The impact of informal institutional disparities between MFIs and their partners from industrialized nations is sigmoid-shaped (Golesorkhi et al., 2019). NGOs outperform credit unions and commercial banks in terms of financial success (Mumi et al., 2018). Smaller and slower-growing businesses are more likely to fail than larger ones. According to Musah et al. (2019), there is a significant positive correlation between a company’s growth and its financial performance as measured by return on assets (ROA), a negligible positive correlation with return on equity (ROE), and a negligible negative correlation with return on capital employed (ROCE). According to Callén and Fernández (2019), expansion increases company profitability in the short run. According to Naz et al. (2019), one of the key elements influencing the profitability and sustainability of MFIs in Pakistan is average loan size. According to Mekonnen and Zewudu (2019), MFIs with a bigger clientele have a greater value of operational self-sufficiency (OSS) and low cost per borrower, demonstrating that the breadth of outreach boosts the sustainability of microfinance institutions. Previous studies have mostly looked at the factors that affect financial sustainability (Burki et al., 2018; Shkodra, 2019), how it affects outreach (Kar, 2020; Remer & Kattilakoski, 2021), and other factors that affect the financial sustainability of MFIs (Ahmad et al., 2019; Memon et al., 2020b; Naz et al., 2019; Parvin et al., 2020).

In short, even if there is a large extent of research and previous studies available on the performance and efficiency measurement of MFIs in the world, there is a lack of studies on the factors affecting the performance of MFIs, specifically in developing countries context. Investigating different factors and their impacts on MFIs’ performance is necessary. It has been noted that it is necessary to find the answer to the questions, that is why MFIs in Pakistan are less efficient. Why is Poverty still high? Why is there low women’s empowerment despite tremendous growth in the country’s microfinance sectors? This study will contribute by examining the impact of organizational structure, women’s empowerment, growth outreach, and an optimum mix of financial resources on the financial performance, and sustainability of the microfinance sector of Pakistan. The question of how to measure financial sustainability is always a problem. Because of this, this study made a new financial sustainability index that looked at the MFPs in Pakistan in a different way.

Hypothesis Development

There are 6 hypothesis have been developed and tested in this study as shown in research frame work in figure 1. The respective supporting theories also have been mentioned in the figure.

Research framework with theoretical support.

Organizational Structure

There are primarily two types of MFPs presents in the industry that is, microfinance banks and non-bank MFIs. Non-bank financial institutions (NBFI) are regulated by the central bank and operate under a combination of public and private ownership. Mumi et al. (2018) noticed that NGOs outperform credit unions and commercial banks in terms of financial success. Chakravarty and Pylypiv (2015) noted that private funding is positively associated with MFI’s abilities to filter borrowers and watch repayment rates. Various studies that is, Cull et al. (2009), Morduch and Graduate (2002), Quayes (2015) show that MFPs can still be profitable while pursuing their outreach objectives. However, Barry and Tacneng (2014) concluded that NGOs are more profitable and have better outreach than banks and cooperatives. Based on the above literature this study tested the following hypothesis to examine the relationship between OS and FS of MFPs.

H1: There is a significance relationship between the OS and FS of the MFPs.

Growth-Outreach

Smaller, slower-growing businesses are more likely to fail than larger ones. The correlation between a company’s growth and financial performance is supported experimentally by a number of studies. According to Musah et al. (2019), the firm’s growth is significantly correlated with its financial performance as measured by return on assets (ROA), insignificantly correlated with return on equity (ROE), and insignificantly correlated with return on capital employed (ROCE). According to Naz et al. (2019), one of the key variables determining the profitability and sustainability of Pakistan’s MFIs is average loan size. The extent of outreach has an impact on financial sustainability (Kinde, 2012). Mekonnen and Zewudu’s (2019) research reveals that MFIs with more customers exhibit better operational self-sufficiency (OSS) and low cost per borrower, demonstrating that the breadth of outreach boosts the sustainability of microfinance institutions. The number of active borrowers has been found to have a substantial influence on the viability of microfinance organizations (Masanyiwa et al., 2022). The following hypothesis was thus investigated in this investigation.

H2: There is a significance relationship between the GO (loan size & number of active borrower) and FS of the MFPs.

Women Empowerment

As women are less mobile, more prone to social pressure, and more responsible when it comes to instalment payback than males, hence, their participation as borrowers increases financial success (Mia et al., 2022). Ahmad and Satti (2017) claim that there are conflicts in findings from earlier studies on microfinance and empowerment. According to Ahmad and Satti (2017), women with higher loan cycles had greater levels of empowerment. According to Khan et al. (2020), the microfinance industry helps women with income, consumption, and financial security. According to Burki et al. (2018) and Muhammad et al. (2019), women are far more likely to be attracted to one another than males (matching theory); hence, the payback rate rises, which benefits the financial viability of MFIs. According to Memon et al. (2020a), the fact that majority of the borrowers are women who reside in remote rural regions raises the cost of transactions, which has an unfavorable effect on the financial viability of MFIs. According to Perera (2021), the percentage of female borrowers had no discernible impact on the financial viability of MFIs in Sri Lanka. According to Memon et al. (2020a), women’s engagement has an influence on outreach that goes beyond financial viability. According to Aziz and Aziz (2019), the performance of MFBs is greatly impacted by the proportion of female borrowers. In terms of loan usage and payback, women are more effective than males (Muhammad et al., 2019). The proportion of female borrowers has a considerable favorable influence on MFIs’ overall financial success. Ghosh and Guha (2019) came to the conclusion that gender diversity improved MFIs’ financial performance. The study by Burki et al. (2018) found a strong correlation between the percentage of female borrowers and the financial viability of micro lenders. Based on the aforementioned research and conflict findings, the following hypothesis was investigated in this study.

H3: There is a significance relationship between PWB and FS of the MFP.

Liquidity

Liquidity risk is exposed to MFPs more as a result of the growing percentage of deposits (Lützenkirchen & Weistroffer, 2012). For MFPs with higher deposits, maintaining an optimal amount of immediately accessible financial resources is crucial. According to Ngumo et al. (2017), the financial performance of MFBs in Kenya is marginally negatively impacted by liquidity risk. Oludhe (2011) drew the conclusion from his research that there is no correlation between liquidity and financial success as shown by the firm’s return on equity (ROE). According to Maaka (2013), the firm’s liquidity and leverage have a detrimental impact on the profitability of commercial banks. Kimari (2013) discovered an association between effective credit risk management and MFIs’ financial success in SACCOS Kenya. The aforementioned material has been used to test the following hypothesis.

H4: There is a significance relationship between liquidity and FS of the MFP

Leverage

The MFIs’ ability to absorb losses is determined by their debt-to-equity ratio (Tehulu, 2013). MFIs frequently become unsustainable when their potential for absorption is lost. The link between the debt to equity ratio (leverage) and the financial performance of MFIs has been the subject of several researches (Masanyiwa et al., 2022; Parvin et al., 2020). Leverage has a negative association with MFI’s sustainability, according to Mia and Ben (2016). Kinde (2012) and Tehulu (2013) found no connection between MFI sustainability and leverage. As a consequence, conflicting findings regarding the effect of leverage on the financial sustainability of MFPs were discovered. Based on the literature mentioned above, this study investigated the following hypothesis.

H5: There is a significance relationship between leverage and FS of the MFP

Cost Efficiency

Cost efficiency is measured by cost per borrower (CPB). According to Aziz and Aziz (2019), MFBs’ financial performance is highly impacted by the adjusted cost per borrower. Mekonnen and Zewudu’s (2019) revealed that MFIs with a larger number of customers exhibit a higher value of operational self-sufficiency (OSS) and low cost per borrower, demonstrating that the sustainability of microfinance institutions is increased by the breadth of outreach. Cost effectiveness has a substantial impact on the profitability and sustainability of MFIs in Pakistan (Naz et al., 2019). The financial viability of MFIs in Ethiopia is greatly impacted by the cost per borrower (Kinde, 2012). To investigate the connection between CPB and FS of MFPs, the following hypothesis has been explored.

H6: There is a significance relationship between the CPB and FS of the MFP.

Methodology

Data Collection and Measurement of Variables

The data is taken from the World Bank’s MIX market for the years 2006 to 2018. Thirty-four MFPs from Pakistan made up the final sample of the imbalanced panel data, which produced 344 MFP-year observations. The MFPs were included in the sample based on a variety of criteria (Ahamad et al., 2022; Maeenuddin et al., 2020; Mia et al., 2016). First and foremost, MFPs must have data for at least the last 3 years, or from 2016 to 2018. Second, observations and MFPs with zero or missing values must be disregarded. As a result, the author obtained a final sample of 344 MFP-year observations from an imbalanced panel of panel data for 34 microfinance providers in Pakistan. The techniques for measuring variables, along with citations from earlier research that have utilized those approaches, are included in the table below. The techniques for measuring variables and citations to research that used them are shown in Table 1.

Measurement of Variables.

Financial Sustainability

Financial sustainability refers to MFPs’ capacity to fully fund their operations and continue providing long-term financial services to the underprivileged. The ability of MFIs to handle their operational, administrative, and financial expenditures out of their own produced income, whether subsidized or not, is known as financial sustainability.

Growth

A firm’s growth is either to increase in amount or development in the process. Increase in specific amount, for example, growth of certain parameters, that is, sales, production, exports, etc. while development in the process as improvement in quality.

Women Empowerment

Empowerment of women economically is a way to help women in their decision-making, asset possession, and support in income increment.

Liquidity

It refers to the ability of the institutions to meet the short-term demands of funds or pay short-term obligations

Leverage

It is a measurement of the relative level of debt. It is measured as Total Debt/Total Equity.

Financial Sustainability Index Principal Components Analysis (PCA)

Measurement of the financial performance of the MFIs is always difficult because most of the MFIs are subsidized, hence, it is still an unresolved issue (Saad et al., 2018). According to Iqbal et al. (2019), ratios do not provide an accurate performance assessment, as MFI can do well on one ratio but fail on another. An index is frequently simpler to understand instead of studying, analyzing, and interpreting trends across individual indicators (Saad et al., 2019). There are four sustainability indexes have been developed by different researchers, including; the Subsidies Dependence Index (SDI) by Yaron (1992), the Financial Self-Sufficiency Index (FSSI) by Christen (1995), the Financial Sustainability Index (FSI) by Rai and Rai (2012), Sustainability Index (SI) by Bhanot and Bapat (2015) and Sustainability Index of Saad et al. (2019), but each one has its demerits and deficiencies. The Subsidies Dependence Index (SDI) of Yaron (1992) focuses on subsidies. The Financial Self-sufficiency Index (FSSI) of Christen (1995) only considers the efficiency indicators. The Financial Sustainability Index (FSI) and Sustainability Index (SI) proposed by Saad et al. (2018) do not consider conventional measures, and the Sustainability Index (SI) of Bhanot and Bapat (2015) does not include the critical indicators of financial sustainability which shows the going concerns of MFIs. The indexes mentioned above did not fulfill the requirement for measuring financial sustainability. In order to measure financial sustainability, this study created a new financial sustainability index utilizing principal components analysis (PCA). The index was developed using both traditional ratios (ROA & ROE) and efficiency ratios (OSS & FSS).

Factor analysis is used to determine the components of PCA and examine the data series’ similarities (Asteriou & Price, 2001 cited by Saad et al. (2018)). It provides a means for identifying unobserved common factors, that is, financial sustainability, using a combination of the linearly independent variables in this study. Based on the study of Saad et al. (2021), the objective is to develop a mix of technical variables out of the initially available variables. The financial sustainability index is developed based on the loading of the variables. The basic conditions for factor analysis are!

Primary components are not correlated, that is, the correlation between variables is not more than .90 (Asteriou & Hall, 2007 cited by Saad et al. (2018)).

Component one has the maximum proportion of the total variations of the group of available variables and Components; the second component has the maxim out of the remaining Components, and so on.

To overcome the shortcomings of the index developed by Bhanot and Bapat (2015), Saad et al. (2019), this study estimated the financial sustainability of the MFPs by using the following equations.

Where; FSI is the financial sustainability Index of MFIs; “w” are the weight assigned by PCA; Conventional ratios ROA and ROE; Efficiency ratios are OSS and FSS. Hence Equation (1) takes the following form.

Measuring Weights Using Principal Components Analysis

PCA assigned the weights to different indicators based on their importance. To determine the scores of financial sustainability for the respective years used during analysis, four indicators have been used, including; ROA, ROE, OSS, FSS, and OSS. The loading for each of the variables is obtained by using PCA.

Table 2 illustrates the correlation between the variables used during the development of financial sustainability index using PCA. The table shows that the pairwise correlation between variables is low. According to Asteriou and Hall (2007) cited by Saad et al. (2018), it may be problematic if the correlation coefficient between two variables exceeds the critical value of .9. Taking the Asteriou and Hall (2007) cited by Saad et al. (2018) coefficient value of 0.9 as the benchmark, we concluded that correlations among primary variables used for PCA are not problematic.

Correlation Matrix of PCA.

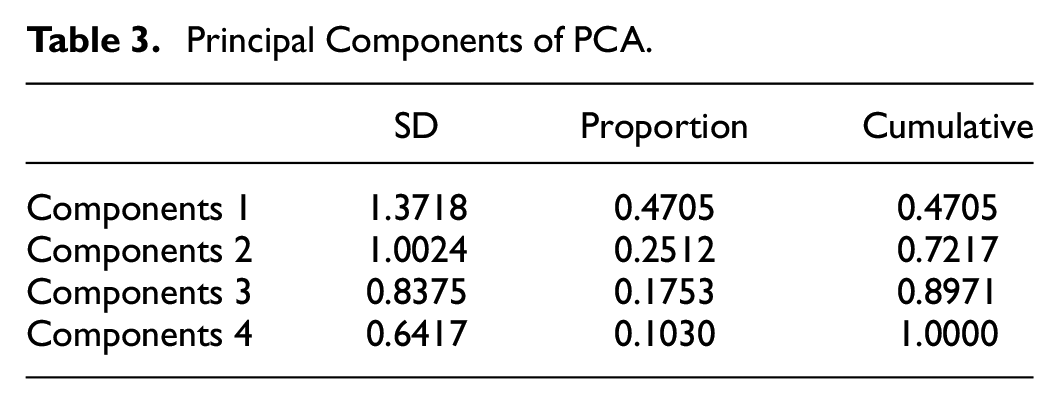

Table 3 shows the details of the four components after applying PCA using the statistical tool “R.”Table 3 shows the proportion of variation caused by each component in the group. Component number one has a maximum proportion of variation of 47.05% of the total variation, component number two has 25.12%, component number three has 17.53%, and component number four has a 10.30% variation proportion. The proportion of variations of each component has also been shown through different charts and graphs below.

Principal Components of PCA.

Table 4 shows the loading attached to each component from each of the primary variables used by PCA. Component one has the maximum variations; hence it is used for calculating the score of FSI. The weights for each of the individual variables assigned to component one are used to develop an index. The assigned weights for component one are ROA, ROE, OSS, and FSS, which are 0.628, 0.509, 0.586, and 0.000, respectively.

Loading of the Components of PCA.

By assigning weights to the respective indicators, Equation 2 takes the following form

As no weight is assigned to FSS by PCA; hence Equation (3) becomes!

The positive values for assigned weights to each of the variables show that each of the variables contributes positively towards financial sustainability. The financial sustainability score was obtained using Equation 4 for each year and every MFP.

Econometric Model

Investigating the effects of organizational structure, growth outreach, women’s empowerment, liquidity, leverage, and cost effectiveness on the FS of MFPs is the primary goal of this study. The dynamic model that follows in its most general form in line with Githaiga (2021), and Thrikawala et al. (2017), is used:

Where!

After the inclusion of the variables of the study, Equation (5) will become!

Where! The subscripts i and t represent microfinance provider and period, respectively. FS

it

is the financial sustainability of MFP i and time t. ALPB is the average loan per borrower, NAB is the number of active borrowers, and GLP is the gross loan portfolio representing the growth outreach of MFP i at time t. PWB is the percentage of women borrowers, Lqdt is liquidity, DER is debt to equity ratio representing leverage, and CPB cost per borrower represents cost efficiency for MFP i at time t. C represents the control variable, and Z shows the moderating variable in equations for each country at time t. The symbol

However, the inclusion of lag dependent variables in the model and the association of the right-side variables with the error terms have led to an endogeneity issue. The current study uses the dynamic Generalized Method of Moment (GMM) estimator or instrumental variable approach as its econometric method since the conventional panel estimators are ineffective in resolving the endogeneity issue. The study’s primary goals, which are to determine the link between financial sustainability and various factors, including organizational structure, growth, women’s empowerment, liquidity, capital structure, and cost effectiveness, are accomplished in the first portion using GMM. As noted from the preliminary regression tests mentioned above, endogeneity, heteroskedasticity, and autocorrelation exist in the model, which has been detected during different preliminary tests. Hence, the Generalized Method of Moments (GMM) is the main model for hypothesis testing. For moderation analysis, all the countries, namely Pakistan, India, and Bangladesh, are run separately to avoid the multicollinearity problem (Maimun et al., 2021).

Analysis and Findings

Descriptive Statistics

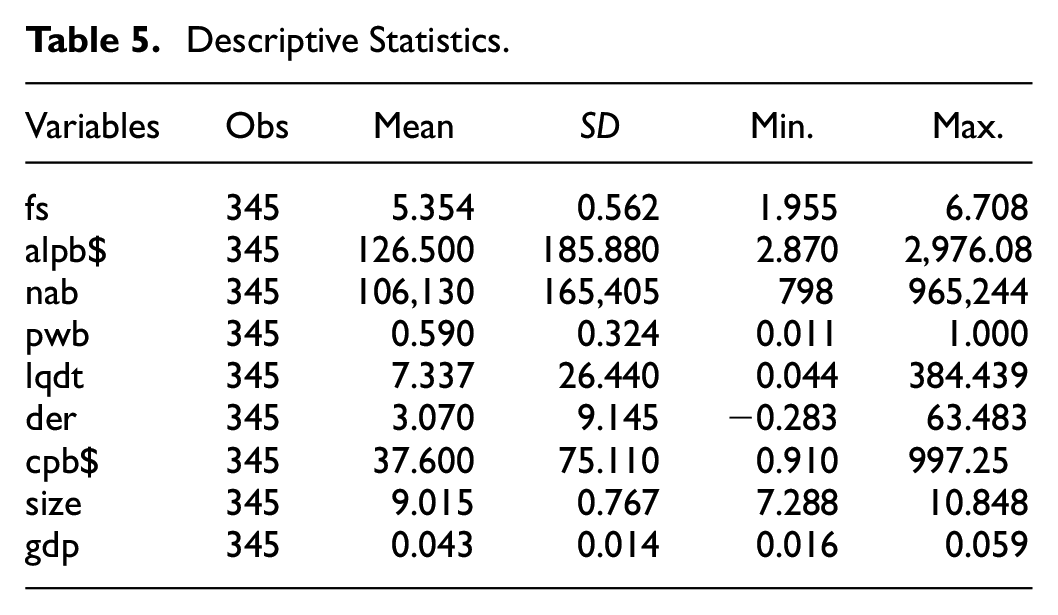

The descriptive statistics for all variables are shown in Table 5 below. Each of the variables used in the study is listed, along with the number of observations, mean, standard deviation, minimum, and maximum values.

Descriptive Statistics.

The statistics for Pakistan’s microfinance industry are shown in Table 5. The average FS value is 5.354, and the highest value is 6.708, indicating that the majority of MFPs have high FS values. The majority of the data set is in the vicinity of the mean value, as indicated by the standard deviation of 0.562. In other words, based on the aforementioned assertion, we may assume that 95% of the value of FS lies between 4.23 and 6.478 or between 5.354-(2 × 0.562) and 5.354+ (2 × 0.562). There have been 345 observations in all. The mean value of ALPB and NAB reveals that the majority of MFPs have numerous borrowers and smaller average loan size. Most data points are closer to the mean value, as shown by the standard deviation (SD) for ALPB and NAB. The depth of outreach is demonstrated by the average loan per borrower (ALPB). The ALPB serves as a stand-in for the borrower’s socioeconomic status (Kinde, 2012). The MIX benchmark estimates that the typical loan amount is USD 307. The mean amount of the typical loan size in the current study is USD 126.50. It demonstrates that MFPs operating in Pakistan have superior loan size performance. The maximum amount of ALPB’s typical loan size is USD 2,976.08. Serving consumers that are comparatively not impoverished is indicated by the greatest value of the maximum value (Kinde, 2012).

The number of active borrowers (NAB) has been used as a proxy for measuring the MFP’s breadth of outreach. The benchmark categorizes MFPs into three sizes: small (defined as having fewer than 10,000 borrowers), medium (defined as having between 10,000 and 30,000 borrowers), and big (defined as having more than 30,000 borrowers) (Kinde, 2012). According to the above tables’ findings, it was determined during the current study that the mean value of NAB is 106,130, which is larger than 30,000 and is regarded as big. The SD value is substantially greater than the mean values, indicating that the scope of most MFPs’ outreach is narrower. The majority of MFPs have a larger percentage of female borrowers, according to the mean value of the percentage of women borrowers (PWB). It shows the MFPs’ emphasis on the participation and empowerment of women. Most data points are closer to the mean value, according to the SD. Similar to that, leverage’s (DER) average value is 3.07. This demonstrates that MFPs operating in Pakistan are primarily financed by debt. The mean score indicates that Pakistan’s microfinance industry still depends on contributions, subsidies, and grants, which are insufficient to keep things running properly. Because of this, their sustainability is never assured in comparison to that of their neighbors. The average cost per borrower is observed to be 37.60, with the maximum value being 997.25, indicating that most MFPs have greater expenses per borrower. The highest values indicate that, in comparison to its neighbors, Pakistan’s microfinance industry spends the greatest money per borrower (Balkenhol, 2007; Hermes and Lensink, 2007; Kinde, 2012).

Pearson’s Correlation

Research projects typically include a correlation matrix to help researcher’s spot multicollinearity among their explanatory variables. Asteriou and Hall (2007) cited by Saad et al. (2018) say that estimating can be hard if the correlation coefficient between two variables is more than .90.

Table 6 illustrates the correlation between all the variables in the data sample from the microfinance sector of Pakistan. It has been noted that there is an issue of collinearity between the control and moderating variables. The correlation coefficient of size with NAB and GLP is more than 0.80 (80%). Some of the moderating variables have a high correlation. Table 6 shows a positive association between FS and ALPB, NAB, GLP, PWB, LQDT, Capital Structure, Size, and GDP. A negative correlation has been noted between financial sustainability and OS, and Cos per Borrower.

Correlation Matrix.

Regression Analysis

Regression is based on the sample, which the author wants to know whether the sample is a good representative of the population, whether the parameters that we estimate with the help of the sample may show the same result in the population, or whether they are good estimators, and we want to know how good is our prediction power, how good we can predict the value of DV based on IVs.

Endogeneity

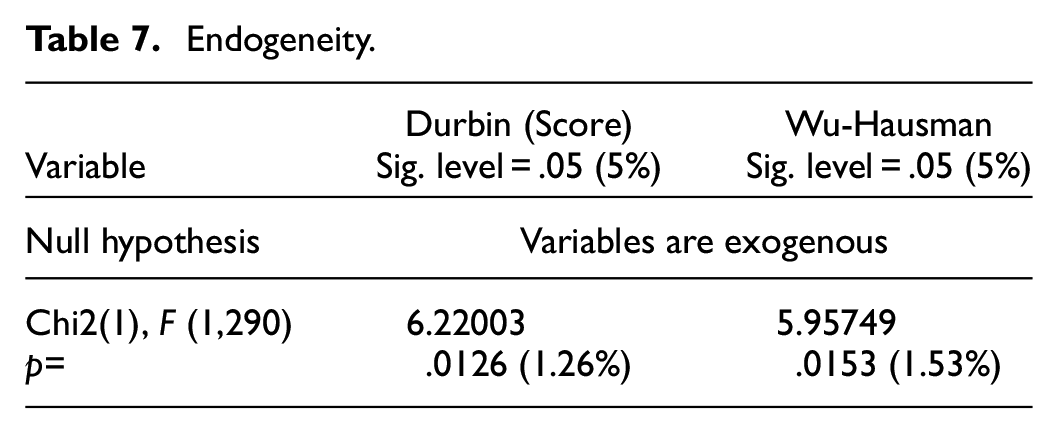

A situation where an independent variable (IV) is correlated with its error term. In the presence of endogeneity, the coefficient is biased. The main causes behind the existence of endogeneity are measurement error, omitted variables, and simultaneity in simultaneous equation models. The result of the endogeneity test has been presented in the follwoing Table 7.

Endogeneity.

An endogeneity test has been conducted with the null hypothesis that the variables are exogenous. Hence, from the results in Table 7, we noted that the p-value was significant at a 5% significance level. Hence, we concluded that endogeneity exists in the model. One of the main ideas behind running the GMM model is that there is endogeneity.

Overall, neither POLS nor fixed effect is the appropriate method for estimating the dynamic relationship between variables. The panel data approach can tackle the correlations between lagged DV and unobserved residual in the model, which is why most studies preferred it. However, the cross-sectional approach leads to biased estimates due to a correlation between lagged DV and country-specific effects. With the panel approach, which is characterized by large samples with large time dimensions, this problem disappears but does not disappear in the case of time averaging. Thus, the nature of the structure must be dynamic due to the existence of the correlation. Hence, the time-averaging cross-section method also can be biased. And the fixed effect model will not be able to correct it. However, all these problems can be solved by the GMM technique of estimation (Generalized Method of Moments. In accordance with the studies of Hussain et al. (2021), the system GMM technique is used in this study to reduce the likelihood of biasness. In a dynamic panel model when there is a correlation between independent variables and their error term, it compensates for the endogeneity of the lagged dependent variables. Additionally, it accounts for measurement errors, unobserved panel heterogeneity, and biases due to missing variables (Hussain et al., 2021).

Regression Analysis Using System GMM

From the following summary table of the system GMM results, also showed in the figure 2, it has been noted that the overall model goodness of fit test (F-statics) has a significant value of 0.0001, which shows that the fit is good. The Hanson test (0.0174) shows that endogeneity exists, the instruments are valid, and the model is well specified. By rejecting the null hypothesis at a 47.4% significance level, the AR (2) test (0.474) proved that there was no second-order autocorrelation in the model.

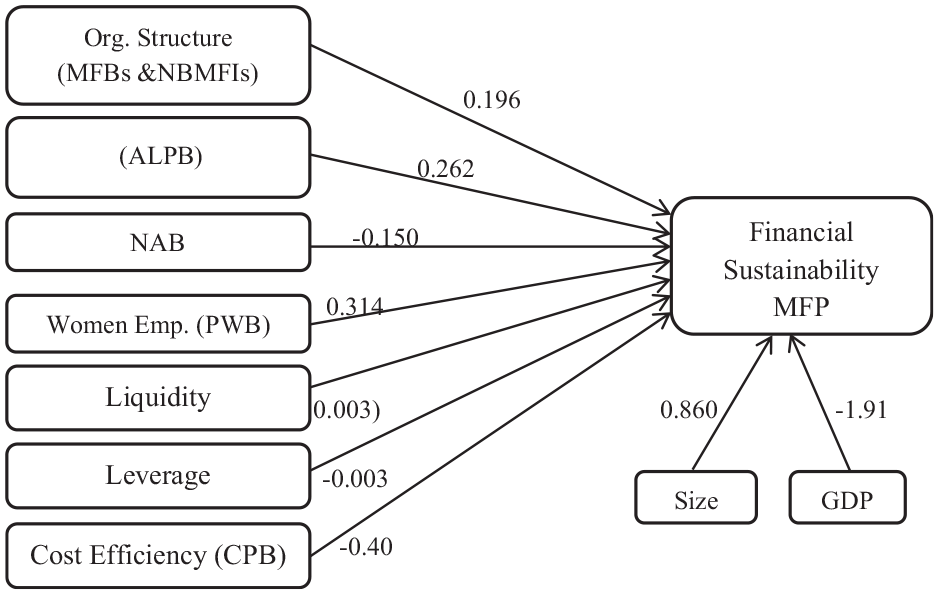

Framework coefficients.

From the summary Table 8 and figure 2, we noted that the p-value of all explanatory variables L.FSI, OS, ALPB, NAB, PWB, Lqdt, DER, CPB_log, and control variable size is less than 0.05 (5%), which shows that all of these variables have a significant relationship with the dependent variable except control variable GDP as GDP has a significant relationship at a 10% level of significance. From the individual significance test t-statistic, we also noted that t-static values for all independent and control variables except GDP (−1.70) are more than the critical value of 1.96 in absolute form, which shows the significance of the relationship. Hence, from both the p-value and t-statistic, it has been concluded that there is a significant relationship between each independent variable and the financial sustainability of the MFPs. System GMM is a short-run estimation. Hence, we tested all the significant relationships in the short run to generate long-run relationships. The explanatory and control variables that have a significant relationship with financial sustainability in the short run also have a significant relationship in the long run. At the 1% significance level, one unit increase or decrease in the financial sustainability index during the current year is associated with a 0.17 unit increase or decrease in the financial sustainability of the next year, at the 1% significance level, on average, ceteris paribus. Hence, the current year’s financial sustainability of MFPs and the next year’s financial sustainability of MFPs exhibit a significant positive relationship.

System GMM Results (Dep. Var: FSI).

Note: ***,**,* denote significance at 1%, 5%, and 10% respectively, Inside parenthesis are t-statics values.

A significant positive relationship between organizational structure and the financial sustainability of microfinance providers has also been noted. ALPB and FS exhibit a significant positive relationship. The beta coefficient of NAB is −0.1496 at a 1% level of significance, which shows that there is a significant negative relationship between NAB and the financial sustainability of the microfinance providers in Pakistan. A significant positive relationship has been noted between the percentage of women borrowers and financial sustainability as the coefficient of PWB is 0.3142 at a p-value of .000, significant at a 1% significance level, all else equal. At a 1% level of significance, the liquidity ratio has a significant positive relationship with the financial sustainability of MFPs. However, leverage, cost per borrower, and control variable GDP negatively affect the financial sustainability of the MFPs of Pakistan. The negative relationship between leverage and FS is significant at a 5% significance level. The relationship between cost per borrower and FS is significant at a 1% significance level. However, the relationship between GDP and FS is significant at a 10% significance level.

Robustness Check

The results from the preceding sections are subject to robustness checks in this section. In this test, additional control variables (capital adequacy ratio, or CAR) have been included to see if the results are subject to the number of independent variables included.

The results of the Two-Step GMM are reported in the above Table 9. The results pass the Hanson test of overidentifying restrictions and the Arellano-Bond test of autocorrelation. The signs and sizes of the coefficients of interest are consistent with the previous estimates (except for some minor fluctuations). At all times, the coefficient of independent variables is also statistically significant at the same significance level. These results suggest that the reported results in the preceding sections are robust. They are not sensitive to the addition of other control variables.

System GMM Results (Dep. Var: FSI).

Note. ***,**,* denote significant at 1%, 5%, 10% respectively.

Discussion

From the results in the previous section, it has been noted that the p-value of all explanatory variables L.FSI, OS, ALPB, NAB, PWB, Lqdt, DER, CPB_log, and control variable size is less than 0.05 (5%), which shows that all of these variables have a significant relationship with the dependent variable except control variable GDP as GDP has a significant relationship at a 10% level of significance. According to Golesorkhi et al. (2019), the relationship between MFIs and their partners in industrialized nations is sigmoid-shaped as a result of informal institutional inequalities. On the other hand, formal institutional variations do not improve the performance of MFIs. Mumi et al. (2018) claim that non-profit MFIs’ (NGOs’) organizational design is ideal for attaining MFIs’ main goals. NGOs outperform banks and credit unions in terms of profitability. Overall, the above results suggest that an increase in ALPB positively affects the FS of microfinance providers. The result is consistent with the findings of Burki et al. (2018), Githaiga (2021), Javid and Abrar (2015). This result is against the study of Rahman and Mazlan (2014), Rizkiah (2019).

The author draws the conclusion that this study opposes the existence of a trade-off between the breadth of outreach and long-term financial viability in the Pakistani microfinance industry. According to this argument, increasing the depth of outreach will have a detrimental impact on the financial viability of the micro lenders by raising the cost per borrower. According to LOGOTRI (2006), cited by Mekonnen and Zewudu (2019), “one of the most important sustainability factors for microfinance providers is the breadth of outreach or NAB.” The negative beta coefficient demonstrates that the FS of MFPs in Pakistan is adversely impacted by the number of active borrowers. The outcome of the studies of Churchill (2020), Rahman and Mazlan (2014) and this study are consistent. The for-profit institution’s financial sustainability is improved as a result of the rise in NAB, whereas the non-profit institution’s FS is reduced (Churchill 2020). This contradicts the research published in Githaiga (2021), Mekonnen and Zewudu (2019), and Rizkiah (2019). The results of the Usman et al. (2016) study indicate a negligibly weak association between NAB and FS. The value of operational self-sufficiency is higher and the CPB is lower in MFIs with more customers, demonstrating that NAB enhances the sustainability of MFIs (Mekonnen & Zewudu, 2019). These findings provide credence to the idea that in Pakistan’s microfinance industry, there is a trade-off between NAB and FS.

Positive correlation exists between financial stability and the proportion of female borrowers (PWB). Mia et al. (2022) found that female borrowers’ improved organizing and monitoring abilities and more responsible loan utilization had a significant favorable impact on MFIs’ financial success. Low-income female borrowers use their loans in a well-programmed manner and have lower default rates than males (Mekonnen & Zewudu, 2019). This demonstrates that decreased arrears and loan loss rates have a favorable impact on the financial stability of MFPs (Mekonnen & Zewudu, 2019). The promising results are in line with studies by Aziz and Aziz (2019), Burki et al. (2018), Ghosh & Guha (2019), Ahmad et al. (2012), Mia et al. (2022), Muhammad et al. (2019). The results are in opposition to those from Hossain and Khan (2016), Mersland and Strom (2010).The findings indicate a strong positive correlation between LQDT and FSI. More financial issues are brought on by a lack of liquidity than by any other financial factor (Njeri, 2014).

Leverage has a negative relationship with FS of the MFPs of Pakistan, which is consistent with the studies by Githaiga (2021), Rahman and Mazlan (2014), Usman et al. (2016). This study contradicts the results of the study Mia et l. (2016). This opposes the study of Hossain and Khan (2016), Kinde (2012), Rai and Rai (2012), Saad et al. (2021), Tehulu (2013), where the result shows an insignificant association between DER & financial sustainability, which supports the argument that different combinations of capital do not enhance the FS of microfinance institutions (Saad et al., 2021). An increase/decrease in CPB reduces/enhances the financial viability of Pakistan’s MFPs, assuming all other factors remain constant. The negative relationship suggests that MFPs’ financial sustainability can be improve with cost reduction strategies (Mekonnen & Zewudu, 2019). This result is consistent with Usman et al. (2016) and contradicts Rahman and Mazlan (2014), who found that CPB had a significant positive association with financial sustainability as evaluated by MFI operational self-sufficiency. MFIs with a low cost per borrower demonstrate that the breadth of outreach promotes the viability of microfinance institutions (Mekonnen and Zewudu, 2019). The positive association between size of the MFP on the FS of MFP is consistent with studies by Agboklou and Özkan (2023), Li et al. (2023). GDP has an inverse relationship with the FS of Pakistan’s MFPs. This is consistent with Memon et al. (2022). It went against what Hussain et al. (2021) found a positive link between the financial efficiency and GDP.

Conclusion, Implication, Limitations, and Recommendations

Conclusion

This study examined the relationship between various factors and its impact on financial stability of MFPs of Pakistan. It analyzes data from 34 MFPs in Pakistan over the period 2006–2018. A financial sustainability matrix was developed using PCA to measure financial sustainability of MFPs. ROA, ROE, OSS, and FSS were used as components for developing the financial sustainability index. Due to the inclusion of lagged dependent variables as part of explanatory variables for the persistency of the estimates, the model becomes dynamic. Hence, GMM is arguably the right regressor for estimating the dynamic panel data. Transformation of MFIs to MFBs has a significant positive effect on the microfinance sector of Pakistan. Proxies for measuring growth outreach: the loan size has a significant positive association with FS, and active borrowers have a negative association with FS of MFPs in Pakistan. The percentage of women borrowers significantly positively impacts FSI in Pakistan. Liquidity has a significant positive effect on FSI in the Pakistan context. The capital structure (D/E) has a significant positive impact on FS in the microfinance sector of Pakistan. The cost per borrower negatively affects the MFP’s financial sustainability in microfinance sector of Pakistan. The control variable MFP size enhances the FS of MFPs in Pakistan. GDP growth negatively affects FS of the MPFs in the Pakistani context.

Implications of the Study

This study has numerous potential applications. To achieve a higher level of sustainability, MFIs in Pakistan must be financially independent, requiring little to no assistance from the government or donor agencies. Since the MFIs’ main goal is to reach as many poor people as possible, they tend to make their loans bigger. Regulatory authorities must carefully monitor loan amounts because larger loans may boost a small business’s chances of success by providing more resources for its growth. Policymakers must recognize that the sustainability level of MFIs can be best attained if they emphasize both financial and social outreach. The MFIs in Pakistan have been continuously expanding their scope during the last 2 decades. For long-term viability, they must prioritize attracting indigent clients and expanding their target population. If sustainability goals are met, the microfinance industry can do better and contribute directly to the attainment of 8 out of 17 UN 2030 SDGs, including SDG1 eradicating Poverty, SDG2 ending hunger, SDG3 decent health, SDG4 quality education, SDG5 gender equality, and SDG10 reducing inequality. Additionally, it can encourage economic growth, enhance industry and infrastructure, and advance gender equality.

Limitations of the Study

The current study has some drawbacks. First off, data for 2018 onward is seriously affected by COVID-19, which also cannot be included in the current data set. Hence, future studies can analyze the data from the pre-COVID-19 and post-COVID-19 periods to compare the analysis and examine the pandemic’s impact. Secondly, the theoretical framework for the study was created from an institutional perspective and does not consider the sustainability of MFIs concerning external factors like unemployment, interest rates, and economic growth. Future studies can integrate external factors and other institutional variables to understand the proposed model better.

Footnotes

Acknowledgements

The authors would like to extend their appreciation to King Saud University for funding this work.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: We would like to extend our appreciation to King Saud University for funding this work through the Researcher Supporting Project (RSP2024R481), King Saud University, Riyadh, Saudi Arabia.

Ethical Approval

This is not applicable.

Data Availability Statement

To our regret, these data are part of a larger research project that has yet to be published and cannot yet be made public.