Abstract

Based on dynamic capability and contingency theory, authors examined the direct connection between Service innovation, Marketing innovation and Customer satisfaction, and the interacting mechanism of competitive intensity. The research model and hypotheses were developed from extant studies. Respondents from 300 microfinance banks participated in the survey. Analyses in Smart PLS software showed that Service innovation positively and significantly affects Customer satisfaction. Marketing innovation promotes customer satisfaction. Furthermore, the influence of Service and Marketing innovation on Customer satisfaction is greater in a competitive environment. Therefore, microfinance bank managers must continue to invest in innovation-related capabilities (service and marketing) to keep their customers satisfied. Theoretical and managerial contributions are highlighted in the study.

JEL Classification: M10, M31

Keywords

Introduction

Changes in demographics and technology have led to firms developing new solutions to satisfy customers (Nwachukwu & Žufan, 2017). More so, intense competition fosters uncertainty in different industries (Gavrea et al., 2011), causing serious issues for firms and executives. Besides, organizations need to monitor the value they are offering to customers (Meyer & Schwager, 2007). “Innovation is the introduction of new or significantly improved goods or services, process, new marketing methods, or new organizational methods in workplace or external relations” (OECD and Eurostat, 2005). Innovation enables new and established firms to gain competitive advantage (Lichtenthaler, 2020). Customers show favorable intentions when they benefit from innovation; a new way of solving existing problems or delivering services (Sakamoto, 2019; Wang, 2019). To have satisfied customers, companies must create and renew their capabilities. In this context, Service and Marketing innovation are organizational capabilities that enable firms to create innovative products/services to exceed customers expectations. It has been established that innovation fosters competitiveness and growth (e.g., Baldassarre et al., 2017; Pitelis, 2009). A recent study has linked innovation in the service sector to economic growth (Rajapathirana & Hui, 2018). Service innovation entails “new ways that service systems,” including microfinance banks can adopt to enhance customer satisfaction (Christensen et al., 2011). Service innovation help firms to stay ahead of competition (Hall et al., 2005) by creating value for customers. Marketing innovation focuses on optimizing marketing methods, resources, and capabilities (Nwachukwu et al., 2018). Marketing innovation involves the successful marketing of a new product or service to exceed customers expectations (YuSheng & Ibrahim, 2020).

Extant literature suggests that customer satisfaction foster superior performance, yet many firms fail to execute customer-focused strategies (e.g., Borowski, 2015; Meyer & Schwager, 2007). External factors such as customer demand and competitors to innovation (e.g., Yalabik & Fairchild, 2011) and internal organizational factors (e.g., Herzog & Leker, 2010; Murat Ar & Baki, 2011; Oke et al., 2013) affect innovation. More so, innovation studies have majorly focused on the manufacturing sector (e.g., Jaw et al., 2010; McDermott & Prajogo, 2012). Yet, studies that explain the relationship between innovative service attributes and customer satisfaction is limited (Truong et al., 2020). Studies on Service innovation, Marketing innovation and customer satisfaction, especially in microfinance banks are scarce. Yet, there is a need to understand the role Service innovation and Marketing innovation play in fostering customer satisfaction, especially in microfinance banks in the emerging market context. Researchers (e.g., Mahmoud et al., 2018; Nwachukwu, 2018) call for more research on innovation in services and customer satisfaction, especially in Africa. Reduced competition can benefit consumers through enhanced innovation (Marshall & Parra, 2019). Extant literature affirms that competitive intensity influences firm behavior, competitive advantage (e.g., Auh & Menguc, 2005; Correa & Ornaghi, 2014), engagement capability and firm performance (Anning-Dorson & Nyamekye, 2020) and innovation performance (e.g., Nwachukwu et al., 2019). Some empirical studies suggest otherwise (e.g., Ghosh et al., 2017; Hashmi, 2013), implying that the context under which competitive intensity should work is relatively unclear. Brodzicki (2019) further buttress that the nature of the association between competition intensity and innovation is ambiguous, scare and not fully established in transition economies. Nonetheless, innovation activities depend on factors outside the firm such as customers, competitors and legislations (e.g., Yalabik & Fairchild, 2011).

Additionally, the understanding of the market or conditions under which service innovation and marketing innovation is more or less beneficial is limited. Therefore, it becomes important to have a better insight into the role of competitive intensity in fostering and/or constraining the effect of innovations (service and marketing) on customer satisfaction. In light of these arguments, the authors introduced competitive intensity as a moderating variable in this study. The authors reasoned that competitive intensity could strengthen the impact of Service and Marketing innovation on customer satisfaction. This study aims to narrow the gap in the literature by uncovering the direct impact of service innovation and marketing innovation on customer satisfaction as well as the moderating effect of competitive intensity in the relationship between Service innovation, Marketing innovation and Customer satisfaction. Our measures are based on the customers’ perception of service innovation and marketing innovation as well as competition levels among firms in the microfinance industry. Arguably, customers’ behavior is likely to depend on how they perceive a specific competitive environment. This approach enables us to investigate the environmental condition (competitive intensity) and the relationship between innovation (service and marketing) and customer satisfaction. The main contribution of this study is the use of contingency lens to uncover the moderating effect of competitive intensity on Service innovation, Marketing innovation and Customer satisfaction in microfinance banks in the emerging market. This is consistent with the basic insight of the contingency perspective that customer satisfaction depends on service innovation and marketing innovation. Competitive intensity has an enhancing effect on innovation and customer satisfaction. Arguably, intense competition will propel firms to engage in innovation in service and marketing to remain competitive. Using dynamic capability perspective, we enrich the literature by providing empirical insights on service innovation, marketing innovation and their effect on customer satisfaction. Moreover, this study also employed a relatively new statistical software (SmartPLS) to test the relationship depicted in the conceptual model.

This paper is arranged as follows. Next section, this paper discusses an overview of the theoretical background, hypotheses development. Then, the methodology employed in the paper. Next is the results. Finally, discussion, conclusions, theoretical and managerial implications and future research agenda.

Theoretical Background

The dynamic capabilities perspective suggests that firms leverage capabilities to remain competitive in a changing business environment (e.g., Bellner, 2013; Teece et al., 1997). Teece (2018) opine that the “strength of a firm’s dynamic capabilities supports the speed and degree of matching resources and business model(s) with customer needs and aspirations.” Dynamic capabilities allow organizations to identify opportunities, threats and take timely decisions (Barrales-Molina et al., 2013; Barreto, 2010). Dynamic capabilities facilitate the combination and transformation of resources and knowledge into products and services that will meet customers’ expectations (Makkonen et al., 2014). Arguably, the ability of firms to change and adapt resources and organizational capabilities promote competitive edge. According to Ambrosini and Bowman (2009), “dynamic capabilities are intangible assets of a firm, specific processes, patterns and organizational routines.” Dynamic capabilities allow firms to locate new markets and technology (Teece, 2007) and evaluate existing and new capabilities to create value for different stakeholders (O’Reilly & Tushman, 2008). Arguably, organizational capabilities and managerial processes firms control foster customer satisfaction. Service and Marketing innovation are dynamic capabilities that can enhance customer satisfaction. In evaluating the role of competitive intensity as a moderator, authors use the contingency perspective as the theoretical lens. Contingency theory assumes that firms need to match’ strategies or capabilities with the environment in which they operate to achieve competitive advantage (Donaldson, 2001). Indeed, the impact of the predictor (service and marketing innovation) on the criterion variable (customer satisfaction) depend on the moderator (competitive intensity). In the light of contingency theory, the extent to which service innovation and marketing innovation will flourish will be contingent on competitive intensity.

Hypotheses Development

Links between service innovation and customer satisfaction

Chen et al. (2018) finds that leisure farm customers are satisfied with the innovative services offered by the firm. In Vietnam, Ta and Yang (2018) observe that interaction and support foster customer satisfaction and retention in telecommunication companies. Using the survey method, Lin et al. (2014) report that service innovation allows cultural parks in Taiwan to satisfy their customers and customer attributes strengthens the impact of service innovation on customer satisfaction. Cabral and Marques (2020) asserts that innovation allows a firm to improve the quality of service delivery and meet their customers need. Wikhamn (2019), highlights the importance of service innovation in enhancing customer satisfaction in the hospitality industry. Yeh et al. (2019) suggest that service innovation enable firms to gain advantage and enjoy long-term relationships with customers by guaranteeing high-quality products and services. In Ghana, Mahmoud et al. (2018) submit that innovative services are important for mobile telecommunication customers. Using structural equation modeling, Bellingkrodt and Wallenburg (2015) observe that customer relations in terms of innovativeness enhance customer satisfaction. In Norway Aas and Pedersen (2011) demonstrates that service innovation improves financial performance in manufacturing firms compared to service firms. Darroch and McNaughton (2002) contend that innovation is important to meet customers expectations. It could be argued that implementing innovative services could foster customer satisfaction.

H1. Service innovation will influence customer satisfaction.

Links between marketing innovation and customer satisfaction

Value propositions and the nature of industry affects a firm’s decision to implement marketing innovation. It can be argued that firms operating in the service sector tend to adopt marketing innovation compared to manufacturing companies. Wang (2015) submits that marketing innovation studies focus on three main areas; “ marketing innovation as a source of competitive advantages, marketing innovations and other types of innovation and the characteristics of firms that use marketing innovations.” “Marketing insight” (Linoff, 2004) and “marketing imagination” are two key drivers of marketing innovation. Firms need to optimize marketing innovation to achieve superior performance (Desouza et al., 2009; Naidoo, 2010). YuSheng and Ibrahim (2020) underscore the importance of marketing innovation to Banks growth and profitability. Simiyu (2013) argues that “strong brands, appropriate pricing, customer retention and satisfaction” are important marketing innovation strategies use by commercial banks. Marketing innovations foster profitability (Soltani et al., 2015) and performance (e.g., Olughor, 2015; Otero-Neira et al., 2009). Similarly, Zuñiga-Collazos and Castillo-Palacio (2016) report that innovative marketing strategies help Colombia tourism companies to satisfy their customers. Using a sample of 538 participants, Lee et al. (2015) observe that the use of marketing innovation improves customer satisfaction in Taiwan. In Tanzania, Senguo and Kilango (2015) report a robust link between marketing innovation, customer satisfaction and performance. Likewise, Raja and Wei’s (2014) submits that marketing innovations significantly influence both society and customer satisfaction. However, Atalay et al. (2013) observe that market innovation is not connected to business performance. Indeed, how marketing innovation affects performance is relatively unclear. It is important to adopt marketing innovation to create value for customers and the firm. We expect marketing innovations to improve customer satisfaction in microfinance banks operating in Nigeria.

H2. Marketing innovation positively and significantly impact customer satisfaction.

Competitive intensity as contingent factor

This contingency theory can be used to explain how competitive intensity affect innovations (service and marketing). Extant literature suggests that the effectiveness of a “strategic orientation (innovativeness)” (Lumpkin & Dess, 2001), innovation orientations (Auh & Menguc, 2005) and the intensity of firm’s innovation activities (Trott, 2012) depend on environmental factors. This study focuses on one environmental factor: competitive intensity (e.g., Prajogo, 2016). “Competitive intensity is the degree of perceived hostility in the environment because of competition or the actions taken by a firm that affect other firms’ survival” (Ang, 2008; Zhang et al., 2019). Competitive environments are often characterized by price war and low-profit margins because customers use price in making purchase decisions. Consequently, firms operating in a competitive environment focus more on leveraging resources to remain competitive. In this study, competitive intensity refers to intra-industry competition which implies competition between firms in the microfinance industry. It is the degree of competition perceived by customers in terms of services offered by the banks. Empirically, Jansen et al. (2006) observed that the impact of “service innovation (exploratory and exploitative)” on financial performance is stronger when environmental dynamism and competitiveness is high. In competitive settings, only high satisfaction can lead to customer loyalty and discourage customer attrition. Previous studies have examined interacting mechanisms of competitive intensity in different contexts (e.g., Anning-Dorson & Nyamekye, 2020; Estrada-Cruz et al., 2020; Zhang et al., 2019). Yet, little is known about the moderating effect of competitive intensity on the effectiveness of Service and Marketing innovation in terms of how they affect customer satisfaction. It is important to consider this issue because the relationship between competitive intensity and innovation may not be the same when service and marketing innovations are treated separately. In this context, authors consider innovation as a multidimensional construct (i.e., service and marketing) based on the assumption that each of the indicators may be effective under different business environments. In a highly competitive environment, customers have several alternatives to meet their needs. Arguably, the effect of Service and Marketing innovation on customer satisfaction may be contingent on competitive intensity.

H3. The positive impact of service innovation on customer satisfaction is stronger when competitive intensity is high.

H4. The positive impact of marketing innovation on customer satisfaction is stronger when competitive intensity is high.

The proposed conceptual model in Figure 1 focuses on the relationship between Service innovation, Marketing innovation, Competitive intensity and Customer satisfaction. The model contains four hypotheses. It predicts that the two types of innovation have positive impacts on customer satisfaction (H1–H2). In addition, the model shows that competitive intensity moderates the two innovation–customer satisfaction relationships (H3–H4).

The conceptual model.

Methodology

Sample and Data Collection

Considering socio-economic challenges such as population growth, high unemployment rate and social unrest, the role of microfinance banks in fostering economic growth in Nigeria cannot be overemphasized. Microfinance banks can develop innovative capabilities to address the inefficiencies and future challenges facing them in Nigeria. EFInA, in its Access to Finance Survey in Nigeria in 2016, reports that about 42 % of adults find it difficult to access financial services. Indeed, there is a serious gap as many poor and low-income households are not able to access financial services. As such, adopting innovative strategies could bring financial services to the unbanked or un-served market. In Nigeria, microfinance banks are confronted with a fast-changing and complex operating environment. According to the Central Bank of Nigeria (2016), “the number of MFBs declined from 879 to 820 in 2013 and grew to 987 in 2016, total asset declined by 5.1% (N343.9 billion to N326.2 billion), total deposit liabilities declined by 6.1% from N159.5 billion in 2015 to N149.8 billion in 2016, net loans and advances increased by 6% to N178.0 billion in 2016 from N167.9 billion in 2015 and investments increased by 13.5% from N17.7 billion in 2015 to N20.1 billion in 2016.” These data reflect the complex nature of the microfinance industry in Nigeria. Thus, the microfinance sector is considered appropriate to test the hypotheses because of the environment in which they operate. Authors selected microfinance banks from three geopolitical zones. These zones have a strong presence of microfinance banks. Four experts and two researchers evaluated our questionnaire before sending them to participants. The survey was conducted from September 2018 to October 2018. The authors employed a cross-sectional quantitative research approach. This approach is appropriate for testing hypotheses quantitatively. Online surveys and emails were used to collect data from 325 participants who were conveniently selected. The online survey was sent to the e-mails of participants to ensure that relevant individuals complete the survey. 300 responses were suitable for the analysis conducted. This represents a 92% response rate which is adequate for data analysis and drawing conclusion (Bryman & Bell, 2015).

Measures and Analytical Approach

Following past studies, we use established measurement instruments. Few changes were made where necessary to suit the purpose of the present study. Our questionnaire considers respondents’ characteristics, Service innovation, Marketing innovation, competitive intensity and Customer satisfaction. Authors use a five-point scale to make the analysis of responses easy, a scale ranging from 1 (strongly disagree) to 5 (strongly agree) was employed to measure service and marketing innovation. To measure service innovations, marketing innovation and customer satisfaction we adapted (Nwachukwu, 2018). Four questions were used to collect data on service innovation, which focuses on “reliability of service,” “speed” “service quality” and “use of advanced technology.” For marketing innovation, four questions were used to elicit information, which included, “use social media” “new marketing methods,” “customer relationship,” and “customers/suppliers’ collaboration.” The questions on customer satisfaction require respondents to choose from options, 1 (very dissatisfied) to 5 (very satisfied). Three questions were used to measure customer satisfaction, which included: “value-added services,” “flexibility in products/services delivery” and “turnaround time.” The variables were evaluated based on customers’ perceptions. The study adapted Jansen et al. (2006) measure of competitive intensity, used in prior studies (e.g., Prajogo, 2016). The items are “competition in our market is intense,” “our organizational unit has relatively strong competitors,” “competition in our market is extremely high” and “ price competition is a hallmark of our market.”

We use Smart PLS software due to the “prediction-oriented nature” of this study (Hair et al., 2016). Smart PLS is appropriate for analyzing many dependency relationships at the same time (Ringle & Sarstedt, 2016). Authors analyzed the reliability and validity of the research model. We carried out “internal consistency” (Cronbach’s alpha α) analysis and a “confirmatory factor analysis” (CFA) in Table 1 and Appendixes 3 and 4. All factor loadings were higher than 0.5, which mean that the latent variables were represented by indicators (see Appendix 3). Authors computed the “average variance extracted” (AVE) and the “composite reliability” (CR) for the measures used in our study. Table 1 illustrates Cronbach’s alpha, the AVE, and the CR of the research variables. All variables are above the acceptable level (0.7), and the results suggest that the measures are consistent and valid (Hair et al., 2014). Indeed, all the measurement items contribute significantly to their examined constructs (Ringle & Sarstedt, 2016). “Rho A and CR values in Table 1 indicate the constructs’ consistency and internal reliability, and the AVE values suggest convergent validity” (Hair et al., 2016). Table 2 shows that multicollinearity is not a problem in this study because all VIF values are less than 5 (Hair et al., 2016). The heterotrait-monotrait ratio (HTMT) results of Table 3 suggest “constructs’ discriminant validity.”

Confirmatory Factor Analysis (CFA), Cronbach’s Alpha α, Rho A, AVE, CR.

Source. Own elaboration.

VIF Values.

Source. Own elaboration.

Discriminant Validity.

Source. Own elaboration.

Common Method Bias Test

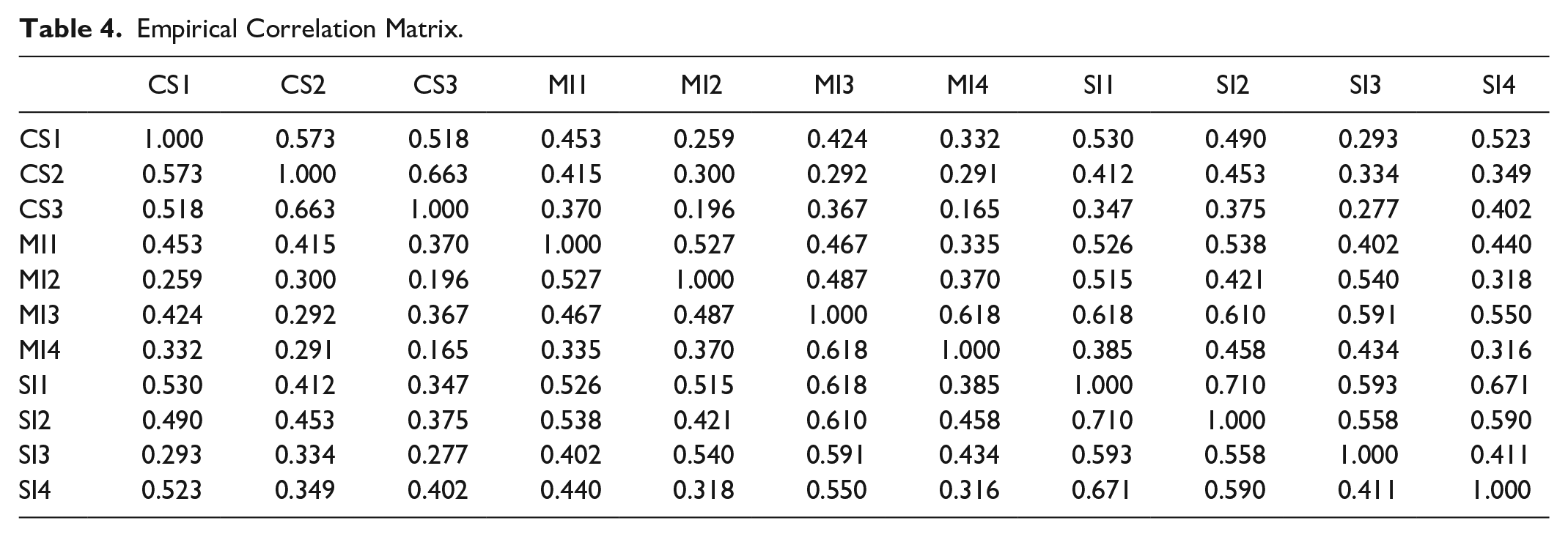

Respondents were assured that their responses will not be revealed to a third party and that is mainly for research purpose (Conway & Lance, 2010; Podsakoff et al., 2003). Participants were informed that study variables (i.e., independent and dependent variables) are not related (Podsakoff et al., 2003). According to Bagozzi et al. (1991), “common method bias is likely when there is a high association among principal constructs (r > .9).” The correlation between the items is well below the recommended threshold, which means the issue of common method bias is unlikely (see Table 4). Based on these analyses, the authors affirm that the model fit the data and appropriate for testing the research hypotheses.

Empirical Correlation Matrix.

Results

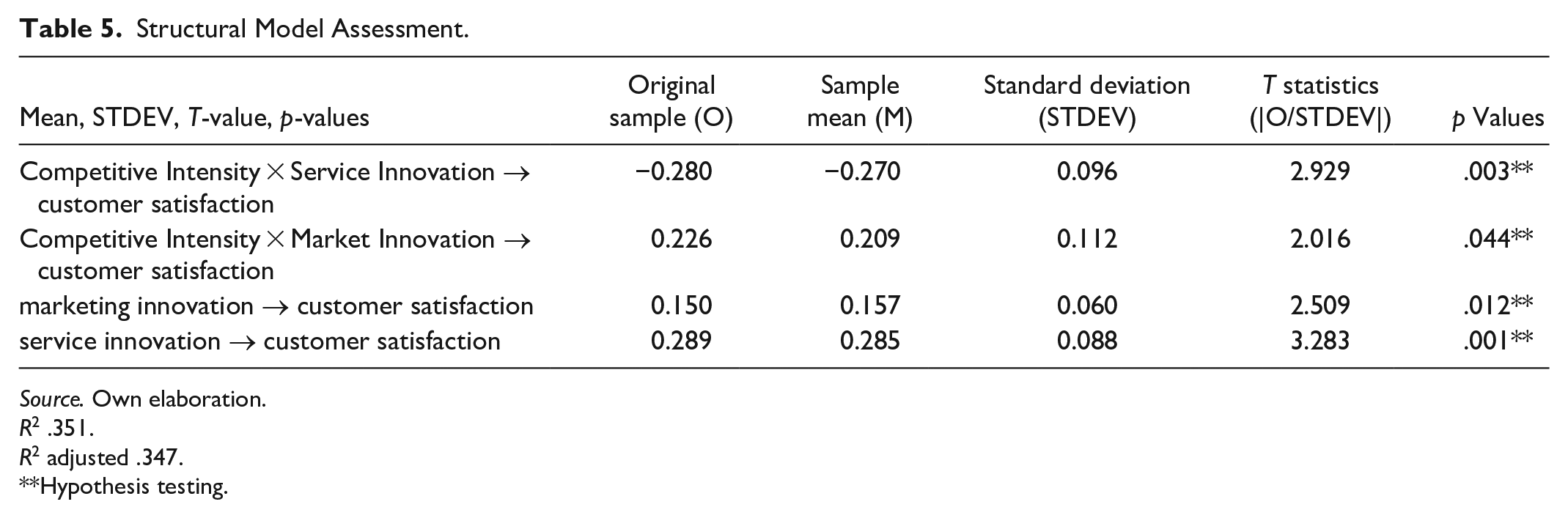

We used PLS bootstrapping method to estimate whether the model is statistically significant using 5000 subsamples. We verify the hypotheses by using the path coefficient and “t” value. The results in Table 5 and Appendix 1, for service innovation (R2 = .442, t = 3.283, p = .001) and marketing innovation (R2 = .184, t = 2.509, p = .012) supports all direct hypotheses (H1 and H 2). Specifically, these results support the notion that service and marketing innovations promote customer satisfaction. Further, competitive intensity moderates the effect of service innovation (t = 2.929, p = .003), and marketing innovation (t = 2.016, p = .044) on customer satisfaction. Thus, providing support for Hypotheses H3 and H4. R2 value .442 and R2 value .184 indicates moderate and relatively weak variance explained in service innovation and marketing innovation respectively. Table 5 shows an R2 value of 35.1%, which means that all the constructs jointly account for 35.1% change in the dependent variable (customer satisfaction). This implies that other variables not considered in this study account for 64.9% variation in customer satisfaction. Table 6 highlights the effect size (f2). f2values of “ 0.02 are small,” “0.15 is moderate “ and “0.35 is strong” (Cohen, 1988). Our results suggest that the f2 for all variables are small. The results of the control variables (firm size and age) were not reported because they did not affect the model.

Structural Model Assessment.

Source. Own elaboration.

R2 .351.

R2 adjusted .347.**Hypothesis testing.

Effect Size f2.

Source. Own elaboration.

Discussion

Recent studies are increasingly giving attention to the important role of innovation in fostering organizational outcomes (e.g., YuSheng & Ibrahim, 2020). To enrich recent research streams, this paper examined the relationship between service innovation, marketing innovation and customer satisfaction. Further, our study explored the moderating effect of competitive intensity on the relationship between service innovation, marketing innovation and customer satisfaction. The result regarding the connection between service innovation and customer satisfaction is fully supported. This finding lends support to previous studies (Aas & Pedersen, 2011; Bellingkrodt & Wallenburg, 2015; Chen et al., 2018; Mahmoud et al., 2018; Lin et al., 2014; Ta & Yang, 2018) concerning the influence of service innovation on customer satisfaction. Interaction and support service innovation dimensions are essential for enhancing customer satisfaction and retention (Ta & Yang, 2018). Microfinance banks can optimize technology to improve the reliability of their service and swiftly deliver services better than competitors. MFBs can differentiate themselves by investing in service innovation that is difficult to copy. Additionally, our findings show that Marketing innovation foster Customer satisfaction. This result is consistent with other arguments in the literature (Zuñiga-Collazos & Castillo-Palacio, 2016) that Marketing innovation foster customer satisfaction and company’s image (Schubert, 2010; Varis & Littunen, 2010), facilitate entry to new markets (Lee et al., 2015; Raja & Wei’s, 2014; Senguo & Kilango, 2015). Microfinance banks can use social media to advertise their products and improve customer relationships. By leveraging marketing innovations companies can better understand their customers’ needs and satisfy them. Collaboration and co-creation with their customers enable firms to create innovative products and services (Osakwe, 2020). However, authors also find that the effectiveness of service and marketing innovation is influenced by competitive intensity. Our findings reveal that competitive intensity positively and significantly moderates the link between Service innovation, Marketing innovation and Customer satisfaction. This implies that the effect of Service and Marketing innovation on customer satisfaction is stronger in more competitive environments. In situations of intense competition, the relationship between Service innovation, Marketing innovation and customer satisfaction improves. Customers’ perception of their industry can impact a firm’s service and marketing innovation activities. The innovation (service and marketing) generates customer satisfaction when competition is high. Intense competition will lead to the introduction and marketing of new products or services which influences customers perception of the firm’s ability to satisfy their needs (Luo & Bhattacharya, 2006). This finding agrees with recent studies (e.g., Anning-Dorson & Nyamekye, 2020; Estrada-Cruz et al., 2020; Prajogo, 2016; Zhang et al., 2019) concerning the moderating mechanism of competitive intensity on business results. However, this finding negates (Hashmi, 2013) who submits that competition does not promote innovation. A possible reason for this result may be due to differences in the study context.

Conclusion

This study examined the impact of Service innovation and Marketing innovation on customer satisfaction in the Nigerian microfinance Banking sector. Further, it uncovers the interacting mechanism of competitive intensity in the relationship between Service innovation, Marketing innovation and Customer satisfaction. Our study shows that both Service innovation and Marketing innovation influence customer satisfaction. The study suggests that the relationship between Service innovation, Marketing innovation and Customer satisfaction is strengthened when competitive intensity act as moderating variable. Intense competition propels Service innovation, Marketing innovation and customer satisfaction. Therefore, firms should develop supportive innovation culture to enhance customers experience and satisfaction.

Theoretical Implications

Considering the scare empirical studies regarding these constructs, particularly in the emerging market context, our study enriches the dynamic capability and innovation literature. This study shows that Service innovation and Marketing innovation contributes to customer satisfaction. Therefore, Service innovation and Marketing innovations are dynamic capabilities that organizations must leverage. Using contingency theory, this study demonstrates the benefit of achieving strategic fit between innovation and customer satisfaction in the context of competitive intensity. In affirming the role of competitive intensity as a moderator, our result aligns with the contingency theory which suggests that the effectiveness of innovativeness depends on environmental factors (e.g., Auh & Menguc, 2005) and market conditions (Trott, 2012). By integrating dynamic capability and contingency theory, the benefits of service and marketing innovation in a competitive environment is affirmed. To our knowledge, this study is among the few that assessed the interacting mechanism between competitive intensity, innovation (service and marketing) and customer satisfaction.

Managerial Implications

Our study has practical implications for managers and their firms. To attract and keep customers, firms must provide innovative services more efficiently and effectively better than the competition (Feldman Barr & McNeilly, 2003). In this context, Service and Marketing innovation can enhance microfinance banks efficiency and make them competitive. Therefore, microfinance banks must adopt service and marketing innovations to positively influence customer satisfaction. Indeed, dynamic capabilities (service and marketing innovations) need organizational investment. Investment in tracking customer satisfaction levels can give useful insights into the level of satisfaction customers derived from consuming a company’s products. Elaborating on this, Oladejo and Akanbi (2012) opined that bank managers see e-banking as a tool for reducing “inconvenience,” “transaction costs,” and “changing customers queuing pattern.” Therefore, microfinance banks must consciously develop and invest in innovation-related capabilities (service and marketing) so, they can achieve higher customer satisfaction levels. The finding that competitive intensity positively moderates the impact of Service and Marketing innovation on customer satisfaction highlight the need for managers to give attention to their marketing initiatives and the quality of service they are providing in the competitive environment. By doing so, managers can leverage opportunities and market segments in such environments. Finally, this study provides valuable insight to managers by highlighting the importance of competitive environment in promoting innovation. On the other hand, if managers fail to recognize the importance of competition, microfinance banks may experience customer attrition and dissatisfaction as they will not be able to implement Service and Marketing innovation.

Limitations and Future Research Direction

We observe below the limitations of this study and some suggestions for future research. First, this study uses perceptual measures for assessing service and marketing innovations as well as customer satisfaction. Future studies can use real metrics and objective data if available. This study employs cross-sectional research design, hence there is a need to view the directional relationship reported in this study with caution. Future research can use longitudinal and qualitative research approach to explain the nature of the proposed relationship. This study focused on the microfinance industry. Though, a single industry study minimizes complexities that are characterized by many industries analysis (Parida & Örtqvist, 2015; Patel et al., 2015). Nonetheless, we suggest that future research should explore multiple industries to provide more insights and support the generalizability of the results. Considering the importance of innovations for firms (Börjesson et al., 2014), future studies should be done to validate the results of this study and to identify other antecedents and consequences of innovation capability and customer satisfaction.

Footnotes

Appendix

Cross Loadings.

| Outer loadings | Customer satisfaction | Marketing innovation | Service innovation |

|---|---|---|---|

| CS1 | 0.849 | 0.491 | 0.564 |

| CS3 | 0.868 | 0.427 | 0.467 |

| CS4 | 0.830 | 0.376 | 0.425 |

| MI1 | 0.490 | 0.797 | 0.576 |

| MI2 | 0.299 | 0.738 | 0.526 |

| MI3 | 0.429 | 0.835 | 0.706 |

| MI4 | 0.318 | 0.716 | 0.472 |

| SI1 | 0.516 | 0.668 | 0.902 |

| SI2 | 0.523 | 0.665 | 0.869 |

| SI3 | 0.355 | 0.626 | 0.728 |

| SI4 | 0.508 | 0.540 | 0.820 |

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This paper is partly funded by Van Lang University, Ho Chi Minh City, Vietnam.