Abstract

With capital markets’ growing attention to sustainable development, environmental, social, and governance (ESG) factors have become increasingly important in shaping corporate financing decisions. However, whether changes in ESG ratings (upgrades or downgrades) effectively signal shifts in a firm’s operational risk and transparency is unclear. Moreover, little research has explored whether these signals influence firm financing costs, particularly across ownership structures and regulatory environments. This study uses data from Shanghai and Shenzhen-listed firms from 2014 to 2023 to examine how dynamic ESG rating changes affect their debt financing costs and analyze the associated market responses. Across the full sample, ESG rating upgrades are associated with modest reductions in the debt financing costs, whereas downgrades raise debt financing costs, revealing an asymmetric pricing pattern in which creditors respond more strongly to negative ESG signals than to positive ones. Ownership structure moderates these effects, for non–state-owned enterprises, upgrades lower and downgrades increase debt financing costs more visibly than for state-owned enterprises. Following implementation of the new Securities Law, the impact of ESG rating changes on debt financing costs has become more pronounced. Robustness checks using alternative ESG providers and instrumental-variables estimation yield consistent results. These findings provide empirical insights for firms, investors, and policymakers to optimize financing strategies and improve ESG-related regulations.

Plain Language Summary

This study uses data from Shanghai and Shenzhen-listed firms from 2009 to 2023 to examine how dynamic ESG rating changes affect their cost of debt and analyze the associated market responses. The results reveal asymmetric responses to such rating changes, showing that while ESG upgrades do not significantly lower debt costs, downgrades substantially increase them, especially for non-state-owned enterprises. Furthermore, the impact of ESG downgrades on debt costs has become more pronounced following the implementation of the New Securities Law, suggesting regulatory reforms have enhanced market sensitivity to ESG information.

Introduction

The concept of environmental, social, and governance (ESG) factors has recently garnered increasing attention in global capital markets. The ongoing refinement of ESG evaluation systems, disclosure standards, and indicator frameworks has significantly advanced the systematic development and practical application of ESG principles (Li et al., 2021). As a key tool for quantitatively assessing corporate ESG performance, ESG ratings communicate the principle of balancing economic gains with social responsibility (Khan, 2019) and have become increasingly integrated into the investment decisions and strategic planning of investors, regulators, and corporate managers.

Driven by China’s “dual carbon” strategy and its commitment to high-quality development, localization of ESG governance concepts has progressed rapidly. ESG aligns closely with China’s new development philosophy of “innovation, coordination, greenness, openness, and sharing,” offering a systematic and quantifiable framework that supports realization of its “dual carbon” goals and advancement of sustainable development strategies (Ge et al., 2022). Policymakers have introduced a series of regulations to promote institutionalizing ESG disclosure standards and rating frameworks. For instance, the China Securities Regulatory Commission revised the Code of Corporate Governance for Listed Companies in 2018, strengthening legal requirements related to ESG disclosure. These institutional changes have not only strengthened the regulatory foundation for corporate responsibility governance but have also allowed ESG ratings to assume an increasingly prominent role in capital market resource allocation.

Existing studies have found that ESG ratings are closely associated with a firm’s development level, and companies with high ESG ratings are more likely than those with low ratings to achieve superior operational performance in the future (Dimson, 2015). Strong ESG performance helps mitigate information asymmetry (Kim & Park, 2023; Luo et al., 2023) and enhances market trust, effectively reducing financing costs (Brogi & Lagasio, 2019; Eliwa et al., 2021). Evidence also suggests that, compared to companies with weak ESG ratings, companies with strong ratings are more likely to deliver high returns (Alda, 2020; Chen et al., 2023a). ESG ratings serve as a non-financial signal that reflects a firm’s governance quality and risk management capabilities, significantly shaping investor decisions during the financing process (Cesarone et al., 2024). Supporting this view, Zhang et al. (2024) found that firms with higher average ESG ratings tend to attract more institutional investors than those with lower ratings.

However, compared to the static level of ESG ratings, research on dynamic changes in ESG ratings remains relatively limited. Emerging studies suggest that shifts in ESG ratings can prompt the market to reassess a firm’s future performance and risk profile. Fatemi et al. (2018) found that improvements in ESG ratings enhance firm value, whereas declines reduce firm value. In particular, ESG downgrades and negative ESG-related news are often interpreted as signals of deteriorating business operations, weakened governance, or declining capacity for sustainability, and thereby trigger adverse market reactions (Galema & Gerritsen, 2025; Shanaev & Ghimire, 2022). Xiao et al. (2024) also highlighted that in the Chinese context, changes in ESG ratings significantly intensify external monitoring mechanisms, such as institutional investor scrutiny and analyst attention, influence firms’ financial behaviors, and shape market expectations.

As both domestic and international capital markets increasingly regard ESG ratings as a key point of reference in investment decision-making, the non-financial information conveyed by these ratings has come to play a growing role in resource allocation, risk assessment, and investor behavior (Ng & Rezaee, 2020). Existing literature primarily focuses on the relationship between ESG rating levels and corporate market performance or financing constraints, while research on how changes in ESG ratings affect corporate financing costs remains limited. As an external evaluation, ESG rating changes often signal improvement or deterioration in a firm’s non-financial governance. An upgrade in ESG ratings may convey a positive signal of enhanced ESG performance and improved governance capacity, whereas a downgrade may trigger investor concerns regarding firm sustainability and potential credit risk.

According to the signaling (Uyar et al., 2020) and limited attention (Sim, 2006) theories, explicit and directional information—such as ESG rating changes—is more likely than implicit and nondirectional information to attract market attention and be incorporated into investors’ decision-making processes, thereby substantively influencing corporate financing costs. Financing costs directly influence a firm’s capital structure, investment decisions, and overall profitability. Therefore, investigating how ESG rating changes impact financing costs not only deepens our understanding of how ESG considerations shape corporate financial behavior, but also offers valuable insights for policymakers aiming to strengthen the sustainable development mechanisms of capital markets. However, existing research primarily focuses on the static effects of ESG ratings, with relatively limited attention given to how dynamic changes in ESG ratings affect firms’ financing costs. Consequently, understanding how shifts in firm ESG ratings influence financing costs has become an important area for further investigation.

The pathways and intensity of ESG factors’ influence are largely determined by a firm’s institutional environment and corporate governance characteristics. State-owned enterprises are more likely to access policy-based financing and bank credit; their incentives to improve ESG ratings often stem from regulatory compliance and reputational considerations rather than genuine engagement in ESG practices (He et al., 2015; Wan et al., 2024). Deng and Cheng (2019) found that ESG performance is positively associated with stock returns among A-share listed firms, with stronger effects observed in non-state-owned enterprises. Therefore, even if a state-owned enterprise experiences a downgrade in its ESG rating, banks typically do not substantially increase its financing costs due to policy-driven considerations and implicit government guarantees. Furthermore, investors in state-owned enterprises tend to prioritize government backing and control over strategic resources, making them relatively insensitive to changes in ESG ratings (Chen, 2024).

Regulators have continued to strengthen institutional guidance regarding ESG disclosures, actively encouraging incorporation of ESG factors into investment decision-making processes. The 2020 amendment to the Securities Law of the People’s Republic of China marked a significant regulatory shift, introducing more stringent disclosure obligations and placing greater emphasis on non-financial information (Yang et al., 2021). This regulatory transformation has enhanced both the reliability and relevance of accounting disclosures (Chen et al., 2024; Li et al., 2022) while reinforcing the influence of ESG ratings on capital market dynamics. Therefore, how ESG rating changes impact financing costs may differ between state-owned and non-state-owned enterprises, as well as across regulatory periods—specifically before and after the new Securities Law’s formal implementation.

This study investigates how dynamic changes in ESG ratings influence corporate debt financing costs. It further examines the moderating effects of firm characteristics—specifically, state-owned versus non-state-owned enterprises—and differing market environments, defined as the periods before and after the new Securities Law was implemented, to identify heterogeneity in the relationship between ESG ratings and debt financing costs.

Literature Review and Hypotheses Development

Due to the growing emphasis on sustainable finance, ESG ratings have come to play an increasingly significant role in capital markets. ESG ratings reflect a firm’s overall performance in environmental protection, social responsibility, and corporate governance. An increasing number of studies have investigated their influence on corporate financial performance and market valuation.

Numerous studies have demonstrated that superior ESG performance can lower a firm’s cost of capital by improving disclosure quality, reducing external uncertainty, and mitigating risk premiums (Eliwa et al., 2021; Luo et al., 2023; Ng & Rezaee, 2020). High ESG performance can enhance corporate reputations and strengthen investor trust, thereby contributing to higher market valuations (Friede et al., 2015). Brogi and Lagasio (2019) further found that firms with higher ESG scores generally have higher return on assets and overall market valuation. Moreover, ESG initiatives may promote long-term competitiveness by reducing information asymmetry, enhancing transparency, and strengthening relationships with key stakeholders. Firms with strong ESG performance often face lower costs of equity capital, as investors perceive them to be less risky and more operationally stable and are therefore willing to accept lower expected returns (Chen et al., 2023b).

Creditors are more inclined to offer low-interest loans to firms with superior ESG performance, whereas firms with poor ESG ratings tend to face higher debt financing costs in subsequent periods (Rong & Kim, 2024; Shi et al., 2024). Chen (2024) further pointed out that ESG ratings can significantly reduce debt financing costs by alleviating external financing constraints and enhancing firms’ debt repayment capacity. In summary, existing literature generally agrees that higher ESG ratings are associated with lower corporate financing costs.

While existing research predominantly focuses on how ESG rating levels impact financing costs, empirical investigations into whether changes in ESG ratings affect financing costs remain relatively scarce. According to signaling theory, changes in ESG ratings function as important non-financial signals to external investors and creditors, conveying information about a firm’s long-term growth potential and governance quality.

Consolandi et al. (2022) confirmed that both ESG ratings and their changes positively affect stock returns. An upgrade in ESG ratings may signal enhanced capital management, indicating that future resources will be directed toward more efficient business operations or innovation initiatives. Upgrades raise expectations of future cash flows and profitability, resulting in positive abnormal stock returns. Conversely, downgrades in ESG ratings may trigger negative market reactions (Giese et al., 2019).

Capelle-Blancard and Petit (2019) investigated how positive and negative ESG-related news affects stock prices and found that negative ESG disclosures tend to trigger stronger market reactions than positive ones. In an event study of U.S. firms from 2016 to 2021, Shanaev and Ghimire (2022) found that upgrades in ESG ratings were associated with positive but statistically insignificant abnormal returns, whereas downgrades led to significantly negative abnormal returns. Galema and Gerritsen (2025) analyzed MSCI ESG rating adjustment events and observed that, in the medium term—within 6 months after the event—downgrades in overall ESG ratings and environmental scores resulted in significantly negative buy-and-hold abnormal returns.

Serafeim and Yoon (2022) found that capital markets tend to react more strongly to positive than negative ESG news, suggesting that favorable ESG events are more likely to boost stock prices. These findings indicate that ESG-related information is increasingly incorporated into investors’ decision-making frameworks. Additionally, Xiao et al. (2024) found that in the Chinese market, changes in ESG ratings significantly intensified mechanisms such as institutional investor scrutiny and analyst coverage, thereby influencing corporate financial strategies and shaping market perceptions.

The correlation between ESG ratings and financing costs is significantly negative, indicating that firms with high ESG ratings tend to face lower costs of capital (Chen, 2024; Chen et al., 2023b; Rong & Kim, 2024; Shi et al., 2024;). Li et al. (2024) further found that firms with strong ESG performance experienced notable declines in debt financing costs following implementation of green finance policies.

According to signaling theory (Uyar et al., 2020), firms can convey information to the market about their underlying quality and future prospects through externally observable characteristics or actions, thereby influencing capital providers’ decisions and pricing strategies. In capital markets characterized by information asymmetry, external investors and lenders typically lack access to comprehensive internal information, rendering them particularly sensitive to externally observable signals. Changes in ESG ratings are an information signal in capital markets. Unlike the static level of ESG ratings, upward or downward adjustments are more salient and directional, making them more likely to attract immediate attention from investors and creditors.

Limited attention theory (Sim, 2006) suggests that market participants tend to focus on information that is unexpected, non-repetitive, and easy to interpret. Therefore, when a firm’s ESG rating changes, the market is more likely to interpret the change as a signal of meaningful shifts in non-financial risk and governance quality and adjust its assessment of the firm’s financing risk accordingly. Specifically, an upgrade in a firm’s ESG rating may be perceived as a positive signal of enhanced governance and strengthened accountability, thereby reducing the risk premium lenders require. Conversely, a downgrade may trigger market concerns about the firm’s reputation, regulatory compliance, and sustainability performance, ultimately leading to higher financing costs.

Compared to equity investors, creditors, as risk-averse financiers, generally place greater emphasis on a firm’s debt repayment capacity and default risk. Strong ESG performance can enhance a firm’s ability to manage environmental and social risks and reduce future cash flow uncertainty, thereby improving its access to favorable lending terms from banks and other creditors. An ESG rating upgrade conveys a positive signal to the debt market regarding a firm’s operational soundness and resulting improved creditworthiness, thereby reducing its debt financing costs. In contrast, a downgrade sends a negative signal to creditors about potential deterioration in the firm’s operations, governance, or sustainability performance, potentially resulting in higher risk premiums. Based on this theoretical framework, the following hypotheses are proposed:

China’s socialist market economy is vast and distinctive. As most listed companies were originally state-owned enterprises that were later restructured through a series of reforms into limited liability companies, many continue to maintain close economic ties with their state-owned controlling shareholders (Chen et al., 2006; Liu & Lu, 2007). This historical legacy has resulted in a prevalent ownership structure in which the state retains controlling stakes in a large proportion of listed firms in China.

Prior research suggests that deficiencies in corporate governance are a primary source of inefficiency among manufacturing firms in China (He et al., 2015). In particular, misallocating resources and productivity losses due to weak governance are more severe in state-owned enterprises, whereas non-state-owned firms tend to demonstrate more effective governance (Chen, 2024). Consistent with this view, Wan et al. (2024) found that ESG performance positively influences innovation efficiency in non-state-owned firms, while the effect is weaker or even statistically non-significant in state-owned firms. This finding is consistent with that of Chen (2024), indicating that non-state-owned firms are more effective at translating ESG initiatives into improved resource allocation and better financing outcomes. This may be attributed to the fact that ESG implementation in state-owned enterprises is primarily driven by policy and regulatory compliance rather than market-based incentives or disciplinary mechanisms.

Therefore, changes in ESG ratings are likely to have a limited impact on the debt costs of state-owned enterprises due to their relatively stable financing environment. In contrast, non-state-owned enterprises are expected to experience more pronounced changes in debt costs, as investors and creditors place greater emphasis on ESG signals when evaluating their risk profiles. Based on this analysis, the following hypothesis is proposed:

Since 2020, China has implemented a revised Securities Law that reinforces disclosure obligations, enhances the registration-based IPO system, and introduces comprehensive reforms in areas like investor protection and legal liability (Yang et al., 2021). This new legal framework has helped improve transparency and strengthen regulatory oversight in the capital market. As a result of the reform, firms have undergone notable changes in both their financial reporting practices and governance structures. For example, Li et al. (2022) reported that the revised Securities Law has effectively curbed earnings management, with non-state-owned firms’ response to the reform more pronounced than that of state-owned firms. Chen et al. (2024) further observed that while overall audit quality has improved under the new regulatory framework, the extent of improvement is relatively limited in state-owned enterprises. In summary, the existing literature generally agrees that institutional reforms significantly influence corporate governance practices.

This regulatory reform enhanced investors and creditors’ confidence in ESG information reliability, increasing the likelihood that changes in ESG ratings will affect financing decisions. Before the new Securities Law, ESG disclosures were inconsistent and only somewhat reliable, limiting the market’s responsiveness to ESG signals. After the law’s implementation, improved disclosure standards are expected to have amplified the market’s sensitivity to ESG rating changes, increasing their impact on firms’ debt financing costs. Based on this analysis, this study proposes the following hypothesis:

Methodology

Data and Sample

This study is based on a sample of listed companies from the Shanghai and Shenzhen stock exchanges, covering 2014 to 2023. This study begins the sample in 2014 because, from that year onward, China’s domestic ESG rating systems and databases underwent substantial standardization and expansion, with more unified methodologies and markedly better data availability, continuity, and coverage (Su et al., 2024). Concurrently, the quality and consistency of ESG-related disclosures improved, providing a more reliable foundation for ESG-based empirical analysis. ESG rating data are sourced from the Huazheng ESG database, while firm characteristics and financial indicators are obtained from the China Stock Market & Accounting Research database. To ensure data reliability and the robustness of the empirical results, firms in the financial industry, those designated as ST and *ST, and observations with missing ESG scores or other key variables are excluded from the sample. All continuous variables are winsorized at the 1st and 99th percentiles to mitigate the influence of outliers. The final sample comprises 20,403 firm-year observations.

Variable Measurement and Research Model

The dependent variable is debt financing cost (DebtCost), measured as the ratio of interest expense to total liabilities at the end of the period. ESG rating changes are calculated as the year-over-year difference in a firm’s ESG rating and is computed as

An ESG rating change in a given year that is greater than zero indicates an ESG rating upgrade, and the dummy variable ESG_UP equals 1; otherwise, it equals 0. Conversely, an ESG rating change less than zero indicates an ESG rating downgrade, and the dummy variable ESG_DOWN equals 1; otherwise, it is 0.

Following the empirical approach of Li et al.(2024) and Shi et al.(2024), a model is constructed to examine the impact of ESG rating changes—both upgrades and downgrades—on debt financing costs. To control for firm-level characteristics that may influence debt financing costs, the model includes a set of control variables: firm size (Size), the leverage ratio (Lev), return on assets (Roa), cash flow from operating activities (Cfo), fixed assets ratio (Fa), revenue growth rate (Grow), firm value (TobinQ), listing age (ListAge), ownership concentration (Top1), board independence (Indep), and state ownership (Soe). Year and industry fixed effects are also included.

Two primary regression models are developed to empirically assess how ESG rating changes—specifically, upgrades and downgrades—impact firms’ debt financing costs. These models build upon empirical frameworks established in prior research (Li et al., 2024; Shi et al., 2024) and incorporate a comprehensive set of firm-level control variables to address other factors that may influence the cost of debt. Model 1 examines the effect of ESG rating upgrades (ESG_UP) on debt financing costs. The regression specification is shown in Equation 1:

Model 2 investigates the impact of ESG rating downgrades (ESG_DOWN) on debt financing costs. The regression specification is as in Equation 2

Models 1 and 2 separately test the hypotheses concerning the asymmetric market responses to ESG rating upgrades and downgrades. By isolating the effects of positive and negative ESG signals, these models offer insights into whether improvement or deterioration in ESG performance has heterogeneous effects on firms’ debt financing costs. Including control variables and fixed effects in the models helps ensure that the estimated relationships reflect the unique impacts of ESG rating changes rather than those of standard firm-level determinants.

Results

Descriptive Statistics

The descriptive statistics presented in Table 1 show that the average debt financing cost (DebtCost) is 1.9%, with a maximum value of 5.8%, indicating that some firms bear relatively high debt financing burdens. Approximately 21.7% of the sample experienced ESG rating upgrades, while 18.6% underwent downgrades; the remaining firms had no changes. These results suggest that ESG ratings exhibited a certain degree of variability over the sample period.

Descriptive Statistics.

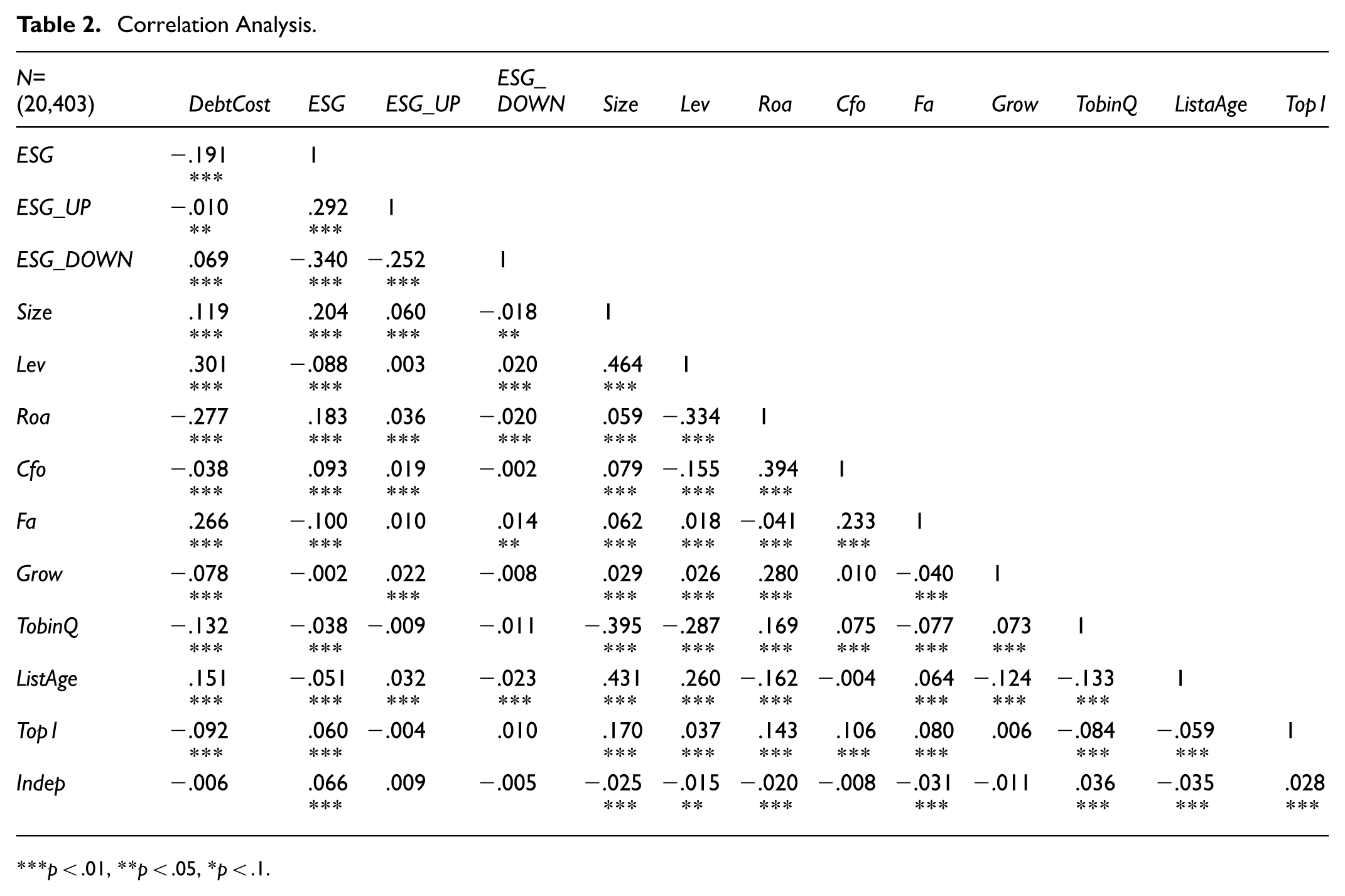

Correlation Analysis

Table 2 presents the results of the correlation analysis, revealing a notable relationship between changes in ESG ratings and debt financing costs. Specifically, the correlation coefficient between ESG rating upgrades (ESG_UP) and debt financing cost (DebtCost) is −0.010, indicating that an increase in ESG rating is associated with a reduction in debt financing costs. The correlation coefficient between ESG rating downgrades (ESG_DOWN) and DebtCost is 0.069, indicating that when a firm’s ESG rating declines, its debt financing cost tends to rise. This result suggests that changes in ESG ratings may influence firms’ debt financing decisions.

Correlation Analysis.

p < .01, **p < .05, *p < .1.

Regression Results

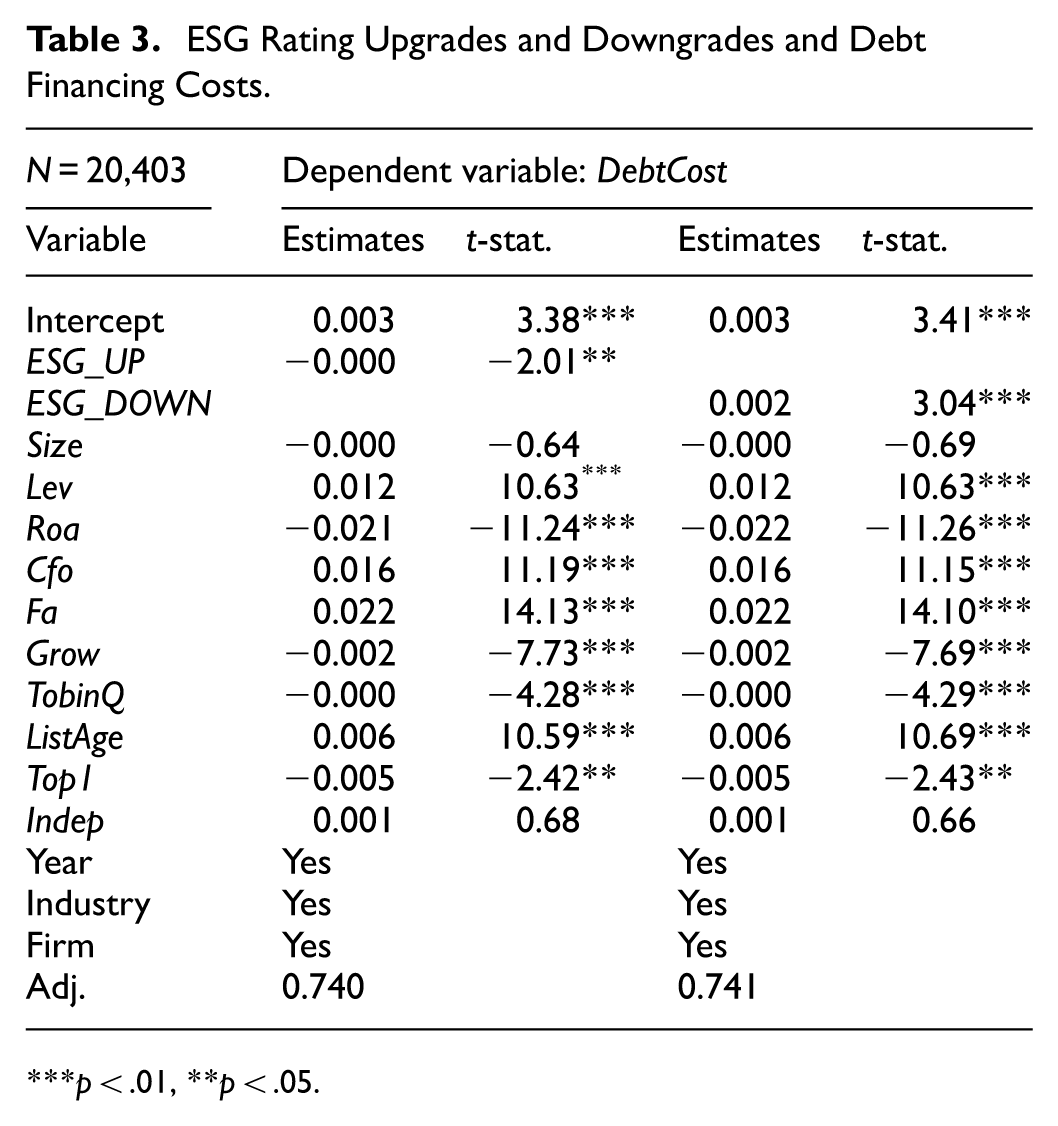

As a comprehensive indicator of a firm’s sustainable development capacity, the ESG rating may be confounded by inherent firm characteristics—such as governance structure and industry attributes—potentially biasing the regression estimates. To address endogeneity stemming from these unobservable, time-invariant factors, this study augments the baseline specification with a two-way fixed-effects framework that includes both firm and year fixed effects. The regression results in Table 3 indicate a negative association between ESG rating upgrades (ESG_UP) and the cost of debt (DebtCost): the coefficient on ESG_UP is −0.000 and statistically significant at the 5% level, implying a directionally meaningful but economically small effect. The results indicate that increases in ESG ratings are associated with a modest reduction in firms’ debt financing costs. Consistent with theoretical expectations, the negative coefficient on ESG_UP suggests that an ESG upgrade conveys credible information about operational stability and improved creditworthiness, which in turn lowers the cost of debt. Although the estimated coefficient (−0.000) appears economically small due to rounding at the three-decimal level, the effect remains statistically significant at the 5% level (t = −2.01), implying that the directional relationship is robust even if the economic magnitude is limited. In contrast, the coefficient on ESG_DOWN is 0.002 and statistically significant at the 1% level, indicating that rating downgrades are associated with higher debt financing costs. Compared with upgrades, creditors appear to treat downgrades as more credible signals of heightened credit risk, yielding an asymmetric pricing response. A plausible mechanism is the market’s greater sensitivity to negative information and the tendency for ESG downgrades to reveal underlying sustainability deficiencies—such as deteriorating environmental compliance or governance weaknesses—which in turn tighten lending terms.

ESG Rating Upgrades and Downgrades and Debt Financing Costs.

p < .01, **p < .05.

To further examine the moderating effect of ownership structure on the relationship between ESG rating changes and debt financing costs, the sample is divided into state-owned and non-state-owned enterprises for separate regression analyses. As shown in Table 4, for the subsample of state-owned enterprises, the coefficient on ESG_UP is statistically insignificant, suggesting that soft budget constraints, relationship-based lending, and implicit government guarantees limit the incremental informational content of ESG improvements and thus prevent further reductions in the debt financing costs. By contrast, the coefficient on ESG_DOWN is 0.001 and significant at the 1% level, indicating that even for state-owned enterprises with state backing, creditors respond more strongly to negative ESG signals and impose higher risk premiums when firms exhibit ESG deterioration.

ESG Rating Changes and Debt Financing Costs by Firm Type.

p < .01, **p < .05.

In contrast, for non–state-owned enterprises, the coefficient on ESG_UP is significantly negative (coefficient = −0.000; t = −2.39), indicating that improvements in ESG performance convey stronger incremental credit information to creditors and slightly reduce the debt financing costs. This pattern suggests that, in the absence of government backing, creditors place greater weight on ESG information when assessing firm creditworthiness, making ESG upgrades more effective in lowering debt financing costs. ESG rating downgrades (ESG_DOWN) have a significantly positive effect on debt financing costs. Specifically, the coefficient of ESG_DOWN is 0.002, and, with a t-value of 2.00, is statistically significant at the 5% level. This suggests that an ESG rating downgrade significantly increases the debt financing cost for non-state-owned firms. It further demonstrates that, in the absence of policy support and implicit guarantees, capital markets are more likely to interpret deteriorating ESG performance as a key signal of heightened credit risk for non-state-owned enterprises. These findings also imply that investors place greater reliance on ESG rating changes when evaluating the sustainability performance of non-state-owned firms.

To examine whether the implementation of the new Securities Law altered the market’s interpretation of ESG rating changes, the sample is divided into two periods based on the policy timeline: before (2019 and earlier) and after (2020 and later) its implementation. Separate regressions are then conducted for each subsample to investigate if the impact of the timing of ESG rating changes on corporate debt financing costs is heterogeneous. The results are provided in Table 5. Before the implementation of the new Securities Law, the coefficient on ESG_UP was negative but statistically insignificant (t = −0.69), indicating that improvements in ESG performance did not translate into meaningful reductions in the debt financing costs under the prior institutional framework. This pattern likely reflects limitations of the earlier regulatory environment—most notably an underdeveloped and weakly standardized disclosure system in its initial stage—which reduced the credibility and market salience of ESG signals. By contrast, the coefficient on ESG_DOWN was positive and significant (t = 2.25), suggesting that even before the reform, creditors were more responsive to negative ESG information and consequently imposed higher risk premiums on firms exhibiting ESG deterioration.

ESG Rating Changes and Debt Financing Costs by Timing of New Securities Law.

p < .01, **p < .05, *p < .1.

After the implementation of the new Securities Law, the coefficient on ESG_UP becomes significantly negative (t = −2.65), indicating that under a stricter disclosure and enforcement regime, ESG upgrades are more credibly recognized by creditors and are associated with a modest decline in the debt financing costs. By contrast, ESG_DOWN shows a significantly positive association with the debt financing costs (coefficient = 0.002; t = 3.34; p < .01), suggesting that ESG downgrades substantially increase debt financing costs. Overall, these results imply that the new Securities Law enhances both the informativeness and the disciplining role of ESG signals in debt pricing: the positive incentive effect of ESG improvements strengthens, whereas the penalty effect of ESG deterioration persists and becomes slightly more pronounced.

Robustness Tests

To assess the robustness of the baseline results, we replace the original dependent-variable measure with an alternative proxy—the ratio of the firm’s financing cost to total liabilities at period end (Cost1)—and re-estimate the models. The corresponding results (Table 6) are consistent with the baseline analysis: the coefficient on ESG_UP is −0.001 (t = −1.81), significant at the 10% level, while ESG_DOWN is positive and statistically significant (coefficient = 0.001; t = 2.31; 5% level). These findings indicate that the main conclusions are robust to alternative variable specifications.

ESG Rating Upgrades and Downgrades and Debt Financing Costs.

p < .01, **p < .05, *p < .1.

To further verify robustness, we replace the original Huazheng ESG data with the SynTao Green Finance ESG ratings and re-estimate Models (1) and (2). The regression results, reported in Table 7, are consistent with the baseline analysis, confirming that the conclusions are robust across alternative ESG data sources.

SynTao Green Finance ESG Rating Upgrades and Downgrades and Debt Financing Costs.

p < .01. **p < .05.

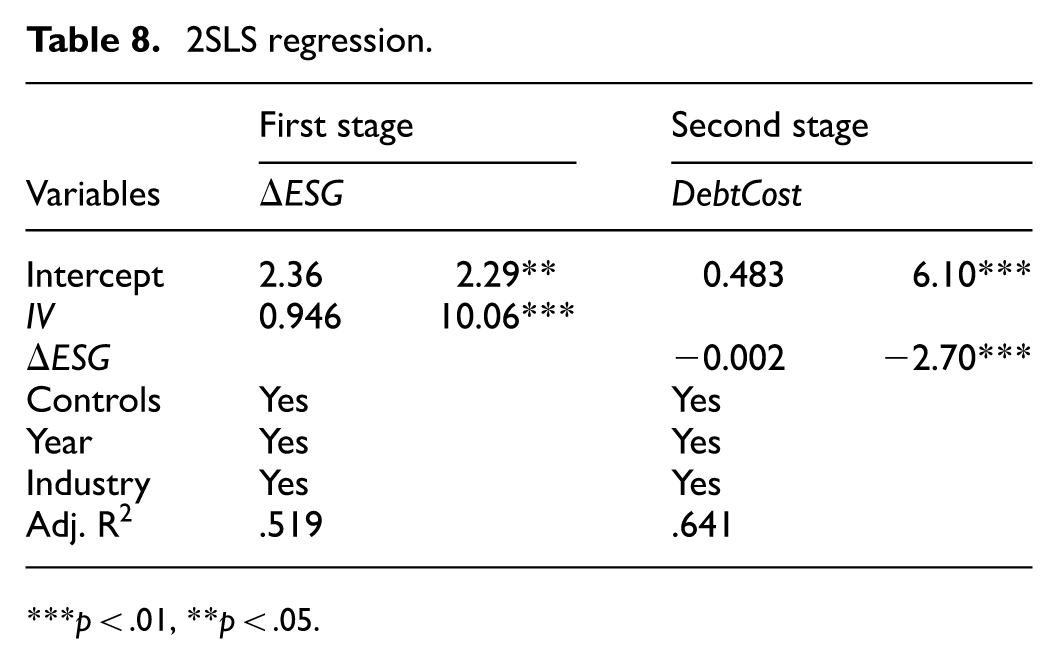

To address potential endogeneity, we employ an instrumental-variables (IV) strategy. Following Ge et al. (2022), the instrument variable is the industry-year average change in ESG ratings, excluding the focal firm. This instrument satisfies the relevance criterion because ESG actions tend to co-move within industries, capturing common shifts driven by industry norms and the external social-responsibility environment rather than firm-specific shocks. It is also plausibly exogenous to a firm’s borrowing costs conditional on controls and fixed effects, as industry-level shocks are accounted for while the instrument affects debt pricing primarily through the firm’s own ESG adjustment. In the first stage, IV exhibits a strong, statistically significant positive association with ΔESG, confirming its relevance. In the second stage, the estimated coefficient is −0.002 and significant at the 1% level, consistent with the baseline results. Table 8 reports the 2SLS regression results. These estimates indicate that, after addressing potential endogeneity, improvements (declines) in ESG ratings are associated with a significant decrease (increase) in firms’ debt financing costs.

2SLS regression.

p < .01, **p < .05.

Conclusions

This study uses data from 2014 to 2023 for a sample of listed firms from the Shanghai and Shenzhen stock exchanges to empirically examine how ESG rating upgrades and downgrades impact debt financing costs. It further explores heterogeneous effects from the perspectives of firm ownership structure and institutional environment. The key conclusions are as follows. First, in the full sample, ESG rating upgrades are associated with modest reductions in the debt financing costs, whereas downgrades raise debt financing costs, revealing an asymmetric pricing pattern in which creditors react more strongly to negative ESG signals. Second, firm ownership acts as a moderating factor. Compared to state-owned firms, ESG rating upgrades and downgrades for non-state-owned firms have a more pronounced impact on debt financing costs, reflecting stronger market discipline and greater investor reliance on ESG signals in credit risk assessments. Third, institutional reform has strengthened the market effectiveness of ESG ratings. Following implementation of the new Securities Law, the impact of ESG rating changes on debt financing costs has become more pronounced, suggesting that the pricing and signaling roles of ESG rating changes in capital markets have been enhanced.

This study examines the relationship between ESG rating changes and corporate debt financing costs, considering heterogeneous firm ownership and institutional backgrounds and offers the following insights. First, it expands the research perspective on the economic consequences of ESG information. By examining the asymmetric effects of ESG rating upgrades and downgrades, this study reveals that the market reacts more strongly to negative ESG information. These findings contribute to a deeper understanding of the informational value of ESG ratings and their role in price formation, while also broadening the research perspective on the economic consequences of non-financial information. Second, the study reveals the mediating role of ownership structure in ESG information transmission. The results deepen the understanding of how market mechanisms vary across ownership structures. Additionally, it provides empirical support within institutional contexts for future studies exploring the mechanisms through which ESG influences firms. Third, the results confirm the strengthening effect of institutional reform on the market effectiveness of ESG ratings. The differing impacts of ESG rating changes on debt costs before and after the new Securities Law was implemented suggest that institutional improvements enhance the signaling role of ESG ratings in capital markets. This provides empirical support for advancing development of the ESG rating system and improving disclosure auditing mechanisms.

We recommend coordinated action by regulators, banks, rating agencies, and issuers. Specifically, regulators and exchanges should institute event-triggered ESG disclosures supported by third-party assurance; banking supervisors should embed references to ESG rating changes in risk-based pricing and covenant design; rating agencies should require transparent methodologies and maintain auditable upgrade/downgrade trails; and issuers should deploy early-warning dashboards and downgrade-response policies. Collectively, these measures will reduce information frictions, curb rating inflation, and accelerate the incorporation of credible ESG improvements into borrowing terms.

This study has limitations that create opportunities for future research. First, the ESG rating data used in the study are sourced from the Wind database and may involve measurement errors due to the lack of transparency in rating criteria and inconsistencies among rating providers. Future studies could consider combining ESG data from multiple sources to enhance data reliability and representativeness. Second, this study does not account for the quality of ESG disclosure or potential impact of greenwashing, which may limit a deeper understanding of how markets interpret ESG signals. Future studies could incorporate greenwashing indicators to more accurately assess the economic consequences of ESG rating changes in capital markets. Third, the conclusions are based on the Chinese capital market, and the generalizability of the findings to other institutional settings requires further investigation.

Footnotes

Ethical Considerations

This article does not contain any studies with human or animal participants.

Author Contributions

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

Data will be made available on request from the corresponding author.