Abstract

ESG rating divergence (ESGRD) and ESG decoupling represent the primary manifestations of ESG information conflicts. Although ESGRD and ESG decoupling have garnered significant attention, research predominantly focuses on their implications at the corporate level. In contrast, the impact of ESGRD and ESG decoupling at the fund level, as well as their influence on fund manager behavior, remains underexplored. This study investigates the effects of ESGRD and ESG decoupling on fund performance, flow, and risk by using Chinese fund holdings and ESG ratings data. Our findings reveal that funds with higher levels of ESGRD and ESG decoupling exhibit lower returns, larger outflows, and higher risks. Moreover, the relationship between ESGRD/ESG decoupling and fund performance, flow, and risk varies across funds with differing cash asset ratios and portfolio concentrations. Additionally, we confirm that ESGRD and ESG decoupling attenuate the positive impact of a fund’s ESG performance. Furthermore, evidence suggests that fund managers incorporate ESGRD and ESG decoupling considerations into their asset allocation strategies. Notably, funds where fund managers invest in their own funds demonstrate lower levels of ESG decoupling compared to those where they do not. Finally, our results indicate that the negative correlation between fund managers’ self-investment behavior and both ESGRD and ESG decoupling is more pronounced in high-risk funds, reflecting a potential risk-mitigation strategy.

Introduction

With the growing emphasis on sustainable development across various sectors of society, a multitude of ESG rating indicators have been developed to quantify the sustainable performance of firms (Gu & Yoo, 2021; Hu et al., 2023). However, due to disparities in underlying data, rating systems, and methodologies, significant discrepancies exist in ESG ratings for the same firm (Berg et al., 2022; X. Wang & Liu, 2024). ESGRD refers to the significant inconsistency in ESG ratings given by different rating agencies for the same firm due to differences in rating methods, indicator weights, and coverage. These variations complicate the assessment of firms’ actual sustainable performance, thereby not only undermining the positive effects of enhanced sustainability but also presenting a substantial barrier to the robust development of ESG. Studies have demonstrated that ESGRD exerts a significant influence on firm stock performance (Christensen et al., 2022; Gibson Brandon et al., 2021; Luo et al., 2023; Serafeim & Yoon, 2023; Tan & Pan, 2023; J. Wang et al., 2024), firm financing (Guo et al., 2024), and firm innovation (T. Li et al., 2024), particularly at the firm level. Nevertheless, there is currently no documented evidence regarding the impact of ESGRD at the fund level.

ESG decoupling refers to the phenomenon where a firm emphasizes ESG publicity more than its actual fulfillment of ESG responsibilities when implementing the ESG concept, leading to a discrepancy between its ESG performance and ESG disclosure. This phenomenon represents a negative factor in the development of ESG, as it undermines its healthy progress and diminishes its positive contribution to achieving sustainable development goals. ESG decoupling predominantly manifests in corporate behavior; consequently, existing literature on ESG decoupling primarily focuses on its effects on firms and the factors influencing firm-level ESG decoupling (Aboud et al., 2024; X. Chen et al., 2024; Di & Li, 2023; Eliwa et al., 2023; Gull et al., 2023; J. Li & Wu, 2020; Tashman et al., 2019; Velte, 2023). ESG decoupling behavior in companies may potentially affect fund performance by influencing the corporate securities assets that are significant investment targets for funds.

The above-mentioned research indicates that although the studies on ESGRD and decoupling are increasing, the academic perspective shows a significant “microscopic tilt,” that is, a large number of literatures focus on the impact of this phenomenon on corporate-level results such as firm financing costs and firm value. This series of studies implicitly assumes that these negative consequences are mainly borne by the firms themselves but ignores the possibility that these risks may be transmitted through the equity investment chain to their owners—that is, the funds holding the stocks of these firms and their investors. However, as important institutional investors and resource allocation centers in the capital market, how do investment funds get affected by the ESG information conflicts in their holdings? How will fund managers respond? These questions are almost blank in the existing literature. This research-level gap limits our understanding of the transmission mechanism of ESG information conflicts throughout the investment chain. Based on this, this paper aims to systematically explore the following core issues:(1) How do ESGRD and ESG decoupling affect the performance, capital flow, and risk of funds? (2) Will fund managers adjust their asset allocation to actively manage such risks? (3) Will the self-interest connection of fund managers (such as self-purchase behavior) play a governance role in this process?

Di and Li (2023) contend that ESG decoupling exacerbates firms’ financing constraints and agency costs. Li et al. (2024) highlight that ESG decoupling enhances short-term stock returns while diminishing long-term returns, thereby influencing investors’ strategic decisions. Teti et al. (2024) demonstrate that decoupling announcements by firms in the European market elicit no significant market reactions and exhibit no substantial correlation with cumulative abnormal returns. Lin et al. (2023) identify a notable positive correlation between ESG decoupling and stock overpricing, suggesting a stronger association between ESG decoupling and stock mispricing. Liu et al. (2024) contend that increased information asymmetry associated with firm ESG decoupling intensifies the risk of stock price crashes. The extant literature provides robust evidence regarding the relationship between ESG decoupling and stock returns and risks, as well as investor behavior. Consequently, it can be inferred that fund managers may account for the implications of ESG decoupling on stock performance, risks, and investor behavior, integrating ESG decoupling into their investment strategies to mitigate potential adverse effects.

The investigation of ESG conflicts at the fund level is of particular urgency and importance, a point underscored by the unique structure of China’s fund market and its regulatory context. Unlike mature markets dominated by institutional investors, the Chinese fund market is characterized by a vast base of retail investors, who typically possess less sophisticated resources to decode complex ESG information conflicts within fund portfolios. This inherent information asymmetry makes them disproportionately vulnerable to the risks posed by ESGRD and ESG decoupling. Furthermore, the ESG regulatory framework in China is still evolving. The absence of standardized, stringent disclosure and evaluation rules at the fund level creates an environment where such conflicts can persist undetected. Therefore, our study directly addresses these critical market features by examining how ESG conflicts manifest and impact funds, thereby providing timely evidence to inform both investor protection and regulatory development.

The rapid, yet recently scrutinized, expansion of ESG-themed funds in China. This growth phase, now entering a period of market maturity and regulatory scrutiny, makes the investigation of underlying ESG quality (such as rating conflicts) both urgent and novel. First, China’s fund market is one of the world’s largest and is predominantly retail-driven. Retail investors typically lack the professional resources to conduct in-depth analysis of the complex ESGRD issues in fund holdings. Their decisions are more susceptible to media reports and short-term emotions, leading to overreactions to conflicting ESG information and causing sharp fluctuations in fund capital flows. Retail investors are more sensitive to net value fluctuations. Once the “greenwashing” risk implied by ESG decoupling is exposed, it is highly likely to trigger panic redemptions among retail investors. This herd effect can quickly transform into liquidity risks for funds and force fund managers to sell assets at unfavorable prices, thereby damaging fund returns.

Retail investors typically lack the professional resources to conduct in-depth analysis of the complex ESGRD issues in fund holdings. Their decisions are more susceptible to media reports and short-term emotions, leading to overreactions to conflicting ESG information and causing sharp fluctuations in fund capital flows. Retail investors are more sensitive to net value fluctuations. Once the “greenwashing” risk implied by ESG decoupling is exposed, it is highly likely to trigger panic redemptions among retail investors. This herd effect can quickly transform into liquidity risks for funds and force fund managers to sell assets at unfavorable prices, thereby damaging fund returns.

Second, China presents a distinctive and influential regulatory context. In emerging markets, regulatory policies are in a state of dynamic evolution. Retail investors may not fully or promptly interpret regulatory trends. When regulatory authorities start to focus on the authenticity of ESG, funds with high ESG ratings but decoupled performance will face more severe regulatory uncertainties. This part of the risk will be priced in by the market in advance, leading to an increase in their risk premiums. China, unlike more mature markets with established ESG frameworks, is actively developing its ESG regulatory system. This evolving, top-down policy environment creates a natural laboratory to examine how ESG conflicts manifest in a market where ESG norms are still being codified, offering insights that may extend to other emerging economies undergoing similar transitions.

We calculate the weight of each asset by dividing its value by the total value of all holdings in the fund. Subsequently, we multiply the ESGRD and ESG decoupling score of each asset by its corresponding weight and sum the products of each asset’s weight and its associated ESGRD and ESG decoupling to derive the ESGRD performance and ESG decoupling score for each fund, which serves as a proxy for fund-level ESGRD and ESG decoupling performance. This methodology enables us to translate firm-level ESGRD and ESG decoupling into fund-level ESGRD and ESG decoupling. From three perspectives, we investigate how ESGRD and ESG decoupling affect fund return, fund flow, and fund risk. We observe that funds with higher ESGRD and ESG decoupling exhibit lower returns, greater outflows, and higher risks. Furthermore, we undertake a comprehensive examination of the influence that fund ESGRD and ESG decoupling have on the correlation between fund performance and fund ESG performance. We observe that fund ESGRD and ESG decoupling weaken the negative impact of fund ESG rating on fund risk while strengthening the positive impact on fund return and fund flow.

From an interest-alignment perspective, we incorporate fund managers’ self-holding behavior as an explanatory variable. If fund managers demonstrate a significant preference for assets with low (or high) ESGRD and ESG decoupling, their self-holding behavior should exhibit a significant negative (or positive) correlation with the fund’s ESGRD and ESG decoupling performance. To operationalize this, we manually extract data on fund managers’ holdings of self-managed funds from annual reports and construct dummy variables indicating whether fund managers hold shares in their own funds, as well as the natural logarithm of the number of shares held, as explanatory variables. We observe a negative correlation between the self-holding behavior of fund managers and their ESGRD and ESG decoupling levels, suggesting that fund managers may decrease their investments in assets with higher ESGRD and ESG decoupling levels to mitigate risk.

Our research pertains to the extensively discussed ESGRD and ESG decoupling topic. While existing studies predominantly examine the impact of ESGRD and ESG decoupling on firms, the effects on funds remain largely unexplored. This paper expands the research perspective on ESG information conflicts from the firm level to the fund level, opening up a new analytical dimension and enriching the theory of institutional investor behavior. This paper develops an innovative measurement method for ESGRD and decoupling applicable to the fund level. By aggregating the ESG conflict data of the individual stocks held to construct fund-level indicators, this study provides a replicable measurement basis and methodological tool for subsequent empirical research on ESG information quality in the fields of asset portfolios, mutual funds, and other institutional investors. The research conclusions provide important empirical evidence and decision-making references for investors to identify fund risks, for fund firms to improve internal governance, and for regulatory authorities to prevent the risk of “greenwashing” in ESG investment.

This paper transcends the traditional framework that views ESG as static attributes, revealing the active management behavior of fund managers in response to ESG information conflicts. We find that the asset allocation decisions of fund managers are influenced by the level of ESG conflicts in their holdings, and their interest alignment (such as self-purchase behavior) significantly moderates this process. This provides new theoretical insights into the complex decision-making mechanisms of institutional investors in an information asymmetry environment, particularly applying the “interest alignment” hypothesis to the emerging scenario of ESG risk governance. This paper confirms that the decoupling of ESGRD from ESG weakens the positive impact of the overall ESG performance of the fund. This finding indicates that simply pursuing a high average ESG score for the investment portfolio may be insufficient, and the consistency and authenticity within the portfolio are equally important. This challenges the common practice of treating fund ESG performance as a homogeneous concept, calling for the academic and industry communities to adopt more refined measurement and evaluation frameworks.

Hypotheses Development

Different ESG ratings have different emphases and may assess firm ESG performance from different perspectives, which facilitates a more holistic comprehension of firm information for investors across various dimensions and thus reduces asset price fluctuations. When ESG ratings differ significantly, the results do not adequately reflect the firm’s actual ESG performance. This reduces the reference value of the ESG rating results, leaving investors to rely solely on their information to assess firm ESG performance. Investors’ limited information and cognitive abilities make it difficult for them to collect all information about the firm and identify invalid information, resulting in increased divergence among investors regarding the firm’s ESG performance, which in turn increases asset price volatility (Christensen et al., 2022).

In the context of the rapid development of ESG, firms can create a positive image of actively fulfilling their ESG responsibilities by publicizing their efforts in ESG to various sectors of society, which helps them gain support from stakeholders. The excessive promotion of ESG efforts by firms can lead to the emergence of ESG decoupling, with the aim of obtaining short-term returns. Therefore, ESG decoupling also reflects the shortsighted characteristics of firm managers (Di & Li, 2023). There is a significant gap between the actual ESG performance of firms with a large ESG decoupling and their advertised ESG performance, which can increase information asymmetry between investors and firms, leading to stock mispricing (Lin et al., 2023). The actual ESG performance of firms with large ESG decoupling is typically poor, and the significant cost of improving ESG performance often leads firms to conceal the negative information about their poor ESG performance through low-cost, exaggerated ESG performance publicity. The pseudo-ESG behavior of ESG decoupling increases the risk of stock price crashes (Liu et al., 2024). ESG decoupling’s effects on corporate stock prices directly influence the returns and risks of funds that hold these stocks.

The core issue with the decoupling between ESGRD and ESG lies in the lack of transparency. When rating agencies render divergent evaluations on the same asset, or when a firm’s external publicity does not match its actual actions, it conveys confusing and uncertain signals to the market. According to information economics theory, this uncertainty significantly increases the information processing costs for investors. To compensate for the higher analysis costs and the risk of inaccurate pricing, investors will demand higher expected returns, which directly manifests as an increase in the risk premium of the assets held by the fund and may lead to greater volatility in the fund’s net value. Therefore, ESG conflicts essentially create an “information risk,” directly translating into a higher fundamental risk for the fund. In particular, individual investors outnumber institutional investors in China’s securities market by a wide margin, which amplifies ESGRD’s influence on investor disparities. The divergence of ESG ratings reflects the uncertainty and high risk of a firm’s development prospects, and investors will demand higher risk premiums (Gibson Brandon et al., 2021).

For firms with high ESGRD or ESG decoupling, their external financing costs (including debt and equity financing costs) will increase significantly. This is because creditors and investors will view ESG information conflicts as signals of business operation risks and poor management and thus demand higher risk premiums. These rising financing costs will directly erode the firms’ profitability and future cash flows and eventually be reflected in their stock prices, dragging down the overall returns of funds heavily invested in such stocks. The intensification of financing constraints will increase the financial vulnerability of firms, reducing their ability to cope with market fluctuations. This will raise the risks (fundamental and financial risks) of individual stocks, which will then be transmitted through investment portfolios, leading to an increase in the overall risk level of the fund.

Behavioral finance indicates that individual investors are more prone to cognitive biases when dealing with complex and ambiguous information. The high ESGRD makes it difficult to accurately assess the true ESG quality of funds, which triggers investors’ aversion and uncertainty avoidance. Once there is slight negative news in the context of already ambiguous information, it is more likely to trigger a herd effect among retail investors, leading to large-scale and disorderly outflows of funds. This irrational capital flow triggered by information conflicts is the direct behavioral cause of the liquidity risk and performance decline faced by funds.

China’s ESG regulatory framework is still in its infancy, and this dynamic regulatory environment itself constitutes an important institutional backdrop. For funds, holding assets with high ESG conflicts means a greater risk of potential regulatory sanctions or reputational damage in the future. For instance, if regulatory authorities intensify penalties for “greenwashing” in the future, those funds with severe ESG misalignment will be the first to suffer. Therefore, the market will price in this future regulatory risk into the value of the funds in advance, leading to an increase in their risk and a decline in their attractiveness. Our findings are consistent with “institutional theory,” indicating that in a regulatory vacuum, the market will spontaneously form a punitive mechanism to deal with potential risks. We thus propose the competitive hypotheses below:

When confronted with varying ESG ratings, investors’ optimistic preferences lead them to trust in superior ESG evaluation performance. As a result, investors may overvalue firms relative to their actual worth, which subsequently leads to a decline in future asset returns (J. Wang et al., 2024). Avramov et al. (2022) argue that significant increases in ESG-related disclosure (ESGRD) raise market risks, change how investors assess firm ESG performance, and reduce their willingness to invest; consequently, the resulting decrease in trading volume may lead to lower returns. Christensen et al. (2022) suggest that firms with highly divergent ESG ratings face substantial uncertainty regarding sustainable development. This uncertainty obstructs external financing channels, prompting firms to rely more on internal financing, thereby increasing cumulative excess rates of return and return volatility. The returns and risks of firm assets directly influence the performance and risk of funds holding these assets. Fluctuations in fund performance and risk can, in turn, affect investor subscription and redemption behavior and impact fund flows. Moreover, the pseudo-ESG behavior associated with ESG decoupling amplifies investor sentiment (Liu et al., 2024). The effects of ESG decoupling on investor behavior may also cause fund managers to be concerned about potential impacts from investor redemption behavior. Consequently, fund managers overseeing their own managed funds may exhibit heightened concern regarding ESG decoupling. Based on this analysis, we propose the following hypothesis:

Research Design

Sample Construction

Our sample utilizes ESG ratings from six rating organizations: Huazheng Index, SynTao Green Finance, Runling Global, Wind, CASVI, and FTSE Russell to calculate the ESGRD of firms. To ensure both a sufficiently large sample size and the validity of ESG ratings, we retain samples for which at least two ESG ratings are available for the same firm in the same year. Following Christensen et al. (2022), we standardize each ESG rating based on all rating grades and then use the standard deviation of these standardized ESG ratings as a proxy for ESGRD. Chinese funds disclose in their annual reports the range of shares held by fund managers in their managed funds. Consequently, we manually extract data on the shares held by fund managers in their managed funds from the annual reports. A limitation of this study lies in its data collection method for fund managers’ self-investment. Despite our meticulous care, the manual collection process inherently carries a risk of reporting errors or omissions. We have rigorously cross-verified the data to ensure its reliability. We obtain fund holdings, balance sheets, financial statements, ESG ratings, and other relevant data from the CSMAR and Wind databases. We select equity funds and equity-biased funds as our research samples, with a sample period spanning from 2015 to 2023. All variables are winsorized at the 1% and 99% levels to mitigate the influence of outliers.

Model and Variables

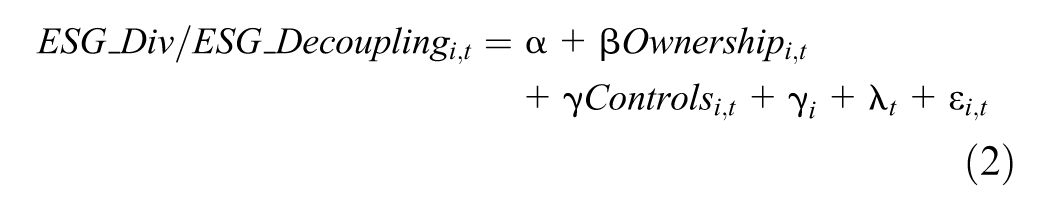

The model below is employed to verify the impact of ESGRD’ influence on fund performance, flow, and risk:

where

where

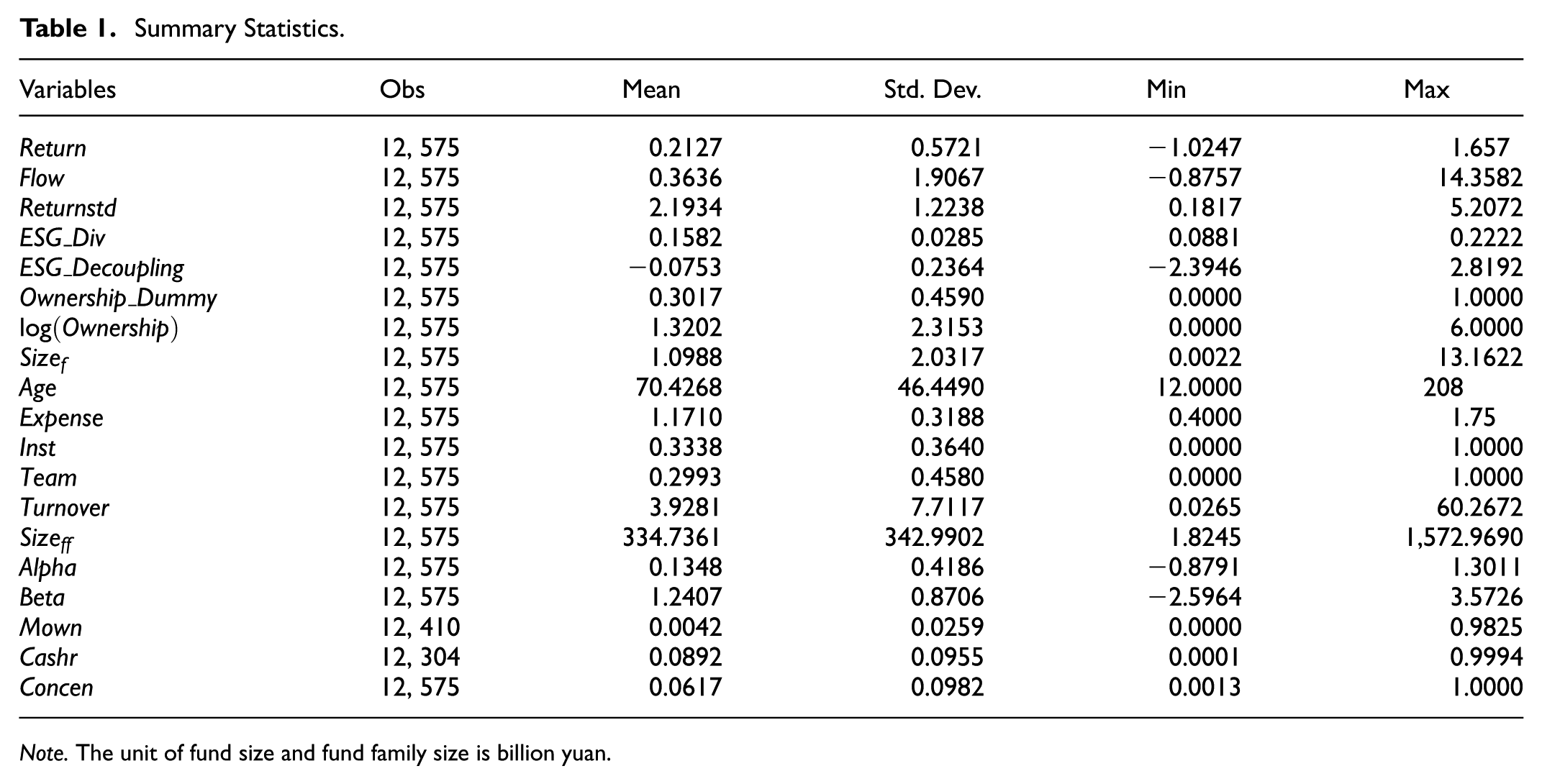

Descriptive Statistics

The average ESGRD of the sample funds in Table 1 is 0.1582, with a minimum value of 0.0881 and a maximum value of 0.2222. This reflects the relatively low level of ESGRD in the funds’ investment portfolios, which may result from the funds’ selective avoidance of assets with high ESGRD. The average institutional shareholding ratio of the sample funds is 0.3338, indicating a relatively low proportion of institutional investors. The mean value of

Summary Statistics.

Note. The unit of fund size and fund family size is billion yuan.

ESGRD and ESG Decoupling and Fund Performance

Baseline Results

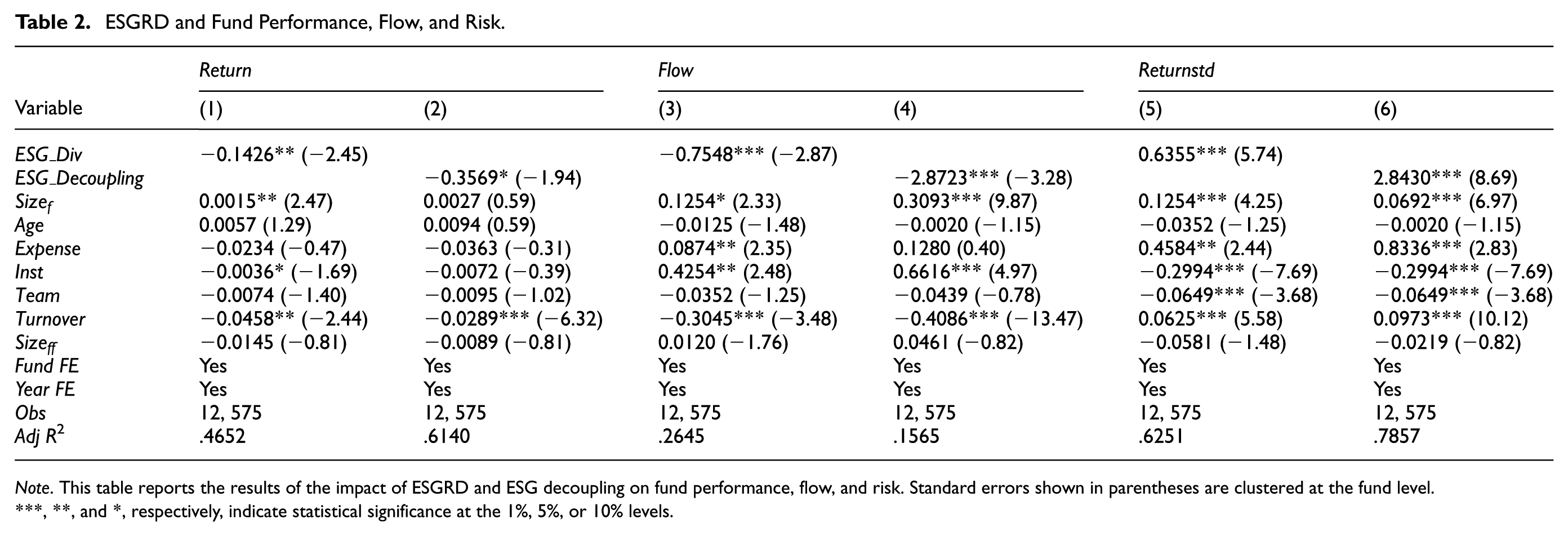

In Table 2, we present the regression results between fund ESGRD and ESG decoupling, as well as fund return, flows, and risk. Columns (1), (3), and (5) only show the explanatory variable of fund ESGRD, while columns (2), (4), and (6) show the explanatory variable of fund ESG decoupling. The coefficients of

ESGRD and Fund Performance, Flow, and Risk.

Note. This table reports the results of the impact of ESGRD and ESG decoupling on fund performance, flow, and risk. Standard errors shown in parentheses are clustered at the fund level.

, **, and *, respectively, indicate statistical significance at the 1%, 5%, or 10% levels.

Prior studies have primarily documented the adverse effects of ESGRD at the firm level, such as reduced stock returns, increased stock risk, and higher financing costs (Christensen et al., 2022; Gibson Brandon et al., 2022; Guo et al., 2024; Li et al., 2024; Luo et al., 2023; Serafeim & Yoon, 2023; Tan & Pan, 2023; J. Wang et al., 2024). The economic consequences of ESGRD and ESG decoupling at the fund level, as provided in this study, contribute to a deeper understanding of its broader impact on financial markets. Our results are also consistent with the observation that the ESGRD and ESG decoupling levels of funds in Table 1 are relatively low. The negative influence of ESGRD and ESG decoupling on fund performance and flows draws the attention of fund managers, prompting them to select assets with lower ESGRD and ESG decoupling levels when adjusting their investment portfolios, thereby mitigating the adverse effects on fund performance and flows.

Robustness Checks

Endogeneity Tests

Despite accounting for several variables in the benchmark regression, endogeneity issues may still arise due to the omission of certain factors influencing fund performance, flow, and risk. To address potential endogeneity concerns, we employ the two-stage least squares (2SLS) method. Industry characteristics contribute to a certain degree of similarity in the ESG performance of firms within the same industry, which may lead to higher similarity in ESGRD and ESG decoupling among these firms. Therefore, we calculate the fund’s ESGRD and ESG decoupling scores by substituting the firm-level ESG divergence with the arithmetic mean of the ESGRD and ESG decoupling of other firms within the same industry. These industry-level averages (

In the first stage, the coefficient of

2SLS.

Note. This table reports the results of the endogeneity test using the 2SLS method. Standard errors shown in parentheses are clustered at the fund level.

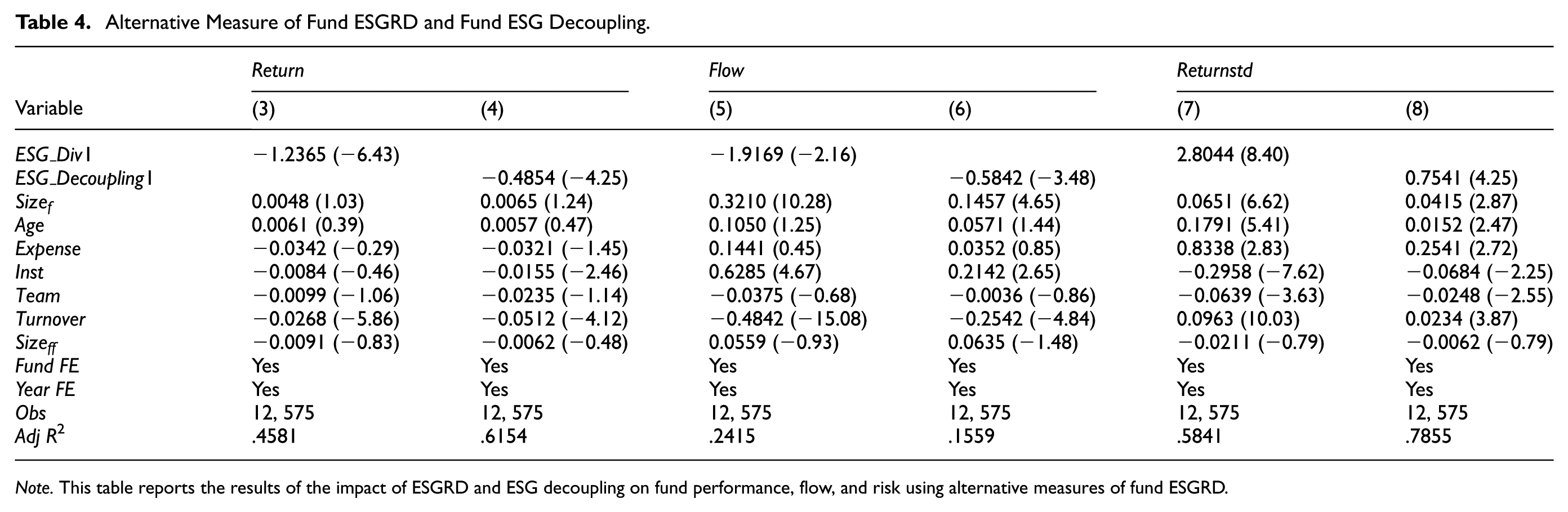

Alternative Measure of Fund ESGRD and ESG Decoupling

We calculate the ESGRD score of each fund by multiplying the ESGRD of each asset by its corresponding weight in Equation 1. To proxy the fund’s ESGRD, we use the arithmetic mean of the ESGRD of all assets, replace the explanatory variable, and re-estimate Equation 1 in the benchmark regression. Differences across various rating systems may lead to discrepancies in ESG ratings assigned by different ESG rating agencies for the same firm, introducing measurement biases in both corporate ESG decoupling and fund ESG decoupling. To address this, we substitute the Huazheng ESG rating indicators with those released by WIND in the benchmark regression to recalculate the fund’s ESG decoupling level. Our findings indicate that the coefficients of

Alternative Measure of Fund ESGRD and Fund ESG Decoupling.

Note. This table reports the results of the impact of ESGRD and ESG decoupling on fund performance, flow, and risk using alternative measures of fund ESGRD.

Propensity Score Matching

The limitation of ESGRD and ESG decoupling data in firms results in the exclusion of assets with ESGRD and ESG decoupling data, where the value held by many funds accounts for less than 67%, from our sample. This leads to the non-random selection of our fund sample. To address this issue, we employ the propensity score matching (PSM) method to mitigate the non-randomness of the fund samples. Specifically, we assign funds to the treatment group if their ESGRD and ESG decoupling scores exceed the sample median. Using the Caliper nearest neighbor method, we construct a control group by matching funds based on covariates derived from the control variables in the benchmark regression, thereby generating a new sample. We then re-estimate Equation 1 using this new sample. The coefficients presented in Table 5 further validate the robustness of our findings, indicating that the fund’s ESGRD and ESG decoupling are negatively correlated with its return and flow but positively correlated with its return volatility.

PSM-DID.

Note. This table reports the results of the impact of ESGRD and ESG decoupling on fund performance, flow, and risk using the PSM sample.

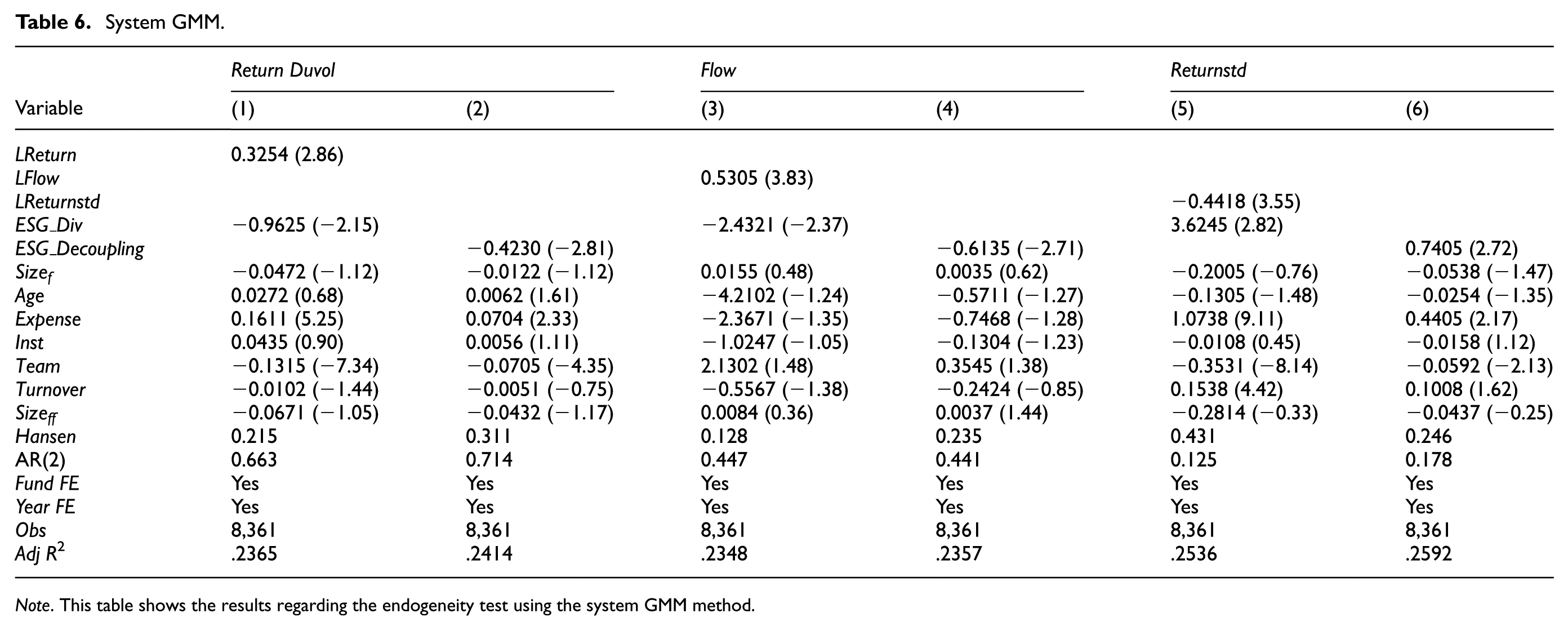

System GMM

To more effectively address endogeneity issues, we further employed the system GMM for dynamic panel data. This method can simultaneously control for unobservable individual effects and endogeneity caused by the mutual causality between explanatory variables and the dependent variable. Specifically, we introduced the lagged terms of the dependent variables (fund returns, fund flows, and risks) as explanatory variables in the model to capture their dynamic characteristics. These instrumental variables meet the relevance requirement (the current ESGRD and ESG decoupling are correlated with their historical values), and under the assumption that the error term sequence is uncorrelated, these lagged values are uncorrelated with the current disturbance term, thus satisfying the exogeneity requirement. The estimation results in Table 6 of the system GMM are consistent with our benchmark conclusions, indicating that after considering dynamic effects and potential endogeneity, the negative impact of ESGRD and ESG decoupling on fund performance remains robust.

System GMM.

Note. This table shows the results regarding the endogeneity test using the system GMM method.

Heterogeneity Tests

Cash Assets

In general, funds maintain a certain percentage of cash assets to meet investor redemptions. Differences in investment strategies across funds lead to significant variations in the proportion of cash assets held by different funds. A high proportion of cash assets may crowd out investment in other assets, potentially affecting the fund’s return (Simutin, 2014). Conversely, if a fund holds a relatively small proportion of cash assets, it may struggle to cope with significant investor redemptions during external risk shocks that cause substantial return fluctuations (Kamstra et al., 2017; Morris et al., 2017). In such cases, fund managers often respond to redemptions by selling assets, which can depress asset prices and increase return volatility. Therefore, holding a higher proportion of cash assets may help mitigate the impact of ESGRD and ESG decoupling on fund flows and return volatility. To examine whether differences exist in the influence of ESGRD and ESG decoupling on fund performance across funds with varying cash asset ratios, we estimate the following model:

where

The Heterogeneity of Cash Assets.

Note. This table reports the results of the heterogeneity of cash assets.

Portfolio Concentration

Previous literature indicates that funds with highly concentrated portfolios tend to achieve superior performance because fund managers possess more profound knowledge of the assets they invest in, and a smaller number of asset types can generate better returns for the fund (X. Chen & Lai, 2015; Fulkerson & Riley, 2019; Qin & Wang, 2021). However, a higher concentration of investment portfolios may expose funds to greater idiosyncratic risks, leading to increased return volatility. Fund managers who favor concentrated investment strategies often prioritize stocks with higher growth potential, which may help mitigate the negative impact of ESGRD and ESG decoupling on fund returns. Nevertheless, when facing external risk shocks, the characteristic risks of high-investment assets in centralized investment strategy funds may exacerbate the influence of ESGRD and ESG decoupling on fund return volatility and trigger concentrated investor redemptions. Consequently, the effects of ESGRD and ESG decoupling on fund performance, flow, and risk may differ among funds with varying portfolio concentrations. We examine the moderating role of fund portfolio concentration in the relationship between fund ESGRD and ESG decoupling and its performance by estimating the following model:

where

The Heterogeneity of Portfolio Concentration.

Note. This table reports the results of the heterogeneity of portfolio concentration.

Our findings give us fresh perspectives on how fund portfolio concentration influences its performance.

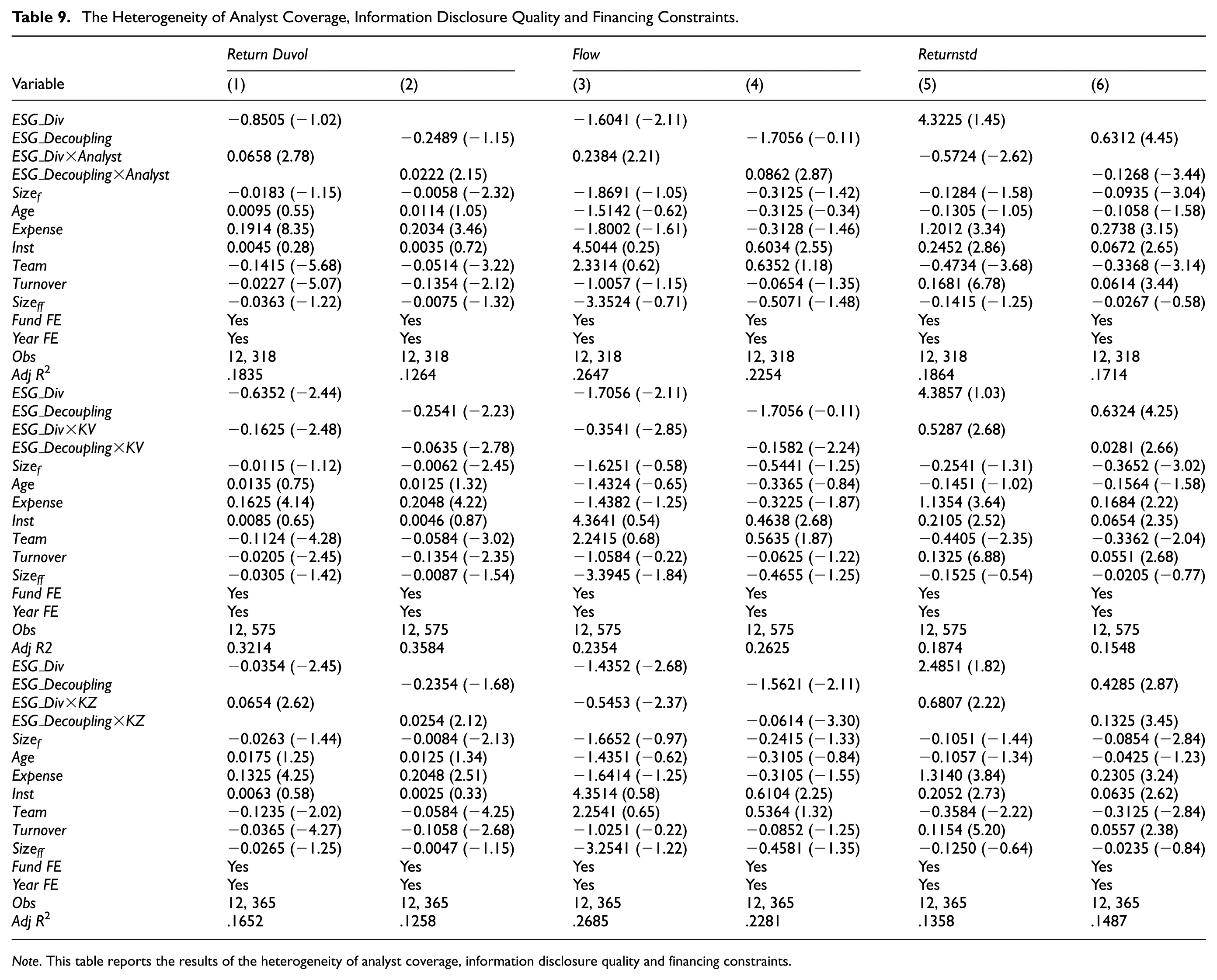

Analyst Coverage, Information Disclosure Quality and Financing Constraints

To deeply reveal the boundary conditions under which ESG conflicts affect funds, this study starts from two core theoretical perspectives of information asymmetry and agency problems and introduces three dimensions of analyst coverage, information disclosure quality, and financing constraints for heterogeneity tests. We anticipate that a worse information environment and more severe agency problems will significantly magnify the negative impact of ESG conflicts.

where

The Heterogeneity of Analyst Coverage, Information Disclosure Quality and Financing Constraints.

Note. This table reports the results of the heterogeneity of analyst coverage, information disclosure quality and financing constraints.

Further Discussions

A large amount of evidence indicates that a fund’s sustainable investment strategy can affect fund return, flow, and risk. Pástor and Vorsatz (2020) show that funds that have higher ESG ratings also exhibit superior performance. Hartzmark and Sussman (2019) conclude that funds that have higher ESG ratings can receive inflows, while funds with the lowest ESG ratings face outflows. H. Wang (2024) indicates that funds with higher ESG performance are less vulnerable. Firms with the same ESG performance may have different ESGRD performance and ESG decoupling, so it is natural to examine the role that ESGRD plays in ESG performance’s effect on fund performance, flow, and risk. Based on this, by investigating the influence of ESG performance on the link between ESG performance and fund performance, flow, and risk, we expand our comprehension of the economic impact of ESG development. We employ the following models to evaluate ESGRD and ESG decoupling’s influence on the connection between ESG performance and fund performance, flow, and risk:

where

Fund ESGRD and ESG Decoupling’s Influence on the Link Between Fund ESG and Fund Performance, Flow, and Risk.

Note. This table reports the results of the effect of fund ESGRD and ESG decoupling on the relationship between fund ESG and fund performance, flow, and risk.

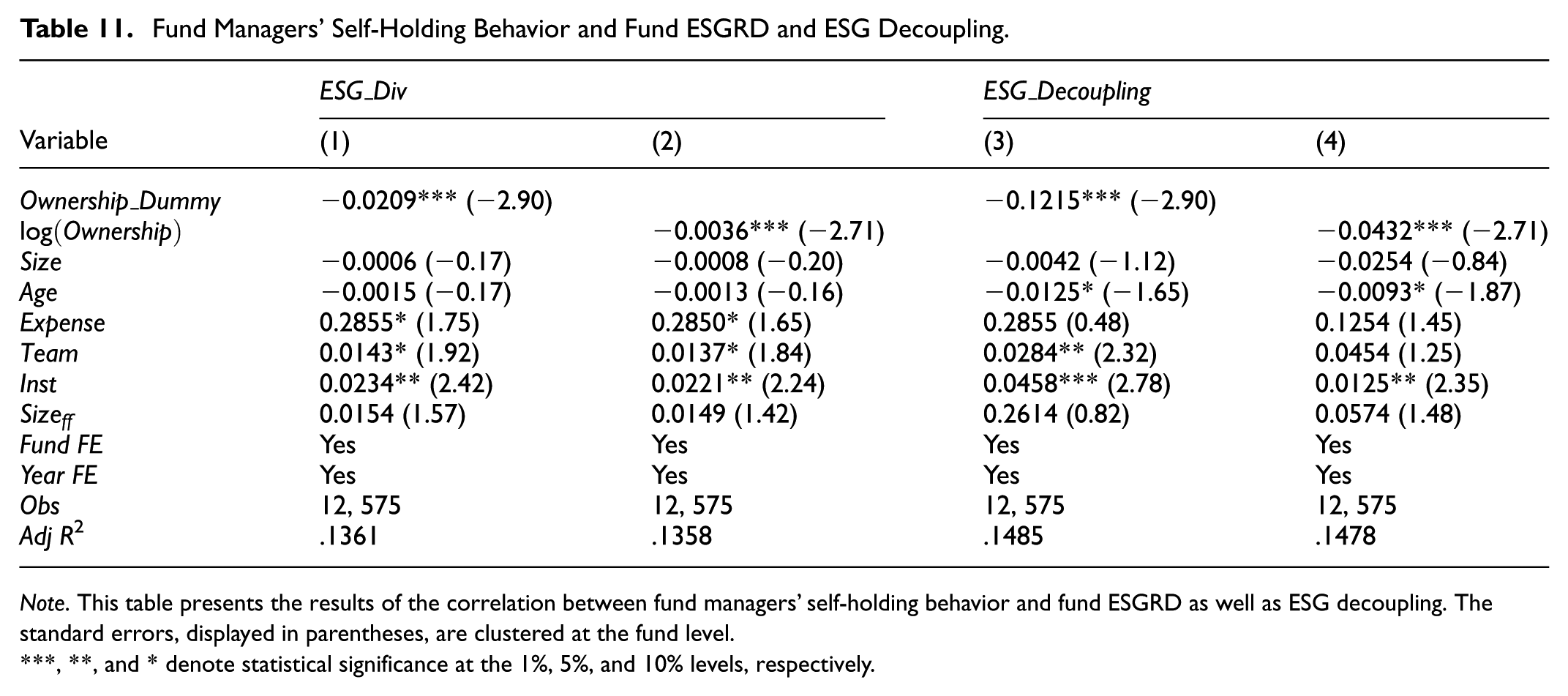

Fund Managers’ Self-Holding Behavior and Fund ESGRD and ESG Decoupling

Baseline Results

In Table 11, the coefficients of

Fund Managers’ Self-Holding Behavior and Fund ESGRD and ESG Decoupling.

Note. This table presents the results of the correlation between fund managers’ self-holding behavior and fund ESGRD as well as ESG decoupling. The standard errors, displayed in parentheses, are clustered at the fund level.

, **, and * denote statistical significance at the 1%, 5%, and 10% levels, respectively.

Robustness Checks

Endogeneity Tests: Lagging One Period

Fund managers who hold shares in the funds they manage may be incentivized to reduce their investment in assets with high levels of ESGRD and ESG decoupling. Conversely, a reduction in the ESGRD and ESG decoupling levels of funds might encourage fund managers to increase their holdings in the funds they manage. To address the potential mutual causality issue mentioned above, we lag the explanatory and control variables by one period. The coefficients of

Endogeneity Tests: Lagging One Period.

Note. This table shows the results of the endogeneity tests by lagging one period of the explanatory variables and control variables.

Endogeneity Tests: 2SLS

We further employ the two-stage least squares (2SLS) method to address potential endogeneity concerns, such as omitted variables that may influence fund managers’ self-holding behavior and fund ESG decoupling. We select the fund’s excess return (

Endogeneity Tests: 2SLS.

Note. This table shows the results of the endogeneity tests using the 2SLS approach.

Propensity Score Matching

The screening of fund samples led to the exclusion of many funds from our analysis, which may raise concerns about the representativeness and validity of the sample. To address this issue, we define the funds where fund managers hold shares in the funds they manage as the treatment group and use caliper nearest neighbor matching to select a control group from the funds where fund managers do not hold shares in the funds they manage. The coefficients of and in Table 14 are consistent with those reported in Section 5.1.

Propensity Score Matching.

Note. This table shows the results of the correlation between fund managers’ self-holding behavior and fund ESGRD and ESG decoupling using the PSM sample.

Heterogeneity Tests

By over-promoting their ESG performance, firms attract more investors and enhance investor optimism, leading to increased investor attention and higher stock returns (M. Chen, 2024; L. Li et al., 2024; Lin et al., 2023). ESG decoupling represents a pseudo-ESG behavior that reduces information transparency by concealing true ESG performance. The disclosure of a firm’s ESG decoupling behavior significantly amplifies investors’ negative emotions, thereby increasing stock risks (Liu et al., 2024). Fund managers who invest in the funds they manage have a direct stake in the fund’s performance, prompting them to pay closer attention to both returns and risks. As a result, they tend to exhibit more cautious risk-taking behaviors when managing funds in which they hold shares (Ma & Tang, 2019). The influence of ESGRD and ESG decoupling on stock returns and risks may encourage fund managers to leverage these characteristics to adjust asset portfolios. Based on this, we posit that the correlation between fund managers’ self-holding behavior and fund ESGRD and ESG decoupling is stronger in funds with poor returns, higher outflows, and greater risks. To test this hypothesis, we estimate the following model:

where

Heterogeneity Tests of Fund Return, Flow, and Risk.

Note. This table shows the results of the heterogeneity tests of fund return, flow, and risk.

Conclusion

ESGRD emerged during the development of ESG and has gradually garnered widespread attention. ESGRD primarily depends on firms, and its impact on firms and stocks constitutes the focus of existing research. Firm-level ESGRD indirectly affects funds through the ownership of corporate securities assets; however, there is currently no documented evidence of its direct effects at the firm level. Based on this, we investigate the influence of ESGRD on fund performance, flow, and risk using Chinese fund holdings and firm ESG rating data. Our findings reveal a negative correlation between fund ESGRD and both its return and flow, as well as a positive correlation with its risk. We further observe that the influence of fund ESGRD on performance varies across funds with differing levels of management ownership, cash asset ratios, and portfolio concentration. Additionally, we examine how ESGRD affects the correlation between fund ESG performance and overall fund performance. Our results indicate that ESGRD diminishes the positive effects of fund ESG performance on return volatility and flow while also reducing its negative impact on return volatility.

ESG decoupling, as a form of pseudo-ESG behavior, can significantly undermine the positive impact of ESG initiatives. This study is among the first to investigate the effects of ESG decoupling on fund manager behavior at the fund level. Specifically, we analyze the correlation between fund managers’ self-holding behavior and fund-level ESG decoupling by leveraging data on Chinese fund managers’ holdings of self-managed fund shares and corporate ESG-related metrics. Our findings indicate a negative correlation between fund managers’ self-holding behavior and fund ESG decoupling. We also demonstrate that fund risk intensifies this negative correlation. These results suggest that fund managers take into account the ESG decoupling levels of assets during the asset allocation process and may exhibit heightened concern regarding the high-risk characteristics associated with ESG decoupling.

This study confirms the negative impact of ESGRD and decoupling on fund performance. These findings can be reasonably explained by information asymmetry and signaling theory. Firstly, ESG conflicts are essentially manifestations of information opacity, which significantly increase investors’ information processing costs and valuation uncertainties. To compensate for this additional risk, the market demands higher investment returns, thereby exerting downward pressure on fund net asset values. Secondly, high ESG conflicts may trigger concerns among investors, especially risk-averse ones, leading to large-scale capital outflows and further intensifying the liquidity risk of funds. Finally, the negative correlation between fund managers’ self-investment behavior and ESG conflicts indicates that the synergy of interests can, to a certain extent, alleviate agency problems and motivate fund managers to manage ESG risks at the portfolio level more prudently. These findings highlight the necessity of incorporating ESG information conflicts into the risk assessment and management framework of funds.

Our results provide empirical support for the ongoing development of China’s ESG policy ecosystem. Specifically, the negative market penalties associated with high ESGRD and ESG decoupling justify the introduction of more granular disclosure requirements at the fund level. Mirroring the spirit of the European Union’s Sustainable Finance Disclosure Regulation (SFDR), which mandates disclosures on principal adverse impacts (PAIs) and promotes transparency, Chinese regulators could consider requiring funds to report not just an aggregate ESG score but also metrics reflecting the internal consistency and potential controversies within their portfolios.

The implications of the Chinese context have significant external validity. Many emerging markets share key characteristics with China: (1) capital markets dominated by retail investors; (2) nascent ESG regulatory frameworks; (3) uneven quality of ESG information disclosure by firms. Therefore, the core conclusion of this study—that ESG information conflicts (disagreements and decouplings) are a major source of risk for fund stability, and this risk is amplified in environments with severe information asymmetry—is likely to hold true in other emerging markets as well. The main limitation of this study lies in the fact that the sample only covers the Chinese market. While this choice enables an in-depth analysis of the influence mechanism under a specific institutional background, it also restricts the direct generalizability of the research conclusions. Our findings suggest that in developed markets dominated by institutional investors and with highly mature ESG regulations (such as Europe and the United States), the influence mechanism and intensity of ESG conflicts may differ. Future research could replicate the study in other emerging markets to verify the generalizability of the conclusions.

Footnotes

Ethical Considerations

This article does not contain any studies with human or animal participants.

Consent to Participate

There are no human participants in this article and informed consent is not required.

Author Contributions

Lei Ding: Conceptualization; Data curation; Formal analysis; Validation; Methodology; Software; Writing; Xin Liu: Revise; Writing; Hu Wang: Methodology; Funding acquisition; Revise; Writing.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research is supported by Natural Science Foundation of Jiangsu Province (BK20240891).

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

Data will be available on request from the corresponding authors.