Abstract

We explore the role of ESG rating divergence (ESGRD) in the sustainable development of firms from the perspective of organizational resilience. Using Chinese ESG ratings and listed firm data, we examine the impact of ESGRD on firm resilience and find that it significantly reduces firm resilience. We further examine the mechanisms by which ESGRD affects firm resilience through information and financing channels. The findings demonstrate the positive role of the information channel and the negative role of the financing channel through which ESGRD affects firm resilience. The positive impact of ESGRD on firm resilience by reducing analyst forecast divergence is lower than the negative impact on firm resilience by increasing financing constraints. In addition, the negative correlation between ESGRD and corporate resilience is more pronounced in firms with lower information transparency, lower analyst attention, and higher ESG decoupling. Our research provides new evidence for ESGRD’s economic consequences at the firm level.

Introduction

ESGRD arises as a result of variances in the ESG ratings of the same firm, given by different rating organizations (Berg et al., 2022; Christensen et al., 2022). The impact of ESGRD has become increasingly prominent with the development of ESG and has become a key factor hindering its healthy development (Wan et al., 2024; Z. Wu et al., 2023). For instance, significant ESGRD may lead to public doubts about a firm’s fulfillment of its social responsibility, damaging its reputation and brand image. Such divergence may also increase investors’ pessimism about the firm’s development prospects, reducing their investment willingness and thereby affecting the firm’s market value and financing. Additionally, firms with significant ESGRD may face stricter regulation and incur additional compliance costs.

In physics, resilience refers to a material’s capacity to absorb energy when it undergoes plastic deformation and fracture. The greater the resilience, the lower the likelihood of a brittle fracture. For firms, resilience indicates their ability to cope with risk shocks. Firms with strong resilience can effectively mitigate external risk shocks and minimize their impact on themselves (Conz & Magnani, 2020; Croci et al., 2024). Firm resilience is also a critical indicator of its ability to develop sustainably, which makes it highly consistent with the sustainable development emphasized by ESG. Exploring the association between ESGRD and firm resilience can help firms more clearly recognize the importance of ESG ratings in risk management, prompting them to take relevant measures to reduce ESGRD and thereby enhance their sustainable development capabilities. Clarifying the impact mechanism of ESGRD on firm resilience can help regulators more effectively reduce the negative impact of ESGRD and leverage the positive role of ESG ratings in promoting sustainable development. However, the association between ESGRD and firm sustainability has not been explored, which makes it significant to assess the impact of ESGRD on firm resilience and its influencing mechanism. We aim to investigate the effect and mechanism of ESGRD on firm sustainability from the perspective of firm resilience in order to supplement the literature on ESGRD and firm sustainability in theory and provide guidance for firms and regulators to better utilize and leverage the positive role of ESG ratings in practice.

Regarding the economic consequences of ESGRD. Gibson Brandon et al. (2021) find that stock returns are positively correlated with ESGRD, indicating that firms with higher ESGRD have a risk premium. Tan and Pan (2023) and Christensen et al. (2022) find that greater ESGRD is associated with higher stock return volatility and stock price volatility. Luo et al. (2023) point out that ESGRD weakens the positive impact of ESG ratings on the stock price crash risk of firms. H. Wang et al. (2024) indicate that ESGRD has a negative impact on stock returns. Liu et al. (2024) show that ESGRD increases the volatility of stock idiosyncratic returns. Both J. Zhou et al. (2024) and Hou and Xie (2024) point out that ESGRD can promote corporate green innovation and green innovation patent applications. However, L. Li et al. (2024) and Geng et al. (2024) find that ESGRD would inhibit corporate green innovation and foster green innovation bubbles. Ling et al. (2024) indicate that ESGRD increases corporate audit fees. H. Zhou and Ma (2025) discover that the increase in corporate ESGRD is associated with the rise in the cost of equity capital. Liu et al. (2024) observe a correlation between analyst forecast errors and ESGRD. M. Li and Chen (2025) claim that ESGRD significantly improves the quality of analyst forecasts. G. Li and Cheng (2024) find that the increase in ESGRD leads to the improvement in earnings management levels.

The above literature records the mixed impact of ESGRD on firms, such as reducing stock returns, increasing stock risks and financing costs, increasing analyst forecast errors, and the quality of analyst forecasts, etc. The impact of ESGRD on analysts’ behavior and firms’ financing capabilities would further affect their ability to cope with risk shocks and thus affect their resilience. ESGRD, as important non-financial information for firms, would attract the attention of analysts and serve as a reference for their forecast results. This may prompt analysts to collect more ESG-related information on firms, which helps them have a more comprehensive understanding of the firms’ operations, thereby reducing the forecast divergence among analysts and causing a decline in stock price volatility. ESGRD may also increase the one-sidedness of analysts’ understanding of firms, thereby increasing the divergence of analysts’ forecasts and triggering an upward fluctuation in stock prices. Therefore, ESGRD may affect firm resilience by influencing analysts’ behavior. Moreover, a larger ESGRD reflects that firms may face greater uncertainty in their operation and development, increasing information asymmetry between firms and external stakeholders. This may reduce the willingness of banks and other financial institutions to grant credit, leading to higher financing difficulties for firms and further affecting their resilience. The above inference inspires us to explore the impact of ESGRD on firm resilience and how ESGRD affects firm resilience through analysts’ behavior and financing constraints.

Using the ESG rating data from Chinese listed firms, we explore the association between ESGRD and firm resilience. Our empirical results indicate a negative association between ESGRD and firm resilience, which is consistent with our hypothesis and further confirms that the adverse influence of ESGRD on corporate in existing research weakens their ability to withstand risk shocks, thereby reducing their resilience. We further explore how ESGRD affects firm resilience from the perspectives of information and financing channels. The results show that ESGRD decreases analyst forecast divergence and increases corporate financing constraints. The positive impact of ESGRD on firm resilience by reducing analyst forecast divergence is lower than the negative impact on firm resilience by increasing financing constraints. ESGRD has an overall negative impact on firms’ resilience. Our heterogeneity analysis results indicate that the relationship between ESGRD and firm resilience is more significant in firms with lower information transparency, lower analyst attention, and greater ESG decoupling.

Our study adds to the existing research on ESG. The resilience of firms is related to their sustainable development, and ESG also emphasizes the concept of sustainable development (Yin et al., 2023). Whether ESGRD, as a disharmonious factor in ESG development, affects firm resilience and contradict the concept of sustainable development emphasized by ESG remains to be verified. We provide new evidence from the perspective of firm resilience that ESGRD weakens the role of ESG in promoting sustainable development. Unlike the existing literature where ESGRD is mainly characterized by negative economic consequences (Christensen et al., 2022; Gibson Brandon et al., 2021; Tan & Pan, 2023; H. Zhou & Ma, 2025). We find the two-side impacts of ESGRD on firm resilience, with ESGRD having a positive impact on firm resilience through the information channel and a negative impact on firm resilience through the financing channel. We provide evidence of the positive economic consequences of ESGRD at the firm level, thereby supplementing the literature on ESGRD.

Our study also relates to firm resilience. Previous research concentrates on the impact of strategic deviation (Kong et al., 2021), the business environment (Fu et al., 2023), and digital transformation (D. Wang & Chen, 2022) on firm resilience, but there is no research on firm resilience from an ESG perspective. Our research is the first to show how ESGRD affects firm resilience. We find a negative correlation between ESGRD and firm resilience. We extend the study of firm resilience to the level of social responsibility, and reveal the important impact of non-financial information asymmetry on corporate resilience. Our research enriches the research on the influencing factors of firm resilience, helps firms to understand and deal with internal and external risks more comprehensively, and provides a theoretical basis for firms to improve their resilience by actively fulfilling social responsibility and improving the transparency of social responsibility information.

Hypotheses Development

The signaling theory suggests that in an environment of information asymmetry, information transmission helps market participants exchange information and influences their behaviors and decisions (Connelly et al., 2011). The theory of information asymmetry states that the information held by the parties in a transaction is unequal. A higher ESG rating usually indicates a better performance of firms in environmental, social, and governance aspects and conveys to the market the information that it actively fulfills its ESG responsibilities, which helps enhance its reputation and social image (Fama, 2021; H. Wang, 2024). Significant differences in ESG ratings would draw the attention and doubts of stakeholders on its fulfillment of ESG responsibilities, especially negative media reports, leading to damage to firms’ reputation and image (J. Zhou et al., 2024). Such damage may trigger a series of negative consequences, such as the decline in sales revenue, the decrease in market share, and the fall in stock prices, thereby reducing its ability to cope with risk shocks.

Significant differences in ESG ratings reflect the uncertainty and higher risks in firms’ development prospects, which can affect the trust and support of stakeholders in the firms (H. Wang et al., 2024; J. Zhou et al., 2024). Financial institutions are less willing to extend credit to such firms and demand higher interest rates to compensate for the risks, thereby increasing the firms’ financing costs and difficulties. Firms with limited financing capabilities usually find it challenging to quickly adjust their development strategies to cope with market changes and maintain market competitiveness (Nikolov et al., 2021). Liquidity shortages can also reduce their debt repayment capacity and profit margins, leading to greater losses when they are impacted by risks. Significant differences in ESG ratings may also increase the probability of firms being subject to regulatory attention and scrutiny by regulatory authorities, as well as the impact of policy adjustments (Hou & Xie, 2024; H. Zhou & Ma, 2025). Such regulatory risks and policy uncertainties prompt firms to invest more manpower, material, and financial resources to improve their ESG performance and increase ESG disclosures to comply with regulations, which increases their operating costs and restricts their strategic flexibility, thereby reducing their resilience. The above theoretical analysis leads to the following hypothesis:

The difference in ESG rating systems among different rating agencies is one of the important factors leading to firm ESGRD, which may also reflect information from different aspects of firms (Berg et al., 2022; Christensen et al., 2022). With a significant increase in social attention to ESG, firms’ ESG performance has become an important reference for analysts to forecast their stocks (Christensen et al., 2022; Schiemann & Tietmeyer, 2022). For analysts, when there is significant disagreement in the ESG performance of firms, they may not consider each ESG rating result but instead choose a certain one result based on their own preferences as a reference to forecast firms’ stock prices. ESG reflects the uncertainty of firm information, which can interfere with analysts’ judgment of the true situation of firms, thereby reducing the accuracy of their forecast. Therefore, a larger ESG rating for a firm may lead to an increase in analyst forecast divergence (Schiemann & Tietmeyer, 2022).

When analysts discriminate ESGRD into complementary information, ESGRD provides ESG-related information about different aspects of firms, which helps analysts to have a more comprehensive understanding of the firm’s operating situation, especially the specific information of firms, thereby reducing analysts’ judgment errors caused by a single source of ESG information and reducing analysts’ forecast divergence. Investors typically rely on the forecast results of analysts to formulate their investment strategies, particularly in the Chinese stock market, where individual investors dominate. The forecast results of analysts can have a significant impact on stock prices (Chan & Hameed, 2006; Kim et al., 2019; Kothari et al., 2016) and further affect firm resilience. The above theoretical analysis leads to the following hypothesis:

The stakeholder theory posits that a firm’s objective should not be merely to create value for shareholders, but also to balance and meet the expectations and interests of all stakeholders. Establishing good relationships with stakeholders is crucial for long-term success. Corporate resilience is highly dependent on stakeholders (such as the support of suppliers during crises, the loyalty of employees, and the inclusiveness of the community). ESGRD confuse stakeholders, erode their trust and commitment to the company, thereby undermining the “relationship capital” and external support networks that the firm relies on for survival, making it more vulnerable in the face of shocks.

The disagreement in ESG ratings suggests that there may be significant uncertainty in the sustainable development of firms, which could weaken investors’ willingness to invest. This uncertainty could lead investors to demand higher risk premiums, potentially increasing the financing constraints and costs of firms (L. Li et al., 2024). Corporate financial constraints and rising financing costs inevitably restrict investment and reproduction, resulting in higher debt costs. Higher debt costs also decrease their current assets, reducing their ability to cope with risk shocks, which is not conducive to maintaining stable performance growth (Carvalho, 2018; Musso & Schiavo, 2008; Santos et al., 2024). As a result, the increased financing constraints and costs for firms would inevitably affect their normal business activities, which are not conducive to sustainable development, and thus reduce their resilience. The above theoretical analysis leads to the following hypothesis:

Research Design

Sample Construction

Our sample comprises A-share listed firms in China. The initial sample period spans from 2015 to 2023. Since the earliest ESG ratings in China were published in 2015, the starting point of our sample is set as 2015. We exclude observations from the financial industry, as well as those classified as ST or *ST, and eliminate samples with missing key financial variables. After these screenings, we obtain an unbalanced panel of 4,971 firm-year observations.

We calculate the ESGRD of firms using the widely adopted ESG ratings in China, including those provided by Huazheng, SynTao Green Finance, Wind, CASVI, Bloomberg, and FTSE Russell. For each firm-year, we retain observations that are covered by at least two ESG rating datasets. Each available ESG rating is standardized following Christensen et al. (2022). The standard deviation of all available standardized ESG ratings for the same firm in the same year is then used as the measure of ESGRD.

Firm resilience reflects the ability of firms to cope with risk shocks. Firms with strong resilience typically exhibit sustained high-speed growth and lower-risk characteristics. Therefore, we characterize firm resilience along two dimensions: high-performance growth and low financial volatility. Following Ortiz-de-Mandojana and Bansal (2016), we use the year-on-year growth rate of sales revenue to measure high-performance growth and stock return volatility to capture low financial volatility. We then employ the entropy method to determine the weights of these two indicators and compute a comprehensive score as a proxy for firm resilience. Specifically, we first standardize the year-on-year sales revenue growth rate and stock return volatility. Next, we calculate the proportion and information entropy of each indicator, derive their total contribution and corresponding weights, and finally obtain the comprehensive resilience score through weighted summation. Data on ESG ratings, firm balance sheets, financial statements, analyst earnings forecasts, and other relevant variables are sourced from the CSMAR and Wind databases.

Model and Variables

To verify the impact of ESGRD on firm resilience, we estimate the model below:

where

Descriptive Statistics

In Table 1, the sample firms’ average resilience score is 0.1133, which is significantly lower than the maximum resilience score of 1.0737, indicating their low resilience. The sample firm’s average ESGRD score is 0.1556, which is significantly lower than the difference between the average resilience score and its maximum resilience score. This indicates that the difference in ESGRD among the sample firms is smaller than the difference in resilience, which also reflects the similarity between the ESG ratings offered by different rating organizations. The differences in resilience and ESGRD among the sample firms are also consistent with the actual situation. Table 2 shows the correlation test.

Summary Statistics.

Correlation Test.

Results

ESGRD and Firm Resilience

In Table 3, regardless of whether we control for the firm fixed effects or the year fixed effects, the coefficients of

ESGRD and Firm Resilience.

Note. The table shows the results concerning the impact of ESGRD on firm resilience. The t-statistics based on robust standard errors clustered by firm are shown in parentheses.

,**, and *** indicate statistical significance at the 10%, 5%, and 1% levels, respectively.

Firms with high debt levels face significant debt repayment pressure, which weakens their ability to cope with risk shocks and reduces resilience. Firms with high debt levels face significant debt repayment pressure, which weakens their ability to cope with risk shocks and reduces resilience. The coefficients of Inst and

Robustness Checks

Endogeneity Tests

Firms with poor resilience may choose to disclose information on their ESG responsibilities to gain market competitive advantages and social resources, especially those aspects with low implementation costs that can significantly improve their ESG performance. This may lead to inconsistent ESG rating scores from different rating agencies, which in turn can affect their resilience. We use two methods: lagging the explanatory and control variables by one period and the instrumental variable method to alleviate the possible endogeneity issues mentioned above. Due to the unique characteristics of different industries, the ESG performance of firms also exhibits significant industry characteristics; that is, firms in the same industry have higher similarity in ESG performance. Therefore, we choose the number of ESG rating agencies of the firm (

In Table 4, the results of the explanatory variable and control variable lagged by one period, as well as the two-stage least squares method, are shown in columns (1) to (2) and columns (3) to (4), respectively. The results of

Endogeneity Tests.

Note. The table reports the results concerning the endogeneity tests. *, **, and *** indicate statistical significance at the 10%, 5%, and 1% levels, respectively.

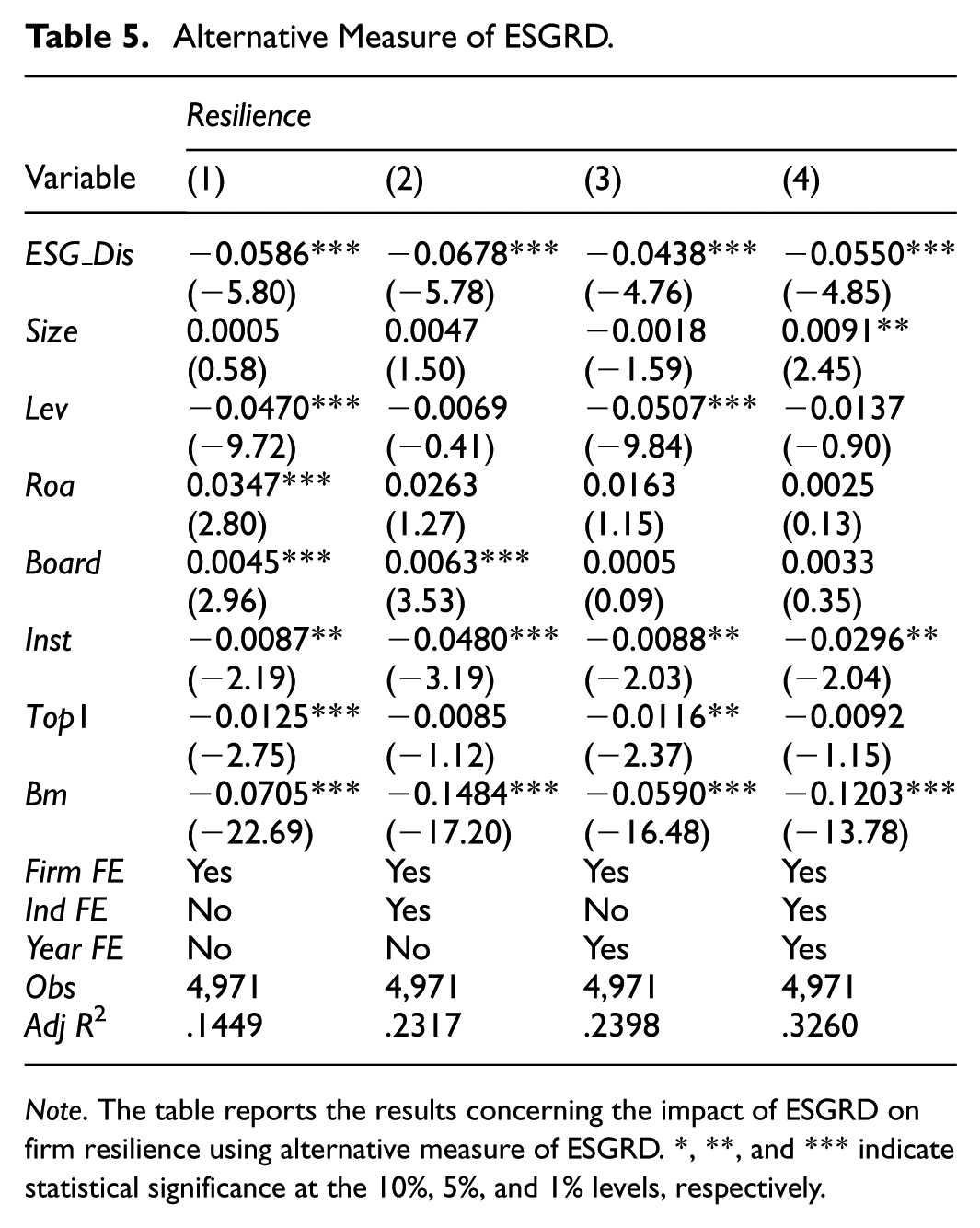

Alternative Measure of ESGRD

Chinese investors also use the ESG ratings of Chinese-listed firms, released by foreign rating agencies like Bloomberg and FTSE Russell, as investment references. Because ESG development in foreign countries is more mature, ESG rating systems are more perfect, and ESG rating scores for firms may be more accurate, which can reflect the true ESG performance of firms. We exclude the Bloomberg ESG rating and FTSE Russell ESG rating used in the benchmark regression and calculate ESGRD using the other four ESG ratings published by Chinese rating agencies. In Table 5, the coefficients of

Alternative Measure of ESGRD.

Note. The table reports the results concerning the impact of ESGRD on firm resilience using alternative measure of ESGRD. *, **, and *** indicate statistical significance at the 10%, 5%, and 1% levels, respectively.

Alternative Measure of Firm Resilience

Different from benchmark regression, which measures firm resilience from performance growth and financial fluctuations, we describe firm resilience in this part from the perspective of a firm’s ability to recover or surpass the original state after risk shocks. In terms of rebound dimension, quick ratio, precipitated redundant resources, non-precipitated redundant resources, and return on equity are selected. In terms of the reverse excess dimension, total asset growth rate, operating income growth rate, and net profit growth rate are selected. We standardize the above indicators and then calculate the arithmetic mean as a proxy indicator for firm resilience (

Alternative Measure of Firm Resilience.

Note. The table reports the results concerning the impact of ESGRD on firm resilience using alternative measure of firm resilience. *, **, and *** indicate statistical significance at the 10%, 5%, and 1% levels, respectively.

PSM-DID

We adopt the propensity score matching method to alleviate the estimation bias that may be caused by the non-randomness of the sample. We define the samples with values above the annual average of ESGRD as the experimental group and the rest as the control group. We use the control variables in the benchmark regression as covariates, apply a one-to-two caliper nearest neighbor matching, and estimate formula (2) based on the new sample. The results in Table 7 further support our conclusion that firms with higher ESGRD have weaker resilience.

PSM-DID.

Note. The table reports the results concerning the impact of ESGRD on firm resilience after controlling the industry fixed effects. *, **, and *** indicate statistical significance at the 10%, 5%, and 1% levels, respectively.

Exclusion of the COVID-19 Samples

The COVID-19 epidemic, which commenced in late 2019, has significantly impacted the economy and society, leading to a severe impact on the real economy. This, in turn, will inevitably weaken the capacity of firms to handle risk shocks, thereby reducing their resilience. This may lead to the negative correlation between ESGRD and firm resilience caused by the impact of COVID-19. Therefore, we further remove the samples of COVID-19 and estimate Equation 1. The coefficients of

Exclusion of the COVID-19 Samples.

Note. The table reports the results concerning the impact of ESGRD on firm resilience after the exclusion of COVID-19 samples. *, **, and *** indicate statistical significance at the 10%, 5%, and 1% levels, respectively.

Mechanism Discussions

The Information Channel

With the advancement of sustainable development, firms’ ESG performance is also evident in the prices of their security assets, which have received widespread attention from analysts, investors, and others. ESG contains complex information, including a large amount of non-financial information from three aspects: environment, society, and governance. This leads analysts and investors to rely mainly on professional rating agencies to evaluate the performance of firms in fulfilling ESG responsibilities (Avramov et al., 2022). Therefore, when the ESG performance of firms varies significantly among various rating agencies, the limited attention of analysts may prompt them to prioritize selecting the ESG rating issued by a certain rating agency as a reference for analyzing stocks based on their own preferences rather than spending a lot of time and energy searching for relevant information about the firm’s ESG information, which may lead to an increase in analyst forecast divergence.

However, when analysts classify ESG as complementary information, different ESG ratings help them to have a more comprehensive understanding of the firm’s ESG performance, reduce the forecast bias caused by a single ESG rating, and thus reduce analysts’ forecast divergence. Analysts are important information intermediaries in the securities market, and their evaluation reports are usually an important reference basis for investors’ investment decisions, which can have a significant impact on investor behavior (Al Tamimi, 2006; Kothari et al., 2016). Therefore, the increase in analyst disagreements may lead to an increase (decrease) in investor disagreements, thereby increasing stock price volatility and reducing corporate resilience. Using the model outlined below, we validate the information channel through which ESGRD influences firm resilience.

where

The Information Channel.

Note. The table shows the results regarding the mechanism analysis of the information channel. *, **, and *** indicate statistical significance at the 10%, 5%, and 1% levels, respectively.

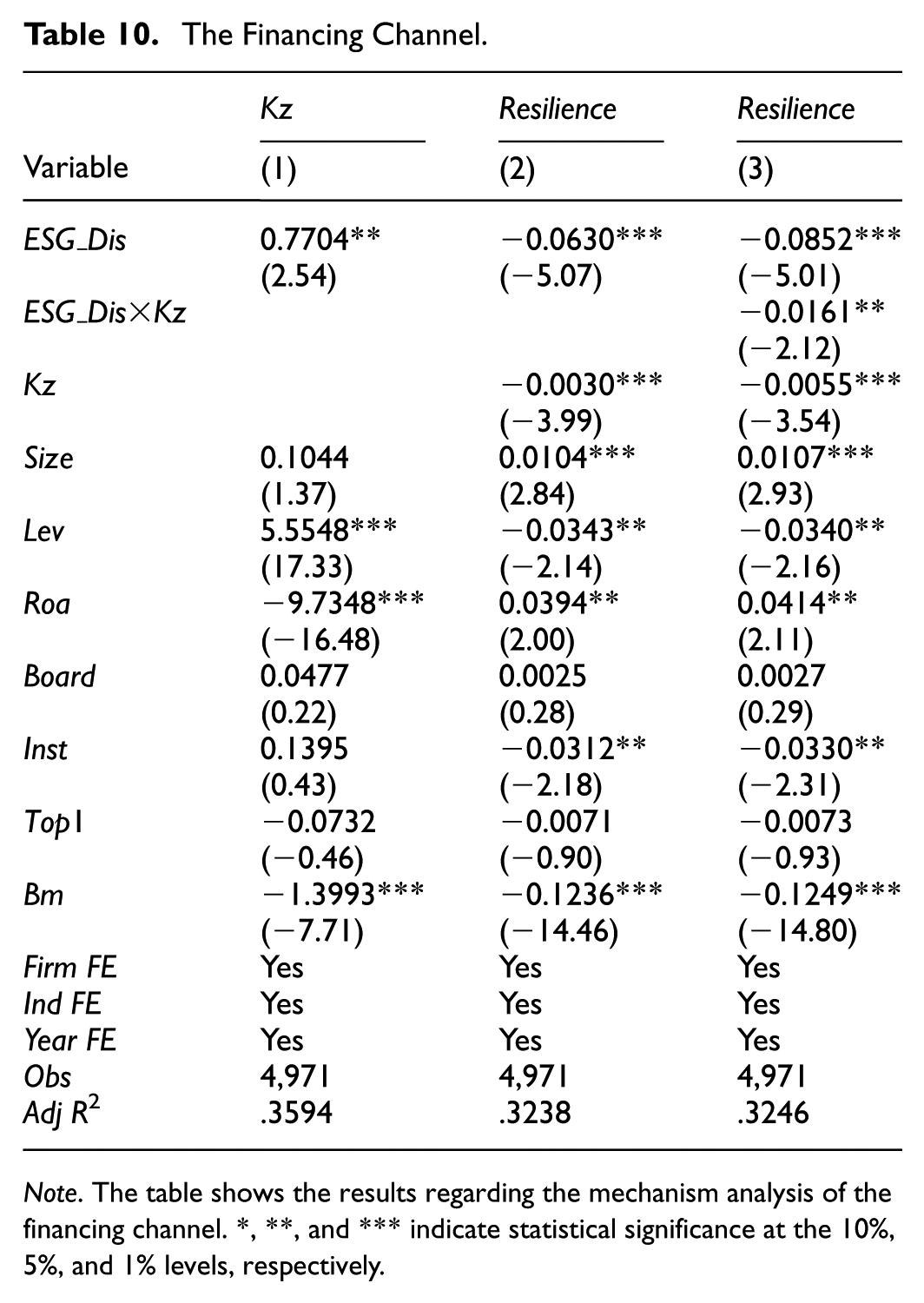

The Financing Channel

A firm’s ESG score is a quantitative indicator of its fulfillment of ESG responsibilities and non-financial performance. It also reflects its ability to sustain development to a certain extent (Fama et al., 2021). Because ESG emphasizes the concept of sustainable development, a firm’s active fulfillment of ESG responsibilities conforms to the concept of sustainable development. Gaining the support of the government, investors, customers, and others enables a firm to gain more resources for its development, thereby enhancing its market competitiveness and resilience to cope with risk shocks (Cornell et al., 2021; Raghunandan & Rajgopal, 2022). When a firm’s ESG performance varies significantly among various rating agencies, it may not reflect its true ESG level, weakening the advantages that better ESG performance brings to the firm (Nirino et al., 2021). Large ESGRDs of firms increase the difficulty of evaluating the real ESG performance of banking financial institutions, and large ESGRDs may also reflect the risk information of firms, which makes banking financial institutions reduce loans to such firms for the purpose of reducing risks (Guo et al., 2024). The decrease in loans from banking and financial institutions leads to a significant increase in financing constraints for firms with large ESGRD, thereby reducing their resilience. We estimate the model below to validate the financing channel via which ESGRD affects firm resilience:

where

The Financing Channel.

Note. The table shows the results regarding the mechanism analysis of the financing channel. *, **, and *** indicate statistical significance at the 10%, 5%, and 1% levels, respectively.

Heterogeneity Tests

Information Transparency

The role of ESG ratings is to provide investors with information about firms’ ESG performance. ESGRD weakens the information effect of ESG ratings, which may encourage stakeholders to collect information on firms’ ESG from other channels to assess its ESG performance (Rubino et al., 2024). Lower information transparency of firms would increase the difficulty for stakeholders to obtain firms’ specific information, making it difficult for them to assess the true ESG performance of firms. As a result, they are more likely to regard ESGRD as a signal of worse true ESG performance or potential risks of firms, thereby deteriorating the relationship between firms and their stakeholders. The deterioration of the relationship between stakeholders and firms would increase firms’ financing constraints, thereby amplifying the negative impact of ESGRD on firm resilience. Based on this, we believe that the impact of ESGRD on corporate resilience should be more significant in firms with poor information transparency. We estimate the following model:

Where

Heterogeneity Tests of Information Transparency.

Note. This table reports the results concerning the heterogeneity tests of information transparency. *, **, and *** indicate statistical significance at the 10%, 5%, and 1% levels, respectively.

Analyst Attention

The mechanism analysis verifies that ESGRD decreases the diversification of analyst forecasts, which in turn decreases analyst forecast divergence. Firms that receive greater analyst attention can disclose more specific information about their operational and financial characteristics. Such information helps investors gain a more comprehensive understanding of firms, thereby reducing investor divergence and further lowering stock price volatility (Kothari et al., 2016). The disclosure of more information at the firm level can also help alleviate information asymmetry between firms and stakeholders. The support of stakeholders can provide the resources that firms need for their operation and development, helping firms to respond more effectively to risk shocks. Therefore, more analyst attention can effectively leverage the positive role of analysts in reducing investor divergence and mitigating information asymmetry, thereby reducing the negative impact of ESGRD on corporate resilience. We estimate the model below to verify the above conjecture:

where

Heterogeneity Tests of Analyst Attention.

Note. The table reports the results concerning the heterogeneity tests of analyst attention. *, **, and *** indicate statistical significance at the 10%, 5%, and 1% levels, respectively.

ESG Decoupling

ESG decoupling refers to the inconsistency between a firm’s actual ESG performance and its ESG disclosure performance. The greater the ESG decoupling, the greater the difference between a firm’s actual ESG performance and its ESG disclosure performance. That is, the firm is more inclined to disclose more about ESG performance while actually doing less in ESG (H. Wang & Shen, 2024; Y. Wu et al., 2020). ESG decoupling reflects the inconsistency between what a firm says and does in ESG and aims to gain support from stakeholders by exaggerating its ESG performance, so as to obtain more social resources and improve its market competitiveness (Eliwa et al., 2023). However, if the ESG decoupling of firms is revealed, it may seriously damage the firm’s reputation, triggering doubts and criticism from investors, consumers, and others about the integrity and authenticity of the firm’s behavior. The revealed ESG decoupling of firms would trigger a large-scale sell-off of their stocks by investors and a reduction in support from stakeholders, which will cause significant fluctuations in stock prices and an increase in financing constraints. They may also be punished by relevant regulatory authorities, which is not conducive to their sustainable development (Delmas & Burbano, 2011). Therefore, ESG decoupling may strengthen or weaken the relationship between ESGRD and firm resilience. We validate the above hypothesis by estimating the following formula:

where

Alternative Measure of ESG Decoupling.

Note. The table reports the results concerning the heterogeneity tests of ESG decoupling. *, **, and *** indicate statistical significance at the 10%, 5%, and 1% levels, respectively.

Conclusion

The disagreement over ESG ratings emerged with the development of ESG and has attracted widespread attention. Firm resilience reflects firms’ sustainable development ability and aligns with ESG’s emphasis on sustainability. Therefore, it is crucial to investigate the connection between corporate resilience and ESGRD. We aim to explore the influence of ESG ratings on firm resilience and how ESGRD affects firm resilience. We discover that firm resilience and ESGRD exhibit a negative relationship, and ESGRD reduces firm resilience by increasing analyst forecast divergence and financing constraints. The negative correlation between ESGRD and corporate resilience is more significant in firms with lower information transparency, lower analyst attention, and higher ESG decoupling.

Enhancing the ESG rating system to mitigate discrepancies across various ESG ratings can be a viable approach to bolstering firm resilience. The ESGRD of firms can serve as a reference for investors to choose investment targets, especially value investors, because firms with a larger ESGRD are more vulnerable to external risk shocks and have poorer sustainable development ability. Regulators can also enhance the ability of firms to cope with risk shocks and reduce the impact of ESGRD on their resilience by improving financing systems and regulating analyst behavior. Regulators should also strengthen the supervision of corporate greenwashing behavior, improve relevant laws and regulations on greenwashing, and increase penalties for greenwashing to restrain corporate greenwashing behavior and reduce its negative impact on ESG development. Firms can also actively improve the quality of information disclosure, especially ESG-related information, which can help reduce differences in ESG ratings among different rating agencies and negative reactions from investors to their ESGRD.

Due to the limitations in data acquisition, our sample is limited to listed firms in China, which makes it necessary to verify whether our conclusions can be generalized to a broader scope. This also indicates the limitations of our research. Examining the impact of ESGRD on corporate resilience based on a global sample could be a potential research direction in the future.

Footnotes

Ethical Considerations

This article does not contain any studies with human participants performed by any of the authors.

Author Contributions

Xin Liu: Conceptualization; Data curation; Formal analysis; Validation; Funding acquisition; Methodology; Software; Writing; Formal analysis; Methodology.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

Data will be available on request from the corresponding author.*