Abstract

In the emerging market economies the influencing power of different strands of ownership structure and ownership concentration on the risk-adjusted returns on assets and equity, dividend yield, earnings, and cost-to income ratio of listed deposit money banks has not been thoroughly investigated. The diminutive research and equivocal findings of previous studies on this subject create grounds for further investigation. Therefore, the aim of this study is to investigate the extent to which these three constructs relate in listed deposit money banks an emerging market economy, Nigeria. Panel data multiple regressions were applied to data extracted from the annual reports from 2009 to 2020 to test the six hypotheses. The results indicate that the disaggregated ownership structure and concentrated ownership relate positively and significantly to the bank performance indices, thereby supporting convergence of owners and managers interests which reduces the agency problems and increases the financial performance of firms. The novelty of this study is the introduction of new indices for measuring performance, ownership structure and concentration which are total departure from the usual method in both emerging and developed market economies. Further research can be extended in other economies using the same computational methods.

Plain language summary

In the emerging market economies the influencing power of different strands of ownership structure and ownership concentration on the risk-adjusted returns on assets and equity, dividend yield, earnings, and cost-to income ratio of listed deposit money banks has not been thoroughly investigated. The diminutive research and equivocal findings of previous studies on this subject create grounds for further investigation. Therefore, the aim of this study is to investigate the extent to which these three constructs relate in listed deposit money banks an emerging market economy, Nigeria. Panel data multiple regressions were applied to data extracted from the annual reports from 2009 to 2020 to test the six hypotheses. The results indicate that the disaggregated ownership structure and concentrated ownership relate positively and significantly to the bank performance indices, thereby supporting convergence of owners and managers interests which reduces the agency problems and increases the financial performance of firms. The novelty of this study is the introduction of new indices for measuring performance, ownership structure and concentration which are total departure from the usual method in both emerging and developed market economies. Further research can be extended in other economies using the same computational methods.

Keywords

Introduction

The financial scandals, the collapse of large companies and advancing figure of distress and failure in the banking industry especially in Nigeria, an emerging economy has sparked much enquiry into the reasons why they failed. At the inception of the banking business in Nigeria, the ownership of banks was largely foreigners, and as a result, indigenous enterprises were unable to access bank credit. To create such opportunities to access credits some indigenous persons established Nigerian indigenous banks late 1920s. Due to total absence of regulation and, inadequate capitalization, quality management, and strong hostile competition posed by foreign banks the 21 out of the 25 existing indigenous banks in Nigeria were self-liquidated by 1954. With the creation of 1973 indigenization decree, the expatriate banks became either fully indigenous owned banks or combined ownership of foreigners and Nigerians, with minimum of 60% shareholding by the later. At various times, the problems faced by indigenous banks in Nigeria have been attributed to the ownership structure.

To salvage the bad situation the Government stepped in to join in the ownership of banks. Government participation in banks dates back to 1952, when the Western Nigerian regional government rescued Wema Bank and National Bank, while the Eastern Nigerian regional government rescued African Continental Bank, out of their slide into failed banks. The federal government of Nigeria (FGN) got involved in the banking business in 1974 when it acquired 40% and later in 1976 extended to 60% shareholding in United Bank for Africa (UBA), Union Bank, and First Bank being the largest three expatriate banks then. It was later observed that Government-owned banks were riddled with frequent changes in board membership as a result of changes of leadership in government. According to Ogunleye (2003), “appointments to boards of government-owned banks were based on political patronage rather than merits and board members saw themselves as representatives of political parties and governments and had little or no loyalty to the banks. As a result, political and social considerations pervaded the decision-making process, and this situation promoted indiscipline in banks as sanctions became very subjective.” He also stated that “privately owned banks were afflicted by undue interference and the pervasive influence of dominant shareholder(s) that were unable to recruit or retain competent management teams.”Olufon (1992) stated that, “bank owners appoint their relatives or friends to key positions instead of professional managers to extend their business empires. Even when the regulatory authorities declined the approval of such appointments, the persons so appointed were sometimes made to remain in the positions either in acting capacity or under different names. As a result of the marriage of strange bed fellows in assembling members of board of directors many banks were faced with boardroom squabbles which precipitated shareholders’ quarrels.” To avert such unpleasant situations in banks, the Central Bank of Nigeria (CBN, 2006) limited direct and indirect government ownership in banks to 10% by the end of 2007 and equity holdings of more than 10% in banks by one investor must have prior CBN approval, on the belief that such equity interest will encourage the board to run the banks well. Despite this legislation, banks were gasping for breath and survival. However, the ghost of distress continues to hover, harass and haunt the banking sector.

From the 1990s to the present 2020, bank failure has been very rampant in the financial sector, some banks exiting from the Nigerian banking space up to 2019. In 1998, 26 banks were liquidated by CBN. The 89 banks existing prior to 2004–2005 bank consolidation exercise were scaled down to 25 by January 2006, in a bid to meet the December 31, 2005 deadline for bank minimum paid-up capital of N25billion and enlarged ownership as stipulated by CBN on July 6, 2004. On 14 August, 2009 the CBN rolled out the names of 14 distressed banks after an on-site audit of the 25 banks in Nigeria. The top management of some banks was removed. Eight banks provided life-support in terms of providing them with soft loans to survive. The major cause of this problem was the extreme weakness in banks’ corporate governance practices. The notoriety of ethical abuse in the industry was allegedly caused by poor corporate governance occasioned by ownership structure of the banks. There were lack of prudential financial reporting, skilled and efficient management. In many cases, the leadership of banks was vested in individual(s) with domineering shareholding. Despite regulations and all measures put in place to salvage the industry, distress and weak corporate governance remains manifesting and the problem remains unresolved. Under a weak regulatory market environment like Nigeria, can shareholders rely on ownership structure to minimize agency problems and ensure convergence of interests as proposed by some scholars?

These developments spur the urge to reassess the impact of corporate ownership structure, as one of the corporate governance mechanisms, especially from the angle of board, board chairperson, chief executive officer, institutional ownership stakes and ownership concentration on banks’ financial performance. The diminutive research and equivocal findings of previous studies on this subject create grounds for further investigation. Therefore, this study aims to find out the nature of association between the strands of ownership structure and the banks’ financial performance in Nigeria, an emerging market economy. There is a need to convince the stakeholders of banks of a logical linkage between the two constructs. Many studies have dwelt on this subject-matter but they did their investigations using samples from around the world, excluding Nigeria. Again, other studies employed accounting measures such as

Some of the methodologies used in establishing the explanatory variables, especially ownership concentration, deviate from the previous methods adopted in previous studies. This makes the study unique and the most recent study on this subject matter. As pointed out by Miko and Kamardin (2015) Nigeria as one of the emerging economies differs from other countries in terms of economic activities, legal frameworks, investments, and investors. Thus, there is a need to conduct this research in Nigerian environment to see whether the findings are consistent or different from previous studies.

The remainder of this work is organized in four sections. In Section 2, stylized facts emerging from earlier theoretical and empirical studies are presented. Section 3 provides the materials and methods, and the results and discussion are captured in section 4. Finally, Section 5 concludes the paper.

Review of Related Literature

Conceptual Review

Different scholars have viewed Ownership structure differently. It has been seen as the distribution of equity shares among different identifiable entities (Demsetz & Villalonga, 2001), widely dispersed ownership and concentrated ownership (Bocean & Barbu, 2007), managerial, institutional, and ownership concentration (Sahut & Gharbi, 2010), ownership of the five biggest shareholders, namely, managerial, institutional, and individual (Alipour & Amjadi, 2011), and ownership of the directors (Shah et al., 2011). However, in this study, ownership structure is the distribution of a firm’s equity shares among different species (identities) of shareholders. These species include inside (managers and employees) and outside owners (individuals, institutions/organizations and the state). Major structure proxies include managerial represented by board of directors, board chairperson, chief executive officer (CEO), executive director, foreign, and institutional ownerships, and ownership concentration. The ownership stake for each category of ownership is the fraction of equity shares held by members of the category (Ruan et al., 2011). For instance, board chairman ownership is the proportion of shares owned by the chairman of the board of directors to the total number of shares issued by the firm (Gohar and Rashid (2021). Institutional (organizational) ownership is the proportion of the total shares owned by institutional investors (Miko & Kamardin, 2015). The same way those of CEO, executive director, and foreign ownership were determined.

Ownership concentration has been viewed differently. Desoky and Mousa (2013) measured ownership concentration by the fraction of shares owned by the largest three shareholding interests and ownership identity as the fraction of shares owned by different type of shareholders.

Munisi et al. (2014) viewed ownership concentration as the portion of shares held by the top five shareholders of the firm, Mamatzakis et al. (2017) used the largest and the second largest managerial block holders who own at least 10% of the total shares in a firm. There are various definitions, but in this study ownership concentration refers to holding a greater number of voting equity shares by a few shareholders. On this note, concentrated ownership is viewed as the proportion of shareholders who own 80% of the total equity shares of a firm. The lower the proportion of shareholders, the higher the level of concentrated ownership is, and vice versa.

The performance indices observed in corporate finance research include return on assets (ROA), return on equity (ROE), earnings per share (EPS) as used by Bajaher et al. (2021), Desoky and Mousa (2013), dividends per share (DPS), and market price per share (MPPS) (Akdogan & Boyacioglu, 2014). ROA shows the profitability of total asset investment, whereas ROE shows the profitability of shareholders’ investment. EPS is a measure of how much profit a company generates for each equity share. DPS is a measure of how much profit a company pays out per share. MPPS measures the worth of a company in the eyes of investors in arm’s length transactions in the stock market. For banks where performance and risk are highly correlated, risk-adjusted ROA and ROE are used instead to reflect the risk-performance nature. One way to achieve this is by using the Sharpe ratio of ROA and ROE, which standardizes the two ratios using a forward- or backward-looking measure of their standard deviation. Other performance metrics adopted include the cost-to-income ratio, which is widely accepted metric of bank performance. In addition, we used EPS growth rate and dividend yield. Two control variables bank size and firm age, have been frequently used in many previous studies (Chunhachinda & Li, 2014; Marashdeh et al., 2021). In addition, the loan-to-deposit ratio, non-performing loans-to-total loans ratio, and bank functional diversification proxy by the non-interest income-to-gross income ratio were introduced as control variables in this study. Change in GDP rates was used to control for the potential economy’s effects.

Theoretical Review

This study is anchored on the agency theory. As separation of firm ownership from management (Abu-Serdaneh & Ghazalat, 2022) continues, conflicts of interests between managers and owners will arise in situations where, the management is self-interest seeking, self-serving, individualistic and opportunistic. To mitigate the divergence of interests and consequential agency problems, agency theory suggests that managers and owners interests converge if shareholders institute ownership structure that can monitor and induce managers to make better decisions that lead to better firm performance (Hart, 1995; Huynh et al., 2020). Thus, a larger managerial ownership stake was recommended by the agency theory in order to reduce the need for and costs of monitoring and control.

Jensen (1993) argues that with board ownership, the oversight and monitoring activities of managers by the board of directors on management would increase. The convergence hypothesis and the entrenchment hypothesis are two competing arguments that attempt to justify the importance of ownership structure on firm performance (Ozdemir, 2020). When there exists a convergence or alignment of owner and manager interests, agency problems will reduce, resulting in an increasing positive effect on firm performance. Thus, ownership structure is an important means to control agency problems. According to Brickley et al. (1988), board stock ownership gives board members an incentive and encouragement to supervise management in more efficient way that leads to improved performance. In light of the entrenchment hypothesis, higher levels of ownership by a group(s) can empower them to be expropriating firm’s resources for their own benefit. Ruan et al. (2011), Lane et al. (1998), and Shleifer and Vishny (1986) submit that care should be taken in furthering the level of ownership beyond a certain level that can serve as a gateway to yielding significant power to the holders to selfishly decrease performance. An increase in managerial equity ownership beyond a certain level can make the holders more entrenched which can decrease performance.

Again, the argument has been that when ownership is concentrated conflicts of interest minimizes through closer monitoring with attendant improvements in firm performance (Kyereboah-Coleman, 2021). Based on the entrenchment view, Lu et al. (2007) argued that concentrated ownership might inversely influence firm performance. Under a weak regulatory market environment like Nigeria, can shareholders rely on ownership concentration to minimize agency problems and ensure convergence of interests as proposed by some scholars (Filatotchev et al., 2013; Jensen & Meckling, 1976; Nguyen et al., 2015). Thus, agency theory views ownership concentration as a mechanism that drives firm performance.

Review of Empirical Literature

A number of empirical studies have dwelt on this topic, ownership structure and firm performance. On a general note, Annisa et al. (2021), Tomar and Bino (2012), Krivogorsky (2006), Gedajlovic and Shapiro (2002) found a substantial influence of ownership structure on bank performance. Onakoya et al. (2013) found positive impact of ownership structure on ROE of nine banks in Nigeria (2006–2010). Fooladi and Ghodratollah (2011) establish an insignificant impact of ownership structure on ROE and ROA on a sample of 30 Malaysian firms. The common notion is that managers will work for the best interests of organizations when they have ownership in the firm and vice versa (Alabdullah, 2018; Shleifer & Vishny, 1997). Thus, an increase in the proportion of shares owned by the managers may help to align the interest of managers and shareholders by restricting them not to waste the firm’s resources for their own well-being (Nyaguthii et al., 2019; Vu et al., 2018). Agency problem may be reduced if managers hold large fraction of the firm’s equity. Alshouha et al. (2021) and Alabdullah (2018) revealed that managerial ownership has a significant and positive impact on performance. Vu et al. (2018), Nyaguthii et al. (2019) showed evidence that managerial ownership has a positive impact on firm performance. Krivogorsky (2006) revealed an insignificant and positive association. While Alabdullah (2018) discovered a positive and significant relationship between managerial ownership control and performance for 109 listed companies on Amman Stock Exchange (ASE), Sheikh et al. (2013) observe a negative relationship between managerial ownership and performance in Pakistani firms. Tayachi et al. (2021) show that managerial ownership has significant and positive effects on debt financing, but significant and negative effects on dividend policy. Demsetz and Villalonga (2001) demonstrated a no association between managerial ownership and firm performance. Specifically, on board ownership, Annisa et al. (2021) showed it has a significant relationship with profitability and efficiency. Faisal (2015) and, Cornett et al. (2009) found significant and positive association between board stake and ROA and Tobin’s Q. Bhagat and Bolton (2013), Z. Chen et al. (2005), Demsetz and Villalonga (2001), R. K. Morck et al. (2000), and Mehran (1995) found a positive relationship between board stake and performance. As these revelations from previous studies are coming from developed economies the case of the emerging economies might be different.

On the relationship between institutional ownership and firm performance Lev (1988) submitted that institutional ownership with large shares and close to perfect information, monitoring power, and a decrease in managerial opportunism and agency cost can have a positive impact on performance. Zouari and Taktak (2014) reported that institutional shareholders do not perform better. Othmani (2022) indicate that banks with more foreign institutional ownership perform better, as foreign institutional investors are considered as good monitors. Liao (2021) broke down the structure of institutional investors in Taiwan and found that when a higher percentage of banks were owned by domestic corporations, the efficiency-augmentation hypothesis was supported, whereas when a higher percentage of banks were owned by domestic trust funds, the efficiency-abatement hypothesis was supported. Kyereboah-Coleman (2021) finds that institutional shareholding enhances market valuation of firms. Tayachi et al. (2021) show that institutional ownership impact positively on financing decisions and dividend policy and their results support a positive relationship between foreign institutional ownership and banks’ performance as measured by Tobin’s Q and return on equity.

Empirical findings on concentration of ownership have yielded conflicting results. For example, Ahmad et al.’s (2020) results of two-stage least squares (2SLS) regression on time series data shows that ownership concentration is significantly and negatively related to firm sustainability of top 200 Malaysian listed companies from 2009 to 2015. Tachiwou (2016) shows, that ownership concentration has insignificant and negative relationships with ROA, but positive relationship with profit margin (PM). Yeung and Lento (2018), Nguyen et al. (2015) confirmed that ownership concentration has a positive effect on firm financial performance in Singapore and Vietnam. The finding supports the prediction of agency theory about the efficient monitoring effect of large shareholders in markets with highly concentrated ownership. Tayachi et al. (2021) show that ownership concentration has significant and positive effects on debt financing, significant and negative effects on dividend policy. Desoky and Mousa (2013) record a significant impact of ownership concentration on firm performance when measured by ROE. Schultz et al. (2010) reported insignificant results for the Australian market. Yabei and Izumida (2008) recorded significant results for the Japanese market. Xu and Wang (1999) reveal a positive relationship (agency cost is likely to reduce in a highly concentrated ownership structure), Hu et al. (2010), Foroughi and Fooladi (2013) indicate a negative relationship, and Haniffa and Hudaib (2006) and Al-Saidi and Al-Shammari (2015) find no relationship, whereas Jaafar and El-Shawa (2009), Sheikh et al. (2013) find a direct relationship for the two. Zouari and Taktak (2014) found no significant linkage with performance at a 49% ownership concentration.

A review of the aforementioned studies leaves research gaps. Previous studies have excluded Nigeria as an emerging economy and also adopted non-disaggregated managerial ownership structure. The disaggregated managerial ownership structure into board ownership, board chairman ownership, CEO ownership, institutional, and ownership concentration would provide policy makers and regulatory authorities with better information on how different ownership structures affect performance in emerging economies as compared to developing and developed economies. While previous studies employed risk-unadjusted returns and stock prices as outcome variables to proxy for performance, we adopt risk-adjusted returns and relative measures of earnings and dividends to reflect the high correlation between performance and risk in banks. Other new introductions are the cost-to-income ratio, growth rate in earnings per share, and dividend yield. Firm size and firm age were majorly employed as control variables by previous researchers (Abdullah et al., 2011; Jaafar & El-Shawa, 2009; Short & Keasey, 1999). This study introduced as control variables loan-to-deposit ratio, non-performing loans-to-total loans ratio, and bank functional diversification proxy by the non-interest income-to-net-interest income ratio and GDP growth rate. No study has yet explored the effect of these dimensions of ownership structure on listed deposit money banks in Nigeria up to 2020. Some of the methodologies used in establishing the explanatory variables, especially ownership concentration, deviate from the previous methods adopted in previous studies. We capture the degree of ownership concentration which has never been considered in any study. Previous researchers have used the percentage of shareholding by the five largest shareholdings (Ahmad et al., 2020; Haniffa & Hudaib, 2006), 49% ownership concentration (Zouari & Taktak, 2014) or by a few substantial shareholders. However, we used percentage of shareholders that hold up to 80% of the total common shares. This makes the study unique and the most recent study on this subject matter.

Hypotheses Development

As managers have more information about the business than atomistic and geographically dispersed owners, shareholders are often at a disadvantaged position to monitor and this gives management wide latitude to fraudulently manage the firm to their personal advantage. Again, as the ownership base becomes increasingly dispersed, management tends to become less accountable and their activities become less observable, at least to shareholders. The authors’ observations aligned with Ogunleye (2003) and Olufon (1992) as appointments to boards of directors of banks in Nigeria are still based on political patronage, friendship, relationship rather than merits. As a result board members see themselves as representatives of their masters or afflicted by undue interference and the pervasive influence of dominant shareholder(s) and have little or no loyalty to the banks, as political and social considerations pervade the decision-making process at board level. A situation where strange bed fellows were assembled as members of board of directors and sanctions are subjectively administered promotes indiscipline in banks especially at management levels. Many banks in this dilemma have boardroom squabbles which precipitate down to their management and other staff. To encourage the board to run the banks well, CBN (2006) limited direct and indirect equity holdings of more than 10% in banks by one investor unless with prior approval by CBN. Despite this legislation, banks are gasping for breath and survival as the ghost of distress continues to hover, harass and haunt the banking sector. Therefore, with the scenario playing out in the banks with respect to ownership structure and its convergence-of-interest and entrenchment, it is the opinion of this study that managerial ownership may not favorably impact financial performance of the banks. Essentially, managerial ownership can be disaggregated into the ownership proportion of board of directors, board chairman, and chief executive officers so we can determine the influence of each on bank performance. Based on the above argument, we predict the following hypotheses in the emerging economy Nigeria.

H1: Board ownership stake has no positive and significant effect on the risk-adjusted return on assets of Nigerian listed deposit money banks.

H2: Board ownership stake has no positive and significant effect on the risk-adjusted return on equity of Nigerian listed deposit money banks.

H3: Board chairman ownership stake has no positive and significant effect on the dividend yield of Nigerian listed deposit money banks.

A number of debates have been presented on the relationship between institutional ownership and performance. These include banking market structure, governance, and supervision (S. H. Chen & Liao, 2011; Mishra & Ratti, 2011; Weir & Laing, 2001), managerial ownership, diversification, and firm performance (C.-J. Chen & Yu, 2012; McConnell & Servaes, 1990; R. Morck et al., 1988), separation of ownership and control (Claessens et al., 2000; Fama & Jensen, 1983), bank ownership and governance quality (Chaudary et al., 2006; Fan & Wiwatanakantang, 2006), ownership structure and bank performance (Nada, 2004). Specifically, Zouari and Taktak (2014) reported no significant impact of institutional shareholders, Othmani (2022) recorded significance but with more foreign institutional ownership, as foreign institutional investors are considered as good monitors. Kyereboah-Coleman (2021) finds that institutional shareholding enhances market valuation of firms. With banks’ performance measured by Tobin’s Q and return on equity Tayachi et al. (2021) show that institutional ownership impact positively on financing decisions and dividend policy. Despite these findings we expect that H4: Institutional ownership stake has no positive and significant effect on the growth rate of earnings per share of Nigerian listed deposit money banks.

According to Thomsen and Pedersen (2000), C.-J. Chen and Yu (2012) dispersed ownership creates a possible lack of management monitoring, which may cause unfavorable effects on firm performance. Fama and Jensen (1983) argue that ownership concentration above a certain level will allow controlling shareholders to become entrenched and expropriate the wealth of minority shareholders by transferring out of the firm resources for their own benefits (i.e., tunneling). This may induce a high cost of capital for the firm and make a hitherto good investment amount for inefficient investments. The argument has been that when ownership is concentrated conflicts of interest minimizes through closer monitoring with attendant improvements in firm performance (Kyereboah-Coleman, 2021). Based on the entrenchment view, Finkelstein and D'aveni (1994), Claessens and Djankov (1999), Thomsen et al. (2006), Holderness (2009), Lu et al. (2007) argued that concentrated ownership might inversely influence firm performance. This is based on the fact that the dominant position attracted to majority shareholders by their substantial number of shares can increase or decrease their divergence of interests, can make them have little or no loyalty to the banks and expropriate the banks’ resources, which can lead to adverse effect on financial performance (Jensen & Meckling, 1976). Under a weak regulatory market environment like Nigeria, can shareholders rely on ownership concentration to minimize agency problems and ensure convergence of interests as proposed by some scholars (Filatotchev et al., 2013; Jensen & Meckling, 1976; Nguyen et al., 2015). Agency theory views ownership concentration as a mechanism that drives firm performance but it is the opinion of this study that concentrated ownership of banks in Nigeria may not have strong favorable impact on financial performance of the banks. Therefore, we predict the following hypotheses in the emerging economy Nigeria.

H5: Ownership concentration has no positive and significant effect on the dividend yield of Nigerian listed deposit money banks.

H6: Ownership concentration has no positive and significant effect on the cost to income ratio of Nigerian listed deposit money banks.

Materials and Methods

Materials

Panel data also referred to as times series with cross-sections means data for many units over many points in time. Data from various units of ownership structure (cross-sections) over the years 2009 to 2020 (times series) constitute a panel data. The panel data contains more degrees of freedom, more sample variability and improves the efficiency of econometric estimates. This makes it appropriate dataset for this study.

The final sample of 10 banks was selected from 13 Nigerian Stock Exchange (NSE) listed Deposit money banks from 2009 to 2020 to form a panel dataset with 120 firm-year observations. The analysis does not include banks with incomplete data (Unity bank and Wema bank) or non-national banks (Ecobank). The use of banking industry data would have been ideal but the study is purely on listed banks on the Nigerian stock exchange with complete and consistent submission of statutory reports to the regulatory authority, the CBN. The 10 selected banks represent adequately the banking industry as they control more than 90% of the industry assets. The dataset used was collected from the annual financial statements of banks approved by the Central Bank of Nigeria (CBN), except for market price per share which was picked from the NSE daily official lists. The study sample spans from 2009 to 2020. The year 2009 serves as the base year because it was the first full year of normal banking operations after the global financial meltdown of 2007 to 2008. The 2009 was chosen in order to avoid the influence of the meltdown since it is not a normal occurrence, it is an aberration. The 2020 is the last year with complete data on the sample banks as at the time of this study. The definitions and measurements of these variables are listed in Table 1.

Definitions and Measurements of the Variables.

Source. Compiled by the authors.

To reduce the potential bias that can be caused by omitted variables, we control for other general firm characteristics, such as bank age, because younger firms tend to have higher growth prospects, and the international operations and innovative capacity of a firm may be affected by age (Alshouha et al., 2021). Alshouha et al. (2021) find the firm age has a negative impact on firm performance. Firm size as an endogenous variable is used to account for the potential effect of economies of scale, as larger firms are harder to manage, tend to be more transparent with more highly qualified managers, have easy access to the debt market at a lower cost, and the maximum benefit of the tax shield influence financial performance.

In Nigeria, deposit money banks (DMBs) comprise of commercial banks that are licensed by the regulatory authority to accept transferable deposits such as demand deposits, carry out the functions of fund safety, savings mobilization, financial resource allocation, loan administration, financial advisory, among others.

Methods

Descriptive statistics were used for the data analysis. In line with Bajaher et al. (2021), to test the relationships and multicollinearity among the independent variables, Pearson product moment correlation was used and the collinear variables were dropped. The multiple regression analysis technique that dominates in previous studies was employed. The models equations are as shown below:

Model 1

Control variables are INSO, OWNC, SIZE, LTDR, NPLR, NIIR

Model 2

Control variables are BCHO, INSO, OWNC, SIZE, FAGE, NPLR, NIIR

Model 3

Control variables are BODO, CEOO, INSO, OWNC, SIZE, FAGE, LTDR, NPLR, NIIR, GDPR

Model 4

Control variables are OWNC, SIZE, FAGE, LTDR, NPLR, NIIR

Model 5

Control variables are BCHO, BODO, CEOO, INSO, SIZE, FAGE, LTDR, NPLR, NIIR, GDPR

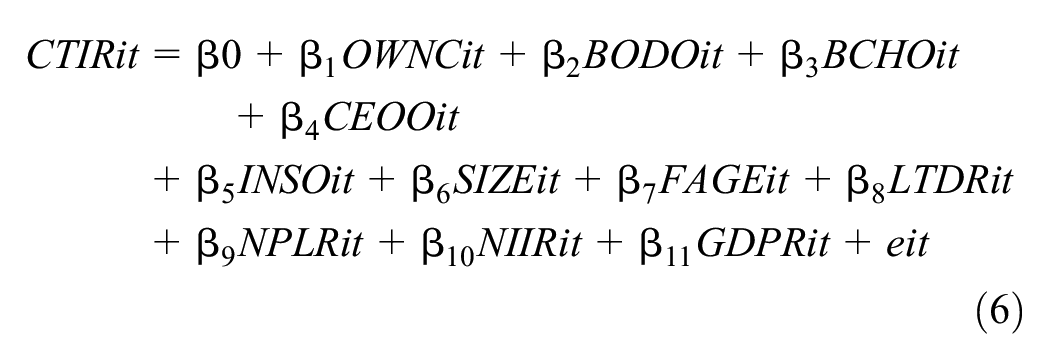

Model 6

Control variables are BCHO, BODO, CEOO, INSO, SIZE, FAGE, LTDR, NPLR, NIIR, GDPR

where, the dependent variables RROA, RROE, DIVY, ESGR, and CTIR are the measures of bank performance; the independent variables BODO, BCHO, INSO, and OWNC are the measures of ownership structure, and the control variables are CEOO, SIZE, FAGE, LTDR, NPLR, NIIR, and GDPR. The eit = the error component. β0 = constant intercept. RROA = risk-adjusted return on assets; RROE = risk-adjusted return on equity; CTIR = cost-to-income ratio; ESGR = earnings per share growth rate; DIVY = dividend yield; BODO = board ownership; BCHO = board chairman ownership; CEOO = chief executive officer ownership; INSO = institutional ownership; OWNC = ownership concentration; SIZE = firm size; FAGE = firm age; LTDR = loan-to-deposit ratio; NPLR = non-performing loan ratio; NIIR = non-interest income ratio; GDPR = gross domestic product growth rate. The uniqueness of this study lies in the introduction of a new credible method for determining the degree of ownership concentration which has never been considered in any study. Previous researchers have used the percentage of shareholding by the five largest shareholdings (Haniffa & Hudaib, 2006), 49% ownership concentration (Zouari & Taktak, 2014) or by a few substantial shareholders. However, in this study, we used the percentage of total number of shareholders that hold up to 80% of the total common shares.

Results and Discussion

Results

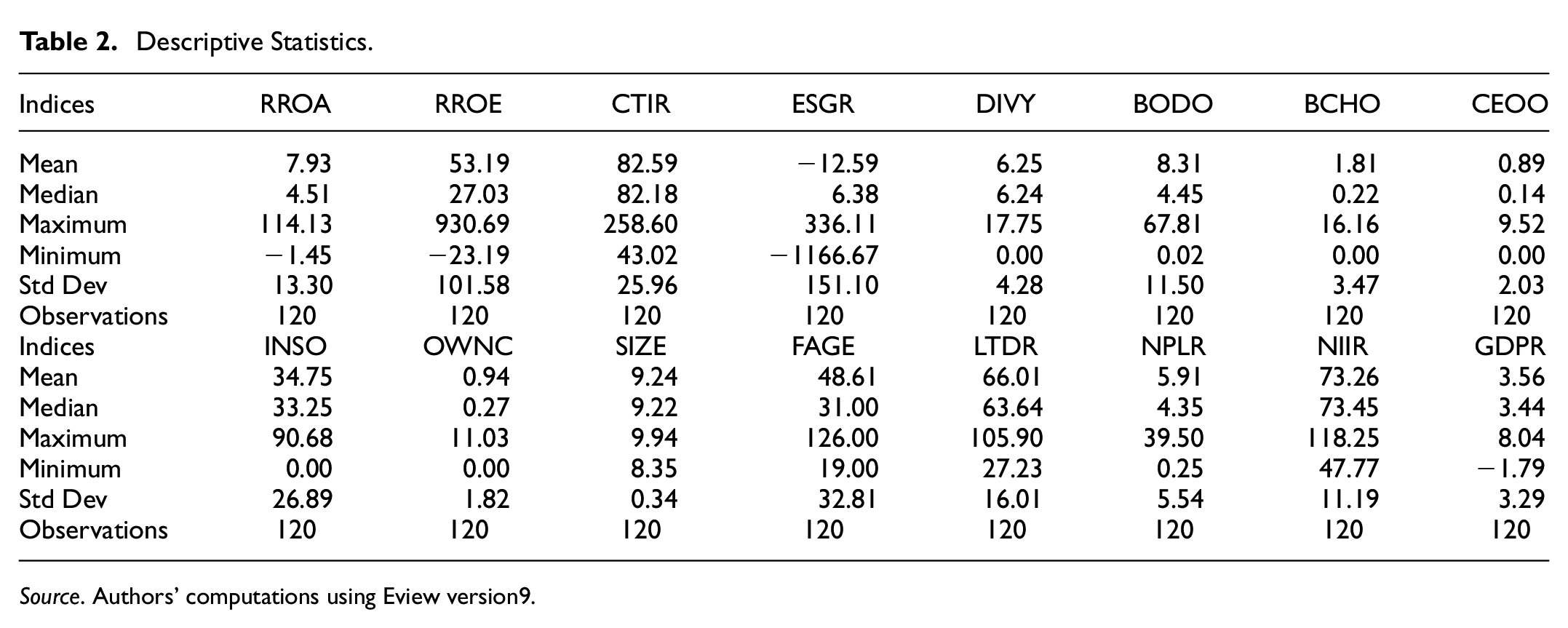

The risk-adjusted return on assets and return on equity averaged 7.93% and 53.19% with maximum and minimum values of 114.13%, 930.69% and −1.45%, −23.19% respectively. The values of the other variables are presented in Table 2. It is surprising that an average of 0.94% of bank shareholders in Nigerian banks holds 80% of the total common shares of the banks, which indicates a very high ownership concentration in Nigerian banks.

Descriptive Statistics.

Source. Authors’ computations using Eview version9.

The correlation matrix in Table 3 shows, no evidence of collinearity among the variables that may lead to outcome bias.

Correlation Matrix.

Source. Authors’ computation using Eview 9.

Regressions were performed at the 95% confidence level. The coefficient of correlation r values in Table 3 are not even near to .70 which means that there is no multicollinearity problem in the models. Any variable that showed signs of multicollinearity was dropped abinitio.

As can be observed in Table 4 board ownership (BODO) relates significantly and positively with risk-adjusted returns (RROA) and, (RROE), relates insignificantly and negatively with cost to-income ratio (CTIR) and dividend yield (DIVY). That is, board ownership has a significant association with RROA, RROE and an insignificant association with the CTIR and DIVY of listed banks in the emerging economy.

Regression Results on RROA, RROE, CITR, ESGR, and DIVY.

Source. Authors’ computation using Eview 9.

Board chairman ownership (BCHO) correlates significantly and positively with dividend yield (DIVY), insignificantly and negatively with risk-adjusted ROE (RROE), insignificantly and positively with cost-to-income ratio (CTIR).

Ownership by chief executive officer (CEOO) increases financial performance and decreases the divergence of interests of owners and managers when the CEO holds a large number of equity shares.

Institutional ownership (INSO) has a positive and significant effect on earnings per share growth rate (ESGR), has an inverse effect on RROA, RROE and DIVY with significant impact on DIVY alone, and has a positive and insignificant effect on CTIR.

Ownership concentration (OWNC) has a positive and significant effect on DIVY and CTIR, a positive and insignificant impact on ESGR but a negative and insignificant effect on RROA and RROE.

Discussion of Results

Board ownership (BODO) relates significantly and positively with risk-adjusted return on assets (RROA) and risk-adjusted return on equity (RROE). This negates the prior expectation of no positive and significant effect of board ownership stake on the risk-adjusted return on assets and equity of Nigerian listed deposit money banks. These findings support the agency theory which recommends that a larger managerial ownership stake will induce managers to make better decisions that lead to better firm performance. This significant and positive relationship align with the findings of Annisa et al. (2021), Huynh et al. (2020), Faisal (2015), Bhagat and Bolton (2013), Onakoya et al. (2013), Tomar and Bino (2012), Fooladi and Ghodratollah (2011), Cornett et al. (2009), Krivogorsky (2006), Gedajlovic and Shapiro (2002), Demsetz and Villalonga (2001), R. K. Morck et al. (2000), Hart (1995), Mehran (1995), Jensen (1993) who reported positive and significant influence of board ownership on financial performance. Also in tandem with the findings of Alshouha et al. (2021), Tayachi et al. (2021), Alabdullah (2018), Shleifer and Vishny (1997), Vu et al. (2018), Nyaguthii et al. (2019), Bhagat and Bolton (2013), Z. Chen et al. (2005), Demsetz and Villalonga (2001), R. K. Morck et al. (2000), and Mehran (1995) who recorded positive and significant influence of managerial ownership on ROE and ROA. However, the study findings are at variance with the studies by Sheikh et al. (2013) who recorded negative and significant influence of managerial ownership on financial performance while Tayachi et al. (2021) showed it against dividend policy. Krivogorsky (2006) registered positive and insignificant influence of managerial ownership on ROE and ROA while Demsetz and Villalonga (2001) observed no significant relationship between managerial ownership and financial performance.

The positive and significant relationship between board chairman ownership and dividend yield negates the prior expectation of no positive and significant effect of board chairman ownership stake on dividend yield of Nigerian listed deposit money banks. The findings support the agency theory which recommends that when there exists a convergence or alignment of owner and manager interests, agency costs will reduce, resulting in an increasing positive effect on firm performance. The study supports the findings of Faisal (2015) and, Bhagat and Bolton (2013) who submitted that when there is a positive convergence-of-interest and less entrenchment, board chairman ownership can favorably impact financial performance, and vice versa when the convergence is negative.

The positive and significant findings support agency theory which states that institutional ownership with its large shares, close to perfect information, and monitoring power decreases managerial opportunism and exerts a positive influence on performance as also observed in Othmani (2022), Kyereboah-Coleman (2021), Tayachi et al. (2021), Hussain et al. (2022), Lev (1988), who discovered positive and significant influence of institutional ownership on financial performance. However, the study does not lend support to Jaafar and El-Shawa (2009), Sheikh et al. (2013) who discovered positive and insignificant influence while Zouari and Taktak (2014) disclosed negative and insignificant effect.

As found in the literature, a high ownership concentration provides stronger incentives to large shareholders at cheap cost to monitor management toward good performance. A significant and positive effect of ownership concentration on dividend yield and cost-to-income ratio, is in line with the findings of Tayachi et al. (2021), Yeung and Lento (2018), Nguyen et al. (2015), Desoky and Mousa (2013), Sheikh et al. (2013), Yabei and Izumida (2008), Haniffa and Hudaib (2006), Xu and Wang (1999). As pointed out by Xu and Wang (1999) a positive relationship indicates that agency problems are reduced in a case of high ownership concentration as is the case of dividend yield and cost-to-income ratio. As pointed out by Fama (1980), ownership concentration does not entrenched large shareholders into expropriating the wealth of minority shareholders. Agency problem is likely to reduce in a highly concentrated ownership structure. The finding supports the prediction of agency theory about the efficient monitoring effect of large shareholders in markets with highly concentrated ownership.

The findings of the study are at variance with that of Tayachi et al. (2021) who observed negative and significant effect of ownership concentration on dividend policy, Ahmad et al. (2020), Hu et al. (2010), Foroughi and Fooladi (2013) recorded same on return on assets, Tachiwou (2016) and Schultz et al. (2010) who arrived at negative and insignificant effect on return on assets. Haniffa and Hudaib (2006), Zouari and Taktak (2014) and Al-Saidi and Al-Shammari (2015) recorded no relationship between the two constructs.

Bank size (SIZE) relates positively and significantly to RROA and RROE, negative and significant to CTIR but has an insignificant and positive effect on ESGR and DIVY. Firm age has an adverse impact on ESGR and DIVY but only strong on DIVY, has a positive and insignificant influence on RROE and CTIR. Loan-to-deposit ratio (LTDR) has significant negative and positive effects on CTIR and ESGR respectively and insignificant negative and positive effects on DIVY and RROE respectively. The non-performing loan ratio (NPLR) and net interest income ratio (NIIR) impact RROA and RROE negatively and insignificantly. While NPLR influences DIVY negatively and significantly NIIR affects CTIR negatively and significantly. Gross domestic product growth rate exhibits negative and insignificant association with CTIR. It also showed a negative and significant effect to DIVY.

The new dimension in this study is that the analyses were conducted on risk-adjusted returns on assets and equity rather than the risk-unadjusted returns used in previous studies. This is the first time such is adopted in emerging market economies. The managerial ownership was applied in disaggregated form. Another uniqueness of this study lies in the introduction of a new credible method for determining the degree of ownership concentration which has never been considered in any study. Therefore, the contributions of this study to existing literature are the introduction of new indices for performance measurement, ownership structure and concentration. These are total departure from the usual method in both emerging and developed market economies.

Conclusion

This study examines the extent different strands of ownership structure variables influence the performance of listed deposit money banks in an emerging economy, Nigeria. Using panel data regression analysis with the fixed effects model, the findings show that board ownership stake has a strong direct effect on risk-adjusted return on assets and equity. Board chairman ownership stake has a strong favorable influence on dividend yield. Institutional ownership has a strong positive effect on growth in earnings per share. Ownership concentration has a strong positive influence on dividend yield and cost-to-income ratio of the listed banks in the emerging economy. The study concurs to agency theory which suggests that to mitigate the divergence of interests and consequential agency problems, internal corporate governance mechanisms in the area of ownership structure should be used to monitor and induce managers to make better decisions that lead to better firm performance.

Policy Implications of the Findings

Since it is now obvious that ownership stake by members of board of directors can strongly influence favorably return on assets and return on equity in their risk-adjusted form, the banks’ shareholders should allocate reasonably substantial equity shares to members of the board of directors in order to encourage them to provide substantial returns. To maintain good dividend policy that generates substantial dividend amounts to shareholders the board chairman ownership stake should be very high as it has a strong favorable influence on dividend yield. To entrench good growth prospects for earnings per share Institutional ownership stake should be very high as well. For the fact that ownership concentration has a strong positive favorable influence on dividend yield and cost-to-income ratio of the listed banks in the emerging economy, it should be encouraged but monitored carefully to prevent the adverse effect of monopolistic tendencies in the industry.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Data Availability Statement

The data that support the findings of this study are available on request from the corresponding author, Emmanuel Chuke Nwude