Abstract

ESG ratings have progressively emerged as a crucial reference for investors in devising investment strategies. However, discrepancies in rating outcomes exist among various rating agencies, stemming from divergent standards. This study delves into the impact of these inter-agency discrepancies on the sustainability of ESG ratings through the lens of market pricing efficiency. The investigation reveals that ESG ratings can ameliorate stock mispricing by alleviating information asymmetry within the capital market and curtailing irrational investor behavior. Nonetheless, these discrepancies undermine the sustainability of ESG ratings and diminish their corrective influence on stock mispricing. Further inquiry identifies that the attenuation effect originates from the suboptimal quality of corporate ESG information disclosure, attributable to a deficiency in external oversight, culminating in an information confusion effect induced by these discrepancies. This research endeavors to offer policy recommendations to regulatory authorities aimed at standardizing corporate ESG information disclosure practices and ESG rating standards, thereby enhancing the sustainability of ratings and the pricing efficiency of the capital market.

Plain Language Summary

This study unveils a relationship between institutional discrepancies and the sustainability of ESG Ratings, and market pricing efficiency. ESG ratings can ameliorate stock mispricing by alleviating information asymmetry within the capital market and curtailing irrational investor behavior. Discrepancies undermine the sustainability of ESG ratings and diminish their corrective influence on market pricing efficiency. The analysis identifies that the attenuation effect originates from the suboptimal quality of corporate ESG information disclosure.

Keywords

Introduction

With the intensifying ecological and environmental challenges, countries worldwide have been strengthening environmental regulations. In 2006, the United Nations introduced the Principles for Responsible Investment (PRI), advocating for ESG investing. As of March 2024, 5,345 institutions have signed the PRI, with assets under management growing from 21 trillion in 2010 to 121 trillion. ESG ratings serve as a cornerstone for ESG investing, linking enterprises with capital markets, improving corporate external information environments, and alleviating information asymmetry. They help ESG-compliant companies gain stakeholder support, reduce financing constraints, mitigate risks, and enhance value. However, rating agencies differ in ESG rating scopes, measurements, and weightings, introducing subjectivity and uncertainty into ESG ratings. Growing rating discrepancies amplify ESG investment risks, increase stock price volatility, reduce external financing opportunities, weaken ESG-performance-driven corporate innovation, and diminish analysts’ forecast accuracy. Whether such discrepancies undermine ESG rating efficacy remains a question that warrants further exploration.

This study examines Chinese A-share listed companies to investigate the impact of ESG rating discrepancies on ESG rating efficacy via stock mispricing. Its potential marginal contributions are: first, expanding ESG rating economic consequence research by analyzing the influence of ESG rating discrepancies on ESG rating efficacy from the stock mispricing perspective. This enriches the exploration of ESG valuation’s corrective effects and provides a new angle for understanding ESG factors in asset pricing. Second, it offers practical insights for ESG information disclosure system development. The heterogeneous characteristics of ESG rating uncertainty’s weakening effect on ESG rating efficacy, revealed under varying disclosure mechanisms with different degrees of external supervision, can inform ESG information disclosure policies. This promotes the valuation system’s ability to fully capture listed companies’ sustainable development capabilities, advances capital market valuation system construction, and facilitates high-quality capital market development.

Hypothesis Development

The classical Efficient Market Hypothesis (EMH) posits that in a perfectly efficient capital market, security prices constantly reflect all available information. However, due to frictions like imperfect market institutions and incomplete information transmission channels, China’s capital market efficacy is far less than perfect, causing widespread stock mispricing.

ESG ratings, a key measure of corporate performance, provide investors with information on corporate social responsibility, environmental performance, and governance beyond traditional financial statements. They are market interpretations from professional rating agencies, featuring horizontal and vertical comparability and becoming vital for investment decisions. ESG ratings supplement the financial-information-dominated value assessment system, helping correct investors’ expectations in corporate value models, improving pricing efficiency by making stock prices better reflect intrinsic value.

Amid the “dual carbon” goals and corporate green transformation, more investors incorporate ESG performance into their decisions. Yet, due to the complexity of ESG information, low data transparency, poor comparability, and high processing costs for external investors, accurately assessing corporate ESG performance is tough. In this context, third-party professional ESG rating agencies’ comprehensive evaluation results are more professional, accessible, and comparable, offering a direct reference for investors. Thus, Hypothesis 1 is proposed:

H1: ESG ratings can sustainably correct stock mispricing.

Based on signaling theory, corporate ESG practices enhance the sense of responsibility, boost corporate value, and reduce financing costs. However, ESG activities require investment. Companies with higher ESG investment and better ESG performance have a stronger incentive to disclose ESG information externally. This signals strong sustainable operational capabilities and green development, alleviates investor adverse selection issues (Tkocz-Wolny, 2019), and improves corporate information transparency.

Companies with higher ESG ratings typically have robust internal governance and external oversight mechanisms. The synergy between internal and external governance effectively restrains irrational managerial motivations for information disclosure, prompting enterprises to provide more transparent and accurate information. This addresses investor information shortages and enhances asset pricing efficiency.

Within the positive feedback loop of ESG investment information transparency → ESG disclosure → ESG rating → ESG investment, information asymmetry between corporate insiders and external investors diminishes. Investors can evaluate corporate value based on more authentic information, gradually aligning stock prices with intrinsic value through investment actions and reducing mispricing.

ESG ratings also enhance the external information environment to mitigate stock mispricing. On one hand, ESG ratings reflect a company’s future potential, offering analysts a valuable information source to predict profitability and operational risks. Analysts can acquire ESG information at lower costs and integrate ESG factors into their frameworks, improving forecast accuracy. On the other hand, as information intermediaries in capital markets, analysts provide investors with operational insights through research reports. Enhanced forecast quality aids investors in making informed decisions, enriches stock price information, and alleviates mispricing. Based on this, Hypothesis 2 is proposed:

H2: ESG ratings correct stock mispricing by reducing information asymmetry in capital markets.

The investor base in the capital market impacts its rationality. China’s market is predominantly composed of small and medium investors lacking professional expertise and information processing capabilities. They are prone to emotional decisions and herding behavior during market fluctuations or policy shifts, leading to stock mispricing.

In contrast, value-oriented institutional investors possess professional and informational advantages, resisting psychological biases and prioritizing long-term returns. Their investment strategies align with ESG principles. High ESG ratings can attract these investors, improving the investor structure and mitigating irrational market sentiment.

Moreover, ESG ratings serve as a certification tool, reducing investors’ information processing costs and cognitive biases. They align investor expectations and suppress sentiment-driven and heterogeneous beliefs, thereby alleviating stock mispricing.Based on this analysis, Hypothesis 3 is proposed:

H3: ESG ratings correct stock mispricing by reducing irrational investment behavior in the capital market.

China’s ESG development is still in the early stage, and corporate ESG information disclosure lacks uniform standards. ESG information has characteristics like unstructuredness, qualitativeness, and complexity, which bring subjectivity into the rating process. Meanwhile, the lack of authoritative guidance in the ESG evaluation system leads to different rating agencies using distinct methodologies and interpreting companies’ ESG performance differently, making rating disagreements common.

Given objective rating discrepancies, investors must understand the potential implications of ESG rating disagreements when using ESG rating data in investment strategies. This helps reduce the adverse effects of rating inconsistencies on investment decisions and promotes a more informed and rational investment approach.

From the perspective of information asymmetry in the capital market, the impact of ESG rating uncertainty on ESG rating efficacy depends on whether disagreements among institutions introduce market noise or provide incremental insights into company characteristics.

On one hand, according to signaling theory, consistent signals are deemed credible. Large ESG rating discrepancies suggest possible inaccuracy or deception in corporate-disclosed information, making it hard to ascertain actual ESG performance and convey effective ESG information value. In such cases, rating results become noise, forcing investors to bear extra information processing costs and interfering analysts’ judgments. This reduces the reference value of ESG rating information for analysts’ earnings forecasts, exacerbates information asymmetry between enterprises and investors, and decreases capital market pricing efficiency.

On the other hand, some studies indicate that ESG rating disagreements reflect different evaluation angles based on unique rating models, conveying distinctive information to investors. However, considering that China’s capital market is individual-investor-dominated and most lack professional information processing capabilities, it is difficult for individuals to extract useful investment information from rating differences. Therefore, this paper assumes that rating disagreements introduce noise rather than incremental information, weakening the restraining effect of ESG ratings on stock mispricing.

From the perspective of irrational investment behavior in the capital market, ESG rating disagreements mean high uncertainty and complexity in rating information. This increases investors’ information processing costs, scatters their limited attention, and makes it hard to accurately assess enterprises’ true ESG performance based on ESG ratings. Moreover, different investors using limited rating data for investment decisions leads to varying expectations about the same stock’s value. This intensifies investor heterogeneous beliefs, resulting in increased valuation bias in stock prices. Faced with ESG rating disagreement-induced uncertainty, optimists tend to accept the highest company—provided rating as the true ESG status. With short—selling constraints, stock prices often reflect optimistic investors’ views more readily, while pessimists struggle to incorporate their views into stock prices in time, causing overvaluation. Based on the above analysis, Hypothesis 4 is proposed:

H4: ESG rating discrepancies weaken the corrective effect of ESG ratings on stock mispricing.

The ESG value chain consists of information disclosure, evaluation, and investment, with disclosure being the rating foundation. Whether ESG rating disagreements indicate incremental information or noise depends on the underlying information’s authenticity and effectiveness. Under China’s “voluntary—with—compulsion” ESG disclosure framework, exploring disclosure quality is essential for understanding rating disagreements and their impact on the ESG value chain.

Currently, Chinese regulators follow the “voluntariness-based, compulsion-supplemented” principle for listed companies’ ESG disclosure. In environmental disclosure, key polluting entities must disclose environmental information, while others follow a “comply-or-explain” policy. For social responsibility disclosure, since 2008, stock exchanges have mandated reports from specific companies, with others disclosing voluntarily. Corporate governance disclosure has clear compulsory requirements in regular reports, offering stronger external supervision and higher information quality. However, the voluntary system lacks clear guidelines, increasing manipulation risks and making ESG rating disagreements more likely to reflect uncertainty, introducing market noise and weakening ESG ratings’ role in reducing capital market mispricing.

Unlike mandatory annual report audits, third-party ESG attestation is currently voluntary. Given the poor quality of ESG information and frequent greenwashing, investors expect higher-quality ESG information. More enterprises are proactively seeking third-party ESG attestation to enhance credibility and stakeholder confidence. There’s a trend towards promoting third-party ESG attestation, moving from voluntary to mandatory and from limited to reasonable assurance. Third-party attestation improves ESG information quality, reduces market noise from rating disagreements, and curbs mispricing. Based on this, Hypothesis 5 is proposed:

H5: The negative impact of ESG rating discrepancies on ESG ratings’ sustainability is more pronounced without external constraints.

From the property rights perspective, SOEs, controlled by state capital, have business objectives beyond profit maximization, including fulfilling social responsibilities and executing government directives. This makes the government more motivated to SOEs’ ESG performance. Also, negative ESG information can greatly damage SOEs’ reputation. If ESG information fraud is exposed, the consequences for management are severe. This restrains management’s utilitarian-driven strategic behavior, encouraging more diligent and authentic ESG information disclosure.

Looking at industry-specific characteristics, heavily polluting industries have significant externalities. Their ESG performance directly affects regulatory scrutiny, which impacts their future operations and risk exposure. Thus, investors are highly sensitive to ESG disclosures of heavily polluting companies, and stakeholders demand high-quality ESG information. Under stronger external oversight, these companies tend to have better ESG disclosure quality, lessening the adverse effects of ESG rating uncertainties. Based on this, the study proposes Hypothesis 6:

H6: The moderating effect of ESG rating discrepancies is more evident among non-state-owned enterprises and those not in heavily polluting industries.

The relationship of hypothesis is shown in Figure 1.

The relationship of hypothesis.

Research Design

Data Sources and Sample Selection

This study selects A-share listed companies in China spanning from 2011 to 2022 as research specimens and applies the following treatments to the samples: (1) Excluding data pertaining to listed companies within the financial sector; (2) Omitting company samples that conducted initial public offerings (IPOs) during the respective year; (3) Excluding companies labeled as ST, PT, *ST, as well as those that have suspended listing or have been delisted; (4) Eliminating samples with missing values in critical variables; (5) Given that this study constructs pivotal variables based on rating data from multiple rating agencies, following the methodology outlined by Serafeim and Yoon (2023), samples rated by two or more ESG rating agencies are retained; (6) To mitigate the impact of extreme values, this study executes a winsorization procedure on continuous variables at the upper and lower 1% percentiles. Ultimately, a total of 22,728 “firm-year” observations are obtained.

Variable Definition

ESG Ratings and ESG Rating Discrepancies

The preponderance of extant literature constructs variables to gauge corporate ESG performance based exclusively on data from a solitary rating agency. Given that ratings from distinct rating agencies can exhibit significant variations, reliance on a single information source is inadequate for a comprehensive and objective revelation of the true circumstances. Therefore, this study constructs ESG ratings and rating disagreement variables utilizing rating data from six major domestic and international rating agencies with authority and influence, including China Securities Evaluation, Bloomberg, FTSE Russell, Shandong Road and Green Development, Wind, and Lianlun.

To ensure comparability across different rating agencies, the study initially processes the rating data from the six major rating agencies as follows: (1) China Securities Evaluation, Wind, and Lianlun’s ESG ratings are divided into nine levels from C to AAA, assigned values ranging from 1 to 9; (2) Shandong Road & Green Development’s ESG ratings are divided into ten levels, employing the same assignment method, assigned values sequentially from 0 to 9; (3) Bloomberg’s ESG ratings are evaluated on a scoring system spanning from 0 to 100, taking 10% of the specific score and rounding off; (4) FTSE Russell’s ESG ratings range from 0 to 5, taking 200% of the specific score and rounding off.

Following the aforementioned processing, the rating ranges of different rating agencies become similar, thereby ensuring that their impact weights are comparable when constructing explanatory variables. Drawing upon Christensen et al. (2022), this study employs the average value of the processed scores from the six major ESG ratings to measure ESG ratings (ESG), where a higher ESG value indicates a higher ESG rating for the company. Additionally, utilizing the standard deviation calculation of the processed scores from the six major ESG ratings, we derive the ESG rating disagreement (ESG_diff) variable, where a larger ESG_diff value signifies greater uncertainty in the company’s ESG ratings.

Stock Mispricing

Stock mispricing captures deviations between market prices and intrinsic value, encompassing both overvaluation and undervaluation. Current literature predominantly employs two measurement approaches: (1) The regression decomposition method (Rhodes-Kropf et al., 2005), which isolates mispricing by regressing market-to-book ratios against fundamental drivers like earnings and dividends, though its coefficients exhibit industry sensitivity; (2) The residual income valuation model (RIVM), which discounts future excess returns over capital costs to derive intrinsic value—theoretically rigorous but contingent on subjective parameterization of financial metrics and discount rates. While the former directly quantifies price-book divergences and the latter anchors in forward-looking cash flows, both face methodological constraints: regression models risk sector-specific bias, whereas RIVM outcomes depend on input assumptions. To mitigate these limitations and ensure conclusion robustness, this study concurrently applies both frameworks, cross-validating results to disentangle sector-driven artifacts from genuine pricing inefficiencies. This dual-method approach not only addresses measurement heterogeneity but also strengthens causal inference about ESG’s role in correcting market misalignments.

Control Variables

To mitigate the influence of omitted variables and enhance the robustness of the empirical analysis, this study draws upon relevant literature on stock mispricing research and incorporates a battery of control variables aimed at accounting for potential factors that may affect stock mispricing. Specifically, the study includes several company-level control variables: Firm Size (Size), Listing Age (Age), Return on Assets (ROA), Leverage Ratio (LEV), and Firm Growth (Growth). Furthermore, to capture the impact of corporate governance mechanisms, the study introduces corporate governance-level control variables such as Dual Roles (Dual), Board Size (Board), Largest Shareholder’s Stake (Top 1), and Board Independence (Indep).

By including these control variables, the study seeks to isolate the independent effect of the primary variables of interest on stock mispricing, thereby providing a more accurate assessment of the relationships under investigation. This comprehensive approach ensures that the empirical findings are less likely to be contaminated by confounding factors, thereby enhancing the validity and reliability of the research conclusions.

The names, symbols, and specific definitions of the variables involved in the empirical research are shown in Table 1.

Variable Names, Symbols, and Definitions.

Model Design

To examine the impact of ESG ratings on the level of stock mispricing, this paper adopts a two-way fixed effects model with fixed time and industry for testing, as shown in equation (1):

Where

It is expected that the regression coefficient of ESG rating (

In order to test the influence mechanism of ESG rating on stock mispricing, this paper analyzes the mechanism from two perspectives: internal and external information asymmetry of enterprises and irrational behavior of investors. The two-step method is adopted for mechanism testing, that is, based on Model (1), Model (2) is constructed for testing:

Where

In order to study the impact of ESG rating differences on the relationship between ESG ratings and the level of stock mispricing, this paper adds ESG rating differences as a moderating variable in Model (1) and tests the moderating effect by introducing interaction terms, as shown in Equation (3):

Where

Empirical Analysis of the Sustainability of ESG Ratings from the Perspective of Market Pricing Efficiency

Descriptive Statistics

Table 2 presents key descriptive statistics: The stock mispricing indicators Misp1 and Misp2 show ranges of 0.0068 to 1.6537 and 0.0135 to 3.1174 respectively, with means of 0.4597 (SD = 0.3471) and 0.6495 (SD = 0.5203), indicating widespread price deviations from intrinsic value in the A-share market and substantial cross-firm variation. ESG ratings (ESG_mean) range from 2.5 to 6.333 (median:4.5), reflecting significant heterogeneity in corporate ESG performance. The moderating variable ESG rating divergence (ESG_diff) spans 0 to 2.8284 (mean = 1.1847), demonstrating notable discrepancies in ESG evaluations across rating agencies. These patterns establish an empirical foundation, revealing both pervasive stock mispricing and marked divergence in ESG implementation and rating consensus among Chinese listed companies.

Basic Descriptive Statistical Characteristics of the Main Variables.

Table 3 reveals three key divergences among six ESG rating agencies. First, coverage and time dimensions vary substantially: Huazheng spans the widest sample (2009–2021), while others show inconsistent temporal ranges. Second, rating scales differ markedly: four agencies use 0 to 9 scales (samples clustered at BBB/BB), whereas Bloomberg employs 0 to 100 (90th percentile = 42.97) and FTSE Russell 0 to 5 (most scores = 1–2). Third, foreign agencies systematically assign lower ESG scores to A-share firms. These systemic discrepancies in methodology and output underscore critical challenges in ESG rating comparability, warranting deeper investigation into their impacts on market reliability.

Descriptive Statistics of Raw ESG Data.

Benchmark Regression Results Analysis

Table 4 presents the regression results of Model (5) employing two-way fixed effects to examine ESG ratings’ impact on stock mispricing. Columns (1) to (2) and (3) to (4) report outcomes using Misp1 and Misp2 as dependent variables, respectively. The ESG coefficient remains statistically negative at the 1% level across all specifications, whether controlling solely for year/industry fixed effects (Columns 1 and 3) or incorporating additional covariates (Columns 2 and 4). This robust inverse relationship indicates that higher ESG ratings correspond to lower degrees of stock mispricing, consistent across both measurement methodologies. These findings provide empirical validation for Hypothesis 1, suggesting that improved ESG performance mitigates pricing inefficiencies in China’s A-share market.

Benchmark Regression of ESG Rating Validity.

Note. The t-values of the coefficients are in parentheses, where ***, **, and * denote significance at the 1%, 5%, and 10% statistical levels, respectively.

Robustness Test

To ensure the reliability of the empirical results, this paper conducts robustness tests in the following ways.

Lagging the Core Explanatory Variable

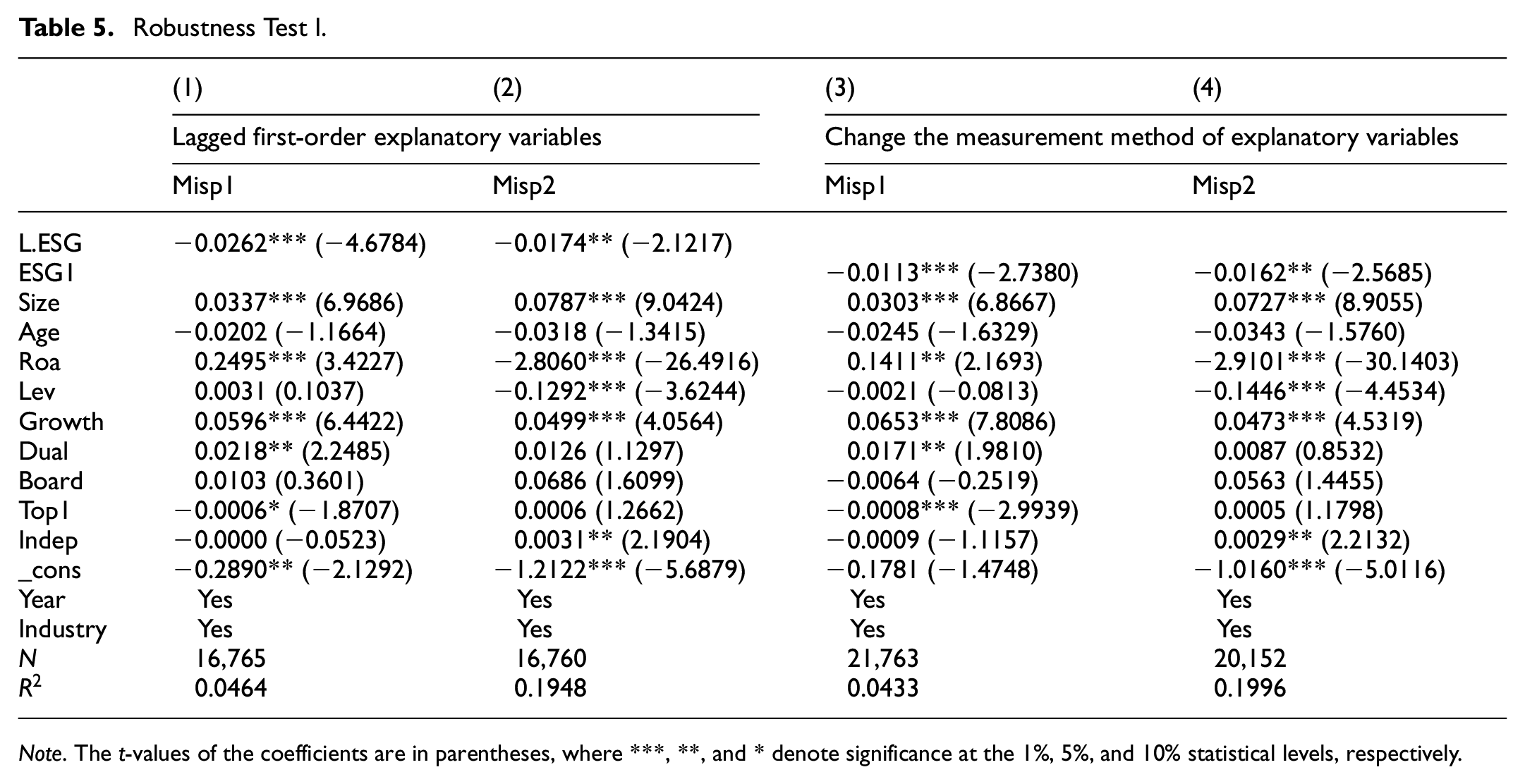

From a temporal perspective, the market may react to ESG rating information with a lag, that is, investors who prefer ESG will decide to adjust their portfolios after a period of time after the rating is released. Therefore, considering the lag of ESG ratings and the endogeneity problem of mutual causality, this paper regresses the stock mispricing again using the lagged ESG rating variable (L.ESG), and the results are shown in columns (1) and (2) of Table 5. The coefficient of the lagged ESG rating is still significantly negative.

Robustness Test I.

Note. The t-values of the coefficients are in parentheses, where ***, **, and * denote significance at the 1%, 5%, and 10% statistical levels, respectively.

Changing the Measurement Indicator of ESG Rating

In the preceding empirical analysis, the ESG rating was determined using the average of the six domestic and foreign rating agencies. Wenjie and Bojian (2023) discovered that there is a noticeable asymmetry in the scoring of companies with varying ownership attributes by domestic and foreign ESG rating agencies. Domestic rating agencies tend to assign higher ESG ratings to state-owned enterprises compared to foreign rating agencies. The primary reason for this divergence lies in the fact that the domestic rating system fully incorporates social responsibilities such as poverty alleviation, economic stability, and employment promotion, which are generally undertaken by state-owned enterprises, while foreign rating systems typically do not place significant emphasis on these “implicit” social responsibilities. Consequently, domestic rating agencies can more comprehensively reflect ESG performance and are better aligned with China’s national conditions.

Furthermore, domestic rating agencies cover a broader range of listed companies on China’s A-share market. Therefore, in the robustness test, this paper employs the average rating of four domestic rating agencies (ESG1) to measure ESG ratings. The regression results following the alteration of the measurement method are presented in columns (3) and (4) of Table 5, and the corrective effect of ESG ratings on mispricing remains significant. This finding underscores the robustness of the initial conclusions and highlights the importance of considering the unique characteristics of China’s market and corporate environment when evaluating ESG performance.

Further Control of Provincial Fixed Effects

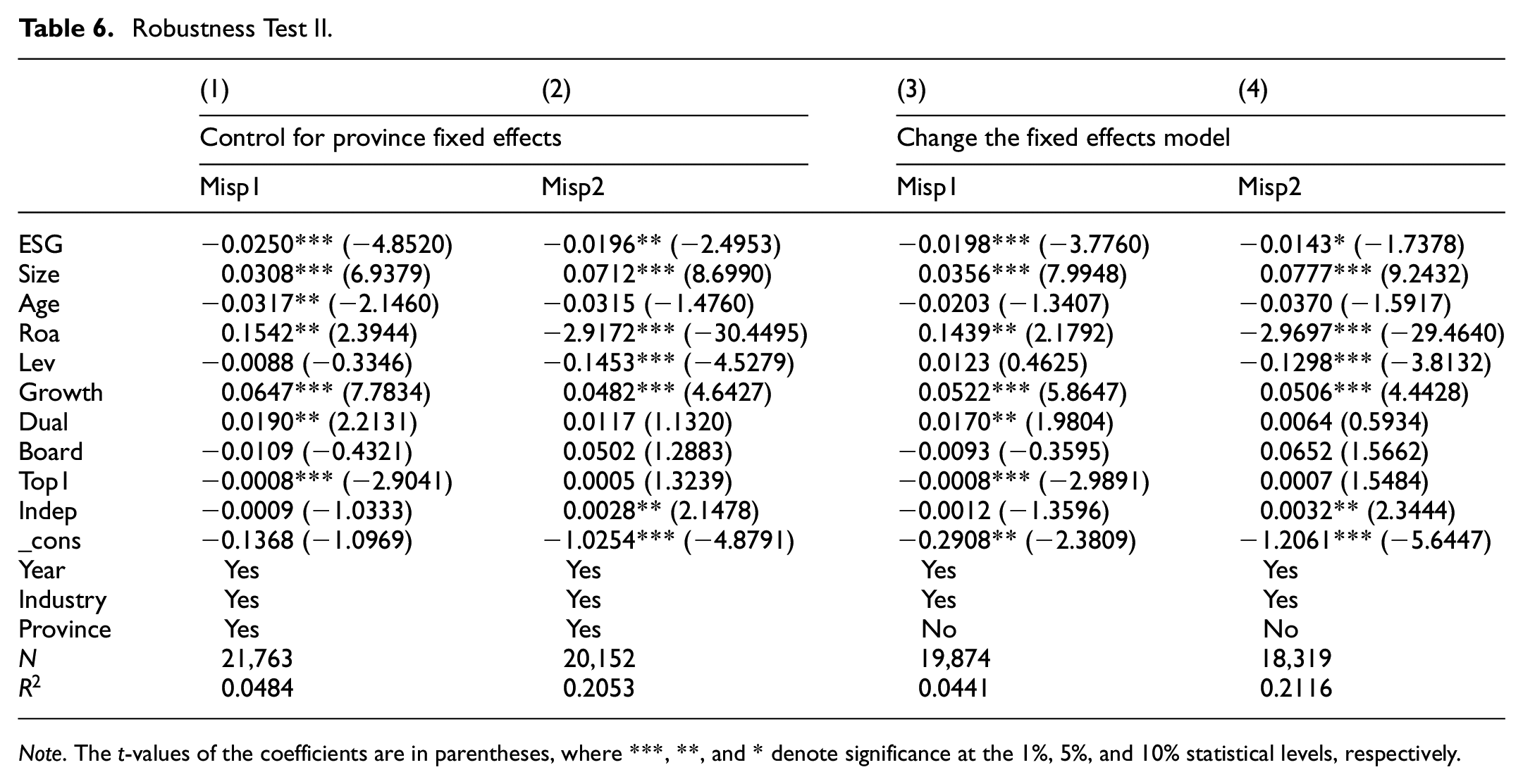

Considering that the regression model (1) does not account for the influence of unobservable regional factors on the regression outcomes, potential endogeneity issues may arise. Drawing on the research of Xiaobing and Shujing (2023), this paper incorporates provincial fixed effects into the original model. Tables 6, columns (1) and (2) display the regression results after further controlling for year, industry, and province fixed effects. The ESG rating coefficient continues to be significantly negative, thereby affirming the robustness of the baseline regression conclusion presented in this paper. This finding underscores the stability of the relationship between ESG ratings and stock mispricing, even after accounting for regional factors, and highlights the reliability of the study’s empirical findings.

Robustness Test II.

Note. The t-values of the coefficients are in parentheses, where ***, **, and * denote significance at the 1%, 5%, and 10% statistical levels, respectively.

Excluding the ramifications of the stock market crash

Given that during stock market crashes, stock prices experience severe fluctuations due to systemic risks, leading to significant deviations of stock prices from their intrinsic values, this study further eliminates the impact of the 2015 to 2016 stock market crash to substantiate the robustness of the basic regression. The regression results are displayed in Table 6, columns (3) and (4). The findings suggest that the ESG rating continues to significantly mitigate stock mispricing, thereby affirming that the research conclusion remains valid.

This analysis is crucial as it demonstrates the resilience of the relationship between ESG ratings and stock mispricing even in the face of extreme market conditions, such as stock market crashes. By controlling for the potential confounding effects of the 2015 to 2016 crash, this study provides robust evidence supporting the hypothesis that ESG ratings can effectively reduce stock mispricing. This finding not only strengthens the empirical foundation of the research but also offers valuable insights for investors and policymakers seeking to understand the role of ESG factors in mitigating market risks and enhancing market stability.

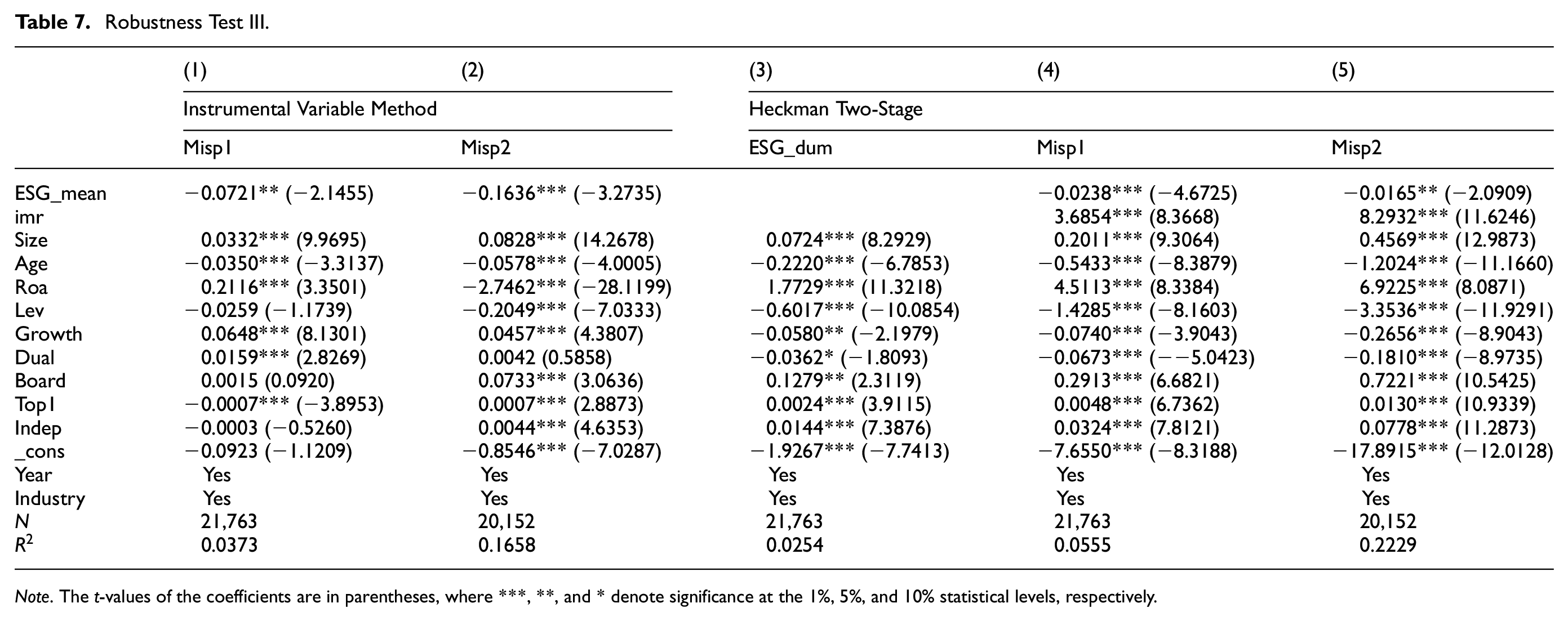

Instrumental Variables Method

Endogeneity issues, such as reverse causality and omitted variables, may exist between ESG ratings and the level of stock mispricing. To mitigate these endogeneity problems, this paper employs instrumental variables and adopts the two-stage least squares (2SLS) method. Currently, many studies utilize the ESG ratings of other companies in the same industry and year as instrumental variables for a given company. Given that ESG ratings exhibit a strong industry spillover effect, they satisfy the relevance requirement of instrumental variables. However, concerns regarding the exclusivity of this indicator remain.

Furthermore, considering that the phenomenon of stock mispricing is closely linked to the industry, in China’s stock market, which is characterized by speculative trends, speculation based on conceptual sectors and industry upstream and downstream leads to synchronized rises and falls, thereby exacerbating the level of stock mispricing. Therefore, to ensure the exogeneity of the instrumental variables, this paper uses the average ESG ratings and rating divergence of other companies in the same province and year as the sample company as instrumental variables, respectively, and conducts two-stage least squares regression.

The regression results presented in columns (1) and (2) of Table 7 indicate that the coefficient of ESG ratings (ESG_mean) remains significantly negative. This finding suggests that even after further accounting for endogeneity issues, the conclusions remain consistent with those presented earlier in the paper and have not undergone substantial changes. This robustness test reinforces the validity of the initial findings, providing strong evidence that ESG ratings significantly mitigate stock mispricing.

Robustness Test III.

Note. The t-values of the coefficients are in parentheses, where ***, **, and * denote significance at the 1%, 5%, and 10% statistical levels, respectively.

Heckman Two-Stage Regression

Considering that this paper excludes companies with fewer than two ESG rating agencies from its analytical scope, potential sample selection bias may arise. To address this concern, the Heckman two-stage regression methodology is employed for testing.

In the initial stage, following the approach outlined by Zengfu and Jiaying (2023), a corporate ESG dummy variable (ESG_dum) is constructed. This variable is assigned a value of 1 if a company’s ESG rating exceeds the median of its industry counterparts within the same year; otherwise, it is assigned a value of 0. The ESG_dum serves as the dependent variable, and the control variables from the baseline model are utilized to conduct a Probit regression, which estimates the inverse Mills ratio (IMR).

In the subsequent stage, the IMR is incorporated into the baseline model to conduct regression analysis. The regression results from the second stage, presented in columns (3), (4), and (5) of Table 7, demonstrate that the ESG rating maintains a significant negative correlation with stock mispricing at the 1% statistical significance level. This finding indicates that even after accounting for the issue of sample self-selection bias, the conclusion that ESG ratings exert a corrective effect on stock mispricing remains valid.

The application of the Heckman two-stage regression methodology ensures that the potential sample selection bias is adequately addressed, thereby reinforcing the robustness and reliability of the study’s findings. This approach not only validates the initial conclusions but also provides a more rigorous analysis of the relationship between ESG ratings and stock mispricing.

Mechanism Analysis

Drawing upon the preceding theoretical underpinnings and empirical evidence, it is evident that ESG ratings can ameliorate stock mispricing via two principal pathways: mitigating both the internal and external information asymmetry inherent in enterprises and curtailing investor irrational behavior. This section endeavors to conduct an in-depth examination by initiating from these two mechanisms.

Information Asymmetry Mechanism

ESG ratings enhance corporate information transparency and the precision of analysts’ forecasts, mitigating the information asymmetry between internal and external stakeholders. Consequently, these ratings facilitate more accurate assessments of stock value by investors, ultimately guiding stock prices towards their intrinsic values.

In the realm of corporate information transparency, a high ESG rating can bestow positive reputation and financing advantages upon enterprises. Consequently, companies that prioritize ESG practices possess the incentive to proactively enhance the quality of their ESG information disclosures to satisfy the information requirements of rating agencies and investors. Simultaneously, a high ESG rating exerts a supervisory influence. Should the irrational information disclosure behavior of management be unveiled, it will incur higher costs. Therefore, ESG ratings can augment corporate information transparency and facilitate the convergence of stock prices towards their intrinsic values.

This study employs the level of earnings management (DisAcc) and the information disclosure quality rating (Evaluation Result) disclosed by the Shenzhen Stock Exchange to gauge information transparency. Specifically, the level of earnings management is calculated as the absolute value of discretionary accruals derived from the modified Jones model. Given that the absolute value of discretionary profits tends to be substantial, it is further subjected to logarithmic transformation. A higher level of earnings management implies greater information asymmetry between internal and external stakeholders within the enterprise. The information disclosure quality rating provided by the Shenzhen Stock Exchange encompasses four levels: excellent, good, qualified, and unqualified, which are assigned values of 1 to 4, respectively. Consequently, a higher information disclosure quality rating corresponds to lower information transparency.

This paper adopts a two-step approach to examine the underlying mechanism. In the first step, the benchmark regression results are reutilized. In the second step, the mechanism variables serve as the dependent variables, and ESG ratings act as the independent variables for multiple regression analysis according to Model (2). The findings are presented in Table 5, where Column (1) represents the regression result of the corporate earnings management level. The coefficient of ESG rating is −0.0499 and statistically significant at the 1% level, indicating that as ESG ratings improve, information transparency is significantly enhanced. Column (2) showcases the regression result of the Shenzhen Stock Exchange’s information disclosure quality rating, with the coefficient of ESG rating being −0.1826, which is also significant at the 1% level. This finding suggests that a higher ESG rating can effectively mitigate information asymmetry between investors and the internal aspects of the enterprise, thereby rectifying mispricing.

In terms of analysts’ forecast quality, ESG ratings are an important channel for analysts to obtain ESG information, which helps analysts better evaluate the long-term sustainable development ability and risks of enterprises. Then, through information release and integration, the improvement of analysts’ forecast quality can play a role in value discovery and information transmission, helping investors to more accurately price the value of listed companies, and finally reflected in the stock price, which is manifested as a mitigation of mispricing. This paper uses analysts’ forecast error rate (Ferror) as a proxy variable for analysts’ forecast quality, and the calculation formula is shown in (4), where is the analysts’ forecasted earnings per share, is the actual earnings per share, and the larger the value of analysts’ forecast error rate, the lower the forecast quality.

The regression outcomes are exhibited in Column (3) of Table 8, wherein the coefficient of ESG rating is −0.3276 and statistically significant at the 1% level. This finding implies that as the ESG rating increases, the quality of analysts’ forecasts is significantly enhanced, information asymmetry is mitigated, and consequently, stock mispricing is subdued.

Analysis of Information Asymmetry Mechanism.

Note. The t-values of the coefficients are in parentheses, where ***, **, and * denote significance at the 1%, 5%, and 10% statistical levels, respectively.

Investor Irrational Behavior Mechanism

This section delves into three pivotal mechanism variables stable institutional investor preference, investor sentiment, and investor heterogeneous beliefs to dissect the transmission pathway of the corporate ESG rating-investor irrational behavior stock mispricing mechanism.

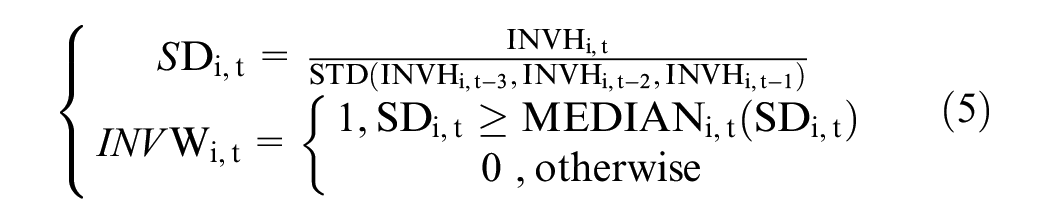

Regarding stable institutional investor preference, a high ESG rating signals long-term sustainable profitability, drawing the focus and investment of stable institutional investors. Boasting professional and informational advantages, these investors engage deeply in corporate operations or exert supervisory oversight, leveraging their governance influence to enhance transparency and curb stock mispricing. Moreover, their long-term stock holdings insulate them from sudden events and short-term market sentiment, stabilizing stock volatility and minimizing overvaluation/undervaluation risks, thereby steering stock prices toward intrinsic value.

To analyze institutional investor stability, this study adopts Li Zhengguang et al. ’s (2014) method, assessing holdings from temporal and industry perspectives. The specific calculation formula is presented in (5):

Analysis of Investors’ Irrational Behavior Mechanism.

Note. The t-values of the coefficients are in parentheses, where ***, **, and * denote significance at the 1%, 5%, and 10% statistical levels, respectively.

The rating information released by external information intermediaries will affect investor beliefs and decision-making behavior, while high sentiment and expectation divergence will induce irrational behavior in investors, driving stock prices away from their intrinsic value. High ESG ratings bring more information content and higher quality of information to investors. The more comprehensive and objective the information received by investors, the better it can suppress investor sentiment and heterogeneous beliefs to reduce mispricing in the capital market.

Therefore, this paper refers to the research of Wei'an et al. (2012) and uses the stock turnover rate (Turnover) to measure investor heterogeneous beliefs; referring to the research of Qing and Dixing (2014), by decomposing the Tobin’s Q value method, the investor sentiment variable (Sentiment) is calculated. Columns (2) and (3) of Table 9 are the regression results of investor heterogeneous beliefs and investor sentiment, respectively. The coefficients of ESG ratings are significantly negative, indicating that a higher ESG rating makes investor sentiment return to rationality, reduces investor heterogeneous beliefs, and thus stock prices also return to intrinsic value.

Empirical Test of the Impact of Discrepancies on the Sustainability of ESG Ratings

This study explores the impact of disagreement on the efficacy of ESG ratings by incorporating interaction terms into the regression model. The results are displayed in Table 10, where the coefficient of the interaction term ESG*ESG_diff in Column (1) is 0.0177, which is significantly positive at the 1% statistical significance level. Moreover, the coefficient of the interaction term ESG*ESG_diff in Column (2) is 0.0145, which is significantly positive at the 5% statistical significance level. These findings indicate that the effectiveness of ESG ratings in correcting stock mispricing depends on the degree of rating disagreement. Specifically, as rating disagreement increases, the mitigating effect of listed companies’ ESG ratings on stock mispricing diminishes, suggesting that rating disagreement undermines the efficacy of ESG ratings. Consequently, Hypothesis H4 proposed in this paper is supported.

Empirical Test of the Effectiveness of Divergence on ESG Rating.

Note. The t-values of the coefficients are in parentheses, where ***, **, and * denote significance at the 1%, 5%, and 10% statistical levels, respectively.

Furthermore, this paper delves into the factors contributing to disagreement that undermines the effectiveness of ESG ratings. Given that the mediums for disclosing sustainable information are not standardized, initial disclosures were primarily made in annual reports. As the corporate social responsibility (CSR) reporting system evolved, CSR reports began to disclose information aligned with ESG principles, encompassing areas such as charitable donations, environmental governance, product safety, and employee rights protection. In recent years, with the growing prominence of the ESG concept, listed companies have increasingly opted to publish standalone ESG reports. Consequently, this study employs CSR reports as a proxy for ESG information to investigate the heterogeneous impact based on the quality of ESG information disclosure.

Initially, considering the variances in the disclosure systems of corporate social responsibility reports, the sample is bifurcated into two groups: mandatory disclosure and voluntary disclosure. The regression results presented in Table 11 indicate that, under the industry regression valuation method, there is no significant disparity in the moderating effect of ESG rating divergence. However, under the residual income valuation method, the interaction term ESG*ESG_diff is significantly positive within the voluntarily disclosed group, whereas it is insignificant under mandatory disclosure. This finding suggests that the lack of standardization and regulation in voluntary disclosure leads to divergence reflecting the uncertainty of rating agencies regarding the true ESG performance of enterprises, thereby intensifying investors’ heterogeneous beliefs. Consequently, the diminishing effect of disagreement on the efficacy of ESG ratings is more pronounced under the voluntary disclosure system.

Heterogeneity Analysis: Mandatory vs. Voluntary Disclosure.

Note. The t−values of the coefficients are in parentheses, where ***, **, and * denote significance at the 1%, 5%, and 10% statistical levels, respectively.

Secondly, the sample is categorized and regressed based on whether the corporate social responsibility report adheres to the GRI (Global Reporting Initiative) standards. The findings are presented in Table 12. The interaction term ESG*ESG_diff exhibits a significant positive relationship in the samples that do not comply with the GRI standards, whereas it lacks statistical significance in the samples that conform to these standards. This finding implies that ESG information disclosed in accordance with the GRI standards aids in alleviating the adverse repercussions stemming from ESG rating divergence and diminishes the extent of stock mispricing.

Heterogeneity Analysis: GRI Standards.

Note. The t-values of the coefficients are in parentheses, where ***, **, and * denote significance at the 1%, 5%, and 10% statistical levels, respectively.

Lastly, this paper uses whether the corporate social responsibility report has been third-party assured as the grouping condition for regression. The results are shown in Table 13. Regardless of the method used to measure the mispricing variable, the interaction term of ESG rating divergence ESG*ESG_diff is significantly positive in the sample group that has not been third-party assured, while it is not significant in the sample group that has been third-party assured. This indicates that third-party assurance of ESG can improve the quality of ESG information disclosed by enterprises, help suppress the noise contained in ESG rating divergence, and reflect more company-specific information. Thus, the negative moderating effect of ESG rating divergence is more pronounced in enterprises that have not undergone third-party assurance.

Heterogeneity Analysis: Third-party Verification.

Note. The t-values of the coefficients are in parentheses, where ***, **, and * denote significance at the 1%, 5%, and 10% statistical levels, respectively.

By categorizing the sample into state-owned enterprises (SOEs) and non-state-owned enterprises (non-SOEs) based on property rights nature, Table 14 displays the outcomes of the grouped regression analysis. In non-SOEs, the regression coefficient of the interaction term for ESG rating divergence is significantly positive at the 1% level. Conversely, it fails to pass the significance test in SOEs. This finding implies that the mitigating effect of ESG ratings on stock mispricing within SOEs remains unaffected by the expansion of rating divergence. The primary reason for this is that the rating divergence of SOEs predominantly reflects the characteristic information identified by different rating agencies, rather than signifying the ESG-related risks of the enterprise.

Heterogeneity Analysis: Property Rights.

Note. The t-values of the coefficients are in parentheses, where ***, **, and * denote significance at the 1%, 5%, and 10% statistical levels, respectively.

Drawing upon the definitions of heavy pollution industries outlined in the ‘Classification Management Catalogue for Environmental Protection Inspection of Listed Companies’ and the ‘Guidelines for Industry Classification of Listed Companies’ revised by the China Securities Regulatory Commission in 2012, the ultimate selection of codes for heavy pollution industries encompasses: Mining (B06–B12); Textile and Leather Industry (C17–C19); Light Industry (C22); Petrochemical Industry (C25); Chemical Industry (C26, C28, C29); Pharmaceutical Industry (C27); Metallurgical Industry (C31, C33); and Thermal Power Industry (D44). Following the division of the sample into heavy pollution and non-heavy pollution industries and the execution of grouped regression analysis, the regression outcomes are presented in Table 15.

Heterogeneity Analysis: Environmentally Sensitive Industries.

Note. The t-values of the coefficients are in parentheses, where ***, **, and * denote significance at the 1%, 5%, and 10% statistical levels, respectively.

In non-heavy pollution enterprises, the regression coefficient of the interaction term for ESG rating divergence is significantly positive at the 1% level. In contrast, it lacks significance in heavy pollution enterprises. This observation suggests that the mitigating effect of high ESG ratings on stock mispricing within heavy pollution enterprises remains unaffected by the expansion of rating divergence. The primary rationale for this phenomenon is that, under stringent environmental regulations and robust supervision mechanisms, the quality of ESG information tends to be relatively high, thereby effectively curbing rating divergence.

Conclusions and Implication

As sustainable development gains traction and “dual carbon” goals advance, investors are increasingly incorporating ESG metrics into their decisions, elevating the significance of third-party ESG ratings in capital markets. This study delves into how ESG rating uncertainty impacts stock mispricing, reaching these key conclusions:

ESG ratings mitigate stock mispricing by reducing information asymmetry and curbing irrational investment behavior. They act as a certification tool, offering reliable ESG performance evaluations through agencies’ expertise. However, their main effect is on suppressing overvaluation rather than undervaluation. ESG rating downgrades may worsen information asymmetry and weaken the corrective power of ESG ratings.

ESG rating uncertainty can undermine the role of ESG ratings in reducing stock mispricing. Greater rating divergence indicates higher uncertainty in corporate ESG performance, lowering ESG rating effectiveness. This increases investors’ information processing costs, leads to more heterogeneous beliefs, and thus exacerbates stock mispricing. Whether ESG rating uncertainty reflects company-specific information or noise hinges on the authenticity and effectiveness of underlying ESG information. The study also conducts heterogeneity analyses based on ESG information disclosure quality and corporate characteristics. It is found that when ESG information is disclosed voluntarily, not in line with GRI standards, and without third-party assurance, the disclosure quality is poor. This intensifies the market noise from rating divergence and weakens ESG ratings’ ability to curb stock mispricing. Moreover, the lack of external supervision in ESG information disclosure tends to enhance the negative moderating effect of ESG rating uncertainty, thus inhibiting the corrective effect of ESG ratings on stock mispricing.

Based on the findings, the following policy recommendations are put forward:

Improve and standardize China’s ESG rating system: Currently, China lacks a unified ESG evaluation system. The significant score differences among rating agencies generate more noise than information, reducing rating effectiveness and comparability. This makes it hard for investors to accurately assess corporate ESG performance and is not conducive to improving the pricing efficiency of China’s capital market. To address this, regulatory authorities should take the lead in building a China-specific ESG evaluation system and developing relevant norms and guidelines. In this way, differences can be gradually reconciled, and the positive role of ESG ratings can be maximized while minimizing the negative effects of rating divergence. When constructing the ESG rating system, the unique characteristics of different industries should be fully considered, and differentiated evaluation indicators and weights should be established. For example, for heavily polluting industries closely related to the environment and ecology, the weight of environmental indicators should be increased. For the financial industry involving national financial risks, greater emphasis should be placed on governance-related assessments.

Establish a comprehensive ESG information disclosure system: At present, China has not yet developed a systematic and standardized ESG information disclosure system. Relevant guidelines are scattered, and ESG information is mostly qualitative with low data transparency. This results in significant differences in the scope and depth of ESG information disclosed by listed companies in terms of environmental performance and social responsibility. The GRI standards offer comprehensive and detailed guidance for ESG information disclosure, which is highly executable and can improve the quality of ESG information. Additionally, China urgently needs to establish a robust ESG information supervision system to penalize information manipulation, such as disclosure fraud and intentional concealment of negative information. In this regard, regulatory authorities can actively promote the use of GRI standards for sustainable development reporting or develop a information disclosure framework tailored to China’s national conditions. The scope, content, indicators, and quality of disclosures should be explicitly defined. Furthermore, third-party audits of ESG information should be introduced to enhance information quality and address market failures in voluntary disclosure.

Deepen the understanding of ESG concepts among corporate management and market investors: Capital market regulators should guide corporate management to recognize that ESG investments are not merely moral obligations but also strategies that can generate long-term benefits. Therefore, companies should adopt sustainable development strategies as a key approach to building long-term value. They should increase ESG-related activities, enhance ESG performance across all areas, and proactively improve the quality of ESG information disclosure. Internal mechanisms should be established to ensure data accuracy, reduce uncertainty in ESG performance, improve the informational value of ESG ratings, and mitigate the noise-generating effect of rating divergence. For investors, incorporating ESG factors into investment strategies when constructing and managing investment portfolios can help accurately identify company value, achieve investment returns, and control risks. Therefore, investors, especially institutional investors, should be encouraged to make greater use of ESG information. ESG-related investment tools and products, such as ESG funds, should be launched to promote scientific ESG investing and strengthen the positive role of financial activities in sustainable development.

To enhance the practicality of the suggestion to “establish a comprehensive ESG information disclosure system,” the following specific steps are proposed, particularly for high-risk industries:

Implement mandatory third-party audits: For heavily polluting and other high-risk industries, require third-party audits of ESG information disclosures to ensure accuracy and reliability.

Develop industry-specific guidelines: Create detailed ESG disclosure guidelines for different industries, especially high-risk ones, specifying key ESG indicators and disclosure requirements.

Enhance regulatory enforcement: Strengthen oversight of ESG disclosures in high-risk industries, imposing strict penalties for non-compliance or misinformation to ensure timely and accurate disclosures.

A cost-benefit analysis of adopting more transparent ESG reporting is essential for companies. While transparent ESG reporting may involve initial costs such as third-party audits and enhanced data collection systems, the long-term benefits include improved reputation, reduced financing costs, and increased market competitiveness. Companies should weigh these factors to make informed decisions that align with their sustainable development goals.

Footnotes

Ethical Considerations

This article does not contain any studies with human participants performed by any of the authors.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: We thank the support provided by the 2024 Research and Cultivation project of Guangdong University of Finance & Economics [Grant No. 2024JLPY02; 2024JYPY07], the National Natural Science Foundation of China [Grant No. 72403150], and the Guangdong Province College Youth Innovative Talent Project [Grant No. 2024WQNCX110].

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

Data sharing not applicable to this article as no datasets were generated or analyzed during the current study.

Declaration of Generative AI in Scientific Writing

Generative AI and AI-assisted technologies only are used in the writing process to improve the readability and language of the manuscript.