Abstract

High out-of-pocket costs coupled with limited health care insurance are the key features of developing countries including Ethiopia. This study explored factors that derive households’ health insurance decision-making behavior by taking the Community-Based Health Insurance (CBHI) scheme in purposively selected four woredas from high and low enrollment rates in North Shoa zone, Amhara, Ethiopia. Both quantitative and qualitative research approaches were utilized.. The study used primary data collected from purposively selected 384 representative households using a semi-structured questionnaire. The study primarily applied a binary logistic regression along with descriptive analysis. Findings revealed that age and education of the head of the household, size of the household, previous year’s estimated annual health expenditure, household’s perception toward the quality and adequacy of public health service, awareness, and trust in the scheme were positively influencing households’ decision to enroll in the CBHI scheme while the distance to the nearest health institution was negatively affecting households enrollment decision. In the same vein, the qualitative analysis also implies that shortage of medicine, limited range of services, and prolonged refunding procedures are critical constraints of the scheme. The findings of this study suggests that the government and stakeholders should implement contemporary strategies to foster the participation of households in the CBHI scheme by raising awareness, building community trust to the scheme, improving administrative procedures, and instigating public-private partnerships to enhance the accessibility of healthcare services and foster health equity within the community thereby reducing households’ health care financial risk.

Introduction

High out-of-pocket health expenses and inadequate health systems are significant challenges for developing countries including Ethiopia (e.g., Asfaw et al., 2022; Mekonen et al., 2018; Noubiap et al., 2014; Wang & Pielemeier, 2012). Strikingly, about 90% of global disease burden prevails in developing countries where the poor suffer worse health and die younger (Gottret & Schieber, 2006; Noubiap et al., 2014; Wang & Pielemeier, 2012). Particularly, impoverished women, elderly and children are the most affected ones. In this regard, the World Health Organization (WHO) advocates for universal healthcare coverage to address healthcare challenges and achieve health equity, although many developing countries continue to struggle to meet the healthcare needs of their populations due to limited resources. Indeed, many developing countries opted for and implemented community-based health insurance as a coping mechanism for reducing the undesirable outcomes of high direct health care service payments, by focusing on poor and marginalized households.

The Ethiopian government has been promoting a community-based health insurance (CBHI) program since 2011, aimed at facilitating the voluntary financing of healthcare for vulnerable populations, including poor rural households, women, children, and individuals working in the informal sectors (EHIA, 2020). As per the CBHI scheme, each district of Ethiopia, or Woreda, has a collective health fund to which eligible members contribute through enrollment on a household basis with voluntary renewal on a yearly basis. The scheme also pools funds from budget allocations by local (district/Woreda) administrations and regional governments, and 25% subsidy from the federal government. The government also covers scheme administrative costs including office space, salaries, and other operational costs. In the North Shoa zone, where this study is conducted, the premium for rural households is affixed based on their economic status, at $10, $20, and $ 23.50 for low, middle, and high income households, respectively, regardless of their core family size (North Shoa Zone CBHI Office Report, 2024). Households are also expected to pay an extra premium of $3 per non-core family member and for children aged 18 years and above.

Administratively, the Ethiopian CBHI scheme is integrated with the health sector and governed by the Health Insurance Board at the woreda level. The board signs a contractual agreement with public health facilities annually. Service users are entitled to utilize all available health services in public facilities with no co-payment required at the time of accessing the service. Members are also eligible for medicines and other services provided in private institutions, as long as they follow the correct procedure. The service charges are reimbursed every 3 months based on a fee-for-service payment method following a medical audit. Kebele leaders and health extension workers are key actors in membership enrollment, renewal, and premium collection at the Kebele level.

Despite the increment the number of enrolees in the scheme over the past decade, the overall participation rate exhibited was still low (about 37%) with considerable dropout rates (Taddesse et al., 2020). Indeed, there has been significant enrollment variation across regions and districts peaking at 57.9% in Amhara and Tigray, in stark contrast to a mere 3% in the Afar region (Moyehodie et al., 2022). In the Amhara Regional state zonal CBHI coverage ranges from the highest (82%) in East Gojjam to the lowest (32%) in Awi zone in the year 2023 (Amhara Region CBHI Report, 2024). This report also revealed that North Shoa Zone, where this study is conducted, performed 64% CBHI coverage with a wider variation across its administrative woredas ranging from the highest (71%) in Ankober and Mojana wedera to the lowest (38%) in Menz Mama (EHIA, 2022). Apart from that, there is also an increase in dropout rate from the scheme by households.

The CBHI enrollment variation across administrative woredas can be associated with households decision-making behavior, which could be driven by several demographic, socioeconomic, institutional, and other factors. To this end, evidences from previous empirical studies -in various countries revealed that membership in CBHI schemes is influenced by key factors including gender, family size, annual income, and occupation (see, e.g., Fite et al., 2021; Geferso & Sharo, 2022; Moyehodie et al., 2022); education level (refer to Moyehodie et al., 2022; Negash et al., 2019); as well as social norms and beliefs, peer influence, household composition, and overall socioeconomic conditions (see e.g., Glazer & Karpati, 2014; Löckenhoff et al., 2011; Riedijk & Harakeh, 2018; Taddesse et al., 2020; Worthy & Maddox, 2012). Additionally, satisfaction with healthcare professionals, perceived quality of healthcare services, family history of illnesses, perceived affordability of health insurance schemes, and anticipated health conditions within the households’ were identified as factors influencing households’ decision to enroll in the health insurance scheme (Fite et al., 2021; Geferso & Sharo, 2022; Ghimire et al., 2023; Mirach et al., 2019; Negash et al., 2019).

Despite the availability of several similar studies, factors affecting households’ participation in the CBHI scheme in the North Shoa Zone, Amhara Region, have not been thoroughly explored. Recently, the CBHI scheme premium determination has been changed from family size-based to income-status basis, which may have a bearing on the participation of households in the scheme. Besides, similar previous study findings often lack consistency likely due to representative subject selection, methods applied, and nature of scheme considered. For instance, many previous studies have utilized datasets that do not adequately represent high and low CBHI enrollment performing woredas in selected study areas. In response to these gaps, this study includes sample rural households from both high and low-enrollment woredas for a comprehensive analysis of the elements that shape household health insurance decisions, considering the Ethiopian government-run community based health insurance using both descriptive and a binary logistic regression model. Therefore, this research singled-out the major factors influencing households’ decision-making to enroll in the government-run CBHI scheme and provide their implications for health equity planning.

Review of Literature

Definition and Concept

Health insurance serves as a mechanism by which individuals who are “insured” can safeguard themselves against the financial repercussions of illness, accidents, or disability (Topan et al., 2024). Community-based health insurance is a resource mobilization model designed to finance access to health care services involving the target population in the design and implementation of the scheme as compared to private health insurance schemes (Ekman, 2004). Commonly, such a scheme has three modalities: community prepayment health organizations, provider-based health insurance, and Government-run health insurance. These CBHI modalities have certain peculiar features in terms of design, community involvement, mobilizing resources, management, and supervision. A government run community-based health insurance (CBHI) is one of the health insurance schemes dominantly applied in low- and middle-income countries that facilitate access to quality health care and to elevate health equity especially in countries where the government and private-based health insurance is minimal (Mladovsky & Mossialos, 2008). It is a modality where community members must prepay for health services and have a pledge agreement requiring the health insurer to cover basic health service costs in exchange for premium payments into a collective fund owned. As a voluntary health insurance scheme, CBHI can be viewed as a decision-making that reflects consumers’ comprehension of health insurance information (Barnes et al., 2015) (Atnafu et al., 2018; Kebede, 2024). High healthcare expenditure, coupled with direct payment for health services, has been a striking feature of the health system in Ethiopia. Due to such situations, the nation has considered the instigation of healthcare financing mechanisms. To this end, Ethiopia implemented a healthcare financing strategy in 1998 to gather additional resources aimed at ensuring sustainable, equitable, and high-quality healthcare service delivery (Taddesse et al., 2020). Particularly, Ethiopia initiated the CBHI scheme by conducting a pilot implementation in a few woredas in 2008. Following the pilot implementation, the Ethiopian government has been promoting a community-based health insurance program (CBHI) to facilitate voluntary healthcare financing for vulnerable populations (EHIA, 2020). Consequently, the scheme has addressed a considerable proportion of the population and improved its management, thereby enhancing the health care service utilization in the country, particularly for poor rural households.

Theoretical Review

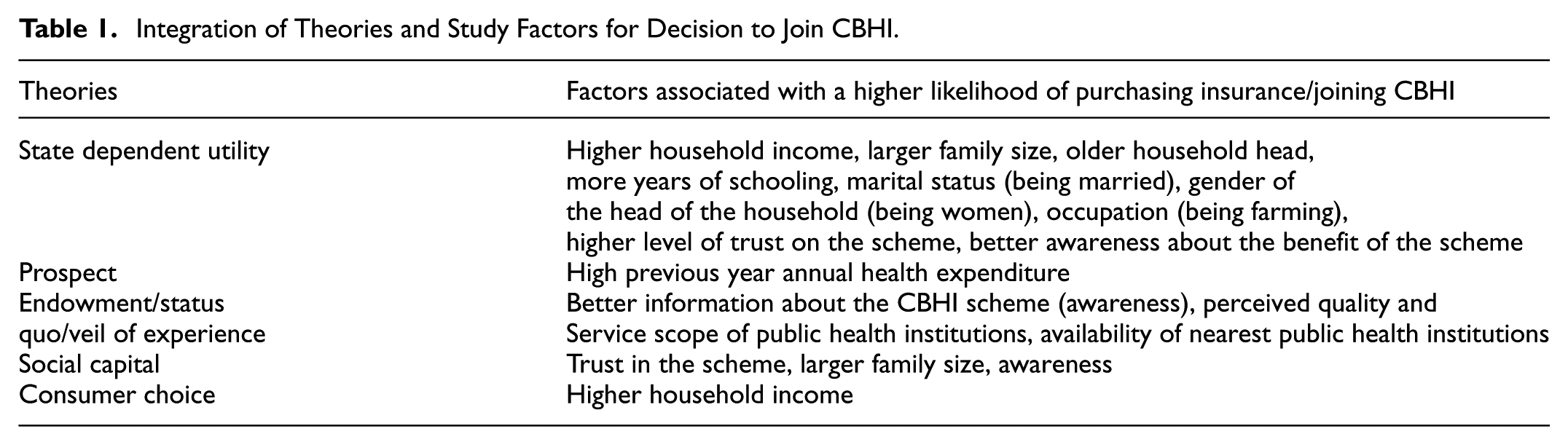

A range of theoretical views exists to facilitate decision-making in the realm of health insurance. These include expected utility theory, state-dependent utility, endowment effect, prospect theory, status quo bias, theories related to trust, social capital, and others.

Expected utility theory implies that the demand for insurance is influenced by individuals’ risk aversion and their desire for income certainty (Harrison & Ng, 2019; Schoemaker, 1982). For instance, households that have experienced health shocks or high medical costs will be more risk-averse and will seek ways like CBHI to reduce their vulnerability to future health-related financial risks. On the other hand, state-dependent utility theory postulates that individuals’ utility and preferences are determined by their current situations like health or socio-economic condition. Hence, if the insurance coverage may not fully compensate for losses if the expected payout from the insurance policy is lower than the actual loss experienced in the event of sickness, households may not decide to enroll in the scheme (Panda et al., 2013; Schneider, 2004; Tenaw, 2017). According to this theory, the degree of risk aversion in relation to the decision to join CBHI is affected by individuals (head of the household in this study) ‘state’, such as income, education, age, gender, occupation, and so on.

The other decision-making theory is prospect theory where the insurance is assessed in a narrow context, isolated from background risks and overall wealth, with the reference point being the level of wealth without insurance coverage. In this theory, insurance can be perceived as a risky gamble: it provides benefits when an accident occurs but yields nothing if no accident happens (Hwang, 2016). An extending of this theory, cumulative prospect theory (CPT) has emerged as a significantly influential model in the realm of risky decision-making. It offers a framework for understanding the risk premium associated with risky lotteries and is regarded by many as an appealing behavioral representation of how individuals make choices under risk (Harrison & Swarthout, 2023). In the context of insurance demand, CPT posits that individuals tend to purchase insurance because they perceive the relatively low probability of experiencing an adverse event, such as illness, as substantial.

Health insurance can also be examined through the lens of the endowment effect, which asserts that individuals tend to value what they own more highly than what they do not possess (Barberis, 2013; Bernstein, 2012; Reb & Connolly, 2007). Another viable perspective is status quo bias (SQB), which indicates that individuals tend to favor their current circumstances due to loss aversion, making them less inclined to pursue change (Do Hwang, 2021; Karl et al., 2019). Moreover, social capital theory views health insurance decisions which posits elevated levels of social capital encourage altruism, enhancing the community’s concern for the well-being of its members (Henning, 2014; Mladovsky & Mossialos, 2008). As per this view, communities with robust social capital are more likely to endorse health insurance initiatives to manage financial risk (Donfouet & Mahieu, 2012). Furthermore, insurance decision can also be viewed from consumer choice perspective, where health insurance is expected to normal good with a positive income elasticity of demand (CITE). For the current study, this theory may associated with the economic status of households.

Although various theories have been proposed to explain health insurance decision-making, the most commonly applicable theories for identifying factors influencing the decision to join the CBHI scheme are concisely integrated with study variables and summarized below (Table 1).

Integration of Theories and Study Factors for Decision to Join CBHI.

Overall, the state-dependent theory of decision-making is considered the underlying basis of the current investigation. Indeed, other theories can also be consulted for the analysis where necessary.

Empirical Review

Numerous studies have focused on identifying factors that influence households’ decisions to purchase health insurance. For instance, Topan et al. (2024) explored that individuals’ decision to participate in a mutual health insurance scheme is likely influenced by individual characteristics, economic considerations, and insurance-related factors. Key empirical findings as bases for the current study from different countries and regions are summarized below.

Table 2 displays previous empirical studies with a particular reference to study focus area, methodology, main findings and gaps to lay down bases of current investigation. In this regard, the socioeconomic, demographic, institutional, and scheme-related factors have been reported as factors influencing people’s decisions to participate in healthcare insurance across various countries. For demographic and socioeconomic factors, studies reported that gender, family size, age, marital status, education, occupation, income, wealth, and health expenditure are decisive (Abdilwohab et al., 2021; Geta et al., 2024; Ibok, 2012; Kibret et al., 2019; Pinilla & López-Valcárcel, 2020; Wan et al., 2020). Similarly, health conditions, frequency of sickness, perceived quality of health services, affordability of the scheme, availability of healthcare institutions, treatment by healthcare providers, and trust in scheme management have been identified as institutional and scheme-related factors. These factors affect households’ decisions to enroll in health insurance schemes (Dror et al., 2016; Eseta & Sinkie, 2022; Geta et al., 2024; Kebede, 2024; Parihar & Ghosh, 2021; Taddesse et al., 2020; Ulbinaite et al., 2013).

Selected Empirical Studies Related to Health Insurance Decision by Economies.

Despite several similar studies, findings reported inconsistent results, likely due to the study area, scheme types, and methodology applied. Even in the same country, like Ethiopia, previous studies reported inconsistent results with respect to the influence of demographic, socioeconomic, institutional, and scheme-related factors. For instance, studies conducted by Minyihun et al. (2019) in Bugna District, Northeast Ethiopia; Ebrahim et al., 2019) in the West Arsi Zone, Oromia; Negash et al. (2019) in Gida Ayna District, Oromia region; and Kibret et al. (2019) in the East Gojjam Zone, Northwest Ethiopia highlight the importance of household income, occupation, education, family dependency level, and health expenditure in influencing households’ healthcare insurance decisions. However, findings from other studies, such as those by Haile et al. (2014) in Benchi Maji Zone, Southwest Ethiopia, reported that income and education are less relevant to households’ healthcare insurance decisions.

Methodologically, previous studies applied various methods of analysis, including multiple linear regressions (Eseta & Sinkie, 2022; Ibok, 2012); binary and multivariate logistic regression (Geta et al., 2024; Taddesse et al., 2020); factor analysis (Parihar & Ghosh, 2021). Besides, some existing studies omitted pertinent factors in their model specification for their investigations. For instance, Parihar and Ghosh (2021) neglected the demographic and socioeconomic factors; Ibok (2012) omitted insurance policy-related factors; Taddesse et al. (2020) did not consider pertinent institutional factors. Moreover, studies also have limitations in terms of sample selection accounting for the difference in the CBHI enrollment performance rate in the same region. Such methodological differences might contribute to the discrepancy in results.

All in all, the inconsistencies about the factors affecting households’ health insurance decision-making open a room for further investigation. Therefore, the current study applied a binary logistic regression with a range of factors from demographic, socioeconomic, institutional, and CBHI scheme-related factors by taking sample households from relatively low and high CBHI enrollment performing woredas in the study area.

Conceptual Framework

Considering the aforementioned theoretical and empirical evidence related to people’s healthcare insurance decisions, this study examined several pertinent variables as potential influences on households’ decisions to enroll in the CBHI scheme. To this end, a household’s membership status in the CBHI scheme serves as the dependent variable, while demographic, socioeconomic, institutional, and CBHI scheme-related factors are considered potential influential factors. The specific variables considered for this study is summarized in the Figure 1.

Conceptual framework of the study.

Based on existing theoretical and empirical evidence, this study hypothesized that several factors impact the household’s decision to enroll in the CBHI scheme. These include the head of household being a woman, being married, being older, being a farmer, having a larger family size, having higher school attainment, higher income, and higher health expenditure. A positive perception of healthcare service quality and adequacy, shorter distance to public health institutions, better awareness of the scheme, and trust in the scheme are also hypothesized to have a positive influence on enrollment to the CBHI scheme in the study area.

Materials and Methods

Research Avenue

The study is restricted to households in the North Shoa zone, Amhara,Ethiopia. With a territorial size of 15,936.13 km2 and roughly 3.5 million people, the North Shoa zone is the sixth most populous in the Amhara region (CSA, 2022). The zone comprises 22 woredas and 9 administrative cities of which 7 woredas identified as food insecure and the Safety-Net programs has been operating in these woredas. This study encompasses four woredas of North Shoa zone, namely, Ankober, Tarmaber, Menz Mama, and Angolela Tera Woredas.

Research Design and Approach

Both quantitative and qualitative research approach were utilized for the fruitfulness of this study. The quantitative research approach was employed to identify major factors affecting household’s decisions to join the CBHI scheme while the qualitative research approach was adopted to solicit detail information about the benefit and challenges of the scheme. These approaches along with descriptive and explanatory research design have also been adopted by similar previous studies (e.g., Bodhisane & Pongpanich, 2019; Haile et al., 2014; Kebede, 2024).

Data Set Information

Data Types and Sources

The study predominantly used primary household-level data for the empirical analysis obtained from 384 sample households through a self-administered questionnaire, which comprised both closed-ended and open-ended questions respective to household’s demographic, socioeconomic, perceived healthcare, CBHI scheme related factors, and other essential pertinent variables. Besides, the study conducted key informant interviews with selected officials from the Ethiopian Health Insurance Agency, as well as zonal and woreda-level healthcare representatives, utilizing semi-structured formats to obtain detailed information for triangulation. This method facilitated the collection of valuable information, including the officials’ opinions, ideas, and experiences concerning community-based health insurance, which in turn shed light on issues related to health insurance and the decision-making processes of households.

Sampling Method and Size

To consider the variation of CBHI enrollment performance across administrative woredas, multi-stage sampling techniques were applied. First, stratified sampling was employed to categorize the administrative woredas into two groups: Woredas under the Safety Net Program and those that do not. Second, within each group, two representative woredas were purposively selected from those having relatively higher and lower CBHI enrollment performance. In fact, it is worthwhile to mention that being a high or low performer in their group doesn’t mean they are high or low performer at zonal level. Consequently, Menz Mama, Angolila Tera, Tarmaber, and Ankober administrative woredas were selected. Third, households were stratified based on their CBHI membership status, and proportional sampling was used to obtain representative households from each group. Finally, the purposive sampling technique was utilized to select sample households from each group.

The sample size for the study was determined by applying Yemane’s (1967) formula as the population of the slected woredas is both large and known with a total of 81,505 households (North Shoa Zone, 2024). The formula applied is:

Where: n = sample size, N = population size of selected woredas, and e = error margin (5% was considered for this study).

Initially, the survey questionnaire was crafted with input obtained from experts, and a pilot test was conducted to check the clarity and validity of the survey instrument. Besides, the finalized version of the survey instrument was translated into the local language “Amharic,” and distributed to sample households.

Ultimately, data were collected from 384 sample households (i.e., 96.5% response rate) including 203 CBHI members and 181 non-members from four purposively selected woredas. This large cross-sectional data and sampling approach facilitated a robust analysis of the targeted population.

Method of Data Analysis

Both descriptive and a binary logistic regression were employed for data analysis. The overall sample profile, characteristics and qualitative reports by respondents analyzed using descriptive analysis. Whereas a binary logistic regression analysis was used to identify key factors influencing households’ health insurance decision-making in the study area.

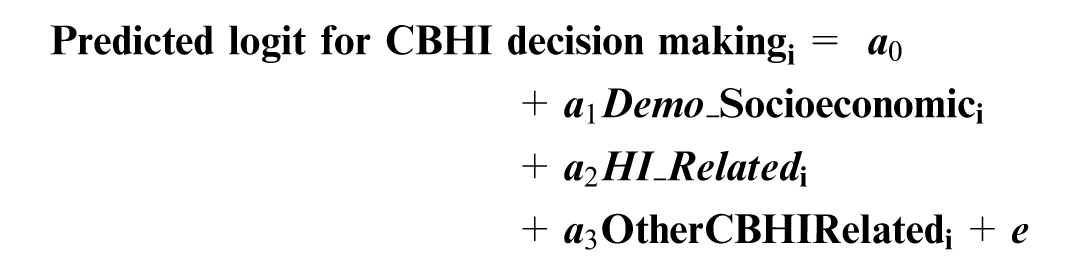

Model Specification

This study applied a binary logistic regression model in which households enrollment status to CBHI scheme serves as dependent variable taking 1 for CBHI member households, and 0 otherwise. Logistic regression is worthwhile for studies where the dependent variable has a choice between two or more discrete as it handles nonlinearity, statistical soundness, and interpretability. Particularly, this study employed a binary logistic regression to identify key factors influencing the household healthcare decision captured by the household’s membership status that has a dichotomous option, that is, member and non-member to the CBHI scheme. This model has also been employed in several prior studies that examined factors influencing individual decisions in several countries (see e.g., Bodhisane & Pongpanich, 2019; Haile et al., 2014; Kebede, 2024). The model specification for this study is:

Where, F = cumulative standard logistic distribution function

The maximum likelihood estimation is used to estimate the parameters of the model and the overall equation of the logistic function for the health insurance decision making is given as:

The

Definitions and Measurements of Variables

Household’s membership status of the CBHI scheme was used as dependent variable for this study. It is constructed as a binary dummy variable where a value of one denotes for member and zero for non-member households to the CBHI scheme. The scheme in Ethiopia allows membership at a household level regardless of their core family size and children under the age of 18 years. This enables to capture to what extent and in which direction that each specified independent variables affect the healthcare decision of households. Similar measurements for variables are applied by previous studies, to mention few, Abdilwohab et al. (2021), Geta et al. (2024), Adebayo et al. (2015), Bodhisane and Pongpanich (2019), Negash et al. (2019), Ebrahim et al. (2019). The study variables along with their definition and measurements’ are provided as below.

Age is a continuous variable that measures the chronological age of the head of the household. The study anticipated that the older the head of the household, the higher the likelihood of the household joining the CBHI scheme, as predicted by the state-dependent theory, which states that older age is perceived to be more prone to health risks.

Gender is a dummy variable that takes 1 for a household headed by a woman and 0 for a household headed by a man. A woman-headed household is expected to have a higher likelihood of being a member of the CBHI scheme than a man-headed household in the study area, as women are more risk-averse comparatively.

Family size is a continuous variable that measures the number of family members in the household. For this study, having a larger household is associated with a higher likelihood of being a member of the CBHI scheme, as a state-dependent theory posits that larger families have more health risk exposure.

Marital Status is a dummy variable that takes 1 for a married household head and 0 otherwise. Being a married household head is expected to have a higher likelihood of joining the scheme, as married individuals have interdependent utility, thereby having large and more diverse health risks.

Occupation is a dummy variable 1 for a farmer household head, and 0 otherwise. In the study area, the majority of respondents are engaged in farming activities, and being a farmer household head is anticipated with a higher likelihood of joining the CBHI scheme, as farmers’ livelihoods depend on their health status and seasons, where joining CBHI provides higher utility in vulnerable states.

Education is a continuous variable that measures the years of schooling by the head of the household. More school years attained by the head of the household are expected for joining the CBHI scheme, as education enhances the analysis of insurance benefits and utilities at different health statuses.

Household’s estimated annual net income: it is a continuous variable that measures the difference between estimated annual income and estimated annual expenditure in Ethiopian Birr. Households that have a higher estimated annual net income are anticipated to have a higher probability of joining the CBHI scheme, as households would have the chance to afford scheme premiums.

Household’s annual health care expenditure in the past year is a continuous variable that measures the household’s previous year’s health expenditure in Ethiopian Birr. The higher the previous year’s health expenditure by a household, the higher the likelihood of joining CBHI, as it might imply the household has more health risks. This can capture a household’s health condition, including illness frequency and the existence of chronic illness within the household.

Distance to the nearest health institutions is a continuous variable that measures the estimated distance of the nearest public health institution for a household in kilometers. The longer the distance, the lower the likelihood of the household joining the scheme, as access to and health service utilization are limited.

Perception toward the adequacy and service quality of public health institutions is a dummy variable that takes 1 for perceiving “Good” and 0 for “Not-Good” by the head of the household. Household heads who perceive “Good” for the health service quality and adequacy are more likely to join the CBHI scheme than their counterparts.

Awareness about the benefit of the CBHI scheme is a dummy variable that takes 1 for being “Aware” and 0 for “Not-Aware” about the benefits of the CBHI scheme by the head of the household. Informed head of households about the scheme are more likely to join the scheme as they can better anticipate how the scheme benefits them in adverse health states.

Trust in the management of the CBHI scheme is a dummy variable that takes 1 for having trust in the scheme management by the head of the household and 0 otherwise. The head of the household that have trust in the scheme management is anticipated with a higher likelihood for joining the scheme, as households believe the scheme will deliver service in their illness state, they will join the scheme.

Results

Study’s sample characteristics, pre and post estimation test, and results obtained from binary logistic regression are presented below.

Sample Characteristics and Diagnostic Tests

The information obtained from 384 sample households are characterized based on demographic, socioeconomic, institutional, and CBHI scheme related factors are presented in Table 3. Diagnostic statistical tests including pre-test (test of correlation and multi-collinearity) and post-test (Hosmer–Lemeshow test) were conducted. Test of Pearson correlation revealed that only the marital status (

Summary of Study Sample Characteristics, and Pearson Chi-Square Test.

Source. Authors own computation (2024).

Note.***p < 0.01 and **p < 0.05, indicating statistically significant correlations at 1% and 5% significance level, respectively. Italicized P-values represents a statistically significant association between independent variable with CBHI membership status at 1% or 5% significance level.

Regarding the post estimation, the goodness of fit of the model was assessed using Hosmer–Lemeshow test at 10 quantiles of estimated probabilities. According to the test, the value and p-value are found to be

Results From Binary Logistic Regression

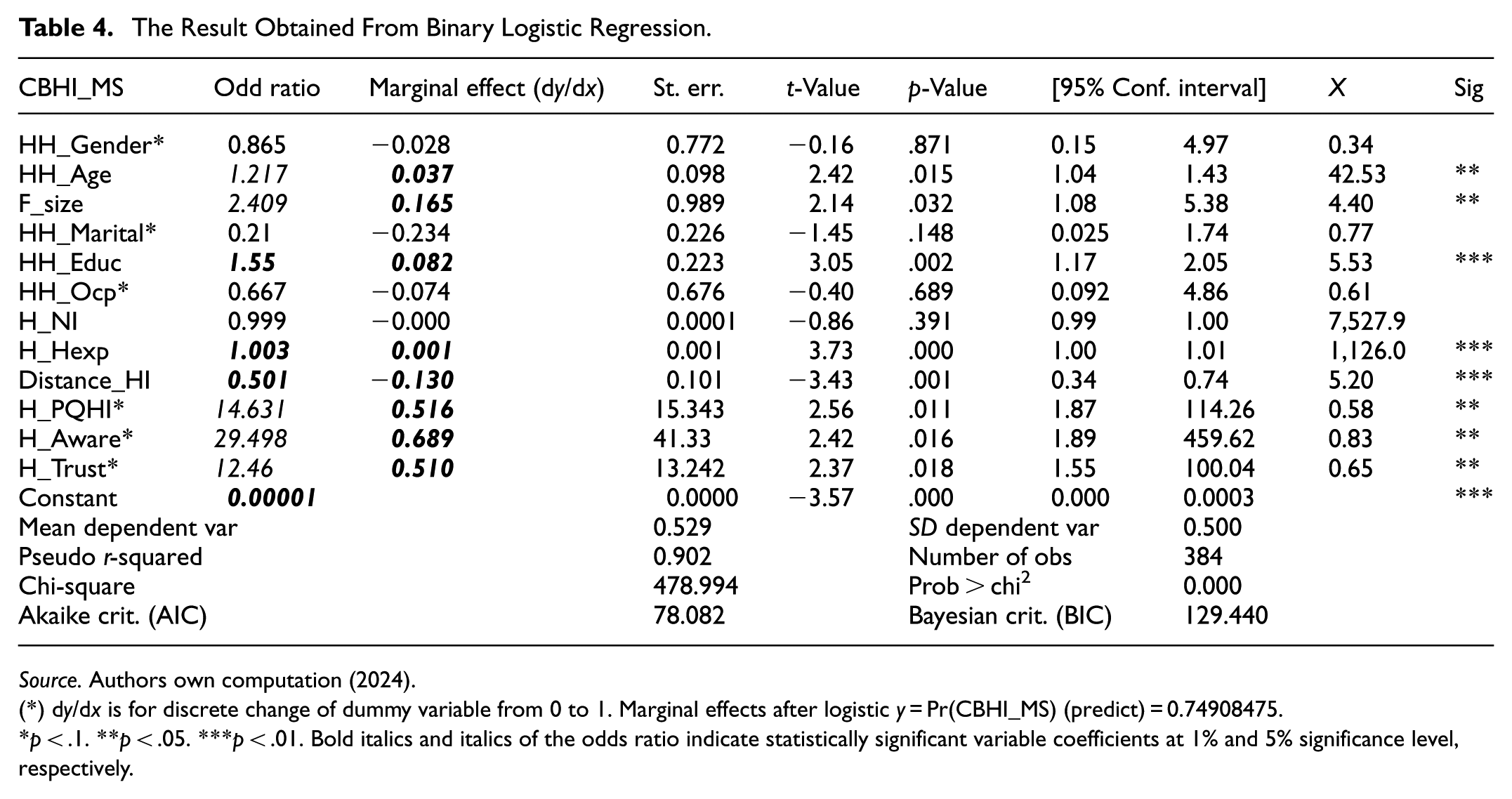

The empirical result obtained from binary logistic regression model is presented in the Table 4. The marginal effect (dy/dx) at mean value of each independent variable (X) in addition to the odd ratio is presented to directly interpret the effect of each specified factor on the decision of households to the CBHI scheme.

The Result Obtained From Binary Logistic Regression.

Source. Authors own computation (2024).

(*) dy/dx is for discrete change of dummy variable from 0 to 1. Marginal effects after logistic y = Pr(CBHI_MS) (predict) = 0.74908475.

p < .1. **p < .05. ***p < .01. Bold italics and italics of the odds ratio indicate statistically significant variable coefficients at 1% and 5% significance level, respectively.

From the model summary, in Table 4, it can be observed that about 90.2% of the variation in CBHI membership status is attributed to the factors in the model. The test statistics from likelihood ratio test (chi-square = 478.994 with p = .000) is also suggest a good fit of the model. Besides, having a value of 0.500 of the standard deviation of the dependent variables indicates its balanced binary outcome with equal distribution of the dependent values. Moreover, the Akaki Information Criterion (AIC) as well as Bayesian Information Criterion (BIC) also affirms the model fit is good. Based on logistic regression, 8 out of 12 specified variables are found statistically significant in terms of their effect on households’ decision to participate in the CBHI scheme in the study area.

Pertinent to the demographic factors, the effects of variables are presented as follows: an additional age of the head of the household, on average, increases the likelihood of being member of CBHI by 3.7% (OR = 1.217, p = .015). This implies that the older the head of the households the higher the probability to join the CBHI scheme likely associated with heightened responsibility, awareness, economic power, and long-term anticipations. The study has also found significant positive effect of family size on CBHI membership with a marginal effect of 16.5% (OR = 2.409, p = .032). This indicates that households that have a larger family member have a higher probability to decide enrolling in CBHI scheme. Gender and marital status were found statistically insignificant in explaining the membership status of the CBHI scheme in the study area.

Pertinent to the socio-economic factors, an additional year of schooling by the head of the households, on average, increases the likelihood of households to join the CBHI scheme by 8.2% (OR = 1.55, p = .002). Healthcare expenditure wise, an increase in households’ previous year annual health expenditure by 1 ETB enhances the likelihood to be a member by an average effect of 0.1% (OR = 1.003, p = .000). However, the occupation and annual estimated income were found statistically insignificant in explaining the household’s decision to join the CBHI scheme in the study area.

With respect to health institutions related factors, households residing an additional kilo meter far from public healthcare institutions are found less likely to be members in the CBHI scheme by 13% (OR = 0.501, p = .001). This could be due to households’ perception of a lower chance of visiting a healthcare institution, high transportation costs, awareness barriers, lower social capital network, and opportunity costs. Besides, household’s perceptions toward public health service quality and adequacy is found as a significant factor in influencing healthcare insurance decision while it has a wider confidence interval (OR = 14.631, p = .011). Respondents imply that the scope of public health institutions should be improved as they sometimes face to directly pay and access health services from private health institutions.

One female household head who participated in the study said:

The CBHI scheme is important for low-income people like me; however, we scheme users face financial reimbursement problems when we access services and medicine that are not available in the public health institutions. I look for a bit of improvement in the scheme related to reimbursement and other similar issues.

Regarding the CBHI scheme-related factors, households that are aware about the benefit of the CBHI scheme are found 68.9% more likely to be members than those households that do not have (OR = 29.5, p = .016). In the same vein, households that have trust in the management of the CBHI scheme are also 51% more likely to be enrolled in the CBHI scheme than those households that do not trust (OR = 12.46, p = .018). Indeed, in both variables, results display wider confidence intervals that indicate prevalence of instability. In connection with this, qualitative information obtained from key informant interview indicates that household’s silicate information about the CBHI scheme when they face health problems.

Though we exert a lot of effort to aware awareness about the CBHI scheme benefits through different social networks and events … many rural households come to join the scheme immediately after one or more family members face a chronic illness … Some households are also keen to renew their membership if their family members frequently face health problem. (in-depth interview with kebele level health extension workers)

The qualitative data also substantiated the findings obtained from regression results as the vast majority of respondents apprised that the availability and scope of healthcare services by public healthcare institutions, awareness about the benefit of the scheme, literacy of households, and trust in the scheme are relevant to decide membership in CBHI scheme. They also reported that improve access to essential medicines, scope of services, and ease of administrative processes for service utilization are the areas where the government and stakeholders need to improve the scheme thereby fostering participation of households.

Discussion

This study obtained several statistically significant results, for which necessary discussions are provided in line with the prior anticipations in the research framework.

The study proposed that the advancement of age is likely to increase the likelihood of membership in the CBHI, and this study has found the same. This finding could be attributed to several older household heads’ cases, including their higher health needs and expenses, membership can allow them to have frequent preventive checks, their higher trust in community schemes, their relatively larger family size, and they find the scheme a less expensive coverage, and some government incentives for older households to enroll in the scheme. In particular, in this study area, older families joining the CBHI scheme are highly associated with their exposure to health risks which make them to demand more health services utilization (Acharya et al., 2019). The finding is consistent with previous studies conducted in different areas (e.g., Abdilwohab et al., 2021). In fact, there is empirical evidence that is inconsistent with this finding. Kebede (2024) found that the age of the head of the household negatively influences households’ CBHI membership in peri-urban areas of Gondar and Bodhisane and Pongpanich (2019) in Laos, who found aging has no significant impact on households’ health insurance decisions.

As anticipated, the current study has found that larger households are more likely to join CBHI, which could be associated with several issues. For instance, the larger the size of the household, the greater the chance of health risks triggering healthcare demands that ultimately increase the likelihood of participating in the CBHI scheme to reduce their financial risks (Ranson, 2002). Larger households prefer insurance scheme that cover all family members like CBHI, and thereby significantly reduce catastrophic health expenditure. The result can also be viewed from diverse income sources of large households that allow them to afford premiums (Conde et al., 2022; Schrecker & Labonte, 2004), and wider social networks and collective decision-making (Fink et al., 2013; Mladovsky, 2014; Robyn et al., 2012).

Respective to education, this study anticipated that a higher education level of the head of the household increases the likelihood of households joining CBHI, and a consistent result was obtained, which could have alternative explanations. This finding is likely attributed to the role of education on health literacy, awareness about the benefit of the CBHI scheme, better understanding of long-term benefits and risk management (Buchmueller et al., 2016; Gertler & Wolfe, 2006; Moyehodie et al., 2022; Negash et al., 2019); strong social networks and community engagement; and higher risk aversion and better decision making (Mladovsky, 2014; Robyn et al., 2012). It may also be associated with better financial literacy, and CBHI is a less costly option to have coverage for family members, a positive attitude toward prevention, and regular care.

Pertinent to health expenditure, a household with higher previous annual health expenditure was found to have a higher likelihood of joining the CBHI scheme, which could be attributed to several reasons. This could be associated with households that have incurred catastrophic health expenditures in the past, likely to develop more risk-averse behavior that demands being a member to avoid future healthcare financial risks. In fact, higher previous annual health expenditure can imply household health status, particularly if they have experienced frequent illness in one or more family members. This result also has empirical support as reported by Mills et al. (2012) in Ghana, South Africa, and Tanzania Xu et al. (2007) in multi-country; Diop et al. (2018) in Senegal.

The distance to public health institutions by households was found to be significant for joining the CBHI scheme in the study area. This could be due to households’ perception of a lower chance of visiting a healthcare institution; high transportation cost, and the time and effort for traveling outweigh the benefits, awareness barriers, lower social capital network, and opportunity costs.

Households’ awareness of the benefit of CBHI was found to be significant in influencing the decision to join the CBHI scheme. Hence, better awareness leads to the understanding of CBHI’s role in terms of protection from high out-pocket health expenditure; awareness enhances the trust in the scheme’s credibility and effectiveness, better assessment to make enrollment decision, and higher perceived financial protection.

The study has found that households with a higher level of trust in the scheme are more likely to join CBHI. The higher trust in the scheme is attributed to several factors, including the accessibility of health services as promised, the fair allocation of premiums for users’ benefits, reduced system fraud, trust stemming from community leaders, and peer endorsements. These results are consistent with the findings of (e.g., Dror et al., 2016; Kebede, 2024).

Study Limitation and Future Research Directions

The study was delimited to investigate factors influencing households’ health insurance decision-making taking Community-Based Health Insurance in four selected Woredas of North Shoa Zone, Amhara, Ethiopia. Future researchers can explore factors that influence households’ decision-making behavior by focusing on other types of insurance such as life insurance, property insurance, and others. Besides, the researcher can also apply an extensive qualitative research approach with additional explanatory variables such as household participation on different local social networks, contact with health extension experts, and peer influence as it provides a more detailed subject analysis. Moreover, the subsequent studies could validate the finding at the individual level or using multi-level models. Furthermore, future study can also be conducted in a wider geographical scope at a regional or national level.

Conclusion and Recommendation

Factors including age and education of the head of the household, family size and previous year households’ health expenditure were the key socioeconomic factors that drive households CBHI enrollment in the study area. While gender, marital status, and occupation of the head of the households and annual net income of the household were found statistically insignificant in influencing household’s decision to participate in the CBHI scheme in the study area.

Regarding the health institution and CBHI scheme-related factors, distance to the nearest public health institution, household’s perceived health care service quality and adequacy, awareness about the benefit of the CBHI scheme, and trust in the management of the scheme are the pertinent factors in determining the decision of households to participate in the CBHI scheme of the study area. The findings underscore that demographic, socioeconomic, health institution-related aspects, and scheme design and operation issues are crucial to improving the coverage of CBHI household membership.

The finding of this study has numerous implications for the government, community, and other stakeholders. In this respect, the government needs to enhance the basic literacy of rural households, improve scheme administration efficiency, and improve health institutions’ service quality and adequacy. To this end, efficiency in financial reimbursement, offering flexible premium payment options, and consideration of incentives for initial enrollment could be relevant. Besides, due attention should be given to enhance community awareness about the benefits of CBHI through campaigns, community meetings, local media, and other possible options. Likewise, the trust in the scheme needs to be strengthened by working with stakeholders. Trustworthiness of the CBHI scheme can be enhanced by effectively communicating the fund management, involving respected community leaders in promotion, ensuring quality healthcare services for scheme users, and addressing grievances immediately could be helpful. Overall, by implementing suggested and other viable strategies, it is necessary to improve the coverage of CBHI household membership to enhance health care services and reduce financial risks.

Footnotes

Acknowledgements

We would like to express our gratitude to the officials and experts of the North Shoa zone, as well as the participating households in the Ankober, Tarmaber, Menz Mama, and Angolela Tera Woredas. Their invaluable support during the data collection process and the validity of their responses significantly contributed to the fruitfullness of the study.

Ethical Considerations

This study obtained letter of ethical clearance from Debre Berhan University Ethical Approval Committee on March 2024.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The data for this study can be available upon reasonable request.