Abstract

The study experimentally investigated the impact of financial literacy confidence (FLC) on financial risk preference confidence (FRPC) constructed from objective and subjective measures of financial literacy and risk preferences. Seven hundred seventy-two responses from 193 subjects were analyzed using the Random Effect Panel Regression (REPR) technique. The study reveals that FLC significantly impacts FRPC differently for overconfident and underconfident individuals. Specifically, the results show that an increase in FLC increases FRPC for overconfident individuals but decreases FRPC for underconfident individuals. Hierarchical Random Effect Panel regressions confirm that financial literacy residuals significantly impact risk preference residuals. The findings entail that cognitive abilities errors on subjective and objective measures of financial literacy correlate with risk preference errors on subjective and objective risk preference measures. Interestingly, the results show that increased financial literacy residuals lead to reduced risk preference residuals for individuals with high financial literacy. The results suggest that individuals with higher financial literacy can better align their subjective and objective measures of risk preferences. The study findings help to explain how FLC shapes the financial behavior of individuals making risky financial choices. The policy implications of these findings are that investing in financial literacy programs can assist individuals in making well-informed investment or saving decisions and can better manage financial risks.

Plain language summary

The study experimentally investigated the impact of financial literacy confidence (FLC) on financial risk preference confidence (FRPC) constructed from objective and subjective measures of financial literacy and risk preferences. Our investigation shows that FLC has a significant impact on FRPC, which is different for overconfident and underconfident individuals. Specifically, the results show that an increase in FLC increases FRPC for overconfident individuals but decreases FRPC for underconfident individuals. Further analysis reveals that financial literacy errors on subjective and objective measures of financial literacy correlate with risk preference errors on subjective and objective risk preference measures. Interestingly, the results show that for individuals with high financial literacy, an increase in financial literacy residuals leads to a reduction in risk preference residuals. This suggests that individuals with higher financial literacy better understand their subjective and objective risk preference standing and can manage financial risk better. The study helps to explain the impact of FLC on FRPC, which is a crucial behavior in financial markets. The policy implications of these findings are that acquiring financial literacy can assist individuals in making saving or investment decisions and can better manage financial risks. The study’s limitations are that it uses university students who may not be a true representation of people in society. Although the use of experiments can help researchers to understand the processes and behavior that is difficult to obtain in a natural environment, the instruments used to collect the data can fail to mimic a natural environment.

Keywords

Introduction

Having less doubt in one self’s financial knowledge is a definition of financial literacy confidence (FLC). Financial literacy confidence is a critical component of financial decision-making. Little financial knowledge, compounded by overconfidence, impairs financial decision-making (Tokar Asaad, 2015). Financial literacy involves making financial decisions, which are critical for improving welfare. Financial decisions also involve making risky choices with probabilities of losses or gains (Hilbert et al., 2022). Further, financial risk preference confidence (FRPC) is the trust in one self’s ability to assume financial risk. Financial risk preference confidence or tolerance is the maximum degree of uncertainty or risk someone is willing to accept when making a financial decision (Roszkowski et al., 2009). Evidence shows that risk preferences are generally stable over time (Frey et al., 2017). Other studies found that risk preferences change due to context, cognitive abilities, and framing effect (Pedroni et al., 2017).

Measuring financial literacy confidence and financial risk preference confidence in a natural environment set-up has always posed a challenge to researchers. Studies have either used subjective questions with Likert scales in surveys or fused subjective and objective instruments to measure confidence (Bonsang & Dohmen, 2015; Fisher & Yao, 2017; Mudzingiri & Koumba, 2021). The divergence between objective and subjective measures of financial literacy or other domain responses represents less or over confidence (Chu et al., 2017; K. T. Kim et al., 2020). Literature shows that being financially overconfident drives individuals to act on financial decisions, while being less confident results in inaction (Yeh & Ling, 2022). There is a need to investigate whether being confident in one domain influences confidence in the other sphere of confidence. Experimental data can go a long way in explaining the behavioral outcomes of FLC on FRPC in financial decision-making, such as investment and saving.

In the study, subjects completed a financial literacy test and a subjective question that ranked their financial literacy ability on a Likert scale (Kaiser et al., 2022). Subjects also completed four incentivized risk preference tasks and a subjective risk preference question that ranked their willingness to take the financial risk on a Likert scale (Andersen et al., 2008; Lusardi & Mitchell, 2011). The study experimentally investigated the effect of FLC (the gap between the subjective ranking of one’s financial literacy ability and the measured financial literacy ability) on FRPC (the gap between the subjective ranking of willingness to take financial risk and the elicited financial risk preference choices from multiple price list (MPL) tasks). The study further applied the hierarchical random effect panel regression technique to investigate the relationship between financial literacy residuals and risk preference residuals (K. T. Kim et al., 2020). A positive gap between the subjective ranking of financial literacy ability or risk preference choices and the objective measure of financial literacy ability or risk preference choices shows overconfidence among subjects, while a negative gap shows less or under-confidence (Barber & Odean, 2001; Kramer, 2016).

Over or under-confidence in financial literacy can create cognitive biases and heuristics in financial decision-making (Jackson et al., 2016). Overconfidence generates disagreements concerning asset fundamentals among trading agents in financial markets. The ultimate result is agents paying prices that exceed their future return on an asset in anticipation that they will find a buyer willing to pay even higher price (Scheinkman & Xiong, 2003). The act has become a significant source of asset bubbles that breed global financial crises. Global financial crises, for example, the 2007 to 2008 financial crisis, resulted in the loss of jobs, trade, and assets, among others (Johnstone et al., 2019). This study investigates financial behavior believed to propagate the rise of financial crises. It is critical to investigate whether confidence in financial literacy induce people’s confidence in making financial risk choices as a way of understanding financial behavior of economic agents in financial markets (Dermesrobian, 2023).

On the other hand, under confidence in financial risk preferences can generate sub-optimal returns on investments and savings in a context where an individual thrives to maximize benefits (Kramer, 2016). Disposing assets at meager prices to people who will sell them at some exorbitant profits is an excellent example of a sub-optimal return on investment. Economic conditions such as the overall state of the economy, inflation, and interest can influence FRPC. Wealthier people with stable incomes and the capacity to invest are more likely to be confident in taking financial risks (Rios & Sahinidis, 2010). Financial literacy, experience, goals, risk perceptions, fear, and greediness have a significant bearing on the FRPC of people (Ahmad & Shah, 2020). An investigation of the effect of FLC on FRPC can further broaden the literature scope.

A study on the impact of FLC on FRPC can assist in explaining the role of cognitive and behavioral factors that influence financial decision-making and behavior in general. Evidence shows that making gainfully financially risky decisions requires using cognitive abilities such as financial literacy (Ling et al., 2023). Suggesting financial literacy motivates individuals to believe in their ability to manage financial risk beneficially. Financial literacy ensures financial inclusivity (Desai et al., 2023). Financial literacy can reduce poverty among individuals through participation in entrepreneurship and the ability to choose lending channels (S. Wang et al., 2022). In addition, financial literacy can improve food security among low-income people (Carman & Zamarro, 2016). Studies show that the nexus between financial literacy, FLC, FRPC, risk tolerance, financial behavior, financial knowledge, and individual characteristics remains to be determined (Atkinson et al., 2007; Hermansson & Jonsson, 2021). FRPC can have a direct bearing on an individual’s financial behavior since knowledge, context, attitudes, norms, perceptions, macro or structural factors, and other individual characteristics (micro-factors) interact to shape an individual’s financial behavior (Ajzen, 2011; Bergner, 2011; García, 2013). FRPC can, therefore, ultimately explain an individual’s financial behavior since it is a fusion of financial attitudes and perceptions.

The study uses a micro-factors framework to investigate how an individual’s measured financial literacy and perceived financial literacy interact with the gap between elicited risk preferences and perceived willingness to take financial risk choices. Given their financial literacy confidence, the findings can help explain the financial behavior of individuals making financially risky decisions. Moreover, there is a need to investigate whether the misalignment of responses from subjective and objective measures of financial literacy and financial risk preferences correlate. Findings from such a study can provide policymakers with information to design financial education programs catering to individuals with different risk preferences and financial literacy (Worthington, 2013). Financial institutions can also use findings from the research to design financial products and services catering to individuals with different risk preferences, financial literacy, and confidence levels (Königsheim et al., 2017). Overall, this study provided valuable insights into the relationship between FLC, FRPC, risk preferences, and financial literacy residuals, which can inform policy and practice in the financial sector.

The study findings show that FLC significantly impacts FRPC for all aggregated categories of subjects. An increase in FLC significantly increases FRPC, and these results affect financial decision-making. The results show that FLC breeds FRPC. Reducing the gap between perceived and objective financial literacy reduces the FRPC gap. Hierarchical random effect panel regressions further confirm that financial literacy residuals significantly impact risk preferences residuals, meaning the misalignment of individual responses on subjective and objective measures of financial literacy and risk preferences correlate. The results further show that for individuals with high financial literacy, an increase in financial literacy residuals leads to a reduction in risk preference residuals, suggesting that individuals with higher financial literacy are better able to align their subjective risk preferences with their objective measures of risk preferences. They show that subjects with higher financial literacy can better understand and manage financial risk.

The equivalence of subjective and objective instruments used to measure financial literacy and risk preferences debate has been raging for some time. Self-assessment or perceived and objective measures of financial literacy are associated with financial behavior (Allgood & Walstad, 2016). Conversely, a weak correlation between objective and subjective measures of financial literacy and risk preference was also concluded in other studies (Mudzingiri & Koumba, 2021; Parker et al., 2012; Parker & Stone, 2014). The uniqueness of this study is that it goes beyond analyzing the correlation between subjective and objective responses collected by instruments used to measure financial literacy and risk preferences. It seeks to investigate the effect of FLC on FRPC and the relationship between risk preferences residuals (errors) and financial literacy residuals (errors). Studies that examined the effect of FLC on FRPC are scarce. By exploring the relationship between FLC and FRPC, the study can assist in explaining the behavioral biases that affect individuals’ financial decision-making (Adil et al., 2022).

Literature Review

Expected Utility Theory, Self-Efficacy, and Framing Effect

Three behavioral finance theories inform this study: the expected utility theory, the self-efficacy, and the framing effect (Mi & Xu, 2023; Vaala et al., 2022). Firstly, the expected utility posits that individuals make rational decisions where they weigh risk and return guided by their financial literacy (Crispino et al., 2023). However, it is sometimes complicated to make rational decisions in a world riddled with information asymmetry and market imperfections (Ma et al., 2023). Imperfect information, such as low financial literacy, can impair and bias the FRPC of an individual. Secondly, self-efficacy is a psychological perspective that suggests that financial literacy motivates individuals to believe their ability to handle financial risk matters to their benefit (Liu & Zhang, 2021). Contrary evidence suggests that not all financially literate people fully utilize their financial literacy abilities (van Rooij et al., 2011). Issues to do with confidence levels could affect one’s ability to take advantage of their financial literacy prowess fully. Lastly, financial literacy can influence risk preference decisions based on how information is presented to subjects (the framing effect) (Pedroni et al., 2017; Ventre et al., 2023). How gains and losses are structured in a financial risk venture such as an investment can induce confidence. For example, abnormal profits and losses on assets can impair FLC and FRPC.

The study considers the influence of the three theories on the research outcomes. The relationship between cognitive abilities such as FLC and FRPC needs further investigation as it can answer the financial markets investment behavior puzzle where aspects of over or under-confidence are prevalent. Errors generated by lower cognitive abilities have been mistaken to represent risk aversion or risk-seeking behavior (Mechera-Ostrovsky et al., 2022). Deviations between subjective and objective measures of financial literacy and risk preferences have been attributed to variations in the cognitive abilities of individuals (Dohmen et al., 2018). Factually, the cognitive abilities of individuals differ from one person to another, making it essential to compare the general behavior of people by financial literacy level. Acquiring financial literacy is made possible by an individual’s underlying cognitive abilities (Muñoz-Murillo et al., 2020). This study seeks to join the debate on the relationship between cognitive abilities and risk preference choices. Cognitive abilities influence subjects to tremble, exhibiting random choice behavior (König-Kersting et al., 2023). In summary, our investigation is cognizant of theoretical contradictions that can bias the outcome of the research findings.

Financial Literacy Confidence and Financial Risk Preference Confidence

A combination of subjective and objective measures of financial literacy or financial risk preferences can assist researchers in understanding cases of less confidence or over-confidence and how financial decisions are formulated (Marinelli et al., 2017). Evidence shows that being overconfident is associated with making risky decisions (Guiso & Jappelli, 2020; Murad et al., 2016). Hermansson and Jonsson (2021) concluded that financial literacy is related to lower risk tolerance levels. They suggest that financially literate people tend to avoid investing in risk assets probably due to their knowledge and understanding of risk. Confidence is associated with subjective or perceived financial literacy and willingness to invest in risk assets such as “Ponzi schemes” (Aren & Nayman Hamamci, 2022). Showing confidence plays a vital role when people invest in risky assets. Evidence also shows that objective financial literacy and confidence significantly increase the probability of holding risk assets by investors (Cupák et al., 2020). Lack of investor self-confidence and low levels of financial literacy can hinder people from investing in high-risk and high-return assets, leading to sub-optimal welfare outcomes.

Aspects of financial literacy, confidence, and risk preference, therefore, drive investment and saving decisions. Confidence can vary multi-dimensionally depending on the context, micro factors (personal characteristics), structural or macro factors (economic, political, and social factors), and psychological factors (Kay & Shipman, 2015). The assertion also suggests that FLC and FRPC can or cannot vary in various situations. Confidence accompanied by objective financial literacy is crucial in financial decision-making. Overconfident individuals usually invest in risk assets such as “Ponzi schemes” and cryptocurrencies, which have a high risk of fraud and losses. Conversely, less confident people are less likely to invest in risky assets, leading to sub-optimal returns (Aristei & Gallo, 2021).

In a broad sense, confidence levels can differ across gender, with females being confident in some domains while males are confident in other specialties (Cooke-Simpson & Voyer, 2007; Rivers et al., 2021). Evidence shows that confidence can differ by geographical location, for example, residing in urban or rural areas (Agus Kurniawan et al., 2020). Lovatt (2011) found that dance confidence differs across gender and age. The bulk of articles reviewed analyzed the effect of confidence on financial literacy or knowledge, risk preferences, risk tolerance, emotional intelligence, risk assets investment, culture, financial advice seeking, and financial behavior among others (Ahmad & Shah, 2020; Aristei & Gallo, 2021; Bertella et al., 2014; Kramer, 2016; Marinelli et al., 2017; Mudzingiri et al., 2018; Yeh & Ling, 2022). This study is an addition to the current literature. It explores the effect of FLC on FRPC to investigate if confidence in cognitive abilities influences confidence in financial behavior.

Data and Method

The study uses data from a purposive and convenient sample of 193 students enrolled in the Bachelor of Commerce degree in 2016 at the University of Free State in South Africa. The subjects completed a questionnaire that collected their demographic characteristics, subjective financial literacy ranking, and subject risk preference ranking responses. The subjects completed four risk preference tasks and a 30-question financial literacy test (see Mudzingiri & Koumba, 2021). An invitation to participate in the study was sent through blackboard, an online learning platform. Participation in the study was voluntary, and subjects completed a consent form before participating. The study targeted 400 students, and only 219 students participated. Of these, 193 subjects had complete and usable information for the study. 53% of the subjects were female, the mean age was 22 years, 69% resided in urban areas, the average household size was five members, and the average monthly income spent by the subject was R1 459 (see Table 1).

Summary Statistics of the Data Used in the Study.

To understand the effect of FLC on FRPC, we first run a random effect panel regression (REPR) before splitting the data across the less confident and overconfident (Barkat et al., 2023). We further analyzed data of subjects that were split across financial risk preference less/under-confident (risk confidence deviations < 0) and financial risk preference over-confident (risk confidence deviations > 0) (see Figure 2). The analysis is split across gender (male or female) and financial literacy (low level of financial literacy [lfl] or high level of financial literacy [hfl]). All subjects that scored below average in the financial literacy test are categorized as having low financial literacy. A random effect panel regression model is specified as follows (van Praag, 2021):

The variable

The research ran a hierarchical random effect panel regression model on risk preference choices and financial literacy scores residuals (Lewis, 2007). The analysis involves fitting a regression for each separate outcome. Hierarchical regressions usually provide results with improved precision with less extreme values (Richardson et al., 2015). The approach is implemented on the assumption that risk preference choice errors correlate with individual cognitive abilities (Mechera-Ostrovsky et al., 2022). The risk preference residuals were predicted from the following regression model.

All other variables in the equation are the same as those in equation (1), except

The Dependent Variable

The measure of financial risk preference confidence (FRPC) in the random effect panel regression is calculated using a subjective risk preference questionnaire and elicited safe choices from multiple price list (MPL) risk preference tasks (Andersen et al., 2008; Lusardi & Mitchell, 2014). The dependent variable in the hierarchical random effect panel regression models is the predicted residuals (errors) of risk preferences (FRPR) (see equations (2) and (4) above) (Richardson et al., 2015).

Subjective Risk Preference Question

The research adopted the 10 Likert scale subjective risk preference question from the financial capability questionnaire (Jaspersen et al., 2020; Lusardi & Mitchell, 2014). The subjects responded to the question below.

When thinking of your financial investments, how willing are you to take risks? Please use a 10-point scale, where 1 means “Not At All Willing” and 10 means “Very willing.”

The subjects completed the question before completing four incentivized MPL risk preference tasks.

MPL Risk Preference Task (Reveal Risk Preferences or Elicited (Objective) Risk Preferences)

The subjects completed four typical MPL risk preference tasks (see Table 2) with different payoffs. For further clarity on the procedure followed (see Mudzingiri & Koumba, 2021). 772 (193 subjects × 4 games) data points were collected.

Typical Payoff Matrix for the Risk Preference Experiments—Task 1.

The four MPL risk preference tasks completed by the subjects had varied lottery pay-offs (see Supplementary). In the MPL risk preference tasks, safe choices are lottery A selections. Selecting a few of the lottery A choice shows that one is risk-loving. Lottery A is considered safe because the pay-off is not widely spread (probability of winning R50 or R60), whereas Lottery B is considered risky (probability of winning R100 or R25). Rational subjects can apply the expected utility theory to complete risk preference tasks (Crispino et al., 2023). Ten percent of the participants were paid the actual value of their choices, as proposed by Andersen et al. (2008). The responses from the subjective risk preference ranking and the elicited MPL risk preference choices were reverse-coded to ensure a more straightforward comparison between responses from the subjective risk preference questions. The variable FRPC is calculated as the difference between subjective risk preference response and MPL risk preference elicited safe choices. The absolute financial risk preference confidence (AFRPC) value is the square of the FRPC variable. As explained in equation (2) above, the financial risk preference residuals (FRPR) were predicted from a regression of objective and subjective measures of risk preferences.

The Independent Variable

The variables of interest in this study are financial literacy confidence (FLC) and financial literacy residual (FLR). The FLC was constructed by calculating the difference between a seven-Likert scale subjective financial literacy question response and a 30-question financial literacy test adopted from dollar sense, jump start, and National financial capability surveys (LaBorde & Mottner, 2013; Lusardi & Mitchell, 2014; Mandell, 2008; Mudzingiri & Koumba, 2021). FLR was predicted from the regression analysis in equation (3) (Richardson et al., 2015).

Subjective Financial Literacy Question

The subjective financial literacy question was adopted from the National Financial Capability survey (Lusardi & Mitchell, 2014). The question is framed as follows.

On a scale from 1 to 7, where 1 means very low and 7 means very high, how would you assess your overall financial knowledge?

The subjects ranked their perceived financial literacy proficiency on the seven Likert scale, and their responses were converted to 100% for easier comparison with an individual total score in the financial literacy test.

Financial Literacy Test

Students completed a 30-question financial literacy test under examination conditions. To calculate the FLC, the researchers calculated the difference between the subjective financial literacy question and the financial literacy test score. For easier comparison, all the responses were converted to out of 100% (Tokar Asaad, 2015). The absolute financial literacy confidence (AFLC) is the square of the FLC variable.

Results

Descriptive Results

There is a positive correlation between FRPC and FLC (.0666) and a positive correlation between AFRPC and AFLC (.0913). A t-test analysis by gender shows that FRPC for males is significantly higher than that of female counterparts. The t-test analysis by gender also shows that male subjects’ FLC is significantly higher than their female counterparts. The results of the t-test and correlation analysis can be availed upon request. Our findings are in sync with studies that have concluded that females are less confident in financial matters when compared to males (Aristei & Gallo, 2022; Bucher-Koenen et al., 2021). A t-test analysis by financial literacy level shows that subjects with low financial literacy are more significantly overconfident on FRPC and FLC compared to subjects with high financial literacy. The results confirm the impact of cognitive abilities on the divergence between subjective and objective measures of financial literacy and risk preferences (I. Kim & Gamble, 2022; Mechera-Ostrovsky et al., 2022). Subjects with little knowledge tend to overestimate their abilities when responding to subjective questions. Evidence shows that overconfidence in stock market participation in low financial literate individuals can result in them taking action, while underconfidence in more literate subjects results in inaction (van Rooij et al., 2011). It can be deduced that the misalignment of subjective and objective abilities does not always optimize an individual’s choices (Yeh & Ling, 2022). It suggests that subjects can make optimal decisions when their subjective and objective abilities coincide.

Female is a dummy variable (1 female /0 male), and urban is a dummy variable where (1 urban/0 rural)

Further, the t-test analysis shows that females’ subjective risk preferences, financial literacy scores, and subjective financial literacy averages are significantly higher than their male counterparts. Some studies concluded that female subjects have lower levels of financial literacy than their male counterparts (Sarpong-Kumankoma et al., 2023). However, results from this study of university students in South Africa show an opposing outcome. The results show that if females are exposed to education, their financial literacy can be better than those of males. The conclusion could be due to the deliberate policies implemented by the South African government toward supporting the girl child, for example, the child support grant (Mudzingiri et al., 2016). A US study found that older females were less financially literate and were generally overconfident (K. T. Kim et al., 2022).

Information in Figure 1 shows that the majority of subjects were overconfident, their FRPC was greater than zero, and a few were underconfident (risk confidence deviations < 0). The study observed the same trend in FLC where more individuals are overconfident (Financial literacy confidence deviations > 0) about their financial literacy ability (see Figure 2). The results show a considerable misalignment between perceived and objective financial literacy. The gap between what subjects think they know and what they know is wide. A wide gap between perceived and objective financial literacy might affect financial decision-making, resulting in individuals’ faulty financial choices, thereby reducing financial literacy self-efficacy (Tang, 2021). Sound financial decisions with minimal errors help improve the welfare of individuals, households, society, and the world (Lusardi & Mitchell, 2014). Studies have confirmed the misalignment of subjective and objective financial literacy and risk preference measures. Subjects tend to subjectively rank themselves higher than their actual ability (Lönnqvist et al., 2015).

Financial risk preference confidence. All bar graphs below 0 show information on FRPC underconfidence subjects, while all bars above 0 show responses for FRPC overconfident subjects.

Financial literacy confidence. All bar graphs below 0 show information from underconfident subjects, while all bars above 0 show responses from overconfident subjects.

Empirical Results

Random Effect Panel Regression

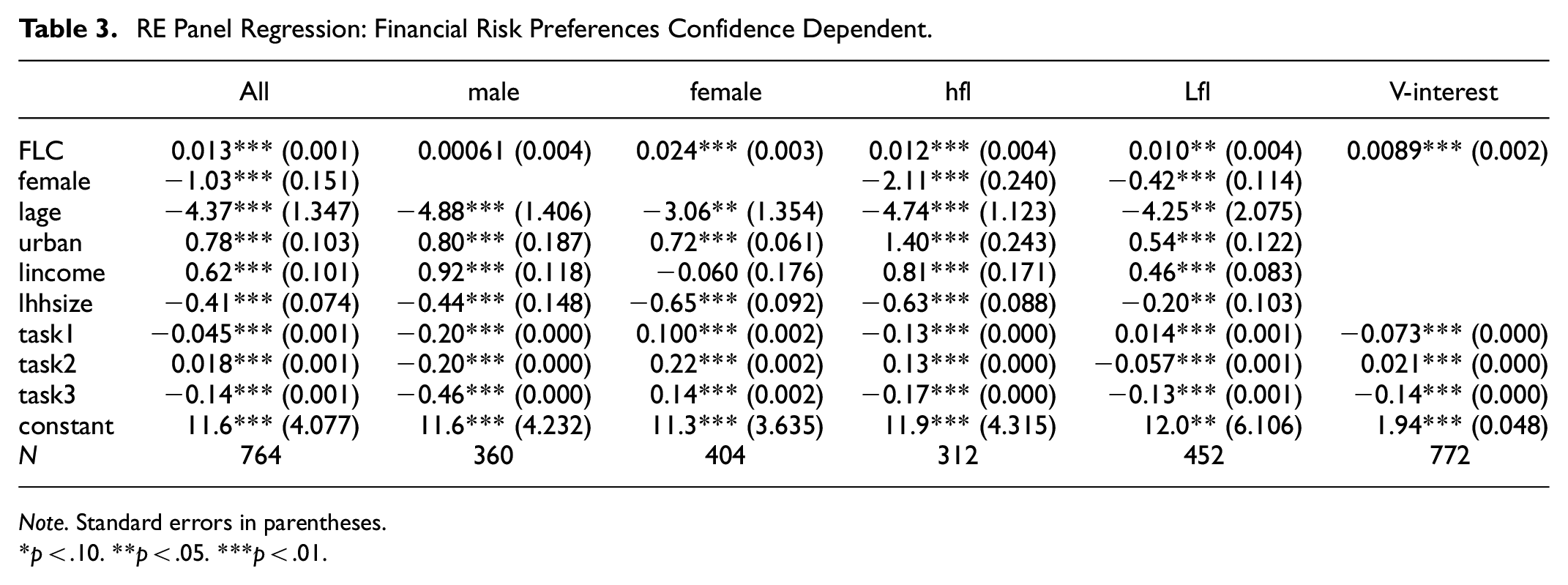

The Random Effect Panel regression (REPR) results appear in Table 3. A Hausman test confirms REPR as the suitable data analysis model (B. Wang et al., 2023). The study findings show that as FLC increases, for all subjects’ variables of interest (V-interest), all subjects with control variables (All), female, high financial literacy (hfl), and low financial literacy (lfl), FRPC significantly increases. The results reveal that increased FLC tends to widen the gap between the revealed and perceived or subjective risk preferences. The results show that FLC impacts FRPC, revealing the transmission mechanism that molds the financial behavior of individuals. Although the results could have been affected by the framing effect of the instruments used to collect the data, the results confirm the impact of cognitive abilities on risk preference choices (Mechera-Ostrovsky et al., 2022).

RE Panel Regression: Financial Risk Preferences Confidence Dependent.

Note. Standard errors in parentheses.

p < .10. **p < .05. ***p < .01.

Given that an increase in FLC encourages individuals to act on financial decision spheres, the results help us to understand individual financial risk preference behavior given their FLC (Aren & Nayman Hamamci, 2022). The behavior triggered by FLC on FRPC is synonymous with aspects that give rise to asset bubbles. Overconfidence in cognitive abilities spurs overconfidence in financial risk preferences (Scheinkman & Xiong, 2003). Other variables that significantly increase FRPC for all categories are living in an urban center and an increase in income measured as a monthly expenditure. The results also show that being female, older subjects, and an increase in household size (hhsize) are significantly associated with a reduction in FRPC.

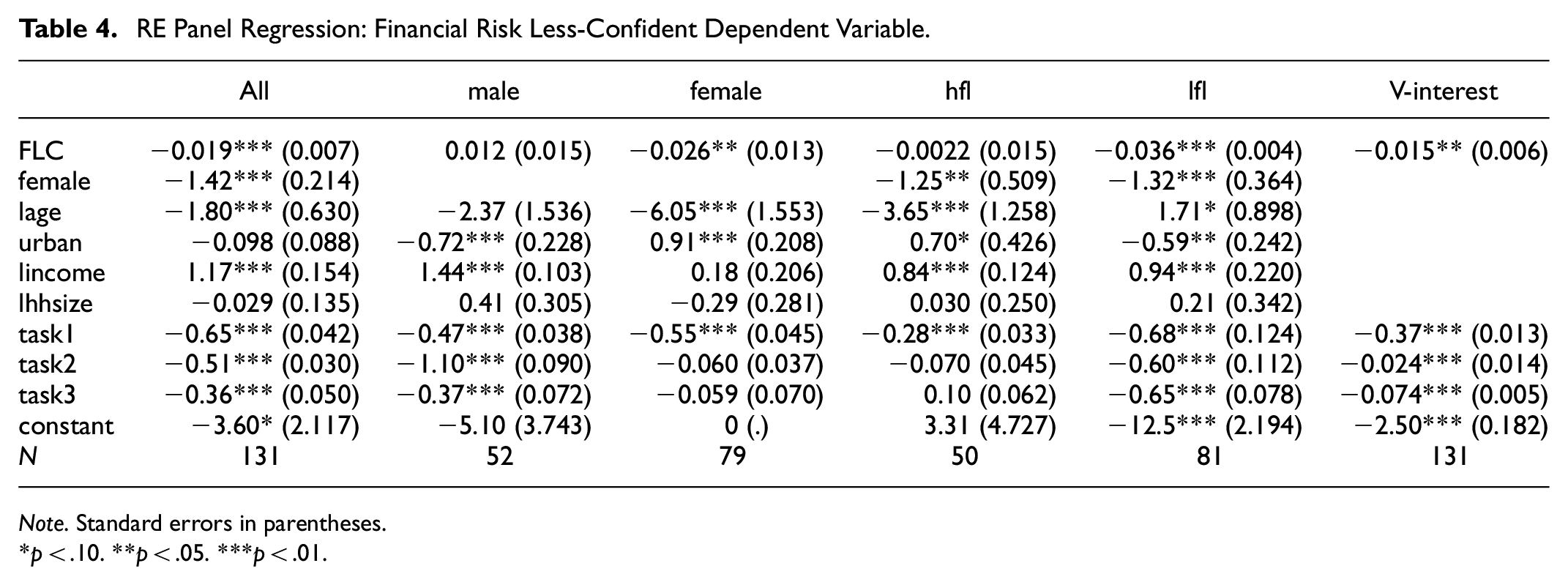

The study further split the data according to whether subjects were under/less confident (FRPC < 0) or overconfident (FRPC > 0). We excluded subjects with FRPC = 0 (confidence) since they are neither overconfident nor underconfident; they know themselves much better (Bertella et al., 2014; Yeh & Ling, 2022). Table 4 shows REPR results for less confident subjects. An increase in FLC significantly reduces FRPC for less confident subjects in the All, V-interest, female, and lfl categories groups. These results are associated with inaction behavior associated with less confident subjects when they are expected to invest or save in risky assets, leading to sub-optimal returns (Yeh & Ling, 2022). Other variables significantly reducing FRPC are being female for All, hfl, and lfl categories, older subjects for All, female, hfl categories, urban male subjects, and lfl groups. The results show that FRPC significantly increases for All, male, hfl, and lfl as income increases. Some studies have confirmed a significant association between income and risk preferences (Cohen & Einav, 2007). Being female and residing in an urban center significantly increases FRPC in the female category.

RE Panel Regression: Financial Risk Less-Confident Dependent Variable.

Note. Standard errors in parentheses.

p < .10. **p < .05. ***p < .01.

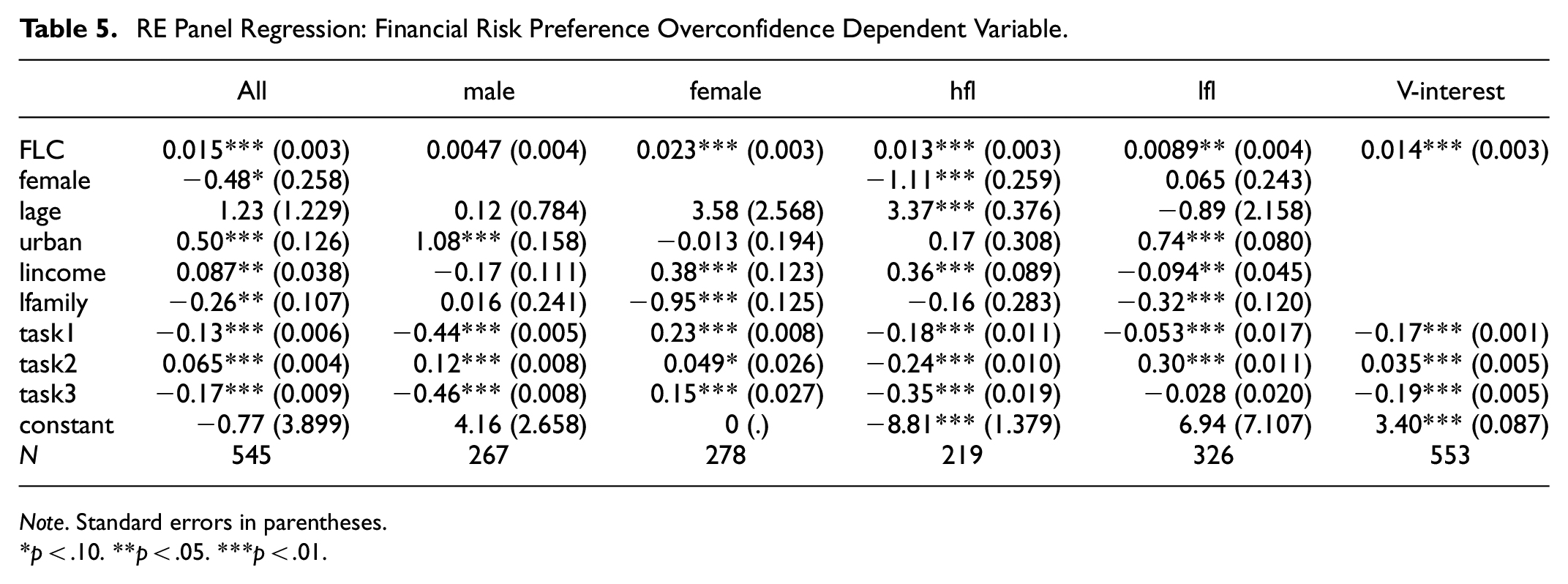

Moving on to the overconfident group (Table 5), an increase in FLC significantly increases FRPC for All, female, hfl, lfl, and V-interest groups. The results reveal that FLC drives FRPC in a positive direction. Subjects with higher FLC are more likely to have higher FRPC, showing that misalignment between subjective and objective financial literacy leads to positive misalignment of perceived and revealed risk preferences. The transmission mechanism is synonymous with the behavior of people investing in “Ponzi Schemes” and assets with a high chance of fraud and losses (Aristei & Gallo, 2021), confirming the influence of cognitive abilities on risk preference errors (Pedroni et al., 2017).

RE Panel Regression: Financial Risk Preference Overconfidence Dependent Variable.

Note. Standard errors in parentheses.

p < .10. **p < .05. ***p < .01.

Evidence suggests that cognitive financial literacy errors impact risk preference choice errors. The results explain why overconfident subjects invest in risky assets (K. T. Kim et al., 2022). The study also found that income significantly increases FRPC for All, female, and hfl groups. An increase in age for hfl and residing in an urban center for groups All, male, and lfl significantly increases FRPC. The study also concluded that being female for categories All and hfl increases income for category lfl and household size (hhsize) for groups All, and lfl significantly reduces FRPC. Revealing that an increase in FLC leads to a reduction in FRPC, showing better financial risk management aspects.

To investigate the absolute effect of FLC on absolute FRPC, we squared the variables FLC and FRPC and regressed the variable in natural logarithms to linearize the data. A REPR in Table 6 shows that in model “All,” a 1% increase in FLC leads to a 6.5% increase in FRPC. In absolute terms, FLC increases FRPC, confirming that an increase in FLC has implications for driving up FRPC, leading individuals to invest in risk assets. If an increase in confidence encourages individuals to act, then an increase in FLC will lead subjects to make risky financial decisions due to high levels of FRPC (Yeh & Ling, 2022). The results also show that in absolute terms for male subjects, a 1% increase in FLC leads to an 8% significant increase in FRPC. Studies have confirmed significant overconfidence in male subjects, which explains why they are more likely to invest in high-risk assets (Yeh & Ling, 2022).

RE Panel Regression: Absolute Financial Risk Preferences Confidence.

Note. Standard errors in parentheses.

p < .10. **p < .05. ***p < .01.

Given that confidence increases the probability of someone taking an action, an increase in FLC drives male subjects to have higher confidence in taking a financial risk. After controlling for task-specific characteristics, the study analyzed a parsimonious relationship between the variables of interest (V-interest), that is, FLC and FRPC. The results show that a 1% increase in FLC leads to a 6.5% significant increase in FRPC. Again, this confirms the fact that FLC breeds FRPC. These results confirm the correlation between cognitive abilities errors and risk preference errors in aligning subjective and objective measures of financial literacy and risk preferences (Pedroni et al., 2017).

The results show that income significantly increases FRPC for all the REPR models in Table 6. For the regression model, “All,” a 1% increase in income leads to an 18% significant increase in FRPC. Results from the “male” and “female” regression models show that a 1% increase in income for the two groups leads to a 15% increase in FRPC. A 1% increase in income leads to a 23% increase in FRPC for the hfl group, while a 1% increase in income leads to a 16% increase in FRPC for lfl. These results show that higher background income significantly increases FRPC in absolute terms. Studies have confirmed that low-income people are risk-averse while higher-income cohorts are less risk-tolerant (Vieider et al., 2019). If income has an effect of increasing FRPC it, therefore, flows that can drive choices to invest in risk assets. Individuals with high-income levels have a low marginal utility for their money and are more likely to be overconfident in investing or saving their income in risky assets. The study also observed that being female in the “hfl” regression model significantly increases FRPC, and increasing hhsize significantly increases FRPC for the “female” regression model. The absolute FRPC REPR (Table 6) also shows that being an urban resident significantly reduced FRPC for models “All,”“female,”“hfl,” and “lfl” in absolute terms. An increase in hhsize significantly reduces FRPC for regression models “All” and “male.”

Results from Tables 3 to 6 confirm that FLC significantly impacts the FRPC of the subjects, but the results differ depending on the data under consideration. Misalignment errors of subjective and objective measures of financial literacy have implications on misalignment errors of subjective and objective measures of FRPC (Pedroni et al., 2017). Errors in risk preference choices are significantly driven by an individual’s cognitive abilities, which can have varied outcomes on an individual’s expected utility (Crispino et al., 2023). The study further conducted a robust check of the results by running hierarchical random effect regression on residuals in the next section.

Hierarchical Random Effect Panel Regression on Residuals

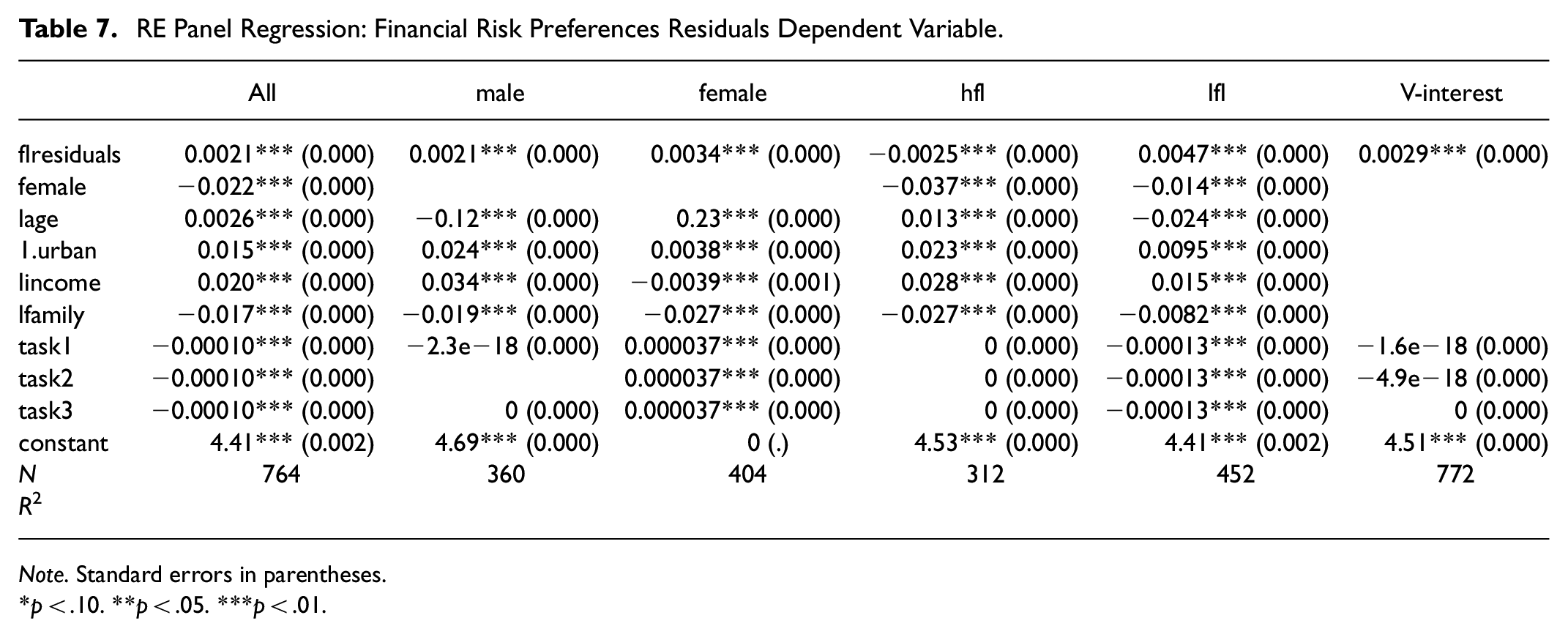

The study used hierarchical random effect regressions to conduct a robust check analysis on the impact of financial literacy errors or mistakes on financial risk preference errors (Richardson et al., 2015). The research predicted the financial risk preference and financial literacy residuals using equations (2) and (3), respectively. A Hausman test confirms the REPR as the suitable model to estimate the results. The results in Table 3 compare well with those in Table 7. The study results confirm that financial literacy residuals/mistakes/errors are significantly related to financial risk preference residual/mistakes/errors for V-interest, All, female, male, hfl and lfl. Except for hfl, all other categories show that an increase in financial literacy residuals leads to a positive increase in financial risk preference residuals. The results confirm a strong and significant correlation between cognitive abilities errors and risk preference choice errors, as confirmed in other studies (Frey et al., 2017; Pedroni et al., 2017).

RE Panel Regression: Financial Risk Preferences Residuals Dependent Variable.

Note. Standard errors in parentheses.

p < .10. **p < .05. ***p < .01.

The results from subjects with high financial literacy (hfl) show that financial risk preference residuals decrease as financial literacy residuals increases. Results show that hfl subjects were more able to align their subjective and objective financial risk preference responses when compared to any other reference group. The results show that acquiring financial literacy helps individuals better understand their risk preference appetite. High financial literacy seems to inculcate the self-efficacy trait among subjects, as financial literacy motivates subjects to handle financial risk matters better (Liu & Zhang, 2021). Financial literacy errors between subjective and objective responses for hfl group do not magnify FRPR. Designing financial literacy programs can help subjects have a deeper understanding of their risk preferences subjectively and objectively. The results also confirm that financial literacy overconfidence among highly financially literate subjects is less detrimental to their risk preference choice errors.

The robust check also confirms that given that one is a male subject, being a female subject is associated with a lower financial risk preference residual. Showing that females could better align their subjective and objective preferences when compared to male subjects. The findings compare very well with the results obtained in Table 3. The findings show that gender differences affect risk preference choices (Alam et al., 2022). An increase in household size is associated with a decrease in FRPR, showing that subjects from bigger households could better align their subjective and objective risk preference responses. Bigger households are usually financially constrained (Ertac, 2020). Belonging to a big household could have an impact on the way one makes risk preference choices. Other variables that show a negative relationship with FRPR are age for male and lfl subjects and income for female subjects.

Turning to the geographical location of subjects, given that one resides in rural areas, residing in urban centers is associated with an increase in FRPR. Subjects in urban areas are more likely to show higher residuals of subjective and objective risk preference responses. Urban areas generally offer better services than rural areas (Oliver-Márquez et al., 2021). Variation in geographical spatial location means that individual resource endowment may differ, impacting the alignment of subjective and objective risk preference choices. Another variable positively related to FRPR is the age for “All” and “female” categories.

The study provides insight into the relationship between financial literary residuals and financial risk preferences residuals. The study is premised on the expected utility theory, self-efficacy theory, and the framing effect theory. This study does not test the applicability of the theories in the current context. However, the study acknowledges that the three theories could have driven the results. Subjects may have made choices to maximize their benefit, or their financial literacy could have motivated them to make beneficial decisions. Further, the way the instruments used to collect data are framed could have influenced the outcome. Aside from theoretical implications, the study confirms the relationship between cognitive abilities errors of FLC/FLR on FRPC/FRPR on subjective and objective responses.

Conclusion

This study investigates the effect of FLC on FRPC. It uses unique experimental data from university students, which collected objective and subjective measures of FLC and FRPC. The gap between subjective and objective measures of financial risk preferences and financial literacy forms the measures of FRPC and FLC, respectively. Analysis of laboratory data shows that FLC has a significant effect on the FRPC of subjects. Results from less/underconfident subjects show that FLC significantly reduces the FRPC of females, lfl, and hfl study participants. Findings from the overconfident group show that FLC significantly increases the FRPC of females, hfl, and lfl subjects.

A robust analysis using hierarchical random effect regressions concluded that FLR is significantly associated with FRPR, suggesting that cognitive ability errors on objective and subjective financial literacy responses correlate with risk preference errors on subjective and objective risk preference choices. The positive relationship between FLR/FLC and FRPR/FRPC mimics the financial behavior exhibited by people who invest in high-risk assets, which causes “asset bubbles” during financial crises. For subjects with high financial literacy, increased FLR reduces FRPR, showing that holding higher financial literacy helped subjects understand their risk preferences better. Bridging the gap between subjective and objective financial literacy reduces the effect of the gap between subjective and objective financial risk preferences. Reducing the gap between subjective and objective financial literacy is more critical for overconfident subjects. Availing financial literacy programs to overconfident citizens with low financial literacy can assist them in managing financial risk in a better way. Such programs can promote financial inclusion, enhance decision-making, and ensure financial stability. In this study, other factors that significantly influence FRPC and FRPR are gender differences, geographical location, age differences, household size, and income differences.

Limitations

This study has its fair share of limitations. The study uses university students who may not accurately represent people in society. Although the use of laboratory evidence can help researchers to understand the processes and behavior that is difficult to obtain in a natural set-up, the instruments used to collect the data, such as MPL risk preference tasks, questionnaire, and financial literacy test, might fail to mimic a natural environment and can have framing effect challenges. Further studies can be pursued with nationally representative population samples to test the impact of FLC on FRPC. A natural experiment on investment and saving focusing on FLC and FRPC can shed light on individual financial decision-making processes. Understanding the effect of FLC/FLR on FRPC/FRPR can also be tested under the framing effect, expected utility, and self-efficacy theories.

Footnotes

Acknowledgements

I am grateful to the Edward Tiffy scholarship that provided funding to run MPL risk preference tasks experiment. The Economic Research for Southern Africa (ERSA) which trained me on some techniques to analyze the data.

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.

Ethical Approval

All procedures performed in studies involving human participants were in accordance with the ethical standards of the institutional and/or national research committee and with the 1964 Declaration of Helsinki and its later amendments or comparable ethical standards. Permission to carry out the study was granted by the University of the Free State Ethics Committee (Number: UFS-HSD2022/1842).

Informed Consent

Informed consent was obtained from all individual participants included in the study.