Abstract

Financial socialisation (FS) plays a vital role in determining the financial decision-making power and risk-taking behaviour of rural households. The present study investigates the interplay between financial socialisation, gender, and marital status in shaping decision-making power and investment risk-taking behaviour. A quantitative approach was employed, with 312 survey responses collected via a cross-sectional survey method from rural investors in Karnataka and Tamil Nadu, India. Financial socialisation was assessed using adapted and validated items from prior studies, while trading frequency was a proxy for risk-taking behaviour. The moderated mediation framework (PROCESS Macro Model 8) was employed to investigate the interplay between the variables. Results show that FS significantly increases women’s risk-taking behaviour, but this effect is partly reduced due to their lower decision-making power in rural patriarchal households. For men, the direct effect of financial socialisation on risk-taking behaviour is positive but weaker, with no mediation through decision-making power. Married individuals exhibit more conservative risk-taking behaviour than unmarried individuals due to familial responsibilities. The study also found that education and income do not significantly impact decision-making power, possibly reflecting deeper socio-cultural influences in rural settings. These findings imply that policymakers should design targeted financial literacy programmes to address gender disparities and cultural barriers to financial participation. By promoting inclusive financial socialisation, households can achieve more equitable decision-making processes and risk management, which will improve the financial well-being of rural communities. This study contributes to understanding financial socialisation within patriarchal contexts and offers insights into targeted financial empowerment initiatives.

Plain Language Summary

Rural households make financial decisions based on their social and cultural influences. This study examines how financial socialization affects decision-making power and risk-taking behaviour, particularly among patriarchal society men and women in rural India.

• Financial socialisation plays a key role in shaping financial decisions.

• Women in rural areas who are exposed to financial socialisation are more likely to take financial risks, but their culture and social norms often limit their decision-making power.

• Married people take fewer risks than unmarried people.

• In rural India, men control financial decisions and are considered family heads.

• To promote gender equality in financial decision-making, a financial education is required.

• Reducing cultural barriers will help women take an active role in decision-making.

• Risk awareness programme for households can improve their financial well-being.

Keywords

Introduction

Rational financial decisions are essential for the functioning of the financial system (Brüggen et al., 2017; Gomes et al., 2021) and broader economic stability (Anvari-Clark & Ansong, 2022). However, individual financial decision-making is shaped by various personal, behavioural, and social factors (Raut, 2020). Behavioural factors, such as overconfidence and heuristics, (Barber & Odean, 2001; Suresh, 2024; Suresh & Loang, 2024) psychological factors (Montinari & Rancan, 2018) and demographic factors, such as gender and education (Bertocchi et al., 2014; Goyal & Kumar, 2020), have been shown to influence an individual’s financial decisions. Among these, social influences, particularly from financial socialisation, have often been overlooked, despite their significant role in shaping financial attitudes and behaviours. Understanding these social influences is important to understand the broader patterns of investors’ behaviour (Joseph et al., 2023; A. Singh & Biswas, 2024).

With this background, the present study explores how financial socialisation influences decision-making power and risk-taking behaviour within rural households, where financial decisions are often shaped by patriarchal norms and intra-household dynamics (Wellington, 2022). In India, policy initiatives like Pradhan Mantri Jan Dhan Yojana (PMJDY) and Self-Help Groups (SHGs) expanded financial access for rural people, particularly women. However, financial access alone does not guarantee financial independence, especially in households where financial decisions remain male-dominated (Islam et al., 2023). This highlights the importance of studying how financial socialisation operates in such complex contexts. Earlier studies on FS mainly focused on urban or general populations (Fan et al., 2022; A. Johnson & Kasztelnik, 2024; Shim et al., 2015) but have understudied rural households, where societal and patriarchal norms play a significant role. Furthermore, earlier studies have established links between financial socialisation and financial attitudes and risk-taking behaviour (Madinga et al., 2022; Utkarsh et al., 2020), but have overlooked the influence of financial socialisation on the decision-making process and its impact on the risk-taking behaviour of rural households. It further examines whether gender and marital status moderate the effects of financial socialisation on financial decision-making and risk-taking behaviour. Generally, gender and marital status influence how a person internalises FS, affecting its impact on decision-making and risk-taking behaviour (Furrebøe et al., 2023; Lemaster & Strough, 2014). With the intention of addressing these gaps, the present study examines the interplay between financial socialisation and decision-making power, as well as risk-taking behaviour, among rural households. The present study makes several contributions to the literature. First, it advances the scope of financial socialisation studies by focusing on rural and patriarchal households in developing countries, such as India, which are often neglected in financial behaviour studies. Second, it provides theoretical and practical insights through an empirical examination of the mediating role of intra-household decision-making power and the moderating roles of gender and marital status. Finally, it contributes methodologically by employing validated instruments from the social learning and behavioural finance literatures to measure financial socialisation, decision-making power, and risk-taking behaviour.

The remainder of this manuscript is structured as follows. Following this introduction, the Theoretical framework section outlines the conceptual basis of the study. The literature review and hypotheses development section reviews prior studies and develops the testable hypotheses. The methodology section describes the data variables, and the empirical strategy.The results section presents the empirical findings followed by the discussion section, which interprets the results in light of existing literature. Finally, the Conclusion section summarizes the key findings, and the limitations and direction for future research section outlines the study's limitations and potential avenues for future work.

Theoretical Framework

To explain the conceptual model guiding this study, we draw on social learning theory to construct financial socialisation, complemented with the theory of gender and power and role theory to account for the moderating effects of gender and marital status.

Social Learning Theory (SLT)

The social learning theory (SLT) emphasises the influence of socialisation, suggesting that observing family members, friends, and others affects an individual’s attitude and decision-making process (Bandura, 1986). The SLT laid the foundation for financial socialisation (FS) by explaining how individual manipulates financial behaviour. Financial socialisation (FS) explains how individuals develop values, financial attitudes, knowledge, and behaviour from implicit and explicit social environments (Danes, 1994). Implicit socialisation means learning about financial management and managing the funds from family members. On the other hand, explicit socialisation means learning from society through formal education and guidance from friends and other members of society (Gudmunson & Danes, 2011). Financial socialisation impacts individuals and household financial dynamics (Van Campenhout, 2015), and thereby the financial system of an economy. The FS influences household members in making investment decisions and managing risks by manipulating their financial attitudes, values, knowledge, and behaviour. Further, implicit and explicit mechanisms shape these behaviours and form the foundation for household financial management. The FS influences a person’s financial attitude and behaviour, and determines decision-making power within a household (Bialowolski et al., 2020). In many contexts, the decision-making power in a household is based on the members’ financial literacy and attitude.

Theory of Gender and Power, and Role Theory

While SLT helps to understand how financial knowledge and behaviours are acquired, it fails to capture the structural barriers that affect translation into decision-making power. The Theory of Gender and Power (Connell, 1987; Wingood & DiClemente, 2002) addresses this gap by highlighting how the rooted social structures create gendered inequalities. It has three interrelated concepts. The first is the sexual division of labour, in which work is allocated based on gender. Secondly, the sexual division of power reinforces male dominance in household and institutional decision-making. Ultimately, the structure of cathexis is grounded in social norms that dictate traditional gender roles. These structures are particularly obvious in a patriarchal rural context like India, where even financially literate women are denied financial independence and lack power in the household financial decision-making process (Bhatia & Singh, 2020). From this theoretical integration, it can be understood whether financial socialisation influences decision-making and risk-taking and how these effects differ, particularly by gender. In addition to gender, role theory (Biddle, 1986) provides a different understanding of how marital status influences financial behaviour. Individuals assume a new role as spouses and adopt the associated responsibilities and norms. These role expectations make them more cautious while taking financial decisions and may shift intra-household power dynamics, influencing both decision-making and risk-taking behaviour.

Review of Literature and Hypotheses Development

Financial Socialisation and Decision-Making Power

Socialisation is the process of acquiring knowledge, skills, and values to participate in a society or forum (Hira et al., 2013). These learned traits can be found in any domain, ranging from spiritual and cultural to behavioural, marketing, and economic spheres. Within this context, financial socialisation (FS) refers to the development of financial values, knowledge, and behaviour that helps individuals manage resources for personal and household well-being (Danes, 1993). Conceptually derived from social learning theory, FS occurs through implicit (from family members & peers) and explicit (formal education, workplace learning, and other sources) agencies. FS plays a central role in determining financial knowledge, helping individuals make informed financial decisions with confidence, control, and the ability to exhibit better financial behaviour (Pahlevan Sharif & Naghav, 2020). However, the level and nature of financial socialisation may vary among individuals according to their socio-economic profile. These variations may lead to differential financial proficiencies and household decision-making power.

In household contexts, a financially literate person often shows higher confidence and competence, which enables them to take the lead in financial decisions (Kim et al., 2017). In households heavily influenced by societal and traditional norms, decision-making power is often concentrated in certain members, even when other members may be more financially literate (Kochar et al., 2022; Tiwari & Dubey, 2024). This reflects the existence of patriarchal authority over merit-based decision roles. In India, studies documented that the patriarchal structure often gives financial decision-making power to the head of the family, typically a man (Sharma & Kota, 2019; S. Singh & Bhandari, 2012). This structurally skewed decision-making can profoundly affect household investment patterns, limit risk diversification, and marginalise the financial preferences of better-informed members.

Financial socialisation (FS) is important in determining household decision-making power, as it determines who acquires financial knowledge and exposure from social interaction. However, in patriarchal societies like India and the UAE, the gender gap persists, restricting women’s access to financial socialisation opportunities and limiting their financial autonomy (Agnew & Cameron-Agnew, 2015; S. Johnson, 2004). These inequalities prevent women from actively participating in household financial decision-making, mainly due to restrictive social and traditional norms and limited opportunities for FS (Sharma & Kota, 2019; S. Singh & Bhandari, 2012; Tiwari & Dubey, 2024). Such gender disparities in FS contribute to a broader gap in household decision-making power, which may, in turn, influence key financial behaviours, like investment decisions. However, financial literacy alone does not guarantee actual decision-making power. Earlier studies have highlighted that, due to gendered norms and family hierarchical structures, even financially literate and capable individuals may remain excluded from the household decision-making process (Kagotho & Vaughn, 2018). This creates a question about whether FS truly translates into decision-making power in a rural patriarchal setting. Building upon this, we hypothesise that.

Financial Socialisation and Risk-Taking Behaviour

However, recent trends suggest a gradual increase in women’s participation in household financial decision-making, due to rising literacy and financial awareness. An empirical study highlighted that increasing literacy rates have led to more joint financial decision-making between men and women, including the shared assessment of household financial risk (Sharma & Kota, 2019). This shift is evident in investment behaviour, as a recent report from the Association of Mutual Funds in India (AMFI) shows that women’s participation in mutual funds has increased to 21% (Rukhaiyar, 2024), suggesting a growing sense of financial agency. However, this scenario is primarily observed among certain socio-economic groups within the population, suggesting that financial engagement remains uneven across the broader population. In response to persistent gender gaps, the Indian government has implemented various schemes, including the Mahila Shakti Kendra, Pradhan Mantri Matru Vandana Yojana, Nari Shakti Puraskar, Mahila E-Haat, and Self-Help Groups, to promote women’s empowerment and financial inclusion. Such schemes have helped enhance women’s financial socialisation by expanding their access to financial resources, increasing awareness, and promoting their participation in household financial decision-making (Patel & Patel, 2021). These expanding opportunities for financial socialisation contribute to increased financial literacy, enhanced access to financial resources, and foster inclusive household financial management.

In rural areas, where explicit financial socialisation options are limited, individuals often acquire financial knowledge implicitly, such as through observation and informal networks. However, cultural norms restrict women’s exposure to these informal learning opportunities, resulting in lower financial literacy, limited financial autonomy, and minimal participation in household financial decisions. Such gender disparity limits women’s role in decision-making dynamics and has implications for household-level risk-taking behaviour and investment decisions (Bialowolski et al., 2020). For example, S. Singh and Bhandari (2012) highlighted that in Indian households, financial decision-making and management are undertaken mainly by men. Social learning theory argues that financial socialisation may increase risk-taking behaviour by improving financial literacy and confidence (Agnew & Sotardi, 2025). However, earlier studies also highlighted that financial knowledge leads to higher risk awareness and, in turn, to more conservative behaviour (Amari et al., 2020). These mixed theoretical views make it uncertain whether FS increases or decreases risk-taking behaviour among households.

Further, Gustafson (1998) argues that gender differences in risk-taking behaviour are also shaped by broader societal ideologies and norms, suggesting that risk perception itself is socially constructed. Given the influence of social learning on financial behaviour, attitudes, and risk orientation, we propose the following hypothesis.

Mediation Between Financial Socialisation and Risk-Taking Behaviour

Individuals with greater decision-making power in household finance often exhibit higher risk-taking tendencies. This relationship is consistent with earlier studies that suggest decision-making autonomy empowers individuals to call on the risk-return proposition (Gopal et al., 2025). Conversely, those primarily responsible for the financial well-being of dependents may adopt more cautious financial behaviour. However, the relationship between FS and risk-taking behaviour remains theoretically ambiguous. Some studies found that FS may increase risk-taking behaviour by improving financial literacy and confidence (Owusu et al., 2023), whereas other studies argue that individuals internalise this improved financial knowledge only when they have actual decision-making power in households (Kumar et al., 2023). In rural patriarchal contexts, individuals with high FS may still lack the power to make decisions, softening any direct relationship between FS and risk-taking behaviour. It suggests that the decision-making power may act as the mediating factor. Hence, we hypothesise that.

Moderation of the Financial Socialisation-Decision-Making Power Relationship

Generally, married individuals tend to be risk-averse compared to their unmarried counterparts due to increased responsibilities, economic constraints, and caregiving obligations for dependents (Roszkowski et al., 1993). Similarly, with increasing gender equality, financial decisions at both individual and household levels are increasingly made through joint discussions of husband and spouse, rather than by a single member alone in the family system (Kim et al., 2017). Similarly, it is a general perception that men show a higher amount of risk tolerance than women (Barber & Odean, 2001; Bertocchi et al., 2014; Kannadhasan, 2015). However, the financial socialisation impact on decision-making power may not be similar across segments of people. Particularly in patriarchal societies, gender shapes individuals’ bargaining power and opportunities to implement financial autonomy (Kagotho & Vaughn, 2016). This means that even with a similar level of FS, gender may play a role in their ability to convert financial knowledge into household decision-making authority (Wagner & Walstad, 2022). Similarly, marital status may restructure the household decision-making system, where married individuals often opt for hierarchical or joint decision-making, which can affect the significance of FS (Lim et al., 2022). These differences indicate that gender and marital status may determine how the FS is internalised into decision-making power. Therefore, we propose the hypotheses that

Moderation of the Financial Socialisation-Risk-Taking Behaviour Relationship

Studies suggest that unmarried individuals tend to exhibit a higher risk appetite than their married counterparts, possibly due to fewer financial responsibilities and fewer dependents (Yao & Hanna, 2005). Similarly, gender plays a significant role in forming financial attitudes. Studies claim that men generally exhibit higher risk tolerance than their counterparts (Barber & Odean, 2001; Bertocchi et al., 2014), whereas women often adopt more conservative behaviour due to societal norms and limited financial autonomy in the patriarchal context (Jianakoplos & Bernasek, 2008). However, as mentioned earlier, the effect of FS on risk-taking behaviour may not be uniform across the groups. Differences in financial autonomy, exposure to financial information and societal norms may influence them to apply financial knowledge differently, even if the level of FS is uniform (Hasler & Lusardi, 2017). These differences indicate that gender and marital status may condition the effect of FS on risk-taking behaviour. We therefore propose the following hypotheses regarding gender and marital status as moderating variables.

These observations raise important questions about whether financial socialisation enhances household members’ decision-making power and whether its effects on risk-taking behaviour are conditioned by gender and marital status. Studies on financial decision-making power have primarily focused on Western countries (Bertocchi et al., 2014; Vogler, 1998; Wagner & Walstad, 2023), with few studies concentrated on women’s power in financial decision-making in Indian households. In the Indian context, particularly among middle- and lower-income households, as well as rural households, financial decision-making is often dominated by male members (S. Singh & Bhandari, 2012). As highlighted, several government schemes have aimed to empower women and promote their participation in household financial decision-making (Patel & Patel, 2021). However, the extent to which these schemes and FS opportunities have translated into actual decision-making power and financial autonomy remains to be explored. Further, while household finance has received scholarly attention, the specific roles of rural women and their FS experiences remain understudied. Hence, there is a strong need for an in-depth study examining how financial socialisation, decision-making power, and risk-taking behaviour intersect in the context of rural households. Although many studies have explored these constructs, the existing literature is predominantly based on Western countries. Given that cultural factors differ in household dynamics (Hasler & Lusardi, 2017), studies in patriarchal societies, such as India, are crucial for understanding household financial decision-making. Such contextual understanding contributes to the literature and offers critical insights for policymakers to devise effective strategies for women’s empowerment and assess household risk-taking behaviour in India.

Methodology

Sampling Procedure and Data Collection

We have adopted a quantitative, cross-sectional research design to examine the relationship between financial socialisation (independent variable), decision-making power (mediator), and risk-taking behaviour (dependent variable) within rural households in a patriarchal society context. Data were collected through a structured cross-sectional survey administered to rural household investors in Karnataka and Tamil Nadu, India. Given the absence of an official database on rural household investors, we adopted the snowball sampling technique, a well-recognised method for reaching hidden or hard-to-reach populations through chain reference (Atkinson & Flint, 2001). The initial 17 respondents were identified with the help of an investment advisor familiar with the rural investment network. These initial participants referred others within their community circles, identifying an additional 324 potential respondents, resulting in a total of 341 rural household investors. To ensure that only rural investors were included in the sample, seven participants were excluded after it was found that they lived in urban areas. Hence, the final eligible rural investors comprised 334 individuals from whom data were collected. Further, 22 responses were excluded due to inattentiveness or incompleteness, resulting in a final valid sample of 312 responses (93.4% response rate).

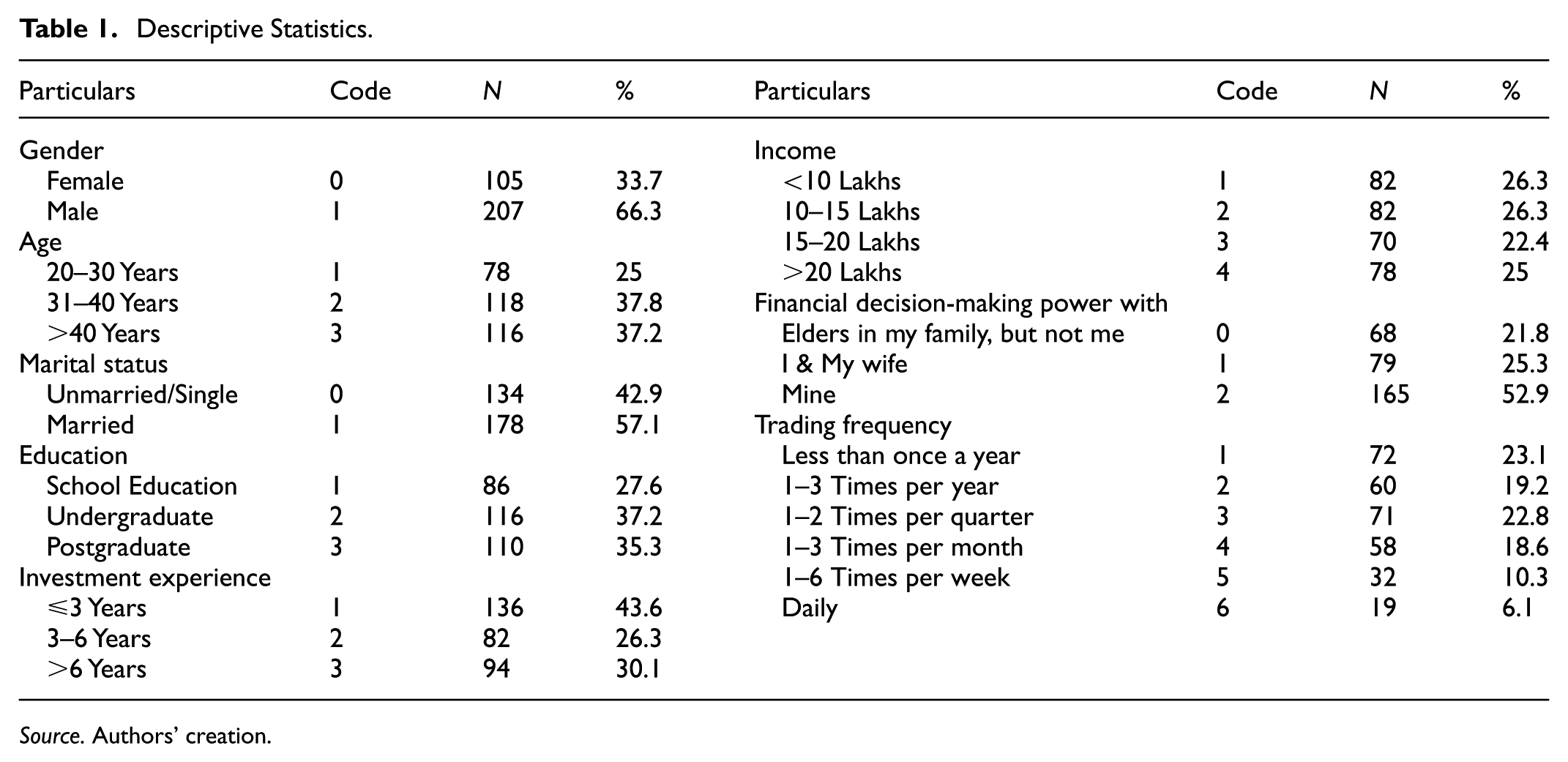

Data were collected using a structured questionnaire specifically designed to capture the study’s constructs. A pre-validated questionnaire for financial socialisation and decision-making power was adapted from Phung et al. (2021). The items capture both implicit and explicit aspects of FS and financial autonomy within the household structure. Consistent with Barber and Odean (2000), risk-taking behaviour was operationalised using trading frequency, a widely used proxy in behavioural finance literature to capture individual investment risk preferences. Though this single-item proxy may not fully capture the multidimensional nature of risk-taking behaviour, it gives a clear behavioural indicator. It is suitable for large-scale field surveys in a constrained environment. A higher trading frequency is considered indicative of higher risk-taking propensity, while a lower number of trades reflects more risk-averse behaviour. Apart from these core constructs, demographic details such as gender, marital status (used as moderating variables), age, qualification, experience, and income (used as control variables) were also collected to examine subgroup heterogeneity and account for potential confounding effects in the model. The control variables, such as age, income, education, and work experience, were incorporated into the model to ensure that the observed relationship between financial socialisation and risk-taking behaviour is not confounded by individual background differences. These demographic and socioeconomic attributes have been consistently shown to influence a person’s exposure to financial knowledge, capacity to process financial information, and willingness to engage in risk-related decisions. By statistically controlling for these factors, the analysis isolates the unique contribution of financial socialisation to risk-taking tendencies. Moreover, including these variables helps in clarifying the role of decision-making power as a mediating factor, ensuring that its effect is not merely a reflection of demographic disparities. In essence, the use of control variables strengthens the model’s internal validity and enhances the robustness and interpretability of the findings by reducing omitted variable bias and improving the precision of estimated relationships. To ensure contextual validity, the draft questionnaire was reviewed by five domain experts (investment advisors and academic experts). Their feedback helped modify the wording to improve the clarity, cultural appropriateness, and relevance of the items in the rural Indian context. Based on their comments and suggestions, minor modifications were made, and the questionnaire was finalised. To ensure linguistic equivalence and conceptual clarity, the questionnaire was translated into the regional language (Kannada & Tamil) using the back-translation method (Abdo et al., 2023) with the help of language experts. The translated questionnaire was pretested with 31 respondents drawn from the population to assess its clarity and response variability. Based on the feedback from respondents and field investigators, we revised ambiguous items and finalised the questionnaire in English, Kannada, and Tamil. The final questionnaire was available in English, Kannada, and Tamil, and administered by eight trained field investigators, including the authors, to ensure consistency in data collection across regions. Collected data were reviewed and entered on the same day to ensure accuracy. Based on this review, 22 responses were excluded due to inconsistency or incomplete information. The demographic characteristics of the final sample are presented in Table 1.

Descriptive Statistics.

Source. Authors’ creation.

Conceptual Model and Statistical Tool for Analysis

Traditional moderation models often overlook variations arising from the interaction effects of third or additional variables and may not adequately account for sample heterogeneity (Hair et al., 2021). Further, this study examines how financial socialisation influences decision-making power and risk-taking behaviour in rural households, while also assessing the interaction effect of gender and marital status. Since the study is based on rural households, where rooted social and cultural norms may interact with financial behaviour (Patil, 2021; Rawat, 2014), a moderated mediation framework was more suitable than the simple moderation and mediation models. Hence, we employed PROCESS Macro Model 8 in SPSS, which is specifically designed to test moderated mediation effects and consider for variance in third variables. Based on the theoretical framework and literature review, the conceptual model presented in Figure 1 was tested using the PROCESS Macro Model 8 in SPSS.

Conceptual framework.

Questionnaire Development and Reliability

As mentioned earlier, the FS and decision-making power constructs were adapted from Phung et al. (2021), which capture both the explicit and implicit dimensions of financial socialisation. The FS construct consisted of 12 items, each serving as an indicator of the underlying latent construct. While the FS constructs were originally adapted from the validated scale, minor wording alterations were made to suit the rural Indian context. The responses were collected using a 5-point Likert scale (1 = strongly disagree to 5 = strongly agree). To ensure attentiveness and response consistency, five negatively worded items were reverse-coded before computing the total FS score. The Cronbach’s alpha for the FS scale was .828, indicating internal reliability.

Aligning with existing literature, the decision-making power (DMP) construct was assessed using a single-item question that captures financial autonomy within the household. Respondents were asked about their role in the family’s financial decision (relating to investment), with the following three options:

(a) Someone else makes the decision, and I have a limited role.

(b) I give my suggestions, but decisions are mostly joint.

(c) I am the main financial decision-maker.

This operationalisation aligns with previous studies that have used a similar single-item question to determine household decision-making power across domains such as income, spending, purchasing, investment, healthcare, education, and social engagement (Lai & Tei, 2020; Phung et al., 2021; Seidu et al., 2022; Vogler, 1998).

As mentioned earlier, risk-taking behaviour (RTB) was captured using a single-item proxy, that is, trade frequency, consistent with Barber and Odean (2000). Though this behavioural indicator does not capture the dynamics of risk preference, it has been widely used in empirical studies. Furthermore, it was deemed contextually appropriate for field surveys in rural households, given the constraints of large-scale data collection.

Analysis Procedure

We began the analysis by checking the key assumptions of regression. Multicollinearity was assessed based on variance inflation factor (VIF) values, all of which were below the threshold value (VIF < 2.5), indicating no serious collinearity issues. The latent construct FS was computed as the composite score after reverse-coding of negatively worded items. The moderator variables, that is, gender and marital status, and control variables, that is, age, income, qualification, and investment experiences, are coded appropriately and included in the model to account for heterogeneity in risk-taking behaviour. To test the moderated mediation framework, we have employed PROCESS Macro Model 8 in SPSS v26 as recommended by Hayes (2017). The model allowed us to examine the mediating role of decision-making power (DMP) in the direct relationship between financial socialisation (FS) and risk-taking behaviour (RTB), along with the moderating effects of gender and marital status. A bootstrap resampling method with 5,000 iterations was applied to generate robust confidence intervals for indirect effects.

Results

We begin the results section with the frequency analysis of the respondents’ demographic variables. Table 1 summarises the descriptives of 312 responses collected in the study area in India. The table provides a snapshot of all variables. Respondents’ age, education, investment experience, and income are controlled variables to ensure accuracy and reduce distorted results in the relationship between the variables. These demographic factors of respondents are considered control variables, as they have the potential to confound decision-making power and risk-taking behaviour (Barber & Odean, 2001; Hasler & Lusardi, 2017). We have considered the marital status and gender of the respondents as moderating variables. The constructs of financial decision-making power and trading frequency were chosen carefully from the existing literature.

Table 2 indicates that nearly 53% of respondents make financial decisions independently, without any intervention from other family members. Regarding trading frequency, 23% of respondents with the highest rank trade once a year, followed by 22% who trade twice a quarter. It is a clear indication that about 45% of household members trade occasionally, which has significant implications for this research work. These descriptive statistics suggest that rural household members are not making joint decisions, indicating financial autonomy in household finance.

Results of Gender and Financial Socialisation Moderated Mediation Analysis – PROCESS Macro Model 8.

Note.β = unstandardised; LB = lower bound for 95% confidence level; UB = upper bound for 95% confidence level.

F-statistics df: (6, 305).

p < .10. **p < .05. ***p < .001.

The results of the PROCESS Macro Model 8 are shown in Table 2. This model assesses the moderation-mediation relationship between the variables after controlling for the effects of respondents’ age, income, investment experience, and educational qualifications. This model executes two regressions. The first regression evaluates the moderating role of gender on the relationship between financial socialisation and decision-making power. The second regression evaluates the moderating role of gender in financial socialisation and risk-taking behaviour. The first regression result indicates that the interaction between financial socialisation and gender is statistically significant (β = −.077; SE = 0.022) and negative. This suggests that the influence of financial socialisation on decision-making power is weaker for females than males (Gender = Female 0; Male 1). It indicates that acquired knowledge from financial socialisation is not transmitted into actionable knowledge for females. Due to cultural and societal norms, there are barriers to female participation in household financial decision-making processes. The results reveal that financial socialisation positively impacts decision-making power (β = .034; SE = 0.008; 95% CI [0.019, 0.050]). This supports hypotheses 1 and 3, which propose that FS has a positive impact on DMP and that DMP mediates the relationship between FS and RTB. Further, a stronger effect was observed in males, supporting hypothesis 5a. This implies that financially socialised people often take the role of decision-makers in a household. Hence, people should acquire financial knowledge from the implicit and explicit environment for better household financial decision-making and management. Therefore, policymakers should design a financial literacy programme tailored for rural households. Similarly, the age of household members has a positive impact on their decision-making power in the household (β = .034; SE = 0.008). This implies that as individual members in rural households grow older, their decision-making power and responsibility for financial outcomes increase. Notably, an individual’s general education and income in a rural household do not influence their financial decision-making power. This result contradicts claims by earlier studies that income and educational qualifications impact a person’s financial decision-making power.

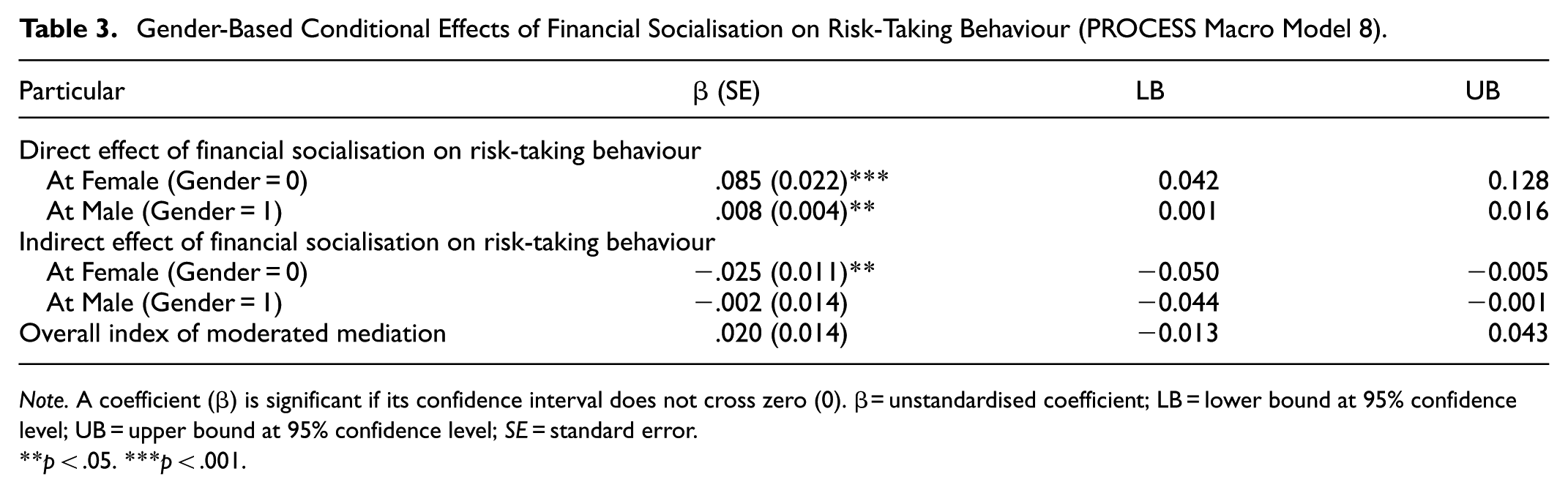

The conditional effects of financial socialisation on risk-taking behaviour are presented in Table 3. The direct effect states that financial socialisation has a significantly positive impact on female risk management (β = .085; SE = 0.022; 95% CI [0.042, 0.228]). Financially socialised females’ risk-management behaviour is sharpened. It implies that financial socialisation empowers females to take calculated risks. Similarly, financial socialisation significantly impacts male risk-management behaviour. However, this impact is less than that of their counterpart (Females).

Gender-Based Conditional Effects of Financial Socialisation on Risk-Taking Behaviour (PROCESS Macro Model 8).

Note. A coefficient (β) is significant if its confidence interval does not cross zero (0). β = unstandardised coefficient; LB = lower bound at 95% confidence level; UB = upper bound at 95% confidence level; SE = standard error.

p < .05. ***p < .001.

A notable point from Table 3 is that the indirect effect, that is, mediated through decision-making power, is significant but negative for females (β = −.025; SE = 0.011; 95% CI [−0.050, −0.005]). This suggests that women limited decision-making power in households hinders their risk-management capacity. Meanwhile, the indirect effect on males is insignificant. This implies that males have higher decision-making power in their families; hence, it does not significantly mediate the relationship between financial socialisation and risk-management behaviour. Although the direct and indirect mediation effects of decision-making power differ between males and females, the overall moderating mediation is insignificant. This supports hypothesis 2 for females, where FS significantly predicts the RTB, but this effect is weak for their counterparts (males). Further, hypothesis 4 is supported among females through significant indirect effects via DMP, while the mediation pathway is not significant for males. Furthermore, these findings support hypothesis 5, which suggests that gender moderates both direct and indirect effects. This implies that financial socialisation benefits are not the same for males and females, as the indirect effect for males is insignificant, while for females, it is significant.

As discussed in the literature section, various studies have found that an individual’s marital status influences their financial commitment and responsibility. Hence, here, we have examined the interaction of marital status in the relationship between financial socialisation, decision-making power, and risk-taking behaviour. The influence of Financial socialisation on decision-making power and risk-taking behaviour, with moderated mediation by marital status, is shown in Table 4.

Results of Marital Status and Financial Socialisation Moderated Mediation Analysis – PROCESS Macro Model 8.

Note.β = unstandardised; LB = lower bound for 95% confidence level; UB = upper bound for 95% confidence level.

F-statistics df: (8, 303).

p < .10. **p < .05. ***p < .001.

Table 4 indicates that the interaction between decision-making power and marital status is significantly negative, with a β value of −.084 (SE = 0.018). This suggests that marital status limits the influence of financial socialisation on an individual’s decision-making power. It implies that the married person considers the spouse’s input while making financial decisions. Age (β = .138, p < .01) is positively correlated, and investment experience (β = −.104, p < .05) has a significant negative impact on decision-making power. Interestingly, educational qualifications and income do not significantly influence decision-making power. Overall, the model explains 12.7% of the variance in decision-making power, and the model is significant and well-fitted (F = 6.323, p < .001).

The underlying risk-management behaviour is statistically significant and positive when all the independent variables are constant. Financial socialisation does not significantly influence risk-management behaviour, but decision-making power has a significant and negative influence on it. It is suggested that the decision-making power, along with responsibility, hinders the risk-taking behaviour of decision-makers in a household. An insignificant β value of −.047, p > .05, indicates no interaction between financial socialisation and marital status. Similarly, age, investment experience, and income also do not significantly affect the risk-taking behaviour of household members. Education and decision-making power have a negative impact, and financial socialisation, age, and investment experience influence decision-making power. Most notably, marital status deteriorates the relationship between FS and decision-making power. These findings support hypotheses 1 and 3, confirming a positive relationship between FS and DMP, and that DMP mediates the relationship between FS and RTB.

The results of the conditional effect of FS on risk-taking behaviour are shown in Table 5. The FS has a significant and positive direct impact on the risk-taking behaviour of unmarried persons with a β of .091, SE = 0.018, 95% CI [0.056, 0.126], p < .001. This implies that unmarried people take more risks as the FS fuels confidence through awareness. Similarly, the financial socialisation of a married person has a significant and positive impact on risk-taking behaviour with β = .007, p < .05. However, this effect is small compared to that of unmarried persons. It is clear from the results that married people are more cautious when making financial decisions due to their responsibilities.

Marital Status-Based – Conditional Effects of Financial Socialisation on Risk-Taking Behaviour (PROCESS Macro Model 8).

Note. A coefficient (β) is significant if its confidence interval does not cross zero (0). β = unstandardised coefficient; SE = standard error; LB = lower bound at 95% confidence level; UB = upper bound at 95% confidence level.

p < .05. ***p < .001.

Financial socialisation has a positive direct effect on risk-taking behaviour for unmarried people compared to married people. Decision-making power does not significantly mediate the relationship between FS and risk-taking behaviour. The overall index of moderated mediation indicates no significant difference in how the decision-making power interacts with FS and risk-taking behaviour.

Discussion

The financial socialisation of a person helps in acquiring financial knowledge, making financial decisions, and calculating risk (Abdul Ghafoor & Akhtar, 2024; Agnew & Sotardi, 2024; Boto-Garcìa et al., 2022; Rahman, 2019). However, there is a gap in the literature that explains this phenomenon in a patriarchal society, as well as the moderating and mediating mechanisms in the relationship. This study aimed to fill this gap by adding value to the literature, stating that decision-making power has an existing mediating role and that gender and marital status have a moderating role in the relationship between FS and risk-taking behaviour. It is important to note that although several effects were statistically significant, some of the effect sizes were modest. Hence, the findings are interpreted as indicative rather than causal.

Financial socialisation has a significant negative indirect relationship with risk-taking behaviour. Increased financial socialisation increases a person’s decision-making power, but this increased decision-making power may create cautiousness and a sense of financial responsibility. Hence, they show risk-aversion behaviour. Hence, it can be concluded that the decision-making power is a counterforce among the rural household members. It is because of their responsibility towards the family’s financial well-being. This result aligns with the findings of and Jorgensen et al. (2017). The study found a positive direct relationship between FS and risk-taking behaviour for females, but it was not very important for males. This result aligns with the study by Anthony et al. (2022). It implies that in a male-dominated society, though females are financially literate and capable of better decision-making, their opinions are ignored due to societal and cultural practices. However, these differences are more pronounced in urban households or non-patriarchal societies. This was highlighted as urban household members make financial decisions jointly, based on the merits of the opinion, rather than the person (Goyal & Kumar, 2020). However, it should be considered that the overall moderate mediation index by gender is insignificant, indicating that these differences are more evident in direct and indirect paths but not in the overall interaction. Further, as found in another study (Phung et al., 2021), the interaction between decision-making power and subjective risk-taking is negatively associated with the objective risk-taking behaviour of investors. Notably, gender-based decision-making power did not significantly determine the risk-taking behaviour of household investors, likely due to the authority of investors in the household financial decision-making process, as pointed out by Sharma and Kota (2019). The findings reiterate that rational financial decision-making is not always objective and is influenced by subjective factors. As highlighted in the literature (Suresh, 2024), financial literacy plays a dynamic role in rational decision-making. These findings help policymakers design a financial literacy programme that considers societal and cultural norms, as one-size-fits-all approaches are not effective. Government existing initiatives, such as PMJDY and SHG programmes, could be further strengthened by incorporating context-specific FS approaches, focusing on female autonomy and culturally embedded decision-making dynamics. To strengthen rural households’ financial capability, policymakers can establish village-level financial counselling centres and introduce practical, simulation-based financial training for women to enhance real decision-making experience. This study also found that educational qualification does not significantly affect the relationship between FS and decision-making power. These results suggest that cultural and social norms play a significant role in this relationship. It should be studied further to explore the reasons for the challenges faced by females in decision-making power and the effectiveness of various types of financial socialisation, among other factors. Furthermore, this study considered only the respondents’ educational qualifications and not those of other members, which should be studied further, as these may influence decision-making power and risk-taking behaviour.

Conclusion

This empirical study examined how financial socialisation influences rural households’ decision-making power and risk-taking behaviour, specifically focusing on the moderating role of gender and marital status. Financial socialisation was measured using a validated scale adapted to the rural Indian context. At the same time, decision-making power and risk-taking behaviour were assessed through single-item measures grounded in earlier studies. Gender and marital status were tested as moderators, with age, income, investment experience, and educational qualification included as control variables.

The results reveal that FS has a significant positive direct effect on risk-taking behaviour in females, whereas it is weaker in males. It reflects persistent structural constraints in patriarchal rural households. These findings highlight the need for tailored financial literacy and empowerment initiatives that consider gender and marital status-based populations in their financial behaviour. Similarly, marital status moderates the relationship, such that unmarried individuals exhibit a higher risk-taking tendency, likely due to their minimal family responsibilities. These findings indicate the need for nuanced financial education in rural patriarchal settings. The indirect effect via decision-making power was negative and statistically significant for females, suggesting that even when financially socialised, greater decision-making responsibility may induce cautious financial behaviour. For males, the mediation was weak and insignificant. Although the overall moderated mediation was not significant, the gender-based pattern suggests that the rooted social norms influence financial agency. It advocates that future research should explore the model with a larger sample size and additional moderating variables, such as digital access or intra-household dynamics.

Importantly, the study confirms that financial socialisation enhances decision-making power, with gender and marital status moderating this relationship. These interaction effect results highlight the ongoing gender disparities in household financial autonomy. Policymakers should consider region-specific, gender-sensitive programmes to promote equitable financial inclusion. Additionally, financial institutions must design accessible decision-making tools and training that cater to the realities of rural households. To conclude, while financial socialisation is an important lever for financial empowerment, its effects vary by gender and marital status.

Limitations and Scope for Future Research

The present study has certain limitations to set a platform for future research. The limitations are

Though the use of snowball sampling helps to target the hidden population, it limits the external validity of findings. Furthermore, the responses captured are primarily from interconnected groups, which may potentially impact the generalizability of the findings. Therefore, future studies can be conducted using random sampling techniques to enhance the generalizability of the results.

The present study adopted a widely used single-item scale to measure decision-making power and risk-taking behaviour. Although it is well recognised in a large-scale survey of a constrained rural environment, they restrict the reliability and validity of these measures. Multi-item measures may provide a strong evaluation of individual psychometric properties and capture multiple dimensions of the constructs. Hence, future studies can adopt multi-item measures to capture the decision-making power and risk-taking behaviour.

Footnotes

Ethical Considerations

Since the study did not use sensitive information about individuals, ethical approval is not required per the institute’s research ethics policy.

Consent to Participate

Informed consent was obtained from all participants prior to data collection. Participants were informed about the purpose of the study, their right to withdraw at any time, and the confidentiality of their responses. No personal identifiers were collected. The study design posed minimal risk to participants, and participation was entirely voluntary.

Author Contributions

Gopal Suresh: Conceptualisation, data curation, data analysis, methodology, project administration, and original draft. Jothi Munuswamy: Conceptualisation, Investigation, writing, reviewing, and editing. Prakash M.: Conceptualisation, Investigation, writing, and editing.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

Data will be made available on request.