Abstract

This paper analyzes the multiple transmission mechanisms of the real estate industry’s risk spillovers to the financial industry. A GARCH-time-varying-copula-CoVaR model is used to measure the spillover effects and dynamic evolution trends of risk in the Chinese real estate industry. The results show that (1) in recent years, the risk spillovers from the real estate industry to the whole financial industry in China has been relatively high, and the possibility of systemic risks has increased. (2) The channel of the risk spillovers of the real estate industry into the financial industry has shifted from being concentrated within a traditional single banking industry to the accumulation and superposition of risk across the banking, securities, trust industries. (3) Current regulations have not fundamentally mitigated the risk spillovers. As such, this paper proposes three suggestions on financial policies and regulations: firstly, the government should reasonably regulate cooperation between the real estate industry and the financial industry, curb excessive speculation and abnormal fluctuations in real estate prices. Secondly, the government should maintain the continuity of regulatory policies, formulate differentiated policies according to the essential attributes of given industries, and eliminate risk contagion among the real estate industry and financial industries. Thirdly, the government should improve the macro prudential management framework.

Introduction

The operation of the Chinese real estate industry—including the supply and demand for real estate, land transfers, housing developments, construction funds and house purchase funds—is closely related to financial services. The real estate industry is a pillar industry of the national economy. When the real estate industry experiences abnormal fluctuations, there are likely to be risk accumulations, spillovers, and contagions that can damage the financial stability and even the healthy and sustainable development of national economy. Take the experience of other countries as an example, Japan’s stock market and real estate bubble emerged in the middle and late 1980s. In addition, the global financial crisis in 2008 caused by the U.S. subprime mortgage crisis is directly related to many defaults of mortgage-backed securitization products.

Since the early 2000s, China’s excessive growth in housing prices, overheated investments, and supply-demand mismatch in the real estate market has led to the development of real estate bubbles. According to the Wind database in China, China’s real estate investment increased by 874.08% and the scale of real estate mortgage loans has maintained a growth rate of roughly 20% from 2005 to 2015. In the first-tier cities of China, house prices have increased by 255.1% during the same period. Thus, the real estate market has already dominated the trend of China’s macroeconomy for a long period (Lu & Liu, 2013). To avoid the economic and financial risks caused by falling house prices, the Chinese government has taken many measures to reduce the liquidity supply of banking to the real estate industry by strictly restricting financing channels, loan interest rates and the down payment ratio. At the end of 2016, the Chinese central government issued a directive that “housing is for living in and not for speculation.” At the Central Economic Work Conference, which is China’s top annual economic meeting that guides next year’s development, held at the end of 2017, preventing and defusing financial risks were deemed vital to fighting the “three tough battles” against major risks, poverty and pollution. The real estate industry and financial industry are the key areas of financial regulation, yet even during the COVID-19 pandemic, the real estate regulatory policy has undergone no significant changes.

However, the domestic real estate market remains overheated in recent years. According to the data released by China’s National Bureau of Statistics, in 2017, the national real estate development investment was RMB 1,0979.9 billion yuan, which represents a nominal increase of 7.0% over the previous year. In 2018, the national real estate development investment was RMB 1,2026.4 billion yuan, which represents an increase of 9.5% over the previous year and accounts for 18.92% of the fixed assets investment. In 2019, the national real estate development investment was RMB 1,3219.4 billion yuan, which represents an increase of 9.9% over the previous year. Even under the impact of the COVID-19 pandemic, the national real estate development investment reached 6,278 billion yuan in the first half of 2020, and it still maintained a positive annual growth rate of 1.9%. However, with the adjustment of the housing prices in the economic downturn, the risk of bad debts among real estate enterprises is gradually being exposed. From the perspective of the financing volume, the government’s regulatory policies cannot effectively curb the real estate craze in China. The capital inflow of the real estate industry is still increasing, but excessive capital in a certain field does not mean that there is excessive risk in that field. Further research should be carried out.

In brief, there are several basic but important issues that have become the focus of government agencies, economists, market analysts, and residents in China following the 2008 financial crisis. These issues have raised several important questions about the risk spillover of real estate industry, including the following points to be addressed in this article:

(1) What are the new changes to the risk spillover mechanism between the real estate industry and the financial industry following the 2008 crisis?

(2) How can we evaluate the dynamic evolution trend of the risk spillover effect between the real estate industry, the financial industry, and each sub-industry of financial industry?

(3) Does the regulation policy contain the spillover and contagion of real estate risk for the financial sector? Can current policies maintain the stability and sustainable development of the real estate and financial industries?

To address these questions, this paper analyzes the mechanisms of risk spillover between China’s real estate industry and financial industries in a multiple transmission framework based on different financing channels. Then, the paper proposes a GARCH-time-varying-copula-CoVaR model to measure the real estate industry’s risk spillover intensity as well as analyzes the dynamic structure and evolution trend of the risk spillover. To test whether China’s real estate financial risk spillover is further intensified by the boom of real estate industry, we examine whether this structure induces systemic risk. Finally, the paper provides suggestions for China’s government to prevent real estate financial risks and promote the healthy and sustainable development of the real estate and financial industries.

Literature Review

Research on the Risk Spillover Mechanism of the Real Estate Industry to the Financial Industry

In 2007, the burst of the US real estate market bubble triggered a subprime mortgage crisis, which led to a tsunami shock of the whole financial system, resulting in the volatility of the global financial market and a recession of the real economy in 2008. Therefore, the risk relevance and spillover effect of the real estate sector to the financial system has drawn public attention around the world.

Some scholars have conducted studies on the risk spillover mechanism of the real estate industry to the financial industry (Chaney et al., 2012; Cvijanović, 2014; Davis & Zhu, 2011; Goodhart et al., 2006; Herring & Wachter, 1999). These scholars mainly focus on the impact of real estate market price fluctuations on the financial industry and the interaction between those two industries on the financial stability. According to Herring and Wachter (1999), banks are willing to underestimate the credit risk of real estate to boost the real estate boom, which will eventually lead to a financial crisis. Davis and Zhu (2011) found that there is a close correlation between the real estate market, monetary policy, and financial stability. Goodhart et al. (2006) added individual heterogeneity, the default behavior and other factors into their model to simulate the rapid decline of house prices in the United States in 2008. In addition, these authors analyzed these prices’ impact on financial institutions and pointed out that the several global financial crises show that the fluctuation of the real estate market is often an important factor that induces a financial crisis and crisis contagion. Meaning evaluated the role of the real estate market price in the business cycle and growth in his published works and confirmed that there are some potential structural impacts of real estate prices on the population growth, the real estate financial system, and other related factors (Maennig, 2011). Chaney et al. (2012) conducted research on American companies that shows that the real estate price fluctuation has an impact on the stability of the financial system by spreading to corporate finance, bank credit and other financial fields through guaranteed business in some investment activities. Cvijanović (2014)’s empirical analysis of developed countries such as the United States shows that real estate prices have a significant impact on the company’s capital structure, and this effect tends to strengthen during a real estate bubble.

In recent years, some domestic scholars have focused on the risk spillover mechanism and the transmission effect of the real estate industry on the financial industry (Sun et al., 2019; Liu & Luo, 2000; Qi, 2015; Shen et al., 2016). Liu and Luo (2000) early analysts believe that a large quantity of capital from China’s bank entered the market, which led to the emergence of the real estate bubble and the risk accumulation of the banking sector. A financial crisis would be triggered once the bubble burst in the real estate market. Qi’s (2015) research results show that bank credit stability is more vulnerable when the real estate price is falling. Shen et al. (2016) pointed out that the excessive fluctuation of house prices has an obvious systemic risk spillover effect on the economy, and they show heterogeneities in economic sectors, among which the most significant is within financial institutions. Further research by Sun et al. (2019) found that the real estate industry has a larger risk spillover intensity on the joint-stock banks and urban commercial banks than on the state-owned banks. Indeed, the risk, scale and debt level of real estate enterprises have significant risk spillovers onto financial institutions.

Studies Measuring the Risk Spillover From the Real Estate Industry to the Financial Industry

In the research on the measurement of the real estate industry’s risk spillover to the financial industry, many literatures evaluate this risk by estimating the correlation between financial institutions. The traditional measurement method has a good effect in studying the correlation relationship to measure the risk spillover, such as Granger causality, multivariate GARCH (Generalized Auto Regressive Conditional Heteroskedasticity) and vector autoregression (VAR). The Granger causality test can analyze the causal relationship between variables and has a significant effect on identifying the correlation degree of a risk spillover. Using the Granger causality test method, Shun and Kangping (2004) found that China’s real estate market and financial market are mutually causal and there is risk symbiosis between them. Using the multivariate GARCH model, Booth et al. (1997) found that there is an asymmetric risk correlation between the real estate market and the financial market. Tan and Wang (2011) believe that the risk spillover relationship between the house price, the credit volatility, and their joint volatility is significant; these authors combined the dynamic stochastic general equilibrium framework with multivariate-GARCH-model empirical analysis. Baffoe-Bonnie (1998) demonstrated that there is a certain degree of correlation between the periodic fluctuation of house prices and the risk spillover of the financial system by constructing a VAR model. Wen et al. (2012) used a VAR model analysis and pointed out that the impact of the real estate price fluctuation on the financial vulnerability in the short and long terms is different.

However, these traditional measurement methods find it difficult to accurately describe the spillover effect of risk. Among the methods of measuring the risk transmission and spillover across industries, though the correlation between industries is the key point of the model setting, the above methods mainly use quantile methods to establish inter-industry correlations. However, quantile methods have great defects in their accuracy. Patton (2006) established a multivariable financial time series model based on Copula theory. This model has the characteristics of time-varying data, peaks, and thick tails, which can effectively solve the problem of insufficient precision. Adrian and Brunnermeier (2016) proposed the CoVaR model based on the VaR model. The CoVaR model measures the value of the entire financial system when a sector is in trouble to reflect the sector’s risk spillover status with respect to the financial system. Then, Adams et al. (2014) used the CoVaR model to analyze the risk spillover effect among financial institutions. Liu and Gu (2014) constructed the AR-GARCH-CoVaR model and found that banks’ credit to the real estate industry may overflow, spread, and become a systemic risk to the entire financial system.

Gaps in Current Literature

In summary, the relevant literature mainly focuses on the risk spillover mechanism and risk spillover measurement. Regarding the risk spillover mechanism, a large amount of literature focuses on the transmission mechanism of risk spillovers from the real estate industry to the banking industry. Throughout the financial industry, this dataset is often replaced by relevant data from the banking industry. There is still a lack of comprehensive analyses of different real estate financing channels, particularly given the rapid development of the shadow banking system in China after the 2008 crisis.

In terms of risk spillover measurements, traditional analysis methods have obvious limitations: the Granger causality test can only describe qualitative causality and cannot measure the specific value of the risk spillover effect, while the VaR (value at risk) method and multivariate GARCH model require the existence of and limitations to variable variance. In practice, financial time series variables often cannot meet this requirement of those models. It is difficult to capture the tail correlation of the market in an empirical analysis, and the results of risk measurement are often underestimated. In contrast, the Copula function can better overcome the limitations of traditional methods for studying the risk spillover relationship and the measurement of risk spillover intensity. In the process of model construction, the Copula function can measure key parameters such as variance and correlation coefficients. For example, Zhang and Zhao (2021) tested the dynamic dependence between West Texas Intermediate (WTI) crude oil and New York Harbor (NYH) daily natural gas prices by using time-varying Copulas. With the marginal models AR(p)-GJR-GARCH(P, Q)-skewed-t, they found that time-varying rotated geometric Gumbel Copula performs better than time-invariant Copulas. Garcia-Jorcano and Benito (2020) compared five Copula models—Gaussian, Student-t, Clayton, Gumbel, and Frank—to analyze the properties of Bitcoin as an asset for diversifying and hedging the movement of international market indices; they found that the Gaussian and Student-t Copulas are the best fit for the structural dependence between markets. Additionally, Pho et al. (2021) analyzed the daily data of Bitcoin and gold over the 2010 to 2020 period by constructing a new Copula-based joint distribution function of returns. They argued that Bitcoin and gold are portfolio diversifiers that have different disadvantages for different risk investors. Nguyen et al. (2020) also used a Copula model, namely the Archimedean and elliptical Copula, to verify that gold is an effective and robust hedge or safe-haven asset. Yang et al. (2015) determined that the application of the hierarchical Archimedean Copula model could accurately identify dependence among international stock markets. When measuring risk spillover intensity, CoVaR’s accuracy is much higher than other models. For example, when comparing several models, Yanget al. (2018) found that the combination of CoVaR and Copula can more accurately identify the spillover effects of systemic risk and global financial crisis on countries with weak economic fundamentals (such as Hungary, which has the highest systemic risk) and contagion effects on two countries with high dependence. In addition, Yang et al. (2020) analyzed the daily data of China’s credit bond market from December 28, 2009, to June 2, 2017, by using the dynamic Copula-CoVaR model. They showed that the dynamic model is more effective than others in measuring risk spillover effects.

In view of the deficiencies of existing risk spillover measurement models, this paper proposes a GARCH time-varying Copula CoVaR model, which combines the advantages of the GARCH, time-varying Copula, and CoVaR models. The proposed model is more in line with China’s current level of financialization, financial structure, and financial system. To better fill the research gap regarding risk spillover mechanisms, we extend the research perspective to the banking, securities and trusts of the financial industry and test the risk spillover and contagion effects of China’s real estate industry on the financial industry. This paper provides empirical evidence to support the improvement of China’s real estate financial risk prevention and control system.

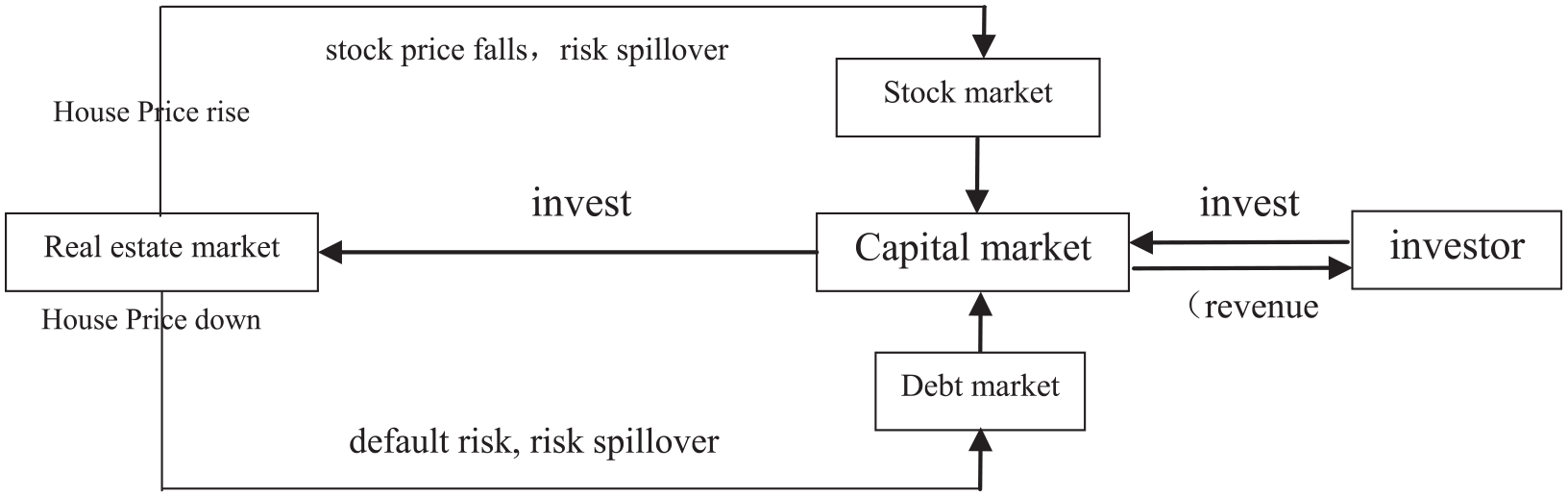

The Multiple Risk Spillover Mechanisms Between the Real Estate Industry and Financial Industries

In recent years, according to the Wind database, the financial channels of China’s real estate industry have mainly relied on indirect financing from the banking sector, which accounts for 40% to 50% of the total financing. Within these funds, trust loans peaked in 2010, when they accounted for more than 20% of the total financing. However, due to the frequent redemption crises since 2015 in China, the proportion of trust loans has fallen below 10%. The proportion of equity financing for large real estate companies has maintained a steady upward trend and now accounts for approximately 30% of corporate financing. Most real estate companies have begun to use bond financing in recent years, and these bonds have shown such explosive growth since 2015 that they account for more than 10% of the total financing. While the financial system promotes the prosperity of the real estate industry, it also experiences real estate market risk spillovers through various subsectors of the financial industry. As the main area of investment in the financial sector, the real estate industry continuously expands its business and accumulates risks during market booms. When the economy is in recession, the real estate industry’s risks will overflow across the market to the financial sector and spread among other financial institutions, which will form a systemic shock to the financial industry. Therefore, clearing out the risk spillover mechanism of real estate risks in various financial subsectors is more conducive to a comprehensive analysis of the transmission path and performance characteristics of China’s real estate financial risks in the new era, and this lays a theoretical foundation for the estimation of the risk spillovers’ intensity.

The Risk Spillover Mechanism Between the Real Estate Industry and the Banking Industry

The process of real estate risk overflowing from the real estate industry to the banking industry is the process by which the real estate industry affects the stability of the banking system. The core channel is the banking system’s credit business with the real estate industry. The transmission process is accompanied by asymmetric information caused by prices’ fluctuations in the real estate market. This pattern has greatly affected the banks’ credit allocations and the sound business decisions of related businesses within China. The transmission mechanism of the real estate industry’s risk to the banking industry’s risk is shown in Figure 1.

The risk spillover mechanism between the real estate industry and the banking industry.

The Risk Spillover Mechanism Between the Real Estate Industry and the Securities Industry

The risk spillover effect between the real estate industry and the securities industry is mainly conducted through two transmission paths: equity financing and bond financing of real estate companies.

From the perspective of the equity market, there are 151 listed real estate companies in China’s A-share market, and basically more than 80% of them are financed by designated placements according to the Wind database. Especially for small and medium-sized developers, the barrier of access to credit financing is high, and equity financing has become an important channel for small and medium-sized real estate companies to improve their competitiveness in recent years. In the bond market, a considerable number of the issuers of corporate bonds are real estate companies, which account for 74% of the total according to the Wind database. With the diversification of the financing methods of real estate enterprises, traditional indirect financing has gradually shifted to direct financing in the securities market, and the contagion and spillover effects of the real estate industry’s risks on the securities industry have become increasingly obvious. The risk spillover mechanism between the real estate industry and the securities industry is shown in Figure 2.

The risk spillover mechanism between the real estate industry and the securities industry.

The Risk Spillover Mechanism Between the Real Estate Industry and the Trust Industry

In 2009, China began to regulate and restrict the overheated real estate market by using macro policies. Indirect financing constraints for real estate companies to obtain credit financing increased, and the government strictly controlled the traditional financing channels. Many small and medium-sized developers who fail to meet the credit financing requirements or large developers with tight funds have had to seek new financing channels, which objectively promotes the rapid development of the shadow banking system represented by the trust industry. According to data released by the China Trustee Association, the scale of the real estate trusts reached 2.7 trillion yuan, and the trust industry has become the main financing channel for real estate enterprises in 2018. However, in the second half of 2019, the regulatory authorities issued a Trust Document on “removing the bank-trust cooperation business, controlling real estate trusts, and optimizing the structure of the trust business,” which was meant to curb the disorderly expansion of the trust business. The peak period of real estate debt payment was also in 2019 (Qian & Wenping, 2018), and it was coupled with the deterioration of the financing environment and a plethora of negative information about real estate trusts, which contributed to the increasing possibilities for the transformation of the real estate debt risk to financial risks. The risk spillover mechanism between the real estate industry and the trust industry is shown in Figure 3.

The risk spillover mechanism between the real estate industry and the trust industry.

The Measurement of the Risk Spillover Effect of the Real Estate Industry on the Financial Industry Based on the Copula-CoVaR Model

A GARCH-time-varying-copula-CoVaR model is established to verify the correlation between the real estate industry and the financial industry. According to the transmission characteristics of real estate financial risks, we employ the principle of risk spillover and conditional value at risk technology (CoVaR) proposed by Adrian and Brunnermeier (2016). Based on the dynamic time-varying correlation between real estate and finance industry subjects, the risk spillover effects of the real estate industry on the financial system and the various subsectors are measured. At the same time, through dimensionless processing, this correlation relationship could be expressed as a risk contribution of individual

CoVaR Model

The CoVaR refers to the maximum loss of an individual

By dividing

Measurement of the CoVaR Based on the Time-Varying-Copula-CoVaR

The key to the CoVaR measurement is the conditional probability density calculation. Then, the CoVaR can be obtained by an integral method with a variational limit. When modeling, the conditional joint distribution function as well as the conditional mean, variance and nonlinear correlation coefficients can be calculated more accurately by using the Copula function instead of a quantile method.

There is a precondition for using the Copula function, that is, it must conform to the Sklar theorem: when F is a two-dimensional joint distribution function with marginal distributions F1 and F2.

There exists a Copula function

Therefore, a density function can be derived from Sklar’s theorem:

where

Regarding the marginal distribution, the monotonic transformation does not change the corresponding Copula function according to Sklar’s theorem. Therefore, the research on the return of each stock can be transformed into the research on the return residual. Since financial time series often do not follow the normal distribution in practical applications, this paper adopts the skewed-t distribution in the modeling process and establishes the

First, this paper analyzes the revenue of each financial subsector by constructing the

where

Second,

where

Finally, we can obtain the time-varying risk spillover effect △

Empirical Results and Analysis

Data and Statistical Description

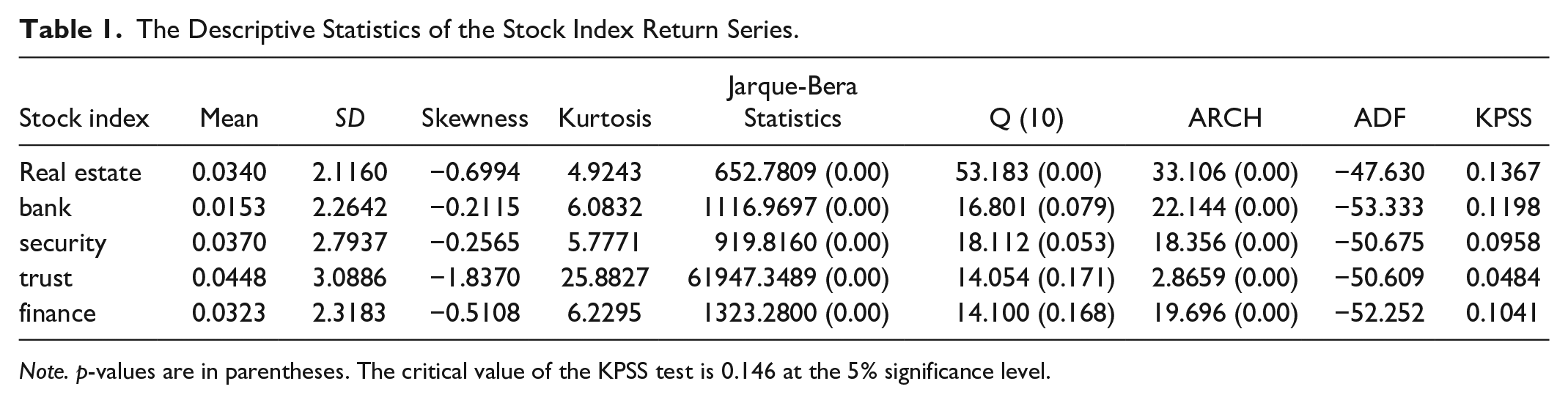

The data in this paper are mainly from the Wind and CSMAR databases. The real estate stock index according to the CITIC Securities industrial classification is used to represent China’s real estate industry, and the banking, securities, and trust sector indices are used to represent the banking, securities, and trust industries, respectively. These indices are the weighted sum of the market value of listed enterprises in related industries. There are some flaws inherent to the use of these indices. For example, the number of listed enterprises in the trust industry is small, and some of the companies included in the indices only participate in trust enterprises, though their main business is not financial fiduciary. As such, this paper cannot fully reflect the true cross-industry risk spillover and should instead be considered to test the spillover situation of related stocks in different industries, which is then used to approximate the risk spillover situation between industries. The sample contains the daily closing prices from January 4, 2006, to December 29, 2017, with a total sample size of 2,917 groups. And this time series has very important research significance because this time period covers important economic events in in the world economy, such as the US subprime mortgage crisis, China’s “four-trillion-stimulus plan,” China’s repayment crisis of the trust industry in 2013 to 2014, and China’s “no speculation on housing” policy in 2016. Despite the issuance of new regulations on asset management in 2018, the old business model of most financial institutions still exists; hence, the new business model is not stable. Consequently, the data after 2018 are of less importance in empirical research.

The daily return rate can be calculated by the equation

The Descriptive Statistics of the Stock Index Return Series.

Note. p-values are in parentheses. The critical value of the KPSS test is 0.146 at the 5% significance level.

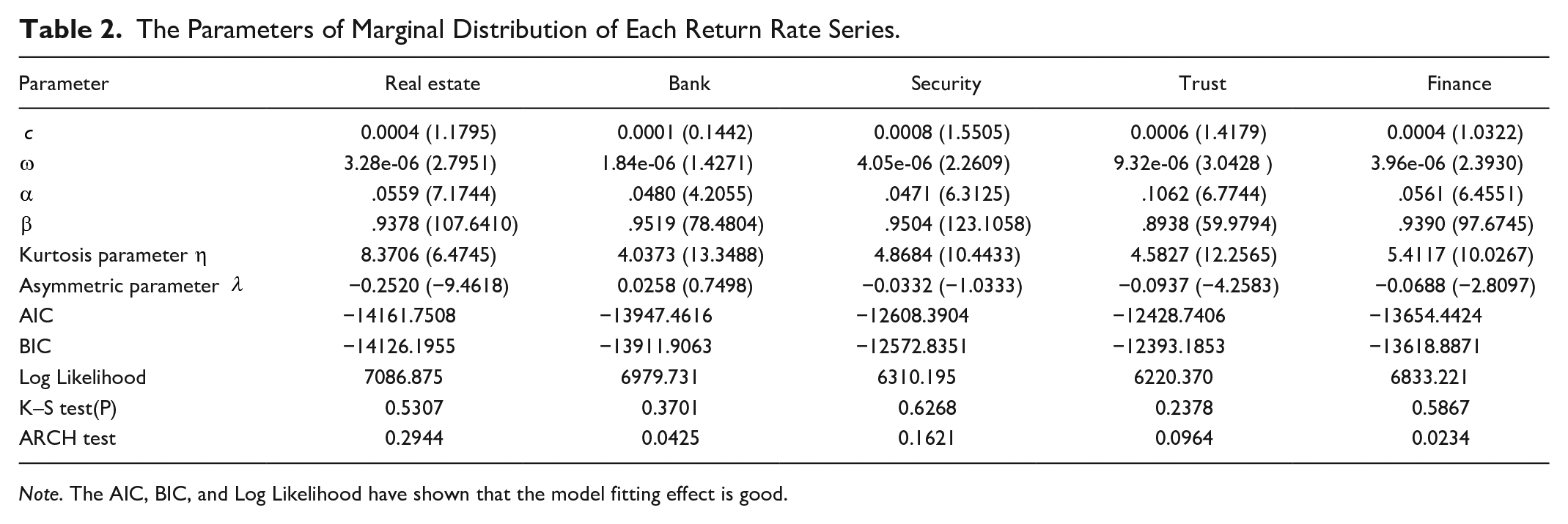

Estimation of Marginal Distribution Model

The traditional GARCH model requires the residuals to obey the normal distribution. However, in recent years, some scholars have believed that the residuals are more in line with the skewed-t distribution. Therefore, this paper assumes that residual series of the GARCH model obeys a skewed-t distribution and use ARMA(0,0)-GARCH(1,1)-skewed-t model to estimate the marginal distribution of each return series. This model can be described as follows: Let ri, t denote the return of the i-th asset at time t. Then:

Thus, each marginal model has six parameters: parameter c in the mean equation, three parameters (ω, α, β) in the variance equation and two distributional parameters (η, λ), η and λ represent degree of freedom and asymmetric parameter of the skewed-t distribution. The parameters of marginal distribution of each return rate series are shown in Table 2.

The Parameters of Marginal Distribution of Each Return Rate Series.

Note. The AIC, BIC, and Log Likelihood have shown that the model fitting effect is good.

The K-S test shows that the skewed-t model can better fit the distribution characteristics of residuals, and the transformed series obey the uniform distribution on (0, 1). Furthermore, the 10-lag ARCH test shows that there are no autocorrelations, heteroscedasticities, and other problems in the transformed series. It can be seen that the ARMA(0, 0)–GARCH(1, 1)-skewed-t model can fit the marginal distribution of each series, and it is more effective to use it to describe the marginal distribution of each return series.

Estimation of the T-DCC-Copula Function

Based on the marginal distribution in section 5.2, this paper constructs a model to estimate the fitting parameters by choosing an optimal time-varying Copula function and a T-DCC-Copula function according to the AIC, BIC, and likelihood ratio. The T-DCC-Copula function is shown in equation (5) (see section4.2.), where the parameters to be estimated are

The Estimation of Parameters of T-DCC-Copula Function.

Note. The marginal distribution of each return series estimated in section 5.2 is used in the estimation of T-DCC-Copula function (equation (5)).

Dynamic Analysis of the Risk Spillover Intensity Based on a Time-Varying T-DCC-Copula Model

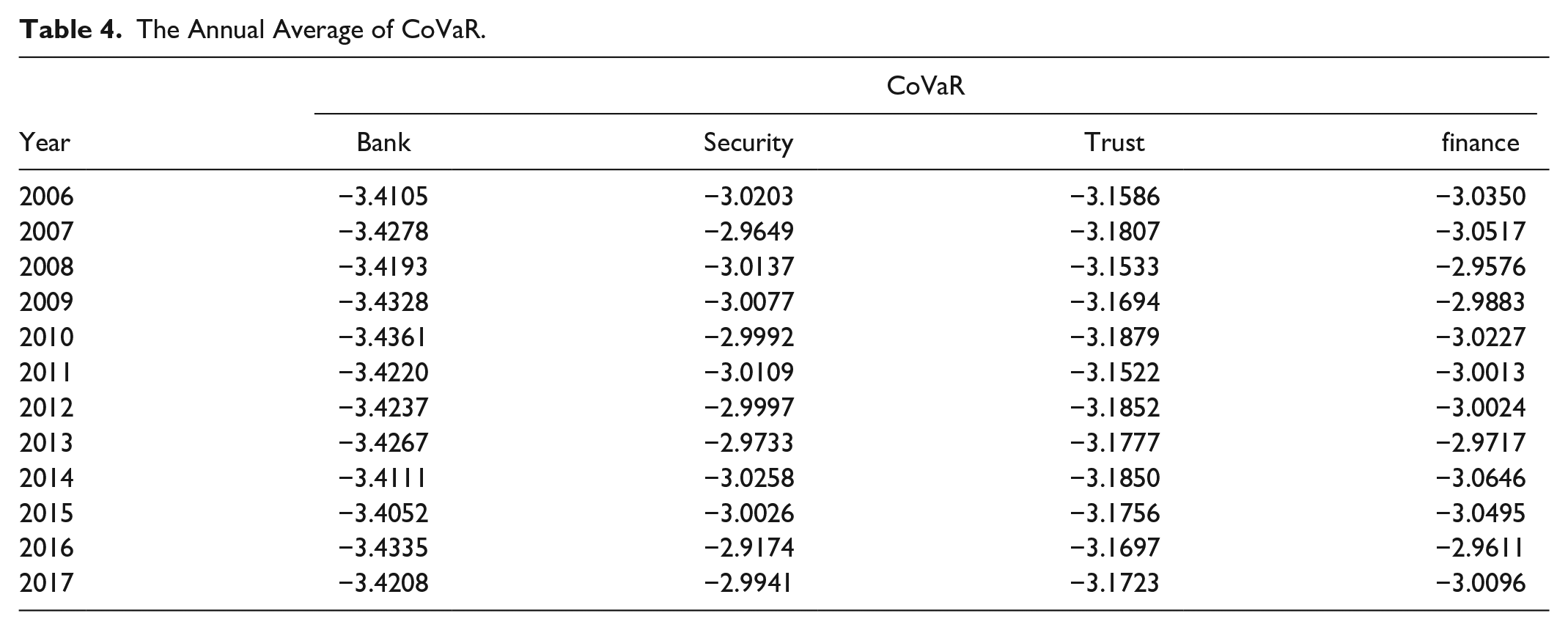

Table 4 shows the annual average CoVaR of the financial, banking, securities, and trust industries when the real estate industry reaches its value at risk (at a 95% confidence level). It can be seen that the annual average CoVaR between the real estate industry and the banking industry is obviously higher than the corresponding figures for the securities, trust, and financial industries overall, which indicates that the banking industry is more dependent on the real estate industry. It should be pointed out that the sign of CoVaR is usually negative, and its absolute value is generally used to express the risk spillover intensity. The larger the absolute value is, the higher the risk spillover intensity is. Moreover, the annual average CoVaR indicating the real estate industry’s risk spillover effect to the banking industry fluctuates very little; basically, there are fluctuations of the approximate average magnitude of 3.42. This behavior mainly occurs because China’s real estate policy has been mainly regulating banking credit loans since 2007. For example, in 2007, the People’s Bank of China and China Banking Regulatory Commission issued the notice on strengthening the Administration of Commercial Real Estate Credit loans. At the same time, the volatility of the annual average CoVaR between the real estate industry and the financial industry is much greater than the corresponding volatility of the banking industry, and in the years after 2012, the change trend of those two CoVaRs shows obvious deviations. At this time, the change trend of the annual average CoVaR of the securities industry and the trust industry is more similar to the trend of the financial industry as a whole. Hence, the banking industry is not the only way to realize the risk spillover from the real estate industry to the financial industry. There are other channels that affect the risk spillover effect of the real estate industry on the financial industry.

The Annual Average of CoVaR.

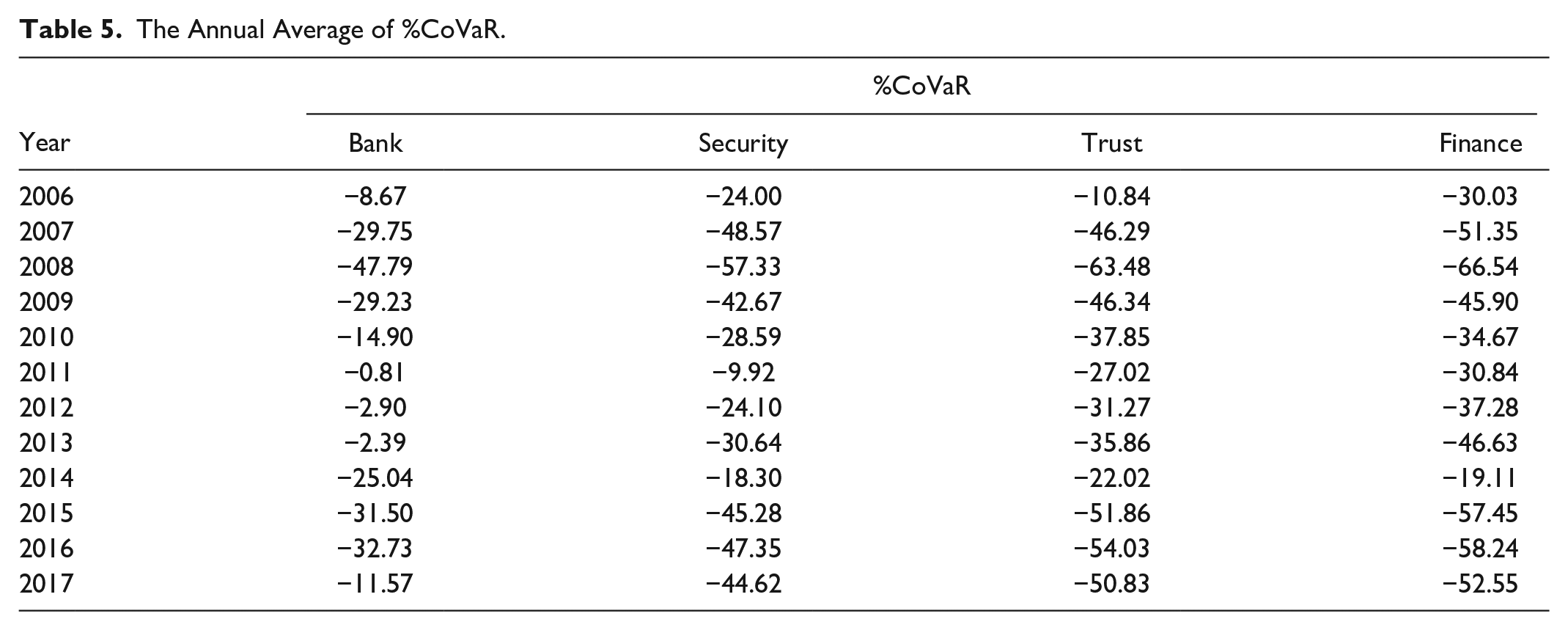

As mentioned previously, compared with the CoVaR, % CoVaR can more clearly reflect the risk spillover intensity and dynamic evolution trend from the real estate industry to the financial industry and its subindustries. The annual average and change trend of %CoVaR of the financial industry and each subindustry are shown in Figure 4 and Table 5. Since this article uses data from stock market, in Figure 4, the abscissa represents the n-th trading day from the starting date of the sample data. In China, there are about 250 trading days in a year. The ordinate represents the corresponding %CoVaR value.

The risk spillover intensity of real estate after 2006.

The Annual Average of %CoVaR.

Discussion

From 2006 to 2009, there is a similar trend of the risk spillover intensity of the real estate industry to the financial industry and the other subindustries, and the spillover intensity has deepened to varying degrees. In 2008, China issued a plan of four trillion Government Investment, a policy called the Chinese economic stimulus program, After that, both the real estate industry and the financial industry experienced rapid development (Fardoust et al., 2012; Qian, 2010). During this period, the real estate market and the financial sector have had a large capital penetration and strong linkage, which contributes to the increasing risk spillover effect of the real estate industry on the financial industry.

Since 2009, China has issued a series of regulatory policies for the real estate industry. With the introduction of various regulatory policies, the risk spillover intensity of the real estate industry to the financial industry declined for a period of time. However, the Table 5 shows that the risk spillover intensity of the real estate industry to the financial industry as a whole has been rising since 2011, and this rise has been very fast. Regarding each sub-financial market situation, the risk spillover intensity of the real estate industry to the banking industry remained at a low level and fluctuated slightly during this period, and it did not show a similar trend to the trend of the financial industry. However, the risk spillover intensity of the real estate industry to the securities industry and the trust industry showed a relatively similar trend to the trend of the financial industry in this period. The reason is that the real estate regulation policy tends to limit the capital supply from the banking industry to the real estate industry. After 2012, the financing mode of real estate enterprises changed from indirect financing to other methods, such as changing from banking financing to securities industry and trust industry financing. As a result, the policy of controlling the real estate risk spillover has no obvious effect. Therefore, it is difficult to effectively prevent the risk spillover of the real estate industry to the financial industry by focusing on the banking credit financing.

After the increasing of the case of payment crisis in trust industry around the year of 2014 in China, China’s supervision of the real estate trust has also tended to be strict. In addition, after the introduction of the housing mortgage policy in 2014, a number of measures to support the diversified financing of real estate enterprises have been implemented. Therefore, in 2014, the risk spillover effect of the real estate industry on the financial industry decreased rapidly, and it reached the lowest recorded level in history, namely, −19.11%.

However, in 2015, the risk spillover intensity of the real estate industry to the financial industry rose rapidly, which to a certain extent showed that the government’s strict purchasing restriction and differentiated credit policy did not have the intended effect. For each sub-sector of the financial market, there is also an increased risk spillover. First, in 2015 but not 2011 to 2013, the risk spillover intensity of the real estate industry to the banking industry showed a slight upward trend. Although the financing mode of real estate has been becoming more diversified and the dependence of the real estate industry on banking financing has been reduced, the problem of the risk spillover effect of real estate on the banking industry is still significant due to a high indirect financing scale. At the same time, to avoid financial supervision, banking sectors have accelerated their mixed operations. Second, the risk spillover effect of the real estate industry on the trust and securities industries increased rapidly in 2015; to a certain extent, it was not effectively restrained by regulatory policies, and it even realized a risk concentration through the shadow banking system to avoid supervision, which led to the aggravation of the systemic risk. In 2017, although the risk spillover intensity of the real estate industry to various sub-industries decreased, the decline rate of the banking industry was greater. Moreover, the overall decline rate of the securities, trust and financial industries was smaller, which indicated that the traditional single-mean policy regulation mode had not been fundamentally changed.

In recent years, China’s systemic risk sources and various forms of financial chaos have been closely related to the risk spillover and cross-infection of China’s real estate industry to the other financial industries in the new period. This connection is also an important reason for China’s central economic work conference at the end of 2016 to clarify the policy of “housing is for living in and not for speculation.” In fact, after this policy was issued, the risk spillover intensity of the real estate industry to the financial industry declined in 2017. However, under the background of accelerated financial mixed operations, single regulatory modes, regulatory system shortcomings and lagging supporting system infrastructures, the possibility of a systemic risk outbreak is still increasing, which endangers the healthily sustainable development of the real estate industry and the financial industry.

Conclusion

Limitations in previous empirical analyses of spillover risk relationships and intensity have resulted in inaccurate conclusions regarding the risk impact of China’s real estate industry on the financial industry Based on concrete analysis of the multiple transmission mechanism of the risk spillover among the real estate and financial industries, this paper constructs a GARCH-time-varying-copula- CoVaR model to measure the risk spillover effect of the real estate industry on the financial industry as a whole as well as on each financial sub-sector, tests the dynamic evolution of China’s real estate financial risk accumulation, and explores the causes of risk spillover and contagion. This paper draws three main conclusions.

Firstly, the risk spillover intensity of China’s real estate industry to the financial industry has increasingly risen since 2013. The manifestation of systemic risks has become more likely and the efforts needed to prevent risks is great. Existing studies have not identified this trend, partially because the model used in related studies is static. However, the time-varying-copula model provides the possibility of observing more dynamic changes. More specifically, we found that the volatility characteristics of the real estate industry’s spillover risks in the financial industry are different from the spillover risks in the banking industry. China’s real estate industry spillover risk for the financial industry has seen three peaks that divide risk spillover volatility into three stages: from 2008 to 2009, 2012 to 2013, and 2015 to 2016. The spillover intensity of risk in the first stage, which occurred during the subprime mortgage crisis in the United States, was high. However, in the second stage, the intensity of risk spillover from the real estate industry to the banking industry followed different trends, fluctuating within a small range around zero; this is completely contrary to the findings of Liu and Gu (2014), Adams et al. (2014). In their research, they maintain that risk spillover from the Chinese real estate industry to the financial industry was only due to the high correlation between bank credit and the real estate industry in this period. In fact, China’s state-owned banks tightened their real-estate-related loans (including real estate development loans and housing mortgage loans) around 2013(Sun et al., 2019). Given the growing risk spillover intensity of the real estate industry to the financial industry overall, bank credit channels could not have been the most important risk spillover channels at this stage. Hence, the banking industry—as a representative of the financial industry in China—does not always reflect changes in the intensity of risk spillovers from the real estate industry to the financial industry. Furthermore, control of real estate financial risks should not be limited to adjusting the scale of bank credit, which is significant in the formulation of real estate financial risk control policies.

Secondly, the rise of the risk spillover intensity of the real estate industry results from innovative financing channels such as securities and the trust industries. This conclusion differs from past studies, which have generally taken the banking industry and particularly bank credit as representative of the financial industry to conduct research (e.g., Oikarinen, [2009],Gerlach & Peng, [2005]). There is little research on the impact of the real estate industry on other non-bank financial institutions. Recently, scholars have observed the impact of the real estate industry on various financial institutions. For example, Shen et al. (2016) consider the risk spillover from the real estate industry to non-bank financial institutions. However, as mentioned, this static research cannot accurately reflect the intensity of risk spillover and the changes in its channels. At the same time, the study of Sun et al. (2019) considered the impact of the real estate industry on the trust and the insurance industries, but not the securities industry. The influence of the real estate industry on the securities industry cannot be ignored. The conclusions of this article show that from 2013 to 2014, the intensity of risk spillovers from the real estate industry to the securities industry significantly increased. Finally, the diversified financing channels of real estate enterprises and the leverage and multilayered nested operations of financial institutions for balance sheet assets have not only accelerated mixed financial operations but have also created many shadow banks that are difficult to supervise. After a series of government policies that were implemented to regulate China’s real estate industry, China did not achieve its goal of curbing the risk of real estate spilling over into financial industries, as discussed in Section 6.

Based on the above conclusions, this paper gives the following policy suggestions to prevent risk spillover from the real estate industry to the financial industry. Firstly, regulatory policies should contribute to the coordinated development of the fictitious economy and real economy. According to Krippner (2003): “The Fictitious Economy is an allusion to Marx’s notion of fictitious capital.” In this paper, the fictitious economy is composed of fictitious assets. Capital circulates in the fictitious assets, which promotes the increase of nominal wealth due to the price changes of fictitious assets, and there is no material conversion process like the real economy. The real economy is a series of production and operation activities of material and spiritual products other than the fictitious economy. Financial industry belongs to fictitious economy. In the process of deepening cooperation among real estate enterprises and financial institutions, a variety of complex, innovative financial instruments are constantly produced. In the absence of supervision, it is easier for real estate industry risk to rapidly spill over into the financial industry on a large scale. This dynamic increases the probability of risk contagion, resulting in a serious distortion of the fictitious economy and the real economy (Xu, 2018). As such, the government shouldguide and standardize financial cooperation between real estate enterprises and financial institutions to reduce pro-cyclical fluctuations and prevent risk contagions between the real estate and financial industries. Furthermore, the government should simultaneously curb excessive speculation and abnormal fluctuations in real estate prices to control the accumulation of financial risks caused by the expansion of the fictitious economy.

Secondly, regulatory policies should combine macro-controls and micro-adjustments. In China, given the dynamic adjustment of both the real estate and the financial industries, macro-controls that work before a financial crisis will be much less effective in limiting banks’ real estate credit investments; this is because different financial sub-industries and the real estate industry will form new business models and create varied risk spillover channels. The government should continue the policy of “housing for living in and not for speculation” and do its best to maintain a policy of housing continuity in choosing macro-control policies.

Thirdly, regulatory policies should combine macro-prudential and micro-prudential supervision. Before the 2008 financial crisis, the mainstream view of global financial supervision emphasized micro-prudential supervision and ignored macro-prudential supervision. However, there is a serious lack of macro-prudential supervision for systemic risk problems such as risk contagion and risk spillover, which are highly related to the real estate and financial industries. Hence, the regulatory authorities should further improve the macro-prudential management framework, complement regulatory weaknesses, and rapidly identify the internal and external factors that induce systemic risks and risk contagion in the real estate and financial industries.

Footnotes

Acknowledgements

We would like to express our gratitude to all those who have helped us during the writing of this article. We deeply appreciate the funding support of Beijing Language and Culture University.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Ethics Statement

This statement is not applicable. Our article does not need any ethics statement.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Science Foundation of Beijing Language and Culture University (supported by “the Fundamental Research Funds for the Central Universities”) (Approval number 21YJ050003).