Abstract

Financial risk tolerance is one of the important factors affecting the financial investment decisions of individuals and institutional investors and a crucial factor of financial planning and financial counseling. It is therefore necessary to determine the major determinants of risk tolerance. In this article, we researched the impact of financial literacy level and demographic characteristics on the financial risk tolerance of the individuals in the sample of Usak University staff, using a multinomial logistic regression analysis and retrieving data through the questionnaire method. Multinomial logistic regression is an extension of binary logistic regression, allowing for three or more categories of the dependent variable. The findings of the empirical analysis reveal that financial literacy and demographic characteristics of age, gender, education, and income levels are significant determinants of financial risk tolerance. In this regard, the improvements in the financial literacy of the individuals through various education programs will probably raise the demand of financial products with different risk characteristics and in turn contribute to the development of financial sector.

Introduction

Risk is a significant component of real and financial investments. While making real and individual investment decisions, both individual and institutional investors consider the possible rate of return and riskiness of the investment. In this context, the financial risk tolerance of individual investors emerges as an important factor influencing the choice of financial investments and the use of savings in financial markets. Therefore, this factor is also highly important for personal financial planning, as well as the optimization of the investor’s portfolio. Hence, determining the financial risk tolerance of individuals is important for financial service-providing companies to offer appropriate services for their customers. Financial risk tolerance is a subjective standard that a person defines as the accepted maximum amount of uncertainty when usually making a financial decision (Grable & Joo, 2004). Sometimes, the concept of being risk averse is also used instead of financial risk tolerance, although it means the opposite; as a person avoids risks, the financial uncertainty and comfort level decreases (Ryack et al., 2016). The related literature has attempted to explain risk tolerance by normative models suggested by traditional finance (such as expected utility theory; see Machina, 2008) and descriptive models based on behavioral and/or psychological factors in the context of behavioral finance (Grable, 2016). However, financial, social, cultural, physical, and ethical factors have been suggested as the possible determinants of the individual financial risk tolerance in the related literature, as seen in Figure 1 (Fisher & Yao, 2017; Wang & Hanna, 1998; Yong & Tan, 2017).

Determinants of financial risk tolerance.

In this context, financial literacy is also an important factor for financial risk tolerance (Grable & Joo, 1999). It is clear from the related empirical literature that the influence of certain demographic and behavioral variables on financial risk tolerance have been the subject of the research. However, few studies have been carried out to reveal the effect of financial literacy on financial risk tolerance. The purpose of this article is to fill this gap in the related literature. For this purpose, in addition to demographic variables, the effect of financial literacy level on the financial risk tolerance for sample of Usak University in Turkey has been studied.

The Turkish economy shifted from import-substituting industrialization strategy to export-oriented growth strategies with the Stabilization Decisions of January 24, 1980. The financial sector synchronously began to develop as of 1980s. In this context, the Capital Markets Board was established in 1982 and Borsa Istanbul was formed in 1985; the Derivatives Exchange was established in 2005. But the Turkish economy experienced serious financial crises due to inadequate institutional, regulatory, and legal infrastructure for the financial sector during the period 1980 to 2001. However, central bank independence has been strengthened, the Banking Regulation and Supervision Agency was established, and regulatory reforms were implemented after the February 2001 crisis. Therefore, the Turkish financial system did not experience any serious negative effects resulting from the global financial crisis and the Eurozone sovereign debt crisis due to the recent regulatory and structural reforms. Furthermore, the Turkish government tries to raise the level of domestic savings and improve the financial sector through the private pension system by fiscal incentives in recent years.

The banking sector is the dominant actor in the financial system, when compared with the other financial institutions, and the size of assets by banks was 1.04 of the GDP in 2018 (Banking Regulation and Supervision Agency, 2019). Furthermore, Borsa İstanbul ranked 13th among the world stock exchanges with a fixed-income securities’ transaction volume of USD 165 billion in 2018. The stock market capitalization of Borsa Istanbul was USD 149 billion in 2018 and ranked 33th among the world stock exchanges. The volume of derivatives’ transaction in Borsa Istanbul was USD 269 billion in 2018 and ranked 24th among the world derivatives exchanges (Turkish Capital Markets Association [TCMA], 2019).

The savers in Turkey can be classified as residents and nonresidents. The share of the residents was 86% of total savings and 2.7 trillion Turkish lira (TL) in 2018, whereas the share of nonresidents was 14% and 0.457 trillion TL. The asset allocation varied considerably among residents and nonresidents. The asset allocation of the residents in 2018 was as follows: 69% deposits, 26.8% fixed-income securities, and 4.1% stocks. In comparison, the asset allocation of the nonresidents in 2018 was as follows: 44.6% stocks, 33.5% deposits, and 22% fixed-income securities (TCMA, 2019). Hence, the residents are highly risk averse, whereas the willingness of the nonresidents to take risks is very high, compared with the residents. The aforementioned difference could be the result of the frequent financial crises in Turkey.

The purpose of this article is to fill this gap in the related literature. For this purpose, in addition to demographic variables, the effect of financial literacy level on the financial risk tolerance of individuals was analyzed by using the multinomial logistic regression method on the Usak University staff sample. The relevant literature review about the research subject is included in the second part of the study and the data and analysis method is introduced in the third part. Reliability analysis and the findings from the descriptive and econometric analysis are then presented within the empirical analysis. The study concludes with the final part.

Literature Review

Numerous empirical studies have been carried out within financial planning and financial consultation to identify the determinants of individual financial risk tolerance due to the remarkable effect it has on financial investment decisions. The effect of demographic variables (age, gender, marital status, educational level, income level, and wealth level), personal qualifications, behavioral factors (being worried, life satisfaction level), and cultural background on risk tolerance has been generally analyzed in these studies (e.g., Duasa & Yusof, 2013; Fisher & Yao, 2017; Irwin, 1993; Mishra & Mishra, 2014; Rahmawati et al., 2015; Weber, 2014). However, the effect of financial literacy on risk tolerance has been researched in a relatively smaller number of studies. In these studies, it was generally identified that there was a positive relationship between financial literacy/financial education level and financial risk tolerance (e.g., Bajo et al., 2015; Bayrakdaroğlu & Kuyu, 2018; Grable, 2000; Grable & Joo, 1999, 2004; Masters, 1989; Nguyen et al., 2016; Wang, 2009).

Masters (1989) analyzed the risk tolerance and investment knowledge for a sample of 480 investors in a Midwestern investment firm through covariance analysis and established that those with knowledge about investment had higher risk-taking tendencies than those with no or less knowledge about investment. Similarly, Grable and Joo (1999) examined the demographic and socioeconomic determinants of 220 white-collar employees through regression analysis and disclosed that financial knowledge had a positive influence on financial risk tolerance. Grable (2000) also explored the demographic, socioeconomic, and attitudinal determinants of risk tolerance for a sample of a large southeastern university through discriminant analysis and discovered that financial knowledge raised the financial risk tolerance. Grable and Joo (2004) conducted a similar research for a sample of two universities’ personnel through regression analysis and reached the same findings. Wang (2009) analyzed the interaction between the financial knowledge levels of investors and risk-taking behavior in a sample of 524 participants through bivariate correlations and identified that financial knowledge influenced risk-taking.

In addition, Grohmann et al. (2014) explored the impact of financial literacy on the middle class in Bangkok through regression analysis and concluded that the increase in financial literacy level raised the demand for more sophisticated financial products by individuals. Furthermore, Bajo et al. (2015) investigated the impact of financial literacy over risk avoidance through data from 38,000 questionnaires in Italy through regression analysis and identified that people with lower financial literacy levels avoided the risk more, whereas Nguyen et al. (2016) discovered a positive relationship between financial literacy level and risk tolerance as a result of their study on 538 people in Australia through structural modeling. Finally, Yong and Tan (2017) also examined the impact of financial literacy on financial risk tolerance of business faculty students from a university in Malaysia and revealed that financial literacy level had no significant impacts on financial behavior on the students.

Extensive studies have been conducted on the determinants of risk tolerance for different samples in Turkey, but the studies generally have focused on the influence of demographic variables on risk tolerance (e.g., see Anbar & Eker, 2010; Arslantürk Çöllü et al., 2019; Çankaya et al., 2013; Kalfa et al., 2015; Kubilay & Bayrakdaroğlu, 2016). Only Bayrakdaroğlu and Kuyu (2018) examined the determinants of risk perceptions of 24 Turkish female investors with different demographic features, through a focus group interview, and disclosed that financial literacy was an important determinant of risk perception. Furthermore, the extensive studies on financial literacy have generally tried to measure the financial literacy levels of the participants in Turkey (see Fettahoğlu, 2015; Öcal & Özcan, 2018; Özer, 2019; Sakınç, 2018; Temizel & Bayram, 2011; Yatbaz & Çatıkkaş, 2019). Hence, our study is evaluated to make a contribution to the related literature in the light of literature summary.

The empirical studies on the demographic determinants of financial risk tolerance have reached the following findings;

Youngsters have a higher risk tolerance than older adults;

Men have a higher risk tolerance than women;

Single people have a higher risk tolerance than married people;

Risk tolerance increases as income and wealth level increase;

Risk tolerance increases as educational level increases;

Personal qualifications and behavioral factors have an effect on risk tolerance; and

Risk tolerance increases as financial literacy level increase (Cavalheiro et al., 2012; Chang et al., 2004; Corter and Chen, 2006; Duasa & Yusof, 2013; Dwyer et al., 2002; Fisher & Yao, 2017; Kannadhasan, 2015; Mahdzan et al., 2017; Mishra & Mishra, 2016; Pinjisakikool, 2017; Rahmawati et al., 2015; Sharma et al., 2017; Sulaiman, 2012; Weber, 2014; Yong & Tan, 2017).

Data and Method

The effect of the financial literacy level and demographic variables on the risk tolerance of individual investors was researched by using the data obtained through questionnaires through multinomial regression analysis in the sample of Usak University’s staff. Therefore, the findings of the study give us an idea about the interaction between financial literacy and financial risk tolerance of the individuals employed in a Turkish public university. The study can be seen as a preliminary step to encourage the scholars approximate the interaction among the variables despite the fact that the sampling imposed some limitations to generalize the findings. Consequently, our objective is not to make generalizations about the overall Turkish population.

Data

The sample of the research consisted of Usak University academic and administrative personnel and the data set was provided from the questionnaire method. Usak University’s population is 1,348 people. The sample is calculated by Equation 1 when the population is known (Evans, 2012):

N: Number of individuals in the target audience

n: Number of individuals to be sampled

p: Probability of occurrence

q: Probability of nonoccurrence

t: Theoretical value from t table at specified significance level (1.95 for 5% significance level)

d: Accepted sampling error (we took 0.05 considering the relevant literature)

We should reach a minimum of 299,13 persons for the study. Nevertheless, we tried to reach all personnel through random sampling; 350 questionnaires could be handed in. The questionnaire data were collected face-to-face and by email. Three hundred and twenty-five (92%) of the collected questionnaires were evaluated as complete and available. Therefore, the completion rate was 92.85% and response rate was 24.11%.

The subjective financial risk tolerance of the participants (RISKTOL) in the study was identified by a question that can be weighed between 1 (I do not take any financial risks) and 4 (I take high financial risks by expecting high returns). However, the financial literacy level (FINLIT) of the individuals in the sample was measured by questions prepared by considering the studies of Lusardi (2008), Lusardi and Mitchell (2007a, 2007b, 2008), and Mahdzan and Tabiani (2013). First, the basic financial literacy level of the individuals was measured by four questions about interest calculation, inflation, and risk diversification. Thereafter, the advanced financial literacy level was measured by nine questions about investment funds, bonds, and stocks. Correct answers were coded as 1 and wrong answers were coded as 0. Finally, adding the basic and advanced financial literacy level, the overall financial literacy level of the individuals was calculated. Therefore, the overall financial literacy level can be weighed between 0 and 13 and higher values indicate a relatively higher financial literacy level. Other variables and definitions used in the study are presented in Table 1. For the data analysis, SPSS 22.0 statistical software program was used.

Data Set Description.

Method

The impact of financial literacy level and demographic characteristics on the financial risk tolerance of individual investors was analyzed by using a multinomial logistic regression approach in the study. First, questionnaires were administered to Usak University personnel face-to-face and through email, and 350 questionnaires were collected of which 325 were evaluated to be complete. Thereafter, the relevant data were collected from the questionnaires and subjected to econometric analysis. Multinomial logistic regression analysis is one of the analysis techniques employed to examine relationships between independent and dependent variables when the dependent variable includes three or more categories. In this study, the dependent variable comprises four categories. Therefore, multinomial logistic regression was used in the analysis. The model was formed as follows:

In Equation 3, α indicates the constant term, β n indicates the estimated coefficient, and ε indicates the error term. The main hypotheses of the research were as follows:

Financial literacy level is expected to influence the risk tolerance of individuals. The increases in financial literacy level make it possible for individuals to make more conscious decisions about the financial investments. However, the direction of the effect may vary depending on the sample. For instance, as can be seen in the literature review, a negative relationship is expected between the age and the risk tolerance, but a positive relationship is expected between the educational level and income level, and the risk tolerance. In addition, it can be seen that men generally have a higher risk tolerance than women.

Empirical Analysis and Discussion

The impact of the financial literacy level of Usak University personnel and demographic characteristics on the financial risk tolerance of individual investors was researched in the study by using multinomial regression analysis. First, a reliability analysis of the questionnaires was conducted in the study and then the demographic features of the participants were presented through a descriptive analysis. In the next part of the empirical analysis, the data regarding the financial literacy levels of the participants were shared. In the final part of the empirical analysis, the effect of financial literacy level and demographic variables on the risk tolerance of individuals was researched through multinomial logistic regression analysis.

For the reliability analysis, Cronbach’s alpha, split-half, parallel, and absolute precision parallel tests are usually used. When the Cronbach’s alpha value is more than 60% (some studies consider it as 75%) in the related literature, the questionnaire is considered successful. However, when other test results are more than 70%, this indicates that the internal coherence of the questionnaire is ensured and reliable inferences can be made from it. By using Cronbach’s alpha, split-half, parallel, and absolute precision parallel tests, the reliability and coherence of the questionnaire was tested in this study and the test results are presented in Table 2, which illustrates that higher values than the ones considered as the threshold for each criterion were obtained. Therefore, it was concluded that the questionnaire was coherent in itself and reliable inferences could be made from it.

Reliability Analysis.

Of the participants, 206 (63.4%) are male and 119 (36.6%) are female; 222 (68.3%) are academic staff and 103 (31.7%) are administrative staff; and 27.4% are single and 72.6% of them are married (Table 3). In addition, 51.4% of the participants have children, while 171 (52.6%) are between the ages of 25 and 34 years and 101 (31.1%) are between the ages of 35 and 44 years. Seven (2.2%) of the participants are high school graduates, 134 (41.2%) have a bachelor’s degree, and 184 (56.6%) have a postgraduate degree. Furthermore, 83.4% of the participants have a bachelor’s or postgraduate degree in the fields of economics and administrative sciences, of whom 47.7% are administrative personnel and 52.6% are academic personnel. Finally, 277 (85.2%) of the participants have a wage higher than 2,500 TL (USD 718) and the aforementioned wage is also higher than average monthly wage and minimum wage. Also 124 (38.2%) of the respondents have a monthly income of 4,501 TL (USD 1,293) and above.

Demographic Characteristics of the Participants.

Note. TL = Turkish lira.

Within the scope of identifying the financial literacy levels of the participants, first, basic financial literacy levels of the individuals in the sample were measured through the questions including percentage, inflation, and interest calculations; the results are presented in Table 4. The results indicate that the basic financial literacy levels of the individuals are very high and the correct answering rate of each question is above 80%.

Basic Financial Literacy Level of the Individuals in the Sample.

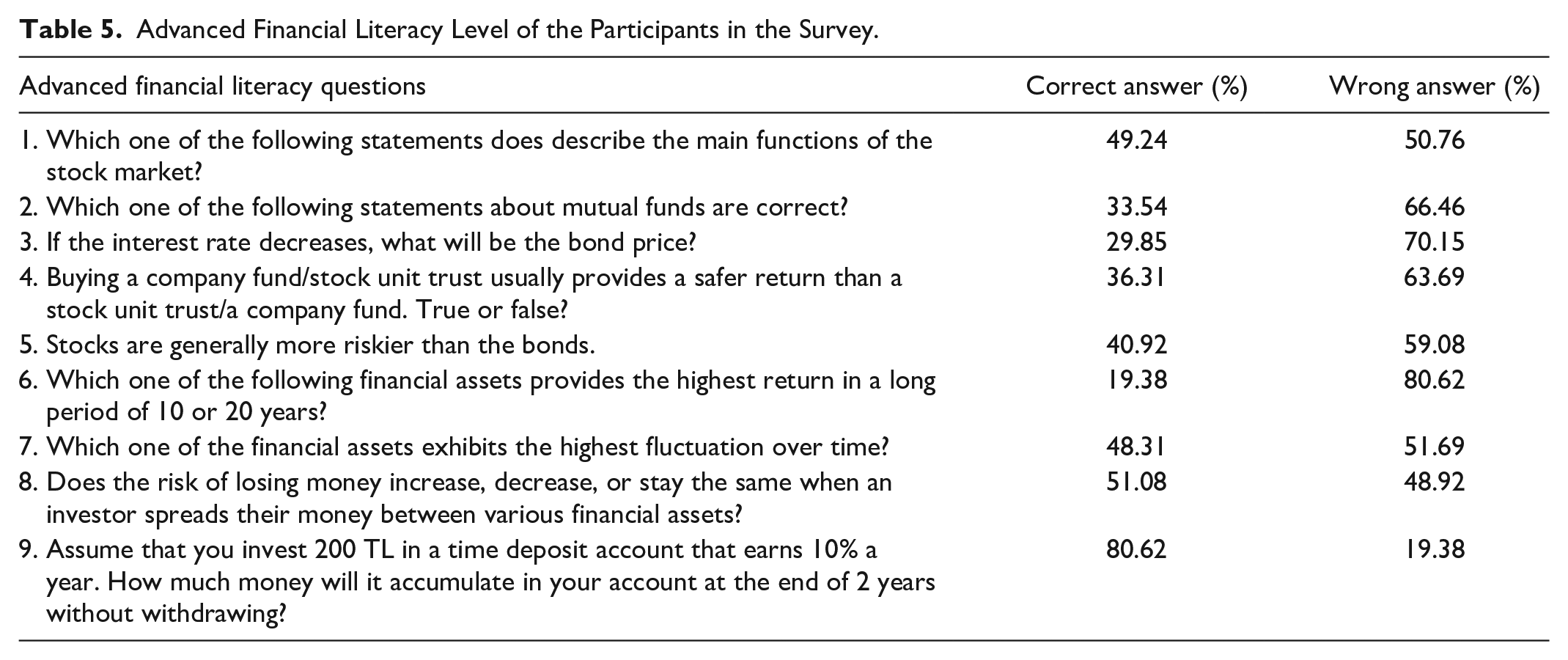

In the second stage, the advanced financial literacy levels of the individuals were measured by the questions shown in Table 5. The lowest correct answering rate, of 19.38%, was observed for the question on financial assets providing relatively higher returns in the long term, while the second lowest rate, of 29.85%, was observed in the question about the interaction between bond prices and interest rate. In addition, approximately one third of the individuals in the sample answered the questions about investment funds correctly. Furthermore, approximately half of the participants answered the questions about stock market and risk diversification correctly. Finally, approximately 80% of the participants correctly answered the question about compound interest calculation.

Advanced Financial Literacy Level of the Participants in the Survey.

By adding the basic and advanced financial literacy levels, overall financial literacy levels were calculated in the study and are shown in Table 6. The basic financial literacy level of the individuals was identified as 3.35 out of 4. Therefore, the participants have a high knowledge level about interest rates, inflation, and percentage calculation. However, the advanced financial literacy level of the individuals was calculated as 3.89 out of 9 on average. Therefore, the participants are at an intermediate level in advanced financial literacy. In addition, the overall financial literacy level of the participants was calculated as 7.24 out of 13 on average. Increases in the overall financial literacy level are partly derived from the relatively higher basic financial literacy scores.

Overall Financial Literacy Level of the Individuals in the Sample.

Extensive empirical studies have been conducted to measure the financial literacy level of various samples such as high school, undergraduate and graduate students, university personnel, accountants, banking employees, and so on. However, a limited number of studies have focused on the measurement of financial literacy of university personnel and the studies have revealed that the basic financial literacy of the university personnel was satisfactory, but needs additional education to achieve an advanced financial literacy level (Celikkol et al., 2017; Gutnu & Cihangir, 2015; Ozturk & Demir, 2015). Hence, our results were found to be consistent with the findings of the aforementioned studies. Furthermore, the basic financial literacy index of Turkey was 55 out of 100 (Financial Literacy and Inclusion Association [FODER] & Visa, 2019). Hence, the basic financial literacy level of the university personnel was found to be relatively higher.

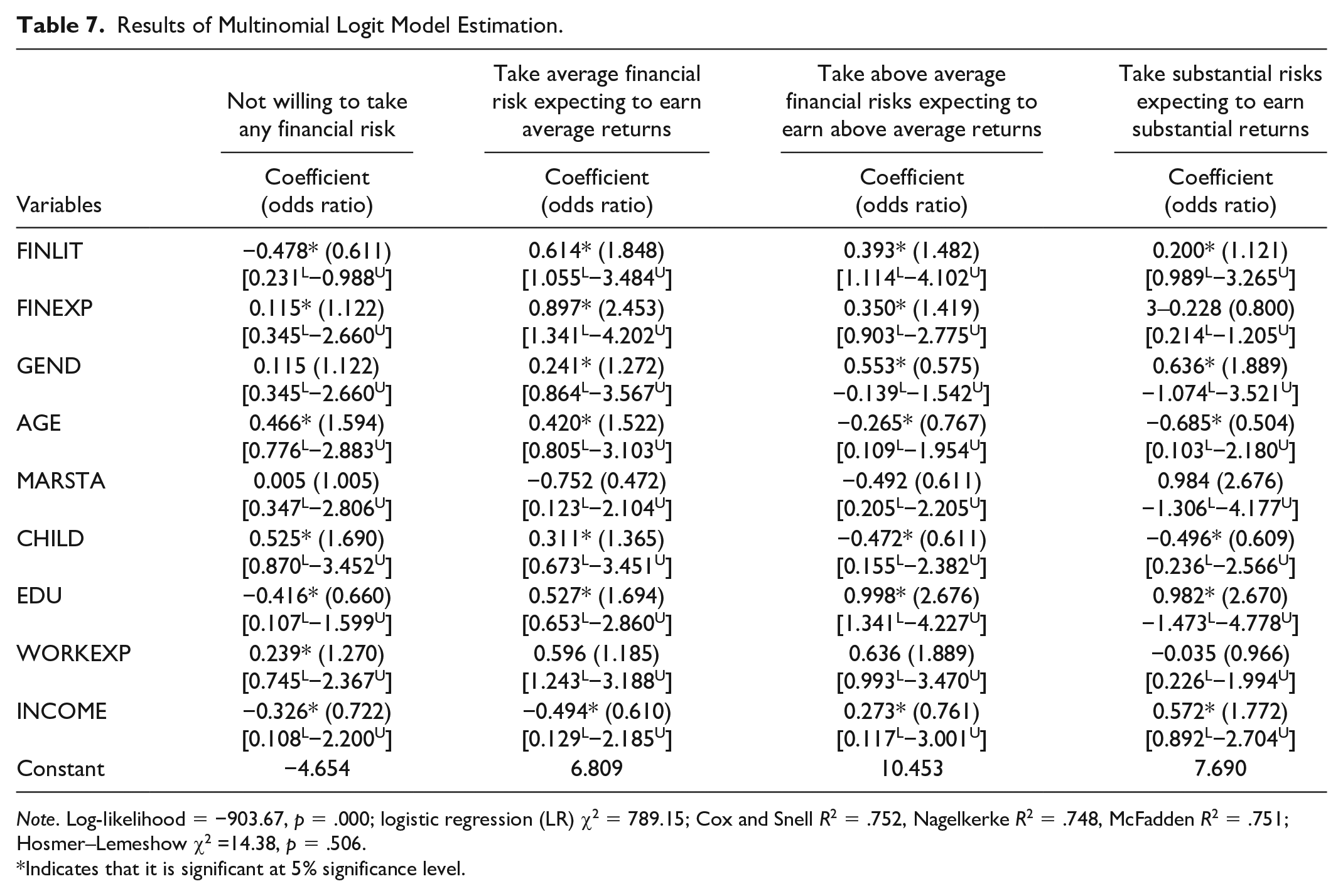

The impact of financial literacy level and demographic characteristics on the risk tolerance of individuals was analyzed through multinomial logistic regression and the results of the analysis are presented in Table 7, illustrating that the Cox and Snell R2, Nagelkerke R2, and McFadden R2 values, which are the percentage that the independent variable influences the dependent variable, are above 70%. In addition, the model is significant because log-likelihood (LL) indicating the goodness of fit is (p) < .05. To test the model’s goodness of fit, the Hosmer–Lemeshow goodness of fit test was used and revealed that the model fits the data really well.

Results of Multinomial Logit Model Estimation.

Note. Log-likelihood = −903.67, p = .000; logistic regression (LR) χ2 = 789.15; Cox and Snell R2 = .752, Nagelkerke R2 = .748, McFadden R2 = .751; Hosmer–Lemeshow χ2 =14.38, p = .506.

Indicates that it is significant at 5% significance level.

According to the model estimated results,

— Financial literacy level, educational level, and income level influenced “No financial risk-taking” status negatively; however, the financial market experience, age, number of children, and work experience influenced “No financial risk-taking” status positively.

— Financial literacy level, financial market experience, age, number of children, and educational level influenced “Average financial risk-taking by expecting to get average return” status positively; however, marital status and income level influenced “Average financial risk-taking by expecting to get average return” status negatively.

— Financial literacy level, financial market experience, and educational level influenced “Average financial risk-taking by expecting to get average return” status positively; however, age and number of children influenced “Average financial risk-taking by expecting to get average return” status negatively.

— Financial literacy level, educational level, and income level influenced “High financial risk-taking by expecting to get high return” status positively; however, age and number of children influenced “High financial risk-taking by expecting to get high return” status negatively.

The objective of the article is to analyze the effect of financial literacy level together with the demographic variables on the financial risk tolerance of individuals using the multinomial logistic regression method in the sample of Usak University personnel. The article aims at contributing to the limited relevant literature by investigating the interaction between financial literacy and financial risk tolerance.

Making complicated financial decisions requires that individuals have necessary information about financial products, their risk and return, and functioning of financial markets. Therefore, financial literacy level is theoretically expected to influence the risk tolerance of individuals because the increases in financial literacy level make it possible for individuals to make more conscious decisions about financial investments. Hence, our findings were consistent with theoretical expectation and also jibed with the findings of Masters (1989), Grable and Joo (1999), Grable (2000), Wang (2009), Grohmann et al. (2014), Bajo et al. (2015), and Nguyen et al. (2016). Furthermore, higher education level is similarly expected to positively affect the risk tolerance positively. In this regard, our findings were found to be consistent with theoretical expectations and the findings of Chang et al. (2004), Sulaiman (2012), Duasa and Yusof (2013), Rahmawati et al. (2015), and Sharma et al. (2017).

On the contrary, a negative relationship is expected between the age and the risk tolerance because older adults are exposed to time constraints to eliminate the possible financial losses (Grable, 1997). Therefore, younger people are liable to take more financial risks. But, the relevant literature on the nexus of age–risk tolerance has stayed inconclusive. But our findings were consistent with Gibson et al. (2013), Weber (2014), Kannadhasan (2015), and Mishra and Mishra (2016).

The studies about the impact of gender on risk tolerance have reached mixed findings depending on the sample. However, our findings were consistent with Dwyer et al. (2002), Anbar and Eker (2010), and Weber (2014). However, the men dominate the Turkish financial markets and the share of women in Turkish financial markets is relatively lower, similar to our sample. Therefore, the nexus of gender–risk tolerance can vary depending on the sample.

Finally, it is assumed that people having higher incomes are more likely to undertake higher financial risks (Cohn et al., 1975) and the relevant empirical literature also verifies the assumption. Our findings were found to be consistent with the findings of Anbar and Eker (2010), Sulaiman (2012), Weber (2014), Rahmawati et al. (2015), and Sharma et al. (2017).

When the general results are evaluated, it is evident that financial literacy level and educational level influenced the risk tolerance positively. In other words, as the awareness of individuals of financial products and markets increases, they tend to take more risks. However, it is evident that income level is also an important determinant of high financial risk tolerance.

The Turkish government tried to develop the financial system and raised the domestic savings through structural and regulatory reforms and private pensions system by fiscal incentives and experienced a significant improvement especially after the new incentive system. However, the rise in the financial literacy level through right policies also increases the demand of different financial instruments with different risks and in turn raises the effects of the current policies on the development of financial sector.

In addition, IIA hypothesis in the Hausmann test was proved and the model results are reliable (Table 8). The model goodness of fit is proved.

Results of Hausman Test IIA Assumption.

Conclusion

Risk tolerance is important for financial service suppliers and the development of the financial sector through individual financial planning and the demand of individuals for financial products. For this reason, numerous studies have been carried out in the related literature to identify the determinants of financial risk tolerance. The effect of demographic variables and behavioral factors on risk tolerance have been generally researched in these studies. To contribute to the relevant literature regarding the determinants of risk tolerance, the effect of financial literacy level on financial risk tolerance in the sample of Usak University personnel was analyzed through the multinomial logistic regression approach. The limitation of the article was that its sample was formed from Usak University academic and administrative personnel and cannot be generalized to the overall Turkish population.

The results of the econometric analysis demonstrate that financial literacy level and educational level influenced the financial risk tolerance positively through easing the complicated financial decision-making. Finally, the demographic findings are consistent with the related literature and revealed that men generally have a higher risk tolerance than women, age negatively affects the individual risk tolerance, and income level positively affects the individual risk tolerance.

The findings of the study are significant for policy makers and financial institutions, given the positive economic effects of financial sector development. In this context, various education programs to improve the financial literacy level will probably raise the financial risk tolerance. Furthermore, the education level is also important for financial risk tolerance directly or indirectly through financial literacy. However, the demographic findings may be a guide for setting the priorities in policy making. Therefore, relatively more financial education programs for young people and women should be organized.

The Turkish government currently tries to improve the financial sector and raise domestic savings through structural and regulatory reforms and private pension system, and has achieved significant progress, but the improvements in financial literacy level through financial education programs, especially for young persons and women, in cooperation with public and private institutions, will make a significant contribution to raise the tendencies of the individual investors for the different financial instruments and in turn feed the development of financial sector. Furthermore, it will also help individuals to use their wealth more consciously and effectively.

Further studies can be conducted with different samples to see whether the findings change or not, depending on the sample. In addition, scholars can focus on the impact of behavioral characteristics on the interaction between financial literacy and financial risk tolerance.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This study was derived from the project No. 2017/HD-SOSB005 accepted and carried out by the Usak University Coordinatorship of Scientific Research Projects.