Abstract

This paper investigates a novel problem of ESG (environmental, social, and governance), namely the decoupling phenomenon that corporate ESG information disclosure is inconsistent with actual performance. Based on 12,551 company-year observations of Chinese A-share listed companies from 2009 to 2022, we investigated the impact of ESG decoupling on corporate sustainable development and explored the underlying mechanisms from the perspective of stakeholder theory. We find that ESG decoupling significantly undermines corporate sustainability. Mechanism analysis shows this negative impact results from reduced stability in customer partnerships and increased corporate financing constraints. Further considering the moderating role of China’s institutional environment on this impact, a strong formal institutional environment (e.g., regulatory framework) reduces this negative effect, whereas the informal institutional environment (e.g., media attention) amplifies it. The research underscores the importance of aligning actions with disclosures, offering practical recommendations for corporate sustainable development.

Plain language summary

The phenomenon of ESG decoupling is a short-sighted behavior that may yield benefits in the short term but is detrimental to the long-term sustainable development of corporations. There is currently a lack of in-depth research on how this behavior affects corporate sustainable development. We focus on the perspective of stakeholders, starting from investors, supply chain partners, regulators, as well as the public and media, and discuss the impact mechanism of ESG decoupling on the sustainable development performance of corporations. Based on this, we propose corresponding suggestions and opinions, contributing ideas to the construction of a more responsible and sustainable business environment.

Keywords

Introduction

As the concept of Environmental, Social, and Governance (ESG) takes hold in the global business world, ESG practice is no longer an add-on to corporate operations but has become an important strategic imperative for sustainable growth and competitiveness (Y. Wang et al., 2023). Against this backdrop, stakeholders, including investors, consumers, supply chain partners, regulators, and other market observers—are scrutinizing corporate ESG performance with unprecedented attention. They are eager to see not only the high ESG standards that companies claim in their reports, but also the actual implementation of these commitments in their long-term planning and daily operations. However, in order to quickly respond to stakeholders’ ESG demands, corporate managers may adopt a strategic disclosure approach and consciously exaggerate the ESG practices, resulting in inconsistencies between the ESG commitments and actual ESG performance, that is, ESG decoupling (Eliwa et al., 2023). ESG decoupling essentially represents shortsighted and socially irresponsible behavior (Aboud et al., 2024). Although it may create a “legitimacy facade” in the short term (Arena et al., 2018) to boost investor confidence, enhance analysts’ earnings forecasts (K. Luo & Wu, 2022) and thus positively impact stock prices (Leite & Uysal, 2023), leading to a false sense of market prosperity. Once exposed, the firm will face a series of cascading consequences, including reduced customer loyalty, diminished brand value, and potential regulatory scrutiny and legal risks (L. Yang et al., 2024). These issues will not only directly affect a company’s financial performance and market position but also fundamentally threaten its long-term survival and development, jeopardizing its competitiveness in the marketplace and its potential for future growth. The cost of shortsightedness is therefore at the expense of corporate sustainable development.

In this context, examining the adverse effects of ESG decoupling and its mechanisms is critical to understanding how corporations balance the pursuit of immediate benefits with the maintenance of long-term sustainability. Recently, a number of academic endeavors have been devoted to understanding the causes and influencing factors of ESG decoupling, which are still few but growing rapidly. Research suggests that the motivation for ESG decoupling involves multiple factors, both internal and external to the firm. Among them, responding to market pressures and image management (Talpur et al., 2024), meeting compliance and legal requirements (L. Li et al., 2018), and lack of effective monitoring and accountability mechanisms (He et al., 2023) are important external influences, whereas managerial traits and corporate ethical culture climate (Wedari et al., 2021; Salehi & Bashirimanesh, 2024) are important internal influences. Regardless of the motivation, the pursuit of superficial achievements rather than substantive improvements in ESG disclosure is a reversal of the original intent of ESG and will ultimately be detrimental to the well-being of society.

Regarding the influencing factors of ESG decoupling, from the internal perspective of organizations, scholars have explored factors such as gender diversity on boards of directors, CEO power, women’s power, ownership structure, and governance committees (Eliwa et al., 2023; Liu et al., 2023; L. Yang et al., 2024); from the investor’s perspective, scholars analyze the impact of mutual fund investors’ behavior and their preferences on ESG decoupling(Liu et al., 2023); from a policy and regulatory perspective, the influential role of mandatory ESG reporting, market rewards and penalties, etc., has been explored (García-Sánchez et al., 2021; Aboud et al., 2024); in addition, technological innovations, especially corporatite digital transformation, are believed to constrain the occurrence of ESG decoupling behavior (Chen, Wan, Ma, et al., 2024). In terms of the consequences of ESG decoupling, a few studies from the perspective of downstream customers find that it reduces customer stability by damaging corporate reputation and increasing information asymmetry (Chen, Wan & Wang, 2024) and is negatively correlated with corporate financial performance (He et al., 2023). In addition, the negative impact of ESG decoupling on corporate R&D investment was explored (Sun et al., 2025), and it was found that ESG decoupling increases financial constraints and agency costs, which ultimately leads to a reduction in the efficiency of corporate labor investment (Di & Li, 2023). Despite initial efforts to investigate the consequences of ESG decoupling, existing research remains limited. There is a notable absence of robust empirical evidence directly substantiating the adverse effects of ESG decoupling on corporate sustainable development, as well as a more comprehensive mechanistic analysis of this impact.

ESG practices were initially widely promoted and implemented in developed countries. However, due to inadequate institutions and regulations, ESG practices are more likely to occur in emerging markets. As the world’s largest emerging market, China occupies a pivotal position in terms of population size, economic scale, and global influence. In 2024, China introduced stricter ESG regulations, marking a new era of mandatory ESG disclosure. This move provides a new reference standard for other emerging markets in ESG information disclosure. Therefore, the study of the ESG decoupling phenomenon can not only highlight the importance of addressing ESG practice alienation and enhance the transparency and effectiveness of ESG practices to truly advance sustainable development, but also provide global investors a window to more accurately evaluate the experiences and challenges of corporate ESG practices in emerging markets.

Based on this, we use a sample of Chinese A-share listed companies in Shanghai and Shenzhen from 2009 to 2022 to conduct a theoretical analysis of the impact of ESG decoupling on corporate sustainability. The empirical results indicate that ESG decoupling has a significantly negative impact on corporate sustainable development. Mechanism analysis reveals that ESG decoupling undermines corporate sustainability by increasing financing constraints and reducing the stability of downstream supply chain relationships. Additionally, a favorable business environment can mitigate the negative impact of ESG decoupling on corporate sustainable development, while intense media attention tends to amplify this effect. It should be especially noted that ESG decoupling in this study refers to the situation where a company’s ESG disclosure exceeds its ESG performance. Another type of ESG decoupling, where a company’s ESG practices are better than its disclosures, is considered to be a pragmatic approach to some extent and is not the primary focus of this paper.

This study aims to contribute to existing research on ESG decoupling by filling the following research gaps. Firstly, although there have been studies involving ESG decoupling, the majority have concentrated on motivations and influencing factors, with limited investigation into its effects on corporate sustainability. This study provides relevant evidence through empirical analysis, enriching the research on the consequences of ESG decoupling. Secondly, this study explores the mechanisms of key stakeholders, such as investors, upstream and downstream supply chain partners, regulators, and the public, in the impact of ESG decoupling on corporate sustainability, which expands the theoretical framework regarding the impact mechanisms of ESG decoupling. Thirdly, this study offers a unique temporal and spatial framework for analyzing ESG decoupling by concentrating on China. It clarifies the specific impacts of ESG decoupling on corporate sustainable development and the underlying differences across varying institutional settings in emerging markets. This enhances the study of ESG alienation behaviors across diverse cultural and institutional contexts.

Literature Review and Hypothesis Development

Stakeholder theory provides a comprehensive analytical framework for examining the mechanisms by which ESG decoupling affects corporate sustainable development. The theory posits that corporations are closely connected to various stakeholders—such as employees, customers, suppliers, investors, and the public—and must proactively address their needs and expectations to attain long-term stable development (Pérez & Rodríguez del Bosque, 2016; Kampoowale et al., 2024). When companies engage in ESG decoupling, their real ESG performance fails to meet the level of their public commitments, which goes against stakeholder expectations for honesty and transparency. This inconsistency can precipitate a widespread crisis of confidence, which in turn triggers a series of negative reactions such as increased capital expenditures, reduced access to financing, termination of collaborations, and reputational damage (García-Sánchez et al., 2021; Markovic et al., 2022; Talpur et al., 2024). In view of this, this study will examine the direct effects of ESG decoupling on corporate sustainability, with particular emphasis on essential stakeholders, including investors, supply chain partners, regulators, and the public. The emotions and behaviors of these groups, which are pivotal to the fundamental operations and reputation management of corporations, enhance our comprehension of the consequence of corporate ESG decoupling.

ESG Decoupling and Corporate Sustainable Development

According to the agency theory, managers will carry out sustainability-related activities only when it helps to improve the firm’s short-term profitability (Singh et al., 2025). For reasons like short-term personal career advancement, competitive pressures, and the need to meet stakeholders’ expectations, managers may be inclined to engage in opportunistic behaviors, selectively disclose ESG information, and even exaggerate ESG performance in an effort to project a positive corporate image (X. R. Luo et al., 2017; Sauerwald & Su, 2019). However, this irresponsible behavior can bring many negative economic and non-economic impacts to the enterprise. In terms of economic impacts, ESG decoupling can result in erroneous resource allocation, affecting a company’s efficiency and profitability. It has been shown to reduce the efficiency of labor investment by increasing financial constraints and agency costs (Di & Li, 2023). Additionally, it can lead to increased capital expenditures, reduced financing sources, and decreased market capitalization, adversely affecting financial performance (Hawn & Ioannou, 2016; Velte, 2023). In terms of non-economic impacts, ESG decoupling may damage a firm’s public reputation (Du, 2015), jeopardize stakeholder relationships, and diminish consumer and investor trust (García-Sánchez et al., 2021). Specifically, environmental performance decoupling, or greenwashing, can hide deceptive environmental claims, affecting customer satisfaction and the firm’s competence reputation, and increase environmental risks, directly impacting green development (Ioannou et al., 2023). The increasing number of corporate social responsibility (CSR) decoupling scandals has raised skepticism about CSR practices (Arli et al., 2019; Ferrón-Vílchez et al., 2021), potentially leading to a loss of competitive advantage (Orazi & Chan, 2020). Decoupling in terms of corporate governance performance can increase the opacity of governance structures and decision-making processes, leading to agency problems, affecting investor trust, and increasing the cost of capital (L. Yang et al., 2024).

To achieve sustainable development, corporations must perform well in both economic and non-economic areas to adapt to the changing market environment and ensure long-term success. However, ESG decoupling weakens the credibility of corporations and undermines the foundation of sustainable development by pursuing short-term benefits while neglecting long-term value, which in turn affects their market competitiveness and ability to sustain growth. Therefore, we propose hypothesis 1:

The Mediating Effect of Supply Chain Partnerships

Supply chain partners, including upstream suppliers and downstream customers, constitute a vital segment of a firm’s stakeholders (Ahmed et al., 2020). Their involvement directly influences critical factors such as value creation, cost efficiency, innovation capacity, brand reputation, and the market responsiveness of a firm’s offerings (Bouncken et al., 2020; Aslam et al., 2020; Al-Omoush et al., 2023). In today’s business environment, competition is no longer just between companies but between supply chains (Bagherpasandi et al., 2024). Stable supply chain partnerships can further ensure the predictability of the supply chain (L. Zhang et al., 2023), promote long-term cost-effectiveness and process optimization to enhance efficiency, strengthen risk management, and innovation cooperation (Yeh et al., 2020; M. Wang et al., 2023), which are key factors in achieving strategic goals and sustainable development (Gu et al., 2024).

Current research on the impact of ESG decoupling on supply chain partnerships is limited, but signaling theory can provide a valuable idea for analysis. Corporations transmit signals to various stakeholders through various behaviors and performances to demonstrate their value and credibility (Asif et al., 2023). ESG decoupling, as a kind of dishonest behavior, undermines this positive signaling mechanism. As the signals transmitted by corporations are distorted, signal recipients are unable to accurately judge the actual performance of corporations and the value of cooperation, thus increasing information asymmetry and uncertainty (Xin et al., 2024).

From the supplier’s perspective, inconsistent ESG performance may be regarded as a potential business risk (In & Schumacher, 2021), which can subsequently weaken the foundation of trust in the partnership. Driven by their instinct to mitigate risks, suppliers will reassess their cooperative relationships with companies and enhance their scrutiny and compliance requirements, which will lead to an increase in the cost of cooperation (J. Yang, 2014; Han et al., 2021). Moreover, to protect their own interests, suppliers may choose to reduce order volumes, demand shorter payment cycles, or even seek alternative partners. These actions can undermine the stability of the supply chain. A decline in the stability of supplier relationships will expose companies to greater challenges in material supply, production planning, and inventory management. This makes it difficult to ensure continuous production and timely product delivery, thereby affecting the company’s operational efficiency and market responsiveness (Nenavani & Jain, 2022). Ultimately, it adversely affects corporate sustainable development.

From the customer’s perspective, as societal focus on sustainable development increases, end consumers and investors are increasingly inclined to support companies that excel in ESG performance (Lee et al., 2022). When companies are associated with those engaging in ESG decoupling, which directly impacts the company’s market appeal and investment value (Aouadi & Marsat, 2018). Moreover, to maintain their own image and meet market demands, clients may pay more attention to the sustainability of their supply chains (Dai et al., 2021). As a result, clients may consider shifting their partnerships to companies with clearer and more consistent ESG commitments (Cui et al., 2024). Losing major clients means that companies will directly face issues such as reduced revenue and declining market share, as well as having to invest more resources in seeking and attracting new clients. These elements will diminish corporate profitability and market competitiveness and further hinder their sustainable development.

Therefore, ESG decoupling can weaken the stability of upstream and downstream supply chain partnerships, undermine the construction and operation of sustainable supply chains, and thus have far-reaching negative impacts on corporate sustainable development.

Therefore, we propose the following hypotheses:

The Mediating Effect of Financing Constraints

Financing constraints refer to the limitations that corporations encounter in acquiring cash flows through financing (Bai et al., 2022), and these constraints may originate from factors such as an imperfect financial system, information asymmetry, and the firm’s own financial condition (Meng et al., 2020; Stiebale & Wößner, 2020; Shi et al., 2023). Increased financing constraints elevate the cost of financing and complicate external fund acquisition for corporations, resulting in investment misalignment from the optimal level, thereby influencing innovation decisions and outcomes (García-Quevedo et al., 2018), which are directly linked to the survival and sustainable development of corporations.

ESG practices are a crucial mechanism for corporations to alleviate financing constraints. According to the information asymmetry theory, the disparity of information between investors and corporations is the root cause of corporate financing constraints (Banerjee et al., 2020). A company’s robust ESG performance signifies its dedication to environmental stewardship, social accountability, and effective governance, which are frequently linked to enhanced information disclosure, thereby mitigating investors’ information asymmetry and investment risk (Ng & Rezaee, 2015). Such information transparency and accountability make corporations more attractive in the capital market and increase their chances of obtaining external financing, which effectively alleviates financing constraints and strengthens potential competitiveness and long-term competitive advantage (D. Zhang & Lucey, 2022). When an enterprise exhibits ESG decoupling, it may be seen as a signal of information asymmetry, suggesting that managers hide information that is unfavorable to the corporation. This inconsistency weakens the firm’s signal to the outside world of its commitment to sustainability and reduces the trust of external investors and creditors. The lack of trust leads to an increase in investors’ and creditors’ perception of the firm’s overall risk, and capital providers may demand a higher risk premium, thereby increasing the firm’s financing costs (Luan, 2024). At the same time, ESG decoupling also reflects internal management challenges, such as myopic managerial decisions or an inattention to stakeholder expectations. These issues may result in suboptimal resource allocation, inadequate performance growth, ineffective risk management, stifled innovation, and diminished market competitiveness, subsequently impacting financial health and future profitability. This directly influences investors’ evaluations of the enterprise, creating a more challenging financing environment that undermines sustainable development.

Therefore, we propose the following hypothesis:

The Moderating Role of the Institutional Environment

The institutional environment refers to the framework of institutions that influence and shape the behavior and decision-making of a society, country, or organization (M. Wang et al., 2024). These institutions can be formal, such as policies and regulations, or informal, such as social norms and public opinion (L. Wang et al., 2023). According to legitimacy theory, corporate operations and production practices need to be subject to the constraints imposed by institutions to ensure that their actions are aligned with the expectations and norms of the external environment. This alignment enables corporations to acquire and maintain their legitimacy (Aboud et al., 2024). Similarly, institutional theory also emphasizes that organizations should operate within a social framework of norms and values (Eliwa et al., 2021).

A favorable formal institutional environment can provide corporations with explicit compliance requirements. When corporations encounter ESG decoupling, the restrictive influence of the formal institutional environment compels them to adjust their strategies (Struckell et al., 2022). To maintain legitimacy, they must adhere to external expectations, thereby halting ESG decoupling before it begins. In addition, a better formal institutional environment usually implies a more explicit and supportive system of policies and regulations. These resources and supports help corporations to solve operational and financial problems caused by ESG decoupling (Abínzano et al., 2023), which helps to reduce the impact of ESG decoupling on corporate sustainable development. Meanwhile, a superior formal institutional environment fosters a transparent and equitable market system, enhancing communication and involvement among stakeholders to mitigate information asymmetry (Azmi et al., 2024). Therefore, when corporations are in a favorable business environment, explicit institutional arrangements can help enhance their overall resilience and adaptability, thus mitigating the negative impact of ESG decoupling on corporate sustainability.

When companies encounter more rigorous informal institutional contexts, such as increased media attention and heightened public expectations, any adverse conduct will be amplified, resulting in greater reputational risk and a trust crisis. Once a firm exhibits such negative behaviors as ESG decoupling, it will be easily captured and quickly disseminated by the public and the media, thus triggering widespread attention and discussion (Davies & Olmedo-Cifuentes, 2016). The amplification of public opinion can further exacerbate the legitimacy gap between the firm and its external environment, exposing the firm to greater social pressure and skepticism. From the stakeholders’ perspective, which may lead to a drop in share price and increase the cost and difficulty of financing for the firm (Maung, 2024). Supply chain partners may also reevaluate the relationship for fear of reputational damage. Negative media coverage can further undermine consumer trust in a firm’s brand, leading to decreased sales and loss of market share (E. Spotts et al., 2014). It can even incur greater scrutiny and regulation from regulators, increasing compliance costs and operational pressure on corporations (W. Li et al., 2023). Therefore, a stricter informal institutional environment represents a higher intensity of social supervision and pressure, which will exacerbate the negative impact of ESG decoupling on sustainable development.

Therefore, we propose the following hypotheses:

To summarize, this paper will examine the influence of ESG decoupling on corporate sustainability and explore its mechanisms from the viewpoints of key stakeholders. Figure 1 illustrates our conceptual framework and primary assumptions.

Conceptual framework.

Materials and Methods

Sample and Data Collection

We use the data of China’s A-share listed companies from 2009 to 2022, ESG disclosure data from Bloomberg, 1 ESG performance data from Sino-Securities Index Information Service Ltd., 2 business environment data from the China Sub-Provincial Business Environment Index Report, media attention data from the Chinese Research Data Service (CNRDS) Platform, 3 and the rest of the data from the China Stock Market and Accounting Research (CSMAR) Database. 4

To ensure the accuracy of the data, the following criteria are used to clean the data: (1) All financial and real estate samples are deleted; (2) ST-type companies are excluded; (3) Samples with missing key variables are excluded. To mitigate the adverse effects of outliers, all the main continuous variables are winorized at the upper and lower 1% levels. We finally obtained 12,551 firm-year observations, including 1,380 companies.

Variables Measurement

Corporate Sustainable Development Performance

Current research typically assesses sustainable development performance through the lens of economic, environmental, and social performance (Shahzad et al., 2020; Aftab et al., 2022). However, in the dynamic landscape of globalization and rapid technological advancement, innovation has emerged as a pivotal element. It enables corporations to penetrate new markets, bolster competitiveness, and secure long-term prosperity, which are essential for sustainable development (Wen et al., 2024). Furthermore, in the realm of ESG performance, which is increasingly in the public eye, corporate governance is recognized as a critical aspect of measuring a company’s sustainability. With this in mind, this paper expands the traditional framework by measuring sustainability performance across five dimensions: economic, environmental, social, governance, and innovation. This comprehensive approach integrates financial and non-financial indicators, considers historical performance, and anticipates future trends, providing a more holistic view of corporate sustainability. For empirical measurement, we utilize the return on assets (ROA) as an indicator of economic performance. The Sino-Securities Index scores of each ESG dimension serve as proxies for environmental, social, and governance performance. Innovation performance is gaged by the logarithm of the number of invention patent applications plus one for the enterprise in the subsequent year. Principal component analysis is then employed to calculate composite scores for each dimension, thereby capturing the overall sustainable development status of corporations.

After standardizing the indicators for each dimension, we conducted the Kaiser-Meyer-Olkin (KMO) test. The KMO test is a statistical method used to assess the common variance among variables in a dataset, with values ranging from 0 to 1. The closer the KMO value is to 1, the greater the common variance among the variables, and the more suitable the data are for principal component analysis or factor analysis. Generally, a KMO value greater than 0.5, combined with a p-value less than 0.05, indicates that the data meet the requirements for further factor analysis (Napitupulu et al., 2017). In this study, the KMO value is 0.661, which is statistically significant at the 1% level, indicating a strong correlation across the dimensions. It confirms the appropriateness of employing principal component analysis for our data set.

ESG Decoupling

The difference between the ESG disclosure score and the ESG performance score is defined as the degree of ESG decoupling, and the larger the value, the higher the degree of decoupling (Liu et al., 2023; Eliwa et al., 2023). The Bloomberg ESG disclosure score is derived from ESG information made public, such as CSR reports, annual reports, and online resources. This metric assesses the comprehensiveness of corporate ESG disclosures, capturing the words component of a company’s ESG strategy. On the other hand, Sino-Securities Index Information Service Ltd. specializes in evaluating the true ESG performance of companies. It draws on a wide range of sources, including corporate reports, financial data, news media, and governmental documents, to measure companies’ performance across ESG dimensions relative to their peers. Both the Bloomberg and Sino-Securities Index utilize a 0 to 100 scale, with higher scores signifying better ESG disclosure and performance. To ensure the scores are directly comparable, we standardize the data using a z-score normalization method. The ESG decoupling degree is then calculated by determining the difference between the normalized ESG disclosure and performance scores.

Supply Chain Partnerships

In this paper, stability is employed as a metric to gage the quality of supply chain partnerships. The concept of supply chain partnership stability is further delineated into two components for assessment: the stability of upstream supplier relationships (Stable_S) and the stability of downstream customer relationships (Stable_C) (Peng et al., 2020). It should be noted that the customer in this paper refers to corporate clients rather than individual consumers. The stability of supplier and customer relationships is quantified by calculating the ratio of the number of overlapping suppliers or customers within the top five rankings of a given year to the total number of suppliers or customers in that list. A higher number of overlapping suppliers or customers indicates a more robust and stable partnership. For instance, if in the current year, the top five suppliers or customers share two entities with those of the previous year, the stability index for the supplier or customer relationship would be calculated as 2 divided by 5, resulting in a stability score of 0.4. The closer this score is to 1, the greater the stability of the supply chain partnership is considered to be.

Financing Constraints

In the current study, financial constraints are primarily measured using the KZ index, WW index, and SA index (Hadlock & Pierce, 2010; Meng et al., 2020; Kim et al., 2021). For the purposes of this paper, we have elected to utilize the SA index to gage the financial constraints faced by corporations. The SA index is constructed using the firm’s size and the year of establishment as two weakly endogenous variables, which is more effective compared to the other two measures. Generally speaking, the SA index is negative, and the larger the absolute value, the more serious the corporate financial constraints are. In order to facilitate understanding, this paper uses the absolute value of the SA index to deal with it.

Institutional Environment

We employ the business environment as a metric to assess the formal institutional environment encountered by corporations, while the informal institutional environment is gaged through media attention. Specifically, we utilize the Business Environment Index from the China Provincial Business Environment Index Report, published by the Social Science Literature Press, 5 which ranges from 1 to 5 points. This index is matched with provinces and corporations to assess the business environment. Media attention is measured by taking the natural logarithm of the number of corporate news reports in the CNRDS after adding one to the count.

Control Variables

We also take into account several control variables that could influence a firm’s sustainable development (SD) performance. These include firm size (Size), the age of the listing (ListAge), the nature of ownership (SOE), financial leverage (Lev), fixed assets (Fixed), intangible assets (Intangible), cash flow (Cashflow), revenue growth rate (Growth), Tobin’s Q at the firm’s financial level (TobinQ), board size (Board), board independence (Indp), and whether the firm has a dual leadership structure (Dual), in addition to controlling for region (Province).

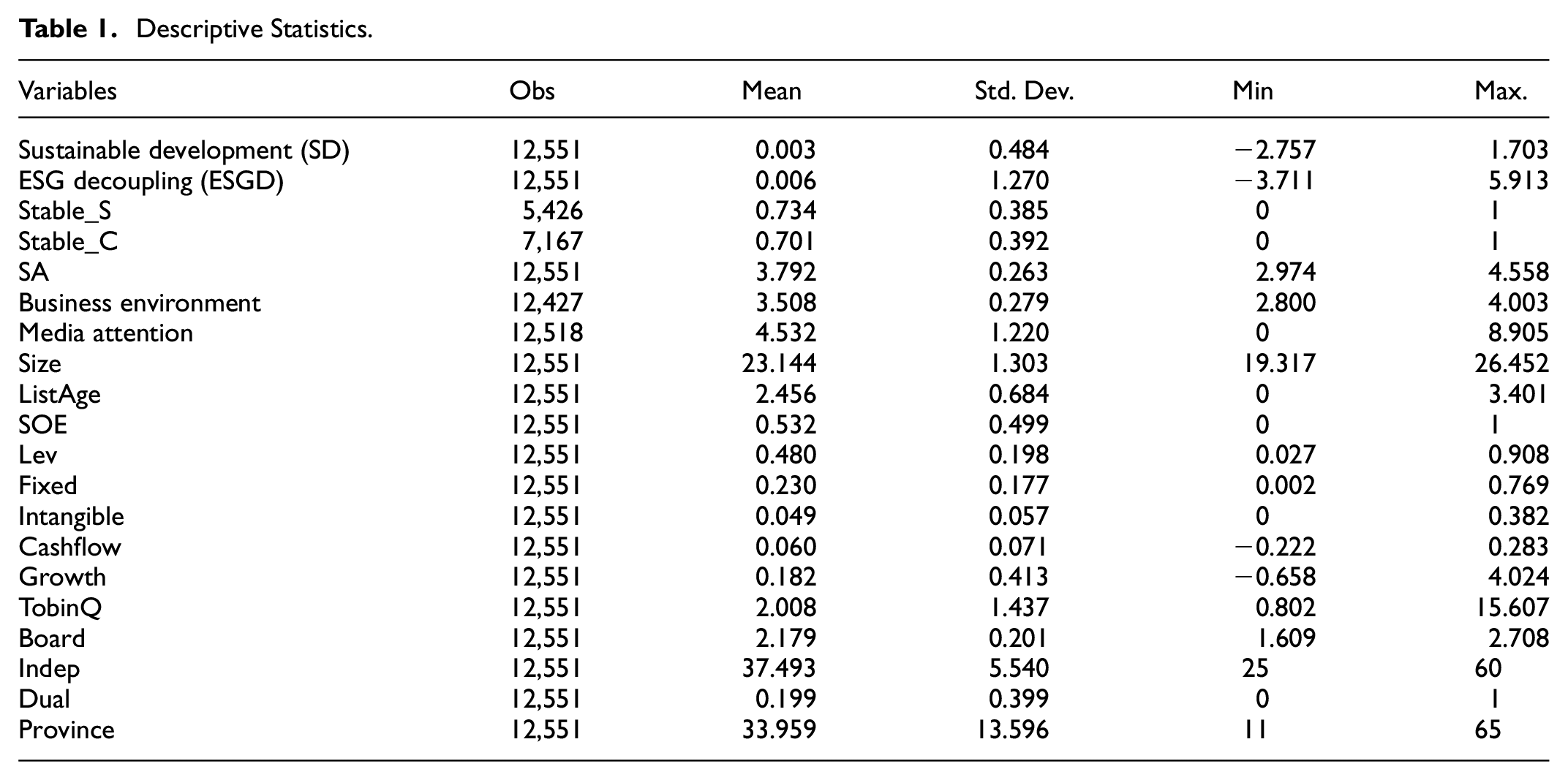

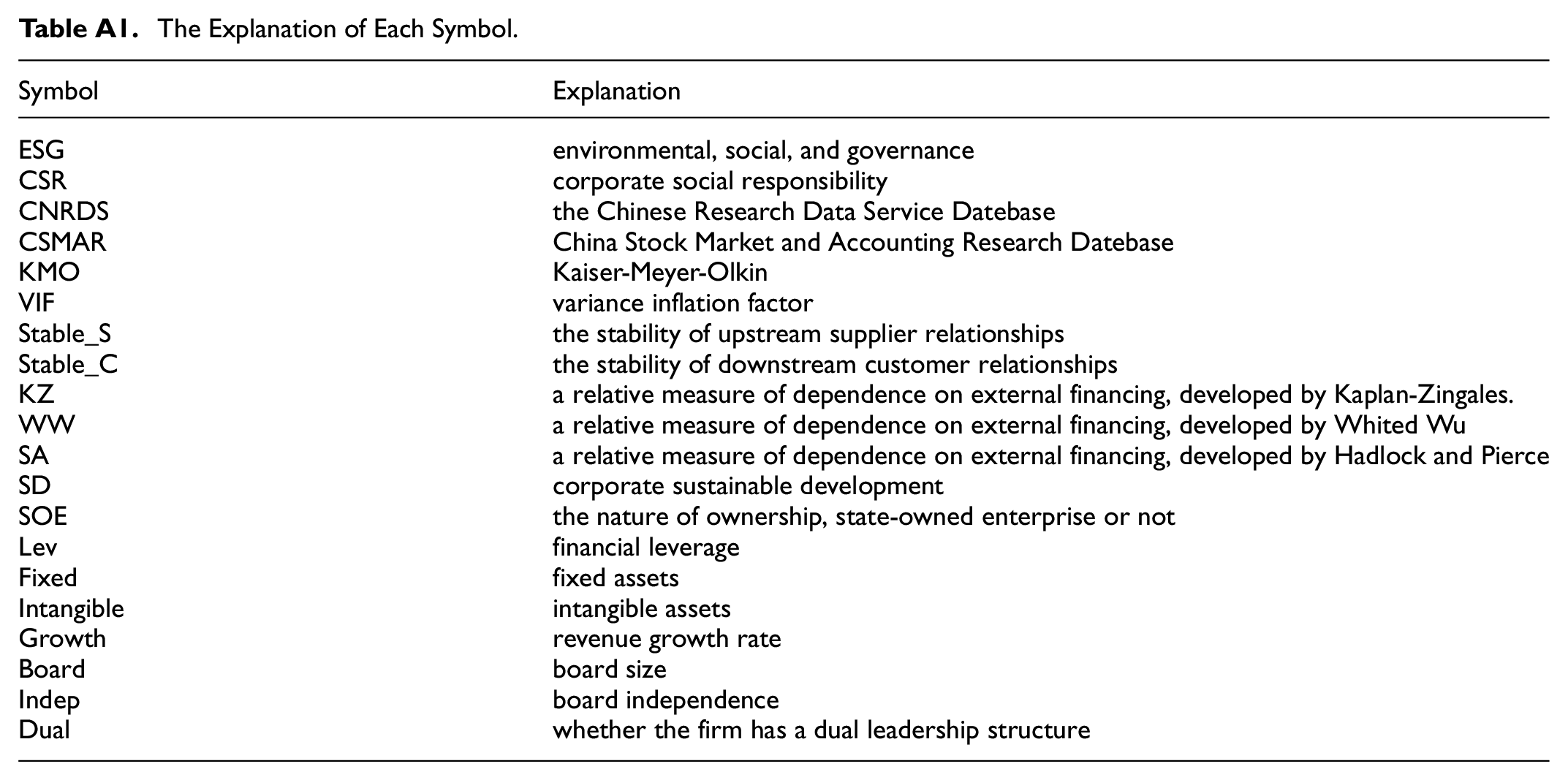

The descriptive statistics of the main variables involved in this paper are as follows (Table 1). The results show that the average score of corporate sustainable development performance is 0.003, with a maximum value of 1.703. This indicates that there is substantial room for improvement in the sustainable development performance of Chinese A-share listed companies, which warrants attention. The average value of ESG decoupling is 0.006, with a maximum value of 5.913. This suggests a significant challenge in ESG decoupling, which is consistent with previous studies (Chen et al., 2024; Sun et al., 2025). Moreover, the average values of Stable_S and Stable_C are 0.734 and 0.701, both of which are at a moderately high level. This indicates that these two variables perform well overall but still have potential for further enhancement. The average values of SA and business environment are 3.792 and 3.508, both falling within the upper-middle range. The average value of media attention is 4.532, suggesting that the sample companies generally attract a relatively high level of attention. Other control variables are not repeated here. The symbols for all variables in this paper can be found in Table A1.

Descriptive Statistics.

Empirical Framework

To test the impact of ESG decoupling on corporate sustainability performance, this paper constructs the following model:

where i represents the firm, t represents time,

To verify the mediating role of supply chain partnership stability in the impact of ESG decoupling on corporate sustainable development performance, this paper refers to the three-step mediation effect procedure outlined by Wen et al. (2024) and constructs the following model:

Among them,

To verify the mediating role of financing constraints in the impact of ESG decoupling on corporate sustainable development performance, the model is constructed as follows:

Where

To verify the moderating role of the institutional environment in the impact of ESG decoupling on corporate sustainable development performance, this paper constructs the model as follows:

Where

Empirical Results

Multicollinearity Test

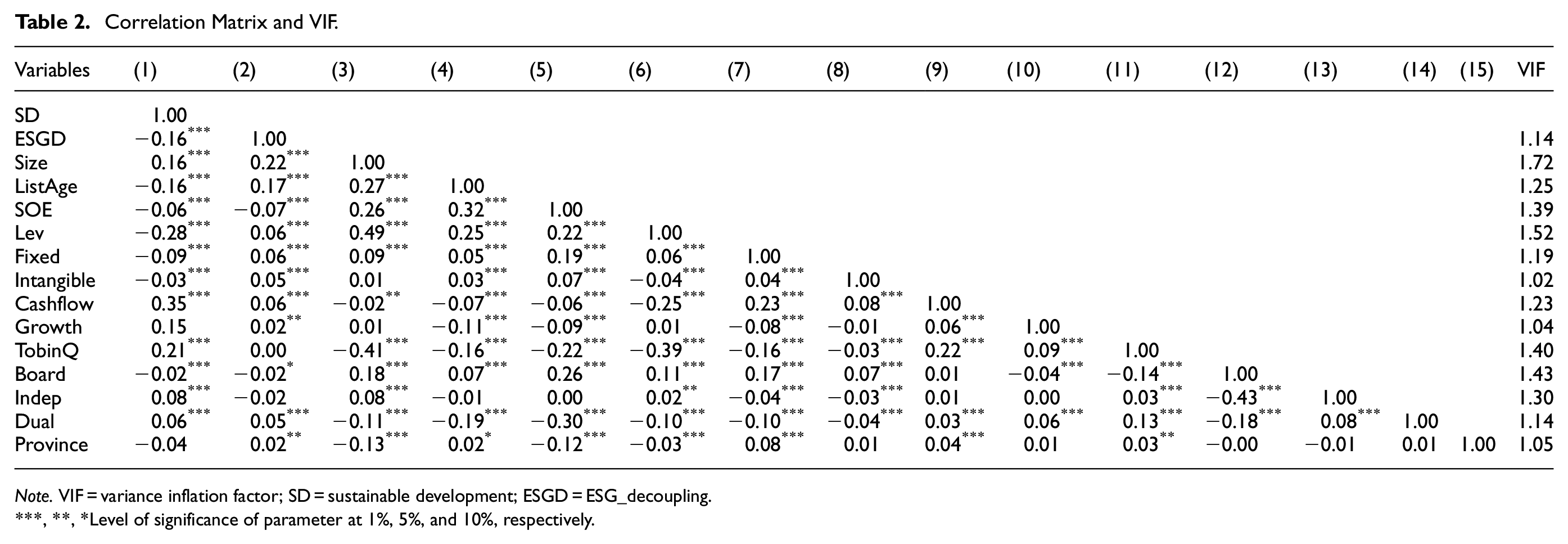

To check for severe multicollinearity in the model specification, we calculate the correlation coefficient and the variance inflation factor (VIF) before performing the following regression analyses. The results in Table 2 show that the correlation coefficients between the variables are all less than 0.5, and the values of the VIF are much less than 10. This indicates that our empirical study does not suffer from severe multicollinearity problems (Brooks, 2014; MacCallum & Browne, 1993).

Correlation Matrix and VIF.

Note. VIF = variance inflation factor; SD = sustainable development; ESGD = ESG_decoupling.

, **, *Level of significance of parameter at 1%, 5%, and 10%, respectively.

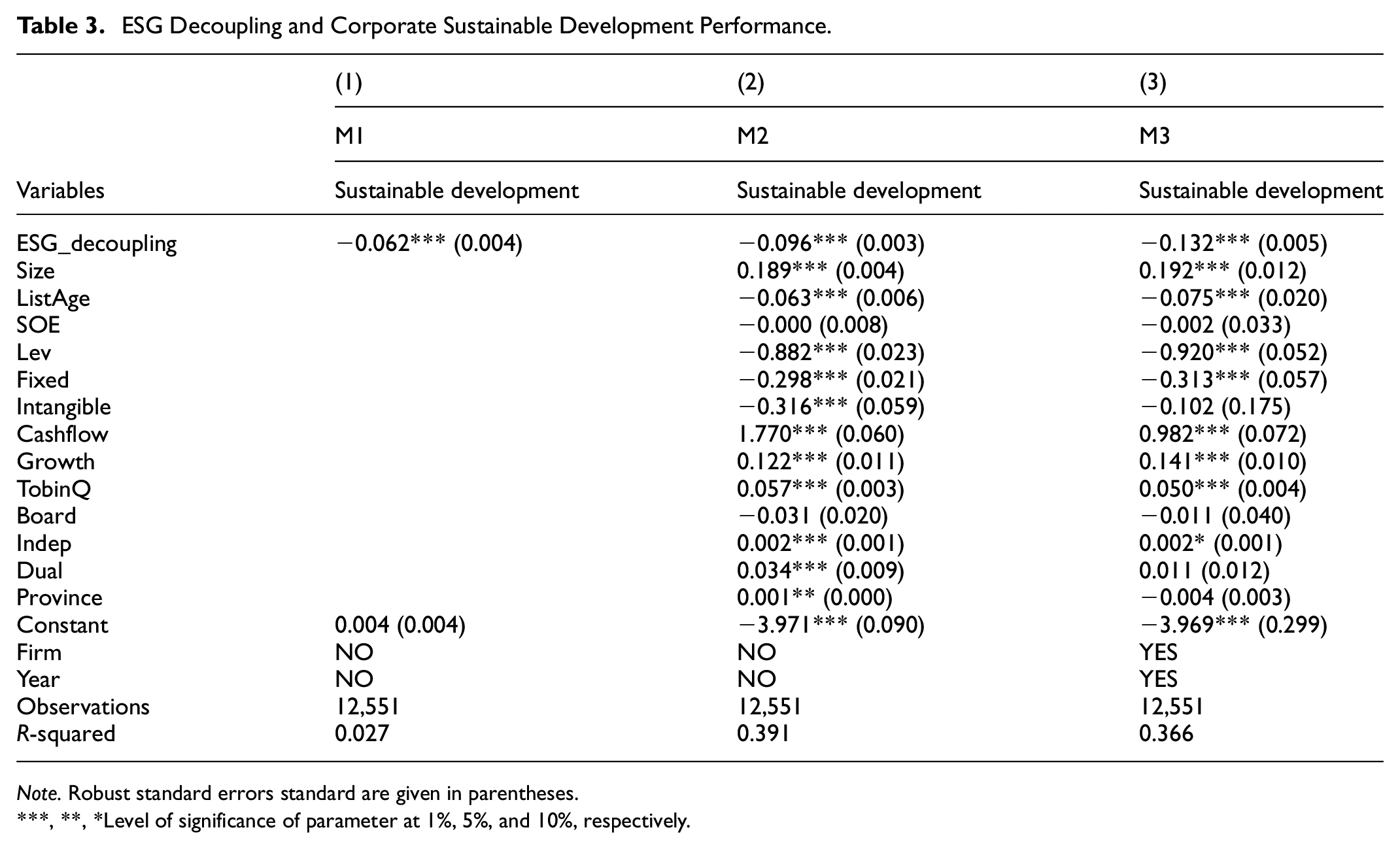

Baseline Result

In this section, we investigate the relationship between ESG decoupling and corporate sustainable development performance, specifically (H1). Table 3 outlines the outcomes of three regression models: Column (1) presents a straightforward OLS regression devoid of control variables; Column (2) refines the analysis with the inclusion of control variables; and Column (3) employs a year-firm fixed-effects model with control variables, each revealing significant results. The main results of the analysis for H1, as reported in Column (3) of Table 3, indicate a highly significant negative relationship at the 1% level (β = −.132, p < .01). This result indicates that the ESG decoupling behavior has a significant negative impact on corporate sustainability. In terms of effect size, the β coefficient of −0.132 implies that for every 1-unit increase in the incidence of ESG decoupling, the corporate sustainability performance will decrease by 0.132 units.

ESG Decoupling and Corporate Sustainable Development Performance.

Note. Robust standard errors standard are given in parentheses.

, **, *Level of significance of parameter at 1%, 5%, and 10%, respectively.

This finding aligns with our expectation. In this paper, we examine the ESG decoupling phenomenon, which refers to the misalignment between disclosed information and actual performance. It is a short-sighted behavior that only pays attention to the short term. As previously discussed, such behavior can erode the trust of stakeholders, potentially leading to the disruption of cooperative relationships and increasing the difficulty and cost of corporate financing, thereby adversely affecting the economic performance of the enterprise. ESG decoupling itself is a direct assault on a company’s environmental, social, and governance performance. The series of issues stemming from capital constraints are also detrimental to the realization of corporate technological innovation, further weakening the enterprise’s ability to achieve long-term sustainable development. The price of shortsighted behavior is the sacrifice of the enterprise’s sustainable development. Therefore, H1 is accepted.

Robustness Checks

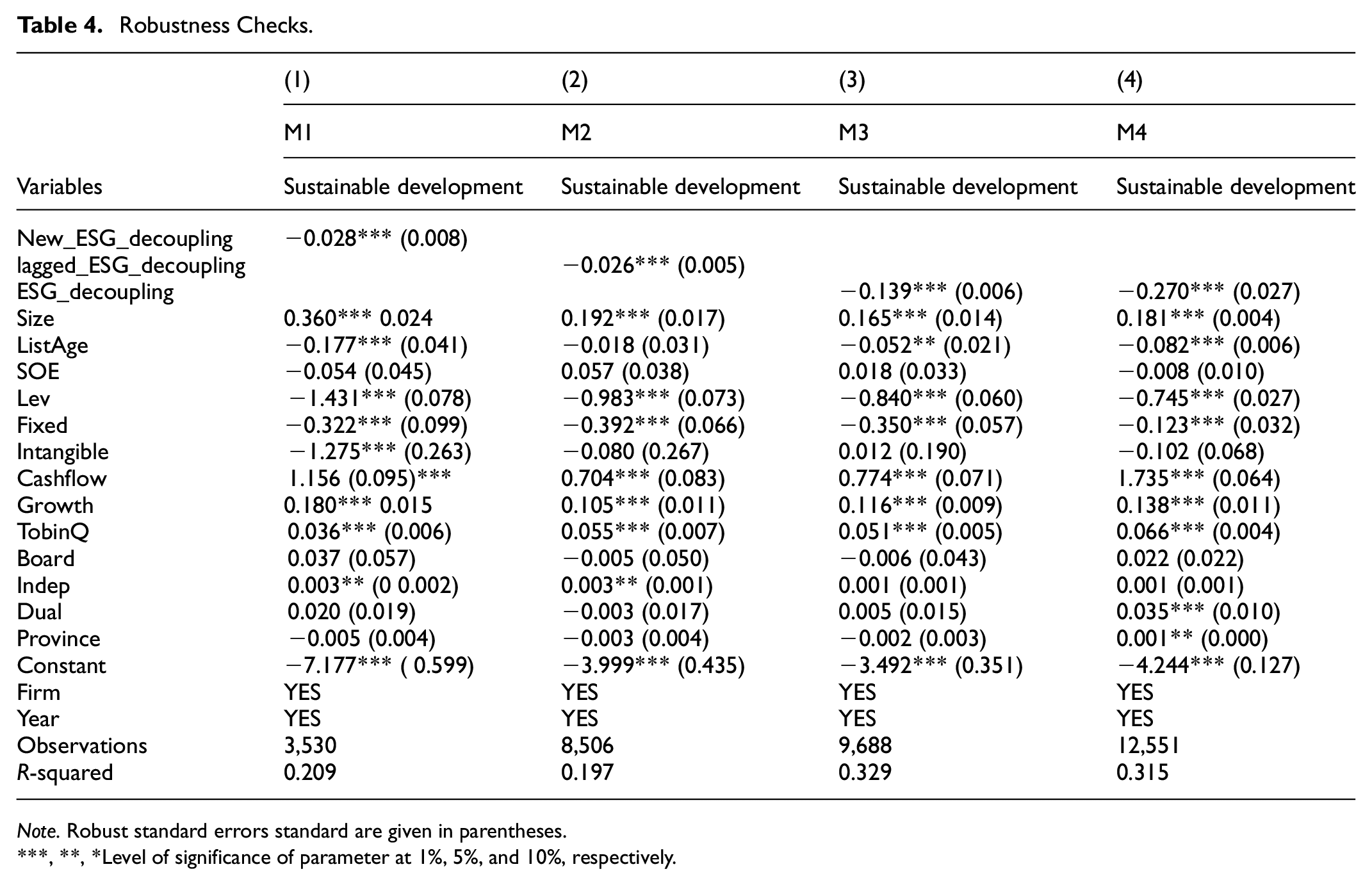

Alternative Explanatory Variable

To strengthen the robustness of our results, we have adopted the method of substituting the ESG rating agency. Specifically, we have chosen the ESG performance data from SynTao Green Finance to measure the actual ESG performance. 6 SynTao Green Finance is a leading professional service institution in China for green finance and responsible investment. It launched its independently developed ESG rating system in 2015 and established the earliest ESG database for listed companies in China. This system is capable of accurately identifying the actual ESG performance of companies in the Chinese market. Based on this data, we further calculated the ESG decoupling. The results show that after substituting the measurement method of the variable, the impact of ESG decoupling on corporate sustainable development performance remains significantly negative (Table 4, column (1)), which confirms the robustness of our findings.

Robustness Checks.

Note. Robust standard errors standard are given in parentheses.

, **, *Level of significance of parameter at 1%, 5%, and 10%, respectively.

Lagged Explanatory Variable

Considering the potential time lag in the impact of ESG decoupling behavior on corporate sustainable development performance, we lag the measurement of ESG decoupling by one period. This means we are exploring the effect of current-period ESG decoupling on sustainable development performance in the next period as part of a robustness test. In Table 4, Column (2) shows that after lagging the explanatory variable by one period, the impact of ESG decoupling on corporate sustainable development performance remains significantly negative. This supports the robustness of the benchmark regression results obtained in this paper.

Alternative Sample

Our research sample spans from 2009 to 2022, which includes 3 years during the COVID-19 pandemic. The impact of the pandemic on corporations could cause the data related to ESG decoupling and corporate sustainable development to deviate from the true state. After removing the samples from 2020 to 2022, the regression results remain generally consistent with the baseline regression (Table 4, column (3)).

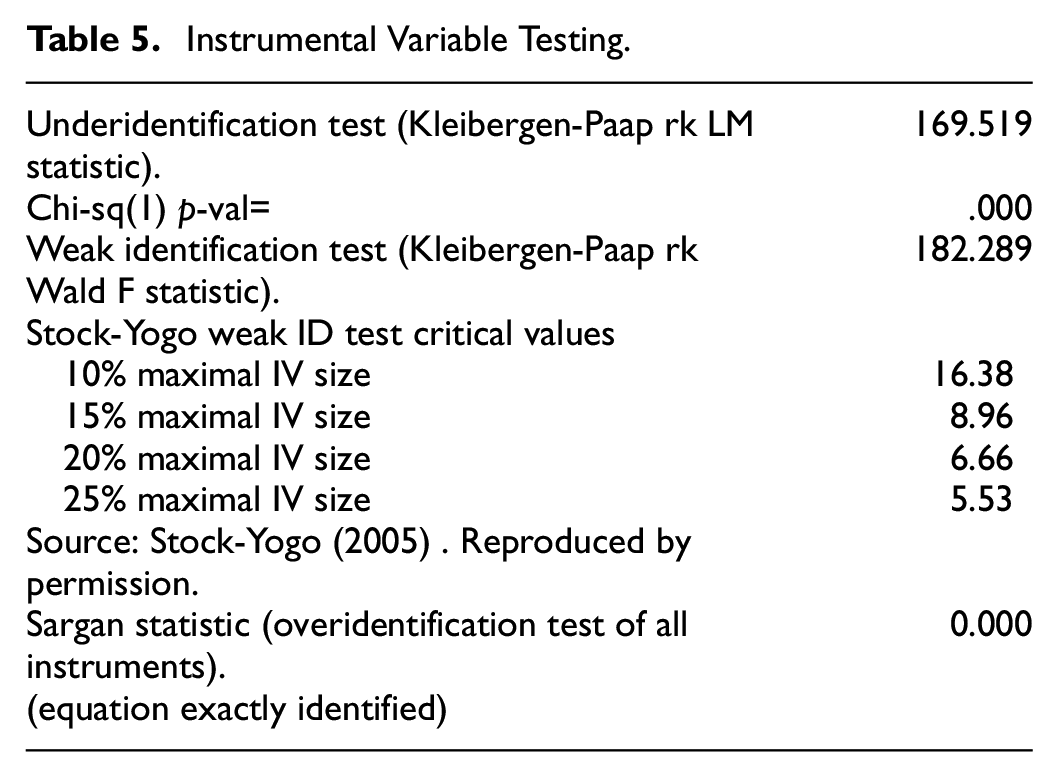

Instrumental Variable

To further alleviate potential endogeneity in the model, we adopt the approach of Huang et al. (2023) and Zhou et al. (2024), using the average value of the ESG decoupling of other companies within the same province as an instrumental variable. The results of column (4) in Table 4 show that after regressing with the instrumental variable, the effect of ESG decoupling on corporate sustainable development is still significantly negative at the 1% level. To further test the validity of the selected instrumental variables, a series of diagnostic tests were conducted, and the results show that the selected instrumental variables in this paper are valid and the benchmark regression results are robust (Table 5).

Instrumental Variable Testing.

Mechanism Analysis

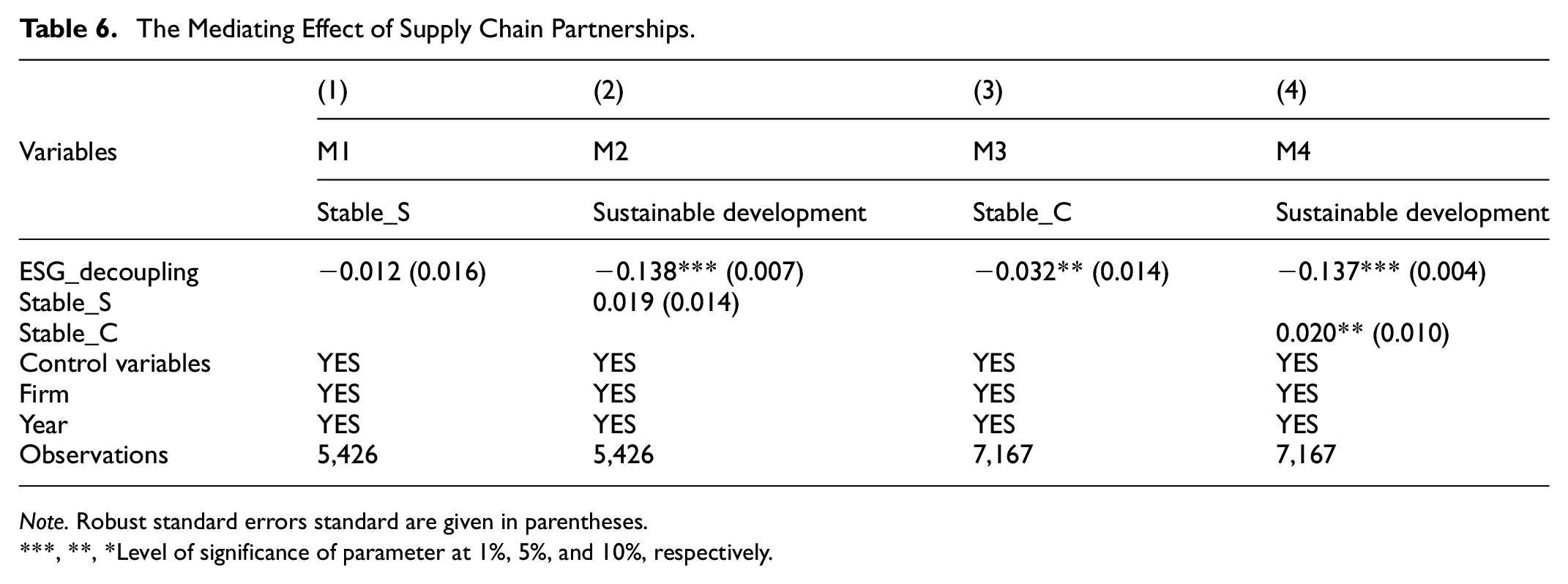

The Mediating Effect of Supply Chain Partnerships

Table 6 shows the results of the mechanism for supply chain partnerships. In column (1), the effect of ESG decoupling on supplier partnership stability is negative but not significant. In column (2), the effect of ESG decoupling on corporate sustainable development performance is still significantly negative, and the effect of supplier partnership stability on corporate sustainable development performance is positive but not significant. This indicates that the mediating effect (H2a) of supplier partnerships in the impact of ESG decoupling on corporate sustainable development performance is not proved in this paper. In Column (3), ESG decoupling is significantly negatively correlated with downstream customer relationship stability at the 5% level (β = −.032, p < .05), which reveals the weakening effect of ESG decoupling on the stability of downstream customer partnerships. In column (4), customer relationship stability is significantly positive at the 5% level (β = .020, p < .05), and the ESG decoupling coefficient is still significantly negative, which indicates that there is a partial mediating effect of customer relationship stability, that is, ESG decoupling negatively affects corporate sustainable development performance by weakening the stability of customer relationships. Therefore, H2b is accepted.

The Mediating Effect of Supply Chain Partnerships.

Note. Robust standard errors standard are given in parentheses.

, **, *Level of significance of parameter at 1%, 5%, and 10%, respectively.

Upstream suppliers and downstream customers are directly involved in the process of corporate value creation, which can help corporations control costs, diversify risks, promote innovation, improve market responsiveness, and shape competitive advantages (Cao & Zhang, 2011; Dubey et al., 2024). As a key stakeholder in the impact of ESG decoupling on corporate sustainability performance, supply chain partnership stability is supposed to play a significant mediating role. However, the non-significant results exhibited by supplier partnership stability lead us to further consider the more complex reasons for this.

Indeed, there is heterogeneity among corporate partnerships with suppliers and customers. Firstly, in the business ecology constructed by enterprises and downstream customers, downstream customers have a strong voice because of their dominant position in the buyer’s market. In this type of market structure, downstream customers often set stricter ESG criteria to meet the growing market demand for sustainable products and protect their brand image and market share. Once a company engages in ESG decoupling, downstream customers are more likely to mitigate potential market risks by reducing orders, reassessing cooperation, or seeking other partners. Such strategic adjustments will undoubtedly have a substantial impact on the stability of the cooperative relationship between enterprises and their downstream customers, thereby affecting corporate sustainable development. In the interaction between companies and their upstream suppliers, companies often find themselves in a buyer’s market, with a dominant position in the cooperative relationship. Under such circumstances, suppliers tend to focus their strategies on meeting the rigid demands of customers, such as product quality and pricing, delivery schedules, and payment terms. In contrast, suppliers are not particularly concerned about a company’s ESG practices. Such resource allocation and decision-making orientation prevent corporate ESG decoupling from significantly impacting the stability of their relationship with suppliers. Secondly, companies closer to end consumers usually have more negotiating leverage in the supply chain (Hillebrand & Biemans, 2011). Downstream customers are closer to end consumers and perceive the firm’s ESG image more directly. ESG decoupling can easily trigger consumer resentment, leading to reduced purchases or even product boycotts, posing a direct challenge to the brand image of downstream customers and winning the trust of end consumers. Accordingly, upstream suppliers are farther away from the end consumer market than downstream customers, and the impact of ESG decoupling is not significant for supplier partnerships. Furthermore, the sample period for this research is 2009 to 2022, during which the Chinese market predominantly exhibited a buyer’s marketplace characterized by excess capacity across most industries. Especially since the end of 2015, when the Chinese government introduced the five primary tasks of removing production capacity, removing inventories, removing leverage, lowering costs, and replenishing short boards, most traditional industries, particularly iron and steel, coal, and building materials, have faced significant challenges in adjusting excess capacity. In the context of supply-side structural reform, downstream customers, as the dominant force in a buyer’s market, tend to impose stricter requirements on corporate ESG practices than upstream suppliers. Therefore, the above analysis of the difference in the impact of ESG decoupling on the stability of different partner relationships has a certain logical rationality and practical basis.

The Mediating Effect of Financing Constraints

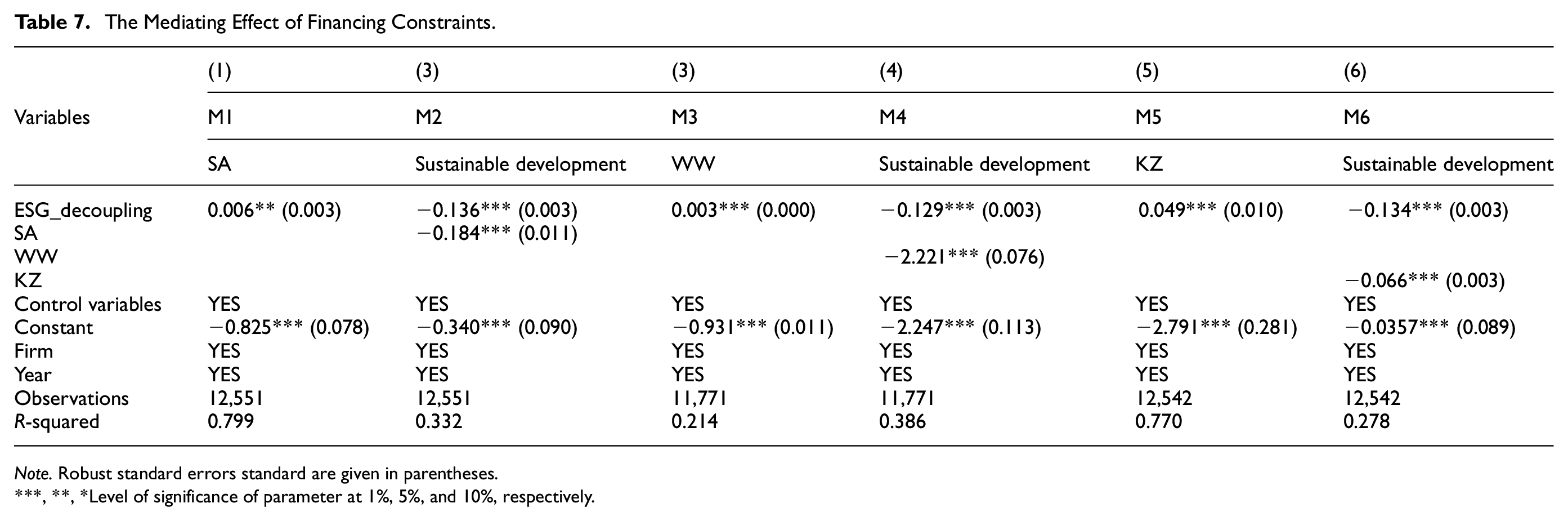

Table 7 shows the results of the mechanism of financing constraints. Column (1) reveals a significant positive relationship between ESG decoupling and the intensity of financing constraints at the 5% confidence level (β = .006, p < .05), and since this paper takes the financing constraint index in absolute value, this result suggests that ESG decoupling exacerbates the intensity of financing constraints faced by corporations. In column (2), the intensity of financing constraints is significantly negative at the 1% level (β = −.184, p < .01), and the coefficient of ESG decoupling is still significantly negative, which indicates that there is a partial mediating effect of financing constraints, that is, ESG decoupling negatively affects corporate sustainable development by exacerbating financing constraints faced by corporations. Although this paper uses the SA index to measure financial constraints, we also recognize that the KZ and WW indexes may have advantages in certain aspects. For instance, the KZ index can more directly reflect a company’s financial leverage, while the WW index can more accurately measure a company’s liquidity. To further verify our results, we conducted regression analyses using the KZ and WW indices as well (columns (3)–(6)). The findings indicate that financial constraints measured by both the KZ and WW indexes also play a significant mediating role in the impact of ESG decoupling on corporate sustainability performance, which is consistent with our results based on the SA index. Therefore, H3 is accepted.

The Mediating Effect of Financing Constraints.

Note. Robust standard errors standard are given in parentheses.

, **, *Level of significance of parameter at 1%, 5%, and 10%, respectively.

We explore financing constraints essentially to dissect the impact of the ESG decoupling phenomenon on stakeholders such as investors (including banks and financial institutions) and regulators, who are intrinsically linked to corporations. As the focus on corporate sustainability intensifies, investors are placing greater emphasis on a company’s ESG performance when evaluating its investment potential. The act of companies engaging in deceptive ESG decoupling, which involves an exaggeration of their true practices, can significantly undermine investor confidence and influence their investment choices. Banks and financial institutions, being pivotal in corporate financing, may respond to such deceptive practices by increasing lending rates or curtailing the volume of loans they extend, thereby increasing the cost of corporate finance. Concurrently, regulators might enforce more stringent measures against corporations that exhibit ESG decoupling, demanding enhanced transparency and disclosure standards. These corporations might also be subject to penalties or other legal repercussions, all of which would inevitably exacerbate the challenges they face in accessing capital markets. This situation poses a significant barrier to their sustainable development. Therefore, adhering to the consistency between ESG commitments and actual actions is a core principle that corporations must abide by.

Further Analyses

The Moderating Effect of Formal Institutional Environment

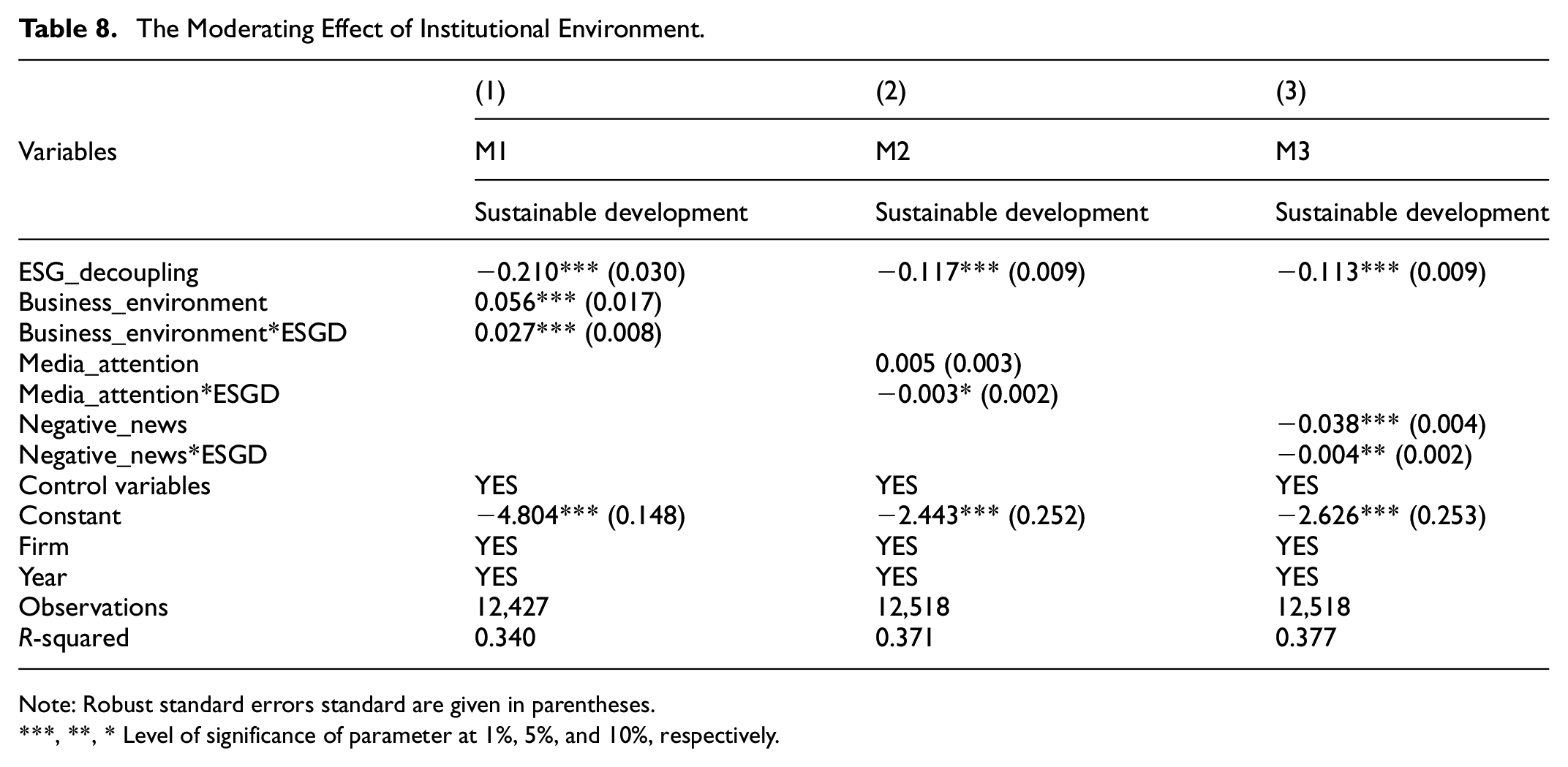

We use the China Business Environment Index as a proxy for the formal institutional environment, introducing the interaction term between the business environment and ESG decoupling to explore the moderating effect of the formal institutional environment on the impact of ESG decoupling on corporate sustainable development performance. The results in column (1) of Table 8 show that the interaction term between the business environment and ESG decoupling exhibits a significant positive effect, indicating that, as a representative of the formal institutional environment, a favorable business environment can mitigate the negative impact of ESG decoupling on sustainable development. Therefore, H4a is accepted.

The Moderating Effect of Institutional Environment.

Note: Robust standard errors standard are given in parentheses.

, **, * Level of significance of parameter at 1%, 5%, and 10%, respectively.

A favorable business environment reflects the presence of robust laws, regulations, and policy support. These formal institutional frameworks can, on the one hand, provide corporations with more resources and support and, through incentives such as tax benefits and subsidies, encourage the practice of sustainable development. On the other hand, a good business environment usually comes with higher requirements for information transparency and stricter accountability systems. Once corporations engage in ESG decoupling behavior, they will face greater institutional punitive pressure, forcing them to take corrective measures in a timely manner. Moreover, a more robust business environment also has more comprehensive corrective mechanisms to help corporations enhance their ability to make corrections. Therefore, although the behavior of ESG decoupling poses a challenge to the sustainable development of corporations, in a more mature institutional environment, corporations can take corrective actions more proactively, promptly, and effectively, which to some extent helps to alleviate the negative impact of ESG decoupling on corporate sustainable development.

The Moderating Effect of Informal Institutional Environment

This paper uses media attention to measure the informal institutional environment. Column (2) of Table 8 presents the estimated results of the moderating effect of media attention as an association between ESG decoupling and corporate sustainable development performance. ESG decoupling remains significantly associated with a decline in corporate sustainability, and the estimated coefficient of the interaction term is significant and in the same direction as the ESG decoupling coefficient. The results indicate that as an informal institution, media attention intensifies the impact of ESG decoupling on corporate sustainability. Therefore, H4b is accepted.

Media coverage is an important channel for various stakeholders to obtain information about the firm (Kölbel et al., 2017). Intensive media attention implies that corporate ESG practices are subject to broader public scrutiny. This prompts diverse entities such as governments, financial institutions, and consumers to activate a joint oversight mechanism. Stakeholders will react more swiftly and sensitively to ESG decoupling. Moreover, once ESG decoupling occurs, the public opinion pressure formed by media reporting can trigger a cascading effect on corporate reputation risk. Compared to regulatory penalties, this reputation loss driven by public perception has stronger persistence and diffusion. Ultimately, it is transmitted to corporate performance through channels such as capital market valuation adjustments and the termination of supply chain cooperation. Therefore, high-intensity media coverage will amplify the impact of ESG decoupling, a negative behavior, on corporate sustainability. To verify the amplification effect of negative news, we further focus media attention on negative media coverage and explore the moderating role of negative news coverage between ESG decoupling and corporate sustainable development performance. The results in column (3) of Table 8 show that negative news coverage indeed exacerbates the negative impact of ESG decoupling on corporate sustainability, and our perceived negative amplification effect is validated.

Conclusion

This study aims to examine the impact of ESG decoupling on corporate sustainable development and its underlying mechanisms. The empirical results show that ESG decoupling has a significant negative impact on corporate sustainability performance. By focusing on key stakeholders such as investors, supply chain partners, regulators, and the public, the mechanisms tests show that financial market participants are highly sensitive to corporate ESG performance, and ESG decoupling exacerbates financing constraints and impedes their sustainable development. At the supply chain level, ESG decoupling reduces the stability of the relationship between corporations and their downstream customer partners, which in turn undermines corporate sustainable development performance. From the perspective of regulators and the public, we find that the negative impact of ESG decoupling on sustainable development is mitigated to a certain extent in a more perfect formal institutional environment, which is not unrelated to the characteristics of China’s economic model of big government and small market. On the contrary, the negative impact of ESG decoupling is further amplified under the more stringent informal institutional environment.

Our findings also provide significant insights for corporate managers and policymakers. It is imperative for company managers to enhance the quality and transparency of ESG information disclosure to alleviate the adverse effects of ESG decoupling. Firstly, integrate sustainable development concepts into corporate strategic objectives, form a dedicated ESG team, and guarantee the incorporation of ESG principles throughout all corporate operations. Secondly, establish appropriate internal procedures, including reward and restraint systems, evaluation and supervision, and risk prevention, to guarantee that ESG report data is accurate. Furthermore, enhance communication with all stakeholders. Ensure consistent communication with investors and conduct frequent briefings on ESG performance. Collaborate with upstream and downstream partners to establish ESG targets and action plans, conduct periodic joint audits and assessments, address ESG issues collaboratively and promptly, and create a sustainable supply chain. Closely monitor national and local ESG policy and regulatory changes, actively engage in policy formulation feedback, develop media communication strategies, proactively disclose corporate ESG achievements and improvement measures, and respond actively to public concerns regarding ESG issues.

For policymakers, it is essential to develop specific and quantifiable ESG standards and guidelines tailored to the characteristics of different industries, and to impose stricter penalties for ESG decoupling behaviors. They should support third-party institutions in conducting independent assessments and certifications of corporate ESG performance, and implement mandatory independent ESG audits to ensure that the evaluations are objective, fair, and accurate. Additionally, policymakers should enhance the supervision of corporate ESG decoupling behavior and refine the penalty mechanisms for violations. In addition, ESG incentive funds should be set up to provide outstanding corporations with financial rewards, tax incentives, and other incentives. At the same time, the ESG investment market should be fostered, and financial institutions should be encouraged to develop ESG-related financial products and services, such as ESG index funds and green bonds, etc. Lastly, an ESG information-sharing platform should be actively built to bring together ESG information from all parties, promote communication and cooperation among stakeholders, and establish channels and mechanisms for public participation in supervision.

Despite its meaningful findings, this study suffers from certain limitations. Firstly, limited by data availability, this study did not investigate the adverse impact of varying degrees of ESG decoupling across different industries or sectors on corporate sustainability. This limitation may restrict the generalizability of the research findings across industries. Secondly, while theoretical analysis has been conducted on the mediating role of supplier relationship stability, more empirical validation is still needed. Additionally, this study primarily relied on publicly available corporate data, without incorporating methods such as field surveys or questionnaires to directly obtain opinions from end consumers and employees. This may affect the comprehensiveness and depth of the research conclusions. Future studies could involve getting detailed opinions from various stakeholders, tailored to the unique needs of specific industries and markets.

Footnotes

Appendix

The Explanation of Each Symbol.

| Symbol | Explanation |

|---|---|

| ESG | environmental, social, and governance |

| CSR | corporate social responsibility |

| CNRDS | the Chinese Research Data Service Datebase |

| CSMAR | China Stock Market and Accounting Research Datebase |

| KMO | Kaiser-Meyer-Olkin |

| VIF | variance inflation factor |

| Stable_S | the stability of upstream supplier relationships |

| Stable_C | the stability of downstream customer relationships |

| KZ | a relative measure of dependence on external financing, developed by Kaplan-Zingales. |

| WW | a relative measure of dependence on external financing, developed by Whited Wu |

| SA | a relative measure of dependence on external financing, developed by Hadlock and Pierce |

| SD | corporate sustainable development |

| SOE | the nature of ownership, state-owned enterprise or not |

| Lev | financial leverage |

| Fixed | fixed assets |

| Intangible | intangible assets |

| Growth | revenue growth rate |

| Board | board size |

| Indep | board independence |

| Dual | whether the firm has a dual leadership structure |

Ethical Considerations

This article does not contain any studies with human or animal participants.

Consent to Participate

There are no human participants in this article and informed consent is not required.

Author Contributions

Xiaoyi Zhan: Conceptualization, Methodology, Software, Investigation, Formal Analysis, Writing - Original Draft. Yong Zhan: Data Curation, Writing - Original Draft. Guangjin Li (Corresponding Author): Conceptualization, Funding Acquisition, Resources, Supervision, Writing - Review & Editing.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The data of this study are available on request from the corresponding author.