Abstract

This study is conducted to investigate the impact of ownership structure on earnings management in emerging countries and Vietnam as the case study. In this research, we explore how three components of ownership structure, including ownership concentration of managers, foreign ownership ratio, and state ownership ratio, influence earnings management. In addition, we also consider whether ownership structure influences profit management during financial constraints. REM, FEM, GLS, and GMM regression methods are employed for processing data. The results show that ownership structure with foreign ownership has a positive effect on earnings management, whereas one with a proportion of state ownership has a contradicting effect. While the degree of ownership concentration does not affect the profit management, in the context of financial restrictions, the ownership ratio has an impact on the management of earnings. Control variables in the model such as firm size, financial leverage, growth rate, profitability, and audit quality, all have an impact on earnings management. The results could, potentially, be the basis to help firms in restricting earnings management behavior.

Introduction

The information in the annual report of the enterprise plays the role of connecting a business with many different information users outside the business as how enterprises provide useful information to a user, so that they can make rational decisions to meet their goals. In particular, earnings information is considered one of the most important financial information affecting all stakeholders of the business because earnings value is an important indicator of the efficiency and growth prospects of the business. Hence, any intervention that may distort the accuracy of the information in the reports influences the decision of those using the financial statements. Financial scandals of Enron, WorldCom and Parmalat in the early 2000s in the world as well as in Vietnam such as Bong Bach Tuyet, Vien Dong Pharmaceutical, all related to distortions of financial statements. It has a significant impact on the economy and influences the public’s confidence in the quality of information on the financial statements of firms, especially listed firms.

According to the agency theory, the separation of owners and managers leads to conflicts of interest between them, thus monitoring managerial decisions can improve the alignment between management and interests of shareholders while, at the same time, minimize the opportunity behaviors due to conflicts of interest. In fact, the hike in accounting scandals has pointed out the need to improve the quality of information on financial statements by establishing good governance structures. Good corporate governance allows maximizing corporate value and transparency in information disclosure. In the view of corporate governance system, the ownership structure is a component that is paid attention to by many researchers. Ali et al. (2008) reveal that managers who own a significant portion of the equity of a firm have little incentive to manipulate accounting information, so it may limit earnings management behavior. Shaikh and Shah (2012) argue that institutional investors are more likely to detect earnings management issues than non-institutional investors because they have access to timely and relevant information. In these studies, the firm’s ownership structure has a significant influence on earnings management, thereby influencing the earnings quality information on the financial statements.

Theoretical Framework

Earnings Management

Earnings management is an issue that many researchers are much interested in and have commented on. However, there is, at least for the time being, still no consensus on the definition of earnings management (Beneish, 2001). According to Schipper (1989), earnings management is understood as the adjustment of profits to achieve the management’s previously set goals, which is a deliberate intervention in the process of providing financial information to achieve personal goals. Levitt (1998) defines earnings management as a dark area where accounting is being wronged because the administrator has “cut” its aspects according to their wishes. Therefore, the comprehensive income statement reflects the management’s wishes rather than the actual financial situation of the business. In addition, Healy and Wahlen (1999) argue that earnings adjustments occur when managers use accounting estimates or internal transactions to influence financial statements, in order to mislead some related parties about the company’s business situation or affect contracts which have commitments based on accounting earnings targets. Akers et al. (2007) define earnings management as management efforts to influence or “manipulate” income statements using special accounting methods (or methods are changing), recognition of an item at a non-recurring level, delaying or accelerating the recording of cost or revenue transactions, or other methods designed to influence short-term income. Beneish (2001) argues that earnings is a deliberate intervention to provide useful and truthful financial information about the business situation of enterprises to investors and stakeholders to help them make financial decisions related to the business.

Summarizing the previous concepts of earnings management, Fogel-Yaari and Ronen (2020) classified earning management into three groups of white, gray, and black. The white group represents earnings management in a beneficial way and increases the quality of financial statement; the gray group involves the manipulation of accounting data within or outside the permitted limits for the purpose of opportunity or (supposedly) economic efficiency, while the black group reveals the use of tactics to falsify or reduce the transparency of financial statements. Since then, Fogel-Yaari and Ronen (2020) has presented a general concept covering all aspects of earnings management. According to them, earnings management is viewed as a set of management decisions resulting in a failure to report the status quo in the short term, maximizing the value of earnings accordingly to management expectations. Earnings management can be beneficial, harmful, or neutral. If it is a beneficial signal, then the value is long-term; harmful, then concealing short-term; long-term and neutral values will detect the true performance in the short term. As such, this concept not only includes the management of earnings but also states other management decisions, for the purpose of presenting profits that are different from the actual profits in the managers’ knowledge. At the same time, this concept also implies that legal or illegal earning management is misleading when providing valuable information to users of financial statements, affecting the quality of financial statements of the business.

We could here argue that earnings management is a purposeful action of managers by using income-controlling methods such as accounting policy selection or through performing economic operations, using management actions intended to be misleading when providing information to users to gain certain benefits. Most studies such as Lo (2008), Graham et al. (2005), Dang et al. (2017) grouped earnings management into two categories including real earnings management as an effect of cash flow, and earnings management based on accrual accounting variable (accrual management) through changes in accounting policies and accounting estimates. However, there are many opinions supporting that managers would employ the approach of accrual accounting adjustments to change revenue shifting between accounting periods or in deferred spending (Dechow et al., 1995; Jones, 1991). Hence, for the purpose of this study, we employ the accrual accounting variable to identify earnings management.

Ownership Structure

In the overall system of corporate governance, the ownership structure is a component that many researchers pay attention to. The concept of ownership structure is an important topic in the broad concept of corporate governance. Jensen and Meckling (1976) employ the concept of “ownership structure” to refer to the capital held between members inside the company (the direct management component) and outside the company (investors not having direct management roles). Similarly, according to Dinga (2005), the ownership structure in the model of firms surveyed is basically fractionated ownership, for example shareholders holding certain capital holdings. In a company, this is an important mechanism to raise a large amount of capital for a modern business organization and create wealth through issuing shares. Thus, the ownership structure is understood as the allocation of equity according to the correlation of equity ratio held by the owners. Ownership structure has a very important influence in running a business because it affects the decision-making of managers. Ownership structure can be defined in two aspects of the degree of ownership concentration and the ownership of shares.

The degree of ownership concentration includes (i) First, the centralized ownership structure is viewed as an individual or a group of related individuals or organizations own a majority of the equity of an enterprise and have the right to manage the decisions of the enterprise. Major shareholders control the business directly by joining the board of directors and management staff. A major shareholder may not own the whole capital but has significant voting rights, so it can still control the business. (ii) Second, distributed ownership structure means that no individual or group of individuals or organizations own the majority of the firm’s capital and have the right to dominate the enterprise. For this form of structure, a company has many shareholders. Each shareholder owns a number of shares, and control of business activities is held by the Board of Directors. Small shareholders have little incentive to closely monitor operations and do not want to participate in running the business.

With regards to the shareholders different ownership rates related to the characteristics of shareholders such as foreign ownership ratio, private ownership rate, state ownership ratio, institutional ownership.

Basic Theories

Agency theory

In a joint stock firm, the authorizing parties or owner are the shareholders who hire the manager—the representative who performs the control and day-to-day decision-making so as to bring the best benefits to the shareholders. However, in the process of operation, managers can make decisions to benefit themselves rather than the interests of shareholders and tend to forget the interests of shareholders when they can achieve certain profitability (Jensen & Meckling, 1976). The separation between ownership and control of the company gives rise to representation. At the same time, when managers have a better knowledge of the future value of the company than shareholders and creditors, they are more likely to take advantage of the owner once the monitoring is ineffective. From the agency theory, it can be seen that there are always contradictions between owners and managers. Contrary to the owner’s expectations of maximizing their benefits, managers sometimes have their own goals and, because of that, these managers make profit adjustments. On the other hand, the manager is also the information provider of the business. For their own benefit, the manager tends to provide little or hide information to the owner. Such action may prevent a financial statement from accurately and reasonably reflecting the company’s operations and fail to provide useful information to its users.

To minimize this behavior, shareholders should align managers with the common interests of shareholders and businesses by salaries, bonuses, or partial ownership of the company’s shares. It is thus necessary to have a mechanism to monitor managers’ decisions to increase shareholder value and disclose information in financial statements accurately and transparently. The level of concentration of ownership has a strong incentive to actively monitor and manage the company to protect their investments. Similarly, institutional investors as well as foreign investors in the company with resources and financial expertise are motivated to supervise managers for reducing representation. For that reason, the agency theory emphasizes that owners need to have appropriate mechanisms to limit the divergence of benefits between owners and managers by establishing appropriate incentive mechanisms for managers through the company’s shareholding ratio and effective monitoring mechanisms to limit managerial self-interest by increasing concentration ownership, ownership of institutional investors, and ownership of foreign investors.

Information asymmetry

The theory of asymmetric information was first mentioned in the study of Akerlof (1970), then further developed by Spence (1973). This theory refers to the existence of information asymmetry. Asymmetric information occurs when one party has less information than the other or has incorrect information. This causes the less informed party to make incorrect decisions when making a transaction, and the more informed party will also have behaviors detrimental to the other party when performing the transaction obligation. The consequence of asymmetric information is the disadvantage caused when the information is concealed before signing the contract and a moral hazard after signing the contract.

In the enterprise, asymmetric information appears in the relationship of managers with shareholders and businesses with investors. Firms that do not send signals or send signals incorrectly will be detrimental to investors. Or the administrator who directly manages will know the business information but intentionally conceal it causing adverse choices for shareholders and the moral hazard of the manager. The lack of information from these organizations will make investors not fully understand the business and production situation of enterprises, securities trading activities, market trends leading to inaccurate investment decisions. The interests of affected investors could lead to the stock market crash. The asymmetric information theory is employed to explain the signaling to the market or enhance the disclosure of good information to help investors distinguish good and bad securities of public joint stock firms. It also helps explain the relationship between information status.

Literature Review

Studies on the relationship between ownership structure and earnings management are investigated in many contexts around the world and are mainly empirical research using quantitative methods. Studies around the world have explored and explained quite fully about the impact of ownership structure on earnings management, but there are differences in results in other countries. These differences might be due to the difference in the selection of determinants related to the ownership structure that affects the earnings management behavior or the model of the earnings management behavior in each country; differences in experimental sample selection (effects of economic, political, and cultural environment in each country); differences at the time of the study (time period chosen for sampling); differences in economic development levels of countries at different time periods.

According to agency theory, the separation of ownership and control leads to a divergence in the pursuit of managerial interests and owner interests (Jensen & Meckling, 1976), thus overseeing management decisions becomes necessary to ensure the interests of shareholders, and to ensure that financial statements are prepared reliably and fully. Corporate governance provides a mechanism to monitor the behavior of managers resulting from conflicts of interest. And the role of the corporate governance structure in financial statements is to ensure compliance with the financial accounting system and maintain the reliability of financial statements (Bushman & Smith, 2003). As such, the properly structured corporate governance mechanism will reduce earnings management behavior since it monitors the performance of managers during the preparation, presentation, and disclosure of financial statements. A number of studies have demonstrated that the management manager’s opportunity is limited by corporate governance (Dechow et al., 1996; Jiambalvo, 1996). The ownership structure of a company is viewed to be an important management oversight mechanism. It can curb profit management ensuring that financial statements provide accurate accounting information. There have been many studies, both theoretical and empirical, that the ownership structure can influence earnings management. The presence of a major shareholder can limit the discretionary behavior of managers to manipulate income, encouraging them to release appropriate and reliable information (Demsetz & Lehn, 1985; Shleifer & Vishny, 1986). Klein (2002) reports that the degree of ownership concentration reduces earnings management in US firms thereby improving the quality of financial information disclosure.

Alves (2012)’s research in Portugal finds that different types of ownership have different relationships with earnings management of businesses, both negative and positive relationships. In the study of Aygun et al. (2014), two components of the ownership structure are the ownership of the manager and the ownership of the organization, find that the organization’s ownership has a negative impact on earnings management, while the effect of the management’s ownership on earnings is positive. Klai and Omri (2011) also examine the impact of ownership structure on earnings management, thereby affecting the quality of financial statements. The results show that the control by foreign countries and ownership concentration is positively correlated with earnings, while the control of the state and financial institutions is negatively correlated with earnings management. Disagreeing with Klai and Omri (2011), Roodposhti and Chashmi (2011) conclude that high ownership concentration has the effect of reducing earnings management behavior, while firms having high amount of organization-owned stocks have considerable earnings. Park and Shin (2004) show that the presence of board members from financial intermediaries and institutional shareholders reduces the earnings management behavior. At the same time, the study also shows that increasing the proportion of external board members increases the earnings management behavior, contrary to the view that increasing the proportion of external board members will help the Board of Directors increase its independence and resolutions for conflicts of interest between small shareholders and major shareholders. Meanwhile, Ali et al. (2008) show that the level of managerial ownership can limit earnings management. At the same time, the study also points out that there is a positive relationship between firm size, and the relationship between management ownership and earnings management. Although managerial ownership may reduce earnings management behaviors, other factors such as firm size might also influence this behavior. Management ownership is an effective monitoring mechanism, especially in small firms, so it should be encouraged in small firms to replace the weakness of other corporate governance mechanisms. Research of Kim and Yoon (2008) shows that the independence of the Board of Directors, ownership concentration, foreign ownership, leverage ratio, and firm size significantly influence the accumulated accruals adjustments and cumulative sum. Yang et al. (2009) find that the rate of earnings management of listed firms in Malaysia was about 16% of total assets the previous year and most firms’ earnings management increased, not decreased. At the same time, the results have no evidence to prove the relationship between the magnitude of earnings management and the proportion of outside directors and institutional shareholders.

Wang and Yung (2011)’s research shows that the level of accumulation of profit management of state-owned firms is lower than that of private firms, which is contrary to the author’s hypothesis as well as the belief of the majority that state ownership is at the root of all inefficiencies in firms. Shaikh and Shah (2012) reveal that institutional ownership has the negative effect on adjusted accruals. Lakhal (2015) shows that the relationship between earnings management and the level of information disclosure is in the opposite direction, that is, less transparent firms have the ability to participate in earnings management activities. The study also finds that family ownership and many major shareholders have a negative influence on earnings. Finally, the presence of institutional investors, which has a supervising role and influences decisions made by managers, is likely to minimize earnings management behavior.

Earnings overstatement can help management have trust from creditors and benefits in negotiating contents in credit agreements (Anagnostopoulou & Tsekrekos, 2017). In contrast, earnings understatement can help adjust debt repayment (Rodríguez-Pérez & van Hemmen, 2010). The magnitude of adjusted earnings seems to know the role of earnings management. In this aspect, creditors have more prudence and supervision increase with firms having high leverage. Anyway, in the studies of Fung and Goodwin (2013) with current liabilities, Lazzem and Jilani (2018) with non-current liabilities, supervision is not enough to control management in earnings management. Recently, some studies have been conducted relating to ownership structure, financial distress such as Jacoby et al. (2019) and El Moslemany and Nathan (2019).

Nguyen et al. (2020) reveals that state ownership has a positive impact on earnings management whereas management’s ownership has a negative impact on it. Wu et al. (2020), Tran (2020) warn the necessity in designing proper policies for reducing earnings management behaviors from policy makers for providing reliable financial information. Saona et al. (2020) find the evidence of earnings management reduction in case of high vote rate of shareholders and a negative relationship between ownership of employees and earnings management.

Research Methodology

Research Model

To identify earnings management, researchers consider the choice of firms’ accounting policies or measure accruals. We employ Modified Jones’s model (Dechow et al., 1995) to calculate cumulative accounting variables representing earnings management. The Modified Jones model is a variant of the Jones’ model (Jones, 1991), and improved by Dechow et al. (1995) by replacing the change of turnover with the change of receivable debt. The modified model was developed to reduce the original model’s error in identifying abnormal cumulative variables:

In which:

NDAit is non discretionary accruals

Variable measurement and expectation of hypotheses are presented in Table 1

Summary of Measurement Variables and Hypotheses.

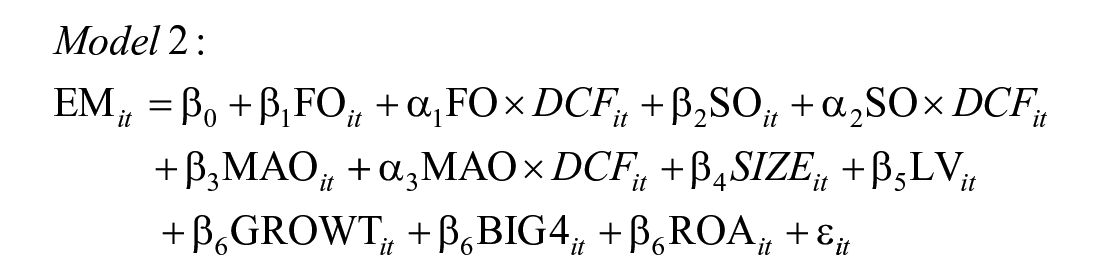

After examining the impact of ownership structure on earnings management, we continue to check whether the fact that the company is financially constrained or not affects asymmetrically. Based on the practical situations in Vietnam, this research employs two criteria to classify the sample as limited and not limited financially. The financial constraint dummy (DCF) has a value of 1 for firms that are facing financial constraints and has a value of 0 for firms that are less likely to face financial distresses. There are some measures of financial constraints used in previous studies to distinguish firms that are facing financial constraints and those that are less likely to face financial constraints. However, which is the best one is still a controversial issue. Therefore, this study classifies firms according to the existence of financial constraints as below:

Data were collected from Vietnam Stock Exchange in the period from 2009 to 2019, from annual reports, audited financial statements of listed firms after eliminating firms in the fields of banking, securities, and insurance. After determining the criteria, the data used to perform the analysis and regression contains 5,431 observations.

Hypotheses Design

The degree of ownership concentration and earnings management

The degree of ownership concentration, also known as blockholders, is the percentage of shares (usually more than 5%) owned by a certain percentage of shareholders. It is argued that major shareholders have a strong incentive to actively monitor and manage the company to protect their investments (Shleifer & Vishny, 1986). Major shareholders are expected to monitor managers’ actions, reducing the opportunity for managers to distort earnings management (Dechow et al., 1996). However, firms with concentrated ownership may experience conflicts of interest between majority and minority shareholders. According to Shleifer and Vishny (1997), large shareholders can exercise their controls to create personal benefits, sometimes appropriating the interests of minority shareholders. Therefore, major shareholders may interfere with the management, and may encourage managers to have earnings management for maximizing their own interests (Jaggi & Leung, 2007). Studies of the relationship between ownership concentration and earnings management have also produced heterogeneous results. Ali et al. (2008) and Roodposhti and Chashmi (2011) find a negative correlation between ownership concentration and earnings management. In contrast, Kim and Yoon (2008) and Klai and Omri (2011) conclude a positive correlation between earnings management and the degree of ownership concentration. Thus, the results of the relationship between ownership concentration and profit management are different. We could not predict the trend of the concentration of ownership rights on earnings management, so the first hypothesis is designed as:

H1: The degree of ownership concentration has an impact on earnings management behavior

State ownership and earnings management

Studies on the impact of state ownership on earnings management are still limited and inconsistent. Specifically, Ding et al. (2007) and Wang and Yung (2011) find that at a low level of state ownership there is a positive effect with earnings management and a negative effect on earnings management when there is a high level of state ownership. In contrast, Firth et al. (2007) conclude that state-owned firms are more likely to engage in earnings management than non-state firms. Meanwhile, Liu and Lu (2007) reveal that the relationship is insignificant between earnings management and state ownership. Most people believe that state owned enterprises (SOEs) are more likely to manipulate income (Wang & Yung, 2011). This is because corporate governance is ineffective, market discipline is inadequate, there are many conflicts of interests, and for the benefits of the SOE controls, management is more likely to perform its discretion in reporting accounting information (Wang & Yung, 2011). Vietnam is in the process of reforming SOEs with a focus on equitizing SOEs. Many joint-stock firms were reformed, with the state still holding a large percentage of ownership. However, equitized SOEs are, for a long time, in the subsidy and planning mechanism and still have not escaped from centralization of financial bureaucracy, organizational structure, and management mechanisms, leading to poor corporate governance in SOEs (Shleifer, 1998) and opportunistic behavior of managers for personal gains rather than for the benefit of shareholders through earnings management. Based on the above arguments and the agency theory, we design a hypothesis as:

H2: The state’s ownership ratio has a negative effect on earnings management

Ownership of foreign investors and earnings management

In the world, foreign investment capital plays an increasingly important role in the development of each country. This source of capital includes direct investment (FDI) and indirect investment (FPI). While FDI capital has a direct role to promote production, FPI has a stimulating effect on the development of the financial market in the direction of improving operational efficiency, expanding scale, and increasing transparency, facilitating domestic firms to easily access new capital; improve the role of state management and corporate governance quality. Therefore, the opening of the economy to foreign trade and investment in many countries in recent years has brought about significant changes in corporate governance. Liberalizing cross-border capital flows in developing economies makes sense on two levels. First, foreign financial institutions, when compared to public financial institutions, might be more motivated to oversee corporate management to ensure a higher return on their investments. Second, foreign organizations might own more efficient instruments for supervisory managers than domestic private financial institutions in developing economies. The ownership ratio of foreign investors is to reduce the level of earnings management to improve the transparency of information disclosure (Firth et al., 2007), therefore a hypothesis is designed as below:

H3: The ownership ratio of foreign investors has a positive effect on earnings management.

In addition to the factors of ownership structure discussed above, earnings management is also affected by firm characteristics such as Klai and Omri (2011), Roodposhti and Chashmi (2011), Xie et al. (2003), and Ali et al. (2008). Controllable variables are then included in the regression model to effectively assess the impact of ownership structure variables on earnings management behavior including firm size, financial leverage, growth rate, profitability, and audit quality.

Results and Discussion

We conduct a regression analysis of the earnings management recognition model according to Modified Jones’s model (Dechow et al., 1995): three Pooled OLS, FEM, and REM models. The results are shown in Table 2.

Regression Results for the Model of Earnings Management.

Note. t statistics in brackets.

p < .1. **p < .05. ***p < .01.

From the above estimation results, we can see that the variables

The data will be presented in the form of descriptive statistics shown in Table 3, including the following items of variable name, variable meaning, observed sample number, min value, max, average, and standard deviation. Table 3 illustrates that the total number of observations is 5,431 in the period from 2009 to 2019. The highest level of earnings management of firms in the sample is 7,425 and the smallest is 0.005, the average value is 0.722 with a standard deviation of 1,048 greater than the average. This shows that the level of earnings management between firms is relatively large. The percentage of foreign ownership (FO) has an average rate of 9.1%, while the state ownership (SO) averages 24.1%, the proportion of board members being a major shareholder accounts for 12.2%. The firm size (SIZE) by asset value with an average post-logarithmic value of 27,001, the average ratio of liabilities to total assets (LV) is 49.6%, average revenue growth rate is 20.5%, the rate of ROA is 6.2%, and financial statements audited by Big 4 firms are 25%.

Descriptive Statistics.

Table 4 reveals the correlation coefficients between the variables, whose purpose is to examine the close correlation between independent and dependent variables to eliminate factors that may lead to multicollinearity before running regression models. The correlation coefficient between independent variables in the model does not have any pair greater than 0.8, so it is less likely to have multicollinear phenomena. So we employed VIF to verify.

Correlation Matrix.

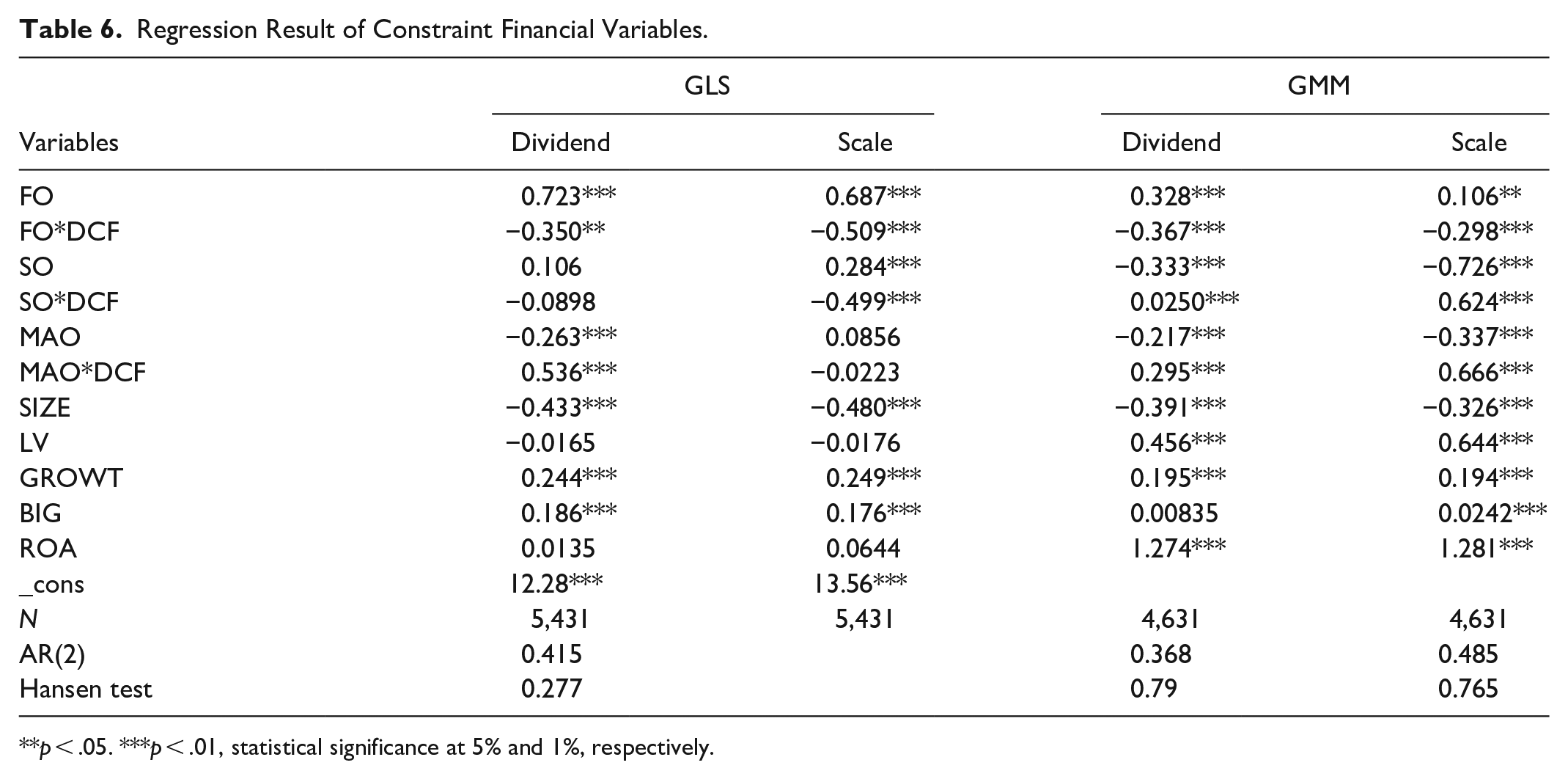

Regression results using FEM, REM, GLS, and GMM methods with the option of overcoming variance and autocorrelation are presented in Table 5. Ordinary Least Squares (OLS) or Fixed Effects Model (FEM), Random Effects Model (REM) have been employed in many studies (Anagnostopoulou & Tsekrekos, 2017; Fung & Goodwin, 2013; Lazzem & Jilani, 2018). These techniques do not repair heteroscedasticity and endogenous variables exist in the research model. That is why, this study is conducted to have some contributions by investigating the impact level of ownership structure, financial distress on earnings management by conducting General Method of Moments (GMM) for reducing limitations of OLS, FEM, REM, and GLS, and presented in Table 6.

Multivariate Regression Results.

Note. t statistics in brackets.

p < .1. **p < .05. ***p < .01.

Regression Result of Constraint Financial Variables.

p < .05. ***p < .01, statistical significance at 5% and 1%, respectively.

Based on the regression results according to GMM model, there are two out of three independent variables in ownership structure affect the level of earnings management statistically significant, that is the state ownership ratio and the ownership ratio of foreign investors. In addition, all five controlled variables included in the model influence the level of earnings management with statistical significance at the 1% significance level, which are the firm size, financial leverage, growth rate, ROA, and audit firm size. The remaining variable of the degree of ownership concentration has no impact on the level of earnings management.

The rate of foreign investors’ ownership variable (FO) with regression coefficient

For controlled variables, only the firm size (SIZE) has the negative effect that limits earnings management, while the remaining four variables of financial leverage (LEV), return on assets (ROA), growth rates, and Big 4 audits all have a positive impact on the level of earnings management and are all statistically significant at the 1% level.

To examine the effect of ownership structure on earnings management in the context of financial constraints, the study focused on the combinations of

From the results of empirical study above, we see that for the concentration of ownership variable, previous studies have found mixed findings, the results of Kim and Yoon (2008), Klai and Omri (2011) have a positive effect on the degree of earnings management while the results of Roodposhti and Chashmi (2011), Alves (2012) have the opposite effect. However, the findings of this study did not find evidence linking the degree of ownership concentration and earnings management, but in the situation of financial constraints, ownership concentration has a positive impact on earnings management.

The state ownership is inversely related to the level of earnings management. This result shows that firms with large state ownership have less earnings management, which is contrary to the initial hypothesis that state ownership has a positive effect with earnings management. This finding is in line with the findings of Wang and Yung (2011) studying the impact of state ownership on earnings management in listed firms in the context of China.

Ownership of foreign investors has the most positive impact on earnings management. This results is inconsistent with the findings of Kim and Yoon (2008) but is in agreement with the finding of Klai and Omri (2011). The explanation for this result might be that, at the same time, foreign investors, especially the controlling shareholders, have the right to attend senior management meetings with advanced management knowledge and skills while having more effective tools to oversee firm management. Thus, we accept the hypothesis

For firm size (SIZE), it is inversely related to earnings management, meaning the larger the firm size, the lower the level of earnings management. The findings of this study are similar to the results of Xie et al. (2003), Abdul Rahman and Haneem Mohamed Ali (2006), but contrast to several studies showing that there is a positive relationship between firm size and earnings management (Hung et al., 2018; Klai & Omri, 2011; Roodposhti & Chashmi, 2011). The reason is that large firms have a team of qualified accountants, and have better control over earnings management. Financial leverage (LEV) has a positive impact on management of earnings, meaning that the more financially leverage a firm has (debt ratio), the more likely it is to engage in earnings management. This result is consistent with the finding of Roodposhti and Chashmi (2011). Currently, listed firms in Vietnam in some sectors are maintaining a high debt ratio. Firms with a higher debt ratio means a large debt situation, a high risk of default, so that in order to secure a loan contract and create good confidence for creditors, managers often perform the act of controlling revenue in the direction of inflating profit. For the growth determinant (GROWT), it has a positive relationship with earnings management—the possible cause to achieve growth targets, investment expansion, so firms will naturally take measures to increase the level of earnings management form giving them a better picture of financial statements to attract investors.

For return on assets (ROA), which is positively correlated with profit management, this result is consistent with the initial prediction as well as previous results confirming that profitable firms will arrange a number of methods for manipulating income (Dechow et al., 1995). If the manager realizes that the risk of failing to meet the profit plan this year, the manager tends to level profit margins between accounting periods to ensure a sustainable profit trend in the long run. In recent years, the situation of huge differences between unaudited financial statements and audited figures has generated a lot for firms listed on Vietnam’s stock market. In particular, there are many firms that make investors or shareholders “fall” when profits fall sharply, from profit to loss or vice versa. The reason for the profit adjustment was explained by the auditors, the main deviation from the firm’s wrong application of accounting policies such as provisioning, depreciation of fixed assets; erroneous recording of revenues, expenses, which is the tip for earnings management.

Audit firm size (Big 4) has a positive relationship with earnings management, that is, firms audited by Big 4 audit firm have higher earnings management than firms that have been unaudited by Big 4. This result is contrary to the initial prediction and to the finding of Ali et al. (2008). Houqe et al. (2011) argue that there is a negative relationship between the presence of a Big 4 audit firm and earnings management. In Vietnam, the majority of large scale listed firms, foreign invested firms tend to choose Big 4 or large local audit firms. Large, established reputation, a long-standing brand, even though the cost of auditing firms is much higher than that of small-sized audit firms. As the presence of large audit firms like Big 4 will provide higher quality audit services than small ones because they have to maintain their reputation, which shows a signal for better oversight mechanism for disclosing financial information is also a question to be asked.

Conclusion and Suggestions

The purpose of this study is to analyze the impact of ownership structure on earnings management through data collected from annual reports of firms listed on Vietnam’s stock market. Financial statements, serving as a useful reference for related users such as investors, business managers, auditors, state management agencies, and others in the context of Vietnamese firms are currently concerned. Determinants related to the ownership structure included in the model are the concentration of ownership, state ownership, and foreign ownership. Data were collected from annual reports from 2009 to 2019 with 5,431 observations. Data organized as tabular data shows the advantages that cross-data and time series data do not. Regression analysis results found two variables of ownership structure including the state ownership rate, the ownership ratio of foreign investors affecting the management of earnings statistically significant at the 1% significance level (except for the percentage of managerial ownership with statistical significance at 5%). Meanwhile, the concentration ratio of ownership has an impact on profit management in the situation of financial distress. In addition, all controlled variables included in the model also influence the earnings management including firm size, financial leverage, growth rate, ROA, and audit firm size. Based on the findings, some policies are proposed for reducing earnings management for listed firms, as below:

The results show that increasing the ownership ratio of managers will reduce earnings management. According to agency theory, associating the interests of the manager with the common benefit of the company reduces the separation of ownership and control of the manager. Therefore, firms should enhance the association of the interests of managers with the common interests of the company for reducing managerial self-interest, thereby reducing earnings management. Specifically, there should be an incentive mechanism for managers to participate in the ownership of the company’s capital through preferential priorities on stock options or stock awards. At the same time, the company needs to build a rewarding criteria for the management team based on performance evaluation for a whole period, but this can be a double-edged sword because if the managers own one a large share of the company and become a major shareholder, they can gain control, dominate the important activities of the company and may harm the interests of minority shareholders, so firms need to consider what is appropriate for their firms. In order to increase the ownership of managers of listed firms, it is necessary to consider in terms of specific characteristics of the capital structure, the current shareholding ratio, and the working efficiency (of managers) of the listed firms to get the appropriate levels up.

Also according to the findings, state ownership has a negative effect on earnings management, that is increasing state ownership has the effect of reducing earnings management. Therefore, it is necessary to strengthen and accelerate the equitization of SOEs and divest from state capital invested in industries and fields that are not in the main business lines of the enterprises. This is the case for equitized firms that reduce state ownership, which can increase earnings management. Therefore, these firms need to take measures, especially corporate governance mechanisms to strengthen supervision to limit abuse of power or take advantage of loopholes to gain personal benefits of the management, restricting the act of earnings management.

Foreign investor ownership has a positive impact on earnings management, that is firms with a high foreign ownership ratio tend to promote earnings management. Therefore, listed firms should implement policies to attract foreign investors form improving their financial, governance, scientific, and technical skills. It is necessary to enhance the ability to supervise and manage the company, limiting earnings management.

We hope that the findings of this research help management, policy makers and investors have an overall view of earnings management in a firm, especially in case the impact of ownership and financial distress. Specifically, the implications of financial distress and earnings management relationship help investors, analysts and auditors as well have more prudent views in accessing financial statements. This pushes some pressure on management to reduce or have more prudence in conducting earnings management of the firms having financial distress. This study also reveals that in a big firm, earnings management is reduced in case of having the participation of investment from organizations, especially foreign ones. This means that apart from fulfilling accounting framework and supervision for reducing earnings management, more joining from organization investments, especially from foreign ones should be promulgated in policies. That is why it helps have peer review, improve financial performance, protect benefits of investors, and improve the transparency and reliability of financial statements.

However, this research investigates the impact of ownership structure in the constraint of new finance in terms of size and dividends. In the future, we will extend other aspects of finance constraints and in specific sectors as well as scrutinize the impact of the role of corporate governance and macro-economic policies on earnings management. So the future research will provide more interesting outcomes with a case study of Vietnam, an emerging country.

Footnotes

Appendix

Definition of All Variables.

| Coding | Variables | Definitions |

|---|---|---|

| EM | Earnings management | EM = DACCj: Discretionary accruals calculated as the residual from the performance adjusted modified Jones model estimated for each industry (4-digit SIC)-year requiring at least 10 observations per industry-year. Specifically, ACjt = α + β0(1/AVGATjt) + β1ΔCASHREVjt + β2PPEjt + β3ROAjt − 1 + β4ROAjt + εjt where ACjt is total accruals for firm j in year t, defined as net income from continuing operations minus operating cash flow scaled by average total assets. AVGATjt is average total assets for firm j based on assets at the beginning and end of year t. ΔCASHREVjt is the change in cash sales (i.e., change in revenue minus change in accounts receivable) for firm j at the end of year t scaled by average total assets. PPEjt is net property, plant, and equipment for firm j at the end of year t scaled by average total assets. ROAjt − 1(jt) is income before extraordinary items for firm j in year t − 1(t) scaled by total assets at the end of year t − 1(t). |

| FO | Foreign ownership ratio | Shares held, as a percentage of shares outstanding, by all foreign institutional investors of firm j at the year end. |

| SO | State ownership ratio | Shares held, as a percentage of shares outstanding, by all State institutional investors of firm j at the year end. |

| MAO | The degree of ownership concentration | Shares held, as a percentage of shares outstanding, by all shareholders of firm j at the end of year. The ratio of major shareholders in the board (≥5% total shares) |

| SIZE | Firm’s size | The natural logarithm of total assets (AT) at the end of the most recent fiscal year. |

| LV | Financial structure | Leverage, calculated as book value of debt scaled by the sum of book value of debt and total assets at the end. |

| GROWT | Growth rate | Sales growth in year t for firm j, calculated as |

| BIG4 | Audit firm’s size | An indicator variable equal to one if auditor is Big 4, and zero otherwise. |

| ROA | Return on assets | Return-on-assets ratio, calculated as net income (NIQ) during year divided by the average total assets of year. |

Authors’ Note

Dang Ngoc Hung is Associate Prof. Dr. at Hanoi University of Industry, Vietnam. He is an honorary member of CPA Vietnam. He teaches and researches in accounting and finance. There have been many articles published in reputable magazines.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research is funded by Vietnam National Foundation for Science and Technology Development (NAFOSTED) under Grant no. 502.02-2019.302.