Abstract

This study examines the relationship between dividend policy, cash holdings, and earnings management (EM) behavior among listed firms in Vietnam over the period 2016 to 2024. Grounded in agency theory and the free cash flow theory, the research empirically investigates the effect of dividend policy and cash holdings on the level of EM, utilizing four widely recognized EM measurement models. The dataset consists of 10,057 firm-year observations analyzed using fixed effects regression models, controlling for firm and year fixed effects. The findings indicate a statistically significant negative association between dividend policy and EM, suggesting that firms with higher dividend payouts tend to engage less in earnings management. Conversely, cash holdings exhibit a positive and significant relationship with EM, implying that firms with higher levels of cash reserves are more likely to manipulate earnings. Among control variables, state ownership and profitability are found to be negatively related to EM. These findings provide important empirical evidence on the role of financial policy instruments in mitigating managerial opportunism via earnings management. The study offers implications for investors, corporate managers, and policymakers in designing effective financial oversight mechanisms in emerging markets such as Vietnam.

Introduction

In the context of globalization and international economic integration, transparency and efficiency in financial activities are increasingly vital for the sustainable development of enterprises, especially in emerging markets such as Vietnam. One of the key issues in corporate financial management is earnings management (EM), where managers exercise discretion in financial reporting to achieve certain objectives such as maximizing market value, meeting investor expectations, or achieving internal performance targets.

EM can negatively affect the accuracy and reliability of financial information, thereby influencing investor decision-making and the overall efficiency of capital markets. In light of this, numerous studies have examined the determinants of EM behavior, among which dividend policy and cash holdings have received significant attention. These two factors are not only associated with the firm’s financial structure but also reflect corporate governance practices, internal control quality, and the level of investor pressure for financial transparency.

Dividend policy is viewed as a managerial control mechanism that restricts discretionary cash usage by distributing earnings to shareholders, thus limiting opportunities for EM (Jensen, 1986). From the perspective of agency theory, dividend payouts help mitigate conflicts between shareholders and managers by reducing free cash flow resources that managers might otherwise misuse for personal gain (Easterbrook, 1984). Empirical evidence suggests that higher dividend payouts can act as an indirect monitoring mechanism of managerial behavior (La Porta et al., 2000). However, the impact of dividend policy on EM remains inconclusive. Studies conducted in Thailand, Pakistan, and China show limited effects (Chansarn & Chansarn, 2016; Shah et al., 2010), whereas those in Finland, the U.S., U.K., and France report significant positive associations (Ben Amar et al., 2018; Daniel et al., 2008; Karjalainen et al., 2023; Kinnunen et al., 2000). Other studies across different countries reveal mixed results (He et al., 2017).

Dividend payouts can restrict managerial rent extraction by reducing available cash, thus lowering the likelihood of its misuse (Pinkowitz et al., 2006). In addition, cash holdings reflect a firm’s financial prudence and can exert bidirectional influences on EM. On one hand, ample cash provides liquidity to cope with financial risks and seize investment opportunities (Opler et al., 1999). On the other hand, excessive cash may enable inefficient investments and financial manipulation to mask poor performance (Harford, 1999). Therefore, high levels of cash holdings pose potential EM risks, especially under weak governance or ineffective internal controls. These complexities make EM behavior a pertinent issue requiring further exploration within the Vietnamese context.

Although both international and local studies have examined the relationships between dividend policy, cash holdings, and EM, much remains underexplored. (Dechow et al., 1995) argue that low dividend payouts may signal higher EM risk. International studies have indicated that higher dividend policies may mitigate earnings management (EM), particularly in countries with weak investor protection and low transparency, thereby enhancing credibility and facilitating access to external capital (He et al., 2017). In Vietnam, a prior study explored the relationship between accrual-based earnings management (AEM), real activities management (RAM), and cash holdings in the energy sector, revealing that RAM exerts a positive effect while AEM exerts a negative effect on cash holdings (Khuong & Liem, 2020).

In Vietnam, while the capital market is gradually expanding in scale and transparency, it still faces significant shortcomings in regulatory oversight, particularly concerning corporate governance and independent auditing. Dividend policies among listed firms are often driven by short-term goals and cross-ownership structures, while cash holdings are influenced by legal frameworks and concentrated ownership patterns. Existing domestic research primarily focuses on the impact of ownership and financial performance on EM (Nguyen & Bui, 2019; Tran & Dang, 2021). Few studies have simultaneously examined the role of both dividend policy and cash holdings on EM within Vietnam’s institutional environment, where the capital market is developing and shaped by multifaceted institutional factors. The Vietnamese context exhibits distinctive characteristics compared to other countries where EM studies have been conducted. Vietnam is recognized as an emerging economy with a developing capital market, characterized by shortcomings in monitoring mechanisms, particularly in corporate governance and independent auditing. The ownership structure in Vietnam also demonstrates unique features, with the average state ownership share close to 30%, serving as a monitoring mechanism that mitigates accounting manipulation, similar to the case of China. Conversely, foreign ownership remains relatively low (averaging 5.3%), reflecting the limited monitoring role of foreign investors. Moreover, dividend policy is often influenced by short-term objectives and cross-ownership relationships, while cash holdings are shaped by the legal environment and the prevalence of concentrated ownership structures.

Through the literature review, the identified research gap lies in the absence of studies that simultaneously evaluate the roles of dividend policy and cash holdings in shaping EM behavior in Vietnam, particularly within the context of emerging markets. Previous works have primarily focused on ownership structures or financial performance. This study addresses that gap by systematically analyzing the combined effects of both factors within a single model, employing four EM measurement approaches to enhance reliability. The analysis is based on updated data from 2016 to 2024 for Vietnamese listed firms and further considers the impacts under different levels of operating cash flows.

Hence, this study seeks to fill this research gap by systematically analyzing the effects of dividend policy and cash holdings on EM in Vietnamese firms. The main contributions of this study include: (1) First, it jointly examines two key financial variables dividend policy and cash holdings in a single analytical model to explore their interactive and combined effects on EM; (2) Second, it employs multiple EM measurement models (Dechow et al., 1995; Jones, 1991; Kasznik, 1999; Kothari et al., 2005), to enhance reliability and allow for comparative analysis; (3) Third, the data sample consists of listed firms in Vietnam during the recent period (2016–2024), offering updated insights into the current business environment; (4) Fourth, the study accounts for variations in operating cash flows to capture contextual differences in financial behavior. This approach is expected to provide robust empirical evidence for improving corporate financial supervision and informing relevant stakeholders. including policymakers, investors, and managers; (5) Finally, by incorporating signaling theory, the study clarifies the indirect mechanisms linking financial decisions to EM.

Theoretical Foundations and Conceptual Framework

Agency Theory

Agency theory, developed by (Jensen & Meckling, 1976), posits that the relationship between principals and agents may lead to conflicts of interest, particularly when their goals diverge. In this context, managers may act to maximize their own utility rather than that of shareholders, resulting in behaviors such as earnings management (EM). EM refers to the strategic manipulation of accounting information to meet specific objectives, such as achieving financial targets or maintaining a stable dividend stream (Healy & Wahlen, 1999).

Within the framework of agency theory, dividend policy and cash holdings can function as mechanisms to monitor managerial behavior. A reasonable dividend policy helps reduce excess cash, thereby limiting the managerial discretion to divert resources for private benefits or inefficient investments (La Porta et al., 2000). Similarly, low levels of cash holdings constrain managerial discretion in cash flow allocation and reduce the potential for EM (Jensen, 1986).

Signaling Theory

Signaling theory, as developed by (Spence, 1973), explains how firms communicate private information to the market through observable actions, such as dividend policies. A stable or increasing dividend payout is often interpreted by investors as a positive signal regarding a firm’s financial prospects (Bhattacharya et al., 2012). However, if actual earnings are insufficient to sustain the promised dividends, managers may resort to earnings adjustments to maintain these payouts (Kasanen et al., 1996).

From the signaling perspective, dividends are not only a means of profit distribution but also a strategic tool for conveying information to investors. When firms manipulate earnings to maintain their dividend levels, EM behavior is likely to occur (Dechow et al., 1995). Thus, this study hypothesizes that dividend policy may influence EM, either positively or negatively, depending on the sustainability of earnings.

Pecking Order Theory

According to the Pecking Order Theory proposed by (Myers & Majluf, 1984), firms prefer internal financing (e.g., retained earnings or existing cash) over external funding (e.g., debt or equity issuance). Consequently, a high cash holding ratio may reflect corporate prudence in preparing for investment opportunities or risk management. However, excessive cash may also enable managerial misuse of funds or financial fraud (Opler et al., 1999).

The relationship between cash holdings and EM may be bidirectional: firms may accumulate cash to “hide profits” in anticipation of difficult periods or use it to manipulate performance metrics when actual earnings fall short. Therefore, analyzing cash holdings in relation to EM is essential to understanding the motives behind financial management practices.

Free Cash Flow Theory

Free Cash Flow Theory, proposed by (Jensen, 1986), extends agency theory by highlighting that when firms possess large cash reserves with limited shareholder oversight, managers are more likely to engage in inefficient investments or manipulate earnings for personal benefit—thus increasing the risk of EM.

While high cash holdings improve liquidity, they also pose moral hazard risks. (Harford, 1999) found that firms with substantial cash reserves are more likely to engage in value-destroying acquisitions and exhibit poor governance. Likewise, (Jiraporn et al., 2011), demonstrated that high cash levels, in conjunction with weak internal controls, provide an ideal environment for managerial earnings manipulation. Consequently, free cash flow theory predicts that elevated cash holdings may be positively associated with EM, especially in firms with poor governance structures.

Literature Review and Hypothesis Development

Recent studies have deepened the understanding of the relationship between dividend policy, cash holdings, and EM, particularly within the context of emerging markets. (Mohammadi et al., 2018), in the case of Iran, demonstrated that managerial entrenchment can mitigate EM, including both accrual-based earnings management (AEM) and real earnings management (REM), thereby highlighting the role of internal governance in constraining financial reporting manipulation. (Haq et al., 2024), examining banks outside the United States, found that dividend payouts may limit income-increasing EM activities, especially when effective investor protection mechanisms and government regulations are in place. Furthermore, (Vahedi et al., 2025) revealed that during economic downturns caused by external shocks (e.g., sanctions), firms may shift from AEM to REM, with this effect being more pronounced when corporate governance is weak and EM incentives are strong. Managerial ability has also been shown by (Hou et al., 2025) to positively influence dividend payouts in China, though this effect is challenged by financial constraints and state ownership. Collectively, these findings underscore the complexity of EM behavior and related financial policies, highlighting the necessity of considering institutional factors and market-specific characteristics when analyzing this relationship (Ahmadi et al., 2025; Salehi, Mahmoudabadi, & Adibian, 2018; Salehi, Hoshmand, & Rezaei Ranjbar, 2020).

Expanding on the influencing factors, (Houqe et al., 2023) demonstrated that firms’ business strategies exert a significant impact on cash holdings and dividend policies. Specifically, “prospector” firms tend to hold more cash and pay lower dividends compared to “defender” firms, with this relationship moderated by financial constraints and free cash flows. Regarding earnings management, (Ghorbani & Salehi, 2021) provided evidence from Iran showing that firms engaging in higher levels of earnings management through income smoothing and discretionary accruals tend to exhibit higher financial leverage. In addition, (Haq et al., 2024) advanced empirical models to examine opportunistic earnings management, including meeting or beating prior-year earnings and abnormal loan loss provisions, while emphasizing the moderating role of investor protection and government regulation. These findings further illuminate how strategic orientations, financial structures, and regulatory frameworks shape corporate financial decision-making (Chaklader et al., 2024; Elberry, 2025).

Dividend Policy and Earnings Management

Dividend policy is a critical financial decision that may influence managerial behavior in earnings management (EM). Financial theories suggest that dividends serve not only as a signaling mechanism to investors but also as a monitoring tool to mitigate agency conflicts between shareholders and managers (Easterbrook, 1984; Jensen & Meckling, 1976). Numerous empirical studies have documented the relationship between dividend policy and EM behavior. In practice, firms may engage in income-increasing practices to meet dividend payout expectations, particularly when institutional or controlling shareholders exert pressure (Kasanen et al., 1996). Companies may also have a stronger incentive to engage in EM to convey favorable signals to the market by reporting stable earnings growth during dividend distributions, especially when issuing new shares (Kinnunen et al., 2000). Furthermore, firms are more likely to use discretionary accruals to sustain dividend payouts when pre-managed earnings fall short of dividend thresholds (Daniel et al., 2008). Several studies support the notion that dividend-paying firms exhibit higher levels of EM, such as those by (Ben Amar et al., 2018; Espahbodi et al., 2022; Nguyen & Bui, 2019; Salah & Jarboui, 2022).

Conversely, studies by (He et al., 2017; Hussain & Akbar, 2022; Tran & Dang, 2021) suggest that dividend-paying firms are less likely to engage in EM than their non-dividend-paying counterparts. This phenomenon is more evident in countries with weak investor protection and low transparency. These authors argue that firms may use dividends as a governance mechanism to reduce earnings manipulation and improve corporate credibility. However, some studies found no significant relationship between dividend policy and EM (Chansarn & Chansarn, 2016; Shah et al., 2010). Based on the theoretical foundation and empirical evidence, the following hypothesis is proposed:

Cash Holdings and Earnings Management

Cash holdings reflect a firm’s financial flexibility. Agency theory suggests that excess cash may lead to managerial opportunism in the absence of effective oversight, thus increasing EM behavior (Jensen, 1986). According to (Opler et al., 1999), firms with substantial cash reserves can more easily finance investment activities, but this also raises concerns about inefficient use of capital. The effect of cash holdings on EM is complex, shaped by factors such as firm governance, firm-specific characteristics, and market conditions. Cash reserves can either facilitate or constrain EM depending on contextual variables.

High cash holdings may enable EM, especially in firms audited by non-Big Four auditors or in state-owned enterprises where oversight is weaker (Li et al., 2022). In such settings, cash reserves may be used strategically to manage earnings and signal financial strength (Mukhlasin, 2024). Ozkan and Alfarhan (2023) investigated the link between EM and cash holdings in G7 countries and found that firms with higher EM likelihood also held more cash—particularly in Canada, France, Italy, the UK, and the US—suggesting that cash reserves can facilitate EM in diverse economic environments. Alves (2021) examined the relationship between free cash flow and EM, noting that firms with higher free cash flow were more likely to engage in EM, and that leverage moderated this relationship. Greiner (2016) demonstrated that firms engaging in real EM tend to derive lower marginal value from cash holdings, indicating a strategic use of cash to influence investor perceptions. In contrast, some scholars argue that excess cash serves as a precautionary buffer against financial uncertainty, enhancing firm value rather than facilitating EM (Thenmozhi et al., 2019). Nonetheless, excess cash may also erode shareholder oversight and incentivize EM. Based on theory and prior research, the following hypothesis is proposed:

Dividend Policy, Cash Holdings, and EM Under Different Operating Cash Flow Conditions

According to agency theory (Jensen & Meckling, 1976), managers may act in self-interest, particularly when firms hold large cash reserves and lack effective control mechanisms. When firms experience positive operating cash flows, managers may use excess funds for suboptimal investments or manipulate earnings to meet personal objectives (Richardson et al., 2006). Conversely, in firms with negative operating cash flows, EM may arise from pressure to maintain a healthy financial image to stakeholders (DeFond & Jiambalvo, 1994). Dividend policy can act as an alternative governance mechanism by forcing managers to distribute earnings rather than retaining funds for potentially opportunistic purposes (La Porta et al., 2000). When cash flows are positive, dividend payouts can curb managerial discretion, reducing the incentive for EM (Ben Amar et al., 2018). On the other hand, maintaining dividends under negative cash flow conditions may encourage EM to preserve investor confidence (Daniel et al., 2008).

Similarly, high cash holdings offer financial flexibility but may also invite misuse in poorly monitored environments (Opler et al., 1999). In firms with negative cash flows, internal financing capacity is constrained, and managers may exploit cash reserves to continue operations or obscure poor performance through EM. Conversely, in firms with positive cash flows, abundant cash may lead to EM as part of profit “optimization” strategies. Based on these theoretical insights and empirical findings, the following hypotheses are proposed:

Research Model and Methodology

Research Model

The research model is developed to examine the impact of dividend policy and cash holding ratio on earnings management (EM), taking into account various control variables. The model is structured as follows:

Where:

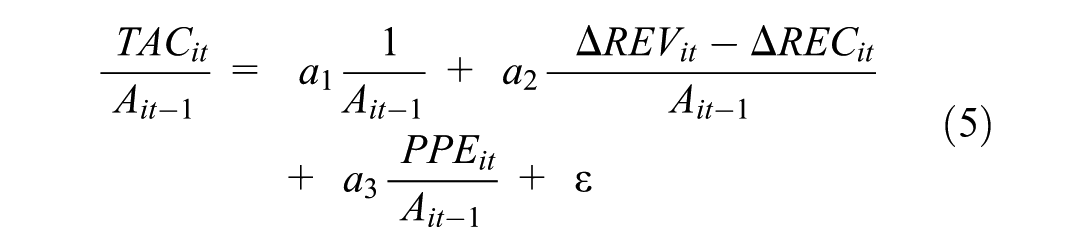

EM it represents the level of earnings management for firm i in year t. This study measures EM using four models: (Dechow et al., 1995; Jones, 1991; Kasznik, 1999; Kothari et al., 2005).

The discretionary accruals (TAC it ) are computed as follows:

where ΔCA it is the change in current assets, ΔCash it is the change in cash and equivalents, ΔCL it is the change in current liabilities, ΔDCL it is the change in short-term debt, and DEP it is depreciation expense. Additional variables include ΔREV it (change in revenues), ΔREC it (change in net receivables), PPE it (gross property, plant, and equipment), ΔCFO it (change in operating cash flows), Ait−1 (total assets at t − 1), and ROAit−1 (return on assets at t−1). Models (4), (5), (6), and (7) are estimated cross-sectionally by industry-year groups with a minimum of 10 firms per group. The absolute value of the residuals from these equations is used to proxy for EM. Advantages and disadvantages of the different earnings management measurement models used and their suitability for the context in Vietnam.

Jones (1991) Model and Modified Jones Model (Dechow et al., 1995):

Advantages: These are fundamental and widely used models that provide the foundation for distinguishing discretionary from non-discretionary accruals. The Modified Jones model improves upon the original by adjusting for receivables, thereby reducing bias when firms manipulate credit revenues.

Limitations: They may be less effective for high-growth firms or during periods of economic fluctuation, when “normal” accruals may vary significantly. The Modified Jones model may still be limited if managers engage in real activities manipulation rather than solely accrual-based manipulation.

Relevance to the Vietnamese context: In an emerging market characterized by rapid growth and limited transparency, adjusting for receivables is particularly important. However, if EM is conducted through real activities, these accrual-based models may fail to fully detect it.

Kothari Model (Kothari et al., 2005):

Advantages: By incorporating return on assets (ROA), the model controls for the effect of firm performance on accruals. This is crucial because firms with naturally good or poor performance will inherently exhibit different accrual levels unrelated to EM.

Limitations: If ROA itself is subject to EM, the model may face endogeneity concerns.

Relevance to the Vietnamese context: Given that many firms face limited profitability and significant losses, controlling for firm performance is essential to avoid bias in EM estimation 3.

Kasznik (1999) Model:

Advantages: By incorporating changes in operating cash flows (CFO), the model captures EM behavior when managers attempt to smooth earnings to align with cash flows or to conceal cash flow volatility.

Limitations: It may be ineffective if operating cash flows themselves are manipulated through real activities.

Relevance to the Vietnamese context: The free cash flow theory is highly relevant here. Since cash holdings are influenced by the legal environment and concentrated ownership structures, managers may be incentivized to engage in cash flow-related EM.

In summary, employing all four models simultaneously enhances the reliability of the findings, as they complement one another and mitigate the limitations of individual models. The strong correlations observed among the EM measures (EM1–EM4) provide supporting evidence for the consistency of results in the Vietnamese context. This suggests that while each model has its strengths and weaknesses, their combined application offers a more comprehensive and credible perspective on EM behavior.

DPR it denotes the cash dividend payout ratio of firm i in year t, calculated as the cash dividend (Dit) divided by the year-end stock price (Pit).

RCASH it is the cash holding ratio of firm i in year t.

Control it includes firm size (SIZE: log of total assets), financial leverage (LEV: total debt to total assets), and profitability (ROA: net income to total assets).

Statistical and regression analysis: The study utilizes Stata software to conduct OLS regressions with robust standard errors or clustered standard errors by firm ID VCE (cluster firmid) to address heteroskedasticity and serial correlation within panel data.

Data: The dataset is sourced from https://fiinpro.com/fiinpro-x and https://vietstock.vn. The sample includes non-financial firms in Vietnam, comprising listed companies on HOSE, HNX, and unlisted firms on UPCOM. Firms with missing data are excluded. The study period spans from 2016 to 2024. Outliers at the 1st and 99th percentiles are winsorized to improve estimation robustness.

Table 1 presents the sample distribution by industry and year from 2016 to 2024, comprising 10,057 firm-year observations across 10 industries. The dependent variable is EM, measured using the models of (Dechow et al., 1995; Jones, 1991; Kasznik, 1999; Kothari et al., 2005). The two main explanatory variables are the dividend payout ratio (DPR) and cash holding ratio (RCASH), which reflect profit distribution policy and internal cash flow control, respectively. These variables are assessed in light of agency theory and the free cash flow theory (Jensen, 1986).

Research Data.

Control variables include foreign ownership (FO) and state ownership (SO), which proxy for ownership structure and monitoring intensity by particular shareholders. Additionally, firm-level financial characteristics such as profitability (ROA), leverage (LEV), loss status (LOSS), and firm size (SIZE) are included to reduce estimation bias in the relationship between DPR, RCASH, and EM.

The comprehensive dataset of 10,057 observations over 9 years ensures temporal and sectoral representativeness. The industrial sector accounts for the highest proportion (43%), whereas sectors like telecommunications and oil and gas are underrepresented.

Results Analysis, Discussion, and Recommendations

Results Analysis

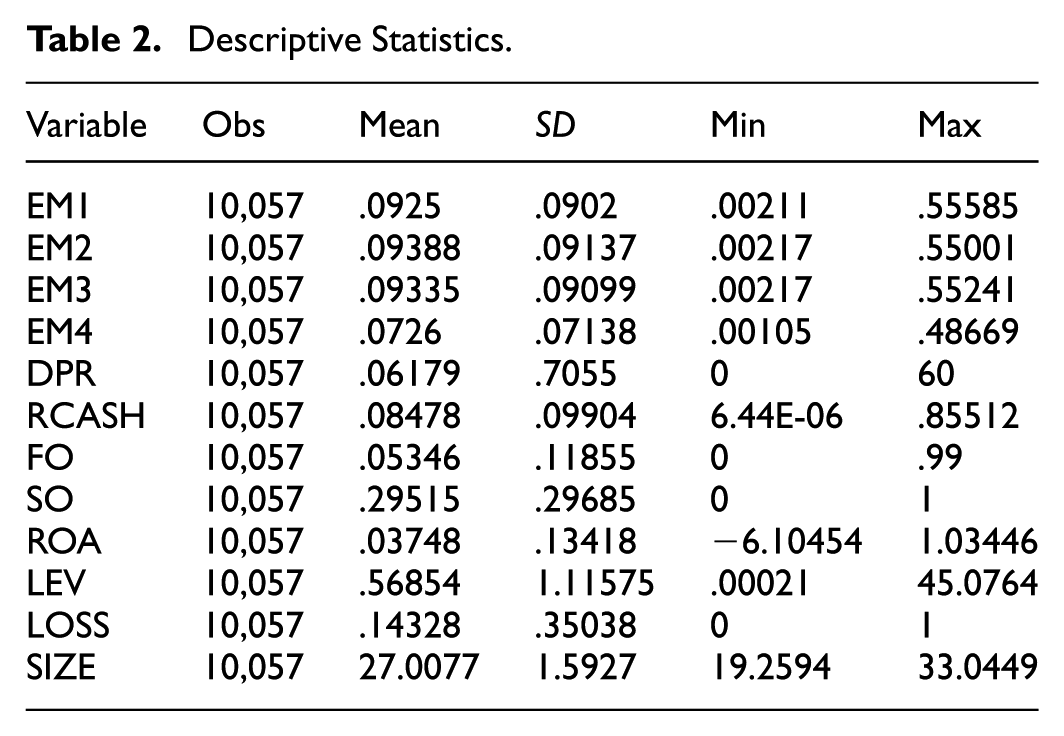

Table 2 presents descriptive statistics outlining the general characteristics of variables used in the study on the impact of dividend policy and cash holdings on earnings management (EM) among firms in Vietnam. With a sample size of 10,057 observations, the earnings management variables are measured using four different models (EM1–EM4), with mean values ranging from .0726 to .09388. These average values indicate a moderate presence of earnings management behavior across the sample, consistent with the findings of (Dechow et al., 1995; Kothari et al., 2005). The dividend payout ratio (DPR) has a relatively low mean value (.06179), but a high standard deviation (.7055) and a maximum value of up to 60, reflecting substantial variation among firms in dividend distribution practices. This variation may influence EM behavior, particularly in firms facing market pressures or possessing unique ownership structures (Fama & French, 2001). The average cash holding ratio (RCASH) is 8.47%, suggesting a reasonably maintained level of cash reserves. This aligns with the increasing emphasis among Vietnamese firms on enhancing liquidity and financial flexibility in recent years. Overall, these descriptive statistics provide an initial insight into the heterogeneity of financial practices and the potential determinants of earnings management in the Vietnamese corporate context.

Descriptive Statistics.

Control variables such as the foreign ownership ratio (FO) average only 5.3%, reflecting the relatively low level of foreign ownership, while the average state ownership ratio (SO) is nearly 30%, indicating the still-significant influence of the state sector—an element that may affect corporate financial strategies and earnings management (EM). Financial health indicators such as return on assets (ROA) show a modest average of 3.75%, reflecting limited profitability across the sample. The average financial leverage (LEV) is high at 56.8%, suggesting that many firms are relying heavily on debt financing. Furthermore, 14.3% of the sampled firms are loss-making (LOSS), and the average firm size (SIZE), measured as the natural logarithm of total assets, stands at 27, indicating a relatively homogenous distribution of firm scale.

Table 3 presents the correlation matrix that explores the relationships between key variables in the investigation of how dividend payout policy (DPR) and cash holdings (RCASH) influence earnings management behavior among Vietnamese firms. The results indicate strong positive correlations among the EM measures (EM1–EM4), particularly between EM2 and EM3 (r = .9829*) and between EM1 and EM2 (r = .9447), suggesting a high degree of consistency among the earnings management measurement models. This finding aligns with previous research by (Dechow et al., 1995; Kothari et al., 2005). The correlations between DPR and the EM variables are negligible and statistically insignificant, implying that dividend policy may not be directly associated with earnings management within this sample. In contrast, RCASH exhibits a small but statistically significant positive correlation with EM indicators (e.g., EM1, r = .0433), consistent with the argument that excess cash reserves may facilitate EM behavior (Richardson et al., 2006). Additionally, some control variables such as ROA and SIZE show negative correlations with EM, suggesting that more profitable and larger firms tend to engage less in earnings manipulation. Meanwhile, LEV and LOSS demonstrate weak positive correlations with EM, implying that firms facing higher financial risk or poor performance may be more inclined to engage in EM to enhance reported financial outcomes.

Correlation Matrix.

Note.*statistically significant.

Table 4 presents regression results indicating that the dividend payout ratio (DPR) exhibits a negative and statistically significant effect in three out of four models (EM1, EM2, EM3) at the 5% or 1% level, while it is not statistically significant in EM4. This finding suggests that firms with higher dividend policies tend to engage less in earnings management (EM). The result aligns with Signaling Theory, which posits that firms use dividends to convey positive performance signals to the market (Bhattacharya et al., 2012). Furthermore, the study by (Liu & Espahbodi, 2014) in the UK context finds that a high dividend payout ratio signals better earnings quality and lower levels of EM. These findings imply that dividend policy serves as an effective disciplinary mechanism to reduce EM behavior, thereby enhancing financial transparency. The observed roles of state ownership and firm performance further reinforce the importance of sound corporate governance systems in constraining opportunistic behavior. Thus, research hypothesis H1 is supported, consistent with prior studies such as (He et al., 2017; Hussain & Akbar, 2022; Tran & Dang, 2021). These results contribute to the earnings management literature and offer practical implications for dividend policy design, ownership governance, and corporate oversight in emerging markets such as Vietnam.

Regression Results of Model 1.

p < .1. **p < .05. ***p < .01.

The foreign ownership variable (FO) is statistically insignificant across all models, despite having a negative coefficient, indicating the limited monitoring role of foreign investors in Vietnamese firms. In contrast, state ownership (SO) exhibits a negative and statistically significant coefficient in all four models, especially in EM4 (p < .01). This suggests that firms with higher state ownership are less likely to engage in EM, consistent with (Chen & Zhu, 2009), who shows that state ownership in Chinese firms acts as a governance mechanism reducing accounting manipulation.

Return on assets (ROA) shows a negative and statistically significant relationship with EM in models EM1, EM2, and EM4. This indicates that more profitable firms are less inclined to manage earnings, consistent with Agency Theory, which posits that high-performing firms have less incentive to “window-dress” their financial reports (Dang et al., 2017; Hung et al., 2018; Watts & Zimmerman, 1986). These findings are also in line with (Dechow et al., 1995; Hung et al., 2022), who suggest that underperforming firms are more prone to earnings manipulation.

Financial leverage (LEV) is not statistically significant in most models, except EM4 (p < .1), suggesting that while financial pressure may encourage EM behavior, the evidence remains weak in the Vietnamese context. The loss variable (LOSS) is only significant in EM4, implying that loss-making firms are more likely to engage in EM. Firm size (SIZE) is not statistically significant in any model, suggesting that size may not be a major determinant of EM behavior in this study.

Table 5 shows that cash holdings (RCASH) are positively and significantly associated with EM at the 1% level across all four models. Specifically, coefficients range from .0332 to .0648, with corresponding t-statistics supporting the robustness of the results. This suggests that firms with greater cash reserves tend to engage more in earnings management. This finding is consistent with Agency Theory (Jensen, 1986; Jensen & Meckling, 1976), and prior studies (Li et al., 2022; Mukhlasin, 2024; Ozkan & Alfarhan, 2023), which argue that excessive free cash flow may provide managers with the discretion to pursue personal interests, such as “beautifying” earnings to meet short-term goals or maintain performance-based incentives. Hence, Hypothesis H2 is supported. The study provides strong empirical evidence indicating that higher cash holdings are positively associated with EM in Vietnamese firms. This raises caution for investors, managers, and regulators regarding the need for more stringent internal monitoring mechanisms in firms with substantial idle cash. Moreover, the findings underscore the roles of state ownership and financial performance in curbing opportunistic managerial behavior. Overall, these insights contribute to Agency Theory and the broader corporate governance framework in emerging market contexts like Vietnam.

Regression Results of Model 2.

p < .1. **p < .05. ***p < .01.

Table 6 presents the regression results illustrating the relationship between dividend policy (DPR), cash holdings (RCASH), and earnings management (EM) behavior under conditions of negative and positive operating cash flows. This classification aims to clarify the role of firms’ internal financial conditions in influencing EM behavior, thereby providing richer empirical evidence for modern corporate finance theories, such as agency theory (Jensen & Meckling, 1976) and free cash flow theory (Jensen, 1986).

Regression Results of the Model Classified by Operating Cash Flow.

p < .1. **p < .05. ***p < .01.

Negative Operating Cash Flows

The results indicate that under negative cash flow conditions, the dividend payout ratio (DPR) is not statistically significant in the first three models (EM1–EM3), but it shows a positive and significant effect in model EM4 (β = .0663, p < .05). This suggests that when firms face cash flow difficulties, maintaining dividend payments may incentivize managers to engage in EM in order to uphold shareholder confidence. This finding is consistent with Liu and Espahbodi (2014), who argue that dividend payment pressure leads managers to manipulate earnings. Conversely, the cash holding ratio (RCASH) does not significantly affect earnings management in this group, contrary to the expectations of free cash flow theory. This may be explained by the lack of financial flexibility under constrained cash flow conditions, where cash reserves are insufficient to enable managerial opportunism. Additionally, state ownership (SO) has a negative and statistically significant effect across all models, reinforcing the monitoring role of the state in financially distressed firms. Financial leverage (LEV) has a positive and significant impact on the first three models, indicating that highly leveraged firms are more likely to engage in EM to avoid violating debt covenants. Therefore, hypotheses H3a and H4a are supported.

Positive Operating Cash Flows

In contrast to the previous group, under positive cash flow conditions, the dividend payout ratio (DPR) has a negative and statistically significant impact across all four models. This aligns with the assumption that firms with regular dividend payments have less incentive to engage in EM, as they aim to preserve their corporate image. The cash holding ratio (RCASH), on the other hand, exhibits a consistently positive and highly significant effect on all models. This indicates that when firms have positive cash flows and ample cash reserves, managers tend to exploit these resources to engage in earnings manipulation, consistent with agency theory (Jensen & Meckling, 1976). This finding starkly contrasts with the negative cash flow group. Similarly, state ownership (SO) continues to have a negative and significant effect, highlighting the stabilizing role of state ownership in curbing EM behavior regardless of cash flow conditions. Return on assets (ROA) has a negative and significant impact on some models, suggesting that highly efficient firms have lower incentives to manipulate earnings. Hence, hypotheses H3b and H4b are supported. In summary, the findings indicate that the effects of dividend policy and cash holdings on earnings management are significantly contingent upon the firm’s operating cash flow conditions. Under favorable financial conditions, cash holdings serve as a driver for EM, whereas under financial distress, dividend policy plays a more prominent role. These insights provide important implications for investors and regulators in assessing the quality of financial reporting and EM behavior in firms.

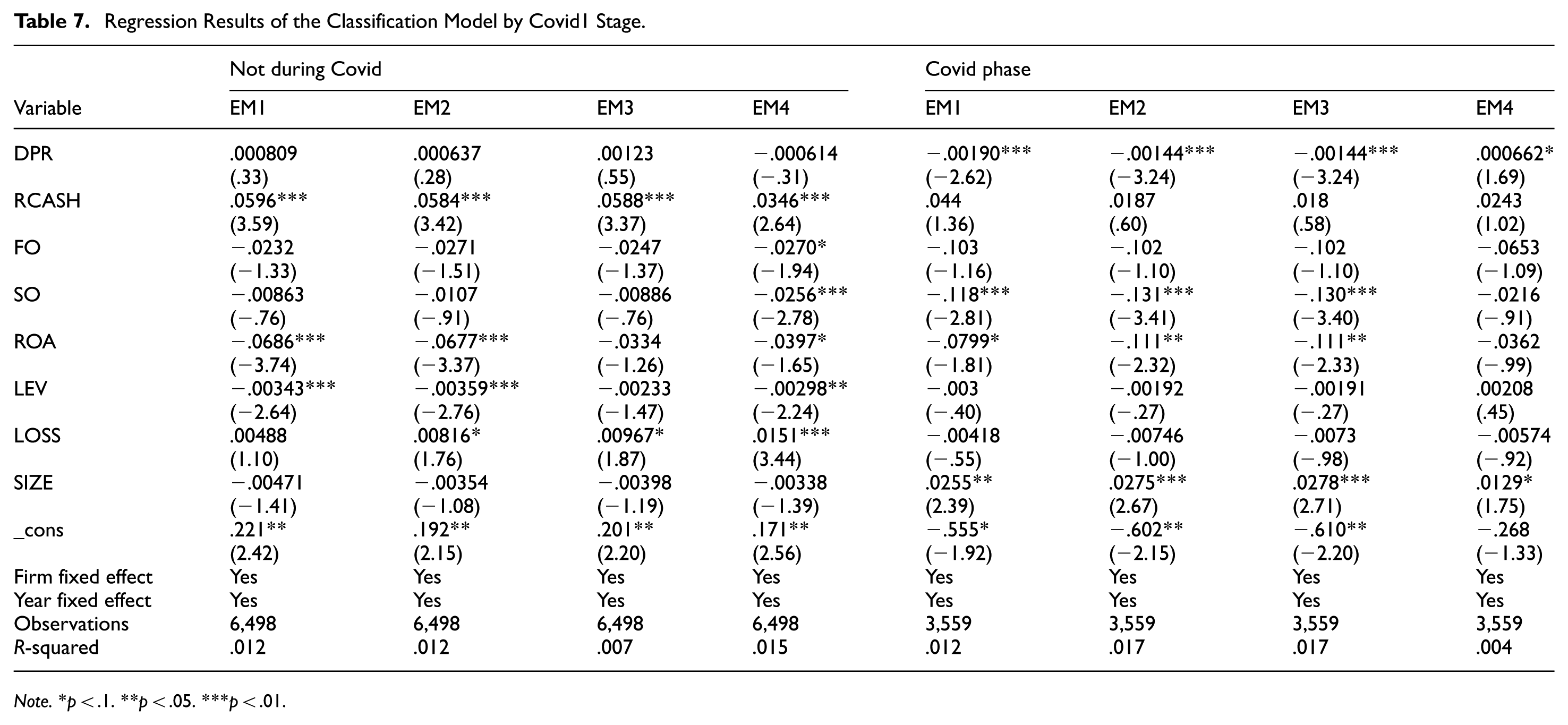

Based on the regression results, several academic inferences can be drawn regarding the impact of dividend policy (DPR) and cash holdings (RCASH) on earnings management (EM) among Vietnamese firms across two periods (before and during the Covid-19 pandemic).

In the pre-Covid-19 period, RCASH exhibits a positive and statistically significant effect on all EM measures (EM1–EM4). This implies that firms with higher levels of cash holdings tend to engage more intensively in earnings management. Such findings are consistent with the argument that abundant cash resources may provide managers with greater discretion to manipulate financial statements in pursuit of specific objectives. By contrast, DPR does not demonstrate a significant effect on EM during this period, suggesting that dividend policy does not serve as a constraining mechanism on earnings management when the economy operates under relatively stable conditions.

However, during the Covid-19 period, the roles of these two variables change markedly. DPR shows a negative and statistically significant impact on most EM measures (EM1–EM3), indicating that higher dividend payouts contribute to mitigating earnings management practices in times of crisis. Conversely, RCASH no longer maintains statistical significance, implying that cash holdings cease to be a decisive determinant of EM in an environment characterized by heightened uncertainty.

Overall, the findings highlight that dividend policy and cash holdings exert heterogeneous effects on EM depending on the economic context, underscoring the moderating role of crisis conditions in this relationship (Table 7).

Regression Results of the Classification Model by Covid1 Stage.

Note.*p < .1. **p < .05. ***p < .01.

Conclusion and Recommendations

This study sheds light on the relationship between dividend policy (DPR), cash holdings (RCASH), and earnings management (EM) behavior among Vietnamese firms, while also analyzing this relationship under varying conditions of operating cash flows. By employing four measures of earnings management and incorporating control variables such as state ownership (SO), foreign ownership (FO), profitability (ROA), financial leverage (LEV), firm size (SIZE), and loss status (LOSS), the study provides robust empirical evidence of the differentiated impacts of financial policies on EM behavior.

Theoretically, the research contributes to the expansion and validation of foundational theories such as agency theory (Jensen & Meckling, 1976), and free cash flow theory (Jensen, 1986), particularly in the context of emerging economies. The findings reveal that dividend payments under positive cash flow conditions may serve as a control mechanism against earnings management behavior, whereas the combination of positive cash flows and high cash reserves tends to increase EM activities. Additionally, state ownership is confirmed to exert a significant negative moderating effect on earnings management across all financial conditions, thereby reinforcing the hypothesis regarding the monitoring role of state shareholders.

Practically, the study offers important implications for investors, regulatory authorities, and corporate executives. Specifically, investors should exercise caution when evaluating financial statements of firms with strong cash flows and high levels of cash holdings, as the likelihood of earnings management may be elevated. At the same time, regulators should enhance oversight of financial transparency in firms with low or irregular dividend payouts, as these may indicate potential earnings manipulation. Corporate executives are also encouraged to adopt prudent dividend distribution and cash management policies to foster trust among shareholders and the broader market. Specific recommendations for each subject are as follows:

For investors: Particular caution is required when assessing the earnings quality of firms with high cash holdings, especially when operating cash flows are positive. Abundant cash reserves may provide managers with the means to engage in earnings manipulation. The cash flow context should be taken into account when evaluating dividend policies. Although high dividend payouts generally reduce EM, if a firm maintains dividend payments under negative operating cash flows, this may signal opportunistic EM aimed at sustaining shareholder confidence. State ownership can be considered a protective factor, as firms with higher state ownership tend to be less involved in EM.

For regulators and policymakers: Oversight mechanisms should be strengthened for firms with substantial cash holdings and positive operating cash flows, particularly through more rigorous independent auditing and stricter corporate governance to limit the misuse of free cash flow. Greater scrutiny should be directed toward the transparency of financial reporting in firms facing cash flow difficulties yet maintaining high dividend payouts, as such practices may create pressure and incentives for EM.

For corporate executives: Dividend policy and cash management should be developed prudently and transparently, ensuring that these decisions do not inadvertently create incentives for EM. In particular, careful consideration should be given to the relationship between dividend payouts and actual cash flows to avoid pressures that could lead to earnings manipulation. Internal control mechanisms over cash utilization should be reinforced, especially when firms possess large free cash flows, in order to mitigate the risk of managerial manipulation of financial results.

The limitations of the study include: (1) The dataset is restricted to Vietnamese firms, which may limit the generalizability of the findings to other countries; (2) The study does not consider the influence of audit quality or corporate governance environment on the relationships investigated; (3) The classification based on positive and negative cash flows may not fully capture the complex financial contexts of firms. (4) Classifying cash flows merely into “negative” or “positive” categories may be insufficient to capture the full range of complex financial scenarios and the nuanced EM incentives that managers may pursue. For instance, a firm with “highly positive cash flows” may exhibit different motivations for EM compared to a firm with only “moderately positive cash flows,” and the same applies to varying degrees of negative cash flows. A more granular classification would allow for a deeper understanding of how managers adjust earnings under specific financial pressures and opportunities associated with different cash flow levels. This represents a promising avenue for future research to further enrich the understanding of the relationship between cash flows and EM.

Future research directions include: (i) Expanding the scope to other ASEAN countries or emerging markets for comparative analysis; (ii) Incorporating additional mediating and moderating variables such as audit quality, institutional ownership, or ESG indices; (iii) Applying nonlinear analytical methods or machine learning techniques to test the robustness of the model.

Footnotes

Funding

The author received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The data supporting the findings of this study are currently unavailable due to ongoing processing and validation.