Abstract

Corporate cash holdings have received increased attention from researchers and practitioners as cash management is a crucial task for executives. Holding too much cash can result in low returns and mismanagement by managers. Conversely, holding low cash reserves can lead to missed investment opportunities. The present study examines the relationship between board governance, financial constraints, and corporate cash holdings. The robust fixed-effects method is used in this study to analyze 860 A-listed firms in China from 2005 to 2020. An index is designed to measure board effectiveness, while financial constraints are measured using Z-score, the Kaplan and Zingales index, and the SA index. The major findings document that the financially less constrained firms hold more cash when there is an effective board governance. Furthermore, financially less constrained firms have more robust board governance to minimize the agency concerns of managers and shareholders. This research provides an inference for stockholders’ activism connected to the cash holdings of the financially constrained and less constrained companies. The findings offer useful policy implications for stakeholders to reform contemporary cash holding policies. Specifically, understanding the role of an effective governance system for financially less constrained firms would help minimize the potential agency conflict.

Introduction

The financial independence of firms depends upon cash reserves, which enable firms to follow their strategic plan with limited or no external intervention (Boubaker et al., 2015). Further, compared to external funds, funds generated internally are much cheaper. Thus, firms with sufficient cash funds can invest in feasible investment opportunities at low financing costs. The literature of economics and finance on this subject acknowledges four motives for hoarding cash reserves. Cash is hoarded primarily for transaction purposes (Drobetz & Grüninger, 2007), followed by the precautionary motive (Drobetz & Grüninger, 2007; Ferreira & Vilela, 2004). It reveals that firms with additional opportunities for growth and investment opportunities hoard their cash reserves for protection against expensive unfavorable shocks in cash flow. According to Foley et al. (2007), the tax motive is the third purpose of hoarding cash. The study maintains that companies worldwide accumulate more cash in hand because of higher tax expenses linked with foreign income repatriation. Agency motive is the fourth motive for holding cash (Zhang & Zhou, 2022), and managers increase their cash reserves to maintain their position of control in the firm (Ferreira & Vilela, 2004; Harford et al., 2008; Jensen, 1986).

Generally, managers prefer internal cash compared to external cash (Lee & Park, 2016), which may result in huge stockpiles of liquid assets. In contrast, the stockholders may also be alarmed about managers’ discretion to use such cash reserves. Further, a selfish management may plan to use extra cash reserves for their personal gain (Jensen, 1986; Pizzini & Sterin, 2023). Additionally, stockholders have an option to mitigate agency conflicts by improving the board governance quality. According to Yang and Xue (2023) highly diverse boards improve the marginal value of cash holding by minimizing the agency problems. When better protected by a sound corporate governance system, stockholders may permit the management to hold excess cash reserves (Harford et al., 2008). The financial and operational transparency of companies may be improved with a well-performing board (Bebchuk, 2007), reducing the probability of managers using cash reserves for their private purposes.

Along with financial constraints, a board governance system performs an essential function in shaping a company’s cash reserves. Firms that are financially constrained have restricted entrance into external markets for fundraising. Their management relies on internal resources and is more liable to set aside adequate cash for precautionary purposes. The owners of financially constrained firms tend to be less worried about high cash reserves, hoarding them for prudent purposes (Almeida et al., 2004). Further, as per the study by Luo and Hu (2011), the firm’s managers who have limited access to markets providing external finance would not waste priceless internal cash reserves; so, financial constraints are considered a disciplinary function.

The existing studies on companies’ cash holding levels have been conducted with evidence from developed countries, such as the US, with meager attention given to the less developed or emerging countries (Akhtar et al., 2018). Second, past studies have not checked the outcomes of the interaction between the financial constraints and board governance systems on Chinese firms’ cash holdings. Several things differentiate the practices of cash holdings in emerging countries’ markets from developed countries’ markets. According to the findings of Al-Najjar (2013), institutional factors may have an impact on financial practices, for example, on dividend policy (Ed-Dafali et al., 2023), and cash holdings. Relative to developed markets, such as the US, socio-economic factors such as law and order conditions are weak, which is one of differences in their financial practices (North, 2005). As a result, the vagueness in transaction increases, encouraging a wide range of unproductive practices such as hoarding large reserves of cash (Al-Najjar, 2013). To fill the existing gap, this study aims to examine the impact of financial constraints on cash holdings and of effective board governance on financially less constrained firms’ cash holdings. Further, this study explores the impact of financial constraints on board governance.

The current study examines the determinants of cash holding by firms with board governance and financial constraints in China’s emerging markets, and contribute to the literature in the following ways; First, this research provides an inference for stockholders’ activism connected to the cash holdings of the companies. Second, this study will also help managers adjust their policy associated with cash holdings in the business’ best interests in different conditions. Third, this study will help managers set the cash at a level that would not create agency conflict. Fourth, present research can thus help shareholders understand the requirements of an effective governance system in financially less constrained firms.

The rest of the paper is organized as follows: Section “Theoretical Background” deals with the review of literature related to corporate cash holdings, financial constraints, and corporate governance, followed by Section “Research Methodology” that outlines the methodology, measurement of variables, and econometric models. Section “Research Results” presents the main results of the study and, finally, Section “Conclusions” concludes the study.

Theoretical Background

Board Governance, Financial Constraints, and Corporate Cash Holdings

The researchers (Jensen & Meckling, 1976) modeled the agency relationships and stated that even after maximum efforts to decrease managers’ selfish behavior, the agency problems in the financial reporting process exist between stockholders and managers. The researchers put forth that there is a difference in the interests of principles and agents. Management decisions will undoubtedly be away from the projects that can maximize shareholders’ wealth, causing agency conflicts. Owing to this, conflicts exist between cash holdings and the financial reporting environment. Bates (2005) proved that firms with extra cash are expected to utilize the excess cash on acquisitions that perform poorly afterwards.

The managers of poorly governed firms hold more assets in shape of cash to increase their discretion on shareholders’ expense (Chen et al., 2020). Agency theory reveals that when there is no proper monitoring of managers by governance bodies, they use the extra cash for their personal advantage (Harford et al., 2008). This selfish behavior involves misusing companies’ precious resources, that is, cash, and reducing its value. This behavior can potentially be controlled by adopting corporate governance provisions to form a system of monitoring the top management and decreasing agency cost (Feng & Huang, 2020). The board of directors are very important indicator for corporate governance because of their role in shaping the firm’s directions and strategies (Al-Najjar & Clark, 2017). The attributes of corporate governance can influence the cash holdings of the firms (Jebran et al., 2019).

In countries with perfect capital markets, it is irrelevant to hold liquid assets such as cash because it is easy for firms to raise finances for profitable projects or to make investments with insignificant transaction costs. Thus, the stockholders’ wealth remains unchanged with liquid asset investment within the firm (Guizani, 2018). The personal benefits of managers increase with an increase in the corporate investment’s total output. Holding high cash reserves is the cheapest approach to keeping up an adequate amount of capital to invest in different projects (Lee & Park, 2016). The objectives of stockholders chased only when the management invest cash in profitable projects and distribute any excess cash among stockholders after making all profitable investments (Amess et al., 2015). Stockholders have agency problems on the subject of the managers’ own benefits, especially when companies accumulate large cash reserves and do not permit the management to build up their cash reserves without a healthy governance system in place (Harford et al., 2008). As per the precautionary motive of building cash reserves, cash is held as a barrier to guard against unexpected emergencies or meet cash deficiencies (Hill et al., 2014). As per the findings by Han and Qiu (2007), there exists a positive association between cash flow volatility and cash holdings among companies that are financially constrained.

Cash holdings of companies are linked with the status of financial constraints. As per Faulkender and Wang (2006) arguments, for financially constrained companies, the marginal worth of holding cash is greatly relative to companies that are not financially constrained. Almeida et al. (2004) stated that the financially constrained companies save cash from recent cash flows and tend to be afraid about expected under investments in the upcoming period. As per the above arguments, it is understood that firms that are financially constrained set aside a larger portion of cash flow to defend themselves against unfavorable shocks of liquidity.

McLean and Nocera (2011) reported that US firms issue less loans in bad times, while Dittmar and Dittmar (2008) reported that there is an expansion in the activity of share issuance in US firms during periods of economic expansion and decreased depression. Campello et al. (2010) found through a survey that companies avoid different investment opportunities because of financial constraints.

Studies on cash holdings in China reveal some interesting results. For example, as per the findings of Lian et al. (2011) study, Chinese firms hoard more cash for precautionary purposes because of the adverse financial constraints resulting from the non-availability of perfect capital markets in the country.

Financial constraints may also influence managers’ discretion regarding cash holdings. Managers who have restricted access to financing from external markets would desire to set aside internal cash to invest in projects that have positive net present value (Han & Qiu, 2007; Harford et al., 2008). This is the corrective function of financial constraints in cash wastefulness (Luo & Hu, 2011). Managers of financially constrained companies are allowed by their stockholders to hoard large cash to avoid external financing costs. In contrast, there may be minimal benefits for shareholders of firms that are financially less constrained. Companies that are financially less constrained have comparatively easy access to stock markets. Therefore, managers are not that worried about the wastage of internal cash holdings. Thus, there are larger agency concerns for firms that are financially less constrained because of the managers’ discretion levels with respect to the cash reserves. Without any disciplinary cash management that requires the involvement of stockholders, these firms are financially less constrained in developing a strong internal check of managers.

The importance of corporate governance has increased in academic research and practice (Bebchuk et al., 2004). The meanings of good corporate governance limit appropriation of the firm’s resources by the managers or controlling stockholders, thereby resulting in the best allocation of the company’s funds and leading to increased performance. Dittmar and Mahrt-Smith (2007) stated that good board governance has an encouraging influence on the worth of the firm. The worth of the cash in firms with good corporate governance is double that of firms with weak governance (Pinkowitz et al., 2006). The findings of Dittmar and Mahrt-Smith (2007) study report that companies with weak corporate governance use cash more rapidly, resulting in low company performance. They also speculated that firms with poor governance are most likely to invest in projects offering low returns and be less attentive in controlling costs. Cremers and Nair (2005) and Durnev and Kim (2005) stated that there is a positive relationship between the firm’s value and governance. In developed financial markets, stockholders can compel managers to pay back more, declining the agency cost because of strong shareholder protection (La Porta et al., 2000). As per the findings of Dittmar and Mahrt-Smith (2007) study, in the US, the governance board extensively impacts the worth of cash hoardings.

The board’s effective governance would be more beneficial for companies that are financially less constrained than companies that are financially constrained. According to Lee and Park (2016), the board is the best channel through which the agency problems of financially less constrained firms can be solved. In contrast, financially constrained firms’ issues are already minimized to some degree by the penalizing function of financial constraints. So, taken as a whole, we anticipate that the cash hoarding of financially less constrained firms is extra responsive to board governance.

H1: Financially constrained firms hold more cash reserves.

H2: With effective board governance, financially less constrained firms’ level of cash holding increases further.

Financial Constraints and Board Governance

Beck et al. (2004) stated that there is much financially constraining effect of financial underdevelopment on small than large companies. Financial constraints are generally considered to be caused by the asymmetric information available among banks (Driver & Muñoz-Bugarin, 2019). Further, Dittmar and Mahrt-Smith (2007) discovered that an effective board governance system can double the value of cash as compared to a weak one.

A study by Luo and Hu (2011) revealed that corporate governance and financial constraints serve as alternatives for the management of cash. As financial constraints do not exercise a large amount of control on the managers of financially unconstrained firms, the stockholders of these firms depend more on internal monitoring than the stockholders of financially constrained firms (Lee & Park, 2016). For better operational and financial transparency, the companies’ stockholders make improvements to the board monitoring system (Bebchuk, 2007). The board governance effectiveness decreases managers’ probability of working as per their own interests, but it does not completely reveal the stockholders’ material information. According to Karamanou and Vafeas (2005), the accuracy and frequency of forecasted earnings increase with the board’s effectiveness. By adopting governance standards for the board’s effectiveness, stockholders can reduce the ability and incentive to obtain corporate investment information (Leuz et al., 2003). Efficient boards that respond to the stockholders’ questions promptly put into practice a suitable voting system that can punish as well as supervise poor management (Manne, 1965), thereby further discouraging the management from exhibiting bad behavior (Bebchuk et al., 2009). Moreover, Ashbaugh-Skaife et al. (2006) argued that companies with effective board governance have superior access to financial markets with lower bond yield and higher bond rating. As a result, it can be suggested that firms that are financially less constrained tend to keep effective board governance, compared to financially constrained companies.

H3: Financially less constrained firms have stronger board governance.

Research Methodology

This section includes the data and methodology, variables description, econometric model, and the statistical description of the variables under the present study.

Data and Variables

The annual data of 860 A-listed Chinese firms in the non-financial sector was collected for the present study. A-Listed Chinese companies are the firms listed on Chinese stock exchanges (Shanghai and Shenzhen). The shares of these companies are traded in Chinese yuan or renminbi. For the current study, we selected A-listed companies because A shares consist of approximately 96% of the total shares traded. This study used the data for 16 years, from 2005 to 2020. China Stock Market & Accounting Research and RESSET databases were used for the data collection which was then winsorized at 1% level. The Fixed Effects Model of regression with robust standard error was used in this study.

Cash Holding and its Measurement

In financial literature (Bates et al., 2009), cash is generally comprised of both cash and cash equivalents. Cash holdings are measured in terms of cash plus cash equivalents to non-cash assets.

Econometric Models of the Study

This study used fixed effect model as baseline estimator, and to deal with diagnostic issues relied on robust fixed effect model. Overall, fixed effects and robust fixed effects estimation in panel data analysis allow for controlling unobserved individual-specific factors, handling unobserved heterogeneity, and dealing with heteroscedasticity and serial correlation. These techniques enhance the validity and reliability of the estimates and help researchers draw more accurate conclusions from panel data.

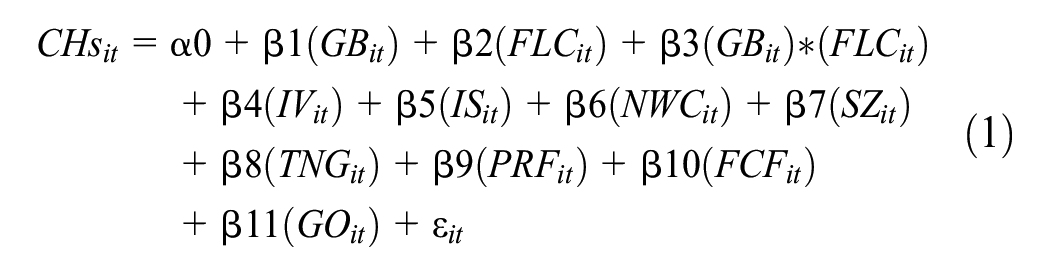

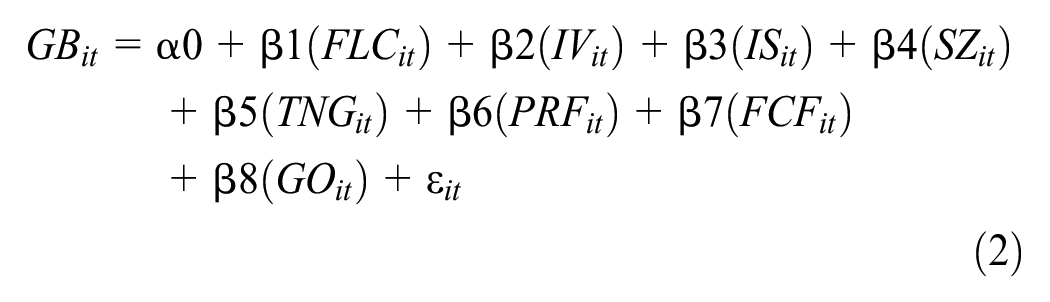

CH (Cash Holdings) represents the LN (Natural Logarithm) ratio of cash plus cash equivalents to non-cash assets; GB (Governance Board) is the LN (Natural Logarithm) of the overall corporate governance index of effectiveness of the board; FLC (financially less constrained) is the dummy variable which is equal to zero (0) if the firm is financially constrained and One (1) for the firm that is financially less constrained, based on the four criteria for measuring the same (Z score, KZ index, SA1 index, and SA2 index); IV (Idio Volatility) is the LN of the current year’s idiosyncratic return volatility; IS (Institutional Shareholdings) is at the end of the preceding year ratio of shareholding by the institutions to total shares outstanding; NWC (Net Working Capital) is the ratio of networking capital to non-cash assets; SZ (Firm Size) is the LN of the book value of the company’s total assets; TNG (Tangibility) is the net fixed assets divided by total assets; PRF (Profitability) is defined as profit before extraordinary items divided by total assets; FCF (Free Cash Flow) is the difference between cash flow from operations and capital expenditures, divided by total assets; GO (Growth Opportunities) is the ratio of market to book value of equity divided by the non-cash assets; and ϵi is the error term.

Financial constraints and board governance

To test H3, the study uses the following model:

Control Variables

In this study, two equations and two sets of control variables are used. In the first regression test, which is corporate cash holdings determinant by the governance board and financial constraint, corporate cash holding is used as the dependent variable. Some of the cash holding determinants used in other studies as control variables were considered (Kusnadi, 2019; Lee & Park, 2016), and idiosyncratic return volatility, institutional shareholdings, tangibility, firm size, free cash flow, growth opportunities, net working capital, and profitability are used as control variables for the first regression test.

In other regression tests, the governance board is the dependent variable, which is the internal governance mechanism. As seen in the literature, a correlation between several characteristics of firms and internal governance systems is affirmed. Therefore, the present study uses the following control variable in regression, as per Lee and Park (2016): idiosyncratic return volatility, institutional shareholdings, firm size, tangibility, profitability, free cash flow, and growth opportunities. Measurements of the variables along with references is shown in Table 1.

Measurement of Variables.

Measurement of Financial Constraints

In literature, many possibilities have been suggested such as investment cash flow sensitivity (Fazzari et al., 1988), as seen in recent literature (Machokoto, 2020), Whited and Wu index (WW) (Whited & Wu, 2006) used by (Qasim et al., 2021), Kaplan and Zingales index (KZ) (Lamont et al., 2001), and a number of other firm-based criteria to measure financial constraints such as Z Score, SA index, etc.

Despite the fact that there are different probable methods for measuring financial constraints, such as the WW index (Qasim et al., 2021), there is a debate on the merits of each of these methods. It is not unanticipated because every approach depends upon some empirical and/or theoretical supposition that may or may not be valid. In the current research, financial constraints are measured using the following methods.

In the first step, Altman’s Z-Score index model by Altman (1968) was used for identifying the firms that are financially less constrained. The model is mentioned bellow:

where Si = the ratio used for the measurement of liquidity of firm; this is the ratio of the working capital to total assets. Sii = the retained earnings divided by total assets which is the amount that is not paid to the shareholders as dividend, but the company retains it to pay debt or reinvest in the core business.

Siii = the ratio used to measure the firm’s EBIT against its total assets; the formula used is EBIT/total assets. Siv = the ratio that shows the relative percentage of equity by shareholders and debt used by the firm to finance its assets; the formula used is market value of equity/total liabilities. Sv = this ratio indicates the ability of the firm to generate revenues using assets; the formula used is sales/total assets. Greater ratio shows that leadership is good in the management of assets and the firm is more efficiently run. If the score is low, it shows more chances of bankruptcy. For instance, the value of Z-score of more than 2.99 shows the financial soundness and less than 1.81 points toward high likelihood of bankruptcy.

The SA index created by Hadlock and Pierce (2010) was used in this study to measure financial constraints. This index is based on the age and size of a company. A high SA index score shows that a company is financially constrained, and a low SA index score shows that it is less constrained. For the measurement of size, the authors used the natural logarithm of the total assets held by the firm or the natural logarithm of its sales. The firm’s age can be calculated by the listing date of the firm. In this research, both the measure of the size, that is, sales, as well as assets were used to calculate the SA index.

SA1 Index = –0.737(log of total assets) + 0.043(log of total assets)2 − 0.040(Firm’s Age)

SA2 Index = –0.737(log of sales) + 0.043(log of sales)2 − 0.040(Firm’s Age)

The values will be divided into three quartiles after calculating the SA index (SA1 and SA2 index). Firms that belong to quartile three (3) are financially less constrained, whereas those belonging to quartile one is classified as financially constrained.

In this study, the KZ index is also used to measure financial constraints, as formulated by Lamont et al. (2001).This index is based on the following five-factor model, as presented by Lamont et al. (2001):

Debt, Market Value, Dividends, Cash Flow, and Cash Holdings, each scaled by total assets. The value of the KZ index will be greater for firms that are financially more constrained.

KZ = −1.001909 CF/K + 0.2826389Q + 3.139193 Debt/Total Capital − 39.3678Div/K − 1.314759 Ch/K

CF = Sum of Income Before Extraordinary Items, Depreciation, and Amortization); K = PP&E t − 1

Q = (Market Capitalization + Total Shareholder’s Equity − Book Value of Common Equity − Deferred Tax Assets)/Total Shareholder’s Equity; Debt = Sum of long term and short-term debts; Div = Total amount of cash dividends paid on common stock as well as on preferred stock, and Ch = Cash plus short-term investments

Measurement of Corporate Governance for Board Effectiveness

La Porta et al. (2000) believe that corporate board governance is a mechanism through which owners of corporations (shareholders) safeguard their interests from exploitation by insiders. In contrast to most indices used for the measurement of corporate governance quality based on survey questionnaires (Black et al., 2006; Klapper & Love, 2004), in this study, for all the A-listed Chinese firms, an index of corporate governance was designed. It is based on the information related to the governance available in these firms’ annual financial reports. The study conducted by Bai et al. (2004) and Tang and Wang (2011) used the same approach to measure corporate governance for individual firms in China. Based on economics and finance literature, the present study scores a variable if the variable adds to the corporate governance quality. The present authors designed a corporate governance index by taking out the average of eleven variables. Therefore, by using this method, the problem associated with variables that are not available for some individual firms will be avoided. A high score of governance index indicates the improved quality of corporate governance and a low score indicates otherwise. The details related to every variable and their criteria of scoring are provided in Table 2.

Measurement of Overall Corporate Governance Index.

Source. Tang and Wang (2011).

Research Results

Table 3 shows the descriptive properties of the underlying variables such as CH, GB, IV, IS, NWC SZ, TNG, PRF, and FCF in terms of the central value, minima, maxima, and standard deviation.

Summary Statistics.

Table 4 reports the fixed-effect results for all the firms (financially constrained as well as less constrained) using Z score, KZ index, SA1 index, and SA2 index. The results show that the amount of cash reserves does not change with the quality of corporate governance. A financially less constrained status maintains a significant and positive impact upon corporate cash holdings when the KZ index and SA1 Index are utilized. It means that with financially fewer constraints, firms hold more cash, whereas using Z score and SA2 index the association is not found. IV shows a highly significant and positive impact on corporate cash holdings when Z score and KZ index are used, implying that firms with high IV are likely to have higher levels of cash for the upcoming periods. There is a possibility for such firms to face cash shortage, so they hold high cash reserves to utilize during rainy days. Further, using SA1 and SA2 indices, IV has an insignificant impact on cash holdings. Across all models, cash holding does not change with institutional shareholdings.

Fixed Effect (Overall).

Note. Sign (***), (**), and (*) show the level of significance at 1%, 5%, and 10%, respectively. Standard errors are in brackets.

Under all the four proxies for measuring financial constraint, the net working capital shows a significant but negative impact on the level of corporate cash holdings, showing that firms with a high amount of networking capital tend to hold low cash reserves. Compared to other assets, liquid assets are easily convertible to cash and with low cost, because of which firms having more net working capital (liquid assets) are expected to hoard lesser cash. This result is consistent with Ali and Yousaf (2013), Gill and Shah (2012), and Lee and Park (2016), who reported the inverse association of cash holdings with net working capital.

There is a statistically significant but negative relation between SZ and corporate cash holdings, showing that large-size firms hold lesser cash for the future. This implies that large firms can easily approach diversified funding sources. Notably, the results of the present study are consistent with Lee and Park (2016), according to whom small-size firms hold more cash because of borrowing constraints and higher costs attached to raising external funds. The findings are consistent with related studies (Al-Najjar & Belghitar, 2011; Bates et al., 2009), which hold that larger firms, due to easy access to different funding sources and the ability to liquidate their non-core assets, hold less cash reserves. In accordance with Khieu and Pyles (2012), firms having good credit rating hold low cash reserves was also affirmed. Firm size displays an insignificant negative relation with corporate cash holdings when the SA2 index is applied as a proxy to measure financial constraints.

There is a significant but negative relationship between tangibility and corporate cash holdings under all the four criteria for measuring financial constraints. It shows that more tangible firms hold a less cash for their future needs, and firms with more tangibility can easily get loans from the market when needed; therefore, these firms hold low cash. Using all the four criteria, that is, the Z score, KZ index, SA1 index, and SA2 index, to measure financial constraints, profitability shows a strongly significant and positive effect upon corporate cash holding. Firms hold on to more cash when they make more profits. The present study’s results are aligned with the Pecking order theory, which claims that firms having more profitability hold more cash. The finding is also consistent with those of prior studies (Al-Najjar & Clark, 2017; Lee & Park, 2016) which show that firms with more profits have more cash reserves.

A significant negative impact is present for free cash flow with the firms’ cash holdings under all the four criteria for measuring financial constraints. It means that firms enjoying high free cash flow hold less cash reserves. This is the reason behind treating free cash flow as a substitute for cash. The present study’s finding is consistent with findings presented by Ferreira and Vilela (2004) that cash flow maintains a negative relationship with cash holdings.

There is a significant and positive relationship between growth opportunities and corporate cash holdings when the Z score SA 1 index and SA 2 index are utilized to measure financial constraints. It reveals that firms with more growth opportunities must hold more cash reserves to avail these opportunities. This result is in line with the trade-off theory, which implies that for firms with high-quality investment projects, the opportunity cost is harsher due to a lack of liquidity. Therefore, to avoid such costs, firms with investment projects of the best quality would hold greater amounts in cash to avoid future underinvestment risk. The present study’s results are in accordance with the literature (Lee & Park, 2016), which reports that firms having growth opportunities try to hold more cash reserves. However, growth opportunities showed no impact upon cash holdings while using the KZ index for measuring financial constraint.

Table 5 indicates an insignificant impact of board governance on the level of cash holdings of the financially constrained firms when Z score and KZ index are used. However, corporate governance has a significant and positive impact on the level of cash holdings by the firms when the SA 1 index and SA 2 index are used, shows that firms having strong corporate governance keep more cash reserves.

Financially Constrained Firms (Robust Fixed Effect Results).

Note. Sign (***), (**), and (*) show the level of significance at 1%, 5%, and 10%, respectively. Standard errors are in brackets.

The present study’s result is consistent with those presented by Harford et al. (2008), and Lee and Park (2016). IV has an insignificant impact on the corporate cash holdings level under all the four criteria for measuring financial constraints. There is a significant positive impact of institutional shareholding on corporate cash holding when the KZ index and SA2 index are used to measure financial constraints. It means that the level of cash for the firms that are financially constrained increases with institutional ownership, which is consistent with the literature (Lee & Park, 2016). When Z score and SA1 index were used as a proxy for measuring financial constraints, there was an insignificant impact of institutional shareholding on corporate cash holding.

Under all the four proxies for measuring financial constraint, Net Working Capital maintains a significant and negative impact on the corporate cash holdings level, showing that firms with a high amount of networking capital tend to hold low cash as reserves.

As compared to other assets, liquid assets are convertible to cash easily and with low cost because of which the firms with more Net Working Capital (liquid assets) are expected to hoard low cash. The result is consistent with that of Ali and Yousaf (2013) and Lee and Park (2016), who reported the presence of an inverse relationship between net working capital and cash holdings.

There is a significant negative impact of size on corporate cash holding while measuring financial constraints using SA2. It implies that large-sized firms hold less assets as cash. This result is in accordance with that of Lee and Park (2016). Size significantly and positively impacts corporate cash holding when the Z score is used to measure financial constraints. However, when the KZ index and SA1 index are used to measure financial constraints, the size has an insignificant impact on corporate cash holdings.

There exists a statistically significant but negative impact of tangibility on corporate cash holdings under all the four criteria for measuring financial constraints. It shows that more tangible firms hoard less cash for the future. Firms with more tangibility can easily get loans from the market when they need to. So, these firms hold low levels of cash.

The finding that firms with more profit hold more as cash reserves is also consistent with other studies (Al-Najjar & Clark, 2017; Ferreira & Vilela, 2004). Free cash flow maintains a significant but negative impact on corporate cash holdings when SA1 and SA2 are used to measure financial constraints. It shows that firms that have high cash flows tend to hold less cash as reserves because the free cash flow is treated as a substitute for cash. The finding that a negative relationship exists between cash flow and cash holdings is aligned with literature (Ferreira & Vilela, 2004). In comparison, cash flow has an insignificant negative impact on corporate cash (Habib et al., 2022) holdings when the Z score and KZ index are used to measure the financial constraint status.

When Z score is used to measure financial constraints, there is a statistically significant and positive impact of Growth Opportunities on cash holdings by firms. It means that firms with higher growth opportunities must hold more cash to avail them. The present study’s result is in line with the trade-off theory and consistent with the findings of Lee and Park (2016). However, there is an insignificant negative impact on growth opportunities when the KZ index, SA1 index, and SA2 index are used to measure financial constraints.

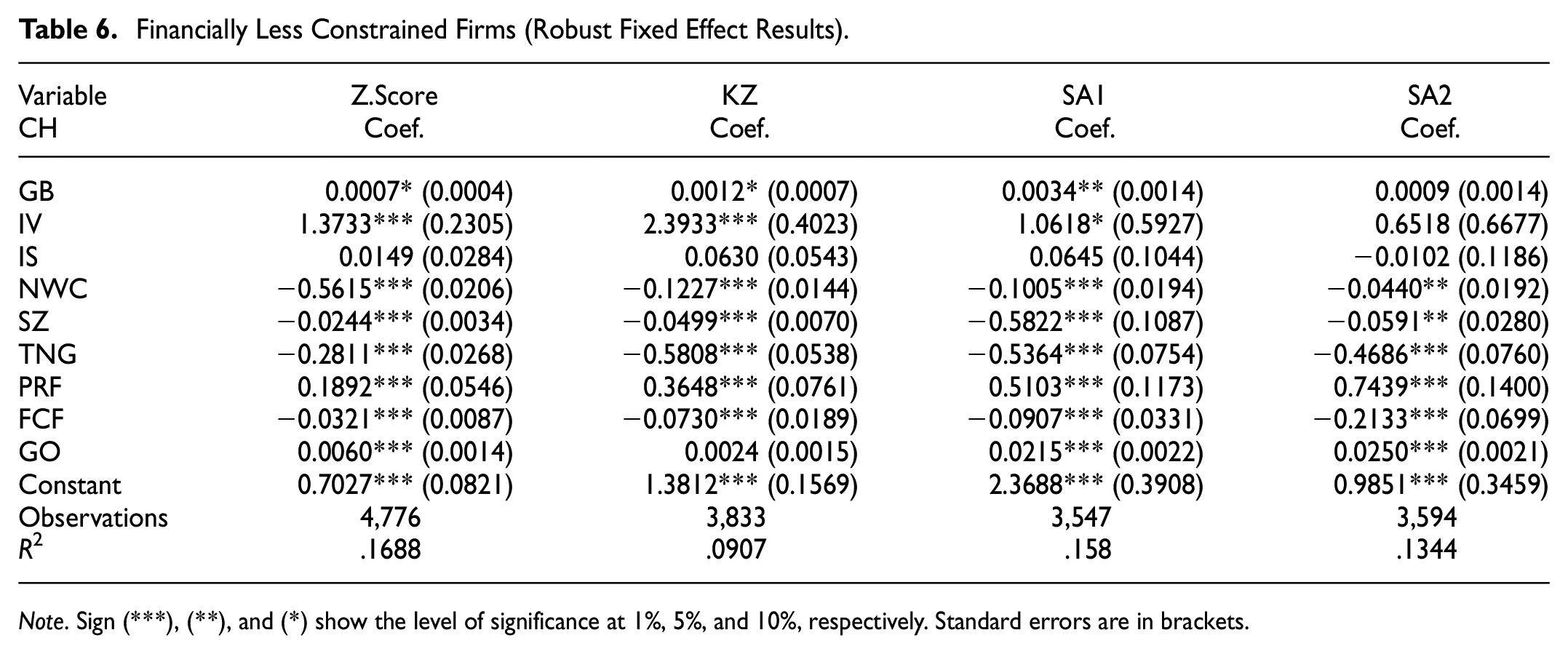

Table 6 depicts the results for the fixed-effects model used in the panel regression for firms that are financially less constrained. GB significantly and positively impacts corporate CH using the KZ index, Z score, and SA1 index as proxies for financial constraints. It means that with a stronger governance board, cash holdings by the firm will increase. It also implies that strong corporate governance mitigates the agency problems between shareholders and managers over cash holdings. Therefore, if corporate governance is more effective, managers cannot use cash for furthering their own interests. As a result, shareholders’ concern about excess cash holding is minimized; thus, firms with less financial constraints hold a higher amount of cash.

Financially Less Constrained Firms (Robust Fixed Effect Results).

Note. Sign (***), (**), and (*) show the level of significance at 1%, 5%, and 10%, respectively. Standard errors are in brackets.

The present study’s findings follow the same patterns as those of Harford et al. (2008) study, which showed that firms having effective corporate governance may hold more amount of cash by mitigating the agency problems. The result of this study is also supportive of Lee and Park (2016), who found that corporate cash holding increases when there is effective corporate governance. However, GB has an insignificant impact on CH when the SA2 index is used as a proxy for financial constraint.

IV has a significant positive impact on CH when the Z score, KZ index, and SA1 index are used as proxies to measure the financial constraint, which means that firms with high IV hold higher amount in the form of cash for future. There is a higher possibility for the firms with high volatility to face cash shortage, so these types of firms hold more cash reserves to utilize during rainy days. Further, IV has no impact on CH when the SA2 index is used as a proxy.

IS has no impact on CH when the Z score, KZ index, and SA1 and SA2 indices are used to measure financial constraints. Under all the four proxies for measuring financial constraint, net working capital shows a significant negative impact on corporate cash (Habib et al., 2022) holding levels, showing that firms with a high amount of networking capital tend to hold low cash as reserves. Compared to other assets, liquid assets are easily convertible into cash and with low cost because of which the firms having more net working capital (liquid assets) are expected to hoard less amounts of cash. This result is consistent with the results of Ali and Yousaf (2013), while Lee and Park (2016) reported that an inverse relationship exists between net working capital and cash holdings.

Under all the four criteria for measuring financial constraints, SZ has a significant negative impact on CH, showing that large-size firms tend to hold fewer amounts as cash for future needs. In comparison to small firms, larger firms can easily approach diversified funding sources and can easily get a loan from the market when they need cash, owing to their larger size in the market. The result is contrary to the results of Marwick et al. (2020). Moreover, the result is very much in line with that of Guizani (2017); according to them, small firms hold higher cash reserves because of borrowing constraints and higher costs attached to raising funds from external sources. The present study’s finding that large firms, due to easy access to different funding sources and the ability to liquidate their non-core assets, hold less cash reserves is also in accordance with the results of Al-Najjar and Belghitar (2011) and Bates et al. (2009).

A significant but negative impact is shown by tangibility on corporate cash holdings under all the four criteria for measuring financial constraints. It shows that more tangible firms hold lesser levels of cash as they can easily get loans from the market when needed, implying low hold of cash.

There is a significant and positive effect of profitability on corporate cash holdings as per all the four criteria, that is, Z Score, KZ index, SA1 index, and SA2 index, for measuring financial constraints. This shows that higher cash reserves will be held by firms having more profit. The study’s finding is aligned with the Pecking order theory, which suggests that firms with more profitability hold more cash. The study results that firms with more profit keep more cash as reserves is consistent with literature (Al-Najjar & Clark, 2017; Ferreira & Vilela, 2004).

Free cash flow has significantly and negatively impacted corporate cash holdings under all the four criteria for measuring financial constraints. It reveals that firms having high cash flow maintain low cash reserves. This is because the free cash flow is treated as an alternative to cash. The study’s finding that a negative relationship exists between cash flow and cash holdings is consistent with those of Ferreira and Vilela (2004).

Growth opportunities significantly and positively impact corporate cash holdings for firms that are financially less constrained when the Z score, SA 1 index, and SA 2 index are used to measure financial constraints. It means that all firms with higher growth opportunities tend to hold more cash to avail these opportunities. The result is in accordance with the trade-off theory, which suggests that for the firms having investment projects of high quality, the opportunity cost is harsher due to lack of liquidity. Therefore, to avoid such costs, firms with investment projects of the best quality will hold larger amounts in cash to avoid the future’s underinvestment risk. These results are in line with the findings presented by Lee and Park (2016), who reported that firms having growth opportunities would hoard more cash. However, there is an insignificant relationship between growth opportunities and cash holdings when the KZ index is used to measure financial constraints.

The fixed-effects regression result with an interaction term of governance board and overall firms’ financial constraints shows that governance board insignificantly impacted corporate cash holdings under all the four criteria used to measure financial constraints (the results are not reported for brevity).

The interaction between corporate governance and the financially less constrained status of firms positively and significantly impacts corporate cash holdings when the Z score, KZ index, and SA1 index are used as a proxy to measure overall financial constraints. It reveals that financially less constrained firms hold a large amount of cash when there is effective board governance. This result is consistent with our second hypothesis (H2), stating that with effective board governance, the level of cash hoarding by financially less constrained firms increases further. This result implies that effective board governance decreases agency problems between managers and shareholders, leading to larger cash holdings by these firms. This result is quite similar to the findings by Lee and Park (2016), who reported that firms with less financial constraints hold more in the form of cash with effective corporate governance. The interaction term shows an insignificant impact on corporate cash holdings when the SA2 index measures the overall financial constraints.

IV shows a statistically significant and positive relationship with cash holdings when proxies SA1 index and SA2 index are used to measure overall financial constraints. There is a higher possibility for firms with high volatility to face cash shortage, so they intend to hold more cash reserves to utilize in the future. It has an insignificant impact on corporate governance when overall financial constraints were measured through the Z score and KZ index.

Institutional shareholding has an insignificant impact on corporate cash holdings under all the four criteria measuring financial constraints. Under all the four proxies for measurement of financial constraint, networking capital significantly and negatively impacts the level of corporate cash holdings, showing that firms with a high amount of the same tend to hold low cash reserves. Compared to other assets, liquid assets are easily convertible into cash. The cost is also low; thus, firms having more net working capital (liquid assets) are expected to hoard less cash. This result is consistent with those put forth by Ali and Yousaf (2013) and Lee and Park (2016), who reported an inverse relationship exists between working capital and cash holdings.

Under all the four criteria, SZ has a significant negative impact on CH, that is consistent with Al-Najjar and Belghitar (2011) and Bates et al. (2009). Tangibility has a strongly significant but negative impact on corporate cash holdings under all the four criteria for measuring financial constraints. It was found that more tangible firms are likely to hold lesser levels of cash in the future. Firms with more tangibility can easily get loans from the market when needed. Therefore, these firms hold low cash. Profitability has an insignificant relationship with corporate cash holdings under all the four criteria used to measure financial constraints.

Free cash flow displays a significant and negative impact on corporate cash holdings under all the four criteria for measuring financial constraints. It shows that firms having high cash flow tend to hold less cash reserves because free cash flow is treated as a substitute for cash. The study’s finding that cash flow has a negative relationship with cash holdings is consistent with the results of Ferreira and Vilela (2004).

Growth opportunities depict a statistically significant and positive impact upon cash holdings under all the four criteria used to measure financial constraints. It was revealed that firms with more growth opportunities hold more cash to avail these opportunities. The results of this study are consistent with the trade-off theory that claims that for firms having investment projects of high quality, the opportunity cost is harsher due to lack of liquidity. To avoid such costs, firms having investment projects of the best quality hold larger amounts in the form of cash to avoid underinvestment risk in the future. The study’s result that firms with more growth opportunities hoard more cash is in accordance with the findings of Marwick et al. (2020).

Table 7 shows that financial less constraint status dummy has a significant and positive impact on corporate governance while financially constrained firms, firms with fewer financial constraints have strong board governance for minimizing agency concerns and imposing effective control on the firms’ current managers. The results are consistent with Lee and Park (2016). Importantly, the result supports the third hypothesis (H3). While there is an insignificant impact of financially less constraint status on corporate governance, with SA1 index. IV has a significant and positive impact on GB implying that firms with high idiosyncratic volatility have strong corporate governance, showing that it is more likely that firms having high advising and monitoring cost to have effective corporate governance. The result is consistent with the findings of Lee and Park (2016). Across all models, the significant and positive association of IS, SZ, and PRF with corporate governance is consistent with related literature see for example Berry et al. (2006), and Lee and Park (2016).

Fixed Effect Regression Overall.

Note. Sign (***), (**), and (*) show the level of significance at 1%, 5%, and 10%, respectively. Standard errors are in brackets.

Robustness with alternative estimator

In this section, we conducted a robustness check using the Driscoll-Kraay Standard Error for financially constrained, and less constrained firms, which serves as a near alternative to the robust fixed effect model employed in the main analysis. This approach allows us to assess the robustness of our findings by addressing issues of serial correlation and heteroscedasticity in the panel data.

The results of financially constrained firms are reported in Table 8, which remain consistent across all columns, reinforcing the robustness and reliability of our findings. The coefficients for the variables of interest, namely Z.Score, KZ, SA1, and SA2, remain unchanged and which indicates that the relationships between these variables and the dependent variable remain robust and unaffected by the adjustment of standard errors.

Financially Constrained Firms (Driscoll-Kraay Standard Error).

Note. Sign (***), (**), and (*) show the level of significance at 1%, 5%, and 10%, respectively. Standard errors are in brackets.

Similarly, we extended our analysis to investigate the less financially constrained firms and applied the Driscoll-Kraay Standard Error to ensure the robustness of our findings. This approach allows us to examine whether the relationships observed in the main analysis hold consistently across different subsets of firms. As shown in Table 9 that our results for the less financially constrained firms also demonstrate robustness. The coefficients for the variables of interest remain consistent and reliable, and the adjusted standard errors provide more accurate estimates and allow for robust statistical inference, ensuring the validity of our findings.

Financially Less Constrained Firms (Driscoll-Kraay Standard Error).

Note. Sign (***), (**), and (*) show the level of significance at 1%, 5%, and 10%, respectively. Standard errors are in brackets.

The robustness of the results across both financially constrained and less financially constrained firms reinforces the robustness of our overall findings. These findings contribute to a comprehensive understanding of the phenomenon under study and enhance the generalizability of our results. They provide additional support to the conclusions drawn in the main analysis and strengthen our confidence in the relationships between the variables examined.

Conclusions

The aim of this study was to examine the relationship between cash holdings, financial constraints, and board governance. We hypothesized that financially less constrained firms would hold more cash when they have effective boards that can monitor and discipline managers’ investment decisions. We also expected that financially less constrained firms would adopt higher board standards to reduce the agency costs of free cash flow. Using a panel data of Chinese firms from 2010 to 2020, we employed a robust fixed effect model to test our hypotheses. The empirical results showed that (1) firms facing more financial constraints tend to hold more cash as a precautionary motive; (2) among financially less constrained firms, those with more effective boards have higher cash holdings, suggesting that board governance can mitigate the underinvestment problem; and (3) financially less constrained firms have stronger board governance than financially constrained firms, as evidenced by more independent directors, more frequent board meetings, and higher CEO turnover-performance sensitivity.

The study provides several insights into how firms can optimize their cash management practices and reduce agency problems. One of the key findings is that effective board governance, such as having independent directors and audit committees, can enhance the monitoring and oversight of cash usage and prevent managerial opportunism. Another important implication is that alleviating financial constraints, such as improving access to external financing and reducing debt costs, can help firms invest their cash more efficiently and avoid over- or under-investment. Furthermore, the study suggests that shareholder activism, such as proxy contests and shareholder proposals, can exert pressure on managers to align their interests with those of shareholders and use cash in value-enhancing ways. Finally, the study recommends that firms reform their cash holding policies, such as setting optimal cash targets and paying dividends or repurchasing shares when excess cash accumulates, to balance the benefits and costs of holding cash. These policy implications aim to improve corporate decision-making, increase investment efficiency, and benefit various stakeholders, including shareholders, executives, and the overall economy.

The findings of this study have useful policy implications, but they may not be generalizable to other contexts because they only include A-listed Chinese firms. Moreover, the study uses a limited set of variables to measure financial constraints and board governance, which may not capture all the relevant aspects of these concepts. Therefore, the readers should interpret the results with caution and consider the limitations and the time period of the study.

This study can be extended in future research by using different classes of shares and different economies to provide a more comprehensive picture of cash holding policies and governance practices. Furthermore, future studies can use more indicators of financial constraints and board governance, such as the WW index, bond rating, firm size, annual payout ratio, and more board standards, to examine the differences in cash holding policies between financially constrained and less constrained firms.po?>

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Ethical Statement

The manuscript for submission has been approved by all authors, and the content of the manuscript has not been published or submitted for publication elsewhere. The Ethics Committee approval is not applicable because study used secondary data.

Informed Consent

Informed consent is not applicable, because the study used secondary data.

Availability of data and material

All raw data used in the study is available at reasonable written request from the corresponding author.