Abstract

This study examines the influence of three forms of uncertainties (firm-specific, market-based, and economic policy uncertainty) on corporate cash holdings in China, particularly considering the moderating role of firms’ ownership structure, financial constraints, and trade credit. Using an annual panel dataset from 2003 to 2023 of A-share listed manufacturing firms on the Shanghai and Shenzhen Stock exchanges, we find that firm cash holdings are positively affected by all forms of uncertainties. The results further show that private and financially constrained firms are positively, while access to trade credit negatively moderates this nexus. Robustness checks, including alternative measures of cash holdings, fixed effect model, and GMM, confirm the validity of the results. The findings contribute to the corporate finance literature by emphasizing the distinct effects of ownership, financial constraints, and access to trade credit in uncertain economic situations. The results offer valuable insights to managers, policymakers, and investors.

Introduction

Cash is a crucial and highly liquid asset for any corporation. Corporate cash holdings (CHs hereafter) refer to the cash and near-cash assets that a company retains to maintain a vital liquidity buffer (Opler et al., 1999). This buffer plays a vital role in ensuring financial flexibility, managing operational risks, meeting short-term obligations, and seizing profitable opportunities (Almeida et al., 2004; Feng et al., 2022; Nguyen et al., 2022). In recent years, a growing number of firms have increased their CHs as part of prudent financial management (Maneenop et al., 2023). This phenomenon has prompted researchers to reinvestigate the motivations behind CHs.

CHs play a crucial role in corporate finance, as firms often amplify CHs for various purposes. Two primary theories shape our understanding of CHs’ behavior: the precautionary motive and agency theory. The precautionary motive (Keynes, 1937) emphasizes firms’ need to maintain CHs as a safeguard against unexpected challenges in the business setting. Firms prefer CHs as a precautionary measure to prepare for short-term debt crises, enhance their resilience, and seize profitable opportunities (Adrian et al., 2018; Bates et al., 2009; Myers & Majluf, 1984). On the other hand, agency theory suggests that poor oversight may lead managers to retain CHs for personal or discretionary spending (Jensen, 1986). Relying solely on these classical theories is insufficient to capture the complexities of firm behavior in emerging economies. Beyond these perspectives, recent research also highlights the impact of institutional environments (North, 1990), managerial behavioral biases, and political dynamics, which jointly shape CHs’ behaviors, especially in emerging markets where financing and governance structures are different from those in developed economies (Chen et al., 2023; Das et al., 2024).

When deciding on CHs, it’s essential to weigh multiple factors, particularly the uncertainties in both internal and external environments. Uncertainty is a crucial factor influencing CHs policy. Studies identify uncertainty from sources such as firm-specific factors (earnings volatility, operational risk), market-driven elements (stock return volatility, investor sentiment), and broader macroeconomic issues (economic policy uncertainty, geopolitical instability; Chen et al., 2023; Das et al., 2024; Gao et al., 2017; Tran, 2020; Xian et al., 2024). Each type of uncertainty affects CHs management differently, but most research focuses on one aspect, overlooking the complex interactions between them. This study extends these studies by adopting an integrative approach. We empirically examine how firm-specific uncertainty (Fsν), market-based uncertainty (Mν), and economic policy uncertainty (Epν) affect CHs in China within a single analytical framework. The reason for focusing on three distinct but complementary types of uncertainty is that they influence managerial expectations, investment timing, financing strategies, and liquidity management in different ways. Therefore, analyzing both their combined and individual effects enhances our understanding of how firms adjust their CHs policies in response to these layered uncertainties. Previous studies on the uncertainty-CHs nexus revealed mixed results across different economies and firm structures. While many find a positive correlation (Chen et al., 2023; Gao et al., 2017; Xian et al., 2024; Zhao & Niu, 2023), others report weaker or opposing effects due to strong governance or investor pressure. Studies show that uncertainty can exacerbate agency conflicts between managers and shareholders due to heightened information asymmetry, which often results in lower CHs for high-uncertainty firms (Drobetz et al., 2010). Research by Attig et al. (2021) has shown a positive link between Epν and cash dividends, indicating that shareholders may leverage dividends as a strategy to alleviate agency issues during uncertain periods. Additionally, in regions with robust investor protection, shareholders can exert influence on managers to distribute cash, thus leading to a less significant negative relationship between uncertainty and CHs (El Ghoul et al., 2023). This study aims to re-examine the relationship in a broader context to reduce confirmation bias and account for these contextual factors.

This study also considers the moderating roles of ownership structure, financial constraints (FC), and trade credit (TC). CHs may alleviate the adverse effects of any uncertainty or external variations, which can enhance their financial flexibility, diminish the influence of policy-related disruptions, meet obligations, and seize profitable investment avenues (Duong et al., 2020; Feng et al., 2022). Thus, understanding how these uncertainties affect CHs in emerging economies like China provides valuable insights for managers, policymakers, and investors. Furthermore, to enhance our theoretical framework, we also incorporate institutional theory (North, 1990), behavioral perspectives, particularly managerial overconfidence (Malmendier & Tate, 2005), and political influences (Tran et al., 2024). By integrating these viewpoints, we create a multi-theoretical framework that captures the complex interplay between external shocks, governance conditions, and firm-specific characteristics in determining CHs policies.

China offers a distinct environment for studying the impact of three important forms of uncertainties on CHs. China, as the world’s second-largest economy, is transitioning from a centrally planned to a market-based economy (B. Xu et al., 2019). The implementation and practice of free-market principles have created numerous investment avenues for firms. However, given China’s rapid economic transition, the constantly changing regulatory environment, and the government’s active engagement in economic decision-making processes, the economic situation is marked by substantial degrees of market and policy uncertainty (Gulen & Ion, 2016). As organizations undergo frequent changes in various aspects during economic transformation, it is clear that uncertainty will impact a firm’s financial behavior, particularly CHs’ decisions. Furthermore, China’s corporate finance industry is still developing, which makes it difficult for businesses to obtain outside funding. Chinese companies may therefore maintain CHs to lessen reliance on outside sources, especially those in specialized industries or with particular ownership arrangements. Moreover, China’s capital markets, though improved over recent decades, remain underdeveloped compared to developed nations. Tran (2020) noted that firms in emerging markets tend to foster CHs during economic crises due to limited funding options. Despite China’s large and active capital markets and extensive banking network, its financial system still faces obstacles, such as high transaction costs that affect firms’ ability to obtain outside funding, particularly during volatile market situations. Private firms may be more sensitive to uncertainty than state-owned enterprises (SOEs), as they lack access to government helping hands and rely on internal funding (Chen et al., 2018). Likewise, financially constrained (FC) firms may seek to stimulate CHs as a precautionary measure against liquidity risks in times of heightened uncertainty (Almeida et al., 2004; Feng et al., 2022). Conversely, trade credit (TC) acts as a substitute for liquidity (Ng et al., 1999); firms with limited access to TC may be more dependent on CHs. These characteristics suggest that firms in China, especially those in the manufacturing sector, may have distinct liquidity management needs in the face of uncertainty that differ from those in developed markets.

Despite the importance of these contextual factors, the existing literature has two notable limitations. Most studies examine a single dimension of uncertainty in isolation, and the majority of the literature concentrates on developed markets (Bates et al., 2009; Duong et al., 2020; El Ghoul et al., 2023; Gao et al., 2017; Opler et al., 1999). Unlike developed markets, China’s distinctive ownership structures and institutional frameworks necessitate a focused study on how these factors influence the CHs strategies. Firms in China have to deal with these uncertainties, which frequently result in higher levels of CHs to shield against regulatory changes and market risks (Chen et al., 2018), particularly given the developing state of China’s corporate finance sector. Moreover, few studies systematically investigate how firm-level characteristics, such as ownership type, FC, and access to TC, moderate the uncertainty-CHs nexus. This leaves an important gap in our understanding of how institutional arrangements and firm heterogeneity shape precautionary CHs behavior in emerging markets.

To address this gap, this study investigates the influence of three forms of uncertainties (Fsν, Mν, and Epν) on CHs in China, particularly considering the moderating role of firms’ ownership structure, FC, and TC. Using an annual panel dataset from 2003 to 2023 of Chinese manufacturing firms, we find that firm CHs are positively affected by all forms of uncertainties. The results further show that private ownership and FC firms positively, while access to TC negatively moderates this nexus. Our findings enhance existing theories by integrating multiple perspectives and offer practical implications for managers and policymakers in emerging markets.

This paper adds to the body of knowledge in several ways. Firstly, unlike previous studies, that has focused on one type of uncertainty in isolation, see for instance (Xian et al., 2024) focus on Fsν, (Gao et al., 2017; Tran, 2020) focus on Mν, and (Chen et al., 2023; Das et al., 2024) focus on Epν. This study extends previous studies and contributes to the growing body of research on the three forms of uncertainty, that is, Fsν, Mν, and Epν, and their combined effects on CHs within a single model in a transition economy. Secondly, our study contributes to the emerging literature by examining the moderating roles of firm-specific attributes, including ownership structure, FC, and access to TC, which are often overlooked in the literature. Though research has shown these factors to influence how firms react to uncertainty, their combined effect on CHs, especially in the context of China, remains underexplored. The role of TC in moderating the relationship between uncertainty and CHs remains largely unexplored, particularly in China, and this study aims to address this gap. Thirdly, our study adds to the growing body of literature on liquidity management in emerging markets. While studies on CHs have predominantly focused on developed countries (Bates et al., 2009; Duong et al., 2020; El Ghoul et al., 2023; Gao et al., 2017; Opler et al., 1999) among others, emerging markets like China present unique challenges and opportunities due to their distinctive institutional environments. Furthermore, it expands the theoretical base of CHs by integrating institutional theory and behavioral perspectives with classical motives, to provide a richer theoretical foundation for explaining CHs behavior in emerging markets under uncertainty.

By focusing on China, this research broadens our insight into how firms in emerging economies adapt to uncertainty, presenting critical insights for both firm managers and policymakers in China and other similar markets. Therefore, this research offers practical recommendations to help Chinese policymakers and corporate managers optimize CHs strategies in uncertain economic conditions, specifically those in private firms or those facing FC. The findings will assist them to understand why and when they should adjust cash reserves, taking into account both internal (Fsν) and external (Mν and Epν) uncertainties.

The remaining study is structured as follows: Section “Theoretical Fremework and Hypotheses Development” reviews the literature and formulates the hypotheses, Section “Data and Methodology” details the data and methodology, Section “Results and Discussion” presents the results along with robustness and endogeneity tests, and Section “Conclusion” wraps up the conclusions.

Theoretical Framework and Hypotheses Development

Theoretical Background

Many researchers have investigated why firms amplify CHs despite their low or no yield (Salehi et al., 2020). Two prominent theories are mainly used to explain CHs behavior: agency theory (Jensen, 1986) and precautionary motives (Keynes, 1937). Precautionary motives highlight that firms maintain CHs due to FC and uncertain future income streams (Gulen & Ion, 2016; Huang et al., 2013; Tran, 2023). Furthermore, enterprises may amplify CHs to grasp optimal investment opportunities that may not materialize quickly (Liu & Wang, 2021). The agency perspective addresses conflicts of interest between owners and managers as a motive for CHs. Agency issues associated with agency costs emerge when managers prioritize their self-interests over the goal of maximizing shareholder value, leading to excessive CHs that serve personal rather than corporate interests or their shareholders (Myers & Rajan, 1998), especially in weak governance environments. While both theories independently explain CHs, combining them offers a more comprehensive understanding of how uncertainty affects liquidity management. This dual-theory approach is particularly relevant in emerging markets like China, where institutional imperfections, uneven credit allocation, and political influence intensify both motives. For instance, SOEs often benefit from preferential access to financing, which may reduce their precautionary CHs but increase agency risks due to soft budget constraints. In contrast, private firms typically face tighter FC, which amplifies the need for precautionary CHs but may limit the potential for agency-driven overaccumulation.

Relying solely on these classical theories is insufficient to capture the complexities of firm behavior in emerging economies. To enhance our theoretical framework, we incorporate institutional theory (North, 1990), which emphasizes the importance of formal and informal rules in shaping firm behavior. Research suggests that firms are adapting their CHs policies in response to factors such as institutional fragility, regulatory uncertainty, and changing macro-financial conditions (Li et al., 2023; Nguyen et al., 2022). Additionally, we consider behavioral perspectives, particularly managerial overconfidence (Malmendier & Tate, 2005), which can skew decision-making regarding CHs under uncertainty. The traits and optimism of CEOs may distort their risk assessments and CHs needs (Chen et al., 2020; Lou et al., 2021). Overconfident managers may underestimate threats, leading to inefficient CHs, while risk-averse managers might adopt overly conservative strategies, resulting in excessive CHs. By integrating these viewpoints, we create a multi-theoretical framework that captures the complex interplay between external shocks, governance conditions, and firm-specific characteristics in determining CHs policies. In summary, by incorporating insights from agency theory, the precautionary motive, institutional theory, and behavioral perspectives, this study clarifies how uncertainty affects CHs. It highlights the variations in its impact across different firms, types of uncertainty, and institutional contexts. This comprehensive approach is essential for understanding firm dynamics in these rapidly changing environments.

Hypothesis Development

Uncertainty and Corporate Cash Holdings

Uncertainty arises from numerous elements, such as firm-specific risks related to a firm, market conditions, and prevalent economic policies.

Firm Specific Uncertainty (Fsν)

Fsν captures a firm’s internal challenges, such as operational risks, managerial choices, strategic decisions, and variations in sales, which are not affected by broader market settings or economic fluctuations. Empirical findings show that firms with higher levels of Fsν, such as firms with higher leverage, poor governance structures, or fluctuating earnings, tend to augment liquidity demands, forcing them to augment CHs as a precaution to ensure stability and operational flexibility (Almeida et al., 2004).

Further, research on the Fsν-CHs relationship has shown that Fsν, such as firms with greater idiosyncratic risks, support larger CHs as a safeguard against operational uncertainties and fluctuations (Bates et al., 2009; Gao et al., 2013). The precautionary approach supports increasing CHs in response to firms’ vulnerability to internal risks to diminish the liquidity issues (Kim et al., 1998).

In China, Xian et al. (2024) observed that firms with higher idiosyncratic risks, including insiders engaged in financial misconduct and more access to private information, tend to amplify CHs. Likewise, Liu and Wang (2021) found that risk-averse managers postpone investments amid significant idiosyncratic risk leading to increased CHs. Overall, these findings underscore the critical role of Fsν in increasing CHs. Drawing from the literature review and arguments, we propose the following hypothesis:

Market-Based Uncertainty (Mν)

Mν reflects uncertainty from external market factors, such as stock market variations and macroeconomic conditions, which strongly influence CHs practices among firms, particularly, in volatile environments. The impact of these market-based risks, often beyond a firm’s control, hinder access to capital markets and creating liquidity shortages (Pástor & Veronesi, 2013). As a result, firms adopt conservative CHs strategies to mitigate the adverse effects of unpredictable FC (Acharya et al., 2007). Empirical evidence supports the view that heightened Mν (market volatility) compels firms to foster their CHs, as a buffer against the operational disruption. For instance, Gao et al. (2017) documented that firms avoid investing during elevated systematic uncertainty (implied volatility of the S&P index), and augment CHs to seize future investment opportunities. Tran (2020) noted that firms in emerging markets strengthen CHs during economic crises due to limited funding options. Although China has active capital markets and a large banking system, its financial system continues to face institutional inefficiencies and uneven financial access. Such insufficient developments result in higher transaction costs and impede firms’ ability to obtain outside funding, particularly during volatile market situations. Consistent with institutional theory, these constraints reinforce firm’s dependency on CHs as a substitute for imperfect markets. Based on the arguments and literature review, we postulate the following hypothesis:

Economic Policy Uncertainty (Epν)

Epν denotes unpredictability in government policies stemming from political shifts and regulatory changes (Baker et al., 2016). Previous research shows that elevated Epν leads firms to increase precautionary CHs (Chen et al., 2023), as a hedging strategy against risks (Demir & Ersan, 2017). Epν also lowers asset returns and exacerbate FC, significantly impacting firms’ CHs behavior (Gong et al., 2024; Tran, 2023). Particularly, in the context of China, where state’s predominant role in the economic matters and the regular variations in fiscal and regulatory structures are common, firms significantly adjust their CHs in response to elevated Epν (Phan et al., 2019) to mitigate the possible adverse effects of abrupt policy alterations, such as modifications in taxation or government expenditure priorities.

N. Xu et al. (2016) suggest that the political landscape heavily influences financial decisions, with firms accumulating more CHs during periods of heightened Epν. Recently, Zhao and Niu (2023) also report the positive Epν-CHs nexus and identify capital expenditure as a key mechanism passing through the impact of Epν on CHs. Chen et al. (2023) observed that higher Epν significantly impact business conditions, leading firms to accumulate CHs to deal with unpredictable regulatory environments. This tendency aligns with the precautionary motive theory, which asserts that firms foster CHs to prepare for unforeseen events that could impact their financial health (Opler et al., 1999). Institutional perspectives also suggest that this behavior is more pronounced in emerging economies like China, where government intervention and policy uncertainty are prevalent. Political influence further complicates this relationship; politically connected firms may retain more CHs as a hedge against shifts in government priorities or as “insurance” against rent extraction (Lou et al., 2021). Based on the arguments and literature review, we postulate the following hypothesis:

Moderating Role of Firm-Specific Characteristics

Moderating Role of Ownership Structure (Private)

The ownership structure significantly impacts corporate CHs strategies. In China, the distinction between SOEs and private firms has a substantial impact on resiliency and financial stability. Due to government backing in the provision of resources, SOEs have easier access to external financing and are better equipped than private firms to deal with economic downturns (Feng et al., 2022). SOEs enjoy substantial government backing, through preferential loans and subsidies, and privileged access to policy information, providing them a strategic advantage in managing risks (Liu et al., 2021). This support lessens their requirement for precautionary CHs in unpredictable times (Tran et al., 2024). Private firms, on the other hand, often depend on internal CHs more than SOEs (Nguyen et al., 2022). Research indicates that private firms suffer more financing issues, prompting them to foster CHs as a buffer against uncertainty (Chen et al., 2018). Thus, ownership structure provides an institutional lens moderating the uncertainty–CHs nexus. Based on the arguments and literature review, we postulate the following hypothesis:

Moderating Role of Financial Constraints (FC)

FC denotes a firm’s challenges in securing favorable external financing, which often result in increased CHs. Firms facing difficulties in seizing external financing, particularly under uncertainty, are forced to rely on internal financing for their survival and investment activities. In such situations, firms maintain large CHs to meet their funding needs, especially when external capital markets are costly or inaccessible. Evidence suggests that this heavy dependence on internal cash reserves is particularly significant among FC firms, especially those operating in less developed financial markets (Nguyen et al., 2022). This phenomenon is driven by precautionary motives, as firms tend to increase CHs to safeguard against potential financing difficulties (Dudley & Zhang, 2016). Additionally, heightened uncertainty exacerbates external financing cost, which further aggravates asymmetric information (Crisóstomo et al., 2014; Myers & Majluf, 1984), leading firms to prioritize CHs for potential investment opportunities (Almeida et al., 2004; Nguyen et al., 2022). In the context of China, research has documented the positive association between FC and CHs during uncertain times. The findings by Feng et al. (2022) suggest that during phases of elevated Epν, increasing CHs serve as a protective measure for FC firms. This aligns with both precautionary and pecking order theories, emphasizing that FC magnifies firms’ reliance on internal liquidity. Based on the arguments and literature review, we postulate the following hypothesis:

Moderating Role of Trade Credit (TC)

TC, or short-term borrowing and lending between suppliers and buyers, is a significant source of funding and investment for firms. TC denotes the credit extended by suppliers to firms. TC permits firms to defer payments to suppliers and acts as a financing tool to alleviate liquidity problems. Strong relationships with suppliers enable firms to rely on TC during periods of heightened uncertainties, which reduce the need for CHs. Previous research indicates that TC offers a viable liquidity alternative, provides firms with a form of short-term financing, thus diminishing their dependence on CHs (Ng et al., 1999). This aligns with the institutional perspective, showing that informal financial channels (TC) substitute for cash in emerging economies. Due to China’s low level of financial development, many firms encounter difficulties funding their operational and financing requirements through commercial bank loans and progressively rely on informal financial systems such as TC (Khan et al., 2019). Studies argue that TC is a frequently employed financial tool in Chinese enterprises to fund their growth prospects (Ge & Qiu, 2007; Zhang et al., 2015), specifically for firms in industries that have limited liquidity. Firms with established TC connections retain lower CHs, relying on TC as a reliable liquidity source, particularly during uncertain times. Based on the arguments and literature review, we postulate the following hypothesis:

Figure 1 presents a conceptual framework of the aforementioned proposed hypotheses.

Conceptual framework.

Data and Methodology

Data

This study examines manufacturing (A-share) listed firms (2003–2023), classifying the industry per the China Securities Regulatory Commission’s 2012 guidelines. This study focuses on the manufacturing sector because it significantly contributes to China’s GDP and industrial output, ensuring our findings have substantial economic relevance. Furthermore, these firms are highly vulnerable to domestic and global uncertainties due to their dependence on complex supply chains and capital-intensive operations. Moreover, narrowing to a single sector reduces industry heterogeneity that could obscure the effects of uncertainties on CHs. The financial statistics of the firms are retrieved from the CSMAR database. Special treatment (ST) firms, financial firms, and firms with missing data are excluded. Outliers are addressed by winsorization. The study considers firms with data spanning at least three consecutive years, employing the two-step system GMM method to properly instrument endogenous variables.

Variables Measurement

Dependent Variable

This study employs firm CHs as the dependent variable. In line with Jebran et al. (2019), and Feng et al. (2022), we define CHs as the ratio of cash and cash equivalents to total assets. To ensure robustness, following Itzkowitz (2013) and Jebran et al. (2019), we also employed an alternative measure of CHs, specifically, we define CHs as the natural logarithm of one plus the ratio of cash and cash equivalents to total assets. This transformation mitigates potential skewness in the CHs variable and improves the reliability of the regression analysis

Explanatory Variables

This study examines three distinct forms of uncertainty—firm-specific (Fsν), market-based (Mν), and economic policy uncertainty (Epν)—selected for their critical relevance to corporate decision-making processes and their unique contributions to influencing firm CHs. These uncertainties encompass internal organizational dynamics, external market conditions, and macroeconomic policy shifts, collectively providing an ample framework for understanding their multifaceted impacts on corporate strategies and CHs.

Firm-Specific Uncertainty (Fsν)

Fsν represents uncertainty stemming from internal organizational factors, significantly impacting resource allocation processes. This study quantifies Fsν by calculating the moving standard deviation of residuals derived from an AR(1) model of sales. A rolling five-period window is employed, requiring a minimum of 3 years of residual data to ensure robust estimates (Bo & Zhang, 2002; Khan et al., 2025; Khan, Qin, Jebran, & Ullah, 2020).

Market-Based Uncertainty (Mν)

Mν reflects the uncertainty stemming from external market dynamics, including stock market fluctuations and macroeconomic factors influencing firms across industries. This dimension of uncertainty is particularly relevant as it encapsulates broader economic forces and external financial risks that influence firm-level strategic decisions. Mν is estimated using a GARCH model, employing annual data on Chinese stock market returns from 2003 to 2023. The GARCH-derived conditional variance is used as a proxy for Mν, following methodologies outlined in prior research (Khan et al., 2019; Khan, Qin, Jebran, & Ullah, 2020; Wang et al., 2017).

Economic Policy Uncertainty (Epν)

Epν captures uncertainty arising from changes in government policies, regulations, and macroeconomic strategies, which substantially influence firms’ strategic planning, particularly in economies with significant state involvement. This study employed the BBD index of Baker et al. (2016) to quantify Epν, which aggregates indicators such as policy-related news, tax code provisions, and forecaster disagreements. The BBD index has been widely adopted as a reliable proxy for Epν in research (Das et al., 2024; Ur Rahman et al., 2023; B. Xu et al., 2021; Zhao & Niu, 2023). We utilize the BBD index to measure Epν for China, transforming monthly data into annualized values by calculating their arithmetic mean, thereby providing a comprehensive metric of policy-related uncertainty.

Econometric Model

This research opts for three estimation approaches: pooled OLS, fixed-effect (FE) panel regressions, and robust two-step system-GMM to analyze the uncertainty–CHs nexus, addressing the endogeneity concerns. Robust standard errors are applied to ensure the reliability of results. We formulate Equation 2 to test H1.

where Cash signifies firm CHs. Uncertainty includes three forms: Fsν, Mν, and Epν. Additional control variables (SG, Size, Roa, TQ, Lev, Age, RD, CF, and Tang) are included to account for potential influences on CHs (See variables’ definitions in Table A1). Industry and year-fixed effects address potential selection bias stemming from unobservable variables, with ε_it representing the error term.

Equation 3 is constructed to test H2, the moderating influence of private ownership on the uncertainty–CHs nexus, using a binary dummy variable, denoted as Private, set to one for state-owned companies and zero for private-owned. Controls refer to a set of control variables: SG, Size, Roa, TQ, Lev, Age, RD, CF, and Tang.

The moderating influence of FC on the uncertainty–CHs nexus is shown by Equation 4 to test H3. Following the literature (Arif Khan et al., 2023; Wu & Huang, 2022), FC is computed by the KZ index (Kaplan & Zingales, 1997).

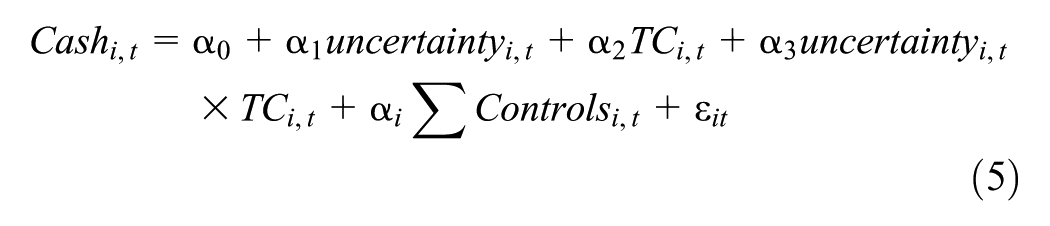

The moderating influence of TC on the uncertainty–CHs nexus is shown by Equation 5 to test H4. TC is computed as the ratio of accounts payable to total assets (Khan, Qin, Jebran, 2020; Zhang et al., 2015).

Results and Discussion

Descriptive Statistics

Table 1 describes the data used in our study. The mean (SD) value of cash is 0.1706 (0.1246), indicating that on average the sample firms hold 17.06% of their total assets as cash, with a SD of 12.46%. In addition, the mean (SD) values of different forms of uncertainties, including Fsν, Mν, and Epν, are 0.1558 (0.1652), −0.0412 (0.5835), and 172.2322 (113.8939), respectively. To check multicollinearity issues, we estimated the VIF. The maximum VIF value is 1.54, which indicates no or low multicollinearity concerns.

Summary Statistics.

Note. The variables’ summary statistics are reported in this table. Corporate cash holdings are represented by Cash, computed as cash and cash equivalents normalized by total assets. Fsν, Mν, and Epν show firm-specific, market-based, and economic policy uncertainty, respectively. SG shows firm sales growth. Size represents the firm’s size in terms of total assets. Roa is the return on assets. TQ represents Tobin’s Q ratio. Lev denotes the total debts to total assets ratio. Age represents the company’s age from its inception year. RD denotes spending on R&D divided by total sales. CF is the cash flow ratio. Tang is the tangible assets ratio to total assets.

Regression Analysis of Uncertainty and Corporate Cash Holdings

Table 2 presents the regression results for CHs and a set of explanatory variables across five models, progressively including each type of uncertainty in the preceding columns. In Column (1), we regress CHs on the control variables alone. The results are broadly aligned with previous research. The inverse impact of SG (Bates et al., 2009), Size (Demir & Ersan, 2017) and Lev (Uyar & Kuzey, 2014) on CHs, indicates that firms with higher sales growth, large size, older age, or high debt obligations significantly diminish CHs, possibly because they prefer reinvesting their cash and due to easier access, rely more on external funding. Tang also exhibits a significantly negative impact on CHs (Uyar & Kuzey, 2014), indicating that firms with more tangible assets maintain lower cash reserves, as these assets can be used as collateral to obtain financing, reducing the need to amplify CHs. Moreover, high debt obligations prompt firms to distribute cash for debt repayment. The positive impact of Roa (Opler et al., 1999), TQ (Duong et al., 2020), and CF (Almeida et al., 2004) on CHs advocates that more profitable firms, an increase in internal funds from the previous period, and firms with better growth prospects are inclined to foster CHs as a precautionary motive to reduce external financing costs and seize lucrative investment prospects.

Uncertainties and Corporate Cash Holdings.

Note. Table A1 defines the variables. Robust SE, clustered at the firm level, are in parentheses.

p < .1. **p < .05. ***p < .01.

Column (2) of Table 2 presents the results for Fsν. The coefficient on Fsν is statistically significant (at 1%) and positive (0.0368), indicating that a one SD increase in Fsν raises CHs by 3.68% points of assets. This supports H1a. The magnitude implies that in industries with higher Fsν (such as operational risks, sales volatility, and more idiosyncratic risks), companies commit nearly 3.68% of their assets to liquidity buffers, which can reduce investments in R&D, innovation, and expansion. The findings support the precautionary motive approach, which predicts firms amplify CHs as a buffer against internal volatility. Our results corroborate prior empirical evidence in Chinese firms (Bates et al., 2009; Gao et al., 2013; Liu & Wang, 2021; Xian et al., 2024). Our findings confirm that in volatile industries, firms treat CHs as a strategic shield.

Column (3) of Table 2 presents the results for Mν. The coefficient on Mν is also statistically significant (at 1%) and positive (0.0025), indicating that a one SD increase in Mν raises CHs by 0.25% points of assets. While the magnitude is smaller than Fsν, the effect is meaningful. This supports H1b. This indicates that firms amplify CHs when exposed to external market volatility. Mν is beyond managerial control and can disrupt access to capital markets. Consistent withthe precautionary motive and institutional theory (North, 1990; Tran, 2020), firms respond to market and macroeconomic fluctuations by increasing their CHs to mitigate operational disruptions These findings are also align with prior empirical studies showing that high level of systematic uncertainty considerably limit access to external financing, prompting them to boost CHs (Acharya et al., 2013; Gao et al., 2017). Importantly, the findings highlight the managerial biased dimension (Chen et al., 2020; Lou et al., 2021), such as managers may overreact to Mν by amplifying CHs even if FC are temporary.

Column (4) presents the results for Epν. The coefficient on Epν is 0.0001 (p < .0001). This supports H1c. In practical terms, even a modest increase in Epν leads firms to commit an additional amount of their assets to cash buffers, which may divert funds from productive activities such as R&D, thereby affecting long-run competitiveness. The results are in line with precautionary motive and institutional theory (North, 1990). Institutional perspectives suggest that this behavior is more pronounced in emerging economies like China, where government intervention and policy uncertainty are prevalent. Our results corroborate prior empirical evidence. Previous research shows that firms facing elevated Epν tend to amplify CHs as a precautionary measure (Chen et al., 2023), to manage challenges like rising borrowing costs and restricted access to external financing (Bates et al., 2009).

Finally, Column (5) shows results for the combined effects of all uncertainties and control variables. The results suggest that the coefficients for all types of uncertainties remain positive and significant, demonstrating that firms respond to multiple uncertainty dimensions collectively rather than in isolation. This supports the idea that firms increase CHs when faced with greater uncertainty. Therefore, firms should consider all forms of uncertainty together when making decisions on CHs, instead of looking at each type separately.

Moderating Role of Ownership Structure

Table 3 reports the results of the moderating role of firm ownership. The findings show that all forms of uncertainties (Fsν, Mν, and Epν) uphold their effect on CHs with significant and positive coefficients, confirming H1a–H1c and prior findings as reported in Table 2. Furthermore, the interaction terms of all forms of uncertainties and private firms (Fsν × Private, Mν × Private, Epν × Private) are also significant and positive with CHs, indicating that private firms significantly exacerbate the positive nexus between uncertainties and CHs. These results support H2.

Moderating Influence of Private Ownership.

Note. Table A1 defines the variables. Robust SE, clustered at the firm level, are in parentheses.

p < .1. **p < .05. ***p < .01.

The results reinforce both institutional theory, which highlights the role of ownership structures in shaping liquidity management under uncertainty, and the precautionary motive. SOEs enjoy substantial government backing, through preferential loans and subsidies, and privileged access to policy information, providing them a strategic advantage in managing risks (Liu et al., 2021). Private firms, on the other hand, often face greater FC that push them to precautionary maintain more CHs as a liquidity buffer (Almeida et al., 2004; Gao et al., 2013). Figures 2 to 4 illustrate the moderating effect of private ownership on the relationship between different types of uncertainty (Fsν, Mν, and Epν) and corporate cash holdings.

Moderating effect of private ownership on the relationship between Fsν and Cash holdings.

Moderating effect of private ownership on the relationship between Mν and Cash holdings.

Moderating effect of private ownership on the relationship between Epν and Cash holdings.

Moderating Role of Financial Constraints

Table 4 reports the results for the moderating role of FC. The findings show that all forms of uncertainties (Fsν, Mν, and Epν) uphold their effect on CHs with all significant and positive coefficients, confirming H1a–H1c and prior findings as reported in Table 2. Furthermore, the interaction terms of all forms of uncertainties and FC (Fsν × FC, Mν × FC, Epν × FC) are significant and positive, indicating that FC firms significantly exacerbate the positive nexus between uncertainties and CHs. These results support H3 and previous research (Almeida et al., 2004; Dudley & Zhang, 2016; Feng et al., 2022). In line with precautionary and agency theories, FC firms amplify CHs as an internal financial substitute. This suggests that FC firms may shift resources away from long-term projects in order to maintain immediate liquidity cushions, resulting in inefficient CHs. Constrained managers could rationalize increased CHs as precautionary measures, but a lack of shareholder monitoring in uncertain circumstances can lead to entrenchment or inefficient CHs. Figures 5 to 7 illustrate the moderating effect of FC on the relationship between different types of uncertainty (Fsν, Mν, and Epν and corporate cash holdings.

Moderating Influence of Financial Constraints.

Note. Table A1 defines the variables. Robust SE, clustered at the firm level, are in parentheses.

p < .1. **p < .05. ***p < .01.

Moderating effect of FC on the relationship between Fsν and Cash holdings.

Moderating effect of FC on the relationship between Mν and Cash holdings.

Moderating effect of FC on the relationship between Epν and Cash holdings.

Moderating Role of Trade Credit

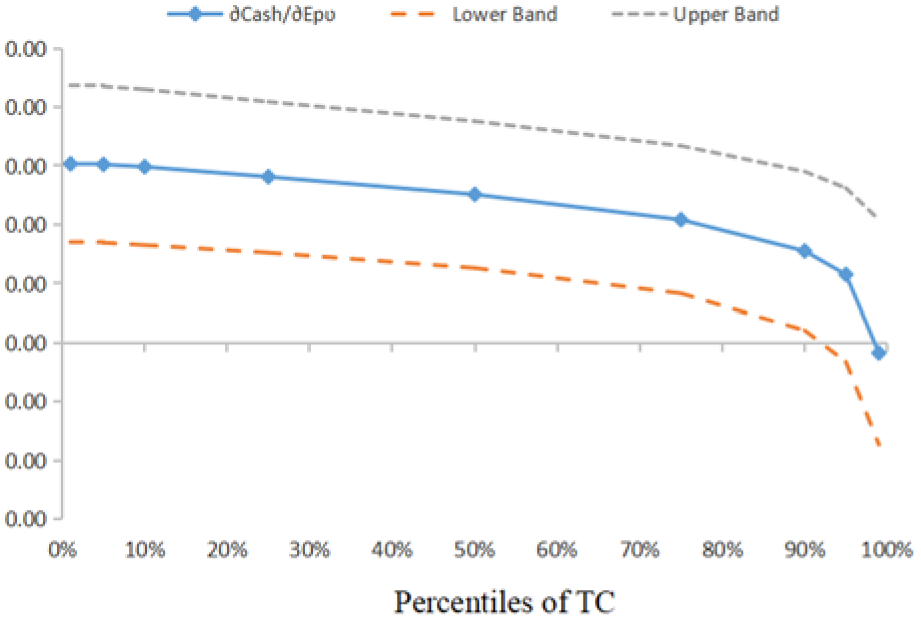

Table 5 reports the results for the moderating role of TC. The findings confirm H1a to H1c and prior findings as reported in Table 2. Furthermore, the interaction terms (Fsν × TC, Mν × TC, Epν × TC) are significant but negative, demonstrating that firms with greater access to TC reduce CHs when facing heightened uncertainty. These results support H4 and align with the institutional perspective. TC acts as an alternative liquidity channel, providing firms with a form of short-term financing, thus diminishing their dependence on CHs (Ng et al., 1999). This underscores the substitution effect, showing that in emerging economies, informal financing (TC) substitutes for formal cash buffers, particularly under uncertainty (Khan et al., 2019; Zhang et al., 2015). Figures 8 to 10 illustrate the moderating effect of TC on the relationship between different types of uncertainty (Fsν, Mν, and Epν and corporate cash holdings.

Moderating Influence of Trade Credit.

Note. Table A1 defines the variables. Robust SE, clustered at the firm level, are in parentheses.

p < .1. **p < .05. ***p < .01.

Moderating effect of TC on the relationship between Fsν and Cash holdings.

Moderating effect of TC on the relationship between Mν and Cash holdings.

Moderating effect of TC on the relationship between Epν and Cash holdings.

Robustness Analysis

To ensure the robustness of our findings, we perform some additional tests, including alternative measure of CHs and alternative estimation techniques, that is, fixed effect (FE) model and GMM.

Alternative Measure of Cash Holdings

To ensure robustness, the study adopts an alternative measure of CHs as the natural logarithm of one plus the ratio of cash and cash equivalents to total assets, following Itzkowitz (2013) and Jebran et al. (2019). The findings are presented in Table 6. As expected, the findings for the alternative measure remain consistent, with significant positive coefficients on all forms of uncertainties (Fsν, Mν, and Epν), reinforcing the robustness of the previous findings.

Robustness Test Using Alternative Measure of Cash Holdings.

Note. Table A1 defines the variables. Robust SE, clustered at the firm level, are in parentheses.

p < .1. **p < .05. ***p < .01.

Fixed-Effect Model

We re-estimate our main model using the FE model, which accounts for unobserved firm-specific effects. The results presented in Table 7’s Columns (1), (2), and (3) demonstrate that uncertainties have a detrimental effect on CHs. These findings are in line with those displayed in Table 2. The results indicate that even after adjusting for firm-specific characteristics, the uncertainty–CHs nexus still exists.

Robustness Test Using Fixed Effect Model.

Note. Table A1 defines the variables. Robust SE, clustered at the firm level, are in parentheses.

*p < .05. ***p < .01.

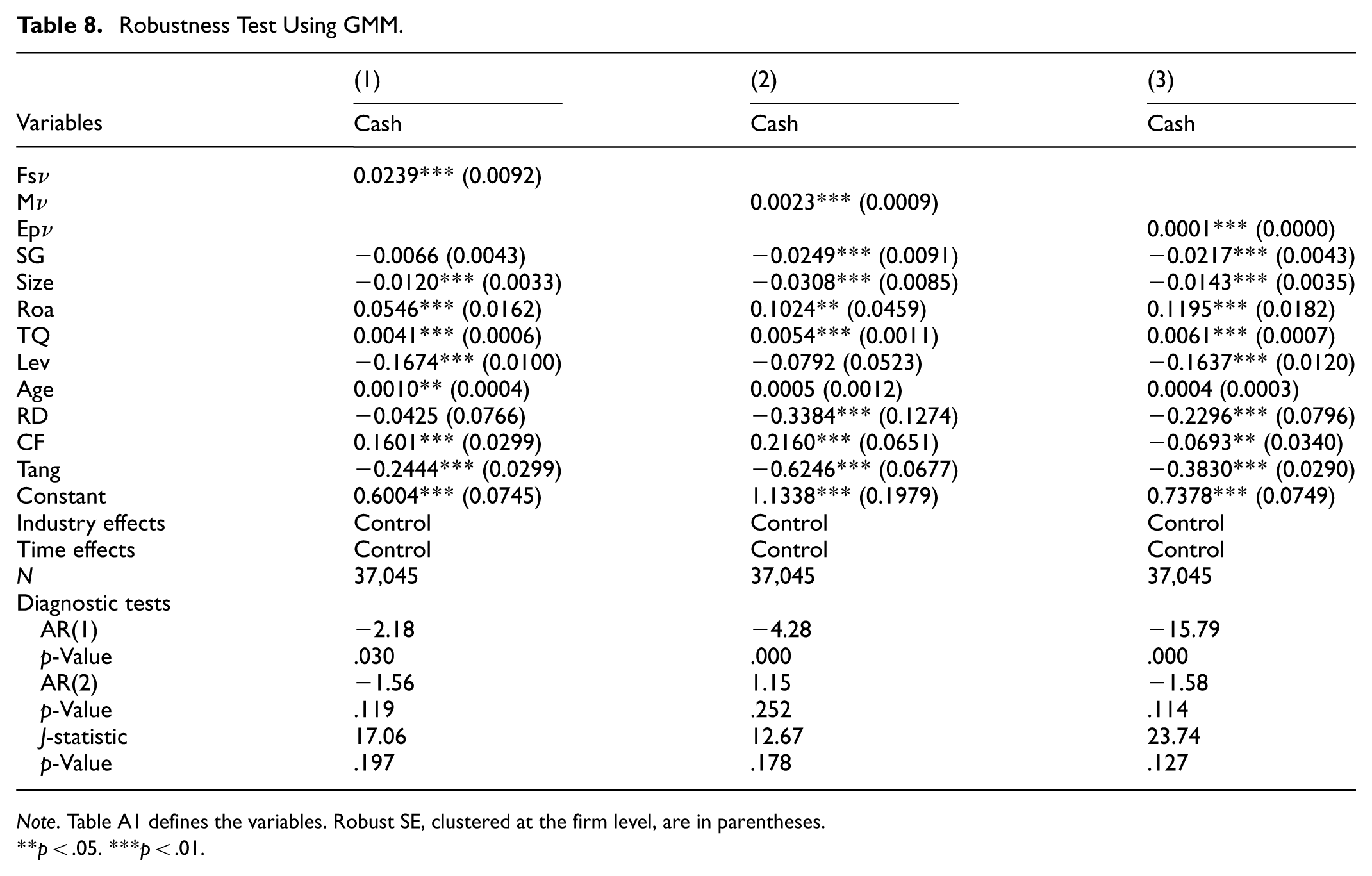

GMM

Finally, we used a two-step system GMM to deal with endogeneity issues (Ullah et al., 2025; Zeb et al., 2024). GMM is an effective technique because it combines observed economic statistics with information about population moment conditions to provide accurate estimates of unknown parameters. The findings presented in Table 8 demonstrate that uncertainties have a positive impact on CHs, corroborating the findings in Table 2. Even after controlling for endogeneity, firm-specific factors, and alternative CHs proxies, the consistent results across these multiple metrics and models support the survival of the positive uncertainty–CHs relationship. As a result, we get similar findings after re-estimating the baseline models. Overall, the reported results are strong, and our findings are unaffected by the endogeneity issue.

Robustness Test Using GMM.

Note. Table A1 defines the variables. Robust SE, clustered at the firm level, are in parentheses.

*p < .05. ***p < .01.

Overall Discussions

The results of this study reinforce the pivotal role of uncertainty in shaping CHs practices in the Chinese economy. The baseline results confirm H1a–H1c, showing that Fsν, Mν, and Epν, each lead to higher CHs, consistent with the precautionary motive and institutional theory. The empirical findings suggest that CHs act as a risk management tool for firms to safeguard their financial stability in the face of various types of uncertainties. In response to uncertainty, whether from internal operational risks, market volatility, or uncertain economic policies, firms increase their CHs to alleviate risks. Importantly, the magnitude of the coefficients has practical implications. For instance, a one SD increase in Fsν raises CHs by 3.68% points of assets, suggesting that uncertainty is not just a statistical driver but a meaningful determinant of treasury policy. In practice, such an increase can translate into millions of yuan in additional idle liquidity, affecting firms’ capacity for investment, innovation, and long-term projects.

These results also resonate with prior work while extending it in important ways. For instance, consistent with Harford et al. (2008) and Chen et al. (2018), we find that uncertainty drives higher CHs; however, our analysis demonstrates that the magnitude of this effect depends critically on firm-specific moderating factors. The moderating effects (H2a–H2c) highlight how ownership, FC, and TC credit availability shape CHs strategies under uncertainty. The moderating effects suggest that uncertainty does not impact all firms unifromly. This perspective is supported by previous evidence (Attig et al., 2021; El Ghoul et al., 2023), who demonstrate that governance and financial flexibility influence liquidity decisions. Recognizing this variability helps prevent confirmation bias and avoids overstating a single theoretical mechanism.

Conclusion

This study investigates the influence of different forms of uncertainty (Fsν, Mν, and Epν) on corporate CHs in Chinese manufacturing firms, with a particular focus on the moderating role of firms’ ownership structure, FC, and access to TC. This study shows that higher uncertainty (Fsν, Mν, and Epν) leads to elevated CHs, consistent with precautionary and institutional perspectives. The results suggest that CHs act as a risk management tool for firms to safeguard their financial stability in the face of various types of uncertainties. Furthermore, the moderating effects demonstrate that the influence of uncertainty on CHs varies depending on ownership structures and financing conditions, suggesting that firms exhibit heterogeneous responses based on their unique circumstances, highlighting that CHs policies are shaped not only by external shocks but also by internal financing and governance conditions. Together, these findings support the hypotheses put forth and add to the body of knowledge by demonstrating how various aspects of uncertainty interact with firm attributes to influence corporate CHs policies. Robustness checks, including the use of alternative measures of CHs, FE model, and GMM, confirm the validity of our results.

Policy Implications

The findings provide powerful insights for practitioners and policymakers. Managers should prioritize building precautionary CHs during heightened uncertainty, while being cautious of the risks associated with excessive CHs. Investors ought to view increased CHs as a strategic response to uncertainty, particularly in volatile emerging markets. Policymakers must recognize that weak financial markets intensify firms’ reliance on CHs. This calls for urgent policies that enhance credit access, strengthen investor protections, and improve financial infrastructure, linking corporate finance theory to effective decision-making in unpredictable environments.

The findings also offer several theoretical contributions. First, the positive uncertainty-CHs nexus supports the precautionary motive, as firms accumulate CHs to buffer against unpredictable shocks. Second, the moderating effect of ownership structure and TC advances the institutional and managerial bias perspectives, suggesting that firms adapt CHs management strategies in line with prevailing financing norms, governance structure, and managerial discretion. Third, the significant role of FC aligns with agency theory, indicating that financial limitations influence precautionary behavior. Overall, these insights enrich contingency-based theory by showing that the effect of uncertainty on CHs is not uniform but contingent upon firm-level and institutional factors.

Research Limitations

The study has significant restrictions. First, the sample is limited to Chinese manufacturing firms, potentially limiting the implications of these results to other sectors such as technology and services. Second, even though widely used proxies for uncertainty were employed, other metrics, such as survey-based indices, might offer more information. Lastly, even with FE and GMM estimations, potential endogeneity and omitted variable bias—such as managerial risk preferences—may still have an impact on the findings.

In conclusion, we recognize that our interpretations may still be affected by confirmation bias, as existing theories often emphasize precautionary motives. Additionally, the relationship between uncertainty and cash may vary depending on different institutional settings or governance structures. This underscores the importance of exploring contextual differences in future studies.

Future Research Directions

Future research should incorporate cross-country comparisons and sector-specific analysis to understand further how institutional and sectoral differences affect the uncertainty-CHs nexus across developed and emerging economies. Comparing different sectors might help identify whether factors like capital intensity, competition, or supply chain complexity influence the effects of uncertainty differently across industries. Further research could also include qualitative aspects, such as the processes involved in board decision-making, to enhance our understanding of the behavioral mechanisms related to liquidity management. Additionally, investigating alternative uncertainty measures, the impact of managerial attributes in liquidity decisions, the influence of ESG concerns, and climate policy uncertainties on CHs will provide useful insights. Our understanding could be further improved by longitudinal studies that monitor these processes throughout time.

Footnotes

Appendix

Variable Definitions.

| Symbol | Variable | Definition |

|---|---|---|

| Cash | Cash holdings | Cash and cash equivalents over total assets. |

| Fsν | Firm-specific uncertainty | Measured as the moving standard deviation of the residuals derived from anAR(1) model of sales, calculated over a 5-year rolling window, with a minimum requirement }of 3 years of residual observations for computation. |

| Mν | Market-based uncertainty | To compute M-u, the conditional variance of stock market returns is estimated using the ARCH/GARCH framework over the sample period. |

| Epν | Economic policy uncertainty | BBD index is employed to measure Ep-u. |

| SG | Sales growth | The growth rate of firms’ sales. |

| Size | Firm size | Natural logarithm of total assets. |

| Roa | Profitability | The sum of total profits and financial expenses divided by total assets. |

| TQ | Tobin’s Q | The ratio of the market value of equity plus total liabilities to lagged total assets |

| Lev | Leverage | Total liabilities over total assets. |

| Age | Firm age | Firm age since the inception year. |

| RD | Research & development | R&D divided by total sales. |

| CF | Cash flow ratio | Firms’ net profits plus depreciation & amortization normalized by total assets. |

| Tang | Tangibility | The ratio of tangible assets to total assets. |

Acknowledgements

We thank the editor and anonymous reviewers for their constructive comments and suggestions.

Ethical Considerations

Ethical permission is not applied because this research does not include any human or animal study.

Consent to Participate

Informed Consent is not applied because this research does not include any human study participants.

Authors’ Contributions

Muhammad Arif Khan: Conceptualization; Data curation; Methodology; Formal Analysis; and Writing—review & editing. Mohib Ur Rahman: Project Administration; Supervision; Data Curation; and Methodology; Writing—original draft. Rameez Kashmeri: Validation; Software; and Writing—original draft.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

Data will be made available upon request.