Abstract

The present study aims to explore the effect of equity incentive intensity on defensive behavior in enterprise cash holding decision-making using ordinary least squares, System GMM, and Heckman tests. This study finds that the higher the intensity of equity incentives, the lower the level of corporate excess cash holdings. The intensity of equity incentives inhibits defensive behavior in corporate cash holding decisions. A substitute relationship is observed between equity incentive intensity and product market competition in the inhibition of management defensive behavior in cash holding decision. Our further research finds that the inhibitory effect of equity incentive intensity on the defensive behavior of cash holding decisions mainly exists in the case of ineffective supervision by large shareholders and creditors. For theoretical contribution, this paper tries to explore the governance effect of equity incentive on the management defensive behavior in a company’s cash holding decision making. It also reveals the substitute relationship between the intensity of equity incentive and the product market competition in suppressing the management defensive behavior in the cash holding decision of enterprises. Moreover, it provides new evidence for the governance effect of equity incentive in the institutional environment and expands the literature on equity incentive effects.

Introduction

Management defensive behavior refers to the behavior of operators choose to stick to the position and strives to maximize their self-utility when they are under pressure and threats from the inside and outside of the enterprise they are working in (Ye et al., 2018). Modern enterprises have brought a series of agency problems owing to the prevalence of separation of two rights. Accordingly, they have also caused a large amount of agency costs. Information-dominant operators are usually in a favorable position to become the main body of control of enterprises. Coupled with the asymmetry of information, conducting comprehensive and thorough supervision of the operator with superior information is difficult for the owner. A rational operator will use the control in his hand to engage in opportunistic behavior for private gain, and the resulting management defensive behavior will bring serious damage to the shareholder value. Although shareholders authorize business operators to engage in business activities in the form of contracts to achieve their own interests, in the real economy, contracts are often incomplete. A company’s cash holding decisions often deviate from the Pareto optimal state owing to the interference of various factors (Caprio et al., 2020). Correcting them using the internal or external alternative mechanisms of the enterprise is necessary. The operator’s equity incentive system is an important alternative mechanism, as demonstrated by extensive research and successful practice (Drakos & Bekiris, 2010; Lv et al., 2009; Pan & Shen, 2021).

Systematic and in-depth research on whether equity incentive mechanism can inhibit the defensive behavior in corporate cash holding decision making is lacking. The small number of scattered empirical research conclusions have also not yet reached an agreement. Both situations provide an opportunity for this study. This study first analyses the relationship between the intensity of equity incentive and the defensive behavior in the decision making of enterprise cash holding. It then further discusses the influence of the two aspects of governance power, namely, the supervision of the internal governance subject and the product market competition outside the company, on the relationship between equity incentive and the defensive behavior in the decision making of enterprise cash holding.

Equity incentive is chosen to examine the company’s cash holding problem on the basis of the following considerations: Firstly, in recent years, the increasingly severe phenomenon of high cash holdings and cash resource erosion of listed companies has incited much discussion in the academic field (Yu et al., 2017). As an asset that is easily wasted by the management, the cash holding decision is an important part of the financial decision making of an enterprise, and the management defensive behavior of the operator plays a decisive role in such decision making. Secondly, Jensen (1986) pointed out that an important factor for the aggravation of agency conflict between owners and operators is that the company holds a large number of liquid assets, and cash is the most liquid asset among all the assets. The decision of cash holding and using is highly controlled and easily eroded by the operator. Therefore, the decision of cash holding and using often reflects the manager’s motivation directly, which has an extremely significant impact on the efficiency of capital use and even the value of enterprise. By examining the impact of equity incentive on cash holding decision, we can not only grasp the main content of corporate governance on corporate financial decision making but also fully consider the impact of institutional factors on corporate governance efficiency (Ye et al., 2020). Thirdly, cash holdings fluctuate greatly in different periods, whereas the corporate governance level of enterprise equity incentive system is relatively stable. In this way, verifying the influence of manager’s defensive behavior on cash holding decision under different corporate governance conditions is convenient (Bharadwaj et al., 2020; Nienhaus, 2021).

To this end, many questions arise in this situation. Will the defensive behavior in corporate cash holding decision making be affected by equity incentives? another question also related to this issue is, If there is an impact, how does it vary under different constraints (e.g. different governance subjects supervising and product market competitions)? Accordingly, the present study looks at the effect of equity incentive under different conditions. Such knowledge is conducive to a comprehensive understanding of the efficiency of equity incentive contracts in restricting the management of defensive opportunistic behavior. This study also provides empirical enlightenment for practical reforms such as the promotion of equity incentives and the improvement of corporate governance efficiency.

The significance of this study focuses on three aspects. Firstly, the study enriches research on the economic consequences of equity incentives. Numerous studies have shown that the implementation of equity incentives has an impact on the value of companies (Long & Huang, 2020; Su & Alexiou, 2019). This study explores how the intensity of equity incentives acts on the dynamic adjustment of the company’s cash holding decisions when the company’s operating status changes, revealing a path behind the following effects: the strength of equity incentives inhibits the defensive behavior in the company’s cash holding decisions, which is conducive to the improvement of corporate value. This study also combines the supervision of governance entities and the different situations of product market competition to conduct a deeper discussion. The results show differences in the role of equity incentives under different circumstances, which deepens the understanding of the effect of equity incentives under different conditions.

Secondly, the study adds new evidence to the exploration of influencing factors of management defensive behavior in corporate cash holding decisions. Given that equity incentives have been implemented in Western countries for a long time, the impact of equity incentives on agency costs and management defensives seems self-evident. However, in the context of China, equity incentives are just emerging, and the level of corporate governance is relatively low, so controversy is ongoing about whether the welfare effect in equity incentives is more dominant (Lv et al., 2009; Xiao & Chen, 2013). This study shows that the overall intensity of equity incentives has a restraining effect on the management defensive behavior in cash holding decision making. It affirms the positive value of equity incentives in the context of China’s reality and expands the research on the influencing factors of management defensive behavior in the cash holding decisions of enterprises in the context of non-Western countries.

Thirdly, the study provides practical inspiration for reforms such as improving the management efficiency of state-owned enterprises (SOEs) and promoting equity incentives. The current situation of management defensive behavior and management inefficiency in corporate cash holding decisions is largely due to the opportunistic motivation of management. However, at present, equity incentives in non-SOEs are developing rapidly, and SOEs are more cautious about them (Xiao & Chen, 2013). Where conditions permit, the introduction of equity incentives in SOEs can help inhibit management defensive behavior and improve the efficiency of cash holding decisions (Liu et al., 2018; Ye et al., 2020). This study shows that in industries with insufficient supervision by major shareholders and weak product market competition, the implementation of equity incentives may be more necessary and more effective. Given the further withdrawal of state-owned capital in China’s future mixed-ownership reforms, the role of equity incentives will become increasingly important (Y. W. Chen et al., 2019).

The contribution of this study to the existing literature lies in two areas. (a) To suppress the negative effect of management defensive behavior, the governance effect of equity incentive on management defensive behavior in corporate cash holding decision is studied from the perspective of corporate governance. This study reveals the substitute relationship between equity incentive intensity and product market competition in restraining management defensive behavior in corporate cash holding decision. It is helpful to fully understand the efficiency of equity incentive contract in restricting management and defending opportunistic behavior so as to enrich the research on corporate governance theory and provide reference for the policy orientation of government supervision and design of enterprise equity incentive mechanism. (b) Further research finds that the inhibitory effect of equity incentive intensity on defensive behavior in cash holding decision making mainly exists in the case of weak supervision by major shareholders and creditors. This study thus provides new evidence for the governance effect of equity incentive affected by institutional environment and expands the literature on the effect of equity incentive.

Literature Review and Research Hypothesis

Institutional Background of Equity Incentives

Equity incentive is a long-term incentive to directors, supervisors, senior managers and other employees based on the company’s shares. As early as the 1950s, this incentive method has appeared in enterprises in developed countries. In the 1980s, enterprises in Western developed countries generally implemented this system. By the end of the 20th century, 90% of the top 1000 companies in the United States had granted stock options to their management (Lv et al., 2009). The exploration of China’s modern equity system starts from the opinions on the standardization of joint stock limited companies issued by the National Economic System Reform Commission in 1992. Since 1998, China’s listed companies have begun to try equity incentive. However, for a long time, this incentive method has no formal system norms as the basis, and only a few enterprises have implemented it. At the end of 2005, the China Securities Regulatory Commission (CSRC) first promulgated the measures for the administration of equity incentive of listed companies (for trial implementation) which systematically standardized and guided the object scope, applicable conditions, implementation procedures, and disclosure requirements of the equity incentive system. This promulgation marked the beginning of substantive and systematic exploration of equity incentive. On January 27, 2006, the State-owned Assets Supervision and Administration Commission (SASAC) of the State Council and the Ministry of Finance issued the Trial Measures for the implementation of equity incentive by state-controlled listed companies (overseas). On September 30 of the same year, the SASAC issued the Trial Measures for the implementation of equity incentive by state-controlled listed companies in China (domestic). On July 13, 2016, the CSRC issued a new management method of equity incentive, namely, the management method of equity incentive of listed companies, based on the results of exploration and officially began to implement it on August 13, 2016. In May 2020, the SASAC issued the guidelines for the implementation of equity incentive by listed companies controlled by central enterprises to promote their improvement and enhance the long-term incentive and restraint mechanism. So far, China’s listed companies have implemented the equity incentive plan and continuously refined and standardized the assessment system, management measures, implementation procedures, and other aspects. They have actively guided the listed companies with various ownership, including private enterprises and SOEs, to implement the equity incentive plan. According to the incomplete statistics of Wind and FactSet, from the beginning of 2006 to the end of 2020, 1819 A-share companies have issued (including those that stopped the implementation) equity incentive plans. A total of 1624 A-share listed companies are implementing equity incentive, and nearly 40% of the total A-share listed companies have implemented equity incentive. As a growing number of listed companies have begun to implement equity incentive plan, its implementation effect has attracted much attention.

Executive Equity Incentive and Company Cash Holding Decision

In the environment of incomplete contract and asymmetric information, managers may use cash holding strategy to carry out rent-seeking activities (Jebran et al., 2019). Cash holding decision making then becomes an important tool for them to implement defensive behavior (Ye et al., 2020). Therefore, the cash holding level of a company often deviates from the Pareto optimal state owing to the existence of managers’ management defensive behavior. Relevant alternative mechanism is needed to correct it. The equity incentive mechanism is an important alternative mechanism. As mentioned above, the fundamental role of equity incentive is to promote the interest coordination between the operator and the owner.

Equity incentive system is widely implemented in Western developed countries. Equity incentive plays an important role in the rapid development of Silicon Valley in 1960s. The substantial improvement of the competitiveness of American enterprises is due to the equity incentive system. However, in China, because the capital market is immature and born out of the transition economy, the vast majority of listed companies are transformed from SOEs. The owner of state-owned shares is “vacant,” and the phenomenon of “insider control” is serious. SOEs are more faced with the risk of management speculation and self-interest behavior (Liao et al., 2020). Listed companies generally have management defensive behavior phenomenon (Ye et al., 2018). Equity incentives were once criticized for being reduced to a tool for the welfare of executives (W. Chen et al., 2021). Agency theory posits that operator’s shareholding can “bundle” the long-term interests of shareholders and operators, which will help reduce the management and defensive behavior of operators and make the two goals tend to be consistent, that is, to achieve “benefit synergy effect” so as to reduce agency costs and enhance enterprise value (Ye et al., 2020).

Regarding China’s listed companies, the proportion of senior executives’ shareholding remains generally low (Zhu & Zhou, 2016). Equity incentive has not yet been popularized, and the methods are too simple (Zhen et al., 2021). To retain the senior managers and fully mobilize their enthusiasm, the shareholders of the company should guide the executives to focus on the long-term development goals of the company. The company should implement long-term equity incentive to “bundle” the long-term interests of shareholders and executives.

Western research on managers’ management defensive usually includes compensation incentive and equity incentive. However, compensation incentive often leads to managers’ short-sighted behavior, which is usually difficult to produce a sustained positive effect on the company’s stock price and market value. Compensation incentive is also often assessed by noisy accounting indicators, which is greatly controlled by the operator. Equity incentive, which links income with market performance, is a compensation method based on market performance. It solves the problem that shareholders cannot directly supervise executives. As long as the equity incentive scheme is designed reasonably, it can still play an effective incentive role (W. Chen et al., 2021).

As a kind of equity incentive system, the original purpose of executive stock ownership system is to solve the agency conflict between shareholders and managers owing to information asymmetry (Bettis et al., 2018). When the shareholding ratio of the manager is at a certain critical point, the more shares the operator obtains from the shareholders, the more active the operator will be, and the goal of improving the long-term performance of the enterprise will be consistent with that of the shareholders (Clarkson et al., 2020; Su & Alexiou, 2019). With the increase of shares held by managers, the synergy effect between managers and shareholders’ interests will become more obvious. When the managers encroache on the interests of the company, their own costs will increase. For the sake of their own interests, they will reduce the tunneling behavior and make them converge with the company’s long-term interests in cash holding decisions so as to reduce their self-interest cash holdings and reduce their management and defensive behaviors in cash holding decisions (Loncan, 2020). When the manager’s shareholding ratio is low, with the increase of the shareholding ratio, the equity incentive can effectively inhibit the managers’ management defensive behavior in the cash holding decision making. However, when the operator’s shareholding exceeds a certain critical point, the entrenchment effect will occur (Griffith, 1999). At this time, with the further increase of managers’ shareholding ratio, on the one hand, the binding force of the internal and external supervision and control mechanism on the operator’s behavior is reduced, and the operator’s control over the company is further enhanced. The influence ability on the company’s cash holding decision is greater and easily produces management defensive behavior that encroaches on the company’s interests in the cash holding decision making (Yang et al., 2016). On the other hand, the operator’s control over the company is further enhanced so that the operator is more able to manipulate the company’s cash holding policy (Myers & Rajan, 1998). The opportunistic behaviors of the managers motivated by defensive will make more serious encroachment on the company’s cash assets, resulting in higher cash holding level and lower cash holding value (Ye et al., 2020). Obviously, with the further improvement of managers’ shareholding level, the greater the intensity of equity incentive, the greater the deviation between the actual and optimal cash holdings. Equity incentive aggravates the defensive behavior of self-interested managers in cash holding decision making (Duong et al., 2020; Shahzad, 2021).

From the above analysis, an inverted U-shaped nonlinear relationship is observed between equity incentive and the deviation degree in corporate cash holding decision making. However, the level of senior executives’ shareholding in domestic listed companies in China is generally very low. From 2004 to 2019, the per capita senior executives’ shareholding is less than 2.6% (and many companies have not yet implemented the executive shareholding system), which is far from reaching the stock holding level with trench defensive effect shown by Western research (Through empirical research, Farinha (2003) found that when the top executives’ shareholding reaches the critical point of 30%, with the increase of their shareholding level, the top executives have self-interested management defensive behavior in dividend payment. Zwiebel (1996) showed that when the equity ratio of top executives is between 7 and 38%, they have serious agency problems in terms of management defensive behavior). Therefore, under the current situation, the level of managerial ownership (or proportion) is generally low in China, so the increase of shareholding level can effectively inhibit the defensive behavior of managers in cash holding decision making. Based on this, we have formulated the following hypothesis:

Product Market Competition, Equity Incentive, and Cash Holding Decisions

In addition to internal governance mechanisms such as equity incentive to alleviate the conflict of interest between the principal and agent, important external governance mechanisms exist, and product market competition is an important one (Ansar et al., 2018). On the one hand, fierce product market competition helps solve the agency problem caused by asymmetric information between shareholders and managers. The competition transmits the information about the financial and market performance of managers in the way of benchmarking, which forces managers to work harder and restrain lazy behavior, thus reducing the agency cost of managers (Wang & Zhang, 2019). On the other hand, in the environment of product market competition and incentive, managers are faced with the risk of business failure, and even the threat and pressure of losing their existing positions, which forces them to reduce immoral behavior and adverse selection and improve management efficiency (H. Y. Li et al., 2020). With the improvement of product market competition, the management cost rate of enterprises shows a decreasing trend (Jiang et al., 2009). The above analysis implies that when the product market competition is strong, the enterprise management efficiency is higher (J. Li et al., 2016), and the marginal effect of equity incentive intensity on restraining defensive behavior in cash holding decision is small. However, when the market competition is weak, equity incentive intensity will show better performance in alleviating defensive behavior in cash holding decision making (Martin et al., 2020).

Based on the above analysis, a substitute relationship can be inferred to exist between equity incentive intensity and product market competition on the issue of restraining management defensive behavior in corporate cash holding decision making.

Research Design

Sample Selection and Data Sources

This study takes A-share listed companies from 2004 to 2019 as the research sample. The research interval began in 2004 because the corporate governance of Chinese listed companies in 2004 has been greatly improved compared with that in the previous years. Since then, the information disclosure and other behaviors of Chinese listed companies have been more standardized (Corporate governance evaluation research group of Corporate Governance Research Center of Nankai University, 2006). The ending time of sample selection is 2019 because this article was written in 2020 when the Annual Report of Listed Companies in 2020 has yet to be disclosed. Therefore, the time span of this study is from 2004 to 2019. To ensure the effectiveness of the data, the following samples are removed: financial companies and loss-making companies, PT and ST companies. To reduce the influence of extreme values, the continuous variables are winsorized by 1% up and down. Samples lacking data such as remuneration and corporate governance required for the study are removed as well. Through this screening, a total of 5783 observed values are finally obtained. The statistical software for data processing is SAS9.1. In addition, the corporate governance and financial data are from CSMAR and WIND databases.

Variable Design

Excess Cash Holdings (Excash)

Referring to the methods of Dittmar and Smith (2007) and Jebran et al. (2019), cash holding level (Cash) is represented by the natural logarithm of the ratio of cash and cash equivalents to non-cash assets, in which cash equivalents are replaced by trading financial assets. Considering that industry factors may have an important impact on the company’s cash holdings, to eliminate this impact, the cash holding level (Cash) should be adjusted on the basis of the above measurement. The specific calculation formula is as follows:

Here, Adcash represents industry-adjusted cash holdings, and Inmecash is the median cash holding in its industry. Referring to Opler et al. (1999) and Dittmar and Smith (2007), Adcash is set as the dependent variable, and relevant financial characteristic factors are taken as independent variables to construct the following model to measure the normal (or optimal) cash holdings of the company.

In model (1), Size is the size of the company, which is described by the natural logarithm of the total assets at the beginning of the year; Lev is the financial leverage, expressed by the asset liability ratio; Capex is the capital expenditure, which is measured by the cash paid for the purchase and construction of fixed assets, intangible assets and other long-term assets divided by total assets; Cf is the operating cash flow, which is characterized by the ratio of net cash from operating activities to total assets; Turno is the operating capacity, measured by the turnover rate of total assets, and it is equal to the operating revenue divided by the average total assets; Growth is growth, which is reflected by the growth rate of operating income; Div is the dummy variable of whether the company pays cash dividends, with the value of 1; otherwise, 0. The annual effect is also controlled in the model.

The absolute degree of the estimated residual (ExCash) of model (1) is the excess cash holding (ExCash), which is the difference or deviation between the actual cash holding and the normal (or optimal) cash holding estimated by model (1). The greater the deviation, the more serious the negative effect on the company.

Equity Incentive Intensity (Mshare)

The practice of Tang et al. (2021) is referred to, and Mshare is characterized by the ratio of the total number of shares held by the general manager to the total number of shares of the enterprise that represents the intensity of equity incentive. It reflects the total proportion of the general manager’s shares in the company.

Market Competition (HHI)

Based on the research methods of Haushalter (2007) and Jiang et al. (2009), Herfindahl–Hirschman Index (HHI) is selected to represent the degree of product market competition. The specific measurement formula is as follows:

where Xi is the operating income of enterprise I in the industry. The lower the HHI value, the more intense the product market competition. On the contrary, the higher the HHI value, the higher the monopoly degree.

Control Variables

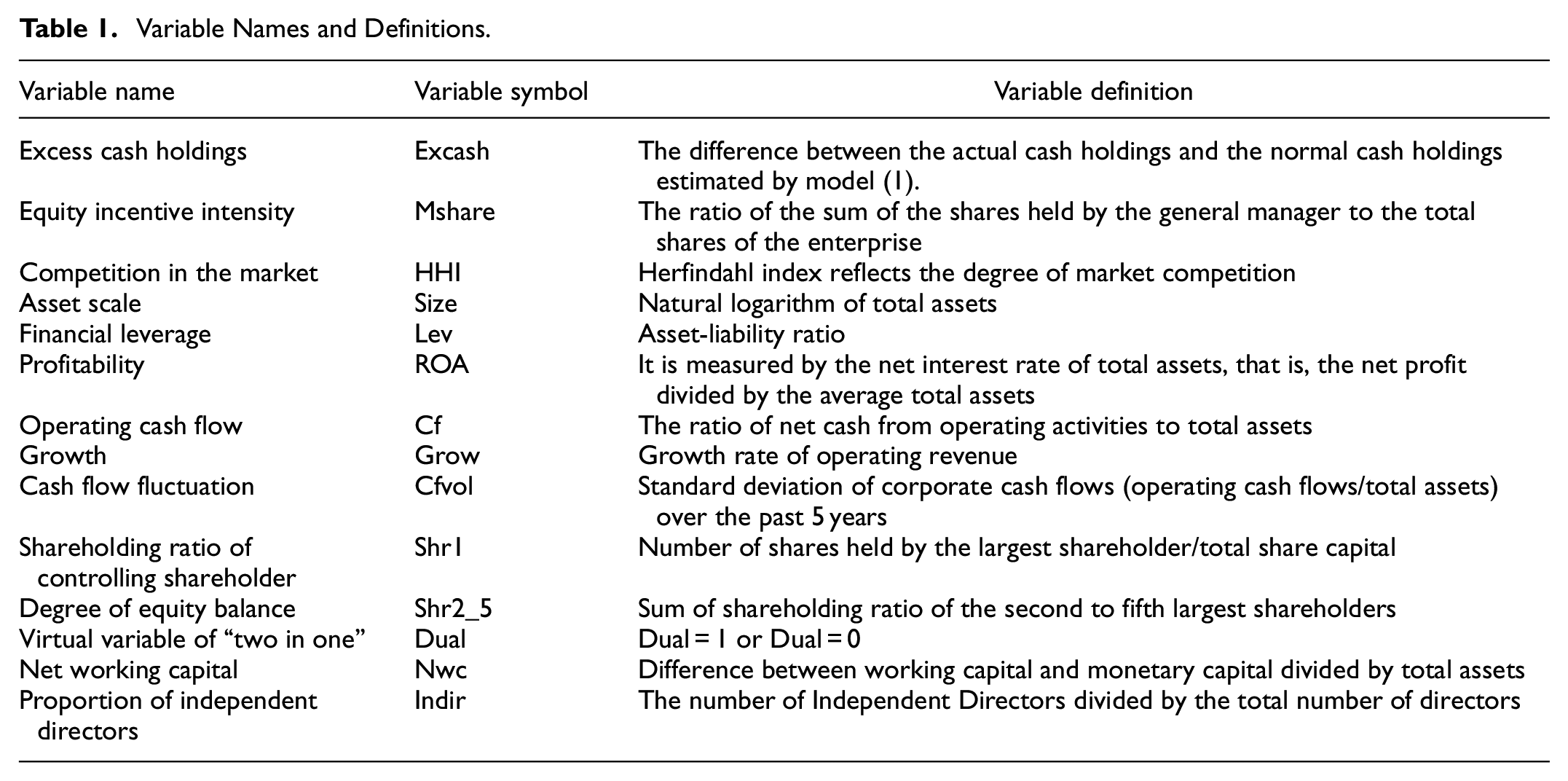

Based on the current situation in China and the research of Yang et al. (2016), considering that enterprise characteristics, corporate governance and financial characteristics also have an impact on the defensive behavior in corporate cash decision making, we also control the following factors: (1) the size of the company (Size) is expressed by the natural logarithm of total assets. (2) Financial leverage (Lev) is expressed in terms of asset liability ratio. (3) Profitability (ROA) is measured by net interest rate of total assets, which is equal to net profit divided by average total assets. (4) Cf is operating cash flow, which is measured by the ratio of net cash from operating activities to total assets. (5) Growth is growth and measured by growth rate of operating income. (6) Cash flow fluctuation (Cfvol) is equal to the standard deviation of cash flow (operating cash flow/total assets) of the enterprise in the past 5 years. (7) The shareholding ratio of controlling shareholders (Shr1) is expressed by the number of shares held by the largest shareholder/total equity. (8) The equity balance degree (Shr2_5) is also controlled. (9) Dual is a virtual variable representing the characteristics of the operator. If the general manager and the chairman of the board are one, then Dual = 1; otherwise, Dual = 0. (10) Net working capital (Nwc) is measured by the difference between working capital and monetary capital divided by total assets. (11) Independent directors ratio (Indir) is equal to the number of independent directors divided by the total number of directors. In addition, the annual and industry effects are controlled in the model. The definitions of the above variables are provided in Table 1.

Variable Names and Definitions.

Model Construction

To test H1 and investigate the effect of equity incentive on corporate cash holding decisions, this study uses the practice of Khieu and Pyles (2012) for reference to build the following panel data model (2).

Among them, explanatory variables Msharei,t−1 is the equity incentive in the t-1 year of the company. According to H1, the Mshare coefficient a1 is expected to be negative.

Empirical Results and Analysis

Descriptive Statistics

Table 2 shows the descriptive statistics of the main variables. The mean value of cash holdings (Cash) is 22.38%, the median is 16.03%, the standard deviation is 20.1%, the minimum is 1.19% and the maximum is as high as 130.35%. These results show that more than half of the companies’ cash holdings do not reach the average level and that the cash levels held by different companies vary greatly. The average value of excess cash holdings (ExCash) is 9.37%, and its standard deviation is as high as 13.03%, which indicates that the deviation of the sample company’s cash holdings and the difference in excess cash holdings are large. The average shareholding of executives (Mshare) is 2.59%, and the median is 0, indicating that the executive stock ownership level of most companies is generally at a low level, far lower than the mean value. The average shareholding of senior executives of listed companies is only 2.59%, indicating that the overall shareholding ratio of Chinese listed companies is low. This is far from the proportion of executives holding more than 10% in Western countries (Zhou & Xue, 2011), indicating that the long-term incentive mechanism of Chinese listed companies needs to be improved, which is consistent with the conclusions of Pan and Shen (2021).

Descriptive Statistics of Research Variables.

Correlation Analysis

Table 3 lists the correlation between variables, and the upper triangle (lower triangle) part lists the Pearson (Spearman) correlation coefficient. A significant negative correlation is observed between the intensity of executive equity incentives (Mshare) and excess cash holdings (ExCash). This correlation indicates that the greater the intensity of operator equity incentives, the smaller the deviation from the optimal level of corporate cash holdings. The degree of market competition (HHI) and ExCash (ExCash) are negatively correlated, indicating that the higher the degree of market competition, the smaller the deviation of the cash held by the company from the optimal level. In addition, the Pearson (Spearman) correlation coefficient is significant, which initially shows effective equity incentives and market competition can inhibit the defensive behavior of operators in cash holding decisions. Moreover, the correlation coefficients among the main variables in Table 3 are all lower than 0.5, which indicates to a certain extent that no serious multicollinearity problem exists among the variables.

Pearson (Spearman) Correlation Coefficient of Main Variables.

Note. *, **, and *** indicate significant at the 10%, 5% and 1% levels respectively. Same below.

Basic Regression Analysis

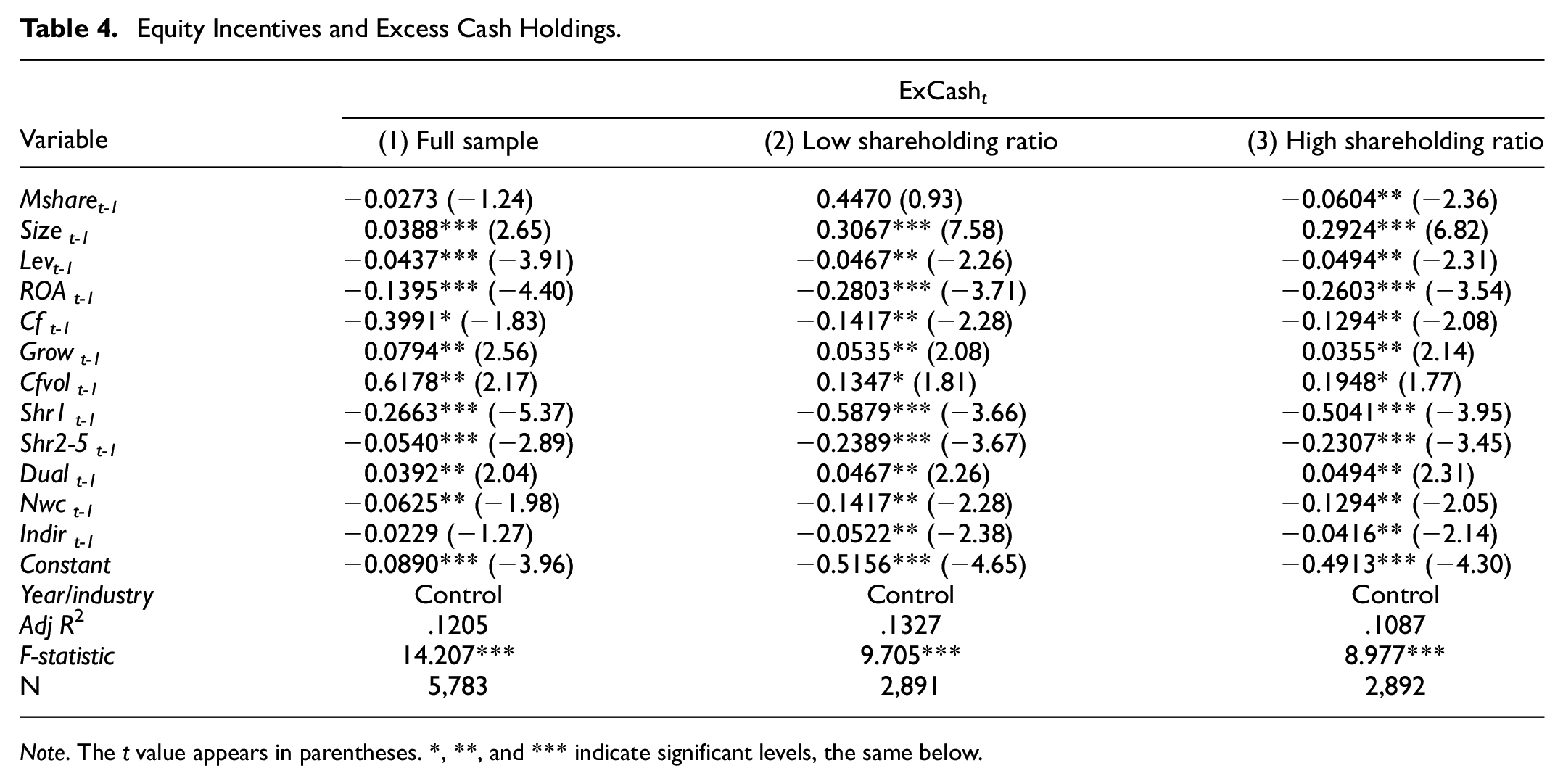

H1 Test: The Intensity of Equity Incentives and the Level of Excess Cash Holdings

To determine whether equity incentive can affect the defensive behavior of the management’s cash holding decisions, we employ an OLS regression analysis. Table 4 lists the results of multiple regression analysis of model (1). Column (1) of Table 4 shows that despite a negative correlation between the lagging period of equity incentives (Msharet-1) and the level of excess cash holdings (ExCasht), it is not significant. This result shows that in the Chinese capital market, equity incentives have not been able to inhibit the defensive behavior of operators in cash holding decisions as theoretically, and sometimes even show the opposite effect, such as the low shareholding ratio group in column (2) of Table 4. The reason for this phenomenon may be mainly due to the generally low level (or proportion) of China’s senior management’s shareholding, which is caused by errors caused by these insignificant or even negligible shareholding levels (Jiang and Huang, 2011).

Equity Incentives and Excess Cash Holdings.

Note. The t value appears in parentheses. *, **, and *** indicate significant levels, the same below.

To further investigate whether the above phenomenon is caused by the low level of senior executives’ shareholding, we divide the equity incentive samples into high shareholding group and low shareholding group with the median shareholding ratio as the critical point in Table 5 and report the distribution of excess cash holdings of the samples of low shareholding group and high shareholding group.

The Distribution of Differences in the Level of Excess Cash Holdings of Companies Under Different Shareholder Holdings.

Note. *** indicate significant at the 1% level.

In the further analysis of the sample of managers’ shareholding, the excess cash holding level of the low shareholding group is significantly higher than that of the high shareholding group. The results show that the governance effect of ESOP has a significant impact on the defensive behavior of corporate cash holdings. The higher the shareholding ratio, the lower the excess cash holding level and the better the governance effect of equity incentive.

To provide empirical evidence for the above explanation, we group the samples according to the proportion of senior executives’ shareholding. The grouping method is the same as that used to test the difference distribution of excess cash holdings. Columns (2) and (3) of Table 4 report the impact of different equity incentive intensity on the excess cash holdings of the company. The results of columns (2) and (3) reveal that in the low shareholding group, the regression coefficient of Msharet-1 is not significant, which indicates that in the case of a low shareholding ratio of executives, the incentives are insufficient to effectively suppress the opportunistic behavior of management and defensive in the company’s excess cash holdings. In the high shareholding group, the regression coefficient of Msharet-1 is significantly negative at the level of 5% (the coefficient difference test between the two groups shows significant difference). Hence, when the proportion of shareholding by executives is high, the incentive effect of equity effectively mobilizes the enthusiasm of executives. This can effectively suppress defensive behaviors in corporate cash holding decisions, confirming H1.

H2 Test: Equity Incentives, Market Competition, and Excess Cash Holdings

To further explore whether a substitute relationship exists between equity incentives and market competition in suppressing the level of excess cash holdings of enterprises, we refer to Ansar et al. (2018) and divide the product market competition degree (HHI) sample into product market competition with the median as the critical point. The two groups, strong and weak, and based on a previous study of effective equity incentives, report whether the relationship between high-share equity incentives and excess cash holdings varies under different product market competition levels. The test results are shown in Table 6.

Effective Equity Incentives, Market Competition and Excess Cash Holdings.

Note. The t value appears in parentheses. *, **, and *** indicate significant levels.

Table 6 (1) is listed as the strong product market competition group, which can be easily obtained from the table. The regression coefficient of Msharet-1 is negative but not significant. Table 6 (2) is listed as the product market competition weak group. The regression coefficient is significantly negative at the 5% level (the coefficient difference test between the two groups shows significant difference). These results indicate that the inhibitory effect of the intensity of equity incentives on the company’s excess cash holdings mainly exists in companies with weak product market competition, thus supporting the suppression of equity incentives and product market competition. A significant substitution effect is noted in the defensive behavior in the corporate cash holding decision, verifying H2.

Heterogeneity Analysis

Numerous studies have found that different levels of intervention by governance entities will affect corporate behavior, especially the management defensive behavior of corporate operators with “free decision-making power” (Ye et al., 2020; Zhou & Xue, 2011). Therefore, the efficiency of the equity incentive mechanism used to alleviate the conflict of management and defensive agency will inevitably be different owing to the difference of governance subjects (Liang, 2016). Based on this and on previous research revealing that effective equity incentives inhibit management defensive behavior in corporate cash holding decisions, we further explore whether significant differences exist in the aforementioned effects under different levels of supervision by governance entities. Prior studies have shown that creditors and shareholders are important governance entities of modern enterprises, and their monitoring and intervention effects have a direct impact on managers’ management defensive behavior by suppressing principal–agent conflicts (Denis et al., 1997; Zhou & Xue, 2011).

As the proportion of corporate debt is relatively large, the creditor’s interest will be more closely related to corporate risk, and creditors will have stronger incentives to supervise the company for their own interests. Therefore, the debt-to-business ratio is very suitable for measuring creditors’ supervision, taking into account that maintaining a high percentage of voting rights can give them more say in decision making. This provides large shareholders with high shareholding ratios with strong incentives and the ability to intervene in decision-making. Thus, the shareholding ratio of large shareholders can well characterize the supervision of major shareholders. Drawing lessons from the methods of Zhou and Xue (2011), we select the debt-to-business ratio and the largest shareholder’s shareholding ratio to characterize the supervision of creditors and major shareholders, respectively. We divide the sample of debt operation ratio into two groups: high and low degree of creditor supervision with the median as the critical point. We divide the sample of the largest shareholder’s shareholding ratio into two groups with high and low supervision degree of major shareholders with the median as the critical point.

The specific regression results are shown in Table 7. Columns (1) and (2) are the regression results of the high degree of creditor supervision group and the low degree group. The results show that the coefficient of msharet-1 is not significant in the high degree of creditor supervision group, but the coefficient of msharet-1 is significantly negative at the level of 1% in the low degree group (the coefficient difference test between the two groups shows significant difference). The inhibitory effect of effective equity incentive on the excess cash holdings mainly exists in the companies with low degree of creditor supervision, but it is not obvious in the samples with high degree of creditor supervision. Columns (3) and (4) are the regression results of the groups with high and low supervision of large shareholders. The coefficient of msharet-1 is not significant in the group with high degree of supervision of large shareholders, but the coefficient of msharet-1 is significantly negative at the level of 5% in the group with low degree of supervision of large shareholders (the coefficient difference test between the two groups shows significant difference). To sum up, the inhibitory effect of effective equity incentive on excess cash holdings mainly exists in the companies with low degree of supervision by major shareholders, but it is not significant in the samples with high degree of supervision by major shareholders.

Effective Equity Incentives, Supervision of Governance Entities and Excess Cash Holdings.

Note. The t value appears in parentheses. *, **, and *** indicate significant levels.

Robustness Test

To verify the reliability of the previous empirical results, we undertake a battery of robustness checks.

System GMM Estimation Method

An endogenous problem of potential causal inversion may exist between the company’s cash holding value, management defensive and equity incentives. To control this problem, we draw on the research of Blundell and Bond (1998) and Bai et al. (2008) and adopt the System GMM estimation method. In the estimation, to avoid the problem of weak instrumental variables caused by the excessively long lag period, we restrict the use of second-order lag term of the dependent and independent variables as the system GMM type instrumental variables and re-examine the previous results. The main results are shown in Table 8. Columns (1), (2), and (3) show a significant positive correlation between the excess cash holding level (L.ExCash) of one lag period and the excess cash holding level (ExCash) of the next period. In column (3), which is the high shareholding ratio sample, equity incentive (Mshare) and excess cash holding level (ExCash) show a significant negative correlation. In column (1) which is the full sample and column (2) which is the low shareholding ratio sample, the relationship between the two is not significant. The statistical values of AR(2) and Sargan’s test are not significant, but the statistical value of AR(1) is significant, indicating no second-order autocorrelation in the residual after the first-order difference. The instrumental variables are reasonable. The regression results of System GMM in Table 8 show that the previous conclusions remain valid after controlling the endogeneity of related variables.

Equity Incentives and Excess Cash Holdings: System-GMM Estimation Results.

Note. The t value appears in parentheses. *, **, and *** indicate significant levels.

Heckman Two-Stage Test

To control the adverse effects of sample self-selection bias on the results, we use the Heckman two-stage model to test. Specifically, the model’s dependent variable in the first stage is the equity incentive dummy variable (Mshare_dum), if the equity incentive intensity in the sample exceeds the annual-industry median, it takes 1; otherwise, 0. On this basis, we construct a model of the influencing factors of equity incentives, referring to the research of Lv et al. (2011) to analyze the influencing factors of equity incentives. We then select the marketization index (Mardex) and the dummy variable of whether it is a state-owned enterprise (Soe). The control variables in the previous model (2) are used as variables that affect equity incentives. The first stage model (3) is constructed as follows:

We perform probit binary regression on the full sample, low shareholding ratio sample and high shareholding ratio sample of model (3) to calculate the inverse Mills ratio (IMR) of each sample. In the second stage, the IMR of each sample in the first stage is included as a control variable into model (2). Regression is performed on the full sample, the low shareholding ratio and the high shareholding ratio sample in turn. The test results are shown in Table 9. Columns (1), (3), and (5) report the first stage results of the full sample, low shareholding ratio sample, and high shareholding ratio sample, respectively. Columns (2), (4), and (6) report the second-stage results of the full sample, low shareholding ratio sample, and high shareholding ratio sample, respectively. The marketization index and the nature of ownership are significant in the first stage. No matter the sample, equity incentives are affected by the degree of marketization and listing years. In the second stage, the results obtained by adding IMR to model (2) and regressing each sample show that in columns (2) and (4), the equity incentive intensity (Mshare) coefficient remains insignificant. In column (6), the equity incentive intensity coefficient is significantly negative at the 5% level. The Heckman two-stage test results are consistent with the existing results.

Heckman Two-Stage Test Results.

Note. The t value appears in parentheses. *, **, and *** indicate significant levels, the same below.

Substitute Variables

When testing the intensity of executive equity incentives, we also use the ratio of the total number of shares held by all executives in the executive team except the general manager to the total number of shares issued by the company as the executive equity incentive intensity. The surrogate variables of (Mshare) are re-regressed, and the empirical results remain unchanged.

Impact of the Financial Crisis

The cash holding decision-making behavior of managers may show systematic changes due to the uncertainty of the external macroeconomic environment (F. Y. Li & Shi, 2016). For example, the international financial crisis in 2008 has a greater impact on corporate cash holding behavior. After removing the observations in 2008, the results are regressed, and the results remain stable. Owing to space limitations, only the results of test (1) are reported.

Conclusion

From the joint-stock reform to the mixed ownership reform, the system reform of China’s listed companies has lasted for nearly 20 years. The ownership structure of listed companies has been dispersed, and the change of governance structure has made the contradicting interest between shareholders and managers increasingly acute. In recent years, problems such as inefficient use of cash, waste of cash resources and cash embezzlement by the management of listed companies have emerged in an endless stream, revealing the management defensive behavior phenomenon. With the implementation of the equity incentive mechanism in listed companies in China, whether this incentive scheme can have a governance effect on the management defensive behavior of the company’s cash holding decision must be explored. The impact of equity incentives on the corporate cash holding decision has profound practical significance and theoretical value.

This study thus selects Chinese listed companies in Shenzhen and Shanghai Stock Exchanges from 2004 to 2019 as the research samples. Using OLS and System GMM methods, this study primarily aims to examine the impact of equity incentive intensity on the management defensive behavior in corporate cash holding decisions. The study finds that the incentive effect of equity incentives on the defensive behavior of corporate cash holding decision making is not obvious on the whole. Only when the proportion of managers’ holding shares is high is the effect of equity incentive more significant. The higher the intensity of equity incentives, the more the enterprise exceeds and the lower the level of excess cash holdings. Effective equity incentives have a significant inhibitory effect on the defensive behavior of the company in cash holding decisions. In addition, a substitute relationship exists between the intensity of equity incentives and product market competition when restraining the management defensive behavior in corporate cash holding decisions. Further research finds that the inhibitory effect of the intensity of equity incentives on defensive behavior in cash holding decisions mainly exists in the case of ineffective supervision by large shareholders and creditors. This study contributes to the existing literature in two aspects. Firstly, this paper explores the relationship between equity incentive and management defensive behavior in corporate cash holding decisions, and reveals that there is a substitution relationship between equity incentive intensity and product market competition in restraining management defensive behavior in corporate cash holding decisions. Provide theoretical support for the listed companies in the emerging transition market on how to improve the equity incentive mechanism to alleviate the defensive behavior of the management, so as to enrich the theoretical literature of corporate governance; Secondly, it further studies whether there is a significant difference in the inhibitory effect of equity incentive intensity on defensive behavior in cash holding decision-making under the different degrees of supervision of major shareholders and creditors, which provides new evidence for the impact of institutional environment on the governance effect of equity incentive.

The findings of this study not only expand the relevant research on the economic consequences of equity incentive but also deepen the understanding of the effect of equity incentive under different conditions. Such a knowledge is helpful to comprehensively understand the efficiency of equity incentive contract in restricting management and defensive of opportunistic behavior. It also provides beneficial enlightenment for the promotion of equity incentive and the improvement of corporate governance efficiency. The listed companies should pay equal attention to the material and non-material incentives when implementing the equity incentive scheme for the management so as to alleviate the interest conflicts and agency problems between shareholders and management, improve the efficiency of cash decision making and realize the improvement of enterprise value, viability and competitiveness.

The main limitations of this study are as follows: Firstly, endogenous problems. Theoretically, an endogenous relationship may exist between equity incentives and the company’s cash holding decision and other variables. Although we use the System GMM estimation method, Heckman test and other methods used by most scholars at home and abroad to consider related endogeneity issues, these methods cannot completely eliminate the endogeneity problem. Secondly, content issues. Owing to the length of this paper and the coordination of the full text, we only choose to study internal and external mechanisms such as major shareholder governance (internal governance mechanism), product market competition, and creditor governance (external governance mechanism). This study is far from covering all corporate governance issues, so important findings may be missed.

Future research directions include the use of instrumental variables, PSM, quasi-natural experiments, and other methods to control endogeneity problems more effectively. At the same time, the external governance mechanism can be expanded. In recent years, some scholars have found that external restraint mechanisms such as control market and manager market may affect the company’s cash holding decision. These variables are not considered in this study owing to the difficulty of data acquisition or measurement. In the follow-up research, field research, questionnaires, network information collection, and search for various statistical data can be used to find effective data on these external restraint mechanisms and expand the internal governance mechanism.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This article is supported by National Natural Science Foundation of China (Project Number:71962023) and Social Science Foundation project of Jiangxi Province (Project Number:23YJ08)