Abstract

This study investigates how corporate green transformation (CGT) enhances corporate sustainable development performance (CSDP) and ensures their positive nexus and effective realization pathways. Using unbalanced panel data from 3,579 A-share companies listed on the Shanghai and Shenzhen Stock Exchanges between 2010 and 2022, the Word2Vec model is applied to measure CGT based on 8,061 green transformation keywords, and its mechanisms of influence on CSDP are explored. The findings show that CGT improves both corporate financial and environmental performance, exerting a significant positive effect on CSDP. Furthermore, CGT can foster corporate green innovation and strengthen the tone of management discussion and analysis (MD&A) reports. These improvements serve as pathways through which CGT promotes CSDP. Heterogeneity analysis confirms that the positive impact of CGT varies significantly depending on the level of CGT actions, the characteristics of heavily polluting firms, and different time periods.

Plain Language Summary

This study measures corporate green transformation using text analysis technology and explores the influence of green transformation on corporate sustainable development performance in China.

Introduction

Since 2015, 193 member states of the United Nations have adopted 17 Sustainable Development Goals (SDGs) at the Sustainable Development Summit. As important micro-entities in the market, corporations play a crucial role in advancing sustainability through environmental and social responsibility. For most corporations, these responsibilities represent commitments to stakeholders, expressed through sustainable practices and green transformation initiatives. Corporate sustainable development (CSD) not only pursues long-term profit growth but also emphasizes the responsible use of resources to mitigate the adverse environmental effects of production activities, thereby securing long-term support from internal and external stakeholders (Ahmed et al., 2014; Tien et al., 2020). Corporate green transformation (CGT) initiatives play a vital role in advancing corporate environmental and social responsibility and in enhancing CSD performance (CSDP). The main purpose of this study is to investigate the endogenous driving forces and influence mechanisms through which CGT promotes CSDP from the perspective of green transformation. Specifically, this study addresses two key questions: (a) Does CGT promote CSDP and thereby achieve a balance between green governance and profitability? (b) Through which effective channels does CGT promote CSDP?

CGT and CSDP are fundamental pillarb of CSD. Green finance is an important driver of both CGT and sustainable growth (Chen et al., 2023; Cheng & Wu, 2024). The agglomeration of bank branches near firms facilitates green transformation by reducing financing constraints, increasing green investment, and fostering green innovation (Teng & Tan, 2023). Enhancing competitive strategic decision-making also improves the level of CGT (Wang & Cao, 2022). Similarly, strengthening carbon risk awareness and environmental awareness promotes CGT by reducing financial constraints, reinforcing environmental regulation, and attracting greater investor attention (Fang, 2024; Liu, Wu & Kong, 2024). Environmental information disclosure has been found to exhibit a positive U-shaped relationship with CGT (Chai et al., 2024; Zhang et al., 2025). Moreover, environmental regulation, green finance policies, and executives’ green experience can enhance CGT and environmental, social, and governance (ESG) performance by improving green total factor productivity (Deng et al., 2024; Ding et al., 2023; Zhang, Zhang, Zhang, & Lan, 2024).

Corporate digital transformation can enhance both the quantity and quality of green technology innovation by reducing corporate risk-taking and increasing research and development (R&D) intensity (Dong et al., 2024; He & Chen, 2024; Sun, 2024; Xu et al., 2023). It also promotes green investment by improving internal control quality, increasing information transparency, and strengthening ESG performance (Zhang, Lai, Li, Wang, & Ru, 2024). Moreover, digital transformation improves corporate environmental and ESG performance by enhancing green capabilities and resource allocation efficiency (Li & Lin, 2023). Green strategy transformation and green action transformation further advance corporate green mergers and acquisitions and boost stock returns in capital markets by increasing investor confidence (Chen, Ma, Ma, Shen & Chen, 2023; Hu et al., 2023). However, CGT may also reduce stock returns by increasing operating costs and weakening investor confidence (Li, 2024).

Sustainable development has become a prominent topic in both academic and business communities. CSD reflects a firm’s ability to maintain sustainable operations, operational profitability, and production (Chen et al., 2022). Sustainable development, green innovation, and social responsibility are key drivers of improved corporate financial performance (Anser et al., 2018; Chang & Kuo, 2008; Charlo et al., 2015; Guerrero-Villegas et al., 2018; López et al., 2007; Papangkorn et al., 2022). The breadth and concentration of the SDGs further strengthen corporate financial performance (Asif et al., 2023; Lassala et al., 2021; Rosamartina et al., 2022). In addition, environmental performance, social responsibility performance, and ESG outcomes align closely with sustainable development objectives, benefiting both society and corporations (Escrig-Olmedo et al., 2017; Gupta, 2020; Lee et al., 2024; Siltaoja, 2014; Wang, Chu & Hao, 2024). Social mission and social innovation also play a role in enhancing CSD (Wang et al., 2021).

Green innovation practices and ESG performance improve the transparency of business activities, strengthen stakeholder confidence, and promote CSDP (Khan et al., 2021; Ng et al., 2022). SDGs and sustainability policies help explain variations in corporate sustainability performance (Jiang & Chen, 2024; Khan et al., 2021; Moldavska & Welo, 2019). Green culture enhances CSDP by fostering green technology transformation and green management transformation (Bai et al., 2023; Li & Lin, 2024). Digital transformation advances green product, process, and management innovation, thereby supporting CSDP (Dou & Gao, 2023; Jan et al., 2024; Wu et al., 2023). It also facilitates business operations, boosts the profitability of manufacturing firms, and drives ESG investments for sustainable development (Wang et al., 2023). In addition, carbon trading policies increase green technology input and strengthen regulatory oversight, which in turn improve the efficiency of pollutant and carbon emission reduction and ultimately enhance CSDP (Bian et al., 2024; Lin et al., 2024; Zhang & Xi, 2024).

In recent years, many scholars have examined from a micro perspective how environmental performance, social responsibility (Escrig-Olmedo et al., 2017; Gupta, 2020; Jiang & Chen, 2024; Ng et al., 2022), green innovation (Khan et al., 2021; Wu et al., 2023), and digital transformation (Jan et al., 2024; Wu et al., 2023) can accelerate CSDP. This study focuses on A-share companies listed on the Shanghai and Shenzhen Stock Exchanges from 2010 to 2022 and measures CGT based on management discussion and analysis (MD&A) texts from annual financial reports using text analysis techniques. This study explores the influence of CGT on CSDP in China and makes three key contributions.

First, this study employs AI tools, the K-nearest neighbor algorithm, and multiple iterative models to construct a green sentiment dictionary in the field of ecological and environmental protection, containing 8,061 positive words and 4,706 negative words. Using this dictionary, textual analysis is applied to MD&A reports to qualitatively measure CGT. This approach enriches both the qualitative and quantitative measurement of CGT compared with prior methods (Chen et al., 2023; Cheng & Wu, 2024; Liu et al., 2024; Tan et al., 2025; Teng & Tan, 2023; Wang et al., 2024; Zhang et al., 2022).

Second, this study confirms that CGT significantly enhances CSDP by fostering corporate green innovation and improving the tone of MD&A reports. This finding deepens the understanding of the mechanisms through which CGT promotes CSDP, and is consistent with previous findings on the promotion mechanisms of green innovation (Wu et al., 2023) and social responsibility (Jiang & Chen, 2024; Ng et al., 2022).

Third, this study reveals that the impact of CGT on CSDP varies significantly across industry types, CGT action levels, and time periods. Firms with lower-intensity CGT actions and those in non-heavily polluting industries achieve greater improvements in CSDP compared with firms undertaking higher-intensity CGT and those operating in heavily polluting industries. Moreover, CGT during the earlier period (2009–2015) is found to have demonstrated a stronger positive effect on CSDP than in the later period (2016–2022).

The remainder of this article is organized as follows. Theoretical analysis and research hypothese explains the mechanisms through which CGT influences CSDP. Research design provides the selection of variables, data sources, and econometric models. Empirical analysis includes fundamental tests, mechanism analysis, robustness tests, and heterogeneity analysis. Conclusion and policy implications concludes the main findings and policy implications.

Theoretical Analysis and Research Hypotheses

CGT is a transformation process that reallocates resources efficiently, restructures market competitive advantages, and promotes both environmental and economic value. This corporate transformation is driven by energy-saving and emission-reduction potential, cost savings and efficiency improvements, and the restructuring of social responsibility, ultimately converting “environmental value” into “economic benefits.” Figure 1 illustrates the mechanism by which CGT influences CSDP.

The mechanisms through which CGT influences CSDP.

CGT drives companies to upgrade green technologies, optimize energy structures, and enhance resource recycling and reuse, effectively promoting the shift from traditional production models to clean production processes and green service practices. Many companies advance energy-saving and emission-reduction technologies, reduce resource consumption, and accelerate the efficient use of energy and materials (Li et al., 2023; Li, Zheng & Li, 2025). According to resource allocation theory, CGT improves energy efficiency and resource recycling, lowers reliance on coal, petroleum, and other fossil fuels, and increases the potential for energy conservation and emission reduction (Zhu et al., 2023). This green transformation helps reduce overall resource usage, promotes resource reallocation efficiency, and lowers the compliance costs associated with corporate green governance.

CGT promotes a fully green industrial chain by integrating activities such as procurement, manufacturing, operations, greenhouse gas emission reduction, sewage treatment, pollutant recovery, and environmental remediation. It enhances performance in environmental information disclosure and social responsibility (Sun et al., 2025), and also helps companies reduce financing constraints, lower financing costs, and access more green financial resources, including green credit, green bonds, and green funds. These financial resources are then invested in energy conservation, emission reduction, and pollution control, thus improving environmental performance and fostering positive cooperation among local governments, financial institutions, and companies. Moreover, CGT reduces emissions of greenhouse gases, sewage, and solid pollutants, and improves environmental governance performance (Chai, Zhang, Wang, Lu & Jin, 2024; Zhang et al., 2025).

CGT requires companies to consider the rights and interests of stakeholders. Efficient resource use and the development of green and low-carbon products promote the green transformation of production and services, generating greater social benefits for government agencies, regulatory bodies, suppliers, customers, and other stakeholders. Stakeholder theory suggests that such activities help corporations fulfill their social responsibilities. CGT enhances social image and reputation, builds trust with stakeholders, and strengthens social responsibility performance (Chen et al., 2023). Consequently, CGT contributes to improved environmental and social responsibility performance, creating mutually reinforcing feedback mechanisms.

CGT promotes resource reallocation and utilization, drives green product development, strengthens market competitiveness, and achieves economic benefits during the survival period (Chai et al., 2025). It supports the development of green and energy-saving products, facilitates the green transformation of products and services, and meets consumer demand for upgraded green products. CGT motivates companies to overcome technological and resource barriers, efficiently integrate internal and external resources, create green product differentiation, enhance brand value, and capture a green premium through persistent market competition. Information theory suggests that implementing CGT improves corporate environmental and social performance while establishing effective communication with financial institutions. This enhances the social trust of financial institutions in a company’s energy conservation, emission reduction, and environmental protection efforts. Therefore, CGT promotes optimized resource allocation and improved economic efficiency (Chai et al., 2025; Mehmood et al., 2024). According to the preceding discussion, the following hypothesis is proposed.

Increasing R&D in green and low-carbon technologies, promoting green innovation, developing green products to meet market demand, and improving the efficiency of green technologies are key for companies to seize future market opportunities and achieve sustainable development (Yang et al., 2025; Zheng & Zhang, 2023). Green finance and fiscal policies, such as government subsidies, tax incentives, green credit, and green bonds, provide companies with the resources needed to iterate and upgrade green and low-carbon technologies (Lu et al., 2022; Ma et al., 2023). Resource allocation theory argues that these financial and policy supports reduce corporate financing constraints and costs for green innovation, enabling firms to obtain more resources for R&D. The efficient reallocation of internal and external resources further increases innovation efficiency and lowers R&D costs, producing positive resource allocation effects (Caglar & Ulug, 2022; Yuan & Pan, 2023). Cleaner production processes and advancements in green technologies directly reduce resource consumption, enhance resource efficiency, lower operating costs, improve economic performance, and strengthen environmental performance by reducing environmental impact.

To achieve energy conservation, emission reduction, and dual carbon goals, local governments encourage corporate clean production and green transformation through subsidy and tax refund policies. They have implemented a range of economic incentives, including energy-saving and emission-reduction policies, ecological and environmental protection measures, and green fiscal policies. These policies increase external regulatory pressure, motivating firms to comply through improvements in green innovation. They also directly stimulate technological advancements in areas such as “end-of-pipe treatment” and process control (Ma et al., 2023). Industrial upgrading theory suggests that firms actively develop green and energy-efficient products, adopt energy-saving and emission-reduction technologies, and implement clean environmental protection practices, thus enhancing cleaner production and environmental governance efficiency (Benkraiem et al., 2023; Li et al., 2025). Through green innovation, corporations advance green technology and improve efficiency, achieving energy conservation, reducing CO2 and SO2 emissions, conserving water, lowering solid waste output, and enhancing overall pollution control and environmental governance. Green innovation also improves firms’ environmental performance via measures such as source emission reduction, process pollution control, and end-of-pipe treatment. According to the Porter hypothesis, improved environmental performance allows companies to reduce compliance costs and mitigate risks associated with fines, production shutdowns, and regulatory rectifications. Consequently, CGT enhances corporate environmental performance, lowers compliance costs and risks, ensures continuity and stability in operations, and ultimately improves economic and social performance, demonstrating the innovation compensation effect (Liu et al., 2024; Zhou et al., 2025).

The Porter hypothesis suggests that green innovation improves green operational capabilities and organizational performance, improves the quality of green products and services, and enhances market competitiveness (Chai et al., 2025). CGT can increase the likelihood of investors, the public, and other stakeholders to “vote with their money,” generating positive market incentives. It encourages companies to actively develop green products and restructure cleaner manufacturing processes, thereby meeting stakeholder expectations for environmental protection. Green technological progress and innovation output enhance corporate green operational capabilities, promote cleaner production and green services (Liang et al., 2022), and improve the efficiency of green innovation. This, in turn, enhances market competitiveness, revenue growth, and economic and social responsibility performance (Chen et al., 2023; Zheng & Zhang, 2023). Green innovation also improves product safety, supports environmentally friendly practices, optimizes the working environment, reduces occupational health risks, reduces community environmental disturbances, and enhances brand reputation, consumer loyalty, and employee satisfaction, ultimately strengthening social responsibility performance. Thus, the following hypothesis is proposed.

The tone of MD&A reports reflects an active, optimistic, and opportunity-oriented message that companies convey to stakeholders. It supplements the information related to green transformation efforts, environmental information disclosure, economic performance, and social responsibility performance. From an information theory perspective, MD&A tone encompasses both optimistic and negative expressions, communicating details about green innovation, cleaner production restructuring, resource recycling, and green strategic management, thereby enhancing the effectiveness of sustainability-related information for stakeholders. When companies implement green transformation and communicate their efforts, such as promoting energy savings, reducing emissions, and developing innovative green products, the positive and optimistic tone of MD&A reports conveys future expectations of environmental performance and profitability. This strengthens the credibility, clarity, and verifiability of information presented in MD&A texts (Niu et al., 2025). Energy-saving and green products foster a trend of green consumption in the marketplace, improve firm market competitiveness, and enhance information transparency in sustainable business performance. CGT reshapes corporate “green cognition and green culture” by embedding environmental protection standards, responding to market demand for green products, establishing green management systems, and developing green supply chains (Li & Lin, 2024; Wu & Shi, 2025). These transformations enhance the positive and optimistic tone expressed in annual financial reports, social responsibility reports, and investor performance briefings, thereby elevating the substantive quality of the MD&A tone. Additionally, an enhanced MD&A tone helps align the internal recognition of green initiatives and alleviates the “short-term cost anxiety” that often accompanies green transformation.

Resource allocation theory suggests that CGT reduces the use of production factors, decreases environmental pollution, increases energy conservation and emission reduction potential, and creates resource and environmental benefits, ultimately improving net MD&A tone (Chai et al., 2025; Zhang et al., 2025). CGT accelerates the development and utilization of energy-saving and emission-reduction technologies, lowering costs associated with energy use, regulatory penalties (such as pollution fees), and environmental restoration costs, thus increasing corporate environmental benefits (Sun et al., 2025). These improvements encourage firms to disclose more environmental information, thereby increasing the net MD&A tone. A more optimistic tone attracts greater attention from analysts and investors, shapes profit expectations, strengthens external supervisory pressure, and improves environmental and social responsibility performance. This, in turn, promotes additional green capital investment and generates a green value premium through investor support (Du & Yu, 2021). Furthermore, the MD&A tone helps guide CGT actions such as optimizing solid waste treatment processes, purchasing energy-saving equipment, and improving resource utilization efficiency, directly enhancing environmental and economic performance and ultimately strengthening CSDP.

CGT encourages managers to disclose a more optimistic MD&A tone, which enhances employees’ sense of belonging and responsibility, boosts job satisfaction and organizational cohesion, and strengthens corporate social responsibility (Chen et al., 2023; Zheng & Zhang, 2023). An optimistic MD&A tone also allows customers to clearly recognize a company’s environmental and social commitments, reinforcing awareness of green brands. By attracting more environmentally aware customers, it helps reshape a responsible brand image, increase customer loyalty, and enhance market competitiveness, ultimately creating a “green premium” for products. Moreover, an optimistic MD&A tone can improve information transparency, increase stakeholders’ expectations of a company’s green capabilities and social responsibility, and create positive informational and resource effects that support sustainable development (Hu, Zhang, Ji & Zhang, 2023; Sun et al., 2025). Therefore, an optimistic MD&A tone directly increases sales of green products, improves economic and social responsibility performance, and ultimately promotes CSDP. The following hypothesis is thus put forward.

Research Design

Variable Selection and Definition

Explained Variable

CSDP is the explained variable. Drawing on the methods adopted by Braam and Peeters (2018) and Wu et al. (2023), CSDP is measured across three dimensions: financial performance, environmental performance, and social responsibility performance. Financial performance is represented by return on assets (ROA), with higher ROA values reflecting stronger profitability. Environmental performance and social responsibility performance are measured using scores from Hua-zheng ESG. To ensure comparability, all three indicators are standardized to a 0 to 1 range using Max-Min normalization. The entropy method is then applied to assign weights and construct the composite CSDP index.

Explanatory Variables

CGT is a green development model guided by the principles of green growth and sustainable development. It promotes green technological innovation, balances energy saving with emission reduction, and enhances the quality and efficiency of sustainable growth. By integrating economic and environmental goals, CGT fosters coordinated development and the harmonious coexistence of humanity and nature (Cheng & Wu, 2024; Teng & Tan, 2023; Wang et al., 2024). In recent years, textual analysis has become an increasingly popular method for measuring CGT, with levels assessed through the total frequency of green transformation-related terms in corporate reports. The literature generally identifies two main approaches to CGT measurement. The first is quantitative, using evaluative indicators such as green total factor productivity and corporate green innovation to capture CGT levels (Liu et al., 2024; Wang et al., 2024; Wen et al., 2021; Zhang et al., 2022). CGT can also be measured through nine secondary indicators across four dimensions: technological innovation, production level, environmental protection, and social evaluation (Lin & Pan, 2024). Another approach relies on qualitative textual analysis. In recent years, most scholars have used textual analysis methods to asses CGT by the frequency of green-related terms in dictionaries covering areas such as green product design, green upgrading, pollution control, technological innovation, green strategy management, and green guarantee transformation (Chen et al., 2023; Cheng & Wu, 2024; Hu et al., 2023; Tan et al., 2025; Teng & Tan, 2023).

In this study, both the CGT level and CGT intensity serve as explanatory variables. First, a dictionary of positive green sentiment in the field of ecological and environmental protection was constructed. Then, the textual analysis of the MD&A sections in the annual financial reports of listed companies was carried out to extract CGT levels. The main steps are as follows.

(a) Data preprocessing: This stage consisted of two steps: large-scale data collection and policy text cleaning. First, policy documents were collected from the Peking University Law Treasure Database across seven dimensions: carbon peaking, carbon neutrality, energy conservation and emission reduction, ecological environment, sustainable development, green finance, and green technology application. Second, policy texts were processed using the Jieba segmentation tool. During this step, incomplete and duplicate data, stop words, punctuation, numbers, and case distinctions were removed to construct a clean and standardized corpus.

(b) Candidate seed sentiment word extraction: After segmenting and performing part-of-speech tagging on the policy texts, only nouns, verbs, adjectives, and adverbs were retained as potential candidate green sentiment words. High-frequency keywords (occurrence > 10) were identified, and their sentiment values were calculated using the SnowNLP method. Words with sentiment values above 0.5 were classified as positive, while those with values below −0.5 were classified as negative. Building on established green transformation keywords (Chang, Li, Xiao & Yang, 2024; Cheng & Wu, 2024; Hu et al., 2023; Tan et al., 2025) and environment and climate risk terms (Deng et al., 2024; Fang, 2024; Tian et al., 2024; Tian & Zhao, 2024), three groups of industry experts manually selected 500 positive and 500 negative sentiment words to serve as candidate seed sentimental words.

(c) Creation of a thematic corpus in ecological and environmental protection: This study adopts the 200-dimensional embedded word vector model developed by Tencent’s AI Laboratory to construct a thematic corpus. Based on the green seed sentiment keywords, the corresponding positions of all keywords were mapped in the word vector space. An appropriate fixed Euclidean distance d was then selected, and all the words within a distance di < d from the seed sentiment vocabulary were included in the thematic corpus. This approach avoids the limitations of selecting a fixed number of words, which may introduce weakly related terms in sparse areas or omit relevant vocabulary in dense areas.

(d) Creation of a multi-iteration algorithm process: Previous studies have demonstrated the effectiveness of dictionary-based sentiment approaches for measuring corporate financial sentiments (Frankel et al., 2022; Nguyen & Huynh, 2022). A fixed-distance vocabulary classification can be conceptualized as using multiple hypersphere surfaces centered on the seed sentiment words to segment the word vector space. However, this method may create gaps between the segmented regions, and separating hypersurfaces can be complex, limiting its applicability for further research. Therefore, this study adopts a multi-iteration algorithm inspired by the K-nearest neighbor algorithm. In each iteration, all words not yet included in the thematic corpus are evaluated. For each word, the proportion pi of the 100 nearest keywords that belong to the specialized corpus is calculated, and words with a proportion greater than 0.8 are temporarily stored. At the end of each iteration, all stored words are added to the thematic corpus. If the ratio of newly added words to the total number of words in the thematic corpus is less than 0.1%, the algorithm terminates and outputs the final thematic corpus; otherwise, a new iteration begins.

(e) Creation of a preliminary green sentiment dictionary: Using the multi-iteration algorithm described previously, the 120 most similar words for each seed vocabulary item were identified based on the highest cosine similarity of each word vector, excluding terms longer than six words. During this expansion process, the similarity of each word to the seed vocabulary was verified to prevent accidental inclusion. This step produced a preliminary expanded green sentiment dictionary, initially containing approximately 6,000 negative sentiment words and approximately 13,000 positive sentiment words.

(f) Screening green sentiment dictionaries: Three groups of industry experts manually reviewed the positive and negative green sentiment keywords. Overlapping or highly similar keywords (approximately 1,200) were removed. For the remaining vocabulary, word frequency and cosine similarity were calculated, and only the most representative and relevant terms were retained. Overlapping or redundant words were merged, and accidental inclusions were removed. Keywords in the stop word list, unclear conjunctions (e.g., “de”), and symbols were also deleted. Finally, semantic repetitions and terms with unclear meanings were manually removed, resulting in a finalized green sentiment dictionary comprising 8,061 positive keywords and 4,706 negative keywords.

(g) Calculating the total frequency of green transformation words: Utilizing the finalized positive green sentiment dictionary, all MD&A texts from the annual financial reports of Chinese A-share companies listed on the Shanghai and Shenzhen Stock Exchanges were segmented with the Jieba tool. Punctuation, numbers, case distinctions, and stop words were removed. The Word2Vec model was then applied to the segmented texts to compute the total frequency of green transformation keywords based on the 8,061 positive sentiment words.

(h) Measurement of CGT level and CGT intensity: The CGT level was measured as the natural logarithm of the total frequency of green vocabulary in the MD&A texts. CGT intensity was calculated by multiplying the total frequency of green vocabulary by 100 and then dividing by the total number of words in the MD&A texts.

For robustness testing, a quantitative indicator approach was also employed to measure CGT. Following Lin and Pan’s (2024) framework, nine secondary indicators across five primary dimensions were used to comprehensively measure CGT (see Table 1). After standardizing each secondary indicator, the entropy method was applied to construct a composite CGT index.

The Construction of Quantitative Indicators for CGT.

Source. The main indicators were sourced from Lin and Pan (2024).

Mediating Variables

Green innovation and management tone were selected as mediating variables. Green innovation was measured by the number of authorized green patents for each company, with the natural logarithm of this count used to represent the level of green innovation (Dong et al., 2024; Jiang et al., 2023). Management tone was measured by analyzing the proportion of positive versus negative vocabulary in the text, calculated as the difference between positive and negative words divided by their total (Yuan et al., 2022).

Control Variables

Basic corporate characteristics also influence CSDP. To ensure more reliable results, firm size, asset-liability ratio, growth potential, ownership concentration, ownership type, firm age, and managers’ shareholding ratio were selected as control variables. The measurement methods for these variables are detailed in Table 2.

The Design and Measurement of Variables.

Sample Selection and Data Sources

This study focuses on Chinese A-share companies listed on the Shanghai and Shenzhen Stock Exchanges, covering the period from 2009 to 2022. The sample was screened as follows: (a) companies designated as Special Treatment (ST) or Particular Transfer (PT) during the study period were excluded; (b) financial institutions were removed; (c) companies with missing data were omitted. The final sample primarily consisted of listed companies from the agriculture, forestry, animal husbandry, manufacturing, and service sectors. ST and PT companies were excluded because they typically exhibit abnormal operational and financial performance.

Corporate data for return on assets, environmental information scores, and social responsibility scores, used to measure CSDP, were primarily obtained from the Wind database and the China Stock Market Accounting Research (CSMAR) database. Textual data for corporate MD&A reports were collected from the China Scientific Research Data Service Platform and the RESSET Financial Text Intelligent Analysis Platform. MD&A tone data were sourced from the China Research Data Service Platform. Basic firm-level characteristics were gathered from the Wind, RESSET, and CSMAR databases. All empirical results were winsorized at the 1% level to reduce the influence of outliers.

Economic Model

According to Hypothesis 1, CGT can improve financial performance, enhance corporate environmental information disclosure, and strengthen corporate social responsibility performance, thereby promoting CSDP. The corresponding model is constructed as follows:

where

According to Hypotheses 2 and 3, CGT can enhance corporate green innovation and the tone of MD&A texts. By promoting green innovation, CGT improves resource utilization efficiency, energy conservation, and emission reduction, while also strengthening market competitiveness and sustainable profitability. Simultaneously, these improvements generate positive and optimistic information in corporate MD&A texts, raising the net MD&A tone. The influence mechanism models for sustainable development performance are constructed as follows:

where

Empirical Analysis

Evolution Trend of Sustainable Development Performance and Green Transformation

Table 3 presents the mean values of CSDP and CGT in the Shanghai and Shenzhen Stock Exchanges from 2010 to 2022. From 2011 to 2014, CSDP exhibited an upward trend, followed by a slight decline in 2015 and 2016. Between 2017 and 2022, CSDP initially increased and then exhibited a subsequent decline.

The Mean Statistics of CSDP and CGT Level.

Note.

Similarly, the CGT level increased steadily from 2010 to 2014. It experienced a slight decrease in 2015 and 2016, and then exhibited a modest declining trend from 2017 to 2022.

Baseline Results

This study empirically investigated the impact of CGT on CSDP, with the results reported in Table 4. Columns (1) to (3) present the regressions including control variables, for which fixed effects for year, industry, and both year and industry were respectively applied.

The Empirical Results of the Impact of CGT on CSDP.

Note. *, **, and *** represent significance at the 10%, 5%, and 1% levels, respectively; standard errors are reported in parentheses.

In columns (1) to (3), the coefficients of CGT are 0.220, 0.264, and 0.216, respectively, all significant at the 1% level. These results indicate that CGT promotes improvements in corporate profitability, environmental performance, and social responsibility performance, thereby enhancing CSDP, which supports Hypothesis 1. In column (4), the coefficient of CGT is 0.081, demonstrating that CGT also significantly contributes to future CSDP.

Corporations implementing green transformation actively adopt energy-saving, emission-reduction, and new energy technologies, while reducing fossil energy consumption and promoting the development and use of clean energy. These measures enhance energy conservation and emission reduction potential and improve environmental governance performance, thereby boosting corporate environmental and social responsibility performance. By promoting green transformation, leveraging green innovation capabilities, and obtaining support from green financial resources, companies can actively explore markets for green and energy-saving products, increase market competitiveness, and generate greater market value. Accordingly, CGT significantly enhances CSDP. Consistent with prior findings on digital transformation and SDGs (Khaled et al., 2021; Wu et al., 2023), this study demonstrates that CGT also has a significant positive effect on CSDP, highlighting its novel contribution to sustainable corporate development (Khaled et al., 2021; Wu et al., 2023).

In addition, the coefficients for firm size are significantly positive, indicating that larger listed companies can more effectively enhance CSDP. These results indicate that corporations with a greater asset size possess stronger market competitiveness, which supports sustainable profitability. The coefficients for firm age and managers’ shareholding ratio are also significantly positive, indicating that older corporations maintain stable market positions, and a higher proportion of managerial shareholding reflects stronger operational capability, further promoting CSDP. Conversely, the coefficients for corporate growth and ownership type are both negative, suggesting that rapidly growing and state-owned corporations may allocate resources primarily to revenue expansion, thus reducing resource investment in sustainability initiatives and thereby suppressing CSDP.

Robustness Test

To further verify the influence of CGT on CSDP, two robustness test methods were adopted, with the results presented in Table 5. In the first method, the measurement of CSDP was replaced with two alternative indicators, namely corporate profitability (ROA) and environmental performance, while the entropy method was still employed to construct the composite index.

The Robustness Test Results of CGT and CSDP.

Note.

In column (1), the coefficient of CGT is 0.011, indicating that CGT significantly enhances corporate environmental performance at the 1% level. This suggests that promoting CGT, improving energy conservation and emission reduction, and strengthening environmental governance are effective pathways for improving corporate environmental performance.

As presented in column (2), when CSDP is measured using two indicators, namely environmental performance and ROA, the coefficient of CGT is 0.336. Compared with the coefficient of 0.216 in column (3) of Table 3, the positive effect of CGT on CSDP is significantly increased at the 1% level. These findings demonstrate that the relationship between CGT and CSDP is robust.

In the second method, the measurement approach of CGT was replaced. Specifically, CGT intensity was calculated as the total frequency of green transformation words in the MD&A texts multiplied by 100, and then divided by the total number of words in the MD&A texts. In column (3), the coefficient of CGT intensity is 0.862, which is significantly positive at the 1% significance level, indicating that increased CGT intensity can substantially improve corporate environmental performance. This result indicates that CGT enhances the potential for energy conservation and emission reduction, accelerates the progress of low-carbon and clean technologies, and boosts the disclosure of environmental information. Collectively, these effects contribute to improving corporate environmental performance.

In column (4), the coefficient of CGT intensity is 4.569, indicating a significantly strengthened positive impact of CGT intensity on CSDP compared with the CGT coefficient of 0.216 in column (3) of Table 3. This finding indicates that greater disclosure of green transformation information in the MD&A texts of annual financial reports reflects higher CGT intensity, which in turn exerts a stronger effect in promoting CSDP. These empirical results confirm that increased CGT intensity demonstrates stronger robustness in enhancing CSDP.

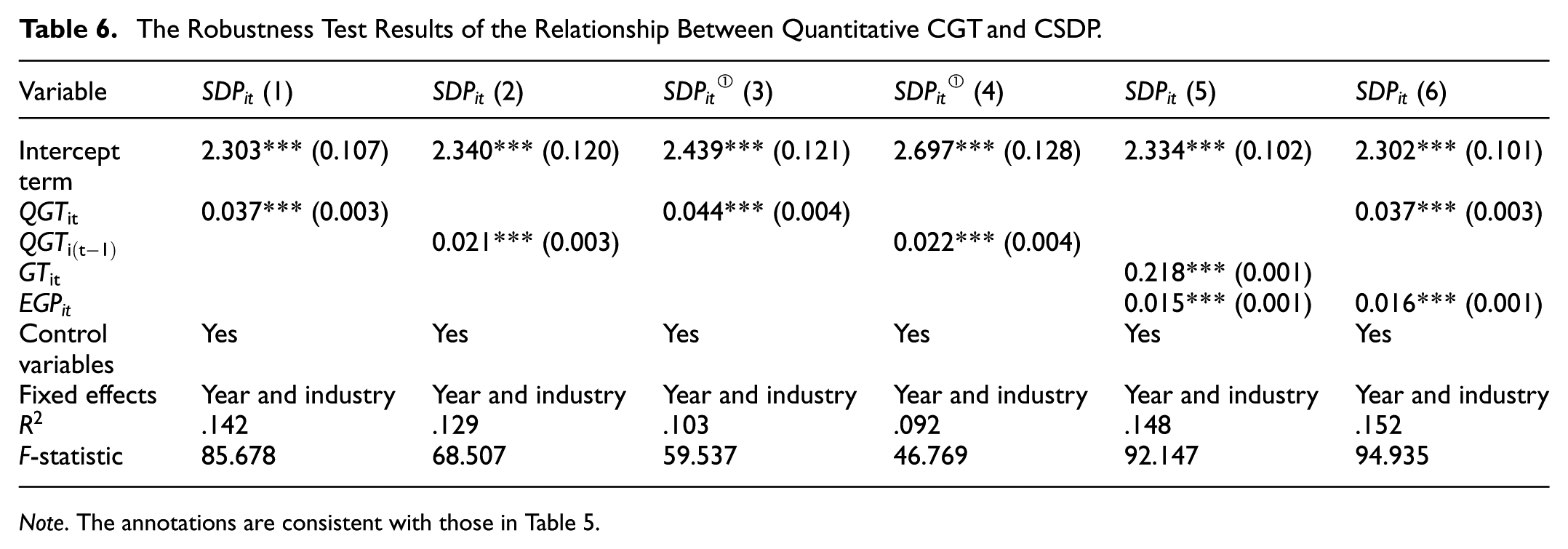

To eliminate the potential influence of different CGT measurement methods, Lin and Pan’s quantitative approach was adopted to re-examine the relationship between quantitative CGT and CSDP. The robustness test results are presented in Table 6.

The Robustness Test Results of the Relationship Between Quantitative CGT and CSDP.

Note. The annotations are consistent with those in Table 5.

As exhibited in columns (1) and (2), quantitative CGT exerts a significant and positive impact on CSDP at the 1% level. However, compared with the

Considering the practical context in China, local environmental governance policy (

Influence Mechanism Test

Two approaches, namely green innovation and MD&A tone, were employed to examine the transmission mechanisms through which CGT affects CSDP. Drawing on the theoretical basis of Hypotheses 2 and 3, Models (2) and (3) were used to empirically test these mechanisms. The results are reported in Table 7.

The Influence Mechanism Test Results Between CGT and CSDP.

Note. The annotations are consistent with those in Table 4.

Green Innovation Mechanism

In column (1) of Table 7, the coefficient of corporate green innovation is 0.060, indicating that CGT significantly promotes CSDP at the 1% level. Implementing CGT enhances the credibility of firms in the eyes of financial institutions, strengthens confidence in their environmental performance and profitability, and helps them secure more green financial resources. These resources increase R&D investment in energy-saving and emission-reduction technologies, as well as clean production processes. As a result, CGT improves the efficiency of green innovation outputs, advances clean production technologies, and increases the overall level of corporate green innovation. Prior studies have demonstrated that digital transformation substantially improves corporate green innovation (Dong et al., 2024; He & Chen, 2024; Lin & Xie, 2024; Sun, 2024). However, the present study provides new evidence that CGT further amplifies green innovation outputs, offering greater novelty relative to previous findings.

In column (2) of Table 7, the coefficients of CGT and green innovation are 0.208 and 0.134, respectively, both of which are significant at the 1% level, indicating that improvements in CGT and green innovation significantly enhance CSDP. In column (3), the coefficients of quantitative CGT and green innovation are 0.036 and 0.006, respectively, further confirming that CGT promotes CSDP through the enhancement of corporate green innovation output.

Green innovation enables firms to accelerate the advancement of energy-saving and emission-reduction technologies, strengthen ecological environment governance efficiency, and expand their potential for energy conservation and emission reduction, thereby improving environmental performance. While prior studies show that ESG performance and digital transformation enhance CGT and sustainable development (Wang et al., 2024; Wu et al., 2023), the present study demonstrates that CGT exerts a significant and positive effect on CSDP specifically through green innovation outputs, providing a novel marginal contribution to the literature on CSDP.

CGT enables corporations to develop green and energy-saving products that are increasingly favored by market consumers. These green products enhance corporate market competitiveness and support future profitability. Implementing CGT actions also strengthens brand image, builds social trust among stakeholders, and ultimately improves corporate social responsibility performance.

MD&A Tone Mechanism

In column (4) of Table 7, the coefficient of CGT is 0.027, which is significant at the 1% level, indicating that CGT positively influences corporate MD&A tone. By promoting energy efficiency, energy conservation, and emission reduction efforts, CGT generates positive and optimistic information. The associated reductions in pollutants and greenhouse gas emissions contribute to a more favorable MD&A tone.

In column (5) of Table 7, the coefficients for CGT and MD&A tone are 0.203 and 0.500, respectively, both of which are significant at the 1% level, indicating that both CGT and MD&A tone enhance CSDP. In column (6), the coefficients of quantitative CGT and MD&A tone are 0.037 and 0.040, respectively, confirming that increased CGT can significantly promote CSDP through positive changes in MD&A tone.

Implementing CGT actions can increase the informational content of MD&A texts, particularly in areas such as pollution control, energy conservation, emission reduction, and clean production. Prior research has found that a positive digital transformation tone can reduce equity costs (Guo & Huang, 2024), while a net positive tone of environmental information exerts positive information and resource effects on corporate green innovation (Hu et al., 2023). The findings of the present study demonstrate that CGT promotes CSDP by improving the positive informational content conveyed by MD&A tone, offering a novel marginal contribution to understanding the link between MD&A tone and CSDP.

These informational increments help corporations reduce production costs, create environmental benefits, and enhance market competitiveness, thus improving profitability. By increasing the transparency of energy conservation, emission reduction, and environmental governance efforts, CGT also enhances social trust among stakeholders and improves environmental performance and social responsibility levels. Overall, CGT actions enhance MD&A tone and provide additional informational value, which collectively promote corporate profitability, environmental performance, and social responsibility, ultimately promoting CSDP.

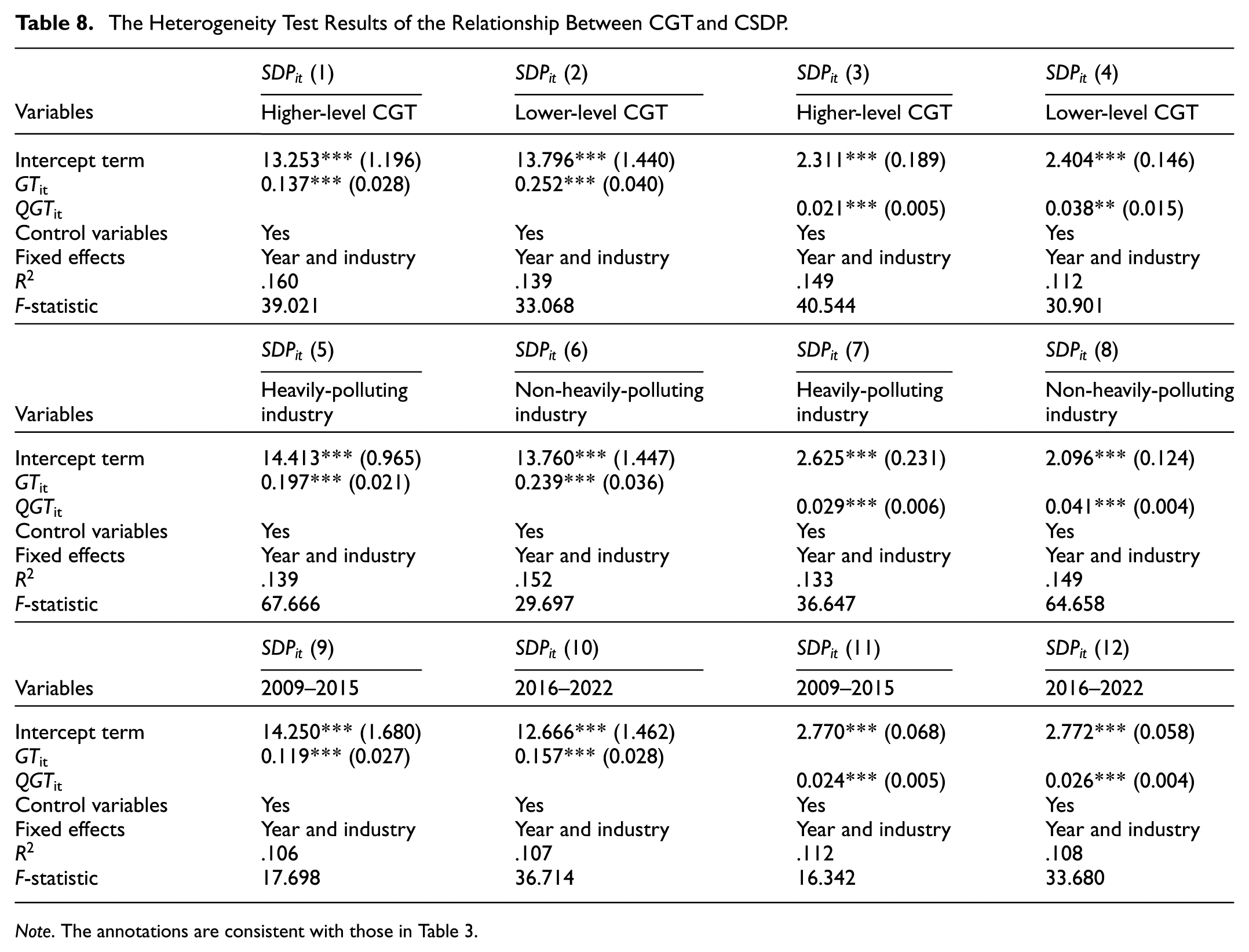

Heterogeneity Analysis

The heterogeneous impact of CGT on CSDP was analyzed across three dimensions: the level of CGT actions, heavily polluting industries, and different periods. The empirical results are reported in Table 8.

The Heterogeneity Test Results of the Relationship Between CGT and CSDP.

Note. The annotations are consistent with those in Table 3.

First, regarding CGT actions, the sample was divided into higher-level and lower-level subgroups based on whether the CGT level exceeds the median value. In column (1) of Table 8, the coefficient for higher-level CGT is 0.137, which is significantly lower than the value of 0.216 reported in Table 3. In column (3), the coefficient for higher-level quantitative CGT is 0.021, which is lower than the value of 0.037 reported in Table 6. These results indicate that higher-level CGT actions significantly promote CSDP but with a relatively weaker effect. In contrast, in column (2), the coefficient for lower-level CGT is 0.252, and in column (4), the coefficient for lower-level quantitative CGT is 0.038. These findings suggest that lower-level CGT actions have a more pronounced effect on CSDP. The results imply that lower-level CGT is more effective at attracting attention from stakeholders, such as investors and analysts, promoting social trust and market competitiveness, and driving greater improvements in profitability, environmental performance, and social responsibility performance.

According to the “Guidelines for Environmental Information Disclosure of Listed Companies” released by China’s Ministry of Environmental Protection on September 16, 2010, industries such as thermal power, steel, cement, electrolytic aluminum, coal, metallurgy, chemical, petrochemical, building materials, papermaking, brewing, pharmaceuticals, fermentation, textile, leather, and mining are classified as heavily-polluting industries. In column (5) of Table 8, the coefficient of CGT is 0.197, and in column (7), the coefficient of quantitative CGT is 0.021. These results indicate that heavily-polluting corporations implementing CGT actions exhibit a relatively weaker promotion effect on sustainable development performance. In contrast, in column (6), the coefficient of CGT is 0.239, and in column (8), the coefficient of quantitative CGT is 0.041. These findings suggest that non-heavily-polluting corporations implementing green transformation achieve a stronger positive impact on sustainable development performance. Compared to heavily-polluting firms, non-heavily-polluting firms are better able to improve energy conservation and emission reduction potential, enhance environmental governance and social responsibility performance, and thus more effectively promote CSDP.

To better capture differences across periods, the sample was divided into two sub-periods: 2009 to 2015 and 2016 to 2022. The heterogeneity results are shown in columns (9) to (12) of Table 8. The results indicate that, during 2009 to 2015, the coefficients of qualitative and quantitative CGT were 0.119 and 0.024, respectively. In contrast, during 2016 to 2022, the coefficients increased to 0.157 and 0.026, respectively. These findings demonstrate that the promoting effect of CGT on CSDP varies across sub-periods: CGT was found to have a relatively weaker effect in the earlier period, while the impact was stronger in the later period.

Conclusions and Policy Implications

CGT is a key practical strategy for enhancing market competitiveness, improving profitability, and promoting environmental and sustainable development performance. Based on corporate sample data, this study developed a green sentiment dictionary in the field of ecological and environmental protection. The green dictionary, containing 8,061 positive keywords, was used to measure CGT levels from MD&A texts using big data analysis techniques. CSDP was evaluated using a combination of financial performance, environmental performance, and social responsibility performance. The mechanisms through which CGT promotes CSDP were investigated from both theoretical and empirical perspectives.

The main conclusions of this study are as follows. First, CGT was found to significantly enhance corporate environmental performance and overall sustainable development performance. Substituting the CGT level with CGT intensity further confirmed that higher CGT intensity has an even stronger positive effect on corporate environmental and sustainable development performance, demonstrating the robustness of the results. In line with previous findings from OECD economies and China, digital transformation was also found to significantly improve corporate environmental and sustainable development performance (Li & Lin, 2023; Safi et al., 2024; Wu et al., 2023). This study highlights the important role of CGT in promoting CSDP, thereby enriching the understanding of their relationship.

Second, this study examined two key dimensions, namely green innovation and management tone, and confirmed both theoretically and empirically that CGT primarily improves CSDP by promoting green innovation and enhancing MD&A tone, revealing significant transmission mechanisms. Compared with previously identified mechanisms present in emerging economies, such as green innovation (Khan et al., 2021; Wu et al., 2023) and green capability (Li & Lin, 2023), this study demonstrated that the dual mechanisms of promoting green innovation and increasing MD&A tone also effectively transmit the impact of CGT on CSDP, thereby expanding the understanding of the influence pathways of green transformation.

Third, heterogeneity tests confirmed that lower-level CGT has a stronger effect on promoting CSDP than higher-level CGT. Similarly, heavily-polluting corporations experience a weaker promotion effect of CGT on sustainable development performance compared to non-heavily-polluting corporations. Additionally, the promotion effect of CGT was found to exhibit slight variations across different periods, with CGT in the latter sub-period exerting a stronger positive impact than in the earlier sub-period.

Globally, countries in Europe and America are advancing toward CSDP at uneven rates (Ahmed et al., 2014; Anselmi et al., 2024; Escrig-Olmedo et al., 2017; Lee et al., 2017). Improving environmental performance, social responsibility performance, ESG performance, and alignment with SDGs are key drivers for promoting CSDP worldwide. However, countries and regions in Asia, Europe, and America exhibit markedly different driving forces in promoting corporate sustainable business performance. In this study, CGT was found to emerge as a significant driver for Chinese companies to enhance CSDP, thereby enriching the understanding of factors that promote CSDP. Considering practical applicability in China, this study incorporated local environmental governance policies, ownership structure and concentration, and firm-specific characteristics. After controlling for these factors, the results demonstrated that CGT exerts a robust positive effect on CSDP.

Based on the preceding research conclusions, the following policy implications are proposed.

First, business managers should recognize the significant role of CGT in improving CSDP. Corporations should adopt the concept of green development, implement CGT initiatives, and integrate green transformation into daily production, operational activities, and supply chain management. By practicing green transformation, corporations can achieve sustainable development objectives. Specifically, managers should integrate green development strategies within the overall CSD strategy, enhancing the level of green innovation through CGT practices. These actions accelerate the development of energy-saving, emission-reduction, and environmental protection technologies, improving both energy efficiency and environmental governance performance. Moreover, practicing CGT can strengthen a corporation’s market competitiveness by promoting green, energy-efficient, and environmentally friendly products, thereby enhancing operational profitability. CGT also enables firms to communicate a positive and optimistic MD&A tone to stakeholders, providing valuable incremental information that improves corporate social image, fosters alignment between corporate performance and environmental protection, and ultimately enhances social responsibility performance. In addition, the promoting effect of CGT on CSDP varies significantly depending on corporate ownership type, CGT intensity, and whether the firm belongs to a heavily-polluting industry. Corporate managers should implement different green transformation strategies according to their development status and property rights. For non-state-owned and non-heavily-polluting corporations, managers should accelerate the adoption of green transformation initiatives and fully leverage local government economic incentives and resource support policies. By actively implementing CGT and pursuing sustainable development, these corporations can improve their green innovation capabilities, attract greater market attention from stakeholders, and ultimately achieve CSD.

Second, government decision-makers should actively guide and vigorously promote the development strategy of CGT, emphasizing its crucial role in enhancing CSDP. Local governments should increase their focus on resource allocation for green transformation and prioritize the flow of technological, economic, and financial resources toward corporations engaging in green transformation. They should accelerate the construction of green transformation infrastructure, encourage collaborative efforts among government, market, and corporate actors, and strengthen competitive mechanisms to promote CSD. Additionally, local governments should optimize policies related to energy conservation, emission reduction, green finance, ecological protection, carbon peaking, and carbon neutrality, and increase the allocation of capital market resources to green-transformed corporations through economic incentive measures, such as financial support, fiscal subsidies, and tax reductions. Local governments should accelerate the formulation of collaborative policy mechanisms for industrial upgrading and energy structure optimization, enhancing the synergy of multi-dimensional policies, including energy conservation, emission reduction, ecological governance, carbon peaking, and carbon neutrality. They should strengthen the implementation of energy and environmental policies to enhance the synergy and efficiency of pollution and carbon reduction. Additionally, local governments should provide targeted support for corporations implementing green transformation, fully leveraging the enthusiasm of non-state-owned and non-heavily-polluting corporations. Incentive policies should be precisely designed to support these corporations in effectively implementing green transformation strategies.

Third, market regulatory agencies should strengthen the supervision of corporations’ green transformation practices and the disclosure of related information, establishing a fair and effective information disclosure system. CGT enhances a corporation’s social image and demonstrates strong environmental and social performance. Regulatory authorities should encourage corporations to implement green transformation, guiding capital market funds toward corporations actively practicing CGT. By doing so, CGT enables investors to “vote with their feet” or “vote with their money,” promoting the rational allocation of industrial capital. Furthermore, regulatory agencies should monitor disclosures to prevent corporations from using illegal or improper practices to manipulate the positive tone or incremental information associated with green transformation. The practice of “green-washing” involves misleading disclosure of environmental information, which can distort the true signals of the green market. Regulatory agencies should establish a system to prevent corporate green-washing, including a supervision framework for institutional investors and small and medium-sized shareholders. Authorities should strengthen measures to prevent collusion or fraud between non-green institutions and corporations, enhancing the collaborative governance role of the public, the market, and investors in preventing corporate green-washing behaviors.

This study was characterized by several limitations. First, it focused solely on Chinese A-share listed companies and considered China-specific factors, such as Hua-zheng ESG data and corporate ownership characteristics. Therefore, the differences in CGT practices between China and other countries may limit the international applicability of the findings in promoting CSD. Second, CGT relies on supportive policies and resource allocations to exert stronger impacts on CSDP. However, this study cannot confirm whether such policy and resource supports effectively facilitate the spread of favorable corporate financial and environmental governance outcomes. Future research should explore the role of crucial policies and resource supports, and their dynamic interactions, in promoting CSDP. This would provide effective empirical insights that could extend the applicability of the findings to other countries and regions.

Footnotes

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The authors are grateful for the research support from the following foundations: Humanities and Social Change Funds of the Ministry of Education of China (25YJC790008).

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

Data sharing not applicable to this article as no datasets were generated or analyzed during the current study.