Abstract

Against the backdrop of global high-quality economic development and technological innovation, digital transformation, as a core driver for cultivating new quality productivity, has drawn academic and industrial attention for its potential to enhance corporate financial performance. The widespread application of digital technologies is reshaping corporate operational models, while environmental, social, and governance (ESG) concepts have increasingly become critical guidelines for corporate sustainable development. Clarifying the intrinsic relationships among these three elements is of profound significance. Using 2014 to 2023 data from A-share manufacturing listed firms in China, this study empirically examines how digital transformation impacts financial performance, focusing on ESG’s mediating role via panel data and regression models with third—party ESG ratings. Results show digital transformation significantly boosts both ESG and financial performance, with strong ESG performance driving financial growth. ESG partially mediates this relationship. Heterogeneity analysis reveals stronger mediating effects in non-state-owned, high-tech, and economically developed-region firms. This study illuminates the impact of digital transformation on financial performance and the mediating role of ESG, enriching the academic discourse on digital transformation. The findings provide critical references for corporate strategic decision-making and policy formulation, offering insights into integrating digital transformation initiatives with ESG practices to drive sustainable development.

Plain Language Summary

Nowadays, promoting high-quality economic development and technological innovation has become a key priority, and enterprises’ digital transformation (such as the application of technologies like cloud computing and big data) and ESG performance (focusing on environmental protection, social responsibility, and corporate governance) are increasingly critical to their long-term development. This study focuses on Chinese A-share listed manufacturing companies from 2014 to 2023, exploring the relationships between digital transformation, ESG performance, and financial performance. The study found that digital transformation in manufacturing enterprises can not only directly improve financial performance such as profits and market value, but also enhance their ESG performance. Moreover, better ESG performance can contribute to improving financial performance. This means that ESG plays an “intermediary” role in this process. Notably, this intermediary role of ESG is more prominent in non-state-owned enterprises, high-tech manufacturing enterprises, and enterprises located in economically developed regions. In general, digital transformation positively impacts enterprises’ ESG performance and financial performance, while ESG helps transmit part of the benefits of digital transformation to financial outcomes. This study suggests that the government should support enterprises’ digital transformation and standardize ESG information disclosure, and that enterprises themselves should integrate digital transformation with ESG practices to achieve sustainable development.

Introduction

Driven by the dual forces of the digital technology revolution and deepening globalization, the global digital transformation is advancing at an unprecedented pace. Cutting-edge technologies such as cloud computing, artificial intelligence, and big data are not only reshaping corporate value chains but also giving rise to new paradigms, including intelligent operations, data-driven decision-making, and platform-based business models. These technological advancements have enhanced total factor productivity (Liu et al., 2025), financing efficiency (W. Li & Zhan, 2025), investment efficiency (Tian, 2024), and innovation performance (P. Li & Pan, 2025). In terms of financial performance, digital transformation strengthens dynamic adaptability, optimizes resource allocation and information flows (Rialti et al., 2019), reduces transaction costs (Wu & Yao, 2023), improves operational efficiency and internal control (Z. Li, 2023), enhances total factor productivity (Zhao et al., 2021), optimizes human capital structure (T. Xiao et al., 2022), fosters business model innovation (Bouwman et al., 2019), and stimulates innovation output (Bai et al., 2022). Simultaneously, it reinforces corporate social responsibility (H. Xiao et al., 2021), cultivates innovation capacity (Pan et al., 2022), and improves governance mechanisms (Lin et al., 2023), thereby elevating non-financial performance. According to the Global Digital Economy Development Research Report (2024), global spending on digital transformation exceeded $2.1 trillion in 2023, accounting for over 52% of total global investment, underscoring its strategic role in economic transformation.

Meanwhile, the Environmental, Social, and Governance (ESG) framework has emerged as a cornerstone of global sustainable development, deeply integrated into corporate strategy and operations. This paradigm expands the scope of value creation beyond economic gains to encompass social and environmental benefits, balancing the legitimate interests of stakeholders. On the environmental front, companies adopt measures such as energy conservation, emissions reduction, and circular resource utilization to address climate challenges, which not only mitigate risks but also strengthens long-term resource access and supply chain resilience. Socially, firms are expected to uphold employee rights, support community development, and promote equity, enhancing brand reputation, talent attraction, and consumer loyalty. In governance, robust structures, transparent disclosure, and compliance mechanisms lay the institutional foundation for sustainable growth. Empirical studies demonstrate that strong ESG performance reduces financing costs (L. Wang et al., 2022), attracts investor preference (Zhou et al., 2020), and unlocks new market opportunities.

Against this global backdrop, China presents distinct policy and practical characteristics. On one hand, the state has elevated the digital economy to a strategic priority, evidenced by the State-Owned Assets Supervision and Administration Commission’s (SASAC) directives on digital transformation for state-owned enterprises, the 20th Party Congress’s emphasis on integrating digital and real economies, and the Government Work Report’s push for intelligent upgrades in traditional industries. On the other hand, ESG practices are accelerating, with the China Securities Regulatory Commission (CSRC) mandating enhanced ESG disclosures in 2022 to embed sustainability into corporate decision-making. As the backbone of the national economy, China’s manufacturing sector—characterized by high capital intensity and extended supply chains—exhibits vast disparities in digital maturity, offering rich research samples. Made in China 2025 is an action plan for implementing the strategy of building a manufacturing power, and digital transformation has become the inevitable path for the transformation and upgrading of manufacturing enterprises. Its transformation experience holds unique insights for global industrial upgrading, particularly in ESG integration.

However, existing research has limitations. First, most studies focus narrowly on either digital transformation’s impact on financial performance or ESG’s financial implications, failing to integrate these three dimensions. Second, sector-specific analyses, particularly in manufacturing, remain scarce. Addressing these limitations, this study constructs a “digital transformation—ESG performance—financial performance” framework for Chinese manufacturers, elucidating ESG’s mediating role. The contributions of this paper may be primarily reflected in the following two aspects: First, existing literature mainly focuses on single-dimensional studies of the impact of corporate digital transformation on ESG or financial performance. This paper takes ESG as the entry point, integrates the three dimensions of corporate digital transformation, ESG, and financial performance, and explores the mediating effect of ESG between digital transformation and financial performance. Second, there is currently a lack of literature on digital transformation research in specific industries. By focusing on empirical analysis of Chinese manufacturing enterprises, this study ensures that the research results have industry-specific characteristics, providing theoretical support and practical guidance for manufacturing enterprises to advance digital transformation and achieve high-quality development.

Theoretical Analysis and Research Hypotheses

Enterprise Digital Transformation and Financial Performance

Based on the Resource-Based Theory, the heterogeneous resources within an enterprise are the fundamental source for building the enterprise’s sustainable competitive advantage (Barney, 1991). An enterprise’s active promotion of digital transformation helps to form its own structurally scarce resources, thereby generating compound advantage, creating the enterprise’s heterogeneous competitive advantage, and driving the improvement of its financial performance (Brynjolfsson & McElheran, 2016). Its mechanism is reflected in: digital technologies are integrated into the entire production and operation process, realizing intelligent management of the whole process and optimizing the operational efficiency of each link (Yin et al., 2022); digital interconnection brings about business model innovation, building differential competitive barriers and obtaining new competitive advantages, thereby promoting financial performance growth (Zhang et al., 2021); At the organizational level, the digital transformation must be deeply embedded in the enterprise’s strategic system rather than deployed in isolation to maximize the supporting role of digital resources in corporate value (Warner & Wäger, 2018). Accordingly, the first hypothesis is proposed:

Enterprise Digital Transformation and ESG Performance

ESG performance focuses on Environment, Social, and Governance (ESG), with a core emphasis on sustainable development that balances economic and social benefits while aligning with green and low-carbon goals. Within the theoretical framework of sustainable development, ESG performance has emerged as a critical dimension for gauging an enterprise’s sustainable development level. A review of relevant literature indicates that most scholars argue that enterprise digital transformation exerts a positive impact on ESG performance (Du & Li, 2024; H. Wang et al., 2023; X. Wang et al., 2023; Zhong et al., 2023). Additionally, some studies have found that the relationship between digital transformation and ESG performance is not purely linear (Kuang & Zhou, 2025; Zeng et al., 2023). In the practice of advancing digital transformation, integrating ESG concepts has become a key to achieving high-quality development goals for enterprises. Digital technologies enhance environmental performance by substituting data for natural resources, optimizing production processes, and reducing pollution (H. Wen et al., 2021). The introduction of digital tools improves the quality of social responsibility information disclosure, enabling more effective fulfillment of social obligations (Koo et al., 2020). The application of new digital technologies alleviates information asymmetry, reduces agency costs, and improves corporate governance. Thus, enterprise digital transformation can leverage digital technologies to enhance ESG performance. This leads to the second hypothesis:

Corporate ESG and Financial Performance

Based on the Stakeholder Theory, enterprises need to balance the interests of all parties. Enterprises with high ESG performance scores can easily establish good relationships with stakeholders and improve financial performance. For example, focusing on ESG performance can enhance employee cohesion and attractiveness (Tamimi et al., 2017). For investors, it can reduce risks and attract investment (Yu et al., 2022). For the government, such enterprises are more likely to obtain policy support. For consumers, it can enhance their sense of identity and loyalty. In addition, the Signaling Theory posits that in the context of information asymmetry, companies with good performance will convey positive signals to the market through information disclosure to distinguish themselves from those with poor performance. Compared with other enterprises, those with large scale and strong profitability have more resources and a greater willingness to disclose ESG rating information (Shen, 2007). Therefore, good ESG performance enhances corporate reputation, forms competitive advantages, and thus improves its financial performance. This leads to the third hypothesis:

The Mediating Role of ESG Performance

From the perspective of information circulation, digital transformation optimizes the information environment of enterprises, reduces information asymmetry, improves decision-making efficiency and transparency. On the one hand, digital platforms facilitate ESG performance disclosure, providing positive incentives for enterprises to enhance their social reputation and improve their financial performance. On the other hand, digitalization amplifies the impact of negative events, restraining opportunistic behaviors, prompting enterprises to optimize their decisions around green performance, social responsibility, and governance, thereby enhancing corporate value. From the perspective of capital cost, digital transformation reduces financing costs through ESG practices. Firstly, high ESG ratings alleviate information asymmetry and reduces the risk premium (Q. Li et al., 2023). Secondly, excellent ESG performance strengthens the corporate reputation, meets the expectations of regulatory authorities, makes it easier for enterprises to obtain financial support such as government subsidies, relieves financing constraints, and provides capital guarantee for the improvement of financial performance. Accordingly, the fourth hypothesis is proposed:

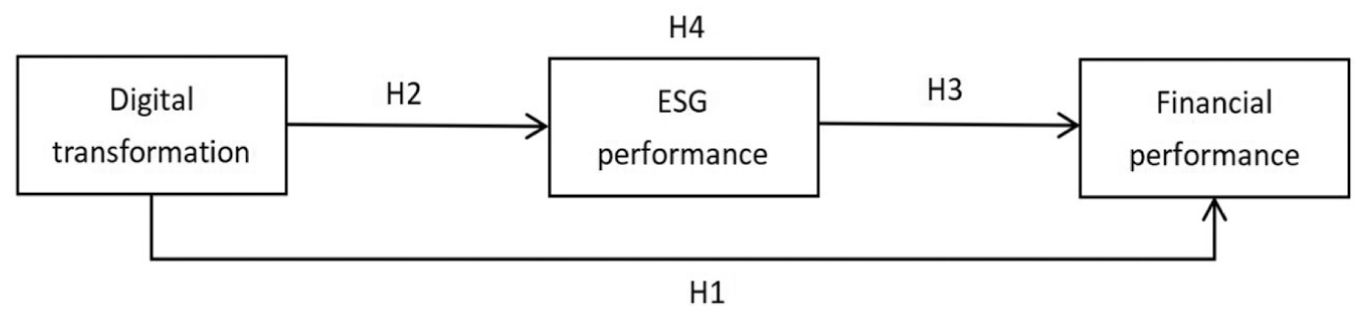

In conclusion, digital transformation has a positive impact on corporate financial performance through channels such as enhancing efficiency, optimizing decision-making, and innovating business models. Good ESG performance can build a better corporate image and gain higher recognition for the enterprise, further promoting the improvement of financial performance, and it plays a mediating role between digital transformation and financial performance. To this end, this paper constructs a research model as shown in Figure 1.

The research model.

Study Design

Sample Selection

This study centers on manufacturing companies listed in China’s Shanghai and Shenzhen A-share markets, spanning from 2014 to 2023. The data processing employed in this study involves several meticulous steps. Initially, companies with missing data for five consecutive years were excluded from the analysis to minimize the negative impact of data discontinuity and interruption on the study. Subsequently, ST and *ST companies were omitted because their financial conditions may not reflect typical market conditions. In addition, in order to minimize the effect of outliers, this paper winsorizes all continuous variables at the 1% and 99%, yielding a total of 14,084 data samples. These data samples are mainly from reputable databases, namely Wind and CSMAR.

Definition of Variables

Dependent Variable

Financial Performance (Perform). Drawing on existing literature (J. Li et al., 2021; J. Li et al., 2023), this study measures financial performance from short-term and long-term dimensions using Return on Assets (ROA) and Tobin’s Q Ratio (Tobin’s Q), respectively.

Independent Variable

Digital Transformation (DT). Drawing on existing literature (Zhao et al., 2021), the text analysis method is used to measure the intensity of digital transformation of enterprises. It is measured by the natural logarithm of the frequency of the occurrence of digital characteristic words in the annual reports of listed companies plus 1.

Intermediary Variable

Corporate ESG performance (ESG). Drawing on the approach in existing literature (Fang & Hu, 2023), the Huazheng ESG Rating is adopted to measure the ESG performance of listed companies, using a nine-point scoring system. Annual ESG performance is measured by the average of quarterly scores, where a higher score indicates better performance.

Control Variables

Drawing on relevant literature (J. Li et al., 2021; Liu et al., 2021), control variables such as firm size (Size), management expense ratio (Manage), leverage ratio (Lev), current asset ratio (Liquity), firm age (Age), ownership nature (Equity), and ownership concentration (First) are incorporated into the model. In addition, this paper controls for year-level (Year) and industry-level (Industry) fixed effects. As the research sample is derived from manufacturing listed companies, industry fixed effects are controlled for 31 sub-industries in accordance with the Classification of High-Tech Industries (Manufacturing; 2017) issued by the National Bureau of Statistics, and referring to the practices of other scholars (Qi & Cai, 2020). The precise definitions of these variables are outlined in Table 1.

Variable Definition.

Model Construction

To test the hypotheses presented earlier, this paper constructs the following baseline regression Model 1:

Among them, the dependent variable

To study the impact of digital transformation on ESG performance, this paper constructs the following regression Model 2:

To explore whether corporate ESG performance enhances corporate financial performance, this paper constructs the following regression Model 3:

In addition, in order to test the mediating effect of ESG performance between digital transformation and corporate performance, this paper draws on previous research methods (Z. Wen et al., 2004), combines Models 1 and 2, and constructs Model 4 for analysis. Model 4 is as follows:

Empirical Results

Descriptive Statistical Analysis

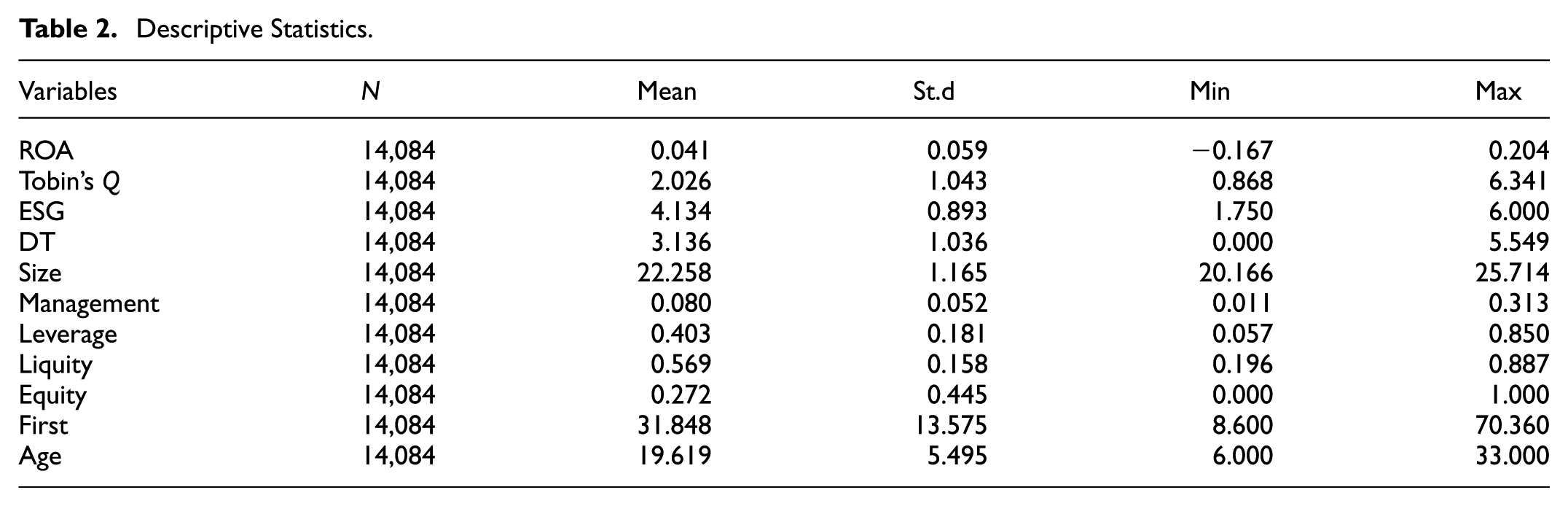

Based on the results of the F-test and the Hausman test, a two-way fixed effects model is selected as the method for the multiple regression analysis in this paper. Table 2 presents the descriptive statistical analysis. The mean value for ROA is 0.041, the minimum value is −0.167, and the maximum value is 0.204. The minimum value of Tobin’s Q is 0.868, the maximum value is 6.341, with a standard deviation of 1.043, showing that there is a large gap in the financial performance levels among enterprises, and there is still significant room for improvement in the overall profitability. The mean score for ESG is 4.134, corresponding to a B grade in the rating, suggesting that the overall ESG performance of manufacturing enterprises is at a moderately low level. The mean value of DT is 3.136, and the standard deviation is 1.036, indicating that the distribution of the digital transformation degree of the sample enterprises is relatively dispersed, with significant differences in digital transformation performance across enterprises. Based on the descriptive statistics of the control variables, the distributions of all variables fall within the normal range. In addition, the Variance Inflation Factor (VIF) of each variable is less than 10, so the presence of severe multicollinearity among variables is ruled out.

Descriptive Statistics.

Basic Regression Analysis

Table 3 presents the regression results for the relationship among digital transformation, ESG performance, and financial performance. Columns (1) and (2) indicate that the coefficient of DT is significantly positive at 1%, suggesting that digital transformation has a positive impact on both short-term and long-term financial performance and thus verifying H1. Column (3) shows that the impact coefficient of DT on ESG is 0.086 and passes the significance test at the 1% level, indicating a significant positive correlation between digital transformation and ESG performance, and thus verifying H2. Columns (4) and (5) reveal that ESG significantly promotes financial performance: the impact coefficient of ESG on ROA is 0.008, and that on Tobin’s Q is 0.057, both of which pass the significance test at the 1% level, supporting H3. Columns (6) and (7) show that after introducing the mediating variable of ESG, the coefficient between digital transformation and financial performance decreases but remains significant with the same sign, and there is still a significant positive relationship between ESG and financial performance. This indicates that ESG plays a partial mediating role in the relationship between digital transformation and financial performance, meaning that digital transformation can promote the development of ESG, which in turn drives the improvement of corporate financial performance. Hypothesis H4 is thus verified. It can also be found from Table 3 that when digital transformation changes by 1 unit, ROA and Tobin’s Q will change by 0.005 and 0.054 units respectively. Among them, 0.001 and 0.004 are the effects of digital transformation on ROA and Tobin’s Q through the mediating variable of ESG, respectively. The mediating effects account for 20% (i.e., 0.001/0.005) and 7.41% (i.e., 0.004/0.054) of the total effects, respectively.

Basic Regression Results.

Note. *, **, and *** represent 10%, 5%, and 1% significance levels, respectively, with t-values adjusted for firm -level clustering in parentheses. Under same.

Robustness Test

To verify the robustness of the results obtained from the aforementioned model, this study employs three robustness testing methods.

Replacing the Core Explanatory Variable

Drawing on existing research (Song et al., 2024), this paper uses the entropy method to construct a new-quality productivity index, which serves as a proxy variable for enterprise digital transformation (NPRO). Table 4 presents the regression results of Model 1, Model 2, and Model 4 after replacing the core explanatory variable. The research conclusions remain unchanged.

Robustness Test Results for Replacing Core Explanatory Variables.

Replacing the Measurement Method of the Explained Variable

Drawing on existing practices (J. Li et al., 2021), return on assets (ROA) and Tobin’s Q value (Tobin’s Q) are replaced with return on equity (ROE) and price-to-book ratio (PB). As shown in Table 5, when digital transformation changes by 1 unit, ROE and PB change by 0.010 and 0.114 units respectively. Of these, 0.001 and 0.011 are the effects of DT on ROE and PB, respectively, through the mediating variable ESG. The mediating effects account for 10% (0.001/0.010) and 9.65% (0.011/0.114) of the total effects respectively.

Robustness Tests for Replacing Explained Variables.

Lagging the Explanatory Variable by One Period

Given the strategic investment nature and long-term sustainability of digital transformation, its economic consequences may exert a significant lagged impact on enterprises’ ESG and financial performance through a long-term transmission mechanism. Therefore, a robustness test is conducted with the digital transformation lagged by one period. As shown in Table 6, when digital transformation changes by 1 unit, ROA and Tobin’s Q change by 0.003 and 0.046 units respectively. Of these, 0.001 and 0.006 are the effects of DT on ROA and Tobin’s Q, respectively, through the mediating variable ESG. The mediating effects account for 33.33% (0.001/0.003) and 13.04% (0.006/0.046) of the total effects respectively.

Lagged One Period Robustness Test Results for Explanatory Variables.

Endogeneity Test

The endogeneity issues in this paper primarily arise in the relationship between digital transformation and corporate financial performance, potentially involving problems of bidirectional causality and sample self-selection. Therefore, this paper employs the instrumental variable (IV) method and the Propensity Score Matching (PSM) method for endogeneity testing.

Instrumental Variable (IV) Method

There may be a reciprocal causal relationship between enterprise digital transformation and financial performance: digital transformation promotes the improvement of financial performance, while the improvement of financial performance provides financial support for digital transformation. Drawing on existing literature (Bai et al., 2022; Larcker & Rusticus, 2010), this paper uses the mean value of digital transformation degrees of other enterprises in the same industry and the same year as the instrumental variable for the digital transformation degree of the enterprise under study in that year. A two-stage least squares estimation is conducted on this variable, with results presented in Table 7. The results of the first-stage regression indicate that the instrumental variable (IV) has a significantly positive correlation with DT at the 1% significance level. The value of the F-statistic is 13.90, which is greater than 10. Moreover, it has passed the weak instrumental variable test and the under-identification test of instrumental variables, confirming the validity of the instrumental variable selection. The results of the second-stage regression show that the coefficients of corporate digital transformation with ROA and Tobin’s Q are both positively correlated, which is consistent with the previous research conclusions. That is, after considering the possible impacts of the endogeneity problem, the conclusion that a higher degree of digital transformation can significantly improve corporate financial performance still holds.

Results of the Instrumental Variable Method Test.

Propensity Score Matching (PSM)

Enterprises with a higher level of digital transformation may inherently have better financial performance, and this potential sample self-selection issue may affect the accuracy and reliability of research results, leading to estimation bias. To effectively address this interference, this paper follows the approach of previous studies (J. Li & Wang, 2023; Y. Wang & Guo, 2023) and uses PSM for endogeneity testing. First, a dummy variable is created using the median of digital transformation degree: samples above the median form the treatment group, and those below form the control group. Control variables are used as characteristics for 1:1 nearest-neighbor matching. When the dependent variable is ROA, the matching results are presented in Table 8. The T-tests show significant p-values before matching (U), indicating notable differences between the treatment and control groups, which meets the balance test criteria. After matching (M), the standard deviations of covariates decrease significantly, with the percentage reduction in bias exceeding 90% for most variables. The p-values of T-tests all exceed .05, suggesting no significant inter-group differences. Overall, the balance of variables is significantly improved after PSM, verifying the effectiveness of the matching method and providing robust support for the reliability of subsequent regression results. The same conclusion holds when Tobin’s Q is used as the dependent variable. Fixed-effect regression on the matched samples (Table 9) shows digital transformation coefficients for ROA and Tobin’s Q remain significantly positive, confirming its promotion of financial performance and robustifying prior findings.

PSM 1:1 Matching Results.

PSM Regression Results.

Heterogeneity Analysis

To verify whether the mediating effect of ESG performance between DT and financial performance varies with enterprise heterogeneity, this paper conducts grouped regression analyses on enterprises based on the nature of property rights, technological attributes, and regional nature, respectively. The results are as follows.

Based on Nature of Property Rights

In this paper, a dummy variable of state-owned and non-state-owned enterprises is introduced. By comparing Columns (2) and (5) of Table 10, the positive promoting effect of DT on financial performance is more significant in non-state-owned enterprises. Combining the regression results of Columns (3) and (6), the partial mediating effect of ESG is more significant in the relationship between DT and financial performance of non-state-owned enterprises (the proportions of the mediating effect of ESG in non-state-owned enterprises are 20% and 8.77% respectively, whereas the mediating effect of ESG in state-owned enterprises is not significant in the test of Tobin’s Q). Non-state-owned enterprises have a more urgent need to ease financing constraints and are not subject to rigid policy constraints. Thus, they rely on their own ESG performance under market mechanisms, serving as a market competition signal. By reducing information asymmetry, they can attract investors and consumers, thus magnifying the financial gains from DT.

Results of Heterogeneity Test Based on Nature of Ownership.

Based on Technical Attributes

In this paper, a dummy variable of high-tech and non-high-tech enterprises is introduced. By comparing with Column (1) of Table 11, the positive promoting effect of the degree of DT on ESG performance is more significant in non-high-tech enterprises than in high-tech enterprises. By comparing Columns (2) and (5), the positive promoting effect of the degree of DT on financial performance is more pronounced in high-tech enterprises. Combining the regression results of Columns (3) and (6), in high-tech enterprises, ESG’s partial mediating effect is more pronounced in the DT-corporate performance relationship (the proportions of the mediating effect of ESG in high-tech enterprises are 20% and 4.41% respectively, and the mediating effect of non-high-tech enterprises is not significant in the test of Tobin’s Q). High-tech firms, with higher R&D investment and an open innovation ecosystem, facilitate process reconfiguration and tech commercialization in DT. Good ESG performance attracts technology-focused capital and optimizes governance, enabling DT to more effectively drive positive financial outcomes.

Heterogeneity Test Results Based on High-Tech Firms.

Based on Regional Characteristics

This paper introduces a dummy variable of eastern region and central-western region enterprises. By comparing with Column (1) of Table 12, the positive promoting effect of the degree of DT on ESG performance is more significant in enterprises located in the central and western regions. From Columns (2) and (5), the positive promoting effect of the degree of DT on financial performance is more pronounced in enterprises in the eastern region. Combining the regression results of Columns (3) and (6), compared with enterprises in the central and western regions, the mediating effect of ESG is more significant in the relationship between DT and financial performance of enterprises in the eastern region (the proportions of the mediating effect for enterprises in the eastern region are 20% and 6.45% respectively, and the mediating effect of enterprises in the central and western regions is not significant in the test of Tobin’s Q). Manufacturing enterprises in developed regions leverage the complete digital infrastructure to achieve more efficient digital transformation. Their ESG performance can be more easily converted into market reputation and financing advantages, thereby generating positive financial performance.

Heterogeneity Test Results Based on Firm Location.

Conclusion and Recommendations

This study is based on the annual data of manufacturing listed companies on the Shanghai and Shenzhen A-share markets from 2014 to 2023 in China, and deeply explores the complex relationships among corporate digital transformation, ESG performance, and financial performance. The research findings indicate that digital transformation exerts a substantial positive influence on the ESG performance and financial performance of manufacturing enterprises. The positive ESG performance of manufacturing enterprises has been found to have a substantial impact on enhancing their financial performance, with ESG performance playing a partial mediating role in this relationship. The heterogeneity analysis reveals that the mediating effect of ESG performance between digital transformation and financial performance is more significant in non-state-owned enterprises, high-tech enterprises, and enterprises in economically developed regions.

Based on the preceding analysis, to facilitate the digital transformation of manufacturing enterprises, enhance their financial performance, and ultimately achieve high-quality and sustainable development, this study proposes the following suggestions from both corporate and governmental perspectives. Firstly, the government plays a crucial role in promoting enterprises development. It should vigorously advance the digital transformation of enterprises by building technology exchange platforms and providing financial support to help enterprises overcome transformation challenges. Meanwhile, the government should strengthen policy guidance, standardize the ESG information disclosure of enterprises, raise enterprises’ attention to ESG performance, and create a favorable market environment. In addition, the government needs to improve digital-related policies and regulations, optimize infrastructure construction, encourage the sharing of innovation achievements, cultivate and introduce digital talents, and adopt a multi-pronged approach to promote the digital transformation and sustainable development of enterprises. Secondly, the manufacturing enterprises should seize the opportunities of the digital economy, make full use of artificial intelligence technologies such as “AI+,” and advance the coordinated development of digital transformation and high-quality development. They must uphold the concept of long-term value growth, leverage digital technologies to enhance ESG performance, and strengthen information disclosure and communication. Advanced manufacturing enterprises should take a leading role. State-owned enterprises should take the initiative in transformation and assist other enterprises. High-tech enterprises and those in developed regions should share their achievements and experiences, driving the digital transformation of the entire industry and fostering a sound ecosystem for sustainable development.

Despite the contributions of this research, it is important to acknowledge its limitations. Firstly, ESG performance relies on third-party rating data, which may be affected by enterprises’“greenwashing” behaviors. Secondly, the sample enterprises are limited to manufacturing firms, and its applicability to other industries remains to be verified. Looking ahead, future research can expand the sample to include more industries and enterprises of different sizes to further verify the robustness of the findings. Exploring more accurate and comprehensive measurement methods for digital transformation and ESG performance will provide more reliable data support for related research.

Footnotes

Ethical Considerations

This study was conducted strictly in accordance with ethical guidelines and did not interact with any identifiable private information.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was partially supported by the Open Fund Project of the Reservoir Resettlement Research Center of China (grant number 2025KF01).

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The data are available from the corresponding author upon reasonable request.