Abstract

Digital transformation (DT) is a long-term strategy for economic sustainability, particularly for manufacturing-oriented economies. This study proposes a digital ESG (DESG) theoretical framework to investigate how DT empowers ESG performance in the manufacturing industry. Using Python, we collected data from Chinese manufacturing firms from 2009 to 2020. This study used the ordinary least squares method to examine the relationships among DT, ESG performance, and manufacturing ESG heterogeneity. The results suggest that big companies and growing firms pay more attention to their ESG performance than others and that state-owned enterprises are keen on ESG performance but underperform. Additionally, DT may contribute to manufacturing ESG performance in general; labor-intensive and non-state-owned enterprises benefit more from DT than their counterparts; and manufacturers in economically developed regions show more significant ESG performance thanks to DT. These findings support the use of a DESG theoretical framework in the manufacturing industry whereby digital technologies facilitate business production and improve the business profits of manufacturing firms, so that manufacturers have sufficient profits to conduct ESG investments for sustainable development in a virtuous cycle.

Introduction

The United Nations announced in 2015, “The 2030 Agenda for Sustainable Development”, which called for sustainable development in all countries. To achieve this goal, the performance associated with sustainability of any organization is assessed using the ESG (environmental, social, and governance) approach (Naffa & Fain, 2020). Since then, ESG has become a complex but very crucial strategy for sustainable development across the world, particularly in the post-COVID-19 era, during which business development was interrupted; each enterprise should have strong environmental awareness, take more social responsibility, and establish a sound governance system to initiate a sustainable business ecosystem.

The ESG concept has attracted a wide range of studies since then, including research in the institutional context (Baldini et al., 2018), on investor preference (Jiang et al., 2022), customer benefits (Akram et al., 2021), digital finance (Mu et al., 2023), etc. The systematic literature review by Daugaard (2020) documents five key strands of research on ESG, including the heterogeneous nature of ESG investment, ESG investment costs, ESG investment motivations, ESG contributions to business management, and ESG performance measurement. It also shows five emerging themes: emerging non-Western investors, human-associated elements, fund flow-oriented perspectives, climate change-based factors, and fixed income-specific factors. In addition, more recent studies discuss ESG disclosure (E. P. Yu & Luu, 2021), the ESG effect on stock markets (Baker et al., 2021; Luo et al., 2022), and the relationship between ESG performance and corporate governance (Agnese & Giacomini, 2023; Z. Chen & Xie, 2022; Gigante & Manglaviti, 2022). All in all, the published research dominantly investigates ESG characteristics and prefers to examine ESG effects on some other factors.

However, little research has shed light on solutions for the improvement of manufacturing ESG, although a comprehensive review study by Gillan et al. (2021) uncovers some factors from various perspectives, such as market characteristics, executive compensation, firm performance and value, ownership, and firm risk. Additionally, Du and Jiang (2022) support the existence of a positive relationship between digital transformation (DT) and firm productivity in Chinese enterprises. Saxena et al. (2023) suggest that advanced technologies empower ESG performance from an Industry 4.0 perspective. The advanced e-learning technologies may contribute to sustainability in the new normality era (Fülöp et al., 2022, 2023). Nevertheless, the baseline theoretical framework of DT as an ESG solution in the specific manufacturing industry has been investigated less often.

This is a vital topic because the economy of developing countries is mostly driven by the manufacturing industry, and economic sustainability in merging nations depends on sustainable manufacturing. Additionally, developing economies are characterized by industrialization, so ESG investment in the manufacturing industry is crucial for economic sustainability in developing countries. Empirical evidence shows that during the COVID-19 outbreak, poorly digitized institutions were fragile, while high-level-digitization organizations were quite flexible (Fletcher & Griffiths, 2020). Accordingly, this study bridges this gap and proposes upgrading ESG to digital ESG (DESG) as a solution for sustainable development in the manufacturing industry. By sampling Chinese manufacturing firms, it further examines how digitization contributes to ESG performance in the manufacturing industry.

Studies investigating the heterogeneity of DT effects on ESG performance are few and far between (no related research could be found in Google Scholar by searching for “ESG spatial heterogeneity”), although the digitization contribution to economic growth from a macro-perspective and to ESG performance from a micro-perspective has been extensively discussed in general. This study bridges the gap to investigate how DT differently contributes to ESG performance in the manufacturing industry in different manufacturing aspects, such as ownership, labor intensity, and spatial heterogeneity. Manufacturers from different regions with different economic and business contexts have various DT demands and ESG awareness, so the general findings from existing studies may not address heterogeneity.

China, as the global leader in manufacturing operations, has achieved remarkable development over recent decades (L. Li, 2013). China’s manufacturing industry consists of 31 categories with 609 sub-categories, fully covering the whole industrial chain of the major categories. Thus, this study, which is based on China’s manufacturing industry, has reference value for other manufacturing-oriented countries. Since the concept of Industry 4.0 transforming machine-dominant into digitization-driven manufacturing was introduced in Germany in 2011 (Aceto et al., 2020), DT has been encouraged by the majority of manufacturing firms, because it can boost enterprise profitability (Du & Jiang, 2022). Additionally, emerging environmentally friendly technologies, such as the Internet of Things (IoT) and cloud computing, may also facilitate sustainable development with less pollution in the long run. Especially during the outbreak of the COVID-19 pandemic, DT facilitated working from home, online teaching, and online meeting; thus, its advantages are prominent and have attracted extensive discussions. On this basis, it is proposed that DT could contribute to the ESG performance of manufacturing firms in developing countries. This study aims to address this question.

Building on the argument above, this study proposes a digital ESG (DESG) theoretical framework to investigate how DT empowers ESG performance in the manufacturing industry. Using Python, we collected data from Chinese manufacturing firms from 2009 to 2020, and we employed the ordinary least squares (OLS) method to examine the relationships among DT, ESG performance, and manufacturing ESG heterogeneity. The results show that DT may contribute to manufacturing ESG performance in general, that labor-intensive and non-state-owned enterprises benefit more from DT than their counterparts, and that manufacturers in economically developed regions show more significant ESG performance thanks to DT. This research presents a DESG theoretical framework whereby digital technologies facilitate business production and improve the business profits of manufacturing firms, so that manufacturers have sufficient profits to invest in ESG for sustainable development in a virtuous cycle.

The research contributions are threefold: First, this study demonstrates a baseline theoretical framework whereby DT contributes to manufacturing ESG performance in developing counties, called DESG theory. This theory can be viewed as a favorable solution for ESG improvement in the manufacturing industry. Second, it uncovers the heterogeneity of DT effects on manufacturing ESG performance in terms of ownership, labor intensity, and spatial aspects. This research also expands the relevant research on the economic spillover effects of DT. Third, as China has the vast majority of industrial chains, this study, which is based on China’s manufacturing industry, has reference value for the sustainable development of manufacturing-driven developing economies. The findings are helpful for policy makers and enterprise managers in developing countries to use DT to promote energy conservation and emission reduction in enterprises, and provide a certain theoretical reference and method reference for realizing green transformation and low-carbon goals.

Theoretical Framework and Hypotheses

From a macro-perspective, digital infrastructures significantly facilitate economic growth in developed and developing countries (Shiu & Lam, 2008), and their contribution penetrates the industry in the Industry 4.0 era as the manufacturing industry upgrades from an equipment-dominated model to a digitization-oriented model (Aceto et al., 2020), namely, it undergoes digital transformation. DT refers to using new digital technologies to improve major businesses by, for example, creating new business models, satisfying customer demands, increasing firm performance, etc. (Fitzgerald et al., 2014).

As Route 1 in Figure 1 shows, these novel technologies include artificial intelligence (AI), data mining, cloud computing, the IoT, block chain, etc., and may contribute to ESG improvement. These digital technologies play a crucial role in accurate ESG reporting, and ESG investment is associated with AI capabilities (Saxena et al., 2023). In addition, Sætra (2023) argues that the AI ESG protocol is a solution for ESG assessment and disclosure. D’Amato et al. (2022) employed a machine learning approach to assess the effect of financial balance sheets on the ESG score. Furthermore, Big Data have been widely used for ESG reporting (Lee & Kang, 2016). Landaluce et al. (2020) suggest that IoT devices facilitate the collection of real-time data for ESG assessment. Liu et al. (2021) assert that a block chain-based framework can be helpful for ESG evaluation. Thus, ESG improvement is significantly related to digital technology development.

A route map of DT contributions to digital ESG in the manufacturing industry.

Route 2 in Figure 1 shows that some literature studies document the relationship between DT and ESG performance from the perspectives of the environment, social responsibility, and corporate governance. P. Chen and Hao (2022) evidence that DT may remarkably promote the corporate environment in Chinese listed firms and that DT willingness is determined by various firm board structures promoting national diversity, different political connections, age diversity, etc. Burritt and Christ (2016) argue that the technological process of Industry 4.0 has motivated a comprehensive digital revolution in general, which could eventually contribute to environmental conservation. Furthermore, Gupta et al. (2020) demonstrate that cloud computing technology such as cloud ERP systems could optimize resource utilization and accordingly contribute to environmental performance. Furthermore, DT may not only cultivate environmental awareness of consumers in terms of shopping activities (D. Li & Shen, 2021) but also motivate environmental innovation, because personalized products cater to customer demands and accordingly maximize product value for both consumers and manufacturers (Varadarajan, 2020).

In terms of social responsibility, Baker et al. (2021) document that green innovation and technological improvement motivate enterprises to take more social responsibility, because DT facilitates recognizing and acquiring information from shareholders, consequently promoting information disclosure quality. Consistently, employees in social responsibility-engaged firms are more motivated to improve new production processes and look for new technologies and methods (Broadstock et al., 2020). Especially during the COVID-19 lockdown period, digital technologies played a remarkable role in social responsibility within business sustainability, as in the cases of working from home, online shopping (Wade & Shan, 2020), and online studying (Fülöp et al., 2022). Accordingly, the association between DT and social responsibility has been strengthened.

Regarding corporate governance, digital transformation contributes to the operating performance of manufacturing firms, because DT facilitates manufacturers in dynamically monitoring the production process and ultimately improving firm operating performance. Jabbour et al. (2018) discuss some crucial determinants for the integration of DT and environmentally sustainable manufacturing and support the existence of a positive relationship between them, because digital technologies could provide firm managers with real-time information about production, logistics, and customer services; thus, this efficient business environment could promote sustainable development. Additionally, excellent ESG performance not only can maximize shareholder value, but it can also maximize firm lawsuits, so that firms have more capital for corporate governance (Albuquerque et al., 2019). On the contrary, underperformance indicates an unsound governance system that may damage the interests of both internal and external stakeholders and result in a range of negative effects, such as decrease in firm value and interruption of firm sustainability (Jones, 1995).

Furthermore, DT contributions to corporate governance have been extensively discussed in other aspects. For instance, DT could contribute to productivity (Du & Jiang, 2022), financial performance (Hajli et al., 2015), competitiveness advantages (Benner & Waldfogel, 2023; Bruce et al., 2017), and innovation performance (Ferreira et al., 2019; Usai et al., 2021). Therefore, outstanding governance performance may promote firm profit and value, resulting in firms having more capital to pursue ESG investment. Therefore, this development concept calls for managers to pursue the upgrading of technologies in the digitalization era.

However, specific studies discussing how DT improves the ESG performance of manufacturing firms are scarce (Route 3 in Figure 1), and there are no existing literature studies directly theorizing the relationship between digital transformation and manufacturing ESG. The indirect relationship can be theorized through Route 1, Route 4, and Route 5, respectively. As discussed above, DT upgrades manufacturing technologies that improve business performance (Du & Jiang, 2022), so that outstandingly performing manufacturers have sufficient money for ESG investment (Aich et al., 2021), as indicated by Route 4; furthermore, economic returns motivate stakeholders to consider ESG performance for sustainable development in the long run.

Based on the above, a DESG theoretical framework for the manufacturing industry is inferred for Route 3 and investigated in this paper. Digital technologies facilitate business production and improve the business profits of manufacturing firms, so that manufacturers have sufficient profits to invest in ESG for sustainable development. Such ESG performance may promote manufacturers’ social reputation and strengthen firm competitiveness, consequently increasing firm value. This virtuous cycle facilitates the sustainable development of manufacturers. This study proposes the below hypothesis.

H1: The greater the digital transformation is, the better the ESG performance of manufacturing firms in developing economies is.

The heterogeneity of DT effects on ESG performance manifests as labor intensity, spatial differences, and ownership. Manufacturing, as an economic driver in developing countries, has characteristic heterogeneity in terms of labor intensity, spatial characteristics, and ownership (Huang et al., 2021). Heterogeneity can result in different effects of DT on ESG performance, so general findings that lack heterogeneity analyses would be unable to address these aspect-specific issues. This study conducted an in-depth analysis to investigate heterogeneity in terms of labor intensity, spatial characteristics, and ownership.

In terms of labor intensity, labor is the most important advantage for manufacturing firms in developing countries, as economic growth may benefit from labor-intensive industries (Banerji, 1975). With the gradually growing labor cost, DT is an optimum option to address labor cost-related issues, through which manufacturers can save more money to invest in productivity and governance performance (Du & Jiang, 2022), which accordingly improves ESG performance. On the contrary, the effect of DT on ESG performance in less labor-intensive industries may be different. Additionally, DT application has remarkably increased labor wage in the manufacturing industry, but it has also reduced the employment rate, and this effect varies across industries (Dai et al., 2022). Graetz and Michaels (2018) report a similar finding, indicating that low-skill-based positions are more easily replaced by AI. This significant unemployment rate challenges the social responsibility of DT-orientated manufacturers; however, some studies suggest a positive relationship between DT and employment rates. Pissarides (2000) asserts that upgrading technologies drives economic growth, which generates a number of new jobs, which in turn increases employment demands (labor intensity).

Furthermore, in labor-intensive manufacturing firms, digital technologies facilitate assessing employee working performance with accuracy, which motivates their innovative potentials and increases their job satisfaction (Leonardi & Contractor, 2018); accordingly, this improves the firm ESG performance, because DT optimizes corporate governance, making insider information transparent, drawing attention to job performance, and making incomes fair (Marler & Dulebohn, 2005). Based on the above discussion, this study proposes a second hypothesis, reported below.

H2: The DT effects on ESG performance are more significant in labor-intensive manufacturing firms than in others.

From the spatial heterogeneity perspective, uneven regional development disparity manifests in many forms in the long run, such as economic, institutional, cultural, and social aspects (Breinlich et al., 2014). As DT is a new technology-based business process, its application and development need a large number of advanced technicians; developed regions may attract more technical talents than others, which potentially leads to DT implementation heterogeneity. Additionally, the disparity is associated with firm performance heterogeneity. Manufacturing firms in developed regions have more transparent governance information, stronger environmental awareness, and more social responsibility than others, which attracts more outside investors and increases firm value (Zhou et al., 2022). Thus, these firms are more likely to invest in ESG and achieve technological innovation.

The ESG options for manufactures in different regions vary and are determined by local economic, institutional, and cultural factors. Furthermore, local digitization varies because of these factors. Accordingly, the spatial heterogeneity of DT effects on ESG performance occurs. South China’s economy develops well with efficient institutions, where manufacturers regard public environmental awareness and social responsibility as important strategies. In addition, well-developed local economies support local fiscal expenditure on improving the business environment and funding manufacturers, which eases the financial pressure on firms, which consequently have more money to invest in ESG performance. Furthermore, manufacturers have more options to deal with their capital shortage in economically developed regions. In contrast, manufacturers in North China have fewer advantages because of underperforming local economies; the majority of manufacturers have no digitization awareness but may want to invest in ESG. Presumably, the DT effect on ESG in South China is more significant than that in North China.

Digital infrastructure disparity may also result in spatial heterogeneity. Comparably, the digital infrastructure is well constructed in South China, where the integration of digitization and production optimizes the industrial structure in the long run, accelerates digital transformation, and eventually drives high-quality economy (Tian & Li, 2022). All these outcomes contribute to the potential of ESG. As North China lags in these aspects, manufacturers have no motivation in terms of technological inputs and ESG investment. Therefore, a hypothesis on spatial heterogeneity is proposed below.

H3: The DT effects on ESG performance in developed South China economies are more significant than those in underdeveloped North China economies.

Regarding ownership heterogeneity, SOEs have greater access to financial support from the government and state-owned institutions (Shih et al., 2021), so they have no short-term capital pressure on business operation and have sufficient money to invest in ESG. Additionally, the marginal effect of ESG improvement is very low in SOEs. Furthermore, SOEs take more social responsibility for media coverage and political promotion, such as employment and environment protection (Hsu et al., 2021). On the other hand, non-SOEs have no incentives; they pursue short-term business and market returns (Zhou et al., 2022), risk management (Wen et al., 2022), and better financial performance (Z. Chen & Xie, 2022) and reduce information asymmetry between managers and shareholders (He et al., 2022). To achieve this target, non-SOEs implement DT programs to improve ESG performance, showing stakeholders development potential in the long run (M. Yu & Pan, 2010).

On the other hand, L. Xu et al. (2020) suggest that SOEs have significant agency issues deriving from managers who engage in ESG investment for their personal reputation and political connections. For instance, SOE managers overdo ESG investments for their political performance when national elections approach. This attempt results in a negative relationship between ESG performance and firm financial performance (Brammer et al., 2006). From this point of view, ESG performance in non-SOEs is more likely to be better than that in SOEs.

SOEs and non-SOEs have different DT purposes. SOEs have dual roles, acting as governors and participants; thus, the DT and ESG strategy is more motivated by institutional and political factors than economic ones (B. Wang & Yang, 2022). On the other hand, non-SOEs, as pure market participants, engage in ESG projects to pursue growing economic returns and market value. Therefore, the relationship between DT and ESG is stronger in non-SOEs than in SOEs.

As Shih et al. (2021) suggest, SOEs have greater access to financial support from the government and state-owned institutions, and sufficient financial support may facilitate DT. They are less likely to improve ESG performance by means of DT. In addition, it is unlikely for SOEs to obtain more economic returns from capital markets by means of DT (Wu et al., 2021). Non-SOEs, on the other hand, do not have these financial privileges, and they seek to achieve sustainable development by means of ESG improvement and obtain more funding from financial institutions in consequence. Therefore, non-SOEs have strong DT incentives and improve ESG performance by upgrading technologies. Based on the above discussions, this study suggests the below hypothesis.

H4: Compared with SOEs, DT contributes to ESG performance in non-SOEs to a great extent.

Having the comprehensive review above, Table 1 demonstrates the literature gaps marked with ☑, which few studies shed light on. While the existing studies mainly concentrated on Route 1 to 2 and 4 to 5 in Figure 1, except Route 3, which this research contributes to.

Summary of Comprehensive Literature Review.

There is no evidence to support the points upon the literature review for this study.

Data and Methodology

Data

Data were collected from some of China’s leading databases, including the China Stock Market & Accounting Research (CSMAR) database (https://cn.gtadata.com), the WIND database (https://www.wind.com.cn/portal/en/WDS/database.html), the MARK database (https://www.macrodatas.cn), and Shenzhen Securities Information Company (http://www.cninfo.com.cn/new/index). These databases have been extensively used by scholars (Cheung et al., 2013; X. Xu et al., 2018).

The initial 31,992 samples came from 2,816 manufacturing firms listed on China’s A-share during 2009 to 2020, and 20,147 samples were ultimately considered valid after various data treatment methods were applied: (1) removal of variable-deficient samples; (2) removal of ST and ST* firms (because of financial deficit in 1 and 2 years, respectively); (3) given the influence of some extreme data values, tail shrinkage of extreme values of all major variables by 1% and 99%; (4) removal of firms with unclear ownership; (5) removal of firms with an asset–liability ratio over 1.

Methodology

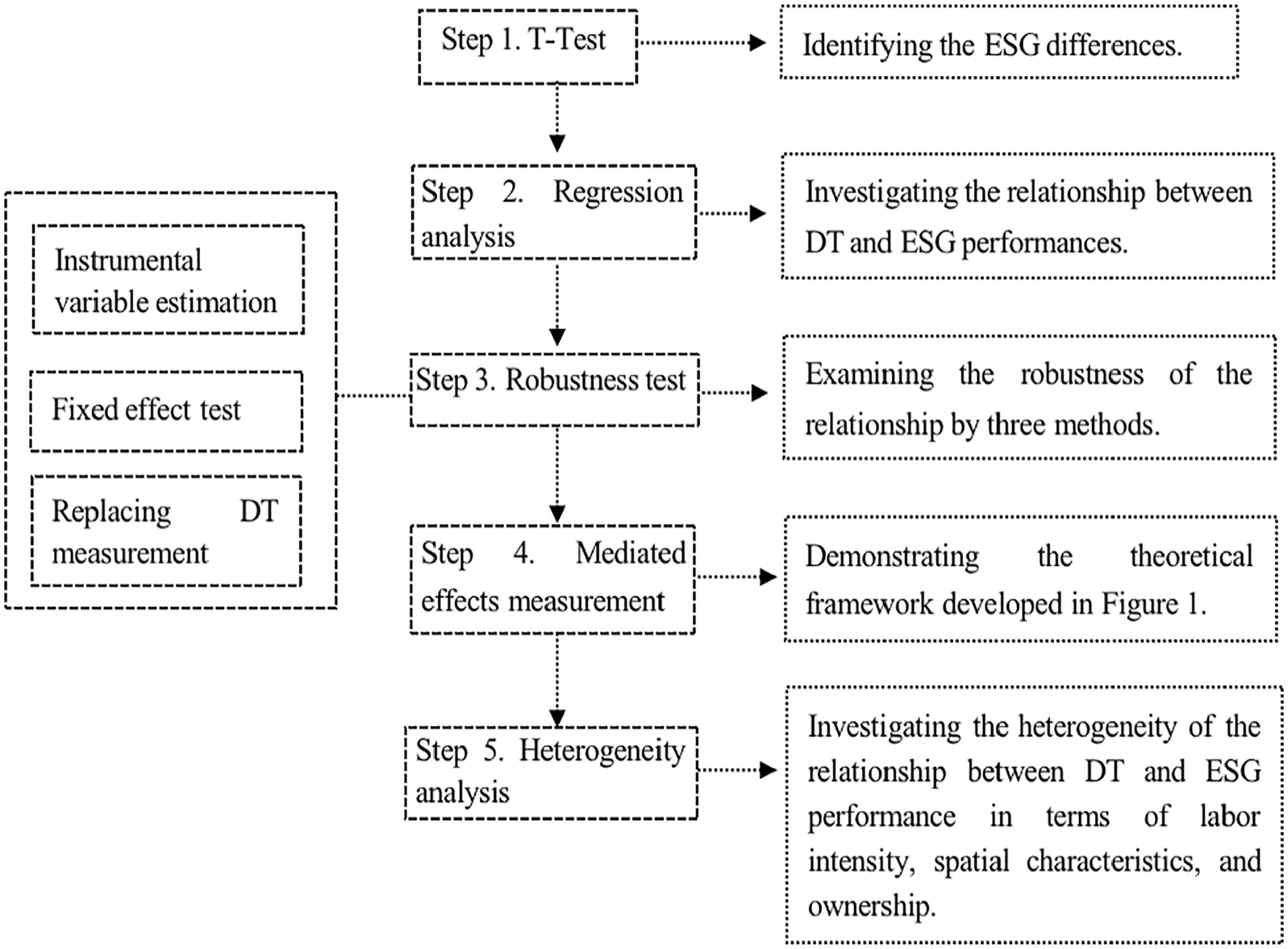

Figure 2 indicates a methodology flowchart. This study conducts a univariate T-test to assess ESG performance. After that, it investigates further what extent digitization improves ESG performance, followed by a robustness test to confirm the relationship between DT and ESG performance. Upon the findings, this study employs mediated effect model to investigate the conductive effect of DT on ESG performance by firm performance. Finally, this study conducts a heterogeneity analysis to offer insights into it in terms of labor intensity, spatial characteristics, and ownership, respectively.

Methodology flowchart.

Based on Khalid et al. (2021), this study developed an OLS regression model to investigate Route 3, which concerns the DT effects on ESG performance.

where DTS and lndts are the indicators measuring the degree of digital transformation of manufacturing companies, and ESG and lnESG are the indicators for measuring the ESG rating of manufacturing enterprises. Because of significant data dispersion, this study separately used logarithmic ESG (lnESG) and DTS (lndts) to address the research questions. Based on previous theoretical analysis, if θ1 is significantly positive, it means that the higher the degree of digital transformation is, the higher the ESG performance is, which in turn highlights that digital transformation is conducive to improving ESG performance.

Digital Transformation

Based on Wu et al. (2021), DTS was measured with the frequency of 76 digitally related words in five dimensions: artificial intelligence, Big Data, cloud computing, and blockchain, as shown in Figure 3. lndts is the result of taking the logarithm after adding 1 to DTS. Specifically, we used Python crawler to download the annual reports of the sample companies from 2009 to 2020, sorted the original report texts into panel data, and then counted and sorted out the length of the full text of the companies’ annual reports. After that, we built a dictionary of corporate digital terms and expanded the vocabulary to the Jieba database after removing stop words. After counting the frequency of these words in the full text of the annual reports, we finally constructed an index to measure the degree of digital transformation of the enterprises.

DT-related indicators searched for word frequency statistics in the manufacturing industry.

ESG Evaluation

Although there are many ways for evaluating ESG performance, considering data availability and referring to Shahab et al. (2020) and Khalid et al. (2021), this study employed the frequently used ESG scores from China’s leading ESG assessment database (Sino-Securities Index). This method assesses three key indicators, that is, environment, social responsibility, and governance, including 80 plus ultimate indicators from some sub-indicators (climate change, resource utilization, environmental management, human capital, product liability, data security and privacy, shareholder interest, governance structure, etc.). The ESG ratings include nine tiers of ratings from AAA to C (AAA, AA, A, BBB, BB, B, CCC, CC, and C) scoring from 9 to 1, respectively. This method has been adopted by other researchers (Lin et al., 2021).

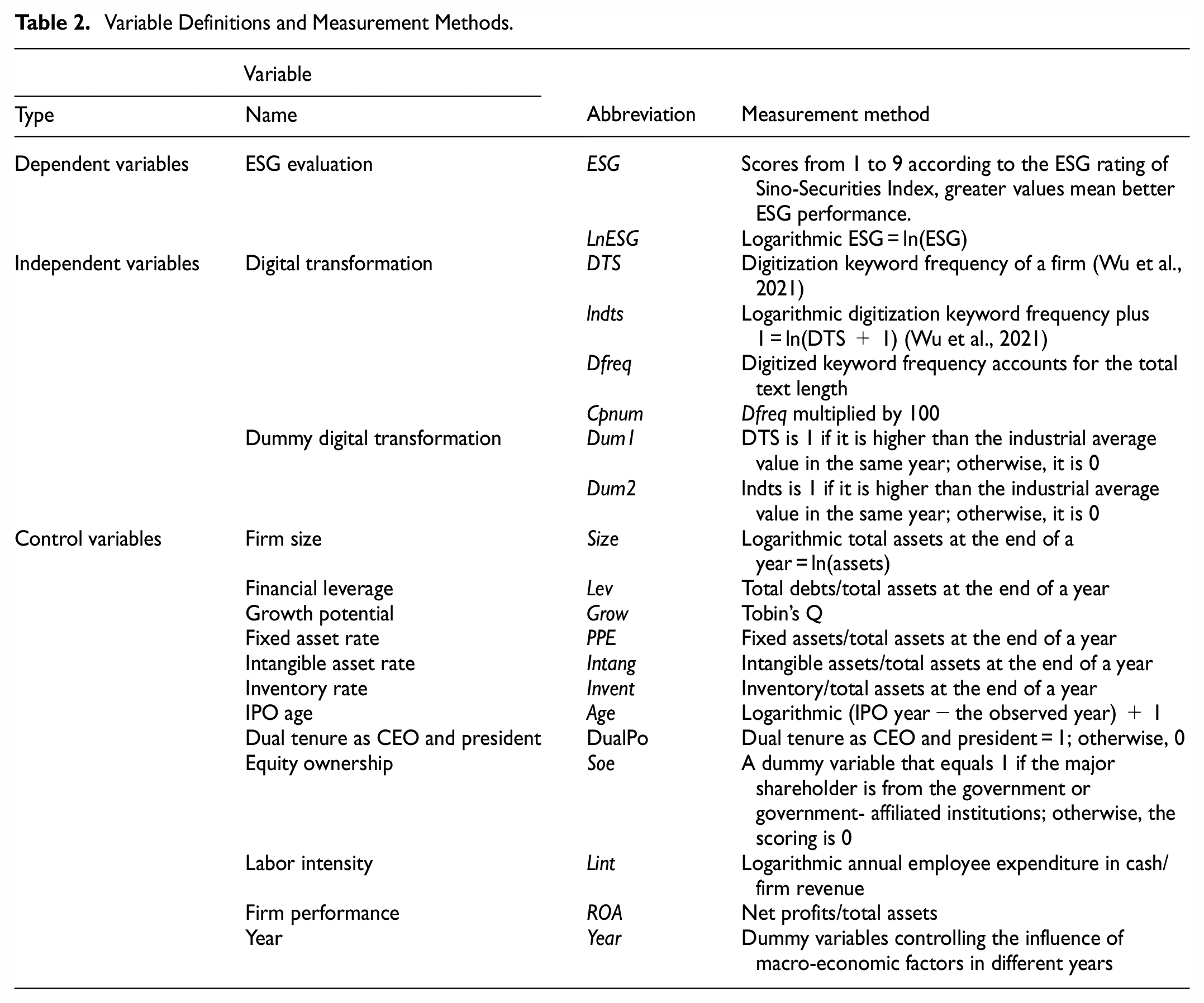

Following Khalid et al. (2021) and Zhou et al. (2022), this study included some control variables, whose description and measurement methods are reported in Table 2.

Variable Definitions and Measurement Methods.

Instrumental Variable Estimation

In line with Breuer et al. (2018), this study used the 1-year-lagged average DT degree of other firms in the same industry and province where the sample firms were registered as an instrumental variable. After controlling for endogeneity, the interactive relationship between DT and ESG still showed a significant positive correlation. The models are expressed below.

where L.MDTS and L.Mlndts represent the average DT values of other manufacturing firms in the province where the sample companies were registered.

To demonstrate the theoretical framework in Figure 1, this study employed mediated effects models to investigate the conductive effect of DT on ESG performance by firm performance. In line with Mackinnon et al. (1995), the mediated models were developed as shown below.

To obtain a general result on the relationship between DT and ESG in the manufacturing industry, this study conducted a heterogeneity analysis to offer insights into it from three perspectives: labor intensity, spatial characteristics, and ownership.

China’s traditional manufacturing industry features labor-intensive companies (Thorbecke & Zhang, 2009), but gradually growing labor costs have pushed many manufacturing firms toward technological upgrading and transformed them into technology-intensive firms. F. Wang et al. (2020) discusses labor cost heterogeneity across industrial and firm-specific labor intensity levels. Furthermore, China’s labor-intensive manufacturing firms have heterogeneous responses to the association between digitization and ESG performance, because the digitization of manufacturing firms may reduce employee quantity and labor costs in China (Yuan et al., 2021).

Results and Analysis

Descriptive Analysis

Table 3 outlines the distribution of the variables. The mean value of ESG was 6.306, ranking between A and BBB. The minimum value of 3.000, ranking as CCC, indicates that all sample firms had embarked on their ESG evaluations, but some of them did not pay attention to it. Furthermore, the minimum value (0.000) of DTS indicates that some companies had not yet initiated digital transformation, so they had other options for their ESG. This result is supported by the minimum value of Dfreq.

Descriptive Analysis of the Variables.

Figure 4 illustrates a remarkable upward trend of digital transformation from 2009 to 2020; this means that the manufacturing industry experienced a significant digitization process in China during this period and that Chinese manufacturing firms did not realize it before 2008.

Changes in digital transformation from 2001 to 2020.

Univariate Analysis

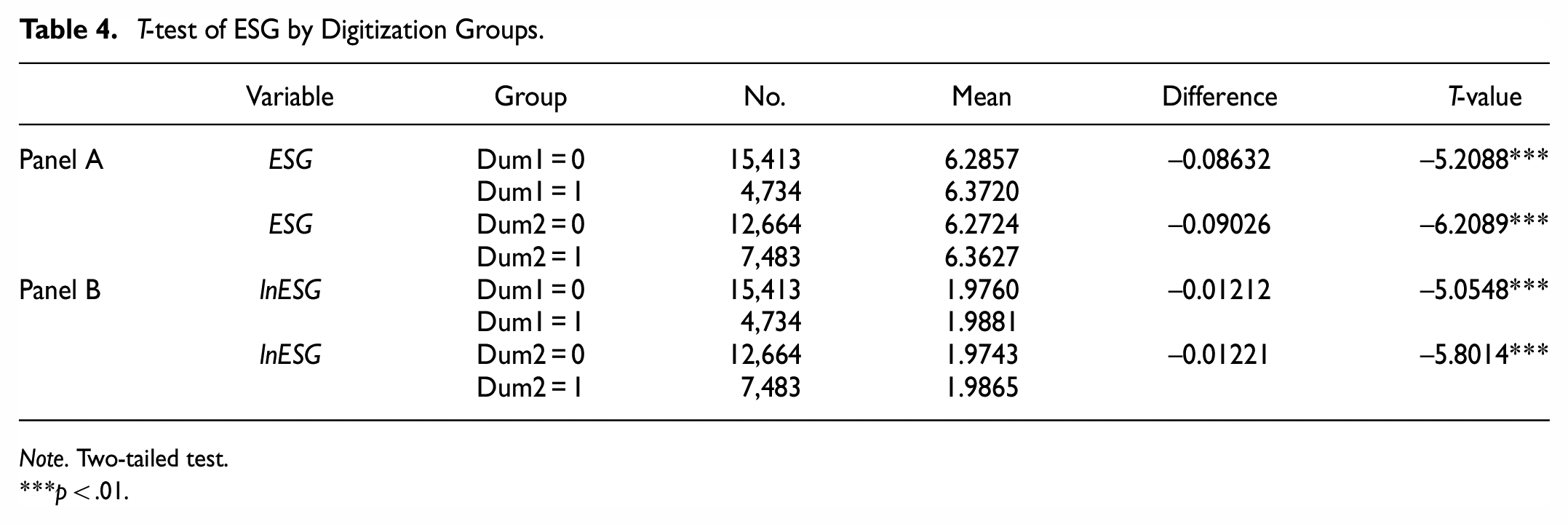

Next, a univariate T-test was conducted to assess ESG performance by setting dummy variables of digital transformation. As Table 2 defines, Dum1 = 1 if the DTS values are greater than the mean values; otherwise, Dum1 = 0. A similar reasoning is adopted for Dum2, evaluated using lndts. As Table 4 shows, the mean values are greater than the counterpart when Dum1, −2 = 1 at a very significant level; this means that the better the digitization was, the better the ESG performance was. The preliminary results support H1.

T-test of ESG by Digitization Groups.

Note. Two-tailed test.

p < .01.

Regression Analysis

The regression analysis presented in the following further investigated to what extent digitization improved firm ESG performance. The coefficients (0.0034 and 0.0445) in columns (1) and (2) indicate a significant positive relationship between firm digitization and ESG performance, which is consistent with the results in columns (3) and (4). These results significantly support H1.

However, there are many other factors associated with ESG performance. We found a positive relationship between ESG and firm size (size), growth potential (Grow), inventory (Invent), and equity ownership (Soe). On the contrary, a negative relationship was found between ESG and financial leverage (Lev), and between ESG and firm age (Age). This indicates that big companies and growing firms paid more attention to their ESG performance than others and that state-owned enterprises were keen on ESG performance. However, both aged firms and higher-leveraged firms were more numerous, regardless of their ESG, because of the negative relationships between ESG and Age, and between ESG and Lev.

To further investigate the digitization contribution to ESG performance, this study employed dummy variables (Dum1 and Dum2) instead of DTS and lndts to further show significance between them. As indicated in Table 5, the coefficients of both Dum1 (.0686 and .0101) and Dum2 (.0662 and .0100) were found to be significantly greater than their counterparts (.0034 and .0005, and .0445 and .0068, respectively) shown in Table 6. This relationship becomes more significant when we consider firm digitization at a higher level, indicating that the greater the digitization was, the better the ESG performance was.

Relationships Between Dummy Digitization and ESG Performance.

Note. t-Statistics in parentheses.

p < .01.

Relationships Between Independent Variables and ESG Performance.

Note. Figures reported in brackets are t-values adjusted by heteroscedasticity.

and ** mean significance at 1%, 5%, and 10% levels, respectively.

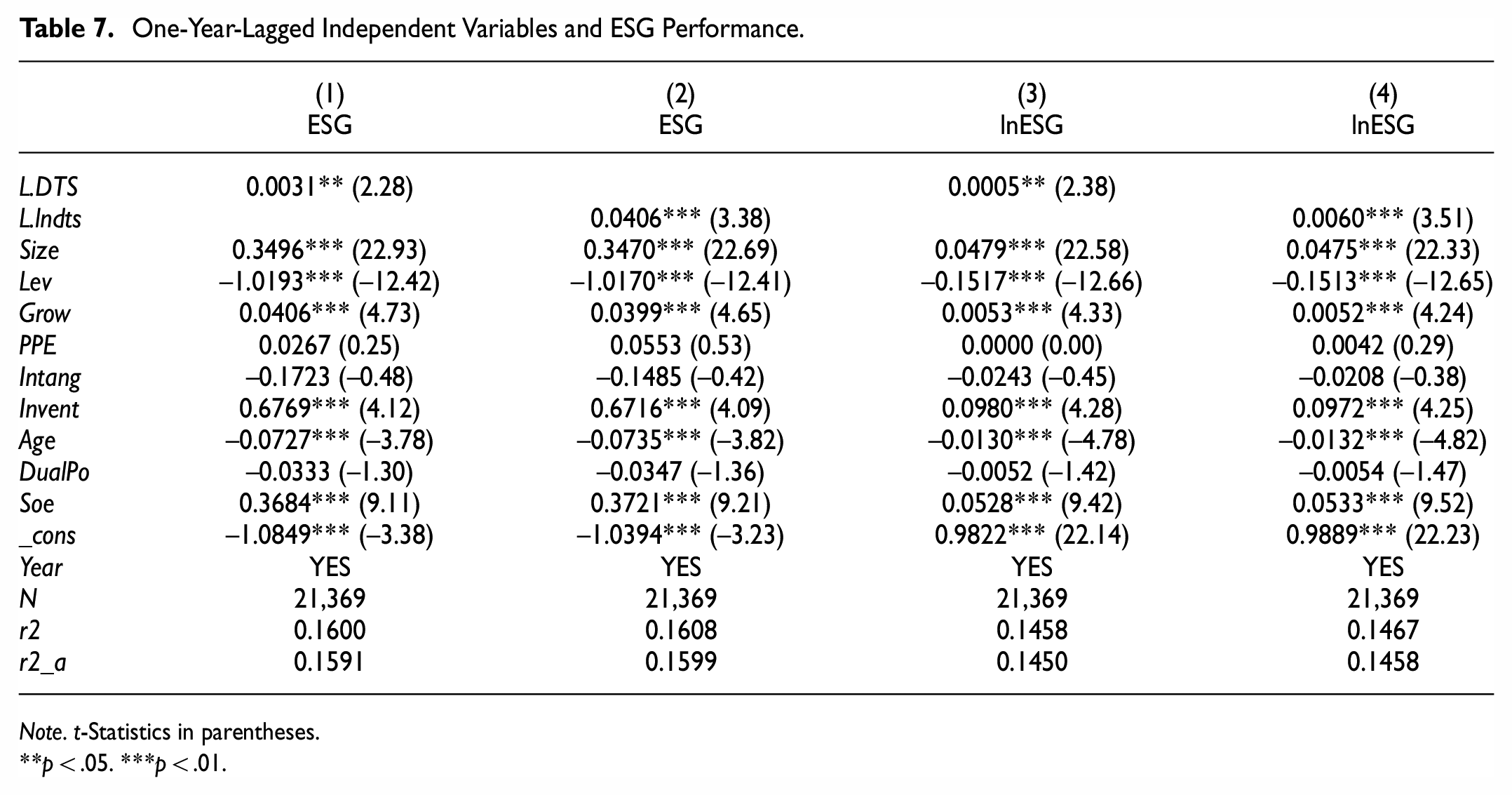

As digitization is a time-consuming strategy, it has lagged effects on firm ESG. This study next investigated the relationship between 1-year-lagged digitization and ESG. Table 7 shows a comparable positive relationship between lagged digitization and ESG compared with that shown in Table 6. This finding suggests that digitization not only contributed to firm ESG performance but also had a profound effect on it. Additionally, financial leverage had a very significant lagged side effect on ESG performance, given that the negative coefficients are greater than those in Table 6. Other factors (Size, Grow, Age, Invent, and Soe) also had comparable lagged effects on ESG performance. Therefore, digitization is a long-term strategy for ESG improvement.

One-Year-Lagged Independent Variables and ESG Performance.

Note. t-Statistics in parentheses.

p < .05. ***p < .01.

Robustness Test

Table 8 shows the regression results of the instrumental variable estimation. The coefficients (0.9265 and 0.8291) of L.MDTS and L.Mlndts in columns (1) and (3), respectively, were found to be significantly positive, indicating that the DT degree of other companies was significantly positive with respect to the digital transformation of the sampled company. After the introduction of instrumental variables, the digital transformation DTS and lndts of manufacturing enterprises was found to be still positively correlated with ESG rating scores in the second stage (columns (2) and (4), respectively), compared with DTS and lndts in Table 6, respectively. After controlling for endogeneity, the relationship between the two resulted in being more significant, further demonstrating that a high DT degree promoted the ESG performance of manufacturing companies, which further supports research hypothesis 1.

Instrumental Variable Estimation.

Note. Figures reported in brackets are t-values adjusted for heteroscedasticity.

mean significance at 1%, 5%, and 10% levels, respectively.

Fixed Effect Test

The control year was further subjected to fixed effect regression for the robustness test. In addition, all other control variables were controlled, and all regression coefficients were adjusted for heteroscedasticity robustness and clustered at the company and year levels; the specific fixed effects regression results are shown in Table 9. Consistently, the DTS, lndts, ESG, and lnESG coefficients were still significant, although they slightly decreased, which shows that the higher the degree of digital transformation in the manufacturing industry was, the better their ESG ratings were.

Fixed Effects Model Results.

Note. t-Statistics in parentheses.

p < .05. ***p < .01.

Replacing DT Measurements

In the above regression, the degree of digital transformation was based on the statistics of the frequency of digital transformation words. Considering that the length and proportion of digital word frequency in the total text may highlight the degree of enterprise digitalization, this study also used word frequency as a percentage of the total text length. The ratio (Dfreq) and the ratio multiplied by 100 (Cpnum) were used to measure the degree of DT. The results after replacing DTS and lndts, shown in Table 10 below, are consistent with those presented above.

Regression Results by Replacing DT Measurements.

Note. t-Statistics in parentheses.

p < .05. ***p < .01.

Therefore, the contributions of DT to manufacturing ESG performance in Route 3 is demonstrated. These findings support hypothesis 1: The greater the digital transformation is, the better the ESG performance of manufacturing firms in developing economies is.

Mediated Effects Measurement

The coefficients (0.0003 and 0.0023) in Table 11 indicate a significant effect of DT on firm performance, and the coefficients values of 1.7759 and 1.7790 indicate a positive relationship between firm performance and ESG, which means that the better the firm performance was, the better the ESG performance was. This finding is supported by the coefficients in columns (5)−(6). Therefore, the DESG theoretical framework for the manufacturing industry in Figure 1 is supported. Digital technologies facilitate business production and improve the business profits of manufacturing firms, so that manufacturers have sufficient profits to invest in ESG for sustainable development in a virtuous cycle.

Mediated Effects of DT on ESG Performance by Firm Performance.

Note. t-Statistics in parentheses.

p < .01.

Heterogeneity Analysis

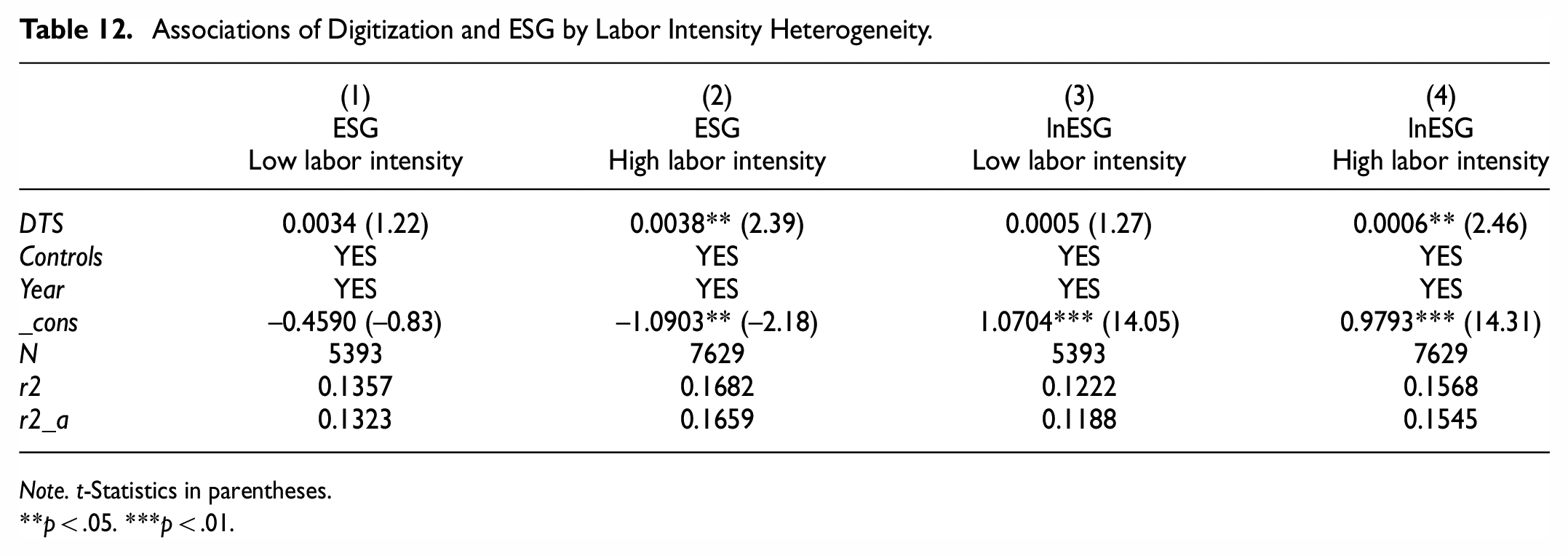

This study employed an existing method for measuring labor intensity through the logarithmic ratio of total cash payment to firm revenue, which has been used by others (Serfling, 2016). Table 12 shows the relationship between digitization and ESG in firms characterized by low and high labor intensity. The coefficients (0.0038 and 0.0006) in columns (2) and (4), respectively, were found to have a significant positive relationship in firms with high labor intensity compared to firms with low labor intensity. This result implies that digitization facilitated firm ESG performance for sustainable development in highly labor-intensive manufacturing firms. This finding supports hypothesis 2.

Associations of Digitization and ESG by Labor Intensity Heterogeneity.

Note. t-Statistics in parentheses.

p < .05. ***p < .01.

Furthermore, because of the imbalanced economic development between North and South China, the effect of digitization on ESG performance should be differentiated among regions. Following Wang et al. (2022), the sampled firms were divided into two groups from North and South China. The coefficients (.0023 and .0004) in Table 13 show the existence of a significant relationship between digitization and ESG performance in South China, but this is insignificant in North China; in other words, digitization may have contributed to ESG in South China. This spatial heterogeneity could be attributed to the economic heterogeneity among regions, with South China showing better economic performance than North China, because a positive relationship exists between ESG and economic development in the long run (Diaye et al., 2022). Therefore, southern companies were more likely to pursue sustainable ESG performance by means of digitization for economic sustainability than northern firms, and vice versa. This result supports hypothesis 3.

Spatial Heterogeneity of ESG Association With Digitization.

Note. t-Statistics in parentheses.

p < .1. ***p < .01.

Lastly, there are remarkable differences between state-owned enterprises (SOEs) and non-SOEs in China; particularly, SOEs are closely politically connected and engage in social responsibility, while non-SOEs pursue profit-related activities. Due to the different strategic purposes, ESG performance also differs. Table 14 shows the heterogeneity between the two different types of firms. The coefficient values of .0042 and .0006 show that digitization made a significant contribution to ESG performance in non-SOEs but this was found to be insignificant in SOEs. Therefore, hypothesis 4 was accepted.

Different Relationships Between Digitization and ESG by Ownership Heterogeneity.

Note. t-Statistics in parentheses.

p < .01.

This novel finding is interesting, because the Chinese economy is dominated by SOEs with strong political connections that experience less financial stress on ESG than non-SOEs (Ge et al., 2022); therefore, SOEs should display more significant ESG performance than non-SOEs. This finding could be attributed to the SOE agency issues whereby SOE managers have incentives to invest in ESG for personal purposes, such as social reputation and political career (L. Xu et al., 2020).

Discussion

These findings enrich the relevant research on ESG influencing factors. At present, the literature has studied the economic consequences of ESG from various aspects, and believes that ESG can resist downside risks (Wen et al., 2022), restrain managers’ misconduct (He et al., 2022), and improve corporate financial performance (Z. Chen & Xie, 2022; Friede et al., 2015), improve corporate value (B. Wang & Yang, 2022), etc. However, few literature discusses the influencing factors of corporate ESG ratings and proposes solutions to ESG performance. This article uses the data of Chinese manufacturing listed companies to directly analyze the impact of manufacturing digital transformation on its ESG performance and its internal mechanism and impact differences from the perspective of enterprise digital transformation. The findings are useful supplements to the study of ESG influencing factors and broaden the relevant literature.

The results expand the research on the economic spillover effects of digital transformation. Currently, there are abundant studies on the economic consequences and influencing factors of enterprise digital transformation. Strengths (Benner & Waldfogel, 2023; Bruce et al., 2017; Mikalef & Pateli, 2017), Organizational Performance (Johnson et al., 2017), Innovation Performance (Ferreira et al., 2019; Usai et al., 2021), customer welfare (Akram et al., 2021), and other aspects discuss the economic consequences of the digital transformation of enterprises in detail. There are also discussions on the influencing factors of the digital transformation of enterprises from the perspectives of corporate financialization (Huang et al., 2022), local economic growth goals (Yang et al., 2021), and the CEO’s compound functional background (Mao et al., 2022). However, there is no literature that directly studies the interaction between corporate digital transformation and its ESG rating. Therefore, this paper studies the inherent economic consequences of digital transformation from another new perspective.

Finally, the research finds that the digital transformation in manufacturing enterprises can help promote their green technology innovation and improve the level of information disclosure, reduce environmental pollution levels, fulfill social responsibilities, improve governance capabilities, and ultimately improve ESG performance. This conclusion provides certain policy suggestions and inspirations for promoting enterprises, especially heavy polluting enterprises, improving ESG performance and fulfilling environmental social responsibilities under the low-carbon development strategy. At present, how to efficiently control carbon emissions to slow down global warming is a hot spot in the political, business and academic circles. As a manufacturing enterprise with high carbon emissions, it is the object of common concern from all countries in the world. The research proves that digital transformation can enable enterprises to carry out environmental governance, and improve their ESG performance. This conclusion is helpful for government policy makers and enterprise managers to use digital transformation to promote energy conservation and emission reduction in enterprises, and provides a certain theoretical reference and method reference for realizing green transformation and low-carbon goals.

Conclusions and Policy Implications

As a concept that focuses on corporate environmental protection, social responsibility, and corporate governance, ESG meets the requirements of sustainable development for green, ecological, low-carbon transformation. The digital transformation of enterprises has also become an important impetus to promote industrial upgrading and will likely continue to play a great role in empowering digital economic development in the future. With manufacturing being a national economic driver, its green, ecological, low-carbon transformation is the key to promoting high-quality economic development. Therefore, it is of great practical economic significance to explore how the digital transformation of manufacturing companies affects ESG performance.

Under these circumstances, this paper proposes a DESG theoretical framework to test the impact of digital transformation on the ESG performance of manufacturing companies by examining the heterogeneity of manufacturing ESG from different perspectives in the manufacturing industry. Based on samples of Chinese listed companies from 2009 to 2020, the research study shows that big companies and growing firms pay more attention to their ESG performance than others and that SOEs are keen on ESG performance but exhibit poorer performance than non-SOEs (see Table 6). Additionally, manufacturing DT may improve ESG performance in general, because DT improves firm operating performance, which in turns means that these firms have sufficient funds to invest in ESG, thus promoting their sustainable development. In particular, this study shows that manufacturers in economically developed regions show more significant ESG performance thanks to DT and that firms with higher labor intensity experience more significant effects of DT on ESG performance than their counterparts (see Tables 12 and 13). DT makes a significant contribution to ESG performance in non-SOEs, but this is insignificant in SOEs (see Table 14). Therefore, DESG contributes to the sustainable development of manufacturing in developing countries.

These findings support the proposed DESG theoretical framework for the manufacturing industry whereby digital technologies facilitate business production and improve the business profits of manufacturing firms, so that manufacturers have sufficient profits to invest in ESG for sustainable development in a virtuous cycle (see Figure 3 and Table 11).

This research has three practical implications. First, manufacturers should speed up the pace of DT, improve corporate green technology innovation, promote the green and low-carbon development of companies, and achieve a win–win situation of economic and social benefits. On the one hand, to provide a basis for business decision making, it is necessary to adapt to the development in the digital age; promote the digital transformation of various elements and links according to the actual situation and market demands; and focus on improving the intelligence level in many aspects, such as production, sales, investment, financing, and personnel management. On the other hand, it is also necessary to fully use the social spillover effects of DT, improve green technology innovation, save resources and energy, reduce ecological pollution and damage, provide employees with a safe workplace, provide the public with energy-saving and environmentally friendly products, improve the environmental performance and social responsibility performance of enterprises, and ultimately improve social benefits. These efforts feedback economic benefits, improve the competitiveness of manufacturing companies, and promote high-quality economic development.

Second, the government should perfect the top-level structure of ESG and provide reference for other countries to build ESG rating systems. In addition, in order to prevent companies from using ESG concepts to mislead market participants, the government should guide and promote the construction of soft-market supervision and encourage rating agencies to continuously improve ESG assessment techniques, improve their ability to tap long-term corporate value, and maximize the soft market.

Third, the government should establish a digital service platform, build a complete digital infrastructure system, cultivate talents with digital skills, and promote the digital transformation and upgrading of the manufacturing industry. To do so, the government should build an efficient communication platform between enterprises and government departments, media, and industries and create a digital service platform to help manufacturing digitization. The government should also build a complete digital infrastructure system and help the digital economy to penetrate traditional industries, in order to provide external technical support for industrial green transformation. Furthermore, improving the digital literacy and skills of citizens and cultivating citizens with digital awareness and social responsibility may provide manufacturers with high-quality digital skills and interdisciplinary talents and effectively promote the digital transformation and upgrading of the manufacturing industry.

Research limitations: ESG was measured by ESG rating from AAA to C scoring from 9 to 1, so one of the research limitations in method is that ESG was not evaluated specifically in terms of environment, social responsibility, and governance, respectively, due to data limitation. The second one is lack of taking further insight into different industrial sections in manufacturing industry, which are expected to be investigated by the future research.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was supported by 2020 Discipline Construction Scheme of the Thirteen Five Plans of Guangdong Philosophy and Social Science, (grant number: GD20XGL12). 2021 The First Round of Industry-University-Research Synergy Education Project Funded by the Bureau of Tertiary Education, Ministry of Education of the People’s Republic of China, (grant number: 202101143023). 2022 Youth Scheme of the Fourteen Five Plans of Guangzhou Philosophy and Social Science, (grant number: 2022GZQN21). 2021 Philosophy and Social Science of Heyuan City, Guangdong, (grant number: HYSK21ZC12). 2017 PhD Research Initial Fund from Guangdong Polytechnic Normal University.

Research Involving Human Participants and/or Animals

N/A.

Informed Consent

N/A.