Abstract

The Environmental, Social, and Governance (ESG) paradigm is emerging as a dominant driver of sustainable economic growth. A growing number of firms are adopting ESG practices, seeking not only to align with contemporary trends but also to cultivate trust. Although ESG, trust, and financial performance are frequently examined in previous studies, the mechanisms underlying their interrelationships remain underexplored. This study analyzes data from 2,351 Chinese listed firms (2015–2022) using static panel model and two-stage dynamic panel generalized method of moments (GMM). The findings reveal that ESG performance significantly boosts financial outcomes through trust. The boosting effectiveness is highly associated with market attention, public attention and the temporal consistency of ESG performance. Further research indicates that non-state-owned enterprises, firms with direct contact between products and consumers, and firms in higher economic development regions are more likely to gain trust and financial performance through ESG performance. The study complements the existing understanding of mechanisms through which ESG impacts financial performance with the crucial role of trust as an informal institution in enhancing financial performance.

Introduction

In recent decades, the issue of corporate sustainability has garnered closer attention (Naseer et al., 2025), and has emerged as one of the largest sources of trust risks faced by businesses (Hunjra et al., 2024). In the meantime, the Environmental, Social, and Governance (ESG) paradigm has gained wide recognition and acceptance (Díaz et al., 2021) as it aligns with stakeholders’ aspirations for sustainable development. ESG has increasingly been deemed an intrinsic driver for mitigating operational risks (Broadstock et al., 2021), enhancing company value (Bagh et al., 2024), and improving trust (Tang & Yang, 2023). Thus, various entities, including governments, companies, and development institutions, have a strong interest in developing effective approaches to improving ESG performance. The increasing diversity of relevant practices enables ESG to transition from compliance to long-term pursuits of competitive advantage and corporate financial performance (J. Li et al., 2024; Tyan et al., 2024).

The ESG-financial performance nexus operates within complex political economies shaped by green policy frameworks (Jin et al., 2024), national governance (Z. Luo et al., 2024), and strategic adaptation to investment risks (S. Chen et al., 2023). However, recent global disruptions including COVID-19, supply chain realignments, and geopolitical tensions have exposed systemic vulnerabilities in formal institutional safeguards. Layoffs and salary cuts have become widespread, and cases of financial fraud, environmental pollution, and greenwashing still exist (Lee & Raschke, 2023). Some firms choose to reduce their environmental and social responsibility governance to allocate more resources to protect their core business. Widespread corporate austerity measures and persistent ethical failures in environmental stewardship and financial reporting (Lee & Raschke, 2023) underscore the limitations of regulatory approaches in sustaining ESG commitments during economic contractions.

This institutional void has intensified scholarly interest in informal mechanisms governing ESG outcomes. Research increasingly highlights how relational factors such as trust, reputational capital, and ethical norms mediate corporate decisions beyond formal compliance (Dak-Adzaklo & Wong, 2024; Shen et al., 2022). Trust represents a typical informal institution (Kong et al., 2023), characterized by social rules that emerge, spread, and operate beyond official channels (Simpson & Willer, 2015). Stakeholders’ perceptions of ESG consistency enable firms to establish relational legitimacy, thereby reducing transaction costs and stabilizing financial performance through enhanced cooperation (Cialdini et al., 1991; Milgram et al., 1969). Meanwhile, trust has been recognized as a vital influence mechanism on corporate operation (Kong et al., 2023). Senior executives now confront the strategic imperative to align trust-building with ESG objectives, balancing operational efficiency against reputational risks in competitive markets (Dong et al., 2018; Tang & Yang, 2023).

While ESG practices are supposed to contribute to corporate financial performance, the exact mechanism linking the two remains a complex and challenging puzzle. Existing research has acknowledged the value of trust in business management (Guiso et al., 2004). However, the shared social embedding mechanism between ESG performance and financial outcomes has not been adequately addressed, and the influence of informal institution on the relationship between ESG performance and financial results remains unclear (Tang & Yang, 2023). This study examines whether trust mediates the relationship between ESG performance and corporate financial performance and explores how stakeholders’ attention and corporate behaviors influence this mechanism. First, we discuss the positive correlation between ESG performance and corporate financial performance, highlighting that the economic benefits of ESG fulfillment can offset additional costs, thereby enhancing financial performance. Second, we underscore the significant role of trust, indicating that firms with better ESG performance are more likely to earn trust, which partially mediates the positive impact of ESG on corporate financial performance. There exists a key pathway of Moreover, we examine the moderating effects of stakeholder attention and corporate behavior. The strength of these effects is highly associated with market attention, public attention and the temporal consistency of ESG performance. The temporal consistency of ESG performance strengthen the positive impact of ESG on trust. Conversely, market and public attention weaken this positive impact.

This study contributes to the related literature in the following ways. First, it extends trust theory by empirically validating how non-opportunistic ESG behaviors function as credible commitment devices (Dong et al., 2018; Guiso et al., 2004). Second, it delineates the micro-foundations of ESG value creation through stakeholder theory, addressing calls to bridge macro-institutional and micro-behavioral perspectives in sustainability research. Third, it offers actionable insights for ESG resource allocation. By analyzing the impact of stakeholders on the relationships mentioned above, which can guide firms to rationally allocate ESG resources among stakeholders and formulate effective business strategies.

Hypothesis Development

According to the resource dependence theory, firms with a higher ESG rating are more likely to obtain resources, trust and support from stakeholders, thus enhancing their ability for sustainable development. We propose a conceptual framework to illustrate the mechanism of ESG performance on financial performance (Figure 1). This conceptual framework outlines the mediating role of trust, as well as the mediating roles of stakeholder attention and the consistency of ESG performance.

Interaction mechanism of ESG, trust and financial performance.

ESG Performance and Corporate Financial Performance

Corporate practices in environmental (E) protection create favorable conditions for obtaining competitive advantage, which enhances financial performance. Investments in eco-friendly technologies serve as crucial strategic resources for firms and have gained stakeholder support. Consumers increasingly prefer products with green rating labels (Austmann & Vigne, 2021), demonstrating that firms can achieve market differentiation by developing green products, which contribute to significant financial returns (Frondel et al., 2008; He et al., 2023; Melnyk et al., 2003). Meanwhile, effective environmental pollution control allows firms to secure more government subsidies (Jackson et al., 2020) and lower compliance costs (Porter & Linde, 1995). Social (S) responsibility performance reflects a company’s ability to create and deliver value to stakeholders. According to signal theory, social responsibility disclosure provides incremental information to stakeholders, helps them filter information noise, reduces hidden costs by promoting cooperation (Chouaibi et al., 2021), and expands access to corporate funding (Cui et al., 2018). Corporate governance (G) coordinates conflicts of interest among shareholders, board members, and executives, mitigates internal agency problems and ensures that external investors receive returns on their investments (M. Zhou et al., 2021).

In summary, all three aspects suggest that strong ESG performance creates opportunities for long-term business growth and value creation, positively impacting corporate financial performance. Thus, we propose the following hypothesis:

ESG Performance, Trust and Financial Performance

Trust functions as a critical informal institution that complements formal governance systems by reducing transaction costs and enabling cooperative exchanges where legal frameworks remain incomplete (North, 1990). Its institutional significance stems from its dual capacity to mitigate opportunism and foster relational contracts—mechanisms particularly vital in contexts with underdeveloped formal ESG regulations (Corradini, 2022; Guseva & Rona-Tas, 2001). When firms engage in ESG practices, they generate reputational signals that stakeholders interpret as commitments to shared norms, thereby reducing perceived risks of exploitation. This signaling process aligns with prediction-based trust formation, where stakeholders extrapolate future reliability from observable ESG behaviors, fostering self-reinforcing cycles of mutual trust and cooperation (W. Luo & Najdawi, 2004). For instance, consistent ESG disclosures provide stakeholders with verifiable historical data, enabling them to assess the firm’s cooperative intent and reducing cognitive effort in trust evaluation (Z. Chen & Xie, 2022).

The institutional duality of trust as a governance substitute and relationship asset explains its significant role in mediating the relationship between ESG and financial performance. In regions where formal institutions fail to internalize ESG externalities, trust compensates by establishing implicit enforcement mechanisms, such as reputational sanctions and relational incentives. Suppliers may prioritize transactions with high-ESG firms, interpreting sustainability practices as non-contractual guarantees against unethical conduct (Park et al., 2014). Similarly, investors in institutionally fragile markets disproportionately reward ESG-aligned firms with trust premiums, effectively substituting for formal risk mitigation tools (Yan et al., 2021).

At a macro-institutional level, trust facilitates the accumulation of social capital—a resource that enhances corporate resilience by embedding firms within durable stakeholder networks. ESG-consistent firms attract symbiotic partnerships, creating collaborative ecosystems that buffer against market shocks. Conversely, at the micro-level, trust operates as a cognitive lock-in mechanism, where consumers develop brand loyalty through repeated positive ESG interactions (Chkir et al., 2023). These multi-tiered effects position trust not merely as an interpersonal phenomenon but as a meso-level institutional infrastructure that reconfigures market dynamics.

Critically, trust’s efficacy as an informal institution is contingent on its ability to resolve information asymmetries. ESG performance serves as a costly signal, and sustained investment demonstrates alignment between a company’s words and actions, which is essential for trust to develop (Kong et al., 2023). When stakeholders perceive ESG consistency, they infer reduced agency costs, enabling firms to access resources typically reserved for institutional insiders (Amiraslani et al., 2023). This process exemplifies trust’s role in creating institutional permeability, allowing firms to transcend formal market barriers through relational legitimacy.

ESG fulfillment follows the logical path of “ESG behavior input—stakeholder perception—trust formation—financial performance improvement.” Trust may serve as a mediating mechanism in the relationship between ESG performance and financial performance. Thus, we propose the following hypothesis:

Moderating Role of Stakeholder Attention

Stakeholder attention refers to the process by which corporate information is noticed, collected, analyzed, and used for decision-making by stakeholders (Zheng et al., 2022). The moderating role of stakeholder attention stems from its dual capacity to amplify ESG signals and calibrate trust formation. ESG initiatives derive value not merely from their substantive quality but from the visibility they garner through stakeholder scrutiny. Firms engaging in ESG practices under stakeholder attention can benefit from increased attention, which amplifies ESG signals, allowing better transmission of ESG information between collaborators and the market (Brummel, 2023; Madsen & Rodgers, 2015), thereby reinforcing the shaping of trust through corporate ESG behavior.

Heightened attention can enhance the visibility of ESG initiatives, facilitating trust-building through two complementary mechanisms. First, under conditions of market scrutiny, firms demonstrating robust ESG performance can leverage transparency as a strategic asset. By reducing information asymmetry through clear ESG disclosures, companies strengthen stakeholders’ confidence and market credibility, as evidenced by research on signal transmission in capital markets (H. Lin et al., 2016; Truong et al., 2021). Second, public attention directed at environmental and social issues, such as pollution disclosures or labor practices, creates institutional pressures that demand authentic ESG commitments. This accountability mechanism forces firms to align their operations with societal expectations, as documented in studies examining stakeholder activism and corporate environmental responsibility (H. Lin et al., 2016; Truong et al., 2021).

This theoretical framework posits that stakeholder attention moderates the ESG-trust relationship by altering the cost-benefit calculus of ESG investments. Under concentrated attention, ESG generates trust premiums by resolving stakeholder uncertainty about corporate intent (Z. Chen & Xie, 2022). To test the above arguments, we propose the following hypothesis:

Moderating Role of Consistency in ESG Performance

The purpose of corporate operations is to achieve sustainable competitive advantages (Rosecká et al., 2024). Faced with increasing expectations and demands from stakeholders, firms recognize the need to allocate more resources to ESG. Firms also face increasing pressure to demonstrate social and environmental responsibility. However, managers are concerned that this may generate additional costs; they may employ negative ESG strategies to address external pressure. Some firms may engage in opportunistic ESG behaviors, relying on short-term symbolic actions to enhance corporate visibility. This leads to a paradox where firms fulfill ESG responsibilities while simultaneously causing social problems (de Vries et al., 2015; Wu et al., 2021).

Corporate ESG behavior and its management are inherently long-term processes. Over time, ESG performance may become more positive or negative (Agle et al., 1999; Porter & Kramer, 2002). This fluctuation affects stakeholders’ levels of trust in the company. ESG performance consistency refers to the sustained and stable characteristics of ESG performance over time (H. Wang & Choi, 2013). When a company consistently invests in ESG activities, it can gain a competitive advantage and build more reliable trust over time (Deese et al., 2021).

As demonstrated by the reputation effect, stakeholders convert information about corporate behavior, social evaluations, and performance levels into judgments about corporate reputation. They then use judgment about corporate capability and character reputation as proxies for decision-making (Mishina et al., 2012). The consistency of ESG performance over time influences stakeholders’ value judgments about the company (Rosecká et al., 2024). When stakeholders cannot directly obtain information about the company and its products, the consistency of ESG performance can serve as a value indicator. This indicator suggests that the products and services are more likely to retain value in the future, generating a stronger sense of identification and trust (Covin et al., 2006). Thus, when ESG performance consistency is high, it can reduce the unpredictability of stakeholders’ perceptions of corporate capabilities and behaviors during investments, thereby moderating the relationship between ESG performance and trust. This leads us to propose the following hypothesis:

Research Design

Model Development

Benchmark Regression Model

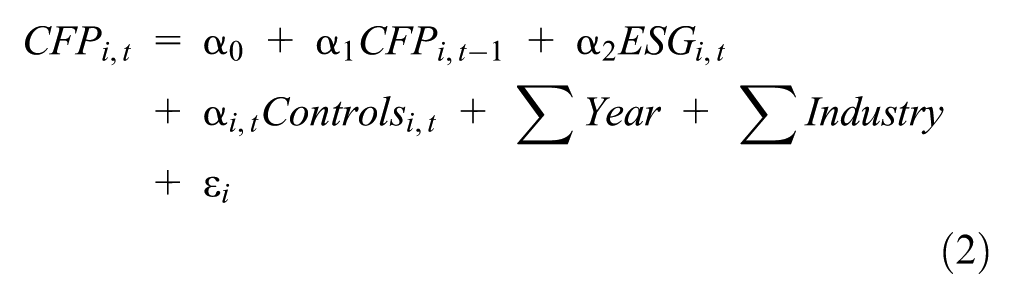

In this study, we employ the stepwise examination technique within the framework of the mediation analysis method for regression analysis. We establish a benchmark regression model to test the impact of ESG performance on financial performance (Hypothesis 1):

The variable subscripts i represents company i. CFP represents corporate financial performance, ESG reflects the ESG performance. Controli refers to control variables. ε represents the random error term. Year and Industry mean dummy variables for year and industry, respectively, aiming to control the impact of year and industry factors on corporate financial performance.

There may be strong reciprocal causality in the impact of firms’ ESG performance on firms’ financial performance, and existing studies point to the possible lagged impact of firms’ ESG performance suggesting that static regression models may not be able to effectively address endogeneity issues (Z. Chen & Xie, 2022; Nazir et al., 2024). The dynamic panel GMM effectively addresses endogeneity issues caused by lagged dependent variables by introducing lagged level variables (Arellano & Bover, 1995). Compared to the one-step GMM, the two-step GMM demonstrates greater efficiency in the presence of heteroskedasticity and mitigates finite-sample bias through Windmeijer’s (2005). This methodology has been widely applied in panel data analyses across fields such as economic growth and investment decision-making (Roodman, 2009). The generalized method of moments (GMM) is recognized as a robust and superior approach for addressing endogeneity in panel data (Arellano & Bover, 1995; F. Li, 2016; Nazir et al., 2022, 2024). Its strengths lie in simultaneously capturing dynamic adjustment processes, controlling for unobserved individual heterogeneity, and resolving endogeneity concerns, thereby providing a rigorous methodological foundation for testing the core hypotheses of this study. For this reason, two-stage dynamic panel generalized method of moments is used to conduct an additional test of the benchmark regression model.

Mechanism Model

Considering that trust may act as a mediator between ESG performance and financial performance, we extend the benchmark regression model (1) to construct models (2) and (3), used to test Hypotheses 2a and 2b, respectively.

To examine the mediating role of trust in the relationship between ESG performance and financial performance, we conducted a three-step analysis following the established procedures of Baron and Kenny’s (1986) mediation framework.

Step 1: Total Effect Verification: Model (1) regresses financial performance on ESG performance to test the total effect (α1). A statistically significant coefficient here preliminarily confirms that ESG performance influences financial performance.

Step 2: Mediator Pathway Validation: Model (3) evaluates the impact of ESG performance on trust. A significant regression coefficient (β1) would indicate that ESG performance systematically affects trust levels, satisfying the prerequisite for mediation.

Step 3: Joint Effect Analysis: Model (4) incorporates both ESG performance and trust into the regression framework to assess their combined effects on financial performance. Two critical outcomes are examined:

Partial Mediation: If the coefficient of ESG performance (γ1) remains statistically significant but diminishes in magnitude compared to its value in Model (1), while the coefficient of trust (γ2) is significant, this suggests that trust partially mediates the relationship.

Full Mediation: If the coefficient of ESG performance (γ1) loses statistical significance while trust (γ2) remains significant, this implies that trust fully mediates the effect of ESG performance on financial performance.

By systematically comparing regression coefficients across these models, we empirically test whether trust serves as a mediator through which ESG performance influences financial outcomes. This approach not only isolates the direct and indirect pathways but also aligns with rigorous methodological standards for mediation analysis in causal inference (Baron & Kenny, 1986).

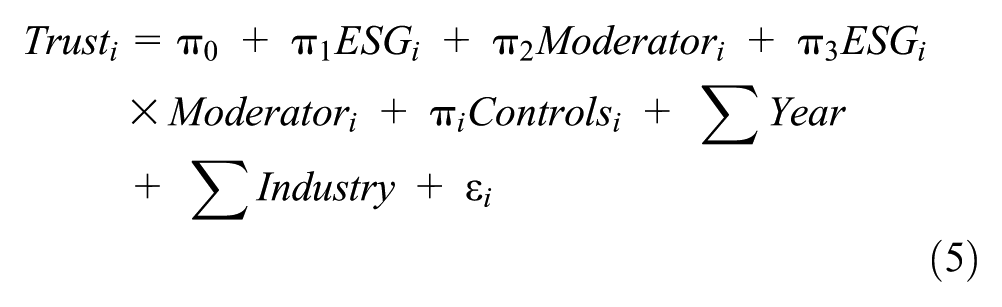

Moderating Effect Model

Taking into account the potential moderating effects of stakeholder attention and the persistence of ESG performance on trust, we introduce interaction terms between ESG performance variables and various moderating variables into the benchmark regression model (1), constructing model (4) to test Hypotheses 3 and 4:

Moderatori represents moderating variables, including public attention (PA), market attention (MA), and ESG temporal consistency (TS).

Variable Definition

Depending on the needs of model, the relevant variables are defined in the following sections:

Dependent Variable

Corporate Financial Performance (CFP). The net profit margin on total assets (ROA) serves as a proxy variable for corporate book value (Duque-Grisales & Aguilera-Caracuel, 2021). ROA is used as a measure of corporate financial performance.

Independent Variable

Corporate ESG Performance (ESG). The Huazheng ESG evaluation system provides ratings for issuers of securities such as A-shares in China across three dimensions: environmental, social, and corporate governance. The ratings range from “C” to “AAA” in nine categories, with higher scores indicating better ESG performance. In this study, we assign scores ranging from “1 to 9” to the Huazheng ESG ratings. Considering that the ESG ratings are issued quarterly, we take the average score for each quarter within the rating year to represent the annual ESG performance of the company.

Mediating Variable: Trust Index System

The complexity of stakeholder trust in firms is shaped by multifaceted determinants. Existing studies typically measure trust through questionnaire surveys (Haidar, 2025; B. Zhu & Wang, 2024), single indicators (Ge & Qiu, 2007), or narrow stakeholder perspectives (W. Tan et al., 2025). To holistically assess stakeholder trust, this study constructs a multidimensional composite trust index grounded in stakeholder theory, synthesizing methodologies from established trust measurement frameworks (Tang & Yang, 2023; B. Zhu & Wang, 2024). This index quantifies the aggregate trust level of listed firms across five core stakeholder groups: investors, creditors, suppliers, governments, and the public (Table 1).

Evaluation Index System of Trust.

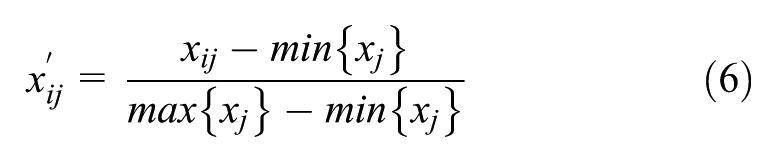

To ensure cross-indicator comparability, we first standardized all variables to address scale and magnitude differences. Positive indicators were normalized using Equation 6, while negative indicators followed Equation 7:

Subsequent weights were derived through entropy weighting (Equations 8–10) and coefficient of variation methods (Equation 11) to ensure stability and minimize subjective bias (Yuan et al., 2024). The entropy method prioritizes indicators with greater informational value:

The coefficient of variation method complements this approach:

Final trust indices are computed as the arithmetic mean of both methods’ outputs to enhance reliability and mitigate single-method biases. This dual-weighting strategy ensures robustness while preserving the informational integrity of each indicator.

Moderating Variables

Control Variables

Asset-to-liability ratio (Lev), cash ratio (Cash), firm size (Size), fixed asset ratio (Fixed), intangible asset ratio (Intan), and growth (Growth) are selected as control variables (DasGupta, 2022; Duque-Grisales & Aguilera-Caracuel, 2021). The variable codes and definitions are detailed in Table 2.

Variable Definition and Measurement Methods.

Sample and Data

Listed companies are widely recognized for their substantial business scale and well-established governance structures. Compared to non-listed companies, listed companies typically have more complete ESG information disclosure, higher dissemination rates, longer durations of ESG practices, and their information is more accessible to the market, attracting broader attention from stakeholders. Therefore, this study focuses on Chinese listed companies from 2015 to 2022, resulting in 16,867 valid observations from 2,351 companies. These companies are distributed across 19 industry categories and 73 subcategories. ESG performance data are sourced from the Huazheng ESG rating database, available through Wind. Financial data and stakeholder attention data are sourced from the CSMAR company research database.

To ensure the reliability of the analysis results, we screen and process the initial sample as follows. First, we exclude listed companies in the financial and insurance sectors. Second, we remove companies with special treatment labels such as ST, ST*, and PT. Third, we exclude companies with a significant number of missing values for variables. Finally, we winsorize continuous variables at the 1st and 99th percentiles.

Empirical Results and Discussion

Descriptive Statistics

Table 3 presents the descriptive statistics for all variables. The results show significant variation in corporate financial performance, while overall ESG performance is at a relatively high level. Pearson correlation coefficients reveal a significant positive correlation between ESG performance and both financial performance and trust, with correlation coefficients below .25. The variance inflation factor (VIF) for each variable has a maximum value of 2.78 and an average of 1.36, which is well below the commonly accepted threshold of 10. This indicates no significant multicollinearity among the variables.

Descriptive Statistical Analysis.

Note. This table displays the analysis results after excluding data from specific companies.

Main Results

Based on Model (1), we use a multiple linear regression approach to examine the impact of ESG performance on financial performance (Table 4). Column (1) represents the baseline regression model. The regression coefficient is significantly positive at the 1% level, supporting the hypothesis 1. Recognizing potential endogeneity issues due to the two-way causal relationship between ESG and financial performance, as well as the lagged effects of ESG performance on economic efficiency, we introduce one- and two-period lags for the ESG performance variable. The results in Columns (2) and (3) demonstrate that, even after lag analysis, ESG performance remains significantly positively related to financial performance.

Results of the Impact of ESG on Financial Performance.

Note. In Table 4, we estimate the relationship between ESG performance and financial performance, we use the fixed effects of year and industry, and in columns (2–3), we use ESG data with a lag of 1 year and 2 years. Column (4) shows the results of the GMM estimates. In parentheses is the t value calculated according to the robust standard error. ***, **, * are significant at 1%, 5%, and 10% levels, respectively.

The regression results based on the two-step system generalized method of moments (GMM) are presented in Column (4). To ensure the validity of the GMM estimation, we conducted two critical diagnostic tests. The Arellano-Bond test, an autocorrelation test, examines whether the error terms in the model exhibit serial correlation. The results show a statistically significant first-order autocorrelation (AR(1) p-value < .1), which is expected in dynamic panel models. Importantly, there is no evidence of second-order autocorrelation (AR(2) p-value > .1), satisfying the key assumption of the GMM framework. The Hansen test, an instrument validity test, evaluates whether the instrumental variables used in the model are exogenous (i.e., uncorrelated with the error term). The test yields a p-value greater than .1, indicating that the instruments are valid and not over-identified. These diagnostics collectively confirm the robustness of our model specification. The GMM estimates are consistent and reliable for analyzing the dynamic relationships in the data.

Table 5 presents the results of the mechanism examination. In Column (1), we estimate Model (3) to examine the impact of ESG performance on enterprise trust. The results show that superior ESG performance increases the likelihood of gaining stakeholder trust. In Column (2), we estimate Model (4) to test the mediating role of trust in the relationship between ESG performance and financial performance. The regression coefficients in both Columns (1) and (2) are significantly positive at the 1% level, providing support for hypotheses 2a and 2b. To account for potential lagged effects of ESG on corporate outcomes, we introduce a one-period lag in the mediation analysis, as shown in Columns (3) and (4).

The Mediating Role of Trust Between ESG and Financial Performance.

Note. In Table 5, we estimate the mediating effect of firm trust on ESG performance and financial performance. In columns (3–4), we estimate ESG data with a 1-year lag. In parentheses is the t value calculated according to the robust standard error. ***, **, * are significant at 1%, 5%, and 10% levels, respectively.

The regression results for the moderating effect are presented in Table 6. Columns (1) and (2) report the regression results for the moderating effect of stakeholder attention. The moderating effect of public attention and market attention on the relationship between ESG performance and trust is significantly negative at the 1% level, rejecting hypothesis 3. In Column (3), the analysis incorporates the moderating effect of ESG temporal consistency, supporting hypothesis 4. ESG temporal consistency exhibits a significantly positive moderating effect in the relationship between ESG performance and trust. In column (4), we add all the moderating variables to the model. The significance of the interaction effects for each moderating variable aligns with the results obtained in Columns (1) to (3), demonstrating the robustness of the model.

Test Results for Moderating Effects.

Note. In Table 6, we estimate the regression results of the moderating effect of stakeholder attention and ESG temporal consistency on trust. In parentheses is the t value calculated according to the robust standard error. ***, **, * are significant at 1%, 5%, and 10% levels, respectively.

Robustness Check

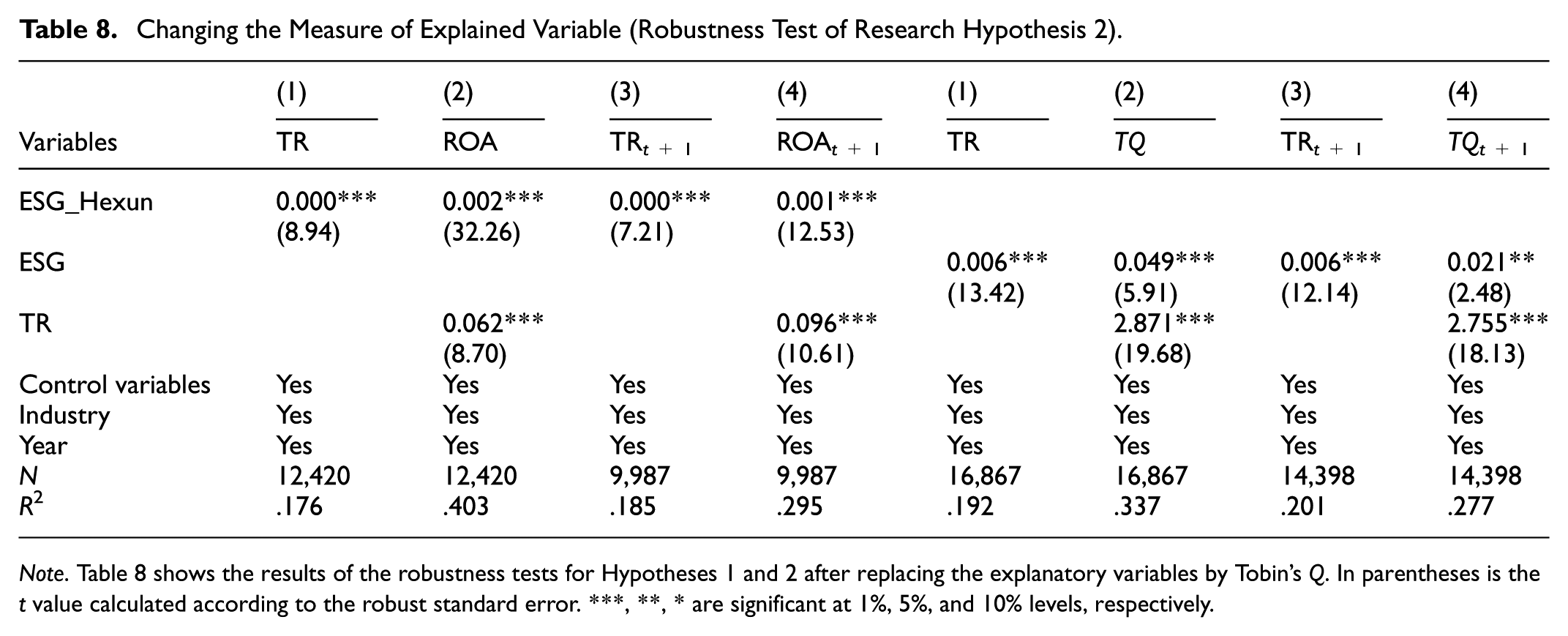

To further mitigate potential measurement biases and enhance the robustness of the study, we employ variable substitution to re-test Hypotheses 1 and 2. ESG Specifically, we replace the original ESG performance measure with ESG ratings from Hexun.com (Hexun; Mao et al., 2024). This substitution addresses potential systematic biases inherent in the initial ESG metric. For the dependent variable, we employ Tobin’s Q (calculated as the ratio of a firm’s market value to its total assets at the end of the period, TQ) as an alternative proxy for corporate value. Tobin’s Q captures long-term value creation by reflecting investor expectations of future profitability relative to current asset valuations. Similarly, we also test the hysteresis effect.

The results of this robustness check are presented in Tables 7 and 8. The findings indicate that the positive impact of ESG performance on financial performance remains robust when Tobin’s Q and ESG_Hexun are used as the substitute dependent variable. The presence of trust as a mediating variable is consistent for both variable of financial performance. This suggests that the conclusions drawn from this study are robust and hold across different measurements of financial performance.

Changing the Measure of Explained Variable (Robustness Test of Research Hypothesis 1).

Note. In parentheses is the t value calculated according to the robust standard error. ***, **, * are significant at 1%, 5%, and 10% levels, respectively.

Changing the Measure of Explained Variable (Robustness Test of Research Hypothesis 2).

Note. Table 8 shows the results of the robustness tests for Hypotheses 1 and 2 after replacing the explanatory variables by Tobin’s Q. In parentheses is the t value calculated according to the robust standard error. ***, **, * are significant at 1%, 5%, and 10% levels, respectively.

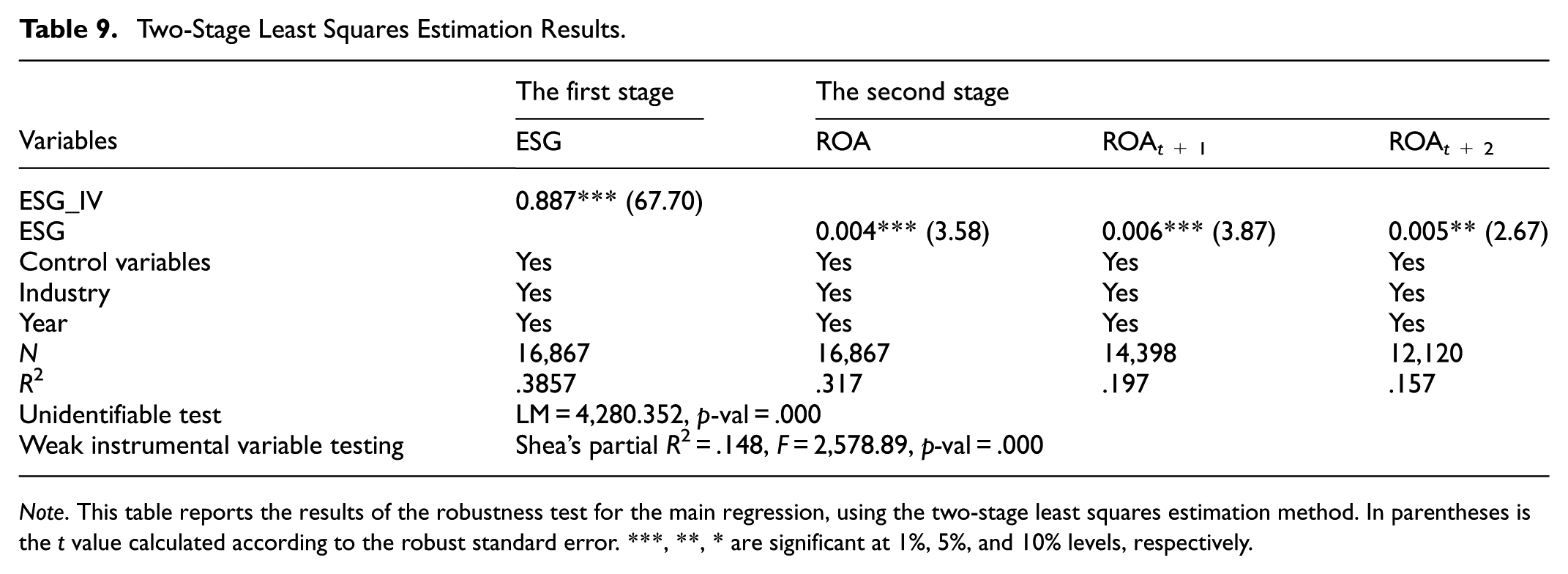

A potential bidirectional causality may exist between ESG performance and financial performance: while improving ESG performance may enhance financial outcomes through risk mitigation and stakeholder trust (Eliwa et al., 2021), firms with stronger financial performance are also better positioned to invest in ESG initiatives (Seow, 2024). To address this endogeneity concern, we adopt a two-stage least squares (2SLS) approach with carefully selected instrumental variables (IVs). We employ the industry-region average ESG performance in the current year (ESG_IV) as the instrumental variable (Q. Li et al., 2024). Firms’ ESG practices are significantly influenced by industry norms and regional regulatory pressures (Cao et al., 2024). For instance, firms in industries with high ESG benchmarks or regions with stringent sustainability regulations face stronger isomorphic pressures to align their ESG efforts with peers (Di Giuli & Kostovetsky, 2014). This ensures a strong correlation between ESG_IV and firm-level ESG performance. The industry-region average ESG performance primarily affects a firm’s financial performance through its own ESG engagement, rather than direct channels. While industry/region characteristics may correlate with financial outcomes, our model explicitly controls for these confounders through industry fixed effects and regional indicators. This satisfies the exclusion restriction (Larcker & Rusticus, 2010).

Table 9 reports the results of the regression results. The average ESG performance (ESG_IV) is significantly positively correlated with ESG performance, consistent with theoretical expectations. After conducting tests for instrument validity and instrument strength, the weak instrument test results show an F-statistic of 2,578.89, exceeding the critical value of 10, with a p-value less than .1. This result rejects the hypothesis of weak instrument presence, indicating that there is no problem of under identification or weak identification issues.

Two-Stage Least Squares Estimation Results.

Note. This table reports the results of the robustness test for the main regression, using the two-stage least squares estimation method. In parentheses is the t value calculated according to the robust standard error. ***, **, * are significant at 1%, 5%, and 10% levels, respectively.

To further validate the mediating effect of trust in the relationship between ESG performance and financial performance, we employ the Bootstrap method. The Bootstrap method is used with 500 repeated samples. The results (Table 10) indicate that the mediating effect of trust is significantly positive (a × b = 0.0003, p = .000, 95% confidence interval CI = [0.0015, 0.0035], excluding 0). This implies that the mediating effect is established, providing additional support for hypothesis 2.

Results of the Bootstrap Mediation Effect Test.

Note. In parentheses is the t value calculated according to the robust standard error. ***, **, * are significant at 1%, 5%, and 10% levels, respectively.

Discussion

ESG Performance and Corporate Financial Performance

The results (Table 4) suggest that the economic benefits generated from corporate ESG practices can outweigh additional costs, thereby enhancing corporate financial performance. ESG ratings contribute to the objective and timely disclosure of corporate information, reducing information asymmetry between stakeholders and firms (Kim & Park, 2023). This aids stakeholders in identifying potential cooperation value and transaction risks, thereby lowering market trading volatility and speculative behaviors. It also helps to curb price fluctuations and improve the liquidity of corporate stocks (Meng-tao et al., 2023). ESG initiatives contribute to inspiring green innovation-driven development strategies within firms (Y. Tan & Zhu, 2022). In the process of fulfilling ESG responsibilities, firms simultaneously optimize organizational structures and business processes. This strengthens the sustainability orientation of corporate operations (Rosecká et al., 2024), restrains short-term self-interest behaviors, attracts resource allocation from regulatory authorities, and provides institutional support for corporate operations.

Mechanism Effect of Trust

As evident in Table 5, ESG performance has a promotional effect on trust, and trust significantly positively influences financial performance. The lagged effects further demonstrate trust’s institutional inertia: once established, it sustains financial benefits even amid short-term ESG performance fluctuations, underscoring its role as a stabilizing informal mechanism. This implies the existence of a pathway where “ESG behavior input—stakeholder perception—formation of trust—improvement in financial performance.”

The micro-macro duality of trust dynamics merits particular emphasis. At the macro-institutional level, trust enables firms to navigate complex stakeholder networks by acting as “social collateral,” attracting partners who value ESG consistency over transactional gains (Chkir et al., 2023). At the micro-behavioral level, it reduces cognitive dissonance among stakeholders—consumers reward ESG-aligned firms through loyalty premiums, while employees exhibit higher productivity when perceiving organizational integrity (Lins et al., 2017). Critically, this duality exposes a threshold effect: trust’s marginal utility diminishes when formal institutions mature, as legal frameworks gradually internalize ESG externalities (Tang & Yang, 2023).

These insights refine resource dependence theory by positioning trust not merely as a relational asset but as a meta-resource that reconfigures power dependencies (Lins et al., 2017). When firms leverage ESG to build trust, they reduce their dependence on coercive formal contracts and gain agency in shaping stakeholder expectations (J. Li & Wu, 2020). For instance, suppliers may accept delayed payments from high-trust firms, interpreting ESG consistency as a guarantee against future exploitation. This rebalancing of dependence is particularly vital for firms in emerging markets, where institutional voids magnify the costs of contractual enforcement (Park et al., 2014).

Moderating Effect of Stakeholder Attention on Trust

Contrary to H3, our results reveal a negative moderating effect of public and market attention, suggesting that heightened scrutiny weakens the ESG-trust relationship (Table 6). First, under conditions of intense stakeholder attention, negative ESG disclosures—such as pollution incidents or governance failures—are disproportionately amplified in public perception, triggering reputational penalties that overshadow broader ESG achievements (Khanna et al., 1998). Therefore, public and market attention to firms may lead to an overload of negative information, resulting in distrust and weakening the positive impact of ESG actions on trust. Second, heightened scrutiny exposes gaps between ESG rhetoric and operational reality, fostering perceptions of greenwashing that erode strategic legitimacy (Aharonson & Bort, 2015; B. Zhou & Ding, 2023). To counteract this, firms should prioritize third-party ESG verification to enhance credibility and demonstrate alignment between commitments and actions.

These findings underscore the need for differentiated strategies to manage stakeholder attention. For firms with low public visibility, standardized ESG reporting remains essential to build foundational trust. In contrast, firms facing high scrutiny should adopt dynamic communication approaches, including multi-platform engagement through social media and interactive sustainability dashboards, to proactively shape narratives and reduce misinterpretation risks. Additionally, targeted engagement with influential stakeholders—such as ESG-focused institutional investors and environmental NGOs—can enhance credibility, as these groups often act as arbiters of corporate legitimacy. Finally, developing metrics to monitor attention elasticity, defined as the sensitivity of trust-ESG relationships to fluctuating scrutiny levels, enables firms to adapt disclosure practices in real time. By integrating these strategies, companies can navigate the dual challenges of visibility and vulnerability inherent in high-attention environments.

Moderating Effect of ESG Performance Consistency on Trust

As indicated by the regression results in Table 6, the better the consistency of ESG performance, the more pronounced the positive moderating impact on trust, supporting the validity of hypothesis 4. Reputation theory and information transmission theory suggest that the temporal consistency of ESG performance can reduce information asymmetry between the company and stakeholders. Consistent corporate behavior encourages stakeholders to play a role in corporate value investment, brand building, and consumer willingness, leading to a significant enhancement of trust. This trust is then further disseminated, creating a virtuous cycle between corporate ESG behavior and trust (Mishina et al., 2012). Moreover, due to the consistent fulfillment of ESG responsibilities, firms that continuously adhere to ESG practices can establish barriers to entry in their respective fields. Such sustained, long-term ESG behavior is more likely to attract the attention of ethical and socially responsible investors (Covin et al., 2006; Rosecká et al., 2024), making it easier to gain the trust of stakeholders. This underscores the importance of ESG performance consistency in fostering trust and creating a positive feedback loop between corporate ESG actions and trust.

Heterogeneity Analysis

We conduct subsample analyses based on the ownership structure, consumer contact with the product and level of regional economic development which could have an impact on the interplay relationship of ESG, trust, and financial performance to further examine the robustness of our results.

Property Right

As a tool for the government to participate and intervene in the economy, it is necessary to further distinguish the heterogeneity of property rights. State-owned enterprises have special social functions such as serving the society, promoting employment, and stabilizing the economy, and they differ significantly from non-state-owned enterprises in terms of asset structure, ESG responsibility, and promotion incentives (Q. Zhu et al., 2016). There are significant differences between SOEs and non-SOEs in terms of asset structure, ESG responsibility, policy burden, promotion incentives, and their economic efficiency and trust acquisition ability will be affected by administrative constraints (Q. Li et al., 2013). In order to test the difference in the impact of interplay relationship of ESG, trust, and financial performance under different property rights, the data samples are divided into state-owned enterprises (SOE = 1) and non-state-owned enterprises (SOE = 0).

Table 11 shows the multiple regression results after grouping. Columns (1) and (2) test the variability of property rights differences in the impact of ESG on corporate financial performance. The regression results indicate that the improvement effect of ESG on financial performance is three times for non-state-owned enterprises than for state-owned enterprises. Columns (3) to (6) test the variability of trust as an influence mechanism. The mediating effect of trust is more pronounced for non-state-owned enterprises.

The Influence of Property Right on the Results.

Note. In parentheses is the t value calculated according to the robust standard error. ***, **, * are significant at 1%, 5%, and 10% levels, respectively.

This divergence originates from distinct institutional logics governing each ownership type. SOEs face competing institutional mandates—as policy instruments, their ESG actions are perceived as compliance with administrative directives rather than strategic investments, eroding stakeholder trust in their sustainability commitments (Q. Li et al., 2013). Three institutional constraints explain this legitimacy discount: (a) soft budget constraints reduce market discipline for ESG outcomes, (b) executive promotion incentives prioritize political alignment over ESG performance, and (c) stakeholders discount SOEs’ ESG efforts as obligatory rather than value-creating (Q. Li et al., 2013).

Non-SOEs, conversely, operate under market legitimacy imperatives that amplify ESG’s strategic value. Their ESG engagements signal authentic stakeholder commitments, functioning as competitive differentiators in capital and product markets. This authenticity strengthens trust mediation effects, as stakeholders reciprocate ESG investments through preferential financing and consumer loyalty—advantages non-SOEs uniquely require to offset their lack of implicit government guarantees.

These findings necessitate differentiated strategies. SOEs should decouple ESG metrics from political evaluations and adopt hybrid governance models balancing social mandates with market responsiveness. Non-SOEs must institutionalize ESG-trust linkages through third-party certifications and transparent impact reporting. Policymakers could further stimulate SOEs’ ESG innovation through outcome-based incentives rather than input targets.

Consumer Contact

When firms use ESG as a market competitive tool in the strategic level, it may lead to different economic effects due to the external visibility of the firm’s own attributes. Consumers, as the most important external stakeholders of the firm, are important in shaping the trust of the firm. Based on signaling theory, direct contact between consumers and products affects the efficiency of information transfer between firms and stakeholders, and makes it easier for stakeholders to perceive firm information (Arian et al., 2023). In this study, the variable representing the degree of consumer contact with corporate products (Consumer) is established based on whether these products are in direct contact with consumers, serving as the classification criterion. We classify firms in the food processing manufacturing industry, apparel and daily necessities manufacturing industry, retailing industry, accommodation and food service industry, and other related manufacturing and service industries as firms whose products are in direct contact with consumers (Arian et al., 2023). The Consumer variable is set to 1 for the above related industries and 0 otherwise.

The regression results are shown in Table 12. The findings in columns (1) and (2) suggest that firms are more likely to translate ESG behaviors into financial performance in industries where their products have direct access to consumers. The regression results in columns (3) to (6) suggest that the mediating role of trust is stronger in these industries. Corporate ESG behavior can be delivered to consumers through products to advertise their corporate ESG responsibility attributes and build a positive brand image, and it is easier to gain competitive advantage and trust through ESG behavior. On the other hand, firms whose products do not reach consumers directly lack opportunities for direct interaction with consumers, and the interaction between consumers and business operations is low, which prevents them from realizing optimal financial results.

The Influence of Consumer Contact Level on the Results.

Note. In parentheses is the t value calculated according to the robust standard error. ***, **, * are significant at 1%, 5%, and 10% levels, respectively.

Regional Economic Development

There are obvious geographical differences in the level of economic development. In regions with a higher level of economic development, the government has a better financial level and can provide more subsidy support for corporate ESG behavior, including tax reductions and loan concessions (W. Li et al., 2020). The public has a stronger awareness of ESG responsibilities, pays more attention to pro-environment behaviors, and the public identifies more with firms with better ESG performance. In regions with a lower level of economic development, firms may face more restrictions on their development, such as limited access to information resources and unstable investment environment, which makes enterprises and stakeholders tend to choose low ESG performance (Yi & Jiang, 2024). The ability of ESG to acquire trust receives limitations. Therefore, this study expects that the financial effects of ESG performance and the ability to acquire trust will be more obvious in regions with higher economic development level.

According to the cluster analysis results of economic development level, the high-level areas include Beijing, Shanghai, Guangdong, Jiangsu, Zhejiang, Hunan, Hainan, Chongqing, Tianjin, etc., while the low-level areas include Guangxi, Qinghai, Ningxia, Liaoning, etc. The regression results are shown in Table 13. The findings in columns (1) and (2) indicate that the regional economic development level strengthens the positive relationship between ESG performance and corporate financial performance, and the regression results in columns (3) to (6) indicate that the mediating role of trust is stronger in regions with higher levels of economic development, which is consistent with the expected results.

The Influence of Regional Economic Development Level on the Results.

Note. In parentheses is the t value calculated according to the robust standard error. ***, **, * are significant at 1%, 5%, and 10% levels, respectively.

Conclusions

Main Findings

This study analyzes the interactive effects of ESG performance, trust, and financial performance, and examines the moderating effects of stakeholder attention and temporal consistency of ESG performance on trust. Our empirical findings provide evidence that: (a) Higher levels of ESG performance are associated with better financial performance, indicating that embracing ESG responsibilities can establish competitive advantages manifesting in both short-term and long-term financial gains. (b) Firms with stronger ESG performance are more likely to gain trust, where trust plays a partially mediating role in the positive impact of ESG on financial performance, following a causal pathway of “ESG behavior input—stakeholder perception—trust formation—financial performance improvement.” (c) The strength of the relationship between ESG performance and trust depends on the level of stakeholder attention and the temporal consistency of ESG. Market and public attention negatively moderates the constructive impact of ESG on trust. Temporal consistency in ESG performance positively moderates the relationship between ESG and trust. Sustained excellence in ESG practices builds psychological contracts with stakeholders, ultimately accelerating the formation of trust. (d) Non-state-owned enterprises, firms with direct contact between products and consumers, and firms in higher economic development regions are more likely to gain trust and financial performance through ESG performance.

This study is one of the first empirical studies to identify how the level of trust affects the relationship between ESG and financial performance. We complement emerging research on the positive effects of informal institutions level by providing direct evidence that non-opportunistic corporate behavior can strengthen trust, thereby enriching new institutional theory. We reveal the intrinsic mechanisms by which ESG performance affects financial performance, deepening our understanding of how trust enhances corporate financial outcomes. By analyzing stakeholders’ influence on these relationships, we guide firms to strategically allocate ESG resources among stakeholders, fostering effective management strategies. This research supports businesses in addressing practical challenges within dynamic socio-economic environments, including mitigating trust crises, alleviating internal and external pressures, and reinforcing resilient operational capabilities.

Policy and Managerial Implications

The findings offer critical insights for policymakers and corporate leaders navigating the evolving ESG landscape. For policymakers, fostering environments that incentivize consistent ESG practices is paramount. Regulatory frameworks should prioritize transparency in ESG disclosures to mitigate information asymmetry, coupled with targeted subsidies for firms in underdeveloped regions to offset implementation costs. Given the amplified trust benefits observed in market-oriented contexts, governments in emerging economies could enhance institutional support through tax incentives or preferential loans for high-ESG performers to reinforce market-driven sustainability initiatives.

For corporate managers, the study underscores the necessity of integrating ESG consistency into long-term strategic planning. Firms should prioritize long-term consistency over reactive adaptations to stakeholder attention spikes while tailoring initiatives to key legitimacy-granting stakeholders. Firms should prioritize third-party ESG certifications to validate commitments and counteract greenwashing perceptions, especially under heightened public scrutiny. Dynamic stakeholder engagement—via multi-platform communication and tailored interactions with influential groups like ESG-focused investors—can amplify trust-building efforts. Additionally, industries with direct consumer interfaces should leverage product-level ESG attributes to strengthen brand loyalty. By aligning resource allocation with stakeholder priorities and regional economic conditions, firms can optimize the financial returns of ESG investments while cultivating resilient trust capital.

Limitations

This study has several limitations that warrant further exploration. First, it does not fully incorporate multi-dimensional corporate strategies. Future research should investigate how firms balance their tripartite strategies across environmental, social, and governance (ESG) dimensions to optimize outcomes. Second, the study does not address the nuanced alignment of segmented stakeholders. For example, under the social dimension, it remains unclear whether firms should allocate equal resources to sub-social responsibilities, such as philanthropic activities and employee welfare, or whether such strategic decisions differentially impact trust and financial performance. Additionally, certain methodological limitations exist. For instance, the measure of public attention relies on web search indices, which capture real-time public engagement but may inherit platform-specific biases. Future studies should consider integrating alternative data sources to mitigate these biases and provide a more comprehensive understanding of public attention dynamics.

Footnotes

Ethical Considerations

This article does not contain any studies with human or animal participants.

Author Contributions

Zhaokun Guo: Conceptualization, Data Curation, Formal Analysis, Methodology, Writing—original draft. Weiyan Jiang: Formal Analysis, Methodology, Validation, Writing—review & editing. Kunhui Ye: Supervision, Funding Acquisition, Writing—review & editing.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the National Natural Science Foundation of China [grant number 72371043]; the Fundamental Research Funds for the Central Universities [grant number 2024CDJSKPT05]; and the Graduate Research and Innovation Foundation of Chongqing, China [grant number CYB25005].

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The datasets generated during and/or analyzed during the current study are available from the corresponding author on reasonable request.