Abstract

This study investigates the impact of digital transformation on firms’ environmental, social, and governance (ESG) performance. Using panel data from 1,157 listed firms in China between 2012 and 2021, obtained from the Bloomberg database and the CSMAR financial database, we find that digital transformation significantly improves ESG performance. The positive effect is more pronounced in non-high-tech industries, indicating greater gains from digital upgrading in traditional sectors. Moreover, financial constraints weaken the positive relationship between digital transformation and ESG outcomes. Further analysis shows that digital transformation has a significant positive effect on both environmental and social performance, but no significant impact on governance performance. These findings suggest that digital transformation can serve as an important lever for promoting corporate sustainability, particularly in firms facing fewer financial constraints and operating in less digitally advanced industries.

Keywords

Introduction

The pursuit of sustainability has become a defining feature of contemporary business strategy, driven by mounting global concerns over environmental degradation, social responsibility, and governance integrity (Kim et al., 2024; Lai et al., 2024). In response, the environmental (E), social (S), and governance (G) framework has evolved into a key performance paradigm for evaluating corporate contributions beyond traditional financial metrics (Kräussl et al., 2023; Long et al., 2024). However, transitioning from environmental, social, and governance awareness to tangible performance remains difficult. Despite growing regulatory pressures and rising stakeholder expectations—especially in emerging markets such as China—many firms still struggle to meet ESG benchmarks (Y. Chen et al., 2022). This gap is often attributed to factors such as organizational inertia, insufficient managerial capabilities, inadequate data infrastructure, and competing short-term financial goals (Liang & Li, 2023; Liu, 2025). As such, identifying mechanisms that can help firms overcome these barriers and achieve meaningful ESG outcomes has become a critical research priority.

Among the potential solutions, digital transformation has gained traction as a promising pathway for advancing ESG objectives. Defined as the integration of advanced digital technologies—such as big data, artificial intelligence, blockchain, and cloud computing—into business strategies and workflows, digital transformation allows firms to enhance operational efficiency, transparency, and stakeholder engagement (Cheng et al., 2023; Guo et al., 2023). For instance, blockchain improves supply chain traceability, artificial intelligence supports environmental risk monitoring, and cloud-based platforms facilitate inclusive stakeholder communication (Bibri et al., 2023; Pu & Zulkafli, 2024). However, the implementation of digital transformation often entails substantial investment in technological infrastructure, managerial capabilities, and organizational reconfiguration (Broccardo et al., 2022; Matt et al., 2022), which may pose significant barriers to firms operating under financial constraints (Li et al., 2024). Furthermore, the effectiveness of digital transformation in advancing ESG performance is contingent upon multiple contextual elements, including digital readiness, human capital in technology, and absorptive capacity for innovation (Van Pham & Tran, 2025; Vararean-Cochisa & Crisan, 2024). Therefore, the realization of such benefits is not guaranteed and often hinges on firm-specific conditions and external environments.

One important organizational factor that may condition the effectiveness of digital transformation in delivering ESG outcomes is financial constraint. From the perspective of the Technology–Organization–Environment (TOE) framework, an organization’s internal resource base—including its financial flexibility—is critical in determining the success of technological innovation (Z. Hao et al., 2022; S. Wang & Zhang, 2025). Digital transformation typically requires substantial upfront investments in infrastructure, data systems, employee training, and managerial realignment (Q. Wang et al., 2025). Firms operating under financial pressure may lack the absorptive capacity to integrate these technologies effectively, leading to fragmented implementation or premature abandonment of ESG-oriented digital projects (S. Lin & Deng, 2024). Although government incentives and regulatory mandates increasingly promote digitalization, their effectiveness is limited when firms cannot mobilize internal resources. This raises an important question: even if digital transformation has the potential to improve ESG performance, does this relationship hold under varying levels of financial flexibility?

In addition to organizational constraints, environmental factors—particularly industry context—may further shape how digital transformation translates into ESG outcomes. Within the TOE framework, the external environment, including sectoral technological maturity and institutional support, plays a crucial role in shaping technology adoption and its outcomes (Z. Hao et al., 2022; Matt et al., 2022). High-tech industries tend to benefit from mature digital infrastructures, better-skilled workforces, and stronger innovation cultures, which facilitate more seamless ESG-related digital integration (P. Hao et al., 2024). In contrast, firms in non-high-tech sectors, such as traditional manufacturing or logistics, often operate with outdated systems and lower digital readiness (Teng et al., 2023). For them, digital transformation may offer larger marginal gains by overcoming structural inefficiencies and compliance gaps. These inter-industry differences suggest the need to explore whether the ESG benefits of digital transformation are more pronounced in non-high-tech sectors.

Moreover, ESG performance is a multidimensional construct, and the effects of digital transformation may differ across its environmental, social, and governance components. Prior studies have largely relied on aggregated ESG scores, thereby overlooking the distinctive mechanisms through which digital technologies may influence each dimension (Broccardo et al., 2022; Kräussl et al., 2023). For example, blockchain and IoT technologies are often directly used in environmental data management and carbon footprint tracking, while cloud-based HR systems can improve labor welfare, diversity reporting, and stakeholder engagement (Luo & Tang, 2022; Pu, 2025). To empirically address these theoretical and contextual gaps, this study constructs a novel patent-based measure of firm-level digital transformation and investigates its ESG implications across different constraint levels, industry contexts, and ESG sub-dimensions. Specifically, we seek to answer the following questions: (a) Does digital transformation enhance corporate ESG performance? (b) To what extent do financial constraints moderate the relationship between digital transformation and ESG performance? (c) Is the effect of digital transformation on ESG performance more pronounced in non-high-tech industries than in high-tech industries? (d) Among E, S, and G components, which dimensions are most affected by digital transformation?

This study makes three key contributions. First, we construct a novel patent-based indicator to capture firm-level digital transformation, offering a more objective and dynamic measure than traditional proxies based on static text analysis. Second, we examine how digital transformation affects disaggregated ESG dimensions (environmental, social, and governance), addressing a critical gap in prior literature that has predominantly relied on aggregate ESG scores. Third, by introducing financial constraints as a moderating factor, we provide new insights into the conditions under which digital transformation can generate sustainability outcomes. These contributions enrich the theoretical understanding of the digital–ESG nexus and offer practical implications for firms seeking to align digital strategies with sustainable development goals.

The rest of the paper proceeds as follows. Section “Theoretical Background and Hypothesis” outlines the theoretical framework and hypotheses. Section “Research Design” details the data, variables, and empirical methods. Section “Result Analysis” presents the main results and robustness checks. Section “Moderation Analysis” examines the moderating role of financial constraints. Section “Exploring Heterogeneous Effects” explores industry heterogeneity in the digital transformation–ESG relationship. Section “Further Analysis” analyzes the effects of digital transformation across the individual ESG sub-dimensions. Section “Conclusions and Recommendation” concludes with a summary of key findings and their broader theoretical and practical implications.

Theoretical Background and Hypothesis

Digital Transformation and ESG Performance

ESG performance reflects a firm’s ability to balance financial success with environmental responsibility, social engagement, and sound governance practices. It includes concrete efforts such as reducing carbon footprints, improving labor conditions, and enhancing board independence—dimensions increasingly used by investors, regulators, and consumers to assess corporate sustainability and long-term value (Kräussl et al., 2023; P. Hao et al., 2024). Despite growing awareness of ESG’s strategic importance, many firms continue to face difficulties in embedding ESG objectives into core operations, often due to agency frictions, resource rigidity, and limited adaptive capabilities (e.g., S. Lin & Deng, 2024; Matt et al., 2022; Q. Wang et al., 2025).

Digital transformation introduces new possibilities to overcome these constraints by reshaping how firms generate, allocate, and govern resources. To understand how digital transformation may influence ESG performance, we draw upon three foundational theoretical perspectives: agency theory (AT), the resource-based view (RBV), and the dynamic capabilities framework (DCF). AT highlights the misalignment of interests between owners and managers, particularly when managerial decisions prioritize short-term financial targets at the expense of long-term value creation. This perspective suggests that improved transparency, monitoring, and incentive alignment are crucial for sustainable decision-making. RBV posits that firms achieve sustained competitive advantage through the possession and strategic deployment of valuable, rare, inimitable, and non-substitutable resources. In this context, digital technologies can be understood as strategic assets that, when effectively leveraged, allow firms to embed ESG priorities into everyday processes while maintaining operational efficiency. DCF, meanwhile, emphasizes a firm’s ability to sense environmental changes, seize emerging opportunities, and reconfigure internal resources in response to volatility. Given the evolving landscape of stakeholder expectations and regulatory pressures related to ESG, dynamic capabilities are especially critical for firms seeking to implement responsive and resilient sustainability strategies. Building on these perspectives, we outline the following theoretical pathways through which digital transformation may support ESG performance:

One key pathway through which digital transformation supports ESG performance lies in its potential to mitigate agency problems and enhance transparency. According to AT, misaligned incentives and limited oversight often discourage ESG investment, which involves long-term horizons and uncertain payoffs (Cheng et al., 2023). Emerging technologies such as AI-driven monitoring, blockchain-based reporting, and automated disclosures can improve real-time transparency and reduce information asymmetry (Q. Wang et al., 2025; Xiao et al., 2024), thereby enabling better accountability and ESG-aligned decision-making.

Digital transformation is likely to serve as a strategic resource that supports ESG integration. Under the RBV, technologies like predictive analytics, platform ecosystems, and real-time data systems can enhance operational coordination, optimize resource utilization, and embed ESG considerations into value-creating processes (H. Huang et al., 2023; Khamisu et al., 2024). These assets help firms pursue ESG goals without compromising competitiveness.

In dynamic environments, digital transformation tends to strengthen dynamic capabilities that enable ESG adaptation. The DCF suggests that firms require agility and foresight to align sustainability strategies with shifting stakeholder expectations (Khamisu et al., 2024; Pesqueira & Sousa, 2024; Xiao et al., 2024). Digital tools facilitate early trend detection, stakeholder sentiment analysis, and ESG performance monitoring (Li et al., 2024; Pesqueira & Sousa, 2024; Tao et al., 2024), enabling firms to continually refine their ESG practices and maintain strategic alignment in dynamic environments.

Based on these theoretical foundations, we propose the following hypothesis:

The Moderating Role of Financial Constraints

While digital transformation can enhance ESG performance through improved transparency, efficiency, and adaptability, its success often depends on firms’ capacity to absorb and sustain such transformation. In particular, financial constraints may significantly moderate the effectiveness of digital initiatives in generating ESG outcomes.

According to resource dependence theory (RDT), firms must secure critical external and internal resources—such as capital, knowledge, and technology—to execute strategic objectives (Drees & Heugens, 2013). Digital transformation, although potentially cost-saving in the long term, requires substantial initial investment in infrastructure, software systems, and employee capabilities (Matt et al., 2022). For financially constrained firms, the lack of discretionary capital may limit their ability to acquire, implement, or scale digital technologies that support ESG goals (Liu, 2025; Long et al., 2024).

Moreover, the TOE framework emphasizes that successful digital adoption depends not only on technological opportunity and environmental support but also on the firm’s organizational readiness—which includes financial flexibility (Z. Hao et al., 2022; S. Wang & Zhang, 2025). Without adequate financial slack, firms may defer or reduce investment in long-term ESG projects, especially when such projects involve uncertain returns and complex interdepartmental coordination.

Empirical studies have shown that under high financial pressure, firms tend to prioritize short-term performance over strategic sustainability investments (Tian et al., 2025). Even when digital tools are available, constrained firms may lack the capacity to integrate them meaningfully into ESG governance systems, resulting in fragmented implementation or symbolic adoption (S. Lin & Deng, 2024; Sulkowski & Jebe, 2022). Therefore, financial constraints may weaken the otherwise positive influence of digital transformation on ESG outcomes.

Based on this reasoning, we propose the following hypothesis:

Industry Heterogeneity in the Digital Transformation–ESG Link

The impact of digital transformation on ESG performance may vary significantly across industries due to differences in technological infrastructure, regulatory expectations, and innovation cultures. From the environmental dimension of TOE framework, industry characteristics represent a critical external context that shapes both the motivation for and the capacity to implement digital strategies (C. Lin & Chen, 2023).

Firms operating in high-tech industries often benefit from advanced digital infrastructure, stronger R&D intensity, and higher digital literacy among employees. These conditions facilitate the seamless integration of digital tools into environmental monitoring systems, stakeholder communication platforms, and data-driven governance processes (Amankona et al., 2025). Moreover, high-tech sectors typically face greater institutional pressures—such as ESG-focused innovation mandates and international reporting standards—which further incentivize digital sustainability practices (Wan et al., 2025).

By contrast, non-high-tech industries—such as traditional manufacturing, construction, or logistics—often lag in digital maturity and rely on legacy systems that inhibit efficient data integration and process automation (X. Huang et al., 2025). Paradoxically, this lower baseline may allow for more visible and substantial ESG gains once digital transformation is implemented. In such industries, digital tools may help overcome long-standing inefficiencies, improve environmental compliance, and enhance transparency in historically opaque operational systems (C. Lin & Chen, 2023; Teng et al., 2023). Therefore, the marginal benefit of digital transformation on ESG outcomes may be more pronounced in non-high-tech sectors.

Based on this logic, we propose the following hypothesis:

Research Design

Data and Sample

This study investigates the relationship between digital transformation and ESG performance using a panel dataset of Chinese A-share listed companies over the period 2012 to 2021. The 10-year horizon captures significant regulatory, technological, and sustainability-related developments in China’s corporate environment, providing a rich empirical setting for analysis. Firm-level ESG performance data are obtained from the Bloomberg ESG Rating database, which evaluates listed companies based on publicly disclosed information across environmental, social, and governance dimensions. Bloomberg’s ESG scores are widely used in academic and professional research for their methodological consistency and international comparability, while still maintaining strong applicability to the Chinese market. Corporate financial, governance, and operational data are collected from the China Stock Market and Accounting Research (CSMAR) database. This database provides high-quality, granular data on firm characteristics such as ownership structure, board composition, profitability, leverage, and industry classification, and is widely recognized in empirical research on Chinese listed firms.

To ensure data reliability and analytical consistency, we implemented the following screening procedures. First, firms in the financial sector, including banks, insurance companies, and other financial institutions, are excluded due to their distinct accounting standards and regulatory requirements. Second, we removed all firms designated as “ST” (Special Treatment) by the China Securities Regulatory Commission (CSRC) during the sample period, as these firms are subject to financial distress warnings or operational abnormalities over two consecutive years. Third, we excluded all observations with missing values for any of the key variables used in the empirical analysis. After applying these criteria, our final sample consists of 9,479 firm-year observations, representing 1,157 unique non-financial listed firms across a wide range of industries.

Measurement of Variables

Each ESG component is scored separately on a scale from 0 to 100, with higher scores indicating greater transparency and stronger alignment with global ESG standards. These scores are then aggregated to construct a firm’s overall ESG performance score. Following prior literature (e.g., C. Chen et al., 2025; Tabur & Bildik, 2025), we use the composite Bloomberg ESG score as a continuous variable in our analysis. Higher values indicate stronger ESG engagement and a greater commitment to sustainability objectives across environmental protection, social responsibility, and governance practices.

To construct this measure, we collected data on all patent applications filed by Chinese A-share listed companies from 2012 to 2021, drawing from China National Intellectual Property Administration. We identified digital-related patents based on keywords and International Patent Classification codes associated with key digital technologies. This approach aligns with recent literature that treats digital patent activity as a proxy for firms’ digital transformation efforts (L. Wang, 2023). The annual count of digital patent applications was aggregated at the firm-year level. To account for the skewed distribution of patent counts, we applied a logarithmic transformation using the formula LN (digital patents + 1), ensuring the measure is more normally distributed and suitable for regression analysis. The resulting variable captures the intensity of firms’ digital innovation and reflects the extent to which they engage in technology-driven transformation.

Variable Definitions and Data Sources.

Regression Model

To investigate the effect of DT on ESG and to explore how FC may influence this relationship, the following regression models are developed:

Baseline Model

The baseline regression model is designed to assess the direct impact of DT on ESG:

where ESG

i,t

represents the ESG performance of firm i in year t, measured using the Bloomberg ESG rating system. DT

i,t

denotes digital transformation. Controls

i,t

is a vector of control variables, including LEV, FA, ROE, SG, LOSS, BS, ID, and OC. Firm fixed effects (

Moderation Models

To analyze the moderating effect of FC on the relationship between DT and ESG, the following models are constructed:

For financing constraints:

Result Analysis

Descriptive Statistics

Table 2 presents the descriptive statistics for all variables used in this study. The sample comprises 9,479 firm-year observations from Chinese A-share listed companies spanning the period 2012 to 2021. The dependent variable, ESG performance, is measured using Bloomberg’s ESG Disclosure Score. The mean ESG score is 28.665, with a standard deviation of 9.113. The values range from 6.198 to 68.917, indicating considerable variability in ESG disclosure quality across firms. This dispersion suggests that while some firms maintain high levels of ESG transparency, others disclose minimally, reflecting different degrees of sustainability engagement within the sample.

Descriptive Statistics.

The independent variable, digital transformation (DT), is proxied by the natural log of one plus the firm-level count of digital-technology patent applications. The mean value of DT is 0.966, with a standard deviation of 1.553, and values ranging from 0 to 8.447. This wide range implies substantial heterogeneity in firms’ digital innovation intensity. A alternative measure (DT1), constructed using an alternative text-based approach, is also reported, with a mean of 1.406, supporting robustness and comparability of results.

As for the moderating variables, financial constraints are captured using the Whited and Wu (WW) index and the Financing Constraints (FC) index. The WW index has a mean of −1.068, and the FC index averages 0.256, both showing moderate variation across the sample.

Control variables such as financial leverage (LEV), firm age (FA), return on equity (ROE), sales growth (SG), loss indicator (LOSS), board size (BS), board independence (ID), and ownership concentration (OC) exhibit distributional characteristics consistent with those reported in prior ESG and corporate governance research. Specifically, the mean value of LEV is 0.492, indicating that, on average, total liabilities account for nearly half of total assets, reflecting a moderate level of financial leverage. FA, measured as the natural logarithm of firm age, has a mean of 2.942, suggesting that the sample consists largely of well-established firms. The average ROE is 0.081, indicating modest profitability across the sample. SG averages 0.170, with considerable variation, capturing differing revenue growth trajectories among firms. The binary variable LOSS has a mean of 0.088, implying that approximately 8.8% of firm-year observations report negative net income.

In terms of governance characteristics, the average board size (BS) is 2.176 (log-transformed), reflecting typical board structures among Chinese listed companies. Board independence (ID) averages 37.629%, indicating that over one-third of board members are independent directors, consistent with regulatory requirements. Finally, ownership concentration (OC) has a mean of 37.065%, suggesting that in most firms, the largest shareholder maintains significant influence over corporate decisions.

Benchmark regression analysis

Table 3 presents the results of the benchmark regression analysis examining the impact of DT on ESG. Across all model specifications—including pooled OLS (Column 1), fixed effects (Column 2), random effects (Column 3), and fixed effects with firm-clustered standard errors (Column 4)—the coefficient on DT remains consistently positive and statistically significant at the 1% level. This provides robust evidence that greater engagement in digital transformation is associated with improved ESG performance.

Main Results.

Note. Statistical significance is indicated by *, **, and *** at the 10%, 5%, and 1% levels, respectively. Firm-clustered robust standard errors are reported in brackets.

Specifically, in the pooled OLS model (Column 1), the coefficient on DT is 0.746 (p < .01), indicating a strong positive association. After controlling for firm-level unobserved heterogeneity using fixed effects in Column (2), the coefficient drops to 0.359 (p < .01) but remains significant, suggesting that the positive relationship is not driven by time-invariant firm characteristics. The random effects model (Column 3) yields a DT coefficient of 0.480 (p < .01), while Column (4), which incorporates firm-level fixed effects and robust standard errors clustered at the firm level, reaffirms the robustness of the findings with a DT coefficient of 0.359 (p < .01). The high adjusted R2 values across specifications, especially .695 in the fixed-effects models, indicate strong explanatory power.

Overall, the results confirm that digital transformation significantly enhances ESG performance, supporting the view that digitalization is a vital enabler of corporate sustainability (Fan et al., 2024; Quttainah & Ayadi, 2024). By improving transparency, responsiveness, and resource efficiency, digital transformation helps firms embed ESG considerations into core operations. These findings align with the resource-based view, which sees digital capabilities as strategic assets for sustainable advantage (Hillman et al., 2009; Khanra et al., 2021), and the dynamic capabilities framework, which emphasizes adaptability to evolving ESG demands (Teece, 2007). They also resonate with agency theory, as digital tools reduce information asymmetry and strengthen oversight, aligning managerial behavior with stakeholder interests (Singh et al., 2024; Stoelhorst & Vishwanathan, 2022).

Robustness Checks

To assess the robustness of our benchmark results, we conduct a series of complementary tests using alternative specifications, samples, and model adjustments. The results are summarized in Table 4.

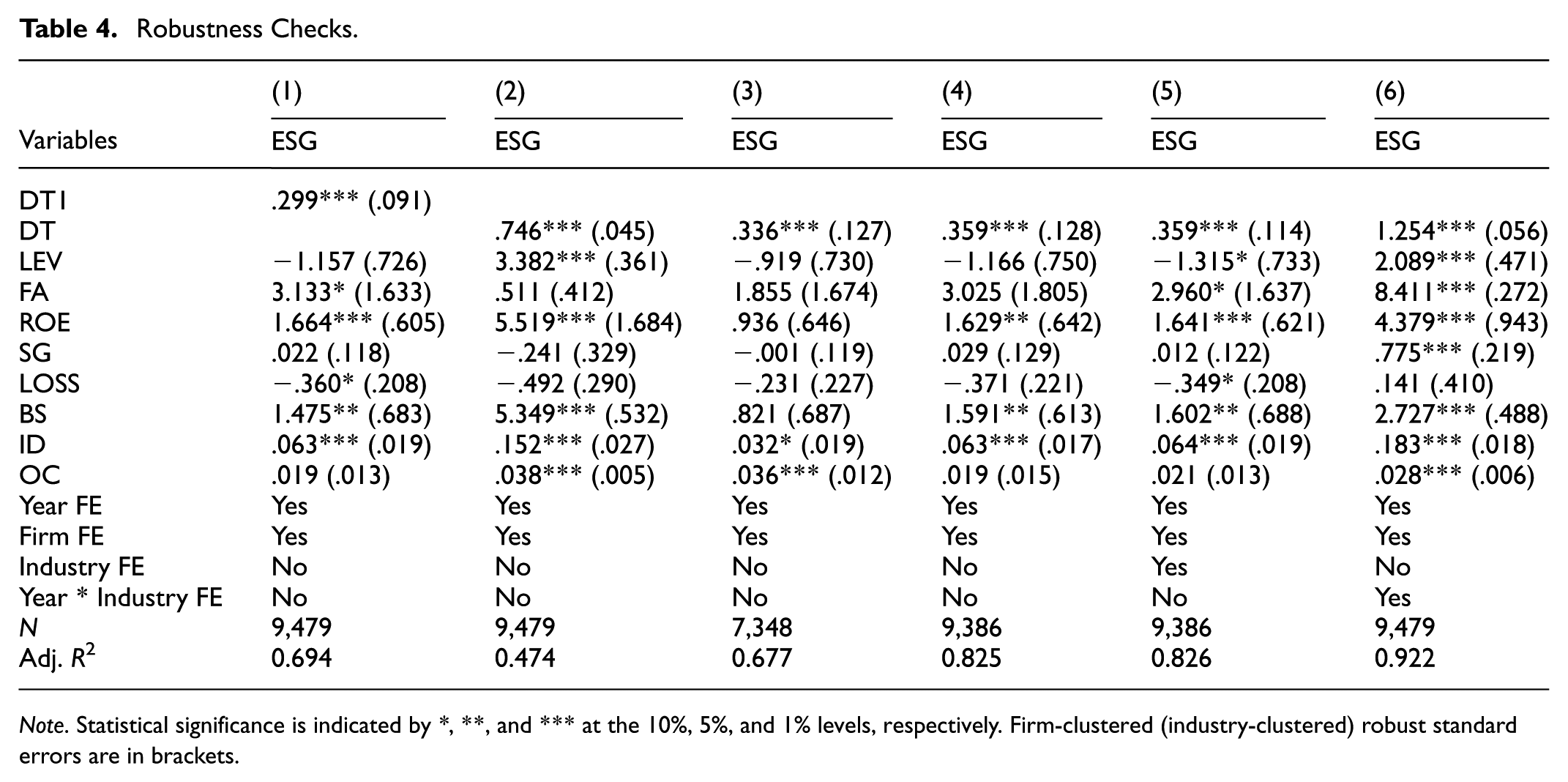

Robustness Checks.

Note. Statistical significance is indicated by *, **, and *** at the 10%, 5%, and 1% levels, respectively. Firm-clustered (industry-clustered) robust standard errors are in brackets.

First, we test the sensitivity of our findings to the measurement of digital transformation. Column (1) replaces the main independent variable with an alternative proxy (DT1), and the results remain significantly positive (β = .299, p < .01), supporting the validity of our core explanatory variable.

Second, in Column (2), we apply the Driscoll-Kraay fixed effects estimator to address potential heteroskedasticity, autocorrelation, and cross-sectional dependence in the panel data structure. The coefficient of DT remains positive and highly significant (β = .746, p < .01), confirming the robustness of our findings under more flexible error assumptions.

Third, we perform a subsample analysis by excluding the pandemic years (2020 and 2021) to mitigate potential distortions caused by COVID-19. As shown in Column (3), the association between DT and ESG performance persists (β = .336, p < .01), suggesting that the main results are not driven by crisis-related anomalies.

Fourth, we adjust the clustering level of standard errors from the firm level to the industry level to account for possible intra-industry correlation. Column (4) shows that the positive effect of DT remains statistically significant (β = .359, p < .01), reinforcing the reliability of our inference.

Fifth, we incorporate additional fixed effects by introducing industry dummies in Column (5). The coefficient of DT continues to be positive and significant (β = .359, p < .01), suggesting that our results are not driven by industry-specific omitted variables.

Finally, Column (6) adds year–industry interaction fixed effects to capture dynamic sector-specific time trends. Even under this stringent control, DT remains positively associated with ESG performance (β = 1.254, p < .01), highlighting the stability of our conclusion across nuanced heterogeneity structures.

Moderation Analysis

Table 5 presents the moderating effects of financing constraints on the relationship between DT and ESG, using two widely recognized indices: the WW index and the FC index. Columns (1) and (2) explore the moderating effect of the WW index, while Columns (3) and (4) incorporate the FC index as an alternative measure.

The Moderating Role of Financing Constraints.

Note. The symbols **, and *** denote statistical significance at the 5% and 1% levels, respectively; Firm-clustered robust standard errors are reported in brackets.

In Column (1), the interaction term DT*WW is negative and highly significant (γ = −4.267, p < .01), even without control variables, indicating that higher financing constraints (as captured by WW) weaken the positive impact of digital transformation on ESG performance. After introducing firm-level control variables—such as LEV, FA, ROE, SG, LOSS, BS, ID, and OC—the negative moderating effect persists (γ = −4.102, p < .01), as shown in Column (2). Columns (3) and (4) replicate this analysis using the FC index. Similar to the WW-based results, the DT*FC interaction term is negative and statistically significant in both the uncontrolled (γ = −.982, p < .01) and fully controlled (γ = −0.895, p < .01) models. These findings consistently suggest that the positive influence of digital transformation on ESG outcomes is dampened in firms facing greater financial constraints.

The moderation patterns imply that firms with limited access to external financing may struggle to allocate sufficient resources toward ESG-related digital initiatives, thereby reducing the efficacy of digital transformation in driving sustainability performance. These results extend prior literature that highlights the resource-dependent nature of ESG advancement and confirm that financial slack plays a pivotal enabling role (e.g., Luo & Tang, 2022; Quttainah & Ayadi, 2024). From a theoretical standpoint, the findings resonate with resource dependence theory, which posits that external capital access is essential for executing long-term strategic investments like digital ESG initiatives. Moreover, the results align with the resource-based view by illustrating how financial constraints diminish a firm’s ability to leverage its digital assets for sustained competitive advantage (Khanra et al., 2021). In financially constrained settings, managers may prioritize short-term operational survival over long-term ESG investments, thereby undermining the sustainability-enhancing potential of digitalization.

Exploring Heterogeneous Effects

To further investigate the boundary conditions under which DT influences ESG performance, we explore industry heterogeneity as a contextual factor. Drawing on the environmental dimension of the TOE framework, industry context shapes both the external pressures and the internal capacity for digital sustainability initiatives (C. Lin & Chen, 2023). Specifically, we hypothesize that the ESG-enhancing effects of DT may vary between high-tech and non-high-tech industries due to disparities in digital maturity, innovation incentives, and regulatory exposure.

Figure 1 presents the regression results for firms in high-tech industries. Although the estimated coefficient of DT is positive (.221), it fails to reach statistical significance, suggesting that in technologically advanced sectors, the marginal contribution of additional digital transformation to ESG performance is relatively limited. This may stem from a ceiling effect—firms in these sectors already exhibit high levels of digital integration, and incremental improvements may not substantially alter ESG outcomes. Furthermore, existing ESG mandates and digital infrastructure in high-tech firms may render additional transformation efforts less impactful.

The impact of digital transformation on ESG performance in high-tech industries.

In contrast, Figure 2 reveals a markedly different pattern for non-high-tech industries. Here, the coefficient of DT is 0.479 and statistically significant at the 1% level, underscoring the pronounced ESG benefits of digital transformation in traditionally less digitized sectors. This finding aligns with prior arguments that non-high-tech industries—such as manufacturing, construction, and logistics—often possess outdated systems and opaque processes. As such, the introduction of digital technologies in these contexts can yield substantial gains in environmental compliance, social responsibility, and information transparency (Teng et al., 2023; X. Huang et al., 2025).

The impact of digital transformation on ESG performance in non-high-tech industries.

Therefore, the results provide strong support for Hypothesis 3. They highlight that the effectiveness of digital transformation in promoting ESG performance is contingent on industry characteristics, with non-high-tech firms deriving greater marginal value from digital adoption. These findings carry important implications for policymakers and managers, emphasizing the need for sector-specific digital strategies and differentiated ESG support mechanisms that recognize industry-level disparities in digital readiness and sustainability potential.

Further Analysis

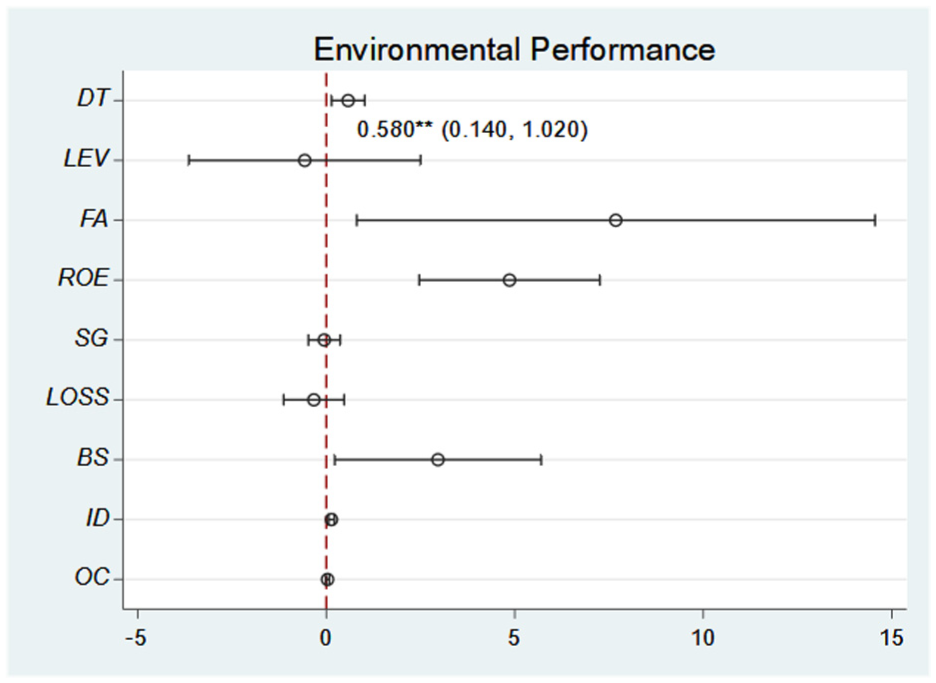

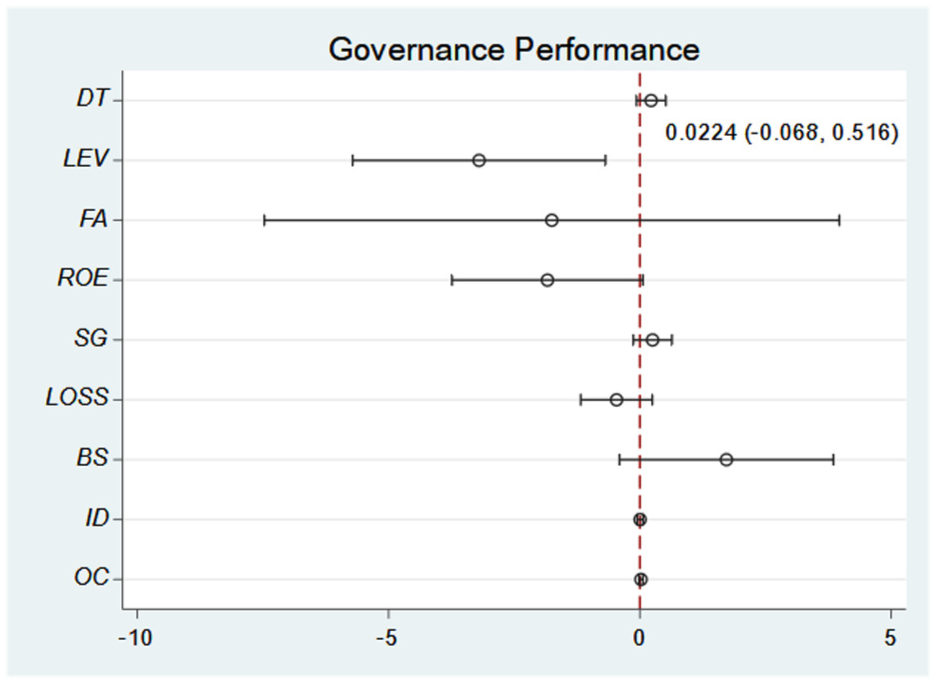

While the preceding analyses confirm that DT significantly enhances overall ESG performance, a critical question persists: Which specific dimensions of ESG are most responsive to digital transformation? To address this, we decomposed the ESG index into its three core subcomponents—environmental (E), social (S), and governance (G)—and conducted separate regressions using DT as the key explanatory variable.

The empirical results, illustrated in Figures 3 through 5, reveal a heterogeneous pattern of effects. Specifically, DT exerts a positive and statistically significant influence on both the E and S dimensions. The estimated coefficient for E is .580 (p < .05), while for S it is .291 (p < .05), suggesting that digital transformation plays a salient role in advancing corporate environmental initiatives and improving social performance. Surprisingly, however, the coefficient for G is .224 and statistically insignificant, indicating that DT may not meaningfully affect governance structures or practices within the firms in our sample.

Impact of digital transformation on environmental performance.

Impact of digital transformation on social performance.

Impact of digital transformation on governance performance.

The strong impact on the environmental (E) dimension aligns with existing research suggesting that digital technologies—such as cloud-based monitoring systems, IoT-enabled emissions tracking, and AI-driven sustainability analytics—facilitate real-time environmental data collection, predictive risk management, and the optimization of resource efficiency (Fan et al., 2024; Singh et al., 2024). These capabilities enable firms to align more closely with environmental regulations and stakeholder expectations, thereby enhancing environmental transparency and compliance.

The positive effect on the social (S) dimension can be attributed to the role of digital transformation in strengthening employee engagement platforms, improving occupational health and safety through smart technologies, and enabling more responsive community outreach and stakeholder interaction (Quttainah & Ayadi, 2024). Digital tools also support diversity and inclusion initiatives by mitigating biases in recruitment and monitoring workforce metrics more effectively.

In contrast, the insignificant effect on governance (G) is notable and warrants further discussion. One plausible explanation is that digital transformation, while capable of improving operational and reporting efficiencies, may not automatically lead to changes in internal governance mechanisms, such as board composition, ownership concentration, or anti-corruption practices. Governance-related reforms often involve institutional inertia, regulatory frameworks, and entrenched power dynamics that digital tools alone may be insufficient to alter (Martínez-Ferrero et al., 2024; Kräussl et al., 2023). Moreover, firms might prioritize environmental and social reporting—especially under increasing ESG disclosures—while treating governance enhancements as secondary, less visible efforts with longer payback periods. These findings underscore the differential channels through which digital transformation affects corporate sustainability. While DT serves as a powerful enabler of environmental and social value creation, its effectiveness in transforming governance structures remains limited, pointing to a need for complementary institutional or policy interventions that explicitly target governance modernization. This nuanced insight enriches the existing literature by revealing that the benefits of digital transformation for ESG are not uniform across all pillars, and highlights the importance of tailoring digital strategies to the specific ESG objectives a firm aims to achieve.

Conclusions and Recommendation

This study examines the influence of corporate digital transformation—proxied by digital patent data—on ESG performance among Chinese listed firms from 2012 to 2021. Leveraging Bloomberg ESG ratings and financial data from CSMAR, we find robust evidence that digital transformation significantly enhances firms’ overall ESG performance. However, the magnitude and direction of this effect vary under different financing environments and industry contexts. Specifically, financing constraints weaken the positive ESG effects of digital transformation, indicating that limited financial flexibility may hinder the full realization of sustainability benefits from digital initiatives. Furthermore, industry heterogeneity analysis reveals that the ESG-enhancing effects of digital transformation are more pronounced in non-high-tech industries, where digital upgrades yield greater marginal improvements due to previously limited digital infrastructure.

From a dimensional perspective, digital transformation exhibits heterogeneous impacts across the E, S, and G components of ESG. While its influence on environmental and social performance is significantly positive—likely due to enhanced data transparency, emission monitoring, and stakeholder engagement—the effect on governance performance is statistically insignificant. This finding suggests that digitalization may not automatically translate into improved corporate governance, which are often shaped by deeper institutional and regulatory frameworks.

Theoretically, this study contributes to a nuanced understanding of how digital transformation shapes sustainability outcomes through both resource and constraint lenses. Drawing on the resource-based view, digital capabilities serve as strategic assets that support firms’ adaptation to ESG-related pressures. Meanwhile, agency theory helps explain why financing constraints and governance frictions may obstruct these benefits. By incorporating heterogeneity analyses, this study also extends the applicability of the Technology–Organization–Environment framework to ESG contexts, emphasizing that external industry environments moderate the efficacy of digital strategies.

Practically, the findings offer timely insights for corporate decision-makers and policymakers aiming to leverage digitalization for sustainability. First, firms—especially those in capital-constrained or traditional sectors—should prioritize digital investments that directly support environmental monitoring and social responsibility, such as AI-driven analytics and cloud-based stakeholder systems. Second, financial institutions and regulators should consider offering preferential financing mechanisms to digitally transforming firms, enabling them to overcome capital barriers to ESG upgrades. Third, ESG reform strategies should not rely solely on digital adoption but also incorporate complementary governance reforms to ensure holistic improvement across all ESG dimensions.

Finally, this study acknowledges several limitations. The use of patent-based digital transformation indicators, while objective, may not capture all qualitative aspects of firms’ digital maturity. Moreover, the dataset focuses on Chinese A-share listed firms, limiting the generalizability of our conclusions to other institutional settings. Future research could extend this framework by incorporating cross-country comparisons or exploring firm-level digital maturity indices that integrate both technological and organizational metrics.

Footnotes

Author Contribution

Funding

The author received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The original contributions presented in the study are included in the article, further inquiries can be directed to the corresponding author/s. The data that support the findings of this study are available from the corresponding author upon reasonable request.