Abstract

This study examines the impact of aggregate and disaggregate environmental, social and corporate governance (ESG) activities on the financial performance of banking firms in the ASEAN-5 countries, a critical market characterized by its bank-based financial system. The analysis draws on data from 32 listed banks in Indonesia, Malaysia, the Philippines, Singapore and Thailand over the period 2015 to 2022 using a two-step Generalized Method of Moments and Least Squares Dummy Variable estimators. By incorporating macroeconomic, bank-specific and financial development indicators, the findings reveal that the aggregate ESG activities positively influence financial performance. Consistently, the disaggregate (individual pillar) ESG activities of social and governance posit positive impacts on FP, whilst the environmental pillar shows no significant influence. These findings underscore the heterogeneous contributions of the individual ESG pillars to bank performance in the ASEAN-5 context. By disaggregating ESG activities into their respective pillars, this study contributes to the literature by offering pillar-specific evidence on the ESG–FP relationship, moving beyond the conventional focus on aggregate ESG. Practically, the findings imply the need for tailored ESG strategies to ensure profitability of banks in ASEAN and other developing markets. Policymakers are encouraged to develop and enforce robust ESG regulations both at country and ASEAN levels to support sustainable banking activities and further promote financial stability in the region.

Plain Language Summary

This study looks at how environmental, social, and corporate governance (ESG) activities affect the financial performance of banks in the ASEAN-5 countries: Indonesia, Malaysia, the Philippines, Singapore, and Thailand. These countries rely heavily on their banking systems, making this an important topic to explore. Researchers analyzed data from 32 publicly listed banks between 2015 and 2022, using an advanced statistical method of dynamic panel data to ensure accurate results. They also considered broader economic factors, bank-specific characteristics, and financial development indicators to get a complete picture. The findings show that ESG activities overall have a positive impact on banks’ financial performance. However, when looking at individual ESG components, the effects are different: Social factors (SOC), such as community engagement and employee well-being, improve financial performance. Corporate governance (GOV), which includes leadership structure and business ethics, has a negative impact. Environmental factors (ENV), such as sustainability efforts and carbon footprint reduction, do not significantly affect financial performance. These findings suggest that while ESG is beneficial overall, its different components affect banks in unique ways. This insight is important for bank managers, investors, and policymakers. Instead of treating ESG as a single oncept, banks should develop targeted strategies to maximize financial performance while ensuring sustainable business practices. For policymakers, the study emphasizes the importance of strong ESG regulations at both national and ASEAN levels. Proper policies can support banks in achieving both profitability and long-term financial stability, benefiting the broader economy. Overall, this research highlights the need for a balanced and well-planned approach to ESG in the banking sector, particularly in developing regions like ASEAN.

Introduction

Environmental, social, and corporate governance (ESG) activities have emerged as critical components of corporate strategy, reflecting the growing importance of sustainability in the global business landscape. The three pillars, that is, environmental, social and corporate governance serve as a framework for evaluating a firm's non-financial performance and its contributions to broader societal goals (Friede et al., 2015). ESG encompasses a wide range of corporate practices, such as reducing environmental footprints, fostering community engagement, and ensuring ethical governance, which collectively aim to enhance long-term value creation. Recent years have witnessed a surge in ESG-focused investments, with global sustainable investments surpassing $35 trillion in 2022 (Global Sustainable Investment Alliance, 2022). This momentum highlights the increasing integration of ESG factors into investment decision-making and underscores the need to understand their impact on financial performance, particularly in the banking sector, which plays a pivotal role in allocating capital toward sustainable development (Chiaramonte et al., 2021).

Despite the growing momentum around ESG integration, the relationship between ESG activities and FP remains theoretically contested and empirically inconclusive. Two dominant theoretical streams underpin this debate. On one hand, Stakeholder Theory (Freeman, 1984) and the Resource-Based View (RBV; Barney, 1991) posit that ESG initiatives enhance firm value by improving stakeholder trust, reducing risks, and creating intangible strategic assets. Recent studies reaffirm that ESG can be a source of competitive advantage, particularly when integrated as a core strategic capability (Pu, 2023; Salem et al., 2024).

On the other hand, Managerial Opportunism Theory (Friedman, 1970) and Trade-Off Theory (Kraus & Litzenberger, 1973) argue that ESG activities may serve managerial self-interest or impose unnecessary financial burdens, diverting resources from profit-maximizing objectives. These perspectives remain influential, especially in studies suggesting that ESG practices often generate weak or negative returns when driven by compliance rather than strategy (Egorova et al., 2022; Follert et al., 2023).

This theoretical divergence is reflected in empirical findings: while some studies find that ESG engagement leads to improved profitability and market performance (Atz et al., 2023; Friede et al., 2015), others report neutral or adverse outcomes, particularly in capital-intensive or highly regulated sectors such as banking (Buallay, 2019; El Khoury et al., 2023). These inconsistencies underscore the importance of contextualizing ESG–FP relationships within firm-specific strategies, industry characteristics, and institutional environments.

The environment pillar deals with environmental challenges, such as deforestation, water scarcity, and urban pollution (Chiaramonte et al., 2022). While environmental activities, such as renewable energy adoption and carbon emission reductions, can yield long-term benefits, they often require substantial upfront investments that may negatively impact short-term profitability (Egorova et al., 2022). This trade-off raises critical questions about the economic feasibility of environmental sustainability initiatives in developing markets like ASEAN.

The social pillar focuses on stakeholder relationships, including employees, customers, and communities. In ASEAN region where financial inclusion and community engagement are key priorities, social activities can enhance banks’ reputations, attract socially conscious investors, and expand customer bases (Giese et al., 2021). However, the benefits of social initiatives may vary across countries with differing levels of socioeconomic development, making it essential to explore their localized impact on FP (Zumente & Bistrova, 2021).

The corporate governance pillar emphasizes transparency, accountability, and ethical leadership, which are critical for risk management and operational efficiency (Kang & Jung, 2020). While strong governance structures are associated with enhanced investor confidence and reduced financial risks, their immediate impact on profitability may be less pronounced, as governance improvements often focus on mitigating losses rather than generating returns (Buallay, 2019). The diversity of governance practices across ASEAN further complicates their evaluation, highlighting the need for region-specific insights.

Adding to this complexity is the role of financial crises, which often undermine banks' FP regardless of their ESG activities. The COVID-19 pandemic, for instance, exposed vulnerabilities in global financial systems, with ESG frameworks being tested for their resilience and adaptability (Agliardi, Arcuri, & Patuelli, 2023). These disruptions raise questions about the true value of ESG activities during economic downturns, particularly whether they can mitigate losses or merely serve as compliance mechanisms. Moreover, understanding which ESG pillars contribute most effectively to FP during such crises remains an underexplored area.

In the context of banking operations, ESG activities and its respective pillars are translated in the uses of funds in the forms of financing and investments that align with sustainability agenda (Shahimi et al., 2023), such as clean energy, human rights, community empowerment, and poverty reduction. By disaggregating ESG into its individual pillars and incorporating macroeconomic, bank-specific, and financial development variables, it is crucial to clarify the nuanced relationships between ESG factors and financial outcomes. Furthermore, sstudying ESG in the banking sector of ASEAN-5 is essential for understanding how financial institutions balance profitability with sustainability objectives in a region characterized by regulatory diversity and bank-based financial systems. This focus offers critical insights for banking executives, policymakers, and investors seeking to align financial outcomes with ESG performance in an emerging market context.

The ASEAN-5 consist of Indonesia, Malaysia, the Philippines, Singapore, and Thailand. These economies are characterized by their advanced economic growth which account for more than 85% of ASEAN’s total GDP. The ASEAN-5 are typically more engaged in regional initiatives such as ASEAN Economic Community (AEC), Regional Comprehensive Economic Partnership (RCEP), and green finance transitions. For instance, financial regulators in Malaysia and Singapore are emphasizing on sustainable finance frameworks. At institutional level, public listed banks in ASEAN-5 are increasingly adopting and integrating ESG as a value-creating strategy. All in all, region-specific regulatory, economic, social and cultural factors, call for localized research (Chang et al., 2023).

This study offers four key contributions. First, it disaggregates ESG into three respective pillars, i.e. environmental (ENV), social (SOC) and governance pillars (GOV), addressing the oversimplification inherent in studies that rely on aggregate ESG indices, which may mask the heterogeneous effects of individual ESG dimensions (Atz et al., 2023; Li et al., 2021). Unlike prior research that often treats ESG as a unified construct, this study isolates each pillar to reveal their distinct financial implications, particularly during crisis periods. Second, it fills a significant gap by examining ASEAN-5 banks a region underrepresented in ESG–finance literature despite increasing regulatory activity, structural variation, and ESG policy uptake (ASEAN Secretariat, 2021; Yusoff et al., 2022). While most existing studies focus on developed markets or listed firms in the West, this study offers insights from a region marked by emerging institutional frameworks and diverse financial development.

Third, it is grounded in the institutional characteristics of bank-based economies, where ESG performance directly influences lending behavior, risk evaluation, and capital flows (Beck et al., 2000; Caporale et al., 2022). Fourth, the study applies a dual estimation approach to the two-step system GMM and Least Squares Dummy Variable Correction (LSDVC) to address endogeneity and dynamic bias, enhancing empirical robustness (Bruno, 2005; Judson & Owen, 1999; Roodman, 2009). To best of our knowledge, this is among few studies applying LSDVC correction for research on ESG in banking firms for Southeast Asian context, providing a methodologically rigorous assessment of the ESG-financial performance (FP) relationship in emerging financial systems.

Literature Review

Despite the growing body of literature examining the relationship between banks’ FP and ESG activities (El Khoury et al., 2021, 2023), there is a significant gap. The results of these studies are often inconsistent, primarily due to the varying methodologies employed, differences in local banking regulations, and diverse economic environments. The ASEAN unique economic growth, legal systems, and cultural perspectives on sustainability introduce additional complexity, which is often inadequately addressed by broader study (El Khoury et al., 2021). Moreover, many previous studies have treated ESG as a single, unified concept, failing to differentiate how the individual ESG pillars impact FP (Deb et al., 2024). This aggregation can obscure the distinct effects of each ESG pillar, leading to a superficial understanding and implementation of ESG activities. Additionally, much of the existing research relies on linear models, which may not fully capture the dynamic relationships and potential endogeneity issues inherent in FP and ESG data (Ali et al., 2022).

The prevailing static analytical methods and the lack of granularity highlight the necessity of more advanced econometric studies, including the GMM, which are better equipped to manage such complexity. By breaking down the individual contributions of ESG activities and utilizing a strong GMM technique, this study seeks to close these gaps and provide a better, more in-depth knowledge of how ESG activities affect financial results in ASEAN institutions. Therefore, this research aims to give banks in the area more specific recommendations, bringing ESG activities closer to FP targets.

ESG Activities and the Financial Performance of the Banks in ASEAN-5

ESG activities have become increasingly central to firm strategy as stakeholders, investors, and regulators emphasize long-term sustainability and ethical corporate behavior. These activities are believed to influence FP by improving efficiency, attracting responsible investment, reducing reputational and regulatory risk, and fostering stakeholder loyalty. Accordingly, firms that actively engage in ESG activities are often assumed to gain competitive advantage through enhanced credibility and operational resilience (Pham et al., 2024).

Despite this theoretical logic, existing empirical evidence on the relationship between ESG activities and FP remains inconclusive. While some studies report positive associations, others find neutral or even negative effects. This inconsistency is often attributed to methodological variation, differing ESG disclosure standards, and sectoral or regional dynamics (Buallay, 2019). Moreover, recent studies highlight the possibility of non-linear relationships, where ESG activities only enhance performance beyond a certain threshold or under specific conditions (Pham et al., 2024). This ambiguity is particularly relevant in ASEAN-5 countries, where ESG integration is still evolving. ESG disclosure practices vary widely across firms and jurisdictions in the region, and institutional pressures to adopt ESG remain fragmented. Scholars have noted that in ASEAN, ESG activities are often motivated by compliance or external signaling rather than embedded strategic alignment (Purnamasari et al., 2022). Therefore, it is essential to investigate whether ESG activities meaningfully influence FP in this emerging regional context.

Recent literature provides mixed support. Studies such as Zhang et al. (2022) and Shaikh (2022) find that ESG activities positively contribute to firm value through enhanced stakeholder relationships and improved risk management. In contrast, Follert et al. (2023) and Auer and Schuhmacher (2016) highlight the potential for ESG activities to raise costs and reduce short-term profitability, particularly when they are not aligned with core business objectives. This study draws on Stakeholder Theory (Freeman, 1984), which emphasizes that firms create value by addressing the interests of all stakeholders, and the Resource-Based View (Barney, 1991), which considers ESG activities as intangible strategic resources that can generate sustained competitive advantage when effectively embedded within firm capabilities. Based on this foundation, the study proposes the following hypothesis:

H1: There is a significant relationship between ESG activities and the financial performance of banks in the ASEAN-5.

Environmental Pillar (ENV) and the Financial Performance (FP) of the Banks in ASEAN-5

The environmental pillar of ESG activities reflects banks’ engagement in practices aimed at reducing their indirect ecological footprint through green financing, paperless operations, and energy-efficient infrastructure. Although banks are not primary industrial polluters, their influence is exerted through the financing of environmentally sensitive sectors and their internal resource usage. In this respect, environmental performance offers not only reputational value but also strategic alignment with sustainability goals, potentially improving long-term financial outcomes in line with stakeholder expectations and regulatory trends (Agliardi, Arcuri, & Patuelli, 2023; Buallay, 2019).

However, the financial outcomes of environmental initiatives in banking remain ambiguous, particularly in emerging ASEAN markets. While developed economies have institutionalized environmental disclosure and integrated it into performance evaluations, ASEAN countries continue to exhibit heterogeneity in ESG enforcement and reporting. Studies highlight that although environmental initiatives such as carbon-neutral policies or digital banking may improve market valuation in the long term, they often impose short-term costs and implementation complexities, especially where regulatory support is weak and stakeholder pressure is limited (Egorova et al., 2022; Huttmanová & Valentiny, 2019).

This study applies Stakeholder Theory and the Resource-Based View to contextualize environmental practices as intangible strategic resources. According to RBV, the competitive benefits of such practices depend on their rarity, inimitability, and embeddedness in the bank’s operational fabric (Barney, 1991). Stakeholder Theory, on the other hand, emphasizes that such environmental efforts generate value only when stakeholders recognize and reward them (Clarkson, 1995; Freeman, 1984). Recent empirical research affirms these theoretical positions. Agliardi, Alexopoulos, and Karvelas (2023) demonstrate that environmental investments can enhance financial resilience when they are integrated into core operational strategies, supporting RBV’s emphasis on internalization and long-term value. Similarly, Atz et al. (2023) highlight that stakeholder recognition of genuine environmental commitment is a key mechanism linking ESG performance to financial outcomes, particularly in sectors where reputational capital is critical. These findings underscore the importance of strategic intent and stakeholder engagement in realizing the financial benefits of environmental initiatives. In ASEAN-5 economies, where institutional pressures vary, it remains uncertain whether environmental engagement yields measurable financial benefits. Therefore, the following hypothesis is proposed:

H1a: There is a significant relationship between Environment Pillar (ENV) and the financial performance of banks in the ASEAN-5.

Social Pillar (SOC) and the Financial Performance (FP) of the Banks in ASEAN-5

The social pillar of ESG activities reflects a bank’s responsibility to its employees, customers, and communities through actions such as fair labor practices, customer protection, and community investment. These initiatives are expected to enhance stakeholder trust, improve customer retention, and strengthen brand loyalty, thereby translating into better financial outcomes. Grounded in stakeholder and legitimacy theories, the premise is that socially responsible behavior reinforces banks’ legitimacy and reputation, which in turn supports long-term profitability (Arayssi et al., 2020; Shaikh, 2022).

However, empirical evidence on the relationship between social activities and FP remains mixed. While some studies confirm that social initiatives positively influence firm value by promoting transparency and meeting stakeholder expectations (Arayssi et al., 2020; Liu et al., 2023), others report nuanced outcomes. For instance, Billio et al. (2021) and Lim et al. (2022) find that while employee engagement yields financial gains, community contributions and product responsibility may not always align with profitability objectives. These conflicting findings suggest that the impact of social efforts may depend on execution quality, stakeholder salience and industry context, all of which vary across regions.

In the ASEAN-5 context, where ESG integration is still evolving and regulatory enforcement is inconsistent, social initiatives may yield delayed or muted financial effects. This study draws upon Stakeholder Theory (Freeman, 1984) and Legitimacy Theory (Suchman, 1995) to assert that the benefits of social activities materialize when stakeholders perceive the firm as committed to social accountability. Recent empirical evidence supports this theoretical foundation, indicating that socially oriented ESG actions such as employee well-being, community development, and inclusive financial services enhance trust, legitimacy, and long-term value creation when they are perceived as authentic and strategically embedded. For instance, Pu (2023) finds that social initiatives in Asian banks significantly improve customer loyalty and reputational capital. Similarly, El Khoury et al. (2023) report that transparent social disclosures in MENA banks contribute to stakeholder alignment and perceived legitimacy. Salem et al. (2024) further demonstrates that firms with proactive social policies experience more resilient performance, especially in volatile environments, by reinforcing their legitimacy and relational capital. Therefore, assessing whether such activities drive financial gains in ASEAN-5 banks is essential. Based on this rationale, the following hypothesis is proposed:

H1b: There is a significant relationship between Social Pillar (SOC) and the financial performance of banks in the ASEAN-5.

Corporate Governance Pillar (GOV) and the Financial Performance (FP) of the Banks in ASEAN-5

Corporate governance is a foundational mechanism through which firms align managerial behavior with shareholder interests. Within the banking sector, governance practices such as board independence, audit quality, and disclosure transparency are assumed to enhance internal controls and reduce agency costs. From this perspective, the agency hypothesis posits that improved governance fosters better financial outcomes by minimizing managerial opportunism and enhancing accountability structures (Jensen & Meckling, 1976). Accordingly, scholars suggest that modern banks must adapt their governance frameworks to cope with increasing ESG scrutiny and stakeholder demands (Gillan et al., 2021; Pu, 2023).

Nonetheless, empirical evidence regarding the financial impact of governance practices remains mixed. While Folger-Laronde et al. (2022) observed a positive linkage between governance indicators and firm performance in ESG-focused investment portfolios, other studies find no significant association in emerging banking systems (DasGupta, 2021; Paltrinieri et al., 2020). These discrepancies have been attributed to contextual differences, varying governance constructs, and the presence of mediating institutional factors. Some scholars argue that interdependencies among ESG components and differing enforcement capacities complicate the financial impact of governance reforms, especially in transitional economies (Sinha et al., 2020).

This study draws on Agency Theory and Institutional Theory to frame governance activities as mechanisms for both enhancing managerial control and responding to regulatory and societal expectations. Agency Theory emphasizes that sound governance structures reduce agency conflicts and align managerial actions with shareholder interests (Jensen & Meckling, 1976). Institutional Theory highlights the role of external pressures in shaping governance practices to gain legitimacy (DiMaggio & Powell, 1983). Recent studies validate these theoretical perspectives in the context of ESG governance. For example, Follert et al. (2023) find that strong governance frameworks in banks significantly reduce risk exposure and enhance investor trust, supporting the agency perspective. El Khoury et al. (2023) provide evidence that banks in emerging markets increasingly adopt governance mechanisms to comply with institutional expectations and build legitimacy among stakeholders. Additionally, Salem et al. (2024) shows that governance quality moderates the ESG–FP relationship, particularly in environments with high regulatory scrutiny, aligning with the propositions of Institutional Theory. In the ASEAN-5 context, where institutional frameworks vary, the financial impact of governance reforms may depend on the maturity of regulatory systems and execution quality.

H1c: There is a significant relationship between Corporate Governance Pillar (GOV) and the financial performance of banks in the ASEAN-5

Research Gap

ESG activities has gained global traction, key research gaps remain, particularly in the ASEAN-5 banking context. First, the impact of disaggregated ESG pillars remains understudied, despite ongoing theoretical tension between stakeholder-driven value creation (Freeman, 1984) and managerial opportunism, which frames ESG as a cost burden (Egorova et al., 2022; Friedman, 1970). This theoretical clash, combined with the inconclusive empirical evidence across developing markets (Buallay, 2019; Khan et al., 2016), raises uncertainty about ESG’s financial implications. Second, the weak nature of ESG reporting across the ASEAN region leads to limited ESG data availability. As a result, existing studies rarely apply a dual-method estimation strategy that combines two-step System Generalized Method of Moments (GMM) and bias-corrected Least Squares Dummy Variable (LSDVC) both of which are well-suited to addressing dynamic endogeneity and small-N panel bias (Bruno, 2005; Judson & Owen, 1999; Roodman, 2009). Third, ESG–finance literature remains heavily concentrated in developed economies, with limited attention to the institutional, regulatory, and financial system diversity of ASEAN markets (Yusoff et al., 2022). This study addresses these gaps by offering a region-specific, methodologically rigorous analysis of the ESG–FP nexus in emerging economies. Additionally, this work complements recent evidence from scoping reviews that call for more nuanced, pillar-level aware analyses of ESG impacts in finance in ASEAN region (Salem et al., 2024).

Methodology

Sample and Data

This study applied purposive sampling, whereby listed banks were selected based on the availability of consistent ESG and financial data over the study period (2015–2022), and the absence of extreme ESG disclosure deficiencies. This study includes 32 banks that satisfied the criteria for data availability and ESG disclosure quality, as determined through a rigorous selection process. The two-step System GMM is employed as the primary estimation technique. The application of GMM in studies with a small cross-sectional dimension (N) is accepted in economic research, particularly when complemented by the bias-corrected LSDVC estimator, as detailed in Section Estimation Methods Selection and Robustness Checks Section. This dual-estimation approach strengthens the robustness of the findings in small-N panel settings. This approach is consistent with prior studies that successfully applied GMM to small samples, including Duong and Nguyen (2021) with 30 banks, Djebali and Zaghoudi (2020) with 10 banks, Maria and Hussain (2023) with 27 banks, and Ali et al. (2022) with 14 banks.

The dataset begins in 2015 to align with the launch of the United Nations Sustainable Development Goals (SDGs), which marked a global turning point for ESG integration. In ASEAN, this period witnessed a rise in ESG disclosures, driven by international frameworks and domestic regulatory encouragement. The 2015–2022 timeframe captures a critical phase of ESG adoption and allows for the assessment of ESG–FP dynamics during both normal periods and the COVID-19 shock, offering insight into ESG resilience under economic stress.

On the other hand; ESG scores and financial indicators for the selected banks were retrieved from the Refinitiv Eikon database (Refinitiv, 2023), which provides firm-level ESG metrics based on standardized reporting frameworks. Macroeconomic variables such as GDP growth, inflation, and private sector credit were obtained from the World Bank’s World Development Indicators (WDI) (World Bank, 2023). A detailed explanation of each variable including its measurement, data source, and relevant references is provided in Tables 1 and 2.

Total Number of Listed Banks in the Sample.

Summary of Variables.

The selection of ASEAN-5 countries, Indonesia, Malaysia, the Philippines, Singapore, and Thailand, is grounded in their shared economic and institutional characteristics that make them suitable for comparative ESG-FP analysis. These countries represent the most developed and systemically important banking sectors within ASEAN, with relatively similar financial structures that are predominantly bank-based markets (Chang et al., 2023; IMF, 2022). Moreover, the ASEAN-5 have adopted regional financial integration goals under the ASEAN Economic Community (AEC) Blueprint 2025, which promotes convergence in regulatory practices, ESG disclosures and banking reforms (ASEAN Secretariat, 2021). Several initiatives, such as the ASEAN Taxonomy for Sustainable Finance and national-level ESG reporting standards, underscore their coordinated push toward sustainable finance. These commonalities enhance the internal validity of analysis by minimizing heterogeneity in legal systems, financial maturity, and ESG reporting mandates (World Bank, 2022), making the ASEAN-5 a robust context for studying the ESG–FP relationship.

The variables

Dependent Variable

The primary dependent variable in this study is banks’ financial performance (FP), which is assessed using three widely accepted indicators in banking and ESG-finance literature. Following prior empirical studies, this research adopts both accounting-based and market-based metrics to provide a comprehensive evaluation (de Franco, 2020). The first measure, Return on Assets (ROA), captures the efficiency with which a bank utilizes its assets to generate net income, and is computed as net income after taxes divided by average total assets (Pasiouras & Kosmidou, 2007). The second measure, Return on Equity (ROE), reflects profitability from shareholders’ perspectives and is calculated as net income divided by average total equity. These indicators remain central to performance modeling in both financial and operational contexts, and are still prominently used in recent applied studies (Belas et al., 2022; Li et al., 2022).

Additionally, Tobin’s Q is used as a market-based indicator, assessing the ratio of a bank's total assets to the sum of its equity market capitalization and total debt book value. This metric provides insights into the market valuation of the bank's assets relative to their replacement cost, offering a comprehensive view of FP that encompasses both market and accounting perspectives (Buallay, 2019; Chung & Pruitt, 1994). Tobin’s Q is particularly relevant in the ESG context because it captures investors’ perceptions of future performance linked to intangible factors such as reputation, social trust, and sustainability alignment. Recent studies suggest that market-based measures like Tobin’s Q are more responsive to ESG signals than traditional accounting metrics, especially in sectors where stakeholder perception is critical (Follert et al., 2023; J. Li et al., 2022). This makes it well-suited to evaluating the market implications of ESG practices in ASEAN-5 banks.

Independent Variables

The ESG pillars and ESG itself are the two primary independent variables investigated in this study. The lagged dependent variable of ESG was used in this study for a period of one year. This decision was due to earlier studies' findings that ESG trends for one era impact subsequent eras (Azmi et al., 2021; Ji et al., 2023). The weighted mean of the ESG scores is calculated by considering ESG differences to determine ESG. The ESG pillars include a variety of topics. ENV of the ESG pillars focuses on resource use, emissions and waste reduction, and innovation. The SOC pillar calculates the sum of the weights assigned to the four dimensions, namely product responsibility, community, human rights, and workforce. The GOV pillar assesses the combined impact of three categories: corporate social responsibility (CSR) strategy, shareholders' rights, and management and oversight (Buallay, 2019).

Control Variables

This study incorporates three control variables: macroeconomic indicators, bank-specific variables, and financial development factors. The bank-specific variables are assessed using three primary indicators: bank size, determined by the natural logarithm of total assets; capital adequacy ratio, calculated by dividing total capital by total assets; and cost-to-income ratio, which is the ratio of operating expenses to operating revenue. These measures are supported by previous research (El Khoury et al., 2023; Platonova et al., 2018; Siueia et al., 2019). This study’s macroeconomic parameters include gross domestic product (GDP) growth, based on the annual percentage increase in GDP per capita, and inflation, measured by the yearly growth rate of the GDP deflator. The reliability of these measures is corroborated by Demirgüç-Kunt and Huizinga (1999).

Additionally, this study employed the DCovid dummy variable, which takes a value of 1 for the year 2020 and 0 for all other years, to account for the significant economic impact of the COVID-19 pandemic on the ASEAN-5 (Yu et al., 2021). The pandemic caused substantial economic downturns due to supply chain disruptions, travel restrictions, and lockdown measures, which severely affected industries dependent on in-person interactions, such as tourism and hospitality (Açikgöz & Günay, 2020). Despite governmental stimulus efforts, the pandemic led to a notable reduction in GDP and economic growth globally and within the ASEAN-5 (Yu et al., 2021). Researchers have suggested managing the variability of banking data during this period to mitigate its potential disruptions (Ali et al., 2022). The study also evaluated financial development factors using three metrics: BC, representing the ratio of domestic credit extended by banks to the private sector relative to GDP; the bank base market, a binary variable indicating whether private credit exceeds market capitalization as a percentage of GDP; and a dummy variable specific to certain national contexts (Demirgüç-Kunt & Huizinga, 1999).

The Model

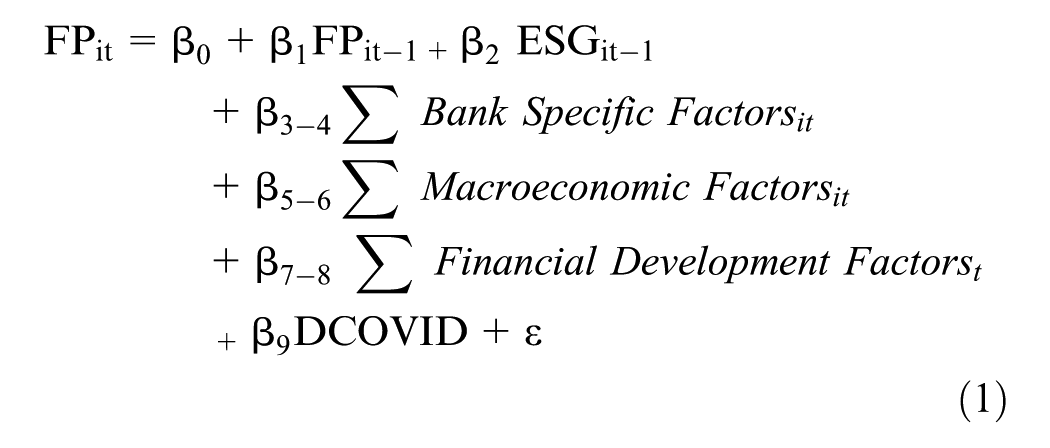

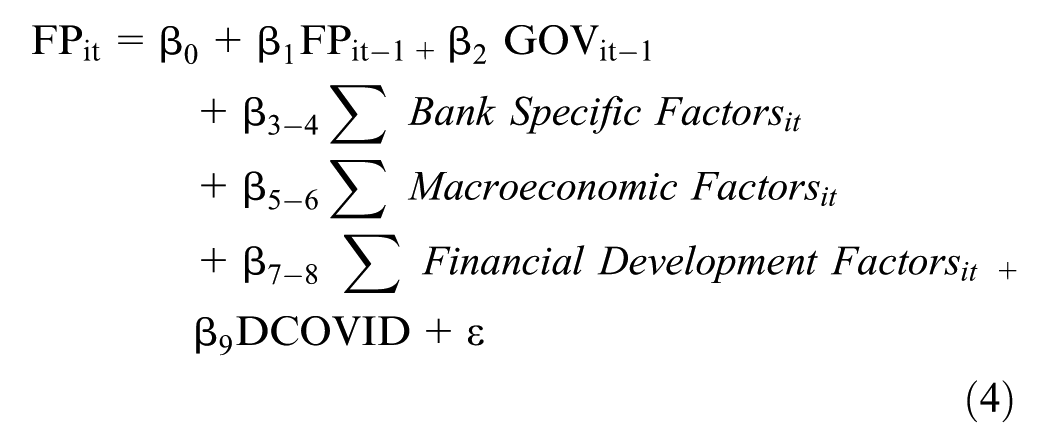

This study follows the model by El Khoury et al. (2021) to test the new sample of banks in the ASEAN-5, as recommended in previous studies. This study addresses the endogeneity concerns by lagging FP to analyze the ESG-FP link (Aybars et al., 2019; Giese et al., 2019). This study utilized the dynamic-linear model with a two-step system GMM technique. This study also introduced the dummy variable of COVID to control for the economic (adverse) effect of COVID-19 on banks' FP. For the aggregate impact of ESG on banks' FP, the following equation (1) is estimated using a two-step system GMM: -

This study also examined the impact of individual ESG pillars, namely ENV, SOC and GOV, on banks' FP based on the following equations respectively: -

Table 2 shows the dependent, independent, and control variables and parameters used to estimate Equations 1, 2, 3, and 4.

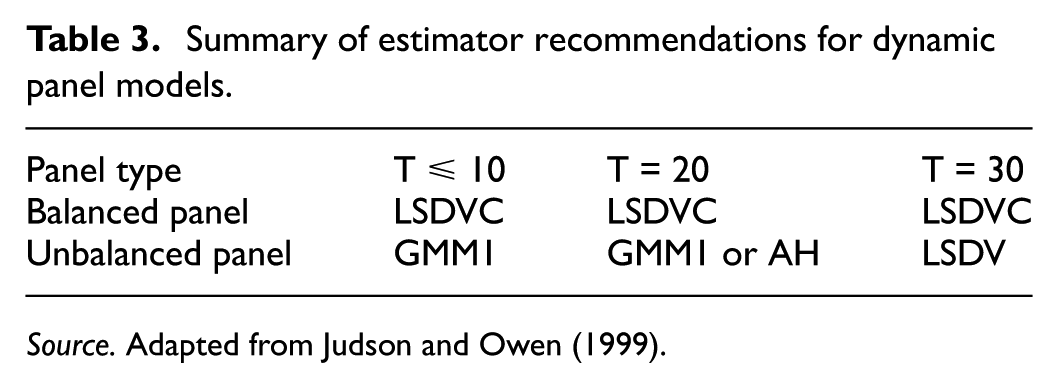

Estimation methods selection and robustness checks

To mitigate potential biases inherent in dynamic panel data models particularly under conditions of a relatively small cross-sectional dimension (N = 32) and moderate time dimension (T = 8) this study adopts a dual-estimation strategy. Traditional fixed-effects estimators are known to produce biased results in such contexts due to the Nickell bias (Nickell, 1981). Therefore, the two-step System Generalized Method of Moments (GMM) estimator is employed as the primary analytical technique. This method is especially effective in addressing endogeneity concerns arising from the inclusion of lagged dependent variables, as it leverages internal instruments constructed from the past values of endogenous regressors (Arellano & Bond, 1991; Blundell & Bond, 1998). System GMM also accounts for autocorrelation and heteroskedasticity, making it well-suited for financial panel datasets characterized by persistence, simultaneity, and omitted variable bias (Roodman, 2009).

However, GMM is not without limitations particularly in small samples, where issues such as instrument proliferation and weak instruments may compromise estimator efficiency and validity. To address these shortcomings and further enhance robustness, this study incorporates the bias-corrected Least Squares Dummy Variable Corrected (LSDVC) estimator as a complementary approach. LSDVC offers analytically adjusted estimates without relying on external instruments, making it especially appropriate for panels with a small N and moderate T (Bruno, 2005; Bun & Kiviet, 2003; Judson & Owen, 1999). Given the structure of the current dataset, which falls within the methodological applicability for LSDVC (Table 3), each model was estimated using four specifications: the two-step System GMM and three LSDVC variants namely, Anderson–Hsiao, Arellano–Bond, and Blundell–Bond corrections. The consistency of results across these estimators affirms the robustness and reliability of the study’s empirical findings.

Summary of estimator recommendations for dynamic panel models.

Results and Discussion

Descriptive statistics

Table 4 presents the descriptive statistics for ESG and FP variables, revealing substantial variability across the dataset. Tobin's Q revealed a relatively low standard deviation, indicating consistent market valuations, while ROA and ROE display more variability, reflecting diverse profitability levels. The ESG scores range widely from 28.44 to 88.11, with the SOC having the highest mean value, suggesting a stronger emphasis on social factors among the banks studied. ENV and GOV pillars also varied significantly. Macroeconomic indicators such as GDP growth and inflation demonstrate moderate variability, reflecting different economic conditions within ASEAN-5. Overall, the data indicates diverse financial and ESG performance among banks, highlighting the need for tailored ESG strategies.

Descriptive Statistics of Variables.

Note. SD = standard deviations; Min = minimum; Max = maximum.

Robustness test

As indicated in Section Estimation Methods Selection and Robustness Checks Section, this study employs the bias-corrected Least Squares Dummy Variable (LSDVC) estimator under three specifications (Anderson–Hsiao, Arellano–Bond, and Blundell–Bond) alongside the two-step System Generalized Method of Moments (GMM) as a robustness strategy to assess the consistency and reliability of the results. Table 5 presents the comparative estimates for the impact of ESG activities and their individual pillars on bank FP across these models. The results indicate strong consistency across all specifications for the key explanatory variables.

Estimation Results for Impact of ESG Activities and Disaggregate Individual Pillars on FP’ of Banks in ASEAN-5: LSDVC-based Models Versus Two Step System Two Step System GMM.

Note. AH refers to Two-Stage Least Squares (2SLS), AB refers to One-Step Efficient Instrumental Variable Estimator, BB refers to Two-Step Estimator Incorporating Additional Moment Conditions. Numbers in parentheses represents the p-values.

, **, and *** indicate significance at the 10%, 5%, and 1% levels, respectively.

The values in bold represent the results of the focal variables that this study specifically investigates. These variables constitute the central constructs of the analysis and are highlighted to distinguish them from the control variables.

In Table 5 The aggregate ESG activities score remains positive and statistically significant at the 10% level or better across all estimators, reinforcing its robustness. The SOC also shows consistent significance across LSDVC and GMM, suggesting a stable positive influence on performance. The ENV remains statistically insignificant throughout, confirming its limited explanatory power in the short term. The GOV is significant in all specifications but positively signed. Given the consistency of these patterns, the study proceeds with the two-step System GMM as the main estimator in the following sections, due to its ability to control for endogeneity, unobserved heterogeneity, and dynamic panel bias. Further diagnostic tests for autocorrelation, heteroskedasticity, and instrument validity are conducted post-GMM analysis to ensure the empirical validity and reliability of the results (as discussed in Sections 4.3 and 4.4).

The Impact of ESG Activities on the FP of the Banks in ASEAN-5

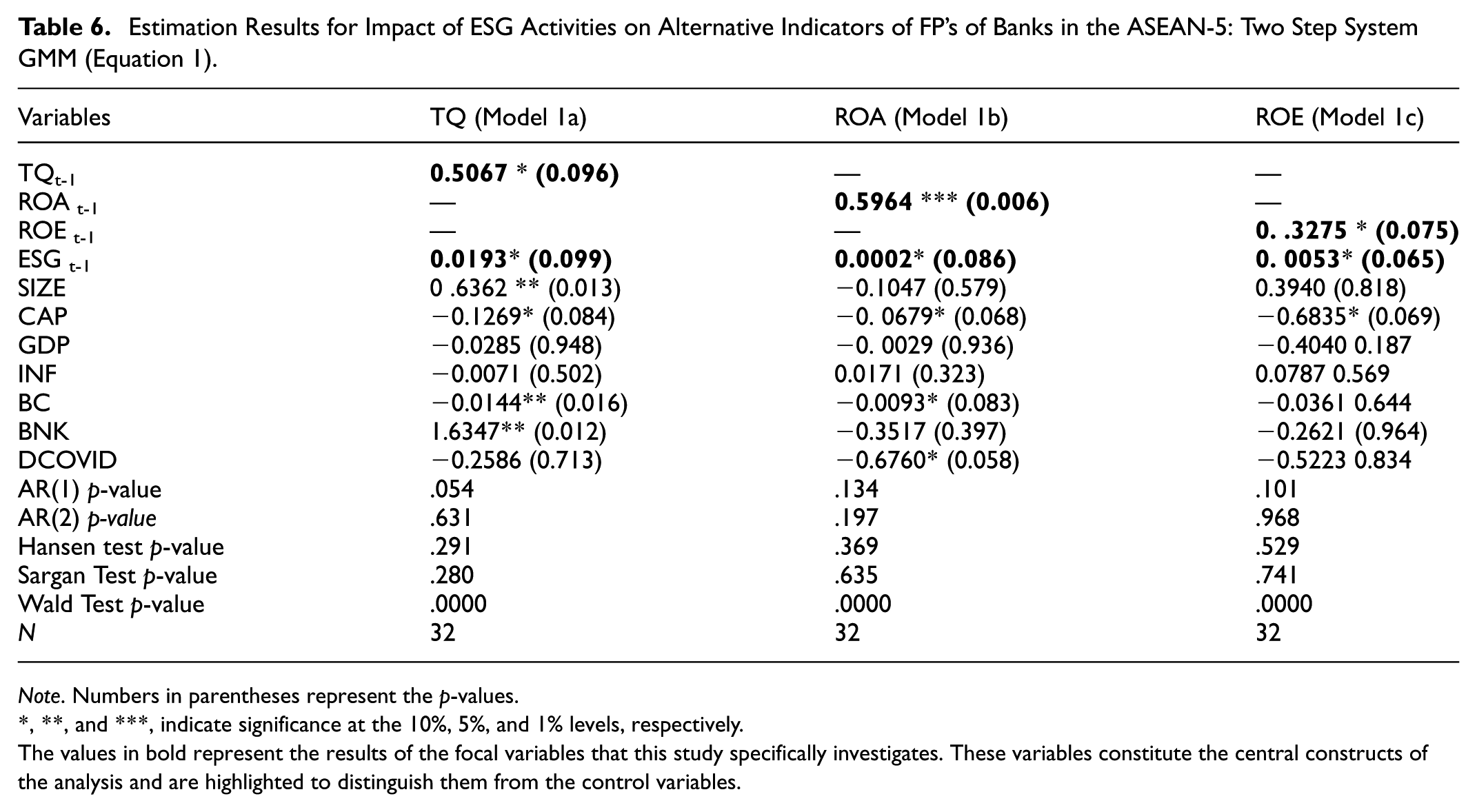

The results presented in Table 6 reveal a consistent and positive impact of ESG activities on FP across the three models, which examine Tobin's Q (TQ), Return on Assets (ROA), and Return on Equity (ROE). In Model 1(a), ESG is found to have a positive and statistically significant relationship with TQ at the 10% level. This indicates that higher levels of ESG activities contribute to improved market valuation, as reflected in Tobin’s Q. In Model 1(b), ESG is positively associated with ROA, and this relationship is statistically significant at the 10% level. This finding suggests that ESG activities play a role in enhancing operational efficiency, thereby improving the FP of banks (Atz et al., 2023; Fernando et al., 2021). Similarly, in Model 1(c), ESG demonstrates a positive and statistically significant relationship with ROE at the 10% level, indicating that ESG activities are linked to better shareholder returns and profitability. The consistent positive and statistically significant results across all three models reinforce the robustness of the findings. These results underline the importance of ESG activities in driving sustainable FP, demonstrating that banks’ commitment to ESG activities can yield substantial benefits across various dimensions of FP.

Estimation Results for Impact of ESG Activities on Alternative Indicators of FP’s of Banks in the ASEAN-5: Two Step System GMM (Equation 1).

Note. Numbers in parentheses represent the p-values.

, **, and ***, indicate significance at the 10%, 5%, and 1% levels, respectively.

The values in bold represent the results of the focal variables that this study specifically investigates. These variables constitute the central constructs of the analysis and are highlighted to distinguish them from the control variables.

For this study, Tobin’s Q is considered the most effective parameter for evaluating FP due to its successful completion of all diagnostic tests. In the field of banking and finance, the preference for Tobin’s Q over traditional metrics such as ROA or ROE for economic analysis is justified by its strong theoretical foundation and practical applicability (Qureshi et al., 2021). Tobin’s Q offers a detailed and subtle evaluation of a bank’s market worth in comparison to the expense of replacing its assets. Tobin’s Q incorporates a future-oriented perspective by considering the complexities of modern financial environments (Buallay, 2019). Furthermore, the relationship between ESG and Tobin’s Q passed AR(1) tests for autocorrelation, indicating that the model is well-specified. Therefore, the subsequent analysis will rely exclusively on Tobin’s Q as the primary measure of FP.

As the results of Model 1(a) indicated that ESG's effect on banks’ FP was significant. This finding suggests that ESG has a positive impact on banks’ FP in the ASEAN-5, consistent with other studies (de Franco, 2020; Sahut & Pasquini-Descomps, 2015). ESG activities positively impact FP by enhancing its reputation, attracting investors, and improving efficiency. Eccles et al. (2014) found that sustainable companies outperform peers in profitability, and Friede et al. (2015) showed a strong positive link between ESG and FP across industries. This relationship is supported by Stakeholder Theory, which posits that proactive engagement with stakeholders including through ESG activities can yield competitive advantages and financial returns by fostering legitimacy, reducing risk, and building long-term value (Freeman, 1984). Accordingly, these findings support Hypothesis H1a, confirming a significant and positive relationship between ESG activities and the FP of banks in ASEAN-5.

For bank-specific variables, the specification includes two main variables: SIZE and CAP. SIZE was positive and statistically significant with FP at the 5% significance level. This finding suggested that FP increased as SIZE increased. CAP was negative and statistically significant, with FP at a 10% significance level. This finding suggested that FP decreased as CAP increased. For macroeconomic variables, specification has two main macroeconomic variables, which are INF and GDP. INF was negative and statistically insignificant with FP, while GDP was not significant. These results indicated that GDP and INF have no impact on banks' FP. The COVID dummy variable is utilized to control the data variance in 2020 during the COVID-19 pandemic. The specification of financial development variables has two main financial development variables: BNK and BC. The latter was negative and statistically significant, with FP at a 5% significance level. This finding suggested that as BC increased, FP decreased. Additionally, BNK is statistically significant with FP at a 5% level of significance. This dummy variable is used to control the model variance as many ASEAN countries are bank-based rather than market-based financial systems.

The Wald test’s findings reject the null hypothesis confirming that the explanatory variables jointly drive bank financial performance with a p-value of less than 0.05 (Wooldridge, 2010). Nevertheless, the Hansen test's findings had a p-value larger than 0.05. Indicate that the null hypothesis of valid overidentifying restrictions cannot be rejected, suggesting that the instruments used in the model are valid and appropriately specified. On the other hand, the AR (2) test confirmed that there was no second-order autocorrelation in the models. Thus, the findings indicated that the dynamic estimators were accurately defined (Arellano & Bond, 1991; Roodman, 2009).

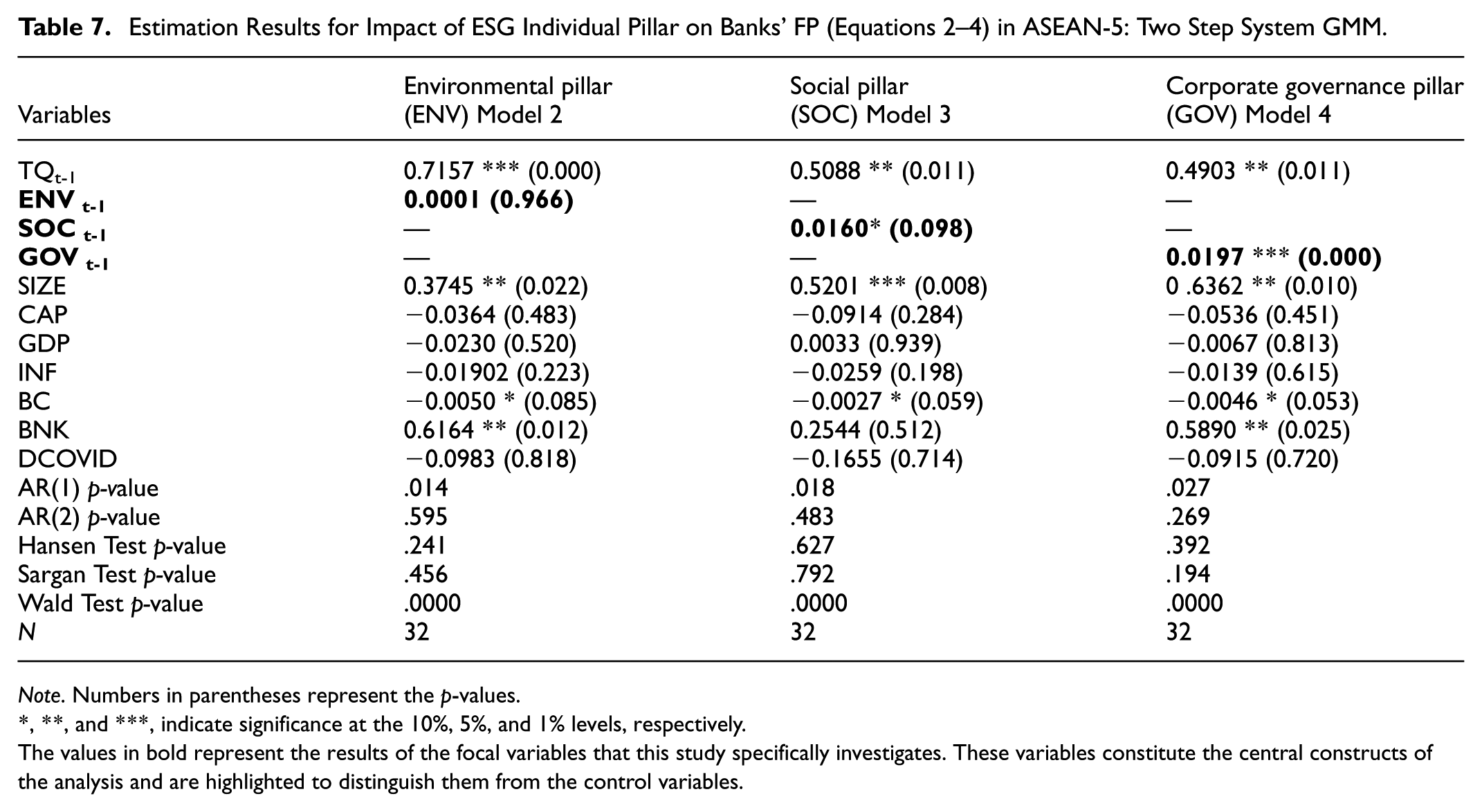

The Impact of ESG Pillars on the Financial Performance of the Banks in ASEAN-5

Table 7 shows the impact of each ESG pillar on the FP. In Equation 2, the results demonstrate that lagged FP remains highly significant, reaffirming the presence of strong path dependence and performance persistence among ASEAN-5 banks. However, the ENV statistical significance, indicating that environmental initiatives do not currently translate into measurable improvements in financial outcomes within the observed period. This result echoes the findings of Agliardi, Arcuri and Patuelli (2023), who noted that firms with higher environmental scores often experience greater long-term stability but do not necessarily achieve superior short-term profitability. Buallay (2019) similarly reported that sustainability disclosures, while enhancing institutional legitimacy and regulatory compliance, are associated with delayed financial returns due to high implementation costs and insufficient market valuation in early stages. Moreover, Huttmanová and Valentiny (2019) observed a weak or insignificant link between environmental performance and short-term financial indicators in emerging European banking sectors, emphasizing contextual limitations in ESG effectiveness.

Estimation Results for Impact of ESG Individual Pillar on Banks’ FP (Equations 2–4) in ASEAN-5: Two Step System GMM.

Note. Numbers in parentheses represent the p-values.

, **, and ***, indicate significance at the 10%, 5%, and 1% levels, respectively.

The values in bold represent the results of the focal variables that this study specifically investigates. These variables constitute the central constructs of the analysis and are highlighted to distinguish them from the control variables.

Theoretically, the Resource-Based View (RBV) argues that while environmental activities may constitute strategic intangible resources, their competitive advantage materializes only when such capabilities are rare, inimitable, and effectively integrated into the firm’s operational fabric (Barney, 1991). This implies a time lag between environmental adoption and financial realization. Additionally, Stakeholder Theory posits that the financial benefits of environmental engagement hinge on stakeholder awareness and institutional pressure (Clarkson, 1995; Freeman, 1984). In emerging ASEAN economies, where environmental consciousness and enforcement mechanisms are still developing, stakeholder recognition may be insufficient to generate financial rewards. These results collectively suggest that while environmental efforts may offer reputational or risk-mitigation advantages in the long run, their short-term impact on FP remains marginal in contexts where ESG integration is nascent and variably reported. These findings do not support Hypothesis H1a, as the ENV does not exhibit a statistically significant relationship with FP.

For the SOC (Equation 3), the analysis indicates that FP exhibits a strong and statistically significant relationship across periods, confirming path dependence in ASEAN-5 banks. The SOC variable is marginally significant, implying that social-related initiatives such as employee welfare, customer service quality, and community development may yield positive financial outcomes, albeit with a time lag. This finding is consistent with prior empirical evidence. For instance, Boussemart et al. (2020) demonstrated that social engagement enhances stakeholder relationships, which gradually translate into FP improvements. Similarly, Jitmaneeroj (2016) found that socially responsible practices are associated with higher long-term firm value in the banking sector, particularly when integrated into core strategic operations. Zhang et al. (2022) also showed that firms with proactive social strategies tend to build trust and customer loyalty, eventually improving their market valuation.

The Stakeholder Theory argues that social activities serve to align firm actions with stakeholder interests, thereby securing sustained access to critical resources and goodwill (Donaldson & Preston, 1995; Freeman, 1984). Legitimacy Theory, on the other hand, posits that social initiatives enhance perceived legitimacy, particularly in highly visible sectors like banking, where public scrutiny is intense (Suchman, 1995). In ASEAN contexts where income inequality, financial exclusion, and community needs are central issues, social responsiveness may therefore offer banks a strategic path to differentiation and reputational advantage, even if the immediate financial returns are limited. These findings support Hypothesis H1b, as the SOC shows a significant relationship with FP

For GOV (Equation 4), the results indicate a statistically significant positive relationship between lagged governance activities and current financial performance (FP), affirming both the dynamic persistence of bank profitability and the enduring benefits of sound governance mechanisms across ASEAN-5 banks. This finding suggests that improvements in corporate governance structures, such as enhanced board oversight, transparent disclosure regimes, and robust internal controls, are not only normatively desirable but also economically efficacious in augmenting bank-level financial outcomes.

The positive coefficient aligns with empirical evidence from Liang et al. (2013), who found that stronger governance frameworks can simultaneously reduce agency-related risks and bolster firm performance by fostering disciplined capital allocation and reducing informational asymmetries. Similarly, Brick et al. (2006) underscored that governance investments, particularly those aimed at aligning managerial incentives and enhancing monitoring efficiency, can yield tangible returns when well-calibrated. In the ASEAN context, where regulatory frameworks are evolving and institutional quality is improving, such gains may be especially pronounced due to the relatively higher marginal benefit of governance upgrades. From a theoretical standpoint, these results are firmly grounded in Agency Theory, which posits that governance mechanisms serve to align managerial behavior with shareholder interests by curbing opportunism and mitigating principal-agent conflicts (Jensen and Meckling, 1976). Enhanced governance structures increase transparency, reduce expropriation risks, and strengthen stakeholder confidence, all of which can contribute to superior financial performance.

Additionally, Institutional Theory offers complementary insights by recognizing that as ASEAN banking systems become more integrated into global financial markets, institutional isomorphism and regulatory convergence drive more substantive, rather than symbolic, adoption of governance reforms (DiMaggio & Powell, 1983). In this transitional setting, governance improvements may signal institutional maturity to external stakeholders, thereby reducing capital costs and improving operational efficiency. This finding support to Hypothesis H1c, confirming a statistically significant and economically meaningful relationship between the Governance Pillar (GOV) and bank financial performance in ASEAN-5.

Policy Implication and Practical Application

To fully leverage the benefits of ESG activities, banks should adopt targeted, evidence-based strategies that align with the distinct performance outcomes of each ESG pillar. For the environmental dimension, the absence of a significant impact on FP indicates the need for more substantial and structured environmental initiatives. Banks should consider expanding green lending portfolios, integrating climate-related risks into credit assessments, and disclosing financed emissions. These measures can enhance environmental accountability and contribute to long-term sustainability alignment.

The social pillar, which demonstrates a positive and significant impact on FP, calls for the strengthening of stakeholder engagement practices. Banks are advised to invest in community-focused programs, improve financial inclusion through the extension of services to underserved regions, and reinforce service transparency. Employee well-being initiatives should also be emphasized to improve customer trust and long-term client relationships, both of which are associated with stable financial returns.

The positive and significant association between the governance pillar and financial performance (FP) highlights the strategic value of strong governance practices for ASEAN-5 banks. This suggests that governance reforms should be seen not as compliance costs but as drivers of long-term value. Policymakers and bank leaders should focus on integrating ESG expertise into board structures, appointing independent directors with sustainability credentials, and establishing ESG oversight committees. Strengthening internal audit and risk functions related to ESG can further enhance transparency and reduce agency risks. To sustain these benefits, regulatory frameworks should promote governance models that are flexible, performance-driven, and tailored to regional contexts.

Bank-specific strategies should also be informed by institutional capacity. Larger banks, with stronger capital bases and more advanced infrastructure, are well-positioned to lead in ESG innovation. They should consider developing sustainability-linked financial products, implementing real-time ESG monitoring systems, and investing in AI-driven ESG analytics. In contrast, smaller banks may benefit from participating in collaborative ESG platforms, forming investment consortia for sustainable projects, or adopting modular ESG toolkits that are scalable to their operational scope.

Policymakers in ASEAN-5 are encouraged to support these bank-level efforts by introducing regionally coordinated ESG benchmarks that reflect the local socioeconomic context while aligning with global standards. Furthermore, stable macroeconomic conditions, including moderate inflation and steady economic growth, are essential to facilitate ESG-related investments. Enhancing financial development indicators, such as access to credit and the quality of regulatory institutions, will further enable effective ESG adoption across diverse banking institutions.

Conclusion

This study rigorously investigates the influence of ESG activities, both in aggregate and by individual pillars, on the financial performance (FP) of banks within the ASEAN-5 region. The findings underscore a differentiated impact of ESG components on FP. Notably, the Social (SOC) pillar exhibits a statistically significant and positive association with FP, affirming that robust social responsibility initiatives, such as stakeholder engagement, community development, and employee welfare, can directly enhance financial outcomes. Conversely, the Environmental (ENV) pillar demonstrates no discernible effect on FP, suggesting that environmental investments may entail longer payback periods or be constrained by limited regulatory or market incentives in emerging economies. The Governance (GOV) pillar, however, shows a strong positive correlation with FP, highlighting that sound governance mechanisms, transparency, accountability, and board oversight, remain fundamental drivers of financial resilience and value creation in the banking sector.

These results provide insights for executives and policymakers. They affirm the necessity of strategic ESG integration, particularly by strengthening governance structures and embedding social initiatives into core business practices. For ASEAN-5 bank management, prioritizing social programs not only fosters stakeholder trust but also catalyzes sustainable financial growth. Simultaneously, governance reforms should be systematically implemented to maximize financial gains and institutional stability. A holistic ESG approach, with targeted emphasis on social and governance dimensions, offers a viable pathway to optimize both performance and sustainability objectives.

Methodologically, this study contributes to ESG–FP literature by disaggregating ESG metrics, offering a more granular and policy-relevant analysis than prior aggregate-based models. By controlling for macroeconomic, institutional, and firm-specific factors, the study ensures robustness in its estimation strategy. The emerging-market focus provides context-specific insights, offering a replicable framework for ESG strategy formulation in other developing regions.

Despite its contributions, this study is not without limitations. The relatively small sample size of 32 banks within the ASEAN-5 restricts the external validity of findings, particularly when extrapolated to broader geographies or sectors. Furthermore, the exclusion of potential moderating and mediating variables may limit the explanatory depth of ESG–FP dynamics. Future research should expand sample diversity, incorporate longitudinal or cross-regional designs, and explore interaction effects to deepen understanding and enhance generalizability.

Footnotes

Acknowledgements

We express our gratitude to the visiting professor and colleagues at the Faculty of Economics and Management, UKM, and the internal & external examiners of PhD thesis for their valuable insights and knowledge, which considerably contributed to the research. It should be noted that they may not fully endorse all the interpretations and results presented in this work.

Author Note

The manuscript has been read and approved by all named authors. All listed authors meet the established criteria for authorship, and the order of authors has been jointly approved. Intellectual property rights associated with this work have been duly considered, and no impediments to publication exist with respect to institutional or legal requirements.

Ethical Considerations

UKM Research Ethics Board Approval Code: JEP-2024-569

Author Contributions

The authors confirm contribution to the paper as follows: study conception and design: Mohammed R. M. Salem & Shahida Shahimi; data collection: Mohammed R. M. Salem; data analysis and interpretation of results: Mohammed R. M. Salem, Abdul Hafizh Mohammad Azam, Mohd Fahmi Ghazali; draft manuscript preparation: Mohammed R. M. Salem, Shahida Shahimi, Suhaili Alma’amun. All authors reviewed the results and approved the final version of the manuscript.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This paper is part of the research funded by the UKM-YTI Endowed Chair Research Grant (YTI-UKM-2022-002) and the Faculty of Economics and Management (FEP), UKM MIICEMA International Grant (MIICEMA-2023-007).

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

No new data were created or analysed in this study. Data sharing is not applicable to this article.