Abstract

This research aims to examine the nexus between the services sector value-added and economic growth using a fractionally integrated heterogeneous panel data analysis for a selected sample of G20 countries from 1999 to 2022. This study considers variables such as service sector value-added, trade in services, foreign direct investment, gross fixed capital formation, and research and development expenditure. The findings reveal a significant positive relationship between service sector value-added and economic performance, underscoring its critical role in driving growth in modern economies. Additionally, the research highlights the negative impacts of external shocks, such as the COVID-19 pandemic and the 2008 financial recession, which stress the need for resilience within the service sector. These results indicate that targeted investments and supportive regulatory frameworks are essential for enhancing competitiveness, fostering innovation, and promoting sustainable practices.

Plain Language Summary

This study looks at how the service sector affects economic growth in some G20 countries between 1999 and 2022. It examines factors like service output, trade in services, foreign investment, capital spending, and research and development. The results show that the service sector plays a strong and positive role in boosting the economy. However, events like the COVID-19 pandemic and the 2008 financial crisis had negative effects, showing the importance of building a more resilient service sector. The study suggests that smart investments and supportive policies are needed to help the sector grow, stay competitive, and become more sustainable.

Introduction

The service sector has emerged as a key engine of economic activity in developed economies, accounting for an increasingly significant share of GDP, employment, trade, and innovation. Its expansion reflects not only structural transformation but also the sector’s role in enhancing productivity and technological diffusion. Beyond its direct contributions, the service sector supports other industries, including agriculture and manufacturing, by providing critical inputs such as finance, logistics, and information technology. These interactions foster economy-wide gains in productive capacity and competitiveness.

In developed economies, the dominance of the service sector is evident in the rapid growth of knowledge-based services and the digitization of traditional business models. Meanwhile, in developing countries, the sector is gaining momentum as a catalyst for economic transformation, with telecommunications and ICT services driving both employment and integration into global value chains. As service activities expand, they enable countries to bypass certain stages of industrial development, offering alternative pathways to structural change and income growth. Several economic theories highlight the evolving role of services in development. The Three-Sector Hypothesis, articulated by Fisher (1939) and Clark (1940), posits a natural transition from agriculture to industry and then to services as economies mature. Services have become dominant in high-income settings due to rising demand for education, healthcare, and professional services. Similarly, Lewis’s Structural Change Theory (Lewis, 1954) identifies the service sector as a destination for surplus labor from low-productivity sectors, boosting efficiency and economic output.

Endogenous Growth Theory, developed by Romer (1990) and Lucas (1988), places services, particularly those related to knowledge and innovation, at the core of long-term growth. Education, R&D, and ICT services generate spillovers that enhance productivity across the economy. In the same vein, the Export-Led Growth Theory recognizes tradable services like tourism and financial intermediation as sources of foreign exchange and competitiveness. Gereffi’s (1999) Global Value Chain Theory further emphasizes the strategic role of services such as logistics, design, and marketing in linking domestic production to global networks. The Knowledge Economy Framework, introduced by the OECD (1996), underscores how finance, ICT, consulting, and health services drive innovation and productivity in advanced economies. Urban-based services also benefit from agglomeration effects, as noted by Krugman (1991), where clustering enhances innovation, labor market pooling, and customer access. These frameworks collectively reinforce the idea that the service sector is a cornerstone of modern economic development.

Recent evidence highlights the growing contribution of the services sector to global output, with services value added accounting for approximately 50–70% of GDP in many G20 countries, reflecting its increasing significance in economic structures (World Bank, 2023). However, the sector has also been highly vulnerable to external shocks. During the 2008 global financial crisis, financial and trade-related services contracted significantly, generating spillovers across broader economies (Ariu, 2016; Borchert et al., 2009). The COVID-19 pandemic exerted an even more severe impact, as restrictions on mobility and face-to-face interactions disproportionately affected services relative to goods. Global services trade fell by more than 20%, compared to a 7% decline in goods trade, while travel and transport services declined by over 60% and 20% respectively (Ando & Hayakawa, 2022). These patterns demonstrate both the critical role of the services sector in driving growth and its structural fragility when confronted with global crises, reinforcing the need for a long-run empirical investigation of how services value added relates to economic performance under conditions of uncertainty and recovery. The present study focuses on the G20 economies, as they encompass both the world’s largest advanced and emerging markets. Collectively, these countries account for the majority of global GDP, trade, and services value-added, making them highly representative of global economic dynamics. By selecting the G20, the analysis captures a balanced mix of developed and emerging economies within a single framework, allowing for meaningful cross-country comparisons and policy-relevant insights.

Henceforth, the service sector has transitioned from a supporting role to a primary driver of sustainable economic growth in developed and emerging economies alike. Its contributions span macroeconomic performance, structural transformation, and innovation diffusion, particularly in the context of globalization and digitalization. The purpose of this study is to investigate how value added by the service sector influences overall economic outcomes in G20 countries. Specifically, the objectives are threefold: first, to assess the long-run relationship between service sector value-added and economic growth; second, to examine the role of complementary factors such as trade in services, foreign direct investment, gross fixed capital formation, and research and development expenditure; and third, to evaluate the resilience of the service sector in the face of major global shocks such as the COVID-19 pandemic and the 2008 financial crisis. Based on existing theory, the study hypothesizes that (H1) service sector value-added exerts a positive and significant effect on GDP growth; (H2) complementary factors such as FDI, trade in services, and R&D reinforce this effect; and (H3) external shocks weaken but do not eliminate the long-run contribution of services to growth.

This study makes a twofold contribution to literature. First, in its thematic scope, it examines the role of the services sector as a driver of economic growth in G20 economies. Despite the G20’s dominance in global output and trade, empirical evidence on services-led growth within this group remains limited, as existing studies have largely emphasized manufacturing as the primary engine of development. By redirecting the focus to services, the study provides new insights into structural transformation and its implications for both advanced and emerging economies. Second, in its empirical approach, the analysis employs a Dynamic Ordinary Least Squares (DOLS) framework, complemented by fractionally integrated heterogeneous panel data techniques, which together address endogeneity, capture persistence, and account for heterogeneity across countries. The inclusion of binary indicators for the 2008 global financial crisis and the COVID-19 pandemic allows for the explicit treatment of systemic shocks, thereby assessing the resilience and vulnerabilities of the services sector under contrasting crisis episodes. Situating the analysis within the G20 context further enhances the study’s relevance by bridging advanced and emerging economies, offering a balanced perspective on the global significance of services-led growth. These contributions strengthen the policy relevance of the findings, offering guidance on strategies to leverage the services sector in enhancing competitiveness, fostering innovation, and promoting inclusive and sustainable development. The remainder of the paper is organized as follows: Section “Literature Review” reviews the relevant literature; Section “Theoretical Framework and Hypotheses” outlines the methodological framework, including data sources, variables, and econometric strategies; Section “Methodology” presents and interprets the empirical findings; and Section “Empirical Results and Discussion” concludes with policy implications and avenues for future research.

Literature Review

Theoretical Evolution of the Role of the Services Sector

The structural transformation of economies typically progresses through two stages: a shift from agriculture to industry, followed by a transition to the service sector. The initial phase, driven by higher productivity in manufacturing, has been extensively analyzed in works by Lewis (1954), Kuznets (1973), and Kaldor (1984), who emphasize industrialization as a catalyst for economic growth. Chenery and Syrquin (1975) further highlight the strong correlation between sectoral shifts and development levels, illustrating how industrial expansion historically spurred broader economic advancement. As economies mature, they enter a second phase characterized by deindustrialization and a growing reliance on services. Scholars such as Kuznets (1973) and Duarte and Restuccia (2010) document this evolution, noting rising service sector shares in GDP and employment. By the 1960s, signs of this shift were already evident (Gemmell, 1982), reflecting changing consumption patterns and the expansion of service-oriented industries. Since the 1990s, the service sector has grown rapidly, particularly in developing countries (Timmer et al., 2015), supported by digitalization and global value chains. These trends underscore the increasing importance of services in shaping economic performance, competitiveness, and employment. Understanding this sector’s evolving role is essential for designing policies that support sustainable and inclusive economic growth.

The expansion of the service sector is shaped by multiple factors, including Baumol’s (1967)“cost disease” hypothesis. This theory posits that stagnant productivity in many service activities, such as education and healthcare, leads to rising costs relative to manufacturing, where productivity growth is faster. As more resources are allocated to these low-productivity services, aggregate economic growth may decelerate, potentially impeding overall performance. Baumol et al. (1985) expanded on this framework by examining sectors that blend progressive and stagnant inputs, finding the adverse effects on growth to be more pronounced than initially assumed. Their findings highlight the challenges posed by unbalanced productivity growth across sectors. However, this pessimistic outlook is not universally accepted. Oulton (2001) offers a contrasting perspective, arguing that Baumol’s model applies primarily to final consumption services. When services function as intermediate inputs, such as business, financial, or IT services, they can enhance productivity in other sectors and support overall economic growth, even if their own productivity gains are limited.

Furthermore, the rise of digital technologies and complex inter-industry linkages has transformed the service sector’s role. Modern services increasingly underpin production processes, innovation, and competitiveness, challenging the traditional narrative of stagnation. As service-oriented economies evolve, particularly through digital transformation and the emergence of new business models, the sector’s contribution to productivity and growth has become more dynamic. This revised understanding suggests that the service sector, far from being a drag on growth, may serve as a central pillar of economic performance in the digital age. Ghavidel and Narenji Sheshkalany (2017) note that service sectors with low total factor productivity (TFP) and limited technological progress are especially prone to cost disease. However, not all services are equally vulnerable; those leveraging innovation and human capital can contribute positively to growth. Pugno (2006), using an endogenous growth model, argues that health and education enhance human capital, driving productivity and long-term economic performance. Yet, as Baumol (2012) cautions, such sectors often suffer from rising costs without commensurate productivity gains, complicating their growth impact.

Business services such as finance, consulting, and information technology play a pivotal role in facilitating economic transformation. As highlighted by Oulton (2001), and Greenhalgh and Gregory (2001), these sectors are instrumental in enabling technological diffusion, enhancing operational efficiency, and supporting innovation across the broader economy. These dynamic segments enhance other industries’ productivity, distinguishing them from stagnant services. Thus, while parts of the service sector face structural constraints, others act as key engines of innovation and economic growth.

Empirical research conducted in developed countries reveals a strong relationship between the share of services, both in terms of Gross Value Added (GVA) and employment—and aggregate productivity growth. While some studies indicate a negative correlation, suggesting that an increasing reliance on services may hinder overall productivity improvements, these findings are often contingent upon the specific definitions and measurements of the service sector used in the analysis (Maroto-Sánchez, 2012, 2013). The complexity of this relationship highlights the importance of a careful and consistent approach to classifying and evaluating service activities, as variations in methodology can significantly influence the observed outcomes. Contrary to the prevailing skepticism surrounding the service sector's impact on productivity, several scholars advocate for a more optimistic perspective. Greenfield (2005) argues for a comprehensive re-evaluation of the service sector, both conceptually and empirically, positing that the notion of cost disease may be a misdiagnosis of the sector's dynamics. This viewpoint challenges traditional narratives that depict services as inherently less productive than manufacturing or agricultural sectors. Moreover, Triplett and Bosworth (2003) contend that the issue of cost disease has been effectively addressed within service industries in the United States, suggesting that advancements in technology and improvements in service delivery have mitigated earlier productivity concerns.

These contrasting viewpoints underscore the need for ongoing research into the role of services in the economy. A deeper understanding of the service sector’s contributions—particularly those services that drive innovation and facilitate technological adoption—can reshape policy discussions and economic strategies aimed at enhancing productivity and growth. By exploring these complexities and recognizing the potential for services to serve as engines of economic performance, researchers can provide valuable insights that inform future economic planning and development initiatives.

Moreover, several key factors contribute to the expansion of the service sector, each interlinked and reflective of broader economic trends. First, income growth plays a crucial role in shaping consumption patterns, as Engel's Law illustrates. This principle suggests that as individuals’ incomes rise, a greater proportion of their expenditures shifts towards services with high income elasticity, such as education, healthcare, and leisure activities. Consequently, higher income levels stimulate demand for these services, promoting their economic expansion and development (Maroto-Sánchez, 2010). Second, the increasing specialization of services necessitates a workforce with higher levels of human capital. As services evolve to meet the demands of a more sophisticated market, the need for skilled labor becomes paramount. This shift highlights the importance of education and training in fostering a capable workforce that can innovate and deliver specialized services (Rubalcaba, 2015). A well-educated labor force enhances productivity and drives the creation of new service offerings that cater to emerging consumer needs.

Third, the advent of Information and Communication Technologies (ICT) significantly influences the service sector by enabling innovation and the emergence of new service categories. ICT facilitates improved service delivery, enhances efficiency, and supports the development of digital services that meet the demands of a tech-savvy consumer base (Falvey & Gemmell, 1996; Howells, 2004). Lastly, the ongoing integration of services with products from other economic sectors underscores the interconnectedness of the modern economy. This synergy enhances product offerings through value-added services, which further supports economic growth and productivity (Messina, 2005; Nordås & Kim, 2013). Collectively, these factors illustrate the multifaceted drivers behind the expansion of the service sector, shaping it into a vital component of contemporary economic structures.

Similarly, In the modern era, the services sector has become deeply intertwined with the manufacturing sector, serving as a critical driver of innovation, efficiency, and competitiveness through advanced technologies and specialized services. Recent studies on the service sector suggest that the rise of advanced manufacturing and Industry 4.0 is closely linked to the integration of new technologies driven by the collaboration between modern services and the industrial sector. This emerging stage of the production system highlights the critical role of a country’s ability to develop advanced service activities, such as those in information technology, research and development, and business services. These modern services act as enablers of innovation, providing the technological foundation and expertise required to transform industrial processes. It is argued that the adoption and dissemination of these technologies, supported by advanced service activities, will significantly influence the industrial sector by enhancing productivity, efficiency, and adaptability in production. This integration is expected to have a profound impact on national productivity levels and economic growth rates. Modern services facilitate the digitalization of manufacturing processes, the implementation of smart factories, and the establishment of interconnected production networks, thereby redefining traditional industrial systems. Schuh et al. (2015), Georgakopoulos et al. (2016), Niggemann and Beyerer (2016), Giovanini and Arend (2017), Giovanini et al. (2020), and Cadestin and Miroudot (2020) emphasize that this convergence of modern services and industry represents a transformative shift. Service-driven technologies are central to creating competitive and sustainable industrial frameworks in the era of Industry 4.0.

Empirical Literature

On a global scale, extensive empirical evidence highlights the relationship between productivity in the service sector and economic growth. For example, Triplett and Bosworth (2000) emphasize the importance of the service sector in comprehending the productivity slowdown experienced in the United States after 1973, arguing that the unique nature of services complicates their measurement compared to manufacturing outputs. Additionally, Li and Prescott (2009) identify several factors contributing to the productivity decline in developed countries between 1973 and 1995, including measurement errors in service productivity, a general slowdown in service sector productivity growth, the oil crisis, demographic shifts, and decreased investments in technology and infrastructure. Their findings indicate that these elements collectively impact productivity assessments. Furthermore, employing a growth accounting framework, Triplett and Bosworth (2003) determine that multifactor productivity is the main contributor to labor productivity growth in U.S. service industries since 1995, with information technology capital and intermediate inputs also significantly influencing this trend.

In several Asian economies, the growth of the service sector has been linked to overall economic balance and development. For instance, Lee and McKibbin (2018) employ an intertemporal general equilibrium model to demonstrate that accelerated service sector growth fosters balanced economic growth in these regions. Specifically in China, Wu (2015) highlights the tertiary sector as a crucial driver of both employment generation and economic expansion, indicating a significant shift in the economic structure towards services. In Pakistan, research by Jalil et al. (2016) employs cointegration and causality approaches to establish a long-term relationship between the service sector and economic growth, concluding that service growth contributes to overall economic growth, while the reverse does not hold true. Similarly, Singh (2010) conducts an econometric analysis of India, confirming a long-term relationship between the service sector and economic growth. His findings suggest that services play a vital role in directly and indirectly enhancing economic growth, particularly through their interconnections with agricultural and industrial sectors. These studies collectively emphasize the pivotal role of the service sector in driving economic growth across various Asian economies.

In addition, Matuka and Asafo (2021) investigate the relationship between the service sector and economic growth in Albania, employing various econometric cointegration and causality models. Their findings indicate that transportation, communication, and financial services positively impact economic growth, while the manufacturing sector negatively correlates with GDP per capita. Notably, they observe bidirectional causal relationships between transportation, communication, financial services, and overall economic development. In the context of Mexico, Castillo et al. (2014) utilize time series analysis to reveal that the tertiary and secondary sectors exhibit common trends with GDP, suggesting a significant interplay between these sectors and economic performance. Expanding the scope, Di Meglio et al. (2018) analyze a diverse range of developing economies through a Kaldorian framework, concluding that business services are vital in enhancing aggregate productivity growth. Meanwhile, Price and Gómez-Lobo (2021) explore the Baumol cost disease hypothesis in urban transport services, providing evidence that supports this theory in several Latin American cities. Collectively, these studies underline the essential role of various service sectors in fostering economic growth across different regions.

Recent studies have increasingly applied advanced econometric approaches, including fractional integration and heterogeneous panel methods, to reassess growth dynamics. Pérez-Rodríguez et al. (2025) revisited the export-led growth hypothesis for OECD economies using a fractionally integrated heterogeneous panel framework, finding robust long-memory dynamics between exports and GDP growth. Their methodological contribution demonstrates the relevance of fractional integration techniques for capturing persistence and heterogeneity across countries. While their analysis centers on exports, the parallels with services trade and value added justify the application of similar methods in examining the services–growth nexus in G20 economies.

Another strand of research has examined the role of external shocks, such as the COVID-19 pandemic, on the services sector. Shingal (2022) highlighted how the pandemic disrupted services trade and greenfield investment in ASEAN+6 economies, revealing that services were hit harder than goods due to their greater reliance on mobility and face-to-face interaction. These findings align with evidence of the disproportionate vulnerability of services to crises, reinforcing the importance of testing resilience mechanisms within the sector, particularly in the context of global shocks like the 2008 financial crisis and COVID-19. Parallel to these contributions, scholars have emphasized the significance of innovation and sustainability as mediating factors in growth trajectories. Pei and Tabish (2025) analyzed G20 economies and demonstrated that technological innovation, higher education, and green finance collectively enhanced sustainable growth outcomes under globalization. Although their emphasis is not exclusively on services, their results provide empirical justification for incorporating R&D expenditure into growth models, as innovation represents a key channel through which modern services contribute to productivity and competitiveness.

Furthermore, research on service sub-sectors further illustrates the sector’s long-run relevance. Azmi et al. (2023), using a panel cointegration framework, investigated the nexus between international trade and tourism in India and SAARC countries, finding persistent long-run linkages between tourism (a major component of services) and growth. This complements broader analyses by demonstrating that service industries such as tourism, transport, and finance possess stable long-run relationships with macroeconomic performance, lending further support to the rationale for focusing on services value added in the G20 context.

This research contributes significantly to the existing literature by providing an empirical approach that integrates fractional integration techniques with heterogeneous panel data analysis. Unlike traditional methodologies that often rely on strict assumptions of stationarity or linearity, the fractionally integrated model allows for a more comprehensive understanding of the relationships between sector value added and economic growth. By accommodating both short- and long-term dynamics, this approach enhances the robustness of the findings and offers deeper insights into the persistent effects of the service sector on economic performance. Moreover, the use of fractional panel cointegration with Whittle estimation provides greater flexibility in capturing long-memory behavior, which is particularly relevant when analyzing macroeconomic data that may display persistence and gradual adjustment processes. Conventional panel cointegration methods, such as fixed or random effects, are often limited in their ability to account for such persistence and may lead to biased or inconsistent estimates when the underlying data exhibit fractional properties. By contrast, the fractional approach allows for heterogeneity across countries, acknowledging that the impact of services on growth is not uniform but shaped by diverse institutional and structural conditions. Applying this methodology to G20 economies, characterized by varying levels of service sector development, openness, and innovation, offers a more accurate and policy-relevant analysis. In this way, the chosen framework not only addresses econometric challenges but also advances the debate on the long-run contribution of the service sector to economic development under heterogeneous global conditions.

Moreover, this study expands the empirical framework by incorporating a wider range of variables that reflect the complexities of modern economies. The inclusion of Trade in Services, Foreign Direct Investment, Gross Fixed Capital Formation, and Research and Development expenditure highlights the multidimensional nature of economic growth, emphasizing that sectoral contributions cannot be viewed in isolation. By adopting this broader perspective, the research not only reinforces the importance of the service sector but also sheds light on how various economic indicators interact to influence overall economic performance. This comprehensive approach adds valuable context to the literature and provides policymakers with a clearer understanding of the factors driving economic growth in G20 countries.

Data and Model Specification

This study aims to analyze the impact of service sector value-added on the economic performance of selected G20 countries, including China, Japan, Saudi Arabia, South Africa, the United States, Australia, Germany, France, Italy, Turkey, and the United Kingdom. Utilizing a panel dataset from 2000 to 2022, the research incorporates a variety of economic and sector-specific indicators. These indicators include GDP growth rate, Trade in Services (TS) as a percentage of GDP, Foreign Direct Investment (FDI) as a percentage of GDP, and Gross Fixed Capital Formation (GCF), also measured as a percentage of GDP. Additional variables include Carbon Dioxide Emissions (CO2) in metric tons per capita, Inflation (INF) as a percentage derived from the consumer price index, and Services Value Added (SERV) expressed as a percentage of GDP (Table 1).

Variables Description.

Model Specification

To analyze the impact of service sector value-added on the economic performance of selected G20 countries, this study employs a panel data regression framework. The dependent variable is GDP growth rate (GDP), representing the economic performance of the countries. The model incorporates several independent variables to capture both sector-specific and macroeconomic dynamics, as detailed below:

where GDP is GDP growth rate, TS is Trade in Services as a percentage of GDP, SERV is Services Value Added, FDI is Foreign Direct Investment as a percentage of GDP, GCFC is Gross Fixed Capital Formation also measured as a percentage of GDP, CO2 is Carbon Dioxide Emissions, INF is Inflation rate and) expressed as a percentage of GDP. The model specification for this study is grounded in theoretical linkages between key macroeconomic variables and economic performance, with a focus on the role of the service sector. The dependent variable, GDP growth rate, serves as a measure of economic performance, reflecting the overall economic expansion influenced by trade, investment, and sectoral contributions. Including explanatory variables captures their theoretical relevance in driving growth dynamics across selected G20 economies. In addition, Trade in Services (TS), expressed as a percentage of GDP, captures the role of cross-border service exchanges, reflecting the globalization of services. Theoretical models suggest that increased service trade enhances efficiency and productivity through specialization, technological diffusion, and resource optimization. Moreover, Services Value Added (SERV), as a percentage of GDP, quantifies the direct contribution of the service sector to economic output. Endogenous growth theories highlight high-value-added activities, such as finance, education, and technology services, as critical drivers of innovation, human capital development, and productivity gains, with positive spillovers to other sectors. Furthermore, Foreign Direct Investment (FDI), expressed as a percentage of GDP, represents capital inflows supporting economic growth through financing, technology transfer, and enhanced managerial practices. FDI integrates domestic economies into global supply chains, amplifying demand for logistics, finance, and professional services. Gross Fixed Capital Formation (GCF), also measured as a percentage of GDP, reflects investment in physical infrastructure such as buildings and machinery, enhancing productive capacity. Classical and neoclassical growth theories emphasize that capital accumulation supports sustainable economic growth and indirectly bolsters the service sector.

Moreover, environmental considerations are addressed through Carbon Dioxide Emissions (CO2), measured in metric tons per capita. The Environmental Kuznets Curve (EKC) hypothesis suggests that economic growth initially increases emissions, but transitions to less resource-intensive service activities can reduce environmental impacts. Inflation (INF), derived from the consumer price index, measures macroeconomic stability. High inflation can hinder growth by eroding purchasing power and discouraging investment, while stable inflation fosters a favourable economic environment. Service-dominated economies face unique inflationary pressures due to their cost structures and wage dynamics. Research and Development Expenditure (R&D), expressed as a percentage of GDP, reflects investment in innovation and technological advancement. Endogenous growth theories emphasize the pivotal role of R&D in driving long-term economic growth through knowledge generation and improved productivity. The service sector, particularly knowledge-intensive industries, disproportionately benefit from R&D investments. Finally, To capture the effects of global disturbances, binary variables are included, coded as 1 during the crisis periods of 2008 to 2009 and 2020 to 2021, and 0 otherwise. These years correspond to the global financial crisis and the COVID-19 pandemic, both of which generated substantial disruptions to services trade, investment flows, and overall economic activity. Incorporating these dummies allows the model to account for structural breaks and temporary shocks that could otherwise bias long-run parameter estimates. By explicitly controlling for such crisis episodes, the analysis is better able to isolate the underlying contribution of the services sector to economic growth while recognizing the sector’s vulnerability to external shocks. he sample consists of G20 economies, selected for their global economic weight and policy relevance, over the period 1999 to 2022, reflecting data availability across key variables. Thus, to examine the long-run relationship between the services sector value added and economic growth, this study applies a fractional panel cointegration framework with Whittle estimation. This approach is particularly suited to macroeconomic data as it accommodates long memory, cross-country heterogeneity, and both short- and long-term dynamics, offering greater reliability than conventional fixed or random effects models. Overall, this framework provides a robust basis for capturing the complex and diverse role of the services sector in economic development.

A Fractionally Integrated Heterogeneous Panel Data Model

This section elaborates on the model proposed by Ergemen (2019), which presents a fractionally integrated heterogeneous panel data framework designed to analyze economic relationships across multiple entities over time. The model incorporates fixed effects and persistent common factors, enabling it to account for cross-sectional dependence and potential correlations among persistent innovations. By treating both regression errors and common factors as fractionally integrated, the model allows for covariates to be endogenous due to influences from unobserved common factors and their innovations.

A key feature of Ergemen’s model is its derivation of persistence from fractional integration, offering an alternative to traditional dynamic autoregressive panel data models. This approach encompasses standard I(0) and I(1) cases, eliminating the need for preliminary unit root or stationarity testing typically required in autoregressive modeling. Additionally, the parameter estimates and corresponding test statistics maintain standard distributions, simplifying the inference process compared to the complexities associated with the I(1) case. Ergemen’s model also builds upon the factor structure established by Pesaran (2006) and the common correlated effects (CCE) estimation, further extending previous work by Ergemen and Velasco (2017). This enhancement allows for contemporaneous correlations among innovations and accommodates factors with varying memory parameters, thus increasing the model’s flexibility and effectiveness in capturing the intricacies of economic relationships in heterogeneous panel data contexts.

The general panel cointegrating regression model proposed by Ergemen (2019) can be expressed as follows:

Where

The key parameters of interest in the model are

Estimating the model (2) involves a two-step process. The first step focuses on eliminating fixed effects by applying first differences to the data. This transformation ensures that any covariate-specific fixed effects, such as

The second step involves using a conditional sum of squares (CSS) criterion to estimate the heterogeneous slope and memory parameters. In this approach, each individual time series is projected onto the (fractionally) differenced cross-sectional averages of the dependent variable and explanatory variables. This method yields generalized least squares (GLS)-type estimates for the slope parameters, improving efficiency in the presence of cross-sectional dependence. Subsequently, the relevant memory parameters are estimated equation-by-equation using the CSS approach, allowing for flexibility in capturing the persistence properties of each series.

From the slope coefficients obtained for each individual series, the common-correlation mean-group estimate for the panel can be computed using the following formula:

All econometric analyses were performed using Stata 17 for panel estimations and R 4.3 (with the fracdiff and related packages) for fractional integration and Whittle cointegration analysis.

Results and Analysis

We start our analysis by evaluating descriptive statistics related to the selected variables. Estimates in Table 2 reveal significant variability in GDP growth and services value-added among the selected G20 countries. The average GDP growth rate is 2.78%, with a standard deviation of 3.5%, reflecting notable fluctuations ranging from −10.36% to 14.23%. Similarly, services value-added, a key indicator of economic performance, averages 61.70% of GDP with a standard deviation of 10.16%, indicating a broad range from 30.51% to 77.18% across the dataset. These figures highlight the diverse economic dynamics within the sample.

Descriptive Statistics.

Similarly, trade-in Services (TS), with a mean of 11.64% of GDP, shows the increasing role of services in global trade. The wide range from 4.15% to 29.29% reflects disparities in service trade dependency among the countries. Research and Development (R&D) expenditure, though relatively low at an average of 1.69% of GDP, reflects varying levels of investment in innovation. Countries with higher R&D expenditures likely exhibit greater innovation-driven growth. Foreign Direct Investment (FDI) shows an average of 2.25%, with some countries experiencing negative inflows (−3.61%), indicating divestments during economic uncertainty(Table 2). In addition to standard descriptive statistics, we report skewness, kurtosis, and the Jarque–Bera (JB) normality test p-values. Skewness indicates the degree of asymmetry in the distribution of each variable, while kurtosis captures the heaviness of the tails relative to a normal distribution. A kurtosis value of three corresponds to the normal benchmark; values above this suggest leptokurtic (fat-tailed) distributions. The JB test formally evaluates whether the joint skewness and kurtosis deviate significantly from normality. As shown in the last column, most variables reject the null hypothesis of normality (p < .05). This is consistent with macroeconomic and financial panel data, which often exhibit non-normal distributions due to structural breaks, shocks, and volatility clustering. To address this issue, all estimations are conducted with heteroskedasticity-robust standard errors, ensuring reliable inference despite deviations from normality (Table 2).

Testing for unit roots is a critical step in time-series and panel data analysis, as it determines the stationarity properties of the variables and informs the appropriate econometric techniques for analysis. Non-stationary variables, characterized by unit roots, exhibit time-dependent statistical properties, which can result in misleading or spurious regression outcomes if not properly addressed. Establishing whether variables are stationary at levels I(0)) or require differencing to achieve stationarity I(1)) is particularly important for identifying meaningful long-run relationships. In this study, the Augmented Dickey-Fuller (ADF) test is employed to assess the stationarity of the variables, ensuring the validity of subsequent cointegration analysis. The Augmented Dickey-Fuller (ADF) test results, as presented in Table 3, indicate that FDI, GDP, TS, and RD are stationary at their levels, suggesting these variables do not exhibit unit roots and are stable over time in their original forms. In contrast, variables such as CO2, GFCF, INFL, and SERVICES are non-stationary at levels but achieve stationarity after first differencing, as demonstrated by statistically significant probabilities (p < .01). This mix of stationarity levels necessitates the use of techniques such as cointegration analysis to ensure valid estimation and inference in models involving long-term relationships.

Unit Root Tests -ADF.

Note. ***p < .01, ** p < .05, *p < .1.

Given that most variables are integrated of order one, I(1), the use of cointegration techniques becomes essential for analyzing their long-run interdependence. Specifically, the Dynamic Ordinary Least Squares (DOLS) method is well-suited for this context as it accounts for endogeneity, serial correlation, and small-sample bias in estimating cointegrating relationships. DOLS augments the cointegrating regression by including leads and lags of first-differenced regressors, ensuring robust estimates even in the presence of integrated variables. The integration of I(1) variables identified through the ADF test justifies DOLS as a reliable technique to explore the long-run dynamics between service sector value-added and economic performance in the context of G20 economies.

Table 4 presents the results from three alternative cointegration tests, revealing substantial evidence of a long-term relationship among the selected variables. The tests conducted include the Phillips–Perron test, the Augmented Dickey-Fuller test, and the Variance Ratio test. The findings from all three tests strongly indicate a stable long-term equilibrium relationship among the variables, thereby supporting the justification for employing dynamic panel estimation techniques, such as Dynamic Ordinary Least Squares (DOLS), for subsequent analysis.

Cointegration Tests.

After identifying evidence of cointegration, we proceed to estimate the panel data Dynamic Ordinary Least Squares (DOLS) model as proposed by Pedroni. Table 5 presents the individual slope coefficients estimated using dynamic OLS, incorporating a linear trend in the cointegration relationship and two leads and lags of the differenced explanatory variables. The estimates reveal that services sector-related factors, including trade in services and value addition, positively and significantly impact economic growth across all selected G20 countries. The value-added component of the services sector drives productivity, innovation, and efficiency across industries. Encompassing diverse activities such as finance, healthcare, education, and IT, it fosters structural transformation by generating high-value jobs, attracting investment, and boosting consumer demand. Additionally, its complementary role to sectors like manufacturing and agriculture further amplifies its contribution to GDP growth and economic resilience. Similarly, trade in services plays a positive and significant role in driving economic growth across G20 countries by expanding market access, fostering specialization, and enabling knowledge and technology transfer. Enhanced service exports in areas such as financial services, tourism, and IT outsourcing contribute to revenue generation and improve the balance of payments. Moreover, the liberalization of trade in services fosters competition and efficiency, prompting domestic firms to adopt global best practices. This has allowed G20 economies to diversify their export portfolios, reduce reliance on traditional sectors, and strengthen their integration into global value chains, amplifying their economic resilience and growth potential.

Individual Dynamic Ordinary Least Squares Estimation.

Note. ***p < .01, **p < .05, *p < .1.

Moreover, the estimates in Table 5 reveal that research and development (R&D) expenditure has a positive and statistically significant impact on economic growth in Canada, Germany, and France. This highlights the critical role of R&D investment in fostering innovation, boosting productivity, and driving technological advancements. In these countries, R&D activities contribute to developing cutting-edge industries, supporting high-value job creation, and enhancing global competitiveness. By prioritizing R&D, these economies have strengthened their ability to address emerging challenges, sustain long-term growth, and maintain leadership in the global knowledge-based economy.

Likewise, foreign direct investment (FDI) plays a vital role in driving economic growth in economies like China and South Africa, highlighting its importance in attracting capital, fostering technology transfer, and enhancing productivity. Similarly, gross fixed capital formation (GFCF) positively impacts economic growth in Italy, Canada, and China, underscoring the significance of investment in physical assets such as infrastructure, machinery, and buildings. These investments contribute to strengthening the productive capacity of these economies, supporting sustainable development, and enhancing their global competitiveness.

Conversely, the analysis reveals negative relationships between economic growth and factors such as inflation, the COVID-19 pandemic, and recession, underscoring their detrimental effects on economic performance. Inflation, for instance, adversely impacts growth in countries like Australia and Germany. High inflation erodes purchasing power, increases uncertainty, and distorts investment decisions, ultimately hampering economic stability and growth. The economic fallout of the COVID-19 pandemic has been profound, with countries like South Africa and Canada experiencing significant disruptions. The pandemic led to sharp declines in economic activity due to lockdowns, reduced consumer demand, and strained healthcare systems, which significantly constrained growth trajectories. Recessionary effects further exacerbate economic challenges, with notable negative impacts observed in Australia and the USA. Recessions typically result in reduced investment, higher unemployment, and weakened consumer confidence, all of which contribute to contractions in economic output. These findings highlight the need for robust policy measures to mitigate the adverse effects of such shocks and promote economic recovery and resilience.

Overall, this analysis highlights the pivotal role of services trade and services value-added in driving economic growth in many countries, alongside the contributions of R&D, FDI, and GFCF. Policymakers aiming to stimulate growth should prioritize enhancing the services sector while addressing the adverse impacts of inflation, pandemics, and recessions. Moreover, we assessed potential multicollinearity among the explanatory variables by calculating Variance Inflation Factors (VIF). For the main regressors of theoretical interest (services value-added, trade in services, FDI, R&D, and gross fixed capital formation), all VIF values were well below the conventional threshold of 10, confirming that multicollinearity is not a concern. Although the inclusion of leads and lags of first-differenced regressors in the DOLS specification may mechanically increase VIF values, these terms serve only as auxiliary controls to correct for endogeneity and serial correlation. Consequently, their collinearity does not affect the consistency of the long-run coefficient estimates, and the robustness of our empirical findings remains intact. Furthermore, the Jarque–Bera test in indicates that the residuals deviate from normality, which is typical in macroeconomic panel data. To address this, all estimations were carried out with heteroskedasticity-robust standard errors, ensuring reliable inference.

Fractional Panel Cointegration

To estimate fractional panel cointegration, we begin by estimating the memory parameters of the selected variable using Robinson's (1995) local Whittle (LW) estimator, employing bandwidths of 0.6 and 0.7. This methodological approach allows for a robust analysis of the long-term dependence structure within the data. Table 6 presents the Local Whittle memory estimates for various economic indicators across selected countries, assessed at two bandwidths. These estimates indicate the degree of long-range dependence in each variable, which is crucial for understanding the persistence of shocks in time series data. Overall, memory estimates are generally higher for GDP and related indicators compared to Foreign Direct Investment (FDI) and other variables, suggesting that GDP growth rates exhibit stronger persistence. For instance, countries like Germany and the USA show significant long-term dependence in their GDP figures, reflecting robust persistence in economic growth trends. In contrast, FDI memory estimates are comparatively lower, indicating less persistence. The slight variations between the two bandwidths suggest that the choice of bandwidth does not significantly impact the overall memory estimates for most variables. These findings underscore the importance of understanding the long-range dependence of economic indicators, particularly GDP, in informing future economic strategies and policies while highlighting the contextual differences across countries.

Local Whittle Memory Estimates.

Subsequently, we estimate the fractionally integrated heterogeneous panel data model. As noted earlier, the memory properties of each individual series are affected by the memory of the underlying factors as well as the memory of the defactored series. A common memory arising from reliance on a persistent common factor can lead to spurious regression results (Ergemen & Velasco, 2017).

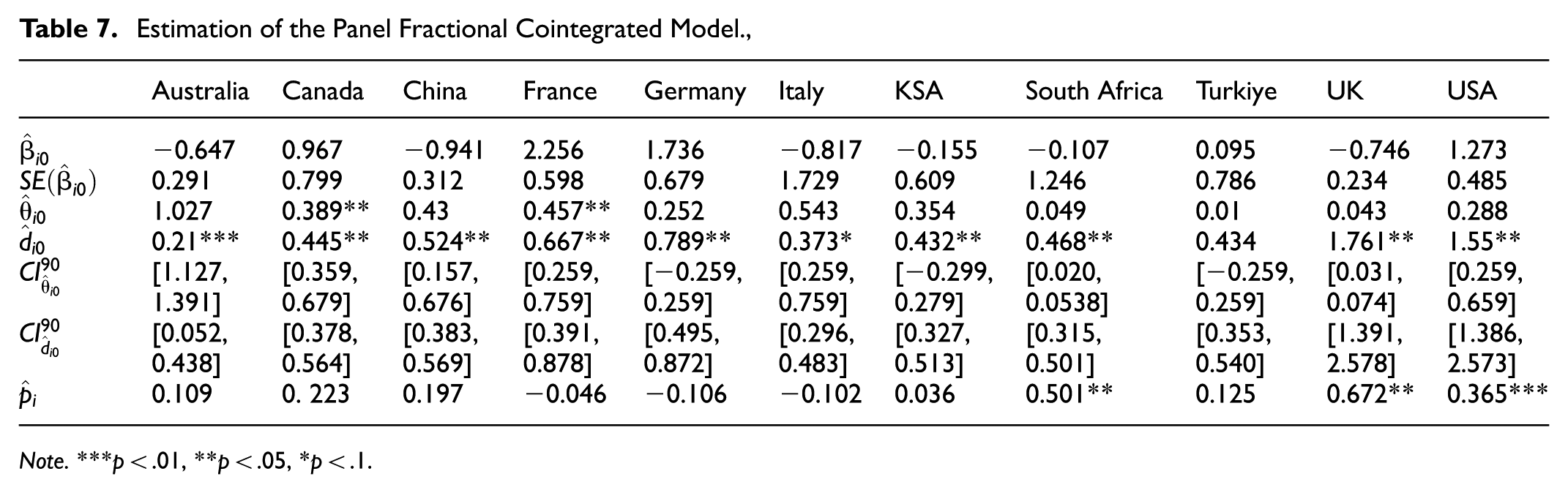

Table 7 presents the findings from the fractionally integrated heterogeneous panel data cointegration model. This table includes the estimated cointegration relationship (

Estimation of the Panel Fractional Cointegrated Model.,

Note. ***p < .01, **p < .05, *p < .1.

These results highlight how fractional cointegration dynamics enhance the insights gained from traditional approaches, such as the Augmented Dickey-Fuller (ADF) test. In particular, significant relationships were identified in countries like France and Germany, where the services sector is pivotal to economic performance. Conversely, countries with weaker correlations in the services sector, like Italy and South Africa, demonstrate a more intricate relationship that may not conform to the patterns typically expected in prominent tourist destinations. These findings emphasize the value of integrating fractional cointegration methods to provide a more comprehensive understanding of economic relationships, especially when accounting for sector-specific factors.

Conclusion

This study examines the relationship between sector value-added and economic growth through a fractionally integrated heterogeneous panel data analysis of selected G20 countries, including China, Japan, Saudi Arabia, South Africa, the United States, Australia, Germany, France, Italy, Turkey, and the United Kingdom. Utilizing a panel dataset from 1999 to 2022, the research highlights the significant positive impact of service sector value-added on economic performance, emphasizing the crucial role of this sector in modern economies. This research employs a fractionally integrated heterogeneous panel data model, which allows for the examination of both short- and long-term relationships among variables. The model accounts for cross-sectional dependence and permits endogenous variables, making it particularly suitable for analyzing complex interactions in economic data.

The findings reveal that increased service sector productivity and efficiency drive substantial economic benefits, reflecting a shift from manufacturing to service-oriented structures. The analysis underscores the importance of various economic indicators, such as Trade in Services (TS), Foreign Direct Investment (FDI), Gross Fixed Capital Formation (GCF), and Research and Development (R&D) expenditure. Investment in these areas is essential for enhancing competitiveness and fostering innovation, ultimately contributing to economic growth.

Moreover, the study examines the negative impacts of external shocks, particularly the COVID-19 pandemic and the 2008 financial recession. These events have significantly disrupted service industries across the G20, highlighting vulnerabilities that necessitate strategies to build resilience within the sector. The pandemic has underscored the need for diversification and adaptability, while the financial crisis emphasizes the importance of robust regulatory frameworks to mitigate future risks. Additionally, environmental considerations are crucial, as the growth of the service sector must align with sustainable practices to address the associated increase in Carbon Dioxide Emissions (CO2) and Inflation (INF).

Drawing on the findings, several policy implications emerge that are directly relevant for G20 economies. First, governments should channel strategic investments toward high-growth service industries, particularly those linked to digitalization and knowledge-intensive activities, supported by targeted incentives for research and development. Second, expanding trade in services through the reduction of regulatory barriers and the negotiation of multilateral agreements can enhance specialization and strengthen global competitiveness. Third, attracting and managing foreign direct investment in a way that promotes technology transfer and managerial expertise is critical for sustaining long-run productivity gains. Fourth, the vulnerabilities revealed by the COVID-19 pandemic and the 2008 financial crisis underscore the importance of regulatory frameworks designed to enhance resilience, including financial safeguards and mechanisms that ensure continuity of critical services during shocks. Finally, integrating sustainability objectives into service sector policies—through the adoption of energy-efficient technologies, green financing instruments, and carbon-reduction measures—will ensure that service-led growth is not only resilient but also aligned with environmental and developmental priorities.

In conclusion, this research highlights the vital link between sector value-added and economic growth in G20 countries, particularly the service sector's contributions. Effective policies that promote service sector efficiency, increase R&D expenditure, and enhance competitiveness while addressing vulnerabilities and environmental impacts will be essential for achieving long-term economic resilience and sustainable growth.

Despite the robustness of the empirical framework and the use of panel data across G20 economies, this study is subject to certain limitations. First, the analysis is confined to the availability and consistency of secondary data, which may not fully capture the informal or rapidly evolving service sub-sectors. Second, while the econometric techniques applied identify long-run relationships, they do not fully address potential endogeneity or structural breaks caused by recent global shocks. Third, heterogeneity among G20 economies in terms of institutional quality and service composition may limit the generalizability of the findings. Future research could extend the analysis by incorporating disaggregated service categories, adopting nonlinear or dynamic panel methods, and exploring the interaction between digital transformation and service-led growth to provide a more detailed understanding of structural change in advanced and emerging economies.

Footnotes

Ethical Considerations

Ethical approval is not applicable because this article does not contain any studies with human or animal subjects.

Consent to Particpate

Informed consent is not applicable because this article does not contain any studies with human or animal subjects.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The data supporting the findings of this study are available upon reasonable request from the corresponding author.