Abstract

This research aims to examine the impact of Corporate Social Responsibility (CSR) on the financial performance of highly polluted national and international companies in Indonesia. Additionally, the study explores the role of industry competitiveness in mediating the relationship between CSR dimensions and financial performance. The research employed a quantitative methodology and collected data from 238 company respondents using primary and secondary sources. Partial least square structural equation modeling (PLS-SEM) was used to analyze the data and establish significant relationships between the variables. The results indicate that both CSR dimensions and industry competitiveness have a substantial impact on financial performance. Specifically, CSR’s economic, environmental, and social dimensions positively and significantly affect financial performance. Furthermore, industry competitiveness significantly mediates between corporate social responsibility (CSR) and financial performance. These findings provide empirical and theoretical insights for improving CSR measures and financial performance in heavily polluted industries. Companies should actively pursue CSR initiatives and increase industry competitiveness to enhance financial performance sustainably.

Keywords

Introduction

Indonesia’s rapid economic growth has brought forth significant environmental, economic, and social challenges, particularly in highly polluting industries. As a result, companies are under pressure to implement Corporate Social Responsibility (CSR) practices to address these challenges (Liu et al., 2023). This study aims to investigate the effect of CSR dimensions on financial performance through the mediation role of industry competitive in highly polluted industries in Indonesia, filling gaps in existing research. It emphasizes the importance of CSR as a strategic element for businesses investing in financial, environmental, and social aspects.

Indonesia’s highly polluted industries face challenges such as poor regulatory enforcement, limited access to technology, and a lack of awareness of environmental issues among stakeholders (Zhao et al., 2020). To address these challenges, environmental regulations and standards have been developed to minimize industrial activities’ ecological impacts (Su & Zhong, 2022). Indonesia’s status as a developing country with significant environmental challenges and a burgeoning corporate sector makes it an ideal research subject (Liu et al., 2023). The insights gained from this study can serve as a valuable reference for other developing economies seeking to balance economic growth with environmental sustainability and social responsibility. Additionally, the study can provide guidance for developing countries grappling with similar challenges.

The study seeks to answer the following research questions:

What is the impact of CSR dimensions on the financial performance of companies operating in highly polluted industries?

Which CSR dimensions have the most significant impact on financial performance in this industry?

What is the role of industry competitiveness in mediating the relationship between CSR dimensions and industry financial performance?

The paper discussed theoretical perspectives on corporate social responsibility (CSR) including ethical, stakeholder, and resource based view (RBV) perspectives. Ethical perspectives focus on moral obligations and promoting the common good (Zakhem & Palmer, 2017). Stakeholder perspectives recognize the influence of companies on various stakeholders and engage in CSR to build trust and reduce reputational risks. While resource based view (RBV) perspectives suggest that CSR practices can enhance a company’s competitive advantage and financial performance (Long et al., 2020).

Industries associated with pollution and social challenges require CSR practices from both ethical and practical perspectives. Adopting socially and environmentally responsible methods can create value for corporations, including those operating in highly polluted industries. While several studies explore the impact of CSR on financial performance, there is a significant gap in research specifically focusing on highly polluted industries in Indonesia. The complex regulatory environment and stakeholder pressure in these industries can significantly influence the relationship between CSR and financial performance. Therefore, more research is needed to understand the effectiveness of CSR in this context.

This study contributes to both academia and practice. Academically, it adds to existing knowledge about the effectiveness of CSR initiatives in highly polluted industries and sheds light on influencing factors. It can inform the development of effective CSR strategies and regulations to promote sustainable financial activities. Practically, it provides insights for companies operating in highly polluted industries, helping them develop effective CSR strategies, improve reputation, brand value, and finances.

The paper is structured as follows: Section “Background of the Study” provides the study’s background, Section “Theoretical Literature Review” presents a theoretical literature review of CSR, industry competitiveness, and financial performance, and Section “Empirical Literature Review and Hypotheses Development” includes an empirical literature review and hypotheses development. Sections “Research Design” and “Empirical Results” describe the research design and present empirical results, respectively. Section “Discussion and Implications for Policy Makers” discusses the implications, and Section “Conclusion and Future Research Direction” concludes with remarks and recommendations for future research.

Background of the Study

Corporate Social Responsibility Practices in Indonesia

Due to current dynamics, rapid economic growth, urbanization, and industrialization, sustainability and environmental issues have become more critical. The difficulties and potential for sustainable development and the approaches that can be used to solve sustainability and environmental issues have all been examined in the empirical and theoretical literature on sustainability and environmental issues. Several significant issues, such as air pollution, water pollution, waste management, deforestation, and climate change, have been cited in Asia as sustainability and environmental difficulties. In Southeast Asia, such as Indonesia, climate change concerning air pollution has been linked to higher mortality rates (Hasnat et al., 2019). Over the past two decades, CSR has become more prevalent across numerous commercial and public organizations. Several distinct sources in Indonesia are moving up the CSR ranking.

In Indonesia, businesses increasingly recognize the significance of Corporate Social Responsibility (CSR), which requires them to positively contribute to society and the environment beyond their economic obligations. CSR has been shown to influence a company’s financial performance positively. Studies suggest that businesses that participate in CSR initiatives exhibit more extraordinary financial performance than those that do not. The reason behind this is that CSR has the potential to bolster a company’s reputation, resulting in amplified customer loyalty and sales. It can also help reduce expenses by improving efficiency and minimizing waste.

The Indonesian government has encouraged businesses to engage in CSR by introducing regulations and guidelines. For instance, the Indonesian Stock Exchange (IDX) mandates that listed companies disclose their CSR activities in annual reports. Furthermore, the government has established the National Action Plan on Business and Human Rights to promote responsible business conduct. Overall, CSR has become a crucial part of doing business in Indonesia, with companies recognizing its advantages to society and their bottom line. Numerous stakeholders in this discussion have stepped up to influence the adoption of CSR in each nation, sometimes singly and sometimes collectively. Regulation and policy guidelines from the governments, industry self-regulation, and pressure from globalization, enlightened self-interest, citizen engagement, and consumer awareness from civil society are all ways the state contributes to society.

Even though CSR participation in various industries benefits society, the critical pillar of the industry continues to be overlooked. From a modern perspective on CSR, the corporate sector has paid more attention to the Asian region (Chapple & Moon, 2005). The world’s most recognized multinational corporations have shown interest in investing in and conducting business in countries in the South East Asian region, such as Indonesia, located in dynamic and economically developing regions. However, CSR issues like economic and environmental conducted little about their contribution. In addition, several multinational corporations have begun operating internationally, particularly in the industry, because of the widespread acceptance of multicultural traditions and increased outside investments from Indonesia. As a result, the researchers in this study combined the financial performance of Indonesia industries with CSR’s environmental, economic, and social components.

Theoretical Literature Review

Corporate Social Responsibility

Various understandings of CSR have been discussed since the 1950s (Low, 2016). CSR enhances social activities beyond the firm’s interests and focuses on the interaction between businesses and stakeholders. Moreover, CSR provides corporations with interaction with society, and organizations need to harmonize their beliefs with accepted norms (Glonti et al., 2020). Businesses should consider more than just their fundamental legal and economic obligations. Social and environmental concerns are incorporated into business operations and stakeholders through CSR, which has been thoroughly defined (Marco-Lajara et al., 2022). CSR has recently been redefined as an organization’s responsibility for its social repercussions (Úbeda-garcía & Claver-cort, 2021). Corporate social responsibility (CSR) involves incorporating social, environmental, ethical, human rights, and consumer issues into business operations (Fortunati et al., 2020). CSR forces businesses to balance minimizing their negative societal impact while maximizing their positive influence on stakeholders (Carroll & Buchholtz, 2008). Companies should conduct their economic operations concurrently with social obligations and not limit their social investments to philanthropic costs converted into sustainable societal contributions (Bosch-Badia et al., 2013).

According to stakeholder theories, CSR was developed to reorient business priorities to minimize adverse operational effects and enhance social well-being (Wang et al., 2015). Businesses might overstate the positive social impact of their CSR programs to mislead consumers, build credibility, and inspire trust, all while boosting their bottom line. Corporate social responsibility (CSR) benefits performance, whereas social irresponsibility actions have a negative impact (Wei et al., 2020). Additionally, every CSR economic, social, and environmental dimension has a favorable relationship with business performance. Reduced operational expenses and a rise in revenue through grants and incentives are possible outcomes of CSR from resource-based views and CSR program implementation (Jhawar & Gupta, 2017). Generally, a company that practices social responsibility meets these societal demands, builds its reputation, and ensures a steady market (Cho et al., 2019). Hence, CSR has incorporated the impact on socioeconomic and stakeholders into business operations.

Corporate Social Responsibility, Industry Competitiveness, and Financial Performance Relationship

The theoretical literature on the relationships between Corporate Social Responsibility (CSR), industry competitiveness, and financial performance in Indonesian highly polluted industries suggests complex and interrelated dynamics. CSR can impact financial performance by improving a firm’s reputation, leading to increased customer loyalty and sales (Saeidi et al., 2015). Additionally, CSR can lead to cost savings and improved efficiency by reducing waste and enhancing productivity. The resource-based view (RBV) theory also suggests that CSR can create a competitive advantage by providing access to unique resources and capabilities that are valuable, rare, and difficult to imitate (Barney et al., 2001). Industry competitiveness is another crucial factor mediating CSR and financial performance (Devie et al., 2018). Highly polluted industries often face significant regulatory and reputational challenges, and CSR can enhance their competitiveness by improving their reputation and reducing regulatory risks. This can lead to increased market share, higher profits, and improved financial performance (Suteja et al., 2023). However, there are also potential trade-offs between CSR and financial performance in highly polluted industries. For example, implementing pollution reduction measures can be costly and negatively impact short-term profitability (Margaretha & Rachmawati, 2016). Additionally, firms that invest heavily in CSR may face higher costs and reduced profits, which could negatively impact their competitiveness.

They are achieving stability between a company’s financial interests, public needs, and environmental preservation in light of rapid development and severe worldwide threats (Barauskaite & Streimikiene, 2021). Businesses must necessarily adjust to succeed in the age of globalization and altering social norms. For example, they must transition from working relationships to partnerships, from quick and easy profits to long-term sustainable business development, and from self-interest to addressing societal and environmental concerns (Matten & Moon, 2020). Since sustainable, moral, and ethical activities can provide the most value to any organization, businesses must engage in socially responsible activities (Boccia & Sarnacchiaro, 2018).

CSR initiatives can boost reputation, boost customer loyalty, and reduce risk (Bhattacharya et al., 2009). The relationship between CSR and financial performance is examined using a variety of academic frameworks, including stakeholder, agency, and legitimacy theories. In contrast, the stakeholder theory argues that companies must balance the interests of their various stakeholders, including the environment, shareholders, and customers (Harjoto & Laksmana, 2018). These theories suggest that firms are responsible for maximizing shareholder value and maintaining a positive societal reputation, respectively. While others criticize, CSR initiatives can be costly and diminish the firm’s primary responsibility to maximize shareholder value (Hou, 2019). Many studies also found no association or a neutral relationship. Because of the intricate connections between financial institutions and society, there is no clear correlation between CSR and financial performance (Soana, 2011). The study by Carnahan et al. (2010) revealed more nonlinear correlations between CSR and financial performance than previously mentioned. Up to a certain point, when the effect of CSR shifts to a negative (−1), CSR has a positive impact on financial outcomes and boosts income. Contrary to the previous model, the second one is different. It indicates that when a company’s revenue starts to increase favorably and CSR starts to have a beneficial impact on financial performance, the result of CSR is negative. A company’s revenue income drops to a certain degree. Therefore, according to the above different arguments of CSR and financial performance relationships, the current study examines the effect of CSR dimensions (environmental, social and economic) on the financial performance of the selected industrial companies in Indonesia.

Empirical Literature Review and Hypotheses Development

Environment Dimension and Financial Performance

CSR comprises various activities carried out by companies to contribute to social and environmental sustainability (Sudirman et al., 2021). These initiatives might focus on lowering greenhouse gas emissions, enhancing working conditions, and assisting regional communities. Empirically, a body of studies has examined CSR factors, particularly the environmental factor, by considering their impact on the financial performance of severely polluted enterprises. As a result, some have found positive, while others have found no correlation or a negative one (Boakye et al., 2021). Instead, the study demonstrates that environmental activities can result in a better reputation, greater consumer loyalty, and lower expenses (Tsoutsoura, 2004).

Furthermore, a study by Hu et al. (2021) found that environmental corporate social responsibility (CSR) policies positively impact severely polluted enterprises’ financial performance. The study discovered that by lowering expenses and boosting a company’s reputation, environmental CSR activities, including waste management, energy saving, and pollution reduction, could boost a company’s financial performance. The study also discovered that highly polluted companies see a more significant financial performance benefit from environmental CSR efforts than less contaminated companies. Similarly, a study by Kao et al. (2018) revealed that environmentally conscious CSR practices favorably impact the financial performance of China’s most polluting businesses. According to the study, companies that adopted environmental CSR policies outperformed those that did not in profitability, return on assets, and return on equity. Another study by Testa and D’Amato (2017) discovered a connection between environmental CSR practices and financial performance in businesses with high pollution levels. Comparing companies that adopted environmental CSR practices to those that did not, the study concluded that the former had greater stock returns and decreased stock volatility.

On the one hand, research revealed by Kao et al. (2018) and Hu et al. (2021) has discovered a clear correlation between financial success and environmental CSR activities in businesses with high pollution levels. According to this research, environmental CSR activities can improve a company’s reputation, lower costs due to better compliance and efficiency, and increase profitability. On the other hand, other studies have discovered conflicting or unfavorable outcomes in the association between financial success and environmental CSR activities in heavily polluted enterprises. For instance, research by Sial et al. (2018) indicated that environmental CSR policies did not significantly impact heavily polluting Chinese enterprises’ financial performance. The study suggests that the mixed results may be due to differences in the effectiveness of environmental CSR practices, the nature of pollution, and the regulatory environment.

Furthermore, some research indicates that in highly polluted industries, the beneficial impact of environmental CSR activities on financial performance may be curtailed or even reversed. For instance, a study by X. Li et al. (2023) discovered that highly polluting companies in the Chinese chemical industry suffered financially because of their environmental CSR policies. According to the study, this might be because environmental CSR initiatives in this sector come with substantial regulatory and compliance expenses. The effectiveness of the practices, the type of pollution, and the regulatory environment may all play a role in the results, which are mixed and may depend on several variables.

Hypothesis 1: CSR’s Environment has a positive effect on the Financial Performance of the companies.

CSR’s Economic Dimension and Financial Performance

The review will delve into both empirical and theoretical evidence concerning the relationship between CSR, economic activity, and financial performance (Barauskaite & Streimikiene, 2021). Research has explored the correlation between CSR economic activities and financial performance by analyzing the financial statements of companies involved in CSR initiatives in Indonesia. The findings of these studies are conflicting, as some have identified a connection between CSR economic activity and financial performance (Han & Kim, 2016). In contrast, others discover no meaningful connection (Cherian et al., 2019).

Companies can utilize CSR initiatives to cultivate and sustain closer relationships with stakeholders, addressing their legitimate concerns and enabling the identification of new opportunities (Tuyen et al., 2023). The relationship between CSR economic activity and financial performance is a topic of discussion that encompasses stakeholder, agency, and resource-based theories. Consequently, within the stakeholder framework, corporate social responsibility encompasses the interests of various parties such as the environment, suppliers, customers, and employees. Apart from this perspective, companies involved in CSR activities can enhance stakeholder relations, resulting in increased customer loyalty, decreased employee turnover, and improved reputation and financial performance. In contrast, the connection between CSR and financial performance is influenced by aligning the motivations of managers and shareholders, as opposed to the agency theory. Managers can engage in CSR activities to signify their commitment to social responsibility, which can enhance their reputation and job security. This alignment of incentives can improve financial performance (Kumala & Siregar, 2021). Likewise, Resource-based theory shows that company resources, including economic CSR activities, can be a source of competitive advantage. Companies that engage in CSR economic activities may have a better reputation, better relationships with stakeholders, and access to resources, which can lead to improved financial performance (Wang et al., 2015).

On the one hand, numerous empirical literature stated and investigated CSR’s economic dimension and financial performance relationships. The studies like López et al. (2007) and Hu et al. (2021) have discovered a clear correlation between the financial performance of highly contaminated enterprises and the economic component of CSR. Based on this research, economic CSR activities like waste reduction and investment in clean technology can result in cost savings, enhanced productivity, and better financial results. On the other hand, the relationship between the economic aspect of CSR and financial success in heavily contaminated enterprises has been the subject of research that has produced conflicting or unfavorable findings. For instance, Wu et al. (2020) revealed that the economic aspect of CSR did not significantly influence the financial performance of China’s most polluting enterprises. The study suggests that the mixed results may be due to differences in the effectiveness of economic CSR practices, the nature of pollution, and the regulatory environment.

Additionally, some research opine that in severely contaminated businesses, the beneficial benefits of CSR’s economic component on financial performance may be curtailed or even reversed. The economic dimension of CSR negatively impacted the financial performance of highly polluting companies in the Chinese chemical industry (Svermova & Cernik, 2020). According to the study, this might be because investing in clean technology and cutting waste in this sector comes with actual prices and risks. While some studies point to a positive relationship between CSR’s economic dimension and financial performance in heavily polluted companies, the results are conflicting. They may depend on several variables, including the efficacy of the practices, the type of pollution, and the regulatory environment. Moreover, due to the significant costs and risks involved with investing in clean technology and decreasing waste, the beneficial impacts of CSR’s economic dimension may be restricted or even reversed in severely polluted industries. Therefore, delving into CSR remains a persistent concern pertinent to economic and finance research due to its significance to investors, stakeholders, and policymakers (Saeed et al., 2023).

Hypothesis 2: CSR Economic dimension has a positive effect on Financial Performance.

CSR’s Social Dimension and Financial Performance

There has been much discussion in recent literature reviews on the impact of CSR’s social component on financial performance in severely polluted enterprises. On the one hand, research by Barauskaite and Streimikiene (2021) and Joo et al. (2017) has discovered a good correlation between the social component of CSR and financial success in businesses with high pollution levels. According to this research, social CSR activities, such as improving working conditions and contributing to the community, have the potential to enhance a company’s reputation, foster client loyalty, and improve financial performance. Conversely, other studies examining the correlation between the social component of CSR and financial success in heavily polluting corporations yielded contradictory or unfavorable results. Research by Barnett (2018) revealed that the social component of CSR had no appreciable impact on the financial performance of Malaysia’s most polluting businesses.

The company’s attempts to address social issues, including poverty reduction, education, and health, are examples of social activity (Nave & Ferreira, 2019). This literature review uses empirical and theoretical to examine the CSR social activities, industry competitiveness, and financial performance relationships. These studies’ findings are conflicting; some indicate a strong correlation between CSR social activities and financial performance, while others find no discernible link. According to a study by McWilliams et al. (2006), businesses that engage in CSR initiatives increase their shareholder value. CSR’s social aspects strive stakeholder theory suggests that CSR not only maximizes shareholder wealth but also considers the interests of all stakeholders, including customers, employees, suppliers, and society (Jamali, 2008). According to this theory, companies that engage in social activities can improve relations with stakeholders, leading to increased customer loyalty, reduced employee turnover, and improved reputation, prominent to improved financial performance (Lee et al., 2009). It illustrates how socially responsible companies grow their brand recognition, increase client loyalty, and attract top talent. Including these elements is one of the keys to raising profitability and sustaining financial performance. Socially active companies may gain a better reputation, stronger stakeholder relationships, and easier access to resources, all of which can improve their financial success and are supported by legitimacy theory. In theory, corporations participating in social activities are seen as more trustworthy and legitimate, enhancing their financial-economic performance (Saeidi et al., 2015).

Empirical findings emphasize that companies are less inclined to engage in socially responsible behaviors in relatively unhealthy economic environments with limited short-term profitability (Gavana et al., 2023). It indicated the beneficial impacts of CSR’s social component on financial success may be curtailed or even reversed in severely polluted businesses. For instance, a study by Kim and Kim (2021) discovered that the social aspect of CSR had a detrimental impact on the financial performance of businesses in the South Korean petrochemical industry polluted heavily. The study hypothesizes that this might result from the significant expenses and risks of sustaining local communities and preserving social permission to operate in this sector. Even though some studies have found a link between CSR’s social component and financial success in heavily polluted businesses, the results are conflicting. They may depend on some variables, including the efficiency of the practices, the type of pollution, and the regulatory environment. Furthermore, the substantial costs and dangers associated with upholding social license to operate may limit or even negate the beneficial effects of CSR’s social dimension in highly polluting industries.

Hypothesis 3: CSR’s Social aspects have a positive relationship with Financial Performance.

The Mediating Effect of Industrial Competitiveness

Industrial competitiveness is the capacity of a business to compete on the international stage. Contrarily, financial performance relates to a company’s long-term profitability and viability. This literature review will scrutinize both theoretical and empirical research on the relationship between financial performance and industrial competitiveness (Mugo, 2020). Many theoretical frameworks have been proposed to describe the relationship between industrial competitiveness and financial success. As per the resource-based view (RBV), a firm can attain a competitive advantage through its diverse array of resources and capabilities. The theory of long-term financial performance is one of the most well-known. Porter’s Diamond Model is another theoretical framework that holds that a firm’s competitiveness is determined through conditions, demand circumstances, supporting industries, corporate strategy, structure, and competition.

A company’s ability to sustain competitiveness can be influenced by various factors, typically categorized into business development advantage, resource advantage, market advantage, product/service advantage, technological advantage, and human capital (Jones & Lee, 2018). Because different tactics and performances may be affected by a company’s competitive edge, a thorough competitiveness analysis is required. Unfortunately, there is little research on companies’ performance and competitiveness, and the study gave proof of the opportunity, relational, innovative, human, and strategic competencies of the entrepreneur’s direct and indirect impact on the long-term performance of the businesses.

The market economy, especially the effective distribution of resources, depends on competition. In this context, national competitiveness is a hotly contested topic among academics and organizations because of the close connections between industrial, national, and corporate competitiveness (Stavropoulos et al., 2017). By adopting a competitive-action approach, the study offers a more comprehensive understanding of CSR and financial performance relationships. According to the current study, competitive action should be considered a significant contingency when assessing how CSR initiatives affect a company’s financial performance. Like increasing firm competitiveness within an industry increases national competitiveness, increasing industrial competitiveness is predicated on increasing enterprise competitiveness (G. Li et al., 2019). Therefore, in this study, industrial competitiveness has been taken as the mediating effect of CSR and financial performance relationships (Hasan et al., 2018).

Numerous scholars argue that CSR can increase industrial competitiveness by enhancing corporate reputation, attracting and retaining customers, and reducing costs (Padilla-lozano et al., 2021). Businesses that use a strategic CSR approach can benefit themselves and Society, eventually boosting financial performance. Industry competitiveness mediates the relationship between CSR and financial performance, indicating that companies that engage in CSR activities tend to become more competitive, resulting in better financial performance (Rinawiyanti et al., 2022)[2]. The study by Saeidi et al. (2015) found that industry competitiveness partially mediates the relationship between CSR and financial performance, suggesting that industry competitiveness plays a role in explaining the relationship between CSR and financial performance, but other factors may also be involved. In contrast, some scholars argue that environmental competitiveness may be a more specific mediator of the relationship between CSR and financial performance Saeidi et al. (2015) and Anwar and Li (2021) found that environmental competitiveness fully mediates the relationship between environmental CSR activities and financial performance.

Hypothesis 4: Industrial Competitiveness has a positive impact on the financial performance.

Environment Dimension, Industrial Competitiveness, and Financial Performance

Currently, the nation’s economic activity and environmental issues are closely related. The relationship between environmental regulations and industrial competitiveness is receiving more attention as a result of limits on both economic development and environmental protection. Numerous theoretical frameworks have been developed to explain how CSR environmental actions and industrial competitiveness are related. The RBV asserts that businesses engaged in CSR environmental activities can create assets and skills that enhance their competitiveness (Marin et al., 2017). Environmental activities can help a business improve its reputation, boost the value of its brand, and draw in customers’ initiates about the environment. Stakeholder theory is another theoretical framework emphasizing the value of involving stakeholders in CSR initiatives. Theoretically, businesses participating in CSR environmental initiatives might forge closer bonds with stakeholders, including clients, staff, and communities. This relationship may increase performance and competition (Saldanha, 2019).

Another argument by Lyon and Maxwell (2008) is that CSR environmental activities can create new business opportunities and generate cost savings. It indicates environmentally conscious businesses can create innovative technologies and procedures that boost productivity and cut waste hence cost reductions and increased competitiveness may result. Some academics say environmental CSR initiatives can be costly and not always boost a company’s competitiveness (Song et al., 2016). Likewise, companies that invest heavily in environmental initiatives may face higher costs that could negatively affect their competitiveness. In addition, CSR environmental activities may not be relevant or feasible for all companies, depending on size, industry, and other factors (Tschopp & Huefner, 2014).

Hypothesis 5: Industrial competitiveness significantly mediates CSR toward Environmental and financial performance.

CSR’s Economic Aspects, Industrial Competitiveness, and Financial Performance

There are some theoretical frameworks in place to explain the connection between CSR economic activities and industrial competitiveness (Chuang & Huang, 2018). The Stakeholder Theory is one such paradigm that highlights the significance of incorporating stakeholders in CSR operations. Theoretically, businesses participating in CSR economic activities can forge deeper linkages with stakeholders like clients, staff, and the community. This relationship may increase performance and competition (Barnett, 2018). In addition, the resource-based perspective is yet another theoretical framework (RBV). The RBV claims that businesses engaged in CSR economic operations can create assets and skills that improve their competitiveness (Donnellan & Rutledge, 2019). One of the claims made in the literature is that CSR economic actions might improve a company’s brand value and reputation, strengthening its competitiveness (McWilliams et al., 2006). Businesses that engage in CSR economic operations are shown as socially and economically sustainable, which may draw in clients who perceive these concerns (Smith & Smith, 2011). CSR economic operations can also assist businesses in adhering to rules and avoiding potential fines, which boosts productivity and competitiveness.

Other academics contend that CSR economic activities might be pricey and don’t always enhance competitiveness (Perry et al., 2014). Businesses that make significant financial investments in CSR initiatives may have to deal with higher costs, which may hurt their ability to compete. Nevertheless, depending on a company’s size, industry, and other variables, CSR economic activities might not apply to or be practical for all businesses (Cuadrado-Ballesteros et al., 2017). Therefore, the study has constructed the following hypothesis based on the above empirical and theoretical arguments.

Hypothesis 6: Industrial competitiveness substantially mediates CSR’s economic aspects and financial performance relationships.

CSR Social Dimensions, Industrial Competitiveness, and Financial Performance

In Indonesia, there have been changes to the place of business in society during the past few decades. Businesses now have a more significant role in society than just making a profit; they also contribute to it in some small way. CSR refers to an organization’s attempts to advance socioeconomic welfare in addition to its profit-making objectives. The intensity of industry competition appears to diminish rather than enhance the influence of Corporate Social Investment (CSI) on the long-term performance of emerging-economy firms (Zhong et al., 2022). Hence, long-term success is ensured by a company’s social responsibility to serve the interests of all its stakeholders (Pradhan, 2016). CSR has become a popular term in industry and academics, and responsible business is a worldwide phenomenon. Businesses are active in society for various reasons, including differentiating themselves, garnering customer respect, and satisfying stakeholder needs. Regardless of the motivations, CSR has been shown to contribute to a company’s increased profitability and can be viewed as an investment.

Prior empirical studies on CSR attempted to link it to profitability and competitiveness (Que, 2015). Nevertheless, they did not discuss the possible implications of CSR, such as how it might affect a company’s reputation and how customers might view it, which could impact how well it performs via competition. Thus, our study has tried to close this gap by examining CSR, industry competitiveness, and financial performance relationships.

Several theoretical studies have examined the connection between social CSR initiatives and business competitiveness. The shared value theory proposed by Porter and Kramer (2018) contends that businesses can generate economic benefit by addressing social challenges through their commercial endeavors. The theory holds that businesses that participate in CSR social initiatives can generate shared value by boosting people’s welfare while boosting their competitiveness. Similarly, the stakeholder theory contends that enterprises must consider the interests of all parties involved, including society, instead of their shareholders. Companies can fulfill their social obligations and enhance their reputation by participating in CSR social activities, which can help them compete more successfully in the long run (Husted & Allen, 2007).

Hypothesis 7: Industrial competitiveness has a substantial mediation effect on CSR and Financial performance relationship.

Theoretical Framework

The study proposed a research model that uses industry competitiveness as a mediator variable to examine the effects of companies’ CSR elements (environmental, economic, and social) on financial performance. Moreover, the theoretical framework model indicates that this theoretical framework model suggests that highly polluted companies in Indonesia can benefit from implementing CSR practices that focus on environmental, economic, and social dimensions. By doing so, they can improve their financial performance, enhance their industry competitiveness, and contribute to reducing environmental pollution levels. However, it is essential to note that high environmental pollution levels may weaken the positive impact of CSR dimensions on financial performance. Therefore, companies need to prioritize environmental CSR practices to achieve sustainable development in the long run.

The model incorporates industry competitiveness as a mediator variable, financial performance as a dependent variable, and CSR practice characteristics such as environmental, economic, and social elements as independent variables. Figure 1 shows a representation of all study variables in the conceptual model.

Authors’ proposed conceptual model for the study.

Research Design

Variables Operationalization

Independent Variables

Corporate Social Responsibility (CSR)

The researchers employed the environment, economic, and social dimensions to generate three independent variables from the CSR dimensions. The study measured environment dimension indicators developed by Nozawa et al. (2017) developed. The economic dimension measurement consists of six items adapted from Alvarado-Herrera et al. (2017), and the social dimension measured six and adapted from Nozawa et al. (2017). The measurement items comprise applying the CSR dimensions toward financial performance. Financial resources are devoted to the sustained activity and environmental, economic, and social extent supporting financial performance. The level of CSR in participating in community development projects and the existence of relevant industry structures to deal with all financial activities.

Dependent Variable

Financial Performance

Financial performance will be assessed considering the unique challenges and costs of managing environmental risks and pollution while maintaining profitability and creating value for shareholders. The study measured financial performance indicators developed adapted from Akomeah et al. (2018). Measurement items will include return on investment (ROI), environmental, social, and governance (ESG) metrics, cost of pollution control, and revenue growth. Likert 5-point scale will be used to rate the aspects of financial performance.

Mediating Variable

Industrial Competitiveness

Industrial competitiveness will serve as a mediator variable. It will be assessed using observed variables as indirect means for evaluating the impact of industrial competitiveness on the environmental, economic, and social dimensions and financial performance. Measurement items for the mediating variable will be adopted from Repinskiy et al. (2021). Likert 5-point scale will be used for scoring.

Data Collection and Sampling

The study examines the influence of corporate social responsibility on the financial performance of heavily polluted Indonesian companies, with a focus on the mediating role of industry competitiveness. We used specific criteria to determine the most appropriate criteria for the specific study. Some factors that could be considered include the type and concentration of pollutants, the location and proximity to the company, the surrounding environmental conditions, and the regulatory standards and guidelines. The sample is selected using a purposive sampling method based on companies listed on the Indonesian domestic and international companies that operate in highly polluting industries. The study employed deductive reasoning and quantitative research methods (Kumar, 2018).

Sampling Selection

In this study, the researchers concentrated on analyzing the impact of corporate social responsibility (CSR) on the financial performance of heavily polluted companies in Indonesia. Additionally, they explored the mediating role of industry competitiveness in this relationship. To conduct the study, specific criteria were employed to determine relevant factors such as pollutant type and concentration, proximity to the company, environmental conditions, and regulatory standards.

The sample for the study was selected using a purposive sampling method, targeting companies listed on both domestic and international Indonesian stock exchanges that operate in highly polluting industries. The research followed a deductive reasoning approach and utilized quantitative research methods. Primary data were gathered from general managers, finance managers, and environmental regulators, while secondary data were obtained from company reports, government annual reports, policy documents, and literature. The sample consisted of 400 businesses operating in the manufacturing, chemical, mining, and energy sectors, with a particular emphasis on 250 industrial companies selected based on their current CSR initiatives, experience, and data availability. These companies fulfilled the criteria for common business classifications, requiring a majority of ownership and involvement of at least two managers in the company’s management and daily operations.

Respondents were chosen using a purposive sampling approach, as management teams were considered to have superior insight into the company’s financial status compared to ordinary personnel (Marić et al., 2021). Prior to data collection, the purpose of the study was explained to all respondents. Robustness check analyses were performed using the collected data. CSR activities were obtained from each company’s database, while ownership data and board attributes were gathered from company reports and supplementary information.

A self-administered questionnaire was distributed to the respondents, including general managers, vice managers, finance managers, and regular employees, to collect the required data. However, due to missing information, 12 surveys were disqualified out of the 238 responses received. Additional analyses were conducted using the remaining surveys. To ensure representativeness, it’s crucial to sample more than 10% of the total population accurately. In this study, 60% of the industrial companies in the study region were included, surpassing the recommended threshold (Memon et al., 2020).

The sample selection process can be outlined in Table 1.

Sample Selection Process in Tabular Form.

Data Analysis

The study also conducted a PLS-SEM analysis utilizing the Smart-PLS statistical tool to scrutinize the relationships between the constructs. PLS-SEM is a second-generation regression model with multiple functions and two distinct components (Shiau et al., 2019). In the initial phase of the analysis, a measurement model was utilized to assess the reliability and validity of various indicators. Subsequently, the structural model was employed to validate the hypothesis and illustrate the structural connections between the variables. The mediation analysis in the study also utilized PLS-SEM to ascertain both the direct and indirect effects of the constructs (Hair Carole et al., 2017).

Empirical Results

Analyzing Demographic Data

In this study, the scale used for demographic variables such as age, position, and service has an ordinal scale. Whereas gender is a nominal scale. Based on the demographic data from the 238 participants in this study, it was found that 72% were male, while the remaining 28% were female. Statistical evidence indicates that female participation is limited. This may stem from companies being hesitant to extend more credit to female employees. The majority of respondents fell within an appropriate age range for the study, implying that they were mature adults capable of comprehending the researcher’s inquiries and providing accurate responses. Concerning the educational backgrounds of the respondents, the study’s results reveal that 31.2% held a bachelor’s degree, 52.9% possessed a master’s degree, and 15.9% held a doctorate. The data presented in Table 2 indicates that the majority of respondents were able to understand the study’s objectives and provide valuable information.

Demographic Information.

Source. Author’s Survey data (2022).

Measurement Model Analysis

The measurement model is a component of the overall model that investigates the correlation between latent variables and the indicators used to measure them (Sarstedt et al., 2014). In our approach, we utilized the measurement model to establish the validity and reliability of the constructs. Within PLS-SEM, the measurement model acts as the initial stage for assessing the precision and consistency of the indicators employed.

Reliability and Validity Test

PLS-SEM statistical techniques were used in this study to evaluate the reliability and validity of each relevant questionnaire item. Validity and reliability were assessed within the measurement model using various metrics, including factor loadings, Cronbach’s alpha, composite reliability, convergent validity, and discriminant validity (Hair et al., 2019). Table 3 below presents the results of the study’s convergent validity analysis. Cronbach’s alpha and composite reliability are utilized to assess the internal consistency of the scale items (Hamid et al., 2017). Both Cronbach’s alpha and composite reliability should ideally exceed .70 on average, indicating acceptable internal consistency. Additionally, the average variance extracted (AVE) and factor loadings should ideally surpass .50 on average, signifying satisfactory convergent validity (Hair et al., 2011). Table 3 and Figure 2 provide evidence that the sample data in the current study is robust and reliable. Both Cronbach’s alpha and composite reliability (CR) values exceed .70, indicating strong internal consistency. Moreover, the AVE and factor loadings values are greater than .50, suggesting significant correlations between the items and confirming convergent validity.

Measurement Model Analysis.

Note. CSR = corporate social responsibility; Eco-CSR = economic corporate social responsibility; Env-CSR = environmental corporate social responsibility; Soc-CSR = social corporate social responsibility; FP = financial performance.

Measurement model assessment (output).

Discriminant Validity

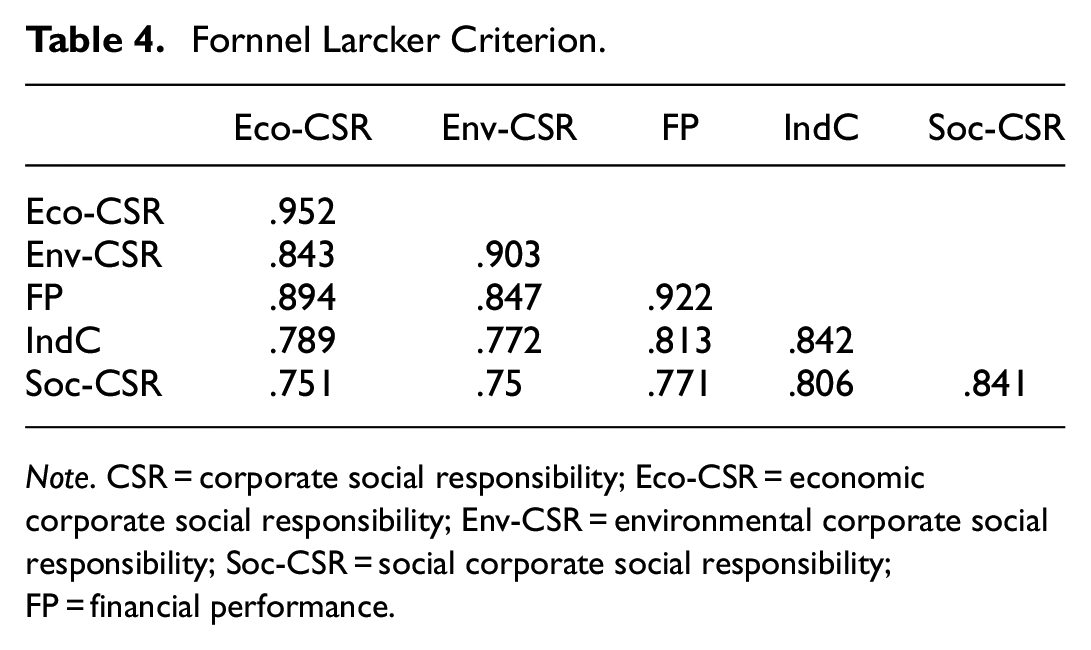

Prior to assessing discriminant validity, we initially evaluated convergence and reliability using statistical measures. The goal was to demonstrate no data redundancy when using items that assess the same construct (Henseler et al., 2015). In Smart-PLS, three techniques were employed to establish discriminant validity (Edeh et al., 2023). The three techniques used in Smart-PLS to establish discriminant validity are cross-loadings, Heterotrait-Monotrait (HTMT) ratio analysis, and the Fornell-Larcker criterion (Hamid et al., 2017). Initially, we assessed discriminant validity by examining the correlations between variables (Larcker, 1981). According to the criterion, discriminant validity is ensured if the square root of the Average Variance Extracted (AVE) for a particular construct is greater than its correlation with other constructs (Edeh et al., 2023). The value in the bold diagonal of Table 4 signifies no issue with discriminant validity, as it surpasses the inter-construct correlation. This indicates that a construct is distinct and explains concepts not captured by other constructs in the model (Afthanorhan et al., 2021).

Fornnel Larcker Criterion.

Note. CSR = corporate social responsibility; Eco-CSR = economic corporate social responsibility; Env-CSR = environmental corporate social responsibility; Soc-CSR = social corporate social responsibility; FP = financial performance.

The second step involved utilizing cross-loadings (CL) to confirm discriminant validity. In this method, a specific item should exhibit higher loadings on its intended construct compared to other constructs included in the analysis (Larcker, 1981). Table 5 indicates that the item displays higher loadings compared to others in the current investigation, suggesting a weak relationship between the variables and supporting comprehensive discriminant validity.

Cross Loadings.

Note. CSR = corporate social responsibility; Eco-CSR = economic corporate social responsibility; Env-CSR = environmental corporate social responsibility; Soc-CSR = social; FP = financial performance.

The Heterotrait-Monotrait (HTMT) correlation ratio serves as a final assessment of discriminant validity. A threshold level of .90 is considered acceptable if the structural model includes constructs that are conceptually very similar. Indeed, if the HTMT value exceeds .90, it indicates a deficiency in discriminant validity. With HTMT values below .90 in our case, it signifies low correlations between variables, indicating sufficient discriminant validity (Henseler et al., 2015). The results are shown in Table 6 below.

Heterotrait and Monotrait Ratio.

Note. CSR = corporate social responsibility; Eco-CSR = economic corporate social responsibility; Env-CSR = environmental corporate social responsibility; Soc-CSR = social corporate social responsibility; FP = financial performance.

Structural Model Analysis

The structural model illustrates the connections between latent variables and assesses the significance of the relationships between them. Assessing collinearity concerns is indeed the first step in analyzing the structural model. Therefore, we first examined the potential for collinearity issues before delving into the structural relationships between latent variables. In cases of collinearity issues, the study may choose to either exclude certain predictor variables or combine them into a single construct. This study utilized the variance inflation factor (VIF) to investigate the presence of multicollinearity issues. The constructs were found to be free of collinearity issues, as indicated by collinearity statistics resulting in VIF values below the threshold of three (3) (Stevens & Pituch, 2011); hence, the result ranged from 1.509 to 2.676.

Furthermore, in this study, we calculated the value of R2. In partial least squares (PLS) structural equation modeling, the R-squared (R2) is a commonly employed metric to gauge the adequacy of fit or model fit of the PLS model. It is derived by squaring the correlation between the observed and predicted values of the endogenous latent variable. The R2 value ranges from 0 to 1, with higher values indicating a better match between the observed and predicted values of the endogenous latent variable. In the partial least square structural equation modeling (PLS-SEM), if R2 is .60 or higher, it has a significant predictive accuracy and is supported by (Hair et al., 2019) [5]. Therefore, the (R2) results in the described dependent variables are above .60 (Table 7).

R 2 Results Report.

Source. Results from the Author’s analysis through SEM-PLS.

On the other hand, the study used SEM to test model fitness by using the SRMR. The standardized root mean square residual (SRMR) serves as a metric to evaluate model fit within partial least squares structural equation modeling (PLS-SEM). It offers a holistic assessment of the disparity between the sample covariance matrix and the model-implied covariance matrix, thereby providing an overall evaluation of the model fit. A lower SRMR value indicates a better model fit, with values below 0.08 generally considered acceptable (Henseler et al., 2015). Therefore, this study found a relevant (SRMR) result, 0.072. Hence, when the result is below 0.10 (<0.1), it indicates that the model adequately fits the data. Additionally, the study reported a Normed Fit Index (NFI) result of 0.882. It’s worth noting that a value closer to 1 signifies a better fit (Hair et al., 2011). This research model is well-fitted based on the SRMR and NFI values and see in the following Table 8.

Model Fitness.

Source. Results from the Author’s analysis through SEM-PLS.

Path Analysis

A system of equations with all variables observed is estimated using path analysis. Path models allow for several dependent variables. In contrast to regression models (structure of regression models). The variables of a path model may be included in Smart-PLS as single-item constructs. The indicators are given the same weights to calculate the construct scores for the dependent Variable on numerous indicators.

Additionally, significance testing for the path model is possible in Smart-PLS for bootstrapping. Hence, the processing module offers all of the modeling and computation capabilities typically available for the process. No additional computations outside of Smart-PLS are needed because Smart-PLS automatically build the process models. Thus, the results are promptly generated, and the process model in Smart-PLS is depicted in Figure 3, while Table 9 displays the corresponding output.

Structural model analysis.

Path Analysis Results.

Note. CSR = corporate social responsibility; Eco-CSR = economic corporate social responsibility; Env-CSR = environmental corporate social responsibility; Soc-CSR = social corporate social responsibility; FP = financial performance.

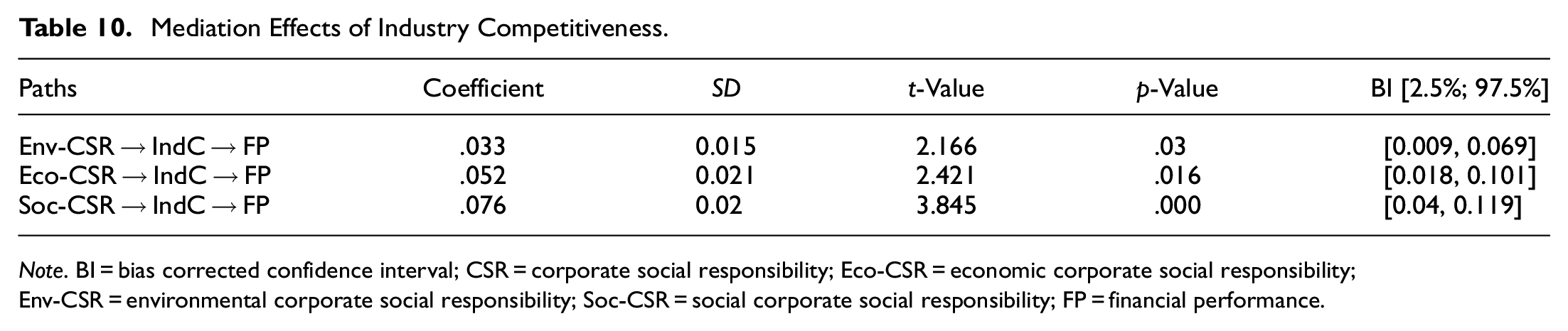

Mediation Analysis

As part of the mediation analysis, the industry’s competitiveness was scrutinized to understand how the relationship between financial performance and CSR dimensions (environmental, economic, and social) was mediated. The correlations between environmental CSR and financial performance, economic CSR and financial performance, as well as social CSR and financial performance, all remain significant even in the presence of the mediating variable industrial competitiveness (β = .095, t = 2.419, p < .001, β = .227, t = 5.356, p < .05, β = .441, t = 8.168, p < .05) in the direct relationship. The indirect effects of environmental CSR, economic CSR, and social CSR on financial performance via industry competitiveness were also found to be significant (β = .033, t = 2.166, p < .05, β = .052, t = 2.421, p < .05, β = .076, t = 3.845, p < .05). Table 10 below illustrates that both direct and indirect pathways were significant, indicating that the relationship between CSR aspects (environmental, economic, and social) and financial performance was mediated by industry competitiveness.

Mediation Effects of Industry Competitiveness.

Note. BI = bias corrected confidence interval; CSR = corporate social responsibility; Eco-CSR = economic corporate social responsibility; Env-CSR = environmental corporate social responsibility; Soc-CSR = social corporate social responsibility; FP = financial performance.

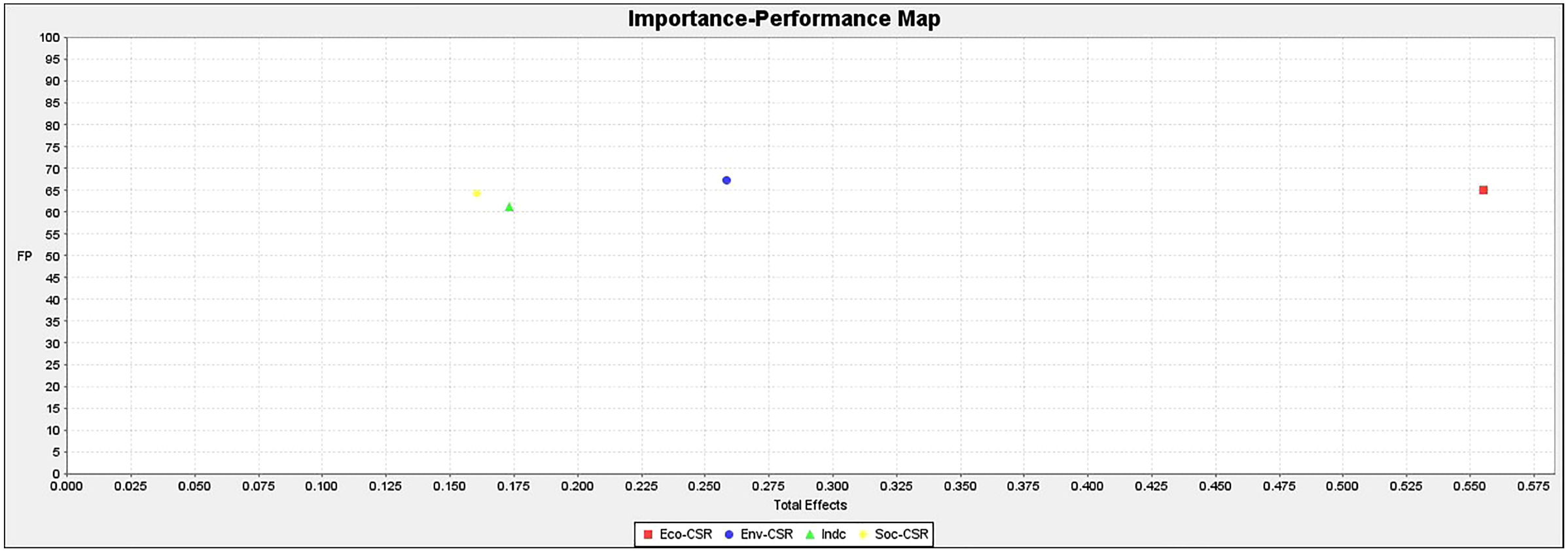

Importance-Performance Map (IPMA) Analysis Results

The Importance-Performance Map Analysis (IPMA) was employed in our study. IPMA is a valuable tool that allows researchers to evaluate and prioritize various aspects of a project or product based on their importance and performance. It serves as a means to identify research priorities, measure research impact, enhance stakeholder engagement, and inform decision-making. By determining priorities and areas for improvement, IPMA enables researchers to make data-driven decisions and allocate resources more efficiently, thereby contributing to the success of the research project.

In our particular study, we employed IPMA to pinpoint the CSR dimensions that exerted the most significant influence on the financial performance of the industries. The analysis findings unveiled that the economic CSR dimension had the most substantial impact on financial performance, whereas the social CSR dimension exhibited a relatively lesser effect. These findings can be observed in Table 11.

Report of Importance-Performance Map Analysis (IPMA).

Note. CSR = corporate social responsibility; Eco-CSR = economic corporate social responsibility; Env-CSR = environmental corporate social responsibility; Soc-CSR = social corporate social responsibility; FP = financial performance.

Moreover, we examined the predominant influence of CSR dimensions on financial performance within these industries using the Importance-Performance Map (IPM) constructs, showcasing standardized effects as depicted in Figure 4. As a result, the automated outcomes on the map demonstrated that the economic CSR dimension wielded the most considerable influence on financial performance in the industries, succeeded by the moderate impact of the environmental CSR dimension, and the weakest impact of the social CSR dimension, respectively.

Importance-Performance Map (FP) constructs, standardized effect.

Hypothesis Testing

Once the validity and reliability of the outer models were established, along with confirming the absence of multicollinearity issues, the hypothesized relationships of the inner models were evaluated. In this instance, Table 6 presents the outcomes of the independent factors’ direct impact on the dependent variable. The significance level of the path coefficient can be determined by considering its magnitude, sign, and t-statistic values. Typically, t-values of 1.96 and above are considered ideal. In this experiment, the significance of each structural path was determined using the bootstrapping method. In the first hypothesis (H1), where the environmental corporate social responsibility dimension is hypothesized to have a positive contribution to financial performance, the estimation result showed (β = .095, t = 2.419, p < .05). As a result, economic and corporate social responsibility positively and significantly affects financial performance at the estimation value (β = .227, t = 5.356, p-value < .001). At the estimation value, it has also been determined that CSR significantly and favorably affects financial performance (β = .441, t = 8.168, p < .05). Likewise, industry competitiveness positively and significantly affects financial performance (β = .285, t = 3.954, p < .05). Hence, the research supports H1, H2, H3, and H4. At the same time, we claimed that all the independent variables (environmental, economic, and social CSR) positively contribute to industry competitiveness. Furthermore, as shown in the analysis part of mediation effects of industry competitiveness in Table 7, all the mediation have found significant and partial effects on state hypotheses. Hence, the connection between CSR components (environmental, economic, and social) and financial performance was partially mediated by industrial competitiveness, as both direct and indirect paths were found to be significant. Therefore, the stated hypotheses H5, H6, and H7 have been found to support the study and are shown in Table 12 below. Finally, all the hypotheses are supported.

Summarized Results Testing the Hypotheses.

Note. CSR = corporate social responsibility; Eco-CSR = economic corporate social responsibility; Env-CSR = environmental corporate social responsibility; Soc-CSR = social corporate social responsibility; FP = financial performance.

Discussion and Implications for Policy Makers

This study empirically investigates the relationship between CSR and financial performance using a sample of Indonesian-listed industries with significant pollution footprints. Incorporating industry competitiveness as a mediating variable, a structural equation model was constructed to examine the mediating impact between the primary CSR dimensions, namely environmental, economic, and social, on financial performance. Hence, the following judgments are made.

First, businesses can increase their financial performance by engaging in environmental, economic, and societal CSR initiatives. Positive CSR performance can address stakeholder needs, improve industry reputation, increase investor confidence, draw talent, and enhance sustainable financial performance considerably. The sectors should alter their ingrained beliefs, fully grasp the additional advantages provided by CSR implementation, build a stellar company reputation in the eyes of the public, increase industry visibility, and increase overall market competitiveness.

This study explores the impact of the environmental component of corporate social responsibility (CSR) on the financial performance of heavily polluted companies in Indonesia. The study uncovered that the environmental component of CSR exerts a positive and significant influence on financial performance (Zago et al., 2018). The findings of this study hold significant implications for companies operating in environmentally sensitive industries. When companies adopt environmentally responsible practices, it can lead to both a better environmental impact and improved financial performance. Participating in environmental and corporate social responsibility (CSR) activities can establish a win-win scenario for both companies and society. It implies that companies prioritizing environmental responsibility are more likely to outperform those that do not, and CSR initiatives can directly and positively influence a company’s profitability (Orlitzky et al., 2003). Additionally, the study contends that advancements in operational effectiveness and risk management are responsible for the favorable association between the environmental aspect of CSR and financial performance (Kao et al., 2018). By implementing environmentally friendly practices, Companies can lower operational expenses, boost productivity, and lessen environmental liability risk.

Conversely, the study unveiled that the economic component of CSR exhibits a positive and significant impact on financial performance, suggesting that companies that embrace economic responsibility are more likely to achieve greater financial success compared to those that do not (Kumala & Siregar, 2021). Moreover, the study argues that improvements in consumer loyalty, employee morale, and risk management ultimately elucidate the advantageous relationship between the economic aspect of CSR and financial performance (Nguyen et al., 2021). By implementing ethical business practices, businesses may enhance their reputation, draw in and keep consumers, and lower the risks of bad press and legal action. The findings of this study carry significant implications for companies contemplating engagement in CSR activities. Through such initiatives, companies can enhance their economic impact and attain improved financial performance, thereby fostering a win-win situation for both the company and society (Margolis & Walsh, 2003).

The study also found that CSR’s social dimension positively and significantly affects financial performance in highly polluted companies in Indonesia. The study examined the correlation between CSR and financial performance in heavily polluted organizations and found that engaging in CSR activities, particularly in the social dimension, can enhance financial success. Companies involved in CSR initiatives are perceived as socially responsible and demonstrate higher industry competitiveness, which in turn contributes to improved financial performance (Joo et al., 2017). This implication has significant ramifications for businesses engaged in highly polluting industries. Companies that participate in CSR initiatives positively impact the environment and society unperformed better financially, benefiting both the organization and society (Shanmuganathan, 2019).

Conversely, it is understood that industry competition will enhance the influence of environmental, economic, and social CSR components on financial performance. The effect becomes sounder as the level of industrial competitiveness rises. On the contrary, industry competitiveness undoubtedly reinforces the positive impact of environmental, economic, and social dimensions on financial performance, perhaps because heightened competitiveness enhances the efficacy of financial activities within industries. Shareholders of publicly traded companies that are more engaged are also more inclined to practice corporate social responsibility. Therefore, the findings of this study indicate that a community-based approach can help transform the shareholder engagement mechanism within the industry. To a certain extent, it raises public awareness of businesses, increases CSR fulfillment, and enhances the long-term financial gains of businesses. Hence, industries ought to fortify their corporate governance systems and foster a harmonious, healthy, and sustainable development environment. Given that the connection between environmental corporate social responsibility and industry competitiveness bolsters the financial value of industries, one straightforward hypothesis could be that environmental CSR motivates industries to strive harder to maintain competitiveness. The environmental CSR factor indirectly raises industry value because competitiveness correlates favorably with financial value. For instance, businesses that face environmental penalties are also investing in resources to reduce these costs in the future. In the future, this will make environmental corporate social responsibility simpler. Hence, increasing competitiveness may have an impact on environmental CSR concerns.

The current study shows that industries can improve their CSR practices and financial performance by adopting a comprehensive CSR strategy (Ayton et al., 2022), engaging with stakeholders, monitoring and reporting on performance, investing in innovation, and building a culture of sustainability (Watson et al., 2018). Developing a CSR strategy that aligns with business goals and objectives can help identify areas with the most significant impact while engaging stakeholders can build trust and goodwill. Monitoring and reporting on CSR performance can help identify areas for improvement and communicate progress. Investing in innovation can develop new products and services that address social and environmental issues, and building a culture of sustainability can embed CSR practices into day-to-day operations.

Finally, the findings show that, even though economic policies will significantly affect financial performance, social policies will also significantly impact financial performance if the company prioritizes the achievement of innovation outputs before developing corporate social responsibility policies. In this way, CSR benefits the organization internally, externally, or both. Investments in socially responsible operations may positively affect the organization internally by assisting a company in developing new resources and capabilities, particularly those connected to knowledge and industry culture. It would appear that CSR provides a firm with immediate benefits through increased morale and productivity and enhances benefits while reducing expenses associated with hiring and onboarding new employees (Branco & Rodrigues, 2006). Consequently, although CSR’s economic and social aspects impact industrial outputs, they are not directly tied to financial performance. Furthermore, within the current industrial landscape of Indonesia, the promotional impact of CSR dimensions on the financial performance of heavily polluting enterprises, despite varying industrial factor densities, appears similar. However, the promotional effect may differ for businesses situated in different locations.

Implications for Theory

The study’s findings carry several theoretical implications: Firstly, it broadens the research perspective on CSR dimensions (environmental, economic, and social) and financial performance. Prior studies have predominantly explored the relationship between industrial competitiveness and financial performance, as well as the extensively researched association between CSR and financial performance. To our knowledge, few researchers have investigated the connection between these factors. This study integrates CSR, industry competitiveness, and financial performance into a unified research framework by incorporating industry competitiveness to evaluate the effects of environmental, economic, and social CSR on financial performance. It elucidates the causal pathway between the three CSR dimensions and financial performance, elucidates the logical relationship between them, and presents a theoretical framework for companies to establish a coordination mechanism among CSR dimensions, industry competitiveness, and financial performance.

Secondly, the PLS model employed in this study assesses every relationship. However, as the selection of relevant indicators is subjective and relies on CSR disclosure, it may not fully capture the true social responsibility of businesses. Similarly, the weighting of numerical indicators is also subject to arbitrariness. In the future, it will be vital to pay attention to the equivalent objective quantitative technique of CSR. Third, this study investigates competition, offers a more solid theoretical foundation for decision-making, and offers practical recommendations for industries to fulfill CSR. The behavior of industries, which drives the social economy, results from the combined effects of internal and external influences. Determining the internal variables that have a substantial impact on an industry’s development can thus encourage an industry’s development that is both socioeconomic and environmentally friendly.

Implications for Practice

The following managerial implications for industries may also result from this study. It helps increase industry knowledge of and commitment to CSR. In the past, most industries felt that CSR would reduce their earnings and give them a competitive disadvantage rather than improve performance. Yet, we discovered that implementing more CSR practices increases industry influence and enhances public, economic, and environmental acceptance, substantially impacting the long-term growth of industries. Managers of highly polluting sectors should consider sustainable development when developing company plans, alter their old business philosophy, and adopt correct and constructive CSR values. To promote significantly polluting industries’ conscious adoption of CSR and enhance their social credibility, the public’s sense of trust in them, and the sustainable economic performance of their organization, the manager should develop the necessary laws and regulations.

Our findings may therefore have scientific ramifications for the business world, urging it to pay attention to the rationalization of industry competitiveness to strengthen CSR’s environmental, economic, and social components and improve long-term financial performance. Fair industrial competition not only boosts performance when given high priority by the highest authority but also encourages CSR at a level that boosts financial results. Economically speaking, a rise in development increases the influence of CSR on financial results. Heavily polluting industries may be able to improve other aspects of their operations, such as competent management, the relationship between their significant shareholders, the implementation of mutual supervision and restriction among shareholders, and the enhancement of their ability to make decisions based on facts and logic. They may also be able to examine how competitive advantage may affect their CSR efforts and financial performance.

Conclusion and Future Research Direction

This study investigates how industry competitiveness and CSR affect financial performance. Data from businesses in the primary and chemical industries engaged in CSR activities on behalf of Indonesian industrial corporations are gathered for this study. This study seeks to enhance the comprehension of corporate social responsibility and financial performance within Indonesia’s primary and chemical industries. One of the most challenging problems to solve in Indonesia is the environment (Usman & Amran, 2015). The rising industrial exploitation in Indonesia is one explanation. Businesses that deal with chemicals and raw materials run a significant danger to the environment. This industry is strongly tied to the environment because the raw materials used in manufacturing are taken straight from nature. This establishes the degree to which CSR impacts the financial success of Indonesia’s high-pollution businesses.

This study integrated primary and secondary data sources from 238 sampled industrial companies in Indonesia, utilizing quantitative research techniques. Additionally, a standardized questionnaire was employed to collect data for the study. The collected data were analyzed using the PLS-SEM modeling version to establish the causal relationship between the CSR dimensions (environmental, economic, and social), industry competitiveness, and financial performance. According to the study findings, implementing CSR initiatives that encompass economic, environmental, and social dimensions can have a positive impact on the financial performance of businesses operating in the primary industrial sector. It indicates that companies may benefit from implementing CSR components related to the community and its surroundings. Industry competitiveness has also significantly mediated the relationship between the financial performance of Indonesian chemical businesses and the three elements of CSR (environmental, economic, and social). Strong industrial competitiveness will consequently affect corporate social responsibility.

Although this study has made significant contributions and has important implications, it is not exempt from limitations. For instance, the study’s focus on highly polluted companies in Indonesia may limit its generalizability and may not represent other industries or countries. Therefore, the findings may not apply to companies operating in different contexts or with different pollution levels. Additionally, the study’s reliance on self-reported data from company managers may introduce bias or inaccuracies, and there is a potential for selection bias if some companies choose not to participate in the research. Moreover, the correlational study cannot establish causality between CSR, industry competitiveness, and financial performance. Other factors not accounted for in the study may also influence the relationships observed. The study uses proxies for CSR, industry competitiveness, and financial performance, which may not fully capture the constructs of interest, and the use of subjective measures may introduce measurement error.

Lastly, the study employs mediation analysis to investigate the relationship between CSR, industry competitiveness, and financial performance, which proves to be a valuable analytical tool. Still, the results should be interpreted cautiously, as mediation analysis cannot establish causality. So, future researchers could incorporate new variables, such as legal and technological ones, as modifying factors in their CSR and financial performance analyses.

Footnotes

Appendix A

Measurements Construct Items.

| Variables | Items | Source |

|---|---|---|

| Environmental CSR | (1) Tries to sponsor green activities. | |

| (2) Tries to offer an environmentally-friendly product development actively | Nozawa et al. (2017) | |

| (3) Tries to account for its environmental actions periodically | ||

| (4) Tries to protect the environment | ||

| (5) Takes into account environmental issues when engaged in its activities | ||

| (6) maximizing energy efficiency and productivity | ||

| Economic CSR | (1) Tries to create paid jobs | |

| (2) Tries to improve its long-term economic performance | ||

| (3) Differentiate product/process by the marketing of the social and environmental performance of the product/process | Alvarado-Herrera et al., (2017) | |