Abstract

The institutional development of carbon trading mechanisms has prompted companies to place greater emphasis on ESG factors and incorporate them into strategic decision-making. This study considers the implementation of the carbon emissions trading pilot policy as a “quasi-natural experiment.” Based on the micro-data of China’s A-share listed companies from 2011 to 2020, this study comprehensively assesses the impact of the policy on corporate ESG performance and its underlying mechanisms using a multi-period difference-in-differences model. The empirical findings indicate that crucial regulated companies participating in the carbon emissions trading pilot policy programs significantly enhance their ESG performance. Further research suggests that the carbon emissions trading pilot policy bolsters corporate intrinsic motivation for ESG practices by fostering green technological innovation and increasing executive awareness of environmental issues. Heterogeneity analysis reveals that firms with large-scale operations and high R&D investments, as well as those located in new energy pilot cities, in regions where local officials are in key promotion periods, or in economically developed areas, experience more significant improvements in their ESG performance due to the carbon emission trading pilot policy.

Keywords

Introduction

The increasingly severe issue of global climate change has driven various sectors of society to explore diverse market strategies and policy tools to control greenhouse gas emissions effectively. Among these, as a market-based approach, carbon emission trading guides companies to achieve emission reduction targets efficiently through price mechanisms, gradually becoming a focal point of academic research and policy practice (Umar & Safi, 2023). China initiated its Carbon Emissions Trading Pilot policy (CETP) in select provinces and municipalities in 2011. Subsequently, the country transitioned to a national carbon market, which became operational in July 2020. The publication of the “Interim Regulations on the Management of Carbon Emission Trading” in February 2024 further signifies a new stage in constructing China’s carbon market. As the world’s most significant carbon trading market, China’s carbon trading system not only plays a crucial role in promoting domestic peak carbon and carbon neutrality goals but also holds a substantial position in global climate governance.

The Environmental, Social, and Governance (ESG) evaluation framework, as a key indicator for measuring corporate non-financial performance and sustainability, has become an important basis for investors and stakeholders in assessing corporate value and risk (Erhart, 2022). The carbon emissions trading policy, as a significant environmental policy tool, fundamentally reshapes the corporate operating environment by marketizing carbon emissions quotas (Yu et al., 2023). From the perspective of the three ESG dimensions, this policy has a systemic impact on corporate ESG performance: at the environmental level, it guides companies to optimize production processes and energy structures, improving environmental performance, while carbon asset management creates new value growth points for companies (Dechezleprêtre et al., 2023); at the social responsibility level, companies build green brand images through participation in carbon trading, enhancing stakeholder recognition (Huang & Du, 2020); at the corporate governance level, the carbon trading mechanism promotes greater transparency of environmental information, strengthens climate risk management awareness, and drives the improvement of corporate environmental governance mechanisms.

The existing literature explores the determinants of firms’ ESG performance from multiple perspectives. Regarding internal factors, scholars have examined the impact of managerial characteristics (Liu et al., 2023), financing constraints (Tan & Zhu, 2022), and corporate innovation (Zhou et al., 2024) on ESG performance. In terms of external factors, market structure (Moskovics et al., 2023), regulatory environment (Yu et al., 2023), and social culture (Bai et al., 2024) have been shown to significantly influence firms’ ESG practices. However, research on how market-based environmental policies, such as carbon emission trading schemes, affect firms' ESG performance remains relatively scarce. The existing studies on carbon emission trading policies primarily focus on two levels: micro and macro. At the micro level, attention has been given to the effects on emission reductions (Zhang et al., 2019), economic development (Zhang & Zhang, 2018), corporate innovation (Zhang et al., 2020), carbon pricing (Lin & Jia, 2019), and market development (Zhao et al., 2016). At the macro level, the literature examines energy structure (Zhang et al., 2024), industrial upgrading (Wang et al., 2023), regional heterogeneity (Zhang et al., 2019), and policy coordination (Wen and Jia, 2024). While some scholars have preliminarily investigated the impact of carbon emission trading policies on firms’ ESG performance (Kong et al., 2024), there is a lack of systematic analysis of the internal transmission mechanisms of these policies. Furthermore, existing research has not delved into the role of micro-level factors, such as firms’ green technological innovation and executives’ green cognition, in shaping the impact pathways. To address these gaps, this paper uses the pilot carbon emission trading scheme in China as a quasi-natural experiment. Employing panel data from 2011 to 2020 and a multi-period difference-in-differences (DID) approach, we examine the mechanisms through which the pilot carbon emission trading policy influences firms' ESG performance.

Compared to existing literature, the marginal contributions of this paper are as follows: First, this study constructs and validates a dual mediation theoretical framework of “carbon emission trading pilot policy-green technological innovation/executive green cognition-corporate ESG performance.” Unlike prior studies that primarily focus on the direct impact of carbon trading policies on ESG performance (Kong et al., 2024), this research unveils the internal transmission mechanisms of policy effects. It not only enriches the application scenarios of carbon trading policies but also provides new theoretical insights and empirical evidence for understanding how these policies influence corporate ESG performance. Second, from the perspective of policy transmission, this study introduces corporate green technological innovation and executive green cognition as mediating factors. By employing structural equation modeling and causal mediation analysis, it explores the mechanisms through which these factors influence the relationship between carbon trading policies and corporate ESG performance. The findings extend Liu et al. (2022)’s research on carbon trading promoting green innovation and deepen Truant et al. (2023)’s discussion on the relationship between technological innovation and ESG. Through multiple robustness checks, the study offers new insights into the policy transmission mechanisms. Finally, the paper examines the heterogeneous impacts of the policy at both micro and macro levels. Unlike Zhang and Xi (2024), which focus solely on regional disparities, and Chen et al. (2022), which emphasize firm-specific characteristics, this study investigates multiple dimensions, including firm size, R&D investment, regional characteristics, official profiles, and economic conditions. By doing so, it deepens the understanding of the heterogeneous effects of carbon trading policies and provides targeted recommendations for policy formulation.

Theoretical Analysis and Research Hypotheses

Carbon Emission Trading Pilot Policy and Corporate ESG Performance

The core concept of carbon emission trading lies in internalizing the externalities of environmental inefficiency through market-based mechanisms. Based on this premise, this paper argues that carbon emission trading pilot policies can enhance firms’ ESG performance through three mechanisms. First, the institutional constraint mechanism. According to new institutional economics, institutional arrangements reshape the structure of transaction costs, thereby influencing the behavior of micro-level entities (Coase, 1998). As a form of mandatory environmental regulation, carbon trading policies directly constrain firms’ emission behaviors through quota management, compelling firms to improve their environmental governance (Shao et al., 2023). Simultaneously, these policies guide firms to incorporate environmental costs into decision-making via price signals (Chen et al., 2022). More importantly, the carbon trading system encourages firms to establish environmental management systems, enhance information disclosure, and optimize governance structures, all of which are critical dimensions of ESG evaluation (Zhang & Xi, 2024). Empirical studies indicate that institutional pressure arising from government environmental oversight significantly improves firms’ ESG performance (Liu et al., 2024). Second, the market incentive mechanism. Stakeholder theory posits that firms must balance the interests of various stakeholders to secure the critical resources needed for sustainable development. Firms’ ESG activities essentially aim to address the needs of diverse stakeholders and maintain social legitimacy (Halbritter & Dorfleitner, 2015). The implementation of carbon trading mechanisms raises investors’ and consumers’ expectations regarding firms’ environmental performance, prompting firms to strengthen ESG management to protect brand reputation and gain social recognition (Sim & Kim, 2024). Na et al. (2024) find, based on a study of Chinese listed firms, that market incentives such as government subsidies enhance firms’ willingness to invest in innovation, mitigate managerial myopia, and improve ESG performance. Third, the resource capability mechanism. According to the resource-based view, carbon emission rights are a scarce strategic resource whose effective management can reduce firms’ compliance costs and generate new revenue streams (Lin & Jia, 2019). Within the carbon trading system, firms can reduce emissions through measures such as improving energy efficiency and optimizing production processes, thereby selling surplus quotas for profit or avoiding the additional costs of purchasing quotas. Dynamic capability theory suggests that firms must continually improve their environmental governance to adapt to increasingly stringent carbon constraints (Chevrollier et al., 2023). Therefore, under the combined effects of these “institutional constraints-market incentives-capability enhancement” mechanisms, carbon emission trading pilot policies incentivize firms to integrate ESG principles into their strategic decision-making, positively impacting their ESG performance. Based on the above analysis, this paper proposes the following hypothesis:

Corporate Green Technological Innovation Mechanism

The mechanism for enhancing corporate ESG performance is a core issue in sustainability research. Existing studies suggest that technological innovation is a critical driving force behind improving corporate ESG performance (Truant et al., 2023), with firms possessing stronger innovation capabilities often achieving better ESG ratings (Wang et al., 2023; Zhou et al., 2023). This paper posits that the carbon emissions trading pilot policy influences corporate ESG performance through green technological innovation, a claim supported by the following three theoretical perspectives:

First, from the perspective of innovation motivation, the Porter Hypothesis argues that environmental regulation can stimulate firms' innovation incentives, achieving a win-win outcome for environmental protection and economic efficiency (Porter and van der Linde, 1995). Carbon trading policies, through mechanisms such as price guidance (Zhang et al., 2020), quota management (F. Zhou & Wang, 2022), and policy incentives (Liu et al., 2022), encourage firms to pursue green technological innovation. The long-term nature of these policies further promotes increased investment in green R&D (Noailly & Ryfisch, 2015), driving sustainable development. Empirical evidence from Liu et al. (2022) confirms that participation in carbon trading significantly boosts firms’ innovation investment and patent output, creating endogenous momentum for continuous innovation.

Second, from the perspective of the mechanism for ESG enhancement, technological innovation improves corporate ESG performance through multiple pathways: in the environmental dimension, innovation directly enhances energy efficiency, reduces pollutant emissions, and optimizes resource allocation (Pan et al., 2022); in the social dimension, clean production and green product development enhance corporate reputation and strengthen stakeholder relationships (Chege & Wang, 2020); and in the governance dimension, innovation facilitates the improvement of management systems, increases information transparency, and strengthens risk control capabilities (Zhang et al., 2024).

Third, from the resource capability perspective, green technological innovation serves as a unique strategic resource for firms (Khanra et al., 2021). Through the accumulation of innovation capabilities and organizational learning, it enhances environmental performance and ESG management levels (Zhang & Zhu, 2019). Sustained innovation activities also improve firms’ dynamic adaptability by enabling them to identify opportunities and integrate resources effectively (Wang et al., 2019), transforming environmental policy pressures into drivers for ESG improvement. Accordingly, the following hypothesis is proposed:

Executive Green Awareness Mechanism

The upper echelons theory posits that executives’ cognition and values profoundly influence firms’ strategic choices and decision-making (Hambrick and Mason, 1984; Harrison et al., 2007). Executive green cognition, defined as the tendency of senior managers to acquire, interpret, and evaluate environmental information and policies when making decisions (Qu et al., 2015), has become a critical factor affecting firms’ sustainable development strategies. Research indicates that executives with strong environmental awareness are more inclined to leverage this awareness to shape a positive corporate ESG brand image (Ronalter et al., 2023). This study argues that carbon emission trading policies enhance firms’ ESG performance by elevating executives’ green cognition. This mechanism operates through two channels: Direct effects of carbon trading policies on executives’ green cognition: First, policy frameworks and regulatory pressures compel executives to reassess corporate environmental responsibilities and prioritize green governance (Tan & Zhu, 2022). Second, market-based carbon pricing mechanisms highlight the economic value of environmental management, linking environmental performance directly to corporate profits (Wu & Tham, 2023). Third, sustained participation in carbon trading practices fosters systematic frameworks of green cognition as executives accumulate environmental management experience (Wang et al., 2024). Finally, the long-term stability of such policies strengthens executives’ confidence in and commitment to green development. Empirical evidence supports this perspective, showing that executives in pilot regions exhibit significantly heightened environmental awareness and stronger identification with sustainability concepts (Liu et al., 2024). Indirect effects of executives’ green cognition on firms’ ESG practices: In the environmental dimension, executives with green cognition are more likely to adopt environmentally friendly technologies and practices to improve environmental performance (Zameer et al., 2021). In the social dimension, they drive initiatives such as employee environmental training and energy-saving campaigns, fulfilling social responsibilities while enhancing social performance and employee satisfaction (Law et al., 2017). In the governance dimension, green cognition motivates executives to refine corporate governance structures and establish robust systems for environmental compliance and risk management, thereby improving governance quality and information transparency. In summary, carbon emission trading pilot policies not only directly regulate corporate emissions but also indirectly and sustainably enhance firms’ ESG performance by cultivating and reinforcing executives’ green cognition. Therefore, this paper proposes the following hypothesis:

Research Design

Data Sources

Considering the start time of the pilot policy and the completeness of ESG data, this study uses data from A-share listed companies in China from 2011 to 2020 as the research sample. Following the approach of Deng et al. (2023), corporate ESG data is sourced from the Huazheng ESG Ratings in the WIND database, while other data are obtained from the CSMAR database. The data processing procedure includes the following steps: (a) excluding ST, *ST, and PT companies to avoid interference from abnormal operational and financial conditions on ESG performance; (b) excluding listed firms in the financial sector due to the significant differences in their asset-liability structures caused by unique accounting standards and regulatory requirements; (c) removing observations with missing or abnormal data to ensure data completeness; and (d) winsorizing all continuous variables at the top and bottom 1% percentiles to mitigate the impact of outliers and enhance the robustness of statistical results. After these steps, the final sample consists of 9,439 valid observations from 1,341 listed companies. Data processing and regression analyses were conducted using Stata 18.0.

Model Specification

To comprehensively analyze the actual effects of the carbon emission trading pilot policy on corporate ESG performance, this study focuses on the pilot policy launched in 2013. The selection of this time point is based on China's approval of carbon emission trading pilots in seven provinces and cities—Beijing, Tianjin, Shanghai, Chongqing, Hubei, Guangdong, and Shenzhen—with the primary implementation period concentrated between 2013 and early 2014. Given the differences in the market launch timing of carbon trading in the pilot regions, this study employs a multi-period difference-in-differences (DID) model to examine the relative differences in corporate ESG performance between the treatment and control groups before and after the policy implementation. Recognizing that the selection of pilot regions was not entirely random, the study incorporates the propensity score matching (PSM) method to mitigate potential endogeneity issues and reduce systematic bias arising from non-random grouping. Based on the above considerations, we construct the following econometric model:

In the above expression (1): i stands for individual, t stands for year, and

This paper employs a causal mediation effect model to identify the causal transmission mechanisms through which the policy impacts corporate ESG performance, with a particular focus on the roles of firms' green technological innovation and executives' green cognition. Taking green technological innovation (InPatent) as an example, the implementation of the carbon emission trading pilot policy generates two potential outcomes for firms' green innovation: one being the innovation level InPatent(1) after policy implementation, and the other being the innovation level InPatent(0) prior to policy implementation. However, due to the nature of counterfactuals, a firm can only exist in one state at a given point in time, allowing observation of only one outcome. Correspondingly, a firm’s ESG performance has two potential outcomes:

To efficiently identify average causal mediating effects, this paper proposes a set of hypotheses (including two sequentially negligible hypotheses, collectively called the sequential negligibility hypotheses). The first assumption is that treatment assignment is considered negligible. After controlling for pretreatment confounders, the treatment or intervention of the policy is randomized, independent of the potential outcome and potential mediating variables. The second assumption is that the observed mediating variable becomes insignificant after controlling for observed treatment variables and pretreatment confounders. In other words, this assumption is likely to be violated if unobservable factors

The above equation

For each object, only

Variable Definitions

The dependent variable is corporate ESG performance (ESG). Given the availability, time span, and reliability of the data, this study adopts the Huazheng ESG rating scores as the primary measure of the dependent variable, drawing on the methodology used by Deng et al. (2023). The Huazheng ESG evaluation system is constructed based on international mainstream ESG evaluation methods, while incorporating the specific characteristics of China's capital market and various types of listed companies. It has been widely recognized by both industry and academia (Zhou et al., 2024). Additionally, for robustness checks, this study follows the approach of Halbritter and Dorfleitner (2015) by using Bloomberg ESG ratings as an alternative measure of firms’ ESG performance. Compared to the Huazheng ESG ratings, Bloomberg ESG ratings provide not only an overall score but also detailed sub-scores for environmental, social, and governance dimensions.

Explanatory Variable

Difference-in-Differences (DID). The explanatory variable is a multi-period difference-in-differences variable (did). Following the study by Cong et al. (2024), corresponding dummy variables are established to indicate whether the region has implemented the CETP. First, if a firm is identified as a key regulated enterprise within the carbon emission trading pilot scheme in the specified region, the pilot region variable treat is marked as 1; otherwise, it is marked as 0. Second, the pilot time variable post is introduced, with 2013 chosen as the pilot year. If the company falls within the period during or after the implementation of the carbon emission trading pilot, the post is set to 1; otherwise, it is set to 0. Finally, the interaction term did is constructed as the product of treat and post (

Corporate Green Technological Innovation (InPatent)

Green technological innovation refers to the various technological innovations that achieve energy saving and environmental protection during the production and R&D processes. Patent output serves as a direct indicator of technological innovation. Specifically, the aggregate count of green patent applications provides a robust measure of a firm’s capacity for eco-innovation (Tan and Zhu, 2022). Following the study by Wan (2024), this paper identifies the number of regional green invention patent applications (Envinv) by matching the Chinese National Intellectual Property Patent Database and the WIPO International Patent Classification Green List. Corporate green technological innovation is quantified using the natural logarithm of green invention patent applications plus one (In[Envinv + 1]).

Executive Green Awareness (Green)

The executive green awareness variable is based on the management team’s core values and knowledge structure, making them highly alert and sensitive to sustainable development issues. In this evaluation, Python tools are utilized to conduct text analysis on the annual reports of listed companies, selecting relevant keywords for word frequency statistics. The analysis centers on the frequency and distribution of commonly used terms like “sustainable development,”“green ecology,”“energy saving and emission reduction,” and “environmental protection strategy” in the company’s reports. By constructing a word frequency index, we measure the green awareness of executives in listed companies, reflecting the management’s attention to green issues in their decision-making.

Control Variables

Drawing on the relevant research by Yu et al. (2023), the following control variables are selected: company size (Size), debt-to-asset ratio (Lev), return on assets (ROA), revenue growth rate (Growth), listing age (ListAge), proportion of independent directors (Indep), dual role of CEO and chairman (Dual), management ownership (Mshare), and most extensive shareholder ownership (Top1). The two-way fixed effects of industry (Industry) and year (Year) are also considered. The specific definitions of the main variables are detailed in Table 1.

Description of Variables.

Empirical Tests

Descriptive Statistics

Table 2 displays the summary statistics. The mean ESG score is 4.409 (standard deviation 1.105), with a median of 4, indicating that the overall ESG performance of the sample firms is slightly below average, with significant differences between firms. The median value for green technological innovation is 0, with a mean of 0.319 and a maximum of 3.807, reflecting that most firms have not yet engaged in green patent applications. However, a few have shown outstanding performance in this area. The median value for executive green awareness is 1, with a mean of 3.274 and a maximum of 24, indicating substantial variation in management’s importance on green concepts, with room for improvement in overall awareness levels. Additionally, as a binary variable in the study, the CETP shows that approximately 33.8% of the sample firms participated in the pilot.

Results of Descriptive Statistics.

Table 3 presents the Pearson correlation coefficients among key variables. ESG is positively correlated with green innovation, executive environmental awareness, and firm size, suggesting potential transmission mechanisms of the carbon policy. The correlation coefficients are all below .6, alleviating concerns about severe multicollinearity.

Pearson Correlation Matrix of Key Variables.

Note. *p < 0.05 (two-tailed).

To further confirm this, we report Variance Inflation Factor (VIF) results in Table 4. All VIF values are below the conventional threshold of 10, and the mean VIF is only 1.330, indicating that multicollinearity is not a serious concern in our empirical models. These diagnostics strengthen the reliability of the regression results.

Variance Inflation Factor (VIF) Results.

Parallel Trend Test

The parallel trend assumption must hold for DID to be valid. Our study examines this crucial condition by analyzing a 7-year dataset. This dataset encompasses two years preceding firms’ participation in the carbon emission trading pilot, the year they joined, and four years post-entry. Through this comprehensive analysis, we assess the applicability of the DID approach in our research context. Additionally, the analysis excludes the first year post-implementation data to avoid initial adaptation effects and reduce multicollinearity. A regression model was constructed with dummy variables for six-time points, using the first period before the policy implementation as the baseline. Figure 1 illustrates the parallel trend test outcomes. Prior to policy implementation, the near-zero coefficients and 95% confidence intervals clearly encompassing zero indicate no significant ESG performance gap between treatment and control groups, strongly supporting the parallel trend assumption. During the policy implementation year, coefficient values exhibit an upward trend, albeit statistically insignificant, potentially indicating a latency period in policy efficacy. After the policy implementation, the coefficients are significantly positive, showing an initial increase followed by a slight decline. The peak occurs in the post2 period, after which there is a slight decrease. Still, the coefficients remain above 0.1, and the confidence intervals do not include 0, indicating a sustained positive impact of the policy. This demonstrates that, in the absence of policy intervention, the comparable ESG performance trajectories of treatment and control groups validate the parallel trend assumption, thus satisfying a fundamental prerequisite for the difference-in-differences analysis.

Parallel trend test results.

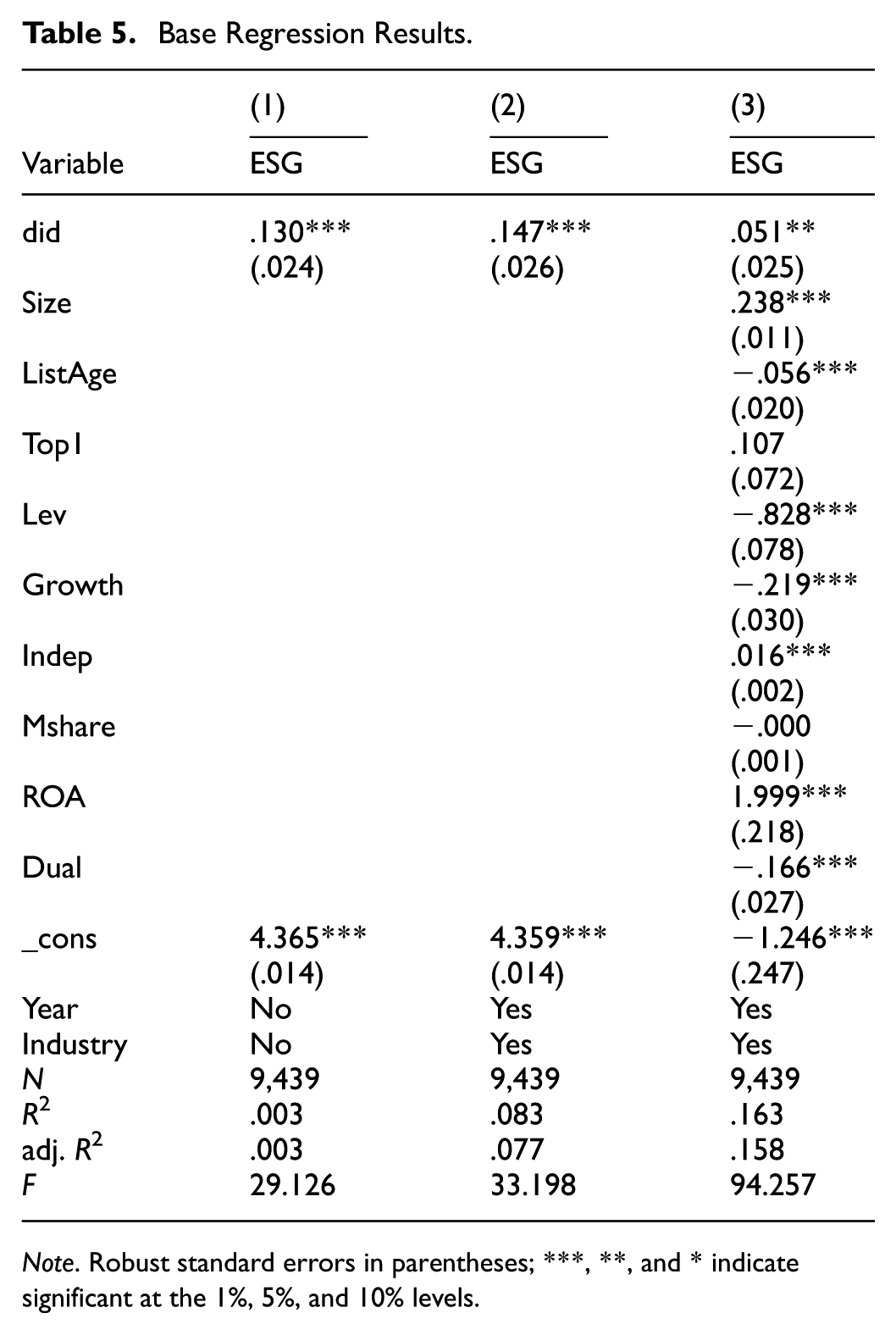

Baseline Regression Results

Table 5 displays the baseline regression outcomes. Column (1) shows the regression results of the core explanatory variable (did) on corporate ESG performance (ESG). Column (2) includes the regression results after controlling for year and industry fixed effects. CETP implementation exhibits a statistically significant (p < .01) and positive association with corporate ESG performance. This relationship remains consistent across models, irrespective of time and industry fixed effects inclusion. Column (3) demonstrates that after accounting for control variables such as firm size and debt ratio, the CETP still positively impacts corporate ESG performance significantly at the 5% level. The existing literature generally finds that the pilot carbon emission trading policy significantly improves corporate ESG performance (Kong et al., 2024; Zhang and Xi, 2024), and the empirical results of this paper are consistent with these findings, thereby supporting the core hypothesis H1 of this paper.

Base Regression Results.

Note. Robust standard errors in parentheses; ***, **, and * indicate significant at the 1%, 5%, and 10% levels.

After including the control variables, the positive impact of the CETP on corporate ESG performance decreases but remains significant at the 5% level. Possible explanations for this result include the Explanatory Power of Control Variables: Some effects initially attributed to the policy may be explained by other firm characteristics. For example, larger and more profitable firms have more resources to improve ESG performance (Feng et al., 2025). Combined Effects of Multiple Factors: Improvements in ESG performance may result from the combined effects of various factors, such as firm size and profitability, rather than the policy alone. The inclusion of control variables makes the estimation of the policy effect more “pure.” Potential Indirect Effects: The policy may indirectly influence ESG performance by affecting other firm characteristics. Research indicates that the CETP positively impacts corporate ESG performance by enhancing executives’ sustainability awareness, providing environmental subsidies, and fostering technological innovation.

Robustness Tests

Replacing the Dependent Variable

The Bloomberg ESG scoring system is widely recognized and extensively used internationally. To further validate the robustness of the research findings, this study follows the approach of Halbritter and Dorfleitner (2015) by substituting the Bloomberg ESG scores for the Huazheng ESG scores as the dependent variable. This metric scored on a 0 to 100 scale, differs from the HuaZheng ESG in data acquisition, evaluation methodology, and sample coverage. The substitution allows for a cross-validation of findings across distinct ESG assessment frameworks. By replacing the data source, we ensure that the conclusions do not rely on a single dataset. The post-substitution regression analysis, presented in Table 6, column (1), corroborates hypothesis H1.

Robustness Test Results.

Note. Robust standard errors in parentheses; ***, **, and * indicate significant at the 1%, 5%, and 10% levels.

PSM-Did

Due to the non-randomness of policy implementation, the motivation for voluntary participation by enterprises, the unequal distribution of policy incentives and support, and differences in internal factors of enterprises, the quality of ESG information disclosure may be affected, leading to sample self-selection bias. Therefore, this study uses a 1:4 nearest neighbor matching method and logistic regression to estimate the propensity scores (PSM) for firms participating in the CETP to control for potential biases between pilot and non-pilot firms. Table 6, column (2) displays the post-matching regression outcomes. The persistent statistical significance of the results reinforces the robust positive association between CETP implementation and corporate sustainability enhancement. This consistency across methodologies substantiates the policy’s efficacy in fostering ESG performance

Dynamic Effects

The quality of corporate ESG information disclosure may influence whether a firm participates in the CETP, not just the other way around. To better control for reverse causality, consider the policy’s lagged effects, and account for short-term fluctuations, this study regresses the core explanatory variable did with a one-period lag to enhance the robustness of causal inference. The results can be found in column (3) of Table 6. The variable didt−1 represents the results of CETP lagged by one period. The results indicate that the lagged CETP significantly impacts corporate ESG performance, consistent with previous conclusions.

Excluding Municipality Samples

In examining the CETP’s influence on corporate ESG disclosure quality, certain municipalities (Beijing, Shanghai, Chongqing, and Tianjin) present distinct attributes. These attributes encompass sample distribution, economic infrastructure, regulatory landscape, and policy execution and oversight mechanisms. Therefore, this study re-runs the regression analysis after excluding samples from these municipalities. Table 6, column (4) presents the regression outcomes, which maintain statistical significance.

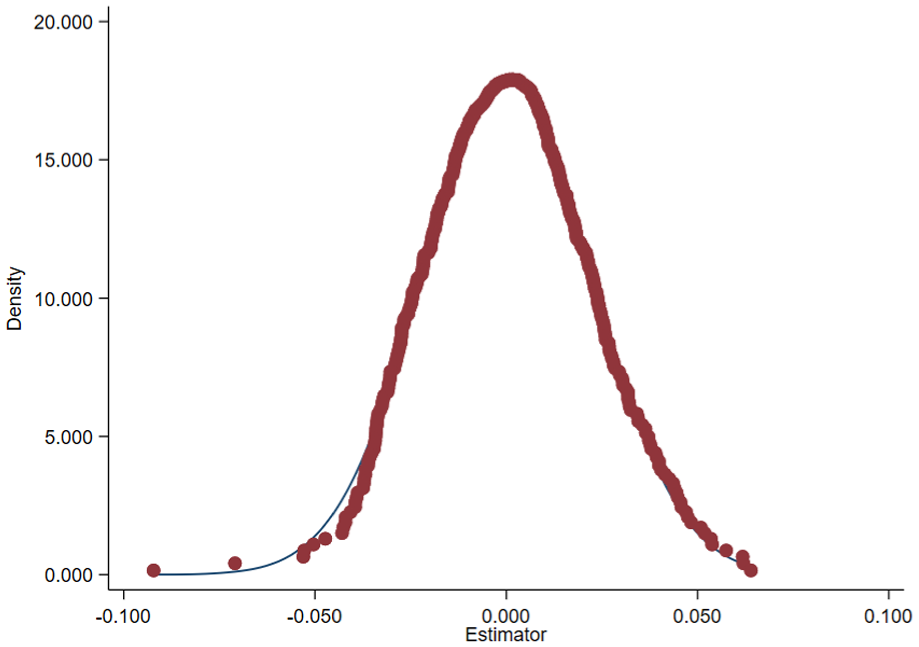

Placebo Test

Certain non-deterministic factors can often influence the statistical significance of the corporate ESG performance index. To ensure the reliability of the results, this study includes a placebo test as a robustness check by conducting 500 regression iterations to account for potential biases from uncontrolled confounding factors and model misspecification. Figure 2 shows the probability density distribution of the P-values and estimated coefficients under the placebo test method. According to Figure 2, the kernel density curve of the random estimations gradually stabilizes around 0. It approximately follows a normal distribution, indicating that the randomly generated policy time does not exhibit a policy effect. The consistent results substantiate the authentic positive influence of the CETP on corporate ESG performance. Importantly, when policy intervention is absent, other variables within the model demonstrate no statistically significant effect on ESG outcomes. In other words, the placebo test is passed, validating the robustness of the model and confirming that the CETP is indeed the primary driver of changes in corporate ESG performance.

Placebo test results.

Further Discussion

Identification of Mechanisms

Structural Equation Modeling and ACME Estimation

We estimate a linear structural equation model, setting the number of simulations for the quasi-Bayesian approximation of parameter uncertainty to 1000 iterations. The analysis reveals statistically significant positive coefficients for the CETP’s impact on both green technological innovation (InPatent) and executive green awareness (Green). These findings indicate that the policy significantly promotes green technological progress and enhances executives’ green awareness. The coefficient estimate of the CETP on corporate ESG performance remains significant, demonstrating the influential mediating roles of green technological progress and executive green awareness. Further, the mediating effects of green technological innovation and executive green awareness are also validated. Although the structural equation results have revealed the potential mechanisms by which the CETP affects corporate ESG performance, it is necessary to discuss the causal relationships involved further. Using the product of coefficients method from the linear structural equation model, we conducted ACME (Average Causal Mediation Effect), ADE (Average Direct Effect), and ATE (Average Treatment Effect) estimations, as shown in Table 7.

Mechanism Analysis Results.

Table 7 column (1) shows that the ACME (Average Causal Mediation Effect) of the CETP on corporate ESG performance through green technological innovation (InPatent) is approximately .0167, with the corresponding 95% confidence interval being above 0, confirming the existence of the mediation effect. The ADE (Average Direct Effect) and ATE (Average Treatment Effect) are approximately .1125 and .1292, respectively, with their confidence intervals also above 0. Similarly, the mediation effect of executive green awareness (Green) is validated, with an ACME of approximately .0058, ADE of approximately .0958, and ATE of approximately 0.1017, all with confidence intervals above 0. In other words, the CETP can enhance corporate ESG performance by promoting green technological innovation and executive green awareness.

The findings of this study enhance the understanding of existing literature. Chen et al. (2022) confirmed that carbon trading policies influence corporate environmental behavior through direct effects and the enhancement of innovation capabilities. This paper further identifies senior executives’ green cognition as a critical mediating mechanism, enriching the theoretical framework of how carbon trading policies affect corporate behavior. Moreover, building on Zhang et al. (2020), which verified that carbon markets promote green technological innovation in firms, this study delves into the intrinsic mechanism by which innovation capabilities are translated into ESG practices, providing a new perspective for understanding the effectiveness of policy implementation.

Sensitivity Analysis

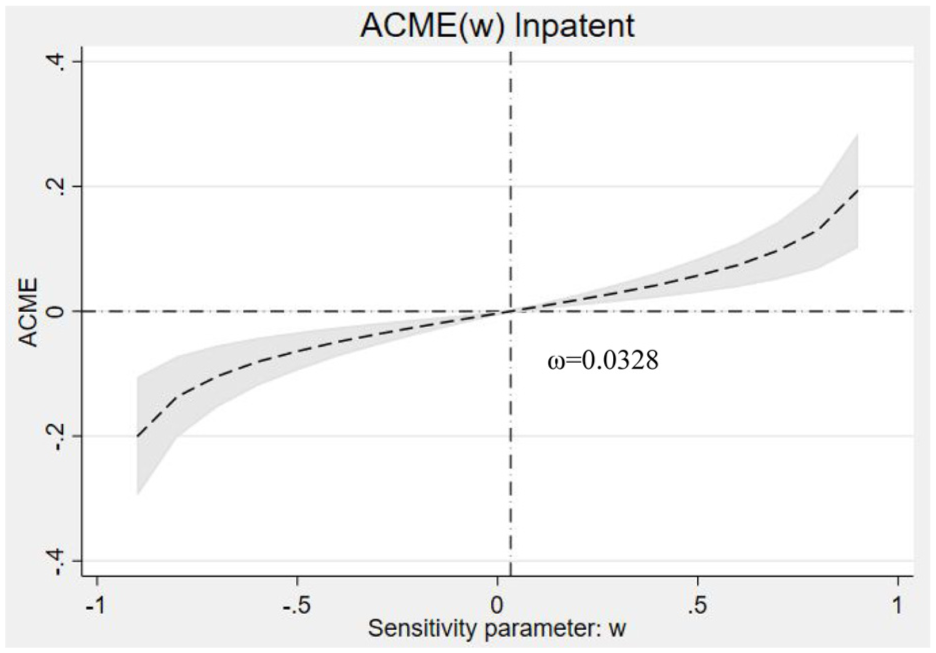

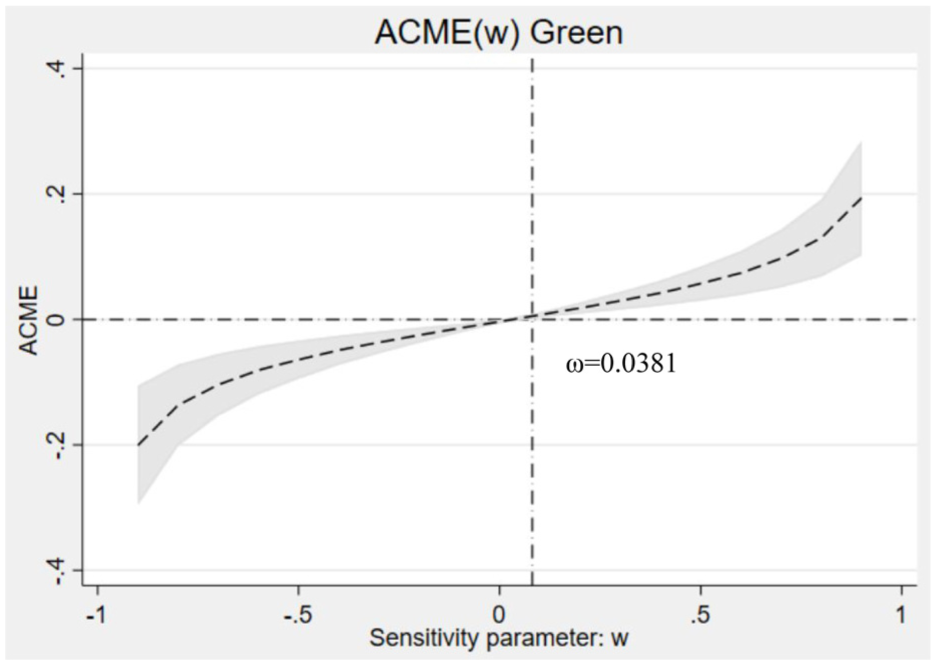

To avoid a series of estimation bias issues caused by the ignorability assumption of the mediator variable, which could confuse the estimation of ACME with potential unobserved influencing mechanisms, leading to results that deviate from reality, we conducted an in-depth sensitivity analysis. Assuming sequential ignorability, we modified the sensitivity parameter ω to move away from the stringent assumption that ω equals zero. Using our established model’s framework, We recalculated the ACME under non-zero correlation conditions. Figure 3 shows the sensitivity test results for green technological innovation (InPatent). The solid line represents the average causal mediation effect, while the shaded area represents the 95% confidence interval obtained through bootstrapping. The sensitivity analysis reports the relationship between ACME and ω. As long as the value ω does not exceed the specific threshold of .0328, the direction of ACME remains stable. Analysis using the structural equation model reveals that the adjusted R2 value stands at .077, while the error term’s coefficient of determination is .922. When ACME equals zero, it suggests that the variance of the confounding factor is at least .0328 times that of the error term. Multiplying by the coefficient of determination reveals that unobserved confounding factors contribute .035 to the total model variance. Given the inclusion of 9 control variables in this study, multiplying this figure by 9 results in .315, substantially surpassing the adjusted R2 value. However, no confounding factor with such high explanatory power exists, which somewhat supports the ignorability assumption of the mediator variable. Therefore, the mediation mechanism of green technological innovation (InPatent) is valid. Using the same method, we find that the executive green awareness (Green) mediation mechanism is also valid (Figure 4).

Sensitivity analysis of green technological innovation.

Sensitivity analysis of executive green awareness.

The results of the sensitivity analysis indicate that, after accounting for potential unobserved confounding factors, the mediating effects of the carbon emission trading pilot policy on corporate ESG performance through two channels—green technological innovation and executives' green cognition—remain significant. This robust finding aligns with several economic theories. It supports the Porter Hypothesis regarding the role of environmental regulations in promoting corporate innovation (Porter and van der Linde, 1995), demonstrating the effectiveness of market-based environmental policies in stimulating firms' intrinsic innovation capabilities. Additionally, it corroborates the upper-echelon theory on the influence of executive cognition on corporate strategy (Hambrick and Mason, 1984), highlighting that executives' green cognition serves as a key link between policy and sustainable corporate practices. These theoretical connections further enhance the credibility of the empirical results and deepen our understanding of the policy's mechanisms.

Heterogeneity Analysis

Firm Heterogeneity Analysis

In the examination of CETP effects on corporate ESG performance, organizational characteristics and attributes emerge as potentially significant moderators of policy outcomes. This study conducts heterogeneity analysis along two key dimensions: firm size and R&D investment. Specifically, firm size may affect the ability to respond to and implement the policy, while R&D investment reflects the firm’s commitment to technological innovation and sustainable development. Therefore, analyzing heterogeneity at the firm level can reveal differences in policy effects among different firms. To deeply analyze the differences between firms of various sizes and R&D investment levels, we divided all samples into two groups based on median firm size and R&D investment values. On this basis, we conducted group regressions. After a rigorous Chow test, the results clearly show that the regression coefficients significantly differ between large and small firms and firms with high and low R&D investment. Table 8 reveals that the CETP’s regression coefficients for large enterprises exhibit positive values with statistical significance at the 1% level. In contrast, small firms do not show statistical significance under this policy. Regarding R&D investment, firms with ample R&D funding show a significant positive correlation between the CETP and ESG performance at the 1% significance level. In contrast, firms with low R&D investment do not exhibit a considerable policy effect.

Results of Firm Heterogeneity Analysis.

Note. Robust standard errors in parentheses; ***, **, and * indicate significant at the 1%, 5%, and 10% levels.

The possible explanations for this result are as follows: From the perspective of scale heterogeneity, large enterprises, equipped with substantial financial resources, advanced technologies, and efficient management experience, are able to quickly update emission reduction technologies and equipment, effectively addressing the cost pressures of carbon trading. Additionally, the advantages of large firms in supply chain management and market influence facilitate the involvement of upstream and downstream enterprises in carbon emission reduction, thereby enhancing their ESG performance. This is consistent with the findings of Wang and Zhang (2022), who found that large firms are more active in carbon markets. From the perspective of R&D investment heterogeneity, firms with high R&D investments typically possess strong technological innovation capabilities, enabling them to independently develop or adopt cutting-edge emission reduction technologies. Through technological innovation, these firms achieve higher energy efficiency and lower carbon emissions, which aligns with the conclusion of Bai et al. (2019) that R&D investment is a key driver of technological progress.

Regional Heterogeneity Analysis

To investigate the impact of regional heterogeneity on policy effects in greater depth, this paper analyzes three dimensions: new energy pilot cities, local officials' promotion cycles, and economic development levels. As key areas for policy implementation, new energy pilot cities possess significant advantages in terms of policy support, resource allocation, and technological innovation. This study categorizes these cities based on the list of new energy demonstration cities released by the National Energy Administration in 2014. The promotion cycle of local government leaders may also affect the intensity of policy implementation. To address this, we cross-validate using multiple sources, gathering data on municipal leadership after 2011, and define leaders aged between 50 and 55 as being in a critical promotion period. Moreover, economic development level is an important regional characteristic that influences policy effectiveness. The study divides the sample into two groups based on the median per capita GDP of each region during the sample period, representing high and low levels of economic development. The regression results in Table 9 show the following: In new energy pilot cities, carbon trading policies are significantly positively correlated with ESG performance at the 1% level, while the correlation is not significant in non-pilot cities. When local officials are in a critical promotion period, the policy effect is significantly positive at the 1% level, while in non-critical periods, the effect is not significant. In regions with high economic development levels, the policy effect coefficient is .071 (significant at the 10% level), while in low-development regions, the coefficient is −.015 and not significant.

Results of the Analysis of Regional Heterogeneity.

Note. Robust standard errors in parentheses; ***, **, and * indicate significant at the 1%, 5%, and 10% levels.

Possible explanations for these results are as follows: From a regional perspective, enterprises in new energy demonstration areas benefit from more abundant policy incentives and resource support, significantly reducing the economic costs of green transformation. This finding is consistent with Zhao et al. (2024), who argue that the greatest green innovation effect of policies is reflected in patents related to low-carbon, energy-saving, and alternative energy technologies. From a political incentive perspective, local officials in critical promotion periods are more likely to prioritize achievements in environmental governance. The government's active signals guide enterprises to accelerate their green transformation, and through positive interactions, attract environmental investment, creating a positive feedback loop between policy promotion and corporate response. This finding supports the assertion of Yu et al. (2023) that local officials' promotion period is a significant factor influencing the spillover effects of carbon market policies. From an economic development perspective, regional differences highlight the importance of market mechanism maturity and the endowment of innovation resources. Enterprises in economically developed areas, with stronger financial capabilities and environmental governance capacities, can more effectively convert policy pressure into motivation for ESG improvement. This corroborates Pei et al. (2018), who found that socioeconomic factors have a significant positive impact on carbon emissions.

Conclusion and Policy Implications

This study employs a multi-period difference-in-differences framework to examine the impact of the CETP on corporate ESG performance in China. Drawing on microdata from A-share listed firms spanning 2011-2020, our analysis yields several vital findings: Firstly, CETP significantly positively impacts corporate ESG performance. Empirical results show that key regulated enterprises participating in the carbon emission trading pilot have significantly higher ESG scores than non-pilot firms. This conclusion remains robust after multiple robustness tests (including replacing the dependent variable, PSM-DID estimation, considering policy lag effects, excluding municipal samples, etc.), and it passes the parallel trend assumption test and placebo test, strongly confirming the positive impact of the carbon trading policy on corporate sustainable development practices. Secondly, based on structural equation modeling and causal mediation analysis, this paper reveals that green technological innovation and executive green awareness are vital pathways through which the CETP enhances ESG performance, and both can simultaneously promote the ESG performance of firms in pilot regions. Sensitivity analysis further verifies the robustness of these two mediation effects, ruling out potential unobserved confounding factors. Finally, the heterogeneity analysis reveals significant firm- and region-level differences in policy effects: firms with larger scale and higher R&D investment exhibit more pronounced improvements in ESG performance; the policy effects are also stronger in pilot cities for renewable energy, regions with local leaders in critical promotion periods, and economically developed areas. Drawing from these findings, we propose the following policy recommendations:

Improve Carbon Market Mechanisms and Strengthen Policy Guidance: Firstly, to maximize the positive impact of the carbon trading policy on corporate ESG performance, policymakers should consider further improving the carbon market construction, gradually incorporating more industries into the national carbon market, and expanding policy coverage. Optimizing the quota allocation mechanism, improving carbon quota allocation methods, and enhancing the carbon market regulatory system with strengthened information disclosure are crucial steps.

Secondly, Increase Support for Innovation and Promote Green Technology Development: Given that Low-carbon technology innovation is an important mediating mechanism through which the carbon trading policy affects corporate ESG performance, it is recommended to increase fiscal support for corporate green technology R&D, improve intellectual property protection for green technological innovation, and develop differentiated innovation support policies, especially to strengthen innovation support for small and medium-sized enterprises. These measures can stimulate corporate green technological innovation vitality and drive continuous improvements in ESG practices.

Thirdly, Optimize Policy Implementation Environment and Consider Regional Differences: Tailoring carbon trading policy implementation plans to local characteristics, incorporating carbon reduction and corporate ESG performance into regional development assessment frameworks, strengthening policy coordination across regions, promoting global interconnection of carbon markets, and increasing policy support and technical assistance to less developed areas can enhance the precision and effectiveness of the carbon trading policy, maximizing its impact on corporate ESG performance.

Although this paper delves deeply into the mechanisms through which the Carbon Emission Trading Pilot Policy (CETP) affects corporate ESG performance, several limitations remain: (a) Data Dimension: The study sample is limited to A-share listed companies, excluding the large number of unlisted firms, which may affect the external validity of the findings. Furthermore, due to data availability constraints, micro-level environmental management data, such as firms’ investments in emission reduction technologies and upgrades to environmental protection equipment, were not accessible, leaving room for future research to address these gaps. (b) Methodological Aspect: While the use of the PSM-DID approach helps mitigate endogeneity concerns, this method only accounts for selection bias from observable variables and cannot fully eliminate the influence of unobservable factors. Additionally, the interaction effects between the CETP policy and other regional environmental policies may not be entirely disentangled, posing further challenges to causal identification.

Footnotes

Ethical Considerations

This study did not involve animals or human subjects. The analysis is based entirely on publicly available data.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the National Natural Science Foundation of China (No. 72172113).

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The data supporting the findings of this study are available from the author upon request.