Abstract

Enterprises’ varied motivations for pursuing green technology innovation (GI) might lead to varying economic and societal outcomes from their creative endeavors. This study employs data of A-share listed firms from 2009 to 2021 and a high-dimensional fixed effect model to explore how ESG rating drives enterprises’ motivations for engaging in GI. The empirical research shows that ESG rating stimulates enterprises to conduct both substantive green technology innovation (SUGI) and strategic green technology innovation (STGI). These findings hold throughout the robustness test. We also employ instrumental variable method and differences-in-differences method for endogeneity test. According to the heterogeneity analysis, the outcomes are more significant for the state-owned, growth stage and patent-intensive enterprises. In the moderating effect analysis, we find multidimensional external attention can make for differences in the impact of ESG rating on SUGI and STGI. External attention from analysts, the media, and investors can positively moderate the influence of ESG rating on enterprises’ motivation for SUGI. The influence of ESG rating on STGI in enterprises is positively moderated by investor attention, but it cannot be moderated by analyst or media attention. That is, external attention from analysts and the media can prevent enterprises from falling into formalism and enable them to leverage the motivating effect of ESG rating on SUGI. Investor attention is a point for further promoting corporate SUGI. This study gives an alternative perspective for the promotion of ESG rating and GI in China.

Keywords

Introduction

Enterprises should consider economic concerns as well as how their operations affect the environment and society (Coleman et al., 2010). The environmental, social, and governance (ESG) concept, which advocates environmental friendliness, social responsibility fulfilment, and governance improvement, is one of the standards used to measure enterprise sustainable development (Velte, 2017). Green technology innovation (GI), as a driver integrates green development and technology innovation, is also intricately linked to ESG (Xu et al., 2022), and holds potential to improve resource utilization efficiency, reduce environmental pollution (Amore & Bennedsen, 2016; Rennings, 2000), and drive enterprises to achieve sustainable development (Huang & Li, 2017). Worldwide, enterprises are representatives of not only economic development but also major disruptors of the ecological environment. Engagement in GI can enable enterprises to generate significant positive externalities for the environment and society while enhancing own competitiveness (Horbach, 2008). At this point, some questions may arise: Are the motivations of enterprises toward engaging in GI pure? Is such engagement a strategic behavior for obtaining policy support and securing compliance with regulatory requirements? Further research is required to respond to these questions, as well as to explore whether ESG rating can mitigate the “formalism” in GI.

Some studies have demonstrated that ESG rating, as a soft market supervision, may help enterprises come up with new green technologies (Chang & Wang, 2024; J. Wang et al., 2023; Z. Wang & Chu, 2024). Still, there is some variance on the evidence regarding the benefits of ESG rating for GI in enterprises. Since the level of investment which includes large amounts of funds, human resources, and other types of resources required for establishing system to quantify, aggregate, and disclose ESG information is very high (Hermalin & Weisbach, 2012). The costs of information manufacturing, transmission, and exclusivity generated by ESG disclosure will drain resources away from other projects (F. Zhang et al., 2020). However, there is literature supporting that ESG rating can make GI shift from a strategic to a substantive process in enterprises (Z. Zhang et al., 2024). Despite some variances in the findings of these cited studies owing to differential research perspectives, the general trend is that ESG can substantially encourage GI in enterprises. It seems that the cited research did not take into account the fact that ESG rating could have different effects depending on whether green innovation activities is for strategic or substantive purpose.

Conceptually, high ESG ratings signify sustainable development; however, can these ratings effectively incentivize enterprises to pursue substantive green technology innovation, or will they only act as a catalyst for strategic speculation? We believe that motivation differences across enterprises as to why they engage in GI may result in their innovative efforts having different economic and social effects. For instance, given the uncertainty surrounding innovation activities, managers may be more willing to invest in less-risky strategic activities to maximize own interests (Y. Chen et al., 2012). This underscores the need for more research on the potential of ESG rating to enhance companies’ propensity to pursue substantive green technology innovation. Previous studies seemingly overlooked the underlying mechanism, which can result in differences between the impact of ESG rating on substantive green technology innovation (SUGI) and that on strategic green technology innovation (STGI). This research aims at examining how ESG rating affects enterprises’ motivation for SUGI and STGI from multidimensional external attention perspectives.

Our findings enrich the literatures on ESG and GI by introducing multidimensional external attention as moderating variable. It categorizes firms’ motivation for GI into substantive and strategic dimensions to assess if ESG ratings incentivize enterprises to pursue GI for substantive objectives. Furthermore, this study delves into the moderating role of multidimensional external attention in substantive and strategic purposes respectively, delivering related findings that may be fruitful for the development of targeted interventions aimed at promoting SUGI.

Literature Review and Research Hypotheses

ESG Rating and Green Technology Innovation

According to stakeholder theory, enterprises must maintain stakeholders’ interests while pursuing value and benefit maximization to obtain comprehensive support for achieving sustainable development (Freeman, 1984). The ecological damage and environmental pollution produced as enterprises develop tend to have negative impacts on society; similarly, an image characterized by a lack of social responsibility and imperfect corporate governance can hamper enterprise value, which in turn harms the interests of shareholders. In this context, ESG rating appears as an indicator that can improve enterprise information transparency, and reduce the costs associated with the process of collecting information meant for alleviating information asymmetry for external stakeholders. F. Zhang et al. (2020) asserted that adherence to ESG principles can guide enterprises to secure environment-friendly development and encourage application of GI, which in turn can smoothen external stakeholder communication to acquire the funding supports. Stakeholder expectations for ESG performance might compel firms to pursue GI and limit managerial speculative tendencies. Simultaneously, enterprise’s ESG performance can affect consumers’ green purchase intention, which then promotes GI (Tao et al., 2022). ESG rating has become an important pathway to promote GI effectively, hereby enhance enterprise’s enduring value (Bai et al., 2024).

Gregory et al. (2014) indicated that enterprises with high ESG ratings have more effective supervisions over own human capital and innovative management, which can lead to more effective resource integration and enhance innovative competitiveness. This may explain why enterprises rely on resources to survive and develop according to resource dependency theory (Pfeffer & Salancik, 1978). ESG is one metric used to assess an enterprise’s performance in sustainable development, and GI is a major factor behind enterprise sustainable development (Rajesh, 2020). High ESG ratings send signals to society that the enterprise attaches importance to ESG-related topics in the light of signaling theory (Spence, 1974), which in turn facilitates the acquisition of resources from stakeholders for enterprises to continue improving their GI performance.

According to earlier research, by enhancing the external information environment, ESG rating can reduce managers’ shortsighted behavior, boost research and development (R&D) investment, ease corporate financing constraints, and promote risk-taking, thereby achieving GI (Chang & Wang, 2024; Long et al., 2023; J. Wang et al., 2023; Zhou et al., 2023). As research on innovative activities advances, experts are increasingly focusing on the quality of innovation rather than merely its quantity (Lahiri, 2010). There are some studies divided innovation activities into exploratory and exploitative innovation (C. T. Chen et al., 2024; Khan et al., 2021), while others classify it as substantive and strategic innovation (L. Chen et al., 2023; Tong et al., 2014) to value the innovation quality. Bai et al. (2024) observed that ESG ratings affect substantive and strategic innovation through different mechanisms. Classifying GI as substantive and strategic may more accurately represent the underlying motivations of enterprises to engage in innovation activities. SUGI refers to innovative behavior characterized by highly-advanced technological content and more difficulties, and behavior that can substantially promote green technological progress and competitive advantages for enterprises. While, STGI refers to a formal innovative behavior characterized by more regular technological contents and less difficulties, and that can enable companies to obtain policy support for increasing green innovation project quantity and pace (L. Chen et al., 2023; Dosi et al., 2006; Hall & Harhoff, 2012). Some scholars believe that only SUGI can enable firms to reach sustainable development, and ESG rating can facilitate the transition toward SUGI (D. Zhang et al., 2019; Z. Zhang et al., 2024). In light of the aforementioned points of view, this investigation examines Hypothesis 1. The proof of this hypothesis provides empirical evidence for policymakers to promote ESG ratings.

SUGI focuses on transformative innovation in products and technologies, and long-term benefits. It follows that substantive innovation requires huge capital investments and is accompanied by higher level of risk and uncertainty. While, STGI focuses on simple improvements in existing products and technologies along with short-term benefits. Therefore, engaging in SUGI tends to be more difficult than engaging in the strategic counterpart, which may lead enterprises to be unwilling and unmotivated to carry out substantive innovation projects. Managers may prioritize investment in STGI to realize short-term achievements (He & Tian, 2013). Indeed, Y. Chen et al. (2012) showcased that to maximize their interests, managers are usually willing or motivated to “divert” R&D subsidies from SUGI activities, which hold high risks and uncertainties, to STGI activities, which hold lower risks and have more certainties. However, the engagement in STGI does not lead to substantive improvements in the green technological competitiveness of enterprises, and rather leads to the “patent bubble” phenomenon. Tong et al. (2014) observed that, within state-owned enterprises in China, the quantity of utility model and design patents rose following the second revision of “Chinese Patent Law.” However, innovation patent counts stagnated, implying neglect toward patent quality. In conclusion, the effectiveness of ESG ratings for enhancing GI may be “formalistic”; hence, Hypothesis 2 is proposed.

ESG Rating, External Attention and Green Technology Innovation

Institutional investors, digital transformation, corporate governance frameworks, and market competitiveness were some of the mediating variables in earlier research on the ESG rating and GI relationship. (Chang & Wang, 2024; Long et al., 2023; H. Wang et al., 2024). Our research focuses on the moderating role of external attention as a means to optimize ESG systems and attain sustainable innovation and development over the long run. The attention placed on enterprises by external sources has been constantly strengthening in recent years. This has been leading enterprises to invest a substantial amount of their resources obtained through ESG performance in GI, curbing managers’ short-sighted behaviors, and generating governance effects on GI. Research indicates that increased intensity of external supervision correlates with a higher probability of enterprise regulation (Snyder & Strömberg, 2010). Furthermore, as enterprises face criticism from various stakeholders, they are increasingly prioritizing environmental preservation and the execution of green growth strategies to cultivate their sustainable development image (Kathuria, 2007). In the capital market, the parties that can exert pressure on enterprises include analysts, the media, and investors.

Analyst Attention

Analysts are excavators and transmitters of corporate information, and they can reduce stakeholder-enterprise information asymmetry through direct communication with managers. They may also provide investors with information via multiple means, which serves as a significant external governance tool that restricts manager conduct and enhances investor oversight (T. Chen et al., 2015; Sun & Liu, 2016). Regarding the supervision and governance effects of analyst attention, their focus tends to be placed more on intangible assets, R&D expenditures, and other subjects related to corporate value, which in turn strengthens supervision and governance and promotes enterprise GI (He & Tian, 2013; Manso, 2011). S. Li et al. (2023) asserted that analyst attention could promote both enterprise innovation quantity and quality. Analyst attention may mitigate information asymmetry, diminish agency costs and finance constraints, and enhance an enterprise’s substantial innovation output (Guo et al., 2019). As a crucial indicator of sustainable development for enterprises, ESG-related information captivates analysts’ interest. L. Li et al. (2024) further demonstrated that there was an external regulating effect of analyst attention making ESG performance to qualify corporate GI. Analysts can exert pressure on enterprises through data tracking and interpretation on ESG, which thereby further promotes both SUGI and STGI. Consequently, we put up Hypothesis 3 and Hypothesis 4 as proposals.

Media Attention

The media is an external stakeholder that can partake in corporate governance through influencing external supervision mechanisms and public opinion (Dyck et al., 2008; Gillan, 2006). Specifically, signaling theory holds that media attention and reporting can serve as an “information intermediary,” effectively alleviating information asymmetry in the capital market by affording stakeholders information about enterprises and facilitating favorable stakeholder responses (Mitra et al., 2017). Research indeed shows that an increase in media coverage make enterprises face more public pressure, thereby effectively enhancing their awareness over the importance of environmental protection, and urging them to take related actions (Ahern & Sosyura, 2015). ESG ratings can help enterprises maintain a good reputation and social image through media, hereby attracting consumers and other stakeholders to the capital market (Mullainathan & Shleifer, 2005). With the media’s attention over an enterprise, its willingness to engage in SUGI may increase accordingly in the light of information effects of media attention; while, the pressure effects of external attention may increase managers’ short-term operational pressure, thereby engaging in STGI as well (Guo et al., 2019). Therefore, we propose Hypotheses 5 and 6 to study how media attention affects the influence of ESG rating on SUGI and STGI.

Investor Attention

As the notion of sustainable development evolves, ESG has gained significance in investment choices, consequently capturing the interest of retail investors and encouraging enterprises to bolster their sense of responsibility and consistently better their ESG performance. Investor attention is the driving force of GI under environmental regulations (Liu et al., 2025). Hirshleifer et al. (2011) mentioned that investor attention reduces information asymmetry and accelerates information flow. Retail investors can promote corporate innovation activity transparency through promoting information transmission and supervisory governance, as well as make the valuation of innovation projects more reasonable, in turn fostering corporate GI (Manso, 2011). Compared with professional investors, most retail investors lack professional and financial knowledge and have only a single channel to obtain information on enterprises (Yang et al., 2025). Retail investors have limited time to interpret the highly professional ESG related information. Therefore, they are unable to discern the motivation behind corporate GI. Thus, it is possible that SUGI and STGI will benefit from retail investors’ focus. Hypothesis 7 and Hypothesis 8 are based on the arguments given above.

Methodology and Data

Methodology

Based on the hypotheses presented before, this paper establishes the following models to investigate whether ESG rating motivates companies to engage in SUGI and STGI (L. Chen et al., 2023; Y. Li & Li, 2024; Z. Wang & Chu, 2024; Z. Zhang et al., 2024):

where, i, t, and ind denote company, year, and industry, respectively;

For the analysis of the underlying mechanisms of the studied effects, this article employs moderating variables and constructs the following model:

where,

Variables

Explained Variable

Patent applications reflect the willingness of enterprises to participate in GI, with invention patents likely impacting enterprise performance from the outset of the application process. Furthermore, the patent application date, which reflects the current level of GI of an enterprise, provides more accuracy than the grant date. Therefore, following prior research (Dosi et al., 2006; Hall & Harhoff, 2012; Tong et al., 2014), this study uses the number of patent applications to measure enterprise GI.

As aforementioned, this study divides GI according to the enterprise’s motivation to engage in such innovation (i.e., substantive or strategic). In general, invention patents contain more advanced technology than utility model and design patents. Thus, and referring to the approach of Berrone et al. (2013) and L. Chen et al. (2023), we use “the number of green invention patent applications” to measure SUGI, and “the number of green utility model and design patent applications” to measure STGI.

Additionally, to test the actual GI capabilities of enterprises, this study employs data from independent green patent applications. To rectify the right-skewed distribution of data, 1 is added to the number of applications, followed by a computation of the natural logarithm.

Explanatory Variables

The Sino-Securities Index ESG rating is utilized due to its extensive data, comprehensive Chinese market coverage, and close fit with China’s local institutional context. It categorizes listed companies as “C, CC, CCC, B, BB, A, AA, or AAA.” This study follows Lin et al.'s (2021) approach, assigning ratings ranging from 1 to 9, and measures ESG rating based on the average rating of a given year.

Control Variables

The model incorporates control variables such as firm age (Age), firm size (Size), leverage ratio (Lev), return on assets (ROA), sustainable growth rate (SGR), CEO duality (DU), ownership concentration (Top1), and the proportion of independent directors (IDR). These variables reflect the basic situation, financial status, and governance level of an enterprise (L. Chen et al., 2023; Y. Li & Li, 2024; Tong et al., 2014; F. Zhang et al., 2020).

Moderating Variables

Considering the supervisory role of external attention, this study analyzes the mechanism of analyst, media, and investor attention (Kim & Zhang, 2014; Yang et al., 2025). Table 1 defines all variables.

Definition of Variables.

Data Sources

The Sino-Securities Index ESG rating started from 2009 and covers all A-share listed companies currently. Thus, this study selects data of A-share listed companies in China from 2009 to 2021 as the sample. Patents, media and investor attention data are sourced from “China Research Data Service Platform (CNRDS).” ESG rating is sourced from “Wind” database. The remaining data are obtained from “China Stock Market & Accounting Research (CSMAR).”

To secure data accuracy, we process it as follows: (1) exclude enterprises in the financial industry; (2) exclude ST, *ST, and PT enterprises in the given year; (3) exclude newly-established companies in the given year; (4) remove samples with missing and abnormal data. Finally, we obtain unbalanced panel data with 22,091 observations from 4,391 companies. To alleviate the problem of heteroscedasticity, we take the natural logarithms of non-ratio, continuous variables. A 1% truncation is implemented on continuous variables to mitigate the impact of extreme values.

Empirical Results

Descriptive Statistics of Variables

Table 2 presents the descriptive statistics of main variables. The average SUGI is 0.554, just above STGI at 0.546. The mean ESG rating is 4.266, indicating potential for improvement in ESG performance among listed enterprises in China. For control variables, the minimum and maximum firm age are 1.000 and 63.000 respectively, and the minimum and maximum firm size are 19.630 and 26.390 respectively. These numbers indicate that the sample includes enterprises of different ages and sizes. All other variables are within reasonable ranges.

Descriptive Statistics of Variables.

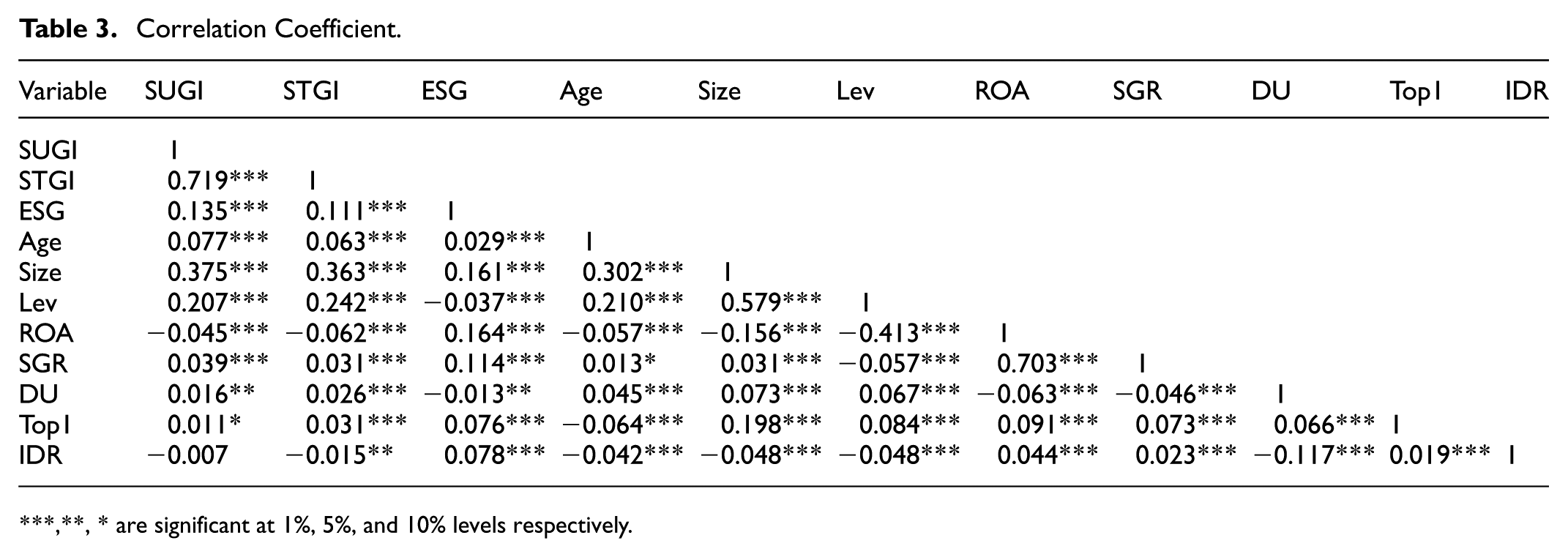

Pearson correlation coefficient tests show that the independent variable is significantly correlated with the dependent variable at the 1% level (Table 3). The variance inflation factor values are all less than 5, with a maximum of 4.73 and an average of 1.99, indicating no serious multicollinearity problem in the data.

Correlation Coefficient.

,**, * are significant at 1%, 5%, and 10% levels respectively.

Benchmark Regression

Benchmark regressions use Models (1) and (2) to examine how ESG ratings affect SUGI and STGI in enterprises, with findings shown in Table 4. Columns (1) and (3) demonstrate significantly positive coefficients for ESG influencing SUGI and STGI at the 1% level. Although the coefficients reduced after control factors were included, the overall results remained the same and were significant at the 1% level (columns (2) and (4)).

Benchmark Regression Results.

Note. t statistics in parentheses.

p < .1. **p < .05. ***p < .01.

The results verify both Hypothesis 1 and 2. This agrees with what was found in the research by Z. Zhang et al. (2024), which found that ESG ratings had a greater impact on SUGI than on STGI. This suggests that ESG rating can help enterprises change their motivations for engagement in GI from strategic to substantive. However, STGI still exists, and the absence of supervision may make shortsighted managers more willing to promote this type of innovation. This is why we investigate the supervisory influence of external attention on the incentive for engagement in GI in further mechanism analysis.

According to the coefficients of the control variables, companies with shorter establishment times are more willing to conduct STGI. Furthermore, firm size, leverage ratio, ROA, and sustainable growth rate positively affect both SUGI and STGI. However, the variables that reflect corporate governance, including CEO duality, ownership concentration, and proportion of independent directors, do not play significant roles in our model.

Endogeneity Analysis

We have employed high-dimensional fixed-effects in benchmark regression. To make the results above convincing, we further use instrumental variable (IV) approach and differences-in-differences (DID) method to avoid endogeneity concerns, including bidirectional causality, omitted variables, and sample selection biases.

Instrumental Variable

We use the average ESG ratings of other listed companies in the same province for the same year as IV (Lian & Weng, 2024). The average ESG ratings of other companies is correlated with ESG rating of the target company, as they are influenced by similar regional policies, public opinions, and market pressures. Moreover, ESG ratings of other companies do not directly affected GI of the target company. Thus, this IV is exogenous. The outcomes shown in Table 5 indicate that IV positively affects both SUGI and STGI, which align with the benchmark outcomes.

Instrumental Variable Regression Results.

p < .01.

Differences-in-Differences

This study also takes the first disclosure of ESG rating as a quasi-natural experiment, and uses the multi-time-point DID method to test the impact of the first disclosure of SynTao Green Finance ESG rating on SUGI and STGI. This addresses the potential endogeneity concerns in this impact (Chang & Wang, 2024). If SynTao Green Finance released its ESG rating in the given year, ESG_DID is 1; otherwise, it is 0. Columns (1) and (2) of Table 6 show the DID regression results, indicating that ESG rating disclosure significantly increased both SUGI and STGI at the 1% level. Furthermore, it had a stronger incentive effect on SUGI than that on STGI. This finding aligns with the benchmark regression outcomes.

Differences-in-Differences and Subsample Regression Results.

p < .01.

Robustness Tests

Alternative Sample

In the year 2020 to 2021, economy was affected by COVID-19 in China, which had a negative impact on market participants (Habibi et al., 2022). Therefore, we exclude data from 2020 to 2021 to avoid the impact of COVID-19. Columns (3) and (4) in Table 6 depict that ESG rating encourages both SUGI and STGI, and that ESG coefficients are considerably positive at the 1% level. Using a subsample did not change the findings, suggesting that SUGI is more strongly influenced by ESG ratings.

Alternative Variables

We also conduct robustness tests by replacing key variables. First, the explanatory variable is replaced by the Sino-Securities Index ESG score (ESG_score). Second, the quantity of green patents that two or more businesses jointly apply for may also be an indicator of how motivated and capable these businesses are to participate in GI. Consequently, SUGI and STGI are replaced with SUGI2 and STGI2 which encompass both independent and joint patent applications for the given year. The regression results are presented in Table 7. The coefficients of ESG have altered in comparison to the baseline regression; yet, the robustness of the primary conclusions is reaffirmed.

Regression Results Using Alternative Variables.

p < .01.

Persistent Effect

Since ESG rating may have a sustained effect on enterprise GI that might not be apparent immediately, this paper pushes SUGI and STGI forward by 1 and 2 periods (He & Tian, 2013). Table 8 presents that ESG ratings have the greatest promoting effect on SUGI at period t + 1, followed by its impact at t period. Meanwhile, ESG rating promotes STGI the greatest at period t, and then the influence decreases over time. A potential explanation here is that engaging in green invention patents requires more time than in green utility model patents.

Persistent Effect Regression Results.

p < .01.

Heterogeneity Analysis

State-Owned Enterprises

Chinese state-owned enterprises (SOEs) possess advantages in resource accessibility due to their economic and political attributes; however, they also encounter increased social responsibilities. The attributes of property rights in enterprises may affect the relationship between ESG and GI due to social responsibilities. Therefore, we use grouped regression to test the heterogeneous influence of property rights attributes on the impact of ESG rating on SUGI and STGI.

The results shown in Table 9 can be summarized in two aspects. Within SOEs, ESG ratings have a greater incentive effect on SUGI than STGI. Among non-SOEs, there is no notable difference in the incentive effects of ESG ratings. Additionally, the positive effect of ESG ratings on SUGI is more significant in SOEs, compared with that in non-SOEs. Conversely, the incentive effects of ESG ratings on STGI are more prominent in non-SOEs. These outcomes may owe to external market pressure, which makes non-SOEs more prone to managerial myopia, thereby affecting their R&D investment and technology innovation output (Cadman & Sunder, 2014; Kraft et al., 2018). Due to the economic and political characteristics of SOEs that provide them with abundant external resources and greater external pressure, ESG disclosure may promote SUGI better than STGI in state-owned contexts.

Heterogeneity Analysis by State-Owned Enterprises.

p < .01.

Enterprise Lifecycle

Since enterprise lifecycle influences development strategies and R&D capabilities, enterprises may also show a divergent willingness to engage in and level of innovation according to the lifecycle (Agarwal & Gort, 2002; Miller & Friesen, 1984). This research employs Dickinson's (2011) cash flow model to categorize a company’s lifetime into three phases (growth, maturity, and decline) based on “the positive and negative conditions of net operating cash flow, net investment cash flow, and net financing cash flow.”

Table 10 demonstrates that ESG ratings significantly positively influence both SUGI and STGI in all three stages at the 1% level. Still, the effects at the growth stage are greater than that at the other two stages. Additionally, ESG ratings have a greater incentive effect on SUGI at the growth and maturity stages, whereas the incentive effect is greater on STGI at the decline stage.

Heterogeneity Analysis by Enterprise Lifecycle.

p < .01.

Patent-Intensive Industries

Industry characteristics suggest different developmental strategies and constraints. We analyze heterogeneity based on the classification of an enterprise as belonging to a patent-intensive industry. The categorization of patent- and non-patent-intensive industries is derived from the “Statistical Classification of Intellectual Property (patent)-intensive industries (2019)” published by the National Bureau of Statistics of China. The results presented in Table 11 indicate that the impact of ESG ratings on green innovation is more significant in industries characterized by a high intensity of patents. In patent-intensive industries, the coefficient of ESG ratings on SUGI goes above that on STGI. By contrast, formalism occurs in the promotion of GI by ESG rating in non-patent-intensive industries.

Heterogeneity Analysis by Patent-Intensive Industries.

p < .01.

Mechanism Analysis

The motivation of enterprises for engaging in GI may be influenced by external attention (Haack & Schoeneborn, 2015; Yang et al., 2025; Zhu et al., 2020). Accordingly, there is the need to further examine whether ESG rating can motivate enterprises to engage in SUGI or STGI as they are under the scrutiny of external supervision. This section explores the supervisory role that external attention plays in the effect of ESG rating on engagement in GI from three perspectives, namely analyst, media, and investor attention.

Analyst Attention

Analysts can often serve as bridges to reduce information asymmetry between investors and enterprises. Their professional analysis and disclosure can constrain the speculative behavior of companies, in turn potentially helping curb managers’ shortsighted behavior such as focusing on SUGI over STGI. This study uses the number of analysts tracking and analyzing a company in the given year (analysts) to measure analyst attention. Table 12 shows the regression results, with columns (1) and (2) demonstrating that analyst attention positively moderates the influence of ESG rating on SUGI, while this moderating role does not occur for the strategic counterpart. Therefore, Hypothesis 3 is accepted and Hypothesis 4 is rejected. Analyst attention may mitigate the extent of information asymmetry between stakeholders and enterprises and bring to the fore more pressure and supervision, thereby correcting speculative behaviors such as short-sighted strategic innovation. This conveys positive signals to stakeholders regarding the enterprises’ engagement in GI, and encourages them to achieve substantive innovation (Haack & Schoeneborn, 2015).

Moderating Effects of External Attention.

p < .1. ***p < .01.

Media Attention

Various studies have discussed the external supervision role of media attention, where the higher the media attention, the more transparent the ESG disclosure information, and subsequently a potential more effective reduction in information asymmetry between external stakeholders and the enterprise. This study uses the total number of news articles from newspapers, financial news, and online news that mentioned an enterprise in the given year to measure media attention. Table 12 presents the outcomes in columns (3) and (4), confirming Hypothesis 5 and refuting Hypothesis 6. Media attention can enhance the impact of ESG rating on SUGI, but not on STGI. These findings resemble those in the study by Zhu et al. (2020), whereby an increase in media coverage increased enterprise external pressure and thereafter promoted improvements in SUGI.

Investor Attention

With increased investor awareness of sustainability, ESG performance has received greater attention, raising the limitations and oversight of management’s innovation activities. According to Yang et al. (2025), we employ “the total number of investor inquiries received on the interactive platform of stock exchanges” as a proxy variable of investor attention. Since the rapid development of the Internet, increasing retail investors ask questions to A-share listed enterprises through the “Interactive Easy platform of Shenzhen Stock Exchange” and the “E-Interaction platform of Shanghai Stock Exchange” to obtain information, thus forming certain external supervision pressure on enterprises. Compared to traditional information channels, investors can actively ask questions on interactive platforms, reflecting the attention of individual investors to enterprises. Columns (5) and (6) of Table 12 demonstrate that investor attention positively moderates the impact of ESG rating on both SUGI and STGI, verifying Hypothesis 7 and Hypothesis 8. This implies that retail investors, due to their limited attention, will value short-term performance, although the pressure formed by investors’ attention also increases SUGI. Compared to analysts and the media, retail investors may be less capable of gaining insights by analyzing the information on GI of enterprises; this may result in an increase in strategic behavior simultaneously.

Discussion and Conclusions

When it comes to enabling environmentally friendly and innovative development, GI is essential. The motivations driving enterprises to engage in GI yield varying economic and social impacts. Concurrently, stakeholders have been driven to place more emphasis on ESG ratings by the notion of sustainable development. Employing a fixed-effects model, we assess ESG ratings’ motivational impact on GI among Chinese A-share listed firms (2009–2021). The results demonstrate that ESG ratings stimulate both SUGI and STGI in enterprises, and this conclusion holds throughout the endogeneity and robustness tests. The outcome aligns with Bai et al.’s (2024) research, which considers the first ESG rating as a quasi-natural experiment. ESG ratings will affect SUGI and STGI through different mechanisms. While, their mechanism analysis focusing on the mediating effects of financing constraints and supervision. In persistent effect analysis, we find the greatest promoting effect of ESG rating on SUGI at period t+1, while the effect on STGI is greatest at period t. These findings indicate that engaging in green invention patents requires more time than in green utility model patents due to higher technology content. In the heterogeneity analysis, we find that the outcomes are more significant for state-owned, growth-stage, and patent-intensive enterprises. This result shows that the effect varies significantly across enterprises” types, lifecycles, and industry characteristics (Long et al., 2023; H. Wang et al., 2024).

To investigate the pathway how ESG ratings affect SUGI in enterprises, we also explore the moderating role of attention from different external sources. Since most prior research has concentrated on agency expenses, operational risks, and funding limitations, this study takes an alternative perspective by looking at how external attention affects the ESG ratings and GI relationship (Bai et al., 2024; Z. Zhang et al., 2024). The mechanism analysis shows that external attention from analysts and the media might avert firms from succumbing to formalism, effectively facilitating the motivating impact of ESG ratings on SUGI. The findings prove that analyst and media attention can relieve information asymmetry and convey positive signals to encourage innovation (Haack & Schoeneborn, 2015). However, retail investors’ attention stimulates an enterprise’s strategic speculation. As the ESG disclosure information differs between rating institutions, retail investors may be confused, thereby there is “bubble” in GI (Geng et al., 2024). In conclusion, ESG rating can motivate enterprises to engage in SUGI rather than STGI to the extent that they have external supervision from professional institutions. Simultaneously, we cannot ignore the role of retail investors in “formalism” of GI. These conclusions provide a new perspective to promote the value of ESG ratings and SUGI in enterprises.

Theoretical Implications

SUGI accurately represents an enterprise’s enduring environmental performance and sustainable development competencies. Our results provide new theoretical support for the influence of ESG rating on GI. First, it broadens the investigation into the economic implications of ESG ratings. ESG rating has become increasingly valued as concerns about sustainable development increase. This study analyzes how ESG ratings affect corporate motivation for GI from the perspective of external attention. Second, this study provides a new theoretical perspective for promoting SUGI. Our findings indicate that ESG rating is an important driving force for corporate GI, but formalism is also inevitable. After introducing external attention, the findings demonstrate that attention from analysts and media can help companies avoid becoming too rigid and instead promote the positive impact of ESG rating on SUGI, rather than just strategic planning. Third, this study enriches managerial myopia theory. By examining the role of external attention in the impact of ESG rating on corporate motivation for GI, we find that investor attention can stimulate STGI owing to the lack of professional guidance. Short-sighted managers believe that STGI sends favorable signals to retail investors. This provides a new theoretical reflection of the role of retail investors in corporate GI.

Practical Implications

Regarding the practical implications, our results suggest policy directions for policymakers, enterprises, analysts, media, investors, and other stakeholders. For policymakers, this study provides empirical evidence to promote and improve ESG rating systems, hereby advancing corporate green shifts and sustainability. Our findings demonstrate that ESG rating can effectively promote corporate GI, particularly SUGI. A required ESG disclosure system must be established to standardize disclosure formats and promote ESG disclosure via legislative laws and institutional standards. The government should concurrently assume a regulatory role, directing ordinary investors to prioritize the green performance of enterprises and pursue long-term value investments. Currently, the Chinese government does not require listed enterprises to report ESG information. According to the Sino-securities Index, 39% of A-share listed companies have released independent sustainability reports with year-on-year growth of 16% in 2024. ESG performance has increasingly become a crucial reference for investors in their long-term value investment choices, making the mandated disclosure of ESG information an inevitability in long run.

For enterprises, they should actively participate in ESG practices to boost their ESG performance. Enterprises must also enhance their information transparency, allowing analysts and the media to use their external oversight to amplify the effect of ESG rating on corporate motivation for SUGI. Enterprises can incorporate their unique characteristics and industry traits when implementing ESG practices, especially for state-owned, growth-stage, and patent-intensive enterprises.

Regarding external stakeholders, analysts and the media are urged to play a positive role in external supervision, creating a favorable external environment and encouraging enterprises to engage in SUGI. External attention from analysts and the media can further promote the impact of ESG rating on SUGI in enterprises, without incentivizing strategic behavior. This study also finds that investor attention will positively moderate enterprises’ strategic speculative behavior. Therefore, the media and analysts can help retail investors better understand enterprises by conveying more transparent information, thereby encouraging them to focus on SUGI. These efforts may collectively help enterprises achieve green and innovative development goals.

Limitations and Future Research

There are also limitations in this research. First, the findings may be limited applicable. Our research, which employs A-share listed enterprises as a sample, may not be relevant to other developed countries due to the late onset of ESG in China and variations in the corporate governance structure and market regulatory framework. To determine if there are any variations in the effect of ESG rating on GI across various market contexts, further study may be expanded. Such an analysis can help verify the universality of the conclusions from this research and provide a reference for the formulation of global ESG policies. Second, the data are all second-hand data from databases, with no further subdivision of GI. Future research could obtain data through survey questionnaires and use more dimensional indicators to measure GI.

Footnotes

Author Contributions

Xinran Liu: Conceptualization, Methodology, Data curation, Writing—original draft. Taihua Yan: Conceptualization, Supervision, Funding acquisition Wen Gao: Writing—reviewing and editing. Ming Zhang: Conceptualization, Data acquisition, Methodology.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the National Social Science Later-stage Foundation of China (21FJYB039).

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The data that support the findings of this study are available from CNRDS, Wind and CSMAR, but restrictions apply to the availability of these data, which were used under license for the current study, and so are not publicly available. Data are however available from the authors upon reasonable request and with permission of CNRDS, Wind and CSMAR.