Abstract

Research and development (R&D) innovation drives sustainable growth in high-tech industries. This study analyses the impact of R&D funding classified as enterprise self-financed, government, foreign, and other sources on technological innovation outputs using China’s interprovincial panel data (2009–2021). Results reveal that self-financed R&D significantly boosts innovation, while government funding shows initial constraints but long-term benefits. Foreign R&D funding offers diminishing returns despite positive spillover effects, and other sources enhance innovation through efficient resource allocation, with room for improvement. The findings offer policy insights to optimize R&D investments, address funding disparities, and promote sustainable development in high-tech industries.

Introduction

The history of world development shows that the contemporary economy’s explosive growth cannot be achieved without a large investment in scientific and technological R&D costs. The economic competition among countries in the world today is increasingly characterized by competition founded on innovative science and technology. Globally, many nations and regions perceive R&D investment as a strategic priority, with a significant escalation in funding for science and technology emerging as a crucial strategy for enhancing productivity. The Chinese economy is shifting from a phase of rapid expansion to one of superior development, and the general trend of manufacturing industry from “Made in China” to “Created in China” is becoming clearer and clearer, in which science and technology innovation plays a significant impact (Li et al., 2019; Xie et al., 2022; Zhou et al., 2017). In the early stages of China’s financial system, which was dominated by capital accumulation, the fundamental contradiction in financial development was the conflict between capital stock and economic growth demand. Currently, financial development has shifted from “quantity” to “structure,” and the fundamental contradiction has transformed into a structural contradiction between financial supply and effective financial demand. The financial system faces new challenges of supply-demand imbalance. The core of financial supply-side structural reform lies in enhancing the efficiency of the financial system in serving the real economy and promoting its innovative development.In the context of the ongoing global science and technology revolution, the fundamental technologies of the high-tech industry are increasingly significant, while the disparity between industrial value generation and capital allocation is becoming more apparent. Financial limitations on R&D innovation have emerged as a significant factor hindering industrial innovation potential. Research and development innovation necessitates significant capital, entails great risk, and involves an extended process, hence making it inherently dependent on robust financial system support. Significant investment, considerable risk, and long development cycles are characteristics of R&D innovation, which are inextricably linked to efficient financial system funding assistance (Davies & Ferlie, 1982; Ding et al., 2008; Liu, 2022; Méndez-Morales & Yanes-Guerra, 2021; Tian et al., 2020). The economic development histories of Europe, Japan, and America make it clear that each of these countries’ financial systems supports technological advancement.

Numerous academic studies have investigated how R&D investments influence technological innovation. However, most of these studies focus on only one type of funding source, failing to fully reflect the overall structural composition of various funding sources. In reality, investments from different sources exist within an integrated structural framework where they may interact, offset, or synergize with one another, thereby achieving an optimal equilibrium state within the overall structure. To address this, this article, this paper analyzes multiple funding sources within a unified framework to investigate the problem. Following the National Bureau of Statistics of China’s (NBS) classification of R&D funding sources, this study examines R&D inputs from self-financed, governmental, foreign, and other funding sources within a single analytical framework. This study aims to analyze the comprehensive framework of R&D financing in China’s high-tech sector and assess any disparities in the allocation of these resources. Compared to previous studies, this paper incorporates multiple funding sources into a single framework, taking into account both the individual differences among funding sources and their compatibility within the overall structure, thereby addressing the limitations of studies focused on a single type of funding source. The article is structured as follows: An introductory section; a literature review in the second section, categorizing studies by R&D funding channels; an analysis of the R&D personnel structure and capital investment trends in China in the third section; the theoretical framework and hypothesis development in the fourth; modeling, data description, and processing methods in the fifth; empirical analysis and robustness testing in the sixth, accompanied by further discussion; and subsequently, the seventh section wraps up with policy consequences.

Literature Review

Scholars have carried out a great deal of useful research on R&D investment and technological innovation from various research perspectives. In this paper, we categorize them into four perspectives: own-funded input, government-funded input, foreign-funded input, and other funded input for the literature review.

Perspective on Own-funded Input

Research on the viewpoint of own-funded contribution for R&D input has discovered that an increase in corporate R&D activities has a positive contribution to the improvement of corporate profitability (Ge et al., 2025; Li & Hou, 2019; Solvay & Sanglier, 1998). The increase in market value resulting from increased R&D investment is greater than the increase in market value resulting from fixed capital investment by listed companies (Nakamura & Tsuji, 2004), and the surge in R&D spending has significantly promoted corporate expansion. Further research on the relationship between R&D investment and enterprise growth reveals a significant positive relationship between them. It enhances the operating profit of the firm (Jinfa & Biting, 2017; Lome et al., 2016; Lu et al., 2013). Although R&D innovation activities are accompanied by uncertainty, R&D investment can achieve higher economic benefits compared with other forms of asset investment of enterprises (Dong et al., 2020; Suhyung Choi & 최철안, 2014). There is a lagging effect of R&D innovation investment on enterprise growth, and only when R&D investment exceeds a certain threshold value can it promote enterprise innovation output in the next period (Dong et al., 2020; Lee & Choi, 2015; Shi & Wu, 2016). Some studies have shown that the positive impact of R&D is more significant in start-ups than in other stages of business development (Davies & Ferlie, 1982; Deng et al., 2025). R&D investment has a positive contribution to the growth of sales (Chen et al., 2023). A reduction in R&D investment will lower the competitiveness of enterprises (Melo Dos Santos et al., 2023). Academic investigations have shown that the increase of own-fund R&D input has a favorable impact on the output capacity of enterprises, which is more obvious for high-growth enterprises.

Perspective on Government-funded Input

Government grants are essential to offset the negative externality and to stimulate R&D innovation activities. Research on government-sourced R&D investment perspective shows that government subsidies have a significant contribution to firms’ innovation performance (Guo et al., 2025; Kang & Park, 2012; Li et al., 2011; Sun et al., 2023). This is especially for government investment in high-growth enterprises. However, the initial impact on the increase in enterprise innovation output is negative, but over time, the impact gradually turns from negative to positive (Chung et al., 2023). Different types of government R&D subsidies have a positive incentive effect on firms’ independent R&D investment. However, its impact on the industrial chain tends to decrease in the order of downstream, midstream, and upstream (Li et al., 2024; Liu & Dong, 2024; Y. Song et al., 2021; B. Song et al., 2024; Wang et al., 2022). It has been contended that government direction is crucial in the commercialization drive and the modernization of science and technology in China, and that government R&D financing exerts both a facilitative and inhibitory influence on innovation output (Wang & Zhou, 2020). Contrary to the above view, when the variability of firm innovation is private specifics that the government cannot capture, the function of government finance assistance will be greatly diminished. While government subsidies boost R&D innovation output of high-tech firms, they reduce total factor productivity of low-tech firms (Pan et al., 2022; Yu & Xu, 2022). But the incentive effect of government subsidies on innovative firms can be further improved by strengthening the monitoring and incentive role of state auditors (Mariev et al., 2022). Research indicates that government-funded R&D contributes positively to societal technological advancement due to its social characteristics; however, to address the variability of innovation among diverse industry sectors and firms, enhanced oversight and incentives are necessary.

Perspective on Foreign-funded Input

Studies on the perspective of foreign-source R&D investment have concluded that foreign-source R&D investment in host countries has the effect of promoting local firms to enhance their innovation capabilities, and the extent of its promotion increases with the enhancement of the host country’s technology absorption capacity (He & Brahmasrene, 2018; Liu & Buck, 2007; Sikdar & Mukhopadhyay, 2018). It is also one of the common ways for local firms to improve their capacity for technical innovation and create new markets (Belderbos et al., 2009; Fu, 2024; Li et al., 2022). For China, additionally, it was discovered that the technology spillover effect of foreign firms’ R&D investment positively influences the technological advancement capability of Chinese high-tech firms (Kim & Mah, 2009). Foreign R&D investment has a dual effect on Chinese firms, on the one hand by increasing the stock of knowledge, and on the other hand by inhibiting local firms’ innovation through factor competition with local firms, while this dual effect works in both directions, with local firms’ R&D investment also acting in the opposite direction to foreign firms’ R&D investment (Petit et al., 2012; Wang & Thornhill, 2010). Foreign R&D investment is an important source of new knowledge production and acquisition of technology spillovers in the home country (Ellimäki et al., 2024; Shin & Park, 2020). Extensive research by scholars indicates that foreign investment in R&D significantly enhances the innovation capacity of the host country and serves as a crucial method for market development. However, once the host country’s technological level attains a certain threshold, it may also encounter the risk of technological attrition.

Perspective on other Funded Input

Other sources of R&D investment mainly come from the financial market, which can be categorized into equity financing and loan financing. An efficient financial market can stimulate and nurture enterprise innovation (Cao, 2025; Hao et al., 2020). The increase of indirect financial efficiency can effectively promote the improvement of R&D investment, while the increase of direct financial efficiency has no considerable influence on R&D investment (Karjalainen, 2007; Sasaki, 2016; Tian et al., 2020). A study based on U.S. data finds that listed companies use patents as loan collateral to effectively enhance the availability of their debt financing (Aivazian et al., 2005; Mann, 2018; Maskus et al., 2019). Contrary to the above-mentioned studies, some studies also suggest that the proportion of corporate debt financing shows a negative relationship with the intensity of R&D, that is, the greater the proportion of debt financing, the lower the amount of corporate R&D innovation (Nakajima & Sasaki, 2016). Firms have difficulty in obtaining R&D investment support through debt financing, and information asymmetry is one of the important constraints (Wang & Thornhill, 2010). There exists a “U” shaped link between debt financing and innovation output, and firms show differences in different life cycle stages (Bragoli et al., 2020; Brown & Petersen, 2010). Studies on equity financing suggest that the explosive growth of R&D in the US in the 1990s was mainly attributed to the rapid expansion of equity financing, and thus equity financing is an effective source of funding for R&D innovation (Bragoli et al., 2014; Li et al., 2025; Ning & Babich, 2018; Wang et al., 2016; Zhao & Wang, 2024; Zhou & Wang, 2024). Studies in China also suggest that debt financing has a dampening effect on Chinese firms’ independent R&D innovation, while equity financing has a significant facilitating effect on independent R&D innovation (Liu, 2020). Studies have shown that other sources of R&D inputs can provide relatively more diversified financing channels for firms, however, the impact of each channel of financing in other sources of R&D inputs on innovation outputs has some variability at different stages of firms’ development.

In summary, the current research conclusions of the academic community on various sources of funding can be summarized as follows: increased R&D investment from own-funded input has a positive effect on a company’s innovation output capacity and is positively correlated with company growth. The contribution of government-funded input to a company’s innovation output is influenced by a variety of factors, but its incentive effect can be enhanced through strengthened supervision. Foreign-funded input promotes the host country’s innovation capacity but may bring risks of technology leakage and interact with local companies. Other funded input, due to the diversity of financing methods in financial markets, exhibits different impacts on R&D investment. The research methods developed by previous scholars have provided valuable theoretical support for this study. Building on this foundation, the paper conducts a comprehensive structural analysis of funding sources across various channels. The potential marginal contributions are primarily reflected in two key dimensions: (a) Academics have focused more on investigated how R&D investment affects innovation output from the standpoint of a single financing channel, and it is less common to incorporate multiple financing channels within the same framework in order to conduct a comprehensive and structural analysis. (b) In this paper, the controversies among the research currently available on whether each channel of R&D investment contributes to or inhibits innovation output are further examined in a multi-channel holistic framework to deepen its comprehension inside the framework of China.

Basic Structure of R&D Personnel and Trend of R&D Capital Input in China

Basic Structure of R&D Personnel in China

The academic structure of R&D personnel reflects the overall theoretical knowledge level, business quality and development potential of the R&D team. Usually, the higher the level of academic structure, the stronger the ability of R&D innovation. As shown in Figure 1, the total number of national R&D personnel in China in 2021 is 7,757,862, of which the number of full-time personnel is 5,823,946. The total number of enterprise R&D personnel is 5,953,268, of which the number of full-time personnel is 4,326,587. The total number of R&D professionals in industrial businesses over the specified was 4,868,504, of which the number of full-time personnel was 3,726,846. A total number of R&D personnel in R&D organizations is 550,596, of which the number of full-time personnel is 416,452. The total number of R&D personnel in higher education is 1,304,822, of which the number of full-time personnel is 573,881. A total number of other R&D personnel is 165,193, of which the number of full-time personnel is 76,375. In terms of educational structure, the number of R&D personnel graduated from undergraduate degree accounted for the largest proportion, the number of R&D personnel graduated from master’s degree accounted for the middle proportion, and the number of R&D personnel graduated from doctoral degree accounted for the relatively smallest proportion. In terms of gender structure, it is still dominated by male R&D personnel. The existing academic structure of China’s R&D personnel may yet be improved further, but it is relatively reasonable in the context of the current stage of development.

Basic structure of Chinese R&D personnel in 2021.

Current Situation and Trend of R&D Input in each Channel

Different financing channels correspond to different constraint mechanisms and contractual relationships behind them, and the financing structure composed of multiple financing relationships has a significant influence on the R&D input decisions of high-tech enterprises. In order to better analyze the impact of each R&D financing channel on technological innovation output in China, we need to understand the overall situation of each financing channel.

As shown in Figure 2, during 2009 to 2021, from the perspective of the whole invested of R&D input in each channel, it shows that the own fund channel of R&D > government fund channel of R&D > other fund channel of R&D > foreign fund channel of R&D, where the total amount of own fund channel is 3.65 times of the total amount of government fund channel, the total amount of government fund channel is 6.74 times of other fund channel, and the other fund channel is 4.72 times of foreign capital channels, and the total amount of own capital channels with the largest amount of invested capital is 116.3 times of foreign capital channels with the smallest amount of invested capital. Viewed through the lens of the trend, R&D input in own funds, government funds and other funds channels all show a continuous growth trend, among which other funds channels have a small drop in 2021, while foreign funds channels remain at a relatively stable level without a growth trend. Compared with 2009, the input of each channel of funds in 2021, the input of own funds channel increased by 4.5 times, the input of government funds channel increased by 3.6 times, the input of other funds channel increased by 2.9 times, while the input of foreign funds channel only increased by 1.2 times, and even showed a slight downward trend.

Current situation and trend of R&D input in each channel.

Theoretical Analysis and Research Hypothesis

Hypothesis 1

Compared with general corporate input, R&D input has special characteristics such as high asset specificity, high risk, long cycle time, and asymmetry in information between the supply and demand of capital. Based on the “reservoir” effect of financial assets on innovation in enterprise resource allocation, when firms devote a greater amount of resources in financial assets, it can enhance the liquidity of enterprises’ assets and help relieve the financing constraints imposed by enterprises, forming a “reservoir” function of financial assets (Suhyung Choi & 최철안, 2014). When firms allocate a bigger share of resources in financial assets, it can enhance the liquidity of the assets and alleviate the financing limitations encountered by enterprises, forming a “reservoir” of financial assets, which in turn can feed the R&D and innovation efforts in enterprises. Such resource allocation can allocate more funds to R&D innovation, lower the possibility of R&D disruptions and raise the tolerance for R&D failures, increase the probability of technological breakthroughs, and thus increase the outcome of innovative R&D (Chen et al., 2023; Jinfa & Biting, 2017; Lome et al., 2016; Lu et al., 2013). On the basis of this, the following hypotheses are proposed.

Hypothesis 2

As a policy resource, government-sourced funds are an effective force to solve the problem of market failure. By reducing the R&D costs of enterprises, government-sourced funds can reduce their innovation risks and enhance their viability. The government’s follow-up on the use of funds can indirectly reduce the information imbalance between the supply and demand sides of market funds (Kang & Park, 2012; Li et al., 2011). At the same time, it can compensate for the innovation loss suffered by enterprises due to technology spillover, enhance the level of innovation benefits obtained by enterprises, and then further motivate enterprises to invest more resources in technological innovation activities, reduce the overall R&D and innovation costs of the industry, and enhance the R&D and innovation motivation (Y. Song et al., 2021; Wang et al., 2022). In addition, government source funds can deliver favorable information to external investors and produce incentive effects on the market. Based on this, the hypotheses listed below are presented.

Hypothesis 3

This exogenous embedding can change the original factor structure and level of the host country and improve the technological innovation capability of the host country enterprises through digestion, absorption and reinvention (He & Brahmasrene, 2018; Liu & Buck, 2007; Shin & Park, 2020; Sikdar & Mukhopadhyay, 2018). At the same time, enterprises can obtain more external information by enhancing the connection between upstream and downstream enterprises at home and abroad, which also enhances their motivation and desire to go global. Under the combined effect of profit incentive and market competition pressure, enterprises are willing to invest more R&D resources to carry out higher-level technological innovation activities, improve product quality and added value, reduce production costs, obtain market expansion opportunities and gain market share. and new technologies and other heterogeneous competitive advantages in the market (Belderbos et al., 2009; Li et al., 2022). In light of this, the following hypotheses are proposed.

Hypothesis 4

Other sources of R&D input mainly rely on the financial market, which are separated into bond financing, equity financing, and bank loans, among which bank loans are used to achieve the best possible distribution of funds through the allocation of credit resources by credit intermediaries, which is beneficial to relieving the knowledge asymmetry between the supply and demand sides of funds, reducing transaction costs, improving corporate governance, and forming long-term cooperative relationships with innovative enterprises, contribute favorably to the steady inflow of R&D funding (Aivazian et al., 2005; Karjalainen, 2007; Mann, 2018; Sasaki, 2016; Tian et al., 2020). The equity and bond financing methods connect the supply and demand sides of funds through the public market platform, lower the price of information acquisition, enrich the financing path of enterprises, and further realize the role of diversifying investors’ risks (Bragoli et al., 2014; Jin & Li, 2023; S. Liu, 2020; Ning & Babich, 2018; Wang et al., 2016). On the basis of this, the following theories are put out.

Modeling and Data Description

Model Setting

The general dynamic panel data model can be thought of as:

By eliminating the individual effects ui by first-order differencing, the differential GMM model can be obtained as follows.

Blundell and Bond (1998) incorporated the level and difference equations into the same system of equations for estimation to obtain the systematic GMM model. Based on the above two estimation methods, the basic model of this paper is set as follows.

Based on the above two estimation methods, the basic model of this paper is set as follows.

In Equation (4), “i” is the ith province, city and autonomous region, “t” is the year, “ui” is an individual effect that does not vary with time and is unobservable, and “εit” is a random error term.

Data Description

China’s classification of high-tech industries is derived from the National Economic Industry Classification. It refers to technology-intensive industries characterized by high R&D investment, high value-added, and promising international prospects, featuring strategic, innovative, knowledge-intensive, and low resource-consuming characteristics. Statistically, it refers to manufacturing industries within the national economy that have relatively high R&D expenditure. High-tech industries can be further divided into high-tech manufacturing and high-tech services. According to data released by the National Bureau of Statistics, as of the end of 2023, China had 53,000 large-scale high-tech manufacturing enterprises, 65,000 high-tech service enterprises, and a total of 118,000 large-scale high-tech industry enterprises. The major industry categories and their main contents are shown in Table 1.

Major Categories and Main Contents of High-Tech Industries.

This paper adopts the categorized source funding data and the number of invention patents of R&D input in high-tech industry in each province of China from 2009 to 2021 as the main data for the study. After screening, the three provinces of Ningxia, Tibet and Qinghai were excluded from the analysis due to missing data. Data sources include the China High-Tech Industry Statistical Yearbook, the China Industrial Statistical Yearbook, the China Science and Technology Statistical Yearbook, and the annual statistical yearbooks of each province. Partially missing data were handled using the mean interpolation method. In addition, considering that GDP per capita, financial development level and openness level are also important factors affecting innovation output, this paper introduces them as control variables to enhance the statistical power of the model and more accurately estimate the core variables. The justification for variable selection is provided in Table 2, with indicator descriptions shown in Table 3.

Variable Selection and Justification.

Indicator Selection and Description.

Empirical Analysis and Further Discussion

Statistical Description of Data

As shown in Table 4, there are certain differences in the numerical distribution of each variable, which provides an appropriate data basis for subsequent analysis.

Statistical Analysis of Data.

Note. The data has been logarithmically transformed.

Unit Root Test

To prevent the pseudo-regression problem in the model’s estimate results, conducting a unit root examination on the panel dataset is essential. In this research, LLC test, HT test and IPS test are used to conduct the unit root test of panel data, and the test results are reported in Table 5.

Regression Variables Statistics.

Note. *** is the 1% level of significance, ** is the 5% level of significance, and * is the 10% level of significance.

Empirical Regressions and Analysis

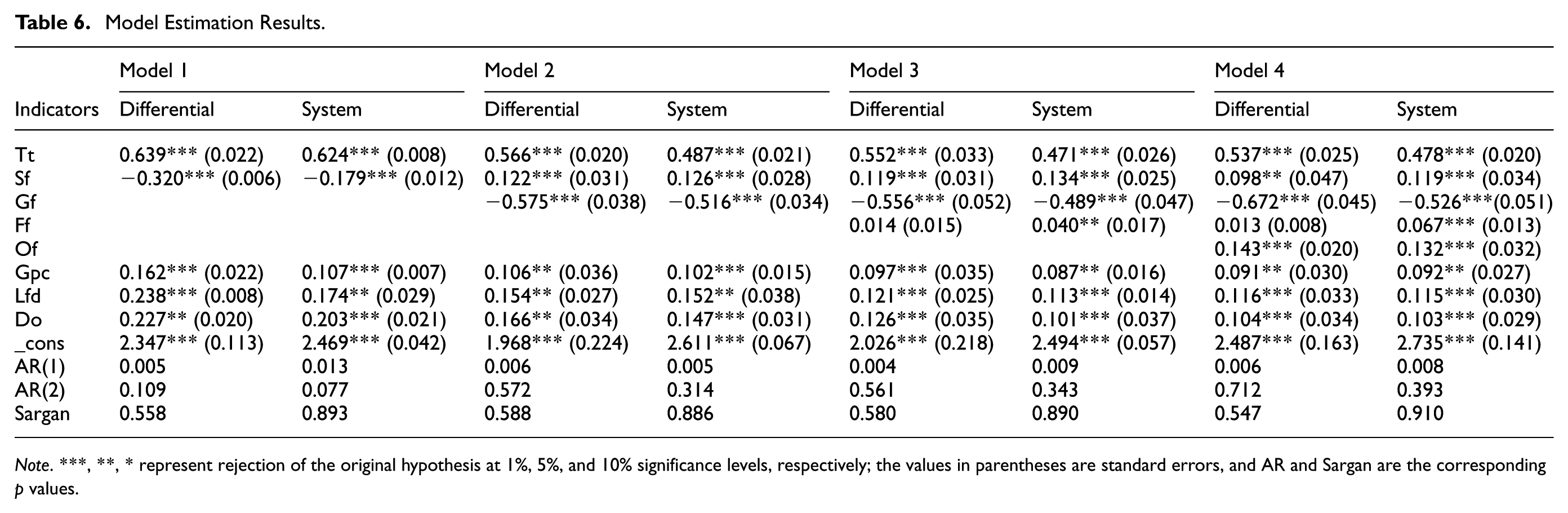

To guarantee the stability of the model estimation outcomes, both differential GMM (Diff-GMM) and systematic GMM (Sys-GMM) models are used in this paper and the data are regressed using the stepwise variable addition method, and the estimation results are shown in Table 6.

Model Estimation Results.

Note. ***, **, * represent rejection of the original hypothesis at 1%, 5%, and 10% significance levels, respectively; the values in parentheses are standard errors, and AR and Sargan are the corresponding p values.

Observing the full estimation results of Diff-GMM and Sys-GMM, it can be found that there is no significant change in the positivity and negativity of the estimation results, the proportional structure and significance of the two, except for a slight change in the estimated value, indicating that the regression results are robust overall. According to Che et al. (2013), it is argued that Diff-GMM regression suffers from weak instrumental variable problem, while Sys-GMM regression has relatively higher estimation efficiency. Therefore, the Sys-GMM regression results in model 4 are selected for further analysis in this paper.

In the Sys-GMM regression results of Model 4, the estimated value of the lagged one-period dependent variable is 0.478, with a positive coefficient that is significant at the 1% confidence level. This indicates that earlier R&D input in high-tech industries has a positive impact on current technological innovation output, with an effect magnitude of 0.478. This suggests that it accounts for a relatively large proportion of innovation output, showing a strong cumulative effect.

The projected value of R&D investment from internal funds is 0.119, exhibiting a positive correlation and significance at the 1% confidence level, thereby corroborating the research hypothesis H1: the “reserve pool” function of own-funded input enables enterprises to independently allocate and reserve assets in response to fluctuations and unexpected disruptions in external capital supply. This, in turn, contributes to the rational allocation of enterprise resources, enhances the stability of R&D capital investment, and increases innovation output. The reasons for this influence may stem from two dimensions. Enterprises, as market entities striving for efficiency and profit maximization, typically initiate R&D innovation activities centered around market demand when investing their internal funds. This approach facilitates the conversion of R&D outcomes into economic benefits, resulting in higher capital utilization efficiency. Furthermore, enterprises can select R&D projects based on their inherent advantages. In selecting R&D projects, firms may choose based on their inherent advantages, developmental strategies, and capital investment plans to optimize their innovation output within specified financial restrictions. Conversely, by evaluating market information, enterprises can establish an appropriate ratio and scale of capital investment to ensure the efficient utilization of R&D funds. Additionally, the flexibility in exploiting internal funds allows enterprises to engage in market competition, leveraging the learning effect and guiding leading enterprises to pursue iterative innovation, thereby enhancing innovation output.

It is worth noting that the estimated value of R&D input from government funding is −0.526 with negative sign and significant at 1% confidence level, which fails to support the research hypothesis H2 above: government sourced funding can help mitigate market failures caused by information asymmetry between enterprises and the market through its guiding role. It can also reduce innovation risks for enterprises through fiscal policy incentives and generate synergies with other funding sources, thereby promoting R&D innovation output at the enterprise level. A possible reason is that government-funded input tends to focus more on strategic and fundamental R&D activities, which have low short-term returns, high risks, and long cycles, and thus do not align with the short-term interest orientation and market-driven nature of enterprises. Enterprises themselves also bear policy adaptation costs, including time lags in strategic adjustments and organizational restructuring. In addition, there are issues in the policy environment, such as lack of policy continuity, restrictions from industry entry barriers, and the absence of coordination mechanisms. In particular, improving the R&D output capacity of key equipment and core technologies requires long-term accumulation and cannot achieve results in the short term. In the long run, however, through enterprise-level adjustments, the cumulative effect of policy implementation, and improvements in the innovation ecosystem in related fields, government-funded input can play a promoting role. Therefore, government investment needs to go through a certain accumulation process before it can effectively promote the formation of a high-quality industrial innovation chain. In other words, there exists a process in which negative effects are followed by positive outcomes.

The estimated value of R&D input from foreign funds is 0.067, which is smaller than the positive effect of R&D input from own funds and R&D input from other funds on innovation output, but the sign is positive and significant at 1% confidence level, which supports the research hypothesis H3 in the paper: foreign sourced funding can promote technological breakthroughs in corporate R&D through technology transfer and knowledge sharing, optimization of talent allocation, and collaborative effects. Therefore, it has a strengthening effect on corporate R&D innovation output. The entry of foreign-source R&D funds into the host country may produce both crowding-out and spillover effects, and both occur with changes in the environment, and the positive spillover effect of R&D innovation is greater than the negative crowding-out effect in the study of this paper. On the one hand, domestic enterprises, in the process of cooperation and exchange with foreign institutions, will meet the requirements of foreign markets for technology, products and other aspects with foreign institutions in order to further jointly enhance R&D innovation activities and increase the input of R&D funds and researchers to obtain the opportunity to develop the market; at the same time, the cooperation and exchange with foreign institutions also provide domestic enterprises with the opportunity to learn technology and improve management capabilities at a close distance, so that the positive impact of the correlation effect and demonstration effect of R&D funds from foreign sources exceeds the negative impact of technology dependence and technology monopoly, which through the advanced The positive impact of the correlation and demonstration effects of foreign-sourced R&D funds outweighs the negative impact of technology dependence and technology monopoly, which promotes the efficiency of input in innovative enterprises through advanced input technology and risk control experience. On the other hand, with the intensification of competition in the domestic market, it also promotes the innovation efficiency of the industry as a whole and the R&D efficiency of the internal source funds of enterprises. However, compared to own-funded R&D input and other-funded R&D input, the contribution of foreign-funded R&D input to R&D innovation is relatively lower, showing a trend of diminishing marginal returns compared with earlier periods. A possible reason is that foreign-funded R&D activities in China also face the constraint of limited resources when continuously increasing their investment. In addition, once other enterprises have mastered most of the current key technologies through spillover effects, continued R&D investment from foreign sources may struggle to break through new technological bottlenecks, thus leading to diminishing marginal returns.

The estimated value of R&D input from other funds is 0.132 with positive sign and significant at 1% confidence level, which supports the research hypothesis H4 above: funds from other sources can alleviate financing constraints for innovative enterprises by expanding corporate financing channels, providing innovative tools, and optimizing resource allocation, thereby offering enterprises multidimensional support for research and development innovation. The potential explanations for this stem from the viewpoint of indirect finance, wherein banks typically restrict the maximum return on profits and maintain a dominating role in the agreement to enhance information screening, informed decision-making, and risk management. From the standpoint of direct finance, equity money does not require collateralization or repayment and can yield substantial profits from innovation. Investors exhibit heightened concern regarding the transformation of outcomes and the innovation performance of firms, fostering a natural inclination toward collaboration with the innovation initiatives undertaken by these enterprises, so facilitating the establishment of a community of interest between enterprises and investors. The financial market improves market activity and liquidity by facilitating efficient fund allocation and maintaining relatively low entry barriers, thereby enabling investors to discern the value of innovation and providing adequate incentives for technological advancement in enterprises.

GDP per capita in the control variables, the estimated value is 0.092, the sign is positive and significant at the 5% confidence level, GDP per capita reflects a nation’s degree of economic development of economic development, as this level increases, the greater the level of innovation resources can be driven to invest in the level of innovation resources, thus providing a good basis for innovation output. The estimated value of the level of financial development is 0.115, with a positive sign and significant at the 1% confidence level. In the past few years, the Chinese government has continuously strengthened the modernization of the financial system, promoted financial innovation, and facilitated the in-depth integration of financial technology with the real economy. The estimated value of the degree of openness is 0.103, the sign is also positive and significant at the 1% confidence level, indicating that as the scale of China’s international trade continues to expand, the technological spillover effect based on international trade is more obvious, and it has a positive impact on China’s technological progress.

Further Robustness Tests

The aforementioned has established that the regression results possess a degree of reliability through the comparison of the difference model, the introduction of control variables, and the incremental addition of variables. To further bolster the credibility of the research conclusions, this paper additionally employs the method of substituting the dependent variable to perform a robustness test. Research and development input and new product sales are two interdependent components in the functioning of high-tech firms, and a strong correlation exists between them. The R&D department delivers firms competitive new products or technology by ongoing technical innovation and research. The sales department supplies the R&D department with guidance and insights for product enhancement via market engagement, hence fostering product innovation. Therefore, this paper uses the sales of new products in high-tech sectors as the dependent variable for the replacement test. Table 7 displays the test findings, and it is clear that the regression values of each variable are not much different from those in Table 6, and the signs are consistent, which further supports the research conclusions presented in this paper.

Further Robustness Tests.

Note. ***, **, * represent rejection of the original hypothesis at 1%, 5%, and 10% significance levels, respectively; the values in parentheses are standard errors, and AR and Sargan are the corresponding p values.

In summary, it can be seen that in the R&D input context of China’s high-tech industry, the increase of R&D input from own funds can promote the output of technological innovation by optimizing internal asset allocation (Chen et al., 2023; Jinfa & Biting, 2017; Lome et al., 2016; Lu et al., 2013) and combined with Figure 2, it is evident that at present, among the various channels of R&D input in China’s high-tech industry, the proportion of own funds input channel is the highest, and it shows a trend of increasing. Compared with the introduction-imitation innovation mode in the past, the high-tech sector has transitioned into a new phase characterized by independent innovation models. The increase in R&D input from government funds shows an overall inhibiting influence on the technological advancement results of high-tech sectors (Pan et al., 2022; Y. Song et al., 2021; Wang et al., 2022; Yu & Xu, 2022). It can be seen that the ratio of R&D input from government funds is second only to that of R&D input from own funds, which to a certain extent reflects the increase in the input of government funds in basic research, which has a certain time lag in transforming into innovation output. The increase in R&D input from foreign funds promotes the output of technological innovation through positive spillover such as correlation effect and demonstration effect (He & Brahmasrene, 2018; Jin & Li, 2023; Liu & Buck, 2007; Sikdar & Mukhopadhyay, 2018) but its contribution to the output of technological innovation in China’s high-tech industry tends to decrease compared with the past, and its share in the four input channels is smaller. The increase of R&D input from other funds promotes the output of technological innovation through the higher resource allocation efficiency of the financial market (Aivazian et al., 2005; Bragoli et al., 2014; Hao et al., 2020; Mann, 2018; Maskus et al., 2019; Ning & Babich, 2018; Wang et al., 2016). And the estimated value of the empirical results is 0.122, which shows that its promotion effect is the most significant among the four input channels, but combined with Figure 2, it has the smallest proportion among the four input channels, indicating that the scale of its input still has a large improvement due to the financial market’s developmental phase. This indicates that, due to the development phase of the financial market, there is still much room for improving the scale of input.

Conclusion and Policy Recommendations

Conclusions

Within the framework of China’s new economic normal, technological innovation is regarded as a key catalyst for restructuring the economy, driving economic transformation, enhancing the quality of economic growth, and promoting advanced development. This paper examines the impact of R&D capital investment in China’s high-tech industries on innovation outcomes within the overall framework of multi-channel investment. Using a dynamic panel data system GMM model, the paper analyzes the effects of different funding channels. Building on previous research, it expands upon the limitations of studies focusing on single-type funding sources. The main conclusions are as follows: (a) Own-funded R&D investment promotes technological innovation through the reallocation of financial assets, optimization of market information, and project evaluation. The research results support the views of Suhyung Choi and 최철안 (2014) and Hutauruk (2024). (b) Government-funded is mainly used for strategic and fundamental research and innovation activities. Although it suppresses short-term technological innovation output, in the long term, it will help technological innovation through policy accumulation effects and improvements in the innovation ecosystem. The research results support the views of Chung et al. (2023), but do not support the views of Sun et al. (2023) and Guo et al. (2025). (c) Foreign-funded investment has a positive impact on technological innovation output through related effects and demonstration effects. The research results support the views of Liu and Buck (2007), He and Brahmasrene (2018), and Sikdar and Mukhopadhyay (2018), but unlike them, under a multi-channel overall structure, the promotional effect of foreign R&D investment on innovation gradually diminishes. (d) Other funded inputs improved corporate innovation performance by increasing the efficiency of resource allocation in financial markets, and the research results supported the views of Hao et al. (2020) and Cao (2025). However, as China’s financial markets are still in the development stage, there is still considerable room for improvement in terms of investment scale.

Policy Recommendations

Based on the study findings presented above, this paper proposes the following policy in-sights.

First, respect the market mechanism and the law of enterprise R&D input development. Activate the core role of the internal driving force and vitality of enterprise technological innovation, improve the protection system of intellectual property rights, strengthen the enforcement, reduce unreasonable government intervention, and eliminate the institutional barriers that restrict the cultivation and enhancement of enterprise innovation capacity. Encourage enterprises to scientifically formulate R&D decisions that are in line with government strategies, form sustainable and predictable public-private partnership R&D investment plans, strengthen the introduction, training, and utilization of R&D talent, and increase investment in the research and development of key core technologies.

Secondly, enhance the funding structure for governmental sources of R&D financing. Enhance the oversight and administration of funding allocation, utilization procedures, and project evaluation to improve the efficiency of fund utilization. Utilize market-based mechanisms to promote the conversion and deployment of innovative achievements. Combine government and market forces to eliminate barriers to industrial development, clarify the responsibilities and rights of different levels of government, improve coordination mechanisms between departments, reduce policy implementation deviations, and maximize the key role of government R&D funds in strategic, fundamental, and public welfare innovation.

Third, continue to promote high-level reform and opening up, and improve the existing policy system. Further introduce specific regulations and preferential policies to attract foreign high-tech enterprises to invest in research and development in China. Strengthen communication, coordination, and policy convergence among departments, increase efforts to attract foreign investment in key areas, expand methods to promote foreign investment in research and development, improve the division of responsibilities among governments at all levels. Give full play to the role of various policies in guidance, incentives, and risk management, and promote the sustainable development of foreign investment in research and development in China.

Fourth, accelerate the market-oriented reform of financial factors and establish a reasonable factor price system. Releasing the resource allocation signal of the financial market through the price of financial factors. Build an R&D input ecological chain that matches the value chain, embed endogenous financing and exogenous financing of high-tech industries into the technological innovation value chain system in concert, improve the efficiency of financial factor allocation, and reduce the internal and external financing costs of enterprise R&D activities.

Limitations

This research has yielded significant results and insights at both theoretical and practical levels; nonetheless, there remains potential for future enhancement. The level of industrial growth in China’s eastern, central, and western regions exhibits variability, indicating a need for greater comprehensive research on the distribution of R&D capital throughout these locations. The categories of enterprises within the high-tech industry might be further subdivided, warranting additional research on various enterprise types.

Footnotes

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The author has attached the dataset as a supplementary file to this submission.