Abstract

Innovation is crucial for the future growth of high-performing firms. Whether firms in the growth aspiration surplus have a conservative or aggressive attitude toward innovation investment is still a matter of concern. Therefore, based on the theory of firm behavior, it is discussed how the state of growth aspiration surplus affects managers’ perception of firms’ risk and return, which in turn affects firms’ innovation investment. Based on the data of China’s A-share listed companies, a two-way fixed-effects model is utilized to draw the following conclusions: The growth aspirations surplus is significantly positively related to innovation investment, which is confirmed by both the historical growth aspirations surplus and the industry growth aspirations surplus. In addition, organizational slack reinforces the positive effect of growth aspirations surplus and innovation investment, while organizational inertia negatively moderates the relationship between growth aspirations surplus and innovation investment.

Introduction

Innovation is an important means for organizations to adapt to changes in the environment and maintain competitive advantage (Zhou & Li, 2012), and is a key driver of firm growth (Romer, 1986; Schumpeter & Swedberg, 2021). Although a large body of literature has explored the antecedent variables of innovation, such as government subsidies (Wu et al., 2022), digital technology (Usai et al., 2021), external knowledge (Hameed et al., 2021), green finance policies (He et al., 2023), business environment (Nguyen et al., 2024), environmental regulation (Shao et al., 2020), etc., but few studies have focused on the impact of growth feedback on firm innovation. Firms’ growth is dependent on their ability to innovate, which in turn is affected by their level of growth. According to the performance feedback theory, aspiration level plays an extremely important role in business decision-making, that is, managers adjust their innovation strategies based on the disparity between the actual growth level and the aspiration level (Cyert & March, 1963). Some studies have pointed out that the aspiration gap is one of the most important reasons affecting firms’ innovation (W. Chen et al., 2022b; Greve, 1998), and suggest that aspiration gap strengthens managers’ tolerance for risk and promotes firms’ innovation (Goyal & Goyal, 2022; Greve, 2003; Keil et al., 2023; Kuusela et al., 2017) or by threatened rigidities, leading to a reduction in innovation activity, among other ideas (Jeong et al., 2023). Existing research on aspiration gap and corporate innovation is extensive and rich, but few scholars have focused on the innovative behavior of aspirations surplus of firms.

As research deepens, some scholars have examined the relationship between organizational slack and innovation, noting that financial slack significantly increases corporate innovation investment (K. Zhang et al., 2021). Generally, high levels of slack resources tend to foster greater corporate innovation (Marlin & Geiger, 2015). However, other scholars studying Korean firms suggest a weaker link between financial slack and innovation, with both factors being more heavily influenced by institutional environments and organizational characteristics (Lee, 2015). Some researchers even propose an inverted U-shaped relationship between organizational slack and innovation, arguing that both excessively high and low levels of organizational slack are detrimental to innovation (Nohria & Gulati, 1996). In summary, while research on organizational slack and innovation is abundant, it primarily focuses on the impact of organizational financial resources on corporate innovation. This differs significantly from the growth positive feedback mentioned earlier. Consequently, the concept of aspirations surplus has emerged. Some scholars indicate that a surplus promotes R&D (Xi et al., 2021), with this effect being more pronounced in exploitative innovation (Lu & Wong, 2019). And managers’ positive perceptions foster a positive relationship between positive performance feedback and innovation (Saraf et al., 2022). However, some scholars hold differing views, pointing out that positive performance feedback among peers may reduce innovative search behavior (Ye et al., 2021). Others even suggest that a positive aspiration gap exhibits a U-shaped relationship with innovation investment (Zhu et al., 2023). A review of the existing literature reveals that current research findings contain contradictory points, and the feedback mainly focuses on profitability indicators (Kuusela et al., 2017; Martínez-Noya & Garcia-Canal, 2021; Sengul & Obloj, 2017; Zhong et al., 2022), there is a lack of focus on the growth capacity of firms. While profitability is the basis for ensuring sound business operations and investor returns, it is firm growth that is key to the long-term survival and development of firms in competitive markets, which is particularly important for investors and capital markets (Haveman, 1993). In particular, will firms in the growth aspirations surplus be satisfied with the status quo and fall into the “success trap” (Leonard-Barton 1992)? Or will they be aggressive and maintain their competitive advantage? Therefore, this paper focuses on how the growth aspirations surplus affects firms’ investment in innovation in order to fill the gap in existing research.

In the process of firm growth, limited-rational managers play a key role in setting and implementing long-term goals and plans. However, decision makers’ ability to perceive and respond to growth aspiration surpluses is not consistent, which is largely influenced by their managerial autonomy. Managerial autonomy reflects the degree of managerial influence over strategy selection, formulation, and implementation, and ultimately reflects the freedom of action enjoyed by policymakers (D. C. Hambrick & Finkelstein 1987). Currently, there is a wealth of research on managerial autonomy, but it is not surprising to find that much of the research focuses on autonomy related to the external market environment (Wangrow et al., 2015) and less on autonomy related to organizational characteristics within the firm. Considering that firms’ innovative actions not only require the allocation of productive resources such as economic, human, and material resources but also require managers to coordinate relevant processes and procedures to ensure the feasibility of the implementation of innovation strategies, Therefore, this paper focuses on organizational inertia and organizational slack within firms to investigate the moderating effect of managerial autonomy on the relationship between growth aspiration surplus and firms’ innovation investment.

The marginal contributions of this paper include: (a) Enriching the understanding of the relationship between performance feedback and innovation. Previous studies predominantly measured performance feedback using profitability metrics, overlooking the critical dimension of corporate growth. This paper focuses on whether firms adopt “aggressive” or “conservative” strategies under growth aspirations surplus, offering a new perspective for understanding innovation drivers in a growth context. (b) It refines the classification of surpluses into historical growth aspiration surpluses and industry growth aspiration surpluses, examining their differentiated impacts on innovation investment. Given the multifaceted and complex decision-making reference points for firms, different types of surpluses may guide managers toward distinct attitudes toward innovation behavior, necessitating a differentiated analysis. (c) Incorporates managerial autonomy into the research framework, revealing its role as a contextual condition for growth aspiration surplus, influencing innovation. A firm’s ability to respond promptly to growth feedback often depends on its internal structure and managerial freedom. Thus, this study not only enriches the application of performance feedback theory in innovation research but also provides insights for firms to optimize internal governance and enhance innovation responsiveness.

The subsequent structure of this paper is as follows: Section II (Literature review and hypothesis development) constructs the theoretical framework and proposes hypotheses. Section III (Methods) details the research design and data methodology. Section IV (Results) presents empirical analysis, reporting core findings and testing result robustness. Section V (Discussion) concludes with an in-depth discussion, managerial implications, and research limitations.

Literature Review and Hypothesis Development

Theoretical Framework

A behavioral theory of the firm was first proposed by Cyert and March, that is, managers compare the discrepancy between the actual performance of the firm and the level of aspiration to grasp the overall business situation of the firm and take strategic actions accordingly. The core of the theory is the organization’s aspirational goals, including historical aspirations and industry aspirations (Cyert & March, 1963). Historical aspirations are levels set through experience based on one’s past performance, while industry aspiration levels are determined from comparisons among firms in the same industry (J.-Y. Kim et al., 2015; Saridakis et al., 2023). Considering historical and industry performance feedback is inherently two different criteria with different impacts on firms’ innovation decisions (J.-Y. Kim et al., 2015). It is therefore necessary to differentiate this to understand the different impacts of two different aspiration surpluses on firms’ innovation. Especially for these high-performing firms with better growth potential, will they rely on the resources and brand effects accumulated in the previous period and build on them? Or will they be satisfied with what they have achieved and fall into a circle of organizational inertia, making it difficult for them to adapt to changes in the external environment and be eliminated by the market? This is still worth exploring.

Literature Review and Hypothesis Development

Historical Growth Aspiration Surpluses and Firms’ Innovation Investment

The level of growth aspirations represents an organization’s anticipated state of satisfaction (Cyert & March, 1963). A historical growth aspiration surplus indicates that an enterprise’s actual growth level exceeds its historical aspirations, signifying the successful overachievement of anticipated targets (Cho et al., 2016; Vidal & Mitchell, 2015). This indicates that the organization possesses available resources to support new ventures and trial-and-error efforts. Thus, this enhances the organization’s risk tolerance, thereby facilitating managers’ engagement in redundancy search behavior (Parker et al., 2017):

First, growth aspiration surpluses are typically accompanied by an increase in the available resources within firms (Lu & Wong, 2019; Titus Jr et al., 2022). This provides firms with a resource buffer (Baum et al., 2005), significantly enhancing organizational risk tolerance. These available resources enhance tolerance for investment failures, enabling firms to broaden their innovation search scope (Chrisman & Patel, 2012) to build competitive advantages and achieve future growth. Research indicates that a firm’s innovation capability is closely linked to the abundance of resources (Khanra et al., 2022; Wernerfelt, 1984). The available resources not only provide ample financial backing for innovation investments (X. Li et al., 2024) but also reduce managers’ fear of innovation failure, encouraging them to pursue new innovative explorations (Yu et al., 2019). Therefore, under historical growth aspiration surpluses, these available resources not only provide financial backing and enhance the organization’s capacity to withstand risks but also influence managers’ innovation willingness (Demirkan, 2018), driving them to seize new innovation opportunities and increase their enthusiasm for innovation.

Second, historical growth aspiration surpluses increase managers’ confidence in future growth, stimulating upward comparison motivation. For these firms, managers attribute such surpluses to themselves (Audia et al., 2000)—that is, to the effectiveness of their own management and strategic decisions. Under the influence of this overconfidence cognitive bias, managers may hold high future expectations and have strong upward comparison motivation (Wood, 1989), leading them to underestimate risks (Cooper et al., 1988). At this point, managers’ focus shifts from “survival issues” to “catching up with high-performing firms,” naturally imposing higher demands on them (Cho et al., 2016; Vidal & Mitchell, 2015), driving them to continuously pursue upward growth. Under this cognitive bias, managers exhibit lower risk sensitivity (Schumacher et al., 2020) and are more inclined to allocate greater resources toward innovation to shape the organization’s future growth advantages and maintain its market position.

Finally, historical growth aspiration surplus represents the company’s potential for growth, which enhances internal stakeholders’ confidence in its future development. If the firm fails to meet expected performance, this triggers a series of negative effects, such as reputational damage and forced managerial departures. Therefore, to meet this requirement, managers typically face growth pressure (Gavetti et al., 2012), leading to increased risk tolerance (Schumacher et al., 2020), seeking risky innovation pathways to achieve future growth (Saraf et al., 2022; Ye et al., 2021). In summary, surplus firms possess both upward comparison motivation and the need to meet high aspirations, coupled with internal resources to support innovation investments. Therefore, we propose the following hypothesis:

The Industry Growth Aspiration Surplus and Firms’ Innovation Investment

The industry growth aspiration surplus refers to the fact that firms’ actual growth level is higher than the industry average, which indicates their ability to grow beyond the industry average. This positive social signal may present both opportunities and challenges for firms, driving organizations to engage in new redundant search behaviors to maintain their growth advantage. This will influence managers’ willingness to take risks on innovation investments:

First, a positive industry growth aspiration surplus indicates that a company is on a promising growth trajectory with considerable growth potential. This positive social image enhances the organization’s ability to obtain resources, alleviates resource constraints on innovation, and consequently strengthens managers’ willingness to innovate. Specifically, a growth surplus conveys positive operational signals, significantly enhancing the organization’s bargaining power and influence (Kotiloglu et al., 2021). This enables the firm to acquire innovation resources—such as technology, capital, and talent—at lower capital costs. Meanwhile, the positive social image generated by the surplus facilitates access to promising technology partners, expands innovation options, and stimulates managers’ willingness to innovate.

Second, industry growth aspiration surplus may trigger catch-up pressures (Singh, 1986). Such pressures impose higher demands on corporate growth, influence managers’ willingness to take risks, and increase the likelihood of long-distance search behaviors. At this stage, managers recognize that relying solely on accumulated internal capital is insufficient to maintain market share (Rosenkopf & Nerkar, 2001). This requires firms to actively pursue innovation search (T. Kim & Rhee, 2017) to shape competitive advantage (Chrisman & Patel, 2012). In this context, managers often show greater risk-taking willingness, attempting to shape competitive advantages through innovation to maintain market competitiveness (Tödtling et al., 2009).

Finally, the industry growth aspiration surplus shifts corporate focus from “organizational legitimacy” issues toward “technological advancement and demand shifts,” making managers more willing to invest in innovation. Growth surpluses are typically viewed as an improvement in corporate legitimacy and market position, significantly reducing operational risks caused by external uncertainties (Haack et al., 2021). Under these situations, managers will pay greater attention to technological transformations, product iterations, and emerging customer demands within the external environment (Oliver, 1991). They will show a stronger willingness to undertake risk investments, attempting to shape competitive advantages and sustain future growth through innovation (Babina et al., 2024). Therefore, based on the above analysis, the following hypothesis is proposed:

The Moderating Role of Managerial Autonomy

The innovation decisions made by managers are not only influenced by growth feedback but are also subject to the level and degree of freedom that managers have within their organizations to choose, formulate, and implement innovation strategies. It is necessary to further explore the role of managerial discretion over internal organizational characteristics—including organizational redundancy and inertia—in mediating the relationship between growth aspiration surplus and corporate innovation.

Organizational slack arises when a firm possesses resources far exceeding those required for its production and operations. By providing additional resources such as capital, manpower, and time, organizational slack effectively alleviates resource constraints on firms during their development (Bourgeois III & Singh, 1983). In the context of historical growth aspiration surplus, firms are often accompanied by an increase in available resources (Lu & Wong, 2019; Titus Jr et al., 2022), significantly enhancing the organization’s tolerance for uncertainty risks (Vanacker et al., 2017) and thereby driving increased innovation investment. Within this mechanism, organizational slack plays a distinct moderating role. On one hand, innovation demand is sustained, substantial capital investment (Khanra et al., 2022; Wernerfelt, 1984), and its inherent high risk, high investment, and high uncertainty make it difficult for enterprises to persist (S. Chen & Shen, 2023). However, redundant resources can alleviate resource constraints (Vanacker et al., 2017) and effectively buffer the impact of innovation failures, enabling firms to tolerate higher innovation risks. On the other hand, organizational slack enhances managers’ resource allocation flexibility, enabling them to prioritize resources toward innovation (Troilo et al., 2014) in response to growth feedback.

Under the industry growth aspiration surplus, organizations gain greater financial backing and reputational advantages in the market. Managers no longer worry about legitimacy issues, which significantly enhances their risk-taking willingness and inclines them toward proactive innovation strategies. However, this mechanism is clearly constrained by redundant resources in practice. Organizational slack provides a resource buffer for innovation (X. Li et al., 2024), making firms more willing to take risks and transform these resources into actual innovation investments. Thus, by alleviating resource constraints, organizational slack further strengthens the risk-taking willingness stimulated by industry growth surpluses, making it more likely to convert into concrete innovation actions. This, in turn, amplifies the positive impact of industry growth surpluses on corporate innovation investments. Therefore, based on the above analysis, this paper proposes:

Organizational inertia is often viewed as a product of path dependence in the process of business development (Hodgkinson, 1997). Usually, scholars pay more attention to the negative impact it brings (Haag, 2014), which is regarded as a manifestation of organizational stagnation. In other words, organizations rely on accumulated historical experience and behavioral patterns, which makes it difficult to adjust their business strategies on time under changes in the external environment and can easily fall into the dilemma of being eliminated from the market (Moradi et al., 2021; Schwarz, 2012). It can be seen that organizational inertia has an extremely important impact on the innovation decisions and future development of enterprises.

Under historical growth aspiration surplus, organizational inertia often suppresses a firm’s capacity to coordinate and allocate resources. Such inertia typically accompanies rigid internal organizational structures and processes (Haag, 2014). This rigidity frequently restricts flexibility in resource reallocation, diminishing the likelihood of converting resources into innovation investments and thereby lowering the organization’s risk tolerance. Furthermore, organizational inertia influences managers’ perceptions of risk and uncertainty. High levels of organizational inertia cause managers to rely on existing decision pathways and methods, making it difficult to adapt to new market changes and hindering the organization’s ability to take on innovation risks (Xie, 2014). Even when conditions permit, managers may still cling to tradition (Greve, 2011), maintain existing business models (Moradi et al., 2021), and prioritize familiar, stable investment decisions.

Under the industry growth aspiration surplus, on one hand, the higher the level of organizational inertia, the greater the constraints imposed by internal rules and regulations. Even when enterprises possess resource advantages and growth potential, they may be reluctant to break existing conventions for strategic adjustments (Greve, 2011). Thus, under the positive feedback of industry growth, the risk-taking willingness that managers should be motivated to exhibit is likely neutralized by traditional organizational practices and logic, leading to conservative attitudes toward innovation. On the other hand, organizational inertia weakens a company’s adaptability to market changes, hindering its ability to fully leverage the resource and reputation advantages brought by the surplus for forward-looking innovation. At this point, organizations often prefer to maintain existing business models (Moradi et al., 2021) and continue with familiar, stable operational paths and investment approaches. This “boiling frog” effect gradually causes enterprises to lose innovation opportunities arising from surplus advantages, suppressing their willingness to take risks for innovation. Therefore, based on the above analysis, the hypothesis is proposed:

Figure 1 shows the theoretical model of this paper.

Theoretical model.

Methods

Sample Selection

Given that China is the world’s second-largest economy, its A-share market stands as one of the largest and most significant emerging markets globally, spanning numerous industries and providing an excellent context for studying corporate innovation strategies. Concurrently, databases such as CSMAR offer high-quality corporate financial data. Therefore, this paper utilizes Chinese A-share listed companies on the Shanghai and Shenzhen stock exchanges from 2008 to 2021 as its sample and processes the data as follows: (a) Excluding financial industry companies, as their unique regulatory frameworks and capital structures render their innovation activities and financial reporting incomparable with non-financial enterprises. (b) Excluding ST and *ST companies to minimize the impact of reasons such as ambiguous or doubtful financial reports on the results. (c) Excluding missing data samples to ensure the completeness and reliability of the research data. This filtering process resulted in a final unbalanced panel dataset comprising 4,292 unique listed companies and 23,708 firm-year observations. Meanwhile, continuous variables were Winsorized with 1% and 99% quantiles to reduce the influence of extreme values on the results. All other relevant financial data were obtained from the CSMAR database. Additionally, the empirical analysis employs a fixed-effects panel regression model to control for firm-level unobservable time-invariant heterogeneity, and all econometric estimations were conducted using Stata version 14.

Additionally, our sample has certain limitations due to institutional differences between China and Western countries, which may affect the generalizability of our conclusions. To mitigate this issue, we divided the sample into state-owned enterprises (Juniarti et al., 2021) and non-state-owned enterprises (NSOEs) for regression analysis. This approach helps test the robustness of our main findings within more homogeneous groups (such as NSOEs). Furthermore, the model controls for year and individual fixed effects to eliminate interference from firm-specific characteristics and macroeconomic fluctuations, thereby enhancing internal validity.

Definition of Variables

Dependent Variable

Innovation investment (RD), considering the differences in size between listed companies, the relative indicator is more stable, so drawing on other scholars’ methods (V. Li, 2016; Lv et al., 2019), this paper adopts the ratio of R&D investment to operating income to measure.

Independent Variables

The growth aspiration surplus (GS) refers to the difference between a firm’s actual growth level and the market’s historically expected growth level (Moradi et al., 2021), or the difference between the industry growth aspiration level (IS). Referring to previous studies, since the aspiration surplus is the effect of past performance on future decisions, the aspiration surplus is treated one period ahead, which is calculated by the following formula:

Where Pi,t−1 is the real growth level of the enterprise. The growth process of the enterprise is mainly reflected in the increase in business income, total assets, and the number of personnel. Since the increase in assets and personnel has a certain lag relative to the business income, it is difficult to reflect the growth of the enterprise on time, so the growth rate of business income is used to measure it (Ho et al., 2011). Among them, Ai,t−1 includes the historical aspiration level HAi,t−1 and the industry aspiration level IAi,t−1; and α1 is a value between [0, 1]. For the value of α1, Equation (2) is fitted by drawing on other scholars’ treatments (W.-R. Chen, 2008). α1 starts from .1 and keeps increasing to .9, with each increment of .1 for weight setting. The fitting results show that the highest fit is achieved when α1 = .4.

Thus, the historical aspiration level of the firm i’s growth in period t−1, HAi,t−1, is a weighted combination of the firm i’s actual growth level in period t−2, Pi,t−2 (with a weight of 0.6), and its aspiration level in period t−2, HAi,t−2 (with a weight of 0.4); and the industry aspiration level of firm i’s growth in period t−1, IAi,t−1, is chosen as the average of all firms in the industry (3-digit Standard Industrial Classification [SIC] code) except firm i, averaged over the actual level of growth in year t−1 (Iyer & Miller, 2008). Finally, since this paper studies a sample of firms with growth aspiration surpluses, zeros are assigned to the sample of observations whose actual growth level is lower than the growth aspiration level.

Moderator Variable

In this paper, organizational slack (OS) and organizational inertia (OI) are used to measure internal factors affecting managerial autonomy (Finkelstein et al., 2009; D. C. Hambrick & Finkelstein, 1987). In this context, organizational slack includes unsinking organizational slack, sinking organizational slack, and potential organizational slack (Bourgeois III & Singh, 1983). Unsinking organizational slack is measured by the ratio of current assets to current liabilities, sinking organizational slack is measured by the sum of administrative and selling expenses as a percentage of sales revenue, and potential organizational slack is measured by the ratio of total owners’ equity to total liabilities. Finally, the above indicators are standardized and then averaged to measure overall organizational slack. Organizational inertia, drawing on the treatment of other scholars (Xie, 2014), is measured by standardizing and summing the two indicators of employee size and the number of years of enterprise establishment, in which the total of the two indicators is added to one and then taken as the logarithm to measure.

Control Variables

Referring to other literature (Banker et al., 2014; Juniarti et al., 2021), this paper incorporates the following control variables for firm characteristics and management characteristics. Meanwhile, we control for the year effect and the individual effect. Detailed variable specifications are provided in Table 1.

Description of Variables.

Design of the Model

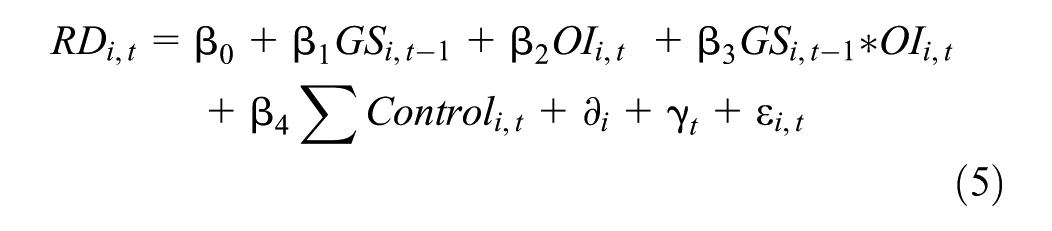

To test the effect of growth aspiration surplus on innovation investment, this paper designs the following model to test the above hypotheses:

Model (1) is used to test the relationship between growth aspiration surplus and innovation investment; Model (2) is used to test the moderating role of organizational slack between aspiration surplus and innovation investment; Model (3) is used to test the moderating role of organizational inertia between aspiration surplus and innovation investment.

Results

Descriptive Statistics

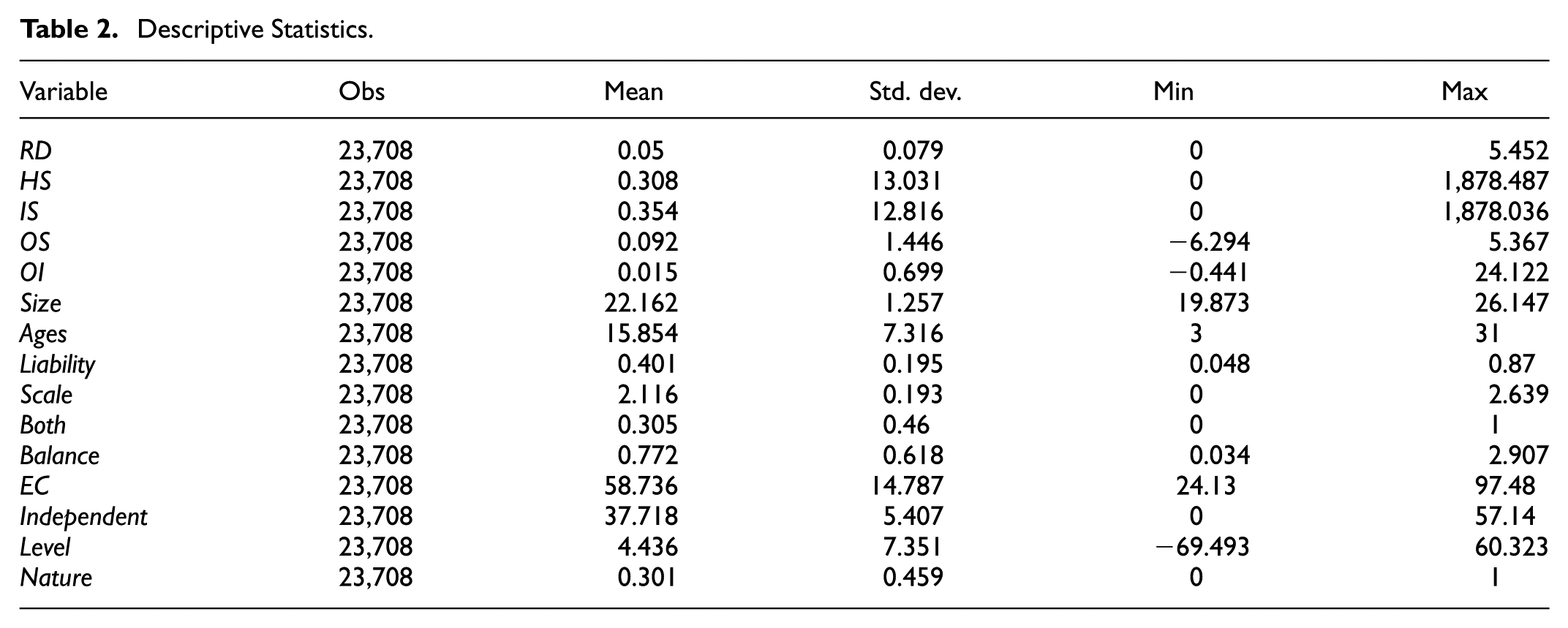

Table 2 presents the results of descriptive statistics. The results show that the mean value of historical growth aspiration surplus is 0.308, and the standard deviation is 13.031; the mean value of industry growth aspiration surplus is 0.354, and the standard deviation is 12.816. This shows that the overall growth aspiration surplus level of firms is low and that there is a large gap in growth levels between firms. For innovation investment, the mean is 0.05 and the standard deviation is 0.079. It can be seen that the overall innovation level of enterprises is generally low. Finally, the mean value of organizational slack is 0.092, and the standard deviation is 1.446; the mean value of the organizational inertia variable is 0.015, and the standard deviation is 0.699. It shows that the phenomena of organizational slack and organizational inertia are more common in listed companies.

Descriptive Statistics.

Correlation Analysis of Key Variables

Table 3 shows the results of the correlation analysis of the main variables. The results show that the coefficients with innovation investment are not significant under both historical and industry growth aspiration surplus. Organizational redundancy and innovation investment are significantly positively correlated at the 1% level (.206***), while organizational inertia and innovation investment are significantly negatively correlated at the 1% level (−.195***). However, considering the limitations of the correlation analysis, considering only the relationship between the two variables, the relationship between these variables will be statistically tested again in the following section. In addition, the variance inflation factor test (VIF) was performed on the model. The results show that the mean value of VIF both are 3.41, which is significantly less than 10, so the problem of multicollinearity is excluded.

Correlation Analysis of Main Variables.

Note. *** Indicate significance at 1%.

Benchmark Regression

To improve the reliability of the results, the models were subjected to the Housman test separately, and the results showed that the original hypothesis was rejected, so the fixed effect model was chosen to test the hypothesis.

Table 4 Column (1) shows the effect of historical growth aspiration surplus on firms’ innovation investment and Column (4) shows the effect of industry growth aspiration surplus on firms’ innovation investment. The results in column (1) show that historical growth aspiration surplus is significantly positively related to innovation investment (0.0002***), consistent with H1. This suggests that with a historical growth aspiration surplus, firm managers hold positive expectations of future growth, show incentives for upward comparisons, and will be more inclined to take risks and innovate, so H1 is confirmed. Column (4) shows that the industry growth aspiration surplus is significantly and positively related to the coefficient of innovation investment at the 1% level, consistent with H2. This suggests that under the industry growth aspiration surplus, firms enjoy a certain degree of voice in the resource and capital markets, and managers are no longer obsessed with the issue of legitimacy, but instead focus their attention on innovation in order to maintain their growth advantage, so H2 is again confirmed.

Benchmark Regressions and Moderating Effects.

Note. *** Indicate significance at 1%.

Moderating Effects Test

Table 4 Columns (2) and (5) show that organizational inertia negatively moderates the relationship between growth aspiration surplus and innovation investment (−0.0001***), consistent with H4a and H4b. This occurs because organizational inertia often follows rigid organizational processes and influences managers’ attitudes toward risk. Thus, higher organizational inertia suppresses the organization’s risk-taking capacity and reduces managers’ risk tolerance, thereby weakening the positive impact of growth aspiration surplus on innovation.

Table 4 Columns (3) and (6) show that organizational slack positively moderates the relationship between growth aspiration surplus and innovation investment (0.001***), consistent with H3a and H3b. This occurs because organizational slack alleviates resource constraints, thereby enhancing the organization’s capacity to withstand risks and managers’ willingness to take risks, enabling the organization to have both the capacity and willingness to invest in innovation.

Robustness Tests

Change the Measurement of Aspiration Surplus

Referring to the practice of other scholars (Lucas et al., 2018), α1 = .4 is reset to α1 = .5, and the historical aspiration level of growth is weighted; at the same time, drawing on the research of Li Xi and other scholars (Park, 2007), the median of the industry is used to measure the aspiration level of the industry. The main effects are re-regressed. The results are shown in columns (1) and (4) of Table 5, where the coefficients of different types of growth aspiration surplus and innovation investment are all significantly positive, which is consistent with hypotheses H1 and H2. For columns (2), (3), and (5), (6), the moderating effects of organizational inertia and organizational redundancy are tested separately, and the results are consistent with H3a, H3b, H4a, and H4b.

Robustness Analysis 1.

Note. *** Indicate significance at 1%.

Replacing the Measurement of Innovation Investment

Funding provides the economic basis for innovation, while researchers ensure that investments are effectively transformed into innovations that push to build the competitive advantage of the company. Therefore, concerning previous studies (Hong et al., 2015), the level of firms’ innovation investment is measured by the ratio of R&D personnel, and the above results are tested again. The results are shown in Table 6, and the conclusions are basically consistent with the above results.

Robustness Analysis 2.

Note. *, ** and *** indicate significance at 10%, 5%, and 1%, respectively.

Treatment of Endogeneity Problems

To solve the endogeneity problem, the article minimizes and eliminates the presence of endogeneity through several methods. First, to mitigate endogeneity caused by individual characteristics (such as corporate culture and managerial capabilities) and common time shocks (such as economic policies and industry shocks), this study adopts LSDV (Least Squares Dummy Variables with Fixed Effects) in the benchmark regression. By controlling for individual and time fixed effects, it effectively isolates the interference from individual heterogeneity and common time trends. Second, at the beginning of model design, we set the growth aspiration surplus in period t−1 and innovation investment in period t, ensuring the independent variables precede the dependent variable in time to mitigate reverse causality (Lemmon & Lins, 2003). Finally, to deal with potential omitted variable issues, we further employed two-stage least squares (IV-2SLS), re-testing using the annual industry median of growth surplus (IV-surplus) as an instrumental variable for aspiration surplus (surplus). Results indicate that the first-stage F-statistic far exceeds the critical value of 10, and the p-value for IV-surplus is <.01, satisfying the “correlation” condition. The second stage (see Column 2 of Table 7) shows that the coefficient for IV-Surplus is positive and significant at the 1% level, consistent with the core hypothesis and again ruling out endogeneity concerns.

Endogeneity Test.

Note. *, ** and *** indicate significance at 10%, 5%, and 1%, respectively.

Heterogeneity Analysis

Within China’s institutional framework, two distinct types of enterprises have emerged: non-state-owned enterprises (NSOEs) and state-owned enterprises (Juniarti et al., 2021). Generally speaking, state-owned enterprises maintain inherent political ties with the government, enjoying greater priority in resource allocation while also bearing more social responsibilities. Conversely, non-state-owned enterprises operate on a self-financing basis, prioritizing loss avoidance and maximizing economic efficiency. This paper argues that SOEs leverage their resource advantages and government background to enhance their capacity to withstand risks, enabling them to boldly pursue innovation for breakthroughs. In contrast, NSOEs operate on a self-financing basis within the economy. When their capacity to withstand risks is weaker, their loss aversion and risk-averse characteristics make them more likely to reduce innovation investment. Therefore, this study argues that the positive effect of growth aspiration surplus on innovation investment is more significant in SOEs.

Research findings indicate (see Table 8) that the coefficients for state-owned enterprises and innovation investment are not statistically significant, whereas a significant positive correlation exists for non-state-owned enterprises. This resource advantage for SOEs is a double-edged sword: when enterprises face no survival pressure, managers tend to adopt a complacent attitude, which to some extent weakens the innovation incentives derived from resource advantages. Moreover, the social responsibilities of state-owned enterprises may lead them to prioritize allocating resources toward fulfilling political missions rather than pursuing risky innovations. In contrast, NSOEs, which constantly face financing constraints and survival pressures, can leverage the available resources and social reputation generated by surplus to invest these resources into innovation, thereby consolidating their market share. This explains why the outcome differs from expectations.

Heterogeneity Test.

Source. The Authors’ own work.

Note. ** and *** indicate significance at 5% and 1%, respectively.

Discussion

Research Conclusions

Based on the theory of corporate behavior, this paper focuses on the impact of feedback from growth on corporate innovation and the role played by internal managerial autonomy between the two using a sample of China’s A-share listed companies from 2008 to 2021, and ultimately draws the following conclusions: From the perspective of main effects, both historical and industry growth aspiration surpluses are significantly positively correlated with corporate innovation investment. Historical growth aspiration surpluses often generate the available resources, increasing an organization’s risk tolerance and making managers more willing to pursue risky innovations to achieve goals. Meanwhile, industry growth aspirations surpluses intensify competitive pressures, prompting firms to engage in distant search and send positive market signals, thereby elevating external expectations and managerial innovation motivation. Thus, both historical and industry growth aspiration surpluses drive corporate innovation by enhancing risk-taking willingness and external expectations. Regarding moderating effects, organizational slack strengthens the positive correlation between historical (or industry) growth aspiration surpluses and innovation investment. Redundant resources not only alleviate resource constraints on innovation activities but also increase managerial freedom in resource allocation, enabling firms to better withstand the risks of innovation failure. Conversely, organizational inertia weakens this relationship. Higher inertia levels lead to rigid organizational structures and inflexible resource allocation, reducing willingness to take innovation risks and ultimately suppressing the innovation opportunities generated by growth surpluses.

In summary, this study extends existing research in three key areas. First, by integrating corporate behavior theory, it incorporates firm growth into the performance feedback framework, thereby enriching our understanding of the relationship between aspiration gaps and innovation. Unlike previous feedback studies that primarily focused on profitability metrics (Keil et al., 2023; Martínez-Noya & Garcia-Canal, 2021; Yang & Chen, 2024; Zhao et al., 2024), this study emphasizes that growth has become a core condition for firms to attract resources and establish competitive advantages in China’s transition economy. It reveals whether firms adopt aggressive or conservative decision-making under growth surplus conditions, thereby deepening the “aspiration—feedback—decision” logic of organizational behavior theory. Second, this study distinguishes between historical and industry-specific types of surpluses, revealing how differing reference points for expectations have differential impacts on firms’ innovation investments. Compared to previous research using singular or composite feedback indicators (W. Chen et al., 2022a; Yang & Chen, 2024; Z. Zhang et al., 2024), this classification not only emphasizes the diversification of reference points but also explains how different types of growth surpluses generate variations by influencing firms’ risk tolerance and innovation motivation. This finding extends the discussion on “reference point diversification” within performance feedback theory. Finally, this paper incorporates managerial autonomy into the research framework linking growth feedback and innovation, highlighting the role of internal factors such as organizational slack and organizational inertia in its mechanism. Unlike previous studies focusing on external managerial autonomy related to national and industry characteristics (Saeed et al., 2025; Wangrow et al., 2015), this responds to scholars’ growing attention to internal managerial autonomy (Gao et al., 2024; Magerakis, 2022). Research indicates that internal autonomy can either amplify the positive impact of growth surpluses on innovation or diminish its effects due to inertia. This not only expands the boundaries of understanding managerial autonomy but also demonstrates that the influence of growth feedback on innovation exhibits significant contextual dependence.

Managerial Implications

Based on the above findings, there are some practical suggestions for future business operations:

(1) Set reasonable growth aspirations to create effective innovation pressure. Companies should dynamically adjust their targets based on growth performance, avoiding both low targets that lack innovation motivation and overly ambitious goals that cause excessive pressure. Therefore, enterprises can periodically benchmark against industry averages and adjust targets in line with their historical growth curves. This approach enables managers to maintain innovation enthusiasm under “moderate pressure,” allowing them to capture market shifts and sustain competitive advantages.

(2) Fully mobilize the available resources to support innovation activities. Specifically, enterprises can establish specialized innovation funds and create cross-departmental flow positions to ensure that innovation activities remain resource-protected even when encountering uncertainty or failure. In the meantime, management should value the dynamic management of available resources to avoid inefficient utilization, enabling redundancy to truly serve as a “buffer” for innovation investment.

(3) Guard against organizational inertia and avoid falling into the “success trap.” Managers should conduct regular strategic reviews to examine and update the company’s business models, processes, and rules, thereby breaking path dependencies. Simultaneously, managers should also encourage rotations within management or external learning opportunities to enhance their sensitivity to environmental changes and adaptability.

Research Limitations and Outlook

This paper examines the relationship between growth aspiration surplus and innovation based on the theory of corporate behavior, but it has certain limitations: First, using Chinese listed companies as the sample, the findings may be limited in applicability to other countries or regions due to factors such as institutional environments and levels of economic development. Future research could verify the robustness of these results using a multinational sample. Second, the growth rate of main business revenue is merely one indicator among many for measuring growth, and innovation is only one strategic option for enterprises. Future research could explore how the surplus under different growth measures affects other corporate behaviors—such as digitalization, investment, and mergers and acquisitionsto enrich performance feedback theory. Finally, this study examined only the innovation investment behavior of enterprises under a growth aspiration surplus, without exploring whether such investment can translate into effective innovation outputs. In fact, innovation is not merely a decision-making issue of “whether to invest,” but also an execution issue of “whether to succeed.” In this process, the attitudes and behaviors of ordinary employees play a significant role, and their resistance may weaken the effectiveness of innovation implementation. Therefore, future research could consider incorporating “employee resistance” into the research framework, examining the relationship between innovation investment and innovation performance. By integrating strategic decision-making with the execution process, we can better reveal the full chain of logic through which growth aspiration surplus influences corporate innovation.

Footnotes

Acknowledgements

We are grateful to Jintao Zhang for his valuable suggestions, and his patience.

Ethical Considerations

There are no human participants in this article.

Consent to Participate

This article does not contain any studies with human or animal participants.

Author Contributions

The conceptualization and design of the study were collaboratively developed by all authors. The initial draft of the manuscript was composed by Shanshan Liu, with subsequent versions receiving insightful feedback from Shanshan Liu and Gengxi Xu. And l am grateful to Yugang Li for his comments and review of the manuscript.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by Humanities and Social Sciences Research Fund of the Ministry of Education (Grant numbers [20YJA630039]).

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.