Abstract

The complex climate risks and China’s “dual carbon” goals will definitely exert a far-reaching influence upon the growth of China’s heavily polluting firms. This paper analyzes climate sentiment’s impact on China’s bond market using the KMV model. The model predicts default probability by linking equity to asset values via Black-Scholes, providing a scientific basis for credit risk quantification in financial decisions and regulation. Meanwhile, a Naive Bayes model is employed to construct climate sentiment. As a Bayesian-based machine learning method, it is widely used in text analysis for its solid theory, simplicity, efficiency, and objectivity. We obtained over 220,000 climate-related posts as our sample by crawling the financial commentary stock bar of Eastmoney Net, with the time span ranging from January 1, 2014 to December 31, 2022. The results show that as climate sentiment becomes more positive, the credit default risk of listed heavily polluting companies rises. Climate sentiment increases the default risk of heavy polluters mainly through increased financing constraint, financing cost and market competition. The impact of climate sentiment on raising corporate default risk is greater for non-state-owned firms, larger size, and higher stock volatility.

Introduction

2023 Global Risks Report indicates that the three major risks confronting the world in the short term are cost-of-living crises, natural catastrophes and extreme weather, and geo-economic rivalry. Climate change is considered to have serious consequences and will be the greatest crisis facing humanity in this century. It has already led to extreme weather and climate events on a global scale, with rapid impacts on agricultural production, human health, ecosystems, international security, energy economy and more (Agovino et al., 2019; Friel et al., 2011; Malhi et al., 2020; McClanahan & Brisman, 2015; H. Li et al., 2023). Moreover, as global warming continues to escalate, the intersection of climate and non-climate risks will generate integrated and cascading risks that are more complex and difficult to manage. As a highly impacted country by climate change (Jia et al., 2022), China has explicitly proposed and committed to “striving to achieve carbon peaking by 2030 and carbon neutrality by 2060.” This signifies China will have accomplished the greatest global cut in carbon emissions. As the world’s top carbon dioxide emitter and energy consumer (Mi et al., 2017), China clearly needs to make tremendous efforts. To ensure the timely realization of the “dual-carbon” target, China is therefore required to introduce and improve a series of regulations and policies. Against this backdrop, the high carbon emission nature of heavy polluters makes them more susceptible to the direct impact of relevant regulations and policies, thus facing uncertainty in the business environment and potential default risks.

Corporate debt defaults not only disrupt the firms’ operation and development, but also most likely lead to market pessimism and systemic risks in the financial market, with these consequences ultimately impinging on a country’s economy in terms of its sustainable and healthy growth. According to the Wind database, the count of bond defaults in China hit a peak of 213 in 2019, with default value of 172.084 billion yuan. In 2020, the count of bonds in default was 175, and the default amount reached a record high of 189.413 billion yuan. Although the number and volume of bond defaults has declined over the past 2 years, the frequent occurrence of climate events and the prominence of environmental issues have forced firms to deal with new challenges. Because corporate default risk is no longer determined solely by traditional commercial factors, but also by a combination of factors such as public opinion and investor expectations.

Hence, investigating the impact of climate sentiment on the default risk of polluting enterprises is of great significance. Theoretically, on the one hand, existing research on corporate default risk mainly focuses on traditional variables such as financial indicators and industry cycles, with limited quantitative analysis of climate-related non-financial factors. As a “soft constraint,” the impact mechanism of climate sentiment on corporate credit has not yet formed a mature theoretical framework and needs to be supplemented by empirical research. On the other hand, climate sentiment involves the intersection of environmental sociology, behavioral finance, big data analysis, and other fields. Such research helps construct a more realistic “climate-sensitive” theoretical system for financial risk.

In fact, extreme climate phenomena such as hurricanes, hailstorms, and sandstorms directly affect the daily production and operation of highly polluting enterprises (e.g., factory shutdowns and supply chain disruptions), while public concern about climate issues—“climate sentiment”—may amplify corporate risks through indirect channels such as public opinion and policies. For example, during the 2023 European energy crisis, public criticism of fossil fuel dependence heightened, leading to a surge in financing cost for traditional energy companies and leaving some facing debt defaults. Studying the correlation between these two factors can help identify the transmission path of “climate sentiment-corporate risk” in advance, providing practical evidence for risk prevention. Most heavily polluting enterprises operate in high-leverage, long-cycle industries (e.g., coal, cement), and their defaults could spread to the financial system and macroeconomy through credit chains and industrial chains. For instance, the default of a large coal enterprise might increase bank bad debts, disrupt the fund chains of upstream and downstream small and medium firms, plus even trigger regional financial risks. As an emerging factor influencing corporate credit, climate sentiment needs to be integrated into risk monitoring frameworks to avoid “black swan” events.

Therefore, this paper primarily explores whether climate sentiment has an effect on the debt breach behaviors of pollution-heavy companies. To examine this hypothesis, the following research questions were developed to guide this study.

The possible contribution of this study includes three aspects. For the first time, climate sentiment is incorporated into credit risk evaluation framework of polluting firms, extending environmental sociology perspective of credit risk theory. By focusing on “polluting enterprises” as a high climate-risk group rather than generalized ESG enterprises, this study accurately captures the “targeted impact” of climate policies. Integrating natural language analytics, machine learning and traditional econometric methods, it constructs a complete technical framework of “sentiment quantification causal identification mechanism deconstruction.” Engaging with the “climate financial market failure theory,” this research examines whether market sentiment pricing mechanisms can correct the negative externalities of polluting enterprises, providing empirical evidence for the boundary of the “invisible hand” in climate governance.

First, this paper introduces the concept of “climate sentiment” (Santi, 2023), which is a relatively new but potentially important factor. It measures favorable or unfavorable stances investors toward climatic shifts. We use Python to capture comments about climate change on the financial commentary stock bar of Eastmoney Net to construct the climate sentiment, which is relatively lacking in the existing literature. Several factors lead this paper to select the posts from financial commentary stock bar. Compared with other popular forums, financial commentary can more effectively represent the real performance of stock market shareholders. There is a large volume of data in the post financial commentary stock bar, easy to apply data mining to gauge investor sentiment. Specifically, this paper chooses climate change-related postings made on Eastmoney’s Stock Bar Forum during the period from January 1, 2014 to December 31, 2022 as the subject of analysis. We build the climate sentiment index via the three steps below: First, we employed Python to pull 4.8 million messages off the stock forum. Second, we used Naive Bayes method to tag and rate textual data within full sample set. Finally, we conducted statistical analyses on the sentiment categories of each sample and developed monthly climate sentiment ratings. To make sure that climate sentiment mirrors the sentiment of a wider range of investors, we performed orthogonalization on climate sentiment and the stock forum’s overall sentiment by adopting Santi’s (2023) approach.

Second, this paper explores the connection between climate sentiment and default risk of highly polluting listed enterprises in China. Behavioral finance models indicate that investor sentiment can potentially deviate prices from their underlying fundamentals (De Long et al., 1990). We extend research into the cross-market impact of climate sentiment on the bond market, which makes up for the deficiency of existing literature that centers on the stock market. Through two-way fixed effect regression analysis, we find that the default risk of heavily polluting listed firms increases when climate sentiment becomes more positive. Mechanism tests show that climate sentiment exacerbates corporate default risk by raising financing costs, intensifying funding constraints, plus increasing market rivalry. Heterogeneous analysis reveals that its role in fueling default risk is more salient among non-state firms, larger-scale enterprises, and those having higher stock price volatility.

Finally, combined with the research of other scholars, we select the variables of quarterly KMV model to enrich literature on measurement methods of quarterly default probability. Although there are many studies using KMV model to gauge corporate default risk, most of them focus on annual data. While some studies have proposed the measurement method for quarterly probability of default, there is still no consensus on the specific parameter setting. Our research provides a useful reference for the parameter setting of the quarterly KMV model.

In conclusion, this study holds implications in theoretical, practical, and methodological aspects. Theoretically, it breaks through the limitation that existing research on corporate default risk mostly focuses on financial indicators, incorporates the “soft constraint” factor of climate sentiment into the credit risk assessment framework for polluting enterprises, and integrates interdisciplinary perspectives such as environmental sociology and behavioral finance to construct a technical framework of “sentiment quantification—causal identification—mechanism deconstruction.” This not only addresses the deficiency in the quantitative analysis of climate-related non-financial factors and improves the “climate-sensitive” financial risk theoretical system, but also provides a reference paradigm for subsequent research on similar non-financial risk factors. Practically, heavily polluting enterprises, especially non-state-owned ones, large-scale enterprises, and those with high stock price volatility, need to pay attention to the impact of climate sentiment and cope with potential default risks by optimizing financing structures and enhancing risk resistance capabilities. Regulatory authorities should incorporate climate sentiment into risk monitoring systems, formulate differentiated policies for enterprises of different natures, and improve climate-related information disclosure systems. Meanwhile, the financial market needs to refine the climate risk pricing mechanism to correct the negative externalities of polluting enterprises and reduce the occurrence of “black swan” events, thereby jointly safeguarding financial stability and the sustainable development of the macroeconomy. Methodologically, the parameter setting method of the quarterly KMV model adopted in this study provides practical reference for subsequent research on quarterly default probability, contributing to the improvement of corporate default risk measurement methods and enhancing the timeliness and accuracy of risk assessment.

This study is structured thus: Section 2 surveys related literature and conducts theoretical analysis; Section 3 explains the construction methods of the climate sentiment index and KMV model, while setting up the regression model; Section 4 presents relevant data; Section 5 examines and discusses the empirical results; Section 6 puts forward study conclusions and policy recommendations based on the empirical findings.

Literature Review and Theoretical Analysis

Literature Review

Factors Influencing the Risk of Corporate Debt Default

Default risk, or credit exposure, denotes the chance a debtor will fail to repay its debts promptly. Since the default of the “11 Chaori Bond,” corporate debt default has become one of the most researched topics in China. To jointly address the potentially serious outcomes of climatic shifts, China has proposed a “dual-carbon” goal. To achieve this goal, Chinese firms, especially heavy polluters, must actively respond to green policies and take the initiative to bear the corresponding pressure to reduce emissions. This brings great uncertainty to the operation and development of firms, and how to effectively assess and prevent corporate debt default has become an urgent issue.

Scholars have increasingly focused on the factors influencing corporate defaults. Studies examining the determinants of firms’ default risk focus on three dimensions: macroeconomic, market, and internal firm-level factors. Giesecke et al. (2011) empirically analyzed the factors influencing bond default risk using company bonds from 1866 to 2008 as research samples. The findings indicated that changes in the country’s GDP, stock yields and their volatility are all strongly linked with bond default risk. X. Zhang et al. (2020) analyzed 981 Chinese listed companies from 1998 to 2013 to identify factors impacting default risk. They found that company-specific factors (leverage, liquidity, firm size) and macroeconomic indicators (interest rate, stock return) influenced default risk in China. H. Li et al. (2022) discovered that higher ESG ratings reduce corporate default risk, with the alleviating effect becoming stronger as default risk’s time structure lengthens. Liu et al. (2023) observed that China’s climate policy uncertainty (CPU) has a marked positive impact on firms’ default risk, and this impact tends to systematically strengthen as the term structure of default investigations lengthens. He et al. (2023) studied Chinese A-share listed firms’ 2011 to 2020 data, finding that Fintech advancements notably decreased corporate debt default risk.

Default risk assessment models are primarily include Z-score method (Altman, 1968), credit rating method (Kraft, 2015) and KMV model. Among them, the KMV model has become a widely adopted measure of corporate default risk since it was proposed by KMV corporate in San Francisco, USA in 1997. Built upon option pricing theory, it not only can effectively quantify corporate default risk through the collection of financial data, but also prospectively and dynamically assess the changes in corporate credit risk. The academic community has conducted multiple studies on the validity of this model. Crosbie and Bohn (2003) utilized the KMV model to evaluate the credit risk of financial enterprises, and their research demonstrates that it can efficiently gauge bond default risk and the credit status of firms before and after bankruptcy. Gokbayrak and Chua (2009) and Kara et al. (2019) examined non-financial enterprises in Asia and Europe via the KMV model, and the findings indicated that the EDF computed by this model could precisely gauge the default rate of listed firms across various regions as well as distinct periods. Zeng et al. (2022) observed that integrating ESG ratings into the KMV model enables effective evaluation of the factors influencing default risk in online finance. In addition, Basel II had publicly recommended the KMV model as a template for the application of internal rating methods for credit risk management. It is evident that the KMV model employed in this study can effectively measure the level of corporate default risk.

Investor Sentiment and Climate Sentiment

Since the 1980s, there have been many financial market irregularities that run counter to the efficient market hypothesis. Many empirical studies on market effectiveness have highlighted that it is not enough to consider only fundamentals because investors are affected by noisy information such as irrational behavior in their decision-making process (Barberis et al., 1998; De Long et al., 1990; West, 1988). This has spurred the emergence of behavioral finance, a field rooted in investors’ psychological activities during specific investment decision-making processes. As the center of behavioral finance research, investor sentiment has garnered substantial academic attention.

Research on investor sentiment has predominantly focused on the equity market, covering stock returns (Antweiler & Frank, 2004; Ranco et al., 2015), market volatility (Bollen et al., 2011; Herrera et al., 2022), stock liquidity (Ammari et al., 2023) and asset prices (Qadan & Nama, 2018; Yang & Zhou, 2015), etc. Previously, analyzing investor sentiment has tended to ignore climate change (Cody et al., 2015; Dunz et al., 2021; Loureiro & Alló, 2020). Additionally, research into the cross-market influence of investor sentiment remains relatively limited. The cross-market effect of investment sentiment refers to the fact that high or low investor sentiment not only impacts the equity market, but in addition spreads to the bond marketplace. On the one hand, the value of stocks and bonds has a common information base, which contributes to the linkage effect between equity and debt market prices (Fleming et al., 1998). On the other hand, as one of most important forms of corporate financing, equities and bonds feature distinct risk traits, which in some cases may cause the mutual flow of funds between the two markets, the so-called “seesaw effect” (Goyenko & Ukhov, 2009). For this reason, research on investor sentiment and climate sentiment should not only be limited to the stock market, but should be extended to the bond market for cross-market test, so as to understand the interaction and influence between different markets more comprehensively.

Currently, proper quantification of climate sentiment is a key issue. Researchers have adopted various methods to construct indicators of investor sentiment, including questionnaires (Brown, 1999; Sayim et al., 2013), market trading data (Baker & Wurgler, 2006; Yang & Zhou, 2015), social media comments (Dahal et al., 2019; Sun et al., 2021). Social networks have become an increasingly important channel for investors to receive and disseminate information. Their interactive discussions on online platforms have turned into a significant driver behind stock market sentiment and investment choices, and their influence on the entire market is not to be overlooked (Da et al., 2015; Kim & Kim, 2014). Therefore, this paper adopts Santi’s (2023) methodology to gauge climate sentiment by analyzing climate-related comments in stock forums.

To sum up, it is clear that home and foreign scholars have produced extensive literature on investor sentiment and corporate default risk, yet research on the connection between the two remains relatively scarce. Although some researches have revealed that investor sentiment impacts corporate default risk, some scholars also proposed to use Twitter to measure climate sentiment. However, there are very limited articles on the cross-market effects of climate sentiment upon debt market default danger. This study’s innovative aspect lies in investigating the inter-market impact of climate sentiment upon debt market default risk, with capital market serving as a bridge. It not only provides an enrichment to the papers in relevant fields, but in addition offers a helpful guide for effectively assessing corporate default risk under the climate change scenario.

Review of Literature

The mechanism by which investor sentiment influences the bond market is diverse: Sentiment among stock investors notably impacts the returns of high-liquidity, high-credit-risk corporate bonds, as well as portfolio returns (C.-W. Wu, 2021). It exerts a negative effect on bond returns through over-investment-induced default risks and capital flow channels, and the bond market’s response aligns with rational logic (W. Chen, 2021). The news sentiment dispersion can predict bond returns (Isakin & Pu, 2023). The deterioration of investor sentiment triggers risk-averse behaviors, leading to a rise in bond co-movement (Bethke et al., 2017). In emerging markets, a negative association exists between investor sentiment and sovereign bond returns, with liquidity frictions intensifying this relationship (Y. Li, 2021). Green bonds’“green premium” is notably affected by media-related sentiment, with printed media exerting a more distinct influence (Fu et al., 2024). Additionally, firm-level sentiment is positively correlated with bond liquidity, and negative sentiment exerts a stronger impact (Dixon, 2021). Stock market sentiment also influences bond fund investment decisions and returns (Islam), whereas how retail investor sentiment affects bond volatility differs according to market conditions (Hadad et al., 2024).

It is noteworthy that in the dynamic development of financial markets, the implication of investor sentiment continues to expand as climate issues gain prominence. As a subset focusing on climate factors extracted from the overarching concept, climate sentiment is embedded in investment decisions through the logical hierarchy of “universal set—subset.” This dimension corresponds to specific dimensions such as climate policies and environmental risks. It is formed by investors’ cognitive processing of signals like carbon neutrality policies and green bond premiums to shape expectations. While retaining the irrational characteristics of investor sentiment, it interacts with other emotional components through a unique logic to influence asset pricing. This transmission mechanism not only uncovers the micro-level channel through which climate factors are incorporated into financial decision-making but also offers a fresh angle for the aforementioned bond market research. Specifically, by isolating the climate sentiment dimension, it becomes feasible to precisely analyze the cross-market impact mechanisms of environmental issues on bond default risks, asset interlinkages, and other aspects.

Drawing on the above research context, this paper constructs a theoretical framework of “climate sentiment—default risk of heavy-polluting enterprises”: Climate sentiment affects the stock prices of heavy-polluting enterprises through investors’ demand differentiation for clean and polluting stocks, which in turn transmits to their financial conditions and increases default risk. This is achieved through a dual mediating pathway: On the one hand, the escalation of climate sentiment leads to poor performance of polluting stocks, driving up equity financing cost. When enterprises shift to debt financing, creditors increase costs and constraints, forming a transmission chain of financing constraint and costs. On the other hand, investors’ preference for clean enterprises enables these firms to gain financing and market advantages, intensifying the competitive pressure on heavy-polluting enterprises and thereby affecting their operational and financial conditions. In terms of heterogeneity, climate sentiment exerts a more notable impact in increasing default risk for non-state enterprises due to their greater reliance on market financing, large enterprises because of stricter environmental regulations and deeper impacts of climate risks, and enterprises with high stock volatility owing to higher market risks and financing uncertainties.

Theoretical Analysis

Climate Sentiment and Default Risks of Heavy Polluting Enterprises

The rising occurrence of extreme weather events triggered by climate change imposes both direct and indirect effects on global socio-economic activities, posing a severe threat to nations’ sustainable development and resource governance. Mitigating climate change and adapting to its impacts have become urgent tasks for the global community and Governments. To this end, China has proposed a “dual-carbon” goal and is gradually introducing and implementing a series of green and low-carbon policies. In this context, heavily polluting firms, as micro-entities in the implementation of the “dual-carbon” goal, are faced with the challenge of mitigating emissions and transforming their operations, but also have the opportunity to adapt to the market and regulations by adopting environmentally friendly measures to minimize business risks and improve sustainability.

Climate sentiment mirrors investors’ stances on climate change—perspectives unlinked to established realities (Baker & Wurgler, 2006)—yet they notably shape investors’ specific investment choices. As climate sentiment rises (falls), irrational investors’ demand for clean stocks is likely to increase (decrease), which in turn lowers their relative demand for polluting stocks. For polluting companies, a poorly performing stock can undermine the overall financial well-being of the enterprise, which in turn elevates the probability of bond nonpayment (Dickerson et al., 2023; Gilchrist et al., 2009). Given this, the subsequent hypothesis is proposed:

Climate Sentiment and the Default Risk of Heavy Polluting Firms: The Role of Financing Constraint, Financing Cost and Market Competition Degree

Rising climate sentiment has led investors to favor cleaner stocks, resulting in the underperformance of heavily polluting stocks. Bonds and stocks are generally seen as substitutes. Weak stock performance can push up the cost of equity financing, prompting companies to opt for debt financing instead, and the opposite holds as well (Zuo et al., 2023). Yet investors respond in the contrary manner: when stock performance is poor, not only does equity financing cost go up, but debt financing cost rises as well. In brief, a company’s stock and bond financing options do not offset each other under identical conditions; instead, they exhibit a “positive feedback” relationship characterized by consistent performance trends. This means that underperforming firms need to consider risks and pressures in other markets (K. Wu & Lai, 2020). Climate sentiment is an indicator measuring investors’ positive or negative attitudes toward climate change issues, directly reflecting investor confidence. As carbon disclosure policies (e.g., mandatory data reporting) alter investor perceptions, such policy changes are inherently embedded in climate sentiment metrics. A. Xu et al. (2025) show that Chinese heavy polluters with complete carbon disclosures reduce debt financing cost by 1.2%, illustrating that climate sentiment—shaped by disclosure policies—alleviates information asymmetry, thereby improving refinancing conditions for polluting firms. This indicates that policy-driven climate sentiment changes will affect corporate refinancing. We have grounds to believe that when polluting stocks perform poorly, investors may raise the costs and restrictions related to debt default for these companies, thereby elevating their likelihood of default.

As for the degree of market competition, if investors are more optimistic about clean shares, they may have an advantage in financing and market competition. This could adversely affect polluting companies, heighten their competitive pressures, impact their operational and financial strains, and in turn boost their likelihood of default. Li et al. (2022), drawing on data from China’s A-share listed firms, found that air pollution notably lowers stock liquidity via the mechanism of investor sentiment, with this effect being particularly pronounced among non-heavy-polluting enterprises, manufacturing sectors, and listed companies in medium-sized cities. This indicates that investor sentiment may alter the financing environment and competitive landscape of different types of enterprises in polluting industries within the capital market. As a climate-focused sub-dimension of investor sentiment, climate sentiment may similarly influence the capital acquisition capabilities and market competitiveness of firms in polluting industries through an analogous logical pathway. Given the above, our hypothesis is as follows:

Heterogeneity of Ownership, Firm Size, and Stock Volatility

Variations in ownership types inherently result in disparities in companies’ access to financial resources and bank financing support. Highly polluting SOEs often serve government political or social objectives and therefore are subject to stricter government regulation and policy requirements. But they are also more prone to obtain financial resources, subsidies and technical assistance from the government, a factor that makes them relatively less prone to financial crises.

In contrast, highly polluting non-SOEs are typically more dependent on market-based financing, which makes them more susceptible to climate change concerns and sentiments among investors and financial institutions. The growing market focus on factors such as environmental and social responsibility implies that shifts in climate sentiment may exert an impact on the financing and operations of non-SOEs. Because the market increasingly tends to finance firms that can demonstrate excellence in sustainable and environmental performance. Thus, we propose the following hypothesis:

Highly polluting firms boasting large market capitalization exert a more significant influence on the overall market than those with small market capitalization, and as a result, they typically face stricter environmental regulations and regulatory oversight. If they fail to meet regulatory requirements, they may face fines, lawsuits and the suspension of their operations and fall into debt. At the same time, highly polluting firms are often vulnerable to climate-related risks that can lead to production disruptions, supply chain problems and financial losses. The size and complexity of large capitalization firms means that these risks are probably having a greater impact on them. In light of the above, the hypothesis is proposed as follows:

Bevan and Garzarelli (2000) argue that there are many factors affecting bond default, among which stock volatility is positively correlated with bond default, and Kuehn and Schmid (2014) hold a similar view. High volatility means that asset prices can fluctuate sharply, which exposes firms to greater market risk and funding uncertainty. Against the backdrop of increasingly severe climate conditions, highly polluting firms are difficult to plan and manage their financial position effectively. Because future revenues and costs are hard to predict. In addition, high volatility can also result in higher financing cost when investors become more cautious and demand higher risk premiums. This uncertainty and tight financing makes it easier for firms to get into financial trouble, which increases the likelihood of default. As a result, an increase in volatility is often seen as a signal that firms face greater operational and financial risks, exacerbating their potential risk of default. Based on the above, we propose hypothesis as follows:

As illustrated in Figure 1, this study proposes a series of hypotheses based on theoretical derivation: First, Hypothesis H1 is put forward, stating that the more positive the climate sentiment, the higher the default risk of highly polluting enterprises; Hypothesis H2 further reveals that this effect is transmitted through financing constraint, financing cost, and market competition; Hypotheses H3a, H3b, and H3c supplement from the perspective of heterogeneity—H3a indicates that the impact is more significant for non-state enterprises due to their greater reliance on market financing; H3b shows that large enterprises are more prominently affected due to strict supervision and easy amplification of risks; H3c emphasizes that enterprises with high stock volatility exhibit a more obvious effect due to the intensification of financing cost and uncertainty. These five hypotheses deepen the analysis layer by layer from the main effect to the intermediary mechanism and then to heterogeneity, forming a complete logical chain.

Theoretical framework.

Methodology

Corporate Default Risk: KMV Model

In this study, the expected default frequency obtained from the KMV model is selected as the surrogate variable of firms’ default risk (Merton, 1974). The fundamental concept of this model is presented in Figure 2. Its core idea is to regard a company’s equity as a call option. If an enterprise’s debt level exceeds the asset worth determined by the Black-Scholes option valuation model on the debt maturity date (Black & Scholes, 1973), the firm is deemed to default; otherwise, it does not.

Basic idea of KMV model.

This model has good agreement and foresight in measuring corporate default risk, but the following assumptions need to be satisfied in calculation:

“Perfect” and frictionless markets: no transaction fees, taxes, divisible assets, rational traders, prices unaffected by individual actions, and free access to complete information;

Adhere to the Miller-Modigliani theory (MM theory), the capital composition does not influence the firm value;

Debt structure: an enterprise has merely a single type of debt, that is, zero-interest bonds with a term of T, and the firm cannot issue additional debt, sign repurchase agreements or pay dividends;

The change in the enterprise’s market worth is governed by geometric Brownian motion, and the stock price process complies with the ITO process.

The KMV model typically follows these three steps to gauge a firm’s default risk. First, the Black-Scholes option valuation formula is applied to derive a firm’s asset worth and asset volatility, based on stock value, maturity period, book value of debts, equity volatility, and risk-free rate of interest. Second, establish the default threshold and calculate the default distance. Third, the expected default rate is obtained from the correlation between default distance and expected default frequency. The specific calculation steps are as follows.

Calculate the Firm’s Asset Value and Asset Value Volatility

In this study, the Black-Scholes option valuation formula is applied to corporate asset value (

Where,

Specifically, we first retrieve relevant stock information and financial figures of listed firms from the WIND database to calculate Equity and Debt; Secondly,

Calculate the Firm’s Default Point and Default Distance

The KMV approach assumes that the total liabilities of firms only include short-term liabilities

Where,

Default distance denotes the relative gap between the default trigger point of a listed enterprise and the projected asset value in the future. The larger the default distance, the lower the probability of the firm defaulting, and the smaller the risk of default. Otherwise, the likelihood of default is higher.

Calculate the Expected Default Frequency of the Firm

A cumulative standard Gaussian distribution of the default distance

The association between

Where,

Model Construction

Drawing on existing research studies (Sun et al., 2020, 2023), this paper employs a two-way fixed effects model to investigate the influence of climate sentiment on the default risk of heavily polluting firms in China. The particular form of this model is as follows:

Where,

To further analyze the pathway through which climate sentiment affects default risk, this paper employs the stepwise regression approach to examine the mediating role (Baron & Kenny, 1986). The model is as follows:

Where,

Data

Data on Heavy Polluting Firms

This paper investigates the link between default risk and climate sentiment using data on heavily polluting A-share listed companies in the Chinese market. The data spans from Q1 2014 to Q4 2022. Following the industry classification criteria established by J. Xu et al. (2021) and Zhong et al, (2022), and in line with the 2012 industry categorization criteria issued by the China Securities Regulatory Commission (CSRC), we define heavily polluting industries by the following sector identifiers: B06, B07, B08, B09, B10, B11, C15, C17, C18, C19, C22, C25, C26, C27, C28, C29, C30, C31, C32, and D44. Specific industry information is shown in Table 1. Stock information and firm financial data are derived from the WIND and CSMAR databases.

Name of Heavily Polluting Industries.

Note. China’s heavy pollution industry classification code and name, refer to the 2012 CSRC industry classification and some literatures.

The data processing procedures of this research were carried out as follows: (1) Data samples of ST, ST*, and delisted firms were excluded; (2) Data samples whose listing year is later than 2014 are removed; (3) Exclude data samples where data on major research variables is missing; (4) To reduce the effects of outliers, all continuous variables were winsorized at the 1st and 99th percentiles. This adjustment successfully lessened the influence of extreme values, yielding a final sample of 17,964 observations.

Data on Climate Sentiment

Despite cross-country variations in investor behavior, extensive research (Barber & Odean, 2013; Kaniel et al., 2008; Kumar & Lee, 2006) demonstrates that retail investors are more susceptible to psychological biases and sentiment. The influence is particularly salient in China’s capital market, which is largely driven by individual investors (Han & Shi, 2022). Thus, constructing a climate sentiment index requires selecting a professional financial commentary forum with significant retail investor participation. Among China’s online stock forums—including Eastmoney Stock Bar, Sina Stock Bar, and Hexun Forum—Eastmoney Stock Bar has been found in relevant studies to outperform others in both retail investor base and activity levels. Notably, its four popular theme bars (Stock Market Practice Bar, Financial Commentary Bar, Shanghai Composite Index Bar, and Shenzhen Component Index Bar) have preserved all post records for nearly two decades, enabling comprehensive information acquisition. Thus, this study constructs an investor investor sentiment index using climate change-related comments extracted from the Eastmoney Stock Bar Forum, spanning the timeframe from January 1st, 2014, through December 31st, 2022. The development of this index follows a four-step methodology: First, Python-based web crawling techniques are employed to systematically collect user comments from the Eastmoney Stock Bar Forum. Second, the raw textual data undergoes rigorous cleaning and preprocessing procedures. Third, sentiment analysis on the preprocessed comments is carried out using machine learning algorithms. Finally, the investor climate sentiment index is built by aggregating and normalizing the quantified sentiment scores in a combined manner.

In this study, 4.8 million records from the Eastmoney Stock Bar forum are gathered using Python’s requests and Beautiful Soup libraries. Given that post titles directly reflect investors’ viewpoints, they are selected as the primary data for sentiment analysis. For constructing a reliable investor sentiment indicator, rigorous data preprocessing is conducted. Redundant and advertisement—laden content is removed. The Jieba library, integrated with a stop—word list, is used for word segmentation. Subsequently, 10,000 posts were randomly selected from the dataset of 4 million records and manually categorized into positive and negative sentiment labels. The sentiment analysis model then assigned scores to this data, where values approaching 1 indicate positive sentiment, while those closer to −1 reflect negative sentiment elicited by events. In addition, from the aforementioned 4 million text data entries, the study further conducted screening based on core climate-related keywords such as “climate change,”“extreme weather,”“natural disasters,” and “global warming,” ultimately obtaining 220,000 valid climate-related text data entries.

Sentiment analysis methods generally fall into two categories. The first is the sentiment dictionary method (Ballinari & Behrendt, 2020; Renault, 2017), which is simple and efficient—relying on predefined dictionaries to judge text sentiment. However, this approach ignores contextual information, leading to low accuracy and poor adaptability. The second category is machine learning methods, which require training on sentiment-labeled datasets. Due to their better fitting performance and higher prediction accuracy, machine learning approaches have been widely adopted by scholars globally in recent years. Common algorithms include SVM, Naive Bayes, KNN, and LSTM (Fitri et al., 2019; Huq et al., 2017; Tsukioka et al., 2018; Zhuge et al., 2017).

Naive Bayes is a machine learning method based on Bayesian theory. This method has the advantages of strong theoretical basis, simplicity, convenience, high efficiency and stability, eliminating subjectivity of researchers, etc., and is widely employed in textual analysis (Adiba et al., 2020; Loughran & Mcdonald, 2016; Villavicencio et al., 2021). Therefore, our paper uses this method to analyze climate sentiment. Its basic definition is as follows:

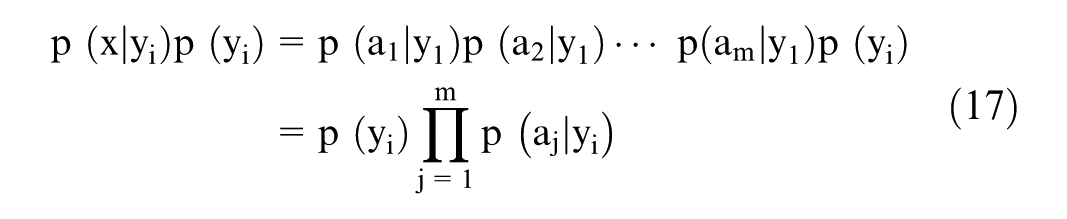

Let

There are n categories to which it belongs, which are represented by the set

Calculate the posterior probability

If

What matters most is computing the conditional probabilities outlined in step (3). According to Bayesian theory, we can write the conditional probabilities as follows:

Given that the denominator remains unchanged across all classes, the numerator can be maximized, and since the feature properties are conditionally independent of each other, we get:

The Naive Bayes model does not necessitate the creation of a sentiment dictionary; however, a portion of labeled sentiment data is required for its training. Because climate sentiment cannot be obtained solely through emotion analysis of separate words, comprehensive analysis focusing on the context is necessary. Therefore, we need to label sentiment on parts of the preprocessed text data by manually divided them into two categories: bearish and bullish, expressed by -1 and 1. Considering that the artificially labeled sentiment may have strong subjectivity, this paper also uses the open-source financial review corpus for sentiment classification. Finally, the samples with sentiment labels are fed into the Naive Bayes model for training. Once the model attains the desired precision, all posts related to the climate are inputted, and a definitive climate sentiment score is obtained.

This study employs the Naive Bayes algorithm and leverages Python’s SnowNLP library to carry out sentiment training on 10,000 text vectors alongside emotional labels. The outcomes of the model assessment show a 75% accuracy level, a metric that demonstrates the model’s favorable classification performance. According to the general criteria in academic research, a classification model may be deemed t to have attained successful categorization results when its accuracy rate reaches 70% or higher.

After applying the Naive Bayes algorithm to complete the scoring of text information in the entire sample set, this study further conducts a statistical analysis on the sentiment categories of each sample, and then obtains the daily investor sentiment scores and market atmosphere sentiment scores. With the goal of making certain that climate sentiment can comprehensively reflect the emotions of a broader group of investors, the research, following the method proposed by Santi (2023), orthogonalizes climate sentiment with the general sentiment of the East Money stock bar forum. On this basis, the ordinary least squares (OLS) regression approach is employed to estimate the following equation:

Where,

Figure 3 presents the changing trends of climate sentiment. Since the release of the IPCC’s Fifth Assessment Report in 2013, investors’ sentiment toward climate change has fluctuated significantly: it declined after the report’s release, particularly from late 2014 to early 2016. When the Paris Agreement was adopted in late 2015 and entered into force in November 2016, China actively assumed responsibilities for global climate governance and promulgated a series of climate policies and legal measures, driving the sentiment to rebound and remain high by the end of 2019. However, from the outbreak of the COVID-19 pandemic to May 2022, the sentiment stayed at a low level. Analysis of these fluctuations shows that major climate policies and conferences generally boost investors’ positive sentiment toward climate change, while significant climate and environmental scandals tend to dampen it.

Climate sentiment, constructed by Naive Bayes text analysis of financial comment posts on Eastmoney Net. The sample period is from November 2013 to December 31, 2022.

Variables Measurement

Explained Variable: Expected Default Frequency

Referring to previous studies (Bharath & Shumway, 2008; Capasso et al., 2020; Merton, 1974). We manually collect the stock and fiscal information o belonging to the high pollution of listed companies. Subsequently, the expected default frequency is estimated through the KMV model and is then designated as the proxy variable for corporate default risk.

Explanatory Variable: Climate Sentiment

We take more than 220,000 posts from the financial comment stock bar of Easymoney Net captured by Python crawler as samples, use Naive Bayes method to classify emotions, and finally refer to the method of Santi (2023) to construct climate sentiment. For specific methods, see The Methodology Section.

Controls Variables

With reference to existing literature (He et al., 2023; Liu et al., 2023; Parka et al., 2022), This paper controls asset-liability ratio (Lev), firm size (Size), Return on Asset (Roa),Tobin Q (TobinQ), market risk (Beta), the proportion of the largest shareholder (Top1), equity balance (Balance), liquidity ratio (Liquidity), and business complexity (Complexity) are a series of factors that may affect the risk of corporate debt default. Table 2 shows the detailed definitions of these variables. Descriptive statistics are shown in Table 3.

Variable Definition.

Note. Specific definition of variables, encompassing explanatory variables, explained variables and control variables.

Descriptive Statistic.

Note. Summary statistics of default risk, climate sentiment and other relevant variables. Sample period spans from January 1st, 2014 to December 31st, 2022, and this timeframe applies to all subsequent analyses.

Descriptive Statistics

Table 3 presents the descriptive statistical results of these variables. The findings indicate that the minimum value of EDF is 0.000 and the maximum value is 0.113, indicating that there is certain variation in corporate default risk within the sample. The mean of CSent is 0.648 with a standard deviation of 0.024, suggesting that the overall climate sentiment is at a certain level and the data dispersion is relatively small. It should be specifically noted that the climate sentiment indicator used in this paper is quarterly processed, so most of the values are positive. The standard deviation of Size is 1.306, reflecting a certain span in the total asset scale of enterprises. The minimum value of TobinQ is 0.161 and the maximum value is as high as 9.799, indicating a large difference in the ratio of enterprise market value to replacement cost.

Empirical Results

Benchmark Regression

Based on the panel data from a total of 36 quarters between 2014 and 2022, this paper employs a two-way fixed-effects model for baseline regression analysis. The regression outcomes are detailed in Table 4, with columns (1) and (2) showing the findings before and after control variables are included, respectively. Our findings indicate that the regression coefficients for climate sentiment stand at 0.021 and 0.085 respectively, both of which are significantly positive. This indicates that there is a positive correlation between climate sentiment and the default risk of listed companies in heavily polluting industries, which verifies the research hypothesis H1. Positive climate sentiment generally reflects society’s supportive attitude toward environmental protection and sustainable development. On the one hand, it makes investors more willing to invest in clean stocks and away from polluting ones. On the other hand, it exposes polluters to stricter regulations and regulations, potentially leading to higher compliance costs and operational pressures for firms. For polluting firms, both aspects may affect the overall financial health of the firm, thereby increasing the risk of bond default.

Empirical Results of Benchmark Regression.

Note. Regression is estimated by the two-way fixed effects using clustering robust standard error. Number of observations N and adjusted R-squared is reported at the bottom of each table, with t-statistics presented in parentheses beneath the estimated coefficients. Specifically, ***, **, and * stand for the 1%, 5%, and 10% significance levels, respectively, with the same notation applying below.

Robustness Test

Alternative the Measures of Explained Variable

To preclude inaccuracies arising from variations in the measurement approaches of explained variables, the explained variables are replaced and tested again. Z-score model is often used at home and abroad to predict bond default risk through five financial indicators reflecting the degree of financial crisis. The calculation expression is Z = 1.2X1 + 1.4X2 + 3.3X3 + 0.6X4 + X5, and the specific definitions of variables are provided in Table 5. A greater value signifies a lower level of default risk and a reduced probability of the firm falling into financial distress.

Z-Score Model Variable Definition.

Note. The five specific indicators of the Z-score were calculated. According to Wind database standards: Z-score >2.675 signals stability, Z-score <1.81 suggests bankruptcy risk, and 1.81 < Z < 2.675 indicates financial instability. If any of the above five indicators is empty, the Z-score value is empty.

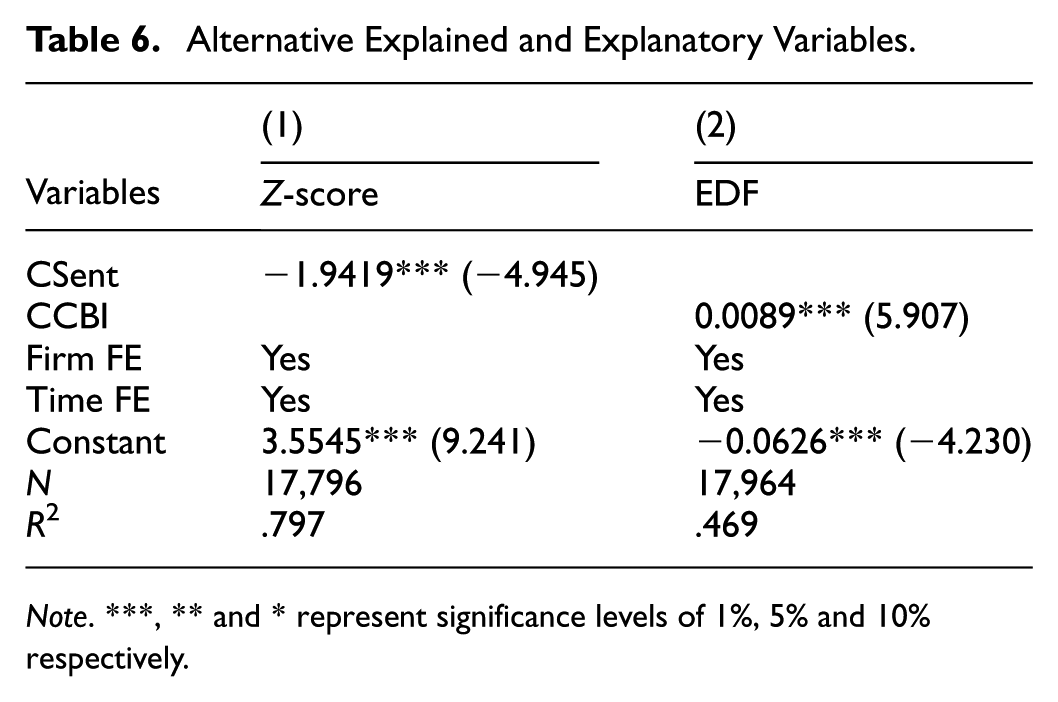

As indicated in column (1) of Table 6, the regression findings replacing the explained variables show that the impact of climate sentiment is significantly negative at the 1% significance level, suggesting that the more positive the climate sentiment, the lower the Z-score of highly polluting listed firms and the greater the default risk. The research conclusion remains robust and credible.

Alternative Explained and Explanatory Variables.

Note. ***, ** and * represent significance levels of 1%, 5% and 10% respectively.

Alternative Explanatory Variable

Through tracking the search frequency of keywords on search engine platforms, the Baidu Index can reflect users’ interest in content related to specific keywords (W. Zhang et al., 2021). Our study employs the Climate Change Baidu Index (CCBI) as a proxy for the explanatory variable, as CCBI can provide more objective, real-time, and trend-based data, which can more comprehensively reflect the society’s overall attitude and attention to climate change. Compared with traditional subjective survey data, CCBI is based on users’ actual search behaviors, enabling more accurate capture of the public’s dynamic attention to climate change issues, thus providing more reliable data support for the research. To avoid the impact of heteroscedasticity on the regression results, this paper applies a logarithmic transformation to CCBI to smooth the data and reduce deviations possibly caused by extreme values (

Mechanism Analysis

The above research shows that the climate sentiment indeed influences the default risk of firms, yet the underlying mechanism remains unclear. Existing research results have shown that financing constraint, financing cost and market competition serve as crucial factors impacting the default risk of firms (K. Chen et al., 2022; X. Zhang et al., 2020), climate sentiment may also trigger market uncertainty and directly affect the financing environment and market performance of firms. Therefore, to further explore the internal mechanism underlying the climate sentiment affecting corporate default risk, this paper introduces three mediator variables, namely financing constraint, financing cost, and market competition, and uses model (13), (14), and (15) to test the mechanism.

Referring to the research of (Whited & Wu, 2006), this paper employs the SA index’s absolute value as a metric for evaluating firms’ financing constraint. As the SA value increases, financing constraints become more intense. The calculation method in detail is as follows:

Where,

Table 7 illustrates the outcomes of the intermediation effect test of financing constraint. Column (2) reveals that, at the 1% significance level, the regression coefficient of climate sentiment on financing constraints is significantly positive, suggesting that the deterioration of corporate financing constraints is associated with a rise in climate sentiment. In column (3), financing and corporate default risk exhibit a significant positive correlation, implying that a rise in financing constraints is associated with greater corporate debt default risk. Based on the empirical test results, financing constraint SA has partial mediating effect. When climate sentiment increases, the financing constraint of firms will be increased thus leading to the increasing of corporate default risk, which partially verifies hypothesis H2.

Mediating Effect of Financial Constraint.

Note. ***, ** and * represent significance levels of 1%, 5% and 10% respectively.

Based on the existing literature, we employ the ratio of financial expenses to total debt (Cost) and the Herfindahl index (HHI) to measure the financing cost and market competition. The higher the Cost, the greater the financing cost; conversely, the smaller the HHI, the more intense the market competition. Tables 8 and 9 present the test outcomes of the mediating effect of financing cost and market competition. We find that financing cost and market competition have partial mediating effect in the process by which climate sentiment influences corporate default risk. Positive climate sentiment will increase the financing cost and market competition of heavy polluting firms, and then reduce the debt default risk of firms, thus partially verifying hypothesis H2. More positive climate sentiment often triggers a preference among investors and financial institutions for environmentally friendly firms, which makes it harder and more expensive for heavy polluters to get financing. At the same time, due to increased social attention to environmental issues, policies and regulations may also become stricter, forcing these firms to bear more environmental compliance costs and increase their operating costs. These factors together lead to heavy polluting firms to face greater financing pressure and market competition difficulties, and ultimately increase the possibility of corporate debt default.

Mediating Effect of Financial Cost.

Note. Financial cost is equal to finance expenses/total liabilities.

***, ** and * represent significance levels of 1%, 5% and 10% respectively.

Mediating Effect of Market Competition.

Note. The Herfindahl index (HHI) is employed to measure market competition, with calculations based on the main business income of the firm’s industry. A lower HHI corresponds to a more intense level of market competition.

***, ** and * represent significance levels of 1%, 5% and 10% respectively.

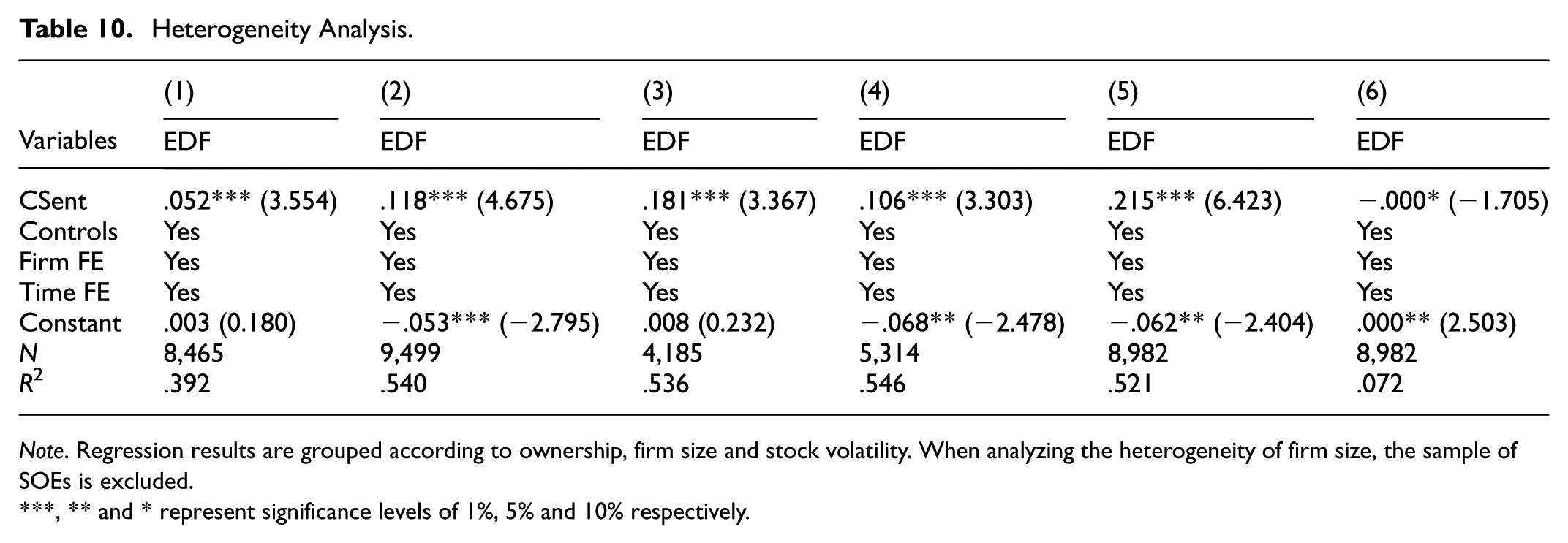

Heterogeneity Analysis

To provide further empirical evidence, this paper has carried on the group heterogeneity regression analysis of ownership, firm size and stock volatility.

First of all, based on differences in the ownership nature of enterprises, The sample is divided by us into SOEs and non-SOEs. Looking at columns (1) and (2) in Table 10, it can be observed that the regression coefficients of climate sentiment on the default risk of SOEs and non-SOEs are 0.052 and 0.118, respectively, with both being significantly positive at the 1% level. And the default risk of non-SOEs is more sensitive to climate sentiment, which verifies hypothesis H3a. Different ownership leads to natural differences between firms in obtaining financial support and bank financing. Compared with SOEs, non-SOEs have a relatively stronger reliance on market financing, so they are easily affected by climate sentiment.

Heterogeneity Analysis.

Note. Regression results are grouped according to ownership, firm size and stock volatility. When analyzing the heterogeneity of firm size, the sample of SOEs is excluded.

***, ** and * represent significance levels of 1%, 5% and 10% respectively.

Second, we analyze the heterogeneity of firm size. Considering that SOEs are generally large firms, we excluded SOEs from the sample in order to eliminate the effect of ownership. Subsequently, we divide them into two groups, large and small, on the basis of the median market capitalization of the firms, and the empirical results are presented in columns (3) and (4) of Table 10. The regression coefficients for climate sentiment stand at .181 and .106, respectively, both of which are significantly positive at the 1% level. And the default risk of large-market-capitalization firms is more sensitive to climate sentiment, which verifies hypothesis H3b. Relative to small market value firms, large market value firms exert a more significant market influence, and usually face more investor attention and supervision. When climate sentiment increases, investors are more likely to support environmentally friendly firms, while showing greater vigilance toward those that can cause negative environmental impacts.

Finally, we split the sample into high-volatility and low-volatility groups based on the median of stock volatility. And the results of the regression are illustrated in columns (5) and (6) of Table 10. The coefficient on the regression of climate sentiment on default risk is .215 and .000. We observe that only the sample climate sentiment with high volatility shows a noticeable impact on default risk, verifying hypothesis H3c. As climate sentiment increases, investors will correspondingly reduce their demand for stocks of highly polluting firms. Among them, especially those with high volatility, default is more likely due to greater uncertainty (Bevan & Garzarelli, 2000).

Conclusion

Drawing on the KMV model, this study explores how climate sentiment affects China’s bond market. A Naive Bayes model was employed to build the climate sentiment index. By crawling through climate-related posts on Eastmoney Net’s financial commentary stock bar, we obtained over 220,000 entries spanning from January 1, 2014, to December 31, 2022, which serve as our research data. The results can be summarized as follows: (1) A more positive climate sentiment is associated with higher default risks among listed firms in heavily polluting sectors. (2) The rise in default risks for these heavy polluters driven by climate sentiment primarily stems from tighter financing constraints, higher financing costs, and intensified market rivalry. (3) The influence of climate sentiment on amplifying firms’ default risks is more significant in non-state-owned enterprises, larger-sized companies, and those with greater stock volatility.

This paper presents the three following enlightenments, in accordance with the conclusions of the research. First, Confronting the pressure from climate change, heavy polluting firms should realize that positive changes in climate sentiment may increase their default risk. In response to the financing constraint, and the pressure of market competition, firms should take active measures to environmental protection, reduce environmental negative impacts, and enhance their environmental protection image. In addition, improving governance structures and enhancing information disclosure are key to improving investor trust, reducing financing cost, and addressing potential environmental risks in advance. At the same time, by pursuing the clean technology and renewable energy transition, firms can better adapt to future changes in environmental regulations, thereby reducing financing constraint. Second, when making investment decisions, investors ought to take ESG (Environmental, Social, Governance) and climate-related factors into account, and support firms that perform well in environmental protection. At the same time, it is essential to be aware of factors such as stock volatility, ownership, and firms’ size in order to effectively deal with the default risk caused by climate sentiment. Third, Governments and regulators should enhance relevant laws and regulations, actively guide firms to proactively disclose climate-related information, reduce the risk of information asymmetry, sustain investor confidence.

This study has limitations in several aspects, as detailed below: In terms of data, due to the difficulty in obtaining data on climate-related comments from other financial platforms, the sample data of this study is only sourced from climate-related posts on the financial commentary stock bar of Eastmoney Net. A single data source cannot fully reflect the overall characteristics of market climate sentiment, nor can it adequately demonstrate the long-term impacts of different climate policy stages or major climate events, thereby limiting the temporal and scenario extrapolation of the research conclusions. In terms of research methods, the Naive Bayes model used for climate sentiment quantification is constrained by the “feature independence” assumption, making it difficult to accurately interpret complex semantics such as metaphors and sarcasm in the text, which may lead to deviations in sentiment scoring. At the application level of the KMV model, this study does not include high-polluting enterprises that are unlisted or have incomplete data disclosure; meanwhile, it fails to consider the sudden impact of climate events on corporate assets, which is likely to cause sample selection bias and the underestimation of actual default risks. Regarding the external validity of the conclusions, the sample only covers listed high-polluting enterprises in China and does not involve unlisted high-polluting enterprises, similar enterprises in other countries, or sub-sectors within the high-polluting industry. As a result, the extrapolation of the conclusions is limited at the national level, enterprise type level, and industry sub-sector level.

Footnotes

Acknowledgements

The authors is grateful for the School of Economics of Xihua University for its database and good research environment.

Ethical Considerations

Throughout the entire process of research design, implementation, and data collection, this study has strictly adhered to relevant international and regional ethical standards. It does not involve any human subjects or animal experiments, and there is no violation of human ethics or animal ethics.

Consent to Participate

All authors of this study have fully been informed of the research objectives, content framework, data sources, analytical methods, core conclusions, and submission intentions of the paper, and they have no objections to the overall information of the paper, including details of the research design, interpretation of results, expression of academic viewpoints, and potential academic risks.

Author Contributions

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The authors are grateful for the funding support from the National Natural Science Foundation of China (No. 72203173), the Sichuan Provincial Departmental-level Project (LD2024Z31), and the 2024 Xihua University Graduate Science and Technology Innovation Competition Project: “Qiuke Three Small Ball Professional Sports Information Platform” (RC2400002282).

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The data of this study comes from legitimate channels, including public databases and authorized data from cooperative institutions. During collection, we strictly verified each source’s terms (confirming compliance with commercial research needs), avoided unauthorized acquisition, and retained complete records and authorization documents. In analysis, we followed the sources’ processing restrictions (no prohibited secondary processing or cross-domain use), desensitized personal information per privacy clauses, and passed internal compliance reviews. Data source descriptions and authorization documents are available for verification to ensure full compliance with all source terms.