Abstract

A firm’s default risk is closely related to its macrofinancial stability. As financial reform deepens, banking competition may ease firms’ credit constraints, encouraging them to increase their leverage and default risks. This study uses contingent claims analysis to examine firms’ asset–liability ratio and default distance. We find that companies have low leverage and low overall default risks. Moreover, a pro-cyclical effect exists between leverage and economic growth. As banking competition becomes more intense, the default risk decreases, but firms’ leverage ratio rises significantly. The impact is more prominent for highly leveraged firms. Our findings also indicate that utilizing the contingent claims analysis method to measure firms’ leverage and default risks provides more accurate results. Moreover, we provide empirical evidence of the impact of banking competition on firms’ leverage and credit risks. The results suggest that enhancing financial competition has a positive effect on easing credit constraints and reducing default risks.

As China’s economic growth enters a new normal, the “high leverage” phenomenon of Chinese firms has become more prominent, and the country must continue implementing “de-leveraging” macro-control policies to reduce macrofinancial risks. For microfirms, the leverage ratio can be reflected by the asset–liability ratio, wherein a lower asset–liability ratio indicates a lower company leverage ratio. In the traditional balance sheet analysis method, the asset–liability ratio is computed by dividing book liabilities by book assets. However, this method has flaws. On the one hand, a firm’s book value only reflects the historical conditions of the market and the firm’s operations; it does not provide information for predicting the company’s future operating conditions. Therefore, it is difficult to accurately measure a company’s future risk status based only on its book value information. On the other hand, even if the market values of firm assets and liabilities are obtained through direct observation and discounted future cash flow methods, their future cash flows remain difficult to determine as firm assets and liabilities may have no observable market prices and their accurate market values may be inaccessible. To more accurately reflect firm leverage, new analytical methods are needed. Contingent claims analysis uses the market information of equity to obtain the market value of assets and liabilities. Thus, the leverage ratio of enterprises and their risk situation can be more accurately reflected. Contingent claims analysis uses option pricing as its theoretical cornerstone. Black and Scholes (1973) and Merton (1974) concluded that the option pricing principle can be used to price firm debt. The main idea is to treat various firm debts, such as common shares, company bonds, and warrants, as options based on firm assets. The company’s entire equity can then be regarded as an option portfolio. The value of the call and put options can be calculated by using the option pricing method by Black and Scholes (1973). The contingent equity analysis method is derived from the classic option pricing theory and is one of the important methods commonly adopted for macro-risk analysis (Liu & Ronn, 2020; Restocchi et al., 2017). The classic KMV model (Credit Monitor Model) adopts the Merton method to obtain the contingent equity value of a single firm and the market value of assets, and the default distance is thereby obtained to enable measurement of the firm’s credit risk. However, in this paper, the measurement of firm risk is done at the micro level, and scarce research exists on the macro level of firm risk. Empirical facts are increasingly suggesting that the firm risk situation at the macro level is closely related to macrofinancial stability. This study draws on the contingent equity analysis method of Barlev (1983) and the modeling ideas of Jones et al. (1984) to expand its scope from microfirms to the macro level and examine the overall risk situation of Chinese listed companies.

Firm leverage reflects a company’s capital structure. A high leverage ratio indicates that a company relies highly on debt to operate. The development of China’s capital market is incomplete, and companies have limited indirect financing channels. Even listed companies generally rely on direct financing channels in post-listing operations. Considering firm debt, the credit ratio is relatively large. While the credit market has long been dominated by commercial banks, the monopoly of their credit supply has a direct impact on the capital structure of enterprises. As China gradually eases restrictions on market access to the banking industry, the market structure of this industry has significantly changed. Small and medium-sized banks, such as joint-stock commercial banks, city commercial banks, and rural commercial banks, have gradually captured part of the market share of large state-owned banks. Competition in the banking industry is also increasing. This study examines whether intensified banking competition will create a monopoly in credit supply and alleviate the “financial difficulties” of Chinese companies to reduce their risk level.

We present two hypotheses on how banking competition affects firm credit availability: the structure-performance hypothesis and the information-based hypothesis. The first states that increased competition in the banking industry will prompt banks to provide firms with more credit at lower interest rates. By establishing a spatial competition model for loans, Babatoundé (2020) demonstrated that competition can lead to a decline in loan interest rates and a rise in deposit interest rates. Bustos et al. (2020) found that bank monopolies are more likely to lead to credit rationing and lower capital accumulation rates than competitive markets. Marquez (2002) stated that fierce market competition would rapidly spread the demand information of borrowers, and commercial banks with strong market competitiveness will increase their relationship loans to small businesses. Durguner (2017) suggested that the loan supply will increase when competition increases, but the default rate will also increase. The information-based hypothesis implies that considering information asymmetry and agency costs, increased banking competition may weaken their incentive to establish long-term relationships with borrowers (Petersen & Rajan, 1995). Moreover, this reduces the efficiency of banks in identifying borrowers (Marquez, 2002), which ultimately makes competition in the banking industry and firm credit availability negative or nonlinear. Empirical research results are also mixed: some studies show that increased banking competition is associated with greater availability of firm credit, establishment of new enterprises, and economic growth (Goetz, 2018). However, there is also evidence that the quality of bank loans and credit availability is higher in markets with a higher degree of monopoly. Few direct domestic studies have been conducted on the relationship between Chinese banking competition and firm credit availability (Lu et al., 2012). It is difficult to accurately measure the credit availability of companies. Contingent claims analysis can obtain a firm’s capital structure based on the fair value in a market, and its changes can more accurately reflect the current credit availability of enterprises. This study examines the relationship between contingent asset–liability ratios and banking competition and investigates the impact of intensified competition in China’s banking industry on firm credit constraints and its risk profile from a macro perspective.

Analysis Model

Contingent Claims Analysis

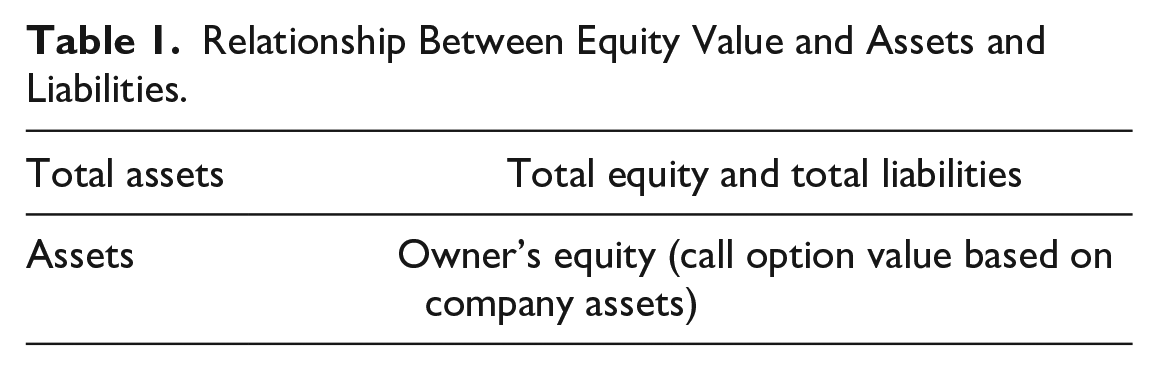

Merton (1974) proposed that firm value is equal to the sum of the values of various securities in its capital structure. In other words, the company’s various debts, such as ordinary shares, firm bonds, and warrants, can be considered a combination of options based on firm value, corporate claims as a risk-free bond minus a put option based on firm assets, and firm equity as a call option based on company assets.

As shown in Table 1, firm debt claims the value of firm assets. The market value of a company’s total assets is equal to the market value of equity plus that of debt. If the value of the company’s assets falls below the book value of its due debt, a default will occur. Therefore, the book value of debt is equivalent to the point of default. Firm risk debt is equal to the market value of company assets minus that of company equity. Since the market value of firm equity can be viewed as a call option based on firm assets, the value of firm risk debt can be viewed as a put option based on corporate assets.

Relationship Between Equity Value and Assets and Liabilities.

We derive the pricing formula for firm contingent equity based on the relationship between the values of firm assets and its equity in the previous section. Based on Black and Scholes’s (1973) theory, we first make the following assumptions:

(1) There are no transaction costs and taxes, and assets can be subdivided indefinitely; (2) there are many investors in the market whose wealth can guarantee that they can buy or sell any amount of any asset at the current price; (3) the market allows short selling; (4) assets are continuously traded in the market; (5) the value of the firm is not related to the capital structure (i.e., the MM theorem holds); (6) the term structure of interest rates is definite and “flat”; (7) the change in firm value can be described by the stochastic differential equation of equation (1).

In formula (1),

Suppose a security has a market value of Y. We can then express the value of the security as a function of the firm’s total asset value and time, given by equation (2):

Therefore, the change in the value of the security can also be described by the stochastic differential equation of equation (3):

where

where

Using a similar approach to the deriving of the option pricing formula by Black and Scholes (1973), we can obtain the partial differential equation of formula (5):

The solution function F of equation (5) satisfies any value that can be expressed as a function of the company’s total assets or time. To apply formula (5) to the pricing of contingent interests, the following assumptions need to be made:

(1) Firms have two types of claims: one is the same level of claims, and the other is equity.

(2) The firm promises to make a total payment of B to the creditor on a specific date T. If this payment cannot be made, the creditor will quickly take over the enterprise.

(3) Prior to the debt maturity date, the company cannot issue new senior equity, nor can it pay any dividends or repurchase its own shares.

Under the above assumptions, using F to represent the market value of firm debt, equation (5) can be written as equation (6):

Since the company does not pay any dividends,

When the firm value is zero, the value of its debt is also zero:

The value of firm debt is less than the value of the company under any circumstances:

The value of firm debt when debt matures is given by:

Using the Fourier transform method to solve equations (6)–(9), we obtain the following:

In formula (10),

In formula (11),

We use listed companies to analyze the above model. A listed company’s equity is regarded as a call option based on the value of its assets, and its value is given by equation (12):

Here, A is the value of the company’s assets, and DB is the value of its non-default debt. Equation (12) indicates that the relationship between the value of the company’s stock and that of its assets minus the change in the value of the tradable stock can affect the change in the market value of the company’s assets. The value of the claim on the company is as follows (13):

Since A = D + E, substituting E and D yields equation (14):

We can substitute the observed market value and default equity point into the call option formula to obtain the market value of the company’s assets. Substituting this value and the default point into the put option formula yields the market value of the implied risk debt.

Measuring Banking Competition

The traditional industrial organization theory framework of structure-conduct-performance (SCP) analysis shows that high market concentration means strong market power and low competition. In accordance with this analysis framework, early research on banking competition often used market concentration to indicate the degree of competition, mainly by structural measurement indicators such as the CRn or HHI index. With the advancement of research, nonstructural measurement methods have emerged. Common indicators include the H index and Lerner index of Panzar-Rosse. Kasman and Kasman (2015) highlighted that the Lerner index measures the individual market power by examining the pricing behavior of banks and has a more solid micro-foundation than the H index. The Lerner index is a popular measurement method to assess the degree of competition in the banking industry. This study draws on the ideas of Kasman and Kasman (2015) and uses the Lerner index to reflect the degree of competition in China’s banking industry. The index reflects the pricing power of individual banks above the marginal cost. The calculation formula is presented in equation (15):

where Pit is the output price of the i-th bank in year t divided by the total bank income (including interest and non-interest income), divided by the total bank assets. MCit is the marginal cost of the i-th bank in year t. This study builds on Kasman and Kasman (2015) and uses stochastic frontier analysis (SFA) to construct a translog cost function and derive the marginal cost (MC). The derivation process is as follows:

We construct the bank cost function based on Fernandez and Maudos’s method (Kasman & Kasman, 2015). Assume that the total bank cost is a function of bank output, bank capital price, bank labor price, bank capital price, and technological change, which is

Equation (16) must satisfy the first-order homogeneous condition of factor prices, namely,

Next, the Lerner index can be calculated according to formula (16). This index ranges between 0 and 1, where 0 means complete competition and 1 means complete monopoly. 0 <Lerner <1 represents monopolistic competition or oligopoly, so the Lerner index and the degree of banking competition are inversely changing. After calculating the individual bank’s Lerner index, its individual asset share is used as the weight to determine the weighted average. Finally, the Lerner index, reflecting the overall competition of the banking industry, is obtained.

Empirical Analysis

Macro-Level Firm Contingent Asset–Liability Ratio and Credit Risk

Consider equation (18) below:

In formula (18),

Here,

Estimated Results Using Contingent Equity Analysis (Unit: 100 Million Yuan).

We draw the traditional asset–liability ratio and contingent asset–liability ratio of Chinese listed companies as shown in Figure 1

Comparison of traditional and contingent debt ratios of Chinese enterprises.

In Figure 1, the contingent asset–liability ratio of a Chinese listed company is much lower than its book assets-liability ratio, indicating that firm risk at fair value is lower than the ratio at book value. Hence, the true leverage ratio of Chinese companies is still relatively low. Further, the contingent asset–liability ratio of Chinese firms is generally rising; thus, Chinese enterprises must continue to be deleveraged.

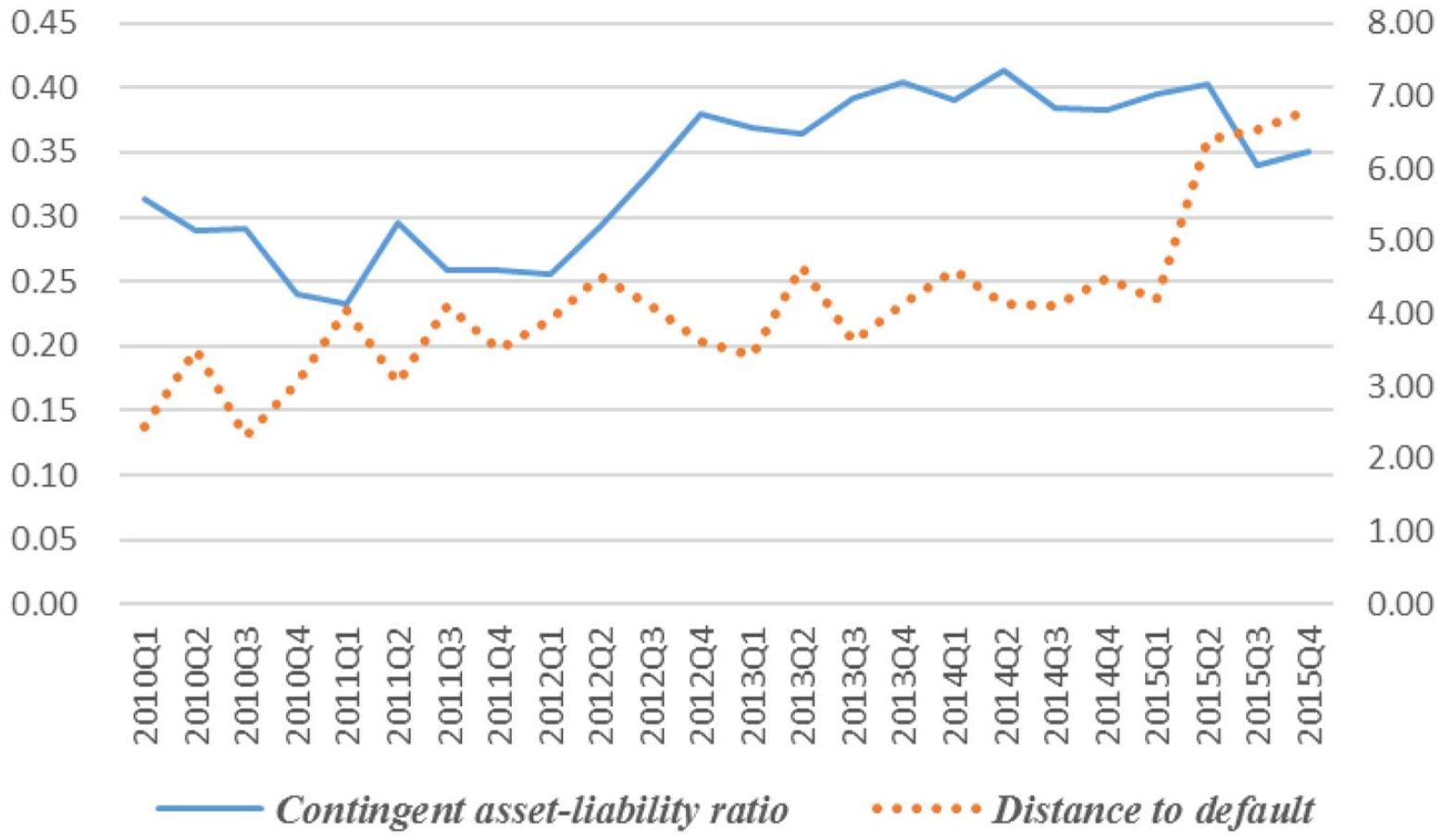

As the contingent asset–liability ratio of Chinese firms is gradually rising, their risk conditions may also be deteriorating. According to the contingent equity analysis method, the overall default distance of Chinese firms is calculated. When firm asset volatility increases, the default distance decreases, and company credit risk increases. This study examines the relationship between firm default distance and contingent asset–liability ratio, as shown in Figure 2.

Relationship between corporate default distance and contingent asset–liability ratio.

The left vertical axis of Figure 2 represents the contingent asset–liability ratio, the right vertical axis represents the default distance, and the horizontal axis represents time (quarter). The default distance of Chinese companies is fundamentally consistent with the change trend of the contingent asset–liability ratio. A Pearson correlation coefficient test confirmed that the correlation coefficient between the two was .3518, significant at the 10% level. Thus, although the overall leverage of Chinese firms is increasing, their credit risk is gradually decreasing.

Macro-Level Contingent Assets–Equity Debt Ratio and Economic Growth

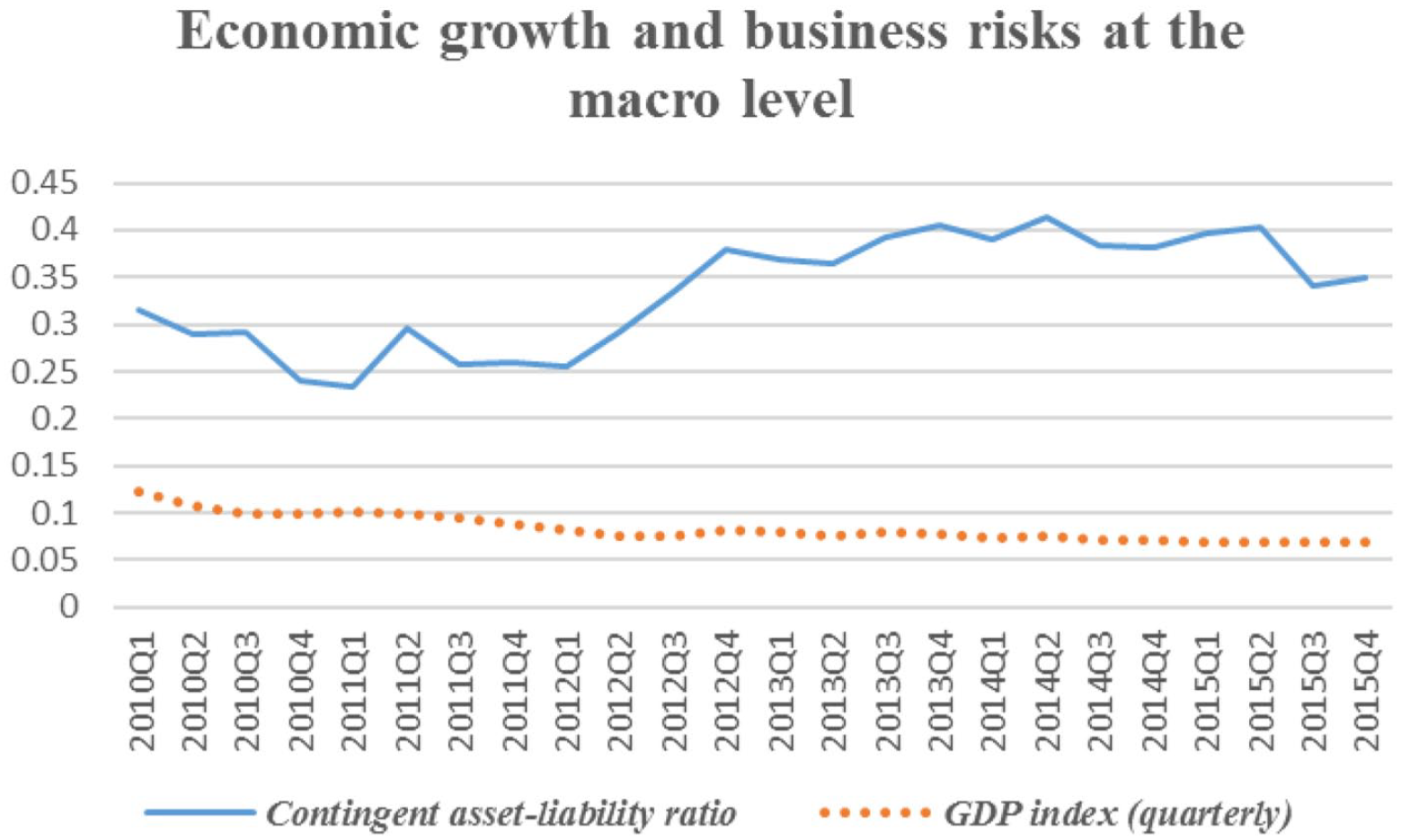

The contingent asset–liability ratio of the firm obtained by the contingent equity analysis method can reflect more accurately its real leverage ratio at the macro level, and especially the trend of this ratio. We further examine the relationship between the macro-level firm leverage and economic growth in the new economic normal. This study uses the (seasonal and price-adjusted) quarterly GDP index to reflect economic growth. The data are collected from the National Statistical Yearbook.

In Figure 3, from the first quarter of 2011, the real growth rate of China’s GDP began to fall below 10% and gradually stabilized at about 7%. Therefore, China’s economic growth rate has changed from rapid to steady: The rate of economic growth has shown a slow decline, and this has become its new normal. However, at the macro level, the true leverage ratio of firms has demonstrated a clear upward trend, showing a “pro-cyclical” trend with economic growth.

Economic growth and corporate leverage at the macro level.

Figure 3 describes the statistical results. In the following, we examine the long-term change relationship between economic growth and the contingent asset–liability ratio of firms more deeply.

Unit root tests

A unit root test was performed on the above two sequences to check whether they were stationary. This study uses the ADF test, as shown in Table 3.

Sequence Unit Root Test Results.

C indicates that there is an intercept term, 0 indicates that there is no intercept term, T indicates that there is a trend term, and 0 indicates that there is no trend term; the third term is a lag order, which is automatically determined by SIC.

The table shows that at the significance level of 5%, neither the contingent asset–liability ratio nor economic growth is a stable sequence. However, the sequences obtained after the first-order difference change are stationary, indicating that both of them are first-order simple integers, and they may have a cointegration relationship.

Cointegration test

Because it contains only two variables, this study uses the E-G two-step method to test the cointegration relationship between sequences. The first step is to return the contingent asset–liability ratio to economic growth, as shown in Table 4.

Regression Results of the Cointegration Test Under Contingent Equity Analysis.

The second step is to perform a unit root test on the residuals of the above regression, as shown in Table 5.

Residual Unit Root Test Results.

In Table 5, the residual sequence of the regression is stable at the 5% significance level. Therefore, there is a cointegration relationship between the two sequences. The cointegration equation is shown below:

It indicates that there is a significant “pro-cyclical” relationship between a firm contingent asset–liability ratio and economic growth: lower economic growth represents higher company leverage at the macro level. This is also supported by the fact that China’s economic downturn coexists with high leverage.

However, using the traditional book asset–liability ratio to reflect the firm operating risk and economic growth for cointegration tests, we find that the two do not have a significant cointegration relationship. The regression results are shown in Table 6.

Cointegration Test Regression Results Under Traditional Analysis.

This table reveals that if the traditional book asset–liability ratio is used as a measure of firm operating risk, then there is no significant correlation between firm leverage and economic growth. It is difficult to accurately capture the expected changes in the value of company assets and liabilities, as well as to measure the real trend of firm leverage when future market conditions change. It is even more difficult to accurately capture firm leverage and economic growth since dependencies may be misleading for macro policymakers in evaluating the economic situation.

Banking Competition and Firm Credit Availability

This study uses the financial data of Chinese listed banks from 2000 to 2015, as well as SFA to calculate the Lerner index, which reflects the level of competition in the banking industry. In Figure 4, the data come from the CSMAR database.

Change trend of competitiveness of China’s banking industry.

Figure 4 indicates that, from 2010 to 2015, the Lerner index of the Chinese banking industry gradually decreased and competition increased, which is consistent with China’s strategy of continuously promoting financial reform. Will intensified banking competition ease firm credit constraints overall, thereby reducing credit risk? This study develops the following two measurement models for testing:

Equation (21) examines the impact of banking competition on the capital structure of Chinese companies, and equation (22) analyzes the impact of banking competition on the credit risk of these companies. Both models include control variables: GDP growth rate reflects China’s macroeconomic environment, and M2 growth rate reflects the trend of China’s monetary policy. The estimated results of equations (21) and (22) are shown in Table 7.

Banking Competition, Corporate Capital Structure, and Credit Risk.

In Table 6, on the one hand, more intense banking competition relates to a higher contingent asset–liability ratio of the firm, with a very significant coefficient. This demonstrates that as the monopoly of credit supply by large banks decreases, the credit constraints of Chinese firms generally weakens. On the other hand, the more intense the competition in the banking industry, the lower the credit risk of the firm becomes, again with a very significant coefficient. Increased banking competition will lower the cost of obtaining credit for companies, making obtaining credit easier and reducing the pressure on financing. This allows companies to arrange investment and production more easily, which reduces uncertainty of business operations and, thus, corporate risk.

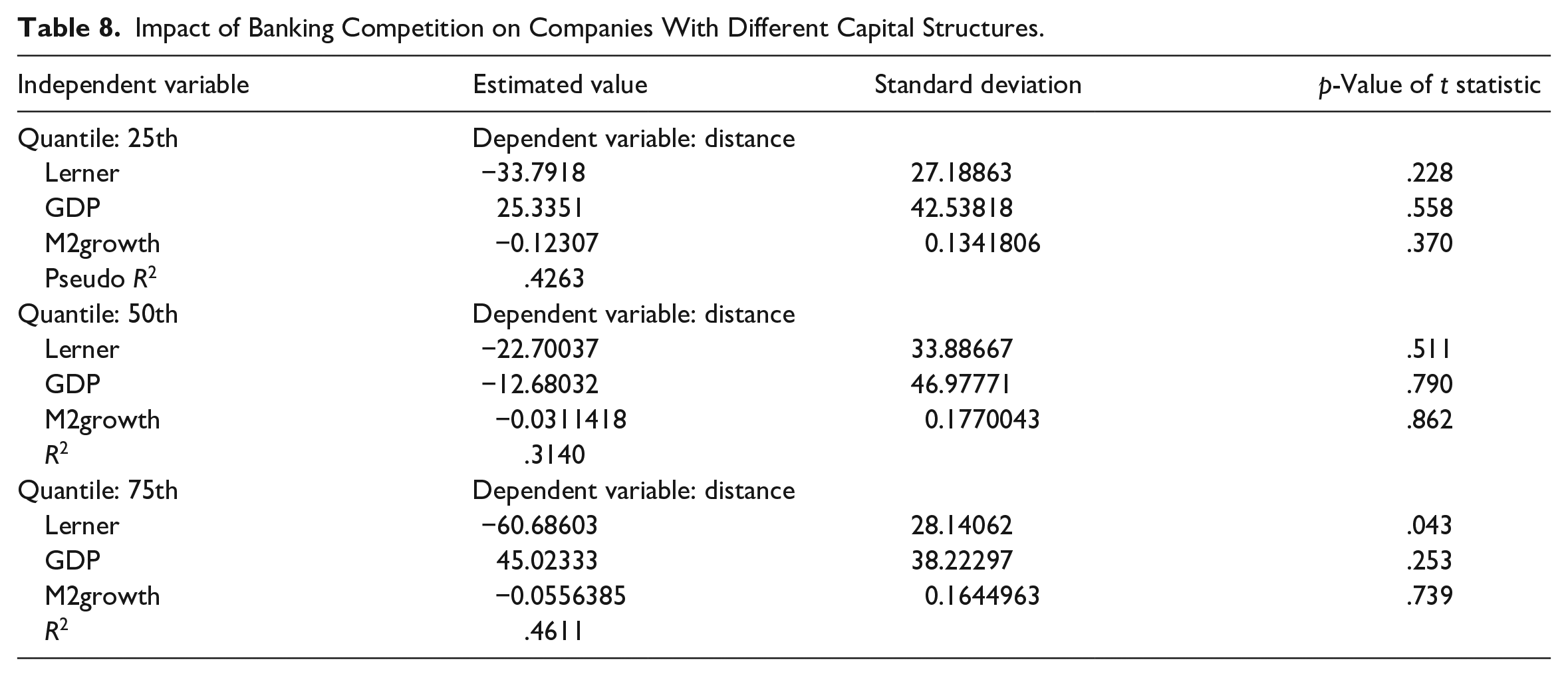

Firms with different capital structures face different risks, and easing credit constraints will have different effects on firms with different capital structures. Considering that the contingent asset–liability ratio of Chinese companies is significantly positively related to credit risk during the sample period, a lower contingent asset–liability ratio means lower credit risk. This study further uses quantile regression to conduct a detailed analysis of formula (22) to test the impact of increased banking competition on companies with different capital structures. We select the 25th, 50th, and 75th quantiles for regression, according to the capital structure from low to high. The robust standard deviation was obtained through a 10,000-times bootstrap, and the regression results are shown in Table 8.

Impact of Banking Competition on Companies With Different Capital Structures.

The quantile regression results in Table 8 show that the intensified competition in the banking industry has significant impact on companies with low credit risk (high leverage), and the absolute value of the coefficient is large. However, the impact on companies with high credit risk (low leverage) is not significant. This demonstrates that after the banking competition intensifies, credit channels become more open, and credit conditions continue to improve, which can ease the credit constraints of firms and promote debt financing. As credit availability is enhanced, financing costs are also continuously reduced, lowering the uncertainty of firm operations and, thus, corporate credit risks.

Conclusions and Recommendations

This study establishes a contingent equity analysis model to derive the market value of firm liabilities and assets. On contingent equity, we measure the leverage and credit risk of Chinese companies at the macro level. Further, considering credit constraints, we examine the impact of increased banking competition on the capital structure and credit risk of Chinese companies. We obtain the following findings:

(1) At the macro level, low and low credit risk coexist in Chinese firms. The leverage ratio measured by the contingent asset–liability ratio is much lower than that measured by the book asset–liability ratio.

(2) At the macro level, there is a clear procyclical effect on the leverage and economic growth of Chinese firms. When the economy is developing well, corporate leverage is generally high, but firm leverage measured by the book asset–liability ratio cannot capture this relationship.

(3) Intensified competition in the banking industry can ease the credit constraints firms face, encourage them to use more debt financing, and increase leverage. Intensified competition in the banking industry can also improve credit conditions, reduce financing costs, and lower uncertainty of firm operations, thereby helping reduce firm credit risk.

This study examines the analytical framework for measuring firm risk at the macro level. Macro policymakers should study the relationship between firm leverage and risk conditions to more accurately grasp the changing trend of firm risk conditions and maintain macrofinancial stability. Further improving financial reforms and reducing credit constraints will be effective in enhancing corporate vitality and reducing company risk levels.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by (1) The 68th batch of general funding projects for postdoctoral fellows in China: Responsible rural digital Inclusive Finance-dynamic monitoring and governance under the reconstruction of ethical dimension [grant number 2020M682377]; (2) National Social Science Foundation of China: Research on the long tail effect of digital Inclusive Finance in alleviating rural relative poverty under the constraint of information gully [grant number 20BJY174].