Abstract

Asymmetric information and economic uncertainty lead to more serious financial constraints on Chinese listed companies, thereby prompting them to hold more cash to guard against uncertainty and market competition. Using a sample of 45,303 observations of Chinese listed companies between 2010 and 2022, this study analyzed the relationship between corporate growth opportunity, product market competition (PMC), and cash holdings (CH). A quantity analysis model is used to examine the correlation between corporate growth opportunity and corporate CH while considering external factors such as PMC. Corporate growth opportunity leads to enterprises increasing their CH. However, fierce PMC reduces the enterprise CH level, and this effect is even more pronounced for high-growth opportunity enterprises, thus indicating that market competition efficiently mitigates such enterprises holding excess cash. Therefore, to improve enterprise cash-use efficiency, reducing information asymmetry under fierce PMC is essential. In summary, this study not only presents valuable insights into enhancing cash-use efficiency but also helps enterprises to implement more favorable market competition strategies and maintain a dominant position under fierce market competition.

Plain Language Summary

This study is based on Chinese-listed companies as the sample to analyze the relationship between corporate growth opportunity, product market competition and cash holdings. This study is based on the quantity analysis model to examine the correlation between corporate growth opportunity and corporate cash holdings and analyze the result while considering external factors such as product market competition. The study reveals that corporate growth opportunity leads to enterprises increasing their cash holdings. However, fierce product market competition reduces enterprise cash holding level, and this effect is even more pronounced for high-growth opportunity enterprises, indicating that market competition efficiently mitigates high corporate growth opportunity enterprises hold excess cash. In summary, this research not only shows valuable insights into enhancing cash use efficiency but also helps enterprises to implement more favorable market competition strategies and maintain a dominant position in the fierce market competition.

Keywords

Introduction

Cash is a firm’s most liquid and crucial asset. An institution’s cash holdings (CH) can provide valuable insights into its financial decision-making and operational strategy. The decision to hold cash directly affects business growth. Holding less cash can lead to financial difficulties owing to a lack of capital, whereas holding too much cash can result in a loss of investment income and increase the risk of managers misusing funds.

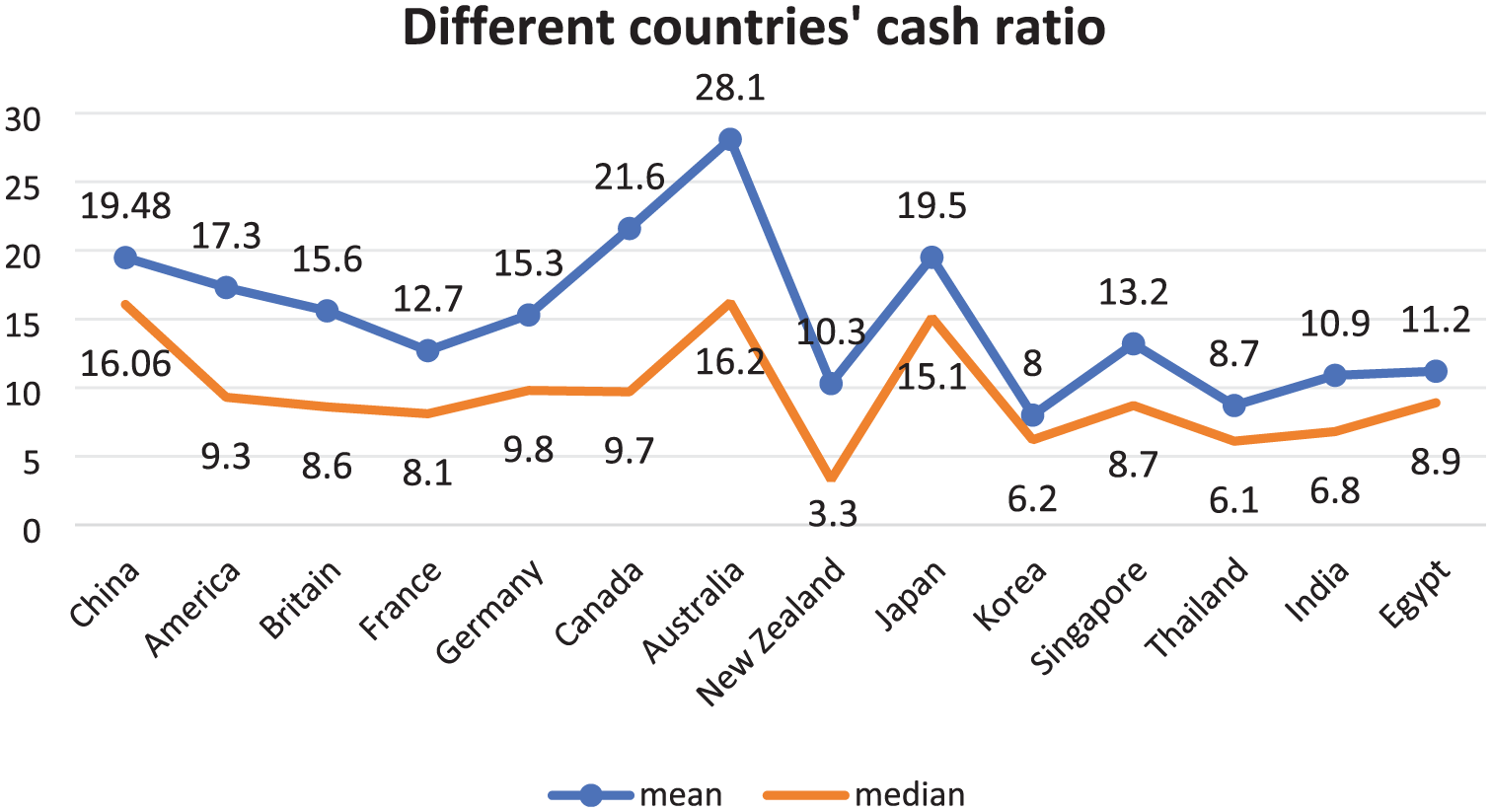

As illustrated in Figure 1, compared with different countries, China has a higher level of CH. This is because of the imperfect capital market and governance mechanisms, and external financing and internal agency costs are both high for companies (Bo & Li, 2025).

Different countries’ cash ratio.

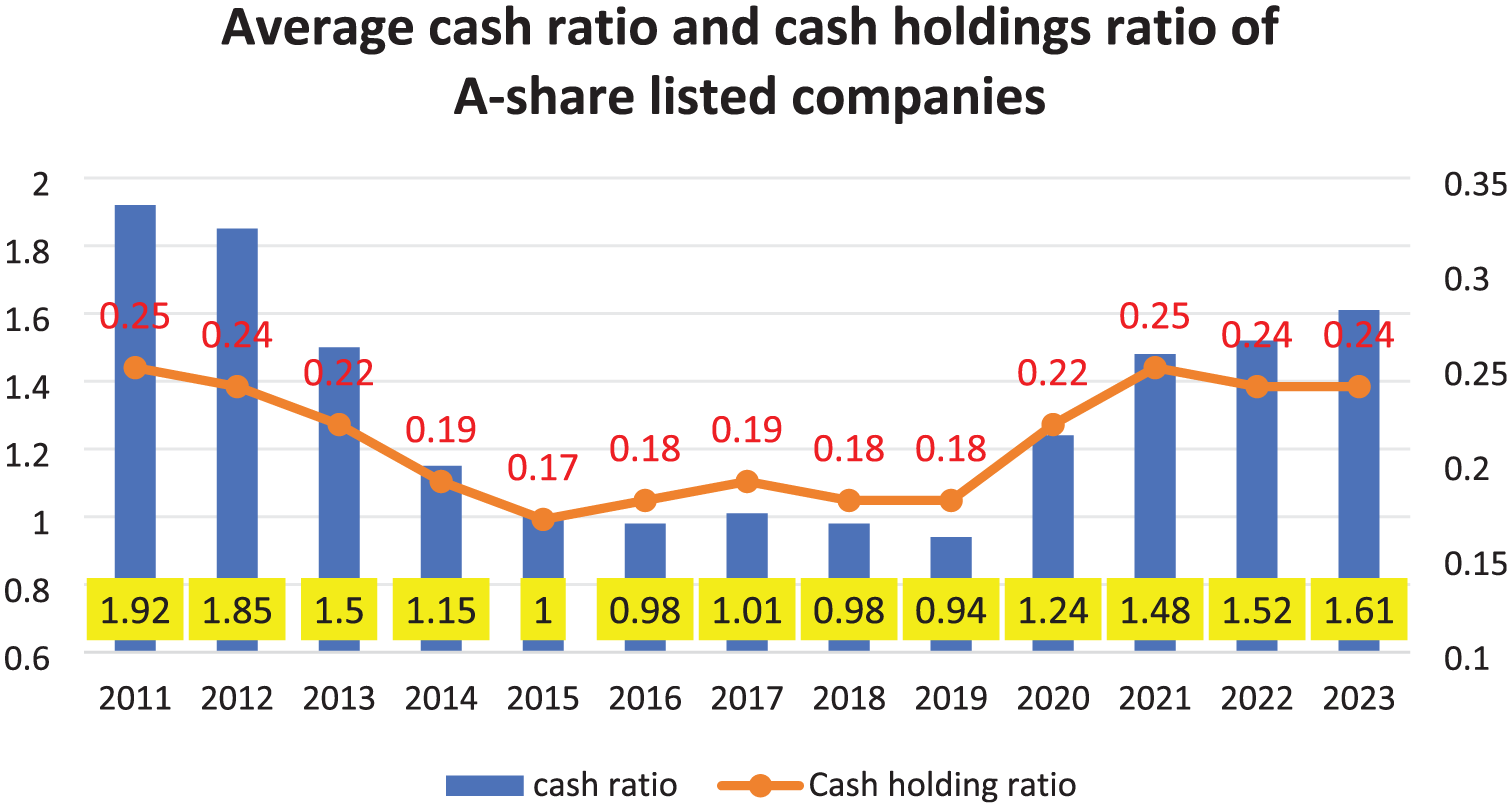

According to Figure 2, Chinese listed companies have higher cash and CH ratios in China. However, holding too much cash can result in a loss of investment income and increase the risk of managers misusing funds. Therefore, how to mitigate the risk of such misuse and improve investment efficiency is a real problem that needs to be solved urgently. Moreover, with the rapid development of the Chinese economy and increasing complexity of business environments, the management of corporate cash flow has become more challenging. The importance of exploring effective strategies to optimize CH and enhance investment efficiency has been recognized by both researchers and practitioners. This study aims to contribute to this ongoing discourse by providing insights into the factors that influence CH and investment decisions of Chinese listed companies, as well as suggesting potential solutions to mitigate the risks associated with excessive CH.

Average cash ratio and cash holdings ratio of A-share listed companies.

Most researchers use company characteristics (Ezeani et al., 2023) and corporate governance mechanisms (Akhtar et al., 2018; Chen et al., 2020) to mitigate the problem. In addition to internal factors, a company’s external environment significantly affects its CH. Regarding external factors, scholars have mainly studied macroeconomic uncertainty (Hoberg et al., 2014), the institutional environment (El Ghoul et al., 2023), and so on. However, external market governance factors have received little attention in relevant research, particularly in product market competition (PMC) (Bo et al., 2024; Sheikh, 2018). PMC has been cited as a unique external governance mechanism. However, inconsistencies exist in terms of the theoretical analysis and empirical research on the impact of PMC on CH. On the one hand, Dasgupta et al. (2018) and Lin et al. (2023) document that an increase in competitive pressures is anticipated to reduce corporate CH. This is because PMC can improve information transparency and supervision mechanisms, which restrains managers’“self-interest” and mitigates information asymmetry, leading enterprises to reduce their CH level. However, some researchers present opposing results. They demonstrate a positive correlation between cash reserves and fierce market competition (Della Seta, 2011; Morellec et al., 2014). First, PMC has a predatory effect. Fierce market competition encourages enterprises to hold more cash to prevent competitors from “plundering” (Fresard, 2010; Guiltinan & Gundlach, 1996). Second, some researchers use agency theory to posit that CEOs tend to maintain substantial cash reserves to enjoy greater discretion and autonomy, which may go unchecked. Furthermore, self-serving CEOs could potentially leverage these excess cash reserves to pursue personal gains. Third, Li et al. (2021) document that the Confucian culture leads to managers holding more cash to defend against crises, and such approach can significantly reduce the adverse impact of financial crises on corporate performance. In addition, Confucianism emphasizes “danger in peace,” namely being prepared before the danger, which often leads to continuous high CH levels.

The above analysis shows that empirical research presents conflicting results, partly because of the challenges associated with accurately gauging the extent of PMC. This is because proxy variables for PMC (such as the Herfindahl–Hirschman Index (HHI) and industry concentration) may not accurately reflect non-price competition in the Chinese market. Accordingly, a need exists to create a comprehensive competition index, which combines HHI, policy dependence, patent density, regional market segmentation and other indicators through principal component analysis (PCA) to form a comprehensive PMC index. Moreover, the complexities surrounding the relationship between CH and market competition extend beyond agency conflict and predatory motivation. For instance, firms operating in highly competitive environments often require significant cash buffers to finance innovative projects, respond swiftly to market dynamics, and capitalize on emerging opportunities. These strategic considerations can overshadow the influence of agency problems in shaping cash-reserve policies. Therefore, how does fierce market competition affect a company’s strategy for managing its cash reserves? Do corporations often increase their cash reserves to manage uncertainty, or decrease their CH to exploit market opportunities? Furthermore, when presented with various growth prospects, do corporations often increase or decrease their cash reserves? Is the objective for preventive purposes, such as addressing market volatility and uncertainty, or for governance purposes, such as enhancing an enterprise’s governance system and market competitiveness? However, the findings of the relevant theoretical analyses do not align with the empirical results. Moreover, considering China’s unique characteristics and market structure, traditional Western economic theory cannot efficiently address these questions. Based on the above analysis, a series of research problems must be considered. First, how does fierce market competition affect a company’s strategy for managing its cash reserves in China? Second, when presented with various firm growth prospects, do corporations often increase or decrease their cash reserves?

Accordingly, through PCA, this study creates a comprehensive competition index, which combines HHI, policy dependence, patent density, regional market segmentation and other indicators to form a comprehensive PMC index. This method solves the problem that proxy variables for PMC (such as the HHI and industry concentration) may not accurately reflect non-price competition in the Chinese market. This study enriches the research framework on CH and adds to the theoretical evidence and empirical support for corporate governance effects among Chinese listed companies.

This study examines the relationship between a company’s growth opportunities and CH and the influence of product market competition on this correlation. The sample period is from 2010 to 2022. The findings revealed a robust and significant correlation between a company’s growth opportunities and CH. However, PMC mitigates the above relationship. The empirical results suggest that PMC encourages enterprises to improve governance and supervision mechanisms, which can reduce agency problems for managers and improve cash investment efficiency by mitigating information asymmetry.

Various checks confirm the robustness of the empirical results. A generalized Method of Moments (GMM) regression was used to recheck the results and address endogeneity problems. The findings indicate that high-growth opportunity enterprises are positively correlated with CH, and PMC alleviates the above positive association.

The remainder of this paper is organized as follows: Section 2 presents a literature review and hypotheses. Section 3 describes the data sources and methodology. Section 4 analyzes and evaluates the findings. Finally, Section 5 summarizes the findings.

Literature Review and Hypotheses

Nexus Between Corporate Growth Opportunity and Cash Holdings

The relationship between growth opportunities and CH is multifaceted and is influenced by various theoretical frameworks and empirical evidence. Some researchers find a positive correlation between corporate growth opportunities and CH. Bo et al. (2024) suggested that firms prefer internal financing over external financing due to information asymmetry and transaction costs. In the context of high-growth enterprises, this preference becomes even more pronounced because external financiers may perceive higher risk and demand higher returns, thereby increasing the cost of capital. Therefore, maintaining higher CH serves as a strategic buffer for these firms, thereby enabling them to fund their rapid growth without being constrained by external financing conditions. In addition, Saravia et al. (2021) highlighted that firms with higher growth prospects tend to have higher systematic risk, which may affect their financing decisions and CH. Abdeljawad et al. (2024) established that firms with high growth opportunities maintain higher cash reserves to mitigate potential financing constraints and seize future investment opportunities. This finding suggests that the relationship between growth opportunities and CH is nuanced and influenced by various financial and strategic considerations. In addition, agency theory posits that managers may use excess cash for personal benefits rather than to maximize shareholder wealth (Hasan et al., 2022; Moolchandani & Kar, 2022). Hence, in high-growth firms with abundant CH, the potential for agency conflicts between managers and shareholders could be exacerbated. Ji and Chen (2020) determined that the higher the enterprise’s growth opportunities, the higher the demand for CH. Myers (1977) divided enterprise values into existing assets and future growth values. High-growth enterprises rely more on future growth value, which, in turn, encourages them to seek more investment opportunities, thereby providing executives with more room for manipulation. However, increasing investment opportunities reduce the observability of management behavior, consequently allowing executives to choose investments that satisfy their personal interests (Smith Jr & Watts, 1992). Furthermore, executives have more information on future investment projects. This means that high-growth enterprises can stimulate executives’ opportunistic behaviors, which may lead to agency issues becoming more prominent (Jensen & Meckling, 2019).

Pecking Order Theory is suitable to explain this problem. Myers and Majluf (1984) proposed that firms prioritize internal funding (such as cash reserves) over debt and equity. This is because high-growth firms face information asymmetry (external investors have difficulty assessing their potential), which results in higher external financing costs and, therefore, greater reliance on internal cash reserves. For example, R&D-intensive firms (such as pharmaceuticals and technology companies) typically use cash reserves to support long-term R&D projects rather than frequently issuing equity (Nguyen & Nguyen, 2025). Furthermore, as small and medium-sized enterprises (SMEs) have limited access to external financing, the positive correlation between growth opportunities and CH is more pronounced (Bo & Li, 2025; Faulkender, 2002). Accordingly, this study proposes the following hypothesis:

Moderating Role of Product Market Competition

Ji and Chen (2020) found that the higher the enterprise’s growth opportunities, the higher the demand for CD. Myers (1977) divided enterprise values into existing assets and future growth values. High-growth enterprises rely more on future growth value, which in turn encourages them to seek more investment opportunities, thereby providing enterprise executives with more room for manipulation. Opler et al. (1999) demonstrated that high-growth businesses have greater investment opportunities when the market experiences financing constraints. However, increasing investment opportunities reduces the observability of management behavior, thereby allowing executives to choose investments that satisfy their personal interests (Smith Jr & Watts, 1992). Furthermore, executives have more information on future investment projects. This means that high-growth enterprises can stimulate executives’ opportunistic behaviors, which may lead to agency issues becoming more prominent (Jensen & Meckling, 2019).

Enterprise CH level is significantly influenced by corporate governance efficiency. Chan et al. (2013) demonstrated that PMC, as a unique external governance mechanism, can link self-profit motivation in an external environment. First, PMC enhances company information transparency, which can prevent managers achieving “self-profit” by holding large amounts of cash and reducing the company’s CH (Lin et al., 2022). Second, PMC enhances enterprise information disclosure, complements equity concentration and executive incentives, and exerts an alternative influence on the governance mechanism of the board of directors (Huang et al., 2023). Third, PMC can reduce agency costs, improve operational efficiency, and influence specific internal governance mechanisms (Lin et al., 2023). Fourth, the higher the PMC, the more efficient the supervision and control system, which results in a more reasonable CH level and higher enterprise value (Mousavi Shiri & Eramiyan, 2022).

The above analysis reveals that PMC reduces information asymmetry efficiently, which mitigates enterprises holding more cash and improves cash-use efficiency. This is because PMC is not only a corporate governance mechanism but also a market competition mechanism (Shleifer & Vishny, 1997). The latter mechanism is the core power in the market economy that regulates resource allocation, determines enterprises’ profits and losses, and promotes technological progress. Moreover, market participants can access price, quality, goods, and service information. Market competition pushes companies to improve efficiency and reduce costs to gain a market share. In addition, through the price mechanism, resources flow to the most efficient areas to achieve optimal allocation. Furthermore, fierce PMC alleviates information asymmetry and financing constraints, significantly improving the likelihood of corporate governance efficiency resulting from market competition. Furthermore, China’s low level of corporate governance has left ample space for market competition. Consequently, PMC promotes the development of corporate governance mechanisms and reduces asymmetric information, which can motivate managers to exert greater effort and enhance their work–performance comparability. According to Jain et al. (2013), PMC not only reduces excess cash reserves, but also increases cash-use efficiency, thereby resulting in improved business performance and enterprise value. As a result, fierce PMC alleviates information asymmetry, which improves cash-use efficiency and help managers grasp future good investment opportunities. Finally, the high level of information transparency efficiently reduces financing costs for companies and information cost for commercial banks, which mitigates financing constraints for companies and improves investment efficiency.

In addition, fierce PMC promotes information transparency, which improves corporate governance mechanisms and alleviates financing constraints and agency problems (Bo et al., 2024). Consequently, the governance effects of PMC are more significant for enterprises with high growth opportunities. PMC effectively alleviates information asymmetry, improves corporate governance and supervision, and mitigates agency issues. Compared to low growth-opportunity enterprises, corporate information asymmetry is more severe in high growth-opportunity enterprises (Bo et al., 2024). However, fierce PMC alleviates information asymmetry and restricts executives’ self-interested behavior when making decisions. Therefore, the governance effects of the PMC are more significant for the CH of high-growth opportunity enterprises. Thus, we propose the following hypothesis:

Data and Methodology

We collected data from A-share Chinese listed firms on the Shanghai and Shenzhen Stock Exchanges between 2010 and 2022, which includes 5023 samples. We sourced data from the China Stock Market & Accounting Research Database (CSMAR) and analyzed them using Stata statistical software. A total of 45,303 observations were obtained, which does not include ST and financial companies. All variable definitions are shown in Table 1.

Definition of Variables.

Models 1 and 2 were constructed to examine the correlation between PMC and CH and how growth opportunities impact this relationship, respectively.

Model 1:

Model 2:

where CH denotes corporate cash holdings. TBQ denotes Tobin’s Q. PMC denotes product market competition. denotes an error term. CV is the control variable.

PMC is a comprehensive competition index, which combines HHI, policy dependence, patent density, regional market segmentation, and other indicators through PCA.

where Xi denotes the primary business income of a company, and X denotes the total primary business income of the industry.

Principal Component Analysis (PCA) Steps:

Extract the Main Components

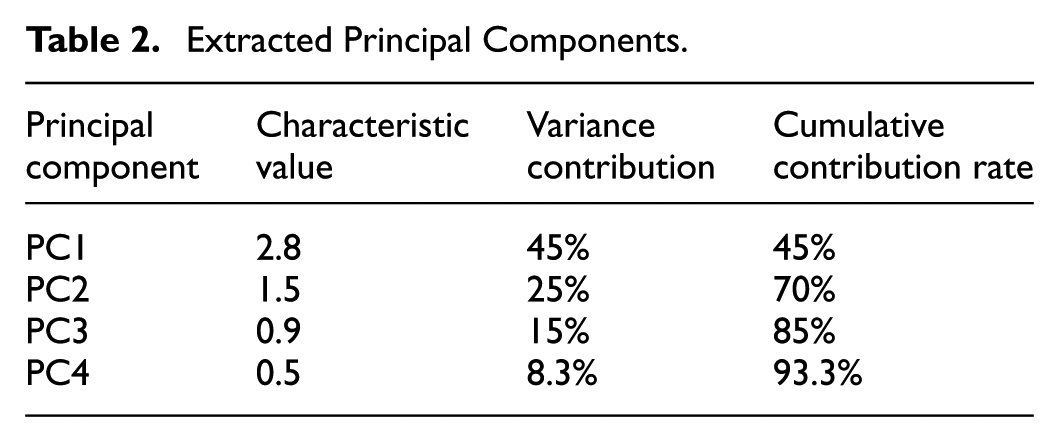

Extract principal components: determine the number of components based on the cumulative variance contribution rate (usually greater than 70%).

According to the Kaiser Criterion, the characteristic value ≥1 should be retained for the principal components. Therefore, we selected the first two principal components with a cumulative contribution rate of 70%.

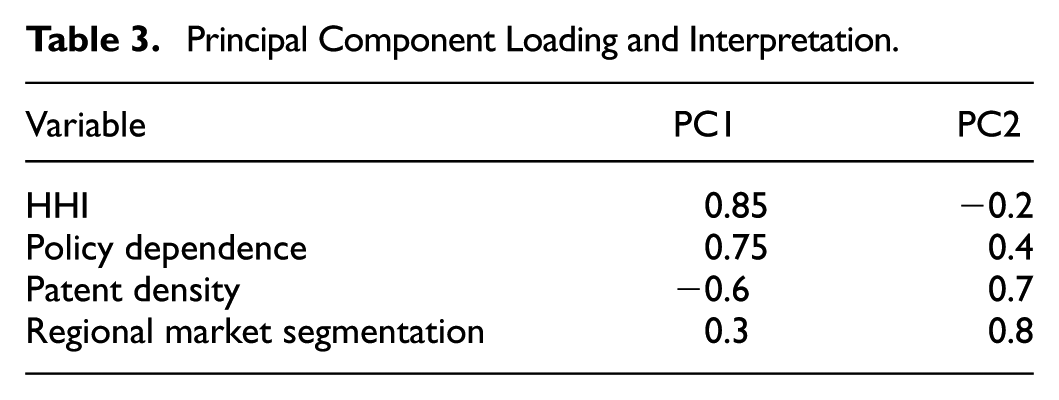

Principal Component Loading and Interpretation

Based on the Table 2, determine the correlation coefficient (loadings matrix) between the principal components.

Extracted Principal Components.

Economic explanation:

Formula: Based on the Table 3, PC1 and PC2 can be calculated as follows:

Principal Component Loading and Interpretation.

Results

This section discusses the panel results. First, descriptive statistics, correlation analysis, and the Hausman test are conducted.

The Hausman test is a statistical test used to determine the appropriateness of using either fixed- or random-effects models in a linear regression analysis. In other words, the test evaluates whether the residuals of the two types of models are correlated with the dependent variables. If no correlation exists, then the random-effects model (REM) is appropriate; otherwise, the fixed-effects model (FEM) should be used. The test is named after economist Jerry Hausman who developed it in 1978. The Hausman test follows three steps: First, the Poolability test is used to test ordinary least squares (OLS) and FEM. The result shows that p = 0. P < 0.05 indicates FEM is better than OLS, which means the FEM outperformed the mixed OLS model. Second, the Breusch and Pagan Lagrangian Multiplier test is used to test for random effects. The result shows that p = 0. P < 0.05 indicates REM is better than OLS, which means the REM outperformed the mixed OLS model. The third step is the Hausman test. The result shows that p = 0. P < 0.05 indicates FEM is better than REM, which means the FEM outperformed the REM. The Hausman test indicates that the FEM is the best model in this regression. Accordingly, we used the FEM as the base regression model.

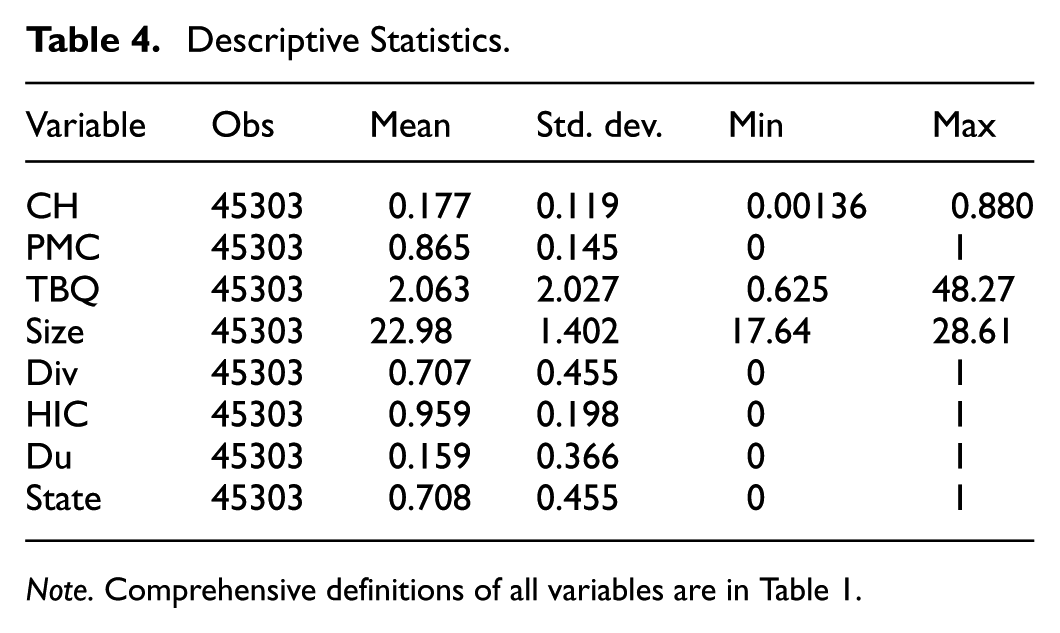

Table 4 indicates that the variable contained 45303 observations. The average value of CH was 17.8%. The mean PMC value was 0.865. A higher PMC value indicates greater competition in the product market.

Descriptive Statistics.

Note. Comprehensive definitions of all variables are in Table 1.

Pearson’s correlation was used to assess the association between the variables (Table 5). The primary objective of the Pearson correlation test is to determine whether multicollinearity among independent variables is an issue, which arises if correlation coefficients are higher than 0.8 (Bo et al., 2024). However, the correlation coefficients for the variables range from −0.123 to 0.145, which did not exceed the upper limit of 0.8, as shown in Table 5. These findings suggest that no multicollinearity issues exist in the current study.

Pearson’s Correlation Matrix.

Note.***, **, and * = p < .01, p < .05, and p < .1, respectively. Comprehensive definitions of all variables are in Table 1.

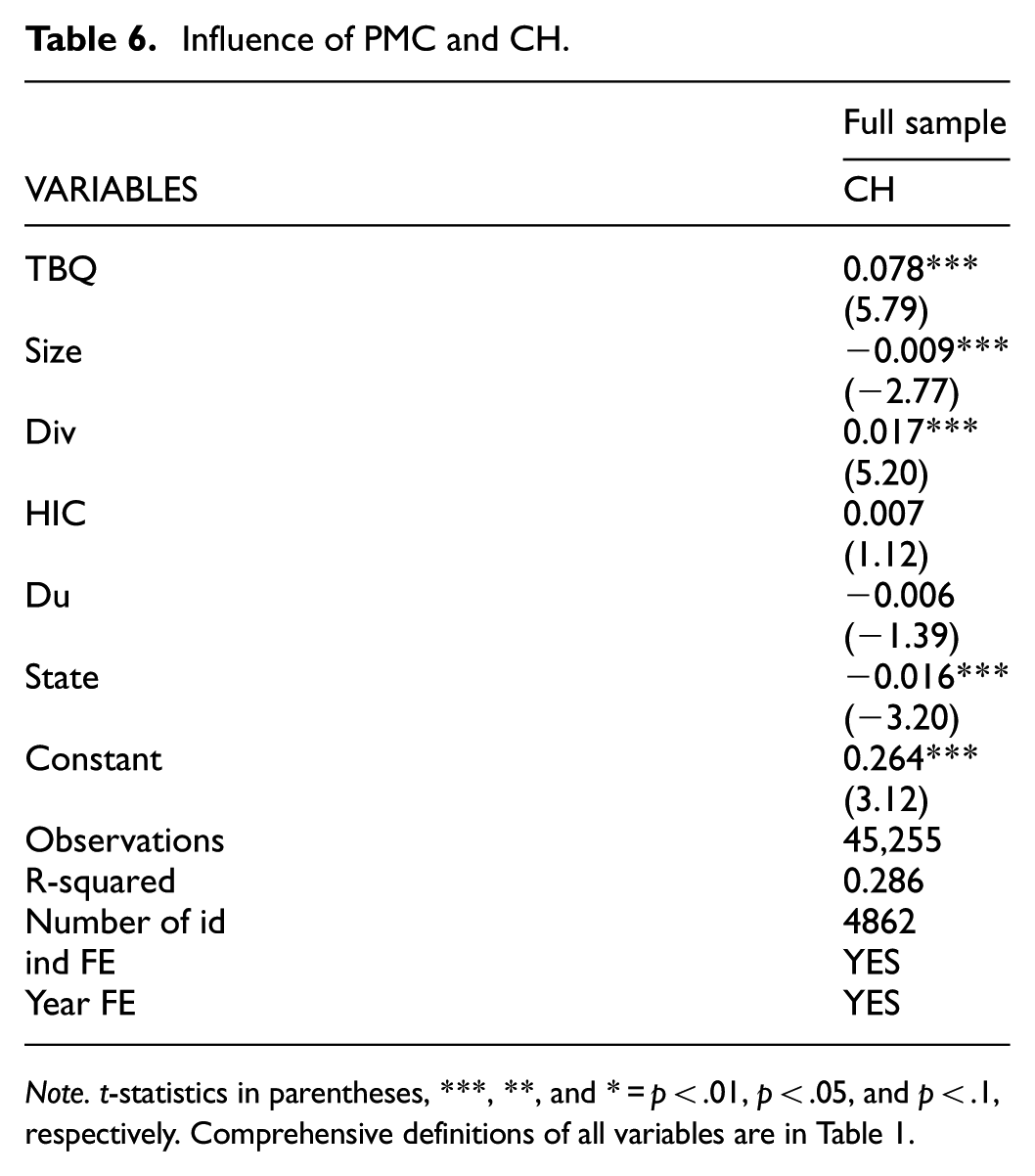

In Table 6, the coefficient of TBQ is 0.078 and significant at the 1% level. This means that enterprise growth opportunity has a positive relationship with CH level. In economic terms, on average, each standard deviation increase in TBQ (2.027) results in an increase in CH of 13.28% of the sample standard deviation ( = 0.078 × 2.027/0.119). In summary, the positive and significant coefficients of TBQ support H1 in regressions that adopt CH; therefore, H1 is supported.

Influence of PMC and CH.

Note. t-statistics in parentheses, ***, **, and * = p < .01, p < .05, and p < .1, respectively. Comprehensive definitions of all variables are in Table 1.

This study uses PMC as a moderating variable to examine the moderating effect. The regression results for TBQ and CH are reported in Table 7. The results reveal a negative correlation whereby PMC reflects the level of market competition condition. The coefficient is -0.002 and significant at the 1% level. This means that PMC mitigates the positive relationship between TBQ and CH, which supports H2. In addition, the coefficient of the PMC × TBQ is −0.003 for the high growth-opportunity enterprises and is significant at the 1% level. However, PMC × TBQ is −0.007 for the low growth-opportunity enterprises, which is insignificant. This means that PMC significantly mitigates high growth-opportunity enterprises holding more cash. This finding strongly supports H2.

Impact of Product Market Competition on Corporate Growth Opportunities and Cash Holdings.

Note. t-statistics in parentheses, ***, **, and *p < .01, p < .05, and p < .1, respectively. Comprehensive definitions of all variables are in Table 1.

Robustness Test

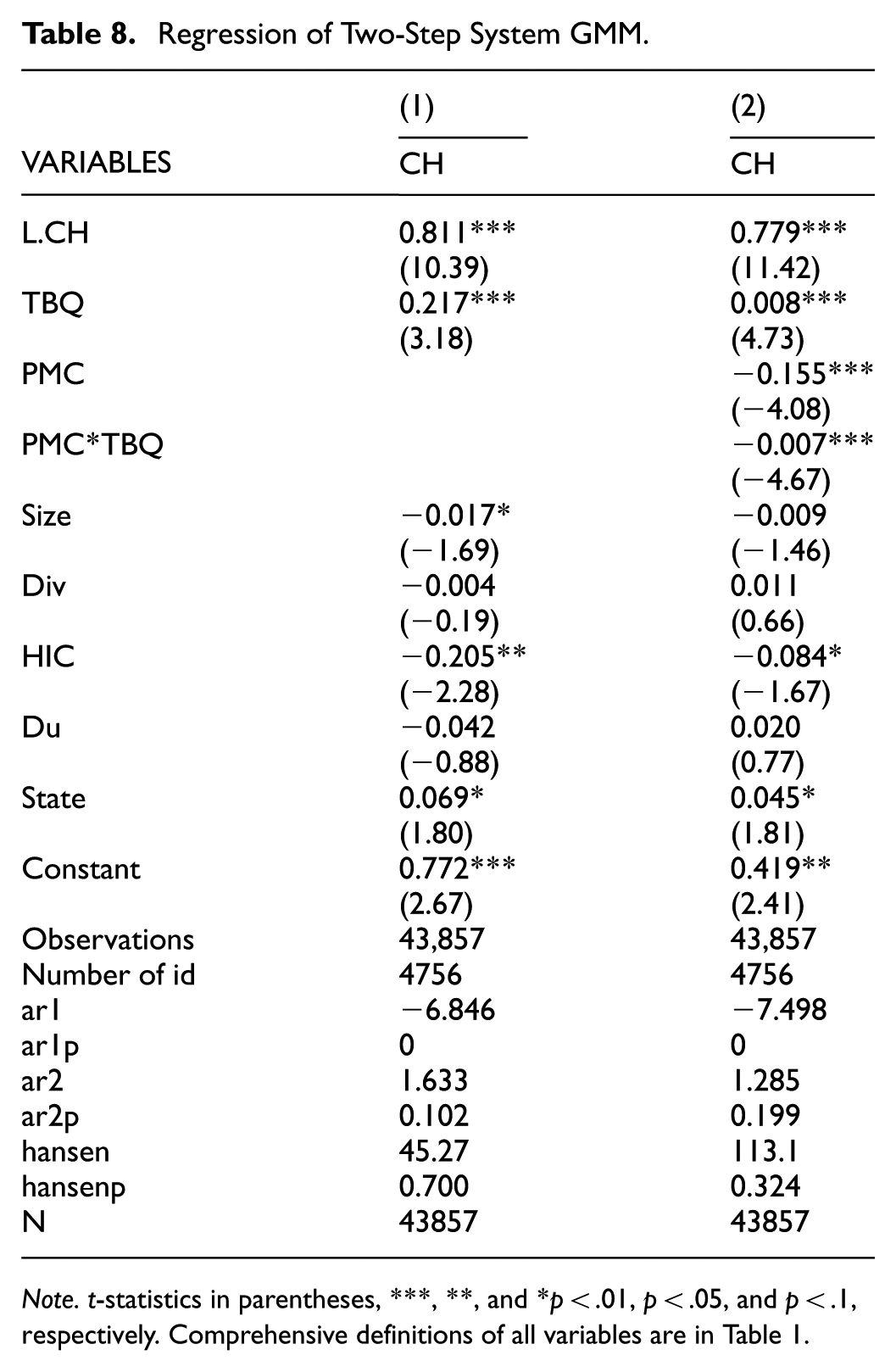

Wang et al. (2023) highlighted that the connection between governance mechanisms and financial problems may face a significant challenge due to endogeneity. The static FEM is prone to bias when a significant dynamic relationship exists between the current dependent and future independent variables. In such cases, a two-step GMM system is recommended (Barros et al., 2020).

The results of the GMM regression in Table 8 reveal a negative relationship for PMC and CH at the 1% level with a coefficient of −0.217. In addition, TBQ*PMC indicates a negative relationship, which means that fierce PMC restrains high growth opportunity enterprises from holding excessive cash. This result is consistent with that of the baseline regression.

Regression of Two-Step System GMM.

Note. t-statistics in parentheses, ***, **, and *p < .01, p < .05, and p < .1, respectively. Comprehensive definitions of all variables are in Table 1.

Further Analysis

The relationship between CH and market competition may be mediated by other factors such as firm size, financial leverage, and governance structure. Larger firms and state-owned enterprises (SOEs) with diverse revenue streams and established market positions may be less reliant on cash reserves compared to smaller, non-SOEs, which are more vulnerable to competitors. Similarly, firms with robust governance mechanisms may be better equipped to monitor and mitigate agency issues, thereby reducing CEOs’ incentives to accumulate excess cash for personal gain.

China’s economic development has led to substantial corporate governance differences between SOEs and non-SOEs. From the perspective of the entire governance transmission process, compared with non-SOEs, a more efficient incentive system is needed for SOEs in the market monopoly position. First, some SOEs have a low degree of market competition. SOEs monopolized almost all industries in China during the planned economic period. With the development of China’s market economy, the rapid growth of the private economy has introduced competition into many fields of the national economy. However, private enterprises encounter various restrictions when entering a monopolistic field. Currently, SOEs dominate many monopoly industries, thus resulting in low market competition and limited governance effects. Second, the executive incentive mechanism of SOEs is inefficient. From appointment to the design of remuneration contracts, the incentive mechanism of SOE executives needs improvement. These include SOE executives’ partial reliance on the administrative appointment of higher authorities, which diminishes competitors’ drive for promotion through performance competition, and the lack of internal promotion incentives (Zeng et al., 2022). In addition, SOEs must assume more social responsibilities and are the “main tools” for the government to implement macroeconomic regulation, control, and industrial policies. However, these tasks are often difficult to measure accurately. The goals of non-SOEs are more focused on corporate performance, and the characteristics of straightforward evaluation of performance make the incentive mechanism for executives relatively effective. In addition, government departments have imposed compensation controls on executives of SOEs in some industries, further weakening the incentive effect of remuneration on such executives. Finally, it is easier for SOEs to obtain bank loans. SOEs with “natural origins” and more political connections are more likely to receive government support and bank loans than private enterprises. This lending convenience will undoubtedly reduce the governance effect of market competition on enterprises’ CH.

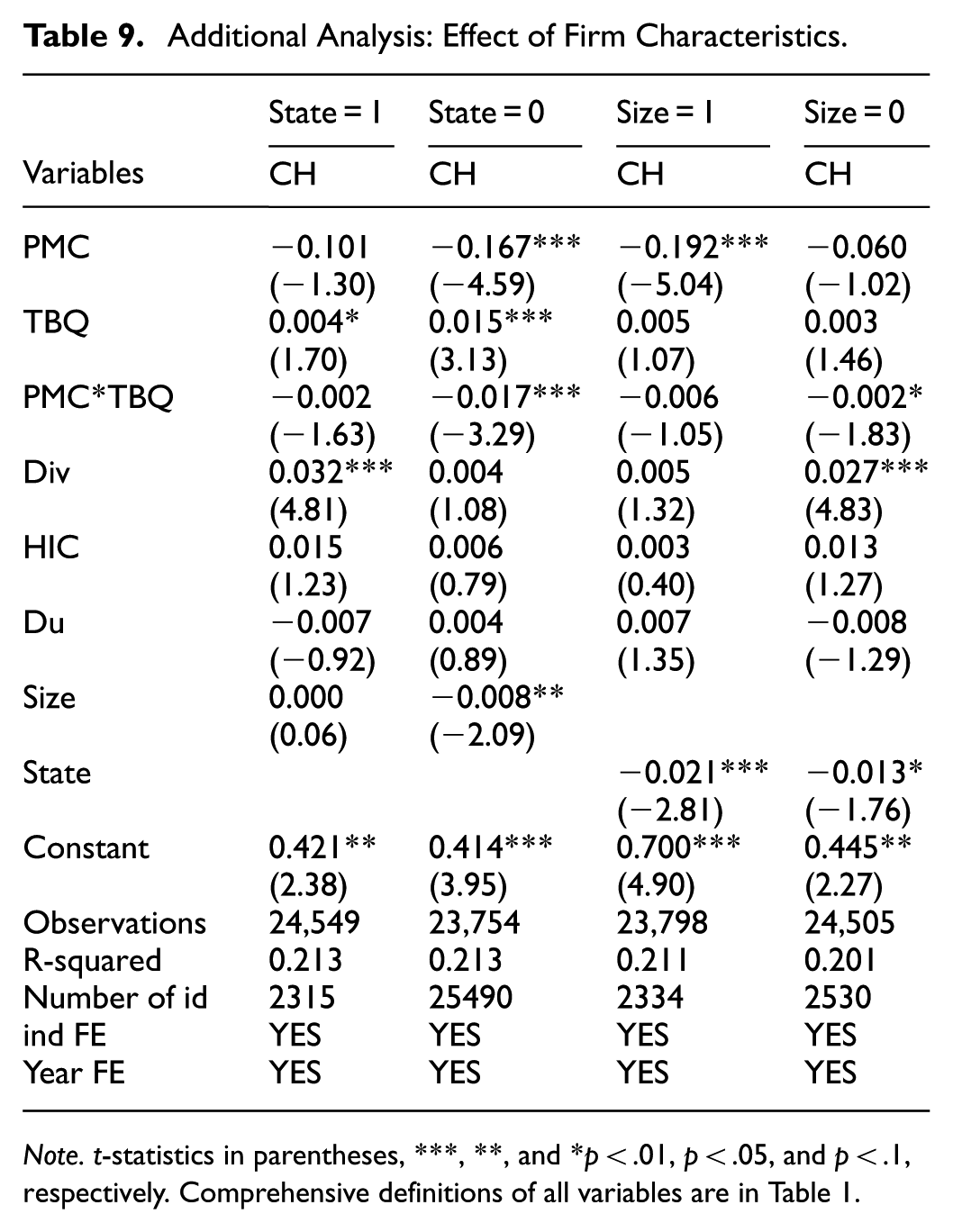

This section investigates the effects of PMC by examining firm characteristics in more depth. Rahman (2018) highlighted that non-SOEs and small-sized firms in China find it harder to obtain external financing than SOEs and large-sized enterprises, and this process is more sensitive and challenging for the former (Cheng & Masron, 2023; Lee & Lim, 2021). However, fierce market competition can mitigate information asymmetry and alleviate financing constraints and costs for both non-SOEs and small firms. This analysis raises the following question: Does increased PMC have a stronger or weaker impact on non-SOEs and small-sized firms with high growth opportunities for CH? The following hypothesis is proposed: PMC is more effective for enterprises’ CH with high growth opportunities when firms are small and non-state-owned. We recalculated the equation using four distinct subsets: SOEs, non-SOEs, and large and small firms, as measured by mean size.

A comprehensive list of the business characteristics that must be considered when analyzing the influence of PMC on the aforementioned relationships is provided in Table 9.

Additional Analysis: Effect of Firm Characteristics.

Note. t-statistics in parentheses, ***, **, and *p < .01, p < .05, and p < .1, respectively. Comprehensive definitions of all variables are in Table 1.

The Model (1) regression results in Table 9 demonstrate a significant regression coefficient of -0.167 for PMC in the non-SOE group, which is significant at the 1% level. This finding suggests that PMC exerts a strong governance effect on CH levels in non-SOEs. The regression coefficient for PMC in the SOE group was −0.101, but insignificant. This means that PMC still has a governance effect on the CH level of SOEs, but it is not significant. The regression results for Model (2) reveal that the SOE and non-SOE groups have interaction coefficients of −0.002 and −0.017***, respectively. Non-SOEs have a significant interaction effect at the 1% level, which suggests that higher growth opportunities enhance the governance effect, thereby supporting H2. At the same time, the interaction term coefficient of the non-SOE group is 8.5 times that of the SOE group; this finding indicates that the increase in market competition intensity will lead to a much faster decline in the CH level of non-SOEs than that of SOEs under the same growth background, which suggests that the governance effect of market competition is more effective for non-SOEs.

In addition, the interaction coefficient in Column (3) is not significant, but is significant in Column (4) at the 10% level. These results suggest that PMC is more effective for SMEs with high growth opportunities. This shows that, under the same growth background, an increase in market competition intensity leads to a much faster decline in the CH level of small firms than that of large firms, thereby implying that the governance effect of market competition is more effective for small firms.

Conclusion

Our findings indicate a positive correlation between high-growth opportunity enterprises and CH level, but fierce PMC mitigates this correlation. This means fierce PMC alleviates information asymmetry, which restrains high-growth opportunity enterprises from holding excessive cash and improves cash-use efficiency. Based on the above research conclusions, this study presents the following recommendations:

First, the degree of market competition among SOEs needs to be increased. To address inefficiencies in corporate governance, policymakers should prioritize increasing market competition among SOEs, particularly in monopolistic industries. Empirical evidence indicates that low competition in sectors dominated by SOEs (e.g., PetroChina, Sinopec, China Unicom) weakens the governance-enhancing role of market forces (Ji & Chen, 2020). To mitigate this, the following measures are critical: First, introduce competition in monopoly sectors. Deregulate entry barriers to allow private and foreign firms to compete in traditionally state-controlled industries (e.g., energy, telecommunications). Second, structural reforms such as separating natural monopoly components (e.g., network infrastructure) from competitive segments (e.g., retail services) to enable fair competition. Third, liberalize resource allocation by replacing administrative monopolies with market-driven mechanisms, thereby ensuring public resources are allocated via competitive bidding or pricing.

Second, the incentive mechanisms for senior executives of enterprises should be improved. Enterprises should fulfill their economic, political, moral, legal, environmental, and social responsibilities. Moreover, enterprises must consider the dual goals of economic and social benefit. However, the current remuneration contract requires an assessment to measure executives’ efforts in non-economic interests, thus necessitating the inclusion of non-economic benefit evaluation indicators to fully measure the extent of these efforts. Promotion theory posits that enterprises can achieve promotion incentives through internal competition, thereby enhancing their future performance. Therefore, if higher authorities can constrain the administrative appointments of senior executives, especially in SOEs, this will enhance their incentive mechanisms. Moreover, the government’s direct “remuneration control” over executives lacks a legal foundation and could potentially impact their incentive effects. Therefore, the influencing factors of executive compensation must first be addressed, the “self-interest” factors of executives such as management power eliminated, and the weight of necessary factors such as performance and scale reasonably determined to optimize the incentive mechanism of senior executives (Allen, 1981; Van Essen et al., 2015; Wang et al., 2023).

Third, political relationships limit the convenience of loans. The “natural origin” of SOEs and their increased political connections have provided credit facilities to these enterprises. The lending effect of political connections is particularly significant in regions with slower financial development, lower rule of law, and more severe government property rights violations (Lin & Bo, 2012; Nguyen & Wong, 2021). This means that SOEs that receive more loans from political connections tend to have less efficient external governance (Huang et al., 2023). Moreover, such governance will give executives of companies with large amounts of cash more room to achieve “self-interested” behavior, and the convenience of financing will also limit the governance effect of PMC on such behavior. In addition, if enterprises rely on political connections to obtain bank loans, they inevitably increase the cost of allocating resources to society. Therefore, improving the financial market and related institutional environment and reducing the loan convenience brought about by the political relations of SOEs play essential roles in improving the governance effect of market competition and the efficiency of social resource allocation.

Although this study possesses certain research value, some limitations must be acknowledged. For example, the impact of market competition on CH may vary across industries. Characterized by rapid technological advancements and short product cycles, some sectors may necessitate higher cash reserves to support continuous innovation and adaptation. Conversely, industries with stable market conditions and predictable demand patterns may not require substantial CH to the same extent. However, this study did not analyze this problem. Therefore, future research should strive to develop more refined measures of market competition and explore the nuanced interactions between cash policies, firm strategies, and industry characteristics.

Footnotes

Ethical Considerations

All procedures performed in studies involving human participants were in accordance with the ethical standards of the institutional and/or national research committee and with the 1964 Helsinki Declaration and its later amendments or comparable ethical standards.

Author Contributions

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The authors declared the following potential conflicts of interest with respect to the research, authorship, and/or publication of this article: The results presented in this manuscript have not been considered for publication elsewhere. None of the manuscript’s contents have been previously published or posted on the internet. The authors do not have any conflicts of interest to disclose. All of the authors have read and approved the final version of this manuscript.

Data Availability Statement

Data sharing not applicable to this article as no datasets were generated or analyzed during the current study.