Abstract

Asymmetric information and economic uncertainty result in more severe financial constraints on Chinese enterprises. This induces them to hold more cash to defend against economic uncertainty and intense market competition. This study examines the correlation between internal corporate governance and cash holdings in China. It uses 6,849 observations from 922 Chinese listed companies between 2010 and 2022. Additionally, it uses the fixed effects method and the generalized method of moments for quantitative analysis, with internal corporate governance as the independent variable and cash holdings as the dependent variable. The observations illustrate that internal corporate governance has a significant positive effect on Chinese firms’ cash holdings. However, product market competition mitigates the relationship between corporate governance and cash holdings. This study efficiently connects internal and external governance mechanisms, and improves our understanding of corporate governance concerning cash holdings.

Plain language summary

This study examines the correlation between internal corporate governance and cash holdings in China, using 6,849 observations from 922 Chinese listed companies between 2010 and 2022. It used the fixed effects method and the generalized method of moments for quantitative analysis, with internal corporate governance as the independent variable and cash holdings as the dependent variable. The findings illustrate that internal corporate governance has a significantly positive impact on Chinese firms’ cash holdings. However, product market competition mitigates the relationship between corporate governance and cash holdings. This study efficiently connects internal and external governance mechanisms and improves our understanding of corporate governance concerning cash holdings.

Keywords

Introduction

The financial crisis had a substantial impact on increasing the public awareness of the necessity for cash reserves. For nonfinancial Chinese listed companies (nonfinancial), the median value of the cash holding level is 13%, with a mean of 18% (Bo et al., 2024). The mean value is higher than the median value. This demonstrates that Chinese public companies have significant cash reserves. In addition, Figure 1 shows that compared with other countries, China has a high level of cash holdings. This is owing to the imperfect capital market and governance mechanisms in China. Both external financing and internal agency costs are high for companies (Liu et al., 2023). Why do Chinese public companies reserve more cash from internal financing: is to defend against external financing constraints or to satisfy personal interests? What factors contribute to high cash holding levels: agency issues or precautionary motives? These questions necessitate an in-depth investigation. Moreover, extensive research has been conducted on the correlation between internal corporate governance and cash holdings (H. Chen, Yang, et al., 2020). Therein, the focus has been on the transaction motives, the precautionary motives, the prevention of underinvestment, and other factors (Almeida et al., 2004). In addition, scholars state that given the external financing constraints, the investment expenditures can be determined by the amount of endogenous capital available (Fazzari et al., 1988). Nevertheless, maintaining significant cash reserves can generate agency issues (Shah, 2018).

Cash ratios of different countries.

Managing liquidity is a crucial issue for many Chinese enterprises. This is particularly so when economic downturns are likely. However, a higher cash holding level may result in agency problems for real-world enterprises. This institutional context provides a distinct opportunity to analyze the influence of efficient internal controls on cash management. Consequently, China’s unique background provides an incentive to assess effective corporate governance to enhance cash management. Additionally, whether the effectiveness of internal corporate governance reduces the information asymmetry for investors and regulators and improves the enterprise operational efficiency for managers remains to be evaluated (Zhu et al., 2020).

Xiong et al. (2020) indicated that in emerging market countries, precautionary and agency motivations affect the cash holding levels. Most relevant studies investigated the effects of board size (Liem et al., 2020), equity structure (Loncan & Caldeira, 2014), financial leverage (Guo et al., 2021), financing constraints (Bukalska & Maziarczyk, 2023), corporate growth, and economic policy on corporate cash holdings (Das et al., 2024; Feng et al., 2022). However, few studies have effectively combined internal and external governance mechanisms to analyze corporate cash holdings. From the perspective of external market competition, this study evaluates corporate governance on enterprises’ cash holding decisions. Additionally, it effectively combines external product market competition (PMC) to enhance the study of corporate cash holdings.

In addition, China has different social and cultural systems and confronts significant challenges when attempting to fully gain from the corporate governance experiences of other countries. The conventional Confucian culture has influenced Chinese businesses. It emphasizes hierarchical and private relationships. These cognitive deviations make it challenging to ensure that governance mechanisms are implemented fully in listed Chinese companies (Zheng & Chen, 2018).

The preceding analysis reveals that several issues cannot be resolved. This makes it critical to consider reasonable cash holding decisions. First, compared with other countries, Chinese listed companies have higher cash holding levels (Bo & Li, 2024). This affects the quality of internal governance and may cause agency problems. Second, previous research did not connect China’s unique culture and market environment, which cannot effectively explain the correlation between internal corporate governance and cash holding level in China. Therefore, the current research conclusions involving various developed and developing countries should be verified to determine whether these apply to China. Third, the use of a single indicator has been studied by many scholars and is relatively mature. However, PCA has been studied less, such as managerial compensation incentives and cash holdings (Y. Jiang et al., 2024; Lou et al., 2021), blockholder ownership and corporate cash holdings (Alomran, 2024), proportion of independent directors and cash holdings (Khidmat et al., 2024; Ullah et al., 2024), board size and cash holdings (Boubaker et al., 2015; Liem et al., 2020), and characteristics of the board of directors’ and cash holdings (Cambrea et al., 2022). Fourth, according to the current research, most studies have focused on internal governance and cash holdings or used the external environment as interaction variables, including variations in the external political and cultural environment. However, further research is required to investigate how product market competitiveness influences the relationship between corporate governance and cash reserves. This implies that external governance mechanisms require more attention in relevant research, particularly with regard to PMC. PMC is a special external governance mechanism that influences the cash-holding levels (Harford et al., 2008; Yu, 2014). However, this also influences the relationship between internal corporate governance and corporate cash holdings. These concerns hinder the decision-making process of listed companies. Therefore, it is important to examine the effect of internal governance on corporate cash holding decisions in China and how PMC influences this relationship.

This study examines the correlation between internal corporate governance and cash holdings by collecting data from 922 public Chinese companies between 2010 and 2022. The empirical results show that high-quality internal corporate governance is positively correlated with cash holdings. Moreover, PMC mitigates these positive correlations.

We conduct a robustness test using these two methods to validate the base regression results. The first method switches the moderating variable from the Lerner index to the HHI. The second approach uses the generalized method of moments regression to solve endogenous problems. The results agree with the benchmark regression results.

This study connects internal and external governance mechanisms to assess the impact of corporate governance on cash holdings. Although researchers extensive research has been conducted on internal corporate governance and cash holdings, PMC has been discussed infrequently as a moderating variable affecting this relationship. This study improves the understanding of internal and external corporate governance in terms of cash holdings. Furthermore, it adds to the theoretical evidence and empirical support for internal and external corporate governance practices and policy formulation among listed Chinese companies.

Literature Review and Research Hypothesis

Internal Corporate Governance and Cash Holdings

Holding cash increases financial flexibility and alleviates financial constraints (Babar & Habib, 2021; Chang & Yang, 2022; R. R. Chen, Guedhami, et al., 2020; Lei et al., 2021; Sun et al., 2022). However, existing literature contains conflicting observations regarding the effect of corporate governance on cash holdings. A few researchers observed a positive correlation between corporate governance and cash holdings (Harford et al., 2008; Hu & Yang, 2022; Zheng & Chen, 2018). In contrast, Akhtar et al. (2024) showed that corporate governance is negatively correlated with cash holdings in areas with high investor protection. Additionally, Lie and Yang (2018) demonstrated that corporate governance does not influence cash holdings.

Confucian culture’s perception of crisis enhances a company’s precautionary cash holding motivation. Owing to imperfect capital markets and external adverse shocks such as financial crises, companies generally encounter potential financial crises. As the “blood” on which companies rely for survival, cash is the most important tool to ensure liquidity and prevent financial risks (Bates et al., 2009). Out of precautionary savings motivation, companies generally hold a large amount of cash to prevent financial difficulties. Recent studies have shown that culture has an important impact on corporate risk-taking and cash-holding behaviors (Y. Chen et al., 2015; K. Li et al., 2013). Confucianism is the foundation of Chinese culture. It consistently promotes the concept of “readiness for hazard” during peaceful times, emphasizes the risk prevention principle of “preparedness for danger,” and induces individuals to maintain a high level of crisis awareness and readiness even in stable circumstances. This perception of crisis and cognitive imprint profoundly affect corporate executives’ risk attitudes and sensitivity to uncertainty, thus significantly enhancing the precautionary savings motivation. This, in turn, induces companies to be more cautious and hold more cash to ensure financial security and circumvent crises.

Scholars have observed that internal financing is less expensive than external financing (Chaklader & Padmapriya, 2021; Frank et al., 2020). Additionally, companies should maintain a certain amount of cash reserves to satisfy their daily transactional requirements (Zhao et al., 2023). High cash holding levels help enterprises reduce their cost of capital (K. Zhang & Zhou, 2023). However, excessive cash holdings can result in agency issues (Javadi et al., 2021). Meanwhile, high-quality internal corporate governance effectively alleviates agency problems and induces managers to make rational decisions for long-term success (Dey, 2008).

In China, corporate financing channels are relatively limited, particularly for small- and medium-sized enterprises (SMEs) (D. J. Denis & Sibilkov, 2010; Rashid & Ashfaq, 2017). Additionally, China’s financial markets are relatively immature, which further exacerbates financing difficulties. Thus, corporations may maintain higher money levels to mitigate the potential limitations of financing constraints (Dittmar & Thakor, 2007; Froot & Stein, 1991). If a company wishes to achieve long-term sustainable development, it is essential to maintain an adequate cash holding level to defend against future risks and financing constraints. Therefore, Chinese listed companies are willing to hold more cash because they can reduce agency problems through high-quality internal governance. Based on the preceding analysis, we propose the following hypothesis:

Hypothesis 1: High quality internal corporate governance is positively correlated with cash holdings.

Moderating Effect of Product Market Competition

Currently, there is no consensus on the impact of PMC on cash holdings. First, a few scholars indicated that when the PMC is high, managers increase their free cash for preventive incentives, and senior executives promote the relationship positively. This implies that businesses require a specific amount of cash reserve to address unforeseen economic situations (Shah, 2018). Haushalter et al. (2007) illustrated that intense PMC generates plundering risk from competitors. This induces enterprises to hold more cash (Hoberg et al., 2014). Consequently, intense market competition can increase the risk of capital chain rupture and cause enterprises to undergo financial difficulties owing to insufficient cash holdings. This, in turn, results in missed investment opportunities and market share (Lin et al., 2023). From this perspective, companies with good internal corporate governance are recommended to implement high-level cash holding policies to increase corporate competition, which helps reduce financing costs.

However, other scholars present different perspectives on this topic. According to the resource orchestration theory, managers who efficiently allocate and utilize their resources can achieve a high level of performance (Q. Zhang & Hua, 2020). Scholars contend that in an intensely competitive market, a higher information transparency induces companies to maintain lower cash reserves and flexibility. This is because the resource orchestration theory highlights the importance of resource scarcity in companies’ decision-making. The opportunity costs should be considered appropriately to prevent wasteful resource allocation. Higher cash holding costs can reduce a company’s market response. This is because it may not effectively utilize funds to adapt to market transitions or capitalize on new business opportunities (Almeida et al., 2004). Given this situation, holding excessive cash could hinder a company from responding rapidly to market transitions. Operations with a significant cash reserve indicate that a company may omit profitable projects, thereby resulting in missed growth and profitability opportunities. Additionally, companies may become overly cautious regarding their investment decisions if they hold excessive cash. This can ultimately reduce their market reaction rates (D. K. Denis and McConnell, 2003). Moreover, intense market competition may enhance asset liquidity and alleviate external financing constraints by mitigating information asymmetry and reducing the need to maintain substantial cash reserves (Dittmar & Mahrt-Smith, 2007). Chan et al. (2013) demonstrated that PMC, as a unique external governance mechanism, can link self-profit motivation to an external environment. First, PMC enhances company information transparency, which can prevent managers from achieving “self-profit” by holding large amounts of cash and reducing the company’s cash holdings (Aburisheh et al., 2022). Second, PMC enhances enterprise information disclosure, complements equity concentration and executive incentives, and exerts an alternative influence on the governance mechanism of boards of directors (Y. Chen et al., 2022). Third, PMC can reduce agency costs, improve operational efficiency, and influence specific internal governance mechanisms (Lin et al., 2023). Fourth, the higher the PMC, the more efficient is the supervision and control system, thus resulting in a more reasonable cash holding level and higher enterprise value (Mousavi Shiri & Eramiyan, 2022). Consequently, an intense PMC enhances enterprise information disclosure, alleviates information asymmetry, and increases the efficiency of the supervision and control system. These, in turn, improve the cash use efficiency and helps enterprises capture future investment opportunities.

The above analysis shows that intense PMC mitigates information asymmetry and helps enterprises reduce financing constraints. This, in turn, induces companies with good governance mechanisms to increase the investment efficiency and alleviate financing constraints. Therefore, Hypothesis 2 is proposed as follows:

H2: Product market competition mitigates the positive correlation between internal corporate governance and cash holdings.

Data and Methods

Sample Construction

The data were collected from A-share Chinese companies listed on the Shanghai and Shenzhen Stock Exchange during 2010 to 2022. The data were sourced from the CSMAR database and analyzed using Stata statistical software. The observation number is 6,849. This does not include ST companies and B- and H-share Chinese listed companies. This is because the trading mechanisms and regulatory requirements for B- and H-shares differ from those for A-shares. For example, the trading rules, settlement methods, and investor groups of B- and H-shares differ from those of A-shares. Therefore, in certain cases, these are not included in the same category. Second, the business demand is concentrated in the A-share market, with less demand for B- and H-shares. In addition, pre-processing steps were conducted, including the removal of outliers and missing-value imputation.

Research Models

Regression Model 1 was constructed to investigate the correlation between internal governance and cash holding levels. Model 2 assessed the impact of PMC on the association between internal governance and cash holdings.

Model 1:

Model 2:

Here, CH denotes corporate cash holdings, and CG denotes internal corporate governance. PMC is measured by (1-Lerner index).

Variable Measure.

Note. The measure of corporate governance level uses principal component analysis to construct comprehensive indicators from the incentive mechanism, supervisory function, ownership structure, and decision-making power. The supervisory function is measured using an internal control instrument. The incentive mechanism is represented by two variables: the variations in the shareholding of senior executives and the relative compensation for management. The ownership structure is expressed by the proportion of institutions in the market and the balance of equity (the balance of the shareholding ratio of the second to the fifth largest shareholder/controlling shareholder). The decision-making power of the general manager is expressed by the integration of the chairman and the general manager. Based on the above six indicators, CG is calculated as a comprehensive index of corporate governance. The maximum number is six, and the minimum is zero. If CG is larger than the mean, it is measured as one. Otherwise, it is measured as zero.

Results of the Empirical Analysis

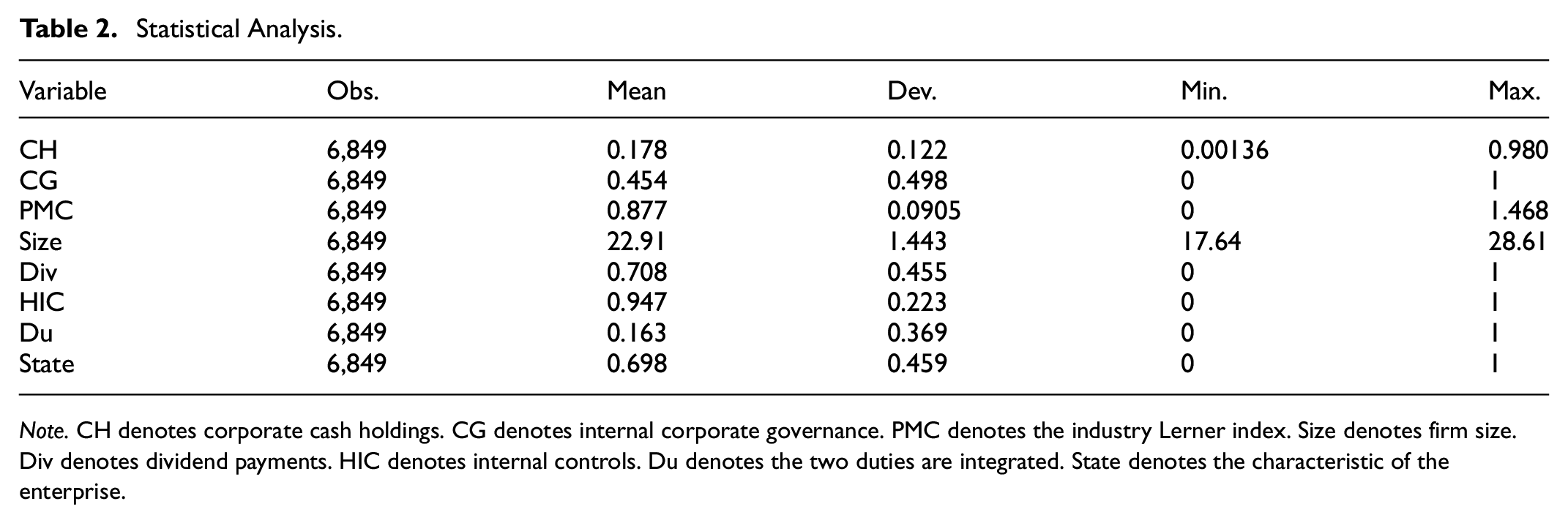

According to Table 2, there are a total of 6,849 observations for the variable. Currently, the mean CH rate is 17.8%. The cash holding levels of different firms vary significantly, with a maximum of 0.98 and minimum of 0.00136. CG is a dummy variable. It adopts a value of one for good governance. Otherwise, it is zero.

Statistical Analysis.

Note. CH denotes corporate cash holdings. CG denotes internal corporate governance. PMC denotes the industry Lerner index. Size denotes firm size. Div denotes dividend payments. HIC denotes internal controls. Du denotes the two duties are integrated. State denotes the characteristic of the enterprise.

Pearson’s correlation was used to assess the association between variables. The correlations between the variables in the sample are presented in Table 3. The primary objective of the Pearson correlation test is to determine whether multicollinearity among the independent variables is an issue. Multicollinearity issues originate if correlation coefficients are higher than .8 (Kim, 2019). However, the correlation coefficients for the variables ranged from −.157 to .109, that is, these did not exceed the upper limit of .8 (Table 3). These observations indicate the absence of multicollinearity issues in the current study.

Correlation Matrix of Pearson.

Note. CH denotes corporate cash holdings. CG denotes internal corporate governance. PMC denotes the industry Lerner index. Size denotes firm size. Div denotes dividend payments. HIC denotes internal controls. Du indicates that the two duties are integrated. State denotes the characteristic of the enterprise.

p < .1. **p < .05. ***p < .01.

Table 4 presents the regression results for internal corporate governance and cash holdings. Columns (1) and (2) display the regression results without the control variables. Meanwhile, columns (3) and (4) display the regression results after the introduction of the control variables. Based on the findings from the Table 4, it is evident that, regardless of controlling for industry and year effects. These observations indicate that internal corporate governance relates positively to cash holdings. This relationship is maintained at both 1% and 5% significance levels. This observation implies that strong internal corporate governance can help enterprises hold more cash. This is because a strong internal governance structure induces managers to prioritize the long-term development of an enterprise over their personal interests (Dawood et al., 2023). In addition, Ling et al. (2024) highlighted that financial constraints significantly hinder the growth of Chinese firms, particularly non-state-owned small- and medium-sized firms. Furthermore, the delayed establishment of China’s financial market, inadequate system development, limited market efficiency, and prevalent information asymmetry have resulted in the financial sector’s incapability to adequately address the financing requirements of private SMEs. This has resulted in what is commonly referred to as the “Macmillan Gap.” Moreover, China’s financial industry exhibits both scale and ownership discrimination. This exacerbates the funding limitations experienced by SMEs and private enterprises (Huo et al., 2024; Serrasqueiro et al., 2021). Therefore, although effective internal governance can mitigate agency problems, enterprises cannot circumvent high financial costs and constraints. Thus, effective internal governance enables companies to increase their cash holdings to protect them against financial constraints and minimize costs.

Regression Test Between Corporate Governance and Cash Holdings.

Note. t-Statistics in parentheses. The explanations of the variables are identical to those in Table 1.

p < .05. ***p < .01.

Table 5 shows a strong correlation between internal corporate governance and cash holdings with a high level of significance at the 1% level. Furthermore, the coefficient of the moderating variable is −0.037, which is significant at the 5% level. This observation indicates that intense market competition mitigates the positive correlation. Additionally, Xian et al. (2023) showed that intense market competition enhances information transparency. This, in turn, alleviates managers’ cognitive bias and reduces the information imbalance between financial institutions and firms. Thus, intense market competition may enhance asset liquidity and alleviate financing constraints. This, in turn, would induce companies with good governance mechanisms to increase the investment efficiency and reduce cash-holding costs. Consequently, intense PMC adversely affected the previously observed positive correlation between internal governance and cash holdings. Moreover, the rigorous test that substituted the moderator variable from the Lerner Index to HHI yielded outcomes identical to those of the base regression. This observation supported Hypothesis 2.

Interaction Effect of Product Market Competition on the Relationship Between Corporate Governance and Cash Holding.

Note. t-Statistics in parentheses. The explanations of the variables are identical to those in Table 1.

p < .05. ***p < .01.

Robust Test

For the robustness test, we modified the corporate governance variable to internal controls to verify Hypotheses 1 and 2.

HIC is an internal control index measured as a variable of internal corporate governance. According to Yang and Wang (2020), H. Chen et al. (2017), and H. Chen, Yang, et al. (2020) measures of internal control index, the model is measured as follows. In Model 1, W represents the weight of each index for the internal controls of listed companies, Strategy represents the strategic index, Operation represents the operational index, Reporting represents the reporting index, Compliance represents the compliance index, Asset safety represents the asset security index, and Correction represents the correction index. When the internal control index exceeds the median value of the sample year, the HIC adopts the value one. When it does not, the HIC adopts the value zero.

In Table 6, the regression coefficient for HIC and CH is .018 and is significantly positive at the 1% level. This outcome indicates that a one-unit increase in HIC corresponds to a .018 unit increase in cash holdings. From an economic perspective, each standard deviation increase in HIC (0.223) causes an increase in CH equal to 0.032 of the sample standard deviation (calculated as 0.018 × 0.223 / 0.122). Therefore, Hypothesis 1 is supported by the observations. This can be explained as follows: First, effective internal controls can reduce the various risks confronted by enterprises, including operational and financial risks. When an enterprise has effective internal controls, managers hold more cash because they consider that they can effectively manage and control the risks associated with cash. Second, companies with good internal controls can rapidly identify and capitalize on investment opportunities. Holding sufficient cash enables businesses to capture these opportunities. This potentially increases competition in the market. Moreover, adequate internal controls can enhance the confidence of investors, creditors, and other stakeholders in the financial strength of an enterprise. The company can hold more cash to demonstrate its financial strength, which can effectively respond to the risk of predation from competitors. As a result, a company with high-quality internal controls holds more cash to defend against external plunder risk, rather than reducing its cash holding level to alleviate agency issues. This is because severe financial constraints and economic uncertainty limit the development of enterprises, particularly SMEs (Luo et al., 2018; Mittal & Raman, 2021; Singh & Kaur, 2021). Furthermore, Table 4 illustrates that Size and State exhibit negative coefficients on cash holdings at the 1% significance level. This observation indicates that larger in-state businesses tend to maintain lower cash reserves than smaller ones do. Moreover, high cash holdings reduce a firm’s prospects for growth. Conversely, Div shows a positive correlation with cash holdings at the 1% significance level. To summarize, the regression analyses using HIC and CH corroborated Hypothesis 1. This is evidenced by the positive and significant coefficients of OC.

Regression Test Between Internal Control and Cash Holding.

Note. t-Statistics in parentheses. All the variables are described in Table 1.

p < .1. ***p < .01.

Moreover, the regression results show that PMC*HIC is negatively associated with cash holdings and is significant at the 10% level. A negative relationship implies that market concentration mitigates the positive relationship between HIC and cash holdings. This, in turn, indicates that intense market competition promotes the above-mentioned positive correlation (Bo et al., 2024; Xian et al., 2023). These observations indicate that companies with robust internal controls are more likely to maintain higher cash reserves to safeguard against the risk of being plundered by competitors and intense market competition. Thus, these support Hypothesis 2.

Endogeneity Problem

Strong corporate governance ensures that management does not misappropriate cash resources and prevents overinvestment and agency problems. Simultaneously, higher cash holdings enable management to be more flexible when confronted with emergencies and to respond to various challenges without affecting daily operations. Therefore, more attention should be paid to robustness tests to address potential issues such as endogeneity, particularly reverse causality and measurement errors.

The endogeneity problem can be solved using a two-step system GMM. The problem may affect the accuracy of the empirical results. According to Table 7, the GMM results include the difference (Hnull = exogenous). The results show that the number is larger than .1. This implies that the two-step system GMM regression is the best method.

The Regression for GMM.

Note. z-statistics in parentheses. The explanations for the variables are identical to those in Table 1.

p < .1. **p < .05. ***p < .01.

Table 7 uses GMM alleviates the endogenous problem and reveals a positive relationship between CG and CH at the 10% level. This is indicated by the coefficient of 0.025 in the GMM regression. In addition, CG × PMC indicates a negative relationship at the 5% level, and the coefficient is −0.371. This implies that the high level of market competition can mitigate cash holdings by well-governed corporates. According to the analysis in Table 4, the negative association also illustrates that intense PMC can promote the positive relationship for the above two variables. The result is consistent with base regression.

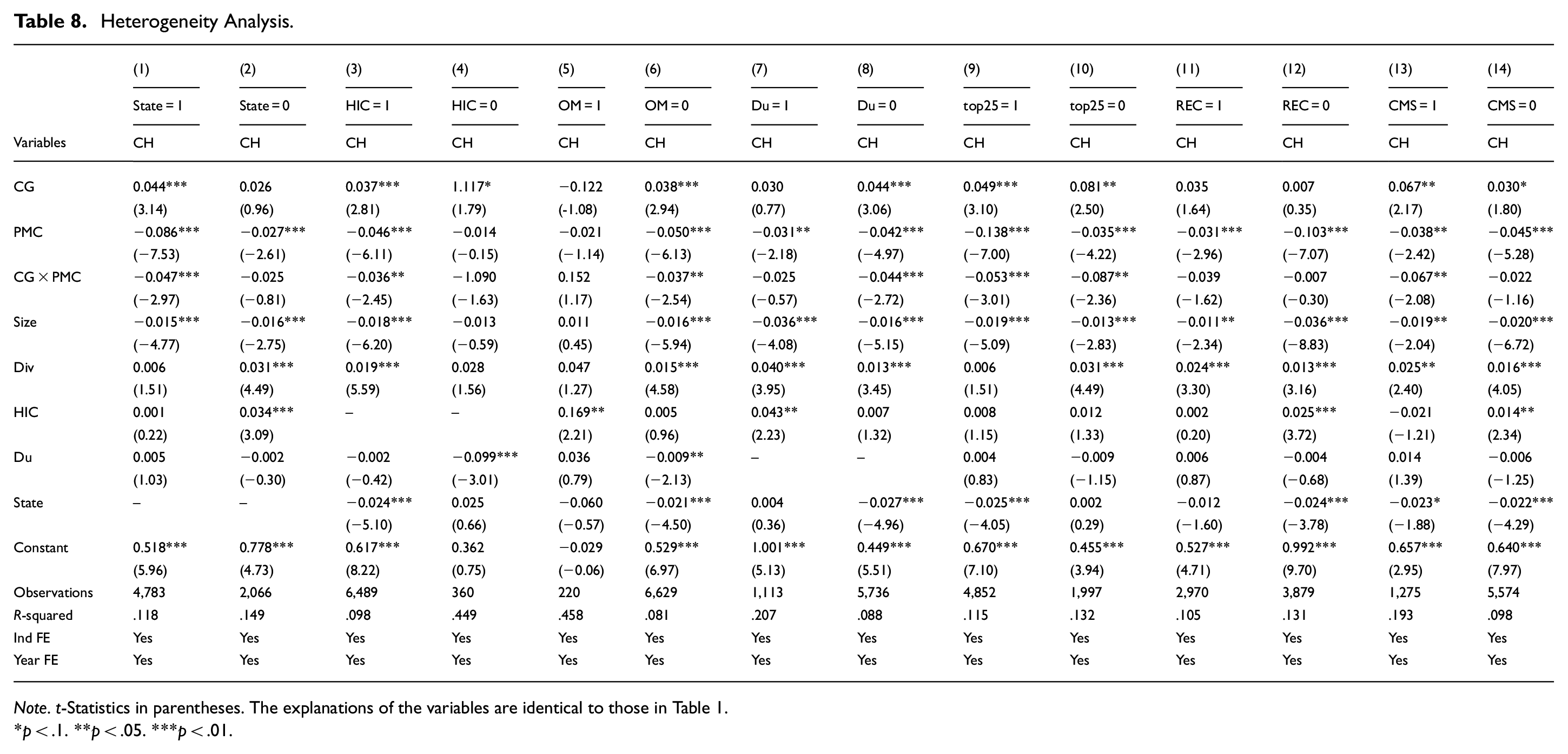

Heterogeneity Analysis

To verify the regression results, we conducted a heterogeneity analysis by dividing each factor of internal corporate governance by the characteristic of the enterprise. Table 8 presents the results for the characteristic of enterprises and each element of internal corporate governance.

Heterogeneity Analysis.

Note. t-Statistics in parentheses. The explanations of the variables are identical to those in Table 1.

p < .1. **p < .05. ***p < .01.

Columns (1) and (2) present the heterogeneity analysis of firm characteristics. The results indicate that state-owned companies (State = 1) are influenced considerably by intense rivalries in the product market. The coefficient is −0.047, which is statistically significant at the 1% level. This is because the government supports state-owned firms, which provides them higher credibility and access to more extensive financing options (Bai et al., 2021). C. Li et al. (2023) highlighted that financial constraints significantly hinder the growth of Chinese firms, particularly state-owned small- and medium-sized firms. Furthermore, the delayed establishment of the Chinese financial market, inadequate system development, limited market efficiency, and prevalent information asymmetry have resulted in the financial sector’s incapability to adequately address the financing requirements of its state-owned small- and medium-sized firms. This has resulted in what is commonly referred to as the “Macmillan Gap.” Therefore, state-owned companies spend more money on investments and plunder market share because they have fewer financing constraints than other companies. This enables state-owned enterprises to invest more in projects aimed at improving their market share rather than stockpiling cash for defending against competitors. These circumstances present favorable prospects for state-owned firms to leverage these advantages and enhance the cultivation of their core competitiveness, thus facilitating their sustained and stable growth. However, non-state-owned firms cannot access equivalent credit assistance and confront considerable financing limitations. Consequently, non-state-owned enterprises emphasize risk management and the potential threats posed by dominant competitors. This results in insignificant results.

Internal controls play a crucial role in ensuring effective internal corporate governance. Implementing strong internal control measures can effectively address the agency problems within enterprises. An increase in PMC induces companies to invest more efficiently in projects in a high-information-transparency market rather than holding excess cash to mitigate future risks.

Columns (5) to (10) display the regression outcomes of equity concentration (OM) and top2-5 (the balance of the shareholding ratio of the second to fifth-largest shareholder/controlling shareholder). These results illustrate that a larger proportion of equity does not support the promotion of effective corporate governance. This is because having an excessive amount of equity concentrated in a single group can result in an imbalance of power. This potentially results in cognitive bias and agency problems. Enterprises with strong power checks-and-balances can prevent the concentration of power with a single individual or small group. This has promoted the successful implementation of corporate governance. When PMC improves, enterprises can better use cash resources under highly transparent conditions. This helps reduce financing constraints, improve cash efficiency, and ultimately promote enterprise development. Furthermore, integrating the two duties (Du) yields identical outcomes as mentioned earlier. This indicates that an excessive concentration of power hinders the advancement of effective corporate governance. Additionally, intense competition in the product market enhances information transparency, thereby resulting in increased investment efficiency and reduced financing constraints.

Columns (13) and (14) display the regression outcomes of variations in managers’ shareholdings (CMS). These show a positive and significant correlation with corporate governance. This indicates that strong corporate governance coupled with well-designed incentive policies enhances managers’ confidence in a company’s growth and promotes optimism for the future. Managers demonstrate their opinions regarding company growth by increasing their ownership and actively engaging with shareholders. This helps address any potential conflicts of interest and enhances the effective utilization of funds. Managers can optimize their cash resources in competitive markets because of the increased information transparency. This can alleviate financing constraints, enhance cash utilization efficiency, and drive enterprise development.

Considering the intensifying competition in the product market, companies with high-quality internal corporate governance can maintain cash reserves within a reasonable range to manage future uncertain risks. During this process, corporate executives should place a higher emphasis on the balance between investment and cash reserves to ensure that organizations can rapidly address risks. Enterprises can strengthen the relationship of trust between shareholders and management and incentivize managers to contribute to the long-term development of the company by connecting internal and external governance mechanisms.

Conclusions and Implication

This study examined whether corporate governance and cash holdings are positively correlated in China. Our empirical results support this hypothesis. Furthermore, intense market competition can mitigate the correlation between high-quality internal governance and cash holdings. Additionally, the results of the robustness test aligned with those of the base regression. To summarize, firms with high-quality internal governance have higher cash holdings to defend against financial constraints. However, intense market competition can alleviate this positive correlation by improving the cash use efficiency. This is because product market competition can efficiently enhance information transparency. Consequently, enterprises should utilize this external mechanism and connect it with internal governance mechanisms to reduce the financing costs and alleviate asymmetric information between financial institutions and firms.

To ensure optimal decision making, it is essential to establish cash holdings that are both reasonable and effective. When making cash holding decisions, a company should consider both its governance level and market competition. Additionally, this strategy enables the enterprise to fully utilize its reserve resources for future enterprise costs while retaining a certain amount of inherent funds to address its daily cash requirements. The implications of this study are as follows:

Optimize Corporate Governance Structure

a. Establishing an effective board of directors: First, companies need clarity of responsibilities. To ensure that board members can perform their duties efficiently, companies should clearly define the scope of each member’s responsibilities, particularly in supervising the company’s financial management and strategic decision-making. This helps increase transparency and efficiency in decision-making and ensures that board members can perform their duties and collaborate to drive the company toward its stated goals. The second is independence. The presence of independent directors on the board of directors is crucial. They can provide unbiased opinions and supervision, which plays an irreplaceable role in preventing internal conflicts of interest, protecting shareholder rights, and safeguarding the overall interests of the company. The perspective of independent directors can help companies better identify potential risks and make more objective decisions.

b. Improved internal control system: Transparency and auditing mechanisms are the most important factors. Establishing a transparent financial reporting system is crucial in the current era of highly transparent information. Companies need to ensure timely and accurate disclosure of all financial information. This helps increase investor and public confidence in the company’s operations and promotes integrity and responsibility within the company. Establishing an independent internal audit department is a critical step in ensuring the financial health of a company. This department is responsible for regularly reviewing the company’s financial status and effectiveness of the internal control system, and rapidly identifying and correcting potential problems. Thereby, it provides a strongly supports for the company’s stable operations.

Establish a Clear Governance Framework and Formulate Clear Governance Policies and Procedures

It is essential to establish a clear governance framework to ensure the efficiency and orderliness of organizational operations. This includes formulating clear governance policies and procedures to guide the daily operations and long-term development of the organization. (1) Clarify responsibilities: It is necessary to define the scope of responsibilities of each senior executive and (by clearly dividing the responsibilities) ensure that everyone clearly understands their responsibilities. This would help improve work efficiency and reduce the overlap or omission of responsibilities. (2) Establish rules: It is essential to develop a clear decision-making process and approval procedure. This would help ensure the transparency and impartiality of organizational decision-making while also enhancing the trust of stakeholders in the organization. Second, strengthening leadership development and executive training and development: In an organization, leadership is a key factor in driving transformation and achieving goals. Therefore, strengthening leadership development and executive training and development are crucial for the long-term development of an organization. (1) Leadership training: Organizations should regularly provide leadership training courses for executives through which they can improve their strategic thinking and decision-making capabilities. This would help them better address current challenges and prepare for future opportunities. (2) Cross-departmental communication: Promoting cross-departmental communication among executives is an effective means for enhancing teamwork awareness. Through cross-departmental communication and collaboration, executives can better understand the work processes and challenges of different departments. This promotes more effective decision making and problem solving.

Although this study displays a certain research value, it is based on Chinese listed companies as the investigation object. The research conclusions may not be applicable to public companies in other countries. This is because China has a different social and cultural system. Conventional Confucian culture has also influenced Chinese businesses. These cognitive deviations make it challenging to ensure that governance mechanisms are implemented fully in the corporate governance experiences of other countries. Therefore, public companies in other countries should effectively connect with their native cultures and social environments to implement the related recommendations.

Footnotes

Author’s Note

The results presented in this manuscript have not been considered for publication elsewhere. None of the manuscript’s contents have been previously published or posted on the internet.

Ethics Considerations

This paper does not involve the ethics of animal and human research.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

Data will be made available on request.