Abstract

The ultimate objective of this study is to shed light on the factors that affect the profitability of firms operating in the manufacturing industry. Using 10,125 observations of 225 manufacturing firms listed on Borsa İstanbul, the author performed regression analysis to identify profitability determinants. Internal factors such as firm size, leverage, the ratio of intangible assets to total assets, the current ratio and the asset turnover ratio are identified as important determinants of sample firms’ ability to generate consistent profits. In contrast, macroeconomic conditions, including inflation and interest rates, do not exhibit statistically significant effects. The robustness checks validate the empirical results. The findings of this study offer several key benefits, both in terms of practical applications and theoretical contributions. By identifying the factors that drive profitability, firm management can make more informed strategic decisions, investors could determine whether a stock is undervalued or overvalued in the stock market, and banks and other creditors can project their future cash inflows by examining the association between financial ratios and profitability.

Keywords

Introduction

In a global economic environment, the main objective of firms is to maximize shareholder wealth. This objective can be achieved by maintaining a steady and continuous growth in profits. Sustainable profitability plays a significant role in enhancing firm value. Firm management is expected to employ well-established policies that contribute to sustainable profitability.

The COVID-19 pandemic, Russian-Ukrainian war, and global inflation waves have significantly adversely affected firms’ profitability over the past 5 years. Despite significant efforts, the profit margins of manufacturing firms have continued to decline and exhibit no recovery over the past 5 years. Many factors can affect the profitability of manufacturing firms. Some of these are exogenous factors that firms struggle to control. The management of firms should consider these factors when making medium and long-term profit projections. In the competitive economic environment, managers of manufacturing firms are expected to eliminate product and operational lines that mitigate overall profitability.

Managers, creditors, investors, and suppliers pay close attention to profitability, which is one of the important factors influencing a firm’s viability. The profitability level of a firm enables decision-makers to compare among firms operating in the same sector or between different industries (Donthu & Gustafsson, 2020). A high-level of competitiveness in the manufacturing industry exerts pressure on firm management to conduct operations that considerably enhance profitability.

The manufacturing industry contributes substantially to the country’s economy by generating employment opportunities and fostering economic growth through its extensive supply chain. Over the last decade, the manufacturing industry has experienced significant changes and regulations. Technological innovations and rapid globalization of the economy continue to create opportunities and challenges for the management of manufacturing firms to maintain sustainable profitability. In this study, the manufacturing industry was chosen because it is the fastest growing and one of the most important strategic industries.

Several studies (discussed in the next section) have provided mixed evidence. Some studies have noted that market structure, firm management, and human resources may affect the profitability of manufacturing firms. On the other hand, some studies claim that macroeconomic parameters such as purchasing power parity, inflation rate, interest rate, and unemployment rate have a much greater impact on profit levels. There is an inconclusive debate about the determinants of profitability; therefore, it is important to empirically scrutinize the factors affecting the profitability of manufacturing firms, particularly for developing markets.

Many theories have been employed to investigate the determinants of profitability, such as resource-based theory (Riahi-Belkaoui, 2003; Sharma et al., 2019;); trade-off theory (Ahmed et al., 2023; Oino & Ukaegbu, 2015); managerial theory (Brauer, 2013; Goddard et al., 2005); agency cost theory (Mitra & Naik, 2021; Pandey & Sahu, 2019); and pecking order theory (Bhutta & Hasan, 2013; Tong & Green, 2005). This study uses resource-based theory and agency cost theory to examine the association between the criterion variable and predictor variables.

Resource-based theory posits that firms achieve superior financial performance by developing valuable and inimitable economic resources. Manufacturing firms with strong operational capabilities, technological assets, and intangible resources such as brand equity, copyrights, patents, licenses, a skilled workforce, and trademarks can effectively differentiate themselves in a competitive business environment.

Agency cost theory suggests that conflicts of interest between firm managers and owners may lead to operational inefficiencies and additional expenses, known as agency costs (Jensen & Meckling, 1976). These costs often diminish profitability by causing misallocation of economic resources or raising the costs of monitoring activities.

While the existence of valuable internal assets lays the foundation for competitive advantage and high profitability, their effective use depends heavily on the quality of a firm’s governance. From a theoretical perspective, resource-based theory clarifies the “what”—the importance of firm-specific resources—whereas agency cost theory emphasizes the “how”—the governance mechanisms required to ensure these assets are effectively used. Without this synergy, firms may fail to fully leverage their strategic and valuable assets to generate earnings.

The Turkish economy is an important developing economy with unique institutional features. Between 2019 and 2023, many firms located in Türkiye attempted to cope with the financial distress resulting from COVID-19 and high inflation rates. The Turkish economy heavily depends on energy imports, especially oil and natural gas, with a significant portion coming from Russia. The Ukraine-Russia war has disrupted supply chains and caused a spike in energy prices, significantly increasing energy costs for Turkish firms and placing pressure on the profits of companies that are highly dependent on energy-intensive manufacturing processes, such as those in other sectors. During this period, reduced demand and supply chain disruptions led to bankruptcy of many firms in different industries. Firms that invested in technological capabilities and effectively navigated the uncertainties achieved strong profitability.

Turkish economy, one of the important emerging economies, deserves standalone attention. A paper that explores the profitability determinants of Turkish manufacturing firms is critically important for other emerging markets for several reasons. First of all, Turkish economy, like many emerging economies, suffers from high inflation, exchange rate volatility, and limited access to foreign capital. These are common structural and macroeconomic challenges that also influence firms in other emerging markets (e.g., Indonesia, Brazil, South Africa, and Malaysia). Analyzing how Turkish firms navigate these challenges can yield valuable insights into firm behavior and resilience in other emerging market contexts. Secondly, most firm-level profitability studies are dominated by evidence from developed countries. The findings from this research do not just clarify local dynamics but also enrich global understanding of how manufacturing firms operate under macroeconomic volatility.

The main objective of this study is to scrutinize the factors affecting the financial performance of manufacturing firms located in Türkiye from 2019 to 2023. First, to the best of my knowledge, there is no other study which specifically concentrates on manufacturing industry in Türkiye. Previous studies focused on different countries and industries such as agriculture, financial, and service. Second, it contributes to the literature by designing an empirical model that enables the management of manufacturing firms to assess the relative position of their financial performance within the sector. Thirdly, this study aims to explore profitability determinants for manufacturing firms listed on Borsa İstanbul, using financial statement data and macroeconomic variables and employing panel data estimation models instead of cross sectional analysis. Lastly, this study offers concrete recommendations for managers of manufacturing firms based on the empirical findings, suggesting strategic steps that could help enhance financial performance in uncertain economic conditions. There is a need to reinvestigate profitability determinants due to rapid changes in the global economy.

The remainder of this paper is organized as follows. The second section presents a literature review and research hypotheses. Third section shows the research design and data. Fourth section puts forward the empirical analysis results. The final section provides recommendations for future studies and concludes the paper.

Literature Review and Hypothesis Development

This section presents previous studies and hypotheses.

Firm Size and Profitability

In a rapidly changing economic environment, firm size is a prominent factor that can influence many aspects of a firm’s operations, including profitability (Alarussi & Gao, 2023). An expanding body of literature is dedicated to investigating the relationship between firm size and profitability. Chen et al. (2024) analyzed the profitability determinants of UK audit firms and concluded that larger firms are more cost-effective and report higher profits than smaller ones. Luhnen (2009) and Karbhari et al. (2018) purported that large-sized firms are expected to report higher levels of profit owing to economies of scale, which enables them to spread fixed costs over a wider range of products. Such firms have better access to a wider range of external financing sources. Considering the organizational structures of manufacturing firms, they are more likely to benefit from economies of scale. However, other studies suggest a negative association between size and profitability. Alhassan and Biekpe (2016) and Fama and Jensen (1983) claim that firm size negatively impacts profitability because large-sized firms can experience agency conflicts and coordination problems. Thus, I propose the following hypothesis:

Leverage and Profitability

Debt financing is an important source of financing for manufacturing firms. Similar to capital markets in other developing economies, the efficiency of capital markets in Türkiye, characterized by a high level of information asymmetry, is not at the desired level. Manufacturing firms in Türkiye rely more on short-term debts. This is a vital factor that differentiates the balance sheet structures of manufacturing firms in Türkiye from those in developing economies. Based on trade-off theory, firms can bolster their profit margins by utilizing debt financing, since interest paid is tax deductible (Modigliani & Miller, 1963). On the other hand, agency theory states that firms that rely more on debt-financing are more likely to experience significant agency costs because of conflicts that emerge between creditors and shareholders, which negatively influence profitability (Myers, 1984). In this context, some previous studies (Alarussi & Gao, 2023; Aryantini & Jumono, 2021; Calcagnini et al., 2022; Eljelly, 2004; Zeitun & Tian, 2007) find that interest expenses exert pressure on firms’ profitability. Sany et al. (2023) suggested that leverage negatively affects the profitability of manufacturing firms in Indonesia when it surpasses the optimal threshold. In contrast, some studies (Boadi et al., 2013; Detthamrong et al., 2017; Margaritis & Psillaki, 2007; Ruland & Zhou, 2005; Zaid et al., 2014) show a positive relationship between profitability and leverage. Additionally, Worku et al. (2024) found that the leverage ratio had a positive effect on the profitability of insurance firms operating in Ethiopia during the period 2011 and 2020. Based on prior studies, the following hypothesis is proposed.

Intangible Assets and Profitability

In today’s economic environment, intangible assets, one of the strategic assets, play a vital role in augmenting profitability, thereby yielding substantial economic advantages for firms. Generally, manufacturing companies have a significant proportion of intangible assets among their total assets. Information technology and product innovations that emerge as a result of R&D activities are critically important for manufacturing firms to maintain their competitive advantage and mitigate financial risks (Santosa, 2020). Understanding the complex relationship between intangible assets and financial performance is paramount for manufacturing firms seeking to thrive in the global marketplace. Prior studies suggest a positive relationship between profitability and intangible assets (Appelbaum et al., 2017; Chen et al., 2005; Clarke et al., 2011; Haji & Mohd Ghazali, 2018). Kothari et al. (2002) claim that firms’ future earnings soar when they increase their spending on R&D. Based on these arguments, the following hypothesis is proposed.

Liquidity and Profitability

Liquidity ratios allow us to thoroughly assess a firm’s capacity to settle short-term obligations. Liquidity management is critically important for manufacturing firms because poor management of liquid assets can lead to serious financial problems, even bankruptcy. Hossain & Alam (2019) state that liquidity and profitability management are important issues to which firm management should pay close attention. Some studies reveal that firms with a high liquidity ratio are more likely to report higher profitability (Ehiedu, 2014; Lim & Rokhim, 2020; Nanda & Panda, 2018; Pant et al, 2024; Samo & Murad, 2019). Churchill & Mullins (2001) and Nastiti et al. (2019) claimed that high liquidity ratios contribute to sustainable profitability in a rapidly changing economic environment. On the other hand,Owolabi et al. (2011), Mohanty and Mehrotra (2018), Eljelly (2004), and Jose et al. (1996) find a negative association between liquidity measures and profitability. Gitman (2003) clarified this relationship as follows; the management of firms can face the dilemma of holding highly liquid assets instead of directly employing them to enhance firm value. Therefore, this dilemma can suppress profitability. Maintaining high liquidity usually involves holding low-earnings liquid assets, which can suppress profitability. In this context, I propose the following hypothesis.

Firm Efficiency and Profitability

Efficiency ratios provide important insights into the ability of a company’s assets to generate earnings in the short term (Alarussi & Gao, 2023). In this study, the asset turnover ratio was chosen to evaluate firm efficiency. Some studies (Denčić-Mihajlov, 2014; Gaio & Henriques, 2018; Okwo et al., 2012; Salman & Yazdanfar, 2012) provide evidence that firms that effectively utilize assets are more likely to report higher earnings. However, Cipta et al. (2020), Keramidou et al. (2013), Kumar and Gulati (2009), and Pratama et al. (2021) analyzed the association between firm efficiency and profitability by employing a multivariate model and found no strong relationship between firm efficiency and profitability. A similar result was obtained by Wulandari and Lubis (2021), who suggest that firms with high operating efficiency are not always capable of reporting high profits. In this context, I propose the following hypothesis.

Macroeconomic Determinants and Profitability

In the current business climate, macroeconomic determinants serve as core contributors that significantly influence firms’ profitability. Broyles et al. (1983), Kanwal and Nadeem (2013), Charles (2012), and Egbunike and Okerekeoti (2018) claimed that inflation can negatively influence the firms’ profitability because it mitigates the purchasing power of consumers and soars the financing costs. It is noteworthy that inflation is assumed to be one of the factors that distorts firms’ balance sheet structures. Even though high interest rates can help decrease the inflation rate, they can also slow economic activities. Firms are more likely to experience little sales growth in a sluggish economy. Rao (2016), Gado (2015), and Osamwonyi and Michael (2014) find that interest rates have a negative impact on firm profitability. Based on these arguments, the following hypotheses are established.

Research Design and Data

This section presents the research design and data. This study employs secondary data manually extracted from the financial statements of 225 manufacturing firms whose stocks are traded on Borsa Istanbul between 2019 and 2023. Initially, 240 firms were obtained with 10,800 observations. After eliminating firms with extreme, insufficient, and missing data, 10,125 observations are utilized in this study to investigate the impact of factors (firm size, leverage, liquidity, firm efficiency, intangible assets, inflation, and interest rate) on profitability measured by return on equity.

Model Specification

The present study employed pooled OLS regression, fixed-effects regression, and random-effects regression models for data analysis. In this study, research hypotheses are tested by using the fixed-effects regression models. There are some advantages to using a fixed-effects regression model. First of all, fixed-effects regression model enables us to control of time-invariant variables (Collischon & Eberl, 2020). Secondly, this method considerably decreases omitted variable bias (Breuer & deHaan, 2024; Rüttenauer & Ludwig, 2023). Thirdly, this method allows for the forecasting of individual-specific effects (Brooks, 2019). In the present study, there is a limited period (2019–2023) that makes it less exposed to the autocorrelation problem (Simon, 2015). Hence, autocorrelation was not tested in this study. The following empirical models are used to examine the factors that can affect profitability.

In which, β0, β1, β2, β3, β4, β5, β6, and β7 are coefficients. ROE, a financial performance indicator, is the return on equity measured by the ratio of net income to stockholders’ equity; ROA, a financial performance indicator, is the return on assets measured by the ratio of net income to total assets; SIZE is firm size measured by the natural logarithm of the sample firm’s total assets; LEV is financial leverage measured by the ratio of total debts to total assets; INTTA is the ratio of intangible assets to total assets; CR is the current ratio measured by the ratio of current assets to current liabilities; and ATO is the asset turnover ratio measured by the ratio of total net sales revenue to average total assets. INF is the annual inflation rate measured by the consumer price index. IR is the weighted average interest rate for bank loans. ε is the error term.

The Results of Empirical Analysis

Descriptive Statistics

Table 1 presents the descriptive statistics for the sample firms. All empirical variables are winsorized at the 1st and 99th percentiles to mitigate the impact of outliers. The mean of ROE is 0.206, ranging from −2.262 to 30.009. The mean of ROA is 0.165, whereas the minimum value is negative, indicating a loss. The mean of SIZE is 9.074. The mean of LEV is 0.498, indicating that the sample firms used in this study intensively use debt to finance their operations. Between 2019 and 2023, the inflation rate in Türkiye persisted at elevated levels compared to other emerging economies, with a mean inflation rate of 39.536%. The interest rate in Türkiye fluctuated between 10.6% and 28%. High interest rates exerted downward pressure on the earnings figures of the sample firms operating in Türkiye. The mean value of INTTA is 0.029, indicating that the ratio of intangible assets to total assets did not reach the desired level when compared to the firms operating in developed economies. Manufacturing firms with a low ratio of intangible assets may struggle to differentiate themselves from their competitors, leading to a low market share and profitability. To gain a sustainable competitive advantage, the sample firms must prioritize the significance of intangible assets. The mean of CR and ATO values are 1.872 and 1.013, respectively.

Descriptive Statistics.

Note. The variable definitions are presented in model specification.

Correlation Coefficients

Table 2 displays the correlation coefficients between the independent and dependent variables. Leverage, inflation rate, and interest rate are negatively and significantly correlated with return on equity and return on assets, while size and the ratio of intangible assets to total assets show a positive and significant correlation with return on equity and return on assets. Alarussi and Gao (2023) and Nguyen and Nguyen (2020) obtained similar results. If the correlation between two variables is higher than 0.70 in absolute value, it indicates multicollinearity between the variables. As shown in Table 2, no correlation coefficient was greater than 0.70.

Correlation Coefficients.

Note. *, **, and *** denote significant in less than 0.10, 0.05, and 0.01, respectively. The variable definitions are presented in model specification.

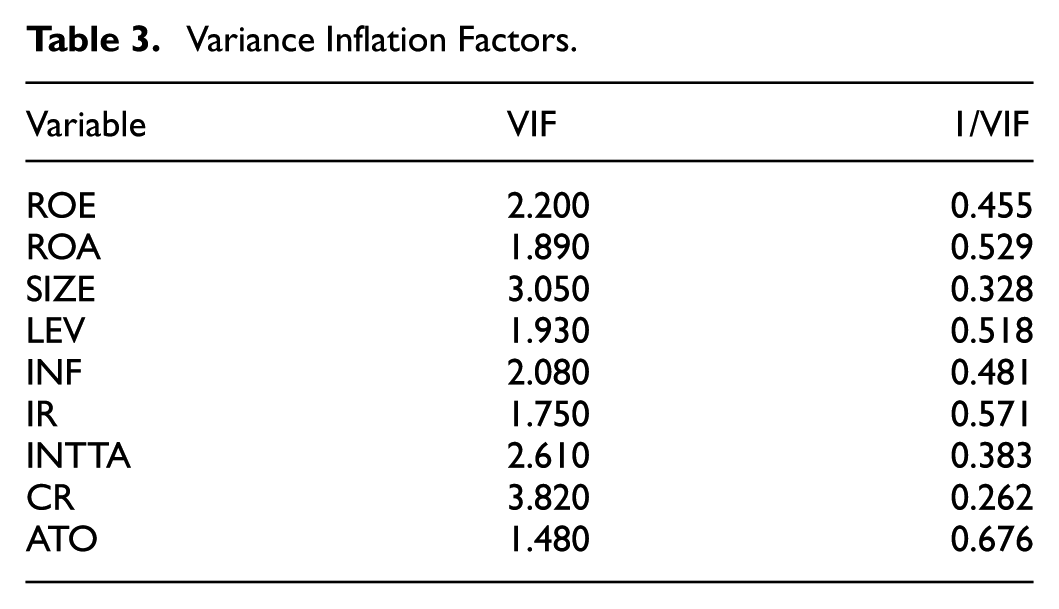

Table 3 reports the variance inflation factors (VIFs) for the variables used in the empirical model. The VIF is a useful tool for detecting multicollinearity. A VIF value greater than ten may indicate potential multicollinearity problems (Yan & Su, 2009). As shown in Table 3, none of the VIF values exceeds ten, suggesting that multicollinearity is not a concern in the model.

Variance Inflation Factors.

Regression Results

Tables 4 and 5 highlight the results of the pooled OLS regression, fixed effects regression, and random effects regression analysis. The F-test and LM test were used to decide between panel data models and pooled regression model. The results of F-test and LM test indicate that panel data models are preferred to pooled regression model. Next, Hausman test is performed to decide whether random effects model or fixed effects model should be employed. The Hausman test result suggests that the null hypothesis is rejected and that the fixed effects model should be used in both estimation models. 35.3% of variation in return on equity and 38.5% variation in return on assets is explained by independent variables. According to Kyereboah-Coleman (2007), individual heterogeneity should be controlled for prior to proceeding further to the empirical analysis. According to the results of the Breusch-Pagan test, the empirical models exhibit no signs of heteroscedasticity.

The Results of Regression.

Note. ** and *** denote significant in less than 0.05 and 0.01, respectively. The variable definitions are presented in model specification.

The Results of Regression.

Note. *** denotes significant in less than 0.01. The variable definitions are presented in model specification.

The results of the study support hypothesis 1, suggesting that firm size has a statistically significant and positive impact on profitability; therefore, large-sized firms tend to report higher profits. For each one-unit increase in firm size, profitability increases by 9.717 units, holding all other variables constant. This evidence supports the findings of Asimakopoulos et al. (2009), Sritharan (2015), and Ahinful et al. (2021). One plausible explanation for this result is that large-sized manufacturing firms possess strong market power and benefit from economies of scale, which considerably enhance corporate earnings.

As expected, the coefficient of leverage turns out to be statistically significant and negative, and Hypothesis 2 is accepted. A one-unit increase in financial leverage reduces firm profitability by −1.486 units, indicating a negative relationship. This finding implies that interest expenses on debt suppress sample firms’ profitability. It is worth mentioning that high leverage significantly heightens the likelihood of financial distress, which can cause firms to encounter higher interest rates on new borrowings and refinancing of existing debt obligations. This result is in line with those of Singhania et al. (2024), Calcagnini et al. (2022), and Eljelly (2004).

The finding that inflation and interest rates had no statistically significant impact on firm profitability during the volatile 2019 to 2023 period in Türkiye is surprising, but it can be explained in several ways. Sample firms may have employed adaptive strategies—such as dynamic pricing, effective cost management, and hedging against currency and interest rate risks—that insulated profitability from macroeconomic volatility. According to resource-based theory, firm-specific capabilities such as strong supplier/customer relationships or financial flexibility can buffer firms against external shocks. In a high-inflation and high-interest-rate economic environment, the sample firms may have passed cost increases on to consumers and benefited from state support, export and tax incentives, or FX-based contracts. Given that the sample firms have been operating within an economic environment characterized by persistently high inflation and interest rates for an extended period, sample firms may have possessed the capability to swiftly adapt to fluctuations in these economic indicators. Even though the coefficients of the inflation rate and interest rate are not statistically significant, these variables are incorporated into the empirical model to enhance robustness.

The results revealed that the ratio of intangible assets to total assets had a positive significant impact on return on equity; therefore Hypothesis 3 is accepted. Similar results were found by Lantz and Sahut (2005), Alarussi and Gao (2023), and Zhang (2017), who find that intangible assets significantly contribute to enhancing profitability. When utilized effectively, intangible assets can considerably enhance the profitability of firms during economic downturns (Gschwandtner & Cuaresma, 2013; Winter, 2003).

This study indicates that the current ratio has a coefficient of 0.981, with a return on equity at a significance level of 1%. A one-unit increase in the current ratio improves profitability by approximately 0.981 units, indicating that better liquidity management is positively linked to firm performance. Hence, Hypothesis 4 is accepted. This implies that a high degree of liquidity enables sample firms to evaluate potential investment opportunities that can boost profitability. Effective liquidity management is a key prerequisite for enhancing profitability and ensuring successful business operations in uncertain economic climates.

The asset turnover ratio was employed to measure the operational efficiency of the sample firms. The result suggests a significant and positive association between the asset turnover ratio and profitability of manufacturing firms operating in Türkiye. Therefore, H5 is supported. This result indicates that the sample firms demonstrated the effective utilization of their assets in generating earnings. This finding corroborates Salman and Yazdanfar (2012), Okwo et al. (2012), Denčić-Mihajlov (2014), andChander and Aggarwal (2008), who state that a high asset turnover ratio leads to higher profitability.

Robustness Check

To ensure the robustness of the empirical findings and address potential endogeneity concerns, a first-difference transformation of the model was used. In the transformed model, the change in earnings per share (ΔEPS) is used as the dependent variable. Endogeneity represents a significant methodological challenge in management and business research. Endogeneity occurs when an explanatory variable in a regression model is correlated with the error term, leading to biased and inconsistent estimates. The First-Difference method enables us to eliminate time-invariant unobserved heterogeneity, a potential source of endogeneity (Lee et al., 2012; Ryu & Kang, 2013). Table 6 presents the results of first- difference regression analysis. The first-difference estimation results support the baseline findings, suggesting that the main conclusions about the profitability determinants of the sample firms are robust to endogeneity concerns.

First-Difference Regression.

Note. *** denotes significant in less than 0.01. The variable definitions are presented in model specification.

Concluding Remarks

This paper aims to address the gap in the existing literature on the determinants of profitability of manufacturing firms operating in Türkiye. Using a sample of 225 manufacturing firms located in Türkiye, this study provides the latest evidence on the factors influencing the profitability of sample firms. Additionally, the potential impacts of macroeconomic environment on profitability are scrutinized.

Between 2019 and 2023, manufacturing firms located in Türkiye encountered economic instability characterized by fluctuations in currency exchange rates and inflation, which exert notable impacts on production costs, pricing strategies, and overall financial performance. The manufacturing sector in Türkiye is highly competitive. The results of studies aimed at identifying the factors affecting profitability are important because understanding profitability determinants enables firm management to boost productivity and maintain strong profitability.

The results of the empirical analysis indicate that size, leverage, ratio of intangible assets to total assets, current ratio, and asset turnover ratio are key variables that can impact the financial performance of manufacturing firms located in Türkiye. The results of the robustness checks validate the results of the regression analysis and enable us to posit that firm-specific factors can influence the profitability of sample firms.

Balance sheet management is important for ensuring that a firm maintains an optimum mix of assets, liabilities and equity to support its operations and financial performance. This study unveiled the pivotal role of balance sheet management in enhancing long-term profitability. Previous studies have revealed that a high level of profitability is a vital precondition for long-term survival. The management of manufacturing firms operating in emerging economies should focus on marketing and advertising strategies to enhance profitability as well as evaluate growth and investment opportunities that favor overall profitability.

Drawing on the results of the empirical analysis, this study recommends that managers of manufacturing firms implement the following concrete measures to enhance profitability. First of all, they should pursue growth strategies such as mergers and acquisitions to increase firm size, thereby benefiting from economies of scale, greater bargaining power, and improved access to economic resources. Secondly, it is advisable to mitigate reliance on debt financing, especially short-term or high-interest debt, in order to minimize financial risk. Thirdly, managers should prioritize technological innovation and digital transformation, as these contribute to long-term competitive advantage. Additionally, improving working capital management can strengthen the firm’s liquidity position and operational stability. Lastly, operational efficiency can be enhanced through the adoption of lean manufacturing practices and automation technologies. Overall, managers of manufacturing firms should aim for sustainable growth, prudent financial management, and strategic investment in intangible assets, while continuously adapting to rapidly changing macroeconomic conditions.

Based on the findings of this study, there are some suggestions for policymakers. Policymakers could develop alternative financing mechanisms to mitigate over-reliance on interest-bearing debt and provide tax incentives for innovation, digital transformation, research and development, and improve intellectual property rights enforcement. Additionally, policymakers could encourage financial institutions to provide flexible liquidity management tools and support investment in lean manufacturing practices and automation to enhance asset utilization.

Like any research, this research has some limitations. Firstly, this study focuses on only manufacturing firms listed on Borsa Istanbul. Therefore, to see if the results of empirical analysis could be generalizable, further studies should focus on other industries in Türkiye. Secondly, the data base of this study is limited to 10,125 observations and only covers 5 years from 2019 to 2023. Future studies can use a larger sample size to obtain more rational and comprehensive results.

The findings of this study support those of previous studies and provide firm management and policymakers with important guidelines for enhancing profitability in uncertain times. Future research could focus on the non-linear effects of financial variables, integrate strategic dimensions such as innovation, technology, and digital transformation, and examine how institutional or ownership contexts moderate the factors that drive profitability. A broader set of macroeconomic variables could also be considered, depending on data availability, and conducting an industry-by-industry analysis is recommended. Additionally, dynamic modeling and cross-country comparisons could yield deeper causal insights and enhance the generalizability of the findings.

Footnotes

Acknowledgements

The author is grateful to the editors and the anonymous referees for their comments and important suggestions.

Author Contributions

The author designed research methodology, analyzed the collected data and interpreted the results. The author reviewed the results and approved the final manuscript.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

Upon reasonable request, the author will provide all supplemental files, data generated and analyses.