Abstract

The main objectives of this study are to examine the impact of stock price performance on firm’s investment and to investigate the counter impact of changes in investment expenditures on stock price performance. The random effects model was applied on the panel data of Chinese manufacturing firms listed at the Shanghai Stock Exchange and the Shenzhen Stock Exchange during the period 2002 to 2016. The sample contains 398 firms with 5,970 observations. Although there is a statistically significant and negative relationship between stock price and investment expenditures, the impact of stock price on investment expenditures is far greater than that of investment expenditures on stock price. Information asymmetry positively mediates both investment sensitivity to stock prices and stock prices sensitivity to investment. This study is a valuable contribution toward the analysis of investment decision making by manufacturing firms in China. It also provides guidelines for investors to assess the informational status of the capital market before making investment decisions and to comprehensively understand the different decisions made by firms with regard to the issue of new stocks and the indirect information attached with such issues.

Introduction

The study of corporate investment has become an interesting topic for researchers after the introduction of irrelevance theorem (Modigliani & Miller, 1958). According to macroeconomic theories, firm investment is important because it creates employment opportunities for the masses, improves their living standards, and plays a decisive role in economic growth and development. Changes in the investment of firms cause the prices of their stocks to fluctuate, thereby prompting stock investors to increase or decrease the volume of their investment in the stocks of the firm. In a well-known theorem called the Fisher separation theorem, it is supposed that the capital market is perfect and free of frictions and that the capital structure and investment decisions are independent when the cost of finance from external and internal sources is constant. However, this theorem is no longer considered valid and has been challenged and negated by researchers (starting from the work of Myers & Majluf, 1984). They believe that good investment can ensure the smooth operation and success of a business, but oppose the existence of perfect capital market.

It is worth noting that certain issues in the capital market, such as information asymmetry, create difficulties in making such investment decisions. While highlighting the importance of market frictions, Morck, Yeung, and Yu (2000) examined the information content of different stock markets. Their results showed that firm-specific return variation is high in countries with well-developed financial systems and low in emerging markets. They argued that in countries with well-developed financial markets, traders are more motivated to gather information about individual firms; as a result, prices reflect more firm-specific information. In sum, their research results remind us that (a) examining the inter-relationship of investment and stock prices (i.e., how much firm investment is sensitive to stock prices) is inevitable and (b) the movements of the stock prices are an important determinant of investment expenditures of manufacturing firms. But the markets of developing countries provide a setup that is conducive to information asymmetry and where complete information regarding firms is not conveyed to the investors, thereby ultimately creating serious problems such as adverse selection and low return on investment.

In this article, we empirically study the impact of stock price movement on firm investment and the feedback of firm investment expenditure under the asymmetric information market environment, which is a factor contributing to the decision-making of investors and managers in developing countries. That is to say, according to investment theory, Tobin’s Q (as a proxy of stock price performance) plays an important role in firm investment only if the market is complete. If the market is incomplete (that is, there is information asymmetry), will Tobin’s Q not have a significant impact on corporate investment? Moreover, how will the degree of information asymmetry affect the sensitivity of investments to stock prices? To clarify these basic issues, we consider China, as the research object and introduce the information asymmetry hypothesis to reexamine the inter-relationship between investment and the stock prices of the firms.

There are four main reasons why we choose Chinese manufacturing listed companies to do this research. First, China is one of the big emerging economies known as BRICs (Brazil, Russia, India, and China) countries, with unique economic, social, and financial market system and regulations. Second, China stock markets are rapidly growing from past 20 years. According to World Bank’s latest data of 2018 on market capitalization, China is ranked the world second largest capital market after United States for its aggregate market capitalization of 6,324.88 billion U.S. dollars. Third, China has large manufacturing industry, which accounts for nearly 34% of China’s gross domestic product (GDP), and it has attracted the attention of scholars, entrepreneurs, and consumers all over the world, including developed countries. Finally, unlike developed countries, firm’s state ownership significantly affects their information environment for local institutional investors and foreign institutional investors in China.

This study has three contributions. First, we propose a new set of variables and construct econometric models to study the relationship between stock price and enterprise investment. The choice of these variables is not limited to the financial statements of listed companies, but also takes into account the information asymmetry under imperfect market development. We use the size and age of the firm to reflect the degree of information asymmetry, and use sale, leverage, trading volume and market capitalization to reflect the financial information of listed companies. Second, our findings support the views of Chaney and Lewis (1995) and Bushman and Smith (2003). Bushman and Smith (2003) believe that information disclosure reports manipulated by management can reduce the degree of information asymmetry in the process of financing and avoid large fluctuations in stock prices, thereby reducing financing costs and improving the efficiency of investment. Chaney and Lewis (1995) find that when there is information asymmetry between managers and potential investors, earnings management will lead to investors unable to make a correct judgment on the value of corporate stocks, leading to irrational overvaluation of corporate value by investors, and stock price overvaluation will reduce financing costs, thereby affecting enterprise investment behavior. Third, this article empirically analyses the sample of 398 listed companies in China’s manufacturing industry from 2002 to 2016. Therefore, it is a summary of China’s enterprise reform and the development of investment and financing markets and has certain reference significance for the development of capital markets in other emerging countries.

The rest of this article is organized as follows. Section “Literature review and hypothesis development” presents our hypotheses through literature review. Section “Empirical methodology and variable description” discusses the characteristics of the model and the definition of variables. Section “Data and its statistical characteristics” introduces the methods of data collection and makes descriptive statistical analysis and correlation analysis. Section “Results and discussion” shows the results of empirical analysis and explains them. Section “Robustness test” analyses the robustness of all models, and finally, section “Conclusion” is the conclusion.

Literature Review and Hypothesis Development

Investment is the backbone of every firm and creates more economic activities for individuals and enterprises. Previous studies have cited many factors that affect a firm’s investment opportunities. Ağca and Mozumdar (2017) find that internal funds and cash flows are important and significant determinants of firm investment. Bialowolski and Weziak-Bialowolska (2014) conduct a study on Polish companies and found that payment delays and legal and macroeconomic factors considerably affect firm investment decisions. Their study also shows that cash flow sensitivity has a significant negative impact on firm investment at the time of high growth rate options. Alti (2003) states that firm investment is sensitive due to its own cash flows in case of stable financing. Asker, Farre-Mensa, and Ljungqvist (2014) document that short-termism distorts the investment decision of stock market-listed firms. Compared with private firms, public firm invests considerably less and are less responsive to changes in investment opportunities, mostly in industries where stock prices are more sensitive to earnings news.

Foucault and Frésard (2018) find that a firm’s strategies can increase the value of the firm because it magnifies its managers’ capacity to prevail over information from stock prices and increase their efficiency in making investment decisions. Dessaint, Foucault, Frésard, and Matray (2018) state that firm managers have limited ability to distinguish the noise in stock prices at the time of signaling their investment opportunities. Also, firms reduce their investment in response to non-fundamental drops in stock prices. Kumar and Li (2016) study the dynamic effects of capital investment in innovation capacity on stock returns and investment and found a positive correlation between cumulative stock returns and investment.

Young and small firms are highly sensitive with high growth rates and low dividend payout ratios. Firm investment is directly associated with stock prices and positively correlated with each other because managers’ investment decisions might be more responsive to stock prices movements. Blanchard, Rhee, and Summers (1993) and Morck, Shleifer, Vishny, Shapiro, and Poterba (1990) document that firms investment expenditures and stock prices are significantly positively correlated.

Information asymmetry is one of the most important factors that affect the investment of firms. Z. Wang and Zhang (1998) provide a model of principal–agent relation and found that information asymmetry has a significant negative impact on firm investment. Han, Kim, Lee, and Lee (2014) proposed that the existence of information asymmetry has a significant negative effect on the stock returns of firms and that information asymmetry is associated with investors due to lack of timely and correct information. Baxamusa, Mohanty, and Rao (2015) addressed the effect of information asymmetry on firm investment and stated that equity is used to fund project with higher information asymmetry, while debt is used to fund investment with lower information asymmetry.

Tsai (2008) documents that information asymmetry has significant impact on corporate investment decisions and increases the expected bankruptcy cost, cost of firm value, and information spread. Similarly, Cui and Deng (2007) develop a theoretical model with theories on information asymmetry and corporate governance and concluded that information asymmetry has a significant negative effect on firm investment. Information asymmetry affects the investment opportunities of firms because superior information is the key element of this effect on firm investment.

Ni and Khazanchi (2009) find that information asymmetry adversely affects information technology investment and increases information cost. Ascioglu, Hegde, and Mcdermott (2008) report similar results, claiming that information asymmetry forces investments to decrease and increases their sensitivity to internal funds. When information asymmetry exists in the market, the investment opportunities become highly sensitive and the volume of firm’s investment decreases with a high ratio.

When regulatory bodies take measures to reduce the level of information asymmetry in the market, additional investment opportunities for firms may be created. Chowdhury, Kumar, and Shome (2016) find that information asymmetry decreased after the implementation of the Sarbanes–Oxley Act, thereby decreasing investment cash flow sensitivity. Generally speaking, lower information asymmetry is positively associated with firm investment at the time of underinvestment and is negatively associated with firm investment at the time of overinvestment (Belleflamme & Peitz, 2014).

From the above discussion on the relation between information asymmetry and investment, we propose the following hypotheses:

Information asymmetry reduces the external funding of firms and affects investment sensitivity to cash flow. According to Fazzari and Variato (1994), the capital of firm investment mainly comes from the credit market, but the credit market is imperfect and asymmetric information exists because of the lack of information on how to identify the confidence of borrowers and investment risks. Banks generally use different rates with borrowers, but higher rates force firms to give away some promising projects.

In simple words, information asymmetry causes under investment in firms. Information asymmetry also has a greater impact on the indirect determinants of firm investment, such as cash flows and external financing. Kaplan and Zingales (1995) and Hubbard, Kashyap, and Whited (1993) prove the dependence of investment on internal funds at the time of information asymmetry. Leitner (2007) investigates the link between the stock market and business investment and found that firm investment has a significant impact on stock prices. Similarly, Himmelberg, Gilchrist, and Huberman (2004) study the increase in stock prices above the real value and found a positive effect on real investment of the firms. Kong, Xiao, and Liu (2010) find that information asymmetry has a significant negative effect on investment sensitivity to stock prices in China. Our study is different from Kong et al. (2010) because they ignored the causal relationship between investment and stock prices in the absence of information asymmetry. Considering the above discussion, we hypothesize the following:

Information asymmetry also influences direct determinants of stock prices, such as ownership structure of firms. The stock market has two crucial factors: market information and market timing. The importance of the two factors is not considerably different, and they have a greater impact on stock market investment. Gelb and Zarowin (2002) state that greater disclosure has a significant positive relationship with stock price informativeness. When stock price information is delayed or is not disclosed properly, then trading volume decreases rapidly and information asymmetry negatively influences stock prices. Durnev (2010) find that investment is 40% less sensitive to stock prices during election years around the world than it is during non-election years. Stock prices become less informative, and investments increase price sensitivity during elections results in uncertainty. Hou and Moskowitz (2005) study the market frictions, price delay, and the cross section of expected returns of U.S. firms, and they found that high information asymmetry corresponds to increased price delay and the slow response of stock prices to new information. Therefore, price delay is a good measure of the degree of asymmetric information. A small segment of delayed firms, constituting only 0.02% of the market, generates substantial variation in average returns. On the basis of the above discussion, our hypotheses are as follows:

Chen, Goldstein, and Jiang (2006) find that private information in stock prices has a significant positive effect on the sensitivity of firm investment to stock prices. Their results show that managers learn from the private information of the stock market and incorporate this superior information at the time of investment decisions. According to Kouser, Saba, and Anjum (2016), when information asymmetry exists, the sensitivity of stock prices to investment is positively correlated and the sensitivity of investment to stock prices is negatively correlated with each other. Baker, Stein, and Wurgler (2003) states that nonfundamental movements in stock prices have a greater impact on stock price sensitivity to investment. The above discussion leads to the following hypothesis:

Empirical Methodology and Variable Description

Model Specification

In summary, we propose two sets of hypotheses through literature review, namely H1a, H1b, and H1c, as well as H2a, H2b, and H2c. To verify these six hypotheses, it is necessary to construct equations for each hypothesis as follows:

where I

i,t

stands for investment (i.e., investment in fixed assets) for firm i during year t. Q

i,t

is Tobin’s Q ratio of firm i in the year t. AsyInoi,t−1 represents information asymmetry, which is measured by information delay. We controlled

Variable Description

Now, we describe and define the variables in the six equations based on the conclusions of the literature.

Investment

In economic theory, investment refers to the economic behavior of a specific economic subject to place a sufficient amount of capital or physical monetary equivalent into a certain area in a certain period to obtain income or capital appreciation in the foreseeable future. On the basis of this idea, researchers usually choose different investment measurement methods according to their research purpose. For instance, in studies on the relationship between internal financing and investment outlays of the firm, some researchers use gross investment (Fazzari and Athey, 1987; Cleary, Povel, and Raith, 2007; Athey and Reeser, 2000), whereas others use net investment. In addition, because fixed asset investment is the main content of an enterprise’s inward investment, many studies define investment as the change in the book value of tangible fixed assets plus depreciation scaled by the book value of tangible fixed assets at the beginning of the year.

In this study, we define investment as the investment in tangible fixed assets after depreciation. The mathematical formula is as follows:

Stock price

A review of literature produced in the last decade shows that almost all empirical results support the idea that stock returns have a significant impact on firm investment. The weak ability of managers to filter the noise of stock prices also impacts firm investment and manager decisions (Dessaint et al., 2018). Therefore, it is a good method to study the impact of stock price fluctuation on corporate investment by using stock return as a measure of stock price. But in data preprocessing, we find that Tobin’s Q is better, so this article refers to Hoshi, Kashyap, and Scharfstein (1991) using Tobin’s Q.

Tobin’s Q

Tobin’s Q was developed by J. Tobin in 1969 to measure firm performance. It is the ratio of the market value of the firm to the book value of its assets (originally the replacement value). This ratio shows an increase in the unit value of the cost of purchasing assets to create value. When the ratio is less than 1, buying or replacing newly generated capital goods is worse than buying ready-made capital goods, thereby making further investment impossible for a company or resulting in low or nonexistent investment opportunities. In practice, Tobin’s Q measurement method varies with different research purposes. This study is based on the ratio of the market value of equity to the book value of total liabilities and that of total assets.

In this study, Tobin’s Q has two roles: it acts as a proxy of the stock price performance and also as the independent variable. In the existing literature, such as Hoshi et al. (1991), using Tobin’s Q and information asymmetry is considered the most relevant to firms with good prospects (i.e., those with Q greater than the median value) and those with bad prospects (those with Q less than the median value).

Information asymmetry

Asymmetric information forces investments to decrease and enables investments’ sensitivity to internal funds to increase. Thus, in the presence of information asymmetry in the market, internal funds may become the basic determinants (elements) of firm investment (Ascioglu et al., 2008). Unlike information symmetry among managers and owners, asymmetric information delays investments (Shibata & Nishihara, 2011). The quality of accounting information will have a positive impact on a firm’s investment behaviors. In sum, in the case of information asymmetry in the capital market, (a) investment depends on internal funds, (b) overinvestment sometimes exists (i.e., in case of managerial discretion problems), and (c) underinvestment sometimes exists as well.

In our study, information asymmetry is captured with the interaction terms of stock prices (measured by Tobin’s Q) and asymmetric information (measured by firm age and size).

Firm age

Firm age is a widely used proxy of information asymmetry. According to Moyen (2004) and Cleary et al. (2007), the age of the firm is taken in years since the date of its listing at the stock exchanges (Shanghai Stock Exchange and Shenzhen Stock Exchange in this case). The natural log of the age of the firms is taken and then averaged out. The mathematical formula is as follows:

Firm age is compared with the average of logged values and categorized as young firms (i.e., firms with a log value less than the average) and mature firms (i.e., firms with a log value greater than the average). Young firms face information asymmetry, whereas mature firms are supposed to be free of asymmetric information.

Firm size

Firm size is also often used to analyze information asymmetry. Works by Arslan-Ayaydin, Ozkan, and Florackis (2006) and Harris (1994) used firm size to measure information asymmetry. In general, the policy disclosures of large firms are relatively transparent and comprehensive, and they can be analyzed by internal and external analysts. Thus, information asymmetry is less intensive in large firms (Ozkan & Ozkan, 2004). Firm size has been used in different ways by different researchers. Sales volumes, number of employees, value of total assets, and market capitalization are some of the common measures used to represent firm size. This study uses average of logged value of total assets to measure firm size. The mathematical formula is as follows:

The whole sample is divided into two subgroups using the median value of the total assets. Each original value of size is compared with this median value. The value that is greater than the median denotes large firms, and the others denote the small firms. We expect that the large firms have lower information asymmetry, and the small firms have higher information asymmetry.

On the basis of previous studies on the relationship among stock price performance and investment, we include the following control variables.

Sales

Sales are also used as a variable to control the accelerators’ effect. Before being used in the model, sales are lagged by one year and scaled by opening of this period book value of fixed assets as well. The mathematical formula is as follows:

According to the accelerator theory of investments, the increasing demand for the output of firms (not the level of demand) determines the level or the demand for investment of the firms. Thus, sales are included in the investment equation as a control for the accelerator effect.

Market capitalization

Many previous studies found that company size (when measured by market capitalization) has a great impact on firm investment. Therefore, we use market capitalization as a control variable. We use natural log value of market capitalization at the end of the prior fiscal year, and its calculation method is as follows:

Leverage

Leverage does not reduce the growth of firms with good investment opportunities, but it negatively affects firms with low investment opportunities (Lang, Ofek, & Stulz, 1995). Thus, the leverage ratio is used as the control variable in this study, and the calculation method is as follows:

Trading volume

According to Assogbavi, Khoury, and Yourougou (1995) and Chan and Fong (2000), a positive relationship exists between stock price and trading volume. We measure trading volume with the proxy of the total number of shares traded by the firms, that is

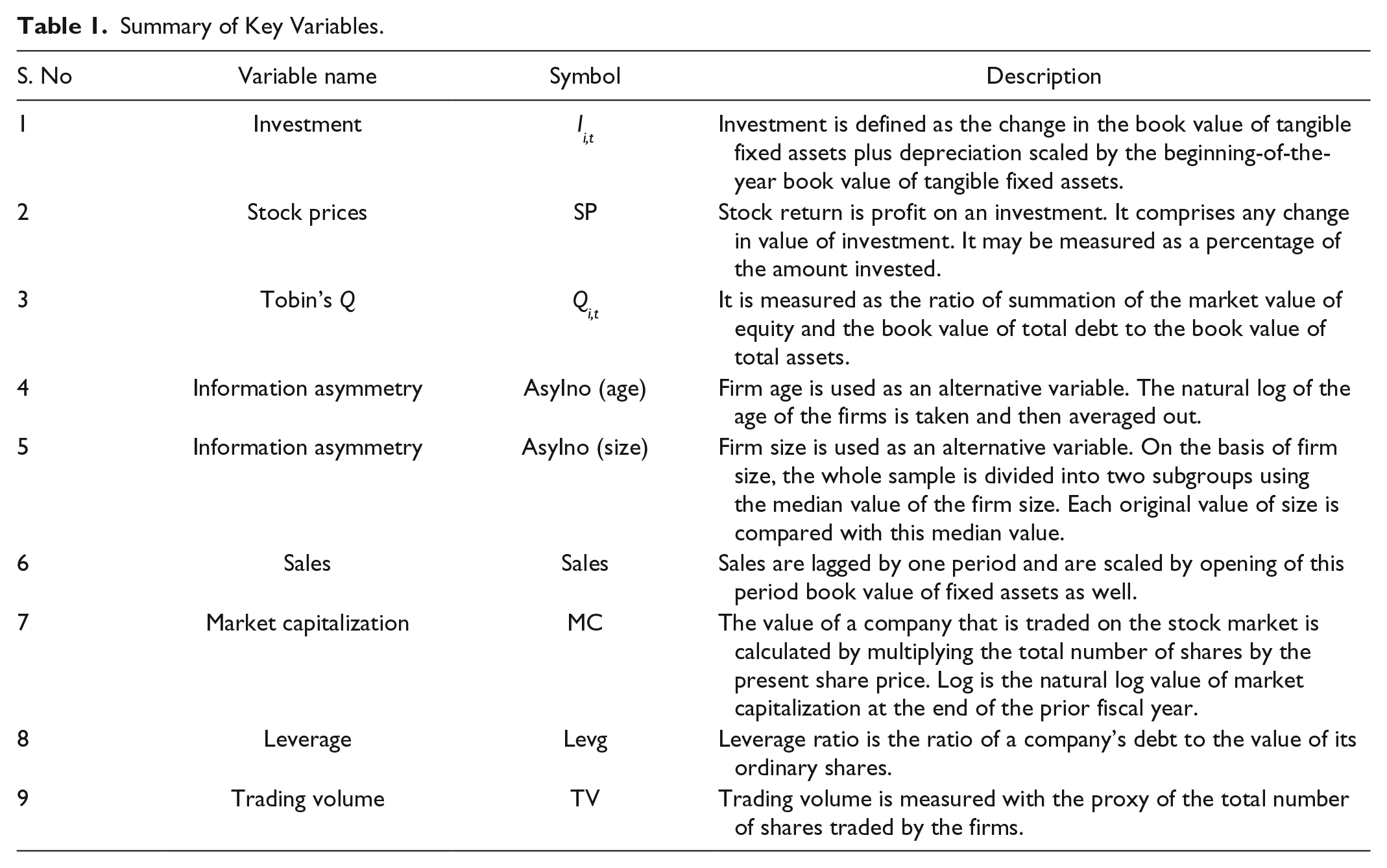

Table 1 presents the definition and proxy of each variable.

Summary of Key Variables.

Data and Its Statistical Characteristics

Data Collection

Considering that China has the three characteristics of developing countries, a large economy, and rapid development of the capital market, we choose the manufacturing industry in China’s stock market as the research object. The entire manufacturing industry, which consists of 2,266 listed firms, constitutes the population for this study.

The final sample consists of 398 companies (representing textile spinning, textile weaving, finishing, jute, information and communication, food, chemicals, paper and board, fuel and energy, sugar, and cement sectors of non-financial companies at the Shanghai Stock Exchange and the Shenzhen Stock Exchange) and 5,970 observations from 2002 to 2016. Convenient sampling is used in the process of sample selection. One major source provided us with access to the data required for the empirical portion of this study, namely, the Wind database, which provided the data for all the variables (i.e., investment, trading volume, market capitalization, stock prices, sales, current assets, current liabilities, total assets, and total debt or total liabilities) used in this study. The source is supposed to be valid. Therefore, no issue exists with regard to the reliability of the data.

Statistical Characteristics of Data

A large sample of data can be easily described by descriptive statistics. Table 2 reports descriptive statistics characteristics of the variables used in this article.

Descriptive Statistics.

Note. SP = stock prices; MC = market capitalization; TV = trading volume.

Table 2 shows that the age difference of the sample firms is very small: the maximum value is 3.2188, the minimum value is 0, and the deviation is only 0.6842. The size difference is large: the minimum value is 7.8383, the maximum value is 16.8365, and the standard deviation is 1.2563. The minimum value of stock return is −100, the maximum value is 849.8556, and the deviation is the largest in the independent variable, which are 90.0604. In addition, the deviation of sales in the control variables is large, reaching 95,919.0000; the minimum and maximum values are 0 and 15.25, respectively. The minimum value of sales volume, stock trading volume, and market value is zero because some of the firms have just been established or were not listed during the corresponding statistical period.

To avoid multicollinearity problems in the model, the Pearson correlation coefficients of all variables are tested, and the results are shown in Table 3. First, except for the correlation coefficients of MC, Levg and Age, TV and Sales, Levg are more than 0.9; whereas the coefficient of other variables are less than 0.5. This result means that multicollinearity does not exist between variables, thus indicating suitability for panel data analysis.

Correlation Matrix.

Note. SP = stock prices; MC = market capitalization; TV = trading volume.

means significance at 10% level. ** means significance at 5% level. *** means significance at 1% level.

In addition, the matrix shows that the relationship between variables is in accordance with the theory. It expresses a stronger correlation between investment and stock prices in the presence of asymmetric information.

Results and Discussion

We run Hausman’s specification test on all our estimation models (the Models 1-6) to differentiate between fixed and random effects panel models. For all the models, Hausman’s specification test accepted the null hypotheses that support the use of random effects models. Thus, we specified all our panel data models as random effects models and testing the hypotheses proposed in section “Literature review and hypothesis development” (see H1a, H1b, H1c, H2a, H2b, and H2c) by using them.

On the basis of our hypotheses H1a and H1b, we conduct an empirical analysis based on to determine whether the information contained in the stock prices assists managers in their decision-making process and whether information asymmetry in the stock market has some influence on firm investment. Before starting the analyses, the firms are divided into two age groups: the younger firms and the older firms. The younger firm is equal to one if the age after taking the natural log (ln) is less than the median value; otherwise, it is equal to zero and vice versa.

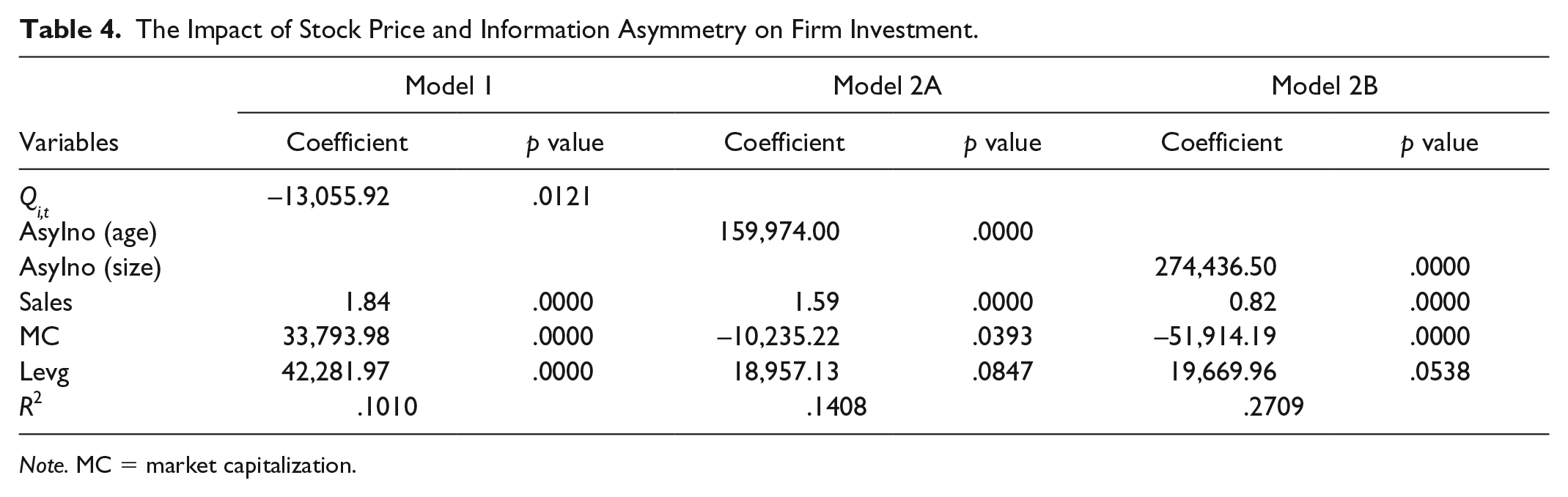

Table 4 provides the detailed results of the three models.

The Impact of Stock Price and Information Asymmetry on Firm Investment.

Note. MC = market capitalization.

In Table 4, we can see that the coefficients of the three main independent variables, stock price, and two interaction terms of information asymmetry that is (Qi,t, AsyIno [age], AsyIno [size]) are −13,055.92, 159,974.00, and 274,436.50, respectively, and their p values are .0000. Therefore, we can affirm that (a) stock prices have a negative effect on investment expenditure, which means that the investment expenditure of firm’s decreases with the rise in stock price, and (b) both proxies of asymmetric information have a positive impact on investment expenditures, which means that asymmetric information is more conducive to investment expenditures.

Continuing to observe the values of other independent variables (control variables) in the table, we can find that (a) the maximum value of p in the three models does not exceed 0.09, which means that the control variables have significant impact on investment expenditures, and (b) in Model 1, the coefficients of all control variables are positive and significant, whereas in Models 2A and 2B, the coefficient of market capitalization turns to be negative and remain significant, and the coefficients of other control variables are consistent to Model 1.

We believe that market capitalization has a significant negative impact on firm investment in the case of information asymmetry, and the degree of this negative impact is based on the information asymmetry of the firm.

To attain the objectives of this study and to prove our hypothesis, we analyze the impact of stock price changes on the sensitivity of investment with interaction terms of standard stock price and dummy of information asymmetry.

Table 5 shows the results to test hypothesis H1c.

Sensitivity of Firm Investment to Stock Price With the Impact of Information Asymmetry.

Note. MC = market capitalization.

Unlike Table 4, Models 3A and 3B in Table 5 take into account the effect of information asymmetry on stock price performance, which is measured by Tobin’s Q, We find that (a) the coefficients of Qi,t are still negative and (b) the coefficients of interaction terms and control variables are positive and highly significant. On the basis of these findings, we affirm that the sensitivity of investment expenditures to stock price performance is negative, while the sensitivity to sales, market capitalization, and leverage ratio is positive. Also, stock price has a significant positive information asymmetry effect on firm investment.

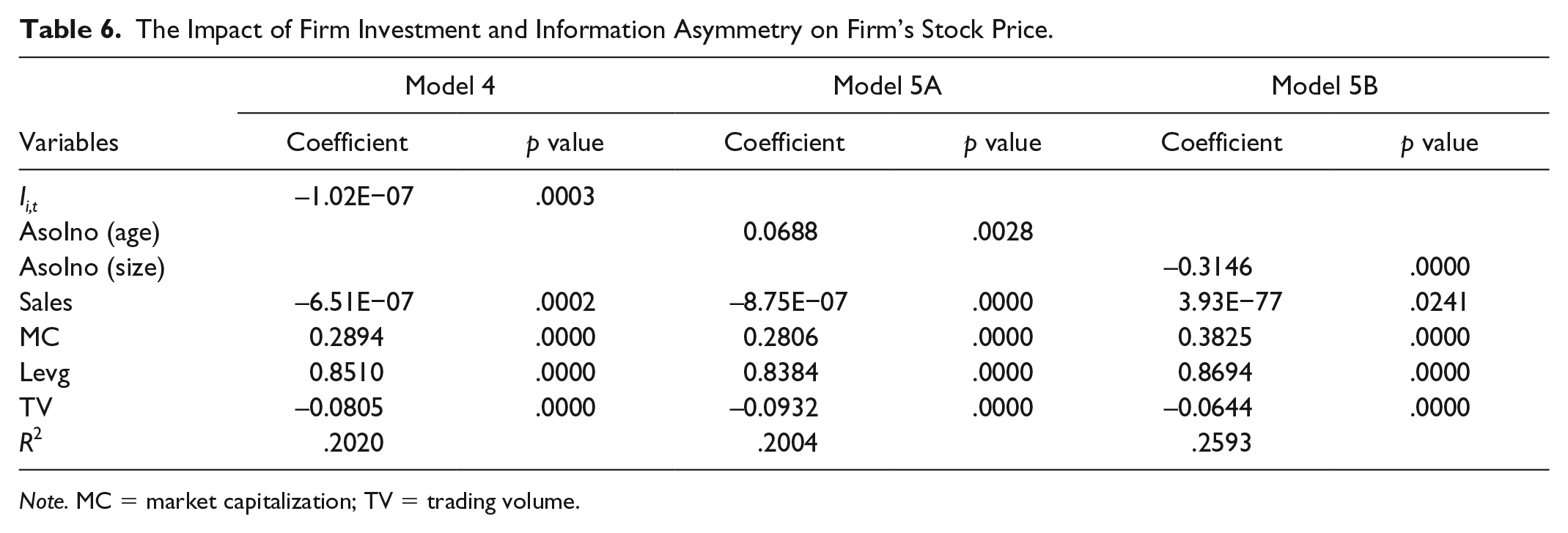

Table 6 reports the results to assess the impact of changes in investment on the stock price of the firm (hypothesis H2a) and the impact of information asymmetry on stock prices of the firm (hypothesis H2b).

The Impact of Firm Investment and Information Asymmetry on Firm’s Stock Price.

Note. MC = market capitalization; TV = trading volume.

The results in Model 4 of Table 6 show that investment expenditures is negatively and significantly related to stock price performance, while information asymmetry shows mixed results, in Model 5A, the coefficient of AsoIno(age) is positive and significant, but the coefficient of AsoIno (size) is negative and significant. Among the four controlling variables, market capitalization (MC), leverage (Levg), and trading volume (TV) have relatively stable effects on stock prices, but the MC and Levg have positive effects, whereas the sales and TV have negative effects.

Table 7 reports the sensitivity of stock price (Qi,t) to major independent variables (Ii,t), interaction terms, and control variables. Results show that (a) the stock price of a firm increases with the decrease in its own investment; (b) the increase in sales and trading volume of a firm have a negative impact on the stock price performance, but leverage and market capitalization have a positive impact on the stock price performance; and (c) there is a positive and significant relation between the stock price performance and the information asymmetry, which means that information asymmetry plays a positive role in improving the negative impact of investment on stock price performance.

Sensitivity of Stock Price to Investment With Direct Effect of Information Asymmetry.

Note. MC = market capitalization; TV = trading volume.

Comparing with the results of Table 5, the sensitivity of stock price to investment is far less than that of investment to stock price. Thus, the impact of firm investment on its market value is very small and can be neglected. The result of our study is also consistent with Liu (2015).

Robustness Test

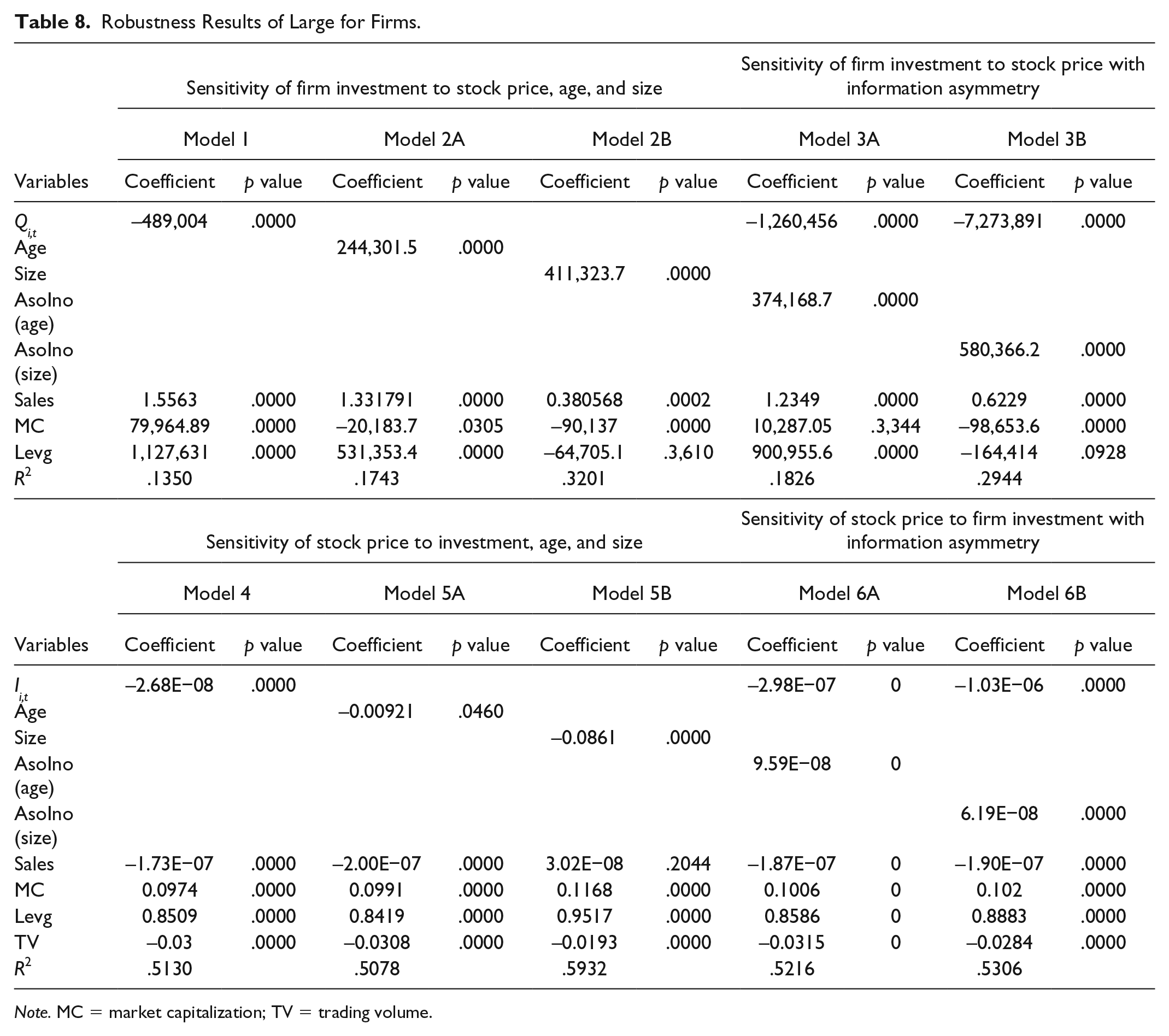

Real-world economic phenomena and effects are objective and impossible to change with the change in economic models. For this reason, we investigate the robustness of dependent and independent variables and check the interaction term of Ii,t and Qi,t with the dummy of information asymmetry measured by firm age and firm size. We split the sample into two groups based on the median value (7,273.53) of sales. One group is the high-sales firm, and the other is the low-sales firm group. We run two robust analyses (see Tables 8 and 9) and find that the results are mostly consistent with the estimates from Models 1 to 6B.

Robustness Results of Large for Firms.

Note. MC = market capitalization; TV = trading volume.

Robustness Results for Small Firms.

Note. MC = market capitalization; TV = trading volume.

Table 8 reports the statistical analysis results of the high-sales enterprise groups based on Models 1 to 6B. From the analysis results, except Levg with AsyIno(size) in Model 2B, MC with AsyIno(age) in Model 3A, and Sales with AsyIno[size] in Model 5B, the possibility of other independent variables affecting dependent variables is more than 90%.

Table 9 reports the statistical results of the low-sales enterprise group. From the analysis results of p values, the probability of independent variables influencing dependent variables is basically more than 95%. Only Levg with AsyIno[age] in Model 2B and Sales with AsyIno(size) in Model 3A and Model 5B have a probability of less than 55%.

In summary, we estimated all models based on high- and low-sales firm groups and find that our results are highly robust. Therefore, information asymmetry in the market, which is composed of differences in firm size and age, affects companies’ investment and stock price decision making and plays a vital role in the decision-making process of company managers.

Conclusion

In an imperfect capital market, the investment of firms facing information asymmetry is more sensitive to fluctuations in their stock prices than that of the firms that do not face information asymmetry. This argument is representative of almost all contemporary researchers in corporate finance. It has been tested and is still being tested by many neoclassical and contemporary researchers. The counter impact of investment on the sensitivity of stock prices is another matter of discussion among researchers. This study is conducted to retest and reexamine this inter-relationship. With the full support of neoclassicism and contemporary literature on corporate investment, we put forward six hypotheses.

To test these hypotheses, the manufacturing industry of China is chosen, with 398 listed companies being selected. After the necessary initial data tests, the random effects model is employed because it best suits the data being analyzed in this research. The results are consistent with some views of contemporary researchers, such as “the asymmetric information has a significant positive impact on the stock price sensitive to investment” (Kong et al., 2010) and “the stock price has a negative impact on investment expenditure” (Kouser et al., 2016), but there are also some inconsistency, such as “the information asymmetric has a significant negative impact on the investment sensitivity to stock price” (Kong et al., 2010) and “investment expenditure has a positive impact on stock price” (Kouser et al., 2016).

All hypotheses are accepted, thereby proving the interdependence of firm investment and stock prices. The conclusion is that firms that face severe financial constraints have higher investment sensitivity to stock prices of firms because of information asymmetry than firms that do not face such problems. This sensitivity transparently explores the fact that information asymmetry exists in Chinese capital markets.

Although our findings are in favor of most contemporary research, this study is conducted in specific context of Chinese manufacturing industry, and there are some limitations. First of all, we report or conduct this research in context of China and its implication is just limited to China manufacturing sector. Second, Tobin’s Q evaluation in this study uses stock price data published by Shanghai Stock Exchange and Shenzhen Stock Exchange, which has limitations. With the deepening of the opening up of Chinese enterprises, it may be more meaningful to extend the data to the share prices of Chinese enterprises listed on the Hong Kong Stock Exchange and the American Stock Exchange. Finally, it is very interesting avenue for future research to conduct a study on all emerging economies, and developing economies with different mediating mechanism and control variables, this could be an interesting extension of our study and become another path of future research in area of corporate finance. Still, many factors need to be incorporated in this field, such as economic policy, bank liquidity, and other proxy variables of asymmetric information (e.g., market expectations, corporate tangible assets, and R&D expenditure). Furthermore, an alternative measure for Tobin’s Q (i.e., Euler equations) may be applied.

Footnotes

Acknowledgements

The authors acknowledge support from the Chinese Government Scholarship Council (CSC).

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.