Abstract

This study contributes to the growing debate on the relation between varying stock market conditions and the profitability of stock market anomalies. We investigate the effect of changed market conditions on time-varying contrarian profitability in order to examine the presence of the Adaptive Market Hypothesis (AMH) in South Asian emerging stock markets. The empirical findings reveal that a strong contrarian effect holds in all the emerging markets. We also find the stock return opportunities vary over time based on contrarian portfolios. We show that contrarian returns strengthen during the down state of market, higher volatility and crises periods, particularly during the Asian financial crisis. Interestingly, the market state instead of market volatility is the primary predictor of contrarian payoffs, which contradicts the findings of developed markets. We argue that the linkage arises from structural and psychological differences in emerging markets that produce unique intuitions regarding stock market anomalies returns. The overall findings on the time-varying contrarian returns in this study provide partial support to AMH. Another significant outcome of this study implies that investors in South Asian emerging markets, like investors in the developed markets, could not adapt to evolving market conditions. Therefore, contrarian profits often exist, and persistent weak-form market inefficiencies prevail in these markets.

Introduction

Momentum and contrarian investment strategies represent the stock market anomalies that are often considered as challenging to be thoroughly explained through the Efficient Market Hypothesis (EMH). A contrarian strategy involves bucking against the current market trend to make profits. Contrarian investors usually search for distressed stocks and short the existing stock market trends in the bull market. Prior studies show that contrarian or momentum profits vary considerably across markets. For example, Chui et al. (2000), Griffin et al. (2003), Locke and Gupta (2009), Asness et al. (2015), and Yu et al. (2019) document strong contrarian effect in Asian emerging markets, while the opposite effect is found in developed markets. Several studies present different risk-based (e.g., Avramov & Chordia, 2006; Fama & French, 2017; Jegadeesh & Titman, 1993; Munir et al., 2020), as well as behavioral (e.g., Bhootra, 2011; Hong et al., 2000; Lekhal & El Oubani, 2020; Nofsinger & Sias, 1999; Yu et al., 2019) interpretations over the past few decades as to why the momentum or contrarian patterns exist in stock returns. However, how the historical performance of stocks contributes to their subsequent performance is still a puzzle in academic literature, which allows trading strategies to generate abnormal returns by exploiting market inefficiency.

A more comprehensive theory needed to be developed to interpret the time-varying behavior of stock market anomalies. In this regard, Lo (2004) proposed the Adaptive market hypothesis (AMH) theory, which claims that the efficiency and inefficiency can coexist in financial markets. Market competition, innovation, natural selection, market participants and their adaptation cause the wax and wane in the degree of market efficiency and profits of investment strategies. The major practical assertion of AMH is in utilizing profitable trading strategies timely, as the return opportunities vary over time. Based on this evolutionary perspective, the abnormal return opportunities arise over time but vanish when they are exploited. Moreover, the emergence of profitable investment strategies is dependent on the specific stock market environment. Hence, in contrast to the EMH’s argument that active management is useless, the AMH supports the portfolio’s active management.

Recent studies offer mounting evidence to support the AMH, the main line of literature focuses on measuring the time-varying probability of stock returns as market efficiency measure (Ito et al., 2016; Kim et al., 2011; Shi et al., 2017). Another line of literature is concentrating on evaluating the time-dependent efficiency of trading anomalies implied in AMH (Al-Khazali & Mirzaei, 2017; Shahid & Sattar, 2017; Todea et al., 2009; Urquhart & McGroarty, 2014; Xiong et al., 2019). The procedure relating to this examines whether trading strategies’ risk-adjusted profits are time-varying. These studies provide empirical evidence based on foreign exchange market (Neely & Weller, 2013; Neely et al., 2009) and stock market indexes in the U.S. and other developed markets (Anghel, 2015; Pätäri & Vilska, 2014; Taylor, 2014; Todea et al., 2009). However, the studies are rare that focus on the profitability of momentum and contrarian investment strategies within the framework of AMH (Akhter & Yong, 2019; Shi & Zhou, 2017). For example, Akhter and Yong (2019) investigate the evolution of momentum strategy returns over time based on the AMH framework. However, as per the best of our knowledge, the studies have yet to be conducted on the evaluation of contrarian returns to the implications of the AMH, particularly in South Asian stock markets. Therefore, this study fills this gap in the literature by examining the dynamic market assumption of AMH within the framework of the contrarian effect.

This study focuses on the stock markets of Bangladesh, India, and Pakistan for two reasons. First, several studies argue that these stock markets are mostly dominated by small investors and noise trading (Brzeszczyński et al., 2015; Chowdhury et al., 2019; Cuthbertson & Nitzsche, 2005; Iqbal, 2012). The investment decisions of small investors in the South-Asian markets are driven by either sentiments or past share price movements which leads to greater price volatility in these markets (Brzeszczyński et al., 2015; Chowdhury et al., 2019; Naik & Reddy, 2021; Shiller, 1990). In addition, the noise trading further contributes toward enhanced risk in the short term, thereby offering unique justifications for the time-varying return patterns of stock market anomalies. Second, South Asian stock markets are relatively young, therefore many studies argue that some idiosyncratic phenomena characterize these markets. For instance, weak-form market inefficiencies (Chui et al., 2010; Liu et al., 2011; Rahman et al., 2020), mean-reversion of stock prices (Chui et al., 2010), non-randomness of returns (Akhter & Yong, 2019; Joshi, 2011), and speculative and manipulative bubbles (Khanna & Sunder, 1999; Khwaja & Mian, 2005) are common issues in these emerging markets. Based on these structural and psychological differences, the selected emerging markets are expected to produce unique intuitions regarding stock market anomalies as compared to their developed market counterparts.

In this study, we construct a sample from 1997 to 2018 for Bangladesh, India and Pakistan stock markets and confirm the existence of a strong contrarian effect, which is statistically significant in all the markets. Interestingly, contrarian strategies gain significantly higher profits during crisis periods, more than twice as compared to non-crisis periods. Upon examining the payoffs to winners and loser portfolios, the study finds that higher contrarian returns are primarily associated with the outperformance of loser portfolios particularly during negative market states and crisis periods. The study findings based on CAPM and augmented Fama and French three-factor (AFFTM) models further indicate that the risk-adjusted profits vary over time, while the factor loading on different risk factors is non-constant. These results partially support the AMH.

Our study contributes to the existing literature in several ways. Firstly, we examine the AMH theory on the neglected South Asian stock markets within the framework of the contrarian effect. The study findings conclude that the raw and risk-adjusted returns of contrarian strategy are time-varying, where price-and volatility-states connect with the local market environment to play a significant role in explaining the return dynamics of selected emerging markets. Secondly, we investigate whether the profitability and significance level of contrarian profits vary in different market conditions as suggested by the AMH. The dependency of contrarian returns on time-varying market conditions in South Asian emerging markets offers support to AMH, which bridges some of the gaps between the conflicting arguments of the advocates of EMH and behavioral school. Along with contributing to the academic literature, our study findings guide the investment community, which intends to exploit returns through a combination of various trading schemes. The outperformance of contrarian strategy under varying market states offers different performance matrices to individual investors and fund managers to form winners and loser portfolios in both the panic as well as stable market states.

The rest of this paper is organized as follows. Section 2 discusses the review of literature and hypotheses development. Section 3 explains data and summary statistics. In Section 4, we examine the relationship between the contrarian effect and time-varying risk premium. In Section 5, we investigate the context-dependent contrarian effects. Finally, Section 6 provides conclusions, together with implications and proposed opportunities for future research.

Literature Review and Hypotheses Development

The researchers complying with classic financial theories encouraging unbounded rationality seek novel risk relating factors for asset pricing models to interpret the abnormal gains of stock market anomalies. On the other stream, the researchers adhering to bounded investor rationality attempt to interpret stock market anomalies with behavioral models by capturing investors’ behavioral biases. Neither the proponents of the efficient market hypothesis (Fama, 1970, 1991; Fama & French, 1996, 2012) nor the behavioral school of finance (Barberis et al., 1998; Daniel et al., 1998; De Bondt & Thaler, 1985, 1987; Hong & Stein, 1999; Jegadeesh & Titman, 1995) can offer a satisfactory interpretation for these anomalies. For example, Fama and French (1993, 2017) tried to link the abnormal profits of these anomalies with various market risk factors and attempted to explain it with multi-factor models. However, the proposed factor models cannot fully explain these anomalies. In contrast, De Bondt and Thaler (1985, 1987) and Jegadeesh and Titman (1995) claim that the overreaction of investors to stock-related information is the leading cause of contrarian anomaly returns. Nevertheless, according to them, it is unclear why investors overreact. Therefore, many researchers have offered alternative explanations of contrarian and momentum returns as per their intuitions based on different circumstances and stock markets (e.g., Asness, 2011; Chen & Lu, 2017; Otchere & Chan, 2003; Yalçın, 2008; Yu et al., 2019; Munir et al., 2021).

As per the Adaptive Market Hypothesis (AMH), efficiencies and inefficiencies can exist simultaneously in stock markets because the participants are not entirely irrational or rational; however, future-oriented and wise investors learn based on their prior experiences. Empirical research on AMH reveals that the uncertainty and predictability of stock returns differ under varying conditions of a stock market, for instance, bear and bull market, equity market bubbles and bursts, etc. (Ito et al., 2016; Kim et al., 2011; Lin et al., 2021; Urquhart & McGroarty, 2014, 2015). AMH has unlocked a new stream of opportunities for scholars to offer a more realistic interpretation from a novel point of view for deviant stock return behavior. The AMH recognizes the presence of cognitive biases that can derive from heuristics and could be adapted in non-financial settings (Lo, 2004). When market participants and investors make investment decisions, they build satisfactory choices for them (bounded rationality), which may not prove to be the optimal choices (rational expectation) (Simon, 1955). The latest studies reveal that the investor’s personality traits and the factors relating to investor’s specific environmental circumstances, which are AMH’s main considerations, play a major role in incorporating the new information into prices and determining the investor’s behavior toward stock market anomalies (Urquhart & McGroarty, 2014). In contrast, the market efficiency treats every market in a similar manner (Lo, 2004); therefore, the varying behavior of stock market participants in different markets toward stock market anomalies is treated as the departure from market efficiency.

Like other anomalies of stock market, the statistical significance and profitability of contrarian and momentum anomalies change over time (Asness et al., 2015). Cooper et al. (2004) reveal that momentum returns are mainly associated with the “up” market state. Huang (2006) confirms the same finding by using the data of 17 MSCI states from 1969 to 1999. He shows that higher and significant momentum profits are linked to the “up” market. Antoniou et al. (2013) state that momentum profits strengthen in optimistic periods of the stock market. Along with “up” and “down” market state, the cycles of market volatility (high/low) and bubbles as well as crashes might also influence momentum or contrarian payoffs. The direct motivation of these possible effects arises from the fact that a dramatic loss to momentum strategies followed high U.S market volatility in late 2008. Furthermore, the momentum strategy returns further deteriorated during the bankruptcy crisis of Lehman Brothers in 2009, where the momentum strategy miserably performed with an average monthly payoff of −17%. The momentum investment strategy performs poorly in some other periods of skyrocketed volatility, such as in the early 1930s, mid-1970s, and after the NASDAQ bubble burst around the turn of the century (Demirer & Jategaonkar, 2020; Lin et al., 2021; Wang & Xu, 2015). Due to these drastic episodes that suggest the market state impact on momentum profits, this study expects that the profitability and significance level for contrarian strategy will vary when market conditions change. At the same time, it is expected that the contrarian effect will prevail primarily in the negative (down) state of the market, as well as higher volatility and crisis periods. In accordance with AMH, if the stock markets are adaptive in nature, the behavior of contrarian anomaly will vary, although the anomalous returns do not entirely fade away over time. Therefore, this study argues that the profitability and level of significance of contrarian strategy will vary with the changing market conditions. Therefore, the study proposes the following hypotheses:

Data and Methodology

To investigate the contrarian returns and their risk-premium relation in the Bombay Stock Exchange (BSE), Pakistan Stock Exchange (PSX), and Dhaka Stock Exchange (DSE), we obtain the monthly data from Thomson and Reuters DataStream. The dataset contains the adjusted closing prices of all the shares listed on each stock market, and monthly Fama and French three factors, that are formed based on Fama and French (1993). The study period extends from 1997 to 2018. To control the impact of inconsistent and small stocks, we eliminate the stocks showing inconsistent trading history. This procedure also helps us to maintain the sample of stocks which usually eliminates the least liquid stocks. This leaves us with a total sample of 2,522 stocks originating from three stock markets over a research period covering 264 months. The monthly closing prices of all listed stocks and market indices, adjusted for dividend, are changed into returns by utilizing the below Equation of continuous compounding return:

Where,

Rt = represents the return of an index or stock

Pt = the dividend-adjusted close price an index or stock at time t

Pt–1 = the dividend-adjusted close price of an index or stock at time t–1

This study adopts the overlapping portfolio construction procedure of Chen et al. (2016). We utilize monthly stock returns to construct the zero-investment loser and winner portfolios based on equally weighted and full rebalancing methods of portfolio formation. At the end of each month (t), we sort all the stocks into winner and loser portfolios based on past 12-month cumulative average returns (CARs). The shares having the highest (lowest) CARs during the formation period t–12 to t–1 are categorized as winners (loser) portfolios.

The winner portfolio contains the stocks with the prior 12-month CARs in the top 20%, while the loser portfolio comprises of the stocks with prior 12-month CARs in the bottom 20%. Following Asness (1994), the study forms contrarian strategy with a one-month delay between the formation and holding phases in order to mitigate microstructure issues such as bid-ask spread, trading cost and liquidity biases. After forming equally weighted winner and loser portfolios, we then measure the returns of each portfolio for 1 month (t + 1) holding period. By assuming the contrarian strategy of longing the loser and shorting the winner with monthly rebalancing, we compute the monthly payoffs (LMW) to contrarian strategy for each country, which is the difference in returns between the equally weighted winner (

After calculating the monthly contrarian return series, the study then investigates the pattern of contrarian profits under changing market and volatility states to verify the existence of AMH. Following Wang and Xu (2015) approach, we define market state as the return on value-weighted index for prior 12 months in each stock market at month t. For instance, a month is treated as in POSITIVE (NEGATIVE) state in cases where the prior 12-month return on market index is positive (negative). In the same manner, a month is treated as in HIGH (LOW) volatility condition in cases where the prior 6-month volatility of market index is larger (smaller) than the prior 12-month index volatility. Given that our sample period covers two major crises, such as the Asian financial crisis and global crisis and keeping in mind the possible effect of these crises’ periods on contrarian returns, we also examine the contrarian effect during these crises periods.

To demonstrate the robustness of our study results, the market state impact on time-varying contrarian payoffs in other major stock exchanges of the Asian region is also studied. We use monthly data on common stocks listed in some major emerging markets of Asia, retrieved from DataStream. These exchanges consist of Bursa Malaysia, Korea Stock Exchange (KRX), China’s Shanghai Stock Exchange (SSE), Indonesia Stock Exchange (IDX), Stock Exchange of Thailand (SET), and Philippines Stock Exchange (PSE). The main stock market index of each selected country is utilized as the proxy for market risk, which is further used to calculate the variables of market state and volatility for additional econometric analysis.

Table 1 reports the summary statistics for the yearly cumulative returns of the companies included in the dataset in each sample country over the full sample period from 1997 to 2018. The years with maximum cumulative returns for Indian and Pakistani companies in the dataset are 2001 and 2000. These years represent the periods of stock market scams for both the markets as the actions of some market brokers artificially inflated the stock prices through manipulative bubbles. The maximum cumulative return for Bangladeshi companies is evident from the year 2009 to 2011 when the stock market was facing a historic stock price boom. The minimum cumulative returns are observed in the year 2001 (−99.76%), 2004 (−39.68%), and 2009 (−37.33%), respectively for India, Pakistan, and Bangladesh. These were the periods when the markets were recovering from a stock market crash. Based on the companies used in the dataset, Indian companies have the highest median cumulative returns (26.54%), while the Pakistani companies exhibit the maximum mean cumulative returns (38.07%). The Bangladeshi companies show the lowest mean and median yearly cumulative profits of 22.45% and 15.50% during the overall sample period.

Summary Statistics for the Yearly Cumulative Returns for the Whole Data Set.

Note. This table provides the yearly minimum, maximum, median and mean returns of each country, computed with the annual cumulative returns of all the companies in the sample. The study period extends from 1997 to 2018.

Contrarian Effect and the Time-Varying Risk-Premium Relation

As suggested by Lo (2004), preferences, the relative size of various traders and certain other factors, such as tax laws, regulatory environment, lead to unstable risk-premium relationships. In this part of the study, along with testing the contrarian effect, we aim to test whether there exists an unstable relationship between risk and reward within the contrarian anomaly framework. Particularly, from contrarian anomaly perspective, the fluctuations in risk-adjusted profits of contrarian portfolios and the time-varying factor loadings on various factors of risk may justify the unstable risk-reward relationship.

To attain the risk-adjusted contrarian profits (α values), we employ the Capital Asset Pricing Model (CAPM) and Fama and French three-factor model (FFTM), as defined by equations (4) and (5). Where, LMW t represents the contrarian portfolio return at month t, while RMKT, RSMB, and RHML, respectively denote the market, size, and value factors from Fama and French (1993).

Empirical Results and Discussion

Profitability of the Contrarian Strategy

Before investigating the risk and reward relationship, the preliminary findings of research confirm a statistically significant contrarian effect in all the emerging markets. Table 2 provides the excess returns to the winners, losers and contrarian portfolios during the entire study period (January 1997–December 2018), while Table 3 reports the results during crises periods (January 1998–December 1999 and October 2007–September 2009). Mean raw and risk-adjusted (CAPM-based) contrarian returns are provided in percentage form. As shown in Table 2, both mean raw and risk-adjusted returns are positive for all the sample countries, with the highest raw (risk-adjusted) contrarian returns in India with 3.30% (3.07%) and lowest in Bangladesh with 0.20% (0.06%). Both raw and risk-adjusted returns are significant for India and Pakistan.

Contrarian Strategy Returns.

Note. This table provides the findings of country-specific contrarian profits over the whole sample period (from January 1997 to December 2018). At the end of every month (t), the stocks are classified into winners and losers portfolios based on past 12-month cumulative returns. The stocks having positive (negative) prior returns during the formation period t–12 to t–1 are categorized as winner and loser stocks. Contrarian profits represent the subsequent returns at (t + 1) month holding period, calculated as the difference in return between the equally weighted loser and winner portfolio (LMW). CAPM-alpha denotes the Risk-adjusted returns. In parentheses are the values of robust t-statistic that are adjusted for heteroskedasticity and autocorrelation based on Newey and West (1987). *, **, and *** denote the significance level at 10%, 5%, and 1%, respectively.

Contrarian Returns During Crisis Periods.

Note. This table provides country-specific contrarian strategy returns during crisis periods, consisting of 48 months. At the end of every month (t), the stocks are classified into winners and losers portfolios based on past 12-month cumulative returns. The stocks having positive (negative) prior returns during the formation period t–12 to t–1 are categorized as winner and loser stocks. Contrarian profits represent the subsequent returns at (t + 1) month holding period, calculated as the difference in return between the equally weighted loser and winner portfolio (LMW). CAPM-alpha denotes the risk-adjusted returns. In parentheses are the values of robust t-statistic that are adjusted for heteroskedasticity and autocorrelation based on Newey and West (1987). *, **, and *** denote the significance level at 10%, 5%, and 1%, respectively.

Interestingly, the contrarian strategies yield significantly higher profits during crises periods, twice or even more as compared to non-crises periods. Table 3 provides the returns during the crises periods, where the highest mean (risk-adjusted) return is again in India with 4.62% (4.48%) and lowest in Bangladesh with 0.63% (0.25%). The raw (risk-adjusted) profits are significant for all the countries during crises periods. It is apparent that contrarian portfolios show varying performance patterns over time. In the next section, we will conduct further investigation on this issue.

We next turn to study the risk-reward relationship by evaluating the performances of contrarian portfolios under the CAPM and FFTM. Table 4 reports the findings for different countries over the whole sample period 1997 to 2018. The slopes of regression βMKT, βSMB, and βHML represent the corresponding loadings on the market (RMKT), size (RSMB), and value (RHML) factors.

Adjusted Returns Under CAPM and Fama-French Three-Factor Model.

Note. This table provides the risk-adjusted profits of contrarian portfolios (α value) obtained from CAPM and Fama-French three-factor model. It also provides factor loadings of various factors of risk (e.g., βMKT, βSMB, βHML). The values of robust t-statistic are in parentheses that are adjusted for heteroskedasticity and autocorrelation on the basis of Newey and West (1987). *, **, and *** denote the significance level at 10%, 5%, and 1%, respectively.

We first analyze the findings based on CAPM model. As reported in Table 4, the risk-adjusted profits (α values) of contrarian portfolios are only marginally reduced compared to the raw returns over the entire sample period in Table 2. The addition of the market risk factor (RMKT) does not significantly reduce the contrarian returns. Moreover, risk-adjusted contrarian profits are positive in all the countries but significant only for India and Pakistan. However, the loadings on market risk factor are significant only for Pakistan. In general, the CAPM lacks the power to interpret the profits of contrarian portfolios. We next move to check the results of the FFTM. The risk-adjusted profits under the FFTM are considerably lower for all the countries. They become statistically insignificant for Pakistan and Bangladesh, indicating that the FFTM has a strong power in explaining the contrarian effect compared to the CAPM. Overall, the market risk factor loadings (βMKT) are positive and significant for Pakistan, while the value factor loadings (βHML) are positive for India. For Bangladesh, the risk-adjusted profits and the factor loadings (βMKT) of the market risk factor are negative but insignificant. The results of the FFTM are mixed. Insignificant and significant risk-adjusted contrarian profits are obtained across countries. Moreover, the magnitude of raw and risk-adjusted returns differs during the crises periods, as shown in Table 3. These findings, consistent with AMH (Lo, 2004), imply that there is possibly the time-varying risk-reward relationship in the form of contrarian effect in South Asian emerging markets.

Our results also raise questions on the standard procedures used in several prior studies, where constant factor loadings are applied for various risk factors by applying time-series regression throughout the whole study period (Fama & French, 2012, 2017; Liew & Vassalou, 2000; Subrahmanyam, 2010). The results may be misleading if factor loading dynamics are not incorporated in traditional risk-adjustment processes. Theoretically, factor loadings are certainly time-varying and depending on the formation frequency of contrarian or momentum portfolios, as suggested by Wang and Wu (2011). As per the authors, individual stock returns are produced through FFTM with constant factor loadings, but the monthly formation of contrarian portfolios applied in most of the studies require different loser and winner stocks each month. While the factor loadings on various risk components for contrarian portfolios are average loadings of individual stocks in the sample, thus resulting in risk factor loadings that fluctuate over time. Moreover, it is natural that loser (winner) portfolios are formed with those stocks that have generally lower (higher) risk factor loadings if the premium on risk factors show positive profits, whereas stocks with higher (lower) risk factor loadings are chosen for the loser (winner) stocks in case the premium has negative profits. Therefore, the loadings on various risk factors will co-vary with respective premium of risk factors in a time-varying nature.

Impact of Changing Market Conditions on Contrarian Payoffs

In order to examine the hypothesis originated from AMH that the varying stock market conditions are the primary reasons of time-dependent market efficiency, this study moves to investigate the behavior of contrarian profits in changing market states (POSITIVE/NEGATIVE) with volatility (HIGH/LOW) clustering within each state of the market. The market state (or direction) plays a crucial role in momentum (contrarian) profitability (Cooper et al., 2004). To achieve this goal, we split the overall sample period in four groups based on market state and volatility pairs. As previously stated, a month is considered to be in a POSITIVE (NEGATIVE) market condition if the prior 12-month return on market index is positive (negative). Every market state is further subdivided into HIGH (LOW) volatility subgroups. A month is treated as in HIGH (LOW) volatility condition in cases where the prior 6-month volatility of market index is larger (smaller) than the prior 12-month index volatility.

The analysis regarding contrarian payoffs reported in Table 5 advocates that both market state and volatility factors are important in explaining contrarian profitability. The higher mean raw and risk-adjusted contrarian returns are obtained in negative market state with higher market volatility. Moreover, the mean return spread between the negative and positive market states with higher market volatility is as high as 6.78% (6.958–0.175), 5.309% (3.607– [–1.432]) and 3.837% (7.298–3.461) for Pakistan, Bangladesh, and India, respectively. The mean and risk-adjusted returns of negative (high volatility) states are both economically and statistically significant compared to other market states. Furthermore, we see a more pronounced effect of market state (POSITIVE/NEGATIVE) that all the combinations in the negative market state consistently outperform their counterparts in the positive market state. However, the volatility effect is found to be slightly less pronounced and asymmetric within each market state (POSITIVE/NEGATIVE) as in one exception under the positive market state of BSE, the lower volatility months generate higher contrarian returns than higher volatility months by 1.312% (4.773–3.461) and 1.46% (4.52–3.06) after risk-adjustment. Apart from this deviation, all the markets show a consistent pattern that the months with higher volatility outperform the months in lower volatility in each market state. The less pronounced volatility impact across each market state indicates the more dominant role of market state than market volatility in the predictability of contrarian strategy payoffs in emerging markets. These findings contradict the results of the U.S equity market, where the volatility factor acts as the primary predictor of momentum strategy payoffs (Wang & Xu, 2015). This variation can be explained through the structural changes in return dynamics among developed and emerging equity markets. Overall, from the point of view of investors, we can suggest that higher profits can be achieved by making contrarian style portfolios in negative market state with higher market volatility. The unreported results provide similar conclusions based on lagged 24-month and 36-month market state and volatility factors.

Market State, Volatility, and Contrarian Strategy Payoffs.

Note. This table report the effect of changing market conditions on contrarian payoffs. At the end of every month (t), the stocks are classified into winners and losers portfolios based on past 12-month cumulative returns. The stocks having positive (negative) prior returns during the formation period t–12 to t–1 are categorized as winner and loser stocks. Contrarian profits represent the subsequent returns at (t + 1) month holding period, calculated as the difference in return between the equally weighted loser and winner portfolio (LMW). A month is treated as in POSITIVE (NEGATIVE) state in cases where the prior 12-month return on market index is positive (negative). A month is treated as in HIGH (LOW) volatility condition in cases where the prior 6-month volatility of market index is larger (smaller) than the prior 12-month index volatility. CAPM-alpha denotes the risk-adjusted returns. In parentheses are the values of robust t-statistic that are adjusted for heteroskedasticity and autocorrelation based on Newey and West (1987). *, **, and *** denote the significance level at 10%, 5%, and 1%, respectively.

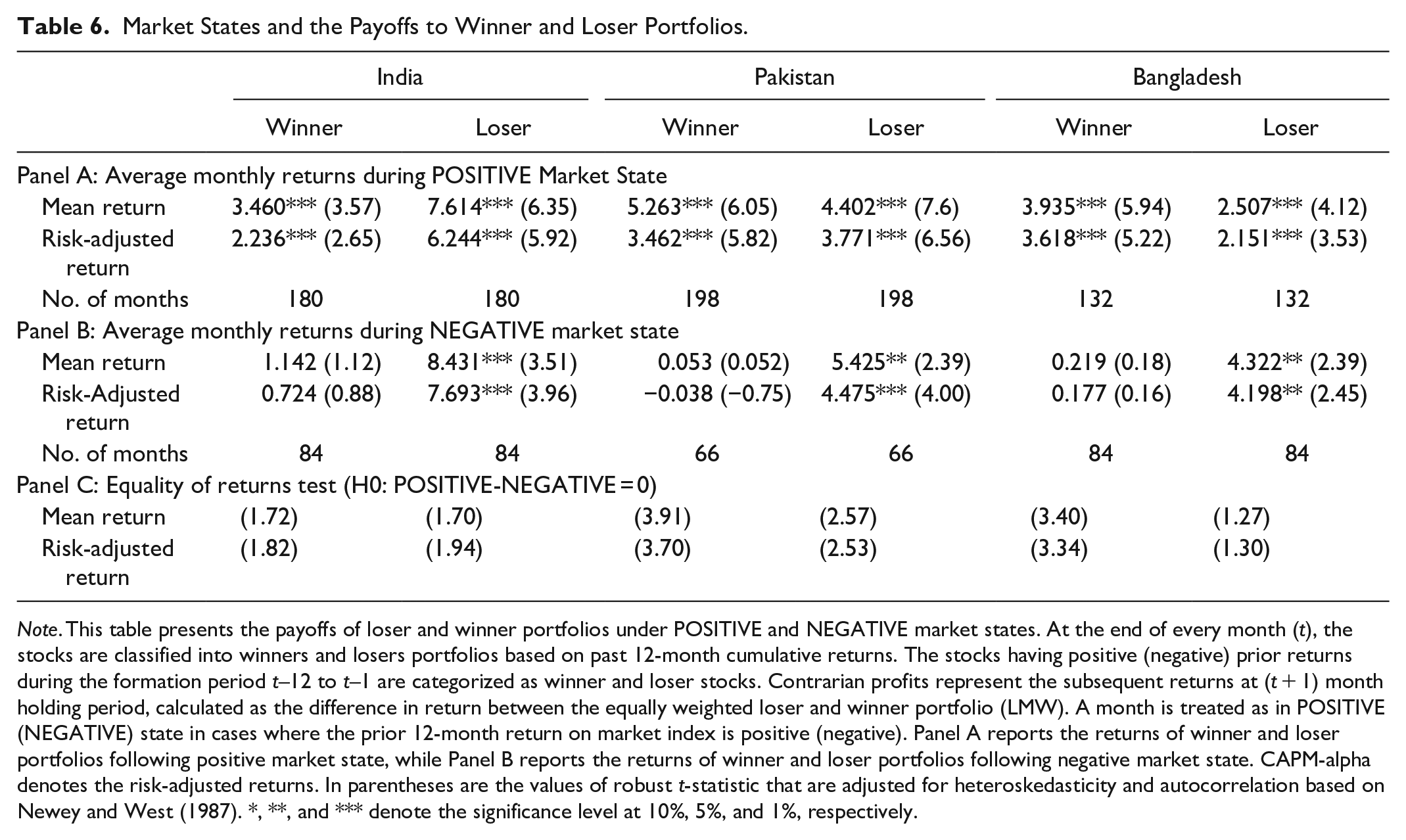

We get more insights by examining the payoffs of loser and winner portfolios within the positive and negative market state. Table 6, Panels A and B provide the results of contrarian payoffs to loser and winner portfolios under negative and positive market states. We can observe that higher contrarian returns are primarily associated with the outperformance of loser portfolios, particularly during negative market states. Following the negative market state, the loser portfolios generate significantly higher mean raw (risk-adjusted) returns of 8.43% (7.69%), 5.42% (4.47%), and 4.32% (4.19%), respectively for India, Pakistan, and Bangladesh. The same trend was observed during crisis periods (Table 3) that the higher ex-ante expected returns of contrarian strategy during crises periods were mainly due to the higher payoffs attached to the past loser (neglected) stocks. These results comply with the latest findings of Daniel and Moskowitz (2016), who state that, specifically in panic and higher volatility states, the momentum investment strategy crashes which is contemporaneous with stock market rebounds.

Market States and the Payoffs to Winner and Loser Portfolios.

Note. This table presents the payoffs of loser and winner portfolios under POSITIVE and NEGATIVE market states. At the end of every month (t), the stocks are classified into winners and losers portfolios based on past 12-month cumulative returns. The stocks having positive (negative) prior returns during the formation period t–12 to t–1 are categorized as winner and loser stocks. Contrarian profits represent the subsequent returns at (t + 1) month holding period, calculated as the difference in return between the equally weighted loser and winner portfolio (LMW). A month is treated as in POSITIVE (NEGATIVE) state in cases where the prior 12-month return on market index is positive (negative). Panel A reports the returns of winner and loser portfolios following positive market state, while Panel B reports the returns of winner and loser portfolios following negative market state. CAPM-alpha denotes the risk-adjusted returns. In parentheses are the values of robust t-statistic that are adjusted for heteroskedasticity and autocorrelation based on Newey and West (1987). *, **, and *** denote the significance level at 10%, 5%, and 1%, respectively.

Furthermore, de Groot et al. (2012) and Blitz et al. (2011) report the similar reversal effects during crisis periods while testing the various stock selection strategies on emerging and developed markets. The possible interpretation for higher contrarian returns during the down-market state or crash period could be that investors search for safe heavens during these times and shift their positions to those winner (quality) stocks that hold higher credit rating. In comparison, the prevalent pessimism against loser stocks pushes their values too low, exaggerating their risk and reducing the probability of gains for those stocks. Subsequently, as the economy recovers and adjusts the prices of under-priced and overpriced shares, the loser stocks then outperform. Hence, the investment strategy of buying the depressed stocks at low price and selling them when they regain yields substantial future profits.

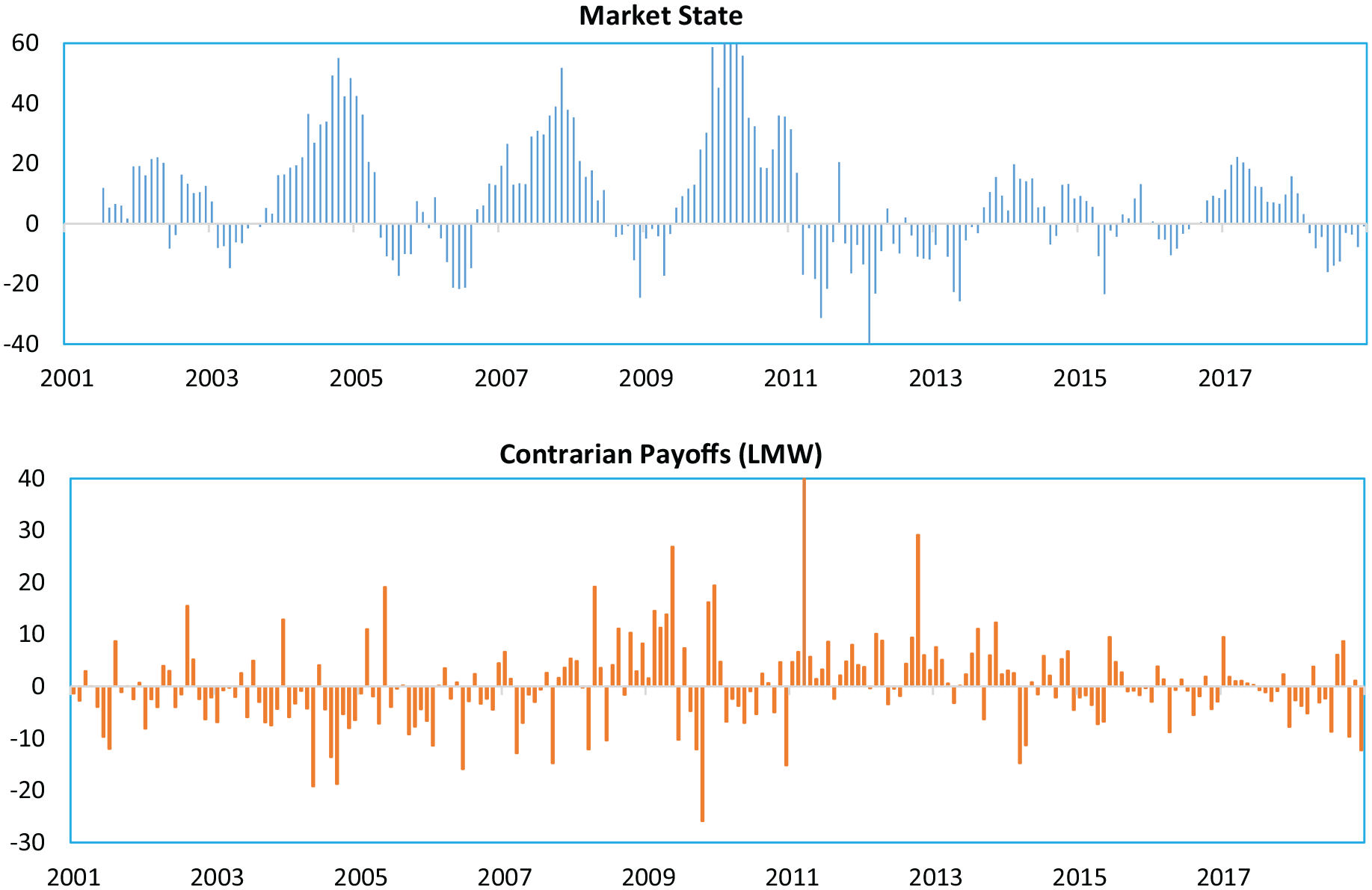

The time-varying nature of contrarian payoffs during different market states can also be observed in Figures 1 to 3, respectively, for Pakistan, Bombay and Dhaka stock exchanges. We can see the hikes in contrarian strategy profits during negative states in Pakistan stock exchange, specifically during the Asian financial crisis over January 1998 to December 1999, then at the start of 2001 to 2002 and later in the times of global crisis, where there are considerable positive hikes in contrarian strategy payoffs. Similar patterns of higher contrarian returns can be seen in the Indian stock market during the Asian financial crisis and after the global crisis. The same trend is present during the stock market crash of the Bombay stock exchange from the beginning of 2001 till the end of 2002. This period was one of the worst periods for the Indian stock market when the actions of some stock market brokers caused the whole market to crash by 21% in March 2001 (Azad et al., 2014). Finally, the hikes in contrarian payoffs in the Bangladeshi stock market can be found at the end of the global financial crisis in 2009, then from the beginning of 2011 till mid-2013, representing a period of Bangladeshi share market scam which exacerbated due to government failure. The market fell by 10% in January 2011 and then further 30% in February 2011 (Chowdhury, 2011). Our findings in this section provide ample support to the argument that the performance of stock market anomalies evolve over time; therefore, the AMH should be taken into account when explaining the behavior of such market anomalies.

Market state and contrarian payoffs (LMW) in Pakistan.

Market state and contrarian payoffs (LMW) in India.

Market state and contrarian payoffs (LMW) in Bangladesh.

We next conduct a similar analysis for six other major emerging markets of the Asian region. The findings are reported in Figure 4. For the Malaysian stock market, the contrarian effect strengthens from 1997 to 1998, possibly during the Asian Financial Crisis, spikes again during the year 2001, disappears from 2006 to 2008 and appears again from the mid of 2008 to 2009 during the downturn of the stock market. Similar peaks in contrarian payoffs during the negative market states can be found in Korea Stock Exchange from 1997 to 1998, during the year 2001, then in 2003 and finally during the global crisis from September 2008 to August 2009. For Chinese equity market, we see a combination of momentum and contrarian effects from 1997 to 1998, strong momentum effect from 1999 to 2000, strong contrarian effects during the market crash from 2008 to 2009 and finally, during the negative market state in 2016. For other major stock markets of the region, we again witness the wax, and wane in the contrarian effects across market states.

Market state and time-variation in contrarian payoffs in other major emerging markets.

Context-Dependent Contrarian Effects—Evidence From Augmented FFTM

To mitigate the impact of various risk factors, we again run the pricing model with the addition of market condition dummies to identify a more accurate relationship between contrarian profitability and stock market conditions (Kim et al., 2011; Taylor, 2014). This analysis also helps in testing the robustness of our previous study findings. Specifically, we employ the augmented FFTM, as shown in equation (6). Where, LMWt represents the contrarian portfolio return at time t, while RMKT, RSMB, and RHML respectively denote the market, size, and value factors from Fama and French (1993). Dt represents the dummy variable of specific market conditions, which takes the value one or zero at time t. We employ various indicators of stock market conditions that are repeatedly used in existing literature (Taylor, 2014; Umutlu et al., 2010), such as market state, volatility and crisis periods (e.g., Asian crisis and global financial crisis).

Market state dummy takes the value one (zero) if the past 12 month return on market index is negative (positive) at month t. Likewise, the market volatility dummy takes the value of one (zero) if the prior 6-month market index volatility is higher (lower) than the prior 12-month market index volatility at month t. The Asian financial crisis occurred between 1998 and 1999, its dummy variable receives the value one in the months from January 1998 to December 1999, while zero otherwise (see e.g., Umutlu et al., 2010 for prescribed length of Asian crisis period). The global crisis, which occurred between 2007 and 2009, its dummy variable takes the value of one in the months from October 2007 to September 2009, while zero otherwise.

Table 7 provides the findings of regression equation (6). As per the findings in panel A based on market state, the risk-adjusted contrarian returns are positively significant only for India but negatively insignificant for Pakistan and negatively significant for Bangladesh. Interestingly, the risk-adjusted returns of contrarian portfolios are lower than their corresponding raw returns in all the countries. Notably, there are positive and significant loadings on the dummy factor of market state in all the countries, indicating the better performance of contrarian portfolios under the periods with negative trends of the market. Panel B provides the findings on the basis of market volatility. The risk-adjusted profits are again lower than their respective raw returns, significant only for the Indian stock market while insignificant and negative for Pakistani and Bangladeshi stock markets. Notably, there are positive but insignificant loadings on the dummy factor of market volatility for Pakistan and India, while negative and insignificant for the Bangladeshi stock market. In comparison, the larger and more significant factor loadings on market state dummies reveal the more dominant effect of market state instead of market volatility, which again supports our prior finding that the market state instead of market volatility is more likely the primary source of contrarian profitability in emerging stock markets.

Context-Dependent Contrarian Effects—Evidence From Augmented FFTM.

Note. This table exhibits contrarian portfolio performance on the basis of three-factor model of Fama and French by including various dummies of stock market conditions, namely,

Panel C and D provide the findings based on the periods of Asian financial Crisis and Global Crisis, respectively. For all the countries, loadings on Asian crisis dummies are highly positive and significant, indicating the strong impact of Asian crisis on contrarian strategy returns. However, the effect of global crisis on contrarian payoffs is unclear as the loadings on global crisis dummies are either small or negative and insignificant for all the sample countries. The large and significant coefficients of the Asian financial crisis dummies reveal its more dominant impact on the market efficiency of South Asian emerging markets compared to the global crisis. These results comply with the findings of previous researches in developed markets. Kim et al. (2011) reveal that the return predictability of momentum investment strategies are higher during stock market bubbles as compared to normal market conditions, while the stock market crashes are considered the worst times for momentum profits (Asness et al., 2015; Daniel & Moskowitz, 2016).

According to the overall study results based on various viewpoints, contrarian profitability is vastly dependent on varying conditions of the stock market. The periods with negative state of the market, higher stock market volatility and the Asian financial crisis relate to higher contrarian profitability. The relationship between contrarian profitability and varying market conditions holds even after enabling for the effect of known risk factors.

Conclusion

In the existing literature of the efficient market hypothesis (EMH), technical anomalies like momentum and contrarian investment strategies are always considered tricky to be fully interpreted by the EMH. This study examines the impact of changed market conditions on time-series predictability of contrarian profitability in South Asian emerging markets, which is also considered the leading cause of time-dependent market efficiency as per the adaptive market hypothesis (AMH). In the empirical analysis, the study specifically focuses on the emerging markets of the South Asian region as the stock price are mean reverting, returns are non-random, while the manipulative and speculative bubbles are persistent issues in these markets. The sample countries include India, Pakistan, and Bangladesh.

The preliminary findings confirm that a strong and significant contrarian effect holds in all the emerging markets. The results based on CAPM and three-factor Fama and French model demonstrate the time-varying nature of risk-adjusted returns, while the loadings of various factors of risk are non-constant. These findings are consistent with AMH. We then investigate the relationship between contrarian payoffs and stock market conditions. The study findings reveal that contrarian returns strengthen during negative market state, higher market volatility and crises periods, particularly during the Asian financial crisis. In line with the results of Wang and Xu (2015), the research confirms the presence of a significantly negative relationship between market state and a positive association of stock market volatility with contrarian payoffs. However, in contradiction with their findings, the market state factor instead of market volatility, serves as a primary source of contrarian payoffs in emerging markets. According to the overall study results based on various viewpoints, contrarian profits are highly dependent upon changing stock market conditions. The relationship between contrarian profitability and varying market conditions holds even after controlling for the effect of known risk factors.

The overall empirical results of this study offer partial support to AMH, which considers the changing market conditions as the primary reasons of time-dependent market efficiency in the shape of higher returns of stock market anomalies. However, another significant result of this research implies that investors in South Asian emerging markets, like investors in the developed markets, could not respond to evolving market conditions. Therefore, contrarian return opportunities frequently arise over time, and persistent weak-form market inefficiencies exist in these markets. Our findings provide alternative evaluation matrices to investors and fund managers by suggesting that a contrarian strategy generally outperforms in South Asian emerging markets, could be employed particularly during negative market states, higher volatilities, and crisis periods in order to generate higher returns.

Implications, Limitations, and Suggestions for Future Research

Amongst some of the repercussions of this study is that researchers and analysts can use evidence provided in this study to support their argument that emerging economies suffer from structural issues and investor behavioral characteristics are distinctive. These issues and characteristics are conducive for allowing speculative and noise trading to thrive which will ultimately be detrimental to investors. Furthermore, the herd-like behavior and lack of sophistication among retail investors during periods of recessions and high levels of uncertainty could potentially lead toward a high degree of destruction and devaluation of the value of investor portfolios. If left unchecked in the long run, the resultant market inefficiencies could lead toward an insipid market where potential investors are less than willing to participate in the stock market.

One of the practical implications of this study is that there are investment opportunities for investors and fund managers investing in emerging economies. Investors need to focus on emerging market economies which exhibit stock characteristics suitable to generate contrarian returns and should time their investments for periods of negative market conditions with high market volatility. This is also a viable alternative for international investors who want to participate in sophisticated developed markets but can’t build contrarian-style portfolios in their own markets. Stock markets in developed economies tend to exhibit momentum returns for investors and provide fewer contrarian portfolio returns especially during recessions.

Policy makers in developing economies could use results of this study as further evidence that there are structural issues that need to be addressed in these countries in order to reduce possibilities of investors taking advantage of market imperfections, which leads toward possible speculative and manipulative activities performed by informed stock market participants. In essence, markets that are more efficient would attract fewer manipulative activities and would encourage greater participation of investors in the long run.

The study has been limited to South Asian economies which suffer from structural issues and imperfect market conditions. An extension of the study to include other countries that exhibit similar structural dynamics would be beneficial. Furthermore, a study on the factors that contribute toward market inefficiencies and their effect on contrarian returns in these emerging economies would also be useful, both from an investment management point of view as well as from a policy making perspective.

Finally, future research can further shed light on the debate by looking into the outperformance of other investment strategies like value, growth or dynamic momentum strategy evidenced in relatively more developed markets, whether the return series of these stock selection strategies exhibit the same pattern as reversals under varying stock market conditions.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.