Abstract

This study explores how digital transformation influences the ability of Vietnamese commercial banks to generate liquidity, utilizing panel data from 2007 to 2022. We adopt rigorous econometric methodologies, including dynamic panel models estimated via the generalized method of moments (GMM) and instrumental variable (IV) techniques, to address potential endogeneity. The analysis reveals that digital innovation in banking significantly boosts liquidity provision through assets, liabilities, and off-balance-sheet instruments. Moreover, the four facets of digitalization—technological infrastructure, skilled personnel, internal system upgrades, and online customer interfaces—all exhibit positive effects on liquidity creation. These outcomes remain robust after applying multiple econometric strategies to mitigate endogeneity concerns. Heterogeneity analysis indicates that banks with diverse operations benefit more from digital advances in terms of liquidity generation. Furthermore, the relationship between digitalization and liquidity creation intensifies in more competitive banking environments and becomes particularly evident during the COVID-19 pandemic, whereas the global financial crisis does not notably alter this linkage.

Plain Language Summary

This study explores how digital transformation in banks affects their capacity to produce liquidity—that is, how banks support the flow of money in the economy. It uses data from Vietnamese commercial banks between 2007 and 2022. The findings show that when banks adopt digital tools, improve technology, train employees, upgrade internal systems, and offer online services, they create more liquidity. The study applies advanced statistical methods to ensure the results are accurate and not affected by hidden biases. It finds that the effect of digitalization is stronger for institutions that are more diversified in their operations. The effect also becomes more noticeable in competitive banking environments and amid the COVID-19 pandemic. In short, the research shows that digitalization helps banks contribute more effectively to the economy, especially when they operate in fast-changing or challenging conditions.

Introduction

In the wake of global crises such as the COVID-19 outbreak, which accelerated the implementation of digital tools across sectors, digital transformation has garnered renewed attention. As a pillar of macro-financial resilience, the banking system has also been affected by these changes. Studies indicate that digitalization may improve banks’ efficiency in operations and enhance risk management. For example, Y. Wang et al. (2021) emphasize its role in improving risk control and reducing financial intermediation costs, while Sheng (2021) notes that digitalization facilitates credit services. Research by Ren et al. (2024) and Chhaidar et al. (2023) similarly shows a positive link connecting digital advancement to improved profitability in banks. However, the benefits of digitalization also come with risks. Zhao et al. (2024) warn that excessive digital investments can increase systemic risk, and Khattak et al. (2023) caution that diversification driven by digitalization may heighten risk-taking. These mixed findings underscore the dual nature of digital transformation in banking—while it enhances performance, it must be carefully managed to mitigate risks. As such, further research is needed to fully understand its impact on banks.

Within the research strand on digital transformation, recent work has increasingly examined its influence on banks’ ability to generate liquidity. This area is crucial since generating liquidity represents a fundamental role of banks (Berger & Bouwman, 2009). Banks generate liquidity within their financial statements by transforming readily available liabilities, like deposits, into less liquid assets, including business-related loans, thereby facilitating investments and supporting economic transactions (Bryant, 1980). Beyond their balance sheets, banks provide funding flexibility through mechanisms such as credit commitments, allowing businesses and consumers to plan for future expenditures, thus contributing to economic stability and growth (Kashyap et al., 2002). It is important to note that the more liquidity a bank creates for the economy, the less liquid and potentially more risky the bank itself becomes (Berger & Bouwman, 2009). Empirical studies confirm the role of liquidity generation in supporting efficient distribution of resources, long-term investments, and economic progress, especially in bank-based financial systems (Berger & Sedunov, 2017). The critical role of liquidity creation becomes even more evident during financial crises, highlighting banks’ essential function in maintaining macroeconomic stability (Berger & Bouwman, 2017). Current research examines various factors that influence bank liquidity creation, including bank-specific characteristics, market conditions, and macroeconomic environments (Dang, 2020; Dang & Huynh, 2022; Evans & Haq, 2022; Hsieh et al., 2024; C. W. Wang et al., 2022; Yeddou & Pourroy, 2020).

Accordingly, the literature presents mixed evidence on how technological adoption affects liquidity creation. It is argued that digital transformation enhances liquidity creation by broadening customer bases, optimizing services to serve customer needs, and enabling better risk management. But, digital transformation could hurt liquidity creation by causing operational risks, increasing technological costs, and boosting careful lending activities due to improved screening and monitoring quality. Empirically, several studies underscore the positive link between bank fintech and liquidity. In detail, Fang et al. (2023) and Guo and Zhang (2023) find that greater fintech innovation within banks significantly raises their liquidity created, drawing on data from Chinese banks. Xu and Yang (2024) also highlight that digital transformation in Chinese listed banks can improve liquidity creation, particularly in larger institutions. However, contrasting evidence comes from Wu et al. (2024), who demonstrate a negative nexus between fintech adoption and liquidity production in US financial institutions. While these studies focus on bank fintech, which are technological innovations developed or adopted by traditional banks, other studies examine non-bank fintech, which involves financial technology developed by non-bank entities such as fintech companies. These entities often compete with traditional banks, potentially reducing their role in financial intermediation. For example, Tang et al. (2024) and Hao et al. (2023) show that the broader fintech industry outside traditional banking can inhibit banks’ ability to create liquidity.

This research adds to existing knowledge by broadening the scope of analysis regarding how digital transformation influences bank-generated liquidity. Compared to previous research, this study introduces several novel aspects. Previous research has examined digital transformation primarily through the lens of fintech (Fang et al., 2023; Guo & Zhang, 2023; Wu et al., 2024), yet these studies often emphasize the technological aspect, potentially overlooking the broader scope of banks’ overall digital transformation. Digital transformation aims to leverage technology to significantly improve organizational performance (Naimi-Sadigh et al., 2022), requiring both technological advancements and the active involvement of skilled employees and effective processes. Therefore, successful digital transformation hinges on a combination of technology infrastructure, human capital, and technological progress (Nadkarni & Prügl, 2021). Additionally, prior studies have typically measured fintech by employing text analysis of banks’ annual reports (Fang et al., 2023; Guo & Zhang, 2023; Wu et al., 2024). The language utilized in these reports primarily reflects their intentions and strategic plans for digital transformation, rather than the actual extent of their digital advancement (Q. Wang & Du, 2022). To overcome this limitation, we construct a bank-level digitalization metric based on the information and communication technology (ICT) index, which follows the structure of the E-Government Development Index and is prepared and published by Vietnam’s Ministry of Information and Communications (MIC). This ICT-based index is a multi-dimensional indicator composed of standardized subcategories including digital infrastructure, human capital, internal systems, and online banking platforms.

This study is closely related to the work of Xu and Yang (2024). However, our research advances theirs in several key ways, making significant contributions to the literature. First, while Xu and Yang (2024) focus only on overall liquidity creation, our study examines both total and specific components of liquidity creation. This deeper analysis provides more nuanced insights into how digital transformation impacts various aspects of banks’ liquidity functions. Second, we extend the analysis by incorporating bank-, industry-, and country-level moderating factors. By integrating these three perspectives—specifically, bank diversification, industry competition, and macroeconomic shocks—we can gain a deeper and more nuanced insight into the determinants that shape the effectiveness of digitalization efforts in enhancing banks’ ability to generate liquidity. We compare the effects of two distinct crises, namely, the 2008 global financial downturn and the COVID-19 outbreak, highlighting how different shocks influence the digitalization-liquidity creation link. These tests offer crucial insights for policymakers and bank managers and emphasize the need to customize digital transformation initiatives based on contextual factors. Third, this study uses an inclusive dataset covering all commercial banks, regardless of whether they are publicly listed, while Xu and Yang (2024) limit their analysis to listed banks, which may not fully capture the diversity of bank behaviors and their responses to technological transformation across the wider banking system. Fourth, we rigorously tackle the endogeneity problem, which Xu and Yang (2024) ignore.

To explore how digital transformation influences the ability of commercial banks to generate liquidity, we look into the case of Vietnam. This country offers a compelling context to address the research issue. Accordingly, Vietnam is a bank-based market, where banks play a central role in the country’s financial intermediation process (Huynh, 2024). Unlike more developed economies with well-established capital markets, Vietnam’s economic growth is heavily reliant on the liquidity created by banks (Dang & Huynh, 2022). This strong dependence on bank-generated liquidity means that any changes in how banks create liquidity, especially through digital transformation, can have profound implications for the entire economy. Furthermore, digital transformation in Vietnam has been progressing rapidly, with the Vietnamese government prioritizing it as a key driver for maintaining economic growth (Q. K. Nguyen & Dang, 2023). Vietnam is widely acknowledged as one of the leading countries in Southeast Asia in terms of rapid digital economic expansion, with projections that by 2030, the digital sector could contribute 30% to the country’s GDP (Vo et al., 2024). As part of this initiative, the government has taken a proactive stance in promoting digital transformation within the banking industry. While doing this, the Vietnamese government is a pioneer in establishing a set of digital transformation indexes for commercial banks to help them gauge their progress (Hoque et al., 2024). Despite these advancements, Vietnam’s digital transformation still trails behind that of more developed nations. In 2022, the country ranked 63rd out of 113 global economies in a digital readiness index compiled by the Asian Development Bank. Key obstacles include limited financial resources for smaller banks to adopt digital technologies fully and a shortage of highly skilled IT professionals in the banking industry (Q. K. Nguyen & Dang, 2023). These constraints make Vietnam an interesting case study for understanding how digital transformation impacts bank liquidity creation.

This study conducts empirical work drawing on data from Vietnamese commercial banks spanning 2007 to 2022. The ICT-based index is used as a measure for banks’ level of digital transformation, and the extent of liquidity creation is assessed by categorizing banking operations into liquid, semi-liquid, and illiquid types to estimate total liquidity provided by banks. Several econometric strategies are utilized to address potential endogeneity concerns. Our analysis shows that digitalization markedly boosts liquidity generation across multiple categories, including assets, liabilities, and items off the balance sheet. The results demonstrate a clear positive relationship between all four components of digital advancement and the overall capacity of banks to generate liquidity. While revealing that bank digital transformation significantly enhances liquidity creation, we further analyze and suggest that this impact varies across different dimensions and is moderated by bank-specific, industry-level, and country-level factors. This approach can tell us more about the potential channels through which digital transformation translates into bank liquidity. Accordingly, our results suggest that digital transformation has a more substantial effect on liquidity creation in banks with greater diversification, suggesting that banks with diversified income streams, assets, and funding sources are better positioned to benefit from digital advancements. Furthermore, this relationship is more pronounced in highly competitive banking markets, where the pressure to innovate accelerates the adoption of digital tools. Lastly, our results show that the favorable influence of digital transformation on banks’ liquidity generation intensified during the COVID-19 pandemic but was unaffected by the financial crisis. These findings offer important insights into how digitalization shapes liquidity generation in banks across various market and economic contexts.

Literature Review and Hypothesis Development

The literature presents two contrasting views on the linkage between bank digitalization and liquidity creation. On the one hand, it is claimed that digital transformation enhances liquidity creation by broadening customer bases, optimizing services to serve customer needs, and enabling better risk management. On the other hand, digital transformation could hurt liquidity creation by causing operational risks, increasing technological costs, and boosting careful lending activities due to improved screening and monitoring quality. Our study now discusses in detail the positive and negative mechanisms through which digital transformation can influence bank liquidity creation.

Bank digitalization has been suggested to boost liquidity creation by broadening the customer base, a critical mechanism for increasing bank deposits and lending capacity. The use of digital banking technologies, like mobile banking apps and online financial services, makes it easier for banks to reach a wider range of customers, including those in remote or underserved areas (Dadoukis et al., 2021). This expanded customer base increases deposit inflows, providing banks with more resources to support lending activities, which ultimately boosts liquidity creation (Wu et al., 2024).

In addition, digital transformation helps optimize banking services to better serve customer needs, which in turn supports liquidity creation. Through advanced data analytics and AI-driven tools, banks could customize their offerings to meet the distinct needs of each client, enhancing customer satisfaction and loyalty (Puschmann & Halimi, 2024). By offering more personalized financial solutions, banks can better attract deposits and facilitate loan offerings, which boosts liquidity creation. The ability to swiftly meet client demands and respond to changes in the market environment further strengthens a bank’s capacity to produce liquidity (Banna et al., 2021).

Moreover, digitalization plays a significant part in improving risk management, which is directly tied to liquidity creation. By leveraging big data, machine learning, and predictive analytics, banks can improve their ability to assess creditworthiness, monitor real-time market conditions, and forecast potential risks. The implementation of digital tools in risk assessment allows banks to extend their lending services to a broader array of sectors and customers while minimizing the associated risks (X. Li, 2025), thus supporting sustained liquidity creation. Importantly, it should be recognized that in case banks produce liquidity, they expose themselves to risk by decreasing their own liquidity (Berger & Bouwman, 2009). Through digital transformation, banks can enhance their ability to identify and manage risks by minimizing information asymmetry in the bank-customer relationship (Buchak et al., 2018). As a result, these advancements strengthen banks’ risk-handling capabilities, enabling them to boost overall liquidity creation, which could be seen as a risky activity.

However, we conjecture that digital transformation could reduce liquidity creation through several other mechanisms. One major drawback of bank digital transformation is the rise in operational risks. With increased reliance on technology and digital platforms, banks face heightened exposure to cyber threats, system outages, and data breaches (Yao & Song, 2023; Zhao et al., 2024). These risks can undermine their capacity to provide liquidity, as a major system failure or cyberattack could disrupt the bank’s core operations and diminish confidence among depositors and creditors.

Apart from operational risks, the high costs of digital transformation represent another challenge, particularly in an emerging economy like Vietnam. Implementing advanced technologies often requires substantial investments in infrastructure and skilled personnel (Nadkarni & Prügl, 2021). These high costs can limit banks’ ability to allocate sufficient resources for liquidity creation activities. For banks in Vietnam, where financial and technological resources may be more constrained (Q. K. Nguyen & Dang, 2023), the investment in digitalization may lead to reduced funds available for lending and other liquidity-generating activities. Moreover, maintaining and continuously upgrading these digital systems further strains the bank’s budget, possibly diverting resources away from core liquidity functions.

Digital transformation often improves a bank’s ability to screen and monitor borrowers effectively (Dadoukis et al., 2021). Enhanced data analytics and digital tools allow banks to assess credit risk with greater accuracy, reducing the likelihood of default (Z. Chen et al., 2023; Yang & Masron, 2024). However, this improved risk assessment can also lead banks to be more selective in their lending, as they may avoid lending to riskier borrowers or sectors. While this reduces non-performing loans and enhances the bank’s financial stability, it could simultaneously reduce the volume of credit available in the economy, thereby lowering liquidity creation.

After discussing the possible routes for how digital transformation affects liquidity generated through on-balance sheet activities, we should also pay attention to liquidity creation occurring off the balance sheet. For instance, as digital transformation allows banks to provide more efficient and accessible credit in the spot market, customer reliance on loan commitments and similar off-balance sheet instruments may decline (Thakor, 2005). Conversely, the complementarity between deposit services and loan commitments could lead to growth in liquidity provision through off-balance sheet channels (Kashyap et al., 2002). Digital transformation often strengthens banks’ deposit-gathering capabilities through improved customer engagement and service offerings, which in turn may induce banks to extend more liquidity via loan commitments thanks to increased loanable funds. As such, how digitalization influences off-balance sheet liquidity creation overall remains ambiguous, as it could either reduce or increase such activities depending on which effect dominates.

In summary, while digital transformation brings many opportunities, it also introduces significant challenges in the process of banks creating liquidity in the economy. Given all the above discussions, we develop two competing hypotheses for testing in this study:

Methodology

Variables of Liquidity Creation

Research on how banks generate liquidity has advanced significantly, particularly with the seminal method introduced by Berger and Bouwman (2009) for measuring the liquidity produced by banking institutions. Building on their three-step methodology, Dang (2020) and Dang and Huynh (2022) tailor the process to better fit the available data for Vietnamese commercial banks, developing a specific approach for calculating liquidity creation. In this study, we adopt this adapted method to represent the key variable of bank-created liquidity (Dang, 2020; Dang & Huynh, 2022).

Initially, we categorize banking components into liquid, semi-liquid, or illiquid groups. In a low-income country like Vietnam, certain assets are categorized as illiquid rather than semi-liquid, and some liabilities are treated as liquid rather than semi-liquid. Then, we assign specific weights: illiquid instruments like corporate loans and liquid liabilities, including customer deposits, are given a weight of 1/2, meaning that converting customer deposits into loans generates liquidity for the economy. Conversely, liquid holdings such as marketable securities and illiquid obligations plus equity are weighted at −1/2, implying that converting equity into liquid securities reduces bank liquidity generated. Assets and liabilities classified as semi-liquid receive a neutral weight of zero. Items recorded off the balance sheet, such as credit commitments and derivatives, carry the same weight as equivalent on-balance sheet positions. Finally, we calculate the weighted sums for liquidity creation on the asset component (LC Asset), the liability component (LC Liability), off-balance activities (LC Off), and the overall total, which reflects the total liquidity a bank generates through all its activities (LC Total).

Following the well-established practices in the relevant literature, we normalize these four measures by gross total assets. This normalization ensures comparability across banks of different sizes, preventing the results from being skewed by larger institutions. Detailed instructions on the step-by-step process of measuring bank liquidity creation, with some modifications to the categorization of illiquid and semi-liquid items, tailored to the context of a low-income market such as Vietnam, are given in previous studies (Berger & Bouwman, 2009; Dang, 2020; Dang & Huynh, 2022).

Variables of Bank Digital Transformation

In the existing documents, various approaches are employed to quantify digitalization. Some scholars utilize indicators such as total expenditures on technology (Khattak et al., 2023) or the valuation of non-physical assets associated with digital technologies (X. Chen et al., 2024), while others apply automated text analysis methods to analyze bank disclosures (Chhaidar et al., 2023; Fang et al., 2023; Guo & Zhang, 2023; S. Liu, Wang, et al., 2024; Shang & Niu, 2023; Tang et al., 2024; Wu et al., 2024; Yao & Song, 2023). However, such indicators are often critiqued for their limited scope, as digital transformation is multifaceted, encompassing not only technological investments but also the integration of these technologies with human resources, infrastructure, and internal business applications (Nadkarni & Prügl, 2021). Additionally, text analysis of annual reports may encounter selection bias issues, potentially compromising the objectivity of the derived index (L. Li et al., 2023).

To address these limitations, this study employs the ICT index, compiled by the MIC, to represent bank digital transformation. This comprehensive index is derived from extensive data submitted by commercial banks and evaluates multiple dimensions: technology infrastructure, human resource infrastructure, internal banking applications, and online banking services. Our digital transformation index is available at the bank level and effectively reflects the digital transformation status of nearly all commercial banks in Vietnam. The technical aspect behind this index is described in the prior study by Hoque et al. (2024).

To overcome these shortcomings, the present analysis employs the ICT index, compiled by the MIC, to represent the digital transformation of banks. This comprehensive measure is constructed using extensive data submitted by commercial banks and evaluates multiple facets, including: technological systems, skilled personnel, internal operational platforms, and internet-based banking functionalities. Our digitalization metric is available on an individual bank basis and effectively reflects the extent of digital transformation across almost all Vietnamese commercial banks.

Model

To test the effects of bank digitalization on the generation of liquidity, we employ a dynamic panel model as follows:

where i and t capture banks and years, respectively. The dependent variable

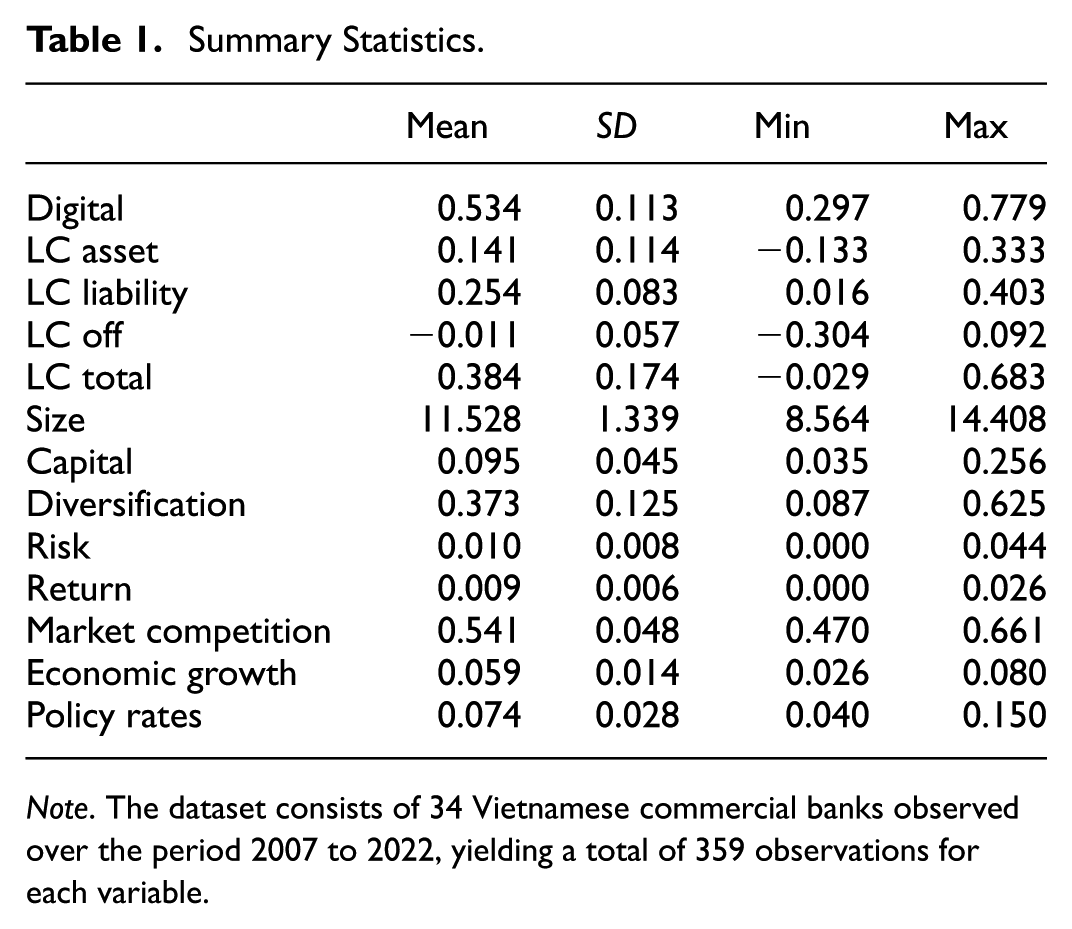

Summary Statistics.

Note. The dataset consists of 34 Vietnamese commercial banks observed over the period 2007 to 2022, yielding a total of 359 observations for each variable.

Given the potential endogeneity issues that arise from the inclusion of the lagged dependent term along with other regressors, we adopt the GMM estimator. This approach is particularly well-suited for dynamic panel data models, as it helps to address endogeneity by using instruments internally generated from the dataset. Specifically, we utilize the two-step system GMM estimator, which leverages moment restrictions for both the level and first-difference equations (Arellano & Bover, 1995; Blundell & Bond, 1998). This method enhances efficiency and reduces potential biases that may originate from weak instruments. It also effectively handles a wide range of potentially endogenous variables. In our GMM approach, the lagged dependent variable and bank-specific factors are treated as either endogenous or predetermined (using the “gmmstyle” option), while macro variables are assumed to be fully exogenous (using the “ivstyle()” option) (Roodman, 2009). When executing the “xtabond2” command in Stata, the collapse option is employed to address instrument proliferation concerns. The corrected standard error is employed to address issues related to small sample sizes (Windmeijer, 2005).

Data

Banks’ financial data are sourced from the FiinPro database, with any missing information needed for liquidity creation computation manually supplemented through financial statement notes from the respective banks. The indicators for digital transformation used in this study are derived from reports produced by the MIC, while macro data come from the International Financial Statistics (IFS) website. The sample selection process begins by including all Vietnamese commercial banks available in the FiinPro database, with the following exclusions: policy banks are removed due to differences in governance and business models, banks with missing data for key variables are excluded, and only those with a minimum of 4 years of data are retained. After applying these criteria, the final dataset consists of an unbalanced sample of 34 Vietnamese commercial banks observed from 2007 to 2022. To mitigate the influence of outliers, we winsorize continuous bank-level data at the 2.5th and 97.5th percentiles (meaning that extreme values below the 2.5th percentile and above the 97.5th percentile are replaced with the nearest values within those limits).

Table 1 displays descriptive statistics for all variables. The distribution of our liquidity variables indicates that Vietnamese banks significantly created liquidity for the economy through their core operations in the sample period (displayed by the average values of 38.4% for the LC Total). Notably, they created most of their liquidity through on-balance-sheet banking operations, as shown by the statistical distribution of three liquidity creation components. Besides, we also calculate the correlation matrix (see Appendix Table A2), which indicates that severe multicollinearity is not problematic in this analysis, as the correlation coefficients between the independent variables remain within small ranges.

Empirical Results

Baseline Results

Table 2 presents the regression results examining how bank digitalization influences different aspects of bank liquidity creation. Before presenting the estimates, we need to discuss those on the diagnostic tests, which ensure the validity of the system GMM results by meeting three key conditions: (i) Rejecting the AR(1) test’s null hypothesis, which indicates expected first-order serial correlation in the differenced error terms; (ii) Failing to reject the AR(2) test’s null hypothesis, confirming the absence of second-order serial correlation; (iii) Failing to reject the null hypothesis of the Hansen test, indicating the instruments are valid and the overidentifying constraints hold. Our results satisfy all these conditions, supporting the soundness of our model.

Main Results: Bank Digital Transformation and Liquidity Creation Components.

Note. The dependent variable (DVA) is bank liquidity creation (displayed at the head of each column). Standard errors are in parentheses.

p < .01, **p < .05, *p < .1.

We initially present a specification with the digital transformation index and fixed effects, followed by specifications that incorporate additional micro- and macro-level controls. From the results in columns 1 to 3, we observe that the digital transformation index has a consistently significant and positive coefficient across all three model versions, even after accounting for various influencing variables. This implies that banks with greater levels of digital advancement are more capable of boosting liquidity through asset management, most likely due to more effective loan processing and enhanced risk oversight. From an economic perspective, an estimate from column 3 implies that a one-standard-deviation rise in the digital transformation index (0.113) could result in a 0.008 percentage point increase in asset liquidity creation (0.113 × 0.072). This magnitude is meaningful, approximating 5.8% of the mean of LC Asset (0.141).

Turning to the next component, the results in columns 4 to 6 for liquidity creation from the liability side similarly show a clear and statistically robust influence of digital transformation. This result implies that as banks become more digitally advanced, they can manage liabilities more effectively, improving their capacity to generate liquidity from deposits and other funding sources. The digital transformation may facilitate quicker and more efficient deposit services, automate processes for managing funding flows, and enhance customer engagement, all of which contribute to stronger liability-side liquidity creation. The economic significance is also reasonable. For instance, a one-standard-deviation rise in Digital is associated with a 0.012 percentage point increase in LC Liability (0.113 × 0.105, column 6), accounting for 4.7% of the average liability-side liquidity creation (0.254).

Besides, from columns 7 to 9 of Table 2, we document that digital transformation also significantly and positively affects off-balance sheet liquidity creation. Banks having advanced digital capabilities can engage more effectively in non-balance sheet transactions, such as loan commitments, guarantees, and derivatives. Digital tools likely improve the efficiency of managing these financial products, reducing operational risks and strengthening the bank’s capacity to facilitate liquidity generation through such activities. The economic impact of digital transformation on this area of liquidity creation is similarly important. For instance, a standard deviation increase in the digital transformation index leads to a rise of 0.033 percentage points in liquidity generated from these activities (0.113 × 0.295, column 9), which is substantial compared to the standard deviation value of LC Off (0.057).

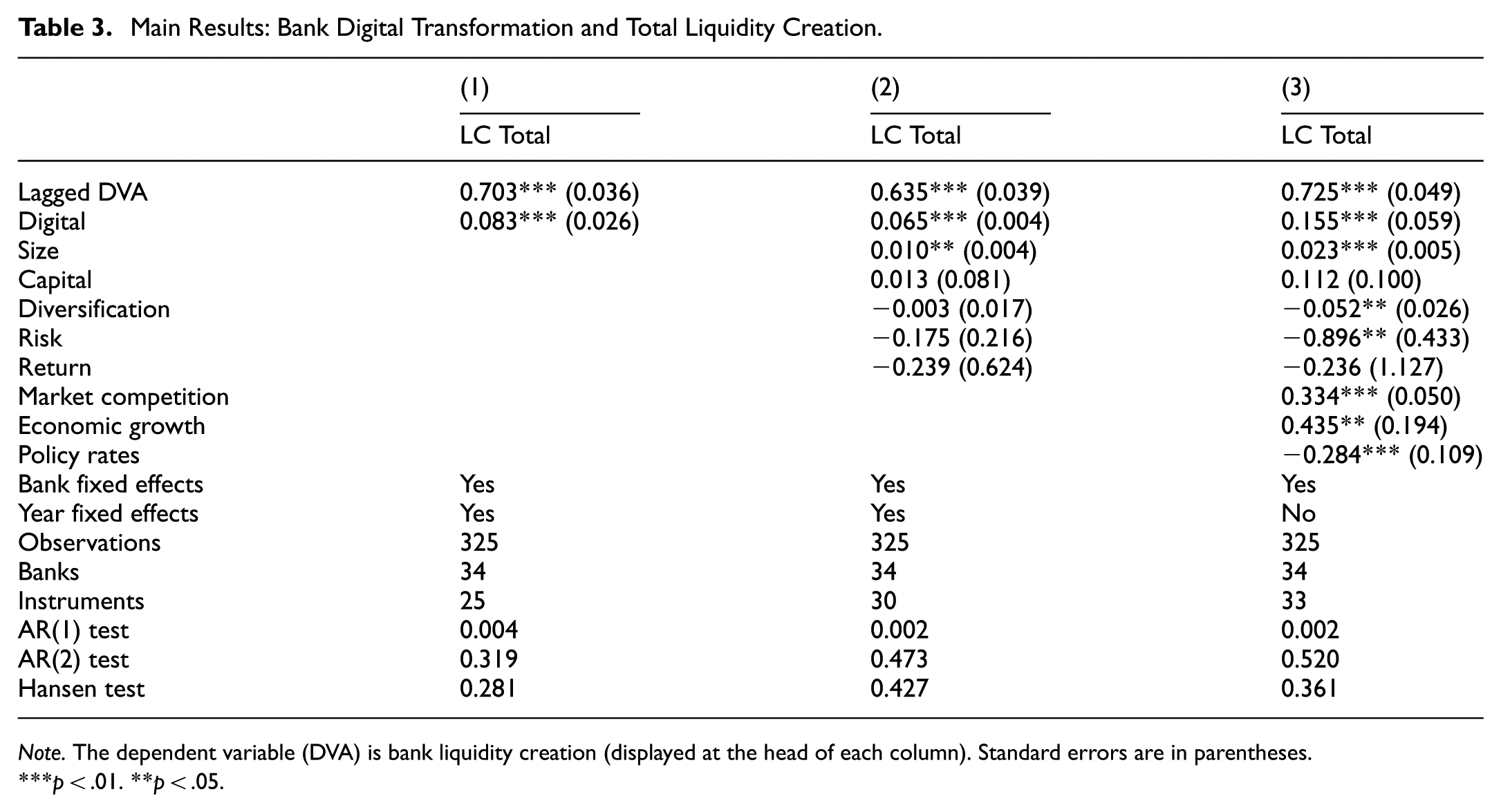

Taken together, the results in Table 2 indicate that bank-level digital transformation consistently shows a strong and positive effect on all three components of bank liquidity creation (with most coefficient significance levels at 1%), which suggests that the overall positive effect may eventually occur for total liquidity creation. Table 3 validates this conclusion, where digital transformation again shows a clear and significant association with the liquidity creation variable (LC Total). This result underscores the comprehensive impact of digital transformation on banks’ ability to generate liquidity across its various operations. The economic importance of these findings is evident: a standard deviation increase in the digital transformation index corresponds to a meaningful rise of 0.018 percentage points in total liquidity creation (0.113 × 0.155, column 3), reinforcing the idea that digital innovations contribute to enhancing the bank’s liquidity generation capacity comprehensively.

Main Results: Bank Digital Transformation and Total Liquidity Creation.

Note. The dependent variable (DVA) is bank liquidity creation (displayed at the head of each column). Standard errors are in parentheses.

p < .01. **p < .05.

In conclusion, the baseline results in this subsection provide robust evidence that digitalization plays a crucial part in improving bank liquidity created across all dimensions—assets, liabilities, off-balance sheet items, and overall liquidity. This pattern strongly confirms

Robustness Checks

Sub-Indicators of Digital Transformation

In addition to the aggregate digitalization index, it is essential to analyze its four sub-dimensions to thoroughly evaluate the impact of bank digital transformation. We perform additional analyses by breaking down the overall digital transformation index into its four constituent sub-indices, each reflecting a specific dimension of digitalization: (1) Technology infrastructure (TEC) captures the availability of core IT systems and digital platforms; (2) Human resources (HRE) reflects the bank’s investment in digitally skilled staff and training; (3) Internal banking applications (APP) measure the integration of digital tools into internal operations; and (4) Online banking services (SER) represent the accessibility and functionality of digital services provided to customers. Together, these dimensions reflect both the technological and organizational depth of a bank’s digital transformation. This approach enables us to identify the primary factors influencing our findings and offers a more detailed understanding of how various elements of digital transformation impact shifts in earnings management practices.

The empirical results across all columns in Table 4 demonstrate that the coefficients for four sub-indices are positive and statistically significant at the 1% level, aligning with the aggregate findings of the overall digital transformation index. Hence, each of these sub-dimensions of digital transformation exhibits a consistent positive effect on total liquidity creation. This consistency suggests that advancements in each dimension of digital transformation, whether through improved technology, skilled human capital, enhanced internal banking systems, or expanded online services, contribute to the bank’s capacity to generate liquidity. By breaking down the overall index, our analysis significantly expands upon previous research that primarily focuses on the technology aspect of digital transformation when analyzing its impact on bank liquidity creation. While earlier studies largely emphasize the importance of technological advancements in enhancing liquidity creation (Fang et al., 2023; Guo & Zhang, 2023), our analysis goes further by indicating that bank liquidity is also driven by the integration of skilled human resources, optimized internal processes, and customer-facing digital services.

Robustness Checks: Sub-Indicators of Digital Transformation.

Note. The dependent variable (DVA) is bank liquidity creation (displayed at the head of each column). Standard errors are in parentheses.

p < .01. **p < .05.

Endogeneity Concerns

To address the potential issue of endogeneity in testing how digital transformation influences the ability of banks to generate liquidity, we employ several econometric strategies aimed at mitigating this concern. (i) We use fixed effects models to control for unobserved characteristics that might influence both digital transformation and liquidity creation. (ii) We include lagged regressors to address potential reverse causality. (iii) We include relevant control variables at both the bank and macroeconomic levels to reduce the risk of omitted variable bias. (iv) We consider the GMM estimator, using instruments in “gmm-style” options in the “xtabond2” command.

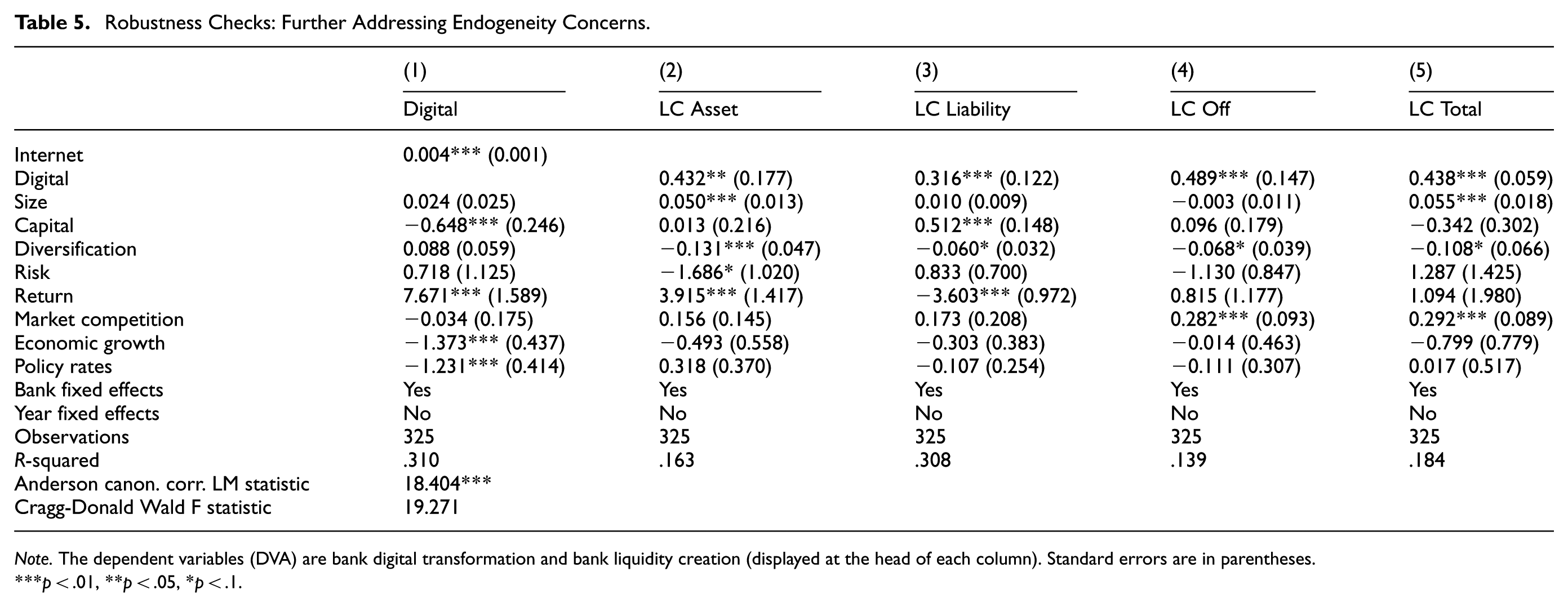

Despite these efforts, endogeneity may still present challenges in fully interpreting our findings. To further address this issue, we implement the IV approach using two-stage least squares (2SLS) estimation. The key to this method lies in selecting an appropriate instrument—one that is correlated with bank digital transformation but uncorrelated with liquidity creation except through its effect on digital transformation. For this purpose, we choose the Internet penetration rate as the instrument. Internet penetration is a strong predictor of digital transformation, as it facilitates greater access to and utilization of digital banking services, while being plausibly exogenous to a bank’s liquidity creation activities (Fang et al., 2023).

The findings derived from the 2SLS setting reported in Table 5 support the robustness of our conclusions. Specifically, the first-stage regression results reveal a strongly positive association between Internet penetration and the level of bank digital transformation (column 1), affirming the validity of our chosen instrument. Further confirmation comes from the diagnostic tests beneath the table: the Anderson LM statistic affirms model identification, while the Cragg-Donald Wald F value shows that the instrument possesses sufficient strength. Collectively, these diagnostics offer statistical support for the reliability and relevance of our instrument. In the second estimation stage, after incorporating fitted values of digital transformation from the initial stage as the explanatory variable and running the regression across multiple components of liquidity creation (columns 2–5), we document that the coefficients on Digital consistently display positive signs and remain statistically significant across asset, liability, off-balance sheet, and aggregate liquidity creation measures. This finding further corroborates our previous assertion that digitalization facilitates bank liquidity creation. Therefore, applying the 2SLS methodology strengthens confidence that the observed positive link between digitalization and liquidity creation is not the result of endogeneity bias.

Robustness Checks: Further Addressing Endogeneity Concerns.

Note. The dependent variables (DVA) are bank digital transformation and bank liquidity creation (displayed at the head of each column). Standard errors are in parentheses.

p < .01, **p < .05, *p < .1.

Heterogeneity Analysis

The Moderating Effect of Bank Diversification

We first explore bank-level heterogeneity by concentrating on bank diversification. Examining how bank diversification moderates the linkage between digital transformation and liquidity creation is of critical importance because diversification reduces asymmetric information and enhances cross-selling opportunities. Banks with diversified portfolios gather more information across markets and segments, which helps mitigate information asymmetry between banks and borrowers (Boot, 2000). These benefits may amplify the effect of digital transformation by providing advanced analytics, allowing banks to make better credit decisions and optimize liquidity creation (Banna et al., 2021). Besides, diversified banks benefit from cross-selling opportunities; for example, these banks are not only involved in traditional lending activities but also offer a range of other financial services (Gallo et al., 1996). Digitalization supports a bank’s ability to cross-sell these products by using data analytics to identify customer needs and tailor products accordingly. Banks that diversify their services and leverage digital technologies can generate additional revenue streams while boosting liquidity creation.

To evaluate the moderating influence of bank diversification, we include interaction terms between the digital transformation index and three distinct types of diversification: income, asset, and funding. Income diversification is defined as the ratio of non-interest income to total operating income, asset diversification as the share of non-loan assets in total assets, and funding diversification as the proportion of non-deposit funding in total funds. These indices capture the degree of spreading from traditional activities to non-traditional segments, with larger values indicating higher diversification (Elsas et al., 2010; Lepetit et al., 2008; T. L. A. Nguyen, 2018; Williams, 2016).

Table 6 reports estimations for the heterogeneity impacts caused by bank diversification. The results display that the interaction terms between digitalization and each dimension of bank diversification are positive and statistically significant, sharing the same sign with the significant coefficient on the standalone Digital. This finding indicates that the impact of digital transformation on liquidity creation is amplified at diversified banks. This pattern is witnessed for various aspects of bank diversification. Diversified banks operate across multiple business lines and funding sources, which introduces operational complexity and coordination challenges. In such settings, digital transformation becomes more valuable—enhancing efficiency in loan processing, automating funding operations, and integrating customer services across divisions. This allows diversified banks to better manage and transform diverse inputs into liquidity, making the effects of digital transformation more pronounced in these institutions. Moreover, it should also be noted that the standalone coefficients on bank diversification are negative, indicating that diversification directly reduces bank liquidity creation. This finding reflects the direct effect: Diversification often involves shifting into less liquid assets or funding structures, such as long-term investments, fee-based services, or wholesale funding (Hou et al., 2018). These activities typically do not support liquidity creation in the conventional sense.

Further Analyses: Heterogeneity by Bank Diversification.

Note. The dependent variable (DVA) is bank liquidity creation (displayed at the head of each column). Standard errors are in parentheses.

p < .01. **p < .05. *p < .1.

The Moderating Effect of Bank Competition

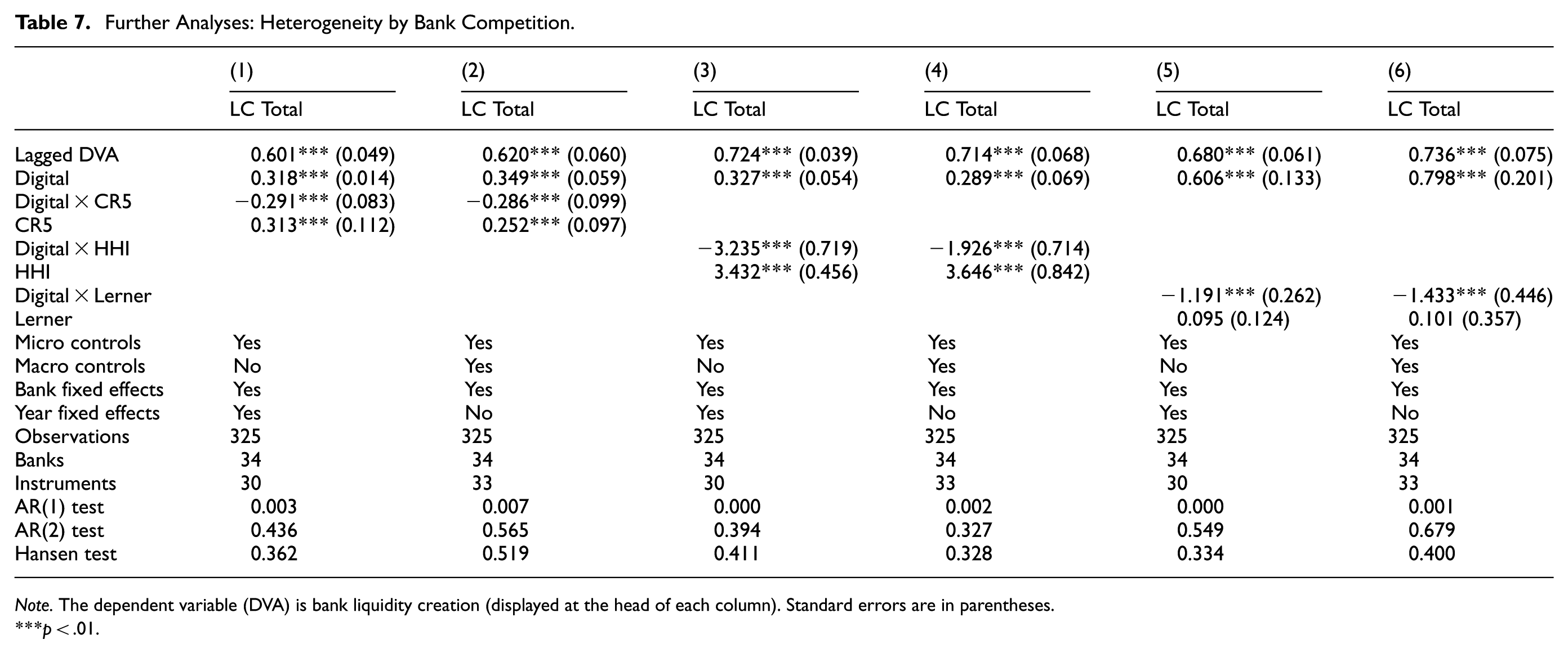

At the industry level, we hypothesize that how digital transformation drives liquidity creation depends on the market structure of the banking system. Specifically, we consider bank competition to be another crucial factor that could influence how digital transformation affects liquidity creation. Banks are forced to innovate and improve operational efficiency in highly competitive markets to stay ahead of rivals (Claessens & Laeven, 2005). In such environments, digital transformation can serve as a critical tool for banks to enhance liquidity creation through better customer service, reduced transaction costs, and optimized lending processes (Ren et al., 2024). For instance, digital platforms allow banks to reach a wider audience and provide liquidity more efficiently, which can be a competitive advantage in a crowded market. However, in less competitive or highly concentrated banking markets, where innovation incentives may be lower, the effects of digitalization could be less pronounced. Banks in these markets may not feel the same urgency to adopt digital solutions (Shang & Niu, 2023), which might diminish the overall effectiveness of digitalization in liquidity creation functions.

Based on the above arguments, we anticipate the positive effect of digitalization on bank liquidity creation to be stronger in markets with higher competitive conditions. To verify our expectations, we introduce interaction terms between digital transformation and three alternative measures of competition: the five-bank concentration ratio (CR5), the Herfindahl-Hirschman index (HHI), and the Lerner Index. Both HHI and CR5 serve as proxies for market concentration, where higher scores signify lower competition. The Lerner Index, on the other hand, reflects market power, determined by the markup of price over marginal cost, and higher values also imply reduced competition. Detailed discussions on the motivations and calculations of these bank competition measures could be found in the previous related studies (Dang & Huynh, 2022; Huynh, 2023).

Across all columns of Table 7, we observe that the interaction terms between digitalization and three reverse proxies of competition (CR5, HHI, and Lerner) are negatively signed and statistically meaningful. This uniform result suggests that the beneficial impact of digital transformation on liquidity creation is amplified in more competitive markets, characterized by lower CR5, HHI, and Lerner values. Simply put, greater competition in the banking sector enhances the effectiveness of digital transformation in increasing liquidity creation. This outcome is consistent with our initial expectations. In highly competitive environments, the pressure to innovate and optimize operations drives banks to maximize the influences of digitalization. Thus, digital transformation becomes a more strategic tool to enhance efficiency, attract customers, and improve liquidity services. This makes the impact of digital transformation more pronounced in competitive settings. Conversely, in less competitive markets, where banks have more market power and face less pressure to innovate, the effects of digitalization on liquidity creation are weaker. Besides, we also find that higher competition is linked with lower levels of liquidity created, as evidenced by the significantly positive coefficients on CR5 and HHI in columns 1 to 4. This reflects that banks operating in highly competitive environments tend to create less liquidity, which aligns with existing literature suggesting that greater competition compresses profit margins, potentially reducing banks’ capacity or incentives to provide credit and other liquidity-enhancing services (Horvath et al., 2016).

Further Analyses: Heterogeneity by Bank Competition.

Note. The dependent variable (DVA) is bank liquidity creation (displayed at the head of each column). Standard errors are in parentheses.

p < .01.

Our findings contrast with Fang et al. (2023), who document that banks with stronger market power are better positioned to leverage fintech for liquidity creation as these banks gain technological advantages, enabling them to expand lending and enhance liquidity. The divergence in our findings likely reflects differences in the incentives driving innovation—while Fang et al. (2023) focus on the advantages conferred by market power, we highlight the necessity for innovation driven by competition. It is worth mentioning that our finding is supported by the work of Shang and Niu (2023), who find that higher levels of banking competition strengthen the effectiveness of digitalization, particularly in promoting green credit.

The Moderating Effect of Macro Shocks

In this subsection, we move on to predict that at the country level, macroeconomic shocks, such as the 2008 financial crisis and the COVID-19 outbreak, can moderate the effects of digital transformation on liquidity creation. These shocks introduce significant disruptions to the banking system, where banks face increased risks of default, heightening the importance of liquidity management (Ivashina & Scharfstein, 2010; Çolak & Öztekin, 2021). As a result, banks often become more risk-averse due to heightened uncertainty in financial markets and economic conditions. Even if banks have adopted digital transformation, they may prioritize capital preservation and risk management over liquidity creation activities, leading to a dampened impact of digital initiatives. Moreover, crises often result in tightened liquidity conditions (Berger & Bouwman, 2017), where banks face difficulties in raising funds through traditional or digital channels. This limits the ability of banks to utilize their digital infrastructure to expand lending, obtain funds, and enhance liquidity creation. Even with advanced digital tools, the external liquidity environment restricts banks’ ability to create liquidity. These factors combine to make the impact of digitalization less pronounced during crises, as banks tend to become more conservative and focus on maintaining stability rather than expanding their liquidity-generating activities.

However, the effects of digital transformation on liquidity creation can be strengthened during periods of crisis for several reasons. Accordingly, banks with advanced digital tools can better engage with customers through digital platforms, offering customized products that align with the changing needs of businesses and individuals in times of crisis (Oikonomou et al., 2023). This flexibility allows banks to respond quickly to market demands, promoting liquidity creation by extending loans or offering tailored financial products via digital channels. Notably, during the COVID-19 pandemic, traditional banking services such as branch visits are restricted, pushing both banks and customers to increasingly rely on digital channels. Banks already investing in digital transformation can continue providing loans and liquidity through digital platforms while adhering to social distancing measures, thus maintaining critical liquidity support to businesses and consumers (Wu et al., 2024). These factors make digital transformation an effective tool for banks to not only withstand the pressures of a crisis but also to enhance their liquidity creation.

Overall, we aim to study how macroeconomic shocks influence the digital transformation-liquidity creation nexus, thereby exploring the role of digital transformation in enhancing resilience during future economic disruptions. We do this by comparing two distinct crises—the financial crisis, which mainly disrupts financial markets, and the coronavirus outbreak, which has broad socio-economic implications. This study helps to determine whether the role of digital transformation varies under different types of macroeconomic shocks, an area that has been underexplored in the literature. While Wu et al. (2024) and Tang et al. (2024) focus on the effects of fintech during the COVID-19 pandemic, both studies find that fintech adoption reduces bank liquidity creation in this context. However, they do not examine the potential effects of other macroeconomic shocks, such as the 2008 global financial crisis, nor do they differentiate between the nature of these crises. Our research fills this gap.

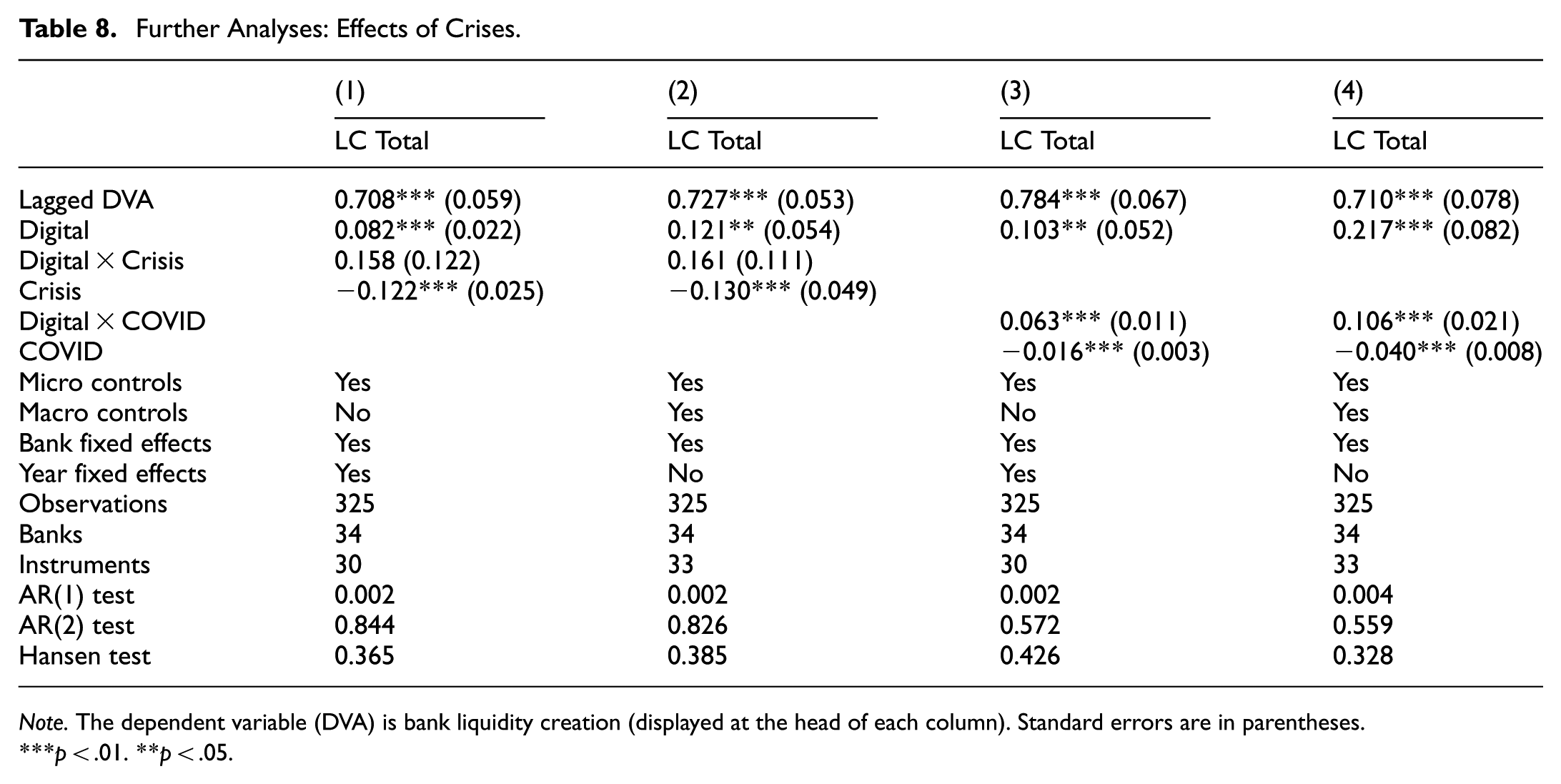

We test the role of macroeconomic crises by including two interaction terms in our model: (i) an interaction term between digital transformation and the financial crisis, captured by a dummy variable equal to 1 during 2007 to 2009 and 0 otherwise; and (ii) an interaction term between digital transformation and the COVID-19 pandemic, represented by a dummy equal to 1 for the period 2020 to 2021 and 0 otherwise. We run regressions incorporating these interaction terms and present the results in Table 8. As shown in columns 1 to 2, the interaction term involving digitalization and the financial crisis is statistically insignificant, suggesting that the financial crisis does not materially influence the nexus between digital transformation and bank liquidity production.

Further Analyses: Effects of Crises.

Note. The dependent variable (DVA) is bank liquidity creation (displayed at the head of each column). Standard errors are in parentheses.

p < .01. **p < .05.

Conversely, the findings in columns 3 to 4 demonstrate that the impact of digital transformation on total liquidity creation is more pronounced amid the COVID-19 pandemic period. In detail, the interaction term for digitalization and the COVID-19 dummy is positive and statistically significant, implying that banks with advanced digital capabilities can enhance liquidity creation to a larger extent during the pandemic. This outcome is consistent with the increased reliance on digital banking channels during the pandemic, as poorly-digitalized banks face significant challenges in maintaining their operations and customer base compared to well-digitalized banks. The pandemic triggers a rapid shift toward digital banking, as social distancing measures, lockdowns, and the need for remote services push customers and businesses to rely heavily on online banking platforms. Well-digitalized banks can capitalize on this shift by offering seamless digital services, ensuring customer engagement, and meeting increased demand for online financial products. As a result, well-digitalized banks expand their market presence, contributing to a more pronounced impact of digital transformation during the pandemic. A similar mechanism of action is not observed during the financial crisis, since the drivers and effects of digitalization are less significant than during the health crisis.

Conclusion

This research analyzes Vietnamese banks over the period 2007 to 2022 to examine the influence of digital transformation on various dimensions of liquidity creation. The main findings reveal that digitalization significantly enhances liquidity creation. This effect is evident across liquidity generated through assets, liabilities, and off-balance-sheet items, contributing to the overall liquidity created by banks. Notably, our analysis reveals a positive relationship between all four subcomponents of digital transformation and total liquidity creation, indicating that advancements in each specific dimension of digital transformation, whether through improved technology, skilled human capital, enhanced internal banking systems, or expanded online services, contribute to the bank’s capacity to produce liquidity. Besides, we document that more diversified banks experience a stronger effect of digital transformation. This moderating effect occurs for bank diversification across different aspects of income, assets, and funds. We also document that the effects of digital transformation are amplified in highly competitive banking markets. Finally, while the effect of digital transformation intensifies during the COVID-19 pandemic, the global financial crisis does not significantly alter the digital transformation-liquidity creation link.

Based on our findings, policymakers should consider digital transformation as a critical lever to enhance bank liquidity creation and financial sector resilience. This transformation should encompass investments across multiple dimensions—technology infrastructure, internal systems, online customer services, and human capital—to enable banks to manage liquidity more effectively across assets, liabilities, and off-balance-sheet activities. Importantly, the benefits of digital transformation are not uniform but are significantly modulated in certain contexts. Specifically, the positive impact of digitalization on liquidity creation is amplified among (i) diversified banks, where greater complexity increases the operational value of digital integration; (ii) competitive banking markets, where heightened pressure to differentiate drives more effective digital utilization; and (iii) crisis periods such as the COVID-19 pandemic, when digital readiness ensures business continuity and the uninterrupted provision of liquidity to the economy. These patterns suggest that digital transformation should not only be encouraged broadly but also strategically targeted—for example, through tailored incentives, supportive regulations, or infrastructure development aimed at banks operating under these conditions. Such an approach would maximize the liquidity-creating potential of digital innovation while reinforcing the stability and adaptability of the banking system.

Our paper has several limitations that should be acknowledged. Importantly, the small bank sample, primarily caused by missing observations in some years due to incomplete ICT index data published by the state agency, may affect the robustness of our findings. The study is also limited in its generalizability, as it focuses solely on Vietnamese commercial banks, and the results may not fully apply to other banking systems, particularly those in developed economies or other emerging markets with different backgrounds. Furthermore, while our analysis demonstrates a significant impact of digital transformation on liquidity creation, we do not conduct detailed mechanism tests to pinpoint the exact channels through which digital transformation drives this outcome. Future research could address these limitations by expanding the dataset to include a broader range of countries and conducting in-depth mechanism tests to better understand the transmission channels.

Footnotes

Appendix

Correlation Matrix.

| Digital | LC Asset | LC Liability | LC Off | LC Total | Size | Capital | Diversification | Risk | Return | Market competition | Economic growth | Policy rates | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Digital | 1.00 | ||||||||||||

| LC Asset | 0.02 | 1.00 | |||||||||||

| LC Liability | 0.06 | 0.44 | 1.00 | ||||||||||

| LC Off | 0.30 | −0.08 | −0.08 | 1.00 | |||||||||

| LC Total | 0.07 | 0.82 | 0.76 | 0.25 | 1.00 | ||||||||

| Size | 0.27 | 0.31 | 0.48 | 0.11 | 0.40 | 1.00 | |||||||

| Capital | −0.09 | −0.11 | −0.59 | −0.05 | −0.33 | −0.39 | 1.00 | ||||||

| Diversification | 0.13 | −0.14 | −0.01 | −0.04 | −0.11 | 0.12 | −0.08 | 1.00 | |||||

| Risk | 0.15 | 0.09 | 0.17 | 0.04 | 0.13 | 0.30 | −0.09 | 0.06 | 1.00 | ||||

| Return | 0.23 | −0.05 | −0.34 | −0.02 | −0.18 | 0.11 | 0.36 | 0.07 | 0.00 | 1.00 | |||

| Market competition | −0.08 | 0.03 | 0.04 | 0.07 | 0.02 | −0.16 | 0.06 | 0.15 | −0.10 | 0.07 | 1.00 | ||

| Economic growth | −0.15 | −0.04 | 0.06 | 0.21 | 0.12 | −0.11 | 0.01 | −0.08 | −0.07 | −0.02 | 0.28 | 1.00 | |

| Policy rates | 0.11 | −0.25 | −0.45 | −0.18 | −0.32 | −0.36 | 0.26 | −0.06 | −0.10 | 0.07 | −0.23 | 0.25 | 1.00 |

Funding

The author received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The datasets generated during and/or analyzed during the current study are available from the corresponding author on reasonable request.