Abstract

The study examines how the 2007 to 2008 Global Financial Crisis (GFC) and the recent COVID-19 pandemic have affected the risk-return profile of the Indonesian financial sector index (IDXFinance). Using weekly return data from 2005 to 2022 and the GARCH-M model, the analysis evaluates volatility persistence and clustering. The study employs two dummy variables to represent the two crisis situations, and daily and monthly data analyses are used to validate the findings. The research reveals that the GFC crisis had a negative impact on stock returns, causing volatility clustering and increased IDXFinance return volatility. On the other hand, the COVID-19 pandemic had a less centralized influence on stock returns and volatility. The COVID-19 pandemic had a more subdued impact than the GFC, which began in and affected the banking sector. This study is among the first to examine the response of Indonesia’s financial sector to two market crises, and it provides investors with insights into how financial crises like the GFC and COVID-19 affect the Financial Sector Index in Indonesia’s return and volatility. The study also highlights the risk and financial sector performance, which can be helpful for policymakers and practitioners to anticipate and mitigate future risks.

Keywords

Introduction

Global market risks are systematic risks that can significantly impact firms’ financial performance and stock prices due to sudden shifts in financial market-influencing factors (Hayes, 2023; Kassi et al., 2019). Two notable examples are the 2008 Global Financial Crisis (GFC) and the COVID-19 pandemic, both of which had profound effects on the global economy, especially on Indonesia’s financial sector.

The GFC started with the collapse of Lehman Brothers, which caused a chain reaction of bank failures, plummeting stock markets, and a loss of confidence in financial institutions (Scott, 2021). This crisis spread worldwide, affecting stock markets worldwide. For instance, the IDX Composite Index in Indonesia experienced a significant decline of 59%, steeper than that of other markets, including the U.S. market (Modjo, 2020).

Fast-forward to the COVID-19 pandemic, which caused another global market risk, arguably more severe than the GFC, and significantly impacted the global economy (Gao et al., 2022). The pandemic adversely affected the solvency profiles of companies worldwide, leading to severe economic downturns, especially in emerging countries with weak financial systems. In Indonesia, the pandemic negatively impacted the financial performance of banks (Yanti et al., 2021).

Despite the increased volatility in stock performance and the financial sector due to these global market risks, more needs to be understood about the extent and magnitude of their impact on the financial sector’s performance. This paper aims to fill this gap by providing a comparative examination of the effects of the GFC and COVID-19 on Indonesia’s financial sector. The insights from this study will be valuable for policymakers and investors in making informed decisions.

This research contributes to the existing literature in several ways. It expands on the previous studies conducted by Abuzayed et al. (2021), Bouri et al. (2021), and Gunay and Can (2022) by investigating the systemic risk spillover and return connectedness across multiple asset classes during the Global Financial Crisis (GFC) and COVID-19, with a specific focus on the financial sector in Indonesia.

Furthermore, it builds upon the research conducted by CHIN and Najaf (2020) and Shahzad et al. (2021) by analyzing the influence of global events, such as the GFC and COVID-19, on financial markets, with a particular emphasis on Indonesia’s market. In addition, it complements Choi’s previous work (2021) by analyzing the effectiveness of the stock market during periods of crisis, highlighting the differences between the GFC and the COVID-19 pandemic.

Moreover, it expands upon the research Iqbal et al. (2024) conducted by examining volatility spillovers during normal and high volatility states and their underlying factors in the context of the Indonesian financial sector. Finally, it adds to the previous work of Yousaf et al. (2023) by exploring the multidimensional connectedness among the volatility of global financial markets, specifically during the GFC and COVID-19.

The paper is structured as follows: Section “Literature Review and Hypotheses Development” provides a literature review and theoretical framework focusing on the impact of global market crises on the Indonesian Financial Sector Index. Section “Data and Methodology” discusses the methods and empirical models used in the study. Section “Empirical Findings” presents the study’s results, and Section “Policy Implications and Recommendations” concludes by providing an overview of the study’s findings, implications, and limitations.

Literature Review and Hypotheses Development

Several Causes of Market Crisis

The Global Financial Crisis (GFC) is one of the causes of the market crisis in a large economy that spread worldwide. This significant global financial crisis has impacted both developed and developing countries, causing widespread disruption. Compared to the 1997 Asian financial crisis, the GFC crisis is more severe and prevalent, with a greater level of contagion (Ali & Afzal, 2012). This crisis is considered the most significant since the Great Recession of the 1930s, impacting the economy and the financial sector. The crisis began in the United States during the latter half of 2007, starting with the subprime mortgage crisis and reaching its peak throughout 2008. The impact of this devastating event was not limited to developed countries; developing countries were also affected, resulting in fluctuations in financial markets and detrimental to the real economies of developing countries. The crisis had a detrimental impact on the economies of developing countries, as they were negatively impacted through trade and financial channels. Inflows of net capital from developed countries to developing countries significantly decreased. Exports from developing countries, portfolio investments, and foreign direct investment were severely affected by this crisis (Iqbal, 2010).

The COVID-19 pandemic is another potential factor contributing to the financial crisis. The global ramifications of the Coronavirus pandemic have led to substantial adverse effects, leading to economic contractions in several countries and perhaps intensifying the probability of severe recessions or depressions. Gao et al. (2022) claimed that the global economy had suffered significant and catastrophic consequences as a result of the new coronavirus, often referred to as COVID-19. Individuals have been confined to their residences as a result of the proliferation of this illness, so affecting the routine professional lives of the populace. After China and South Korea officially declared a pandemic on March 12, 2020, the United States market saw significant disruptions caused by the widespread transmission of COVID-19 throughout the country, which led to a decrease in oil prices. These accidents had a detrimental impact on the economy, leading to a recession (Su et al., 2021). The Covid-19 epidemic is having a significant effect on the U.S. economy, which is already grappling with the oil market crisis. As a result, the stock market has greater fluctuations, unemployment rates rise, consumer confidence and spending diminish, and industrial production declines. The repercussions and variations resulting from the present economic and monetary policies are equally or even more severe than those observed in the United States during major crises such as the Great Depression (1929), the Stock Market Crash of 1978, and the Global Financial Crisis (2008).

The global impact of the pandemic has already been felt, especially in the United States. Both small and large businesses have been impacted by Covid-19, disrupting physical production and supply chains. This includes disruptions to air and sea transportation routes to and from the U.S. These disruptions ultimately result in restrictions on people’s ability to work, leading to job losses. Additionally, reduced production and increased demand may lead to higher product prices, potentially resulting in inflation and a recession. The downturn of the U.S. economy due to high daily positive cases of COVID-19 is also having a huge impact on the Dow Jones, Oil Index, and major stock exchanges (Alber, 2020).

Furthermore, Mirza et al. (2020) analyzed the solvency profile of companies in European Union member states amidst the Coronavirus pandemic. The authors have ascertained that the solvency profiles of all companies were adversely affected during the COVID-19 outbreak. In addition, Alber (2020) has studied the effect of Covid-19 spread within the worst six countries worldwide. The results of the robustness analysis have validated the adverse impact of the Covid-19 outbreak on the performance of the stock market in Spain, Germany, France, and China. Nevertheless, this study did not confirm these effects for the United States and Italy. From these discussions, it is interesting to see the differences and gradations of impact between the pandemic-led market crisis and the global financial crisis on financial stocks.

Global Market Crisis in the Financial Sector

The financial sector is crucial to the functioning of the economy as a whole because of the services it offers consumers, which significantly impact daily activities. In addition, the financial sector plays an essential role in the lives of individuals because it provides a sense of security and stability when it comes to their finances. A robust financial system encourages people to save and channels those funds into investments that boost the economy. During the Global Financial Crisis of 2008, the crisis consistently revolved around the banking sector. The bankruptcy of Lehman Brothers, ranked as the fourth-largest bank and investment company in the United States, was the initial event that triggered the crisis. The global financial crisis caused bank losses due to mortgage defaults and halted credit growth provided to consumers and businesses through interbank lending. The excessive credit has also resulted in losses for financial institutions and deposit insurers. As a result, people have lost faith in the financial system’s stability and its stock markets. Besides that, as a direct consequence of the financial system’s dependence on various financial markets worldwide, the crisis adversely impacted the global economy.

After Lehman Brothers declared bankruptcy in September 2008, the impact of the subprime mortgage crisis on the global economy began to spread. The crisis’s impact on the economy of Indonesia was marked by the withdrawal of funds in foreign currencies, especially in U.S. dollars, by creditors, financial institutions, and investors in the U.S. The funds were withdrawn by selling stock and debt instruments acquired in rupiah and repurchased in dollars. In addition, funds can be withdrawn by transferring funds deposited in Indonesian banks and directly exchanging them for the dollar currency (Sudarsono, 2009). A significant amount of money has been moved back to the United States due to the financial crisis, which led to the sale of numerous stocks and bonds. As a result, the prices of stock and debt securities drop, resulting in a severe plunge in the stock price index. A decrease in the price of financial assets will cause a loss (capital loss) so that the company’s capital and the capital adequacy ratio (CAR) are depleted.

Volatility in exchange rates and the anticipation of significant fluctuations in the depreciation of the rupiah may lead to the movement or transfer of public funds to both domestic and foreign banks with a reputation for providing high-quality services, a phenomenon commonly referred to as currency substitution. Debtors of the banks may also experience financial difficulties due to the disruption. This may also result in the inability of debtors to repay both the principal and interest owed to the bank, thereby leading to a greater negative consequence. As a result, banks cannot meet their obligations to Third Party Financing due to liquidity constraints and the resulting rise in the cost of financing (Sudarsono, 2009). Furthermore, the financial crisis in the United States in 1998 and 2008 impacted Indonesia’s existing economic system, including a rise in inflation. This increase in inflation will indirectly make banking management raise its lending rate so that banks do not suffer losses (credit risk). Credit risk includes non-performing loans. Sari et al. (2012) showed that the non-performing loans (NPL) ratios in banks listed on the Indonesia Stock Exchange from 2003 to 2010 still have a high NPL (around 6%) compared to the stipulated Bank Indonesia standard. Furthermore, the high NPL ratio also indicates a decrease in the collectability of credit provided to consumers due to the rise of inflation, which lessens the ability of creditors to pay their debt as people’s purchasing power falls. Therefore, during the global financial crisis, Indonesia’s economy significantly impacted the banking sector, especially the increase in non-performing loans and the decline in credit growth.

Apart from the Global Financial Crisis, financial markets and institutions worldwide, especially the banking sector, are experiencing severe consequences from the Coronavirus outbreak. The pandemic causes many problems, most noticeably rising default rates. It will probably be more severe in developing countries with weak financial systems. For instance, the devastating effect of the pandemic on the banking industry in Bangladesh was studied by Barua & Suborna Barua (2021). Non-performing loans (NPLs) are already high in Bangladesh’s banking industry, and this pandemic will only worsen things. In addition, the Indonesian banking sector was severely impacted during the initial stages of the pandemic, which started in March 2020. However, several steps and measures have been taken to prevent the spread of the pandemic from having a broader harmful impact on the economy and the financial system.

Nevertheless, Yanti et al. (2021) showed that the pandemic had negatively affected Indonesian banks’ financial performance. Using Kruskal-Wallis’s test, the study examines the variations in economic performance indicators between pre-pandemic and post-pandemic years for Indonesian banks classified as BUKU 2, BUKU 3, and BUKU 4. The researchers asserted that bank profitability plunged during the pandemic because of higher costs, fewer customers who could use new credit, an increase in non-performing loans, and lower capital adequacy ratios than required. Hence, it is reasonable to conclude that the pandemic represents an enormous risk to banks’ profitability, sustainability, and expansion in developing nations, particularly in countries where banks play a key economic function (Damak et al., 2020).

Banking performance in credit management may be impacted by the spread of Covid-19, which has disrupted the effectiveness and ability of debtors to satisfy their credit obligations. Therefore, the Indonesian government has issued a policy to provide national economic stimulus by implementing Financial Services Authority Regulation No.11/POJK.03/2020 to encourage the optimization of the intermediary banking role (Disemadi & Shaleh, 2020). This policy outlines the existence of credit restructuring by ensuring that the quality of restructured loans can be determined without interruption if they are extended to debtors identified as being impacted by the spread of Covid-19. The practice of the restructuring scheme might vary and is governed by each bank’s regulations based on the debtor’s profile and ability to pay. According to the research by Wardhani et al. (2021), the pandemic had no significant effect on financial performance before or during the epidemic. Furthermore, with the implementation of the credit restructuring policy, the impact caused by Covid-19 can be mitigated in the banking sector. In contrast, Yanti et al. (2021) showed that cost increases, a decrease in customer credit, rising non-performing loans, and a decline in capital adequacy contributed to a steep fall in bank profitability during the pandemic.

Market Volatility and Spill Overs Transmission

The term “volatility” refers to the degree to which the price of a financial instrument rises, falls, or fluctuates over a given period. The standard deviation of its returns measures the volatility of a financial time series. Volatility could also refer to the degree of movement of asset returns in the overall market, not only for several or particular asset classes. For instance, the fluctuations in the stock market price index occurred in seconds and minutes, and the variations in stock returns occurred at the same frequency and during the same period. The first refers to the market’s volatility, while the latter is the volatility of the stock return. As a result of the heightened volatility of the market and stock returns, financial assets will be riskier and have greater uncertainties.

The spillover effect can be seen in all asset classes. Alshubiri (2021) conducted a study on portfolio returns of Islamic indices in the Gulf Cooperation Council (GCC) countries. According to his findings, three indices (S&P et al., S&P GCC Composite Shariah Dividend, and S&P Shariah Domestic Total Return Index) exhibit a positive correlation with the Islamic Stock Price Index in the long term. In contrast, S&P GCC Investable Shariah shows a negative correlation. The study concludes that to ensure positive growth in the price of Islamic stocks, it is essential to diversify the Islamic investment portfolio to mitigate unexpected risks.The enhanced uncertainties, in turn, caused investors’ confidence to decrease. Besides that, volatility affects the existence of international financial markets in terms of risk. Therefore, financial market volatility, particularly in the stock market, is normally used as a proxy for risk.

The world’s financial markets are more interconnected than ever before, which has made them more volatile. This is due to the increasing globalization and technological advancements, which have made the global financial market more transparent and interrelated (King & Wadhwani, 1990). As a result, the market shares of different countries are now linked, and there are shared risks between them. Increased volatility across the global financial market means one market can transmit risk to others. For example, geopolitical events like the Russian-Ukrainian conflict can cause financial instability (Yousaf et al., 2023). It has become more challenging to prevent elevated risk in one market from spilling over to other markets, which can cause financial instability in affected markets.

The financial crisis that originated in the United States has harmed economies worldwide. Since the peak of the global financial crisis in 2008, most financial markets have been severely affected, and even emerging countries have not been immune to its impact. The crisis has affected the investment, commercial banking, and insurance sectors, leading to a significant decrease in stock prices worldwide. This has increased the risk of volatility in the financial market, as any adverse circumstances in one country or market can have a ripple effect on other markets across the globe.

In recent studies, researchers have examined the system of volatility spillovers across various equity markets and asset classes under normal and high volatility states. The study found that the US stock market is at the center of volatility spillovers in the normal volatility state. In contrast, European and Chinese stock markets and strategic commodities have become major volatility transmitters in high-volatility states (Iqbal et al., 2024). The studies have also highlighted the crucial role of major economies like China in shaping the broader effects of the pandemic on the financial sector (Chin & Najaf, 2020). The identity of transmitters and receivers of volatility shocks differed between normal and high volatility states, with the US stock market being at the center of volatility spillovers in the normal volatility state, while in the high volatility state, European and Chinese stock markets, as well as strategic commodities, became major volatility transmitters (Choi, 2022).

In their study conducted in Indonesia, Sari et al. (2017) examined how the volatility of stock returns in another stock market affected the volatility of stock returns in Indonesia’s market, particularly before and after the 2007 crisis. In their study, Sari et al. (2017) built upon previous findings, which established the influence of stock markets on global and regional economies. The authors focused on seven countries as examples: the United States, the United Kingdom, Japan, Hong Kong, Australia, Singapore, and Indonesia. Through analyzing the immediate reaction of Indonesia’s stock market volatility to shocks in the volatility of other stock markets, the study revealed that Hong Kong and Singapore had the most significant impact as transmitters of volatility, both before and after the 2007 crisis. The research findings show that Indonesia’s stock market became more susceptible to shocks following the crisis, highlighting the influence of increasing interdependence among global financial markets on Indonesia’s stock exchange. Furthermore, the variance decomposition analysis demonstrated that during the 2007 crisis, the mature markets of the U.S. and U.K. had a major influence on Indonesia’s stock market return volatility.

From the above study, Sari et al. (2017) concluded that three factors are pertinent to the transmission of the crisis spillover from one market to another. These factors are:

First, the degree of economic power that the U.S. has. After the Second World War, the United States economy rose to prominence, and the dollar was adopted as the world’s primary trading currency. This finding was also supported by the study by Achsani and Strohe (2006), which stated that the U.S. stock market has a major influence on global markets. The statement was also supported by the research from (Karunanayake et al.2010), which stated that the performance of the U.S. stock market significantly influences the volatility of other markets across the world.

Second is the geographic and cultural proximities. Common investor groups—investors in the markets of countries that are close together geographically and culturally—tend to behave and respond to an event similarly. According to this postulate, there is a gradation in response between Asian and North American or European markets in responding to an event that may or may not have led to a market crisis.

Third, the existence of multiple listings across markets. Thus, a stock market like the U.S. New York stock exchange and the Frankfurt stock exchange, where many stocks listed are cross-listed elsewhere, will be more prone to the crisis than other markets.

Studies on the Impact of GFC and COVID-19 Pandemic on Stock Markets

Several studies have been conducted to evaluate how the COVID-19 pandemic has affected the stock market. These studies analyze the correlation between stock returns and volatility, particularly how it has changed during the pandemic. Abuzayed et al. (2021) discovered that the pandemic has heightened the systemic risk contagion between global and individual stock markets. This suggests that the pandemic has increased the interconnectedness of financial markets worldwide, which could potentially affect the stability of the financial sector. Bouri et al. (2021) found that the pandemic has significantly disrupted the typical patterns of return connectedness across various assets such as gold, crude oil, world equities, currencies, and bonds. This could potentially affect the risk and return profiles of various financial instruments. Gunay and Can (2022) evaluated the impact of the COVID-19 pandemic and the Global Financial Crisis of 2008 (GFC) on stock markets and determined that the US stock market was the source of financial contagion and volatility spillovers during both crises. Moreover, they found that the COVID-19 pandemic induced a more severe contagious effect and risk transmission than the GFC. Choi (2021) analyzed the efficiency of the US stock market during crisis periods, comparing the global financial crisis and the COVID-19 pandemic. The results of this study could provide insights into how different crises impact market efficiency and the implications for investors and policymakers.

Olowe (2009) utilized the E-GARCH-in-mean model to analyze the behavior of the Nigerian stock market to various events, including the global financial crisis, stock market crash, insurance reform, and banking reforms. The primary focus of the research was to investigate the patterns exhibited by stock returns and volatility during these events. Based on the study’s findings, there has been a noticeable increase in the persistence of high volatility within the Nigerian stock market due to the global financial crisis and the 2008 stock market crash. In addition to that, Adamu (2011) employed traditional statistical methods, including variance analysis and standard deviation, to investigate the global financial crisis’s impact on the Nigerian stock market. The research was separated between the pre-crisis and post-crisis periods. The study has shown that the financial crisis period was accompanied by increased stock market volatility in Nigeria.

Additionally, Ali and Afzal (2012) use the E-GARCH model to analyze the influence of the global financial crisis on the stock markets of India and Pakistan. The results show that negative shocks affect volatility more significantly than positive shocks. These stock markets also experienced persistent volatility clustering during this crisis. Besides that, the study reveals that the global financial crisis had a considerable negative influence on stock returns in Indian and Pakistani markets.

However, both the stock returns and increased volatility of the Indian stock market due to the global financial crisis are more pronounced than the Pakistani stock markets. One possible explanation for the disparity between the Pakistani and Indian stock markets is that India has a more robust economy. Additional research by Ravichandran and Maloain (2010) found that the recent financial crisis had a detrimental impact on stock markets in six Gulf countries. These markets, however, have grown stronger since the crisis’s end. Furthermore, Al-Rjoub and Azzam (2012) studied the patterns of stock return and volatility in the Jordanian Stock Market (ASE General) during the market crisis period using the GARCH-M model. Their findings indicate that all episodes of market crises had a detrimental effect on stock returns across all sectors, with the banking sector experiencing the most significant impact. The global financial crisis in 2008–2009 had the most severe impact, characterized by substantial declines in stock prices and enhanced volatility. The study also shows that volatility is highly persistent, and both before and following the crisis, there exists a significant inverse correlation between stock return and volatility.

Regarding the COVID-19 pandemic, numerous academic journals have already explored the effects of COVID-19 on stock markets. Yousef (2020) researched the effects of the corona virus outbreak on stock market volatility in the main stock market indices of G7 nations. The study used GARCH and GJR-GARCH models and found that the conditional variance of all seven indices of stocks within the G7 countries was significantly influenced positively by the coefficients associated with COVID-19 in the conditional variance equation. This finding provides additional evidence that Covid-19 has increased market volatility. In terms of the relationship between stock return and volatility, Chaudhary et al. (2020) have examined the impact of Covid-19 on both the return and volatility of stock market indices in the top 10 nations based on GDP by using the GARCH model. The findings indicate that throughout the first quarter of the COVID period (January 2020 to June 2020), consistently negative mean returns were observed in the daily performance of all market indices. While the second quarter of the COVID period displayed a bounce-back recovery across the market indices, the volatility level remained high compared to normal periods.

Another study by Liu et al. (2020) has focused on assessing the immediate effects of COVID-19 on twenty-one prominent stock market indices within highly impacted countries such as Korea, Japan, Singapore, the USA, Germany, Italy, the U.K., and others. The paper suggests that new confirmed cases during Covid-19 harm stock abnormal returns by employing an event study method. Specifically, Asian countries have experienced more pronounced negative abnormal returns than other countries. In contrast with the Liu et al. (2020) study, at the beginning of the pandemic, there was research done by Onali (2020), where they studied the impact of daily cases and related deaths in the first quarter of 2020 and used historical prices of the US stock market (S&P 500 and Dow Jones proxy) to conduct a Generalized Autoregressive Conditional Heteroskedastic model.

The study concluded that COVID-19 cases do not impact U.S. stock market returns. It was also supported by Sharif et al. (2020), who analyzed the relationship between the COVID-19 outbreak, geopolitical risk, oil price, economic uncertainty, and the U.S. stock market. The study reveals that the impact of the COVID-19 outbreak is more pronounced on U.S. geopolitical risk and economic uncertainty than its effect on the U.S. stock market. Furthermore, Narayan et al. (2021) examined the impact of government responses to the recent pandemic in G7 countries on stock market returns. The researcher demonstrates through the use of time series data that introducing travel restrictions, lockdowns, and economic stimulus packages resulted in favorable outcomes for the G7 stock markets, experiencing positive impacts.

Theoretical Framework

This paper examines the effects of global market risk on the risk-return profile of the Indonesian Financial Sector Index. To achieve this primary objective, we have broken it down into the following sub-objectives and hypotheses.

By studying these objectives, the paper aims to comprehensively understand the relationship between global market risks and the performance of the Indonesian financial sector, including the mechanisms behind this relationship.

Data and Methodology

The purpose of this study is to analyze the performance of Indonesia’s financial sector during two significant global market crises: the Global Financial Crisis (GFC) and the COVID-19 pandemic. To achieve this, the study uses a data sample consisting of the weekly return of the financial stocks index (IDXFINANCE) from the Indonesian Stock Index (IDX) between 2005 and 2022. The IDXFINANCE comprises 105 listed companies as of January 2023, providing a diverse and representative sample of the Indonesian financial sector.

To analyze the impact of COVID-19, the study uses the data from March 2, 2020, to December 2022, which signifies the COVID-19 period, while the period from December 2007 to March 2009 is selected to signify the GFC (Rahman et al., 2017). The COVID-19 period represents the ongoing impact of the pandemic on global financial markets, while the GFC period is widely recognized as the duration of the most intense impact of the GFC. By comparing these two distinct periods, the study aims to evaluate and contrast the impact of these worldwide market crises on Indonesia’s financial sector.

In this study, the IDX Finance return is calculated as the continuous compound return of:

where Xt represents IDX Finance return, Pt is the closing price of IDX Finance index return at time t, and Pt-1 is the closing price at one time before. The financial data including the price is calculated from the OSIRIS database.

To evaluate and model the volatility and returns of IDXFINANCE during the two crises, the study adopts the GARCH (Generalized Autoregressive Conditional Heteroskedasticity) framework, which is widely recognized for analyzing time-varying volatility in economic and financial time series. The use of the GARCH model is justified by its ability to capture volatility clustering and persistence, which are key characteristics of financial market data during crises. Specifically, this study employs the GARCH-M (GARCH with Mean) model, as proposed by Engle, Lilien, and Robins (1987). This model allows for the conditional variance (volatility) to directly influence the mean returns, enabling a nuanced analysis of the interrelationship between volatility and returns during periods of market turbulence.

The choice of the GARCH-M model is supported by its flexibility in modeling both the volatility and mean dynamics, making it particularly suitable for assessing the persistence of volatility and mean-reverting behavior in financial time series. Moreover, this approach has been successfully applied in prior studies of financial crises, such as Al-Rjoub and Azzam (2012) and Li and Kwok (2009), providing robust validation for its adoption in this study.

The GARCH (Generalized Autoregressive Conditional Heteroskedasticity) model is utilized to analyze the returns and volatility of IDX Finance during two episodes of crises. This framework is widely used in analyzing economic and financial time series and has proven effective in estimating stock market volatility in both developed and emerging markets. To be more specific, the authors of the study use the GARCH-M model (Generalized Autoregressive Conditional Heteroskedasticity with Mean), which allows for both the modeling of the volatility and mean dynamics, as well as capturing the persistence of volatility and any mean effects in the data. The GARCH-M model provides a flexible framework for accurately representing the dynamics in financial markets. The authors follow the approaches of Al-Rjoub and Azzam (2012) and Li and Kwok (2009) to analyze and forecast volatility in the Indonesian financial sector index (IDXFINANCE).

The basic GARCH model with p, q lags (GARCH p, q) can be written as:

with the mean Equation of:

where

In the GARCH-M framework, the conditional variance is incorporated into the mean Equation (2) to account for the potential effects of volatility on mean returns. The modified mean equation becomes:

To analyze the effects of the crises, two dummy variables (

Mean Equation:

Variance Eqution:

Here,

The use of dummy variables allows the study to isolate and quantify the effects of each crisis on IDXFINANCE returns and volatility. This methodology ensures that the model captures both the direct and indirect impacts of these global events, providing insights into the varying responses of the Indonesian financial sector to different crises. Table 1 provides a summary of the variables used in this study.

Variable Definitions and Measurements.

Empirical Findings

Descriptive Analysis

This study evaluates the effects of two significant global crises, namely the Global Financial Crisis (GFC) and the COVID-19 pandemic, on the volatility of the Financial Stock Index (IDXFINANCE) in the Indonesian Stock Market. The study utilizes weekly return data from 2005 to 2022. Before discussing the outcomes derived from the GARCH-M model, it is crucial to consider the descriptive statistics of IDXFINANCE during the two crisis periods.

Figures 1 and 2 display the volatility of IDXFINANCE during the observed periods in terms of both return and variance. These figures indicate that both the GFC and COVID-19 crises resulted in an increased level of volatility in IDXFINANCE. Figures 3 and 4 further substantiate this observation by demonstrating a higher variance during the crisis periods. During these periods, the data points appear to be more widely dispersed from the mean, indicating a higher degree of variability in the dataset.

IDX finance log return monthly (January 2005–December 2022).

IDX finance log return weekly (January 2005–December 2022).

IDX finance variance weekly (January 2005–December 2022).

IDX finance variance monthly (January 2005–December 2022).

These descriptive statistics suggest a high level of volatility during the two crisis periods. However, it is important to note that the volatilities of the return and variance of IDXFINANCE were more significant during the GFC period (December 2007–March 2009) than during the COVID-19 period (March 2020–December 2022).

The implications of these descriptive statistics for the estimation of the GARCH-M model are substantial. The high volatility observed during the crisis periods and the differences in volatility between the two periods provide a rich context for the GARCH-M model to capture and quantify the time-varying volatility. This allows for a more nuanced understanding of the impact of global crises on the volatility of the Indonesian financial sector. As a result, the model can provide valuable insights into the sector’s resilience and vulnerability in the face of global financial shocks.

Furthermore, the authors carry out several diagnostic tests for the specified model in Equations (5 and 6) to validate their appropriateness for the study. First, the author computed Engle’s Lagrange Multiplier (L.M.) test to check the existence of ARCH (autoregressive conditional heteroskedasticity) effects in the specified model. In addition, the author also checks the normality of the data to select the appropriate distribution assumption when running the model by verifying the skewness of the kurtosis. Results for these two tests are presented in Table 2 and Table 3.

Lagrange Multiplier Test for ARCH Effect.

Source: Authors calculations.

Skewness and Kurtosis Tests for Normality.

Source: Authors calculations.

Estimates of the L.M. test in Table 2 indicate significant autoregressive conditional heteroskedasticity (ARCH) effects in the model in all three lags tested. This result suggests that the volatility of the disturbances is not constant over time but rather varies and is influenced by past volatility levels. The result also indicates the presence of conditional heteroskedasticity in the data and autocorrelation in the squared residuals. Therefore, a simple OLS model is inappropriate for achieving the study objectives. Adopting GARCH-M (1,1) as per Equation 6 is justified as it can help capture and model these time-varying volatility patterns more accurately.

Meanwhile, Table 3 shows the result of a joint test for normality on the residuals. Probabilities associated with the residuals’ skewness and kurtosis are represented by the “Pr(skewness)” and “Pr(kurtosis)” values, given that both probabilities in this situation are reported as 0.000, with the test statistics’p-value significant at the 5% level. It could be concluded that the residuals do not follow a symmetric and normally distributed pattern. Thus, the authors will assume that the errors follow Student’s t distribution in the GARCH-M estimations.

Empirical Results and Discussions

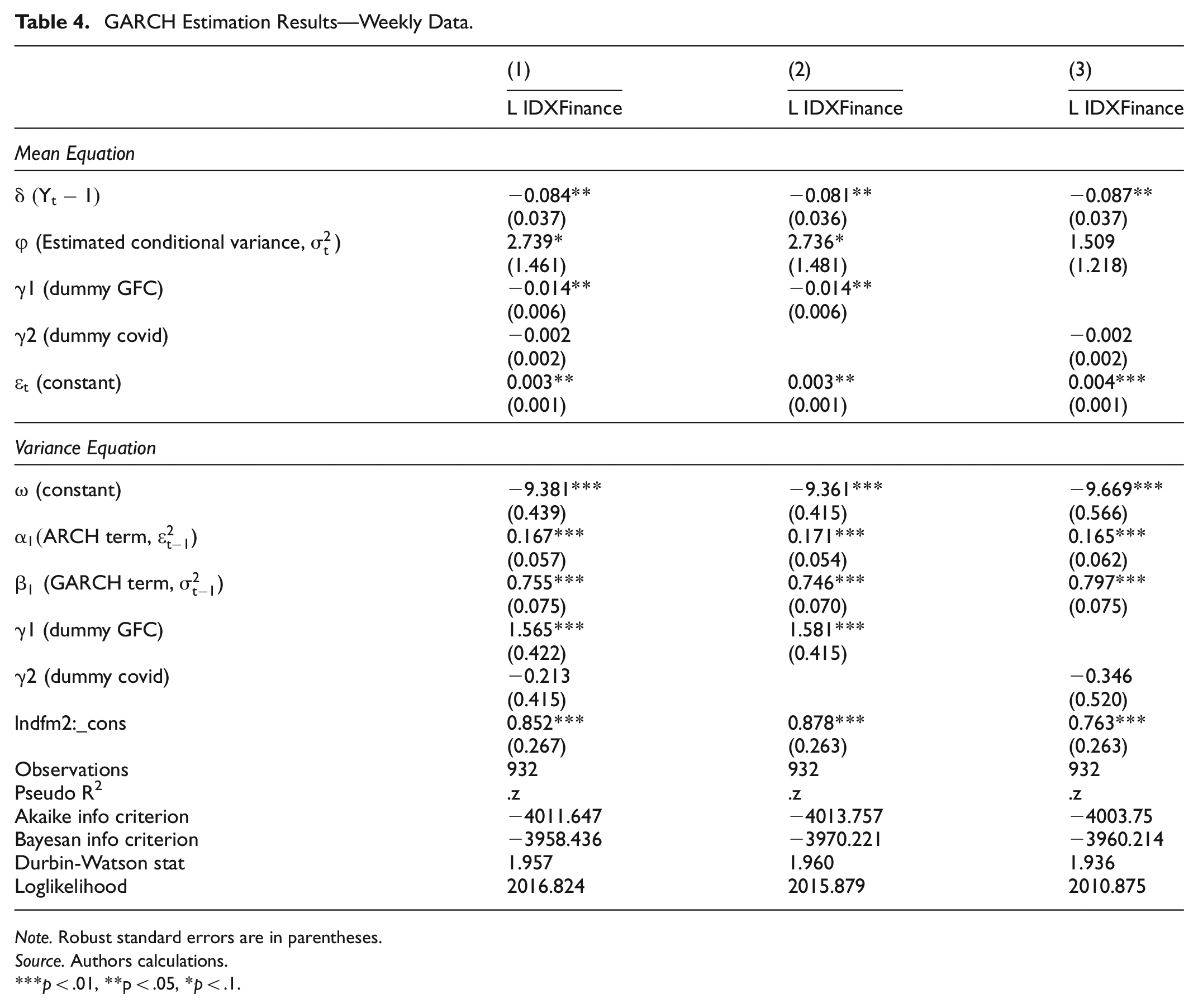

Table 4 presents the results of the estimation of the GARCH-M model using weekly return data from IDXFINANCE. The author included the GFC and COVID-19 dummies in the mean and GARCH-M equations in the first model, specified in Equations 5 and 6. The estimation was conducted for Model 1. However, in Model 2, only the GFC dummy variable was included, while in Model 3, only COVID-19 was included.

GARCH Estimation Results—Weekly Data.

Note. Robust standard errors are in parentheses.

Source. Authors calculations.

p < .01, **p < .05, *p < .1.

The coefficients of the GFC dummy (

These findings align with Alshubiri (2021), who observed that financial crises originating from the financial sector, such as the GFC, tend to cause more pronounced and persistent volatility compared to crises with broader economic origins, such as COVID-19. Similarly, Sufian and Habibullah (2016) emphasized that the GFC had a direct and detrimental impact on bank performance in Indonesia, leading to prolonged instability within financial markets. These studies corroborate the observation that crises linked to systemic financial disruptions lead to heightened volatility.

The coefficient of the lag index (

The variance equation of the three models shows that the sums of ARCH and GARCH parameters are close to one (0.922, 0.917, and 0.962), implying that the shocks generated by the GFC and COVID-19 crisis to the conditional variance were highly persistent. The highly significant GARCH terms (0.755, 0.746, and 0.797) in all models suggest that there was variance clustering during the crises, where volatility tended to be high for a prolonged period. This result also indicates that the GARCH model is a superior forecasting model to a simple OLS or ARCH model in periods of high volatility.

This persistence of volatility, particularly during the GFC, is consistent with the findings of Alshubiri (2021), who noted that financial disruptions often exacerbate inefficiencies in financial institutions, resulting in prolonged periods of instability. The variance clustering observed in this study supports the notion that heightened risk perception during financial crises leads to enduring market volatility.

In the variance equation, the GFC dummy coefficients (

The lower impact of COVID-19 on volatility aligns with Alshubiri (2021), who found that financial markets in GCC countries experienced relatively moderate portfolio fluctuations during the pandemic due to improved regulatory measures implemented post-GFC. This suggests that lessons learned from previous crises contributed to more stable market conditions during COVID-19.

The GARCH-M estimations indicate that there was a highly volatile period during the GFC from December 2007 to March 2009 and the COVID-19-induced crisis period from March 2020 to December 2022. The coefficient of GARCH terms was highly significant, reflecting this volatility. The study found that the GFC had a significant negative impact on stock returns and that there was high volatility clustering during the crisis, resulting in increased volatility of IDXFINANCE returns. In contrast, the impact of the COVID-19 crisis on stock returns and volatility was less pronounced than that of the GFC. As a result, it can be concluded that the impact of the GFC on the stock returns and volatility of IDXFINANCE was greater than that of COVID-19. The results of the study confirm the hypothesis that there are differences and gradations of magnitude between the two major crises, the GFC and the COVID-19-induced crisis, in terms of their impact on the Indonesian financial stock index returns and volatility.

The difference in the impact of the GFC and the COVID-19 pandemic on the volatility of IDXFINANCE can be attributed to the nature and origin of the crises. The GFC began in the financial sector, specifically within the housing market in the United States, and quickly spread to other sectors and across global markets due to the interconnectedness of the global financial system. Financial institutions worldwide were directly impacted, leading to a significant increase in market volatility. This is reflected in the GARCH-M estimations, which significantly negatively affected stock returns and high-volatility clustering during the GFC.

On the other hand, the COVID-19 pandemic is a health crisis that indirectly affected the financial sector. The pandemic led to widespread economic disruptions due to lockdowns, travel restrictions, and changes in consumer behavior. However, its impact on the financial sector was less direct than that of the GFC. Financial institutions were not the epicenter of the crisis. While the pandemic caused economic uncertainty and market volatility, its impact on IDXFINANCE returns and volatility was less pronounced.

Furthermore, governments and financial institutions’ responses to the two crises were also different. The lessons learned from the GFC led to improved financial regulations and crisis management strategies, which may have helped mitigate the impact of the COVID-19 crisis on the financial sector.

These findings underscore the importance of tailored crisis management strategies, as highlighted by Sufian and Habibullah (2016), who emphasized the critical role of regulatory frameworks in reducing the systemic risk posed by financial crises. By adopting these measures, markets can better withstand the adverse effects of global disruptions.

In conclusion, the differences in the origins, nature, and responses to the GFC and the COVID-19 pandemic can explain why the GFC had a greater impact on IDXFINANCE returns and volatility. These findings underscore the importance of understanding the specific characteristics and dynamics of different crises when assessing their impact on financial markets.

Validations and Robustness Checks

The authors confirm the main results with several validations and a robustness check. First, we run several diagnostic tests and compare different specifications to validate the main model in Equation 5 and 6. The reported Durbin-Watson statistics for serial correlation in Table 4 also suggest that all models are serial correlation-free. Combined with the ARCH-LM test calculated in the previous section (Section 4.1 Table 2), to examine the existence of ARCH terms in residuals, both diagnostic tests suggest that all models (Model 1, Model 2, and Model 3) are correctly specified. Second, three different test statistics are carried out to compare Model 1, Model 2, and Model 3. These are the Loglikelihood ratios, Akaike’s information criterion (AIC), and the Bayesian information criteria (BIC). As reported in Table 4, in all requirements, Model 1 is superior to Model 2 and Model 3.

Furthermore, in our primary analysis, we use the weekly return data model to investigate the impact of the two crisis episodes on the IDXFINANCE return and volatility. To test the robustness of our findings, we employ monthly and daily data in the estimations instead of weekly data (Patrocinio et al., 2024). The results of our robustness check in Table 5 and Table 6 confirm the results of our primary analysis using weekly data. The market crisis has adversely affected the return and increased volatility of the Indonesian Financial Sector Index. Model 1 estimations using monthly data and daily data show that the coefficients of dummy GFC and dummy covid in the mean Equation are negative (GFC = −0.076 and −0.003, COVID-19 = −0.003 and −0.001), with highly negative significance in GFC dummy. Likewise, the dummy GFC and COVID-19 in the variance equation are primarily positive and significant for the dummy GFC. However, the dummy COVID is negative but insignificant in the monthly and daily data. All in all, the robustness checks confirm the acceptance of our hypotheses 1, 2, and 3.

GARCH Estimation Results—Monthly Data.

Note. Robust standard errors are in parentheses.

Source. Authors calculations.

p < .01, *p < .1.

GARCH Estimation Results—Daily Data.

Note. Robust standard errors are in parentheses.

Source. Authors calculations.

p < .01, *p < .1.

Policy Implications and Recommendations

The findings of this study highlight the need for robust policy measures to mitigate the adverse effects of global crises on financial markets. Strengthening financial regulation and oversight is essential, as the significant impact of the GFC underscores the vulnerabilities within the financial sector. Policymakers should enhance macroprudential regulations, enforce stress-testing requirements, and strengthen capital adequacy standards, particularly for institutions with high exposure to volatile sectors.

Transparency and timely dissemination of information are equally crucial to reducing market volatility. Regulators should mandate accurate and prompt reporting by financial institutions and develop centralized platforms for real-time market data dissemination to minimize information asymmetry, particularly in emerging markets like Indonesia. Tailored regulatory responses, such as Indonesia’s credit restructuring policies during COVID-19, demonstrate the importance of adaptive frameworks to address unique crisis characteristics. Expanding such measures to include other affected sectors can further stabilize the financial system.

Encouraging innovation within the financial sector can also enhance resilience. Technology-driven risk management tools and improved financial literacy programs can equip stakeholders to better navigate market uncertainties. Additionally, localized approaches to policy-making are necessary to address regional disparities. For example, region-specific tax relief and liquidity support for crisis-affected industries can prevent prolonged economic downturns.

Finally, improving crisis preparedness through early warning systems and international coordination can strengthen financial markets’ resilience. The greater impact of the GFC compared to COVID-19 underscores the need for proactive measures to detect emerging risks and foster global collaboration. By implementing these recommendations, policymakers can build a more resilient financial ecosystem capable of withstanding future global shocks while promoting stability and growth.

Conclusion and Limitations

In conclusion, our results provide valuable insights into the impact of the GFC and COVID-19 crises on financial sector stock returns and volatility. The analyses indicate that the GFC crisis had a significant adverse effect on stock returns, as evidenced by the significant coefficients of the GFC dummy variables in both the first and second models. In contrast, the impact of the COVID-19 crisis on stock returns was found to be less pronounced, with none of the COVID-19 dummy variables being significant across all three models. This phenomenon occurred because the Global Financial Crisis (GFC) predominantly originated and affected the financial sector, whereas the Covid-19 pandemic does not possess a similarly centralized impact. Furthermore, the Indonesian government has issued a policy to provide national economic stimulus by implementing Financial Services Authority Regulation No.11/POJK.03/2020 to encourage the optimization of the intermediary banking role (Disemadi & Shaleh, 2020). This policy outlines the existence of credit restructuring by ensuring that the quality of restructured loans can be determined without interruption if they are extended to debtors identified as being impacted by the spread of COVID-19. Hence, with the implementation of the credit restructuring policy, the impact caused by COVID-19 can be mitigated in the banking sector.

This study may also have some limitations. First, the analysis is based on a specific dataset and period. Hence, the findings may not be applied to other markets or timeframes. Readers are advised to proceed with due diligence when applying the findings to different circumstances. Second, the chosen model and methodology have inherent limitations and assumptions. Thus, it is recommended that alternate specifications be investigated to verify the robustness of the findings, as other modeling methodologies may yield different results.

Future research could explore the impact of past financial crises on the Indonesian financial sector and different sectors within the economy. Further investigation with additional variables beyond GFC and COVID-19 dummies could provide a more comprehensive understanding of the factors affecting stock returns. It’s important to note that the study’s findings are based on historical data, and future market conditions may differ significantly. Therefore, caution should be exercised when using the results to make investment decisions or forecasts for future market trends. Exploring other factors that may influence IDXFINANCE returns, such as macroeconomic indicators, policy changes, and global economic trends, with other econometric models, could also be beneficial.

In conclusion, the study’s results highlight the importance of having robust financial regulations and crisis management strategies in place to enhance the financial sector’s resilience to global crises. For stakeholders in the financial sector, effective risk management strategies are crucial during crises.

Footnotes

Acknowledgements

We extend our gratitude to the Editor and anonymous reviewers for their invaluable insights and constructive suggestions, which have significantly enhanced the quality of the manuscript. Additionally, we wish to acknowledge that a certain section of the paper underwent editorial and grammatical review with the aid of an AI tool, specifically a Large Language Model (LLM) known as ChatGPT. This AI assistance played a role in enhancing the clarity and coherence of the manuscript.

Author Contributions

The authors have contributed to this manuscript as follows: Mohamad Ikhsan Modjo contributed to topic and idea generation, manuscript writing, and data analysis. Clara Calista was responsible for data collection, data analysis, manuscript writing, and conducting robustness tests. Gatot Soepriyanto worked on the final revision, ensuring consistency, and providing theoretical analysis. All authors have reviewed and approved the final version of the manuscript.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

We obtained the data from Indonesia Stock Exchange website, firm’s annual report and relevant public information. The authors performed further calculations. The data and necessary code are available upon request (in a good faith and fair use).