Abstract

Chinese financial institutions continue to encourage digital transformation in the context of the digital economy, which may impact their operations. This paper analyses the impact of bank digital transformation on operational performance based on the characteristics of the bank’s digital transformation from the surface to the inside, further explores the operation mechanism from the perspective of asset operation efficiency and industry competition, and empirically examines the sample data of 39 listed commercial banks from 2012 to 2021. The findings indicate that digital transformation is beneficial to enhancing bank operational performance, which is influenced by the ownership and location of banks. Digital transformation mainly promotes business performance by increasing the efficiency of bank asset operations. Increased bank competition weakens the impact of digital transformation on business performance. As a result, commercial banks must identify their digital ambitions and improve their digital capabilities by their endowments. The government must strengthen its regulatory framework, data governance, and talent training and retention mechanisms.

Keywords

Introduction

The potential value of the digital economy has been consistently investigated in recent years. The digital economy is critical to achieving high-quality economic development and stable growth, particularly in public health emergencies, demonstrating strong resilience and vitality and reducing economic downward pressure (Mansour, 2022). China has issued a series of digital transformation policies that have been systematically implemented to gradually encourage the growth of digital industrialisation and industrial digitalisation and to figure out a way for financial institutions’ digital transformation. At the same time, big data, artificial intelligence, and other technologies are reshaping the face of the banking industry, the layout of Internet enterprises’ financial business has brought an impact on traditional banking business, and commercial banks are actively carrying out digital transformation to seek new development (Lotriet & Ditshego, 2020). However, because digital transformation is a long-term process affected by their conditions and other factors, banks face several challenges, including the contradiction between the ineffectiveness of digital transformation and the irreversibility of the digital trend, as well as a mismatch between business needs and their capabilities (Trang et al., 2022). The impact of banks’ digital transformation needs to be demonstrated further. Simultaneously, analysing the mechanism of digital transformation on business performance can help to understand the essence of digital transformation deeply, avoid entering the digital transformation black box, avoid transformation in form and on the surface, and play the role of digital empowerment to promote high-quality bank development.

Currently, research on digital transformation is conducted from both the macro and micro levels. For society, digital transformation is a micro embodiment of China’s digital economy’s high-quality development, which can give rise to new business forms and models, create more employment opportunities, adjust the employment structure, and expand the demand for digital talents (Hjort & Poulsen, 2019). When the substitution effect of technology is greater than the job creation effect, digital transformation raises labour income (Li et al., 2023). However, when digital technology outperforms labour, labour substitution reduces labour income, causing an employment crisis and a drop in consumption (Acemoglu & Restrepo, 2019).

For enterprises, digital transformation is more than just integrating technology into business processes; it involves a fundamental organisational change (Pertusa et al., 2010). Digital transformation can improve an enterprise’s internal organisational structure and decision-making process (Liu et al., 2020). Enterprise digital transformation can foster enterprise innovation by reorganising superfluous resources and enhancing resource utilisation efficiency (Wang et al., 2023), improving enterprise quality and efficiency (M. Liu et al., 2023). At the same time, industry competitive pressures can be translated into forces for bank digitisation, thus amplifying the financial effects of digitisation. Bank business performance is also affected by the bank’s size; the larger the bank, the more significant the positive impact of digital transformation on bank performance (Liu et al., 2023a). Digital transformation can promote the productivity of financial services enterprises; Digital transformation improves the cost-plus ratio of enterprises by reducing marginal costs (Yaser & Mohammad, 2022; Zuo et al., 2021). Another substantial impact of digital transformation is reducing information barriers (Z. Y. Chen et al., 2023). Enterprise digital transformation broadens access to information and improves information processing ability, allowing it to keenly perceive external economic policy uncertainty and minimise business risks (Tian et al., 2022). However, internal workflow changes brought about by digital technology in management activities need to match the capabilities of employees and managers, which can trigger a holistic dissonance and raise the difficulty and cost of management.

In the study of the factors influencing bank business performance, scholars believe that the development of digital finance realises accurate matching of financial resources, reduces communication costs, breaks time and space constraints, positively affects bank business performance (Xie & Wang, 2023), and improves the efficiency of digital investment (Zhu & Jin, 2023). Digital transformation can reduce risk-taking (Al Shanti & Elessa, 2023), alleviate information asymmetry, increase resource allocation efficiency (Beck et al., 2018), improve service quality (Al Shanti & Elessa, 2023; Zhu & Jin, 2023), and lowering service costs (Agarwal et al., 2010). However, due to the underlying fintech’s significant investment and slow effect, the impact on bank business performance shows “U-shaped” (Dahl et al., 2017). In the late stage of fintech development, banks will experience the phenomenon of homogenisation of products and services, coupled with increased risk exposure, adversely affecting the bank’s business performance and profitability (Gupta et al., 2018). Market competition impacts bank operating performance; when market concentration decreases and industry competition increases, it helps improve bank operating performance, and competition is conducive to enhancing bank cost efficiency (Chan et al., 2015). At the same time, industry competitive pressures can be translated into forces for bank digitisation, thus amplifying the financial effects of digitisation (Zeng et al., 2022). Bank business performance is also affected by the bank’s size; the larger the bank, the more significant the positive impact of digital transformation on bank performance (Trang et al., 2022).

More research on the impact of financial technology and digital financial inclusion on business performance was discovered by reviewing the literature. Although digital transformation is also about innovation through technology, it is not only about innovation in products and services but also focuses on penetrating digital concepts from the outside to the inside. Regarding the impact of digital transformation on banks, the research mainly focuses on risk-taking, financing enterprise performance, labour force, etc., and the research on the effect on their business performance involves less. It does not form a unanimous conclusion, which still has room for further study. In light of this, this paper examines the impact of bank digital transformation from a theoretical perspective, and we use text analysis to construct the digital transformation index and empirically test the effects of digital transformation on business performance and the role of the mechanism using data from 39 listed banks from 2012 to 2021. Selecting data from 2012 to 2021 as the research subject is due to the widespread adoption of smartphones after 2010, which led to the gradual rise of mobile banking apps, marking the beginning of banking digital services in the information age. Following this, large banks faced the need for process-oriented transformation, aiming for flat management goals, and underwent a reorganisation of their organisational structures. This coincides with the digital management of organisations mentioned in this article. Therefore, this article takes data from after 2012 as the research subject for studying banking digital transformation.

In comparison to previous studies, this paper may make the following contributions: (1) analyse the impact of digital transformation on commercial banks’ business performance from three perspectives: business, organisational operations, and business model digitalisation, to assist banks in understanding the nature of digital transformation, avoiding the black box of digital transformation, and better playing the role of digital empowerment. (2) The text analysis method is used to measure the digital transformation index of banks. Specifically, the word frequency statistics of banks’ annual reports are used to build a vocabulary of features in the dimensions of “technology foundation” and “digital technology application,” and the statistical word frequencies are standardised to eliminate the influence of industry factors and improve the accuracy of the estimation. (3) Examine the influence of digital transformation on business performance from the standpoints of asset operation efficiency and bank competitiveness to enrich the theoretical mechanism of digital transformation’s impact.

Theoretical Mechanism And Research Hypothesis

Digital Transformation And Business Performance Of Commercial Banks

Banks’ digital transformation has the characteristics of moving from the outside to the inside and from the surface to the inside, starting with digital innovation of frontend products and services, then moving to operation management and organisational structure innovation, and finally presenting business model innovation (Abdulquadri et al., 2023).

To begin, business digitalisation is a method for banks to encourage the integration of digital information technology with business operations to achieve innovation. Emerging technologies create new products and services for banks by breaking industry and business boundaries, cooperating with other technology companies, and engaging in open innovation (Agboola, 2019). By providing banks with new ways of supplying products and services, digital transactions can break the constraints of space and time and the limitations of the bank account and provide financial services. Digital technology alleviates the problem of information mismatch, expands the scope of financial services, and brings significant economic benefits to banks. From the asset business, digital technology accurately captures customer transaction behaviour, identifies customer information, and predicts market demand and customer behaviour through algorithms (Liberti & Petersen, 2019), thus expanding the scope of services (Liu et al., 2023b). From the liability business, banks changed the form of fixed and lower deposit rates in the past, used data intelligence analysis to accurately locate user needs, tap potential customers, used big data to build models to analyse the reasons for customer loss, and make timely adjustments to retain customers (He et al., 2019); From the intermediate business, the application of digital technology has, to a certain extent, innovated the products, channels, and processes of intermediate business, while the innovation of bank intermediate business is conducive to expanding the scope of intermediary business, optimising the structure of income, and improving the profitability of banks.

Second, organisational operations are being digitalised. With online business development, physical outlets have become intelligent and digitalised, lowering bank operating costs, such as explicit costs. The application of digital technology within the bank is conducive to realising the real-time and transparent activities of internal departments (Tian et al., 2023), lowering the cost of supervision, avoiding some agency problems, and improving the efficiency of bank operations. Digital technology accelerates the diffusion and dissemination of information and passes product information to consumers through online platforms, which reduces the dual search costs, such as hidden costs, of banks to customers and customers to products. In terms of risk-taking, banks utilise blockchain technology for distributed storage of shared customer information, big data to assess the creditworthiness of customers, and artificial intelligence for machine learning to operate risk control management, thus improving risk-taking capacity and risk screening (Wu et al., 2023); On the other hand, risky behaviours are monitored in real-time under digital technology, and the information becomes more transparent (Ji et al., 2022), which means that the default cost rises during the transaction process, lowering the likelihood of default (Cheng & Qu, 2020).

Enterprise digital transformation affects production capacity through innovation-induced (Ma et al., 2022) and organisational decentralisation. In terms of organisational structure, the digital transformation of commercial banks makes the organisational structure tend to be modular, flat, and agile (Berg et al., 2020). A flat organisational structure improves communication efficiency between departments, making decision-making more flexible and efficient, thus enhancing the bank’s ability to cope with external risks. Furthermore, banks are gradually moving deeper and deeper from organisational restructuring to data and organisational coherence to improve organisational resource flexibility. When the external environment changes, resource flexibility can meet the bank’s resource needs and lessen the risk of resource shortages (Yang et al., 2021). Digital transformation increases the bank’s demand for technical personnel, which can optimise the enterprise’s human capital structure (Wu & Yang, 2022), avoid employee redundancy in the bank (Acemoglu & Restrepo, 2019), save operating costs (Chen & Xu, 2023), and improve commercial banks’ business performance (Zhou & Xu, 2023).

Finally, business models are becoming digitalised. The impact of digital transformation on enterprises is a process that progresses from “empowerment” to “enabling,” and “enabling” innovation is the process of applying digital technology to multiple aspects and fields of operation and management to promote business model innovation and value creation (Yang et al., 2021). Digital technology and business integration to create value and increase competitiveness is a digital business model. The bank’s business model has shifted from the traditional concept of “selling products” to the digital concept of “platform + scene,” with a greater emphasis on generating complex digital ecological scenes and a focus on non-financial scenes (Boot & Hoffmann, 2021). Banks have begun to tap into the connotation of digital ecology, from the initial salinisation of business at the retail end and the construction of smart outlets, gradually expanding to the creation of customer-centred online, non-financial service scenario platforms, tapping into areas closely related to people’s lives, and integrating financial products into them, to satisfy the needs of people’s better lives. The core logic is that banks differentiate themselves based on their resource endowments, create financial and non-financial one-stop services through high-quality products, strengthen the correlation between the bank and its customers, and obtain more user traffic to create value and achieve a win-win situation. Combining the above analyses, the research hypothesis H1 is proposed (Verhoef et al., 2019).

Bank Digital Transformation, Asset Operation Efficiency, And Business Performance

Commercial banks serve as intermediaries in the deployment of funds in the financial system, and their value creation is produced through rational resource allocation. The allocation of resources by the bank is mainly reflected in the operating efficiency of assets. The digital transformation of banks employs digital technology to broaden business channels, create diverse income institutions, and improve fund absorption capacity; it employs emerging technology to mine users’ basic information, credit status, and consumption behaviour; it combines with machine learning technology to process as structured data, reduce information asymmetry, and identify ex-ante risks and process risks; and it tracks and supervises the use of loans, realises 24-hour mobile supervision, and creates an intelligent risk early warning system in the process of lending to reduce the rate of bad debts of assets, and maximise the security of funds. Reducing banks’ various operating costs also means that banks can maximise the value of their investments. The increased utilisation efficiency of the bank’s assets means that the bank’s loan business’s interest income rises and the alarming debt rate falls, boosting the bank’s operating performance (Cheng et al., 2022). Combining the above analysis, the following research hypothesis H2 is proposed Figure 1.

The impact of banks’ digital transformation.

The Moderating Role Of Bank Competition

Internal and external factors of banks jointly determine bank competition. Internal factors are the individual characteristics of banks, including banks’ internal resources, business strategies, business capabilities, etc.; external factors include the competition among peers and the competition of fintech companies outside the industry that banks face. The bank’s profit margin will decrease as competition increases, primarily because the deposit and loan spread space is shrinking. The intensification of external operational risks will also make bank managers’ decision-making behaviour more cautious and reduce the bank’s efficiency. Due to limited market resources, regulatory authorities will place additional regulatory pressure on the bank’s business behaviour to avoid violent competition (Tabak et al., 2016). As a result, banks undergo digital transformation, the profit margin of their main business is limited, and the innovative activities of banks will be limited under the cautious psychology of managers and strict supervision of regulators. However, digital transformation is primarily the use of digital technology to carry out various degrees of innovative behaviour, and thus, the effect of digital transformation on banks will be affected; that is to say, the impact of digital transformation on company performance will be weakened in the high degree of bank competition. Combining these analyses, the research hypothesis H3 is proposed.

Research Design

Data Source

Given the incomplete disclosure situation of small and medium-sized banks, while the disclosure of listed commercial banks is more comprehensive and standardised, and the annual reports are easily accessible, this paper chooses 39 commercial banks listed on China’s A-share market as the research object, including five state-owned banks, nine joint-stock banks, 15 city commercial banks, and ten agricultural and commercial banks. The period of data from 2012 to 2021 is chosen as the research sample. The data were obtained from the CSMAR database and China Currency Network, and some missing values were filled in by looking up the financial statements of banks and the interpolation method. Stata15.1 was used to analyse the data.

Description of Variables

Explanatory Variables

The explanatory variable in this research is commercial bank operating performance. Based on the existing literature, there are several main methods to measure operational performance: one is to use a single indicator from the profitability or security perspective. The other is to select multiple indicators from different dimensions to construct a system of operating performance indicators and then assign them to get the final value, for example, Khader (2013) in analysing the impact of operating performance of commercial banks in Palestine, measured financial performance from three dimensions, internal, market, and economic, respectively: total return on assets (ROA) to measure the internal performance, Tobin’s Q value to measure the market performance, and economic Value Added (EVA) to measure financial performance. The disadvantage of this method is that autonomous empowerment has a subjective solid colour. Additionally, some studies synthesise multiple indicators that can reflect bank operational performance into one indicator by using principal component analysis to reduce the dimensionality of the indicator. Still, it is challenging to explain practically the changes in this indicator. This paper uses return on total assets (ROA) as the explanatory variable. The banking industry has a high gearing ratio, and the return on total assets (ROA) reflects the ability of banks’ total assets to be converted into net profit, which can be a better measure of banks’ operating performance considering their liabilities. It can also respond to their competitiveness and development ability. So, this paper chooses ROA as an explanatory variable. Furthermore, by the “Commercial Bank Performance Evaluation Measures” issued by the Ministry of Finance, this paper replaces ROA with net profit per capita to perform the robustness test. It measures operational performance from the perspective of human capital structure. The higher the net profit per capita represents, the higher the value created by the bank’s employees and the better the operational performance.

Core Explanatory Variables

The digital transformation index of commercial banks is the primary explanatory variable in this paper, referring to the method of Wu Fei et al. (2021), who used text analysis to measure the digital transformation index of enterprises and assessed the degree of digital transformation of banks through statistics and standardisation of the frequency of relevant keywords in the bank’s annual report. The more significant number of keywords appearing in the annual report indicates that the bank pays more attention to digital transformation. The higher the number of keywords in the annual report, the more importance the bank attaches to digital transformation and the higher the level of digitalisation. The measurement of digital transformation indicators can be roughly divided into three steps: first, crawl the bank’s annual report. The annual reports of enterprises summarise and guide, reflecting the strategic goals and visions of enterprises, and can indicate the concept of digital transformation and the digital status of enterprises. Therefore, this paper takes the annual reports of commercial banks as the object of analysis and uses Python crawler technology to download the annual reports of banks in bulk from China Currency Network and then extracts the information related to digital transformation. Second, build a keyword thesaurus. From the two levels of “application of underlying technology” and “application of technology in practice,” we make a thesaurus of digital transformation features. The underlying digital technologies applied in banking include big data technology, artificial intelligence technology, cloud computing technology, and blockchain technology, and expand to specific applications of these technologies in practice. Adding to Wu Fei’s study, the final vocabulary constructed is shown in Table 1. Finally, the critical information in the annual report is extracted from the generated feature word thesaurus. The downloaded annual report text is read and cleaned, and the material is precisely partitioned, identified, and extracted using the Jieba partitioning module, and keywords such as “none,”“didn’t,” and “don’t” are removed before the keywords. The frequency of keywords is categorised by “Big Data Technology,”“Artificial Intelligence Technology,”“Cloud Computing Technology,”“Blockchain Technology,” and “Digital Technology Application.”

Keyword Thesaurus.

Since the digital development of banks is closely related to external competition and market uncertainty, simple absolute numbers of word frequency statistics are not persuasive, so they are standardised in this paper. Referring to the study of Lou Yong and Liu Ming (2022), this paper takes the weight of the word frequency of the same kind of keywords in each bank’s annual report to the total word frequency of the same type of keywords in all the sample yearly reports of that year as a measurement index. The formula for calculating the same kind of keywords is as follows:

The resulting percentage of each type of keyword is summed up to get the final indicator of commercial banks’ degree of digitalisation.

Intermediary Variable

This paper investigates whether asset operation efficiency mediates commercial banks’ digital transformation and how it affects operation performance. The total asset turnover ratio reflects the bank’s operational quality and efficiency of asset utilisation. A higher total asset turnover ratio indicates that the bank’s assets are efficiently utilised, the cost of idle assets is reduced, and the bank’s operating capacity is more robust. Therefore, the total asset turnover ratio can be used as a proxy variable for the operational efficiency of assets. The non-performing loan ratio is the proportion of bank loans rated as substandard, doubtful, or loss to the total loans, which can measure the level of risk faced by the bank, and the higher the non-performing loan ratio, the greater the risk borne by the bank’s operation.

Moderator Variable

The moderator variable in this paper is the degree of bank competition. Bank competition was divided into internal and external. Internal competition is the competition within the traditional banking industry, and external competition refers to the impact outside the sector brought about by FinTech companies. Bank competition can be measured in two ways: structurally and non-structurally. Structural measurements include the market concentration ratio (CR) and the Herfindahl index(HHI), while non-structural measurements include the Panzar-Rosse model and the Lerner index. In this paper, the Lerner index (Lerner) is chosen to measure the competitive behaviour of banks directly, and the ability of banks to obtain excess profits is used to determine the degree of competition; the specific formula refers to the study of Tang Wenjin et al. (2016), which is expressed as:

Where

Where TC is the total cost, including interest expense, labour cost, and capital cost; TA is the bank’s output, expressed as total assets; W1, W2, and W3 are the bank’s funds, capital, and labour costs, respectively, with W1 being expressed as interest expense over total deposits, W2 being expressed as operating costs, net of personnel expenses, as a percentage of the bank’s fixed assets, and W3 being expressed in terms of staffing expenses compared to the number of employees. Trend denotes technological change and takes values from 1 to 10 for 2012 to 2021.

Control Variables

Banks with large asset sizes have stable production and operation, strong risk-bearing ability, a dominant position in the industry, a wide range of business operations, and many profit channels, so they show better business performance. Loan interest income is the primary source of business income for banks, the deposit-to-loan ratio and the share of non-interest income reflect the utilisation of funds and the income structure of banks, respectively, and the cost-to-income ratio and the capital adequacy ratio reflect the operating costs and risk-bearing capacity of banks, respectively. All of the above have an impact on the operating performance of banks. Employee skill level refers to the educational structure of bank employees; the higher the level of education, the more innovative potential the bank has and the more excellent economic value it can create. The macro level controls the ratio of money supply to GNP. Therefore, this paper takes asset size, deposit and loan ratio, non-interest income ratio, cost-income ratio, capital adequacy ratio, employee education level, and money supply/GNP as control variables Table 2.

Definitions of Variable Indicators.

Modelling

This paper uses panel data for empirical analysis, which has time series and cross-section duality. To test hypothesis 1, whether the digital transformation of commercial banks promotes business performance, this paper constructs the following regression model 1:

Where

This paper uses the mediation effect to test the mechanism of digital transformation on bank business performance. To test hypothesis 2, whether the asset operating efficiency plays a mediating role in the digital transformation process promoting bank operational performance, based on model 1, the following model is constructed to test the mediation effect.

Under the condition that hypothesis 1 holds, if

This paper applies the moderating effect model to test whether the relationship between banks’ digital transformation and operational performance is affected by banks’ competitive pressure. Model 4 is constructed to test hypothesis 3; the independent variables and moderating variables are centred, and the interaction terms of the independent variables and moderating variables are added based on Eq. 5 to test whether the coefficients of the interaction terms are significant and if they are substantial, it means that there is a moderating effect, and vice versa, it does not exist. In addition, the samples were divided into two groups according to the values of the moderating variables, and group regressions were performed to test the consistency of the results.

Analysis of Empirical Results

Descriptive Statistics

In this paper, panel data of 39 commercial banks for the period 2012 to 2021 with a sample size of 390 is created. Firstly, preliminary descriptive statistics of all the variables are carried out by stata15.1 to observe the maximum, mean, and overall dispersion of the data, and the results are shown in Table 3.

Descriptive Statistics.

From the statistical results, the explained variable is the operational performance of the bank, the minimum value of the mean of the return on total assets (ROA) is 0.455, and the maximum value is 2.450, which indicates that there is a significant gap in the operational performance of commercial banks; the standard deviation of ROA is 0.245, which is relatively small, indicating that the mean value of 0.975 of the ROA is a better reflection of the overall level of the operational performance of commercial banks.

The explanatory variable is digitization level (DIG) with a mean of 0.128 and a standard deviation of 0.206, which indicates that the selected sample does not have a significant gap in digitization level. However, the minimum value of the digitalization level is 0, and the maximum value is 2.444. From this, it can be seen that even though commercial banks pay attention to digital transformation, some banks have started digitalization late and need to be more digitalized.

Among the mediating variables, the mean value of Turnover of Assets (TAT) is 0.025 with a standard deviation of 0.005, which indicates that the mean value of the turnover of assets of the sample banks is a good reflection of the overall level of asset turnover. Its maximum value is 0.047, and its minimum value is 0.01, indicating a gap in management efficiency and utilization of assets among banks. Among the moderating variables, the mean value of Bank Competitive Pressure (Lerner) is 0.5561, indicating that overall bank competition is moderate and no particular bank has formed a monopoly. The maximum and minimum values are 0.8629 and 0.1762, respectively, indicating a significant difference in the ability of banks to obtain excess profits, resulting in varying degrees of bank competition.

A further test for multicollinearity was carried out. Generally speaking, the mean value of VIF is greater than 10, indicating severe multicollinearity between the variables. The result shows that the mean value of the variance inflation factor (VIF) is 1.43, which is less than 10, indicating that the correlation between the variables is small and there is no multicollinearity problem.

Regression Analysis

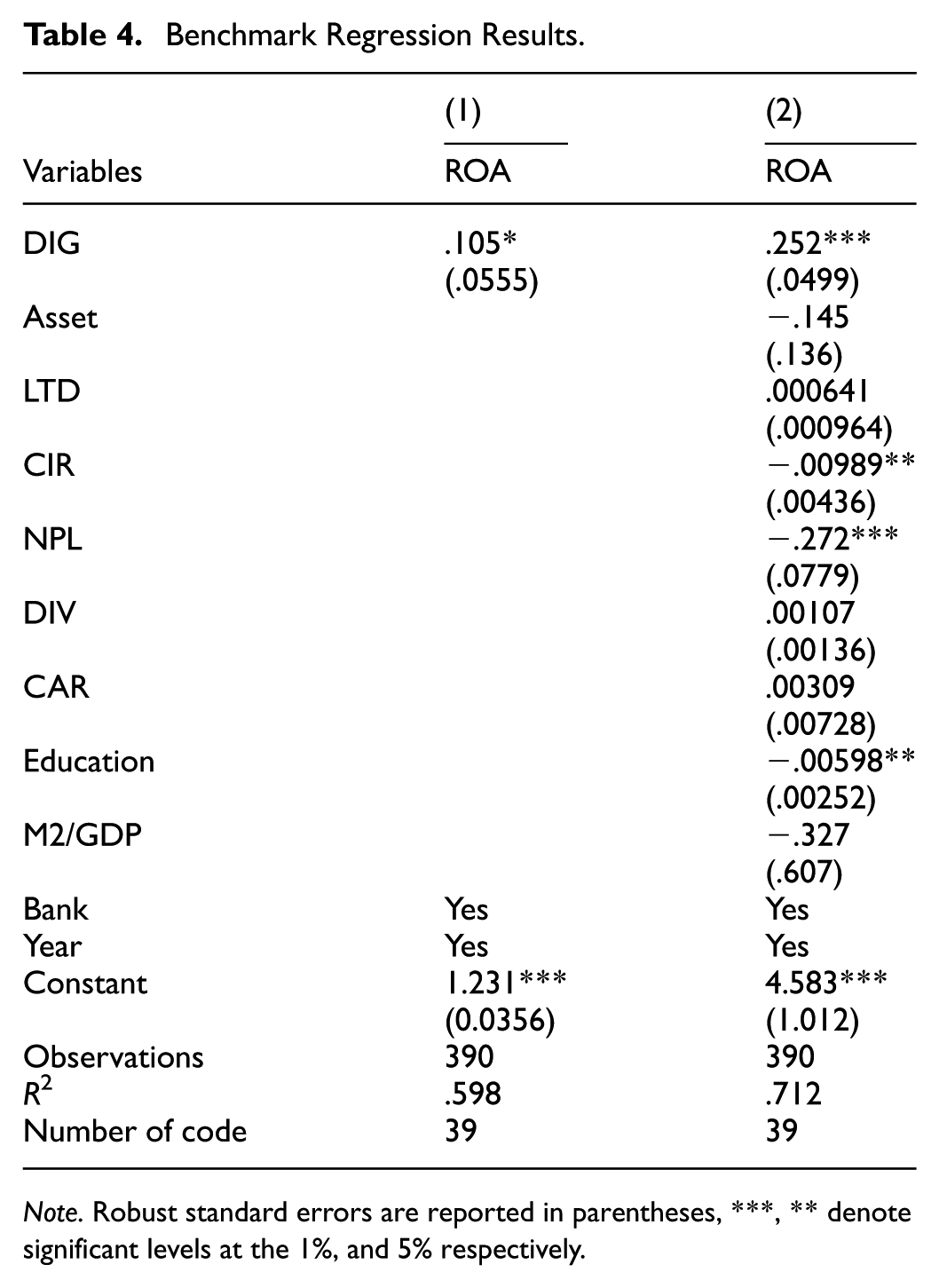

The sample of this paper is panel data. To reduce the impact of time and individual differences on the study’s results, this paper chooses a two-way fixed effects model for empirical analysis, controlling for individual banks and years. The results are shown in Table 4: column (1) shows that the coefficient of digitization degree of commercial banks is significantly positive at the 10% level without adding control variables; column (2) adds a series of control variables to analyse the relationship between the degree of digitalization and business performance of commercial banks, and obtains a coefficient of 0.252 and is significant at the 1% statistical level, which is consistent with the hypothesis 1, suggesting that the digital transformation can promote the business performance of commercial banks, and the higher the degree of digitalization, the better the bank’s business performance. After adding control variables, the model’s goodness of fit R-squared reaches 0.712, indicating that the model can better explain the relationship between the degree of digitalization and the bank’s total return on assets. From a practical point of view, digital transformation of commercial banks can help banks to innovate their business processes, organizational operations, and business models to adapt to changes in the market environment and demand, reduce the cost and risk of bank operations, and enhance profitability and efficiency of asset utilization to improve operational performance.

Benchmark Regression Results.

Note. Robust standard errors are reported in parentheses, ***, ** denote significant levels at the 1%, and 5% respectively.

Regarding control variables, the regression coefficient of the cost-income ratio (CIR) is significantly negative at the 1% level, indicating that the larger the cost-income ratio, the worse the bank’s business performance, which is in line with the theoretical expectation. The cost-income ratio reflects the bank’s operating costs; high costs rob profit margins, and the bank’s performance deteriorates, so the bank needs to reduce the operating costs. The non-performing loan ratio (NPL) is negatively correlated with the return on total assets at a 1% significance level, consistent with the expected scenario. A higher NPL ratio indicates that the bank is exposed to a higher risk of loan defaults and a higher likelihood of loss of the bank’s assets, which can hamper operational performance. The percentage of the number of people with bachelor’s degrees and above in commercial banks (Education) is negatively related to the return on total assets at a 1% significance level, which is inconsistent with the theoretical assumptions. The higher the educational level of the employees, the higher the employee compensation the bank needs to pay. Thus, the labor cost increases, which leads to a decline in operating performance.

Further Analysis

Mediation Effect Test

The results of the mediation effect regression model are shown in Table 5. The coefficient of the digital transformation index in column 1 is positive at the 1% significant level, indicating that digital transformation can improve commercial banks’ operational performance. The effect of digitalization degree on asset operating efficiency in column 2 is significantly positive at the 1% statistical level, indicating that the digital transformation of commercial banks can enhance asset operating efficiency. In column 3, the explanatory variable digital transformation index is significantly positive, and the mediating variable asset operation efficiency is also significantly positive, indicating that asset operation efficiency plays a mediating role in the process of digital transformation to promote the operational performance of banks, which argues that hypothesis 2 is valid. According to the mediation effect model, the positive coefficients indicate that asset operation efficiency partially mediates in the digital transformation process to promote commercial banks’ business performance. The proportion of the mediating effect to the total effect is 0.63.

Mediating Affect Test Results.

Note. Robust standard errors are reported in parentheses, ***, ** denote significant levels at the 1%, and 5% respectively.

Moderating Effect Test

To investigate whether bank competition enhancement weakens the impact of digital transformation on bank business performance, this paper constructs a model to test it and adopts group regression to prove it. First of all, the bank is categorised into the high competition group and the low competition group in the following way: if the median Lerner value of the bank during the sample period is greater than or equal to the sample mean, then the bank belongs to the low competition group, otherwise, the bank belongs to the high competition group. The empirical results, as shown in Table 6, show that the estimated coefficient of digital transformation for banks with low competition is significantly positive. In contrast, the coefficient of digital transformation for banks with high competition is positive but insignificant, which suggests that increased bank competition can weaken the impact of digital transformation on business performance. In the regression results analysed with the total sample, the coefficient of the interaction term (Dig*Lerner) is positive and significant at the 5% statistical level, again validating these findings. Both subgroup regression and full-sample regression results show that the digital transformation of banks with a low degree of competition performs better regarding business performance improvement. Higher competition means that banks face a more competitive environment, bank managers will be cautious, and regulators will adopt stricter regulatory requirements, which is not conducive to digital innovation behaviour, thus weakening the effect of bank digital transformation.

Moderating Affects Test Results.

Note. Robust standard errors are reported in parentheses, ***, ** denote significant levels at the 1%, and 5% respectively.

Heterogeneity Analysis

To further study the impact of banks’ digital transformation on business performance in different natures and regions, banks are divided into three categories: state-owned banks, joint-stock banks, city commercial banks, and agricultural, commercial banks, and into two categories of eastern regions and central and western regions by the location of their registration in group regression. The results show that the coefficients of the different groups are significantly different. Table 7 shows the results of group regression, and columns 1 and 2 show the empirical results of banks by region. In the eastern region group, the coefficient of the degree of digitalization of commercial banks is significantly positive. In contrast, in the central and western region group, the coefficient of the degree of digitization of commercial banks is a non-significant positive value, which indicates that compared with the west and central regions, the digital transformation of commercial banks in the eastern region has a more substantial effect on the promotion of business performance. The reason for this is that the east region has a high level of economic development and a sound financial service system, and commercial banks in the eastern region are in the national leading position in the scale of loan and deposit business. Moreover, their asset quality is improving, and they are enhancing their capital strength through exogenous financing, such as issuing perpetual bonds and preferred shares and introducing strategic investments, thus enhancing their ability to prevent and control financial risks. On the other hand, the central and western regions have long been affected by the lower level of economic development, weak banking strength, shortage of talent, and insufficient business innovation, resulting in a disadvantageous position in peer competition.

Results of Heterogeneity Analysis.

Note. Robust standard errors are reported in parentheses, ***, **, and * denote significant levels at the 1%, 5%, and 10%, respectively.

Columns 3, 4, and 5 of Table 3 show the impact of digital transformation on business performance for banks of different natures. The degree of digitalization of state-owned banks shows a significant negative correlation with business performance, the degree of digitalization of joint-stock banks shows a non-significant positive correlation with business performance, and the degree of digitalization of urban and rural commercial banks shows a significant positive correlation with business performance, that is to say, the digital transformation of state-owned banks can inhibit economic performance improvement, while urban commercial banks and rural commercial banks undergoing digital transformation can increase operational performance. The reason may be as follows: digital transformation utilizes information technology for business innovation, which better meets the diversified needs of long-tail customers; it promotes the universality and fairness of financial services, a goal consistent with the service objectives of small and medium-sized commercial banks. As a result, digital transformation facilitates a more pronounced role for banks in the urban and agribusiness categories. Urban commercial banks and agribusiness banks also have a geographic advantage. They are small, flexible in organizational structure, able to react quickly to external fintech impacts and have a more vital willingness to digitalize. As a comparison, state-owned banks have significant assets and mainly serve SOEs, large enterprises, and people with solid assets and a stable customer base, leading to a lack of incentive for digital innovation. Moreover, state-owned banks have been established for a long time, and they need help to break the traditional internal hierarchy. The hierarchical division of labour makes the grassroots a heavy burden. And their incentives and constraints need to keep up with internal efficiency, which hinders business performance improvement. Although they are taking the lead in digital transformation in business, digitalization is challenging in emulating the organization internally. Digital transformation emphasizes flattening internal organizational structures and agility to achieve efficiency gains.

Robustness Analysis

To further test the robustness and reliability of the empirical results, this paper conducts the robustness test through the following four methods, and the results are shown in Table 8.

Results of Robustness Analysis.

Note. Robust standard errors are reported in parentheses, ***, ** denote significant levels at the 1%, and 5% respectively.

Replacement of explanatory variables: net profit per capita (NPPC) evaluates the bank’s business performance from the perspective of the labour force, which reflects the value created per capita by the bank in the past year and the higher the net profit per capita, the higher the value created by each employee, and the better the bank’s business performance in general. Therefore, the regression test uses it as a proxy for return on total assets (ROA). The results are shown in column (1): the regression coefficients of the core explanatory variables are positive and significant at a 5% statistical level, which is in line with the results of the benchmark regression, proving that it is robust.

Shrinking 5% treatment: To eliminate outliers, both explanatory and interpreted variables are subjected to a shrinking 5% treatment simultaneously. The results, as shown in column (2), show that the digitization coefficient is significantly positive at the 1% level, proving the robustness of the benchmark regression results.

Selection of Tobit model: considering the presence of a large number of urban and agricultural banks in the sample of this paper, which accounts for about 64% of the total sample (250/390), there will be a situation of broken tails of the dependent variable, specific observations are compressed at a single point, and thus the replacement model is selected as the Tobit model. The results are shown in column (3); the marginal effect of the independent variable on the latent variable return on total assets is significantly positive. Furthermore, the marginal impact of the degree of digital transformation is 0.229 (calculated using the Stata software): for every unit increase in the degree of digitalization, bank operating performance improves by 0.229 units, which indicates that the digital transformation promotes the bank’s operating performance, which is in line with the results of the benchmark regression.

Lagging the independent variable by one period: there may be a time lag in the impact of digital transformation on banks, making it difficult to manifest itself in full in the current year. There may be a bidirectional causality between banks’ digital transformation and business performance; the higher the business performance, the more banks pay attention to digital transformation, and the higher the degree of digitalization, which leads to an endogenous problem. In this paper, the independent variable lagged first order is brought into the model to test the effect of digital transformation on the business performance of commercial banks. The results are shown in column (4) of the table below; the coefficient of the lagged first-order term is significantly positive at the 1% confidence level, which indicates that digital transformation can promote the improvement of banks’ operational performance, consistent with the results of the benchmark regression, further proving that the results are robust and reliable.

Research Conclusions and Recommendations

Research Conclusion

This paper studies the impact of digital transformation on the business performance of commercial banks from the perspective of digital transformation. Digital transformation, as a unique form of industrial change in the era of the digital economy, is an emerging thing, and the existing ways of measuring the degree of digital transformation still have certain limitations. The impact of digital transformation on the operational performance of banks through empirical research is still in the preliminary stage of research. Therefore, this topic is still of research value. Based on theoretical analysis, this paper selects a total of 390 samples from 39 commercial banks from 2012 to 2021 as the research object, constructs a vocabulary base according to the digital development of commercial banks, and carries out word frequency statistics on the text of the bank’s annual report through python program. In this way, we construct the indexes of the degree of digitization of commercial banks, then adopt the two-way fixed effect model to carry out an empirical analysis of the impact of digital transformation on the business performance of commercial banks and draw the following conclusions.

First, the digital transformation of commercial banks has a positive impact on operating performance and can promote an operating performance increase.

Second, the mechanism test shows that digital transformation increases operating performance by improving banks’ asset efficiency. Asset operation efficiency plays a part in mediating the operation. Increased bank competitiveness weakens the impact of digital transformation on operating performance.

Third, the impact of digital transformation on bank operating performance is heterogeneous. Regarding the bank’s ownership, the digital transformation of urban and rural commercial banks has a facilitating effect on operating performance. In contrast, it is having a hindering impact on the operating performance of state-owned banks and a non-significant facilitating effect on that of joint-stock banks. In terms of the geographic location of banks, digital transformation has a more significant impact on the business performance of banks located in the eastern region and a less significant effect on banks located in the central and western areas.

Policy Recommendations

The digital transformation of China’s commercial banks is an inevitable trend. Banks should increase their investment and application of digital technology in daily production and operation, comprehensively promote the banking industry’s digital transformation, and adapt to the development requirements of the times. Based on the above analysis, combined with the pain points and difficulties in the current development of banks, this paper puts forward the following development proposals.

First, clarify the digital transformation strategy and carry out differentiated development. The digital strategy should be customer-centric, balancing innovation and transformation with sustainable development, further pursuing business model digitalisation based on business digitalisation and organisational operation digitalisation, and establishing a technology- and data-driven digital platform. Commercial banks need to adopt appropriate digital transformation strategies according to their own operating conditions and resource advantages; large commercial banks need to make clear the necessity of digital transformation to lead the industry; small and medium-sized banks should cultivate the characteristics of the local industry, focus their resources on the development of particular businesses or take a specialised and distinctive digital transformation path according to their specialties, and take on the responsibility of supporting local enterprises.

Second, strengthen the investment in digital technology and enhance digital capabilities. Banks’ digital transformation results from changes in business, organisational processes, and business models brought about by digital technology. So, banks must strengthen their investment in digital technology and enhance their digital capabilities, including digital resource management and application capabilities. Banks need to pay attention to the mining and utilization of data resources, expand data sources, build a closed-loop analysis system for big data, create a “1+N” data analysis team, improve data asset management and application capabilities, and improve the data storage system, to give full play to the maximum value of the production factors of data resources. Banks also need to learn from the digital transformation strategies of industry-leading banks and use technology to construct banks unique competitive advantages.

Third, improve the financial regulatory system and strengthen data governance. The relevant financial regulatory authorities should improve the financial regulatory system, whose content needs to keep pace with the times, enhance the supervision of emerging products and businesses of banks, make up for the regulatory gaps brought about by emerging technologies, urge banking institutions to carry out compliance, focus on the supervision of day-to-day business activities, and eliminate the use of digital technology for fraud, money laundering, and other behaviours, to form an all-around, scientific, regulatory system. At the same time, regulators should also safeguard the security of digital governance. Concerning data sharing, a national data application platform should be established to explore the value of data and improve data quality; standards for the compliant use of data should be formulated to regulate the use of data by banks; and a “firewall” should be built to avoid data leakage and to create a safe environment for the use of data.

Fourth, talent training should be focused on, and the talent introduction system should be improved. The competition of digitalisation is the competition of talent. Banks need to increase their investment in the training and development of technical personnel, improving the digital competence of their employees through employee job training and job adjustments to create a talent team that meets the needs of development. Banks should also focus on cultivating employees’ digital thinking, establish a perfect incentive mechanism within the bank, and set up a promotion channel for employees to improve their work efficiency. For society, the school talent training mode needs to keep pace with the times, follow the trend of technological change, and meet the market demand for talent. In addition, the government also needs to improve the talent introduction system, especially in the central and western regions. In addition to introducing technology, the west and central areas must also introduce high-quality technical personnel. Local governments must enhance their talent retention policies, pay attention to the real needs of talents, alleviate their concerns, foster a favourable business climate, and do an excellent job of reserving, using, and retaining talents.

Footnotes

Author Contributions

Availability of data: the data supporting this study’s findings are available from the corresponding author upon reasonable request.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.