Abstract

This paper explores the impact of market competition on banks’ diversification strategies. Through a unique sample of Vietnamese commercial banks during 2007 to 2021, our most important finding is that the bank competition impact may depend on the specific type of diversification under analysis. Specifically, we document that banks are more likely to diversify their asset portfolios and income sources into non-lending activities and non-interest revenues amid high competition. In contrast, loan portfolios of banks facing more competition tend to be less diversified across different economic sectors. Besides, funding diversity in another vein may not react to changes in the banking market structure. Further empirical results reveal that the influence of market competition on bank business models is more pronounced at smaller and riskier banks, suggesting that a competitive market places greater pressure on more vulnerable banks and causes them to adopt a more aggressive diversification strategy. Based on these findings, critical policy implications include the development of frameworks to guide banks’ activity diversification strategies, monitoring sectoral concentration risks, and providing targeted support and guidance for specific groups of banks, particularly smaller and riskier institutions, within a competitive banking environment.

Plain language summary

This paper explores the impact of market competition on banking diversification strategies. We simultaneously incorporate structural (market concentration) and non-structural approaches to establish the measurement of competition, as any analysis relying on only one competition measure could be misleading. Unlike prior research, we comprehensively analyze different dimensions of bank diversification from asset, funding, income, and sectoral loan portfolios. Through a unique sample of Vietnamese commercial banks from 2007 to 2021, our most important finding is that the bank competition impact may depend on the specific type of diversification under analysis. Specifically, we document that banks are more likely to diversify their asset portfolios and income sources into non-lending activities and non-interest revenues amid high competition. In contrast, loan portfolios of banks facing more competition tend to be less diversified across different economic sectors. Besides, funding diversity in another vein may not react to changes in the banking market structure. Our results not only survive after alternative econometric strategies and subsample analysis but are also robust to a series of modifications in the bank diversification and competition measurements. We further ask whether bank-level heterogeneity matters to the impact of market competition on bank diversification. The empirical results reveal that the influence of market competition on bank business models is more pronounced at smaller and riskier banks, suggesting that a competitive market places greater pressure on more vulnerable banks and causes them to adopt a more aggressive diversification strategy.

Introduction

The banking industry has undergone significant changes in its market structure over recent years due to factors such as globalization, technological advancements, regulatory reforms, and evolving customer demands. These changes have profound implications for how banks operate and compete. In this context, banks may adjust their business models to respond to the new situation. These adjustments are critical to the bank’s business philosophy and performance. For example, a diversification strategy may be preferred, and the literature indicates that on the one hand it can be highly beneficial, such as eliminating idiosyncratic risks and reducing the likelihood of bankruptcy (Berger et al., 2010; Diamond, 1984), but on the other hand an expansion of new activities is also associated with weakened monitoring effectiveness and increased agency problems (Denis et al., 1997; Deyoung & Roland, 2001). Given the changes in banking market structure and the significance of bank diversification strategies, studying the link between bank competition and diversification is critical. While banks need to adapt their strategies to the evolving competitive landscape, understanding how competition impacts diversification helps banks make informed strategic adjustments. Further, insights into the link between competition and diversification inform policymakers and regulators, enabling them to design regulations that regulate competition while ensuring financial stability. However, a careful and comprehensive investigation of this link has been limited in the literature.

This study aims to empirically explore a link between bank competition and diversification strategies. An important mechanism is that banks can diversify in different business and financing segments, which may affect banks themselves and the economy differently. Hence, to gain a broad analysis, we allow for an investigation of multiple diversification dimensions, including (i) asset diversification—how banks make their investments, (ii) funding diversification—how banks organize their financing resources, (iii) income diversification—the way banks earn their revenues, and (iv) sectoral diversification—the way banks design their loan portfolios across many economic sectors. To perform our regressions, we employ financial data from the banking sector in Vietnam, an emerging market, for the 2007 to 2021 period. While it is argued that relying on only one bank competition measure could be misleading and it is more appropriate to consider various alternative measures of banking market structure (Khan et al., 2016; Lapteacru, 2014), this paper uses a large pool of different competition measures, under the structural and non-structural approach strategies, to overcome one of the most significant limitations in the literature on banking market structure analysis. We primarily rely on the dynamic two-step system generalized method of moments (GMM) estimator to mitigate the endogeneity concerns. In addition to examining the average effect of market competition on bank diversification, we investigate how this effect varies based on bank-level heterogeneity. Banks with diverse financial and performance characteristics tend to view competitive pressures differently, causing them to behave differently within one market.

Focusing on a single market from Vietnam enables us to examine the impacts of the banking market structure within a uniform environment. More importantly, Vietnam also introduces a sound setting for our empirical investigation due to multiple aspects. The economy in this country is characterized by an underdeveloped capital market, and banks play the role of the leading financing provider for businesses and households (Dang & Huynh, 2022a). Thus, any changes in banking operations may greatly influence economic growth. As a member of the World Trade Organization (since 2007), the country was subject to financial reforms and the banking sector was required to adopt global standards in banking operations and prudent regulations, as well as loosen restrictions on the establishment of new banks and the entry of foreign banks. The State Bank of Vietnam (SBV) exerts strong regulatory control over the banking industry, implementing a comprehensive framework that includes liquidity requirements, capital adequacy standards, and risk management protocols. These regulations are aligned with international norms, such as Basel III, ensuring that Vietnamese banks adhere to global best practices. Notably, one of the primary aims of the reforms was to change the monopolistic dominance of state-owned banks. Various reforms have focused on the market structure in the Vietnamese banking sector, which is sufficient to check the competitive environment and its significance in banking strategies. Following banking reforms, the whole sector shifted progressively toward a market-oriented system that could foster competitive conditions. The banking system’s total assets have enormously increased, and more large banks have emerged. The banking sector in Vietnam currently includes a mix of state-owned banks, private domestic banks, joint-venture banks, and branches of foreign banks. State-owned banks still hold a significant market share, influencing market dynamics and competition. Since 2012, the banking sector of Vietnam has suffered substantial losses from the bad-debt peak, and it has extensively restructured its financial and operating architecture (Nguyen et al., 2018). Such reorganizations may exert further pressure on banks and promote diversification initiatives to move away from crowded conventional sectors. Hence, an investigation into the effect of bank competition on diversification strategies needs close attention in the case of Vietnam. For the background and other features of the Vietnamese economy and banking system, see Dang and Huynh (2022a, 2022b).

By studying the impact of bank competition on diversification strategies, this study complements the literature in several aspects. Regardless of the practical and theoretical motivations, the existing literature on the topic is scarce and needs to be enriched (Căpraru et al., 2020). We do this by highlighting a comprehensive way of approach. We simultaneously employ various measures of bank competition that have been separately considered in the existing literature, namely, (i) the market concentration ratios, (ii) the Herfindahl-Hirschman index, (iii) the Lerner index, (iv) the H-statistic indicator, and (v) the Boone indicator. For bank diversification strategies, we examine this issue in the Vietnamese banking market from the asset, funding, income, and sectoral diversification. All of these measures conceptually focus on different aspects of bank competition and diversification in the banking sector. Our approach in this regard is novel since, to the best of our knowledge, no studies have considered the influences of various bank competition measures on different dimensions of bank diversification. Prior work only pays attention to bank diversification in a generic manner. This is a major shortcoming in the existing literature, as the banking market structure may have different impacts on different forms of bank diversification. As evidence, we find that high competition levels may be a stimulating source of asset and income diversification, while increased competition leads to less diversification across economic sectors. Meanwhile, we also reveal that banks do not modify their funding diversity in response to changing market structures. Additionally, identifying the conditioned bank diversification when banks are under competitive pressure is another significant contribution of our work. We investigate the specific features of banks, such as capital buffers, bank size, riskiness, and profitability, in terms of their mediating effects on the competition-diversification linkage. In doing so, we propose that bank heterogeneity plays an integral part in determining how bank diversification strategies respond to changes in bank competition. This identification technique would assist regulators and banking supervisors in drawing precise policy frameworks.

Literature Review and Hypothesis Development

Traditional views suggest that competitive pressure has forced banks to diversify their business segments to maintain and enhance their market positions (Lepetit et al., 2008). This shift could lead to increased investment in non-credit assets, an expansion in non-interest income contributing to bank profits, or greater exposure to various economic sectors (Acharya et al., 2006; Allen & Santomero, 2001; Laeven & Levine, 2007). Furthermore, in highly concentrated and poorly competitive markets, banks could pay lower deposit rates and charge higher lending rates to generate sufficient profits, hence bank managers are not incentivized to work hard to expand banks’ strategic scope and manage a more complicated business (Berger & Hannan, 1998; Hidayat et al., 2012). Under these arguments, we develop the first hypothesis as follows:

Hypothesis A: Higher market competition increases bank diversification.

However, the existing banking literature does not exhibit consensus on this mechanism. Instead, there is evidence supporting a contrasting argument that dominant banks with more market power tend to diversify to gain more profits, with an important obligation to maintain their previous levels of profit and market positions (Santoso et al., 2021). In the meantime, in highly competitive markets, banks might choose to focus on their core competencies to remain competitive. By specializing in their most profitable and efficient areas of operation, banks can maximize their returns and reduce operational complexity. Boot and Thakor (2000) discuss how banks under competitive pressure may concentrate on their primary strengths to enhance their market position and profitability. In other words, the supporters of these notions claim that banks in a competitive market may decrease their diversification levels. Based on these mechanisms, we develop a competing hypothesis as follows:

Hypothesis B: Higher market competition decreases bank diversification.

The link between market competition and bank diversification has attracted little empirical attention from the existing literature, with the exception of previous studies by Nguyen et al. (2012) and Căpraru et al. (2020). While Nguyen et al. (2012) reveal a U-shaped relationship between market power and revenue diversification after focusing on commercial banks in ASEAN countries, Căpraru et al. (2020) document that competition stimulates bank diversification in European markets. Despite sharing a common interest, our study differs from theirs in many significant ways. First, they exclusively consider income diversification and disregard other diversification aspects. To address this void, we pay special attention to bank diversity in asset, financing, revenue, and sectoral loan portfolio, given that each form of diversification contributes differently to the operation of banks and that a combined analysis may provide a comprehensive understanding of the competition-diversification linkage. Secondly, prior authors only look at bank competition from the perspective of the Lerner index, while we are interested in a variety of structural and non-structural approach strategies. Thirdly, previous studies highlight an average linear or inverse U-shaped relationship between market competition and bank diversification. Differently, our analysis focuses on the difference in response to increased competition by examining bank-level heterogeneity.

Bank Competition and Diversification Measures

Bank Competition Measures

As mentioned earlier, for the leading-bank concentration ratio under the structural approach, we take the share of the top three banks’ total assets in the whole banking sector (CR3), and we also consider another similar ratio using the five leading banks (CR5) as a robustness verification. With regard to the Herfindahl-Hirschman index, we calculate the sum of the squared market shares of each bank (by total assets), marked as HHI market. Greater market concentration indirectly suggests higher market power of banks and less competition in the sector.

Under the non-structural approach, we first consider the Lerner index as a reverse measure of bank competition. This measure also highlights a bank’s market power by showing its pricing power above marginal costs. Consistent with the prior authors (Beck et al., 2013; Berger et al., 2009; Turk Ariss, 2010), the Lerner index is computed by the difference between a bank’s output price and marginal cost, as a proportion of output price, which is shown in equation (1):

In more detail, the output price

in which

We continue with the construction of the Boone indicator—an advanced competition measure and widely employed in the recent banking literature. This indicator could demonstrate the association between bank profits and efficiency, and it could be measured each year by equation (4) as follows:

where

Finally, we set up a model of profit-maximizing behavior to calculate the H-statistic indicator, which measures the extent to which a fluctuation in input prices could be observed in the equilibrium revenue of banks (Panzar & Rosse, 1987). Accordingly, this market structure indicator is estimated from the following model:

where the single input

Bank Diversification Measures

The other key group of variables to analyze in this study, bank diversification, is measured from the perspective of assets, funding, income, and sectoral loan portfolios. We first capture asset diversification using the share of non-lending activities in total assets. As the core function of banks is to provide loans to the economy, any actions that shift toward non-lending activities could lead to a diversified asset portfolio. Apart from this measure, we also gage asset diversification according to the Herfindahl-Hirschman approach, where we subtract the squared share of all asset items in total assets from 1. The formula is as follows:

where

Similarly, for the aspect of funding diversification, we construct two measures (i) the share of non-deposit funds in total liabilities (plus equity), and (ii) the squared share of all funding items in total funds subtracted from 1. Applying equation (6) to the case of funding diversification, we use five funding categories: interbank deposits, customer deposits, issued debts, equity, and other market funds. Next, with income diversification, we also have two ways to define our diversification variables by (i) taking non-interest income divided by total operating income, and (ii) subtracting the squared share of all income sources in total operating income from 1, given that a bank has four main sources of income: interest income, fees and commissions, trading-based income, and other non-interest income.

Turning to our final dimension—sectoral loan portfolio diversification, our strategy differs slightly from the one expressed above. In more detail, we utilize the methodology in the seminal paper by Acharya et al. (2006) that suggests a categorization of banks’ loan portfolios into six sectoral exposures, comprising the five largest exposures and the sixth one summing all remaining exposures. Each sectoral exposure is then treated as one single share, in line with the spirit of equation (6). For a robustness proxy, we move on to create portfolios with a total of ten sectoral exposures and simulate a similar procedure.

Data and Model

Data Sources

Data at the bank level are extracted from the annual financial statements of Vietnamese commercial banks. Given the availability of audited data, we choose the period 2007 to 2021 for our study, excluding banks that were acquired or placed under special governance by the SBV because of variations in business regime and strategies, as well as those with heavy missing data throughout the period. We also do not consider joint-venture banks and foreign bank branches for our sample, as they represent a very small portion of the Vietnamese banking sector and do not meet our data criteria for regression analysis. We gather macroeconomic indicators from the International Financial Statistics database. Consequently, our dataset comprises 30 banks, which cannot contain all commercial banks in Vietnam but account for more than 90% of the system assets at the end of 2021, providing a sound representative. We tackle the issue of extreme outliers by substituting the two tails with the value at the 2.5th and 97.5th percentiles. Table 1 reports descriptive statistics for our designed variables. Our final sample contains 30 commercial banks with a maximum of 439 observations from 2007 to 2021.

Summary Statistics.

In addition, we also compute the pairwise correlations for the explanatory variables. In general, the correlation matrix findings (not included to save space) indicate that our sample data is not subject to extreme multicollinearity. As a side note, our regression excludes the COVID-19 pandemic dummy since it is substantially correlated with economic cycles; such a strong correlation may result in a severe multicollinearity issue.

Based on a mean concentration level of 0.586 from the five-largest-bank ratio (CR5), we realize that the banking sector in Vietnam is highly concentrated, with several banks accounting for most of the total sector assets. Nevertheless, a different picture emerges if we consider additional market structure indices. In particular, unlike the CR5 statistic, the HHI market index provides proof of a non-concentrated sector with an average sample value of 0.088. Other estimates from the Lerner, the Boone, and the H-statistic approaches serve to demonstrate that the Vietnamese banking sector is moderately competitive. Such early findings support our identification method, which does not depend on one competition indicator since each looks at a specific facet of the market structure. Moreover, the overall market picture for Vietnam varies from those of European countries presented in prior research (Căpraru et al., 2020; Leroy & Lucotte, 2017; Wang et al., 2020), while holding certain parallels with the analysis of developing markets (Sinha & Grover, 2021; Yuanita, 2019).

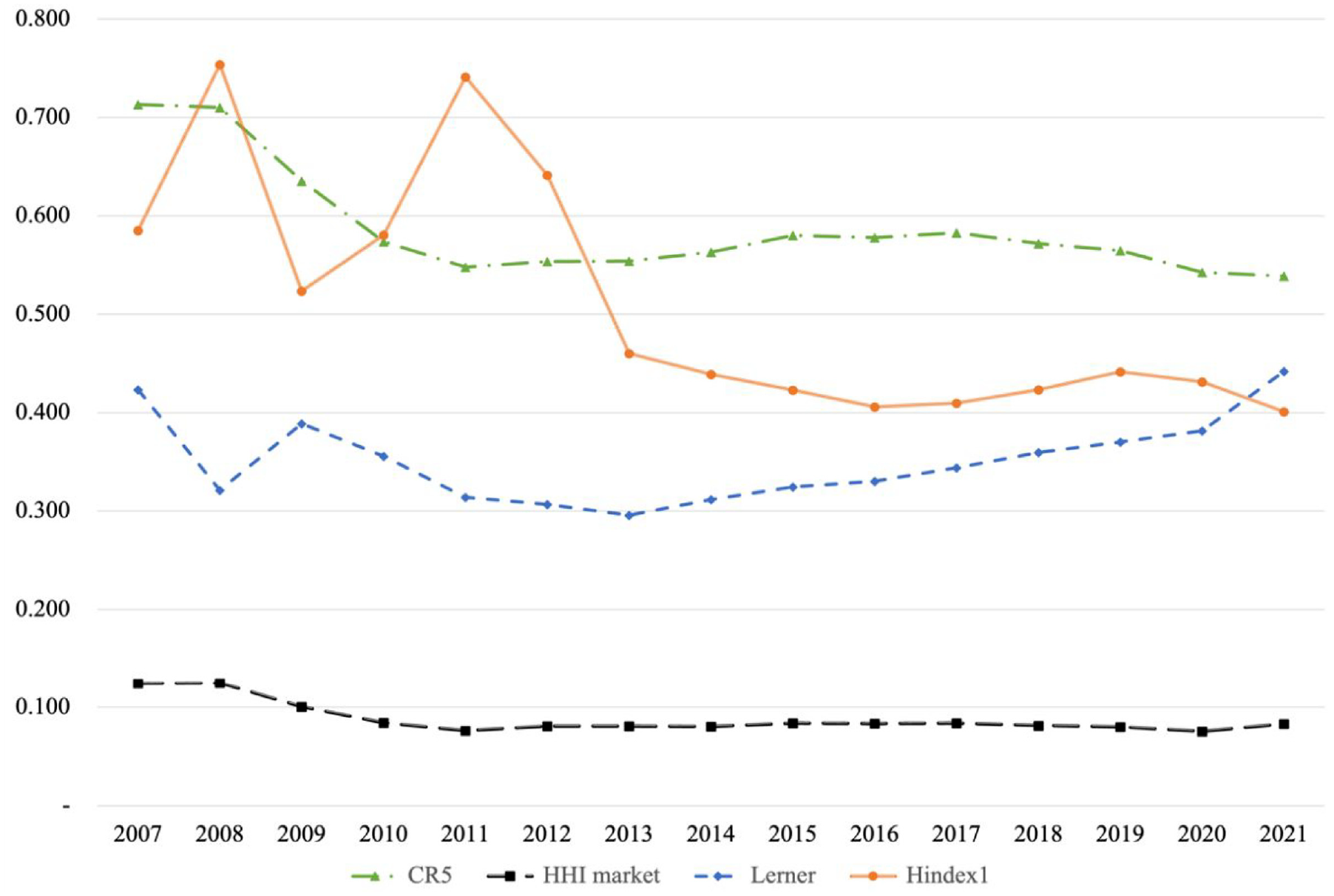

Figure 1 offers a comprehensive view of the competitive environment in the Vietnamese banking sector from 2007 to 2021, utilizing four key measures: CR5, HHI market, Lerner, and Hindex1. During 2007 to 2010, both CR5 and HHI market show a decreasing trend, indicating reduced market concentration. Then, the 2011 to 2021 period sees a stabilization in these two structural measures, reflecting steady market concentration. For the non-structural measures, the average Lerner index and Hindex1 exhibited significant fluctuations during the survey period, with the trends of these measures generally moving in opposite directions, which consistently indicates substantial changes in bank competition in Vietnam. In sum, the Vietnamese banking sector has experienced varying degrees of market competition over the years. The CR5 and HHI market measures consistently indicate similar trends in market concentration, while the Lerner index and Hindex1 provide aligned insights into the competitive environment. These observations further support the notion that different measures complement each other in our analyses of bank competition. We did not include the Boone index due to its differing range of values compared to the other variables. However, it is essential to note that the overall picture of bank competition does not significantly change with this index.

Competitive environment in the Vietnamese banking sector from 2007 to 2021.

Model

As bank behaviors are likely to persist over time, we design the following dynamic model to explore the relationship between bank competition and diversification:

where

The dynamic model faces the issue of the endogeneity bias resulting from the association between the lagged diversification and unobservable factors. Hence, we apply the two-step system GMM setting to address this problem (Blundell & Bond, 1998). The GMM estimator is well-suited for panel data, helping to control for unobserved heterogeneity and providing robust and efficient parameter estimates. It is particularly suitable for our study as it captures the temporal dynamics of bank diversification and effectively addresses endogeneity issues, which are common in banking studies due to the potential correlation between explanatory variables and the error term. It uses internal lagged regressors to construct suitable instruments and manage endogeneity bias appropriately. To evaluate the consistency of our GMM estimates, we need the Arellano-Bond tests (no second-order serial correlation required), and the Hansen test (the joint validity of instruments desired).

Results

Estimation Results for Asset Diversification

We start our discussion with the results of the dynamic GMM model of asset diversification. Based on findings in Table 2, where we use the non-lending asset share as a proxy for asset diversification, the coefficient on market power (the Lerner index, column 1) is negative and statistically significant, indicating that more market power lowers the proportion of non-lending assets. Next, the association between three structural measures (CR5/CR3 and HHI market, columns 2–4) and the dependent variable is significantly negative, demonstrating that highly concentrated sectors discourage banks from investing in more non-lending assets. The estimation of the Boone indexes (columns 5–6) produces a significantly negative coefficient, regardless of the changes in the method of calculating the Boone variants. All six aforementioned alternative indicators are reverse proxies for bank competition, thus their estimates consistently indicate that increased market competition results in greater asset diversification.

Estimation Results for Asset Diversification by the Non-Lending Asset Share.

*p < .1. **p < .05. ***p < .01.

In the remaining columns of 7 to 8, where we employ the H-statistic methodology to reflect bank competition, the findings indicate that asset diversification increases in the context of augmented competition, as shown by the positive coefficients on Hindex1 and Hindex2 variables. Overall, consistent with Hypothesis A, Table 2 reveals that higher competition may cause a greater movement toward non-traditional asset classes.

As an alternative check, we replace the share of the non-lending asset with HHI-based asset diversification. In Table 3, we observe that all estimates yield the same conclusion confirming the positive link between bank competition and asset diversification at Vietnamese banks. The economic impact of our results is also significant. For instance, a unit standard deviation rise in the Lerner index results in a 0.032 (0.360 × 0.089) percentage points fall in the non-lending asset share (column 1 of Table 2). Alternately, asset diversification might decrease by 0.022 (0.415 × 0.052) units in response to a one standard deviation rise in the CR5 index (column 2 of Table 3).

Estimation Results for Asset Diversification by the HHI Asset.

*p < .1. **p < .05. ***p < .01.

Estimation Results for Funding Diversification

The estimation results between bank competition and funding diversity, using two alternative measures based on the non-deposit fund share and the HHI funding indicator, are reported in Tables 4 and 5, respectively. Our analysis starts with the model of the Lerner index in Table 4, where we find a negative coefficient of market power that is statistically significant at the 10% level, thus showing that the competition impact is not strong. The significance even vanishes in Table 5 when we adopt the HHI approach to capture funding diversification. Turning our attention to other estimated results in two tables, we realize that all measures of market structure, based on the aspects of banking market concentration and competition, are statistically insignificant, with only two minor exceptions in column 8 (Table 4) and column 7 (Table 5) where the effect found is significant but rather weak.

Estimation Results for Funding Diversification by the Non-Deposit Fund Share.

*p < .1. **p < .05. ***p < .01.

Estimation Results for Funding Diversification by the HHI Funding.

*p < .1. **p < .05. ***p < .01.

To sum up, all competition measures almost exhibit insignificant coefficients in the functions of funding diversification, indicating that funding diversification is not explained by transformations in the banking market structure. Funding diversification, unlike asset diversification, is not influenced by the fluctuation in the banking market structure. The diversified financing structure of banks in Vietnam appears to be immune to the higher competitive nature of the banking market. This finding can be largely attributed to the strong regulatory control exercised by the SBV and adherence to international norms such as Basel regulations. These controls and regulations ensure a standardized approach to funding practices, emphasizing stability and risk management over competitive dynamics. The strict regulatory environment ensures that all banks follow similar guidelines for funding practices. This standardization means that regardless of the level of competition, banks are required to maintain a certain level of funding diversity, minimizing variations that might otherwise arise from competitive pressures and neutralizing the impact of competition.

Estimation Results for Income Diversification

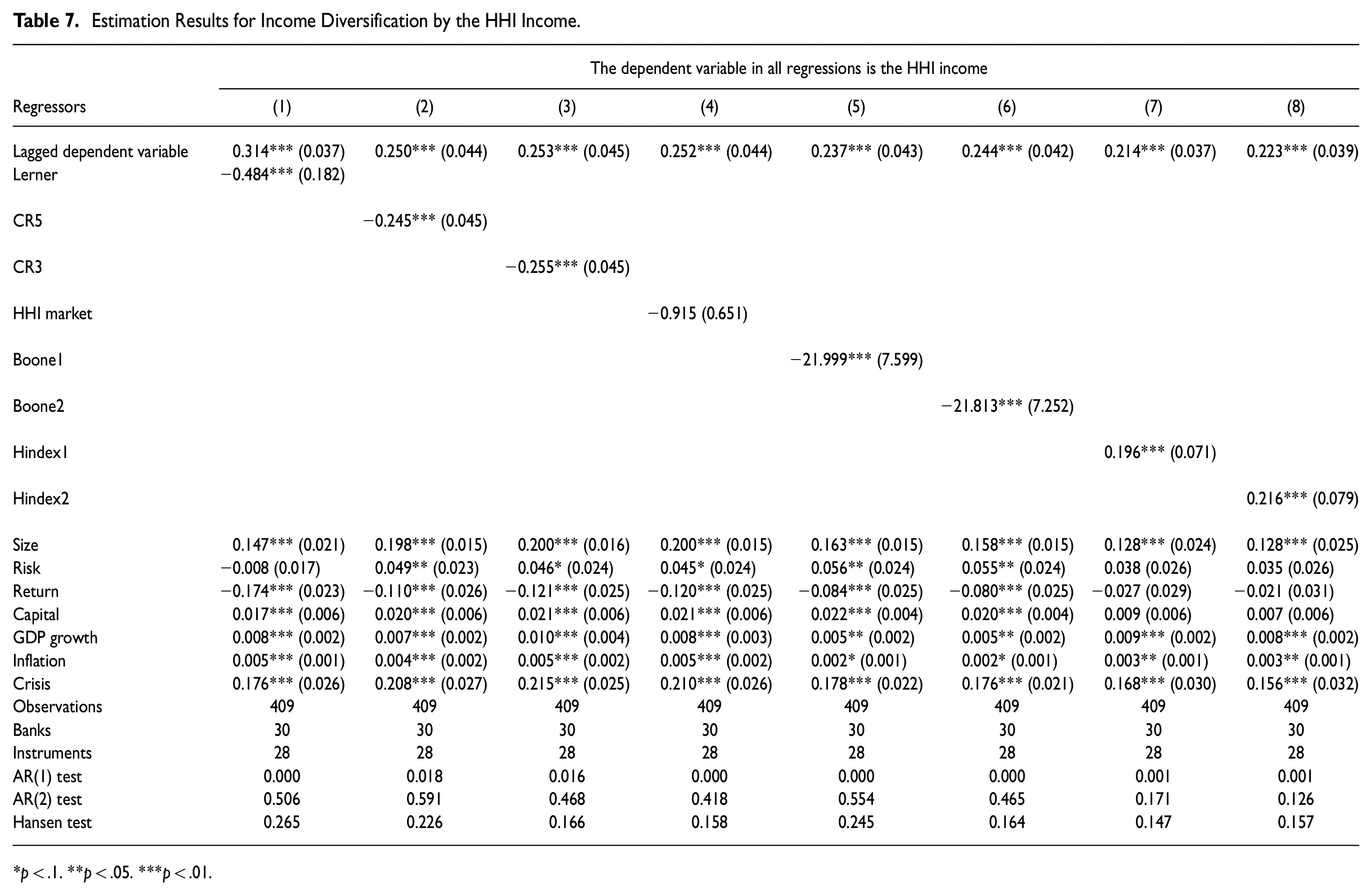

Tables 6 to 7 report the impact of market structure on income diversification in the models of the non-interest income share and the HHI income indicator, respectively, while using all eight proxies of bank competition. Before interpreting our results, we need to remind that the group of the Lerner index, concentration ratios, and the Boone indicator offer inverse measures of bank competition. Table 6 shows that both bank concentration (CR5/CR3 and HHI market) and market power (Lerner index) are negative and statistically significant with the diversification variable. This result implies that increased competition leads to a greater shift toward non-interest income sources. For other measures of competition based on the Boone and the H-statistic methodology, while the coefficients on the former are insignificant (columns 5–6), the latter displays positive and significant coefficients, suggesting that greater competition may support the growth of non-interest income segments. In terms of the HHI income diversification as given in Table 7, the significance of our estimates exhibits some change, especially with the notable case of the Boone indicators where two alternative versions have a significant negative relationship with income diversification. The findings consistently reveal the presence of more diversified income structures amid high competition.

Estimation Results for Income Diversification by the Non-Interest Income Share.

*p < .1. **p < .05. ***p < .01.

Estimation Results for Income Diversification by the HHI Income.

*p < .1. **p < .05. ***p < .01.

Hence, our results offer evidence of more income diversification during the period of high competition, confirming Hypothesis A. Importantly, this finding holds across a variety of competition measures. It is also consistent with previous studies on the competition-diversification link in developed markets (Căpraru et al., 2020). We complement this study by using a number of structural and non-structural measures to capture the competition impact on income diversification. Previous authors reach their conclusion based on one single market proxy.

Overall, our finding for the positive impact of competition on asset and income diversification could be explained as follows. In a highly competitive environment, banks face increased pressure to maintain their market share and profitability. Diversification of asset portfolios and income sources allows banks to spread their risk across different sectors and activities, reducing their vulnerability to sector-specific downturns and economic shocks. In other words, diversification can help banks manage risk better by not being overly reliant on any single revenue stream or asset class (Acharya et al., 2006; Allen & Santomero, 2001; Laeven & Levine, 2007). In the meantime, banks can maintain lower deposit rates and higher lending rates to ensure adequate profits in markets with low competition. As a result, bank managers have little motivation to expand the strategic scope of their institutions or to manage more complex business operations (Berger & Hannan, 1998; Hidayat et al., 2012).

Estimation Results for Loan Portfolio Diversification

In Table 8, when using the Lerner index as the competition variable, its coefficient is positive but not significant. However, when we consider other bank competition measures, the coefficient on these measures turns significant. The group of structural measures (CR5/CR3 and HHI market) and the Boone indicators (Boone1 and Boone2) document positive and significant coefficients, while the H-statistic-based proxies (Hindex1 and Hindex2) are negative and significant. These estimated signs consistently reveal that when banking markets experience increased competition, banks are less likely to diversify their loan portfolios across many economic sectors. Economically, the sectoral diversification measure may increase by 0.024 units (7.858 × 0.003) if the Boone1 index rises by one standard deviation (0.003); for another example, an increase of one standard deviation in the Hindex1 may result in a decrease of 0.031 units (0.261 × 0.117) in the sectoral diversification measure. Other estimates in Table 8 are both statistically and economically significant.

Estimation Results for Loan Portfolio Diversification by the HHI Loan Portfolio.

*p < .1. **p < .05. ***p < .01.

We gain the same results when an alternative variable of sectoral diversification is employed in Table 9. The result estimated with the Lerner index in column 1 even turns significant in this case. Hence, our finding implies that banks may not prefer to diversify into new areas with little or no expertise and experience, which could weaken their loan monitoring effectiveness. This mechanism could be seen as a precautionary strategy when banks handle the competitive pressure in the banking market. It is risky for banks to expand their credit lines into additional industries and sectors, as it may result in a poorer quality loan portfolio under the pressure of competition.

Estimation Results for Loan Portfolio Diversification by the HHI Loan Portfolio (Alternative).

*p < .1. **p < .05. ***p < .01.

Taken together, our sectoral diversification finding contrasts with earlier conclusions that bank diversification increases in asset and income dimensions with increased competition. Interestingly, our results in this regard shed some light on the necessity to differentiate the types of diversification when analyzing the effect of bank competition. Under the competitive pressure of the market, average banks try to acquire additional market share through the diversification of assets and income, while they prefer to involve in a few economic sectors where they could show their expertise and enjoy their comparative advantages. Our results for sectoral loan diversification support Hypothesis B.

Robustness Checks

In addition to using various metrics to represent market competitiveness and bank diversity, we now conduct other robustness tests. We first conduct sensitivity tests using the subsample. Our original sample from 2007 to 2021 could suffer from structural breaks, including the financial crisis between 2007 and 2009 and the COVID-19 pandemic recorded between 2020 and 2021. In detail, structural breaks can lead to abrupt changes in banks’ risk perceptions. For instance, a financial crisis might make banks more risk-averse, leading them to reduce diversification into non-lending activities and focus on safer, traditional banking operations. Structural breaks can disrupt market dynamics, affecting competition levels and the profitability of various banking activities. This can cause banks to re-evaluate and adjust their diversification strategies to align with the new market conditions. Hence, structural breaks introduce significant biases in estimating the impact of bank competition on diversification by altering the underlying relationships between two variables. In order to overcome this issue, we modify our present dataset by excluding the years affected by economic and medical shocks. Subsample estimation results are summarized in Table 10, demonstrating that our previously obtained conclusions hold true despite the structural disruptions.

Robustness Checks in Subsamples.

This table presents system GMM regressions with 30 banks from 2010 to 2019.

*p < .1. **p < .05. ***p < .01.

We next employ a different econometric method. In an emerging body of literature, authors claim that the least squares dummy variable corrected (LSDVC) estimator may perform better than the GMM when the panel analyzed is relatively small and severely unbalanced. In this case, the LSDVC method effectively deals with the endogeneity issue by incorporating fixed effects to control for unobserved heterogeneity and applying a bias correction to the LSDV estimator. This approach reduces the bias associated with lagged dependent variables and provides more accurate and consistent parameter estimates, especially in small panels like ours (Boukhatem & Djelassi, 2020; Dang & Nguyen, 2022; Wang et al., 2019). Accordingly, we construct LSDVC estimates by adopting the approach accomplished by Bruno (2005) in applying 100-repetition bootstrapped standard errors. As a result, our estimates are identical regardless of changes in different versions of LSDVC, which reveals the consistent relationship between competition and diversification. Table 11 contains only the LSDVC findings that highlight bias-corrected standard error estimates recommended by Blundell and Bond (1998), for the purpose of brevity.

Robustness Checks by LSDVC Regressions.

This table presents LSDVC regressions with 30 banks from 2007 to 2021. Bootstrapped standard errors are reported in parentheses.

*p < .1. **p < .05. ***p < .01.

Does Market Competition Cause All Banks to Diversify Equally?

Our confirmed findings support the view that market competition places significant pressure on financial institutions, causing them to diversify across segments of assets and revenues to enhance their market positions. In the following subsection, we investigate the conditionality for this competition-diversification linkage, thereby shedding some light on how competition affects the working of banks. Accordingly, we propose that the effect of bank competition on diversification is conditional upon the features of the banking industry. As banks have different financial characteristics and operation productivity, they may assess bank competitiveness variably, causing them to respond differently to competitive pressures within the same environment. Furthermore, several studies analyze the impact of bank competition on diversification, but the implications on bank-level heterogeneity have still been unexplored (Căpraru et al., 2020; Nguyen et al., 2012). These arguments give us a natural motivation for testing the role of bank-level heterogeneity in the relationship between bank competition and diversification. In particular, we examine the mediating effect of bank-specific variables, including bank size, capitalization, risk, and profitability. These variables have been identified as standard characteristics to reflect banks’ financial strength and operating performance in the literature (Altunbas et al., 2010; Kashyap & Stein, 2000). We expect strong banks to be less influenced by competitive pressures thanks to their underlying capacity and competitive advantages.

Empirically, we employ the interaction terms between competition measures and bank-level variables in performing the task. The extended model is as follows:

where the results for the coefficient of the interaction term could indicate the differential impact of competition on bank diversification based on bank-level heterogeneity.

For brevity, Tables 12 to 15 only provide estimates for the stand-alone term of competition and its interaction with bank-level moderators. All controls are included, but their estimates are not displayed. Similar patterns are acquired when using alternative measures of bank diversification, but we only report those from the HHI approach. Consistent with our prior results, the coefficients on most competition measures remain unchanged or only lose some statistical significance in some columns, again confirming banks’ tendency to diversify when operating under high competitive pressures.

Moderating Role of Bank Size.

Competition measures are shown at the top of columns.

*p < .1. **p < .05. ***p < .01.

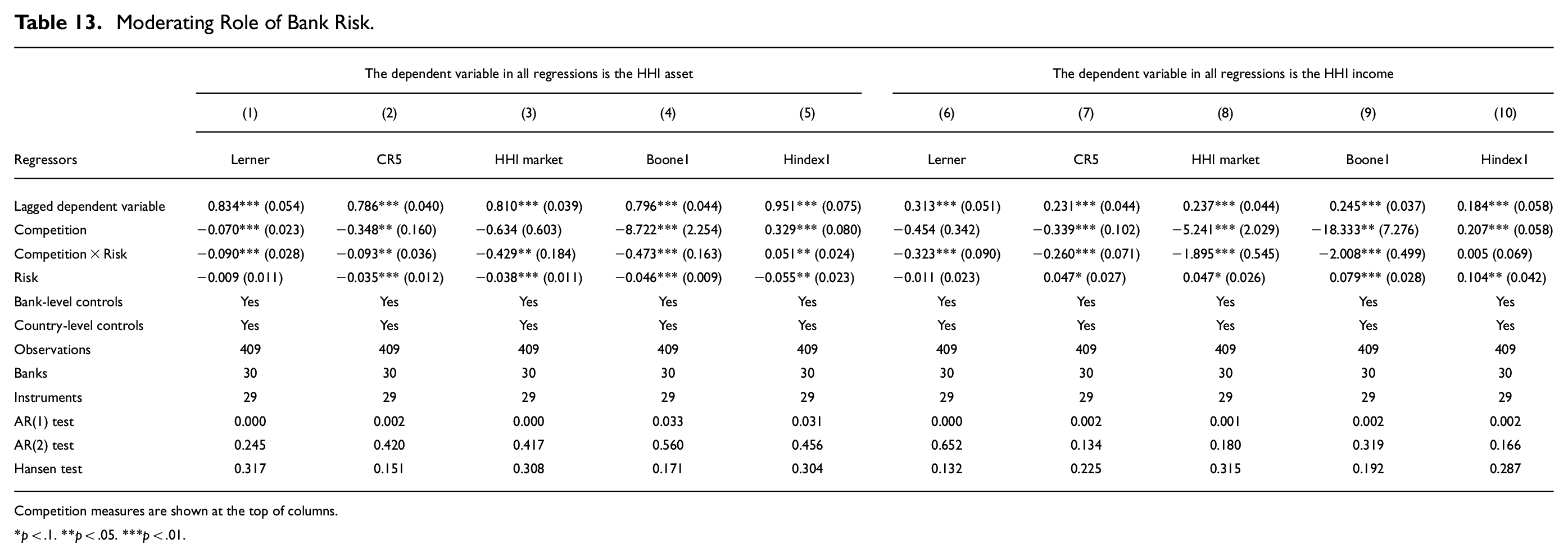

Moderating Role of Bank Risk.

Competition measures are shown at the top of columns.

*p < .1. **p < .05. ***p < .01.

Moderating Role of Bank Return.

Competition measures are shown at the top of columns.

*p < .1. **p < .05. ***p < .01.

Moderating Role of Bank Capital.

Competition measures are shown at the top of columns.

*p < .1. **p < .05. ***p < .01.

In Table 12, the estimates on the interaction term between competition and bank size exhibit statistically significant coefficients, and the signs are all opposite to those observed from the stand-alone competition measures. This result suggests that the effect of competition on the diversification of banks decreases with bank size. Next, we investigate the role of bank risk in Table 13. There is consistent evidence that the interaction term Competition × Risk yields significant coefficients, with signs similar to those gained from stand-alone competition measures. This result implies that the impact of bank competition on diversification is more pronounced for riskier banks.

The estimates in Table 14 suggest that the return ratio has no significant effect on the link between competition and diversification. We also report a similar result for the mediating role of bank capital in Table 15, as this factor does not significantly shape diversification behavior due to heightened competition. The results are consistent no matter which competition proxies are used. They indicate that the impact of bank competition on diversification is not found to be conditioned by bank profitability and capital buffers.

Overall, we gain evidence in line with our expectation presented earlier. Accordingly, a highly competitive market places greater pressure on small-sized banks and riskier banks, causing them to adopt a more aggressive diversification strategy. Moreover, as a broadened scope is also considered a risky strategy (Deyoung & Roland, 2001), strong banks do not necessarily accept additional risks to diversify when they already have substantial competitive advantages.

Conclusions

Based on a unique sample of Vietnamese commercial banks during 2007 to 2021, we document that banks are more likely to diversify their asset portfolios and income sources into non-lending activities and non-interest revenues amid high competition. In contrast, banks tend to be less diversified across economic sectors when offering credit in the context of higher competition. Meanwhile, the results indicate that banking market structure has no significant impact on banks’ decisions about their funding diversity. We further deepen our work by investigating whether some bank-specific characteristics potentially interact with the market competition when stimulating the diversification decisions of banks. While the stimulating impact of competition on the diversification of assets and income sources is confirmed, it is also worth noticing that this impact changes due to the influence of riskiness and the size of individual banks. The empirical results reveal that the effect of market competition on bank business models is stronger at smaller and riskier banks.

We can suggest some policy implications from this paper in the context of strong regulatory control by the SBV. Given the finding that different forms of bank diversification are affected differently by market competition, policy frameworks regarding activity strategies should be assessed carefully with specific reference to each dimension of bank diversification and not in a generic manner. In light of the tendency for banks to be less diversified across economic sectors when offering credit under high competition, the SBV should closely monitor sectoral concentration risks. Implementing guidelines to ensure balanced credit distribution can help mitigate risks associated with overexposure to specific sectors. Besides, given the finding that the diversification strategies are more pronounced at smaller and riskier banks, regulators and banking supervisors should closely scrutinize those vulnerable banks diversifying their business models since being subject to greater competitive pressure and having insufficient operational resources may pose potential risks. Along this line, the SBV should consider offering targeted support and guidance to these banks. At the same time, stakeholders and investors should be informed about the competitive pressures and their impact on bank diversification strategies. Understanding these dynamics can help stakeholders make more informed decisions regarding investments and partnerships with banks. Finally, from a perspective of research implication, this paper helps to remind other researchers of the significance of multidimensional analysis instead of generalizing the result when considering only a single aspect of bank diversification or competition.

We should acknowledge the current database as the limitation of the study, as we fail to include all commercial banks in Vietnam, which may affect the comprehensiveness of our analysis. We do not have sufficient data on foreign-owned banks to perform a thorough analysis for the impact of bank ownership (foreign vs. domestic banks). Future research could expand the dataset to contain more banks, including joint-venture banks and foreign bank branches, for a more complete representation of the banking sector and a valuable exploration of the role of bank ownership. Interestingly, apart from bank competition, investigating the role of technological innovation in shaping diversification strategies is a promising area for future research. This could provide valuable insights into how advancements in technology influence banks’ investment and business strategies. Hence, we suggest that future studies examine the impact of digital banking, fintech, and other technological advancements on banks’ strategic decisions, particularly in the context of diversification. Understanding these dynamics would contribute significantly to the ongoing scholarly discourse in the field.

Footnotes

Acknowledgements

The author is grateful to six anonymous reviewers and the editor for their valuable comments and suggestions. The author appreciates their time and effort in reviewing the manuscript and providing constructive feedback.

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.

Ethics Statement

Not applicable.

Data Availability Statement

The datasets generated during and/or analyzed during the current study are available from the corresponding author on reasonable request.