Abstract

With the rapid rise of mobile payment services in China, its welfare effect on residents has attracted wide attention from all sectors of society, but little is known about its negative consequences. Using panel data from the China Household Finance Survey in 2017, 2019, and 2021, and based on both subjective and objective perspectives, this study aimed to empirically analyze the impact of mobile payment usage on household over-indebtedness risk, its transmission mechanism, and role differences in different social groups. The results showed that mobile payments significantly increased the possibility of household over-indebtedness, including objective and subjective over-indebtedness. The mechanism analysis showed that mobile payments amplified the risk of household over-indebtedness mainly through two channels: promoting household consumption and alleviating household credit constraints (especially demand-oriented credit constraints). The heterogeneity analysis of sub-samples showed that mobile payments led to clear group differences in terms of increasing the risk of household over-indebtedness, with its promotion and popularization having a more profound impact on vulnerable groups, such as rural households, low-education households, and low-income and low-wealth households. This study addresses a key gap in the literature, helps with understanding the characteristics of household over-indebtedness in the mobile payment environment, and provides evidence-based guidance to assist individuals to engage with mobile payments more rationally and reduce their exposure to debt risks.

Plain Language Summary

This study, using detailed micro survey data from the China Household Finance Survey in 2017, 2019, and 2021, aimed to determine the role of mobile payments in promoting household over-indebtedness from both subjective and objective micro perspectives and to provide a new economic explanation for households’ over-indebtedness behavior and potential debt risks. We believe that our study addresses a key gap in the literature, helps with understanding the characteristics of household over-indebtedness in the mobile payment environment, and provides evidence-based guidance to assist individuals to engage with mobile payments more rationally and reduce their exposure to debt risks. The mechanism analysis showed that mobile payments amplified the risk of household over-indebtedness mainly through two channels: promoting household consumption and alleviating household credit constraints (especially demand-oriented credit constraints). The heterogeneity analysis of subsamples showed that mobile payments led to clear group differences in terms of increasing the risk of household over-indebtedness, with its promotion and popularization having a more profound impact on vulnerable groups, such as rural households, low-education households, and low-income and low-wealth households. Further, we believe that this paper will be of interest to the readership of your journal because it provides evidence-based findings highlighting the need to build a secure digital payment system and improve the risk supervision mechanism in the process of promoting the development of mobile payment services.

Keywords

Introduction

In recent years, global electronic payments, especially mobile payments, have experienced rapid development, and the issue of “going cashless” and “building a cashless society” has become a hot topic in the field of money management. The 2023 Annual Report on the Operation of China’s Payment System released by the People’s Bank of China showed that China was the world’s largest mobile payment market, with mobile payment transactions reaching 185.15 billion in 2023, totaling 555.3 trillion yuan (CNY) in transaction volume, up by 16.8% and 11.2% year-on-year, respectively, setting new records for both the number of transactions and transaction volume. According to the “Statistical Report on the Development of China’s Internet Network (December 2023)” released by the China Internet Network Information Center, as of December 2023, the number of Chinese Internet users had reached 1.092 billion, with an Internet penetration rate of 77.5%. The number of mobile payment users had reached 954 million, accounting for 87.3% of all Internet users. The technological innovation of Internet communication and the promotion and popularization of mobile terminal devices have led to mobile payments, mainly mediated by Alipay and WeChat Pay, rapidly replacing traditional cash and bank card payments to become the mainstay in China’s financial payment field.

The rise of mobile payments and its impact on people’s production and living behaviors have aroused extensive concern and discussion among scholars. Existing literature has studied the positive social effects of mobile payments from the aspects of financial regulation (Riley, 2018), financial transaction costs (Bachas et al., 2018), residents’ consumption (Zhao et al., 2022), consumption structure (Li et al., 2022) and social welfare effect (Chen et al., 2023). However, the exploration of the negative consequences of this new form of payment on individual behavior has been relatively more limited. Nevertheless, mobile payments, which have been developed based on the substantial scale of the e-commerce market and Internet technology to address consumer demand by facilitating payments and relaxing credit constraints, have also brought about excessive household debt and consequent financial vulnerability. The speed and portability of mobile payments have greatly optimized the consumption environment, improved users’ payment efficiency (Jack & Suri, 2014), and helped induce consumers’ unplanned purchase behavior. Furthermore, the digital currency used in mobile payments reduces the “pain of payment,” which helps weaken the psychological impact and potential payment discomfort caused by cash loss to users to a certain extent. The illusion of payment caused by such cognitive bias may result in an imbalance of self-control in terms of consumption desire (Zhang et al., 2022). Over-consumption increases the risk of families falling into financial distress and worsens their financial vulnerability (Gutiérrez-Nieto et al., 2017).

Mobile payments based on platforms such as WeChat Pay and Alipay can also provide users with credit services of different amounts according to their credit scores. While effectively alleviating the liquidity constraints of households, this also amplifies the risk of their over-indebtedness. The 2023 Annual China Leverage Ratio Report released by the Chinese Academy of Sciences showed that the resident leverage ratio rose from 8.3% in 1993 to 27.8% in 2011; an increase of less than 20 percentage points over 18 years. However, with the rise of mobile payments, the leverage ratio rose from 27.8% to 64.1% in just 12 years from 2011 to 2023, showing an accelerating upward trend and approaching the alert threshold set by the International Monetary Fund (65%). Moreover, long-term debt accumulation leads to frequent problems such as “short-term borrowing for long-term use” and “borrowing new to repay old.” People rely on “debt to finance debt” to continuously enlarge their leverage multiple, which may trigger a series of chain reactions and exacerbate potential risks in the financial market once natural disasters or other external adverse events occur (Albuquerque & Krustev, 2018).

In this context, it is of great theoretical and practical significance to examine the relationship between mobile payments and household over-indebtedness. This study aimed to address the following questions: How can household over-indebtedness be identified and measure?; Is it the case and, if so, how does the use of mobile payments magnify the risk of household over-indebtedness?, and; Is the impact of mobile payments the same on people from different social strata? In relation to the relevant literature, the contributions of this study are mainly reflected in the following three aspects.

First, regarding the identification of household over-indebtedness, most of the current literature is limited to fragmented evaluations of single-dimensional indicators (Diamond & Landvoigt, 2022; Santos & Veronesi, 2022). This study measured household over-indebtedness from both an objective perspective (whether the debt-to-income ratio exceeded 100% and whether the debt-assets ratio exceeded 50%) and a subjective perspective (whether the household reported difficulties in repaying loans for production and business projects, housing, education or medical care), which compensated for the one-sidedness of only using a single-dimensional indicator.

Second, there is currently no literature providing direct evidence that mobile payments promote household over-indebtedness. Relevant studies have only discussed the intrinsic connections between household consumption, consumption structure, credit constraints, and mobile payments (Ahmed & Cowan, 2021; Li et al., 2022; Manshad & Brannon, 2021). This study used panel data from the China Household Finance Survey (CHFS) in 2017, 2019, and 2021, and empirically demonstrated the significant promoting effect of mobile payments on household over-indebtedness, which provides a new economic explanation for understanding residents’ over-indebtedness behavior and potential debt risk issues.

Third, this study identified a key channel through which mobile payments promote household over-indebtedness. Taking credit constraints and consumption expenditure as breakthrough points, this study explored the transmission mechanisms involved in the impact of mobile payments on household over-indebtedness, finding that mobile payments magnify household financial leverage and aggravate over-indebtedness risk by alleviating household liquidity constraints and promoting their consumption expenditure. These finding enrich the research on micro-mechanisms related to the economic effects of mobile payments.

Literature Review

Household Over-Indebtedness and Its Influencing Factors

As an early-warning indicator to measure the potential financial risks of a household, over-indebtedness usually refers to the behavior or phenomenon in which households bear substantial debts and have difficulties in debt repayment (Hyytinen & Putkuri, 2018), or where their debt scale may lead to financial distress in the future, endangering the financial security boundary of the household (Enders & Hakenes, 2021). Concerning the identification and measurement of household over-indebtedness, the representative methods can be classified into two categories. One involves objective measurement, mainly based on household financial indicators, which is manifested as insolvency or inability to repay maturing debts, and expressed the asset-liability ratio (Santos & Veronesi, 2022; Tian, 2022), debt-to-income ratio (Jones et al., 2022), debt-to-service ratio (Bezawit & Hermann, 2018; Diamond & Landvoigt, 2022), and multiple liabilities (Brown et al., 2019). The other category involves subjective measurement, mainly based on a self-assessment index of household debt repayment ability, which is manifested as living beyond the household’s income and difficulty in maintaining a balance between household income and expenditure. Specifically, this can manifest in terms of whether a household feels that it is difficult to repay debts (Daud et al., 2019), whether it is necessary to make unacceptable structural sacrifices in the repayment process (Lusardi et al., 2020), whether it is difficult to cope with emergencies (French & McKillop, 2016), and whether it is unable to maintain basic living expenses (O’Connor et al., 2019 ).

The influencing factors of household over-indebtedness can be divided into three levels: household economic characteristics, demographic characteristics, and the macroeconomic environment. Household economic characteristics are the most direct factors affecting household over-indebtedness. Santos and Veronesi (2022) found that the lower the quantile of household net worth, the higher the debt-to-net worth ratio, which in turn intensified the risk of household over-indebtedness; moreover, this phenomenon was more pronounced among low-income households. Low income does not necessarily lead to over-indebtedness; in fact, low-income families are usually less inclined to be in debt (Noerhidajati et al., 2021). Bazillier and Hericourt (2017) found that high-income families were more willing to use leverage because they were more inclined to take on debt to gain more benefits. Families with a strong risk tolerance are more likely to take on additional risks through borrowing in pursuit of maximizing utility, which leads to a higher household leverage ratio. However, in good economic conditions, families with a higher risk tolerance may become wealthier, resulting in a decrease in the debt-to-net asset ratio and reducing the possibility of household over-indebtedness (Santos & Veronesi, 2022).

In terms of family demographic characteristics, families with a high ratio of infants and toddlers have a lower financial risk tolerance. A large number of dependent children can reduce the family’s wealth level, making the family more likely to become financially vulnerable and exacerbating the risk of over-indebtedness (Buleca et al., 2022). Greater financial literacy and cognitive ability can help households analyze borrowing costs more effectively and identify opportunities more accurately to accelerate wealth accumulation or maximize the value of household resources, which can in turn reduce the possibility of household over-indebtedness while promoting responsible household debt behavior (Gaffeo, 2019; Tang, 2021). In addition, employment status, health condition, risk preference and marital status can all have an impact on household over-indebtedness (Ali et al., 2020; Daud et al., 2019; He & Zhou, 2022). In terms of the macroeconomic environment, monetary policy and financial innovation (Mian & Sufi, 2018), financial liberalization and deregulation (Brown et al., 2019), expectations of rising house prices (Abid & Shafiai, 2018; Jarmuzek & Rozenov, 2019), and the social welfare system (Coletta et al., 2019) are regarded as important factors influencing household over-indebtedness.

The Social Effects of Mobile Payments

The use of mobile payments effectively addresses issues arising due to poor security, strong time-space constraints, and serious resource waste in traditional cash transactions (Kalckreuth et al., 2014). Moreover, the traceability of mobile payment tools can prevent tax evasion, corruption, and other criminal acts when using cash; reduce anti-money laundering pressure on financial institutions and relevant regulators; and help maintain the stability of the social order, thereby improving the efficiency of social operations (Riley, 2018). In recent years, scholars have conducted many explorations of the role of mobile payments in relation to individual behavior. Bachas et al. (2018) report that mobile payment tools facilitate transfer, payment, and other functions by virtue of digital finance and information technology, which spares retailers the cumbersome procedures and costs in applying for card-swipe equipment (e.g., POS machines) and makes financial services more popular. Ahmed and Cowan (2021) used household survey data from 2013 to 2016 in Kenya and reported that mobile payments helped reduce financial transaction costs, enabling households to obtain more loans and effectively reduce their liquidity constraints. In addition, some studies have also found that mobile payments can effectively reduce costs in terms of holding coins/cards and reduce the currency inventory, thereby promoting the growth of individual welfare (Chen et al., 2023), promoting household consumption while reducing the transparency of payments (Manshad & Brannon, 2021; Zhao et al., 2022), and improving the consumption structure of households while easing the credit constraints of households (Li et al., 2022; Riley, 2018).

Research Hypotheses

In contrast to extensive research on the positive effects of mobile payments, the exploration of the negative consequences of this new payment form on individual behavior has been relatively limited. The key aim of this study was to determine whether and how the use of mobile payments affect household over-indebtedness. There is currently no direct evidence concerning the impact of mobile payments on household over-indebtedness in the literature. However, theoretical and empirical analyses in previous relevant studies suggest that mobile payments may have an impact on household debt risk mainly through two mechanisms.

One influencing mechanism could be that mobile payments stimulate residents’ consumption demand through convenient payment and increase household consumption expenditure, thereby promoting household over-indebtedness. First, compared with traditional payment methods, mobile payments do not require carrying cash or bank cards, and transactions can be easily completed with the help of mobile terminal devices (such as smart phones and iPads) and payment tools (such as mobile banking, Apple Pay, WeChat Pay, and Alipay), which can mitigate dependence on financial physical outlets (Yin et al., 2019). The speed and portability of mobile payments have greatly optimized the consumption environment and improved users’ payment efficiency (Jack & Suri, 2014), while convenient payments help stimulate residents’ consumption (Boden et al., 2020). Second, mobile payments can integrate multiple bank cards and provide multiple payment channels (Karaivanov, 2012), which can overcome restrictions on users’ temporary or accidental consumption demand because they might not be carrying cash and therefore help induce consumers’ unplanned purchase behavior. Third, from the perspective of currency form, compared with traditional payment methods, the consumption involved in mobile payments is more hidden. The digital currency used in mobile payments reduces the “pain of payment,” which helps weaken the psychological impact and potential payment discomfort caused by cash loss to users to a certain extent (Manshad & Brannon, 2021). The illusion of payment caused by such cognitive bias may cause people to break out of budget constraints derived from a “mental account,” resulting in an imbalance of self-control in terms of consumption desire (Meyll & Walter, 2019; Wang et al., 2022), and even induce consumers’ purchase motivations without restraint, which eventually leads to the tightening of capital liquidity and an aggravation in household over-indebtedness risk. Based on the above analysis, we propose the following hypotheses:

Another influencing mechanism could be that mobile payments help broaden users’ external financing channels, which can increase household financial leverage by alleviating household liquidity constraints, thus inducing household over-indebtedness. In addition to the most well-known and widely recognized payment functions, mobile payments comprise diversified financing services for different users (T. Liu et al., 2020; Munyegera & Matsumoto, 2016). For example, Alipay users can use “Ant Credit Pay” for a certain amount of consumer overdraft, and third-party payment platforms can rely on the credit points accumulated by users in the process of mobile payment to provide credit services with varying amounts of credit, such as Tencent Financial’s “Microloan,” Ant Group’s “Ant Cash Now,” and Jingdong Mall’s “JD White.” This kind of credit service does not require guarantees on application, has a simple review procedure with lending extended quickly, which greatly reduces financial transaction costs and the financial service threshold (Ahmed & Cowan, 2021). In particular, it can effectively alleviate the liquidity constraints faced by users and allow vulnerable people who are usually excluded from traditional financial institutions to access more credit support (Gabor & Brooks, 2017; Y. Liu et al., 2021).

Li et al. (2022) report that mobile payment platforms conduct big data analysis and credit rating assessment based on “scenarios” derived from online shopping and the use of social media, which encourages expansion and deepening of the reach capacity and coverage of financial credit services. Yin et al. (2019) used data from the Chinese Family Panel Studies and found that mobile payments provided a new technology and channel to ease household liquidity constraints, reducing the formal financial constraints faced by households and with a more significant impact on disadvantaged groups from the mid-west regions and rural areas of China. Riley (2018) compared the difference in consumption changes between households using mobile payments and households not using mobile payments under the shock of adverse external events, such as floods or droughts, and found that only mobile payment users had no decrease in consumption, with mobile payments releasing the pent-up consumption demand of households by significantly overcoming their liquidity constraints. However, as Mian et al. (2017) point out, household debt accumulated by increasing leverage is likely to cause over-indebtedness and aggravate household financial vulnerability in the event of major or unexpected negative shocks, such as natural disasters, diseases, and unemployment. Accordingly, this study proposes the following hypothesis:

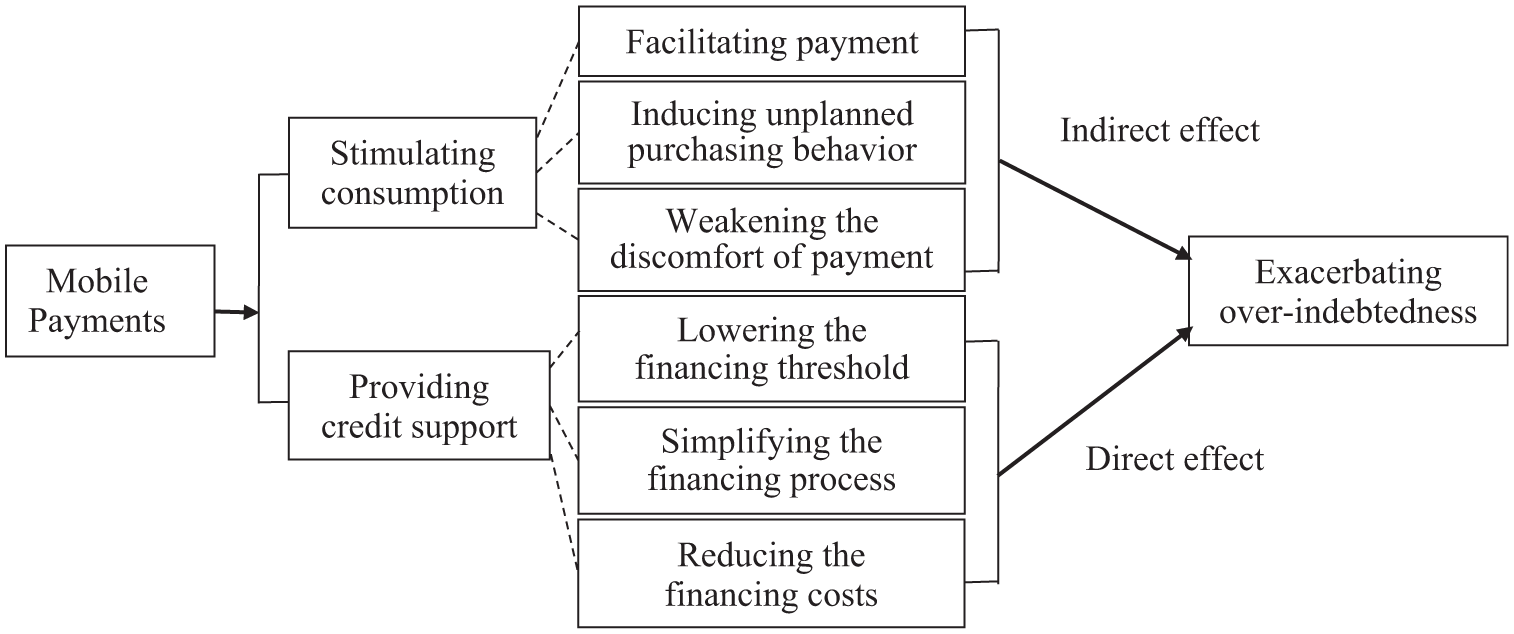

To summarize, the impact path through which mobile payments magnify the risk of household over-indebtedness is shown in Figure 1.

The impact path of mobile payments on household over-indebtedness.

Methods

Data

The data used in this study were derived mainly from the CHFS in 2017, 2019, and 2021. The CHFS is a nationwide large-scale social survey project launched by the Southwestern University of Finance and Economics, aiming to collect relevant information on household finance. The survey questionnaire covers three subject types: community, family, and individual. This questionnaire is used to collect detailed information on families and their members’ employment and income, assets and liabilities, consumption behaviors and payment methods, social security and insurance, and other aspects. These types of data are ideal for examining household over-indebtedness behavior and its relationship with mobile payments, as undertaken in this study. The sample sizes were 40,011 in 2017, 34,643 in 2019, and 22,027 in 2021, covering 355 counties (districts or county-level cities) across 29 provinces in China. In the data processing, based on the household code, we only selected the household samples that were collected in all three rounds of surveys, and eliminated the samples with missing data for the main variables, leaving 19,280 valid samples (the total sample sizes of the three periods were 57,840).

Variables

Over-indebtedness

Common methods for measuring household over-indebtedness include subjective and objective measures. In general, subjective measures are superior to objective measures in terms of information richness because subjective indicators not only reflect the objective financial situation of the family to a certain extent, but also include factors that cannot be examined by objective indicators (Nielsen et al., 2015). For example, multiple observable and unobtainable factors, such as future income expectations, the social and economic environment, family social networks, and health risks, may affect the household’s ability to repay debt. Subjective indicators can accurately capture more sensitive aspects of household financial status and provide far more information than objective indicators. However, subjective measurements are easily affected by respondents’ emotions, which may lead to inconsistent subjective judgments when facing the same debt situation (Santos & Veronesi, 2022). To compensate for the one-sidedness of using a single-dimensional index, this study measured household over-indebtedness from both objective and subjective perspectives.

Objective Over-Indebtedness Indicators

The current literature mainly uses stock indicators (such as the debt-to-assets ratio) and flow indicators (such as the debt-to-income ratio or debt-service income ratio). Considering that flow indicators can more directly measure the financial vulnerability of households and are more extensively used (Diamond & Landvoigt, 2022), and that various data concerning household’s debt repayment are not collected in the CHFS questionnaire, this study used the debt-to-income ratio to measure household financial leverage. Studies have shown that when the debt-to-income ratio exceeds 100%, the household financial situation will deteriorate sharply (Jones et al., 2022). Therefore, this study selected households whose ratio of total debt to total income exceeded 100% as over-indebted households. The higher the ratio, the higher the debt repayment pressure on the sample households, the greater the possibility of households falling into financial distress, and the more serious their potential debt risk. Total household income in the CHFS includes five categories: agricultural income, industrial and commercial income, wage income, investment income, and transfer income, where total household debt refers to the total amount of household debt in relation to house purchases, car purchases, entrepreneurship, education, medical care, and consumption. In the robustness test, this study also used the stock indicator, that is, households with a debt-to-assets ratio of over 50%, to define over-indebted households. When the household debt-to-assets ratio exceeded 50%, the objective over-indebtedness indicator was valued as 1; otherwise, it was 0.

Subjective Over-Indebtedness Indicators

Considering that objective indicators of over-indebtedness cannot capture the potential impact of future household income expectations and socioeconomic circumstances, this study adopted the approaches of Mutsonziwa and Fanta (2019) and Lusardi et al. (2020) to introduce a self-evaluation indicator of household debt service capacity to depict whether households subjectively believe that they have over-indebtedness issues. The CHFS asks, “At present, what is your family’s financial ability to repay loans for production and business projects, housing, education and medical care?” The answer options range from 1 to 4, corresponding to “completely no problem,”“basically no problem,”“difficult to repay,” and “completely unable to repay,” respectively. This study constructed a self-evaluation indicator of household over-indebtedness based on respondents’ answers. When one or more types of debt in the household were reported as being completely unable or difficult to repay, the dummy variable was valued as 1, indicating that the household subjectively believed that there was a financial dilemma in terms of over-indebtedness; otherwise, the value was 0, indicating that the household subjectively perceived no financial distress.

Table 1 illustrates the basic situation concerning the distribution of over-indebtedness among the resident households in the sample. The statistical results show that objective over-indebtedness in Chinese households accounted for 17.08%, and subjective over-indebtedness accounted for 5.78% in 2017. Compared with 2017, the proportion of objective over-indebted households increased by 3.41% and 1.83% in 2019 and 2021, respectively, while the proportion of subjective over-indebted households increased by 1.68% and 1.73%, respectively. From the comparison between urban and rural areas, regardless of whether the year was 2017, 2019, or 2021, the objective over-indebted ratio of rural households was lower than that of urban households, but the subjective over-indebted ratio was higher, which may be related to the weaker borrowing ability and greater financial vulnerability of rural households.

The Basic Status of Households’ Over-Indebtedness Distribution in China (Unit: %).

Mobile Payments

Mobile payments refer to financial transaction behavior in which consumers use wireless communication technology and mobile terminal devices (such as portable tablets, and smartphones) to pay retailers equal-value currency to obtain goods or services (Yin et al., 2019). In the CHFS, payment methods are measured using the following question: “The payment methods you and your family members usually use when shopping (including online shopping) are (multiple options): (1) Cash; (2) Swiping bank card (including credit and debit card) by POS machine; (3) Payment by computer (e.g., online banking); (4) Payment by smart phone, pad and other mobile terminals (including WeChat Pay, Alipay, mobile banking, Apple pay, etc.); (5) Other.” Following the approach of Yin et al. (2019), this study regarded households that selected option (4) as households using mobile payments and assigned a value of 1 if they selected (4) and 0 otherwise.

Table 2 shows that the proportion of households using mobile payments in China was 33.50% in 2021, among which the proportion of urban households was 49.06%, and the proportion of rural households was only 11.54%, less than a quarter of the proportion of urban households. From 2017 to 2021, the proportion of both urban and rural households using mobile payments rose significantly, and the increase in urban households was even greater. From the comparison of different regions, regardless of being urban or rural, the penetration rate of mobile payments in the eastern region was higher than that in the central and western regions. The use of digital finance, which is being actively promoted by the Chinese government, has clearly been undergoing major expansion. However, the proportion of households using mobile payments in the central and western regions and in rural areas was much lower than that in the eastern regions and urban areas, indicating that the popularization of mobile payments still differs significantly between urban and rural areas and among different geographical regions.

The Usage Status of Mobile Payment in Chinese Households (Unit: %).

Table 3 shows that the subjective over-indebtedness ratio of households using mobile payments was 8.13%, and that of households not using mobile payment was 7.17%; basically the same. However, from the perspective of objective over-indebtedness, the proportion of objective over-indebted households not using mobile payments nationwide was 16.30%, while that of households using mobile payments was 30.13%, which was nearly twice as high. Moreover, compared with households not using mobile payments, the proportion of objective over-indebted households using mobile payments was significantly higher in both rural and urban households, with the former being 15.97% and 16.68%, respectively, and the latter being 24.08% and 31.14%, respectively.

Mobile Payment and Households’ Over-Indebtedness Distribution in China.

Control Variables

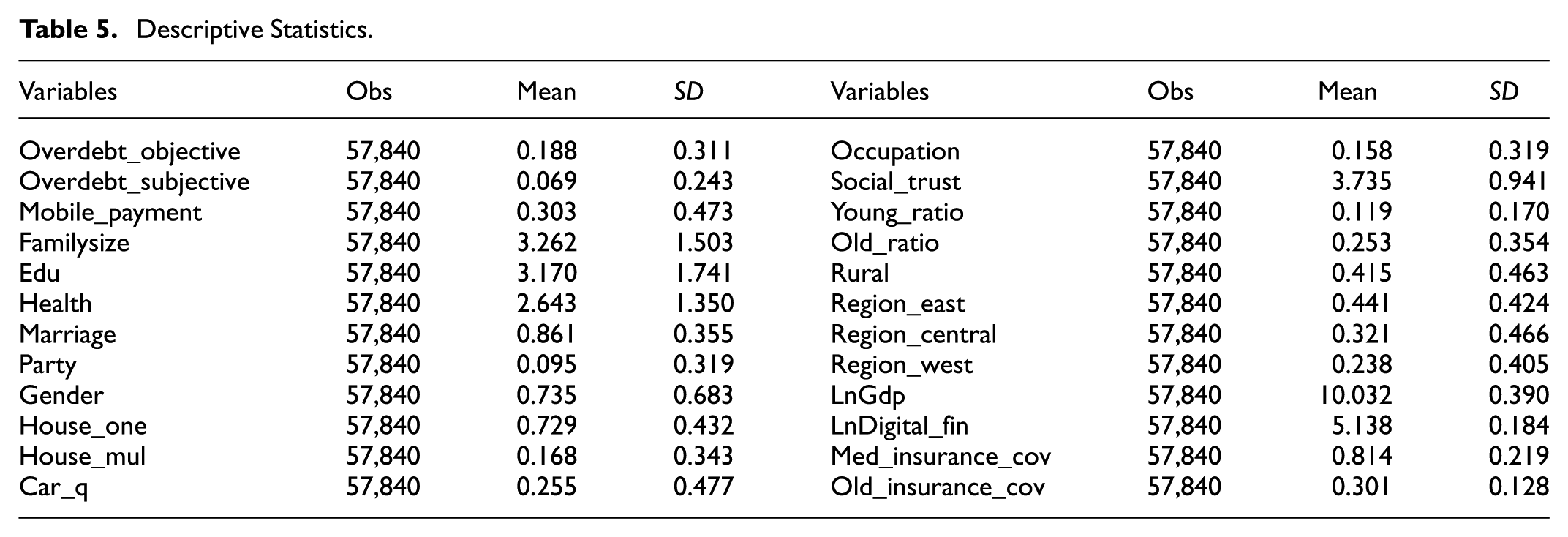

Referring to previous studies on household debt decisions and over-indebtedness behavior (Diamond & Landvoigt, 2022; Frazzini & Pedersen, 2022; Jones et al., 2022), the control variables selected in this study covered three categories: household head characteristics, household unit characteristics, and regional and economic characteristics. Household head characteristic variables include gender, health status, marital status (whether there is a spouse), political status (whether the householder is a member of the Communist Party of China), education level, social trust level, and occupation (whether the householder is engaged in self-employment). Household debt is the product of collective decision-making of the whole family. The choice and degree of household debt are not only affected by the individual characteristics of the household head but also depend on the family structure and wealth characteristics (Frazzini & Pedersen, 2022; Noerhidajati et al., 2021). Household unit characteristic variables include the size of the household, the number of cars owned by the household, the status of the household owning real estate (whether the household owns only one property, whether the household owns two or more properties), the proportion of older adults (over 60 years old) in the household, and the proportion of children (under 16 years old) in the household. The external regional characteristics and financial environment in which residents are located may also affect household debt decisions (Brown et al., 2019; Coletta et al., 2019). Regional and economic characteristic variables include household registration (urban or rural), region where the sample households are located (eastern, central, or western), per capita GDP, digital financial inclusion development index, endowment insurance coverage rate, and medical insurance coverage rate at the provincial level. The definitions and descriptive statistics of the main variables are presented in Tables 4 and 5, respectively.

Variable Definition.

Descriptive Statistics.

Empirical Models

The explained variable in this study is a binary categorical variable; therefore, we used a Probit model to estimate the impact of mobile payments on household over-indebtedness. The econometric model is as follows:

Such that

where

Results and Discussion

Baseline Results

Columns (1) and (3) of Table 6 present the baseline regression results for the impact of mobile payments on objective and subjective over-indebtedness, respectively. The results show that the regression coefficients of mobile payments in the two groups of models were 0.0934 and 0.0510, respectively, and that both were positively significant at least at the 5% statistical level. These results indicate that the use of mobile payments did indeed amplify the household financial leverage (debt-to-income ratio), and the probability of subjectively believing that the family was over-indebted and would fall into financial distress also increased significantly. Because the Probit model cannot be used to calculate the marginal effect of the regression parameters, the parameter values given in Table 6 are all estimated coefficients and do not represent their marginal contributions to objective and subjective over-indebtedness.

The Impact of Mobile Payments on Households Over-Indebtedness: Panel Fixed Effect.

Note. Robust standard errors clustering by community/village are shown in parentheses.

p < .01. **p < .05. *p < .10.

From the perspective of empirical methods, the estimation results concerning mobile payments in the above regression may be endogeneity biased. On the one hand, households with small credit needs or overdraft habits in daily life may deliberately use mobile payments as a credit channel, so a reverse causality mechanism can be involved. On the other hand, household debt behavior and mobile payment usage may also be jointly affected by unobservable factors such as the local economic and financial environment, behavioral habits, or social interactions, and the omitted variable problem can also lead to biased estimation results. Following the approach of Yin et al. (2019), this study selected the “number of smartphones owned by the family” as an instrumental variable (IV) in relation to mobile payments. First, as the most popular mobile terminal device, smartphones are necessary for people to make convenient mobile payments. There is a close relationship between smartphone ownership and mobile payment behavior. Second, smartphones are basic communication tools for families. Despite some instances of loans to purchase smartphones, for most families, whether they own smartphones and how many they own does not usually directly lead to over-indebtedness; thus, this variable has good exogeneity in relation to estimating household over-indebtedness.

Columns (2) and (4) of Table 6 present the estimated results of the two-stage regression using the IV-Tobit model. The results show, in terms of the Wald endogeneity test in both groups of models, that the null hypothesis (

In addition to mobile payments, household unit and household head characteristics significantly affected the risk of household over-indebtedness. Among the influencing effects of the control variables in Columns (1) to (4) of Table 6, significant and robust findings were determined in relation to the following. Having male heads of households, engaging in self-employment, and poorer health significantly increased the risk of household over-indebtedness. The higher the proportion of older adults and the higher the coverage of medical insurance in the household’s location, the lower the risk of household over-indebtedness. Compared with households without property (the reference group), households owning only one property and those owning two or more properties had significantly higher subjective and objective over-indebtedness risks. These regression results are in line with intuitive expectations and are consistent with the conclusions of the mainstream literature (Ali et al., 2020; Buleca et al., 2022; He & Zhou, 2022).

The one exception involved the situation where higher levels of education among household heads increased the household’s objective over-indebtedness behavior, but reduced its subjective over-indebtedness probability. One possible explanation for this finding is that higher levels of education increase households’ ability to borrow and repay debt, which magnifies their debt-to-income ratio but simultaneously reduces the likelihood that they will perceive financial distress. From the perspective of regional and urban-rural differences, compared to central and eastern regions, the subjective and objective over-indebtedness risk of households in the western regions was significantly higher; the objective over-indebtedness risk of rural households was significantly lower than that of urban households; and the subjective over-indebtedness risk of rural households was significantly higher than that of urban households; all consistent with the statistical findings presented in Table 1.

Robustness Testing

Robustness Test I: Using the Debt-to-Assets Ratio Instead of the Debt-to-Income Ratio

The debt-to-assets ratio is also an important dimension for measuring the degree of household over-indebtedness (Santos & Veronesi, 2022). Normally, borrowers are at risk of bankruptcy and default when their total debt exceeds their total assets, and they can be considered to be insolvent. “Insolvency,” as the strictest criterion to measure the potential debt risk of households, is not universally adaptable in reality. In practice, although financial institutions set different thresholds for the debt-to-assets ratio in household financial risk assessments, most do not exceed 50% (Michelangeli & Pietrunti, 2014). When the ratio of household debt-to-assets exceeds 50%, the debt burden and financial vulnerability caused by over-indebtedness become prominent, and the risk of default is very high when faced with external shocks such as unemployment, major illness, or interest rate fluctuations. Therefore, this study applied a second definition of the objective over-indebtedness of households: households with debt-to-assets ratios above 50% were considered over-indebted households and were assigned a value of 1; otherwise, 0.

Columns (1) and (2) of Table 7 present the regression results in terms of mobile payments on whether the household debt-to-assets ratio exceeded 50%. The results show that, regardless of the baseline model estimate or the IV model estimate, mobile payments significantly increased the probability of the household debt-to-assets ratio exceeding the 50% threshold, indicating that mobile payments increased the possibility of objective over-indebtedness of households. The p-value of the Wald endogenous test for the smartphones instrumental variable was .1104, close to the significance level of 10%, indicating that the conclusion was robust and reliable.

Robustness Test: Using Different Over-Indebtedness Indicator and Lag Variable Regression.

Note. The control variables are the same as Table 6.

p < .01. **p < .05. *p < .10.

Robustness Test II: Lag Variable Regression

To overcome the endogeneity problem, we used the predetermined variables for assessing mobile payments. Specifically, we examined the impact of mobile payments in 2017 and 2019 on household over-indebtedness in 2019 and 2021, respectively. On the one hand, the over-indebtedness of current residents can be considered unlikely to have affected the mobile payment behavior of the household in previous years. On the other hand, people’s economic behaviors and activities can maintain relative continuity and stability over a short time span (Chai et al., 2024); that is to say, mobile payment variables can be expected to be highly correlated between two adjacent periods of data. Therefore, these predetermined variables would be expected to have good exogeneity. Columns (3) and (4) of Table 7 provide the estimation results for the lag variable regression. The β values of mobile payments were 0.0627 and 0.0256, respectively, and both were significantly different from 0 at least at the 10% significance level, indicating that mobile payments significantly enhanced the possibility of objective and subjective over-indebtedness of households. These results are basically consistent with those presented in Columns (1) and (3) of Table 6.

Robustness Test III: Deleting the Upper and Lower 5% Samples

In household questionnaire data, a non-normalized and unbalanced distribution of sample data is widespread (Chai et al., 2023). For the CHFS data used in this study, household income and debt data were aggregated from various categories (including the aggregation of household members and the aggregation of income and debt categories). Families are usually reluctant to provide detail or do not accurately provide details concerning income and debt owing to financial privacy concerns, resulting in a large number of zeros in some accounts, which may cause excessive measurement errors in the calculation of household over-indebtedness. In view of this, we removed the samples with the highest 5% and lowest 5% household income (as shown in Panel A of Table 8) as well as the samples with the highest 5% household debt (as shown in Panel B of Table 8) to re-verify the impact of mobile payments on the risk of household over-indebtedness. The regression results are shown in Table 8, where Columns (1) and (3) are the benchmark estimates and Columns (2) and (4) are the IV estimates. All four groups of models showed that the use of mobile payments increased the risk of objective household over-indebtedness and the probability that households subjectively believed that they would be in financial distress also significantly increased, further supporting the conclusion that mobile payments increase the risk of household over-indebtedness.

Robustness Test: Deleting the Upper and Lower 5% Samples.

Note. The control variables are the same as Table 6.

p < .01. **p < .05. *p < .10.

Mobile Payments and Household Over-Indebtedness: Transmission Mechanism Analysis

Impact Mechanism I: Stimulating Household Consumption

The above analysis showed that the use of mobile payments significantly promoted household over-indebtedness behavior, including objective and subjective household over-indebtedness. What mechanism underlies this promoting effect? As noted, theoretically, mobile payments may amplify the risk of household over-indebtedness by releasing residents’ consumption demand; thus promoting household consumption expenditure. To identify any mediation effect, this study constructed the following recursive model to test whether mobile payments (

Household consumption expenditure in the CHFS is classified into eight categories: daily necessities, clothing, food, daily living, medical care, transportation and communication, education and entertainment, and other service expenditures. In accordance with Chai et al. (2023), the following steps for identifying a mediation effect were applied. First, it was tested whether mobile payments significantly affected household over-indebtedness; that is, whether

Specifically, the criterion for evaluating whether the intermediary effect existed was as follows. If both

Table 9 reports the estimated results of the above recursive model. Columns (1) and (2) show that the use of mobile payments significantly increased household consumption expenditure. Columns (4)-(6) show that after the intermediary variable of household consumption expenditure was included in the regression equation of household over-indebtedness, although the value of

Impact Mechanism I: Stimulating Household Consumption.

Note. The control variables are the same as Table 6.

p < .01. **p < .05. *p < .10.

Impact Mechanism II: Relaxing Household Credit Constraints

Another influencing mechanism could be that the use of mobile payments broadened users’ external financing channels, which may amplify the risk of over-indebtedness by relaxing household credit constraints. The CHFS asks, “Why did your family not apply for a loan from a bank or credit union to obtain the required funds?” The corresponding options are: (1) needed but not applied for, (2) the application was rejected, (3) the loan interest is too high, (4) the repayment period or method does not meet the demand, (5) do not know the bank or credit union staff, (6) there is no loan guarantor, and (7) worry about not being able to pay. Following the approach of Yin et al. (2019), if the reason why a household did not apply for a loan from a bank or credit union to obtain the required funds was “needed but not applied for,” or “the application was rejected,” the household credit constraint was considered to equal 1, otherwise it was 0. Further, we generated two dummy variables “need but no application” and “application rejected” in the sample with credit constraints, and measured demand-oriented credit constraints and supply-oriented credit constraints, respectively.

Following the same approach, this study used the recursive model set out above to test whether mobile payments affected over-indebtedness by alleviating household credit constraints. The regression results in Columns (1) and (2) of Table 10 show that, regardless of the benchmark regression estimates or the IV estimations, households using mobile payments were subject to lower credit constraints than those that did not use mobile payments, and the difference was statistically significant at the 1% level, indicating that the use of mobile payments significantly reduced household liquidity constraints.

The Impact of Mobile Payment on Household Credit Constraints.

Note. The control variables are the same as Table 6.

p < .01. **p < .05. *p < .10.

To further clarify the impact of mobile payments on the type of credit constraint and, ultimately, on household over-indebtedness risk, this study examined the impact of mobile payments on demand-oriented and supply-oriented credit constraints, as well as the differences in the impact of different mechanism variables on objective and subjective over-indebtedness. Columns (3)–(6) of Tables 10 and 11 show the results. The main conclusions are as follows. First, the use of mobile payment only reduced household demand-oriented credit constraints but had no significant impact on supply-oriented credit constraints. Second, demand-oriented credit constraints reduced both subjective and objective over-indebtedness risk, whereas supply-oriented credit constraints increased household over-indebtedness (especially objective over-indebtedness). Third, compared with the benchmark regression results in Table 6, the

Impact Mechanism II: Relaxing Household Credit Constraints.

Note. The control variables are the same as Table 6.

p < .01. **p < .05. *p < .10.

These findings can be explained from three perspectives. The first involves the lending channel. Mobile payments provide diversified financing services for different users (Ahmed & Cowan, 2021; T. Liu et al., 2020), but are limited to the third-party payment platform on which they rely, and cannot directly affect the lending of banks or credit unions to customers. In other words, as expected given this context, there was negligible impact found of mobile payments on supply-oriented credit constraints. The second involves behavioral guidance. Households that have rigid credit needs but which are refused loans from formal financial institutions may turn to informal financial institutions (e.g., private credit institutions) that charge higher interest rates. However, informal credit is much more likely to create household over-indebtedness than formal credit. In other words, supply-oriented credit constraints may increase the risk of over-indebtedness. The third involves demand driving. Third-party payment platforms on which mobile payments rely provide diverse credit services to different groups with a simple approval process, fast lending speed, and no loan guarantee requirements, greatly enhancing users’ expectations of credit access and stimulating household credit demand, thus promoting household borrowing behavior through demand-driven mechanisms, which increases the possibility of over-indebtedness, including objective and subjective over-indebtedness. These results confirm the existence of a relaxing credit restraint mechanism; thus

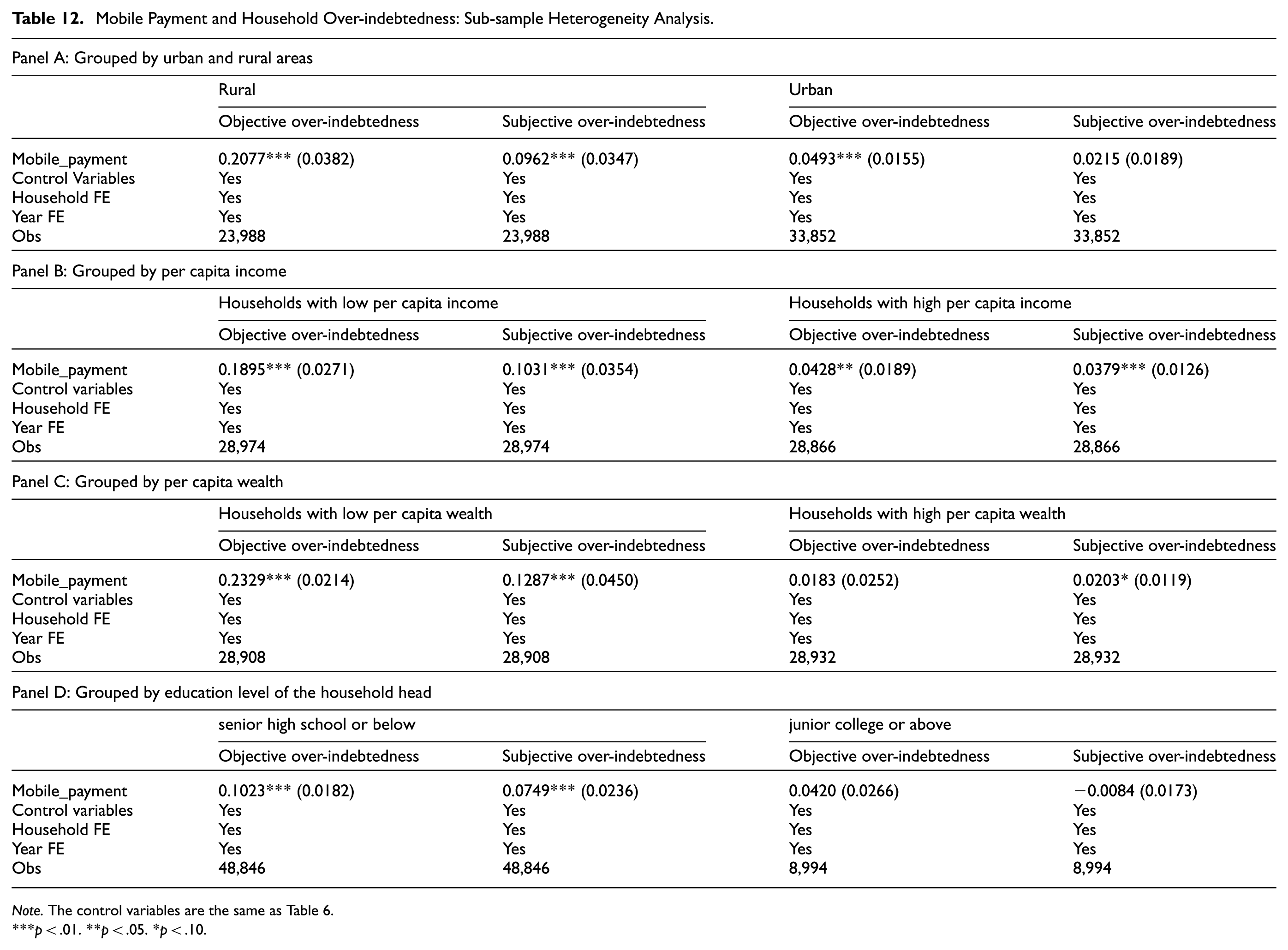

Mobile Payments and Household Over-Indebtedness: Sub-sample Heterogeneity Analysis

The above research results show that mobile payment significantly increased the possibility of household over-indebtedness, including objective and subjective over-indebtedness. Further, we addressed the question: Is the impact of mobile payments the same on people from different social strata? In this section, to explore the differences in the impact of mobile payment on over-indebtedness risk among different social strata, we conducted a sub-sample heterogeneity analysis according to household different registrations, household income, wealth stratum, and education levels. The estimation results are presented in Table 12.

Mobile Payment and Household Over-indebtedness: Sub-sample Heterogeneity Analysis.

Note. The control variables are the same as Table 6.

p < .01. **p < .05. *p < .10.

Panel A of Table 12 divides households according to their urban and rural registration and presents an analysis of the difference in the impact of mobile payments on the over-indebtedness of urban and rural households. The results show that the use of mobile payments significantly increased the possibility of objective over-indebtedness in both urban and rural households; however, the marginal impact of mobile payments on the objective over-indebtedness of rural households was greater. From the perspective of subjective over-indebtedness, mobile payments only significantly increased the risk of subjective over-indebtedness in rural households. One possible explanation for this is that if mobile payments amplify the risk of over-indebtedness by diminishing household liquidity constraints and releasing pent-up consumption demand, then for rural households with insufficient resource endowments and more severe financial constraints, the consumer overdraft (such as “Ant Credit Pay”), and micro-lending (such as “Ant Cash Now” and “Microloan” ) services provided through mobile payments belong to the “reprieve from the brink” category, whereas, for urban households, the role of mobile payments is only to enhance their external financing channels, belonging to the “icing on the cake” category. In other words, mobile payments have a more significant promoting effect on the over-indebtedness of vulnerable groups with smaller endowments, namely, rural households.

Regressions grouped by wealth and income yielded similar conclusions. In Panels B and C of Table 12, the sample households are divided into low-income groups (below the median) and high-income groups (above the median) based on their per capita income and into low-wealth groups (below the median) and high-wealth groups (above the median) based on their per capita wealth ((total household assets – total household liabilities)/number of household members). The results show that, regardless of objective or subjective over-indebtedness, the use of mobile payments increased the risk of over-indebtedness in low-income and low-wealth households at a statistically significant level of 1%; however, for high-income and high-wealth households, the impact of mobile payments was smaller or even insignificant.

Mobile payments had differing roles in households with different educational levels. According to the educational differences of the household heads, the sample households were divided into two sub-samples: households with low education levels (senior high school or below) and households with high education levels (junior college or above). Panel D in Table 12 presents the regression results of the impact of mobile payments on household over-indebtedness among the different education-level groups. The results show that when the head of the household had a senior high school education or below, the use of mobile payments significantly increased the risk of household over-indebtedness, including objective and subjective over-indebtedness risk. However, for highly educated households (where the head of the household had a junior college education or above), the role of mobile payments was not significant.

This may be because individuals with a higher level of education generally have higher income and greater wealth (Gaffeo, 2019), and a stronger ability to insulate themselves against external uncertain risk shocks (Santos & Veronesi, 2022). Even if they use mobile payments to relax liquidity constraints and smooth household unexpected expenditures, these households do not tend to fall into subsequent financial difficulty or endanger the household’s financial security boundary. Therefore, the use of mobile payments only increased the risk of over-indebtedness among households with low levels of education and had little effect on households with high levels of education. The above results indicate that the current development of mobile payment services in China has generated clear group differences in terms of increasing the risk of household over-indebtedness, with the promotion and popularization of such services having a more profound impact on low-income, low-wealth, and low-education level households in China.

Conclusions

In recent years, China’s mobile payment services have experienced rapid development, which has not only played a positive role in promoting entrepreneurship, stimulating consumption, and reducing financial constraints but also in catalyzing and aggregating various innovative elements, achieving regional inclusive financial and digital economic growth, and promoting the development of social welfare.

In contrast to extensive research on the positive effects of mobile payments, research on the exploration of the negative consequences of this new financial form on individual behavior has been relatively rare. Using detailed micro-survey data from the CHFS in 2017, 2019, and 2021, this study empirically analyzed the impact of mobile payment usage on over-indebtedness risk, the transmission mechanism, and role differences in different groups (in relation to urban-rural divisions, education level, income, and wealth level). This study not only provides new evidence in relation to household debt behavior and potential debt risks but also enriches the research on the micro-household welfare effect arising from mobile payment usage.

The results showed that mobile payments significantly increased the possibility of household over-indebtedness, including both objective and subjective over-indebtedness. The conclusions were found to be reliable and robust when using different measures of household over-indebtedness and IV estimation. The mechanism analysis showed that mobile payments increased household over-indebtedness risk by increasing household consumption expenditure and alleviating household credit constraints, particularly demand-oriented credit constraints. The heterogeneity analysis of sub-samples showed that mobile payments amplified the over-indebtedness risk for both rural and urban households, but that the impact on rural households was greater; the use of mobile payments increased the over-indebtedness risk for low-income and low-wealth households, whereas the marginal impact on high-income and high-wealth households was clearly smaller or even insignificant; and mobile payments only increased the risk of over-indebtedness for low-educated households (heads with a senior high school education level or less) but had little effect for high-educated households (heads with a junior college education level or above). These findings indicate that the current promotion and popularization of mobile payment services in China has had a more profound impact on vulnerable groups: rural households, low-education level households, and low-income and low-wealth level households.

The policy implications of these conclusions are as follows. Continued promotion and development of mobile payments as a new form of financial services are needed, especially to improve the breadth of users’ participation and depth of use and improve the service level in relation to payment, credit, and investment. Efforts are needed to strengthen the positive role of mobile payments in promoting resident consumption, entrepreneurship, improving people’s livelihood, and stimulating the development of the digital economy. However, the emergence of mobile payments has changed people’s consumption habits and borrowing preferences by facilitating payments and encouraging a relaxation of liquidity constraints, which has increased the risk of household over-indebtedness. More importantly, this promotional effect has been unevenly distributed among different groups. For rural, low-education level, low-income, and low-wealth level households, the accumulation of household debt through leveraging is likely to tighten household liquidity, worsen financial vulnerability, and trigger household debt default risk once such households encounter adverse shocks from the external economic environment. Therefore, while encouraging the use of mobile payments and nurturing and promoting the scale of mobile payment services, there needs to be vigilance exercised against the attendant excessive growth of household financial leverage, with strengthened risk supervision, curbs on over-indebtedness behavior, the provision of traceable records for transactions, the use of big data risk control technology for risk rating, and improved supervision mechanisms for credit investigation, credit guidance, and risk warnings.

This study provides valuable new insights for judiciously guiding people’s debt behavior and in risk amelioration. However, this study has some limitations that could be addressed in future research. First, we explored only two mechanisms: household consumption and credit constraints. There may be other ways, especially in terms of subjective factors such as life attitude, social interaction, and future income expectations, through which mobile payments could affect the behavior of household over-indebtedness. Limited by data availability, we could not discern differences in subjective psychological factors among households. Second, this study was only based on data drawn from the context of China. However, its core theoretical conclusions and mechanisms assessment, namely, that mobile payments can stimulate consumption and relax credit constraints, thus promoting household over-indebtedness, have broad application and validity beyond China. Although the breadth and depth of the action pathways may differ in other contexts, the underlying economic principles are the same. Notably, in Western countries where financial infrastructure and consumer credit systems are highly developed, the marginal effect of mobile payments on people’s economic activities may be much smaller than in China. The heterogeneity analysis in this study also suggests that mobile payments have a more significant impact on the behavior of people with smaller resource endowments. Thus, future studies could attempt to establish a generalized model from a broader perspective to supplement and explain in greater depth how and the extent to which the use of mobile payments amplifies the risk of household over-indebtedness.

Footnotes

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This study was supported by National Social Science Foundation of China (23BGL205) and Tianzhong Scholar (Category B) Award Program of Huanghuai University.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.