Abstract

The advancement of technology in the field of telecommunications and increasing use of smartphones worldwide has simplified the purchasing and payment process via mobile devices. This new payment method enables people to enjoy services in a flexible and convenient manner while going about their daily activities. This study explores the continued use of mobile payment antecedents in Sudan. A total of 453 questionnaires were collected; SPSS and AMOS were used to test the proposed theoretical model using structural equation modeling. According to the findings, satisfaction was the most important factor in the intention to use mobile payment. Hedonic motivation and price value were found to have a negative influence on the intention to use mobile payment in Sudan.

Introduction

The rapid advancement of information technology and communication is altering communal lifestyles in several parts of the world. One of the most visible manifestations of this is the way businesses operate. The smartphone payment system enables an electronic value transfer based on a secure ICT infrastructure, an effective regulatory framework, and widespread public and business understanding (Mukhopadhyay & Upadhyay, 2022).

Mobile technology is a major ICT financial instrument in many emerging economies (Francesco, 2018). Smartphones provide fast finance, affordability, and security for millions of people worldwide (Potnis et al., 2020). The first mobile banking application allows unbanked people to manage their accounts. Furthermore, users may access their accounts at any time and location (Alampay et al., 2017; Ochara & Mawela, 2015). Mobile finance can enhance socio-economic development in developing countries (Elzahi Ali, 2022; Roztocki et al., 2019). Previous research has confirmed the relationship between mobile devices and the GDP of developing countries (Qureshi & Najjar, 2017; Samoilenko & Osei-bryson, 2011). A mobile payment platform can also contribute to developing the economies of developing countries (Elzahi Ali, 2022; Kemal, 2019; Rotondi et al., 2020). In many developing countries such as India, Kenya, and Iraq (Ameen & Willis, 2019; Potnis et al., 2020), the government strives to offer government-to-person payment through mobile technology, enabling it to pay salaries, wages, and pensions, which renders the system more transparent. Moreover, it makes collecting taxes more efficient. These advantages could be utilized through developing the mobile finance market in developing countries (Kemal, 2019; Potnis et al., 2020).

M-payments and mobile banking are two popular mobile finance technologies. Mobile banking refers to the use of mobile devices to gain remote access to a person’s bank account (Francesco, 2018; Potnis et al., 2020). As such, it works as an extension bank service, using mobile technology to access users’ bank accounts (Kemal, 2019).

For mobile payment, consumers do not require a bank account (Francesco, 2018). Rather, mobile payment is linked to the mobile phone number. Users may deposit and withdraw funds directly from their accounts using a mobile payment platform, eliminating the requirement for human intervention from the service provider. Mobile payment enables users in remote areas to conveniently perform transactions via short messaging services (SMS; Potnis et al., 2020).

The leading development economist (Sen, 2001) commented that economic facilities are core components of socio-economic development that can be accomplished by improving financial inclusion. Mobile payment systems for vulnerable communities include financial inclusion opportunities (Canh et al., 2020; Donovan, 2012). For example, M-Pesa has transformed the economy of Kenya by allowing the unbanked population to participate in financial transactions using their mobile phones (Pal et al., 2020). Mobile phone transfers have also helped to integrate, in the absence of bank accounts, the simple flows of migrant remittances to home countries such as Uganda, Bangladesh, Afghanistan, and the Philippines (Mirabaud, 2009). Despite effective instances of mobile payments and financial services such as M-Pesa in Kenya and GCash in the Philippines (Elzahi Ali, 2022; Poisson, 2011), global mobile payment adoption, especially in developing regions, has been significantly low (Singh & Bindlish, 2019). The broad adoption and usage of ICTs is considered to provide development opportunities for improving people’s lives in underprivileged places (Qureshi, 2020).

M-payment has witnessed steady growth in some emerging economies in Africa, such as in Kenya, Tanzania, Uganda, and Rwanda, as well as in Asia including in Bangladesh (Evans & Pirchio, 2015; Ezechukwu, 2021). However, Sudan has seen several significant payment system innovations in recent years, including M-Banking in 2009, M-Gorooshi, Hassa, and mobile Cash (Report, 2011; Zain, 2014). Adopting these mobile payment services not only offers consumers convenience and security, but also plays an important role in encouraging economic development, lowering businesses’ cash and check handling, and extending the pool of customers guaranteed to pay. Furthermore, governments are more likely to earn more tax revenue by lowering the volume of unreported transactions in the grey economy (Kemal, 2019; Potnis et al., 2020). The discrepancy between the growing market of m-payment, with low adoption and stickiness among users in Sudan, presents an intriguing question: Which factors influence the use of mobile payment systems in Sudan?

Companies must consider customer practices that cannot be successful without accepting how consumers use emergent technology such as mobile payment to better realize the benefits of IT (Hong et al., 2015; Seethamraju et al., 2018). Although different approaches can be used to motivate users to adopt technologies, the long-term effectiveness of a new information system (IS) further depends on consumers’ continuous behavior rather than on initial decision-making (Venkatesh et al., 2011). Previous post-adoption research in the field of IS, according to (Bhattacherjee, 2001a), focused primarily on one behavior after adoption, namely persistent usage. Prior research indicates that the ongoing intention to use ISs is crucial to companies’ performance in a competitive market because of the benefits of corporate investments (Bhattacherjee, 2001b). User retention is becoming critical for related businesses such as mobile services, and these companies may profit from an awareness of how users create continuous intentions and subsequently, effectively deliver new applications to meet user needs (Albashrawi & Motiwalla, 2019; Kim et al., 2010). Consequently, the authors ask the following research question: How does a mobile payment driver’s pre-acceptance decisions affect the intention to continue using it? Using two current and experimental theoretical models, namely the expectancy confirmation model (ECM; Bhattacherjee, 2001b) and unified extended theory of technology acceptance and use (UTAUT2; Venkatesh et al., 2012), we formulated a research model. On one hand, UTAUT2 showed a powerful and dramatic change in the description of IT behavior pursuance and use decisions. This is critical in the first stage of IT. On the other hand, as it enhances long-term viability, the intention of continuity beyond the initial stage can become the most pressing issue, and the ECM model is best suited for this research. However, research on m-payment, with the majority of available studies confined to the researcher’s region, focused on countries such as the United States and China (Migliore, et al., 2022; Patil et al., 2020). To date, m-payment is not well studied in developing countries like Sudan.

Thus, by incorporating a smooth transition between (UTAUT2) and (ECM) models, we plan to clarify the major drivers of initial acceptance that impact the continuing intention of m-payment. We expect this study to help companies and individuals develop mobile-related information technology to understand the most critical factors that will lead end-users to use it regularly. Specifically, we aim to clarify the expectations and concerns regarding mobile payment usage in Sudan.

First, we combined the UTAUT2 model (Venkatesh et al., 2012) with the ECM (Bhattacherjee, 2001b) to enhance our understanding of the continued usage of mobile payments, which are associated expansion determinants. To our knowledge, the ECM (Bhattacherjee, 2001b) and UTAUT2 model (Venkatesh et al., 2012) are combined in very few studies (Sasongko et al., 2022; Tam & Carlos, 2020) to examine the intention to continue using mobile payment. Second, looking at the ongoing determinants of the intention of individuals to use m-payment, we contribute to another field of scientific experience that has not yet been addressed, namely the continuance intention of using m-payment. This is significant because while most previous studies of ISs focus on initial acceptance, current research aims to explore the direct effects of the continued intention to pay by mobile phone, which is crucial to the long-term sustainability of ISs (Bhattacherjee, 2001b). The third contribution is its replication to the model in Sudan, which is the first attempt (or one of the first) in this area and in Sudan. Finally, validating the model gives other researchers and practitioners a well-ground for future work.

The usefulness of m-payment in people’s daily lives brought the importance of studying its continued usage. For underdeveloped countries, for example, Sudan, the majority of m-payment users are mostly educated people with the ability to afford smartphones. Hence, the need for more experienced users is necessary for the current study.

The rest of the paper is organized as follows: Section 2 status of mobile market in Sudan, Section 3 presents related work. Section 4 theoretical model and research hypotheses. Section 5 provides research methodology. Section 6 provides discussion. Section 7 implications of the study. Section 8 present limitations and future research. Section 9 conclusions.

Status of the Mobile Market in Sudan

Sudan is a large country in Africa, with a population of more than 44.38 million people in January 2021 (Kemp, 2021). Sudan is a culturally diverse Afro-Arab country (Bernal, 1994). It is a lower-middle-income country in which the majority of people (46.5%) live in poverty (Ahmed et al., 2016). However, Sudan is a prosperous country with many different natural resources, wide agricultural land, extensive water resources, and underground resources including gold. Sudan’s unemployment rate increased to 17.7% in 2020. The maximum unemployment rate was 17.7% and minimum rate 13% (Org, 2020). In 2018, the mobile subscription rate per 100 individuals was 72.1 (Data, Business and Economic, 2018) and the smartphone adoption rate was 72.1 (Statista, 2018). As such, the mobile market is witnessing increasing adoption in in the country.

ICTs in Sudan have greatly improved since the 2000s, and access and service penetration rates are aligned with those of its African peers. In the early 2000s, 60% of the population was covered by Global System for Mobile Communications (GSM) signals (Rupa & Cecilia, 2011), which increased to 80% by 2010. Moreover, the mobile subscription rate also increased from less than 1% in 2000 to 33.74 million in 2021, equivalent to 76% of the total population (Kemp, 2021). Sudan has progressed in terms of mobile telephony, and only a few African countries have achieved 20% or more penetration, such as Kenya, Tanzania, and Uganda (Rupa & Cecilia, 2011). Furthermore, Sudan has also witnessed growth and development in the banking industry, starting with ATMs, bank cards, and mobile banking to offer good services to individuals and develop a culture of using mobile payment. The purpose has been to ensure alignment with global advancements in mobile financial services (Tingari & Sanhori, 2016). Recently, the mobile market has penetrated around 75% of the population. In accordance with regional norms, the country has a relatively well-designed telecommunications system including a national backbone of fiber optics and international fiber connections (Henry, 2020). Moreover, Sudan launched a satellite from China in 2019 to support its economic growth and improve military capability and the agricultural sector (Henry, 2020).

Today, businesses cannot flourish without the effective use of available ICT. Mobile finance is an ICT technology that helps people meet their financial needs (Hossain & Sarker, 2015; McBride & Liyala, 2021). It can reduce the operation cost of reaching distant customers, develop the economic situation, and improve services for existing customers (Kabir et al., 2010; Sasongko et al., 2022). Moreover, mobile payment could reduce the need for staff and branches in rural areas, which constitute about 90% of the geographical area in Sudan (Ahmed et al., 2016), and increase bank efficiency. When the customer performs a payment electronically, staff efficiency will increase and they would be able to evaluate the customer’s adoption of mobile payment services. Finally, we consider mobile payment a promising financial inclusion, especially for poor people in countries with no solid financial and banking infrastructure. The gap in the financial service market in Sudan has created a unique niche for mobile payment. To our knowledge, few studies have been conducted in the field of m-payment services in Sudan (Ahmed et al., 2016). Thus, the current research aims to clarify the key initial acceptance factors that impact the ongoing intention to use m-payments.

Related Work

Mobile payment is a technical innovation, which can be defined as “any payment where a mobile device is used to initiate, authorize and confirm an exchange of financial value in return for goods and services” (Au & Kauffman, 2008). Although the term mobile payment refers to all mobile devices such as personal computers and PDAs, mobile devices with mobile phone capabilities are often referred to in general (Albashrawi & Motiwalla, 2019). For the purposes of this analysis, we focus on the initiation, activation, and confirmation of the mechanism as a form of m-payment. There are two major forms of mobile phone payments. The difference between them depends on the consumer (purchaser) situation, retailer (seller) relationship, and various use scenarios. M-payment is also known as a remote or nearby payment, while close-up or point-of-sale payment occurs when the consumer is close to the seller. In this payment system, credentials are stored on a mobile phone and exchanged for short-distance barcode scanning (Hoehle & Venkatesh, 2015; McBride & Liyala, 2021). The customer base for technology is growing, giving consumers more convenience and protection (Dahlberg et al., 2015). Mobile phones built over the last few years are enabled by abilities that make them ideal for this payment method, which can be achieved using existing infrastructure. While remote payments seem more mature than nearby payments (because the former has a larger and more versatile market, and consequently, suffers from time and place constraints), both forms should be combined to boost the future market for m-payment technology. The newest technology can only be used near the point of sale (X. Chen & Li, 2017; McBride & Liyala, 2021).

Previous research has proposed several models to study the distinct nature of m-payment. With this in mind, we seek to explain users’ behavior regarding the mobile payment system and provide examples of the different methods used in the study of mobile payment. Some researchers investigated the determinants of individuals’ behavior toward mobile payment using consumer value theory (L. D. Chen & Nath, 2008; Shankar & Datta, 2018). Kulviwat et al. (2009) dealt with user satisfaction on a mobile app store basis, using discovery facilitators to apply an environmental psychology perspective. Kim et al. (2010) focused on the purpose of mobile payment by applying the UTAUT model. They examined the impact of the acceptance and usage of the brand’s mobile phone distinction on subsequent sales using the difference-in-difference (DDD) model. From a cultural perspective (Hoehle & Venkatesh, 2015), addressed the intent of continuing to use mobile applications for social media. Recently, Kumar et al. (2010), in a study similar to ours, examined the factors affecting customer satisfaction with mobile payment and their persistent intention to use these. Finally, Kumar et al. (2010) and Sleiman et al. (2021)explored the motives for accepting mobile payments.

Customer acceptance and the continued use of new technologies have been the subjects of numerous studies (McBride & Liyala, 2021; Sasongko et al., 2022; Sleiman et al., 2021). Many scientists have employed classical theories to describe individual decisions to adopt technology, such as the technology acceptance model (TAM), theory of reasoned action (TRA), unified theory of acceptance and use of technology (UTAUT), ECM, and social cognitive theories (SCT; Liébana-Cabanillas et al., 2014; Sasongko et al., 2022). Much research has been undertaken to explain consumers’ technology adoption behaviors using these models, each of which has significantly contributed to the literature on technology acceptance and adoption. Because behavioral intents are motivating elements that reflect how much individuals are motivated to undertake a behavior, most of these theories focus on behavioral intention and usage as essential predictor variables in understanding technology acceptance (Ajzen, 1991). As a result, it is widely considered the most influential paradigm in describing information technology adoption behavior (Rao & Troshani, 2007).

Most technological models have certain limitations. Despite that TAM is a well-known paradigm in the field of technology acceptance and adoption, it has limitations including the “exclusion of the possibility of influence from institutional, social, and personnel control factors" (Morris & Dillon, 1996). Following this finding, many modifications have been made to the original TAM. The most remarkable of these models is the UTAUT, which was formulated based on conceptual and empirical similarities across eight models (Migliore et al., 2022; Sasongko et al., 2022). The UTAUT model clarifies how intention and behavior factors evolve over time. It identifies three factors directly affecting the intention to use—performance expectancy, effort expectancy, and social influence—and factors of usage behavior, namely intention and facilitating conditions. Nevertheless, both theories have faced criticism (Migliore et al., 2022; Rao & Troshani, 2007).

We conclude that there are many common trends and approaches in the field of mobile payments based on different models. However, to our knowledge, there is relatively little research on the function of continuity in mobile payments combining the ECM and UTAUT2 model (Sasongko et al., 2022; Tam et al., 2020). Here, these two well-established theories are integrated into a single theoretical model, which we expect will contribute to the IS literature. The models employed in this investigation are described in the sections below.

Expectation Confirmation Model

The expectation confirmation model (ECM) evolved as an adaptation of the ECT. The ECT suggests that preferences lead to post-purchase satisfaction along with perceived expectations. This impact can be evaluated by a negative or positive difference between results and expectations (Oliver, 1980). An expectation confirmation model (ECM) for IS continuation was proposed by Bhattacherjee (2001b), who concluded that IS users’ continuation decisions are identical to consumers’ repurchase decisions, because both are impacted by the early experience of using ISs or products. Furthermore, these decisions are closely linked to customer satisfaction (Bhattacherjee, 2001b). The model consists of three factors designed to forecast and clarify the continued intention of people to use IT: satisfaction, confirmation of expectations, and perceived usefulness. In the ECM, confirmation and perceived usefulness are the two major factors to assess IS continuity intentions, and are determined by users’ initial preferences. They also affect customer satisfaction. Satisfaction and perceived usefulness predict a person’s decision to continue using ISs.

Regarding IT products and services, numerous studies have employed various theories to explore post-acceptance concepts and examine individual behaviors. To explore the continued use of IS, studies have been conducted on topics similar to our mobile payment research. The most recent (Albashrawi & Motiwalla, 2019; Ezechukwu, 2021; Hsu & Lin, 2015; Kumar et al., 2010; Ly et al., 2022; Migliore et al., 2022; Sasongko et al., 2022) incorporated the ECM into their frameworks. The same approach is employed in this study to achieve one of its main objectives, namely to determine individual actions after using mobile payment.

The current research extends the ECM to explain the post-accession phenomenon of mobile payment. We believe that the decision after the initial stage of acceptance has a significant effect on the mobile payment continuity strategy, which affects the long-term profitability of the consumer.

Extended Unified Theory of Acceptance and Use of Technology (UTAUT2)

Venkatesh et al. (2003) created UTAUT to clarify users’ intention to use an IS and the subsequent use of technology in organizational contexts. The model synthesizes eight theoretical models based on sociological and psychological theories to explain this behavior (Venkatesh et al., 2003). UTAUT employs four key frameworks to explain behavioral intent to use technology and use behaviors: expected efficiency, social impact, expected effort, and encouraging conditions. These structures are tailored to the behavioral purpose of using technology. The use of technology defines the behavioral purpose and conditions that promote it. To explain individual differences, gender, age, volunteerism, and experience are considered moderators of the four dimensions of the UTAUT model.

Subsequently, UTAUT2 was developed (Venkatesh et al., 2012), which extended and adapted the theory to the market context. The original UTAUT model was replaced with three new constructions (hedonic motivation, price value, and habit). The study found that the extension of UTAUT relative to the original model resulted in a major increase in the explained variance in behavioral intention and behavioral patterns.

Research using the UTAUT model provides no evidence of reaching saturation. As such, UTAUT is considered one of the most prominent theories in IS adoption. Furthermore, it provides insight into mobile payment research by integrating a seamless transition between UTAUT2 and ECM, namely between the beginning process of adoption and the continuation plan.

Our major model is based on Bhattacherjee (2001b), which shows that the ECM extension model better contributes to the use of IT by addressing the weaknesses of the novel model. Several studies were based on extensions of the ECM, as evident in the current literature. However, to our knowledge, no previous research has been conducted using the ECM along with UTAUT2 in Sudan. The constructs from UTAUT2 were assigned to a relatively new model that focuses on behavioral intention and actual usage, which we propose can provide a greater descriptive influence on the critical constructs of our main model: performance expectations and intention to continue mobile payment use. With this in mind and following Bhattacherjee (2001b) and Venkatesh et al. (2012), we extend these models to various technologies and other related factors. For these purposes, to better understand the intention to continue m-payment use, we propose integrating the ECM with UTAUT2.

Theoretical Model and Research Hypotheses

The expectation confirmation model (ECM) is the foundation of the whole process, as it measures the level of people’s satisfaction and expectation. Some additions to this model are discussed in more detail to better conceptualize the concept of intention to continue to use mobile payment. Thus, we suggest integrating the seven UTAUT2 combinations, which are essential direct factors of intent to use, to identify meaningful changes in variance reflected in behavioral intention and use of IT (Venkatesh et al., 2012). We propose a model for the study that extends and integrates the ECM with UTAUT2. To investigate the continuity intention of end users using electronic payment, a theoretical model is presented in Figure 1. Furthermore, the respective hypotheses are discussed later in this section.

Research model.

Expectancy confirmation is defined as the anticipated advantages obtained by users’ familiarity with IT (Dabholkar et al., 2003; Loh et al., 2022). According to the ECM, users’ confirmation of expectations significantly impact perceived usefulness, also referred to as information technology success expectation. This is also significantly linked to satisfaction with the use of ISs, because it implies understanding the anticipated benefits of using these systems (Bhattacherjee, 2001b). In addition, confirming IT users’ expectations means that users receive the anticipated benefits from their use of IT, which positively impacts user satisfaction and performance expectations therewith. Adapted to m-payment, all its advantages can be easily understood by a customer who confirms the previous prediction. Thus, a customer’s happiness with mobile payment depends on the assurance that its usage is closer to the real experience. Hence, we presume the following:

Perceived usefulness is defined as “the degree to which a person believes that the use of a particular system enhances their job performance” (Davis, 2013). According to UTAUT, performance expectation is “the degree to which the use of technology will provide a benefit to customers in accomplishing certain activities” (Venkatesh et al., 2012). Bhattacherjee (2001b) calculated user satisfaction by confirming expectations from past usage and anticipating performance. If a mobile payment user considers using mobile payment as useful, adapting to our research, he/she may be more satisfied with it. On the other hand, performance expectation in terms of utility has been confirmed as a robust indicator of behavioral intention (Sasongko et al., 2022; Venkatesh et al., 2003). Our study assumed that users would continue to use m-payment if they believed it would have a good outcome. Therefore, we presume the following:

Satisfaction is the post-ban assessment of customers’ initial encounter with services, and measured as a significant sense of satisfaction, indifference, or negative dissatisfaction (Bhattacherjee, 2001a; Sasongko et al., 2022). The ECM supports the assumption that the key reason for its continuation is product or service satisfaction (Oliver, 1980). Bhattacherjee (2001b) showed that the forward relationship between satisfaction and consistency of purpose is at the heart of the IS continuance model, which has been experimentally validated. (Bhattacherjee, 2001b; Kumar et al., 2010; Maria & Sha, 2018; Sasongko et al., 2022) argued that usage intentions were better for consumers with higher satisfaction levels. The purpose of repurchasing a product depends on whether customers are happy with it or not (Hsu et al., 2007; Qu et al., 2018). If satisfied, the customer will decide to continue the business relationship (Anderson et al., 1994). The findings of a study by X. Chen and Li (2017) indicate that customer satisfaction with m-payment services significantly influences the intent to continue. Adapted to our study, customers seem to continue to use it if mobile payment consumers are pleased with them. Thus, we believe the following:

Perceived ease of use (PEOU) is characterized as the degree to which a person thinks m-payment will be easy to use (Davis, 1989). The degree to which innovation is not considered difficult to understand, learn, or operate (San Martín et al., 2012; Sasongko et al., 2022) is the PEOU. PEOU represents the expected effort. According to Davis (1989), when consumers think that m-payment is beneficial, they may also consider it difficult to use and that the benefits of its use are offset by efforts to use it. Previous studies showed that the more complicated technology is, the lower is the rate of intention to reuse it, particularly among users (Meuter et al., 2005; Venkatesh & Davis, 2000). In contrast, (Venkatesh et al., 2003) indicated that in addition to its indirect effect, anticipated effort positively affects the intention to continue. The less effort involved in m-payment usage, the greater the user’s preference for continuing its use. Hence, we presume the following:

Social influence is the extent to which a consumer considers important how others think a technology should be used (Chiu & Wang, 2008; Sleiman et al., 2021). In other words, it represents the degree to which the attitudes, values, and actions of a person are impacted by others (Lin & Wang, 2006). Social influence is a concept adapted from the theory of planned behavior, which implies that an individual is more likely to follow a certain system if the people around him demonstrate a positive attitude (Okocha & Adibi, 2020). Social impact has been shown to directly influence behavioral intent (Hong et al., 2008; Ly et al., 2022; Venkatesh & Morris, 2000). Previous studies (Ding et al., 2011; Zhou, 2014) suggested that social influence affects craving and impacts continued use. In this study, the higher the social impact of m-payments, the greater the continuity of usage by users. Hence, we presume the following:

The term facilitating conditions is described as “consumer expectations of the resources and support available to conduct a behavior” (Venkatesh et al., 2012). Facilitating conditions are infrastructures that promote the use of technology (Venkatesh & Morris, 2000), which leads to the adoption thereof. In addition, the facilitation of requirements simplifies the implementation of technology for sustainable implementation and use. According to Nysveen et al. (2005), a consumer with access to a favorable set of concessional conditions will likely have a greater intent to use the technology. Facilitating situations are constructions that reflect the expectations of an individual’s influence over actions (Migliore et al., 2022; Venkatesh et al., 2008). The more applicable the usability requirements associated with the use of mobile payments are to mobile payment users, the longer the user will tend to use it. Hence, we presume the following:

Hedonic motivation is the enjoyment of using technology and plays a significant role in encouraging its acceptance and use (Hong et al., 2017; Migliore et al., 2022). Utilitarian-motivated individuals focus on instrumental meaning, while hedonistic individuals are more concerned with satisfaction, fun, and enjoyment (Hsiao et al., 2016; Ly et al., 2022). Hedonic motivation is a crucial determinant of behavioral intent and has been shown to be a more significant driver in non-organizational contexts than success expectation achievement (Venkatesh et al., 2012). Davis et al. (1992) found that the key determinant of behavioral intention to use a personal computer is perceived pleasure, and that it is analogous to hedonic motivation. Mobile payment users are more interested in optional features such as events and mobile payment promotions than mobile payments alone. In addition, users’ attitudes about adoption will be favorable if they can enjoy one service. When two identical services are available, people frequently select the one that is more enjoyable (Mackey & Ho, 2008; Migliore et al., 2022; Qu et al., 2018). For our purposes, we assume that the increased entertainment provided to users by mobile payment leads to their continued use and enjoyment thereof. Hence, we presume the following:

Price is the financial expenditure needed to purchase and use a commodity (Ly et al., 2022; Xu et al., 2015). On the other hand, value is an abstract term with meanings that differ according to context (Chiu et al., 2005). According to Porter (1980), if a free alternative offer is open, consumers will usually choose that over the paid edition. Venkatesh et al. (2012) suggested that the cost and price system could have a major effect on consumers’ use of technology. Not only do users have several mobile payment options with similar features in the mobile payment industry, but most are free, reducing the drive of the user to purchase a mobile payment system with similar features, despite that the paid version may provide better quality (Hsu & Lin, 2015; Migliore et al., 2022). Thus, we recommend that the value of the price be related to the continuance intention, as the costs related to mobile payment can directly affect consumers’ use of technology. Therefore, we assume the following:

Habit is the degree to which individuals appear to practice behaviors (use IS) automatically (Limayem et al., 2007). Users with previous experience using ISs typically develop behaviors that strengthen the persistence of the same behavioral type (Amoroso & Lim, 2017; Gefen et al., 2003). Construction patterns rather than initial adoption have been shown to be a crucial factor in predicting the use of technology (Limayem et al., 2007; Suo et al., 2022). According to Collier & Barnes, (2015), the continuance intention can be predicted by the degree to which the action due to prior learning habits has become automatic. In our case, patterns of mobile payment use would promote intention to continue to use the same mobile payment, as individuals appear to perform automatic behaviors. Hence, we presume the following:

Research Methodology

Data Collection

Our research examines the behavior of people in relation to m-payments. An online questionnaire was created to collect the data on Facebook from Sudanese groups, because it appears to be the easiest and most productive way to gather opinions on this issue, with the exception of those without an Internet connection the survey took more than on month. The sample of this study has been selected by using the equation of Krejcie and Morgan (1970), S = X2 NP (1 − P) ÷ d2 (N − 1) + X2 P (1 − P; Zulkipli & Ali, 2018). A survey was conducted to address the hypotheses of the proposed conceptual framework. Data were collected from the users of leading mobile payment platforms in Sudan, namely M-Gorooshi, Hassa, and mobile Cash (Report, 2011; Zain, 2014). In total, 487 surveys were collected online in Sudan, of which 453 were complete and determined to be sufficient to produce accurate results for the entire study population (Table 1). The sample size was considered large enough for the entire research population to yield reliable results. The participants in the study were aged 18 to 45 years.

The Demographic Data.

Instruments

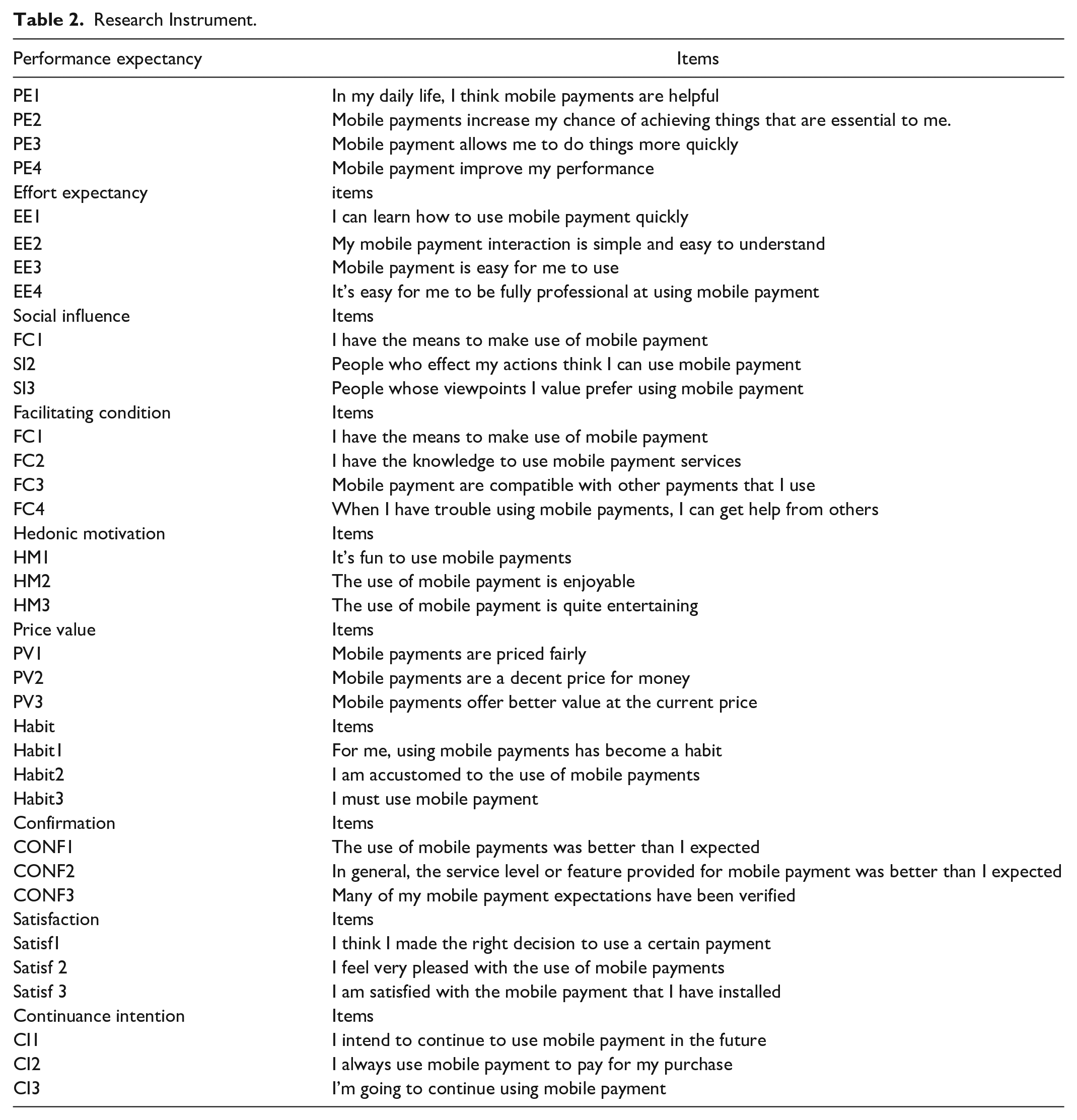

The instrument used in this study was adopted from (Bhattacherjee, 2001b; Venkatesh et al., 2012; Vila & Kuster, 2011). All constructs were measured with three to four items via a 5-point Likert scale. The questionnaire was written in Arabic and English. The elements of the study were modified to fit the current research context of mobile payment in Sudan, which took approximately three months. For validity, a construct pilot measurement was used. For this 50 users who had experience using mobile payment platforms were invited to complete the initial questionnaire. Based on the feedback, we adjusted some items to fit the current study. The questionnaire employed is shown in Table 2.

Research Instrument.

Research Results

Exploratory and Confirmatory Factor Analysis

To validate the evaluation, a validity analysis was needed. Construct validity is used to assess questionnaires where the degree of theoretical assumptions can be calculated by the scales (Santoso et al., 2014). Convergent and discriminant validity can also be assessed. To measure the collected data, we used a Bartlett’s sphericity test and the KMO measure of sampling adequacy. Table 3, shows the suitability of indicated by a factor analysis, the result of which is χ2 = 2,065.257 (ρ = .000). A value above 0.7 would be appropriate based on Kaiser’s widely used KMO measure, and is better the closer it is to 1. The KMO measure = 0.655, which means there is valid convergent validity for the collected data. ρ = .000 means that the data are appropriate for differentiation (Williams et al., 2010).

KMO and Bartlett’s Test.

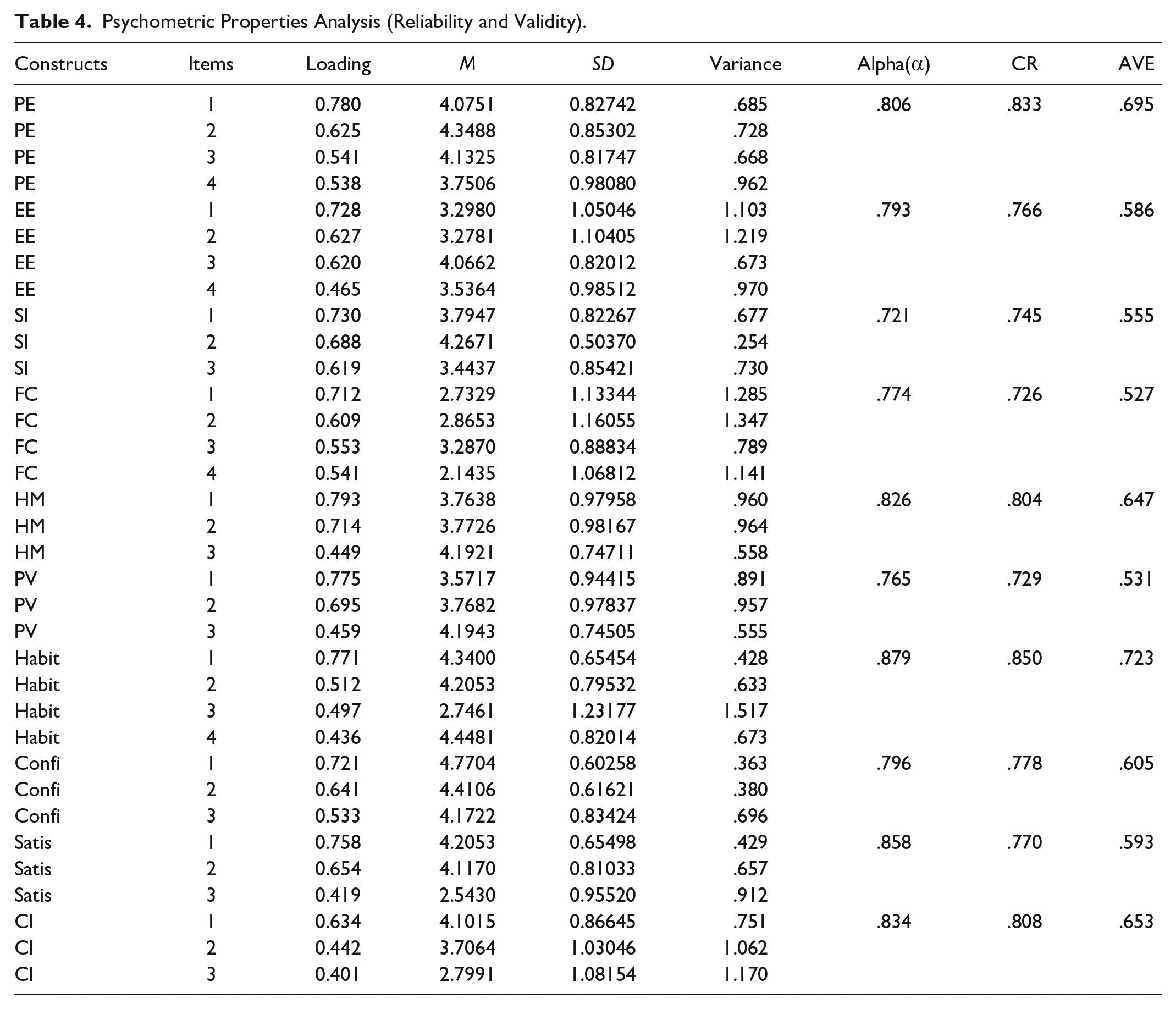

Structural equation modeling (SEM) was employed to test the suggested theoretical model. In addition, the partial least squares (PLS; Chin et al., 2003) method was chosen because it is known as an effective statistical analysis method for measuring and analyzing psychometric properties (reliability and validity; Chin et al., 2003). The assessment requires tests for construct reliability and validity. In this study, the alpha coefficient (H. Chen et al., 2017) was used for the internal consistency of the collected data, the results of which are shown in Table 3. The entire alpha is greater than .700, meaning that the collected data meet the requirements (H. Chen et al., 2017). We also tested the CR, which was found to be higher than the .70 threshold as shown in Table 3, thereby supporting the model’s good reliability and internal consistency (Featherman et al., 2016). The item loading of each construct was calculated to ensure convergent validity through an AVE (H. Chen et al., 2017). The results showed that all item loadings were above 0.40, and the AVEs were above .50, as shown in Table 4. Table 5 provides the results of the discriminant validity analysis. The final questionnaire of this study contained 33 items after excluding 1 item based on the confirmatory factor analysis and final factor models.

Psychometric Properties Analysis (Reliability and Validity).

Discriminant Validity Analysis.

p < .05. **p < .01.

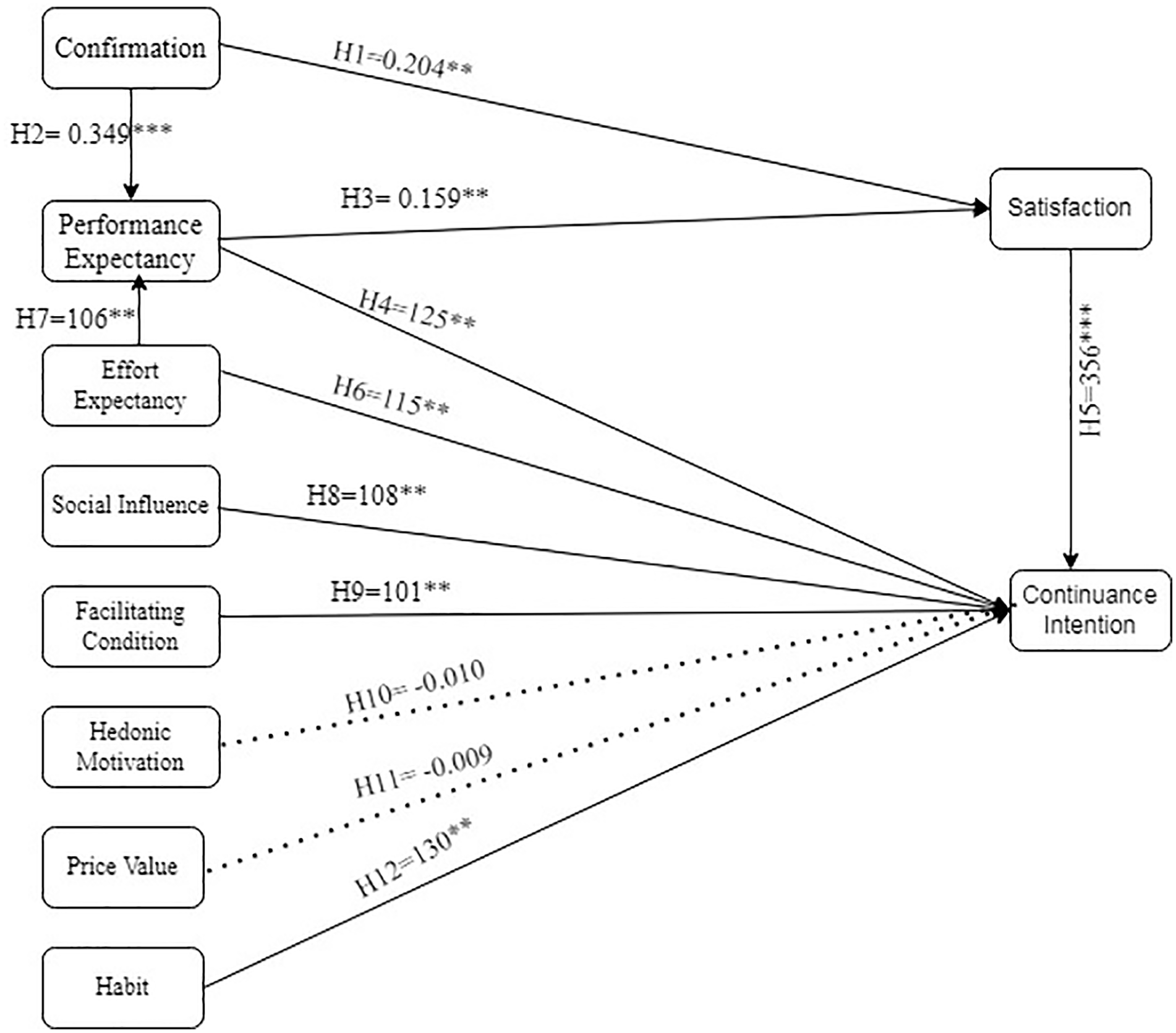

Based on the examination of structured routes, we analyzed the relationships between the hypotheses and constructs. Table 6 and Figure 2 display the path coefficients and R2 of our proposed model. Eight of the 12 hypotheses of the integrated model were accepted as follows. The proposed model demonstrated a good fit, and most relationships were confirmed.

The Hypothesis Finding.

p < .01. ***p < .001.

Research model results.

Research Finding

In addition, a confirmatory factor analysis was conducted to determine if the model fit index was good. Table 7 provides the findings. Many indexes such as the goodness-of-fit index are used in SEM to evaluate the overall model. The most important fit index is χ2, which serves as the foundation for other indexes and could be used to evaluate null hypotheses. We analyzed the fitness of the model in this study using the indexes in Table 7, which shows that it satisfies the criteria (Staphorst et al., 2014).

Model Fit Indices.

Note. χ2 = chi-square; DF = degree of freedom; CFI = comparative fit index; GFI = general fit index; AGFI = adjusted goodness of fit index; TLI = Tucker–Lewis Fit Index; CFI = Comparative Fit Index; RMSEA = Root-Mean Square Error of Approximation.

Discussion

According to the results of the path analysis, with the exception of hedonic motivation and pricing values, the majority of the variables in the study model—namely expectancy confirmation, performance expectancy, satisfaction, effort expectancy, social influence, facilitating condition, and habit—have emerged as statistically significant factors in the intention to continue using mobile payment in Sudan.

Confirmation expectations influence user satisfaction and performance expectations positively. This implies that consumers get the expected advantages from using mobile payment. Moreover, performance expectancy directly and indirectly influences the intention to continue using mobile payment in Sudan. This result indicates that more complex technology has less intention to continue using it in the future. Furthermore, effort expectancy directly and indirectly influences users’ continued intention to use mobile payments in Sudan. This indicates that the easier it is to use mobile payments, the more likely it is that people will keep using them (Sasongko et al., 2022; Tam et al., 2020).

The importance and validity of the satisfaction construct as a major factor stayed the same as in previous research (Jaiswal et al., 2022; Tam et al., 2020), in which the variable affected the intention to continue both indirectly and directly. The satisfaction factor had the greatest impact on the intention to continue to use mobile payment in the future, followed by the expectancy confirmation factor on performance expectancy, these finding consent with (Nguyen & Ha, 2022; Sasongko et al., 2022). According to a study by Tam, the benefits provided by mobile services are critical to consumer satisfaction (Tam et al., 2020). Furthermore, satisfaction is a strong determinant of future intention, a finding similar to that of (Nguyen & Ha, 2022). Moreover, users’ continuous intention to use m-payment is significantly influenced by their performance expectancy and satisfaction. This indicates that Sudanese users place a high value on the relative advantage of the technology. They believe m-payment will help them enhance their performance and make transactions more satisfactory.

Similarly, social influence has been shown to be a significant factor in users’ intention to continue using mobile payment, this result demonstrates the importance of social influence on the intention to continue using mobile payment in the future. This might imply that the opinions and recommendations of people who are important and significant may in reality drive the adoption of mobile payment platforms, which is consistent with earlier research that found users are greatly impacted by the opinions in their social context (Seethamraju et al., 2017; Shao et al., 2018). The acceptability of mobile payment by customers is significantly influenced by social influence. According to research, users’ motivation to continue using mobile payment is impacted by the attitudes of other people in their immediate environment. If others whose opinions are important to us believe that utilizing mobile payment is a good idea, we are more likely to pursue mobile payment in the future. This finding is aligned with that of other studies (Qasim & Abu-shanab, 2016; Tam et al., 2020). Furthermore, perceived habit has been found to significantly influence the continuance intention to use m-payment. Users with previous experience using ISs typically develop behaviors that strengthen the persistence of the same behavioral type (Merhi et al., 2019).

However, some additional dimensions were not shown to be significant predictors of continuance intention. According to the results of our study, our respondents are implementing mobile payments in their everyday lives, as indicated by their responses. As a result, when the optimum conditions for using mobile payment services are present, customers place less emphasis on their hedonic motivations or price values. Furthermore, it was shown that hedonic motivation did not have a statistically significant association with continuance intention, indicating that consumers may not care about entertainment as much as they thought. Thus, it may not be a suitable construct for gauging customers’ continued usage of mobile payment for utilitarian reasons, such as accomplishing a specific activity more successfully or efficiently (Migliore et al., 2022). Furthermore, we discovered that the price value was not significant in our suggested model, which may be because the late adopters are usually low price sensitive and the majority of applications available on the market are either free or inexpensive. According to the findings of the study, the proposed model has brought additional value to the investigation of the intention to continue using mobile payment.

Theoretical Implications

The assumed model of the study is suitable for the current research, and most of the construct relationships have been confirmed. The model explores the strong relationship between performance expectancy and continuance intention. Satisfaction has been found to have the strongest relationship with continuance intention (X. Chen & Li, 2017). The UTAUT2 model, which includes performance expectancy, effort expectancy, social influence, facilitating conditions, and habit, added more value to the proposed model and demonstrated a greater impact on continuance intention than the ECM. Furthermore, other constructs of UTAUT2 (hedonic motivation and price value) were found to have a negative impact on continuance intention. The findings of the current study reveal that mobile payment users in Sudan are not influenced by hedonic motivation and price value, which is aligned with other research (Chopdar et al., 2018; Marinković et al., 2020; Tam et al., 2020).

The current study has made many contributions. First, it integrated the ECM with UTAUT2 to identify the factors of satisfaction and continuance intention in Sudan. The study showed that the factors of the proposed model could explain the continuance intention of using mobile payment in Sudan. Second, to our knowledge, no previous studies investigated mobile payment continuance usage from the perspective of users in Sudan. Moreover, the study revealed that confirmation, satisfaction, performance expectancy, effort expectancy, social influence, facilitating conditions, and habit should be considered when investigating the continuance intention of mobile payment use.

Practical Implications

The positive findings of the current study provide insight for managers in terms of explaining continuance intention. These findings include guidelines for companies and mobile payment developers to support users’ intention to continue use. Service providers should consider performance expectancy and satisfaction because they are the main constructs of the ECM and determine continuance intention. Service providers should explore the benefits associated with mobile payment, positively impact customer satisfaction and their continuance intention. Social influence and facilitating conditions significantly affect continuance intention; thus, service providers should enhance facilitating conditions and social influence to meet users’ expectations. Hedonic motivation was found to be negatively associated with continuance intention to use mobile payment, which unexpectedly suggests that users are not interested in the amusement of using mobile payment. Service providers should find a suitable way to maintain user loyalty when using m-payment services. Price is negatively related to the continuance intention to use mobile payment. Service suppliers should realize that customers tend to use free applications (Hsu & Lin, 2015). As such, paid mobile payment applications may negatively affect their adoption thereof. Finally, the study investigated many significant antecedents that enhance our perception of the continuance intention of m-payment usage in Sudan.

We conclude by investigating the criteria for managing and establishing a mobile payment platform. Service providers should recognize the importance of mobile payment characteristics and develop m-payments based on user needs and wants, as well as take advantage of performance expectancy, effort expectancy, price, amusement, and satisfaction to develop more appropriate m-payments that are flexible and manageable to suit Sudanese users. Furthermore, service providers should provide effective facilitation conditions that allow users to continue utilizing m-payment. Finally, operators should improve public perception and generate good word of mouth (WOM) among users.

Limitations and Future Research

Similar to previous studies, this research has several limitations that offer opportunities for further work. We used an online questionnaire and did not gather data from people without Internet access. This may render certain pathways irrelevant. Therefore, including a method to collect offline data will ensure a good mix of respondents from various strata for research that includes an assessment of Internet access. Paper questionnaires could be distributed to those without technological knowledge, as obstacles to IT usage such as mobile payments will be more evident to these respondents. Thus, academics may seek to broaden their study on multi-nationalities by increasing the geographical scope of future research to enable better generalization. Furthermore, we highly recommend collecting data offline on technology access or knowledge, especially in low-income countries, as the majority of the population will be excluded if the survey is conducted online, furthermore, the future research could consider users experience associated with mobile payment. Moreover, the respondents in this study have received some level of education. The majority are young people with experience in using a smartphone. Future studies could test our proposed model in other countries with different users also the model could be apply in e-commerce instead of m-payment to see whether the same findings are produced. Future research could also consider users’ culture and income as moderators in the theoretical model to explore different behaviors and focus on the factors of continuous intention in the m-payment context in Sudan. Moreover, future research could examine the effects of other factors on continuance intention, such as accessibility, reputation, and trust in other countries. This study can extend our knowledge about customers’ continuance intention of using m-payment and it can be useful for the different users group.

Conclusions

The use of mobile payment is widespread and continuance use intention in Sudan may enable e-commerce, which will attract female customers. This is important as the market in Sudan is dominated by males based on Sudanese Arab culture restrictions. Moreover, the adoption of m-payment allows unbanked people to join in financial transactions, which will help economic development. This research studied Sudan’s potential in the continuance intention to use m-payment, a topic not widely discussed in the literature. Continuance intention has not been widely investigated for different types of IT. We integrated the ECM and UTUAT2 to better understand continuance intention. The findings of this study show that continuance intention is directly influenced by satisfaction.

Footnotes

Author Contribution

All the authors contributed equally to the development of this article.

Data Availability Statement

The data of the current study were created by the authors.

Disclaimer

The opinions expressed in this paper are those of the authors.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was supported by the Shaanxi Provincial Philosophy and Social Science Foundation Project in 2021: Research on “Embedded Climbing” of Agricultural Industrial Cluster in the context of Rural Revitalization Strategy (No. 2021D033). This work was partially supported by research on the governance mechanism of cooperatives Embedded and Village Organizations in Northwest China” (No. 16XJC630008). This work was partially supported by the Natural Science Foundation of China (No. 61977002). This work was also supported by Social Science Publicity and Popularization Funding Project in 2022 of Shaanxi Federation of Social Sciences: Rural e-commerce marketing and popular science activities (No. 2022KP073).