Abstract

Although digital transformation generates operational efficiencies for firms, it simultaneously introduces novel complexities into the audit process. Using a longitudinal panel of China’s A-share listed firms from 2007 to 2020, we examine how digital transformation affects the risk premium of audit fee via multivariate regressions that control for industry, year, and firm fixed effects. Endogeneity problem are addressed using two-stage least squares (2SLS) estimation, propensity score matching (PSM), and lagged independent-variable specifications to mitigate reverse causality. We find that digital transformation is positively associated indicating that auditors price technological disruption into fee structures. Path analysis reveals that auditor effort fully mediates this relationship, establishing it as the key transmission mechanism. This effect is amplified among non-state-owned enterprises, in non-high-tech industries, and with non-Big four auditors. The findings withstand endogeneity concerns, as demonstrated by instrumental-variable and quasi-experimental robustness tests. This study contributes to the audit pricing literature by (1) establishing digital transformation as an emerging determinant of risk premium, (2) providing empirical evidence for the previously understudied auditor effort mechanism, and (3) identifying the institutional factors that condition technology-audit interactions. The findings call for a re-evaluation of audit pricing in the digital economy era.

Introduction

Digital transformation is the process by which enterprises use digital technologies to transform their operating models and the ways they create value for customers (Chen et al., 2024). Although this transformation enhances operational efficiency, it injects fundamental uncertainties into audit practice—particularly when pricing intangible risks that elude conventional measurement (Stuart-Delavaine & Willis, 2025). Auditors therefore confront a paradox: technological adoption simultaneously lowers observable transaction costs yet heightens latent risks arising from algorithmic opacity (Li & Li, 2025). For instance, although algorithmic-trading simulation frameworks furnish traders with an environment for developing automated decision-making systems, the opacity of trading algorithms precludes regulators from detecting strategy convergence in real time (Banciu et al., 2024; Borch, 2022). Proactive governance of algorithmic risk can preclude audit failures and litigation costs that would otherwise arise from algorithmic errors; however, Manita et al. (2020) do not address real-time algorithmic risk. Resolving this tension requires an understanding of how audit markets price digital disruption-a question that remains open in contemporary literature.

Simunic (1980) still anchors audit-pricing work, but the literature has since fanned out along distinct paths. Morgan and Stocken (1998) shifts the lens from client size to forward-looking business risk, but the study does not address the impact of digital transformation. Later studies add audit-committee quality (Almaqoushi & Powell,2021), industry specialization (Ding et al., 2022), partner rotation gaps (Florio, 2024), regulatory shocks (Hodula, 2025), and climate events (Fortuna et al., 2024) as separate audit-fee drivers. Yet all of these variables treat risk as something measurable after the fact. Historical financials anchor the estimates, while the technology layer inside the firm evolves in real time. When algorithmic processes reset their own parameters daily, the misstatement probabilities become neither observable nor stable. Auditors may overstate or understate risks in digitally intensive clients, leaving them without a clear way to price technology uncertainty.

Corporate digital transformation complicates audit pricing through two understudied channels: (1) asset intangibility and (2) process opacity. Data assets elevate risk for auditors due to the limitations of traditional valuation methods (Tejedo-Romero & Araujo, 2025), while increased process opacity necessitates more extensive verification procedures, thereby increasing audit costs and reducing profit margins (Shin & Jitkajornwanich, 2024).These dual forces generate information asymmetry between auditors and clients, thereby challenging the calibration of risk premium central to audit pricing models. Consequently, two research gaps emerge: (1) Does digital transformation systematically influence the risk premium of audit fee? (2) Does auditor effort mediate the relationship between digital transformation and the risk premium of audit fee?

We explore these questions using China’s A-share listed firms (2007–2020). Our analyses reveal that digital transformation intensity significantly increases the risk premium of audit fee, with auditor effort mediating the relationship. Cross-sectional evidence demonstrates that the effects are stronger among non-state-owned enterprises and non-Big four clients, which highlights the institutional constraints in technological risk assimilation. This study advances audit research along three dimensions: first, it establishes digital transformation as a dynamic determinant of audit pricing, thereby complementing analyses grounded in traditional client-auditor dyads (Deng et al., 2024). Second, by employing path analysis, it disentangles the mediating role of auditor effort, thereby redressing the methodological limitations identified in prior studies (Jaffar et al., 2023). Third, it identifies three boundary conditions for the risk premium of audit fee: the nature of ownership, the intensity of auditors’ effort, and key enterprise attributes.

The remainder of this paper is organized as follows. Section “Literature Review and Hypotheses Development” reviews the literature and develops the research hypotheses. Section “Methodology” delineates the sample selection, variable measurement, and model specification. Section “Results” presents the empirical results, robustness tests, and an analysis of the moderating role of auditor effort. Section “Further Analyses” reports additional analyses, and section “Discussion” discusses the findings. Section “Conclusion and Recommendation” presents the conclusions, practical implications, and limitations, while outlining directions for future research.

Literature Review and Hypotheses Development

Digital Transformation

The digital transformation of enterprises is a complex project that integrates policy utilization (Zhou, 2024), technological innovation (da Silva Nascimento et al., 2025), organizational change (Knudsen & Kishik, 2024), information integration (Babaei et al., 2025) and value creation (Aranyossy & Halmosi, 2024). It will drive companies to make substantial investments in data collection, algorithm development, hardware procurement, and the acquisition of new technologies in order to construct entirely new business logics and models, thereby creating new products and services (Rong & Hu, 2025). Digital transformation is not only a technology-driven problem of enterprises, but also a profound organizational change, the core of which is to reveal how digital technology interacts with internal and external elements of the enterprise (Xiao et al., 2025), thereby bringing about a fundamental change in the competitive advantage of the enterprise. The digital transformation of enterprises is a process of continuous evolution, highly dependent on contextual factors such as industry characteristics, market competition, enterprise scale, organizational strategy, and resource endowment.

Audit Fee

Audit fees are the remuneration paid by the client enterprise for the purchase of audit services of accounting firms, and its pricing is affected by three factors: the scale of the client’s business (Mao et al., 2024), the bargaining power of the accounting firm (Donelson et al., 2019), and the audit risk (Bowen et al., 2025). First of all, the scale and complexity of the client’s business are the pricing basis of audit fees (Taylor, 2025), which directly determine the investment of audit resources of accounting firms. Secondly, the market position and technical capabilities of accounting firms determine the pricing power of audit fees. Finally, the higher the audit risk, the higher the risk premium required by the accounting firm to cover potential litigation losses and reputational costs (Kim et al., 2025).

Digital Transformation and the Risk Premium of Audit Fee

The inherent specialization and rapid iteration of digital technologies heighten investors’ cognitive barriers, thereby widening information asymmetry and fostering insiders’ opportunistic behavior (Jensen & Meckling, 1976), which in turn indirectly elevates audit risk. In its traditional sense, audit risk comprises inherent risk, control risk, and detection risk (Yang, Jiao, & Liao, 2025).

During firms’ digital transformation, inherent risk is reshaped: while certain human errors are mitigated, new technological hazards—such as data-security breaches and algorithmic bias—emerge (Ruiz-Barbadillo et al., 2024). Regarding control risk, automated controls enhance efficiency, yet system-permission loopholes, algorithmic black boxes, and heightened reliance on third-party platforms redefine the pathways through which controls can fail (Yang, Hui, et al., 2025). As for detection risk, advances in audit techniques reduce sampling limitations, but skill gaps in validating electronic evidence and auditing complex models dynamically push detection risk upward (Wang, 2025).

The audit risk premium is the additional fee charged by auditors—over and above normal audit fees—to compensate for potential audit failures, litigation, or reputational losses when audit risk is elevated (Ranasinghe et al., 2023). When a firm’s audit risk or internal-control deficiencies are high, the probability of audit failure rises, prompting auditors to demand higher remuneration to hedge against future losses. Accordingly, this study proposes:

The Mediating Effect of Auditor Effort

Traditional audit procedures cannot penetrate the technological black box, and firms’ digital transformation has expanded the audit object from structured financial data to algorithmic decision-making systems and distributed data sources (Sun et al., 2015). When the depth of a firm’s digitalization surpasses the generational gap in audit technology, the control mechanisms embedded in traditional audit risk models may cease to function effectively, compelling auditors to invest continuous effort to bridge the technological divide (Zhai et al., 2022).

The audit cognitive model posits that such effort comprises learning effort and diagnostic effort (Adikaram & Higgs, 2024). Learning effort denotes the time cost incurred in mastering new technological tools. Zhang et al. (2021) document that the adoption of such tools actually lowers audit fees. Diagnostic effort, by contrast, is the cognitive load imposed by verifying non-traditional evidence; it forces auditors to reallocate scarce cognitive resources to cope with technological uncertainty. The technological training on which learning effort depends generates observable cost increases, leading audit firms to recoup their human-capital investments through a risk premium (Ranasinghe et al., 2023). Diagnostic effort, by contrast, arises from auditors’ potential misjudgment of complex system risks, raising expected losses and prompting auditors to demand a premium to cover prospective litigation risk (Kim & Park, 2024). Therefore, this study proposes:

Integrating the above arguments, Figure 1 illustrates the resulting theoretical model.

Theoretical model.

Methodology

Research Sample

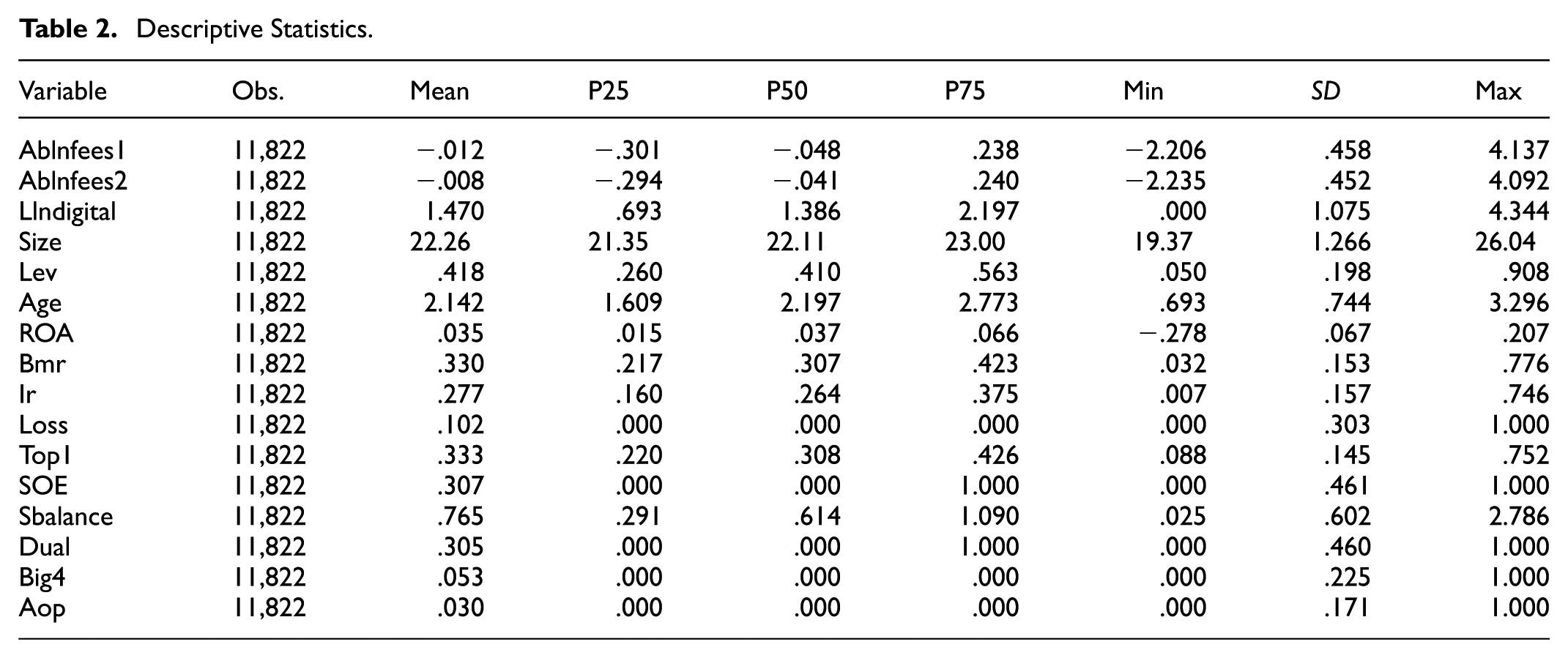

To test our hypotheses, we assemble a comprehensive panel of China’s A-share non-financial listed firms from 2007 to 2020. We exclude financial and insurance companies to ensure industrial homogeneity, omit special-treatment (ST) firms and observations with negative net assets, and drop any firm-year with missing data. The resulting sample comprises 11,822 firm-year observations. To mitigate outlier influence, we winsorize all continuous variables at the 1st and 99th percentiles. The raw data are extracted from the China Securities Market and Accounting Research (CSMAR) database. All estimations are performed in Stata 14.

Variables

The dependent variable is the natural logarithm of total audit fees, Lnfee. We measure the risk premium of the audit fee, Ablnfees1, as the residual from Model (1), following Lu et al. (2020). The residual captures fee components orthogonal to firm size, business complexity, and auditor characteristics.

The independent variable is digital transformation, Llndigital. Early studies captured it with binary indicators (Peng & Tao, 2022); more recent work uses text analytics to obtain richer, multidimensional measure (Tian et al., 2022). Following Li et al. (2025), we parse annual reports to extract digitization-related keywords, clean the resulting corpus, and take the natural logarithm of keyword frequency as our continuous measure.

We proxy auditor effort (Ainvest) with audit delay, as prior studies have established that longer engagements reflect greater resource allocation when perceived risk is high (Bryan & Mason, 2020; Ruiz-Barbadillo et al., 2024). Specifically, Ainvest is defined as the natural logarithm of one plus the number of days between fiscal year-end and the audit report date.

Following Wang et al. (2019), we further control for audit-firm characteristics in model (2) and use the resulting as an alternative measure of the risk premium of audit fee, Ablnfees2.

This study incorporates a series of control variables following established research (Hsieh et al., 2020; X. Yang et al., 2023). Specifically, the measurement and operationalization of the control variables are provided in Table 1.

Measurement and Operationalization of Variables.

Models

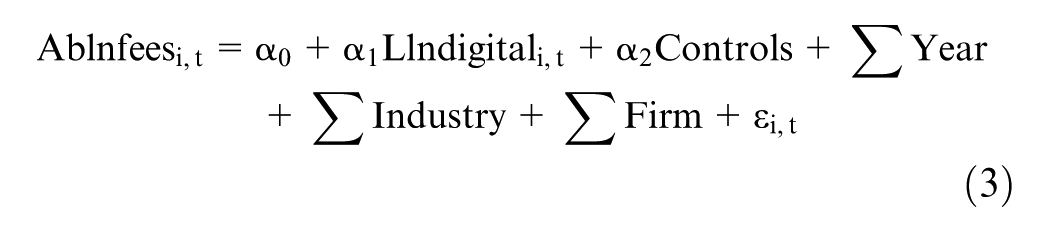

To test the effect of digital transformation on the risk premium of audit fee, we construct model (3).The model also includes year, industry, and firm fixed effects to control for time-invariant characteristics and heterogeneity across industries and individual firms.

In order to examine the impact path of digital transformation on the risk premium of audit fee, this article draws on Baron and Kenny’s (1986) research to construct mediation effect models (4) and (5).

Ainvest denotes auditor effort(the mediator); its mediating role is validated by bootstrap inference. Table 2 reports summary statistics for the main variables.

Descriptive Statistics.

Table 3 presents Pearson (lower diagonal) and Spearman (upper diagonal) correlations.

Correlations.

p < .01. **p < .05. *p < .1.

Results

Descriptive Statistics and Correlations

Table 2 reports descriptive statistics. The risk premium of audit fee(Ablnfees1 and Ablnfees2) average −.012 and −.008, with medians of −.048 and −.041, indicating a relatively low premium in the Chinese market. Digital transformation (Llndigital) averages 1.47 (median = 1.386, SD = 1.075, range = 0–4.344), revealing substantial cross-sectional variation and confirming that many firms have yet to embark on digital initiatives.

Table 3 shows that digital transformation intensity(Llndigital) is positively and significantly associated with the risk premium of audit fee(Ablnfees1 and Ablnfees2), providing preliminary support for Hypothesis 1. All pairwise correlations remain below .5, alleviating multicollinearity concerns.

The Effect of Digital Transformation on the Risk Premium of Audit Fee

Table 4 presents the empirical results examining the relationship between digital transformation and the risk premium of audit fee. Columns (1) and (3) include controls for yearly, industry, and firm-specific effects. The results indicate a positive and statistically significant relationship between digital transformation (Llndigital) and the risk premium of audit fee(Ablnfees1, Ablnfees2), with coefficients of .03 at the 1% significance level. Specifically, Columns (2) and (4) incorporate additional control variables, and the coefficient of digital transformation remains positive and significant at the 1% level, with a value of .018. These findings provide robust evidence supporting Hypothesis 1, suggesting that digital transformation significantly increases the risk premium of audit fee.

Regression Results: Digital Transformation and the Risk Premium of Audit Fee.

Note. t-value is in parentheses.

p < .01. **p < .05. *p < .1.

Empirical results show that digital transformation significantly raises the risk premium of audit fee, as auditors price in greater technological risk and complexity.

Robustness Checks

Propensity Score Matching

We used propensity-score matching followed by regression analysis to mitigate potential sample-selection bias. Following Zhang et al. (2021), we first control for industry effects and then partition the sample into high- and low-digital-transformation subsamples using the sample median of the digital transformation index. We then calculate the propensity scores using the covariates firm size (Size), leverage (Lev), and firm age (Age). We then apply 1:1 nearest-neighbor matching and estimate the matched-sample regressions. The results are presented in Table 5. Consistent with Hypothesis 1, the digital-transformation coefficient is positive and significant at the 5% level, confirming the robustness of our results to sample-selection bias.

Results of Propensity Score Matching.

Note. t-value is in parentheses.

p < .01. **p < .05. *p < .1.

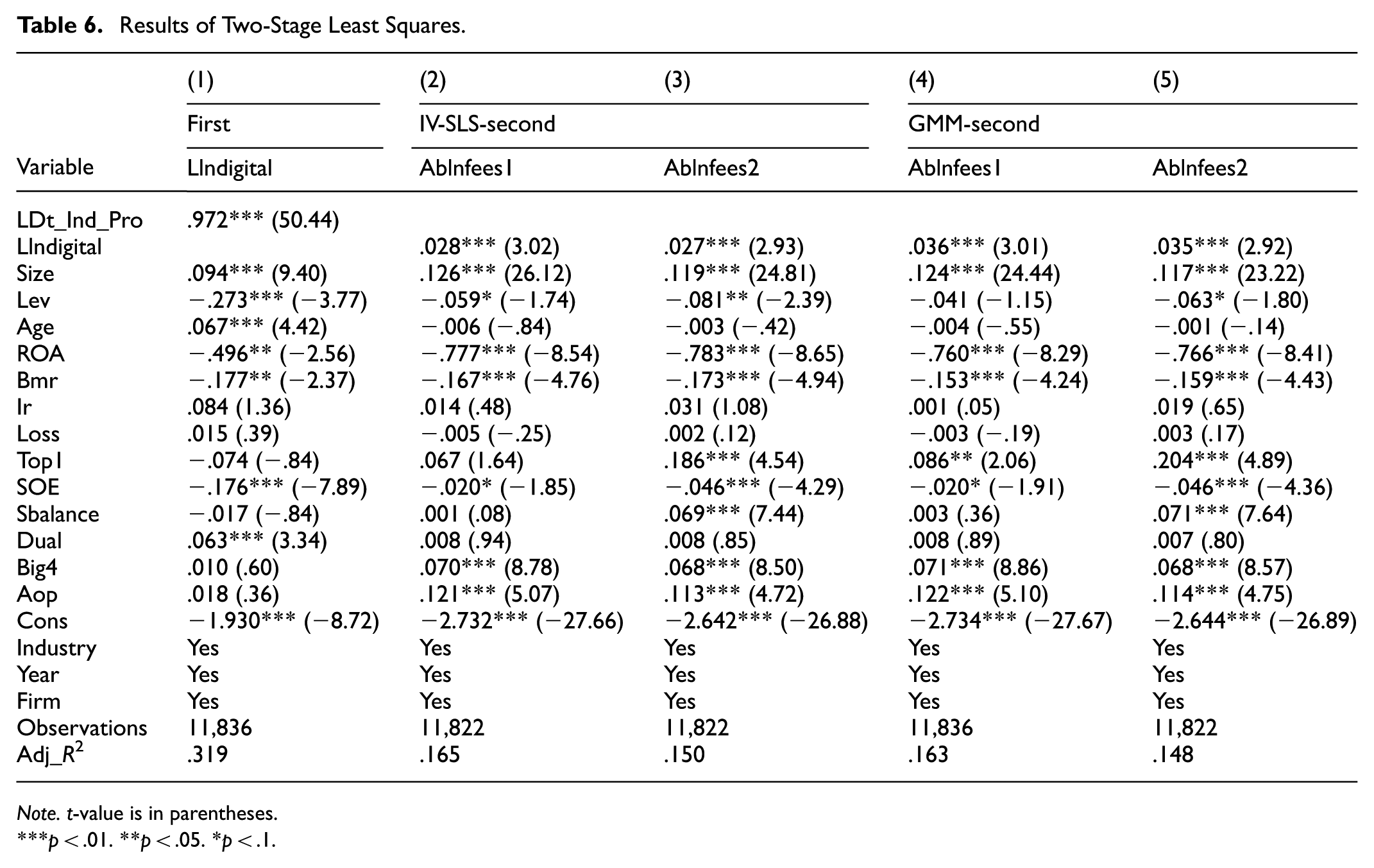

Instrumental Variable Method

We conducted the instrumental variable method and estimate two-stage least squares (2SLS) regressions to address potential endogeneity issues arising from reverse causality or omitted variables. Following Wu et al. (2022), we use the lagged peer-firm average digitization—defined as the mean digitization of other firms in the same region, industry, and year—as the instrumental variable. This variable is strongly correlated with firm-level digitization but exogenous to the risk premium of audit fee, thus satisfying the exclusion restriction for a valid instrumental variable. The results of the two-stage least squares regressions are presented in Table 6. In the first stage, LDt_Ind_Pro displayed a positive and statistically significant coefficient (p < .01), confirming the strength of our instrumental variable. Second-stage show that digital transformation coefficient remained positive and significant at the 1% level. These findings are consistent with Hypothesis 1, indicating that our empirical results are robust to potential endogeneity issues.

Results of Two-Stage Least Squares.

Note. t-value is in parentheses.

p < .01. **p < .05. *p < .1.

GMM Estimation

Furthermore, we use GMM to address dynamic endogeneity, enhancing result robustness. The regression results are shown in columns (4) and (5) of Table 6, and the results support our hypothesis.

The Delayed Effects of Digital Transformation on the Risk Premium of Audit Fee

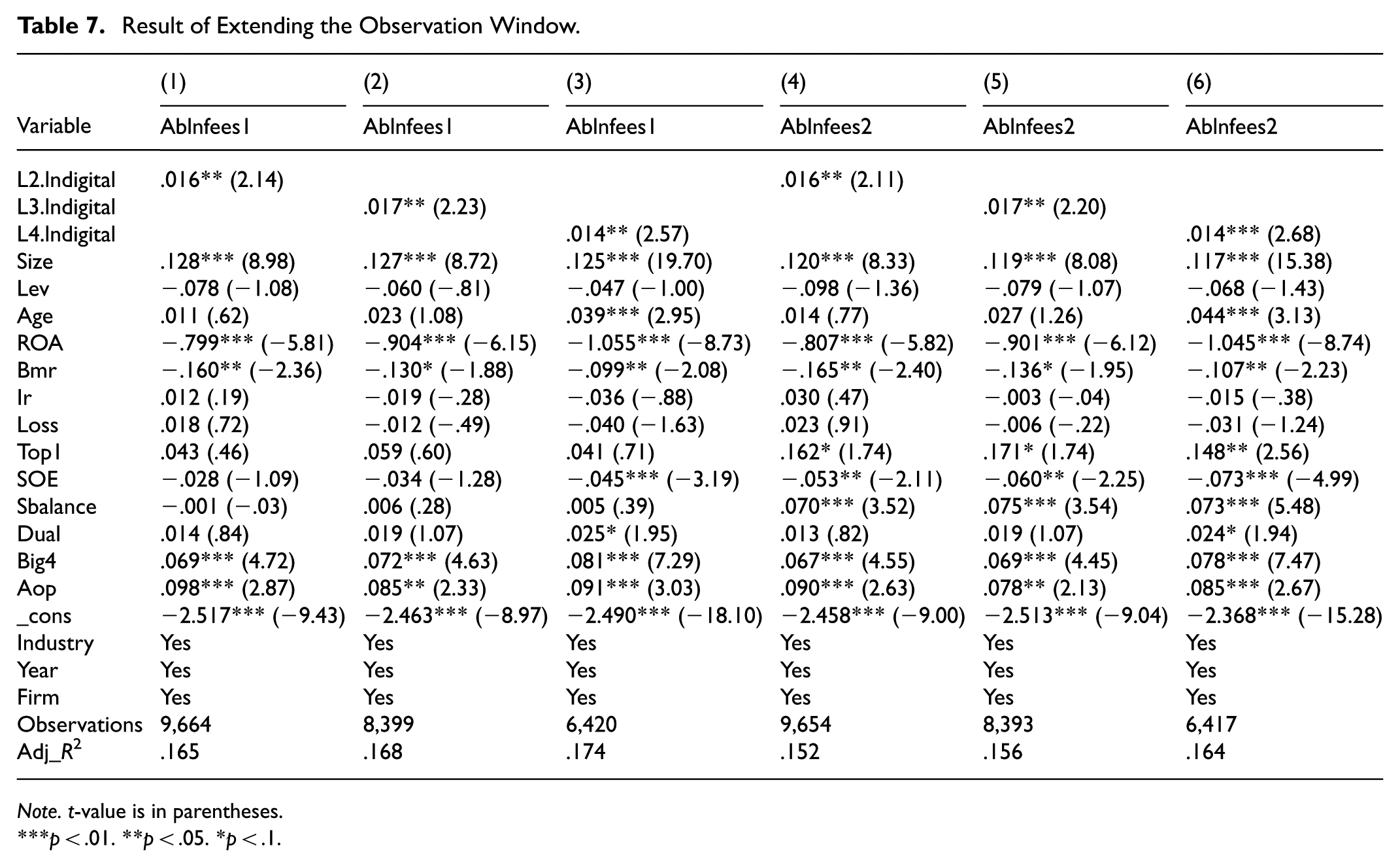

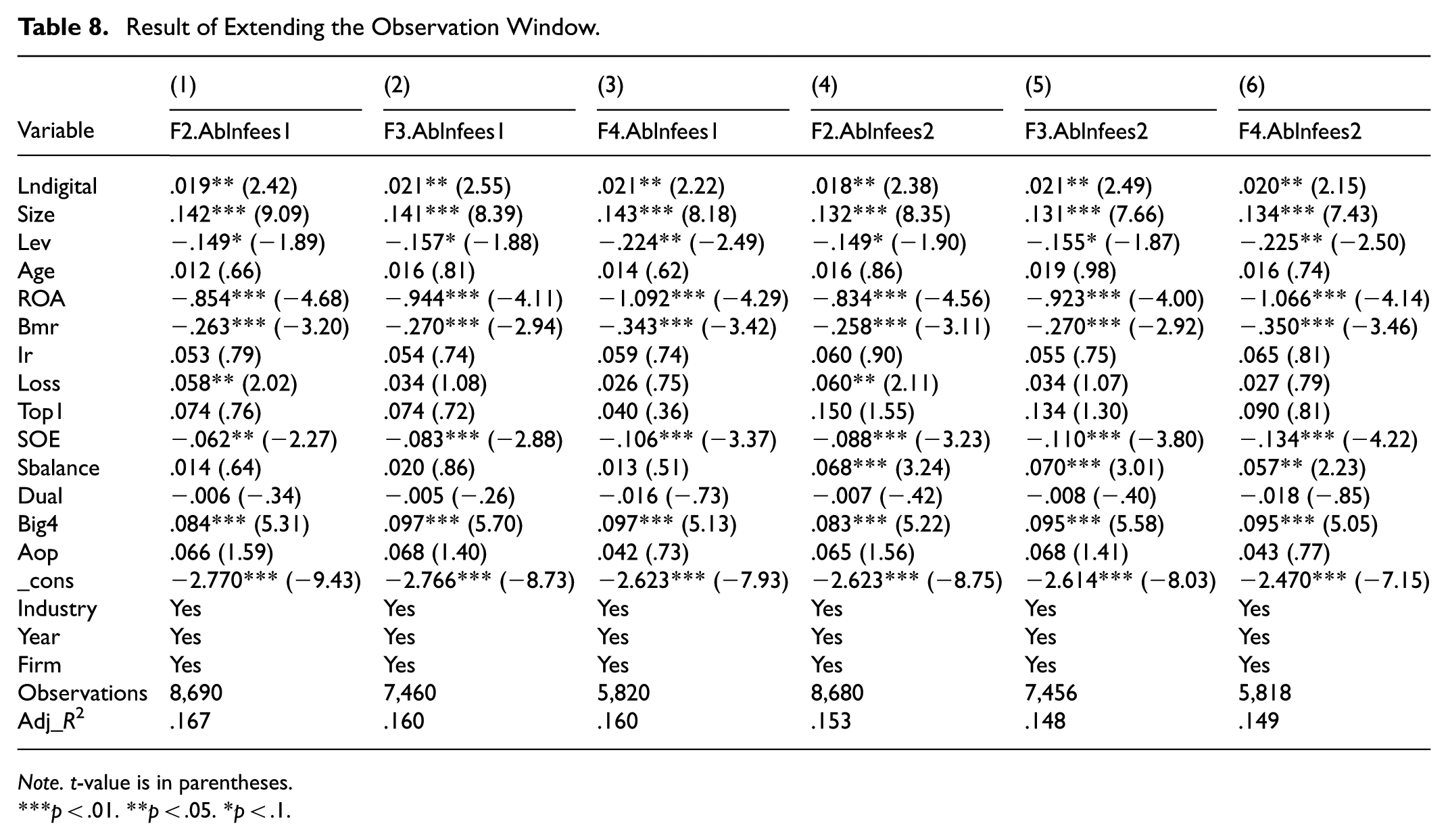

First, we extend the time window to examine the impact of digital transformation on the risk premium of audit fee. We used the independent variable (Llndigital) lagged by 2 to 4 periods and conducted regressions. The results are presented in Table 7. Consistent with Hypothesis 1, the coefficients digital transformation lagged by 2 to 4 periods are positive and significant at the 5% level. Second, we performed a cross-comparison by treating the dependent variables(Ablnfees1, Ablnfees2) with adjustments for the first 2 to 4 periods. As shown in Table 8, the coefficients of digital transformation (Llndigital) remain significantly positive, providing further evidence in support of Hypothesis 1.

Result of Extending the Observation Window.

Note. t-value is in parentheses.

p < .01. **p < .05. *p < .1.

Result of Extending the Observation Window.

Note. t-value is in parentheses.

p < .01. **p < .05. *p < .1.

The Mediating Effect of Auditor Effort

Our findings show that digital transformation significantly increases the risk premium of audit fee. Drawing on the theoretical analysis in the previous section, we use audit delay (Ainvest) as a proxy for auditor effort to test whether digital transformation affects the risk premium of audit fee through auditor effort. Following Sanchez et al. (2024), we use the mediation effect models (4) and (5) to conduct a step-by-step test. First, given that the coefficients (α1) of model (3) are significant, we proceed to evaluate the models (4) and (5). If the coefficients of β1 and b are significant, we then proceed to test c; if either β1 or b is not significant, a further Sobel test is needed. Second, if c is significant and β1 × b has the same sign as c, there is a partial mediation effect; if c is not significant, there is a full mediation effect. Third, compared to the Sobel model, the bootstrap method is more powerful and provides robust evidence in support of the mediation effect.

Column (3) of Table 8 reports the effect of digital transformation on auditor effort. The results indicate that digital transformation significantly increases auditor effort, with the coefficient of digital transformation (Llndigital) being .006 and significant at the 5% level. Columns (4) and (5) present the results examining the effects of digital transformation and auditor effort on the risk premium of audit fee. The findings reveal that both Llndigital and Ainvest exhibit significant and positive coefficients at the 5% level, suggesting that auditor effort partially mediates the relationship between digital transformation and the risk premium of audit fee. Specifically, the digital transformation of enterprises increases the effort required from auditors, which subsequently elevates the risk premium of audit fee. To further test the indirect effect of the mediator (auditor effort, Ainvest), we employed a bootstrap model. The bootstrap test yielded p-values of .001 and .008, both significant at the 1% level, confirming that auditor effort partially mediates the relationship observed in our baseline regression (Table 9). These results provide robust evidence in support of Hypothesis 2.

Results of Mediating Effect.

Note. t-value is in parentheses.

p < .01. **p < .05. *p < .1.

Further Analyses

Effects of Heterogeneous Ownership

In China’s capital market, state-owned enterprises (SOEs) and non-state-owned enterprises (non-SOEs) exhibit substantial differences in resource endowment and governance mechanisms (Yan et al., 2023). These differences may lead to variations in the degree of digital transformation between SOEs and non-SOEs, and in turn potentially result in distinct impacts of digital transformation on the risk premium of audit fee. SOEs, as extensions of government, play a critical role in supporting the achievement of specific social and economic goals set by the government. Given that digital transformation is a key national development strategy, SOEs are likely to adopt more vigorous approaches to digital transformation. However, despite this, compared to non-SOEs, SOEs are subject to stricter external regulatory oversight, which often results in higher levels of corporate governance and lower business risks. This raises the question of whether the effect of digital transformation on the risk premium of audit fee varies by ownership nature.

To address this, we classify the sample enterprises into SOEs and non-SOEs and present the regression results in Table 10. For the SOEs group (Columns [1] and [2]), the coefficients of digital transformation (Llndigital) are positive (.011 and .01) but insignificant. In contrast, in non-state-owned enterprises, the effect of digital transformation on the risk premium of audit fee is more significant (b1 = .02, p < .01; b2 = .019, p < .05). These findings suggest that the positive relationship between digital transformation and the risk premium of audit fee is more pronounced in non-SOEs. This may stem from non-state-owned firms’ relatively concentrated equity and weaker internal controls. Digital-transformation-driven algorithmic opacity more readily amplifies the risk of a material misstatement, prompting auditors to demand a higher risk premium (Hu et al., 2023).

Results of Heterogeneity in Ownership Natures.

Note. t-value is in parentheses.

p < .01. **p < .05. *p < .1.

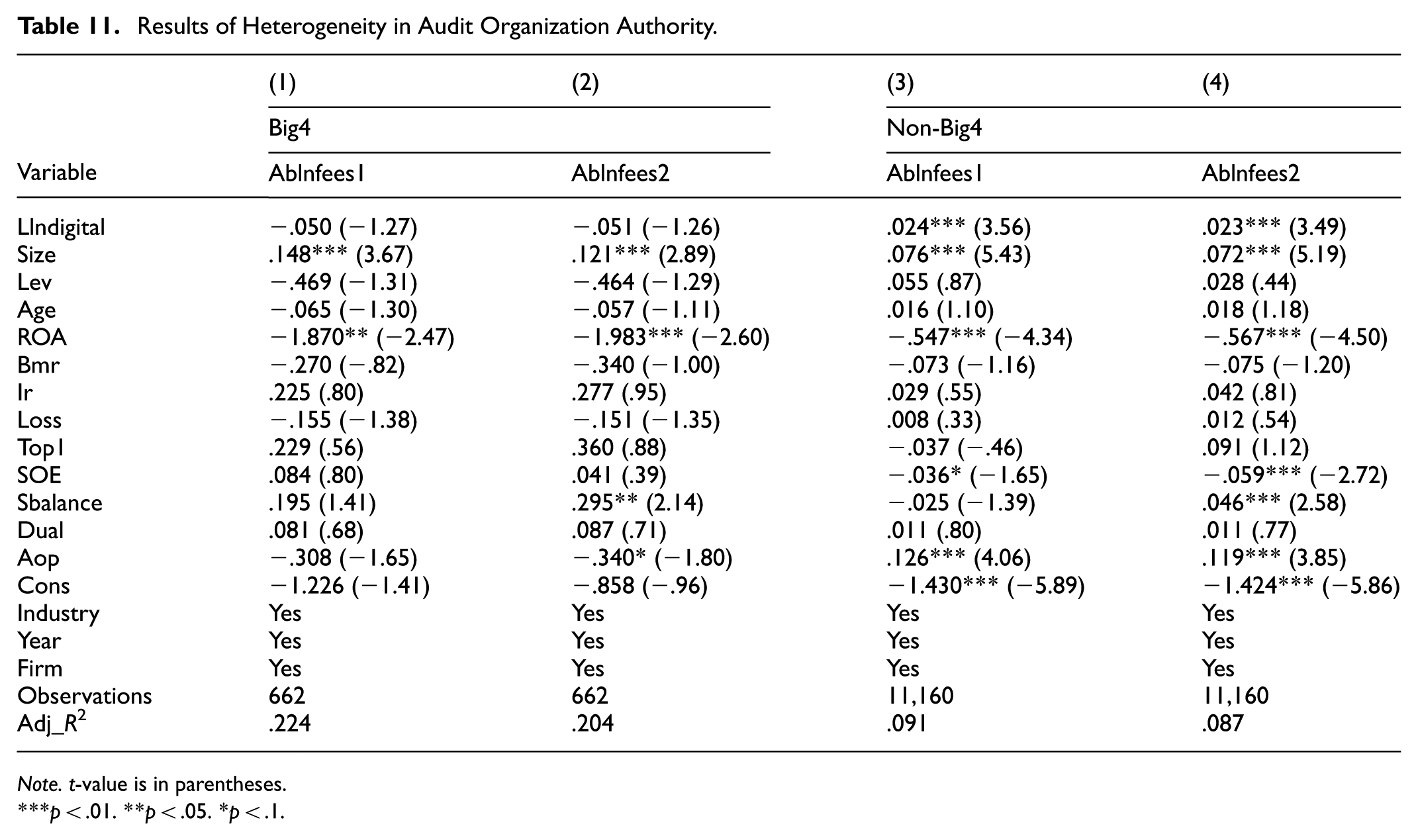

Effects of Heterogeneous Audit Organization Authority (or Auditor Capacity)

In recent years, enterprises have made significant advancements in implementing information technologies such as the Internet, big data, and cloud computing. However, auditors have lagged behind firms in adopting technologies like big data, with many firms—particularly domestic accounting firms—struggling to transition to these technologies (Manita et al., 2020). Despite this, accounting firms with higher levels of integration have strategically advanced the informatization and intellectualization of auditing work, with some taking initiatives to explore the application of big data and other technologies in their operations. As industry leaders, the Big4 accounting firms are at the forefront of developing the digitalization and intellectualization of audit work. In contrast, the lower degree of integration among domestic accounting firms hinders their ability to achieve scale effects that are necessary to promote the application of big data and other digital technologies in auditing. Overall, domestic accounting firms lag behind the Big4 in the development of audit work digitalization and intelligentization, with some domestic practitioners even lacking the concept of big data auditing. Consequently, when faced with digital transformation, domestic accounting firms may incur higher costs to adapt to accommodate such transformations.

To examine the moderating role of audit firm capability, we introduced a dummy variable, Big4, which equals 1 if the company is audited by a Big4 accounting firm and 0 otherwise. The regression results are presented in Table 11. For companies audited by Big4 accounting firms (Columns [1] and [2]), the coefficients of digital transformation (Llndigital) are insignificant. However, for companies audited by non-Big4 accounting firms (Columns [3] and [4]), the coefficients of digital transformation are positive and significant at the 1% level. These findings indicate that the positive effect of digital transformation on the risk premium of audit fee is more pronounced when a firm is audited by a non-Big4 accounting firm.

Results of Heterogeneity in Audit Organization Authority.

Note. t-value is in parentheses.

p < .01. **p < .05. *p < .1.

Effects of Heterogeneous Technological Intensity

There are significant differences in how high-tech and non-high-tech firms are affected by digital transformation. High-tech firms operate distinctive business models in which digital technology constitute a critical means of production. They exhibit a higher degree of digitization than their non-high-tech counterparts, stronger incentives to transform, and greater adaptability to the digital era. By contrast, non-high-tech firms, which possess limited digital capabilities, bear a disproportionately larger impact from digital transformation. Consequently, digital transformation injects additional uncertainty into their business models and governance structures, thereby raising the risk premium of audit fee.

To classify high-tech listed companies, we used the 2013 Classification of High-Tech Industries (Manufacturing) and Classification of High-Tech Industries (Service) issued by the National Bureau of Statistics. Under these standards, we identified 20 high-tech sectors with the following codes: C26, C27, C34, C35, C37, C38, C39, C40, C43, I63, I64, I65, L72, M73, M74, M75, N77, R85, R86, and R87. We then assigned each sample firm to either the high-tech and non-high-tech group. The regression results appear in Table 12. For the high-tech group (Columns [1] and [2]), the coefficients on digital transformation (Llndigital) are positive (.009 and .009) but insignificant. In contrast, for the non-high-tech group (Columns [3] and [4]), the coefficients on digital transformation are positive (.025 and .025) and significant at the 5% level. These findings indicate that the positive effect of digital transformation on the risk premium of audit fee is more pronounced among non-high-tech enterprises.

Results of Heterogeneity in High-Tech Enterprises.

Note. t-value is in parentheses.

p < .01. **p < .05. *p < .1.

Discussion

This article contributes to the literature on the predictors of the risk premium of audit fee by providing the first large-sample evidence on how digital transformation affects that premium. As incremental information on firm-level risk, the risk premium of audit fee offers investors valuable insights into a company’s underlying operating conditions. Prior research has examined the determinants of risk premium indirectly, via the level of audit fees (Teng & Han, 2023); direct evidence on the drivers of the premium itself remains scarce. Different from the research of Zhai et al. (2022), we construct a direct measure of the risk premium of audit fee to explore how digital transformation affects this premium, offering auditors deeper and more comprehensive insights into controlling client-specific audit risks.

Distinct from the work of Xu (2025), we conduct an in-depth investigation of the impact of digital transformation on the risk premium of audit fee from the perspective of auditor effort, addressing the methodological call made by Jaffar et al. (2023). This study opens the black box of how digital transformation influences the risk premium of audit fee and provides a reasonable explanation for the mechanism through which digital transformation increases auditor efforts, thereby elevating the risk premium of audit fee.

We further explore how ownership natures, auditor ability, and enterprise attributes moderate the relationship between digital transformation and the risk premium of audit fee. Our findings reveal that the positive effect of digital transformation on the risk premium of audit fee is more pronounced in non-state-owned enterprises (non-SOEs), enterprises audited by non-Big4 accounting firms, and non-high-tech enterprises. Distinct from the findings analyzed in (Zhang et al., 2021), our findings enhance our understanding of how digital transformation affects the risk premium of audit fee in different contextual settings and deepen our comprehension of the risk premium in the context of digital transformation.

Conclusion and Recommendation

Drawing on China’s A-share listed firms from 2007 to 2020, the study investigates how digital transformation influences the risk premium of audit fee. Our findings indicate that digital transformation amplifies the risk premium of audit fee. Furthermore, we establish auditor effort as a significant mediator transmitting the positive effect of digital transformation on the risk premium of audit fee. The positive association between digital transformation and the risk premium of audit fee is significantly amplified among non-state-owned and non-high-tech enterprises. The effect is significantly amplified when the auditors are affiliated with a Big4 accounting firm. Collectively, these findings novel insights into the dynamics of the risk premium of audit fee amid digital transformation and substantially advance scholarly understanding of how digital transformation reshapes contemporary audit practice.

This article offers several practical implications for stakeholders. First, enterprises should seize the opportunities afforded by digital transformation and deploy digital technologies to control audit risk within tolerable limits, thereby minimizing the likelihood of future liabilities. By fostering a dynamic interplay between digital transformation and risk premium of audit fee, organizations can catalyze innovation and continuous refinement in their corporate audit-governance models. Second, as external governance agents, auditors should deploy their professional expertise proactively—especially in accelerating digital transformation landscape—to anticipate risks and enhance assurance quality. In audit engagements, they must rigorously execute prescribed procedures, formulate appropriately modified opinions, and thus attenuate audit risk to within tolerable limits. These measures will enhance audit quality and, in turn, foster enterprise-level sustainable development in the digital era.

This study has two main limitations. First, although the digital economy is a global phenomenon, our sample is restricted to A-share firms listed on the Shanghai and Shenzhen exchanges in China; findings may not generalize to other institutional settings. Cross-country evidence is therefore warranted. Second, the absence of a widely accepted benchmark for the risk premium of audit fee obliges us to rely on empirical proxies; improved measurement remains an avenue for future research.

Footnotes

Acknowledgements

The authors acknowledge the anonymous reviewers and editors for helpful guidance on prior versions of the article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

All data generated and analyzed during this study are included in this article. Due to privacy laws, more detailed raw data are not publicly available. However, upon reasonable request, data can be obtained from the corresponding author.