Abstract

As critical external governance actors, auditors proactively shape cross-border regulatory outcomes. Using data from Chinese A-share listed multinational corporations from 2017 to 2023, our study analyzes text from the “Key Audit Matters” sections of audit reports to develop an index measuring auditors’ host-country risk perception(RP). We empirically investigate how RP influence earnings manipulation practices in multinational corporations. Results show that RP significantly reduce earnings manipulation in multinational enterprises. Mechanism tests reveal that auditors address heightened risk perceptions by raising audit fees and lengthening audit timelines, which directly curbs opportunities for earnings manipulation. The heterogeneity analyses indicate that this negative relationship is more pronounced when auditors possess multinational expertise, the host countries of overseas subsidiaries have weaker rule of law, the geographical distance between overseas subsidiaries and the home country is greater, and the enterprise’s ownership is non-state-owned. By establishing RP as an effective alternative governance mechanism, this research advances the theoretical framework for cross-border audit governance. It also offers practical guidance for emerging markets seeking to reduce multinational corporations’ earnings manipulation through enhanced audit oversight.

Introduction

In today’s globalized economy, multinational Enterprises (MNEs) play a pivotal role in international economic activities. The standardization of their financial practices is closely tied to the stability of capital markets. Investigating the quality of accounting information in MNEs is therefore of significant practical importance. According to United Nations criteria, a MNE is defined as any company that controls assets in two or more countries, with foreign subsidiaries that possess at least 10% of voting rights or account for 25% of the parent company’s sales or assets. In 2023, data showed that overseas subsidiaries accounted for an average of 23% of the total revenue of Chinese parent companies, underscoring the strategic value of international operations for corporate groups. However, as cross-border operations expand, instances of earnings manipulation have become more frequent. Notable cases include Abbott’s 2015 inflation of revenue by 200 million yuan through a fabricated Pakistani construction project and Erkang Pharmaceutical’s 2018 profit manipulation via its overseas subsidiaries. These incidents highlight the significant challenges in regulating cross-border financial activities. Research indicates that factors such as uncertainties in the host countries’ legal environments, cultural disparities, levels of investor protection, and the intensity of enforcement (Beuselinck et al., 2019; Han et al., 2010; J. Huang, 2018; Lang et al., 2006) greatly increase MNEs’ incentives to manipulate earnings. Particularly during foreign direct investment, political-economic risks and financial uncertainties in host countries (Wu & Hu, 2015) can lead to fluctuations in a company’s future cash flows. In response, MNEs often engage in earnings manipulation through various accounting techniques, including adjusting accounting estimates (such as bad debt provisions), altering the timing of revenue recognition, and modifying deferred items. Both real-world cases and theoretical studies demonstrate that earnings manipulation in MNEs is a critical issue that demands immediate regulatory attention and effective solutions.

High-quality audits are widely recognized in academic literature as effective deterrents against earnings manipulation (O'Reilly et al., 2006). However, auditing multinational operations introduces additional challenges due to the geographic dispersion of subsidiaries. Auditors must navigate cross-jurisdictional language and cultural barriers, political regime changes, diverse economic and financial regulatory systems, and various communication obstacles. These compounded risks significantly increase audit complexity (Downey & Bedard, 2019). To effectively manage misstatement risks and maintain professional integrity, auditors must adopt tailored strategies for MNEs operating in high-risk countries. In this context, auditors’ host-country risk perception(RP) become critical. Risk perception serves as a comprehensive evaluation mechanism for external risks, involving an integrated assessment of both the probability and potential impact of specific risk events. In audit practice, RP refers to their professional judgment during engagements. This process involves identifying and assessing the severity of risks related to the political, economic, cultural, and legal environments of the MNE’s overseas investments. Auditors can systematically reveal and warn about enterprises’ cross-border risks by using Key Audit Matters (KAMs) in the audit report, through standardized expressions such as risk assessment section disclosures and emphasis of matter paragraphs. KAMs represent the areas of the audit that, in the auditor’s professional judgment, were of most significance (China Ministry of Finance, 2016; International Auditing and Assurance Standards Board [IAASB], 2015). These matters typically involve a higher degree of risk concerning material misstatement. Auditing standards mandate that auditors not only disclose the selected KAMs in the report but also provide the rationale for their designation as key matters (IAASB, 2015). This requires auditors to elucidate the associated significant risks of material misstatement (or significant risks), significant management judgments, and significant transactions or events involved (Sun et al., 2024). Consequently, the process of selecting and describing KAMs inherently reflects the outcome of the auditor’s risk assessment procedures, demonstrating heightened attention and professional skepticism toward specific areas of the client’s financial statements and operations (Sirois et al., 2018). Prior research shows KAMs disclosure demonstrates the auditor’s work in forming an audit opinion (Gutierrez et al., 2018) and provides information for assessing audit value, thereby enhancing the audit’s information content and communication effectiveness (Reid et al., 2019). For example, Jiangsu Favored Nanotechnology Co., Ltd.’s 2017 audit report explicitly stated in its KAMs section that “objective differences in political, economic, legal, and cultural environments between the host countries/regions of overseas subsidiaries and China create cross-border management risks.” Similarly, Henan Rebecca Hair Products Co., Ltd.’s 2018 audit report emphasized that “overseas subsidiaries are spread across multiple jurisdictions, including the UK, the U.S., Africa, and Cambodia, where geographic dispersion and institutional heterogeneity intensify cross-border management risks.” In its 2019 audit report, Guangdong DP Co., Ltd. highlighted risks related to foreign sales revenue by noting that “the complexity of political and economic environments in some client countries increases the risks associated with accounts receivable recovery.” Additionally, China Oilfield Services Limited’s 2017 audit report included similar risk alerts concerning the assessment of accounts receivable impairment. These examples demonstrate auditors’ ability to identify operational risks in the host countries where MNEs operate. Their heightened risk perception leads to enhancements in specific audit procedures. For instance, in response to the key matter of “cross-border operational risks of overseas entities,” Jiangsu Favored Nanotechnology Co., Ltd.’s audit team systematically implemented enhanced procedures: verifying going concern assumptions, assessing revenue recognition principles, examining commercial substance, authenticity testing of sales transactions, confirming overseas customers, and performing physical asset inventories. This multidimensional response system reflects the practical application of mental accounting theory (Thaler, 1999) in audit decision-making. Auditors categorize host country risks into a “high-uncertainty mental account” and mitigate these risks by allocating additional audit resources, such as increasing audit fees and extending audit timelines, thereby curbing MNEs’ earnings manipulation.

Building on this foundation, we developed a variable to measure RP using a sample of A-share listed MNEs from 2017 to 2023. This enabled us to empirically assess how RP influence MNEs’ earnings manipulation. Grounded in multinational operational risk theory, our study employs a textual analysis of KAMs sections related to cross-border risks within audit reports. Using Python statistical software, we conducted text mining on these sections of these audit reports to identify semantic features associated with host country risks. From this analysis, we created a risk keyword lexicon and quantified the frequency of cross-border risk-related terms in the KAMs section. This frequency served as a proxy for RP. Additionally, we utilized the modified Jones model as a proxy to measure corporate earnings manipulation. To establish a causal relationship between RP and corporate earnings manipulation, we applied a one-period lag to the variable. Our findings indicate that higher levels of RP are associated with a reduction in MNEs’ earnings manipulation. In our mechanism analysis, we discovered that RP leads to increased audit fees and greater audit timelines, which in turn reduce the likelihood of earnings manipulation. Furthermore, we explored whether the relationship between RP and earnings manipulation varies across different contexts to support our causal interpretation. Our results show that the suppressive effect of RP is particularly significant in cases where auditors have multinational expertise, host countries possess weaker rule of law, host countries are geographically distant from China, and the multinational enterprises are non-state-owned. These findings enhance our understanding of the economic consequence of auditor behavior and offer valuable insights for regulating corporate financial practices.

Compared to existing research, our study makes significant contributions in the following areas: Firstly, we deepen the understanding of the auditor’s role within the corporate governance framework. While previous studies primarily explain the governance effects of auditing through information asymmetry and agency costs, our research incorporates external governance and mental accounting theory (Thaler, 1999). Additionally, we utilize textual analysis to develop a metric for RP. Our findings indicate that auditors do not simply adapt passively to the institutional environments of host countries. Instead, they proactively adjust their audit strategies by creating a “cross-border risk mental account.” This challenges the traditional view in the literature that portrays auditors as “passive recipients of institutional constraints” and offers a fresh perspective on the active role auditors play in cross-border governance. Furthermore, our research expands the scope of informal governance mechanisms within corporate governance theory. It highlights the theoretical significance of RP capabilities as an alternative governance mechanism in contexts with institutional disparities, thereby providing a novel framework for understanding the effectiveness of audit governance in emerging markets.

Secondly, our study advances research on factors influencing earnings manipulation in MNEs. Previous studies have seldom examined how auditor characteristics or capabilities impact the MNEs’ earnings manipulation behaviors. By integrating multinational investment, RP, and earnings manipulation into a cohesive analytical framework, we demonstrate that RP is a crucial external factor in deterring MNEs’ earnings manipulation. Moreover, we find that auditors mitigate earnings manipulation by reallocating resources—specifically by increasing audit fees and extending audit durations. This finding not only validates the applicability of the “risk premium effect” (Simunic, 1980) in a cross-border context but also shifts the focus of audit governance from ex-post oversight to ex-ante risk warnings, underscoring the proactive role of auditors in governance. These findings provide empirical evidence for regulating earnings manipulation in in MNEs and help clarify regulatory priorities.

Thirdly, our study offers valuable insights for global cross-border audit supervision. We developed a Python-based semantic analysis method that quantifies the frequency of cross-border risk terms in KAMs sections from audit reports. This method can be applied to other jurisdictions to identify variations in RP. For example, regulators in the EU or the U.S. could adopt this textual analysis framework to enhance standardized disclosure requirements for KAMs of MNEs. Our findings reveal that auditors address host country risks by reallocating resources, such as increasing audit fees and extending audit timelines. This approach is universally applicable for supervising subsidiaries in regions with weak rule of law or high geopolitical risks. It suggests that international audit standard-setting bodies should refine procedural guidelines for high-risk countries and promote cross-border regulatory collaboration. Additionally, our study highlights the governance benefits of auditors’ multinational expertise, supporting the argument for MNEs to prioritize professional qualifications when selecting auditors. It also implies that firms operating in high-risk host countries need to optimize internal control systems in their overseas subsidiaries to support enhanced audit procedures, thereby reducing compliance risks. Overall, these findings provide methodological guidance for improving international audit standards and strengthening cross-border regulatory coordination in emerging markets.

The remainder of this paper proceeds as follows. Section 2 formulates our hypotheses by synthesizing insights from prior literature. Section 3 describes the sample selection criteria, data sources, and key methodological components of our research design. Section 4 reports the core empirical findings, supplemented by robustness tests, mechanism analyses, and cross-sectional heterogeneity assessments. Section 5 concludes by summarizing key insights and discussing theoretical and practical implications.

Theoretical Analysis and Research Hypotheses

The financial performance of MNEs is closely linked to the macroeconomic conditions of their host countries. Systemic risks such as political regime changes, financial market volatility, economic policy uncertainty, and cultural value conflicts not only jeopardize the security of overseas assets but also increase the complexity of decision-making for corporate managers (Peng et al., 2022). In response to these challenges, MNE executives often engage in earnings manipulation strategies—such as intertemporal earnings smoothing and the selective application of accounting policies—to artificially inflate financial reporting metrics (Q. C. Huang et al., 2022). These practices undermine the reliability of financial data for stakeholders and heighten professional risks, particularly for auditors. The combination of MNEs’ complex organizational structures, limited internal governance, and ambiguous host-country regulations exacerbates information asymmetry. This lack of transparency makes it difficult to discern discretionary decisions in accounting policy adoption and asset valuation adjustments (Dyreng et al., 2012). Additionally, geographic distance, institutional complexity, and the need for localization enhance the operational autonomy of foreign subsidiaries. Managers’ excessive discretion in accounting estimates—through methods like flexible provisioning for asset impairments and strategic timing of revenue recognition—significantly increases auditors’ exposure to risks of misstatements and omissions (Lu et al., 2023). Importantly, when MNEs respond to host-country risks with aggressive accounting strategies, disparities in cross-jurisdictional regulations and evidentiary barriers can cause auditors to underestimate the significance of financial misstatements. This mechanism not only challenges auditors’ professional expertise but also exposes them to legal liabilities and reputational harm, especially in cases of systemic governance failures.

Host country risks not only heighten audit risks by encouraging corporate earnings manipulation but also activate auditors’ dynamic risk perception mechanisms. When companies exploit cross-border regulatory differences to engage in accounting policy arbitrage, auditors face not only technical verification challenges but also oversight gaps caused by the interaction of formal institutional disparities (political, economic, financial) and cultural-cognitive misalignments (Zhang et al., 2020). This complexity makes traditional passive compliance models—relying solely on contractual clauses—ineffective, compelling auditors to proactively develop subjective interpretations of host-country risks. This perceptual process involves filtering, decoding, and assigning weights to risk signals such as abrupt policy changes, stringent foreign exchange controls, and the reliability of local audit evidence (March & Shapira, 1987). This framework challenges conventional “objective risk-dominant” perspectives, which suggest that auditor responses are automatically driven by quantifiable indicators—for example, automatically increasing scrutiny of foreign exchange risks when host-country central banks report declining reserve levels (Chang et al., 2024). However, objective metrics often fall short in unstructured risk scenarios like regulatory arbitrage or sudden institutional disruptions. In these cases, auditors must cognitively process fragmented risk signals, such as unexpected tariff adjustments or social media rumors of political instability. When auditors develop negative mental anchors based on past project failures or industry-wide risk events, their sensitivity to risk becomes disproportionately heightened through the availability heuristic (Tversky & Kahneman, 1974), leading to non-routine audit procedures. For instance, auditors’ expectations about local officials’ discretionary enforcement power can fundamentally alter their decision-making. Even when official risk ratings are identical, audit teams anticipating selective law enforcement in a jurisdiction may respond by inflating fees, extending inventory observation periods, or increasing the sampling intensity in substantive testing (Florou et al., 2020). This behavior aligns with mental accounting theory (Thaler, 1999), where auditors categorize host-country risks into a “high-uncertainty mental account” and allocate disproportionate resources to mitigate perceived threats within this category.

Under the dynamic influence of risk perception, auditors often implement a dual constraint mechanism—raising audit fees and extending audit timelines—to curb earnings manipulation. RP directly affects the cost boundaries of earnings manipulation through audit fee pricing. In high-risk environments, factors like political uncertainty, disparities in legal systems, and information asymmetry significantly increase auditors’ professional risks. To mitigate potential losses from audit failures and compliance costs, auditors incorporate risk premiums into their fees (Lyon & Maher, 2005). Higher fees not only compensate for complex risk exposures but also encourage auditors to invest these premiums in more extensive substantive procedures, such as cross-border document verification (Choi & Wong, 2007). Additionally, audit teams may incur extra costs by hiring local compliance experts or deploying cross-jurisdictional data-tracking systems, which are ultimately passed on to clients through risk premiums. This risk-driven audit investment bolsters the detection of abnormal accounting practices and diminishes the marginal gains from earnings manipulation, thereby deterring such opportunistic behavior. Furthermore, RP exerts governance effects by extending audit timelines. Coordinating multi-jurisdictional evidence chains (e.g., confirmations from foreign subsidiaries, audits of cross-border fund flows) and navigating host-country data privacy laws or bureaucratic inefficiencies inevitably prolong audit cycles (Bamber et al., 1993). These audit delays create an “uncertainty window” for financial reporting, potentially triggering skepticism in capital markets about the quality of the disclosed information. This skepticism pressures management to proactively reduce accounting manipulation to avoid negative market reactions. Moreover, the extended verification of complex cross-border matters—such as valuing foreign exchange derivatives or assessing the commercial substance of related-party transactions—limits firms’ ability to use time constraints to conceal manipulations (Lambert et al., 2017). Additionally, audit delays often coincide with heightened frequency of audit adjustments and disclosure mandates, compelling firms to surface financial misstatement risks earlier. This creates a time-for-quality monitoring feedback loop, which further constrains earnings manipulation in cross-border contexts. Based on the above analysis, we propose:

H1: RP Inhibits MNEs’ Earnings Manipulation

RP can vary significantly across different contexts. Multinational expertise refers to auditors’ experience in conducting cross-border audit engagements, and greater expertise in this area enhances their ability to perform audits for MNEs. Compared to auditors without such expertise, those with multinational specialization—achieved through professional training and extensive cross-border audit experience—are more adept at identifying host-country risks and effectively preventing clients from manipulating earnings. These specialized auditors possess a nuanced understanding of differences in accounting practices, standards, and legal frameworks between host and home countries (Gunn & Michas, 2018). Additionally, they systematically detect and mitigate aggressive earnings manipulation by implementing strategies such as modular auditing and real-time communication protocols (Downey & Bedard, 2019). Based on this analysis, we propose:

H2: Auditor international expertise positively moderates the negative relationship between RP and MNEs’ earnings manipulation. That is, when auditors possess international expertise, the mitigating effect of RP on MNEs’ earnings manipulation becomes more pronounced.

As a crucial external governance mechanism, the quality of a host country’s rule of law plays an essential role in deterring corporate earnings manipulation. Firstly, robust legal frameworks increase the likelihood of detecting such practices. In countries with strong legal systems, government enforcement agencies operate efficiently, enabling the effective identification of earnings manipulation by listed companies. Secondly, stringent legal framework heightens the severity of penalties for earnings manipulation (Almadi & Lazic, 2016). Jurisdictions with well-developed legal framework often empower independent enforcement bodies to rigorously apply national regulations when addressing earnings manipulation by listed companies. Conversely, in regions with weaker rule of law, listed companies frequently engage in rent-seeking activities to mitigate administrative penalties, allowing earning manipulation to persist (Dyreng et al., 2012; Prencipe, 2012). Based on this analysis, we propose:

H3: The host country’s legal system negatively moderates the negative relationship between RP and MNEs’ earnings manipulation. That is, when the host country has a weaker rule of law, the inhibitory effect of RP on MNEs’ earnings manipulation becomes more pronounced.

Geographic proximity between auditors and their clients provides significant informational advantages (Choi et al., 2012). This closeness allows auditors to gain deeper insights into clients’ motivations and operational capabilities related to earnings manipulation, thereby enhancing the effectiveness of audit oversight. However, in multinational audits, the physical distance between overseas subsidiaries and the parent company leads to information delays and distortions. Additionally, it increases the costs associated with cross-border data verification and on-site audits, while also creating substantial barriers to accessing tacit information—such as the logic behind management decision-making and the implementation of internal controls. These challenges heighten the risk of opportunistic earnings manipulation through sophisticated tactics like adjusting the timing of revenue recognition. To navigate these regulatory obstacles and protect their professional reputation, auditors’ ability to perceive risks in host countries becomes indispensable. Based on this analysis, we propose:

H4: The geographic distance between the overseas subsidiary and the parent company positively moderates the negative relationship between RP and MNEs’ earnings manipulation. That is, when the overseas subsidiary is geographically farther from the parent company, the mitigating effect of RP on MNEs’ earnings manipulation becomes more pronounced.

Differences in state ownership can lead to varied behaviors in enterprises. From a motivational perspective, non-state-owned enterprises (non-SOEs) generally have stronger incentives to manipulate earnings. Investors tend to prioritize corporate credibility and operational performance when making financing decisions. In contrast, state-owned enterprises (SOEs) benefit from their dual role as pillars of the national economy and leaders in strategic emerging industries (Xiao & Wang, 2015). Their access to government guarantees and implicit bailout expectations bolster market confidence in their ability to bear risks (Jin et al., 2023). Conversely, non-SOEs are often perceived as having weaker risk resilience and profitability, facing stricter financing conditions. This structural disparity drives non-SOEs to engage in earnings manipulation to enhance their financial metrics. From a feasibility standpoint, non-SOEs operate under fewer institutional constraints. SOEs face stricter institutional constraints on earnings manipulation due to their unique ownership structures and significant government intervention. In contrast, non-state-owned enterprises benefit from high levels of autonomy and market-driven decision-making processes that effectively avoid administrative interference, granting them greater independence and flexibility in their financial operations. Based on this analysis, we propose:

H5: The state ownership moderates the negative relationship between RP and MNEs’ earnings manipulation. Specifically, when the enterprise is a non-SOE enterprise, the mitigating effect of RP on MNEs’ earnings manipulation becomes more pronounced.

Research Design

Data Sources and Sample Construction

The new audit reporting standards were first implemented for A+H-share listed companies effective January 1, 2017 in China. Consequently, we selected MNEs listed on the Shanghai and Shenzhen A-share markets from 2017 to 2023 as our research sample. Using the “Overseas Affiliated Companies Table” from the China Stock Market & Accounting Research (CSMAR) database, we identified the overseas subsidiaries of listed companies and their respective host-country regions of investment during this period. Subsequently, we determined the domestic and international audit firms engaged by these listed companies based on CSMAR’s “List of Listed Companies’ Audit Institutions” and matched this information with the sample of listed companies that have overseas subsidiaries. The sample was meticulously refined to ensure data consistency and validity by excluding the following categories: (1) samples with specific overseas investments made in Hong Kong, Taiwan, and Macau; (2) samples with inconsistencies between domestic and foreign audit institutions for the listed companies; (3) samples marked with ST and *ST (Special Treatment) companies; (4) samples originating from the financial industry sector; and (5) Samples where KAMs and other relevant data were not disclosed because the auditors issued a disclaimer or an adverse opinion on the financial statements. As a result, a total of 9,148 valid observations were obtained for subsequent analysis. To measure RP, we constructed variables using the KAMs section of the audit reports of listed companies. The necessary firm-level data, information on overseas subsidiaries, and details of audit firms and partners were sourced from the CSMAR and Wind (WIND) databases. Additionally, host-country risk data were obtained from the Worldwide Governance Indicators (WGI) and the International Country Risk Guide (ICRG) published by the Political Risk Services Group (PRS).

Model Construction and Definitions of Variables

We construct Model (1) to verify the relationship between RP and MNEs’ earnings manipulation.

The explained variable is MNEs’ earnings management (DAC). In line with the adjusted Jones model proposed by Dechow et al. (1995), it is measured as the absolute difference between total accruals and non-discretionary accruals. The estimated model is presented as follows:

Where

The explanatory variable in this study is RP. Grounded in the theoretical framework of multinational business risk, our research utilizes text analysis to examine the KAMs section of audit reports. We extract semantic features related to host-country risks through a detailed process described below. First, we established a seed set comprising 22 core risk terms, including “financial crisis,”“exchange rate risk,”“political risk,”“economic risk,” and “country risk.” Next, we employed a Word Embedding neural network language model to calculate vector similarities, identifying additional related words. This iterative expansion process resulted in an extended set of 107 derived words, such as “geopolitical conflict,”“capital controls,”“economic sanctions,”“European debt crisis,” and “non-tariff barriers.” Together with the initial seed set, this formed a comprehensive host country risk vocabulary totaling 129 terms. To ensure the validity of our vocabulary, we cross-validated the risk term indicator set against established risk indicators, such as the Country Risk Index (ICRG) provided by the US Political Risk Services Group (PRS). This step confirmed the rationality of our word set. Using Python, we then analyzed the frequency of these multinational risk terms within the KAMs sections, excluding terms appearing in sentences with negative connotations (e.g., “not,”“without”). The frequency of these terms served as a proxy variable for measuring the RP. To explore the causal relationship between the RP and corporate earnings manipulation, we introduced a one-period lag to the RP variable.

Drawing on existing literature (Bédard et al., 2004; Katmon & Farooque, 2017), we control for various factors that may influence corporate earnings manipulation. First, we consider firm-level factors. From a financial perspective, larger firms often face higher political costs, which may incentivize aggressive earnings manipulation to mitigate these expenses (Warfield et al., 1995). To account for this, we include firm size (Size) as a control variable. Additionally, firms with high leverage may manipulate earnings to avoid breaching debt covenants (Al-Okaily et al., 2020), prompting us to control for the firm’s leverage ratio (Lev). Moreover, firms experiencing poor performance are more likely to engage in earnings manipulation to conceal underperformance, leading us to include return on assets (ROA) as a control. From a corporate governance standpoint, board characteristics significantly influence a company’s propensity for earnings manipulation. For instance, the size of the board (Board) can affect its supervisory effectiveness, thereby impacting earnings management practices (Jensen & Meckling, 1976). Similarly, the proportion of independent directors (Indep) and the ownership stake of the largest shareholder (TOP1) may affect the detection and prevention of earnings manipulation (Chen et al., 2015; Gong et al., 2021; Klein, 2002). Furthermore, we consider the type of ownership (SOE), as state ownership can influence financial behavior (B. Liu et al., 2018). CEO characteristics also play a role; for example, overseas experience (CeoOversea) may lead to higher voluntary disclosure and lower incentives for earnings manipulation through informed cross-border investment decisions (Hao et al., 2021). Additionally, CEOs with financial expertise (CeoCw) possess specialized knowledge and experiences that shape financial decisions (Custódio & Metzger, 2014).

Second, we examine host country-level factors. Higher levels of rule of law and regulatory quality in the host country may suppress a company’s motivation for earnings manipulation (Almadi & Lazic, 2016). Conversely, the geographic distance between foreign subsidiaries and headquarters can hinder auditors’ ability to access subsidiary information, thereby reducing the likelihood of detecting opportunistic earnings manipulation (Choi et al., 2012). To address these aspects, we control for regulatory quality (RQ), rule of law (RL), and geographic distance (Distance). Additionally, host-country risks—such as political, economic, or financial risks—may incentivize earnings manipulation due to increased earnings volatility (Enomoto et al., 2018). Therefore, we control for host country risk (CR) in our overseas operations by adopting Liu et al. (2020) methodology, which involves calculating the weighted sum of the ICRG country composite risk indices for all host countries where company i has overseas subsidiaries. The weights are assigned either equally or based on the number of subsidiaries in each country. Subsequently, we apply a linear transformation: CR = 1 − ( CR÷ 100). This ensures that the magnitude of risk is consistent with the direction of the variable’s values.

Third, we control for subsidiary-level factors. The lifespan of a subsidiary (SubsidyLife) can indicate greater host-country experience and familiarity with institutional environments, potentially facilitating earnings manipulation.

Fourth, we account for auditor and partner characteristics. Audits conducted by Big Four firms (Big4) may enhance audit quality and deter firms from manipulating earnings (DeFond & Jiambalvo, 1993). Changes in auditor partners (PartnerChange) may improve independence but reduce client familiarity, thereby affecting audit quality (Arthur et al., 2017; Daugherty et al., 2012). Additionally, prolonged partner tenure (PartnerTenure) may degrade audit quality over time (Carey & Simnett, 2006). Consequently, we include both partner turnover and tenure as control variables. We also control for the fixed effects of firm and year. The definition and measurement of the variables used in this study are detailed in Table 1.

Theoretical framework.

Definition and Measurement of the Variables.

Empirical Analysis

Descriptive Statistics

Table 2 presents the descriptive statistics for the main variables. The mean value of DAC, which represents MNEs’ earnings manipulation, is 0.051, with a median of 0.037. This indicates considerable variation in the extent of earnings manipulation across these firms. The mean value of RP, measuring auditors’ host-country risk perception, is 0.007, accompanied by a 25th percentile of 0.003 and a 75th percentile of 0.010, demonstrating moderate variability in risk perception among firms. Abnormal audit fees (AudFee) have a mean of 0.055 and a median of 0.035, suggesting differences in audit fee anomalies across the companies studied. Audit delay (lnDelay) shows a mean of 4.630 and a median of 4.654, reflecting typical delays in the audit process. Regarding the control variables, the 75th percentile of SOE is 0.000, indicating that the majority of firms are non-state-owned enterprises. Both CeoOversea and CeoCw have 75th percentile values of 1.000, implying that most CEOs possess overseas experience and financial expertise. The standard deviations of RL and RQ are 0.678 and 0.697, respectively, highlighting significant heterogeneity in the host countries’ rule of law and regulatory quality. Additionally, the 75th percentile of PartnerChange is 0.000, signaling that changes in audit partners are infrequent. The distributions of all other control variables remain within reasonable ranges, ensuring no extreme values that could potentially skew the analysis.

Descriptive Statistics.

Regression Analysis

Table 3 presents the baseline regression results examining the relationship between RP and corporate earnings manipulation. Column (1) analyzes the impact of RP on earnings manipulation while controlling for firm and year fixed effects, but excluding other control variables. Column (2) extends the analysis by including additional control variables alongside firm and year fixed effects. The results demonstrate that the regression coefficients for RP are consistently and significantly negative in both models. This suggests that RP inhibits firms from engaging in earnings manipulation, thereby validating Hypothesis 1.

Results of Baseline Regression.

Note. T-values are presented in parentheses.

and *** Indicate significance at the 10% and 1% levels, respectively.

Robustness Tests

Sample Matching Method Test

This study may be subject to sample self-selection issues, potentially introducing endogeneity in the causal relationship between RP and MNEs’ earnings manipulation. To address this concern, we first employ propensity score matching (PSM) to pair samples and mitigate the impact of observable differences between groups. Specifically, firms with RP above the industry median are classified as the treatment group, while the remaining firms constitute the control group. Using covariates such as Lev, Size, and ROA from earlier sections as matching variables, we apply a 1:1 nearest neighbor matching method. Additionally, Mahalanobis distance matching is utilized to account for correlations between covariates and eliminate scale effects. Furthermore, entropy balancing is adopted to reduce potential biases arising from the subjective design inherent in propensity score matching. Columns (1)–(3) in Table 4 present the results after implementing these three matching approaches. The coefficients of RP remain significantly positive across all specifications, indicating that the inhibitory effect of RP on MNEs’ earnings manipulation is robust. These findings support our hypothesis.

Matched Sample Analyses.

Note. T-values are presented in parentheses.

Indicate significance at the 1% levels, respectively.

Instrumental Variable Approach

To mitigate potential endogeneity issues that might affect the research conclusions, we employ an instrumental variable approach to re-estimate the regression results. We use the average RP of auditors from other firms in the same industry and year as the instrumental variable for RP (Ind_RP). We argue that this variable meets the requirements of relevance and exogeneity. From a relevance perspective, firms within the same industry encounter similar industry characteristics and external environments, which leads to a correlation in their RPs. Additionally, there is no evidence to suggest that RP from other firms in the same industry influence the earnings manipulation behavior of the MNE in question, thereby satisfying the exogeneity condition. As shown in Column (2) of Table 5, after controlling for endogeneity, RP remains significantly negatively correlated with MNEs’ earnings manipulation. This finding aligns with the expectations outlined in Hypothesis 1.

Results of Instrumental Variable Regression Results.

Note. T-values are presented in parentheses.

Indicate significance at the 1% level. The regression is adjusted for heteroscedasticity and cluster-adjusted by firm-level.

Using Tax Haven Samples

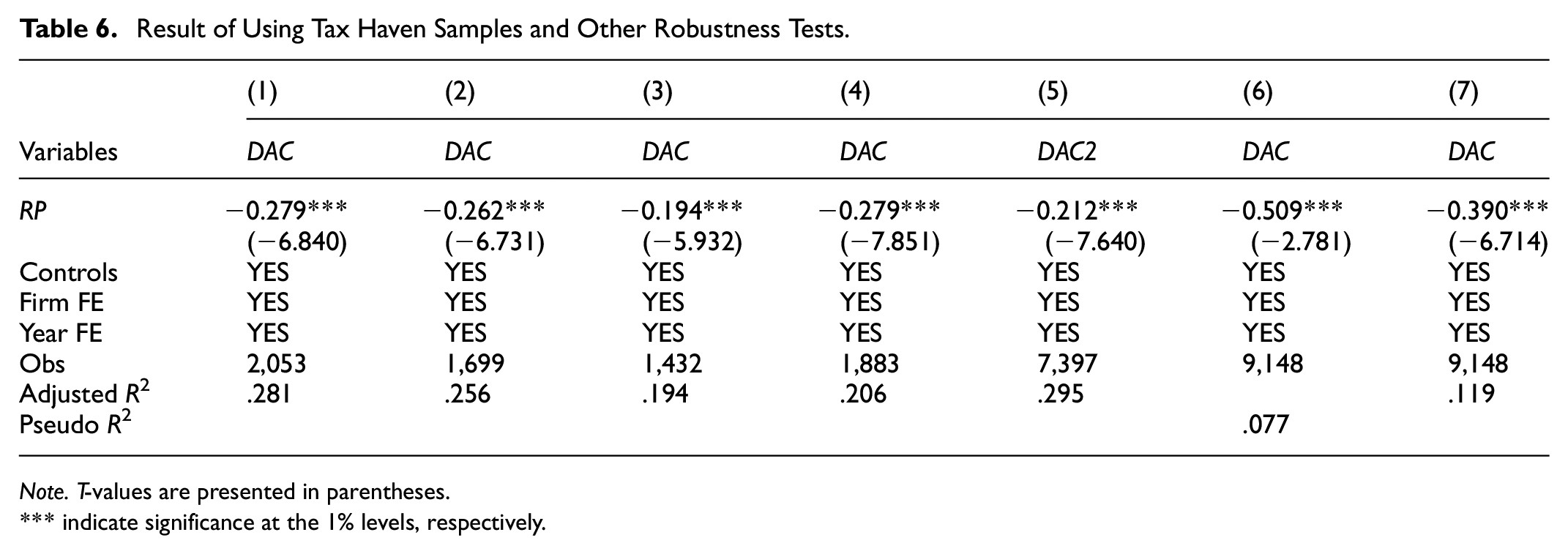

Tax havens, such as the Cayman Islands, Bermuda, and Ireland, typically offer extremely low or zero tax rates. MNEs can take advantage of these favorable conditions by transferring profits from high-tax regions to subsidiaries in tax havens. This strategy reduces their overall tax burden and increases corporate cash flow (Hines & Rice, 1994). However, making direct investments in tax havens also heightens the risk of insider expropriation (Atwood & Lewellen, 2019). Subsidiaries in tax havens that hold large amounts of funds provide management with significant capital that could be used to misappropriate company assets. Furthermore, the lower financial transparency requirements in tax havens make it easier for companies to obscure the true distribution of profits and the flow of funds, facilitating more flexible manipulation of financial data. Therefore, we use a sample of outward direct investments in tax havens for analysis. Currently, there are three widely recognized lists of tax havens in academic research: the first is the list published by the Organization for Economic Co-operation and Development (OECD); the second is the list identified in the U.S. “Stop Tax Haven Abuse Act”; and the third is the list utilized by Hines (2010) in his research. This study identifies sample firms with direct investment in jurisdictions appearing on any one of the three widely recognized tax haven lists, yielding a final subsample of 907 unique firms, corresponding to 2,053 firm-year observations. The results, presented in Column (1) of Table 6, indicate that the regression coefficient for RP is significantly negative. Additionally, we conduct regression analyses using each of the three lists of tax havens mentioned above, and the results remain consistently negative and statistically significant. This finding suggests that RP can effectively curb earnings manipulation by companies operating in tax havens.

Result of Using Tax Haven Samples and Other Robustness Tests.

Note. T-values are presented in parentheses.

indicate significance at the 1% levels, respectively.

Other Robustness Tests

In the preceding analysis, the modified Jones model was used to measure earnings manipulation. To ensure the robustness of the results, this study also employs the nonlinear accrual model developed by Ball and Shivakumar (2006) to calculate earnings manipulation (DAC2) for multinational corporations. The regression results shown in Column (2) of Table 6 reveal that the coefficient for RP is −0.212, which is significant at the 1% level. This finding confirms that the results remain consistent even when using an alternative method to measure earnings manipulation.

We also evaluated the sensitivity of our research conclusions to extreme values in the data. In Column (3) of Table 6, we present results from median regression, which is robust to outliers. The coefficient for RP remains significantly negative at the 1% level in relation to corporate earnings manipulation. This indicates that our findings are not influenced by outliers.

Additionally, following Petersen (2009), we adjusted the standard errors by double clustering on both individual and time dimensions to address potential autocorrelation and heteroskedasticity in our statistical inferences. To ensure the robustness of our conclusions, we employed double-clustered standard errors for the t-tests. The regression results in Column (4) of Table 6 continue to support our initial research conclusions.

Mechanism Analysis

RP, Abnormal Audit Fees and Corporate Earnings Manipulation

Based on the theoretical analysis above, we infer that when auditors perceive a higher level of transnational risk faced by a company, cautious auditors may increase abnormal audit fees. This increase serves to transfer potential risks and compensate for possible future direct or indirect losses, thereby discouraging corporate earnings manipulation. To test this hypothesis, we adopt the classic audit pricing model developed by Simunic (1980). We estimate normal audit fees by considering factors such as the size of listed companies, audit complexity, audit risk, and auditor characteristics (Hribar et al., 2014). Abnormal audit fees (Audfee) are calculated as the difference between the actual audit fees for a given year and the estimated normal fees, representing the risk premium. Column (1) of Table 7 presents the relationship between the RP, abnormal audit fees, and corporate earnings manipulation. The interaction term RP×Auditfee has a significantly negative coefficient, indicating that RP leads to increased audit fees, which effectively suppresses corporate earnings manipulation.

Results of Mechanism Tests.

Note. T-values are presented in parentheses.

, and *** indicate significance at the 10%, 5%, and 1% levels, respectively.

RP, Audit Delay and Corporate Earnings Manipulation

Additionally, RP may lead to longer audit durations. When auditors identify high risks associated with a company’s multinational investments, they may increase their work effort—either proactively or reactively—due to risk aversion and the additional workload from overseas audit projects. This heightened effort extends the audit timeframe, thereby mitigating potential legal liabilities and economic losses. To measure audit delay, we draw on Hammami et al. (2020) and use the natural logarithm of the number of calendar days plus one between the balance sheet date and the audit report date (lnDelay). Column (2) of Table 7 presents the effect of RP on audit delay. The coefficient for the interaction term RP×Delay is significantly negative, indicating that higher RP is associated with longer audit durations. This increase in audit time contributes to the suppression of corporate earnings manipulation.

Heterogeneity Analysis

Analysis From the Perspective of Auditors’ Multinational Expertise

Auditors’ multinational expertise is demonstrated through the professional skills they develop from extensive cross-border auditing experience. This international exposure allows them to accurately identify variations in accounting systems and operational risks in host countries. Moreover, it equips them to effectively mitigate MNEs’ earnings manipulation through innovative strategies, such as modular audit process design and real-time communication systems. This professional edge is derived not only from a thorough understanding of diverse accounting standards and legal frameworks across different countries but also from the ability to apply theoretical knowledge to create systematic risk prevention and control measures. As a result, we hypothesize that auditors with multinational expertise are better positioned to significantly curb corporate earnings manipulation due to their enhanced perception of host-country risks. To test this hypothesis, our study adopts methodologies from Gunn and Michas (2018) and J. H. Liu and Yu (2022). We begin by analyzing a sample of MNEs’ overseas subsidiaries, identifying the host countries based on their operational locations. We then count the number of these subsidiaries audited by each firm, categorized by year and country. If auditing firm i has audited the highest number of subsidiaries in country j during year t, demonstrating the greatest level of experience, it is classified as having audit expertise (XPT) for that specific country-year. If not, the firm is considered to lack country-specific audit expertise (Non-XPT). The empirical findings, presented in Columns (1) and (2) of Table 8, show a significantly negative coefficient of −0.597 (p < .01) for auditors with multinational expertise, while the coefficient for the Non-XPT group is statistically insignificant. These results confirm that auditors with multinational expertise have a significant inhibitory effect on earnings manipulation due to their heightened perception of host-country risks.

Results of Heterogeneity Analysis.

Note.T-values are presented in parentheses.

, **, and *** Indicate significance at the 10%, 5%, and 1% levels, respectively. The p-value for the coefficient difference is calculated from the Suest test model’s estimated results.

Analysis From the Perspective of Rule of Law

The strength of a country’s rule of law serves as a critical external governance mechanism that helps prevent corporate earnings manipulation in two key ways: by improving regulatory effectiveness and by enhancing punitive deterrence. In nations with strong legal systems, efficient enforcement mechanisms can accurately identify and severely punish financial manipulations. In contrast, regions with weaker legal frameworks often experience regulatory failures due to institutional deficiencies and opportunities for corruption. As a result, the ability of auditors to perceive risks in host countries becomes particularly valuable in areas with weaker legal systems, as they can compensate for the shortcomings of formal institutions through additional monitoring mechanisms. This study employs the Rule of Law (RL) indicator from the Worldwide Governance Indicators (WGI) database to evaluate the legal system development in host countries. The RL scores range from −2.5 to 2.5, with higher scores reflecting more developed legal systems and a stronger rule of law. A country is considered to have a high level of rule of law (High-Law) if its score is above the industry median; otherwise, it is classified as having a low level of rule of law (Low-Law). The findings in Table 8 reveal that for firms operating in countries with a high level of rule of law (Column 3), the coefficient of RP is −0.428 and statistically significant at the 10% level. For firms in countries with a low level of rule of law (Column 4), the coefficient of RP is −0.455 and significant at the 5% level. Bootstrap tests confirm that the differences between these groups are statistically significant. These results suggest that RP effectively mitigates institutional weaknesses in regions with weaker rule of law, resulting in a more substantial governance impact on MNEs’ earnings manipulation.

Analysis From the Perspective of Geographical Distance

The geographical proximity between auditors and their clients grants an informational advantage, facilitating the detection of earnings manipulation and bolstering regulatory effectiveness. However, the geographical distance between MNEs’ foreign subsidiaries and their home country creates an information barrier, diminishing auditors’ ability to monitor opportunistic earnings manipulation abroad. To address this regulatory blind spot, we propose that in the subsample where foreign subsidiaries are geographically distant from the home country, auditors’ non-geographical information channels, built through their risk perception capabilities in host countries, will play a more significant governance role. This difference in capabilities is crucial for resolving the “distance paradox” and upholding audit quality. The French CEPII database provides measurements of geographical distances between national capitals. Using this data, we calculated the average distance from Beijing to the capitals of the host countries where each subsidiary is located. We then categorized these distances into high and low groups, using the median as the dividing line. The regression results in Table 8 show that for the high geographical distance group (High-Distance) in Column 5, the coefficient of RP is −0.514 and statistically significant at the 5% level. In contrast, for the low geographical distance group (Low-Distance) in Column 6, the coefficient of RP is −0.346 and significant at the 10% level. Bootstrap tests confirm that the differences between these groups are significant, indicating that the inhibitory effect of RP on earnings manipulation strengthens as geographical distance increases. These findings suggest that when geographical distance heightens information asymmetry, RP have a more pronounced governance value in curbing MNEs’ earnings manipulation.

Analysis From the Perspective of State Ownership

SOEs are pivotal to China’s economy, yet their distinctive ownership structure diminishes the incentive for management to engage in profit maximization through financial manipulation. Moreover, oversight and auditing by government bodies and the State-owned Assets Supervision and Administration Commission (SASAC) further complicate attempts at earnings manipulation.

This study examines the earnings manipulation practices of SOEs and non-SOEs to understand how RP affect earnings manipulation across different types of ownership. The empirical findings, detailed in Table 8, reveal that in Column (7), the impact of RP on earnings manipulation in state-owned MNEs is measured at a coefficient of −0.119, which is not statistically significant. Conversely, in Column (8), the coefficient for non-state-owned MNEs stands at −0.498, indicating a significant effect at the 1% level. Further analysis through inter-group difference tests underscores the significance of the findings for non-SOEs, confirming that RP more effectively curb earnings manipulation in non-state-owned MNEs.

Conclusions and Policy Recommendations

This study examines the mechanism and impact of RP on MNEs’ earnings manipulation in cross-border auditing, using a sample of China’s A-share listed MNEs from 2017 to 2023. Leveraging textual features from the KAMs sections in audit reports, we innovatively construct a risk perception indicator for auditors and systematically analyze its governance effects. Empirical results demonstrate that RP significantly suppresses earnings manipulation activities in MNEs. To address potential endogeneity concerns, robustness tests—including sample matching, instrumental variable approaches, and subsample analyses focusing on tax havens—consistently validate our findings. Mechanism tests reveal that auditors reduce the scope for earnings manipulation through dual pathways: increasing audit fees and extending audit timelines. Heterogeneity analysis further highlights that the governance efficacy of RP is more pronounced in the following contexts: when auditors possess multinational expertise, when subsidiaries operate in host countries with weaker rule of law, when subsidiaries are geographically distant from the home country, and when enterprises are non-state-owned. The theoretical contribution of this study lies in transcending traditional paradigms of cross-border audit governance research, demonstrating that RP serves as a critical complement to informal governance mechanisms. Practically, our findings provide policy insights for optimizing audit regulatory frameworks in emerging markets and curbing financial fraud in MNEs.

Although our study focuses on China’s A-share market, its findings have significant implications for global transnational audit regulatory systems. The inhibitory effect of RP on earnings manipulation arises from the pervasive information asymmetry and regulatory arbitrage opportunities inherent in cross-border auditing—a theoretical framework that is likely applicable across various jurisdictions. While differences in regulatory frameworks, such as the EU’s audit directive coordination mechanisms and the U.S. cross-border review system, may influence the pathways and intensity of RP, the behavioral paradigm of professional audit institutions—leveraging textual analysis to capture risk signals and enhance audit quality—holds transnational relevance. Particularly within the context of emerging markets’ audit cooperation and cross-border regulatory practices under initiatives like the Belt and Road, the RP indicator system and dual mechanisms proposed in our study can provide theoretical support for developing an informal governance coordination framework.

Based on the research findings, we propose the following recommendations:

First, China’s risk-oriented audit model should be optimized. Auditors should incorporate host-country risk perception into audit procedures to reduce audit failures and curb MNEs’ earnings manipulation. Second, it is recommended that accounting firms optimize the layout of their transnational audit services, prioritize cultivating and developing specialized expertise in cross-border auditing, and engage auditors with transnational proficiency to offer differentiated service portfolios to enterprises. These measures will enhance their oversight and governance efficacy. Third, given the influence of diverse risk factors, audit firms should prioritize scrutiny of non-state-owned MNEs operating in regions with weaker rule of law or located farther from China. Auditors should conduct more thorough assessments of the host-country environments for such enterprises to mitigate jurisdiction-specific risks. The last but not the least, in the context of capital market liberalization and the Belt and Road Initiative, it is crucial for relevant government authorities to promptly disclose all information related to host-country risks. They should ensure that this information is comprehensively and timely disseminated, and they must establish supportive policies. These actions will strengthen the government’s capacity to regulate MNEs through effective auditing mechanisms.

Limitations and Future Research

The interpretation of our results should consider measurement limitations. While our text-based measure of RP represents a significant advancement by capturing manifestations of such perception within standardized audit reports (specifically, the KAMs disclosures), it is important to acknowledge a key limitation. The RP variable, derived from disclosed KAMs, primarily reflects the outcome of auditors’ risk assessment process that they deemed material and worthy of communication. It may not fully encapsulate the entirety of auditors’ subjective judgment and internal risk evaluation processes, including nuances of risk severity weighting or concerns considered but ultimately not disclosed in the KAM section. Future research could address this limitation by employing alternative methodologies, such as in-depth interviews with audit partners or large-scale surveys of audit practitioners. These approaches could provide deeper insights into the formation and drivers of auditors’ risk perceptions in multinational contexts, complementing the objective indicators captured by textual analysis.

Footnotes

Acknowledgements

We are gratefully to the financial support from Sichuan International Studies University.

Ethical Considerations

This article does not contain any studies with human or animal participants.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Sichuan International Studies University under Grant [SISU202310].

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

Data can be provided upon request.