Abstract

The purpose of this study is to examine the relationship between top management school-ties represented by the CEO (Chief Executive Officer), CFO (Chief Financial Officer), and the Auditor with the Audit Fee. This study uses 627 observations from companies listed on the Indonesia Stock Exchange from 2010 to 2018 and uses the Ordinary Least Square Regression analysis model. This study finds that the combination of school-ties between CFO and Auditor showed a positive relationship with Audit Fee, while the combination of school-ties between CEO and Auditor did not. This study contributes to literature related to the relationship between school-ties and audit fees of public companies in Indonesia. It is also hoped that it can contribute to the implementation of company policies, management, external parties, named regulators, and investors. This study chose school-ties as a part of social-ties to represent the condition of Top company officers and Auditors ties.

Introduction

Independence expressly stated precludes bias against the audit results in favor of the interests of their clients (Moore et al., 2006). The case experienced by most auditors is that they are always trapped and found to be involved with the company management’s interest in order of collusion, corruption, and certain fraud (Levitt & Dwyer, 2002). The reason is that auditors tend to minimalize on giving negative audit opinions to managers who employ them and pay their audit fees. Research conducted by Beck et al. (1988), Deis and Giroux (1992), Mautz and Sharaf (1961) believed that audit quality will worsen when there is a relationship between the auditor and the client. Guan et al. (2014) assured that the relationship between executives and auditors will open up new problems related to audit quality, accrual discretionary, and paid audit fees.

Recently research on tests conducted by J. R. Cohen et al. (2022) states that personal ties and/or professional ties between the CEO and audit committee members can potentially impair members’ objectivity. These results of course makes “ties” an important issue to be considered further. Research conducted by Kwon and Yi (2018) in Korea states that CEO-EP school ties are associated with high-quality audits and audit fee premiums. Recent research also shows the importance of ties and states that audit firm alma mater ties between the auditor and the audit committee (AC) are associated with significantly greater non-audit services (NAS) (Sharma et al., 2022). This new evidence shows how significant “ties” impact to the audit outcomes.

Guan et al. (2016) determined social ties that can arise due to various kinds of similar backgrounds, one of the strongest is being in the same school alma mater (school-ties). In Korea, the similarity of school alma mater plays an important role in building social relations (Chang et al., 2017). Several previous studies from C. Lennox (2005), C. S. Lennox and Park (2007), Menon and Williams (2004), Naiker and Sharma (2009) convinced that the similarity of the school alma mater bonds will be a very accurate measure in examining the relationship in every matter and decisions made by company management and their external parties. This research predicts that there are school-ties between top management (CEO and CFO) and auditors will have implications for the audit fee.

Accurate school testing related to high audit fees is an interesting thing because there are not many studies that have conducted testing. For example, research on school-ties among executives, recently conducted by Guan et al. (2016) stated that it can damage the quality of the audit which is proxied by audit fees, He et al. (2017), Johansen and Pettersson (2013) stated that the school-ties between the audit committee and the auditors are associated with an increase in audit costs and provide fewer benefits. In 2022, literature is limited, even though psychological studies on the relationship between auditor and client attract attention, ties in education still need evidence. We believe individual characteristic involving the psychological domain will offer more explanation. As Fang et al. (2022) individual characteristics attached to the external social network involved in their behavior and decisions, in a relationship influence or influenced. More specifically, the selection of school-ties variables is made one to one relation that are a relationship between the CEO with the Auditor and the CFO with the different Auditors from Guan et al. (2016) who chose many to one relation to representing the phenomenon of top management and auditors. Indonesian characteristics, attach a pattern of strong connections in relational business connections, for example politics that has strengthened since the New Order era (Harymawan & Nowland, 2016) or family businesses that have formed conglomerate empires (Harymawan et al., 2020). Therefore, analyzing connections from educational background might provide a new picture, is the almamater relationship valid amidst the relational characteristics offered by Indonesia?

Auditors who have school-ties relationships are believed to provide higher audit fees, with a tendency for a better audit opinion even when the company is under financial pressure. Like Davis et al. (1993), Francis (1984), Francis and Simon (1987), Simunic (1980) in their research, an increase in audit fees is positively related to auditors who provide modified audit results. As a result, auditor independence is damaged (Francis & Ke, 2006; Khurana & Raman, 2006; Krishnamurthy et al., 2006). The provision of high audit fees will always be associated with relatively low litigation risk so that auditors can compromise their independence (Piotroski & Wong, 2012), as well as support and career guarantees for auditors from management (M. L. DeFond et al., 2000; Wang et al., 2008). The positive assumption, it is not because of modification, but because of persistence in audit work, their audit quality that leads to higher audit fees (Koehn & Del Vecchio, 2004; Whisenant et al., 2003)

However, in the case of low audit fees, it is an inevitability because auditors consider their audit risk costs. This means that auditors may not receive an audit fee lower than the risk they take. Using the theory of social reciprocity, the high audit fees when school-ties are formed between the executive and the auditor are more explainable than the lower audit fees (Batson et al., 1981; Caliendo et al., 2012; Cialdini et al., 1987; Fehr & Gächter, 2000). Besides, there is still a tendency to maintain the auditor’s reputation as an independent auditor while at the same time trying to retain their big clients in the future by receiving lower audit fees. Theoretical and empirical research from Watts and Zimmerman (1983); Z. V. Palmrose (1988); J. Krishnan and Krishnan (1997) explained that there is still a high concern about reputation and litigation costs for auditors so that auditors keep trying to maintain their independence.

The purpose of this study is to examine the relationship between the similarities in the educational background (school-ties) that was built between top management (CEO, CFO) and company auditors to the audit fees paid by the company to their chosen auditors. This study used 769 samples of public companies listed on the Indonesia Stock Exchange from 2010 to 2018. Data processing was done to test the relationship of the dummy school-ties variable between the CEO, CFO, and Auditor on the audit fee using STATA 14.0 software Regression OLS. This test is also convinced by using a regression analysis of the school-ties interaction results with the control variable so that it can explain in detail the results of the interpretation of the sample data used.

The results of this study indicate that the school-ties which exist between the CEO and the Auditor have no relationship with their audit fees, but the school-ties that exist between the CFO and the Auditor increase their audit fees. Interestingly, the school-ties that exist between the CFO and the auditor relating to audit fees do not happen in the characteristics tested in the interaction regression of this study. In short, school-ties that exist between CFO and Auditor and related to audit fees indicate collusion, corruption, and certain fraud (Levitt & Dwyer, 2002) which undermine their independence (Francis & Ke, 2006; Khurana & Raman, 2006; Krishnamurthy et al., 2006); J. Krishnan et al., 2005) as explained closely related to the modification of audit results and their audit quality (Guan et al., 2016).

Furthermore, this research will be structured as follows: section 2 contains an explanation of the literature review; section 3 contains an explanation of the research methodology; section 4 contains the results and discussion, and section 5 contains conclusions and suggestions.

Literature Review

Social Reciprocity Theory

Social Reciprocity Theory refers to the social psychology of human behavior and actions. As a social construction, reciprocity theory is built to respond to the various actions of “revenging” equally, which might be much better and more cooperative than the interest model. On the other hand, revenge is much eviler and more brutal (Caliendo et al., 2012; Fehr & Gächter, 2000).

Reciprocal action focuses on the initial actions of the other person so that the “expectations” of the other person’s actions will influence subsequent actions (Batson et al., 1981; Cialdini et al., 1987). Strong reciprocity has the power to trigger feelings of “debt of gratitude” even when being faced with uninvited help (Paese & Gilin, 2000) and regardless of liking the executor of the action (Regan, 1971).

Reciprocity is closely related to moral, generosity that goes beyond the significant amount determined and predicted by conventional, economic models of rational self-interest. The reasons above, make a social dilemma (a situation where the incentives of groups and individuals conflict) which is controlled by the existence of social, economic, or physical sanctions and including the economic punishment experiments (J. Carpenter & Matthews, 2004; Fehr & Gächter, 2000; Henrich et al., 2001; Masclet et al., 2003; Myers et al., 2003; Sefton et al., 2007; Walker et al., 2002).

In reciprocity, there is a phenomenon that can form a pattern of “reciprocating,”“debt of gratitude,”“moral” as based on cultural groups (Cavalli-Sforza & Feldman, 1981; Henrich et al., 2001). This cultural choice and commonality lead to decisions about trust, cooperation, and all the context implied (J. P. Carpenter et al., 2004). School, for example, continues to reciprocate the past because the wants to reciprocate events for past behavior and actions in a sustainable form. As for the last, accounting and money accounts are used to falsify measures of value and economic equity in reciprocity (Carmona et al., 2002). Through this theory, we perceive that school-ties that occur between two individuals can be established from the similarity of the alma mater. Moreover, this is included in the issue of ties between top company officers and auditors, who are in key positions in an engagement.

Audit Fee

Audit fee reflects the business risk of the company which is being audited, but some auditors state that business risk is not explicitly considered in determining audit fees because it cannot be measured (Morgan & Stocken, 1998). Several studies on audit fees have found that an increase in the cost of audit services is positively related to auditors who provide modified audit reports (Davis et al., 1993; Francis, 1984; Francis & Simon, 1987; Geiger & Raghunandan, 2001; Geiger & Rama, 2003; Simunic, 1980) relatively low risk of litigation so that auditors can compromise their independence (Piotroski & Wong, 2012). Besides, high audit fees can occur due to persistence in audit work and audit quality (Koehn & Del Vecchio, 2004; Whisenant et al., 2003) as happened after SOX 404. However, low audit fees are explained in the research of Watts and Zimmerman (1983); Z. V. Palmrose (1988); J. Krishnan and Krishnan (1997) stated that auditors have concerns about their reputation, so auditors still try to maintain their independence.

Similarities in the Background of the School Almamater (School-Ties)

Guan et al. (2016) define that social-ties can arise due to various kinds of similar backgrounds, one of the strongest is the similarity in the background of the school alma mater (school-ties). In Korea, the existence of school equality plays an important role in building social relations (Chang et al., 2017). In previous research, it was found that the director’s perspective was influenced by the existence of school-ties (L. Cohen et al., 2008, 2010; Engelberg et al., 2012, 2013; Phan et al., 2003; Sarkar & Sarkar, 2009; Yermack, 2004).

The advantage of school-ties is that they provide benefits in terms of interactive and audit negotiations and are related to policies taken by top management with auditors. An experience in one school address becomes a valuable source of social interaction that will form closeness and create a common way of thinking, emotions and build comfort for having similar experiences and characteristics (McPherson et al., 2001). The long-term effect is achieving decisions, easily accessing or transferring information, (Granovetter, 2005) and also doing better in decision making (Kalmijn & Flap, 2001), including in their managerial abilities, risk preferences, personality traits, and incentives, making it possible to evaluate audit risk better, and increasing their confidence (Silver, 1990).

C. Lennox (2005); C. S. Lennox and Park (2007), Menon and Williams (2004), Naiker and Sharma (2009) convinced that school-ties will be an accurate measurement in testing their effect on every matter and decisions made by company management, both in audit arrangements and in building cooperation (Massa & Simonov, 2011). On the contrary, the same social background will lead to weak independence from the company board (Kim & Aldrich, 2005). This is very possible because there are interests that will suppress transparency and accountability of their own decision making, for example, is the activity of hiding their opportunistic behavior (Chun et al., 2013), abusing social connections to exercise rights, and abusing their power (Dawson et al., 2000).

Hypothesis Development

In this study, school-ties focused on top management positions represented by two different pioneers, the CEO (Chief Executive Officer) and CFO (Chief Financial Officer) in making corporate strategic decisions. The CEO as the owner of the highest position in the company can involve the CFO in accounting manipulative actions to meet or beat market expectations (Feng et al., 2011). Thus, even though the CEO is not directly involved in preparing the financial statements, the CEO can easily give his orders to the CFO. Besides, the compliant CFO will give judgment in the decision to select auditors to smoothen their objectives. Both the CEO and the CFO will be interested in working with the auditors based on social ties and repeat the beneficial cooperation process in their earnings management. G. V. Krishnan et al. (2011) documented the positive influence of social-ties formed on earnings management in the period before and after SOX. Referring to Guan et al. (2016)school-ties are defined as the similarity in the background of a school or college alma mater, both at the same and different periods, both at undergraduate, postgraduate, or doctoral levels, also not limited to the study program being taught. Therefore, hypothesis 1a and hypothesis 1b in this study was made to test the specific and objective results of the school-ties relationship between each top management, that were the CEO and CFO, and the auditors on the audit fee.

H1a: School-ties between CEO and Auditor related to Audit Fee.

H1b: School-ties between CFO and Auditor related to Audit Fee.

From the hypotheses, this study adds analysis, providing identification on the characteristics from the auditor’s side and the company side, which are the BIG4 variable and also the FSIZE variable. The audit firm that is differentiated into Big 4 and Non-Big 4 will provide a special identification where the Big 4 audit firm is believed to be more careful or conservative so that it is profitable for companies with modified financial statements (Francis & Krishnan, 1999) compared to non-Big 4 audit firms. This kind of logic is also built into FSIZE. Thus, the choice of the CFO to cooperate to obtain the security of modified financial statements will be guaranteed, also by providing a higher audit fee (Basioudis & Francis, 2007). However, with the school-ties between CFO and auditors, the choice of using non-Big 4 audit firms is considered easier to be directed in supporting the manipulation of the company’s financial statements because of their lower audit quality (Tee, 2019). Based on the statements, the second hypotheses of this study are:

H2: Audit Firm Big 4 strengthens the School-ties relationship between CFO and Auditor on audit fee

H3: Firm size strengthens the School-ties relationship between CFO and Auditor on audit fee

Balancing with the analysis using auditor characteristics, the third hypothesis of this study is based on firm characteristics. Companies that have above-average subsidiaries or also have above-average leverage will provide control over their subsidiaries. In general, controlling the selection of auditors and with whom they will cooperate, will follow the characteristics of their company (Ismaya & Winarno, 2006). Companies that have more subsidiaries, tend to choose Big 4 auditors who already have a good reputation to keep their assets guaranteed and willing to provide higher audit fees. However, another fact states that companies with above-average subsidiaries do not need to do this, because the auditor’s reputation has been adjusted for audit risk so that it is possible to provide appropriate fees (Brinn et al., 1994). Meanwhile, companies that have leverage above-average, may tend to secure their position to be able to maintain confidence in the results of the audit they get. Therefore, the third hypotheses of this study are

H4: Companies that have above-average subsidiaries strengthens the School-ties relationship between the CFO and the Auditor on the audit fee

H5: Companies that have above-average Leverage strengthens the relationship School-ties between the CFO and the Auditor on the audit fee.

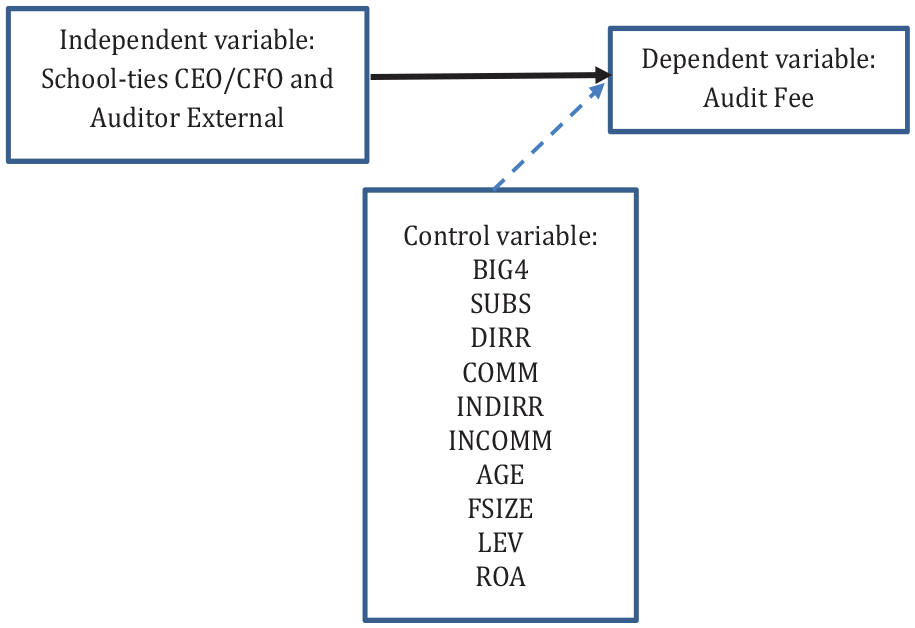

Figure 1 illustrates the research framework used in this study. This study wants to empirically prove the relationship between school-ties top company officers and audit fees, where several control variables control this relationship. For further details, the operational definitions of variables are reported in Table 2.

Research framework.

Sample and Measurement of Key Variable

This study uses secondary research sources from the Annual Report, ORBIS, LinkedIn, Google Scholar, Google, and the KAP Official Website. This study collected data on companies listed on the Indonesia Stock Exchange for the period 2010 to 2018 consist of 627 companies out of4,289 total sample populations. These samples are obtained by eliminating if the company has missing data in one of the variables used. The following is Table 1. Sample Selection Process in this study.

Sample Selection Process.

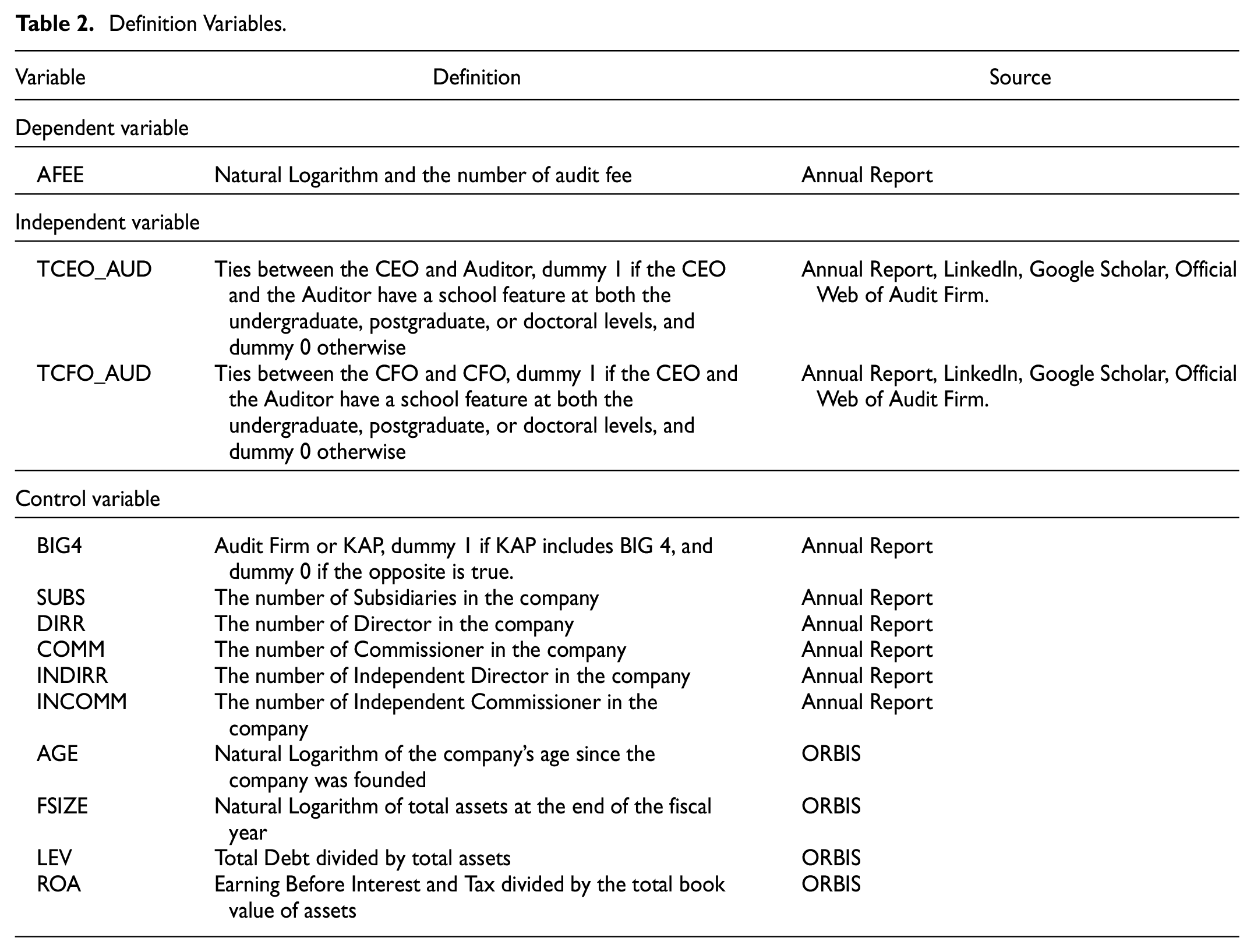

This study uses the Ordinary Least Square (OLS) regression model from STATA 14.0 software to be able to test the relationship between the dependent variable and the independent variable that involves the control variable in it. The selection of control variables is chosen using several bases of previous research, that is the Big Four (BIG4) to determine the characteristics of auditors used by the company. Subsidiaries (SUBS), Firm Size (FSIZE), Leverage (LEV), Age (AGE) were chosen to represent company characteristics, and Return on Asset (ROA) was chosen as the profitability ratio to represent company performance as in Guan’s research, (2016). Number of Directors (DIRR), number of Commissioners (COMM), Independent Directors (INCOMM) to represent the characteristics of Good Corporate Governance, or good corporate governance. For further information, here is Table 2. definitions of variables used in this study.

Definition Variables.

Empirical Result

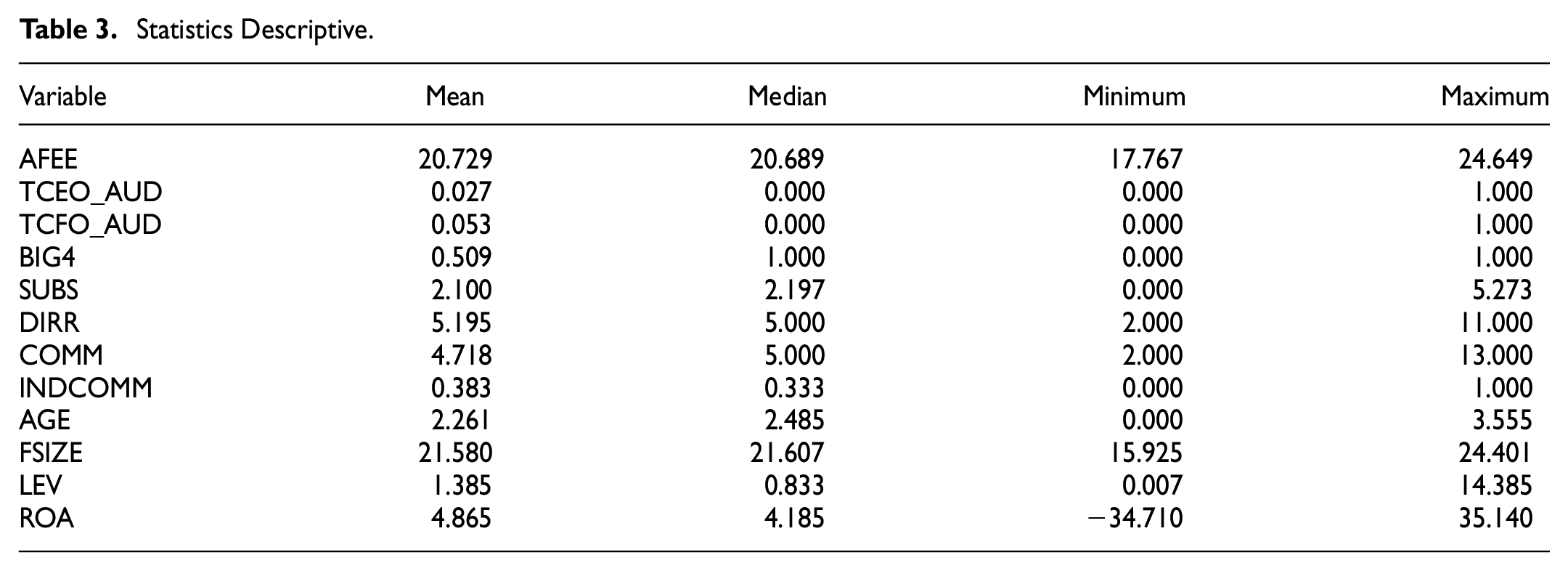

Table 3 shows the descriptive statistics of the total observations, contained with 627 research samples from 2010 to 2018. We can see that the mean of School-ties between CEOs and Auditors is less than companies that have School-ties between CFO and Auditor. This shows that the company tends to be interested in School-ties between CFO and Auditor.

Statistics Descriptive.

Table 4 shows the results of the Pearson correlation between the variables used in this study. The Audit Fee variable was chosen as the dependent variable significantly and positively with BIG4, SUBS, DIRR, COMM, AGE, FSIZE, and ROA. Conversely, AFEE in this correlation matrix does not show significance on the main independent variable in this study.

Pearson Correlation.

Note. p-values in parentheses.

p < .1. **p < .05. ***p < .0.

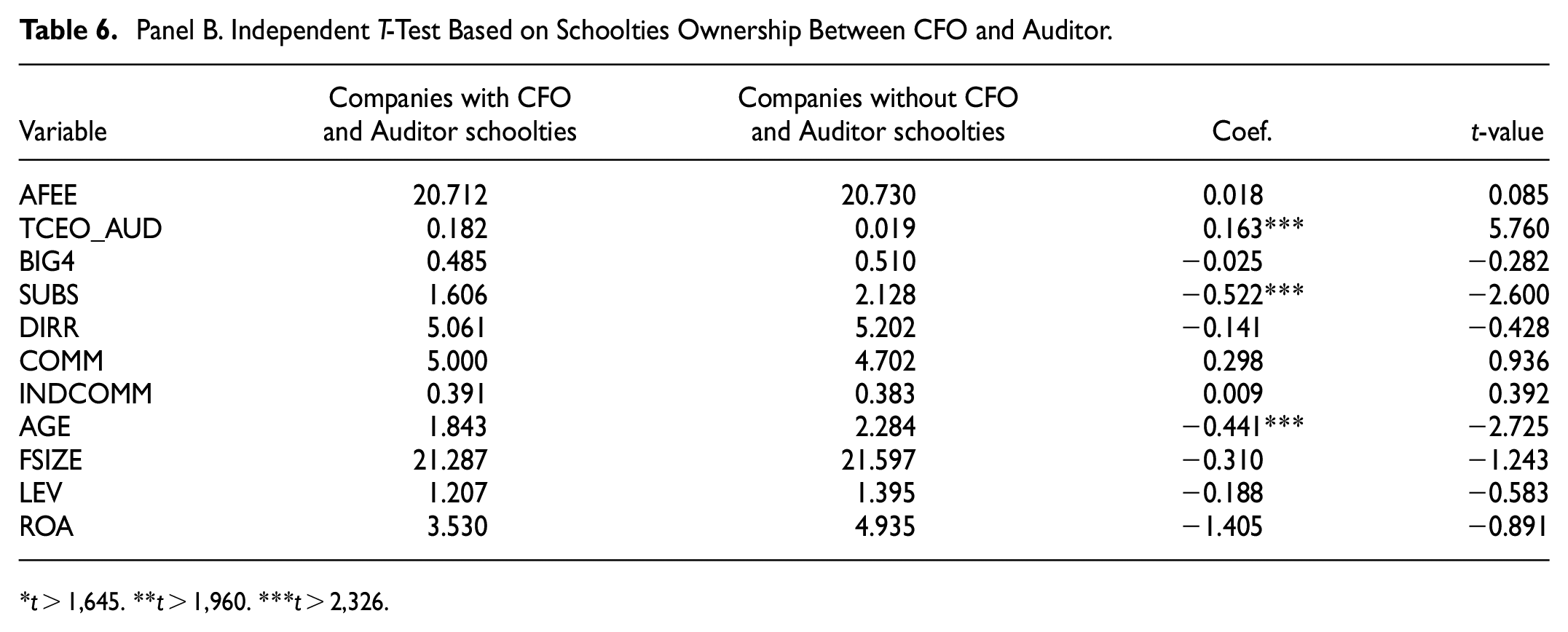

Table 6 Panel B. shows the univariate test of the characteristics of companies that have school-ties between the Top Company Officer, which were the CEO and CFO with the Auditor. This first test focuses on school-ties between the CEO and the Auditor. Interestingly, in the review (TCFO_AUD), companies that have TCEO_AUD show significantly greater value than companies that do not have TCEO_AUD. This means that companies that have school-ties on CEO and Auditor will prefer the school-ties between their CFO and Auditor.

Panel A. Independent T-Test Based on Schoolties Ownership Between CEO and Auditor.

t > 1,645. **t > 1,960. ***t > 2,326.

Panel B. Independent T-Test Based on Schoolties Ownership Between CFO and Auditor.

t > 1,645. **t > 1,960. ***t > 2,326.

In Table 5 Panel A. shows the univariate test of the characteristics of companies that have school-ties between the Top Company Officer, that are the CFO and the Auditor. An interesting finding in this table is that if you look at the TCEO_AUD, companies that have TCFO_AUD show a higher TCEO_AUD value than companies that don’t have TCFO_AUD. This indicates that companies with TCFO_AUD will also tend to have school-ties in it from the CEO_AUD side.

Top Company’s Officer and Auditor School-Ties, Audit Fee

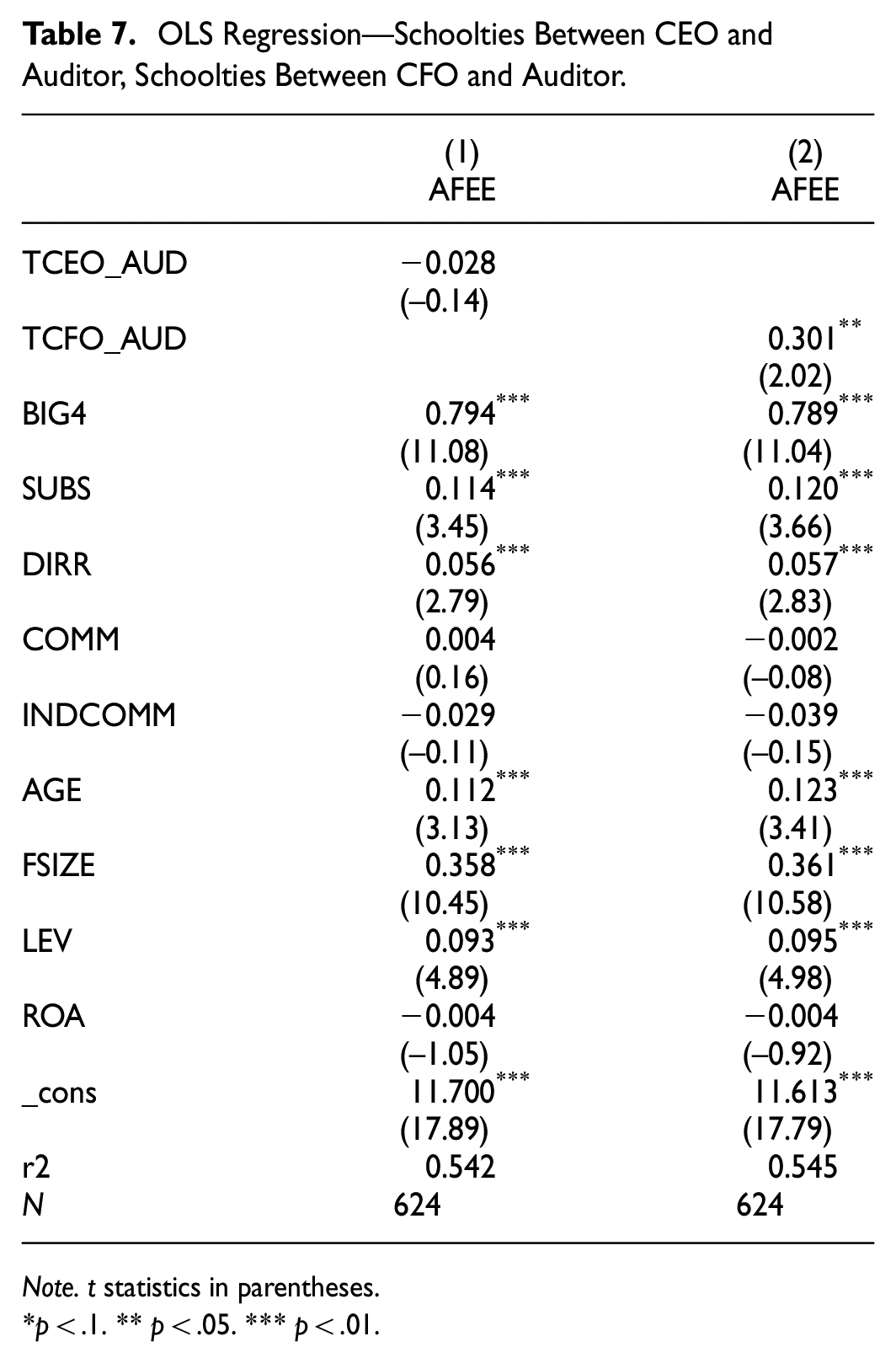

In this section, companies with Top Company’s Officer School-ties have a relation with the audit fee. Specifically, I examined the relation between CEO and Auditors’school-ties with audit fees. To test Hypothesis 1a, I specified a regression model linking dependent variable, test variable, and batteries of control variables as follows:

In Table 7. The regression results of this study indicate a relationship between the independent variable and the dependent variable. The regression results show that hypothesis 1a is rejected because School-ties between CEO and Auditor (TCEO_AUD) do not show any relationship with Audit Fee (AFEE). There is no school-ties relationship between CEO and Auditor (TCEO_AUD) and Audit Fee (AFEE), representing a phenomenon that occurs within the company.

OLS Regression—Schoolties Between CEO and Auditor, Schoolties Between CFO and Auditor.

Note. t statistics in parentheses.

p < .1. **p < .05. ***p < .01.

The consideration that TCEO_AUD is less than TCFO_AUD illustrates that the school-ties function built by the CEO is not considered by the company. If it is being analyzed, this occurs because the CEO’s goals may have been represented by the CFO. With regards to manipulated corporate reports, the CEO could still easily pressure the CFO to engage in this action and give the influence. As in the research conducted by Feng et al. (2011) that the act of material accounting manipulation the CEO wants to achieve can be represented by the collaboration with the CFO and obscuring the influence of the CEO directly.

To test Hypothesis 1b, we specified a regression model linking dependent variable, test variable, and batteries of control variables as follows:

The results of the regression test for hypothesis 1b are shown in Table 7 above, indicating that hypothesis 1b is accepted. It can be seen that there is a significant relationship at the 5% level between School-ties CFO and Auditor (TCFO_AUD) on the Audit Fee variable (AFEE) and is positive with a coefficient of 0.301. This means that companies that have School-ties between CFO and Auditor (TCFO_AUD) will increase the Audit Fee (AFEE) of their company auditors. The positive relationship that is formed, can occur because the CFO is the closest in the company’s financial reporting and is directly related to the auditor, as well as the importance of achieving the goals of the company as a result of the formation of the school.

School-ties between CFO and Auditor (TCFO_AUD) is positively related to the cost of the audit (AFEE) indicating the existence of collusion, corruption, and certain fraud (Levitt & Dwyer, 2002) which undermine their independence (Francis & Ke, 2006; Khurana & Raman, 2006; Krishnamurthy et al., 2006; J. Krishnan et al., 2005). Recent research on ties also supports this argument (Du et al., 2023; Fang et al., 2022). As in Guan et al. (2016), this is closely related to the modification of their audit results and audit quality. This behavior is in reciprocal theory or so-called Social Reciprocity Theory, where the Audit Fee (AFEE) is given in response to the company because of the advantages of the company’s destination site and for the cooperation of the School-ties between the CFO and the Auditor (TCFO_AUD).

We perceive that the importance of Social Reciprocity Theory can bind school ties between CFO and auditors in three stages:

The relationship is formed from a pattern of reciprocity, debt of gratitude, and morals as a form of bond between individuals who go to school in the same place.

They will be bound by the similarity of the school’s alma mater background. In this context, the existence of school ties plays an important role in building social relations between individuals.

After having the background and comfort, as well as the bond formed from the theory of reciprocity, the relationship between key position holders, namely the CFO and the auditor, can have a significant impact on the company and deserves deeper consideration.

To test Hypothesis 2, I specified a regression model linking dependent variable, test variable, and batteries of control variables as follows:

To test Hypothesis 3, I specified a regression model linking dependent variable, test variable, and batteries of control variables as follows:

To test Hypothesis 4, I specified a regression model linking dependent variable, test variable, and batteries of control variables as follows:

To test Hypothesis 5, I specified a regression model linking dependent variable, test variable, and batteries of control variables as follows:

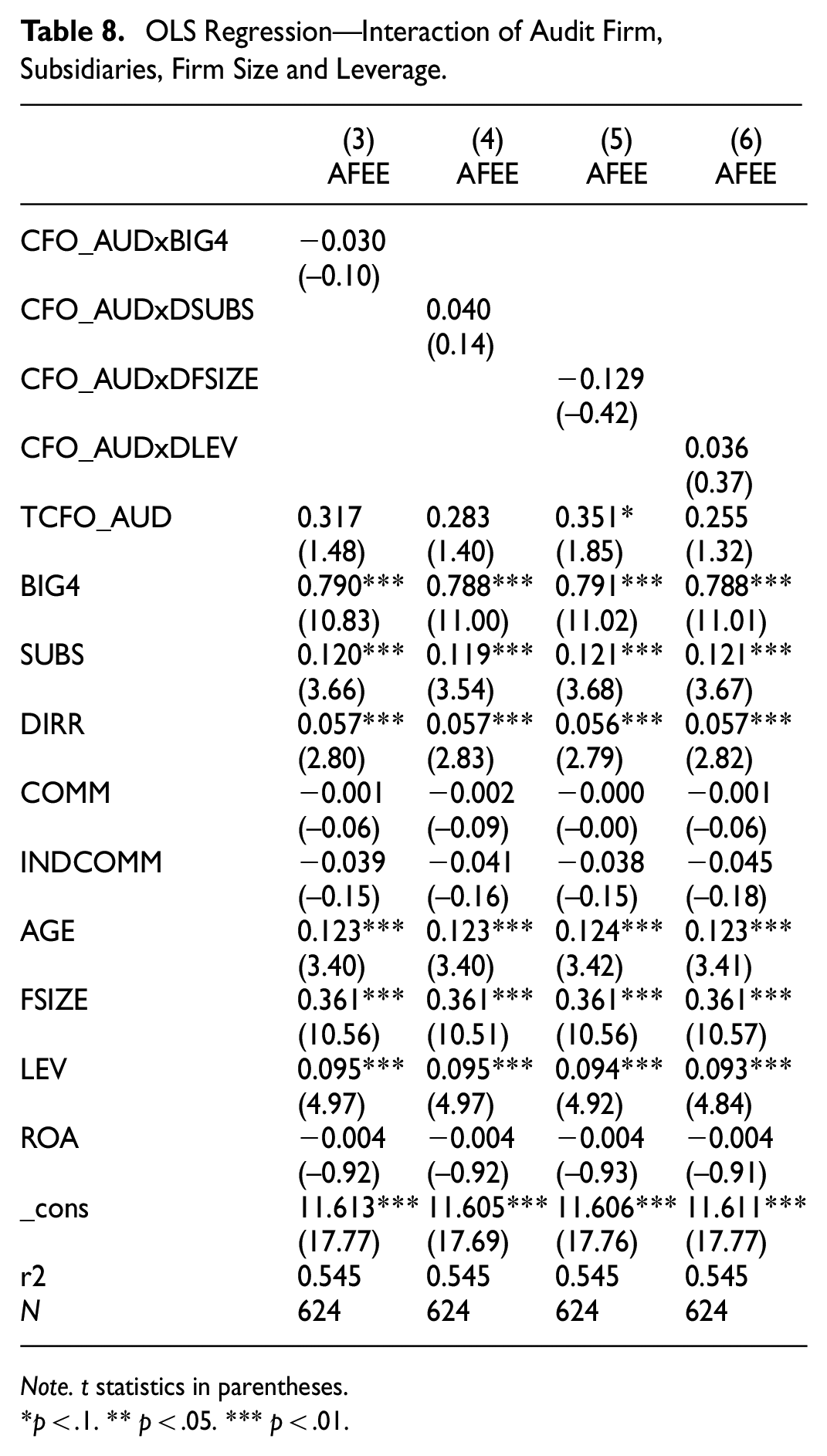

In Table 8, the regression results show the second hypothesis to the fifth hypothesis which is a form of company interaction regression that has a relationship between School-ties CFO and Auditor (TCFO_AUD). The result is that no tests performed from this table are accepted. However, our interesting findings show that companies with FSIZE below-average show a significance level of 10% and are positive with a coefficient of 0.351 on audit fees. If explained, this can occur because below-average FSIZE is still a small-scale company and is still trying to improve their audit performance, and the tendency to choose auditors based on school-ties is possible. The high audit fee will also show an increase due to the school-ties that are in their company.

OLS Regression—Interaction of Audit Firm, Subsidiaries, Firm Size and Leverage.

Note. t statistics in parentheses.

p < .1. **p < .05. ***p < .01.

We have not found any previous research that specifically discusses school-ties between CFO and auditors. However, relevant research (Kwon & Yi, 2018) can be used to compare with research results that CEO-EP school ties are associated with high-quality audits and audit fee premiums. They interpret the results of their research that CEO-EP social ties might be essential to secure a high-quality audit in a setting with low investor protection. In addition, (Qi et al., 2017) research can also be used as a comparison by looking at the social ties between auditors and clients (CEO or CFO) with audit quality. The results show that clients with social ties are significantly and positively associated with abnormal accruals and reporting small profits and are more likely to receive clean audit opinions compared to clients without social ties.

Conclusion

Research conducted to examine the school-ties relationship between the CEO, CFO as top management, and auditors with audit fees show several interesting things. School-ties between CFO and Auditor (TCFO_AUD) is positively related to audit fees (AFEE), this reason is based on the research results of Levitt and Dwyer (2002) that indicate certain collusion, corruption, and fraud, as well as strengthen the research conducted by Guan et al. (2016). Recent research on ties also supports this argument (Du et al., 2023; Fang et al., 2022). In other tests, TCEO_AUD did not show the significance of audit fees. Besides, in our interaction test, the results show that companies with a firm size are below-average, TCFO_AUD shows a higher audit fee.

From the conclusions, this study contributes to the development of literature regarding the relationship between school-ties CEO, CFO as top management and auditors on audit fees and completes research analysis on the characteristics of audit quality of public companies in Indonesia. This research can also contribute to the implementation of company policies, as well as external parties, named regulators and investors, in paying attention to the bad effects of school-ties in the company body. Suggestions for this research are submitted to practitioners or related stakeholders, both internal and external, in implementing policies within the company, developing regulations regarding the disclosure of educational history, school-ties, also audit fees to support transparency and as a form of prevention from the creation of corporate manipulative actions. Furthermore, regulators may consider mandatory disclosure of audit fees as well as educational history on their company’s board of directors.

We suggest future research to explore how the existence of corporate CSR or other mandatory disclosures might impact the relationship between top company officers and auditors and audit fees. We can also provide suggestions for future researchers to investigate the impact of the COVID-19 pandemic on this research. We recommend a different approach, such as a case study or experiment, to see the impact intensely.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Data Availability Statement

Data sharing not applicable to this article as no datasets were generated or analyzed during the current study.