Abstract

In recent years, the phenomenon of excessively inefficient M&As by listed companies has become increasingly serious, negatively affecting the stability of the capital market and the benign development of enterprises. In view of this, we select A-share nonfinancial listed companies in Shanghai and Shenzhen from 2012 to 2022 as the research sample, and use a series of methods such as OLS, PSM, and 2SLS, to explore the impact of ESG performance and corporate M&A behavior. The results show that good ESG performance can effectively reduce the size of M&As and excess goodwill, with agency cost, reputational constraint, and innovation crowding-out as the key transmission paths. The inhibitory effect is more pronounced in privately held firms and firms with higher management shareholding. Furthermore, firms can improve M&A market performance. This study provides a reference for encouraging firms to actively implement ESG concepts and carry out high-quality M&As and restructurings.

Plain Language Summary

In recent years, the phenomenon of excessively inefficient M&As by listed companies has become increasingly serious, negatively affecting the stability of the capital market and the benign development of enterprises. In view of this, we select A-share nonfinancial listed companies in Shanghai and Shenzhen from 2012 to 2022 as the research sample, and use a series of methods such as OLS, PSM, and 2SLS, to explore the impact of ESG performance and corporate M&A behavior. The results show that good ESG performance can effectively reduce the size of M&As and excess goodwill, with agency cost, reputational constraint, and innovation crowding-out as the key transmission paths. The inhibitory effect is more pronounced in privately held firms and firms with higher management shareholding. Furthermore, firms can improve M&A market performance. This study provides a reference for encouraging firms to actively implement ESG concepts and carry out high-quality M&As and restructurings.

Introduction

Leveraging the price discovery and property rights trading functions of the capital market, Chinese listed companies have been keen to engage in mergers and acquisitions (M&A) and reorganization, aiming to achieve leapfrog expansion at the corporate scale. According to the data released by the Listing Department of the Securities and Futures Commission (SFC), in 2022, A-share listed companies carried out 6,832 M&A and reorganization transactions, with a cumulative transaction amount of approximately RMB 2.8 trillion. However, while China’s capital market merger and acquisition activities are booming, listed companies’ mergers and acquisitions have failed to realize the expected value-enhancing effect; in contrast, a phenomenon of “twice the effort for half the result” inefficiency is prevalent. The reason lies in the fact that M&As, as activities with a high degree of uncertainty and strong subjectivity, are motivated not only by the “M&A efficiency view” (i.e., value maximization) but also by the “M&A arbitrage view” (i.e., self-interest pursuit). In China, the common M&As include “scale-oriented” M&As, which are initiated by executives in pursuit of political promotion; “pulling together” M&As, which are a form of government intervention; and “transfer of benefits” M&As, which is where major shareholders hollow out an organization for the benefit of another (Cheung et al., 2009). Under such circumstances, M&As have gradually become a means for M&A players to satisfy their selfish desires without considering the consequences, and as a result, inefficient M&A behaviors have led to the frequent occurrence of goodwill mines, the transfer of benefits, etc., which have severely constrained the long-term development of enterprises and harmed the interests of shareholders of small and medium-sized enterprise (SMEs).

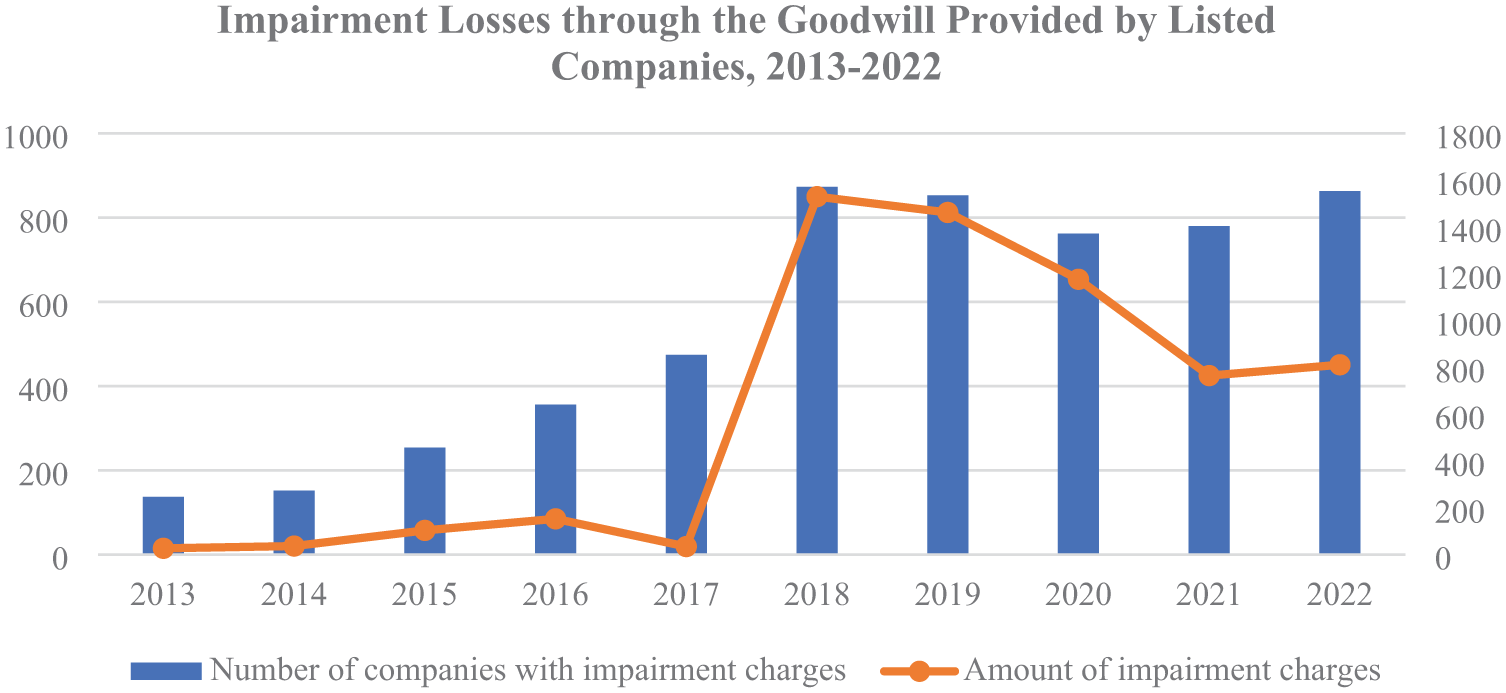

As shown in the data in Figure 1, numerous listed companies experienced frequent and substantial goodwill impairment during the course of mergers and acquisitions. In 2021, 780 listed companies reported a total of 76.506 billion yuan in goodwill impairment. The following year, in 2022, 863 listed companies incurred a total of 81.129 billion yuan in goodwill impairment. Some companies have also incurred the risk of a performance crash as a result. Moreover, cases in which large shareholders utilize M&A activities to help hollow out another company, thus encroaching on the interests of small and medium-sized shareholders, are also commonplace. The above cases indicate that M&As are a major strategic choice in the face of high risk and uncertainty, requiring the shareholders of SMEs to reexamine whether the M&A behavior of listed companies is conducive to the sustainable development of enterprises. The current phenomenon of destructive and inefficient M&As, which are characterized by blind and excessive M&As with poor benefits, has attracted the attention of regulators and investors in the capital market.

Impairment losses due to goodwill recorded by listed companies, 2013 to 2022.

The CPC Central Committee attaches great importance to the task of preventing and resolving major risks, clearly stating that this is the first of the three major battles to win to build a moderately prosperous society in all respects and that financial risk, as one of the most prominent major risks at present, is particularly crucial to its prevention and resolution. In October 2024, the Shenzhen Stock Exchange again issued a document emphasizing pricing fairness and regulated, orderly, pragmatic and efficient mergers and acquisitions to improve the quality of listed companies’ mergers and acquisitions. At present, the risk caused by the inefficient M&As of listed companies has become a key financial risk factor hidden in the capital market, and accordingly, how to effectively prevent and resolve M&A risks has become an important issue to be solved.

In recent years, the development philosophy of enterprises has not been limited to short-term profit targets; rather, they have pursued a more long-term-oriented management philosophy. Notably, ESG, a development concept that advocates the harmonization of corporate development in multiple areas, such as the environment, social responsibility and corporate governance, has emerged globally (Gillan et al., 2021). Many scholars at home and abroad have also examined the economic and social benefits brought about by ESG practices in enterprises, which are specifically reflected in the reduction of operating costs (Houston & Shan, 2022), the enhancement of stock returns (Garel & Petit-Romec, 2021), the promotion of corporate value (Pedersen et al., 2021), and the enhancement of innovation efficiency (Kweh et al., 2024). Furthermore, subsequent studies have also clarified the institutional effects of ESG, which can be categorized as improving stakeholder relations (Gjergji et al., 2021), reducing information asymmetry (Raimo et al., 2021), and establishing a good reputation effect (Reber et al., 2022). The above study shows that the financial behavior of enterprises is changing under the ESG framework. Good ESG performance effectively promotes the transformation of financial behavior in a high-quality, sustainable direction and helping enterprises develop. However, few scholars have linked ESG performance to corporate M&As.

On the basis of our analysis, we believe that long-term value orientation in ESG performance significantly impacts corporate M&A behavior. In summary, we examined data from Chinese A-share listed companies in Shanghai and Shenzhen from 2012 to 2022 to explore the intrinsic relevance and logic of the impact of ESG performance on M&As. Our analysis focused on three key questions:

Answering these questions will provide practical, reliable evidence and references to promote ESG concepts and prevent major risks in China.

Compared with the literature, the possible research contributions are related to three main areas. First, this study expands upon the research concerning ESG performance and M&A behavior. While most existing studies explore the positive impact of ESG performance on accounting performance (Khan et al., 2016) and risk (Khorilov & Kim, 2024), few have examined its impact on corporate M&As. Second, we examine M&A size and excess goodwill within the same framework, promoting the in-depth development of M&A research. Meanwhile, this study analyzes the mechanism through which ESG performance impacts corporate M&A behavior. This analysis provides strong support for promoting ESG development and high-quality M&As. Third, we examine the heterogeneity of the impact of ESG performance on corporate M&A behavior on the basis of the nature of property rights and the level of management shareholding. This aids the government and relevant departments when implementing targeted policies to encourage high-quality M&A behavior.

Literature Review and Hypotheses Development

Literature on M&As

In the complex and changing business landscape, M&A activities are often influenced by a combination of factors, such as the external environment at the national level and internal governance at the corporate level.

With respect to macroenvironmental factors, the current research has focused mainly on the impacts of national policies, external regulations and geographical environmental factors on corporate M&As. At the level of economic policy, the implementation of an antidumping policy in foreign trade has a significant inhibitory effect on the scale and number of cross-border M&As (Carline et al., 2021). Moreover, policy uncertainty, as an important source of risk, has a significant promotional effect on cross-border M&A willingness and the success rate of enterprises. In addition, policy uncertainty, when acting as an important source of risk, also affects corporate M&As (Gregoriou et al., 2021), as concluded by Bonaime et al. (2018), who found that uncertainty related to monetary policies, fiscal policies, and financial regulations has a particularly inhibitory effect on corporate M&As. Furthermore, Liu et al. (2024) showed that the SEC plays a key role in the capital market through regulations and enforcement, which can reduce information asymmetry in M&A activities and facilitate the completion of M&A transactions. For the geographical environment factors, Lin and Pursiainen (2023), using a sample of M&A events in the United States, reported that regional cultural differences lead to a lower likelihood of M&As and a substantial degree of complexity.

In terms of microfirm factors, the literature is categorized into internal characteristics such as the personal characteristics of directors and executives and corporate governance mechanisms. Factors such as executives’ political ideologies (Elnahas & Kim, 2017), directors’ sex (Levi et al., 2014), and executives’ age (Jenter & Lewellen, 2015) can have important impacts on corporate M&As. Furthermore, executive incentives are an important corporate governance mechanism, and Croci and Petmezas (2015) showed that the proportion of CEOs’ equity compensation is directly proportional to the number of M&As and that equity incentives are therefore more likely to induce CEOs to take on risky M&A projects (Edmans et al., 2011). Harp et al. (2018) argued that the level of internal control of a firm also affects acquisition performance.

In summary, the majority of studies focus on the governance dimension from the firm’s perspective, while few studies have focused on the dimensions of social and environmental responsibility. Therefore, it is worthwhile for future research to explore the impact of M&As from a comprehensive ESG dimension.

Literature on ESG Performance

On the basis of the development of CSR theory, ESG incorporates important corporate environmental responsibility (E), emphasizes the comprehensive assessment of corporate environmental, social and governance dimensions, and has become an important basis for measuring corporate sustainable development. With the rise and wide application of ESG, scholars have conducted extensive theoretical and empirical research.

Focusing on the antecedents and drivers of ESG performance, scholars have explored firm characteristics such as corporate attributes, executive manipulation tendencies, and board of directors’ characteristics, as well as country-level factors such as government regulations, market power, and the institutional environment. From a firm attribute perspective, Drempetic et al. (2020) noted from a firm size perspective that, compared with smaller firms, larger firms have a significant advantage in improving ESG performance. Moreover, Villalonga et al. (2025) analyze how the structure and identity of firms’ material owners influence their ESG performance. Furthermore, Amiraslani et al. (2025) find that firms with more risk-aware boards of directors are more likely to exhibit superior ESG performance, especially in the environmental performance dimension. At the national level, factors such as the political system (legal framework and corruption), the labor system (labor protection and unemployment), and the cultural system (social cohesion and equal opportunities) have significant effects on firms’ ESG disclosure practices (Baldini et al., 2018).

Furthermore, with respect to the level of economic consequences, most scholars have affirmed the positive effects of practicing ESG concepts with respect to increasing enterprise value, reducing the cost of capital and enhancing corporate efficiency. Specifically, Qureshi et al. (2020) report a significant positive correlation between ESG performance and firm value in a study of 812 European listed companies. Moreover, practicing ESG concepts can reduce the adverse effects of negative events, thus alleviating financing constraints (Eliwa et al., 2021) and lowering the cost of capital (Wong et al., 2021). In addition, good ESG performance can significantly improve the efficiency of firms’ capital investments and provide an impetus for high-quality development (Anwar & Malik, 2020). Yan et al. (2025) examined stock market performance and report that ESG performance reduces the proportion of institutional investors when ESG attention is high, which significantly affects asset returns.

Successively, the literature has also initially examined the impact of ESG performance and corporate M&As from the three single indicator dimensions of E, S, and G. In terms of environmental responsibility, it has been determined that command-and-control environmental regulation promotes green M&As, as there is a U-shaped relationship between market-based environmental regulations and green M&As (Sun et al.,2024). In terms of social responsibility, Arouri et al. (2019) reported the corporate social responsibility performance is significantly negatively correlated with the uncertainty of the completion of the merger, Twardawski and Kind (2023) find that board overconfidence drives firms to engage in high-premium M&As that result in poorer M&A performance. The above literature provides useful insights for understanding the relationship between ESG performance and M&As.

In summary, the academic community has developed an understanding of the impact of ESG sub-indicators on corporate M&As. However, few studies have analyzed ESG performance as a whole under the contextual framework of corporate M&As, especially in terms of examining the intrinsic transmission mechanism and the deep logical relationship between ESG performance and the inefficient M&A behaviors of corporations. Accordingly, these areas require further study. Therefore, it is highly significant that our study explores the dual perspectives of ESG performance from a holistic view of M&As. We argue that under the long-term value orientation of the ESG concept, ESG-performing enterprises are more cautious in initiating M&A events, which is manifested by a “steady” implementation of M&As whereby their M&A activities are characterized by “do less but better”.

Hypothesis Development: ESG Performance and M&As

We refine the impact of ESG performance on corporate M&A behavior into two key issues: one is that ESG performance affects the size of payment for M&A decisions, and the other is that excess goodwill, as a direct result of M&A pricing, are also affected by ESG performance together. On the basis of these two issues, this study provides insights into the transmission mechanism of corporate ESG performance and M&A behavior and concludes that corporate ESG practices affect inefficient M&A behavior through three main mechanisms: mitigating agency costs, reinforcing reputational constraints, and increasing innovation crowding out.

Agency Cost Mechanism: ESG Performance is a Practical Tool for Mitigating Agency Conflicts in M&As

The agency cost mechanism, that is, ESG performance, influences M&A decisions by reducing agency costs. The literature suggests that ESG performance plays an important role in mitigating principal–agent conflicts (Atif & Ali, 2021). From the perspective of internal governance, good ESG performance implies that a company has established a more complete and efficient internal management system and monitoring and governance mechanism, which can significantly reduce the degree of information asymmetry, prevent the opportunistic behavior of management, and thus reduce agency costs.

The agency cost problem is particularly prominent in the complex and risky business activities of M&As, and Nguyen et al. (2012) report that approximately 59% of all M&A activities are driven by agency motives. The complexity of M&A transactions, the uncertainty of the underlying valuation and the asymmetry of M&A information all provide room for controlling shareholders and management to maneuver in decision-making and execution. Specifically, controlling shareholders can use M&As to carry out opportunistic behaviors such as the transfer of benefits or the hollowing out by major shareholders, which seriously harms the interests of enterprises and the shareholders of small- and medium–sized enterprises (Grossman & Hart, 1988; Bae et al., 2002). Conversely, management often has a strong “empire building” motive and to implement large-scale mergers and acquisitions (Mueller, 1969) regardless of the cost to their own private interests. For example, management may use M&As to increase their own compensation and use their power to seek rents to manage more assets, ultimately leading to personal gains in terms of monetary compensation, on-the-job spending, and increased social prestige. Furthermore, according to the managerial ego hypothesis, overconfident management tends to underestimate the potential risks of M&As and overestimate the M&A premium of the target firm, which results in valuation bias during the M&A process, and therefore tends to engage in aggressive expansion activities such as M&As and to recognize more goodwill (Ham et al., 2018). ESG practices can effectively adjust the internal interest distribution pattern and information communication mechanism of the enterprise to encourage management to consider the rights and interests of small and medium-sized shareholders and other stakeholders when making M&A decisions instead of just focusing on their own self-interests or the short-term interests of the majority shareholders, which minimizes the occurrence of ineffective M&A behaviors such as blind M&As and excessive M&As due to the agency conflict.

In summary, good ESG performance indicates that companies have better internal governance capabilities, which can effectively prevent the opportunistic behavior of controlling shareholders and management, leading to a more prudent assessment of the expected returns when making M&A decisions, thus suppressing the emergence of M&A scale and excess goodwill.

Reputational Constraint Mechanism: ESG Performance is an Effective Facilitator of Reputational Constraints in M&As

The reputational constrain mechanism, that is, ESG performance, influences M&A decisions by exerting reputational constraint effects. The fulfillment of ESG responsibilities is an important channel for the construction of corporate “reputation capital,” that is, companies with good ESG performance usually pay more attention to their own governance construction and their environmental protection and social responsibilities for the purpose of establishing a good corporate image and reputation for the outside world (Meng et al., 2023). According to reputation building and maintenance effects (Tadelis, 1999), corporate reputation is a type of asset that can be built and continuously maintained and managed, while the value of reputation lies in the credibility of the commitment, which, as an informal mechanism, creates internal constraints at a relatively low cost.

Given the long-term and fragile nature of one’s reputation, once damaged, it is difficult to recover and expensive to repair. In recent years, risky events caused by incorrect mergers and acquisitions have become common, which have not only damaged the economic interests of enterprises but also caused serious negative impacts on their reputations. Therefore, to maintain their own reputation capital, when making strategic decisions, enterprises are extra cautious in considering the possible negative impacts of M&As, and therefore, they have increased their risk awareness (Shu & Wong, 2018), making decisions that are more beneficial to the long-term value of the enterprise and taking the initiative to avoid high-risk, low-quality merger and acquisition projects that may damage the reputation of the enterprise. Moreover, media attention, as an external governance force that can supervise corporate behavior, is an important realization channel of the reputation mechanism, especially in the context of China’s capital market, which is in a relatively immature stage of development. Hence, social supervision via media attention plays a more prominent role. Under the influence of the reputation mechanism, media attention can inhibit management’s self-interest and reduce the blind expansion behavior of corporate management for personal gain.

Therefore, companies with good ESG performance pay more attention to the standardization of M&A decision-making and the rigor of the evaluation process due to the motivation to maintain and enhance their own reputation, thus inhibiting risky M&A behavior and ensures that future goodwill risk caused by excessive goodwill recognition is considered in the M&A decision-making scope.

Innovation Crowding-Out Mechanism: ESG Performance is a Key Lever for Balancing Innovation Crowding-Out Due to M&As

The innovation crowding-out mechanism, that is, ESG performance influences M&A decisions by crowding out innovation investment. According to the basic framework of the theory of finite resources, when a firm’s overall investment is fixed, the allocation of its resources between outward expansion (e.g., market expansion activities such as mergers and acquisitions) and inward innovation (e.g., internal capability enhancement activities such as R&D investments) shows a trade-off (Orhangazi, 2008). That is, firms must engage in a trade-off between the two strategic choices of outward expansion and inward innovation.

The willingness perspective is manifested in the fact that the ESG concept focuses on the sustainable development of the enterprise, thus enterprises with better ESG performance are more inclined toward internal R&D, a strategy that contributes to long-term development. At the same time, enterprises with better ESG performance receive more attention from the media, the government, the public, etc., and the reinforcement of external supervision further inhibits opportunistic behaviors and encourages enterprises to strengthen their investment in innovation (Peña-Martel et al., 2024). From the perspective of capability, R&D activities, because of their long duration and high resource consumption, require firms to have sufficient resource reserves and efficient resource allocation capabilities to support the long-term orderly development of R&D activities. Moreover, enterprises with better ESG performance are more likely to gain the trust and support of investors, thereby alleviating financing constraints and enhance their ability to acquire resources, which can then be allocated to innovation and R&D investment projects that are closely related to the future development of the enterprise. When enterprises invest a large number of resources in the field of innovation, it will, to a certain extent, have a “crowding out effect” on the allocation of resources in other fields, especially some short-term, speculative, blind, excessive mergers and acquisitions that will result in resource constraints.

As a result, ESG-performing firms prefer the strategic path of internalized innovation to external expansion, are more cautious in deciding whether to initiate M&A activities given their limited resources and are likely to reduce paying excess premiums during the M&A process to ensure that their resources are more effectively used to support the firm’s long-term innovation and growth strategy.

On the basis of the above analysis, we present the following research hypotheses:

The mechanisms are shown in detail in Figure 2. We conclude from the above theoretical analysis that the agency cost mechanism and innovation crowding out mechanism support Hypothesis 1 and Hypothesis 2, whereas the reputation constraint mechanism primarily supports Hypothesis 2.

Analysis of the mechanism of ESG performance and corporate M&A behavior.

Empirical Setting

Sample Construction and Data Sources

We take the data of China’s A-share listed companies in Shanghai and Shenzhen from 2012 to 2022 as the research sample. The ESG performance data of the companies are from the Wind database (Wind), and the financial data and corporate governance data are from the CSMAR and CNRDS databases, respectively.

We screen the M&A and reorganization events of listed firms during the sample period in the “China Listed Companies M&A and Reorganization Research Database” of the CSMAR database. Referring to the practice of Wang et al. (2024), on the basis of the date of the first announcement of the M&A, we screen the M&A events implemented by listed companies as follows: (1) the listed companies are required to be in the “buyer” position, as this study is conducted from the perspective of listed companies as the main merging company; (2) samples of unsuccessful M&A transactions are excluded; (3) samples of listed companies in which the acquirer is a listed company in the financial industry or in the ST and PT categories are excluded; (4) samples in which the type of M&A is divestiture, asset replacement, debt restructuring, share repurchase, or equity transfer are excluded; and (5) samples in which the M&A buyer’s expenditure is less than 1 million yuan are excluded. Finally, we obtain 3,877 firm-year observations for which mergers and acquisitions occurred. All the continuous variables are subjected to a 1% reduction at the top and bottom.

Model

On the basis of the above theoretical analysis, we examine the relationship between ESG performance and corporate M&As from two aspects: one is to examine the relationship between ESG performance and the M&A scale to determine whether ESG performance can reduce the degree of M&A implementation; and the other is to explore the relationship between ESG performance and the scale of goodwill to determine whether ESG performance can inhibit the emergence of excess goodwill.

To verify Hypotheses 1 and 2, we construct Models (1) and (2), respectively:

Among them, the explanatory variable

Variables

Independent Variables

ESG performance (ESG). Currently, academics mainly use the ratings or scores of third-party rating agencies to measure corporate ESG performance. Referring to the study of Lu et al. (2024), we adopt the CSI ESG rating index to measure corporate ESG performance. Compared with other ESG evaluation systems, the CSI ESG rating system combines mainstream foreign ESG evaluation frameworks and the characteristics of the Chinese capital market, with a total of 26 key indicators and more than 130 sub-indicators, which has the advantages of wide coverage and high update frequency. The CSI ESG ratings are divided into nine levels, from low to high: C, CC, CCC, B, BB, BBB, A, AA, and AAA. The ESG variables in our study are composed of the nine levels from C to AAA of the CSI ESG ratings, which are accordingly assigned values from 1 to 9, and quarterly averages are selected to measure annual ESG performance.

Dependent Variables

Two variables are selected here to measure corporate M&As. One is the merger and acquisition scale (MA), which measures M&A behavior quantitatively. As defined by Li et al. (2022).MA is the ratio of the total amount spent by the buyer in an M&A transaction to the acquirer’s total assets at the end of the period. The other variable is the excess goodwill (GW), which qualitatively measures M&A behavior. This variable is essentially the difference between actual and projected goodwill, that is, the portion of the amount of goodwill recognized in an M&A transaction that exceeds the amount of reasonable goodwill, creating an overvaluation of goodwill. Drawing on the research of Yuan et al. (2023), we adopt a model prediction method to measure the excess goodwill (GW), that is, the regression residuals from the goodwill expectation model are used as a proxy variable for excess goodwill. The specific model is as follows:

where

Control Variables

Referring to the existing literature (Hossain et al., 2023; Li & Yuan, 2024), we also control for firm characteristics and related factors that may affect M&As, including firm size (Size), firm age (FirmAge), the gearing ratio (Lev), the return on total assets (ROA), the top shareholder’s shareholding (TOP1), institutional shareholding (INST), and the size of the board of directors (Board). In addition, the article controls for industry (Industry) and year (Year) fixed effects. The specific variables are defined in Table 1.

Definitions of Variables.

Empirical Results

Descriptive Statistics

Table 2 reports the descriptive statistics of the main variables. Table 2 shows that corporate ESG performance (ESG) has a minimum value of 1 and a maximum value of 7, with a mean of 4.097 and a standard deviation of .929, which indicates that there are some gaps in the ESG performance of Chinese firms under this M&A sample. The minimum value of the M&A scale (MA) is .000327, the maximum value is as high as 8.517, and the mean value is .211. The minimum value of the excess goodwill is −.085, the maximum value is .408, and the mean value is .0258, which indicates that the amount paid by some enterprises when they initiate mergers and acquisitions is much larger than their own total asset size, and the phenomenon of excess goodwill is common, that is, there is a high probability that there is a phenomenon of blind and excessive mergers and acquisitions.

Descriptive Statistics.

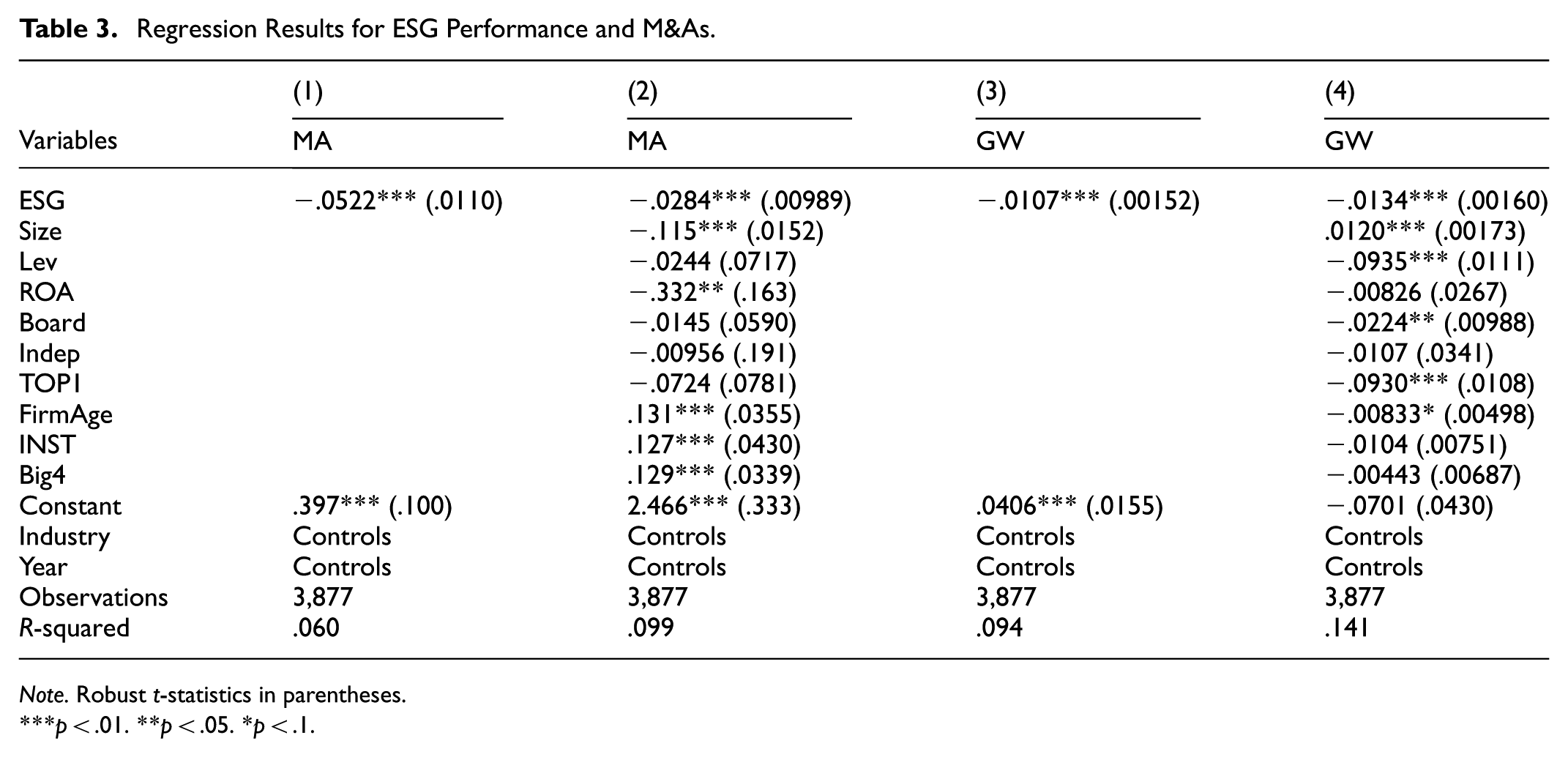

Baseline Regression Results

Table 3 reports the results of the tests of Models (1) and (2). Columns (1) and (2) show the results of the tests where the dependent variable is the size of firms’ mergers and acquisitions (MA), and the regression results with the inclusion of control variables and fixed effects show that the regression coefficient of the ESG performance (ESG) indicator is −.0522, which is significant at the 1% level, which suggests that the better the ESG performance of firms (ESG) is, the smaller the size of the merger and acquisition (M&A) deals implemented by firms, that is, ESG performance inhibits the size of M&As. Columns (3) and (4) show the results of the test where the dependent variable is the excess goodwill (GW), and the regression results after adding control variables and fixed effects show that the regression coefficient of the ESG performance (ESG) indicator is −.0134, which is also significant at the 1% level. The economic significance of this is that for every one-point increase in ESG performance, the excess goodwill generated is reduced by 1.34%.

Regression Results for ESG Performance and M&As.

Note. Robust t-statistics in parentheses.

p < .01. **p < .05. *p < .1.

In summary, the regression results indicate that ESG performance significantly suppresses the size of corporate M&As and excess goodwill. Moreover, ESG performance encourages enterprises to carry out high-quality mergers and acquisitions characterized by “fewer but better.” On the one hand, this “fewer but better” characteristic is manifested as a reduction in the scale of ineffective and inefficient M&A projects from the source and using enterprises’ limited resources for high-quality mergers and acquisitions. On the other hand, this characteristic increases the selection of the target companies purchased and the control of M&A goodwill assessment, which prevents excess goodwill and improves the M&A quality.

Therefore, the baseline regression results preliminarily indicate that H1 and H2 are valid.

Endogeneity and Robustness Tests

Instrumental Variable 2SLS Test

To mitigate the endogeneity problem due to reverse causation and other reasons, we attempt to construct two sets of instrumental variables for robustness testing. Referring to Zhang et al. (2024), we adopt firms’ ESG performance in the previous year and the number of Confucian temples within 100 km of the firm’s registered location as instrumental variables for the two-stage least squares (2SLS) regression. In this case, regarding the measure of the number of Confucius temples, we combine the latitude and longitude of the address disclosed in the company’s annual report to calculate the number of remaining Confucius temples within 100 km and +1 to take the logarithm. Theoretically, a firm’s ESG performance in the previous year only affects the firm’s ESG performance in the later period because of its “predetermined” characteristics and does not affect the perturbation term of the model in the current period. In addition, the number of Confucius temples in the neighborhood can reflect to some extent the degree of the firm’s exposure to Confucian culture, which advocates the principles of “benevolence, righteousness, propriety, wisdom, and trust,” which is consistent with the concept of “altruism” in corporate ESG. Moreover, Confucianism advocates the principles of “benevolence, righteousness, propriety, wisdom, and trust,” which coincides with the corporate ESG concept of “altruism.” The results in Table 4 passed the K-P LM Test, the K-P Wald F Test, and the Hansen J Test, and the regression coefficients for ESG were significantly positive at least at the 5% level. After controlling for potential endogeneity issues, the regression results do not change significantly, and the reliability of the findings is confirmed again.

Results of IV-2SLS.

Note. Robust t-statistics in parentheses.

p < .01. **p < .05. *p < .1.

PSM Test

To mitigate sample selection error, we refer to Su et al. (2024), assigning a value of 1 when ESG performance is greater than the median and 0 otherwise, and construct dummy variables for PSM propensity score matching. To calculate the propensity score, we select control variables such as firm size (Size), return on assets (ROA) and the gearing ratio (Lev) in the benchmark regression model as covariates for the regression. For pairing, we use .05 radius matching. Before PSM, there are significant differences in the paired variables within the sample group, but after PSM treatment, the differences between all paired variables are no longer significant, and the deviation from the overall mean of the sample is also no longer significant. Columns (1) and (2) in Table 5 present the PSM regression results; the regression coefficients of ESG are −.0283 and −.0134, respectively, and both are significant at the 1% level, indicating that the main conclusions still hold after the propensity score matching method is applied.

Results of the PSM Test.

Note. Robust t-statistics in parentheses.

p < .01. **p < .05. *p < .1.

Lagged Independent Variable

The above results confirmed that firms with better ESG performance initiate smaller M&As and generate smaller excess goodwill, but it is also possible that firms with smaller M&As and goodwill excess place more emphasis on corporate sustainability, which in turn promotes ESG performance. Considering that the robustness of the above empirical results may be affected by reverse causality, we lag the explanatory variable (ESG) by one period and introduce it into the model for regression. The regression results are shown in Columns (1) and (2) of Table 6. The regression results indicate that ESG performance is significantly negatively related to the M&A size at the 5% level and to excess goodwill at the 1% level, which suggests that the inhibitory effect of ESG performance on corporate M&As has a certain degree of persistence.

Results of the Lagged Independent Variable.

Note. Robust t-statistics in parentheses.

p < .01. **p < .05. *p < .1.

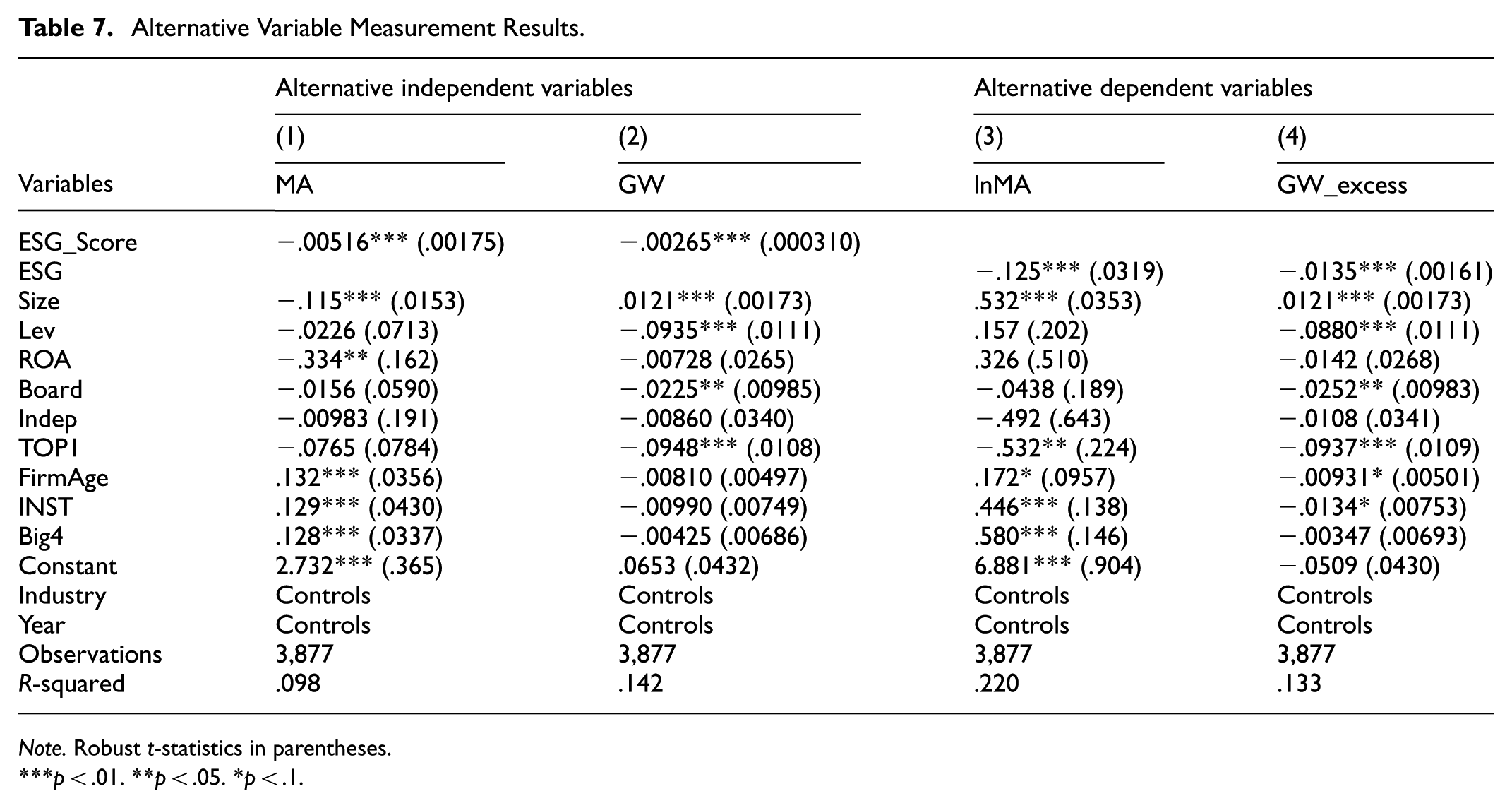

Alternative Variable Measurement

Considering the impact of the core explanatory variable measurement, to further enhance the robustness of the research results, we refer to Qian (2024) to change the measurement of the core explanatory variables. That is, the quarterly rating assignment of ESG performance (ESG) in the original model is changed to the annual composite score. The regression results after the substitution are still robust: the impact of ESG performance on corporate mergers and acquisitions (M&As) is still significantly negative, thereby verifying the conclusions. Second, the explanatory variable M&A size is changed from the relative M&A size (MA) to the absolute M&A size (lnMA), that is, the logarithmic treatment of the amount paid by the buyer, In addition, referring to the study of Wang et al. (2022), excess goodwill, which is measured by the book value of corporate goodwill minus the average of the annual book value of goodwill of the industry in which the enterprise is located and normalized by total assets (GW_excess), is used as a proxy variable to measure the excess goodwill (GW) of firms. The regression results in Table 7 remain robust after the above treatments.

Alternative Variable Measurement Results.

Note. Robust t-statistics in parentheses.

p < .01. **p < .05. *p < .1.

Changing the Sample Period

The unprecedented major external shock of the 2020 Xin Guan epidemic had a profound and complex impact on China’s capital market, including increased market volatility, the disruption of business activities, changes in investor sentiment, and other factors, which may have caused unpredictable disruptions to M&A activities and the assessment of the value of goodwill. For this reason, the sample data of 2020 are excluded and regressed, aiming to eliminate the data bias that may have been caused by the unusual event of the epidemic and to ensure the robustness and reliability of the research results. The results in Table 8 show that the impact of ESG performance on the M&A size and excess goodwill remains significantly negative, indicating that the epidemic shock did not affect the findings.

Regression Results after Changing the Sample Period.

Note. Robust t-statistics in parentheses.

p < .01. **p < .05. *p < .1.

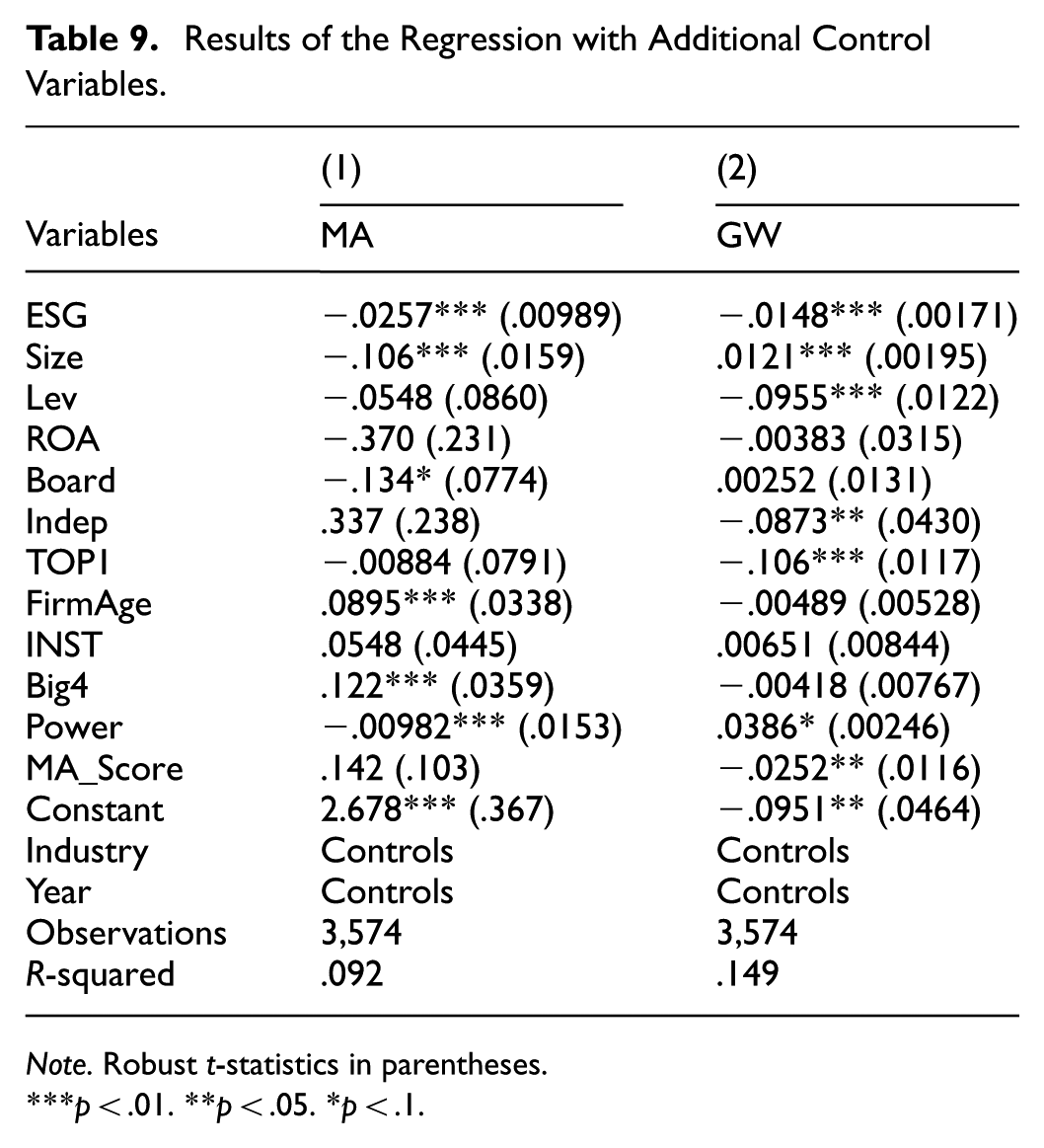

Adding Other Control Variables

We control for variables such as firm characteristics, but there may still be an omitted variable problem. On this basis, we further consider the impact of management’s personal characteristics. Considering that management decision-making is affected by ability and power, which in turn affects the inhibitory effect of ESG performance on corporate M&A behavior, we introduce two indicators of management ability and power into the original model. Drawing on the study of Demerjian et al. (2012), a two-stage model combining data envelopment analysis (DEA) and the Tobit model is used to measure managerial ability indicators (MA_Score). Moreover, referring to Finkelstein (1992) and Hu and Kumar (2004) indirect measures of managerial power, and combined with China’s actual practices, we selected the years of service of the general manager (Tenure), CEO duality (Dual), board size (Boardsize), the proportion of inside directors (Insider), and the proportion of managerial shareholding (Mgshder) and synthesized a composite indicator of management power according to the principal component analysis method. The results in Table 9 remain robust after controlling for management capacity and power.

Results of the Regression with Additional Control Variables.

Note. Robust t-statistics in parentheses.

p < .01. **p < .05. *p < .1.

After conducting endogeneity and robustness tests, such as 2SLS, PSM, and replacement variables, we found that H1 and H2 still hold.

Further Analyses

Mechanism Analysis

Agency Cost Mechanisms

On the basis of the previous analysis, under the role of agency conflict, M&A activities are often easily manipulated into a means for management to seek personal benefits rather than to enhance the company’s strategic development or maximize shareholders’ interests. Good ESG performance implies that firms have a sound and standardized internal governance mechanism, which can mitigate the principal-agent problem in M&As by reducing agency costs. To examine the impact of ESG performance on agency costs, drawing on the study of Ang et al. (2000), the management fee ratio (Mfee) is used as a measure of agency costs. Column (1) of Table 10 shows that the regression coefficient of ESG performance and agency costs (Mfee) is −.00404, which is significantly negative at the 1% level, indicating that good ESG performance can simultaneously and significantly reduce the agency costs of firms and that an internal governance mechanism for ESG performance is established. Moreover, ESG performance (ESG) in Columns (2) and (3) is still significantly negative at the 1% level, whereas agency costs (Mfee) are significantly positive at the 5% level, indicating that the mechanism of action holds. In summary, ESG performance can significantly reduce agency costs to alleviate the principal-agent problem of firms, which in turn reduces the size of mergers and acquisitions and excess goodwill.

Agency Costs Mechanism Test.

Note. Robust t-statistics in parentheses.

p < .01. **p < .05. *p < .1.

Reputational Constraint Mechanism

According to the above theoretical analysis, the establishment and maintenance of an enterprise’s reputation can form an intangible constraint mechanism within the enterprise, so ESG performance may inhibit the risky behavior of corporate mergers and acquisitions via the reputation constraint mechanism. To verify this speculation, we refer to the practice of Guan and Zhang (2019), who considered the evaluation of corporate reputation by various stakeholders, and select 12 factor indicators to calculate the corporate reputation (Rep) score by factor analysis and assign it values from 1-10; the larger the value is, the better the corporate reputation. As shown in Column (1) of Table 11, the regression coefficient between ESG performance and corporate reputation (Rep) is .112, which is significantly positive at the 1% level, indicating that good ESG performance can significantly promote corporate reputation (Rep). Moreover, ESG performance (ESG) in Columns (2) and (3) is still significantly negative at the 5% and 1% levels, respectively, whereas corporate reputation (Rep) is significantly negative at the 1% level, indicating that the mechanism of action holds. In summary, ESG performance can significantly maintain corporate reputation to create internal constraints, which in turn reduces the occurrence of risky M&A behavior.

Reputational Constraint Mechanism Test.

Note. Robust t-statistics in parentheses.

p < .01. **p < .05. *p < .1.

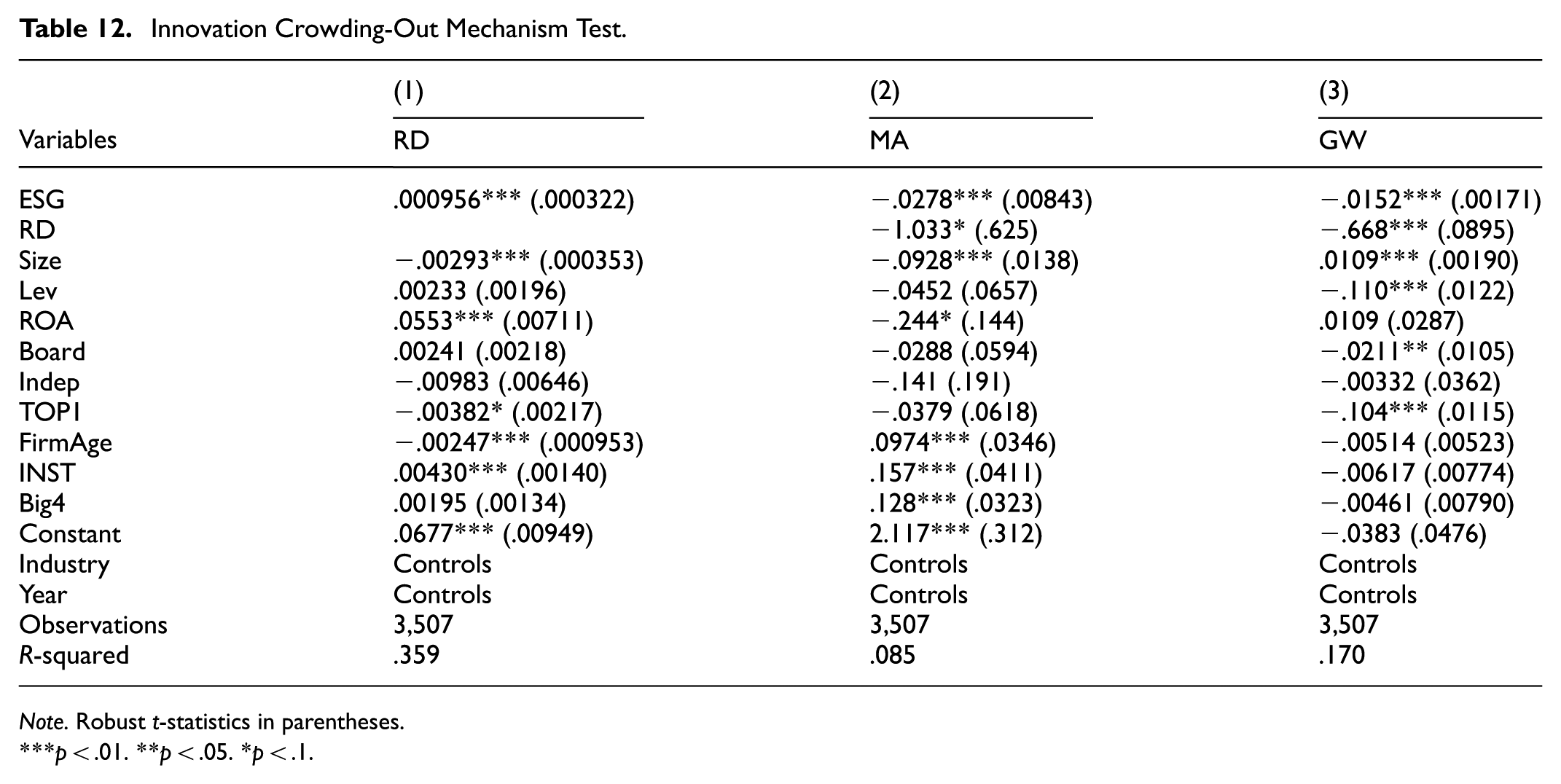

Innovation Crowding-out Mechanism

From the previous theoretical analysis, it can be expected that enterprises with better ESG performance tend to pay more attention to long-term value creation and sustainable development and put more resources and energy into R&D and innovation activities, aiming to drive business growth and enhance market competitiveness through technological innovation; however, given the limited nature of corporate resources, ESG performance can also impact merger and acquisition (M&A) behavior through the innovation crowding-out effect. Therefore, the ratio of research and development (R&D) investment to total assets (RD) is used as a measure of innovation investment to empirically study this mechanism. As shown in Column (1) of Table 12, the regression coefficient between ESG performance and R&D investment (RD) is .000956, which is significantly positive at the 1% level, indicating that good ESG performance can simultaneously and significantly promote firms’ R&D investment. Moreover, ESG performance (ESG) in Columns (2) and (3) is still significantly negative at the 1% level, whereas R&D investment (RD) is significantly negative at the 10% and 1% levels, respectively, indicating that the mechanism of action holds. Overall, the above regression results suggest that ESG performance crowds out M&A investment by increasing R&D investment, which in turn reduces the M&A size and excess goodwill.

Innovation Crowding-Out Mechanism Test.

Note. Robust t-statistics in parentheses.

p < .01. **p < .05. *p < .1.

Mechanism analysis results show that ESG can reduce M&A and excess goodwill by lowering agency costs and reinforcing reputational constraints. These results support the H1 and H2 paths of action by increasing innovation crowding out.

Heterogeneity Analysis

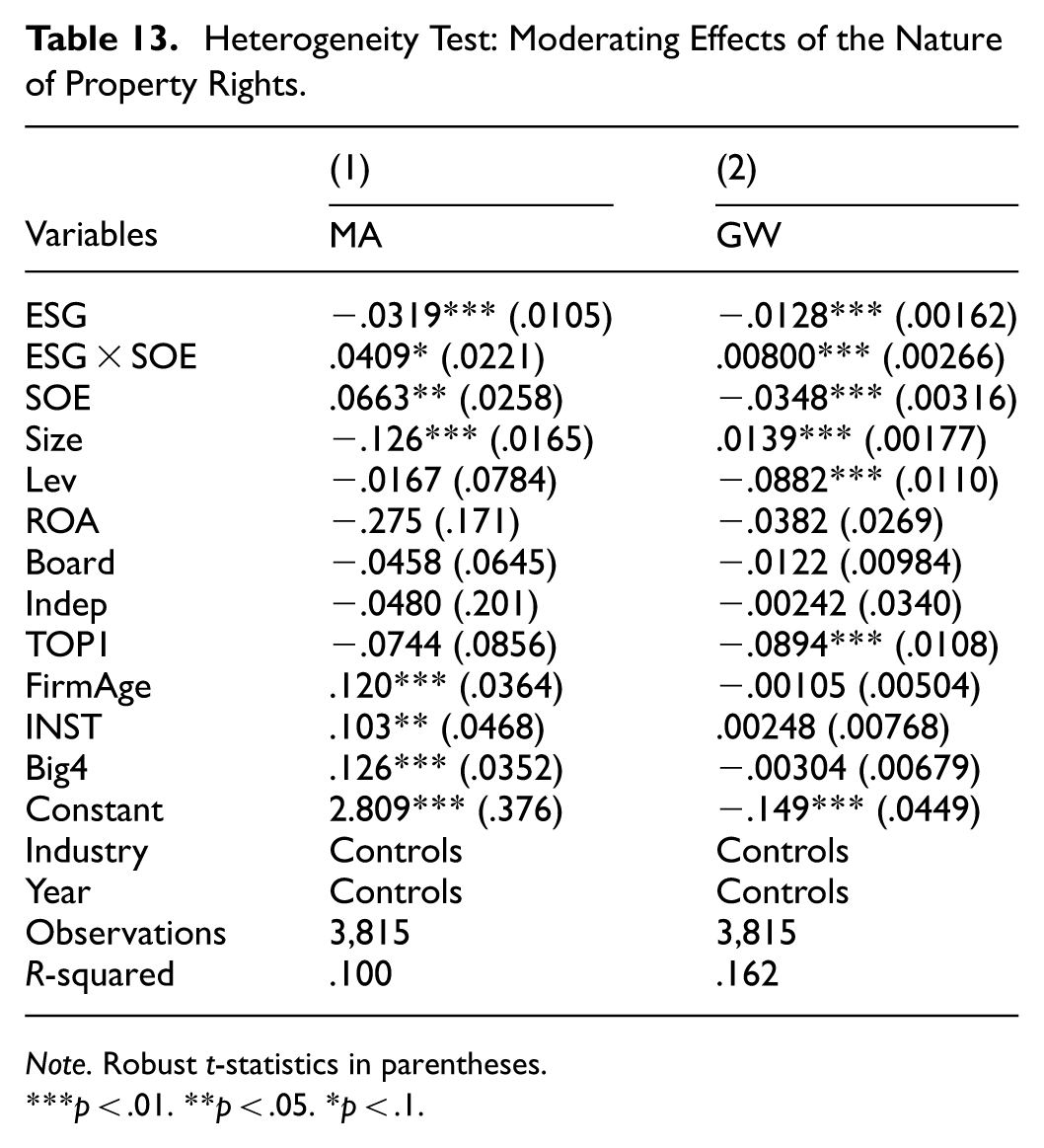

Impact of the Nature of Business Ownership

Enterprises are divided into state-owned enterprises (SOEs) and private-owned enterprises (POEs) according to the nature of their property rights. SOEs have strong administrative ties and their business activities are heavily influenced by the government’s policy orientation and management supervision, which results in SOEs tending to be more cautious and standardized in their mergers and acquisitions (M&As) and other major decisions by considering more political and social factors. In contrast, private enterprises have greater operational autonomy and flexibility and are subject to less intervention in their corporate governance activities. Moreover, the institutional environment and organizational structure of private enterprises are generally lower than those of state-owned enterprises, and the internal governance mechanism is relatively weak. In the absence of effective supervision and constraints, management is more likely to make use of opportunistic motives to engage in irrational or excessive M&A behaviors; thus, this article argues that private enterprises need to play a more important role in ESG to prevent the risk of M&As by strengthening their internal governance mechanisms and improving the transparency of decision-making.

On this basis, we construct an interaction term using the nature of property rights (SOE) and explanatory variables (ESG) to test this hypothesis, and the results in Table 13 show that the regression coefficients of ESG × SOE are significantly positive, indicating that ESG is more conducive to regulating the M&A behaviors of enterprises and results in more rational M&A decisions in private enterprises.

Heterogeneity Test: Moderating Effects of the Nature of Property Rights.

Note. Robust t-statistics in parentheses.

p < .01. **p < .05. *p < .1.

Impact of Management Shareholding

When managers have greater say and control in the company’s operational decisions because they hold a higher percentage of equity, this concentration of power often results in a series of negative effects. In particular, in the absence of effective monitoring and checks and balances, M&A activities may be used as a tool for managers to seize company resources and seek personal benefits. Such self-interest maximization-oriented M&A behavior may not only deviate from the long-term development strategy of the enterprise but also harm the legitimate rights and interests of other shareholders and stakeholders, thus exacerbating the agency conflict between executives and shareholders (Morck et al., 1990). In this context, we use the total number of shares held by executives at the end of the year divided by the total share capital of the company at the end of the year to measure the executive shareholding ratio (Mshare).

The results in Table 14 show that the regression coefficients of Columns (1) and (2) are both significantly negative, which means that the inhibitory effect of ESG performance on firms’ M&A behavior is more pronounced when the percentage of management shareholding in the firm is greater.

Heterogeneity Test: Moderating Effect of Management Shareholding.

Note. Robust t-statistics in parentheses.

p < .01. **p < .05. *p < .1.

The results of the heterogeneity analysis suggest that H1 and H2 have a stronger impact on firms with private ownership and higher management shareholding.

Analysis of Economic Consequences

The above empirical results have shown that ESG performance directors can reduce the scale of mergers and acquisitions and alleviate excess goodwill through three mechanisms: agency cost, reputation constraint and innovation crowding out. However, in the current “wave of mergers and acquisitions,” there is the phenomena of “merging but not integrating” and “integrating but not integrating” in the reorganization of some listed companies. Therefore, this study further verifies the impact of ESG performance on the integration performance of enterprises after the implementation of M&As.

To examine the impact of corporate ESG performance on M&A performance, with reference to the existing literature, drawing on the approach of Du et al. (2022), we measure the change in Tobin’s Q (ΔTobinQ), that is, the difference between the mean value of Tobin’s Q 2 years after the completion of the M&A by a listed company (years t + 1 and t + 2) and the mean value of Tobin’s Q 2 years prior to the M&A of a listed company (years t − 1 and t − 2), which represents the change in Tobin’s Q (ΔTobinQ) to assess long-term corporate M&A performance. The larger the value is, the better the financial performance after the M&A.

The specific regression results are shown in Table 15. The value of the change in ESG performance and Tobin’s Q (ΔTobinQ) is significantly positive at the 10% level, so corporate ESG performance can also lead to incremental M&A performance, stronger and better enterprises, and the realization of high-quality M&As.

Regression Results of the Impact of ESG Performance on Firms’ M&A Performance.

Note. Robust t-statistics in parentheses.

p < .01. **p < .05. *p < .1.

The results of the analysis of the economic consequences suggest that ESG can enhance the performance of the M&A market and promote high-quality M&As.

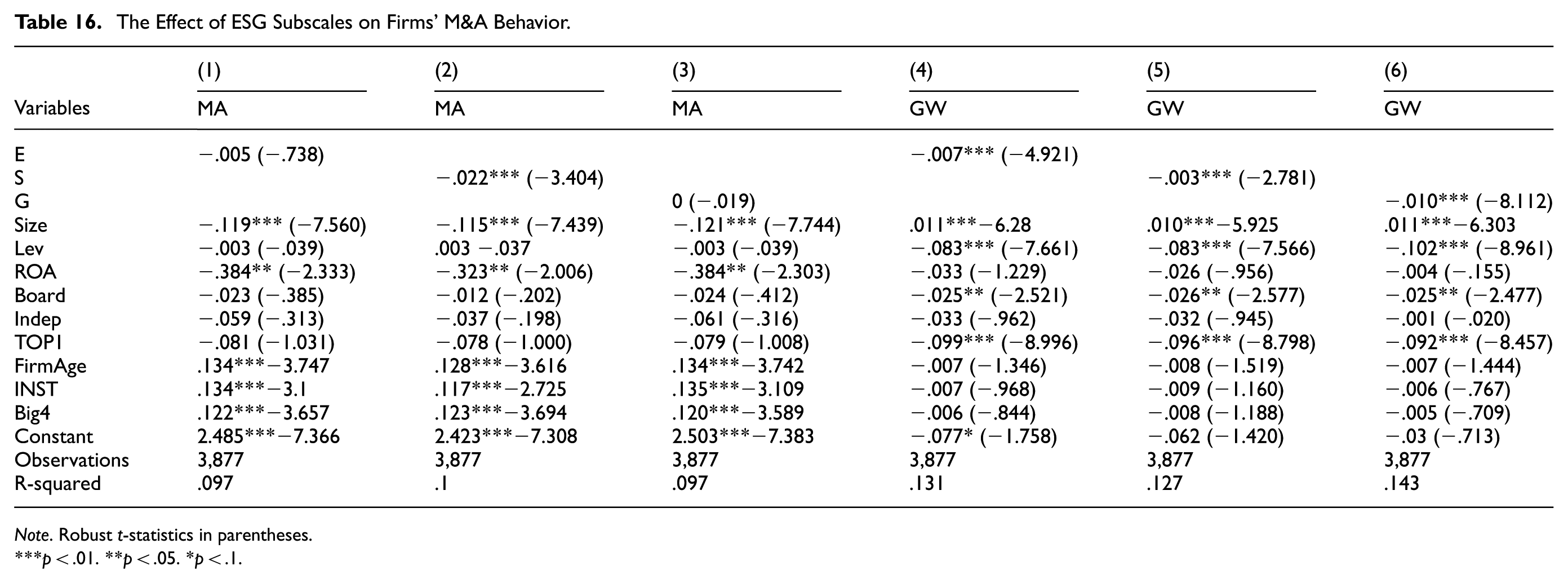

Subdivision of ESG and M&A Behavior of Firms

To further examine the separate impacts of the sub-items of ESG (i.e., elements E, S, and G), we regressed the sub-item data of the CSI ESG on firms’ M&A size and goodwill. The results are shown in Table 16. We found that, for M&A size, S plays the main role, while E, S, and G all play a role for excess goodwill, with G having the greatest inhibitory effect.

The Effect of ESG Subscales on Firms’ M&A Behavior.

Note. Robust t-statistics in parentheses.

***p < .01. **p < .05. *p < .1.

Conclusion and Discussion

Preventing systemic financial risks and utilizing the efficiency of financial services in the real economy are important embodiments financial governance in the new era. We empirically examine the impact of ESG performance on the M&As of listed companies in the Shanghai and Shenzhen A-shares from 2012 to 2022 as the research sample. The study reveals that good ESG performance has a significant inhibitory effect on corporate M&A behavior. The multiple mechanism results show that ESG performance reduces agency costs and enhances the reputation constraint and that the innovation crowding out effect is the main behavioral logic behind the observed effects. The results of the heterogeneity analysis show that ESG performance significantly inhibits corporate M&As, which are mainly concentrated in enterprises with private ownership and high management shareholding. Moreover, further economic consequence analysis reveals that ESG performance can significantly enhance the incremental M&A performance of enterprises. On the basis of these findings, the following policy recommendations are proposed: Firstly, the policy and regulatory level. The government should actively act to comprehensively promote the improvement and development of the environmental, social and governance (ESG) system, and promote the whole society to move steadily in the direction of sustainable development. Secondly, at the corporate governance level, Managements need to strengthen ESG concepts and M&A regulatory synergies, study the relationship and internal logic between corporate ESG performance and M&A risks, prevent financial risks, and promote healthy economic development. Finally, at the level of small and medium-sized shareholders, investors should incorporate ESG concepts into their investment decision-making system and continue to closely track the dynamics of subsequent M&A by enterprises to guard against performance meltdown and goodwill impairment risks.

Our research findings are based on a Chinese sample, so there may be some differences when applying them to developed versus emerging market contexts. ESG concepts are relatively mature in developed versus emerging market contexts, which may be more conducive to exerting a positive influence on M&A activities. Specifically, it is necessary to combine institutional theory, emerging market characteristics, and cross-cultural comparative frameworks to understand the experiences of Chinese companies and formulate appropriate strategies. At the same time, international companies, investors, and regulators will pay more attention to the positive role ESG plays in M&A activities. However, due to the limited access to data, we can’t further and discuss the following issues, such as the incomplete disclosure of data on ESG performance of the subject party firms, and therefore are unable to explore its impact on the M&A decision. In future research, it is necessary to take the ESG performance of the subject firms into account when the corporate disclosure is perfected. Furthermore, our study does not consider data from a sample of firms that do not engage in M&A activities and does not consider the impact of confounding events that may coincide with M&A announcements.

Ultimately, it is hoped that policy and corporate stakeholders will promote ESG concepts among corporations and monitor their efforts to reduce inefficient M&A behavior and prevent financial risk.

Footnotes

Ethical Considerations

This article does not contain any studies with human participants or animals performed by the authors.

Authors Contributions

Conceptualization, Resource, Supervision, Funding acquisition, Validation and Project administration: Xinjian Huang. Data curation, Software, Formal Analysis, Investigation, Visualization, Methodology, Writing—original draft and Writing—review & editing: Xinping Ji.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Fundamental Research Funds for the Central Universities (No. 2023CDSKXYJG007). The National Social Science Fund of China (24BGL083).

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The data that support the findings of this study are available as follows; (i) the Wind database, which provides annual dataset of environmental, social, and governance (ESG) performance indicators applied to a universe of publicly traded companies and (ii) the CSMAR and CNRDS databases, which provides financial data and corporate governance data.